Linear Regression for Power Law Distribution Fitting

Abstract

We fit the exponent of the Pareto distribution, that is equivalent or can approximate the continuous power law distribution given a cutoff point, using linear regression (LR). We use LR on the logged variables of the empirical tail (one minus the empirical cumulative distribution function). We find the distribution of the consistent LR estimator and an approximate sigmoid relationship of the mean that underestimates the exponent. By factoring out a sigmoid function used to approximate the mean we transform the LR estimator so it is approximately unbiased with variance comparable to the minimum variance unbiased transformed MLE estimator.

1 Introduction

Power laws in the probability distribution appear across a wide number of disciplines [3]. We shall focus in this paper on continuous power law distributions that approximate variables such as income, wealth and stock returns [5]. Several definitions of a power law distribution appear in the literature. We focus on the piecewise power law distribution and the regularly varying distribution which we define in the next section. The power law part of the former distribution can be exactly viewed as a Pareto distribution whereas the power law part of the latter can only be approximated as a Pareto distribution. We fit only the exponent of the distribution and not the cutoff point which can be estimated using a Monte Carlo method found in Clauset et al. [3]. There are several methods of fitting the exponent of a Pareto distribution that are consistent (the estimator tends to the true parameter as the sample size tends to infinity) including the method of moments, maximum likelihood estimation (MLE), quantile methods and linear regression (LR) [11]. Many have pointed out, for example [3], that LR is inferior to MLE but to the author’s knowledge it has not been analysed in detail why this is the case. We focus in this paper on fitting the exponent with LR on the empirical tail (one minus the empirical cumulative distribution funciton). We give a theoretical result on the distribution of the LR estimator as well as approximations on the mean and variance via simulation222Simulations are found at the author’s github [4]. We find evidence that the LR estimator is biased with a mean that underestimates the true exponent in a sigmoidal fashion depending on the sample size. Factoring out a sigmoid function we find this non-linear transformation of the LR estimator is roughly unbiased and comparable though greater in variance to a non-linear transformation of the MLE estimator which is unbiased of minimum variance [13]. We emphasise that the MLE estimator is superior however we present these results on the LR estimator as they may be of interest.

2 Definitions of a Power Law Distribution

As in Clauset et al. [3] we define the power law in two ways: one as a piecewise distribution and the other asymptotically as a regularly varying distribution. The piecewise power law distribution approximates the regularly varying distribution after a cutoff point which we assume is known. In this paper we will fit only the exponent of the piecewise power law distribution assuming the cutoff. We show below how this is identical to fitting the exponent of the Pareto distribution.

2.1 Piecewise Distribution

Let be a continuous random variable. We define the power law distribution as one that has a power law tail333We note Clauset et al. [3] defines the power law such that so the density is for an appropriate constant

| (1) |

with We call the power law exponent and the cutoff. Before we assume the tail of is defined by another function so that is a piecewise distribution. By taking the negative of the derivative of (1) we have that the density of is

| (2) |

Let us define the truncated distribution:

| (3) |

then one can integrate over the entire domain, to find that is a Pareto distribution with tail (1) and density (2) such that Now, for all

| (4) |

Thus in general We shall assume the cutoff is known (or has been fitted) and we are concerned only with fitting the exponent We refer the reader to Clauset et al. [3] for a Monte-Carlo method using the Kolmogorov-Smirnov statistic to fit

2.2 Regularly Varying Distribution

We shall briefly discuss a more general asymptotic representation of the power law distribution, the regularly varying distribution, and show how the piecewise distribution above approximates this distribution for large enough We mention here that the method for fitting in Clauset et al. [3] has useful statistical properties such as consistency when applied to regularly varying distributions, see [2].

Definition 1 (Regularly Varying Distribution, see e.g. [7]).

A continuous random variable has a regularly varying distribution if for all there exists a such that the tail distribution is a regularly varying function:

We see simply that the piecewise distribution (1) is a regularly varying distribution.

One can show (p2 of [15]) that a regularly varying distribution can be written as

where is a slowly varying function. We have the following properties (p18 of [15]) of slowly varying functions: for all

| (5) |

We now show that a regularly varying distribution can be approximated by the piecewise power law distribution (1).

Proposition 1.

If is a regularly varying distribution then for any there exists an such that with and

Proof.

Suppose for any that there exists an such that for and that

which is true by the definition of the above limits of slowly varying functions (5). ∎

Thus Proposition 1 shows that for there exists an such that for we have with

2.3 Examples

We now give an example of each of the two types of power law defined above. First a power law distribution that is piecewise (and regularly varying) that has an exponential then power law shape:

Example 1 (Piecewise power law, similar to (3.10) in [3]).

For define the continuous random variable by the piecewise tail

| (6) |

Second a power law distribution that is not piecewise but is regularly varying:

Example 2 (Lomax [9] or equivalently Pareto Type \@slowromancapii@ [1]).

For define the continuous random variable by the regularly varying tail

| (7) |

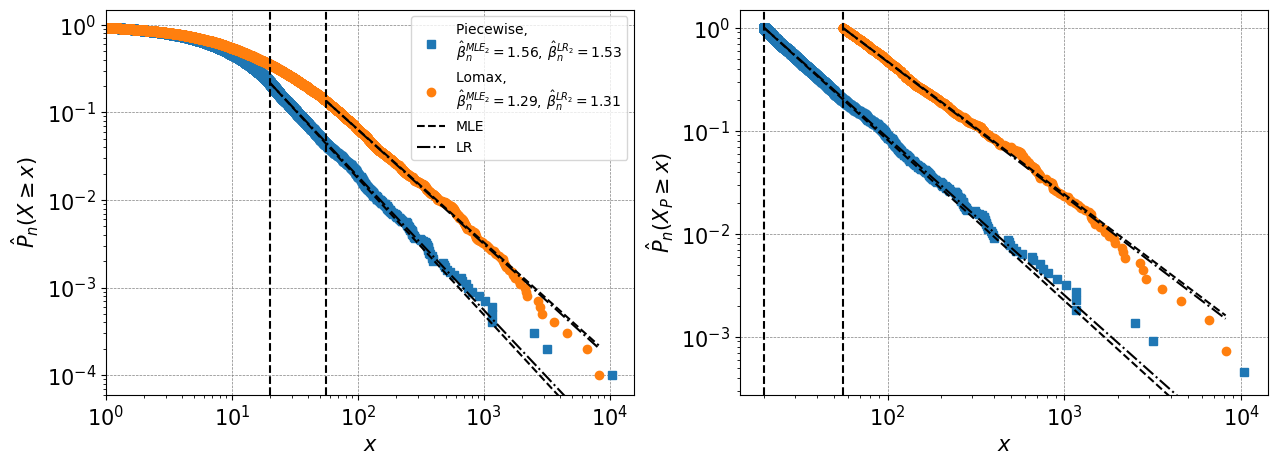

We now sample once from each of the distributions in the above examples and plot the empirical tail, see the appendix. We fit with the unbiased minimum variance MLE and roughly unbiased LR power law exponent estimators found in Sections 3.1 and 3.2. For the piecewise distribution the power law part can be viewed exactly as points from a Pareto distribution. For the Lomax distribution a cutoff point must be chosen so that beyond we can only approximate by a Pareto distribution. We choose the cutoff exactly for the piecewise distribution and only approximately using the technique in Clauset et al. [3] for the Lomax distribution. We see the fits with both methods for the exponent of this particular Lomax distribution are not very accurate even for a large sample size. Thus we urge caution when using these methods for fitting the exponent of a regularly varying distribution (we find evidence from simulation not presented here that in this case a larger initial sample with a subsequently larger is required to get a closer estimate consistently).

3 Fitting the Power Law Exponent

We consider an i.i.d. sample from a random variable that is from the power law tail part of the distribution (1). We assume and are known or have been fitted and emphasise is not from the sample but is the cutoff in (1) for which for all . We note from (4) we only have to fit the Pareto distribution and thus take from the Pareto distribution (3).

3.1 Maximum Likelihood Estimation

Suppose follows a power law distribution defined by (1). We saw that follows a Pareto distribution with density Assume is an i.i.d. sample from then the log-likelihood is defined

By maximising the log-likelihood (respectively the likelihood) with respect to we find that the MLE estimator for given is

| (8) |

The MLE estimator (8) for the Pareto distribution has been known for a long time with Clauset et al. [3] referencing Muniruzzaman, 1957 [10] as an early paper containing this result. We refer the reader to [3] for a summary of useful statistical properties of this estimator which includes consistency. We note that (8) is exactly the Hill’s estimator for the Pareto distribution [6]. In particular it can be shown, see Rytgaard [13], that has an inverse Gamma distribution with mean and variance

| (9) |

This MLE estimator (8), as noted in [13], can be corrected for bias. From (9) we see the unbiased MLE estimator is (for )

| (10) |

with mean and variance (for )

| (11) |

It is shown in [13] that the unbiased MLE estimator (10) has minimum variance and is asymptotically normally distributed with mean and variance and is a consistent estimator (the same for the untransformed MLE estimator (8) [3]).

Now approximating either MLE estimator with the asymptotic normal we have that % of values of the estimator lie within one standard deviation i.e. lie within the interval

| (12) |

Thus for the size of this interval to be less than we want

Therefore for a majority of the values of the MLE estimator to be within for example of either side of we would want a sample of size at least Now for many real-world situations see e.g. Table 6.1 in [3], thus the sample is required to be quite large before one is reasonably confident that the minimum variance MLE estimator is close to

3.2 Linear Regression

We shall now apply linear regression to fit the power law exponent to the power law model (1) using the empirical tail (one minus the empirical distribution function, see the appendix). Let us again assume is an i.i.d. sample from defined above. Then for any the empirical tail is

| (13) |

where the error has the following properties (see the appendix):

| (14) |

where is the truncated Binomial distribution that restricts the support to , for large

and

| (15) |

Applying ordinary least squares, see e.g. Section 3.1 of [14], to (16) the LR estimator for can be found to be

| (19) |

We note that if then by the change of base formula for logs that

and so due to cancellation it does not matter which base we take for the log in (19). As the are a function of the independent then they are independent. However as we will see from simulation, the mean of (19) is biased, indicating that the errors do not satisfy the properties of zero mean and constant variance to satisfy the further Gauss-Markov conditions, see e.g. Theorem 3.2 of [14]. Due to the relatively complicated distribution of (18) it is however hard to prove these properties formally. However as we have by (15) and (17) that

thus the estimator will tend almost surely to as and so the LR estimator (19) is a consistent estimator as noted by Quandt [11].

Now let be the ordered sample of thus

We have that the empirical tail, see the appendix, of the ordered sample is

| (20) |

As is from a Pareto distribution with parameters and then (specifically for the natural logarithm which we use from now on) is exponentially distributed with parameter . Now the result by Rényi, see [12], on the distribution of the order statistics for an exponential distribution gives

| (21) |

where (exponentially distributed with parameter ). Substitution of (20) and (21) into the the OLS estimator (19) leads to

| (22) |

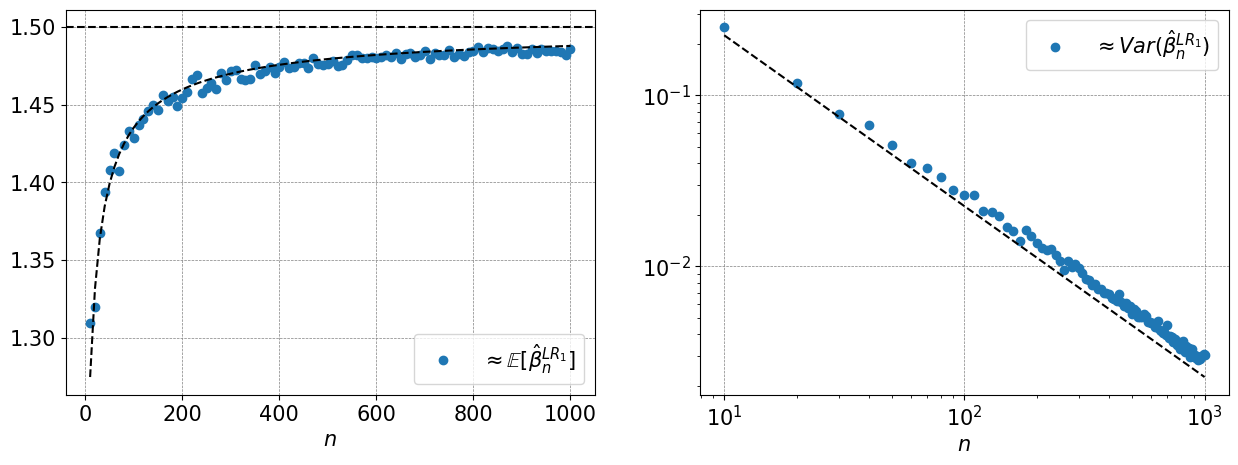

Thus we have a representation of the distribution of the LR estimator (19). It is a rather complicated formula which is beyond the scope of this paper to analyse fully so we make do with analysing the LR estimator via simulation. We note though that the term in the brackets of (22) does not depend on thus the distribution of the LR estimator is a random factor multiplied by From simulations, see Figure 2, we hypothesise two results:

| (23) | ||||

| (24) |

where is Euler’s number. The free parameter in (23) was approximated using non-linear least squares. Let

This function we propose is an approximation to the mean of the random factor in the brackets in (22). We see for finite and as so that (23) underestimates but tends to as We note that the mean approximation (23) is sigmoidal but imperfect especially for small and further simulation would be needed to check if it is still a good approximation above see Figure 2. It would be future work to determine more about the form of (22) and whether it has an analytic mean or variance. If an analytic mean exists then a strictly unbiased LR estimator can be found.

We can though still approximately correct for the bias to obtain the approximately unbiased, consistent LR estimator

| (25) |

with

| (26) |

We note though that this transformation is greater in terms of variance:

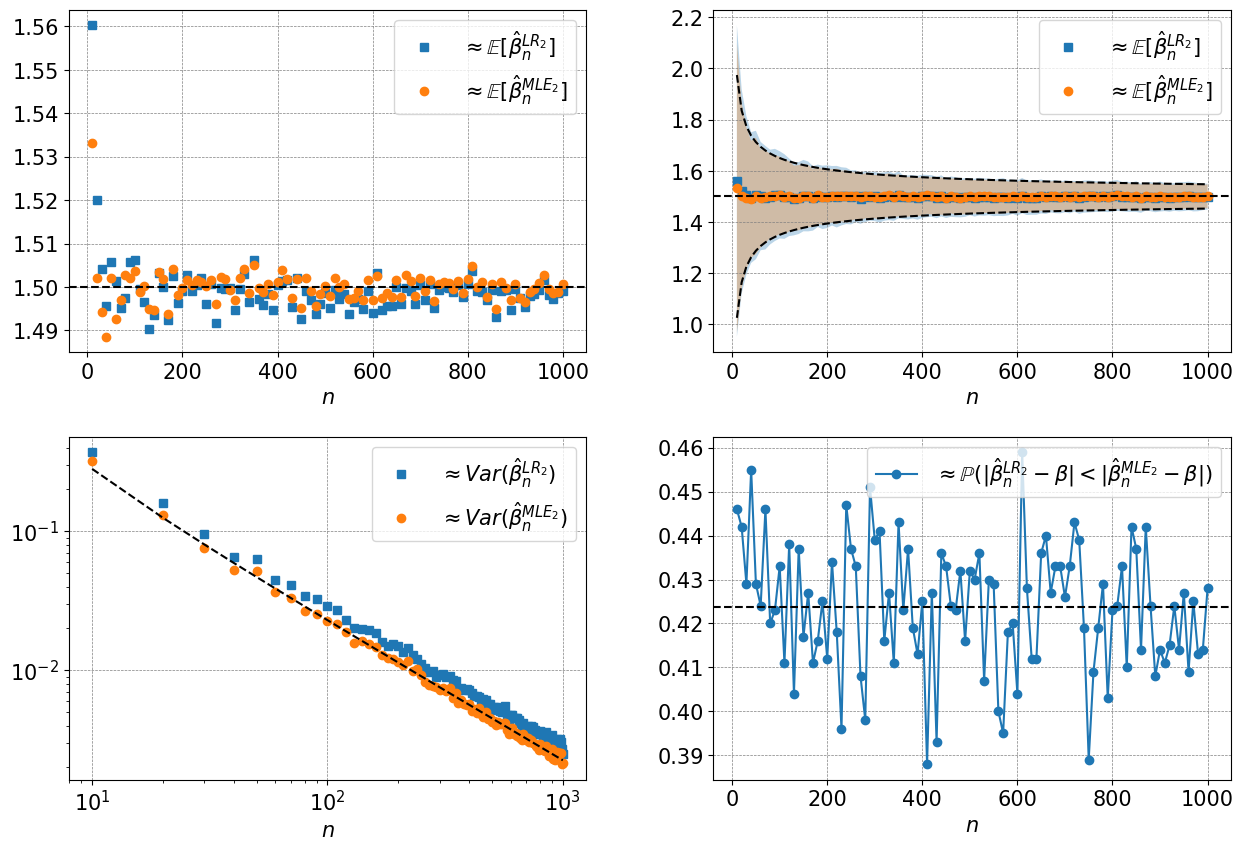

However we find through simulation, see Figure 2 and Figure 3 in the next section, that the variance of both LR estimators are not too much larger than the minimum variance of the unbiased MLE estimator.

3.3 Comparison Between LR and MLE with Simulations

In Figure 3 we compare the approximately unbiased LR estimator (25) with the minimum variance unbiased MLE estimator (10) on 1000 samples with sample sizes of We show in Figure 3 that although the transformed LR estimator is worse than the transformed MLE estimator it is comparable.

4 Conclusion

We use linear regression on the empirical tail to fit the exponent of the Pareto distribution that approximates or is identical to a continuous power law distribution given a cutoff value. We give an analytical representation of the distribution of the LR estimator and show evidence it’s mean underestimates the true exponent in a sigmoidal fashion. By factoring out a sigmoid function of the LR estimator we find comparable results to the transformed MLE estimator. Although the minimum variance unbiased transformed MLE estimator is superior we nonetheless present these novel results for the LR estimator.

References

- Arnold, [2008] Arnold, B. C. (2008). Pareto and generalized Pareto distributions. In Modeling income distributions and Lorenz curves, pages 119–145. Springer.

- Bhattacharya et al., [2020] Bhattacharya, A., Chen, B., van der Hofstad, R., and Zwart, B. (2020). Consistency of the plfit estimator for power-law data. arXiv preprint arXiv:2002.06870.

- Clauset et al., [2009] Clauset, A., Shalizi, C. R., and Newman, M. E. (2009). Power-law distributions in empirical data. SIAM review, 51(4):661–703.

- Forbes, [2023] Forbes, S. (2023). GitHub simulations code. https://github.com/saf92/power_law_fitting.

- Gabaix, [2009] Gabaix, X. (2009). Power laws in economics and finance. Annu. Rev. Econ., 1(1):255–294.

- Hill, [1975] Hill, B. M. (1975). A simple general approach to inference about the tail of a distribution. The annals of statistics, pages 1163–1174.

- Jessen and Mikosch, [2006] Jessen, H. A. and Mikosch, T. (2006). Regularly varying functions. Publications de L’institut Mathematique, 80(94):171–192.

- Johnson et al., [2005] Johnson, N. L., Kemp, A. W., and Kotz, S. (2005). Univariate discrete distributions. John Wiley & Sons.

- Lomax, [1954] Lomax, K. S. (1954). Business failures: Another example of the analysis of failure data. Journal of the American statistical association, 49(268):847–852.

- Muniruzzaman, [1957] Muniruzzaman, A. (1957). On measures of location and dispersion and tests of hypotheses in a pare to population. Calcutta Statistical Association Bulletin, 7(3):115–123.

- Quandt, [1964] Quandt, R. E. (1964). Old and mew methods of estimation and the Pareto distribution. Metrika, 10.

- Rényi, [1953] Rényi, A. (1953). On the theory of order statistics. Acta Math. Acad. Sci. Hung, 4:191–231.

- Rytgaard, [1990] Rytgaard, M. (1990). Estimation in the Pareto distribution. ASTIN Bulletin: The Journal of the IAA, 20(2):201–216.

- Seber and Lee, [2003] Seber, G. A. and Lee, A. J. (2003). Linear regression analysis. John Wiley & Sons.

- Seneta, [2006] Seneta, E. (2006). Regularly varying functions. Springer.

- Van der Vaart, [1998] Van der Vaart, A. W. (1998). Asymptotic statistics. Cambridge university press.

Appendix: the Empirical Tail

Suppose is an i.i.d. random sample from any random variable . The empirical cumulative distribution function is defined, see e.g. Section 19.1 of [16]

where is the indicator function. We define the empirical tail as

| (27) |

which takes values We also introduce the error of the empirical tail

We now state some results which follow from known results on the empirical cumulative distribution function, see e.g. Section 19.1 of [16]. We have

with mean and variance

By the law of large numbers

By the central limit theorem

in distribution.

From the above we have the following properties for

with mean and variance

and for large we can approximate the error

Let and be respectively the min and max of the sample Also let be the ordered sample of so that

Then we have that

and in particular for

Thus for this case the empirical tail with will not be zero and so

where is the truncated Binomial distribution, see e.g. Section 3.11 of [8], excluding values that take and thus with support