Particle Gibbs for Likelihood-Free Inference of State Space Models with Application to Stochastic Volatility

Abstract

State space models (SSMs) are widely used to describe dynamic systems. However, when the likelihood of the observations is intractable, parameter inference for SSMs cannot be easily carried out using standard Markov chain Monte Carlo or sequential Monte Carlo methods. In this paper, we propose a particle Gibbs sampler as a general strategy to handle SSMs with intractable likelihoods in the approximate Bayesian computation (ABC) setting. The proposed sampler incorporates a conditional auxiliary particle filter, which can help mitigate the weight degeneracy often encountered in ABC. To illustrate the methodology, we focus on a classic stochastic volatility model (SVM) used in finance and econometrics for analyzing and interpreting volatility. Simulation studies demonstrate the accuracy of our sampler for SVM parameter inference, compared to existing particle Gibbs samplers based on the conditional bootstrap filter. As a real data application, we apply the proposed sampler for fitting an SVM to S&P 500 Index time-series data during the 2008 financial crisis.

Keywords: approximate Bayesian computation, financial time series, particle MCMC, sequential Monte Carlo

1 Introduction

State space models (SSMs) describe dynamic systems via a time series of unobserved variables and observations generated conditional on those variables (Kitagawa,, 1998). The unobserved variables are commonly known as hidden states, and are often taken to be a discrete-time Markov process; then the SSM is specified via the transition probability of the hidden states and the likelihood of the observations. When the model also involves unknown parameters, Markov chain Monte Carlo (MCMC, Jacquier et al.,, 1994) and sequential Monte Carlo (SMC, Liu and West,, 2001; Storvik,, 2002; Carvalho et al.,, 2010) are general computational methods for inferring the parameters and hidden states together, by drawing samples from their joint posterior distribution in a Bayesian setting. However, the inference problem is more difficult when the likelihoods are intractable: examples are stochastic kinetic models in systems biology (Owen et al.,, 2015; Lowe et al.,, 2023) and stochastic volatility models with an intractable noise term (Vankov et al.,, 2019). In this likelihood-free setting, standard inference methods are no longer applicable, and this paper develops a new sampler which we illustrate in the context of stochastic volatility modeling.

In the analysis of financial time series, volatility is commonly used to quantify uncertainty or risk. Given a time series of observed prices , for the return is defined as and the volatility is defined as . A classic SVM (Jacquier et al.,, 1994, 2004; Taylor,, 2008), which has been widely used in option pricing and portfolio management, adopts the form of an SSM: for ,

| (1) |

where denotes the parameters, and are independent noise terms, and an initial distribution is assigned for . In the log-volatility process, contributes to the mean, is an auto-regressive parameter that governs the persistence (with required for second-order stationarity) (Jacquier et al.,, 2004), and is a noise level that governs the amount of autocorrelation. Model (1) has a hierarchical structure: we let denote the likelihood density, and denote the transition density.

In practice, and in Model (1) are often assumed to follow standard Gaussian distributions. Then we can integrate out analytically to directly obtain the likelihood , and the SVM parameters can be estimated by standard methods, e.g., maximum likelihood in a frequentist approach (Fridman and Harris,, 1998), and MCMC in a Bayesian approach (Jacquier et al.,, 1994). However, empirical studies suggest that the Gaussian assumption for may not adequately capture the heavy tails and skewness of financial time series (Engle and Patton,, 2001); as a more flexible alternative, the so-called stable distribution (Mandelbrot,, 1963; Nolan,, 1997) can be adopted for instead (Lombardi and Calzolari,, 2009; Vankov et al.,, 2019). The stable distribution does not have a closed-form density function, hence employing it for leads to an analytically intractable likelihood that is expensive to evaluate; this is the setting of interest in this paper.

Particle Markov chain Monte Carlo (PMCMC, Andrieu et al.,, 2010) is a general sampling approach that can be adapted to handle Model (1) in a Bayesian setting with intractable likelihoods. Initially proposed for inference of SSMs, PMCMC provides a class of algorithms that combine the features of MCMC and SMC; in this context, SMC methods (also known as particle filters) are well-suited for drawing posterior samples of the hidden states in an SSM (e.g., in Model (1)). To our best knowledge, PMCMC is the main type of approach for SVM parameter inference when it is not possible to integrate out (Vankov et al.,, 2019). Letting denote the joint prior for , PMCMC then targets the joint posterior of and , namely

if can be evaluated. (The corresponding version of PMCMC that bypasses this likelihood evaluation is discussed in Section 2.) When closed-form conditional distributions of the parameters are available, a special case of PMCMC, known as particle Gibbs, can be implemented. As applied here, the basic strategy of particle Gibbs alternates between sampling from and at each iteration. With the help of conjugate priors, sampling from can be straightforward. Sampling from can potentially be handled by SMC as for an SSM; e.g., one might apply SMC and obtain a particle approximation of , denoted by . However, it is not valid to simply substitute sampling from with sampling from in particle Gibbs, because doing so does not admit the target distribution as invariant (Andrieu et al.,, 2010). To correctly embed SMC within a particle Gibbs algorithm, the form of SMC known as conditional SMC (cSMC) should be implemented instead; we review cSMC algorithms in Section 2.2.

Approximate Bayesian computation (ABC) is a general technique that can be used to bypass the evaluation of an intractable or expensive likelihood, if one can directly simulate observations from the likelihood (Marin et al.,, 2012). Thus, to perform inference on Model (1) with an analytically intractable , ABC may be combined with cSMC. The basic idea is to introduce a sequence of auxiliary observations (that are sampled from the likelihood) and then assign weights according to the “distances” between the auxiliary observations and the actual observations; ABC-based methods are further reviewed in Section 2.3. It is straightforward to construct ABC versions of existing cSMC algorithms based on the bootstrap filter (BF, Gordon et al.,, 1993); however, in practice the particles they generate can tend to have many near-zero weights due to large “distances”, i.e., the algorithms suffer from weight degeneracy. In the SMC literature, specific techniques to mitigate weight degeneracy include the SMC sampler with annealed importance sampling (Del Moral et al.,, 2006), weight tempering via lookahead strategies (Lin et al.,, 2013), and drawing multiple descendants per particle (Hou and Wong,, 2023); however, as cSMC must be embedded within every iteration of particle Gibbs, these techniques would be computationally expensive to apply. In contrast, the auxiliary particle filter (APF, Pitt and Shephard,, 1999) is a common alternative to the BF that can help reduce weight degeneracy, since the resampling step of the APF accounts for the one-step-ahead observation.

In this paper, we use the APF as a strategy to reduce weight degeneracy and improve parameter estimation in the particle Gibbs and ABC setting. In related work, Vankov et al., (2019) proposed an ABC-based APF that uses auxiliary observations to assign importance weights for PMCMC. However, that ABC-based APF has only been embedded within a particle Metropolis-Hastings algorithm; a Gibbs sampler is preferred over Metropolis-Hastings proposals when closed-form conditional distributions are available for the parameters. Therefore, as the main contribution of this paper, we propose to embed an ABC-based APF within a particle Gibbs algorithm. We show that our proposed algorithm satisfies the form of cSMC, and thus admits the target posterior distribution as invariant. We then perform inference on Model (1) when is assumed to follow the stable distribution. The results demonstrate that our particle Gibbs algorithm significantly outperforms existing ones, thereby providing a useful computational method for handling SSMs with intractable likelihoods.

The paper is organized as follows: in Section 2, we review ABC and particle Gibbs methods, and present the proposed ABC-based particle Gibbs algorithm with a conditional auxiliary particle filter (ABC-PG-cAPF). In Section 3, we illustrate the effectiveness of the proposed sampler for inference of Model (1) with the stable distribution. In Section 4, we present a real data application by fitting an SVM to S&P 500 daily returns during the 2008–2009 financial crisis. In Section 5, we briefly summarize the paper and its contributions and discuss some potential future directions.

2 Methodology

2.1 Model setup

The stable distribution is defined via its characteristic function (Nolan,, 2020): we denote if follows a stable distribution with parameters for heavy-tailedness, for skewness, for scale and for location, and has characteristic function

Its corresponding density function, , does not have an analytical form in general; some basic facts are that if , (and undefined otherwise); if , (Mandelbrot,, 1963; Nolan,, 1997, 2020). Evaluation of is expensive and commonly needs to be approximated by the fast Fourier transform (Mittnik et al.,, 1999) or numerical integration (Nolan,, 1997, 1999), but it is feasible to simulate realizations of according to based on the work of Kanter, (1975) and Chambers et al., (1976); in this paper, we use the R package stabledist (Wuertz et al.,, 2016) for generating random draws of .

The main model of interest in this paper is then the SVM specified in (1) with and for , all independent. We also set according to the stationarity of the log-volatility process. The goal is to infer the parameters given a time series of returns . We take a Bayesian approach to inference and assign conjugate priors for the parameters:

i.e., the joint prior for is a truncated normal–inverse Gamma with hyperparameters , which we denote as ; the truncated support for ensures the required second-order stationarity of the log-volatility process. The conjugacy of these priors follows from the results of Bayesian linear regression, i.e., by defining

then is a truncated with , where

Thus, a Gibbs sampler update of only depends on these sufficient statistics. The choice of hyperparameters could be informed by previous empirical studies, or set to resemble a flat or weakly informative prior.

2.2 Particle Gibbs for the SVM with tractable likelihoods

In the SVM context, a particle Gibbs algorithm alternates between sampling from and . As described in the Introduction, sampling from requires the use of conditional SMC algorithms. The basic idea of cSMC is to take an input trajectory (i.e., a sample for ) as a reference and produce an output trajectory via SMC-style propagation; furthermore, cSMC accounts for all random variables generated during propagation via an extended target distribution of higher dimension (Chopin and Singh,, 2015). The steps for a sweep of particle Gibbs then consist of (i) updating the parameters based on the input trajectory, (ii) generating new trajectories based on the updated parameters and input trajectory, and (iii) selecting an output trajectory as input for the next iteration (Andrieu et al.,, 2010). The use of cSMC in particle Gibbs guarantees the target distribution is admitted as the invariant density. Here, we briefly review two existing cSMC algorithms that are applicable within particle Gibbs when the likelihood can be computed.

The first is the conditional bootstrap filter (cBF, Andrieu et al.,, 2010) as summarized in Algorithm 1. A key feature is that it preserves the input trajectory throughout propagation and resampling; holding intact, new trajectories are generated “conditional on” in SMC fashion; finally one of the trajectories (i.e., among the input trajectory and the generated trajectories) is selected to be the new input trajectory for the next iteration. As shown in Algorithm 1, for any particle with simulated at step , we denote the index of the ancestor particle of by , i.e., is propagated from . For simplicity, let , and for ; then the -th trajectory can be written as after propagation and resampling steps.

The second is the conditional bootstrap filter with ancestor sampling (cBFAS, Lindsten et al.,, 2014) as summarized in Algorithm 2. The cBF keeps the input trajectory intact, i.e., , and preserved throughout for all , so the early parts of generated trajectories may tend to closely resemble (or be identical to) the input trajectory, which when too extreme is known as path degeneracy. The key idea of cBFAS is to stochastically perturb the input trajectory by breaking it into pieces via ancestor sampling. Ancestor sampling, as presented in Algorithm 2, takes to be stochastic, so the input trajectory can be partially replaced by other generated trajectories at each step . Consequently, the input trajectory interacts much more with the other trajectories (Svensson et al.,, 2015), which can help cBFAS mitigate path degeneracy while maintaining the target distribution as invariant (Lindsten et al.,, 2014; Svensson et al.,, 2015).

2.3 Review of ABC methods and ABC-SMC methods

To briefly review ABC methods, consider observations and parameters where the likelihood is intractable and expensive to evaluate. Consequently, the posterior is also intractable. In this setting, ABC can be used for inference of if sampling from is straightforward. The basic idea of ABC methods is to construct an approximation to the posterior with the help of auxiliary observations (denoted by ) and an ABC kernel (denoted by ). The simplest example of an ABC method is a likelihood-free rejection sampling algorithm with a uniform kernel (i.e., for a chosen ) that implements the following steps: (1) sample a candidate from the prior ; (2) sample a realization from ; (3) accept if . Then accepted samples of follow the density defined by , which can be viewed as the ABC approximation of the extended distribution . In practice, Gaussian kernels (i.e., ) are more commonly used than uniform ones. It is clear that as and as . Therefore, an ABC kernel with a small can lead to many near-zero weights of generated candidates (or more rejected samples), while a larger can lead to more uniform weights (or more accepted samples); however, the accuracy of the ABC approximation will decrease as a tradeoff.

For an SSM with intractable likelihoods, we can similarly construct the ABC approximation of the corresponding extended distribution and sample from it using an SMC algorithm; this is known as ABC-SMC (Peters et al.,, 2012). Thus, the target distribution of ABC-SMC involves the auxiliary observations for evaluating importance weights and has the form

| (2) |

To sample from (2), Vankov et al., (2019) proposed an ABC-based APF, which is summarized in Algorithm 3 and applicable within a particle Metropolis-Hastings algorithm. Within a particle Gibbs algorithm, however, Algorithm 3 cannot be directly used (recall that particle Gibbs requires a cSMC setup to admit the target distribution as invariant). Thus, in the following we propose a new ABC-based APF, which we call the ABC-based conditional auxiliary particle filter (ABC-cAPF), that can be embedded within a particle Gibbs algorithm.

2.4 Likelihood-free ABC-based cSMC for the SVM

Now we consider the SVM with stable distribution as presented in Section 2.1. In the ABC setting with a chosen kernel , Model (1) can then be rewritten as

| (3) |

with and all independent for , and . Here, each , corresponds to an auxiliary observation for importance weight calculation according to . The extended posterior distribution of interest is then

| (4) |

and the goal is to sample from (4) in a likelihood-free manner, i.e., without computing . We shall focus on the particle Gibbs case, and develop ABC-based algorithms to sample from (4) that alternate between sampling from and .

The cBF and cBFAS algorithms can be applied in the ABC setting with slight modifications: in the step where we draw each , we also draw an auxiliary observation from and then assign the importance weight for the particle . We shall call these algorithms the ABC-based conditional bootstrap filter (ABC-cBF) and ABC-based conditional bootstrap filter with ancestor sampling (ABC-cBFAS), respectively. However, these two algorithms can encounter severe weight degeneracy in practice, if we choose a small in the ABC kernel to obtain an accurate approximation of the true target distribution. Thus, in the following we also propose a novel ABC-based cSMC algorithm using the auxiliary particle filter as the building block.

We shall call this third algorithm the ABC-based conditional auxiliary particle filter (ABC-cAPF), as presented in Algorithm 4. To initialize the ABC-cAPF at , particles, , are sampled from the log-normal distribution and is assigned the initial log-volatility of the input trajectory. Then after the -th propagation step (), the -th particle is set to be the input trajectory and the remaining particles are generated with weights that satisfy

for . Following the concept of properly weighted particles in SMC (Liu,, 2001), this weight ensures that the set of generated particles is properly weighted with respect to . As an important feature of the APF (Pitt and Shephard,, 1999) when propagating the particles from to , the tempered weights , i.e., the adjusted importance weights that incorporate the one-step-ahead observation , are computed and utilized; in the ABC setting, the computation of these tempered weights require an intractable integration, namely

| (5) |

where the double integral does not have a closed form; Vankov et al., (2019) suggest approximating it with a more heavy-tailed distribution such as a -class distribution.

Specifically, given , we construct an approximation of the stable distribution noise with a standard Cauchy noise as (thus and ). Then we approximate with a linear combination of and to match the conditional mean and variance, which gives , so is approximately proportional to

Note that the quality of the integral approximation in (5) does not influence the validity of ABC-cAPF; however, the tempered weights should cover the high-density regions of the true importance weights for a more efficient algorithm.

For , resampling and propagation are implemented with the tempered weights, but otherwise similar to the cBF: (i) resample the first particles from proportional to the tempered weights while leaving the -th particle intact as the input trajectory; (ii) propagate the resampled particles as in the cBF; (iii) compute the importance weights of the propagated particles so that cAPF targets the same density as cBF, i.e., the weights of the propagated particles satisfy

Each of the three algorithms, i.e., ABC-cBF, ABC-cBFAS, and ABC-cAPF, can be combined with a Gibbs sampler for the parameters to construct particle Gibbs samplers for (4). We call these algorithms the ABC-based particle Gibbs with ABC-cBF (ABC-PG-cBF), ABC-based particle Gibbs with ABC-cBFAS (ABC-PG-cBFAS), and ABC-based particle Gibbs with the conditional auxiliary particle filter (ABC-PG-cAPF), respectively. Algorithm 5 shows how the ABC-cAPF is embedded within the particle Gibbs sampler: each Gibbs sweep uses the ABC-cAPF to draw an output trajectory for (given the current draw of and the input trajectory), and then draws an updated from its closed-form NIG conditional posterior (given the output trajectory, which becomes the input trajectory for the next iteration). The ABC-PG-cBF and ABC-PG-cBFAS algorithms are constructed analogously. To initialize the particle Gibbs sampler, we draw parameters from and an input trajectory from the log-normal distribution given those parameters.

Proposition 1.

Proof.

See Section S1 of the Supplementary Material. ∎

While ABC-PG-cAPF is proposed with Model (3) as the focus in this paper, the computational strategy is not limited to this specific problem and can be applied to other SSMs with intractable likelihoods, e.g., stochastic kinetic models (Owen et al.,, 2015; Lowe et al.,, 2023) and models with likelihoods that follow g-and-k distributions (Rayner and MacGillivray,, 2002; Drovandi and Pettitt,, 2011).

3 Simulation study

We consider the model described in Equation (3) with a second-order stationary log-volatility process. Since conditional on follows a log-normal distribution, we have and . Therefore, the (squared) coefficient of variation, , can be written as . Practical ranges of that have been suggested from empirical analyses are , or more loosely, (Jacquier et al.,, 1994); following their simulation study we take , , and set . Given the values of , , and , the corresponding values of and can be easily computed. Following the setup for in Vankov et al., (2019), we hold and fixed throughout and consider respectively as three experimental settings; (1.75, 0.1) gives the least heavy-tailed stable distribution and the least (right) skewness and is expected to be the easiest to handle; (1.5, -0.3) gives the most heavy-tailed stable distribution and the most (left) skewness and is expected to be the hardest to handle; (1.7, 0.3) has heavy-tailedness between that of the above two cases and the most (right) skewness. Following Yang et al., (2018), we assign a weakly informative conjugate prior for with , , and .

For each combination of , CV, and , we simulated a time series of length observations. We then ran each of the particle Gibbs samplers (ABC-PG-cBF, ABC-PG-cBFAS, and ABC-PG-cAPF) using particles for the embedded cSMC algorithm and a Gaussian kernel with . We discarded the first 2000 iterations as burn-in and took the 5000 iterations after the burn-in period as the posterior sample. The posterior means are treated as the Bayes’ estimates for the parameters. To compare the performances of the different PG samplers, we repeated this procedure for 100 simulated datasets. The simulation results, summarized by computing the root-mean-squared errors (RMSEs) of the parameter estimates over the 100 repetitions, are presented in Tables 1, 2, and 3 for , respectively.

| CV | Algorithm | RMSE | RMSE | RMSE | |

|---|---|---|---|---|---|

| ABC-PG-cBF | 0.518 | 0.068 | 0.463 | ||

| 10 | 0.9 | ABC-PG-cBFAS | 0.594 | 0.078 | 0.505 |

| ABC-PG-cAPF | 0.173 | 0.025 | 0.141 | ||

| ABC-PG-cBF | 0.647 | 0.086 | 0.420 | ||

| 10 | 0.95 | ABC-PG-cBFAS | 0.747 | 0.099 | 0.489 |

| ABC-PG-cAPF | 0.324 | 0.049 | 0.145 | ||

| ABC-PG-cBF | 0.817 | 0.112 | 0.414 | ||

| 10 | 0.98 | ABC-PG-cBFAS | 0.916 | 0.131 | 0.510 |

| ABC-PG-cAPF | 0.547 | 0.079 | 0.214 | ||

| ABC-PG-cBF | 0.571 | 0.080 | 0.441 | ||

| 1 | 0.9 | ABC-PG-cBFAS | 0.663 | 0.094 | 0.486 |

| ABC-PG-cAPF | 0.157 | 0.029 | 0.179 | ||

| ABC-PG-cBF | 0.819 | 0.116 | 0.466 | ||

| 1 | 0.95 | ABC-PG-cBFAS | 0.946 | 0.134 | 0.524 |

| ABC-PG-cAPF | 0.425 | 0.068 | 0.216 | ||

| ABC-PG-cBF | 0.988 | 0.142 | 0.449 | ||

| 1 | 0.98 | ABC-PG-cBFAS | 1.125 | 0.161 | 0.516 |

| ABC-PG-cAPF | 0.645 | 0.099 | 0.245 | ||

| ABC-PG-cBF | 0.578 | 0.084 | 0.455 | ||

| 0.1 | 0.9 | ABC-PG-cBFAS | 0.709 | 0.103 | 0.520 |

| ABC-PG-cAPF | 0.171 | 0.033 | 0.254 | ||

| ABC-PG-cBF | 0.855 | 0.123 | 0.463 | ||

| 0.1 | 0.95 | ABC-PG-cBFAS | 1.012 | 0.146 | 0.526 |

| ABC-PG-cAPF | 0.484 | 0.078 | 0.259 | ||

| ABC-PG-cBF | 1.038 | 0.150 | 0.459 | ||

| 0.1 | 0.98 | ABC-PG-cBFAS | 1.214 | 0.176 | 0.534 |

| ABC-PG-cAPF | 0.699 | 0.109 | 0.268 |

| CV | Algorithm | RMSE | RMSE | RMSE | |

|---|---|---|---|---|---|

| ABC-PG-cBF | 0.514 | 0.067 | 0.455 | ||

| 10 | 0.9 | ABC-PG-cBFAS | 0.610 | 0.079 | 0.503 |

| ABC-PG-cAPF | 0.170 | 0.025 | 0.144 | ||

| ABC-PG-cBF | 0.653 | 0.087 | 0.431 | ||

| 10 | 0.95 | ABC-PG-cBFAS | 0.768 | 0.102 | 0.502 |

| ABC-PG-cAPF | 0.335 | 0.051 | 0.156 | ||

| ABC-PG-cBF | 0.879 | 0.120 | 0.475 | ||

| 10 | 0.98 | ABC-PG-cBFAS | 0.993 | 0.136 | 0.530 |

| ABC-PG-cAPF | 0.557 | 0.080 | 0.218 | ||

| ABC-PG-cBF | 0.564 | 0.080 | 0.435 | ||

| 1 | 0.9 | ABC-PG-cBFAS | 0.686 | 0.098 | 0.503 |

| ABC-PG-cAPF | 0.148 | 0.029 | 0.178 | ||

| ABC-PG-cBF | 0.831 | 0.117 | 0.477 | ||

| 1 | 0.95 | ABC-PG-cBFAS | 0.959 | 0.136 | 0.531 |

| ABC-PG-cAPF | 0.443 | 0.071 | 0.226 | ||

| ABC-PG-cBF | 1.025 | 0.148 | 0.472 | ||

| 1 | 0.98 | ABC-PG-cBFAS | 1.167 | 0.167 | 0.550 |

| ABC-PG-cAPF | 0.677 | 0.104 | 0.265 | ||

| ABC-PG-cBF | 0.622 | 0.089 | 0.495 | ||

| 0.1 | 0.9 | ABC-PG-cBFAS | 0.745 | 0.109 | 0.548 |

| ABC-PG-cAPF | 0.200 | 0.037 | 0.265 | ||

| ABC-PG-cBF | 0.892 | 0.129 | 0.487 | ||

| 0.1 | 0.95 | ABC-PG-cBFAS | 1.041 | 0.151 | 0.550 |

| ABC-PG-cAPF | 0.482 | 0.078 | 0.261 | ||

| ABC-PG-cBF | 1.101 | 0.160 | 0.504 | ||

| 0.1 | 0.98 | ABC-PG-cBFAS | 1.246 | 0.181 | 0.560 |

| ABC-PG-cAPF | 0.707 | 0.110 | 0.274 |

| CV | Algorithm | RMSE | RMSE | RMSE | |

|---|---|---|---|---|---|

| ABC-PG-cBF | 0.681 | 0.088 | 0.614 | ||

| 10 | 0.9 | ABC-PG-cBFAS | 0.812 | 0.105 | 0.722 |

| ABC-PG-cAPF | 0.174 | 0.027 | 0.158 | ||

| ABC-PG-cBF | 0.830 | 0.110 | 0.596 | ||

| 10 | 0.95 | ABC-PG-cBFAS | 0.986 | 0.130 | 0.702 |

| ABC-PG-cAPF | 0.378 | 0.057 | 0.179 | ||

| ABC-PG-cBF | 1.007 | 0.137 | 0.566 | ||

| 10 | 0.98 | ABC-PG-cBFAS | 1.174 | 0.158 | 0.685 |

| ABC-PG-cAPF | 0.615 | 0.090 | 0.253 | ||

| ABC-PG-cBF | 0.714 | 0.101 | 0.569 | ||

| 1 | 0.9 | ABC-PG-cBFAS | 0.889 | 0.126 | 0.671 |

| ABC-PG-cAPF | 0.174 | 0.035 | 0.202 | ||

| ABC-PG-cBF | 0.960 | 0.136 | 0.580 | ||

| 1 | 0.95 | ABC-PG-cBFAS | 1.153 | 0.163 | 0.684 |

| ABC-PG-cAPF | 0.482 | 0.078 | 0.254 | ||

| ABC-PG-cBF | 1.145 | 0.164 | 0.579 | ||

| 1 | 0.98 | ABC-PG-cBFAS | 1.338 | 0.192 | 0.681 |

| ABC-PG-cAPF | 0.708 | 0.111 | 0.290 | ||

| ABC-PG-cBF | 0.739 | 0.108 | 0.587 | ||

| 0.1 | 0.9 | ABC-PG-cBFAS | 0.896 | 0.131 | 0.674 |

| ABC-PG-cAPF | 0.204 | 0.041 | 0.286 | ||

| ABC-PG-cBF | 1.018 | 0.148 | 0.583 | ||

| 0.1 | 0.95 | ABC-PG-cBFAS | 1.209 | 0.176 | 0.682 |

| ABC-PG-cAPF | 0.553 | 0.091 | 0.306 | ||

| ABC-PG-cBF | 1.210 | 0.176 | 0.591 | ||

| 0.1 | 0.98 | ABC-PG-cBFAS | 1.392 | 0.203 | 0.671 |

| ABC-PG-cAPF | 0.754 | 0.120 | 0.309 |

The numerical results show that the proposed ABC-PG-cAPF outperforms the corresponding cBF-based algorithms with parameter RMSEs that are 30–70% smaller, depending on the scenario considered. The Gaussian ABC kernel tends to produce very uneven particle weights and the cBF-based algorithms become hindered by weight degeneracy. While ancestor sampling (in cBFAS) is designed to tackle path degeneracy, doing so has limited effectiveness for weight degeneracy and appears to be slightly worse than cBF in these scenarios. In contrast, the weight tempering strategy of the cAPF helps reduce the variability in the weights, which leads to more plausible trajectories being sampled, and in turn improves the accuracy of the parameter estimates.

Some specific patterns in the results can be noted: the RMSEs tend to be higher for a smaller (i.e., a larger or a smaller CV) or a more heavy-tailed (i.e., a smaller ). Intuitively, volatility is more persistent for a smaller ; however, can still have large fluctuations due to the heavy tails of , so it may be difficult in practice to disentangle the variability coming from and . More heavy-tailed ’s make the estimation problem even more challenging. Finally in the ABC setting, a smaller is generally preferred for a better ABC approximation of the target distribution; however, the cSMC algorithms may suffer from more severe weight degeneracy when is very small. When we decreased to 0.0005, the parameter RMSEs were worse for all three algorithms, but ABC-PG-cAPF was the most robust; see Section S2 in the Supplementary Material for details.

4 Application: the S&P 500 Index during the Financial Crisis in 2008

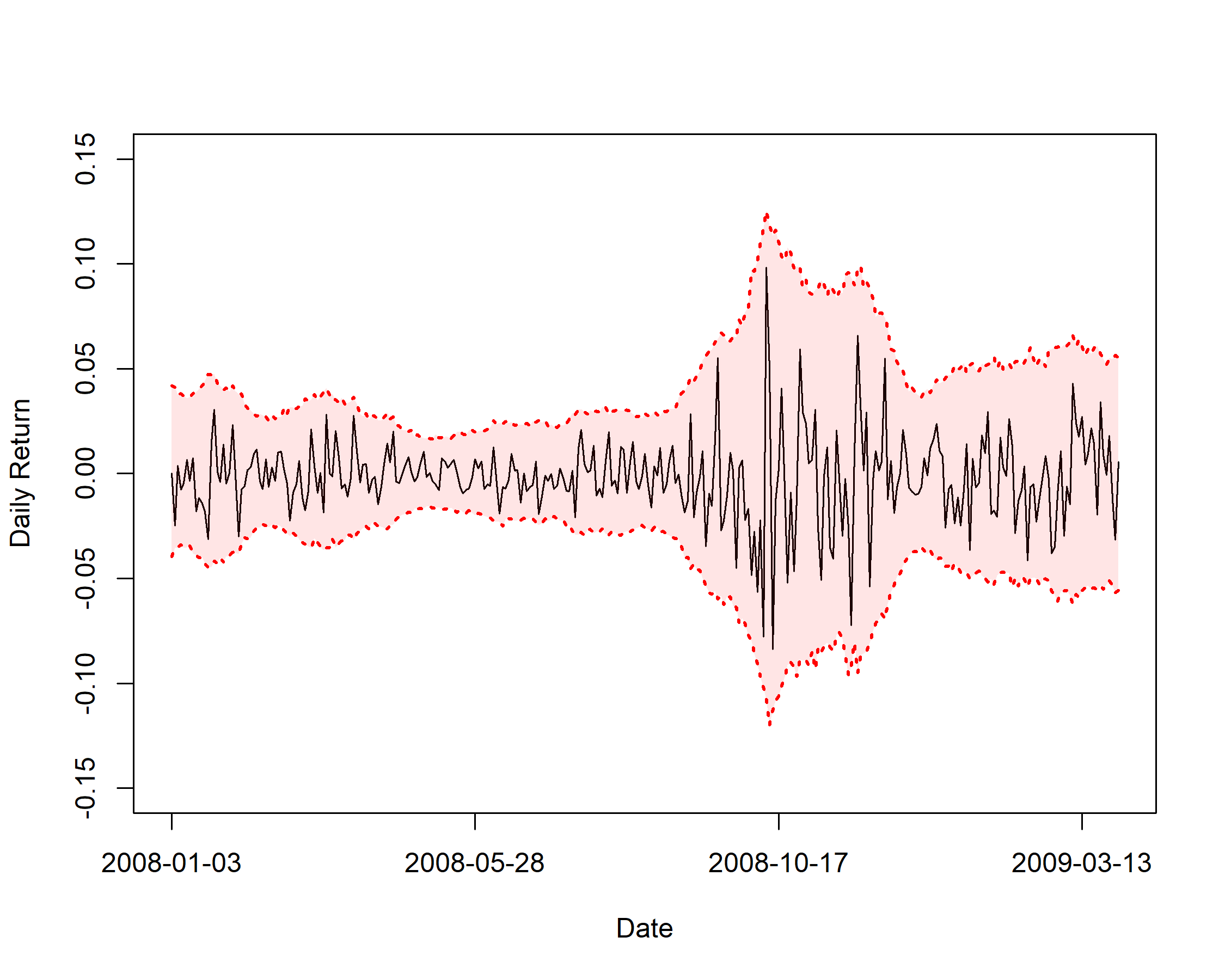

We now apply the ABC-PG-cAPF algorithm to fit an SVM to time-series data obtained from the Standard & Poor 500 (S&P 500) index. Given the time-series of the daily price (i.e., the average of the open and close price on each day), we computed the daily returns for the period January 2008 to March 2009. These are displayed via the black line in the left panel of Figure 1. The large fluctuations around October 2008 indicate the climax of the well-known global financial crisis. Following the suggestion of Kabašinskas et al., (2009) to take stable distribution parameters in the ranges and for financial data, we set and to be the midpoints of these ranges for our analysis.

|

|

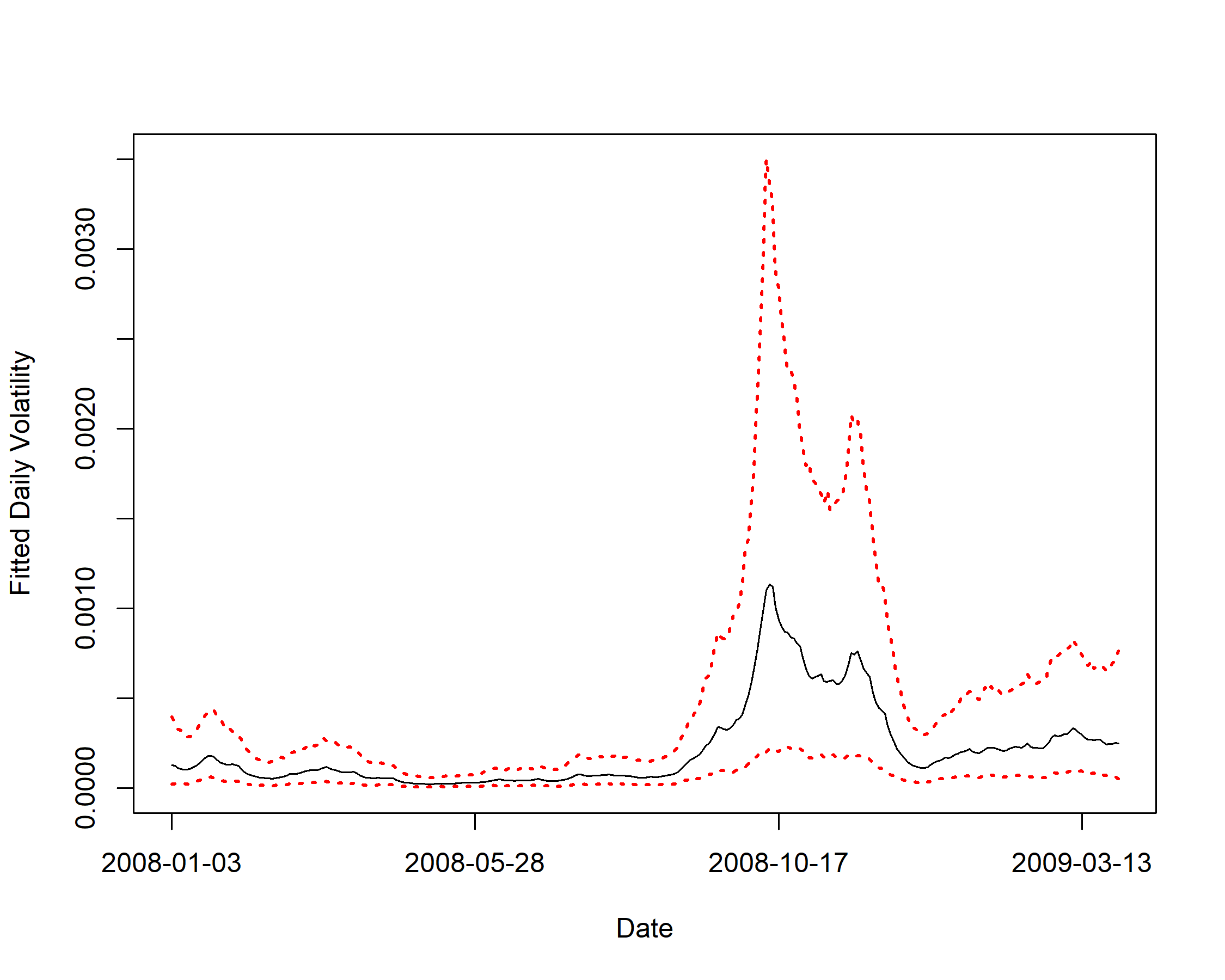

We estimated the SVM parameters based on these data, running 2000 burn-in iterations of ABC-PG-cAPF followed by 5000 sampling iterations, using particles and a Gaussian ABC kernel with . The Bayes’ estimates (posterior means) and credible intervals of the parameters are reported in Table 4. In the right panel of Figure 1, we plot the fitted daily volatility along with a central 95% credible interval based on the posterior samples; the estimated volatility peaks at the climax of the financial crisis. Lastly, the estimated 95% credible intervals for the returns are also superimposed on the left panel, which were computed via the samples generated from for each draw of at each time and indicate a good fit to the data.

| Parameter | Estimate | 95% credible interval |

|---|---|---|

| -0.294 | (-0.639, -0.042) | |

| 0.967 | (0.930, 0.995) | |

| 0.098 | (0.052, 0.174) |

5 Conclusion and Discussion

In this paper, we proposed an ABC-based cAPF embedded within a particle Gibbs sampler for likelihood-free inference of the SVM. Our proposed sampler builds upon a rich SMC and SVM literature, e.g., the idea of using MCMC for parameter estimation in SVMs (Jacquier et al.,, 1994), particle Gibbs samplers for state space models (Andrieu et al.,, 2010), and ABC-based PMCMC for SVM inference with intractable likelihoods (Vankov et al.,, 2019). Compared to existing particle Gibbs samplers, the proposed ABC-PG-cAPF algorithm produces more accurate parameter estimates with the help of its weight tempering strategy, as demonstrated in the simulation study.

Our sampler can be adapted for broader use with different models and setups. First, if there are any model parameters without closed-form conditional distributions (e.g., chosen to be a -distribution and thus no conjugacy available for ), or if the hyperparameters of the stable distribution also need to be estimated, this can be handled by incorporating an additional block of Metropolis updates within the particle Gibbs algorithm. However, the tuning of Metropolis kernels needs to be done carefully (Vankov et al.,, 2019). Second, the computation of the tempered weights for cAPF can be adapted as appropriate to cover the high-density regions of the true importance weights. For example, if the likelihood involves a stable distribution with , the Lévy distribution (which corresponds to a stable distribution with ) can be a better choice of approximating distribution than a Cauchy. However, for a stable distribution with or other kinds of intractable distributions, alternative approximation schemes or numerical methods might be necessary to perform weight tempering efficiently. Finally, other application areas that use SSMs with intractable likelihoods could be considered, e.g., stochastic kinetic models in systems biology (Owen et al.,, 2015; Lowe et al.,, 2023).

Acknowledgments

This work was partially supported by Discovery Grant RGPIN-2019-04771 from the Natural Sciences and Engineering Research Council of Canada.

References

- Andrieu et al., (2010) Andrieu, C., Doucet, A., and Holenstein, R. (2010). Particle Markov chain Monte Carlo methods. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 72(3):269–342.

- Carvalho et al., (2010) Carvalho, C. M., Johannes, M. S., Lopes, H. F., and Polson, N. G. (2010). Particle learning and smoothing. Statistical Science, 25(1):88–106.

- Chambers et al., (1976) Chambers, J. M., Mallows, C. L., and Stuck, B. (1976). A method for simulating stable random variables. Journal of the American Statistical Association, 71(354):340–344.

- Chopin and Singh, (2015) Chopin, N. and Singh, S. S. (2015). On particle Gibbs sampling. Bernoulli, 21(3):1855.

- Del Moral et al., (2006) Del Moral, P., Doucet, A., and Jasra, A. (2006). Sequential Monte Carlo samplers. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 68(3):411–436.

- Drovandi and Pettitt, (2011) Drovandi, C. C. and Pettitt, A. N. (2011). Likelihood-free Bayesian estimation of multivariate quantile distributions. Computational Statistics & Data Analysis, 55(9):2541–2556.

- Engle and Patton, (2001) Engle, R. F. and Patton, A. J. (2001). What good is a volatility model? Quantitative Finance, 1:237–245.

- Fridman and Harris, (1998) Fridman, M. and Harris, L. (1998). A maximum likelihood approach for non-Gaussian stochastic volatility models. Journal of Business & Economic Statistics, 16(3):284–291.

- Gordon et al., (1993) Gordon, N., Salmond, D., and Smith, A. (1993). Novel approach to nonlinear/non-Gaussian Bayesian state estimation. IEE Proceedings F (Radar and Signal Processing), 140(2):107–113.

- Hou and Wong, (2023) Hou, Z. and Wong, S. W. (2023). Estimating Boltzmann averages for protein structural quantities using sequential Monte Carlo. Statistica Sinica, to appear.

- Jacquier et al., (1994) Jacquier, E., Polson, N. G., and Rossi, P. E. (1994). Bayesian analysis of stochastic volatility models. Journal of Business & Economic Statistics, 12(4):371–389.

- Jacquier et al., (2004) Jacquier, E., Polson, N. G., and Rossi, P. E. (2004). Bayesian analysis of stochastic volatility models with fat-tails and correlated errors. Journal of Econometrics, 122(1):185–212.

- Kabašinskas et al., (2009) Kabašinskas, A., Rachev, S., Sakalauskas, L., Sun, W., and Belovas, I. (2009). Alpha-stable paradigm in financial markets. Journal of Computational Analysis and Applications, 11(4):641–668.

- Kanter, (1975) Kanter, M. (1975). Stable densities under change of scale and total variation inequalities. The Annals of Probability, 3(4):697–707.

- Kitagawa, (1998) Kitagawa, G. (1998). A self-organizing state-space mode. Journal of the American Statistical Association, 93(443):1203–1215.

- Lin et al., (2013) Lin, M., Chen, R., and Liu, J. S. (2013). Lookahead strategies for sequential Monte Carlo. Statistical Science, 28(1):69–94.

- Lindsten et al., (2014) Lindsten, F., Jordan, M. I., and Schon, T. B. (2014). Particle Gibbs with ancestor sampling. Journal of Machine Learning Research, 15(1):2145–2184.

- Liu and West, (2001) Liu, J. and West, M. (2001). Combined Parameter and State Estimation in Simulation-Based Filtering. Springer.

- Liu, (2001) Liu, J. S. (2001). Monte Carlo Strategies in Scientific Computing. Springer.

- Lombardi and Calzolari, (2009) Lombardi, M. J. and Calzolari, G. (2009). Indirect estimation of -stable stochastic volatility models. Computational Statistics & Data Analysis, 53(6):2298–2308.

- Lowe et al., (2023) Lowe, T. E., Golightly, A., and Sherlock, C. (2023). Accelerating inference for stochastic kinetic models. Computational Statistics & Data Analysis, 185:107760.

- Mandelbrot, (1963) Mandelbrot, B. (1963). The variation of certain speculative prices. The Journal of Business, 36(4):394–419.

- Marin et al., (2012) Marin, J.-M., Pudlo, P., Robert, C. P., and Ryder, R. J. (2012). Approximate Bayesian computational methods. Statistics and Computing, 22(6):1167–1180.

- Mittnik et al., (1999) Mittnik, S., Doganoglu, T., and Chenyao, D. (1999). Computing the probability density function of the stable paretian distribution. Mathematical and Computer Modelling, 29(10-12):235–240.

- Nolan, (1997) Nolan, J. P. (1997). Numerical calculation of stable densities and distribution functions. Communications in Statistics. Stochastic Models, 13(4):759–774.

- Nolan, (1999) Nolan, J. P. (1999). An algorithm for evaluating stable densities in Zolotarev’s (M) parameterization. Mathematical and Computer Modelling, 29(10-12):229–233.

- Nolan, (2020) Nolan, J. P. (2020). Univariate Stable Distributions. Springer.

- Owen et al., (2015) Owen, J., Wilkinson, D. J., and Gillespie, C. S. (2015). Scalable inference for Markov processes with intractable likelihoods. Statistics and Computing, 25:145–156.

- Peters et al., (2012) Peters, G. W., Fan, Y., and Sisson, S. A. (2012). On sequential Monte Carlo, partial rejection control and approximate Bayesian computation. Statistics and Computing, 22:1209–1222.

- Pitt and Shephard, (1999) Pitt, M. K. and Shephard, N. (1999). Filtering via simulation: auxiliary particle filters. Journal of the American Statistical Association, 94(446):590–599.

- Rayner and MacGillivray, (2002) Rayner, G. D. and MacGillivray, H. L. (2002). Numerical maximum likelihood estimation for the g-and-k and generalized g-and-h distributions. Statistics and Computing, 12(1):57–75.

- Storvik, (2002) Storvik, G. (2002). Particle filters for state-space models with the presence of unknown static parameters. IEEE Transactions on Signal Processing, 50(2):281–289.

- Svensson et al., (2015) Svensson, A., Schön, T. B., and Kok, M. (2015). Nonlinear state space smoothing using the conditional particle filter. IFAC-PapersOnLine, 48(28):975–980.

- Taylor, (2008) Taylor, S. J. (2008). Modelling Financial Time Series. World scientific.

- Vankov et al., (2019) Vankov, E. R., Guindani, M., and Ensor, K. B. (2019). Filtering and estimation for a class of stochastic volatility models with intractable likelihoods. Bayesian Analysis, 14(1):29–52.

- Wuertz et al., (2016) Wuertz, D., Maechler, M., and Rmetrics core team members. (2016). stabledist: Stable Distribution Functions. R package version 0.7-1.

- Yang et al., (2018) Yang, B., Stroud, J. R., and Huerta, G. (2018). Sequential Monte Carlo smoothing with parameter estimation. Bayesian Analysis, 13(4):1137–1161.

Supplementary material

Appendix S1 Proof of Proposition 1

In the ABC setting, we extend the dimension of the target distribution by introducing a sequence of auxiliary observations . For simplicity, write and for , and we denote the target distribution by (dropping to simplify notation as it is known and fixed). Then we have the same target distribution as Andrieu et al., (2010), where they showed that particle Gibbs with the conditional bootstrap filter (cBF), i.e., Algorithm 1 in the main text, admits the target distribution as the invariant distribution under some mild assumptions (i.e., Assumptions 5-7 in Andrieu et al., (2010)). Here, we shall show that Algorithm 5 in the main text also admits the target distribution as the invariant distribution under the same mild assumptions.

The sweep of particle Gibbs has three steps (see Section 4.5 in Andrieu et al., (2010)): for cBF, given an input trajectory ,

-

1.

update the parameters, denoted by

-

2.

generate new trajectories with ancestor indices conditional on and using cBF

-

3.

draw a trajectory from the union of the generated trajectories and the input trajectory, as the new input trajectory for the next iteration

and we propose to substitute the cBF for Step 2 with the conditional auxiliary particle filter (cAPF). Therefore, to prove the proposition, it is sufficient to show that with the same input trajectory, the cBF and the cAPF target the same distribution.

Write the target distribution of the cBF at each as for and (see Equation (33) in Andrieu et al., (2010) for the explicit form); for a particle , its particle weight generated by cBF (Algorithm 1) is denoted by , and its particle weight generated by cAPF (Algorithm 4) is denoted by . Then for the input trajectory , it is obvious that we have . The input trajectory is set to be the -th particle, i.e., , for each . Furthermore, for each generated trajectory , , we have

| (S6) |

where is any squared integrable function and with denoting the tempered weights in cAPF as defined in Equation (5) in the main paper. Given the same input trajectory, Equation (S6) justifies that the particles produced by cBF and the particles produced by cAPF are properly weighted with respect to the same distribution (Liu,, 2001), and thus these two algorithms target the same distribution at each step .

Appendix S2 Impact of a smaller in the ABC kernel

To further investigate the influence of in the ABC kernel, we set while keeping the rest of the settings to be the same as in the Simulation Study of the main paper. The results for the three algorithms, reported via parameter RMSEs analogous to Tables 1–3 of the main paper, are shown in Tables S5, S6 and S7. A comparison of these results with indicates that all three algorithms overall have higher RMSEs with this smaller , but ABC-PG-cAPF still consistently outperforms the other two algorithms. Moreover, these results suggest that weight degeneracy is more severe for ABC-PG-cBF and ABC-PG-cBFAS with the smaller , as their RMSEs increased significantly more than those of ABC-PG-cAPF. Therefore, these results provide further numerical evidence that the proposed cAPF-based algorithm is more robust to weight degeneracy.

| CV | Algorithm | RMSE | RMSE | RMSE | |

|---|---|---|---|---|---|

| ABC-PG-cBF | 0.740 | 0.098 | 0.598 | ||

| 10 | 0.9 | ABC-PG-cBFAS | 0.874 | 0.114 | 0.691 |

| ABC-PG-cAPF | 0.214 | 0.037 | 0.163 | ||

| ABC-PG-cBF | 0.901 | 0.121 | 0.596 | ||

| 10 | 0.95 | ABC-PG-cBFAS | 1.050 | 0.139 | 0.690 |

| ABC-PG-cAPF | 0.447 | 0.068 | 0.201 | ||

| ABC-PG-cBF | 1.095 | 0.150 | 0.601 | ||

| 10 | 0.98 | ABC-PG-cBFAS | 1.225 | 0.169 | 0.664 |

| ABC-PG-cAPF | 0.691 | 0.103 | 0.298 | ||

| ABC-PG-cBF | 0.824 | 0.116 | 0.582 | ||

| 1 | 0.9 | ABC-PG-cBFAS | 0.994 | 0.140 | 0.672 |

| ABC-PG-cAPF | 0.328 | 0.054 | 0.264 | ||

| ABC-PG-cBF | 1.078 | 0.153 | 0.603 | ||

| 1 | 0.95 | ABC-PG-cBFAS | 1.262 | 0.179 | 0.693 |

| ABC-PG-cAPF | 0.577 | 0.089 | 0.285 | ||

| ABC-PG-cBF | 1.239 | 0.178 | 0.597 | ||

| 1 | 0.98 | ABC-PG-cBFAS | 1.446 | 0.207 | 0.682 |

| ABC-PG-cAPF | 0.818 | 0.125 | 0.330 | ||

| ABC-PG-cBF | 0.851 | 0.123 | 0.604 | ||

| 0.1 | 0.9 | ABC-PG-cBFAS | 1.008 | 0.146 | 0.672 |

| ABC-PG-cAPF | 0.379 | 0.061 | 0.345 | ||

| ABC-PG-cBF | 1.114 | 0.161 | 0.593 | ||

| 0.1 | 0.95 | ABC-PG-cBFAS | 1.306 | 0.189 | 0.674 |

| ABC-PG-cAPF | 0.682 | 0.105 | 0.356 | ||

| ABC-PG-cBF | 1.295 | 0.188 | 0.593 | ||

| 0.1 | 0.98 | ABC-PG-cBFAS | 1.511 | 0.219 | 0.678 |

| ABC-PG-cAPF | 0.892 | 0.136 | 0.370 |

| CV | Algorithm | RMSE | RMSE | RMSE | |

|---|---|---|---|---|---|

| ABC-PG-cBF | 0.765 | 0.101 | 0.620 | ||

| 10 | 0.9 | ABC-PG-cBFAS | 0.898 | 0.118 | 0.710 |

| ABC-PG-cAPF | 0.224 | 0.038 | 0.162 | ||

| ABC-PG-cBF | 0.942 | 0.126 | 0.635 | ||

| 10 | 0.95 | ABC-PG-cBFAS | 1.056 | 0.140 | 0.700 |

| ABC-PG-cAPF | 0.457 | 0.069 | 0.219 | ||

| ABC-PG-cBF | 1.091 | 0.151 | 0.596 | ||

| 10 | 0.98 | ABC-PG-cBFAS | 1.263 | 0.174 | 0.694 |

| ABC-PG-cAPF | 0.695 | 0.103 | 0.292 | ||

| ABC-PG-cBF | 0.875 | 0.123 | 0.623 | ||

| 1 | 0.9 | ABC-PG-cBFAS | 1.022 | 0.145 | 0.690 |

| ABC-PG-cAPF | 0.308 | 0.052 | 0.257 | ||

| ABC-PG-cBF | 1.090 | 0.155 | 0.616 | ||

| 1 | 0.95 | ABC-PG-cBFAS | 1.288 | 0.182 | 0.705 |

| ABC-PG-cAPF | 0.602 | 0.094 | 0.302 | ||

| ABC-PG-cBF | 1.271 | 0.183 | 0.607 | ||

| 1 | 0.98 | ABC-PG-cBFAS | 1.491 | 0.214 | 0.715 |

| ABC-PG-cAPF | 0.840 | 0.128 | 0.351 | ||

| ABC-PG-cBF | 0.870 | 0.126 | 0.618 | ||

| 0.1 | 0.9 | ABC-PG-cBFAS | 1.024 | 0.149 | 0.693 |

| ABC-PG-cAPF | 0.346 | 0.058 | 0.336 | ||

| ABC-PG-cBF | 1.125 | 0.163 | 0.607 | ||

| 0.1 | 0.95 | ABC-PG-cBFAS | 1.348 | 0.195 | 0.706 |

| ABC-PG-cAPF | 0.682 | 0.106 | 0.357 | ||

| ABC-PG-cBF | 1.325 | 0.192 | 0.619 | ||

| 0.1 | 0.98 | ABC-PG-cBFAS | 1.555 | 0.225 | 0.715 |

| ABC-PG-cAPF | 0.889 | 0.136 | 0.367 |

| CV | Algorithm | RMSE | RMSE | RMSE | |

|---|---|---|---|---|---|

| ABC-PG-cBF | 0.946 | 0.122 | 0.824 | ||

| 10 | 0.9 | ABC-PG-cBFAS | 1.094 | 0.141 | 0.907 |

| ABC-PG-cAPF | 0.258 | 0.044 | 0.197 | ||

| ABC-PG-cBF | 1.109 | 0.146 | 0.790 | ||

| 10 | 0.95 | ABC-PG-cBFAS | 1.279 | 0.168 | 0.896 |

| ABC-PG-cAPF | 0.503 | 0.076 | 0.243 | ||

| ABC-PG-cBF | 1.273 | 0.174 | 0.749 | ||

| 10 | 0.98 | ABC-PG-cBFAS | 1.476 | 0.200 | 0.870 |

| ABC-PG-cAPF | 0.730 | 0.109 | 0.318 | ||

| ABC-PG-cBF | 1.042 | 0.147 | 0.772 | ||

| 1 | 0.9 | ABC-PG-cBFAS | 1.203 | 0.170 | 0.861 |

| ABC-PG-cAPF | 0.350 | 0.060 | 0.298 | ||

| ABC-PG-cBF | 1.260 | 0.178 | 0.765 | ||

| 1 | 0.95 | ABC-PG-cBFAS | 1.504 | 0.213 | 0.890 |

| ABC-PG-cAPF | 0.655 | 0.102 | 0.346 | ||

| ABC-PG-cBF | 1.430 | 0.205 | 0.753 | ||

| 1 | 0.98 | ABC-PG-cBFAS | 1.686 | 0.241 | 0.878 |

| ABC-PG-cAPF | 0.880 | 0.135 | 0.382 | ||

| ABC-PG-cBF | 1.038 | 0.150 | 0.764 | ||

| 0.1 | 0.9 | ABC-PG-cBFAS | 1.230 | 0.179 | 0.862 |

| ABC-PG-cAPF | 0.419 | 0.069 | 0.389 | ||

| ABC-PG-cBF | 1.264 | 0.183 | 0.727 | ||

| 0.1 | 0.95 | ABC-PG-cBFAS | 1.546 | 0.224 | 0.867 |

| ABC-PG-cAPF | 0.712 | 0.112 | 0.389 | ||

| ABC-PG-cBF | 1.483 | 0.215 | 0.751 | ||

| 0.1 | 0.98 | ABC-PG-cBFAS | 1.733 | 0.252 | 0.860 |

| ABC-PG-cAPF | 0.944 | 0.145 | 0.420 |