Estimating Counterfactual Matrix Means

with Short Panel Data††thanks: First version: December 11, 2023. Authors listed alphabetically. We thank Dmitry Arkhangelsky, Susan Athey, Stéphane Bonhomme, Kirill Borusyak, Jiafeng Chen, Rebecca Diamond, Matthew Gentzkow, Bryan Graham, Christian Hansen, Guido Imbens, David Ritzwoller, Vasilis Syrgkanis, and the participants of the Stanford Econometrics Lunch and the Stanford Causal Panel Data Conference for their thoughtful comments and valuable feedback.

Abstract

We develop a more flexible approach for identifying and estimating average counterfactual outcomes when several but not all possible outcomes are observed for each unit in a large cross section. Such settings include event studies and studies of outcomes of “matches” between agents of two types, e.g. workers and firms or people and places. When outcomes are generated by a factor model that allows for low-dimensional unobserved confounders, our method yields consistent, asymptotically normal estimates of counterfactual outcome means under asymptotics that fix the number of outcomes as the cross section grows and general outcome missingness patterns, including those not accommodated by existing methods. Our method is also computationally efficient, requiring only a single eigendecomposition of a particular aggregation of any factor estimates constructed using subsets of units with the same observed outcomes. In a semi-synthetic simulation study based on matched employer-employee data, our method performs favorably compared to a Two-Way-Fixed-Effects-model-based estimator.

Keywords: panel data, missing not-at-random, low-rank, factor model, interactive fixed effects, event study, bipartite network data

1 Introduction

Researchers are often interested in estimating average counterfactual outcomes in a population when “short” panel data with missing outcomes are available, namely, observations of several but not all outcomes for each unit in a large cross section. For example, in event study settings, units receive a treatment at different times, units’ outcomes are observed over several time periods pre and post-treatment, and researchers are interested in estimating average counterfactual outcomes of treated units had they not been treated (Ashenfelter \BBA Card, \APACyear1985; Bertrand \BOthers., \APACyear2004; Angrist \BBA Pischke, \APACyear2009). As another example, several empirical literatures estimate average outcomes of counterfactual “matches” between pairs of agents of two different “types,” e.g. wages of workers at various firms (Abowd \BOthers., \APACyear1999), test scores of students taught by various teachers (Jackson \BOthers., \APACyear2014), and earnings and health outcomes of people living in various places (Finkelstein \BOthers., \APACyear2016; Chetty \BBA Hendren, \APACyear2018; Card \BOthers., \APACyear2023).

In such settings, exogenous variation in which outcomes are observed for different units is often hard to come by, and outcome missingness is plausibly determined by unobserved, confounding variables that also affect the outcomes themselves. To make progress, since only a few outcomes are observed per unit (Andrews \BOthers., \APACyear2008; Bonhomme \BOthers., \APACyear2023), researchers often assume unobserved confounders are low-dimensional and use multiple observations per unit to estimate an explicit model of how those confounders affect outcomes.111Usually, these models also require “strict exogeneity,” namely that, conditional on low-dimensional confounders, outcomes are independent of missingness. In keeping with much of applied practice, this paper does the same. However, Ashenfelter \BBA Card (\APACyear1985) and Bonhomme \BOthers. (\APACyear2019) discuss strict exogeneity’s plausibility in event study and match outcome contexts, respectively.

A canonical model applied in these settings is the Two-Way Fixed Effects (TWFE) model, which assumes outcomes only differ systematically within and across units in levels.222In event study settings, a TWFE model of control potential outcomes across time periods implies that units’ control potential outcomes follow “parallel trends” over time (Borusyak \BOthers., \APACyear2023; Ghanem \BOthers., \APACyear2022). While the TWFE model enables outcome means to be identified and estimated under a myriad of outcome missingness patterns and a small number of observations per unit (Jochmans \BBA Weidner, \APACyear2019; Borusyak \BOthers., \APACyear2023), it meaningfully restricts how unobserved confounders can affect outcomes (Ghanem \BOthers., \APACyear2022).

In event study settings, a large literature has sought to allow for richer confounding relationships than those implied by parallel-trends-type assumptions by using a low-rank factor model of outcomes (see Section 1.1 for references).333Factor models are also frequently called “interactive fixed effect” models. In contrast with the TWFE model, the factor model allows potentially multidimensional unobserved confounders to have differential effects on different outcomes. However, existing factor model-based methods cannot be applied generally, both because they only work under certain outcome missingness patterns, and because many require a large number of observed outcomes per unit.

In this paper, we seek to bridge the gap between the versatility of TWFE-based methods and the expressivity of factor model-based methods. In particular, we develop an approach for identifying, estimating, and conducting valid inference on counterfactual outcome means under factor models in short panels with general outcome missingness patterns.

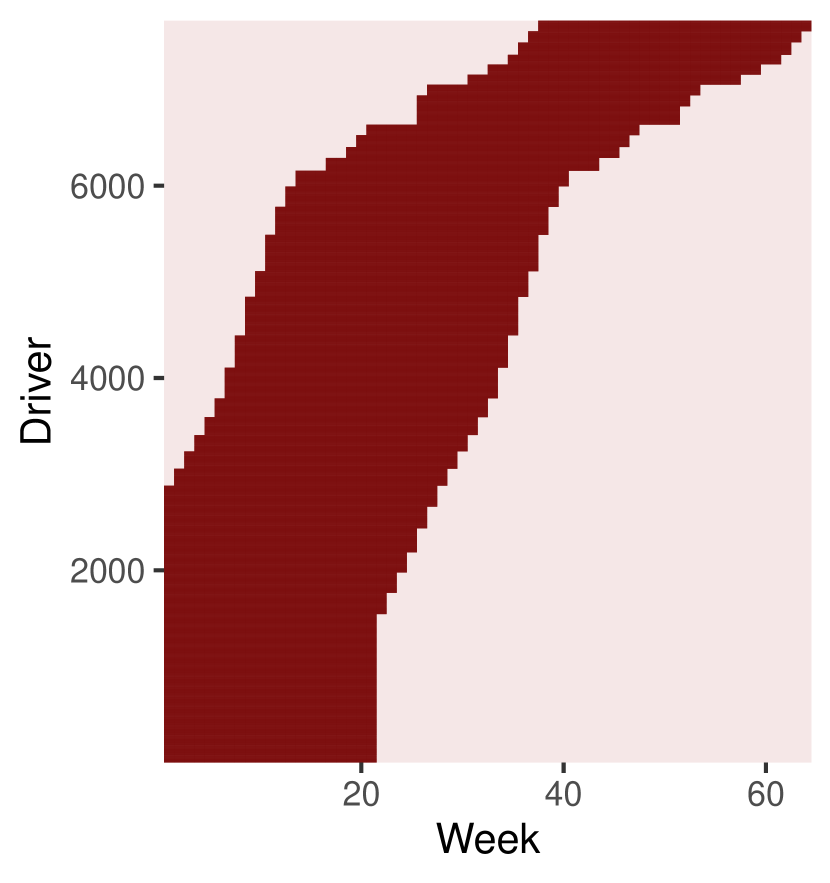

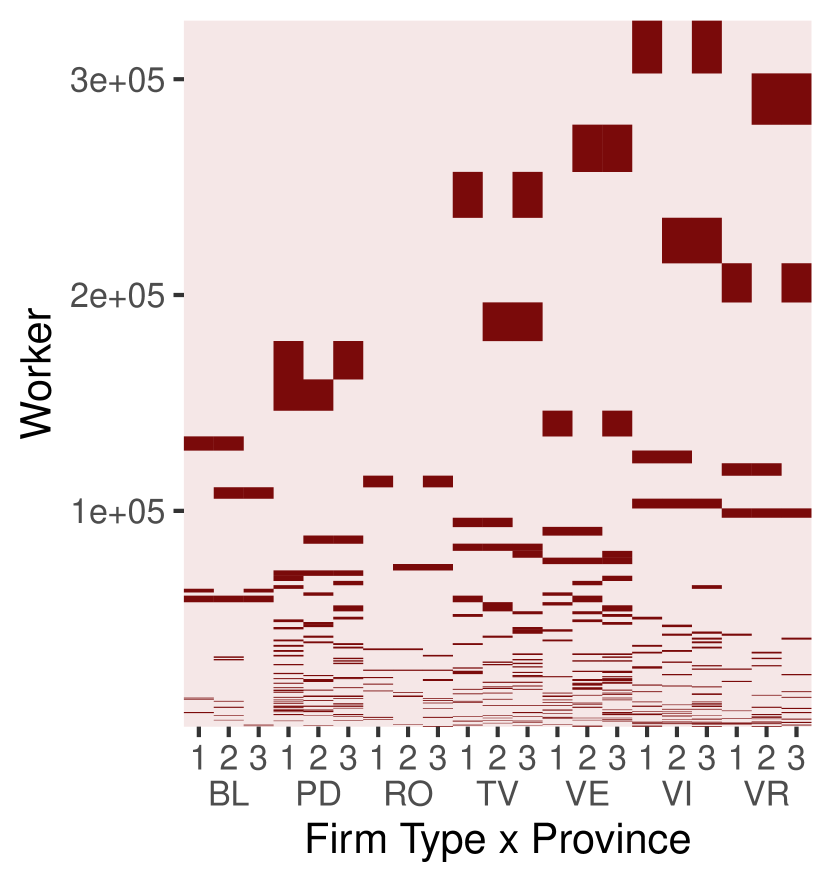

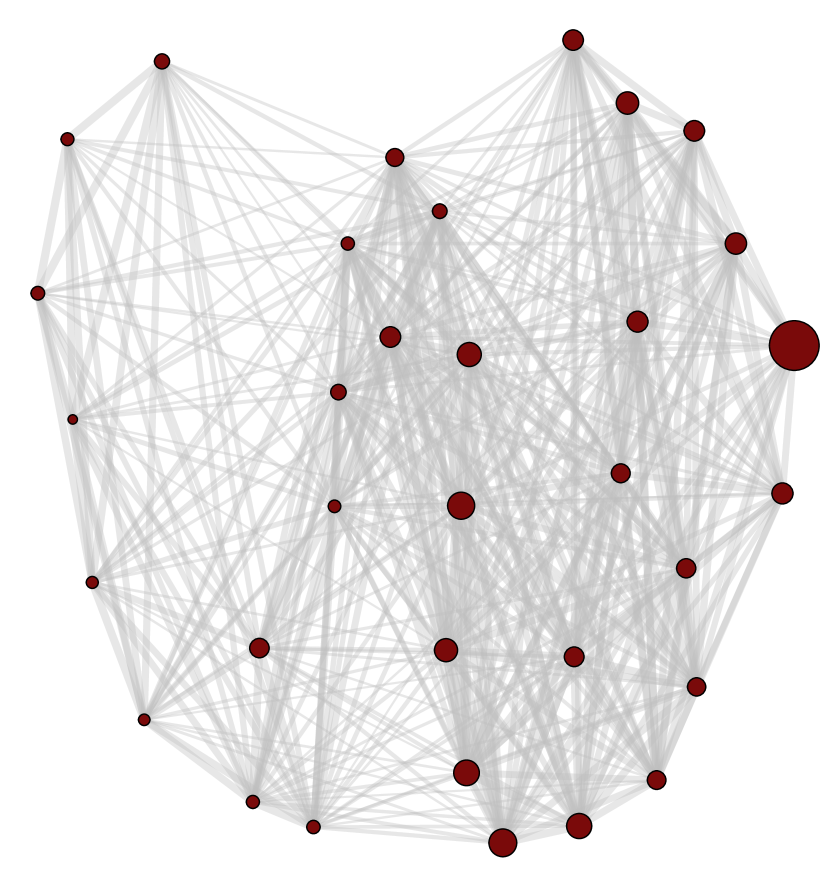

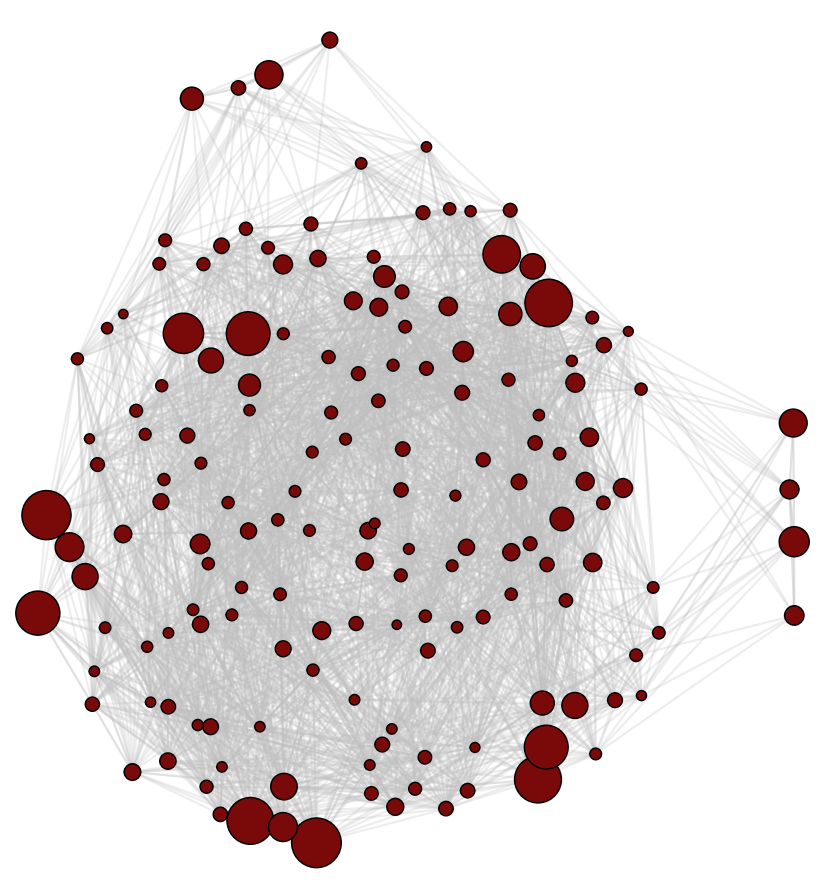

Figure 1.1 provides two empirical examples of complex outcome missingness patterns under which the methods developed in this paper can be applied. As an example of an event study setting, Figure 1(a) displays the control potential outcome observation pattern from Ater, Shany, Ross, Turkel\BCBL \BBA Vasserman (\APACyear\bibnodate), which evaluates the effect of a government-run usage-based congestion pricing incentive on the driving behavior of several thousand Israeli drivers from January of 2020 through July of 2021. As can be seen in Figure 1(a), drivers were recruited for observation in a staggered fashion over time and received treatment after a non-random 20 weeks of monitoring. As an example of a bipartite matching setting, Figure 1(b) shows which of a subset of Italian workers in the Veneto Worker Histories (VWH) dataset received wages in each of seven provinces and three firm types within each province between 1991 and 2001;444 The VWH dataset was developed by the Economics Department in Università Ca’ Foscari Venezia under the supervision of Giuseppe Tattara, and can be accessed at https://www.frdb.org/en/dati/dati-inps-carriere-lavorative-in-veneto/. see Section 5.1 for details.

In both cases, outcome missingness patterns are credibly determined by unobserved characteristics of units that also affect outcomes. In Figure 1(a)’s setting, it is possible that drivers who would benefit more from the treatment like remote workers joined the study earlier, while in Figure 1(b)’s setting, workers likely live in the regions with job opportunities that would pay them the highest wages. In addition, the TWFE model’s restriction that unit-level heterogeneity does not affect how outcomes differ within units is plausibly unrealistic in both examples. In Figure 1(a)’s setting, drivers in remote-work-compatible occupations plausibly changed their commuting patterns differently in response to COVID-19 lockdowns than drivers whose occupations required continued in-person work. In Figure 1(b)’s setting, if industries are unequally distributed across space, workers whose skills are disproportionately valued by the industries in some region might receive higher wages there than if they lived in a region without those industries. Finally, in both examples, only a small number of outcomes are observed per unit relative to the number of units in each sample.

Our identification strategy for counterfactual outcome means in short panels with missing outcomes is based on a novel type of matrix we call an Aggregated Projection Matrix (APM). Surprisingly, any basis for an APM’s null space serves as a collection of the factor vectors corresponding to all outcomes with respect to the same basis. To construct an APM, we first group units into cohorts that share the same sets of observed outcomes. Next, we use the observations for each cohort to recover the collections of factors corresponding to each cohort’s observed outcomes up to cohort-specific bases using any of the myriad of existing approaches for identifying factors in short panels without missing data, e.g. those discussed in Section 4.3. Finally, we aggregate the projection matrices onto the spans of the matrices whose non-zero rows are the recovered cohort-specific factors in a particular manner into an APM. Having identified the factors corresponding to all outcomes via the APM’s null space, we then leverage an idea proposed in various forms in Imbens \BOthers. (\APACyear2021), Brown \BBA Butts (\APACyear2022), and Agarwal, Shah\BCBL \BBA Shen (\APACyear2023) to recover cohort-specific outcome means by learning a linear relationship between the factors corresponding to the observed and missing outcomes in the target cohort.

We prove that our approach identifies the collection of factors corresponding to every outcome so long as a particular graph is connected, where the graph is constructed based on the overlap in observed outcomes between pairs of cohorts. Importantly, our method accommodates more general missingness patterns than other approaches for short panels, and it automatically stitches together different pieces of identifying information each used in isolation by existing methods. It also does not make assumptions on how units select into cohorts based on their low-dimensional unobserved confounders. Moreover, unlike approaches designed for long panels with many observed outcomes per unit, our approach does not require exact recovery of those unobserved confounders, and is thus not vulnerable to the incidental parameter problem (Neyman \BBA Scott, \APACyear1948; T. Lancaster, \APACyear2000).

We also translate this identification strategy into a plug-in estimator. In particular, we compute an estimated APM using estimates of cohort-specific factors constructed using the data corresponding to each cohort. We then use the rows of the matrix of eigenvectors corresponding to the smallest eigenvalues of the estimated APM as estimates of the factor vectors corresponding to all outcomes. As such, our estimator is quite simple to compute. In an asymptotic regime in which the number of outcomes remains fixed as the cross-sectional dimension of the panel grows, we show that this estimator is consistent and asymptotically normal, and that a weighted bootstrap procedure provides valid asymptotic inference. These results rely on an exact, first-order expansion of the operator mapping a symmetric matrix into the projection matrix onto the space spanned by some subset of its eigenvectors. To our knowledge, this expansion is new.

Finally, we demonstrate the empirical performance of our estimator via a semi-synthetic simulation study based on the VWH dataset of wages earned by workers at different types of firms in the Veneto region of Italy. To define outcomes, we cluster firms within each province into three types by their weekly wage distributions as in Bonhomme \BOthers. (\APACyear2019) and define a worker’s outcome corresponding to a given type of firm in a given province as the average weekly wage they would earn were they to work for that type of firm in that province. Importantly, the outcome missingness pattern for this setting, which we illustrate in Figure 1(b), is complex enough to preclude counterfactual outcome mean estimation using existing factor-model-based methods.

To assess the accuracy of our factor-model-based procedure relative to an estimator based on a TWFE model of counterfactual outcome means, we mask an observed outcome for some cohort of units in our data and resample units from these masked data to construct synthetic datasets. We then compute various error metrics of both estimators of the artificially hidden cohort outcome’s mean across resampled synthetic datasets. Across many masked cohort outcomes, our procedure consistently delivers outcome mean estimates with lower bias and root mean squared error than the TWFE-based estimator. In line with Bonhomme \BOthers. (\APACyear2019), our simulation results suggest that complementarities between workers and firms do affect wages.

1.1 Related Work

Recently, a variety of methods have been proposed that can be used to estimate and conduct inference on a target cohort outcome mean by aggregating accurate imputations of individual-level factor structure estimates for units in the target cohort constructed using data on units’ observed outcomes, e.g. Gobillon \BBA Magnac (\APACyear2016); Xu (\APACyear2017); Athey \BOthers. (\APACyear2021); J. Bai \BBA Ng (\APACyear2021); Arkhangelsky \BOthers. (\APACyear2021); Ben-Michael \BOthers. (\APACyear2022); Xiong \BBA Pelger (\APACyear2023); Agarwal, Dahleh\BCBL \BOthers. (\APACyear2023); Chernozhukov \BOthers. (\APACyear2023); Farias \BOthers. (\APACyear2021); Choi \BBA Yuan (\APACyear2023); Choi \BOthers. (\APACyear2023); Arkhangelsky \BBA Hirshberg (\APACyear2023); Fernández-Val \BOthers. (\APACyear2021). These methods require the number of outcomes and maximum number of observed outcomes per cohort to grow as the number of units grows, since outcome-specific factor vectors can be estimated consistently using variation across many units and unit-specific loading vectors can be estimated consistently using variation across many outcomes. However, under our asymptotic regime of interest in which only a finite number of outcomes are observed per unit, we cannot recover each unit’s loadings without bias that persists as the number of units grows and does not average out to zero across units in the population, precluding averages across imputations. Further, this bias can contaminate the outcome-specific factor estimates themselves even if the cross-sectional panel dimension is large (Neyman \BBA Scott, \APACyear1948; T. Lancaster, \APACyear2000). On the other hand, when the missingness pattern is complicated, a restriction on the missingness mechanism, such as missing at random, or knowledge of it, such as the probability of jointly observing each pair of outcomes, is often needed even in long panels (Xiong \BBA Pelger, \APACyear2023). However, this information is typically unavailable and hard to come by in settings like those illustrated in Figure 1.1.

Instead, we build on an approach suggested in various forms in Imbens \BOthers. (\APACyear2021), Brown \BBA Butts (\APACyear2022), and Agarwal, Shah\BCBL \BBA Shen (\APACyear2023): given just factor vectors corresponding to all outcomes, we can construct a linear combination of the target cohort’s observed outcome means that equals the target cohort outcome mean. Imbens \BOthers. (\APACyear2021) call any such linear combination a bridge function to highlight the connections they make between this setting and the proximal causal inference literature (Miao \BOthers., \APACyear2018; Deaner, \APACyear2018).

The bridge function-based identification strategy was originally developed in the context of settings with a block missingness pattern, as illustrated in Figure 1(a). In these settings, there exists a “reference” cohort of units for whom all outcomes are observed, so any method for identifying and estimating a factor model without missing data can be applied to the data from the reference cohort to recover the factor vectors for all outcomes with respect to the same basis; we discuss several such methods in Section 4.3.

The bridge function approach can still be applied to identify some cohort outcome means under even more general missingness patterns so long as a reference cohort exists. In event study settings with staggered treatment adoption, so long as there is a “never-treated” group of units for whom all control potential outcomes are observed,555Athey \BOthers. (\APACyear2021) also require a nontrivial share of never-treated units for their estimator to be consistent in the staggered treatment adoption setting. these units can be used as a reference cohort, and the approaches developed in Callaway \BBA Karami (\APACyear2023), Brown \BBA Butts (\APACyear2022), Brown \BOthers. (\APACyear2023), and Callaway \BBA Tsyawo (\APACyear2023) identify and yield consistent estimates of outcome means when the number of outcomes remains fixed as the cross section’s size grows. Agarwal, Dahleh\BCBL \BOthers. (\APACyear2023) show that the bridge function approach can be applied to identify some cohort outcome means in even more general settings like the one illustrated in Figure 1(b) by finding block missingness patterns embedded within the broader outcome missingness pattern.

However, several important challenges remain in estimating and conducting valid inference on cohort outcome means under factor models that are common in empirical settings such as those illustrated in Figure 1.1. First, many embedded block missingness patterns may exist within a broader missingness pattern to identify some cohort outcome means, and it is unclear how one should combine information gleaned from each of them in a computationally efficient manner to improve estimate precision. Second and more importantly, embedded block missingness patterns cannot always be found to identify all cohort outcome means. Our identification and estimation approach automatically combines information about factor vectors from all cohorts to identify and estimate cohort outcome means without requiring embedded block missingness patterns to exist.

The graph connectivity assumption underlying our identification argument bears resemblance to those made in several papers in the rich literature on fixed-effect-like models of bipartite match outcomes under strict exogeneity, e.g. Abowd \BOthers. (\APACyear2002); Jochmans \BBA Weidner (\APACyear2019); Bonhomme \BOthers. (\APACyear2019); Hull (\APACyear2018); see Bonhomme (\APACyear2020) for a review. As it happens, we show in Appendix D.2 that, while our connectivity requirement enables identification for general numbers of factors and loadings, in the special case where the factors and loadings are unidimensional, our assumption is essentially equivalent to theirs.

Our consistency and asymptotic linearity results are also related to a large literature applying perturbation-theoretic results to characterize the concentration of eigenspaces of random matrices.666See Yu \BOthers. (\APACyear2015) for clear and concise statements of several results from the literature useful for statistical applications, and Z. Bai \BBA Silverstein (\APACyear2010) for a textbook treatment To characterize the asymptotic distributions of eigenspaces of estimated matrices as we do in this paper, the concentration guarantees implied by canonical zeroth-order approximation bounds like the Davis–Kahan theorem (see Yu \BOthers. (\APACyear2015) for a convenient version) are too coarse. In our paper, we instead characterize the asymptotic distributions of estimated eigenspaces and the estimators on which they depend by deriving a non-asymptotic, first-order eigenspace projection operator expansion based on Kato’s integral (Kato, \APACyear1949). Several other papers have also applied Kato’s integral to derive concentration results for eigenspaces of random matrices with (approximately) independent entries, e.g. Oliveira (\APACyear2010); Mao \BOthers. (\APACyear2021); Lei (\APACyear2020). Relatedly, Simons (\APACyear2023) applies an asymptotic linearization of the eigenspace operator from J\BHBIg. Sun (\APACyear1991) to derive asymptotically valid hypothesis tests concerning eigenspaces of an estimated, potentially non-symmetric matrix.

2 Setup and Intuition

2.1 Setup

We describe our setting of interest formally as follows. Researchers observe a large, i.i.d. sample of units, and each unit has outcomes associated with them, where denotes unit ’s outcome . Importantly, not all outcomes are observed for each unit. To describe which outcomes are observed, we group units into cohorts, where denotes unit ’s cohort. For the units in cohort , we only observe the outcomes with indices in a subset of all outcome indices . To distinguish between observed and missing outcomes, we define if outcome is observed for unit (i.e. if ) and otherwise. Given these unbalanced panel data, researchers are often interested in estimating aggregations of cohort-level outcome means:

| (2.1) |

We refer to as a counterfactual outcome mean since outcome may not be observed for the units in cohort . To model the small number of observed outcomes per unit in our asymptotic theory in Section 4.2, we will focus on the case where the number of outcomes remains bounded as the sample size grows.

The setup described above encapsulates several kinds of causal panel data analyses. In event study settings like Figure 1(a)’s, is unit ’s control potential outcome had they not yet been treated by period , units belong to cohort if they first received treatment at time , and researchers typically estimate aggregations of average treatment effects on the units in each cohort like dynamic effects across post-treatment periods.777See L. Sun \BBA Abraham (\APACyear2021) and Callaway \BBA Sant’Anna (\APACyear2021) for more in-depth discussions of this model of event study settings with staggered treatment adoption, and De Chaisemartin \BBA d’Haultfoeuille (\APACyear2020) for treatment effect definitions relevant to settings in which treatment is not an absorbing state. In bipartite matching settings like Figure 1(b)’s, is “row-type” unit ’s outcome if matched with “column-type” unit , row-type units belong to the same cohort if they were matched with the same set of column-type units, and researchers typically estimate aggregations of s that characterize the degree to which row-type and column-type unit heterogeneity affect differences in average observed outcomes across column-type units.888In Appendix D.1, we discuss a variant of the decomposition proposed in Finkelstein \BOthers. (\APACyear2016) for this purpose that only requires estimates of the outcome means identified in this paper. We leave identifying the higher-order outcome moments required by outcome variance decompositions in the literature (e.g. Abowd \BOthers. (\APACyear1999)) to future work.

We assume outcomes are generated according to a rank- factor model, i.e. that outcomes are determined by the inner product of a fixed vector of outcome-specific factors and a vector of unit-specific loadings plus an error term that has zero mean given unit ’s loadings and cohort membership :

| (2.2) |

As in other fixed-effect-like models like the TWFE model or the static model studied in Bonhomme \BOthers. (\APACyear2019), the assumption that is mean-independent of cohort membership conditional on loadings implies that only the coordinates of can serve as confounders that affect both units’ cohort memberships and their outcomes. By considering the factor vectors to be fixed, we essentially condition our inference on the factors . If we consider the factors to be random, the residual mean condition in (2.2) can be read as .

Throughout this paper, we assume the rank of the factor model is known.999Papers that use empirical strategies based on TWFE models or parallel trends assumptions are also making a choice about the dimension of unobserved confounders. In keeping with other methods based on fixed-effect-like models of short panels with unobserved heterogeneity (e.g. Bonhomme \BOthers. (\APACyear2019)), we suggest that researchers using our method assess the robustness of their results to different values of , insofar as the cohort outcome means they would like to estimate are identified given that choice of , as discussed in Section 4.1.101010The problem of determining the number of factors from short panel data without assuming a the distributions of residuals belong to a known parametric family has only recently been studied to our knowledge (Ahn \BOthers., \APACyear2013; Fortin \BOthers., \APACyear2022, \APACyear2023), unlike the well-established literature on determining in panels for which both and are large (J. Bai \BBA Ng, \APACyear2002; Onatski, \APACyear2009; Ahn \BBA Horenstein, \APACyear2013; Gagliardini \BOthers., \APACyear2019). The simulation study in Section 5.2 that assesses the performance of our estimation procedure on held-out cohort outcomes also provides a blueprint for assessing the relative performance of our estimator given different choices of .

2.2 Intuition

Broadly, our approach for identifying and estimating a target cohort outcome mean proceeds in two stages. First, we recover all of the factor vectors across outcomes with respect to a common basis. Then, we use the factor vectors corresponding to the target cohort’s observed outcomes and the target outcome to extrapolate from the target cohort’s observed outcome means to the target outcome mean. To highlight the additional challenge posed by the first stage, we proceed by first providing intuition for the second stage in a setting where the first stage happens to be straightforward.

In particular, we focus on a simple, three-cohort outcome missingness pattern illustrated in Figure 1(b) and consider estimating a target cohort outcome mean , where is the target cohort and is the target outcome. Suppose also that we have access to the factors for all outcomes. Then, under regularity conditions, there exist many vectors of coefficients we can construct such that a linear combination of the factor vectors for the target cohort ’s observed outcomes with those coefficients equals the factor vector corresponding to the target outcome :

| (2.3) |

As it happens, the same linear combination of the target cohort’s observed outcome means for will equal the target cohort’s target outcome mean (Agarwal, Shah\BCBL \BBA Shen, \APACyear2023; Imbens \BOthers., \APACyear2021; Brown \BBA Butts, \APACyear2022):

| (2.4) |

In keeping with Imbens \BOthers. (\APACyear2021), we refer to any linear transformation where satisfies (2.3) as a bridge function.

Turning to the first stage of our approach, we now discuss how to recover the factors used to construct bridge functions via solutions to (2.3). A well known fact in the rich literature on factor models is that, even in settings where all outcomes are observed, only a common linear transformation of each factor vector can be identified, where is an unknown, invertible matrix we refer to as a basis.111111This basis indeterminacy is inevitable because, for any invertible , the distributions of and are observationally equivalent; see e.g. Anderson \BBA Rubin (\APACyear1956) for an early reference and Anderson (\APACyear2009) for a textbook treatment.

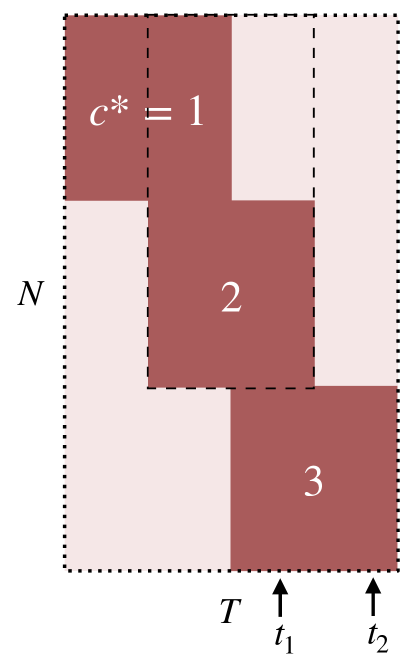

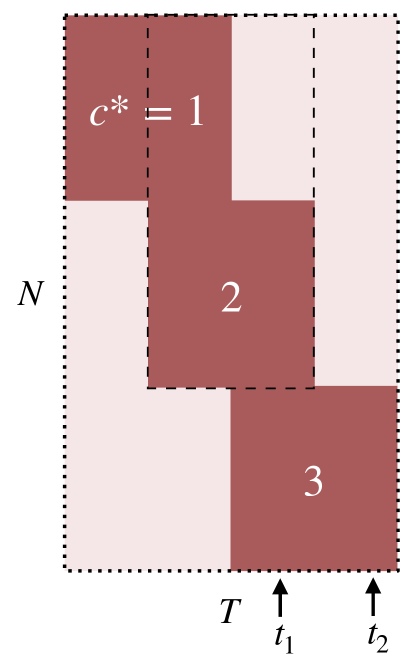

Luckily, the bridge function approach renders this basis indeterminacy immaterial when our target cohort is and our target outcome is . To see why, note that in this case, there exists a “reference” cohort of units for whom we observe both the target outcome and some of the outcomes also observed for the units in the target cohort (Agarwal, Dahleh\BCBL \BOthers., \APACyear2023; Brown \BBA Butts, \APACyear2022). In other words, the set of units and outcomes inside the black dashed rectangle in Figure 1(b) constitutes a block missingness pattern like the one shown in Figure 1(a) embedded within the broader outcome missingness pattern in Figure 1(b). Then, under a variety of additional assumptions discussed in Section 4.3, a myriad of methods can still be applied using just the data from cohort to recover transformed factor vectors corresponding to the target outcome and for corresponding to the overlapping observed outcomes between cohorts and , where is a common basis. Since the set of valid bridge functions satisfying (2.3) is invariant to multiplying all of the factor vectors by the same basis matrix , the second stage of our identification approach remains unaffected.

Unfortunately, when our target outcome is instead , no reference cohort exists for whom we observe both the target outcome and any observed outcomes for our target cohort . As such, there is no subset of the data we can directly use to recover the factors corresponding to the target outcome and the target cohort’s observed outcomes with respect to the same basis.121212The lack of a reference cohort also precludes the imposition of a common normalization that ensures the factor vectors are uniquely defined; see J. Bai \BBA Ng (\APACyear2013) for a detailed discussion of such normalizations. Instead, again under different sets of additional assumptions (see Section 4.3), we can only use the observed outcomes of units in each cohort to recover transformed factor vectors corresponding to cohort ’s observed outcomes with respect to a cohort-specific basis .131313As will be made clear in Section 4, our approach will not actually require the identification of for some fixed basis matrices ; we introduce them here for simplicity of exposition. In other words, at best, we can recover cohort-specific factor vectors that are “misaligned.” To be able to find bridge functions that satisfy (2.3), we need to construct an aligned set of factor vectors expressed with respect to a common basis that correspond to both the target outcome and the target cohort’s observed outcomes .

To describe our solution to this factor vector misalignment problem, we define some additional notation. First, stack the factor vectors row-wise into a matrix , and stack the cohort-specific transformed factor vectors recovered from the data for cohort into the matrix , where the -th row of equals if outcome is observed for the units in cohort and a vector of zeros otherwise. In addition, let be the diagonal matrix whose -th diagonal entry is one if outcome is observed for cohort , i.e. , and zero otherwise. Finally, for any matrix , we denote the projection matrix onto ’s column space by , where is the Moore-Penrose pseudo-inverse of .

Armed with this notation, we can now describe the two insights that underpin our solution to the factor vector alignment problem introduced above. First, since the column space of does not depend on , the projection matrix is the same as the projection matrix onto the column space of the matrix whose non-zero rows are exactly the true factor vectors corresponding to cohort ’s observed outcomes.141414By definition, we have that . Thus, the projection matrix derived from cohort ’s data provides a unique representation of the available information about the factor vectors corresponding to cohort ’s observed outcomes free from contamination by the cohort-specific .

Given the cohort-specific projection matrices , we then must aggregate them in such a way so as to recover the factor vectors defined with respect to some common basis. Along these lines, our second key observation is that the column space of is a subset of the null space of the matrix for each cohort .151515Since and , . To leverage this insight, we define we define the Aggregated Projection Matrix (APM) operator as follows for any matrices :

| (2.5) |

Despite its name, is not itself a projection matrix in general. However, since is by definition the sum of the matrices across cohorts , the column space of must lie in the null space of as well. In Section 4.1, we show that, perhaps surprisingly, so long as there is sufficient overlap between the observed outcomes across pairs of cohorts, the null space of is in fact exactly the column space of . Thus, the rows of any basis matrix for the null space of can serve as valid factor vectors when applying the bridge function identification strategy.161616One might imagine instead explicitly recovering the matrix that aligns cohort ’s factors with cohort ’s by regressing cohort ’s factor vectors on cohort ’s factor vectors corresponding to the overlapping observed outcomes between the two cohorts as in J. Bai \BBA Ng (\APACyear2021). One could then chain multiplications of these “pairwise aligning” matrices together to align cohort-specific factor vectors with each other, evocative of the identification and estimation strategy proposed in Hull (\APACyear2018) under a TWFE-like model of outcomes. However, constructing these aligning chains is nontrivial in realistic applications with more than a few cohorts like those illustrated in Figure 1.1, and it is not clear how one would aggregate information about factors across potentially large numbers of possible aligning chains. In Section 4.1, we discuss how the procedure we propose next makes use of information from all available aligning chains to identify the column space of without needing to enumerate them explicitly.

3 Estimation and Inference Procedure

Having provided intuition for the conceptual underpinnings of our approach, we now introduce our general estimation and inference procedure, which has four high-level steps. First, we consider the data corresponding to units in each cohort separately and use them to estimate the factors corresponding to the observed outcomes for each cohort. Second, we aggregate these cohort-specific factor estimates into a particular matrix whose eigendecomposition yields valid estimates of the factors corresponding to all outcomes. Third, given those factor estimates, for each cohort, we construct the minimum norm bridge function that consistently extrapolates from that cohort’s observed outcome means to all target outcome means. Finally, we conduct valid inference on cohort outcome means by taking advantage of the asymptotic normality of our estimator.

We now describe our procedure in more detail, beginning with step two outlined above. We assume for now that for each cohort , we have access to estimates of the factor vectors corresponding to each outcome observed for cohort . In Section 4.3, we discuss a variety of methods that exist for constructing valid cohort-specific factor vector estimates under different sets of additional assumptions beyond the factor model (2.2). Importantly, most estimators cohort-specific factor vectors require minimal computational overhead for small , and they can be computed in parallel across cohorts using subsets of the data associated with each cohort. We then stack these cohort-specific estimates into the matrix whose -th row is if , i.e. if outcome is observed for the units in cohort and a vector of zeros otherwise.

Given cohort-specific estimated factor matrices , the second step of our procedure consists of constructing the estimated APM and computing its eigendecomposition. Because is typically small in settings in which we envision our method will be applied, this step can be done extremely quickly using the myriad of optimized eigendecomposition routines available in most programming languages.171717 Examples include the eigvecs function in Julia’s LinearAlgebra module and the eigen function available in base R. Let be the matrix whose columns are eigenvectors corresponding to the smallest eigenvalues of ;181818Recall that eigenvectors are unique up to magnitudes, signs, and permutations between indices corresponding to repeated eigenvalues. as we show in Section 4.2, row of is a consistent estimate of the factor vector with respect to a particular error metric.

Describing the third step of our procedure requires several more definitions. Collect unit ’s observed outcomes into the vector , and note that although has undefined entries corresponding to unobserved outcomes, all entries of the vector are well-defined since the entries corresponding to the unobserved outcomes are zero. We also let denote the number of units in cohort . We can then define our estimator of the vector whose -th entry is the target cohort ’s mean value of outcome , :

| (3.1) |

Given that is simply a vector of least-norm solutions to underdetermined linear equations, it can also be computed efficiently in most programming languages.191919Given that is small, the simplest method is to compute the singular value decomposition , e.g. using the svd function available in Julia’s LinearAlgebra module or base R, and then compute , where is simply the diagonal matrix with its positive diagonal entries replaced by their inverses.

Often, researchers are actually interested in estimating a known, vector-valued function of cohort outcome means , along with a vector of nuisance parameters that are estimable from the data. For example, in event study settings, it is common to report average effects of a treatment across different numbers of time periods relative to units’ treatment times. As introduced in Callaway \BBA Sant’Anna (\APACyear2021) and L. Sun \BBA Abraham (\APACyear2021) and reviewed in Example D.1 of Appendix D.1, we can express these estimands as weighted averages of the differences between each cohort’s average control potential outcome means and their observed, treated potential outcome means (part of ), where the weights are determined by the relative sizes of each cohort (also part of ).

In the context of bipartite match data on patients’ health outcome when living in different geographic areas, Finkelstein \BOthers. (\APACyear2016) suggest an approach to attributing shares of the differences in average health outcomes across regions to people and places that can be expressed in the form , albeit based on a TWFE model of match outcomes. In Example D.2 of Appendix D.1, we discuss nonparametric analogs of their estimands of the form that do not depend on a particular model of outcomes, but that can be estimated under the factor model (2.2) using our procedure.

Given ’s relevance in applied contexts, as an extension of the third step of our procedure, we compute a plug-in estimate of , where the vector collects the cohort outcome mean vector estimates defined in (3.1) across cohorts, and is an estimate of the nuisance parameter vector . For convenience, we summarize the three steps of our estimation procedure in Algorithm 1.

For the fourth and final step of our procedure, we construct simultaneous confidence intervals for the coordinates of .202020A set of confidence intervals for the coordinates of has simultaneous coverage if the probability that all coordinates of lie inside their respective intervals simultaneously is at least . For simplicity and numerical stability, we construct these intervals via a Bayesian bootstrap (Rubin, \APACyear1981).212121In principle, any bootstrap procedure that weights or resamples units could also be used, but to avoid pathological cases where no units from some cohort are sampled, we prefer weighted bootstrap procedures. To describe how we construct these intervals, we introduce more notation. Given a vector of non-negative weights that sum to one, we will assume that both our cohort-specific factor matrix estimators and our nuisance parameter estimator can be adapted to accommodate non-uniform sampling weights , which we denote and , respectively; see Section 4.3 for details on weighted versions of . We also let denote the APM constructed from the weighted, estimated cohort-specific factor matrices , we let denote the equivalent of constructed from the weighted estimated APM , and we let denote the weighted equivalent of defined as follows:

| (3.2) |

A weighted version of our plug-in estimator of is , where is the weighted analog of . Before continuing, we note that under uniform weights , all of the quantities defined previously in this paragraph equal their unweighted counterparts defined above.

Given this notation, our inference procedure proceeds as follows. First, for each iteration of a large number of repetitions,222222We recommend . we take i.i.d. draws from the distribution,232323Other non-negative distributions are also possible as long as they satisfy regularity conditions; see Section 3.6.2 in van der Vaart \BBA Wellner (\APACyear1996) for more examples. construct a vector of normalized weights , and compute a weighted target parameter estimate .242424Since is small, each computation of should be quite fast, as discussed when describing Algorithm 1 above. Further, can be computed in parallel across iterations , boosting computational efficiency further. However, in settings where but and are both very large, the simplicity of this weighted bootstrap procedure may be outweighed its computational burden. In such cases, one could instead construct a multiplier bootstrap inference procedure like the one proposed in Belloni \BOthers. (\APACyear2017) using the influence function expression given in Theorem 4.4, Theorem 4.5, and Corollary D.1. Next, for each coordinate of , we compute an estimate of the standard error of , e.g.

| (3.3) |

where we let denote the th quantile across scalars , and we let denote the th quantile of the standard Gaussian distribution.252525We suggest this interquartile-range-based estimate of estimator standard errors because it is more robust to outliers than other standard error estimators like the standard deviation over weighted bootstrap draws; see the discussion in Remark 3.2 in Chernozhukov \BOthers. (\APACyear2013) for details. Finally, we let denote the following estimated critical value:

| (3.4) |

and we define our simultaneous confidence intervals for across as follows:

| (3.5) |

For convenience, we summarize the steps of our inference procedure in Algorithm 2.

4 Theoretical Properties

4.1 Identification Given Cohort-Specific Factors

To highlight the contributions of this paper, we assume for now that we have identified the column spaces of the cohort-specific factor matrices :

Assumption 4.1.

The projection matrices are identified for all cohorts .

In Section 4.3, we will discuss several sets of additional assumptions standard in the rich literature on factor models under which Assumption 4.1 holds.

To characterize which outcomes our approach can and cannot identify given identified cohort specific factor projection matrices , we define an object we call the Observed Outcome Overlap Graph . The graph consists of vertices, one corresponding to each cohort, and an edge between two distinct cohorts and if the space spanned by the factor vectors corresponding to the two cohorts’ overlapping observed outcomes has at least dimensions, or formally, if

| (4.1) |

While (4.1) is a requirement on the unobserved factor matrix , we note that a necessary condition that only depends on the known sets of observed outcomes across cohorts is that cohorts and have at least overlapping observed outcomes: . As we show in Appendix D.2, this condition is also sufficient when . In Figure E.1, we illustrate for the two empirical examples introduced in Section 1.

Our key requirement to identify all of the outcome means for a given cohort can be stated succinctly in terms of the connectedness of :

Assumption 4.2.

The observed outcome overlap graph is connected.

Before continuing, three remarks concerning Assumption 4.2 are in order. First, Assumption 4.2 implies that every cohort must have at least observed outcomes, and that every factor must affect at least one outcome in every cohort (a proof is provided in Appendix A.1):

Lemma 4.1.

Under Assumption 4.2, for all cohorts .

A consequence of Lemma 4.1 is that our identification, estimation, and inference results hold for the subset of units for whom at least outcomes are observed, i.e. conditional on .262626Such an assumption is analogous to restrictions of the samples in empirical work on bipartite matching settings to the row-type units who are matched with at least two column-type units.

Second, if is not connected, our identification, estimation, and inference results apply instead to the subset of cohorts belonging to the connected component of that contains the target cohort and the subset of outcomes observed for at least one of those cohorts. Third, we show in Appendix D.2 that when , Assumption 4.2 is equivalent to typical connectedness assumptions made in the literature on fixed-effect-type models of bipartite network data under strict exogeneity (see Abowd \BOthers. (\APACyear2002); Jochmans \BBA Weidner (\APACyear2019); Bonhomme \BOthers. (\APACyear2019); Hull (\APACyear2018) for examples, and Bonhomme (\APACyear2020) for a review).

Given identification of the cohort-specific factor projection matrices , we denote the population APM by substituting the population cohort-specific factor matrices into the APM definition (2.5) as follows:

| (4.2) |

We are now equipped to state our main identification result:

Theorem 4.2.

The containment of the column space of in the null space of the APM can be shown succinctly even without Assumption 4.2 (see Footnote 15). However, the containment of the null space of the APM in the column space of under Assumption 4.2 requires a more involved argument, which we provide in Appendix A.2.

Given identification of the column space of the factor matrix , we can then identify the target cohort’s outcome means via the bridge function approach articulated in Section 3:

Corollary 4.3.

Before continuing, we note that, because we impose the factor model functional form (2.2), our identification argument for does not rely on any support assumptions about the cohort-specific loading distributions , unlike some other approaches to estimating counterfactual outcome means in the presence of unobserved heterogeneity. For example, in the context of event study settings, methods in the Synthetic Control family like Abadie \BOthers. (\APACyear2010) and Arkhangelsky \BOthers. (\APACyear2021) typically require the average target cohort’s loadings to lie in the convex hull of the loadings of the units in the donor pool. In the context of bipartite match outcomes, Bonhomme \BOthers. (\APACyear2019) require every latent type of row-type unit to be matched with every latent type of column-type unit. In Section 4.3, none of the additional sets of assumptions we discuss require overlapping support in the cohort-specific loading distributions for Assumption 4.1 to hold either. As such, our approach is robust to large discrepancies in the unobserved confounding variables across cohorts, so long as the low-rank factor model (2.2) is correctly specified.

4.2 Asymptotic Linearity of Given Cohort-Specific Factors

Having shown how to identify the column space of and, by extension, , we now turn to showing that the plug-in estimator described in Section 3 yields asymptotically linear estimates of these parameters. First, we introduce some convenient notation. Let denote the vectorization of the matrix , i.e. the vector containing the columns of the matrix stacked in order, and let denote the expectation operator with respect to the empirical measure with sample size .

To highlight the contributions of this paper, as in Section 4.1, we will assume in this section that we are equipped with asymptotically linear estimators of the column spaces of , represented uniquely by :

Assumption 4.3.

For each cohort , there exists a function of and such that the vectorization of the estimated cohort-specific factor projection matrix satisfies the following asymptotic expansion as :

| (4.4) |

, and .

In Section 4.3, we will discuss several sets of additional assumptions standard in the rich literature on factor models under which estimators satisfying Assumption 4.3 exist.

Before continuing, we note that, at first glance, Assumption 4.3 might appear to be chosen simply to imply asymptotic linearity of the empirical APM without much effort, since the population APM and its plug-in counterpart can be directly expressed as sums of and across , respectively. While Assumption 4.3 is certainly convenient for this reason, perhaps more importantly, it is also a weaker requirement on the cohort-specific factor matrix estimators than assuming the kind of asymptotic linearity guarantees typically shown under stronger assumptions in the literature on factor estimation, as discussed in more detail in Section 4.3 and Appendix D.3.

Next, we can show that the plug-in estimator of is asymptotically linear in the following sense, where denotes the Kronecker product:

Theorem 4.4.

We provide a proof of Theorem 4.4 in Appendix A.4. Our proof relies on an exact, first-order expansion of the operator mapping a symmetric matrix into the projection matrix onto the space spanned by some subset of its eigenvectors derived using Kato’s integral (Kato, \APACyear1949). Since the projection matrix onto the space spanned by a matrix’s columns is a unique representation of that matrix’s column space, this expansion allows us to directly bound the error incurred by as an estimator of the column space of under minimal assumptions on the eigenvalues of . Because it is exact, our expansion appears to be new as far as we are aware. Since this expansion may be of independent interest, we provide a self-contained description and proof in Appendix B.

Having shown that our plug-in estimator of the column space of is asymptotically linear, we now turn to showing that is therefore also an asymptotically linear estimator of . To do so, we require the following additional regularity conditions on cohort sizes and outcome moments, where denotes the vector that collects unit ’s outcomes:

Assumption 4.4.

For all cohorts , and .

As it happens, we can express as a known function of and , which enables us to derive a first-order asymptotic expansion of our plug-in estimator with respect to .272727Such a result may be no surprise given that the Moore-Penrose pseudo-inverse of a tall matrix is invariant to an invertible transformation of the matrix’s rows. This result implies has exactly our desired properties:

Theorem 4.5.

We provide a proof of Theorem 4.5 in Appendix A.5. We note that both and are invariant to changes of ’s basis.

Given ’s asymptotic linearity, we can derive the asymptotic properties of the plug-in estimator of some target estimand and the inference procedure for introduced in Section 3 as corollaries, where is a known, smooth function of and a vector of nuisance parameters that are consistently estimable at a parametric rate. In particular, in Appendix D.1, we prove that is asymptotically normal and that our Bayesian-bootstrap-based simultaneous confidence intervals for described in Section 3 have valid simultaneous coverage of the coordinates of under minimal additional regularity conditions.

In Appendix D.1, we also formally describe two examples of target parameters that satisfy those regularity conditions. For event study settings, we show how the dynamic treatment effect parameters discussed in Callaway \BBA Sant’Anna (\APACyear2021) and L. Sun \BBA Abraham (\APACyear2021) fit into our framework. For studying match outcomes, we introduce a decomposition of the difference in average observed match outcomes between two column-type units that attributes shares of that contrast to differences in the column-type units’ effects on match outcomes and selection of row-type units into certain matches, analogous to the target parameter in Finkelstein \BOthers. (\APACyear2016).

4.3 Identifying and Estimating Cohort-Specific Factors

Having established that, given sufficiently accurate estimates of cohort-specific factor projection matrices , our approach yields consistent estimates of and allows us to conduct valid inference on functions of outcome means, we now turn to constructing such estimates of . Importantly, without additional assumptions, cannot be identified (Anderson \BBA Rubin, \APACyear1956). As such, in this section, we provide a non-exhaustive discussion of several common sets of assumptions from the rich literature on estimating factor models without missing outcomes that enable identification and estimation of when the number of observed outcomes for cohort remains fixed as grows.

Uncorrelated, Homoskedastic Outcomes.

First, we discuss a minimal set of assumptions that allows the canonical Principal Components (PC) estimator to yield consistent estimates of when we require to stay finite as grows. In particular, let denote the matrix of cohort ’s observed outcomes’ second moments:

| (4.9) |

and let be any matrix whose columns are eigenvectors of corresponding to ’s largest eigenvalues. Further, let denote a weighted empirical counterpart of for some vector of weights that are non-negative and sum to one:

| (4.10) |

and define the (weighted) PC estimator of to be any matrix whose columns are eigenvectors of corresponding to ’s largest eigenvalues.282828As discussed in Footnote 17 in Section 3, eigendecompositions can be computed efficiently using optimized routines available in most programming languages. When , we abuse notation slightly and let and .

Importantly, the PC estimator does not require any auxiliary data like covariates or instruments to be consistent, and, since it is equivalent to an eigendecomposition, efficient algorithms exist for its computation. The costs of its simplicity are the assumptions it requires. First, all loadings must have nontrivial variances, which rules out the case where all units have the same loadings. Second, the residuals must be uncorrelated across units and outcomes , and, while they can have arbitrarily varying variances across units , they must be constant across outcomes .

While these assumptions are weaker than the requirement from the classical factor model literature that be drawn independently from the same mean-zero Gaussian distribution (see e.g. Anderson (\APACyear1963)), Theorem 4 in J. Bai (\APACyear2003) proves that they are both sufficient (as shown in Connor \BBA Korajczyk (\APACyear1986)) and necessary for the PC estimator to be consistent when remains fixed as grows. In Appendix D.3, we state these assumptions formally and prove directly that is an asymptotically linear estimator of as required by Assumption 4.3 under slightly weaker conditions than are typically imposed in the literature. To do so, we again rely on our first-order expansion of the eigenspace projection operator described in Appendix B.

Uncorrelated, Heteroskedastic Outcomes.

If we are instead only willing to believe that the residuals are uncorrelated across units and outcomes but can have arbitrarily heterogeneous variances across both units and outcomes, then the PC estimator will be inconsistent for if remains fixed as grows (Chamberlain \BBA Rothschild, \APACyear1983; J. Bai, \APACyear2003).292929In fact, the PC estimator is numerically equivalent to minimizing a least squares objective with respect to and every so, as shown in Chamberlain \BBA Rothschild (\APACyear1983), suffers from the incidental parameter problem under residual heteroskedasticity (Neyman \BBA Scott, \APACyear1948; T. Lancaster, \APACyear2000). Instead, the literature suggests estimating via an optimization-based approach called Factor Analysis (FA) (see e.g. Chapter 14 of Anderson (\APACyear2009)). While the global maximizers of the FA objective yield asymptotically linear estimators of assuming the population parameters maximize the population objective (Anderson, \APACyear2009), the objective is non-concave, and even state-of-the-art algorithms for verifiably computing its global maximum are difficult to scale for even moderate and (Bertsimas \BOthers., \APACyear2017; Khamaru \BBA Mazumder, \APACyear2019).

Instead, in Appendix D.4, we sketch a new, computationally efficient procedure for estimating that can be applied when residuals are uncorrelated but heteroskedastic so long as at least outcomes are observed per cohort, like internal-instruments-based approaches to identifying factors under uncorrelated but heteroskedastic residuals (Madansky, \APACyear1964; Heckman \BBA Scheinkman, \APACyear1987; Freyberger, \APACyear2018; Harding \BOthers., \APACyear2022). The procedure is based on the fact that, if we split the observed outcomes for a given cohort into two disjoint subsets, the matrix of covariances between pairs of observed outcomes from the two subsets is determined solely by the factor structure. As such, the top left singular vectors of this matrix yield estimates of the factor vectors corresponding to each subset of outcomes with respect to the same basis. Repeating this procedure for a particular sequence of partitions of a cohort’s observed outcomes yields factor vector estimates that can then be “stitched together” via another application of our APM-based factor estimation procedure. This procedure is guaranteed to recover with only eigendecompositions.

Other Identifying Assumptions Via Auxiliary Data.

With access to auxiliary data, we can also relax the assumption of uncorrelatedness of residuals across outcomes using several different approaches. One approach is to assume that some vector of at least unit-and-outcome-specific covariates are also outcome-specific linear functions of plus covariate residuals that are uncorrelated with and . Then one can apply the Common Correlated Effects method (Pesaran, \APACyear2006; Westerlund \BOthers., \APACyear2019), Essential Regression (Bing \BOthers., \APACyear2022), transfer learning (Duan \BOthers., \APACyear2023), or the Diversified Projections method (Fan \BBA Liao, \APACyear2022) to estimate . Alternatively, given access to at least unit-and-outcome-specific external instruments that are correlated with the coordinates of but not , one can apply the GMM estimators proposed in Ahn \BOthers. (\APACyear2013) and Robertson \BBA Sarafidis (\APACyear2015) to estimate .

5 Empirical Illustration

5.1 Setting

Our empirical illustration of our methods is based on data from the Veneto Worker Histories (VWH) dataset, which is a dataset derived from the Italian social security administration containing the full history of weekly wages for every person who ever lived or worked in any of the seven provinces in the Veneto region of Italy from 1975 to 2001.303030As noted in Footnote 4, the VWH dataset was developed by the Economics Department in Università Ca’ Foscari Venezia under the supervision of Giuseppe Tattara, and can be accessed at https://www.frdb.org/en/dati/dati-inps-carriere-lavorative-in-veneto/. Each observation corresponds to a worker working for a firm in a given year, and contains information about the number of weeks that person worked at that firm in that year as well as the total wages they were paid for doing so.

We will focus on characterizing the performance of our procedure as an alternative to TWFE-based methods for assessing to what degree worker’s locations causally affect their wages as opposed to differences in workers’ observed wages across locations being driven by purely worker sorting, in the spirit of Card \BOthers. (\APACyear2023). As discussed in Example D.2 inspired by Finkelstein \BOthers. (\APACyear2016) in Appendix D.1, an important input to any such analysis are predicted counterfactual wages for workers had they instead worked in locations we do not observe them working at in the data. The workhorse methods for constructing these predicted counterfactual wages are based on the TWFE model (Abowd \BOthers., \APACyear1999; Finkelstein \BOthers., \APACyear2016; Card \BOthers., \APACyear2023), such methods rule out any complementarities between workers and certain locations, unlike predicted average counterfactual wages given by our factor-model-based method.313131Bonhomme \BOthers. (\APACyear2019) note that typical empirical tests in the literature that claim to not detect match effects in fact have no power under a variety of models that allow for worker-firm complementarities (see Card \BOthers. (\APACyear2013) for an example deploying such tests). As mentioned in the discussion of their results, Card \BOthers. (\APACyear2013) do find some evidence for the existence of match effects and suggest that characterizing them further is worth future study.

To assess how our method performs relative to a TWFE regression at predicting counterfactual mean wages for workers across provinces, we construct a panel dataset that fits within our setup of interest as follows. First, we restrict our attention to workers and the 174,470 unique within-Veneto firms at which they worked between 1991 and 2001 to diminish the impact of long-run secular trends on our results. To avoid understating the degree to which wages are determined by workers’ provinces of employment by ignoring within-province firm heterogeneity (Card \BOthers., \APACyear2023),323232Borrowing an example from Card \BOthers. (\APACyear2023), if a worker moves from a low-wage province to a high-wage province, they are likely moving between firms that pay relatively similar wages. As such, the origin firm in the low-wage province must pay well relative to the other firms in the low-wage province, while the destination firm must pay poorly relative to the other firms in the high-wage province. Thus, if we only let outcomes correspond to the average wages workers could earn in different provinces, we would wrongly assume that because workers’ wages didn’t change much when moving across places, the places must not have large effects on wages. we cluster the between 8,000 and 30,000 firms located in each province into three types using the -means-based procedure proposed in Bonhomme \BOthers. (\APACyear2019); details can be found in Appendix E.1. We then let index the pair of provinces and firm types within provinces, meaning , and define the observed outcome as the natural logarithm of worker ’s average weekly wage earned while working at all firms belonging to province-and-firm-type pair between 1991 and 2001. Outcomes can then be defined similarly, but correspond to potentially counterfactual average weekly wages earned at province-and-firm-type pairs that worker never actually worked at during the relevant time period.

After defining the dimension of our panel dataset, we restrict our sample to the 327,125 unique workers who moved between province-and-firm-type pairs at least once between 1991 and 2001, in keeping with the literature on matched employer-employee data (Abowd \BOthers., \APACyear1999; Card \BOthers., \APACyear2013). Figure 1(b) illustrates the complexity of the outcome missingness pattern generated by this dataset. We note that no embedded block missingness pattern exists for many target cohorts and outcomes, precluding the use of methods that rely on the existence of reference cohorts, as discussed in Section 2.2. In contrast, the observed outcome overlap graph (which is illustrated in Figure 1(b)) is connected, so Assumption 4.2 holds and and are identified so long as . As such, we focus on comparing our method to imputations based on TWFE regressions in our empirical evaluation below. We note that assuming rules out the existence of multidimensional unobserved confounders still allows for complementarity between worker and province-by-firm-type effects in determining outcomes, unlike the TWFE model.

5.2 Semi-Synthetic Simulation Study of Estimator Performance

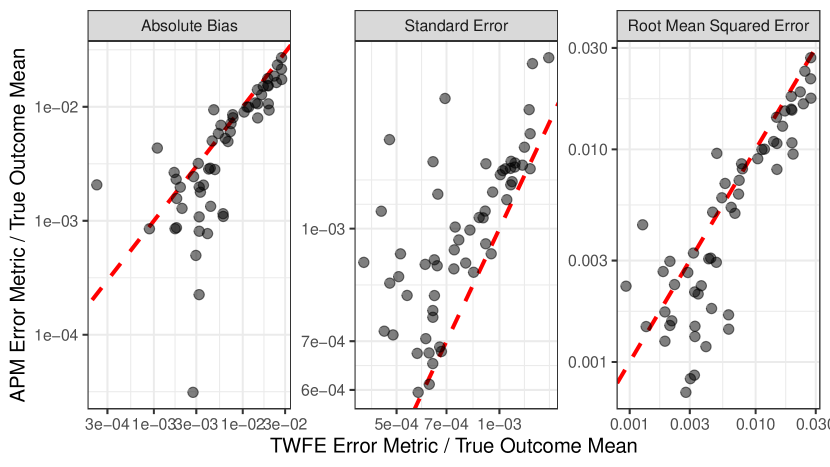

To evaluate the performance of our method at predicting counterfactual outcome means, we conduct a semi-synthetic simulation study based on the dataset whose construction we described in Section 5.1. First, we choose a target cohort of workers that move between province-by-firm-types at least twice (so that at least three of their outcomes are observed) and “mask” one of their outcomes , treating it as if it were unobserved. Next, we resample with replacement from each cohort in this masked dataset 100 times, constructing 100 synthetic datasets drawn from the same distribution and with the same cohort sizes as our masked dataset but without the target outcome observed for the units in the target cohort . For each masked synthetic dataset, we compute using our method, as well as a TWFE-based analog. Finally, we evaluating the accuracy of each estimator by computing the absolute bias, standard error, and root mean squared error over the 100 estimates constructed using each estimator, treating the actual sample mean in our original, unmasked dataset of the target outcome for the units in the target cohort as the ground truth. To give a representative sense of each estimator’s accuracy, we repeat this bootstrapped estimator evaluation procedure across every observed outcome for the 15 largest cohorts of workers that work for firms of at least three different province-by-firm types.

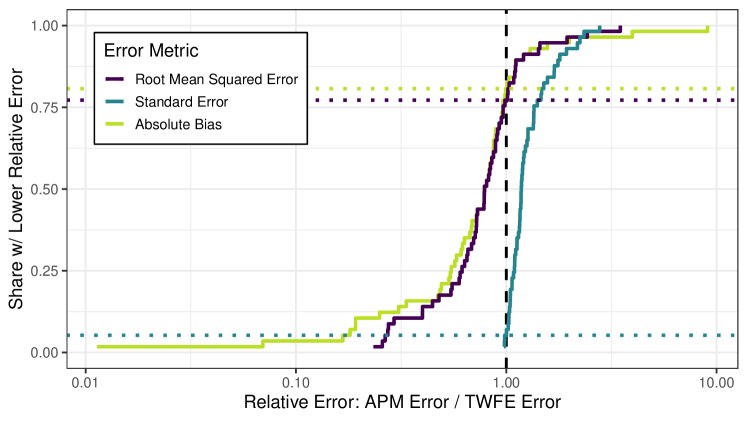

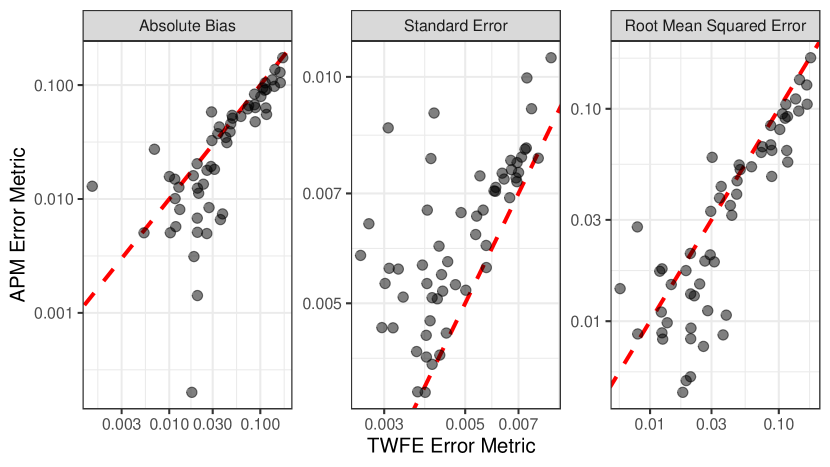

We illustrate the distributions of our estimation error metrics across target cohorts and outcomes in Figure 5.1. In particular, Figure 5.1 plots the cumulative distribution functions (CDF) of error metric ratios between our estimator and the TWFE-based estimator across masked target parameters. For over 75% of target cohorts and outcomes, our factor-model-based method attains smaller root mean squared error than the TWFE-based estimator. This frequent better performance is due to our estimator having lower bias than the TWFE-based estimator for over 80% of target cohorts and outcomes. The price of using our estimator over a TWFE-based estimator tends to be slightly higher variance, as indicated by the fact that the TWFE-based estimator had lower variance for over 90% of the target cohorts and outcomes we considered. However, the increased variance of our estimator is not enough to outweigh our estimator’s smaller bias relative to a TWFE-based estimator when comparing the root mean squared errors of the two methods, as discussed above. In Figure E.2, we provide scatter plots illustrating the estimators’ absolute error metric values and error metric values relative to the values of the target cohort outcome means across target cohorts and outcomes. Overall, this semi-synthetic simulation study provides more evidence that accounting for complementarities between workers and firms using a method like ours can yield more accurate estimates of average counterfactual match outcomes in bipartite matching settings.

6 Conclusion

In this paper, we develop a new approach for identifying and estimating average counterfactual outcomes with short panel data applicable in settings like event studies and studies of bipartite match outcomes. Relying only on an eigendecomposition of a new spectral operator, our method produces consistent, asymptotically normal estimates of means of outcomes generated by a latent factor model under general outcome missingness patterns as only the cross-sectional dimension of a panel grows large. Importantly, our procedure accommodates more general missingness patterns than other approaches for short panels, and it automatically stitches together different pieces of identifying information each used in isolation by existing methods. Through our simulation study based on the Veneto Worker Histories dataset, we also demonstrate the practicality of our approach in real-world “short” panel data settings.

References

- Abadie \BOthers. (\APACyear2010) \APACinsertmetastarabadie2010synthetic{APACrefauthors}Abadie, A., Diamond, A.\BCBL \BBA Hainmueller, J. \APACrefYearMonthDay2010. \BBOQ\APACrefatitleSynthetic control methods for comparative case studies: Estimating the effect of California’s tobacco control program Synthetic control methods for comparative case studies: Estimating the effect of california’s tobacco control program.\BBCQ \APACjournalVolNumPagesJournal of the American Statistical Association105490493–505.

- Abowd \BOthers. (\APACyear2002) \APACinsertmetastarabowd2002computing{APACrefauthors}Abowd, J\BPBIM., Creecy, R\BPBIH.\BCBL \BBA Kramarz, F. \APACrefYearMonthDay2002. \APACrefbtitleComputing person and firm effects using linked longitudinal employer-employee data Computing person and firm effects using linked longitudinal employer-employee data \APACbVolEdTR\BTR. \APACaddressInstitutionCenter for Economic Studies, US Census Bureau.

- Abowd \BOthers. (\APACyear1999) \APACinsertmetastarabowd1999high{APACrefauthors}Abowd, J\BPBIM., Kramarz, F.\BCBL \BBA Margolis, D\BPBIN. \APACrefYearMonthDay1999. \BBOQ\APACrefatitleHigh wage workers and high wage firms High wage workers and high wage firms.\BBCQ \APACjournalVolNumPagesEconometrica672251–333.

- Agarwal, Dahleh\BCBL \BOthers. (\APACyear2023) \APACinsertmetastaragarwal2021causal{APACrefauthors}Agarwal, A., Dahleh, M., Shah, D.\BCBL \BBA Shen, D. \APACrefYearMonthDay2023. \BBOQ\APACrefatitleCausal matrix completion Causal matrix completion.\BBCQ \BIn \APACrefbtitleThe Thirty Sixth Annual Conference on Learning Theory The thirty sixth annual conference on learning theory (\BPGS 3821–3826).

- Agarwal, Shah\BCBL \BBA Shen (\APACyear2023) \APACinsertmetastaragarwal2020synthetic{APACrefauthors}Agarwal, A., Shah, D.\BCBL \BBA Shen, D. \APACrefYearMonthDay2023. \BBOQ\APACrefatitleSynthetic Interventions Synthetic interventions.\BBCQ \APACjournalVolNumPagesarXiv preprint arXiv:2006.07691.

- Ahn \BBA Horenstein (\APACyear2013) \APACinsertmetastarahn2013eigenvalue{APACrefauthors}Ahn, S\BPBIC.\BCBT \BBA Horenstein, A\BPBIR. \APACrefYearMonthDay2013. \BBOQ\APACrefatitleEigenvalue ratio test for the number of factors Eigenvalue ratio test for the number of factors.\BBCQ \APACjournalVolNumPagesEconometrica8131203–1227.

- Ahn \BOthers. (\APACyear2013) \APACinsertmetastarahn2013panel{APACrefauthors}Ahn, S\BPBIC., Lee, Y\BPBIH.\BCBL \BBA Schmidt, P. \APACrefYearMonthDay2013. \BBOQ\APACrefatitlePanel data models with multiple time-varying individual effects Panel data models with multiple time-varying individual effects.\BBCQ \APACjournalVolNumPagesJournal of Econometrics17411–14.

- Anderson (\APACyear1963) \APACinsertmetastaranderson1963asymptotic{APACrefauthors}Anderson, T\BPBIW. \APACrefYearMonthDay1963. \BBOQ\APACrefatitleAsymptotic theory for principal component analysis Asymptotic theory for principal component analysis.\BBCQ \APACjournalVolNumPagesThe Annals of Mathematical Statistics341122–148.

- Anderson (\APACyear2009) \APACinsertmetastaranderson2009introduction{APACrefauthors}Anderson, T\BPBIW. \APACrefYear2009. \APACrefbtitleAn Introduction to Multivariate Statistical Analysis, 3rd Edition An introduction to multivariate statistical analysis, 3rd edition. \APACaddressPublisherWiley-Interscience.

- Anderson \BBA Rubin (\APACyear1956) \APACinsertmetastaranderson1956statistical{APACrefauthors}Anderson, T\BPBIW.\BCBT \BBA Rubin, H. \APACrefYearMonthDay1956. \BBOQ\APACrefatitleStatistical Inference in Factor Analysis Statistical inference in factor analysis.\BBCQ \BIn \APACrefbtitleProceedings of the Third Berkeley Symposium on Mathematical Statistics and Probability: Held at the Statistical Laboratory, University of California, December, 1954, July and August, 1955 Proceedings of the third berkeley symposium on mathematical statistics and probability: Held at the statistical laboratory, university of california, december, 1954, july and august, 1955 (\BVOL 1, \BPG 111).

- Andrews \BOthers. (\APACyear2008) \APACinsertmetastarandrews2008high{APACrefauthors}Andrews, M\BPBIJ., Gill, L., Schank, T.\BCBL \BBA Upward, R. \APACrefYearMonthDay2008. \BBOQ\APACrefatitleHigh wage workers and low wage firms: negative assortative matching or limited mobility bias? High wage workers and low wage firms: negative assortative matching or limited mobility bias?\BBCQ \APACjournalVolNumPagesJournal of the Royal Statistical Society: Series A (Statistics in Society)1713673–697.

- Angrist \BBA Pischke (\APACyear2009) \APACinsertmetastarangrist2009mostly{APACrefauthors}Angrist, J\BPBID.\BCBT \BBA Pischke, J\BHBIS. \APACrefYear2009. \APACrefbtitleMostly harmless econometrics: An empiricist’s companion Mostly harmless econometrics: An empiricist’s companion. \APACaddressPublisherPrinceton university press.

- Arkhangelsky \BOthers. (\APACyear2021) \APACinsertmetastararkhangelsky2021synthetic{APACrefauthors}Arkhangelsky, D., Athey, S., Hirshberg, D\BPBIA., Imbens, G\BPBIW.\BCBL \BBA Wager, S. \APACrefYearMonthDay2021. \BBOQ\APACrefatitleSynthetic difference-in-differences Synthetic difference-in-differences.\BBCQ \APACjournalVolNumPagesAmerican Economic Review111124088–4118.

- Arkhangelsky \BBA Hirshberg (\APACyear2023) \APACinsertmetastararkhangelsky2023largesample{APACrefauthors}Arkhangelsky, D.\BCBT \BBA Hirshberg, D. \APACrefYearMonthDay2023. \BBOQ\APACrefatitleLarge-Sample Properties of the Synthetic Control Method under Selection on Unobservables Large-sample properties of the synthetic control method under selection on unobservables.\BBCQ \APACjournalVolNumPagesarXiv preprint arXiv:2311.13575.

- Ashenfelter \BBA Card (\APACyear1985) \APACinsertmetastarashenfelter1985using{APACrefauthors}Ashenfelter, O.\BCBT \BBA Card, D. \APACrefYearMonthDay1985. \BBOQ\APACrefatitleUsing the longitudinal structure of earnings to estimate the effect of training programs Using the longitudinal structure of earnings to estimate the effect of training programs.\BBCQ \APACjournalVolNumPagesThe Review of Economics and Statistics674648–660.

- Ater \BOthers. (\APACyear\bibnodate) \APACinsertmetastarater2023can{APACrefauthors}Ater, I., Shany, A., Ross, B., Turkel, E.\BCBL \BBA Vasserman, S. \APACrefYearMonthDay\bibnodate. \BBOQ\APACrefatitleCan usage-based pricing reduce traffic congestion? Can usage-based pricing reduce traffic congestion?\BBCQ \APACjournalVolNumPagesWork in progress.

- Athey \BOthers. (\APACyear2021) \APACinsertmetastarathey2021matrix{APACrefauthors}Athey, S., Bayati, M., Doudchenko, N., Imbens, G\BPBIW.\BCBL \BBA Khosravi, K. \APACrefYearMonthDay2021. \BBOQ\APACrefatitleMatrix completion methods for causal panel data models Matrix completion methods for causal panel data models.\BBCQ \APACjournalVolNumPagesJournal of the American Statistical Association1165361716–1730.

- J. Bai (\APACyear2003) \APACinsertmetastarbai2003inferential{APACrefauthors}Bai, J. \APACrefYearMonthDay2003. \BBOQ\APACrefatitleInferential theory for factor models of large dimensions Inferential theory for factor models of large dimensions.\BBCQ \APACjournalVolNumPagesEconometrica711135–171.

- J. Bai \BBA Ng (\APACyear2002) \APACinsertmetastarbai2002determining{APACrefauthors}Bai, J.\BCBT \BBA Ng, S. \APACrefYearMonthDay2002. \BBOQ\APACrefatitleDetermining the number of factors in approximate factor models Determining the number of factors in approximate factor models.\BBCQ \APACjournalVolNumPagesEconometrica701191–221.

- J. Bai \BBA Ng (\APACyear2013) \APACinsertmetastarbai2013principal{APACrefauthors}Bai, J.\BCBT \BBA Ng, S. \APACrefYearMonthDay2013. \BBOQ\APACrefatitlePrincipal components estimation and identification of static factors Principal components estimation and identification of static factors.\BBCQ \APACjournalVolNumPagesJournal of Econometrics176118–29.

- J. Bai \BBA Ng (\APACyear2021) \APACinsertmetastarbai2021matrix{APACrefauthors}Bai, J.\BCBT \BBA Ng, S. \APACrefYearMonthDay2021. \BBOQ\APACrefatitleMatrix completion, counterfactuals, and factor analysis of missing data Matrix completion, counterfactuals, and factor analysis of missing data.\BBCQ \APACjournalVolNumPagesJournal of the American Statistical Association1165361746–1763.

- J. Bai \BBA Ng (\APACyear2023) \APACinsertmetastarbai2021approximate{APACrefauthors}Bai, J.\BCBT \BBA Ng, S. \APACrefYearMonthDay2023. \BBOQ\APACrefatitleApproximate factor models with weaker loadings Approximate factor models with weaker loadings.\BBCQ \APACjournalVolNumPagesJournal of Econometrics.

- Z. Bai \BBA Silverstein (\APACyear2010) \APACinsertmetastarbai2010spectral{APACrefauthors}Bai, Z.\BCBT \BBA Silverstein, J\BPBIW. \APACrefYear2010. \APACrefbtitleSpectral analysis of large dimensional random matrices Spectral analysis of large dimensional random matrices (\BVOL 20). \APACaddressPublisherSpringer.

- Belloni \BOthers. (\APACyear2017) \APACinsertmetastarbelloni2017program{APACrefauthors}Belloni, A., Chernozhukov, V., Fernandez-Val, I.\BCBL \BBA Hansen, C. \APACrefYearMonthDay2017. \BBOQ\APACrefatitleProgram evaluation and causal inference with high-dimensional data Program evaluation and causal inference with high-dimensional data.\BBCQ \APACjournalVolNumPagesEconometrica851233–298.

- Ben-Michael \BOthers. (\APACyear2022) \APACinsertmetastarben2022synthetic{APACrefauthors}Ben-Michael, E., Feller, A.\BCBL \BBA Rothstein, J. \APACrefYearMonthDay2022. \BBOQ\APACrefatitleSynthetic controls with staggered adoption Synthetic controls with staggered adoption.\BBCQ \APACjournalVolNumPagesJournal of the Royal Statistical Society Series B842351–381.

- Bertrand \BOthers. (\APACyear2004) \APACinsertmetastarbertrand2004much{APACrefauthors}Bertrand, M., Duflo, E.\BCBL \BBA Mullainathan, S. \APACrefYearMonthDay2004. \BBOQ\APACrefatitleHow much should we trust differences-in-differences estimates? How much should we trust differences-in-differences estimates?\BBCQ \APACjournalVolNumPagesThe Quarterly Journal of Economics1191249–275.

- Bertsimas \BOthers. (\APACyear2017) \APACinsertmetastarbertsimas2017certifiably{APACrefauthors}Bertsimas, D., Copenhaver, M\BPBIS.\BCBL \BBA Mazumder, R. \APACrefYearMonthDay2017. \BBOQ\APACrefatitleCertifiably optimal low rank factor analysis Certifiably optimal low rank factor analysis.\BBCQ \APACjournalVolNumPagesThe Journal of Machine Learning Research181907–959.

- Bing \BOthers. (\APACyear2022) \APACinsertmetastarbing2022inference{APACrefauthors}Bing, X., Bunea, F.\BCBL \BBA Wegkamp, M. \APACrefYearMonthDay2022. \BBOQ\APACrefatitleInference in latent factor regression with clusterable features Inference in latent factor regression with clusterable features.\BBCQ \APACjournalVolNumPagesBernoulli282997–1020.

- Bonhomme (\APACyear2020) \APACinsertmetastarbonhomme2020econometric{APACrefauthors}Bonhomme, S. \APACrefYearMonthDay2020. \BBOQ\APACrefatitleEconometric analysis of bipartite networks Econometric analysis of bipartite networks.\BBCQ \BIn \APACrefbtitleThe econometric analysis of network data The econometric analysis of network data (\BPGS 83–121). \APACaddressPublisherElsevier.

- Bonhomme \BOthers. (\APACyear2023) \APACinsertmetastarbonhomme2023much{APACrefauthors}Bonhomme, S., Holzheu, K., Lamadon, T., Manresa, E., Mogstad, M.\BCBL \BBA Setzler, B. \APACrefYearMonthDay2023. \BBOQ\APACrefatitleHow much should we trust estimates of firm effects and worker sorting? How much should we trust estimates of firm effects and worker sorting?\BBCQ \APACjournalVolNumPagesJournal of Labor Economics412291–322.

- Bonhomme \BOthers. (\APACyear2019) \APACinsertmetastarbonhomme2019distributional{APACrefauthors}Bonhomme, S., Lamadon, T.\BCBL \BBA Manresa, E. \APACrefYearMonthDay2019. \BBOQ\APACrefatitleA distributional framework for matched employer employee data A distributional framework for matched employer employee data.\BBCQ \APACjournalVolNumPagesEconometrica873699–739.