Partial Information Breeds Systemic Risk

Abstract

This paper considers finitely many investors who perform mean-variance portfolio selection under a relative performance criterion. That is, each investor is concerned about not only her terminal wealth, but how it compares to the average terminal wealth of all investors (i.e., the mean field). At the inter-personal level, each investor selects a trading strategy in response to others’ strategies (which affect the mean field). The selected strategy additionally needs to yield an equilibrium intra-personally, so as to resolve time inconsistency among the investor’s current and future selves (triggered by the mean-variance objective). A Nash equilibrium we look for is thus a tuple of trading strategies under which every investor achieves her intra-personal equilibrium simultaneously. We derive such a Nash equilibrium explicitly in the idealized case of full information (i.e., the dynamics of the underlying stock is perfectly known), and semi-explicitly in the realistic case of partial information (i.e., the stock evolution is observed, but the expected return of the stock is not precisely known). The formula under partial information involves an additional state process that serves to filter the true state of the expected return. Its effect on trading is captured by two degenerate Cauchy problems, one of which depends on the other, whose solutions are constructed by elliptic regularization and a stability analysis of the state process. Our results indicate that partial information alone can reduce investors’ wealth significantly, thereby causing or aggravating systemic risk. Intriguingly, in two different scenarios of the expected return (i.e., it is constant or alternating between two values), our Nash equilibrium formula spells out two distinct manners systemic risk materializes.

MSC (2020): 91G45, 91A80, 93E11

Keywords: mean-variance portfolio selection, relative performance criterion, systemic risk, partial information, filtering, regime switching, soft inter-personal equilibria

1 Introduction

Central to financial stability is the understanding of systemic risk, the risk that numerous financial institutions default concurrently or successively. Various aspects of systemic risk has been studied (see e.g., Fouque and Langsam [14]) and one essential endeavor is to recover systemic risk through rigorous mathematical modeling, which helps us determine the causes of the risk.

Under homogeneous inter-bank lending and borrowing, exogenously modeled by coupled Ornstein-Uhlenbeck-type processes, Fouque and Sun [15] find that systemic risk shows up constantly. Carmona et al. [7] upgrade the exogenous inter-bank interaction by adding an endogenous control element, allowing each bank to control its interaction with a central bank. The resulting game with multiple banks is further investigated in Carmona et al. [6] under delayed controls (which resemble realistic repayments), in Fouque and Ichiba [13] and Sun [33] under coupled Cox-Ingersoll-Ross-type processes, and in Garnier et al. [18, 19, 20] under a bistable dynamics for banks. While homogeneity among banks underlies the above studies, it has been generalized in several directions, capturing heterogeneity in reserve dynamics and cost structures (e.g., Fang et al. [11] and Sun [34]), in capital requirements (e.g., Capponi et al. [5]), and in locations (such as “core” versus “periphery”) on a banking network (e.g., Biagini et al. [2] and Feinstein and Sojmark [12]).

In this paper, we present a new cause of systemic risk, relying on financial models distinct from all the above. While the literature has focused on how inter-bank activities contribute to systemic risk, our thesis is that systemic risk is more general than this: it can be triggered by other factors beyond the inter-bank market.

We consider investors (e.g., fund managers) who trade a stock on a finite time horizon , subject to a relative performance criterion. That is, in line with Espinosa and Touzi [10] and Lacker and Zariphopoulou [28], when choosing her trading strategy , the -th investor () is concerned about not only her terminal wealth , but also how it compares to the average wealth of all investors (i.e., the relative performance), thereby considering the mixed performance for some . In [10] and [28], each investor chooses by maximizing expected utility of given others’ strategies , which results in a Nash equilibrium for this -player game. By contrast, we assume that each investor selects under a mean-variance objective associated with ; see (2.7) below.

As a mean-variance objective induces time inconsistency, what constitutes a Nash equilibrium is nontrivial. As explained in Huang and Zhou [24], in a dynamic game where players have time-inconsistent preferences, two levels of game-theoretic reasoning are intertwined. At the inter-personal level, each player selects an action in response to other players’ chosen strategies. The selected action, importantly, has to be an equilibrium at the intra-personal level, so as to resolve time inconsistency among this player’s current and future selves. As a result, we say is a Nash equilibrium, if for every , is the -th investor’s intra-personal equilibrium given others’ strategies —namely, every player achieves her own intra-personal equilibrium simultaneously (Definition 2.2). This amounts to a “soft inter-personal equilibrium” in [24], while the stronger notion “sharp inter-personal equilibrium” therein cannot be easily defined for a mean-variance objective; see the discussion below Definition 2.2.

The focus of this paper is to investigate how a Nash equilibrium changes from the case of full information (where investors know the precise dynamics of ) to that of partial information (where investors only observe the evolution of ). Note that it is the latter case that reflects the reality: investors in practice do not know the precise dynamics of , but attempt to infer that from the observed evolution of . As we will see, this change from an idealized case to a realistic one can drastically enlarge systemic risk.

For concreteness, we assume that investors do not know precisely the expected return of , except that it has two possible values (with ). Our analysis breaks into two distinct scenarios: (i) is a fixed constant, and investors attempt to infer the true value of between and ; (ii) , where is a two-state continuous-time Markov chain, and investors attempt to infer the recurring changes of between and . The first scenario applies to the stock of a company with unreported innovation (see Koh and Reeb [27]), for which investors need to infer if an innovation has raised the expected return from to . The second scenario, on the other hand, models the repeated shifts between a bull and a bear market.

As baselines of our analysis, Theorem 2.1 (resp. Theorem 3.1) presents an explicit Nash equilibrium under full information (i.e., when is perfectly known). These results are already new to the literature. The former generalizes the extended Hamilton-Jacobi-Bellman (HJB) equation in Björk et al. [3, Section 10], derived for the classical mean-variance problem of one single agent, to the current multi-player setting. The latter further integrates the regime-switching framework of [36] into our multi-player extended HJB equation.

When is an unknown constant, investors compute the probability of conditioned on the observed evolution of by the current time ; see (2.15) below. By the theory of nonlinear filtering, this posterior probability, denoted by , satisfies a stochastic differential equation (SDE), i.e., (2.18) below, that involves only known model parameters (such as ); see Lemma 2.2. This allows the original dynamics of , which involves the unknown , to be expressed equivalently in terms of the observable process , such that portfolio selection can be performed based on the joint observation . The additional state process complicates the search for a Nash equilibrium. To fully capture the dependence on , we need the solutions to two intricate Cauchy problems, one of which depends on the derivative of the other; see (2.25) and (2.34) below (with ). As the first Cauchy problem is degenerate, we construct a classical solution to it by elliptic regularization, i.e., through a careful approximation by uniformly elliptic equations. By analyzing the -derivative of the process with respect to (w.r.t.) its initial value (introduced in Friedman [17]), we further show that the constructed solution and its partial derivative w.r.t. are both bounded and admit concrete stochastic representations; see Lemma 2.3 and its proof in Section A.3 for details. For the second Cauchy problem, which is also degenerate, a solution and its stochastic representation are constructed by similar arguments (Corollary 2.1). Ultimately, by solving the extended HJB equation for the investors (which is a coupled system of partial differential equations), we obtain a Nash equilibrium and the corresponding value functions in semi-explicit forms, in terms of the solutions to the two Cauchy problems; see Theorem 2.2 for details.

In the second scenario where alternates between and behind the scenes, investors compute the probability of (i.e., ) conditioned on the observed evolution of by the current time ; see (3.9) below. Arguments for the previous scenario can then be similarly carried out. Specifically, the above posterior probability, denoted again by , also satisfies an SDE—in fact, it is the one in the previous scenario plus a drift term (i.e., (3.12) below); see Lemma 3.1. This drift term shows up in the aforementioned Cauchy problems, as an additional coefficient of the first derivative w.r.t. . Solving the -player extended HJB equation then yields the same formulas as before (for a Nash equilibrium and the corresponding value functions), except that the involved Cauchy problems contain a new term induced by the added drift; see Theorem 3.2 for details.

Now, we compare numerically the results under partial information with those under full information. In the scenario of a constant , as shown in the first and third plots of Figure 1(a), investors’ wealth processes under partial information (i.e., under Theorem 2.2) is significantly lower than those under full information (i.e., under Theorem 2.1), with some falling below the default level 0. The empirical loss distribution (the second plot, Figure 1(c)), computed via 100 simulations of investors’ wealth processes, shows no default at all under full information but numerous defaults under partial information. In the scenario of an alternating , as shown in the first and third plots of Figure 2(a), investors’ wealth is again substantially reduced under partial information (i.e., under Theorem 3.2) from the baseline levels under full information (i.e., under Theorem 3.1). The empirical loss distribution (the second plot, Figure 2(c)), computed again via 100 simulations, shows a jump of the probability that all investors default from 43% under full information to 56% under partial information. The finding is clear across the board: partial information curtails the growth of wealth, thereby causing or aggravating systemic risk. Despite this clear message, exactly how partial information reduces wealth demands a closer examination.

Under partial information, each investor’s equilibrium trading strategy (i.e., in (2.37) below) contains two terms. The first one is identical with the full-information trading strategy (i.e., (2.12) or (3.5) below), except that investors replace (unknown under partial information) by the estimate , where is the aforementioned probability of conditioned on the observation of by the current time . Based on how reliable this current judgement is, the second term jumps in to make adjustments. As explained in detail below Theorem 2.2, the second term of involves the aforementioned -derivative of w.r.t. the initial value , which crucially measures how intensely will oscillate on . When will oscillate wildly on (making unreliable), the second term of tends to be large, adjusting our action based on (i.e., the first term of ) significantly. When will be stable on (making reliable), the second term of tends to be small, providing only a slight adjustment.

With the precise understanding of the equilibrium trading strategy in (2.37), we can see clearly how systemic risk occurs. Intriguingly, in the two distinct scenarios of , systemic risk is triggered in different ways. When is a constant, the posterior probability satisfies an SDE (i.e., (2.18) below) that oscillates forcefully between 0 and 1, but generally moves in the right direction quickly (i.e., towards when , and when ). Hence, the estimate tends to move near the true value of quickly, bringing the first term of close to the ideal (full-information) trading strategy (2.12). The strong oscillation of , however, inflates the second term of significantly. This can heavily distort as a whole away from ideal trading, whence reduces investors’ wealth markedly; see Section 4.1 for detailed discussions and numerical illustrations. When is alternating, satisfies an SDE (i.e., (3.12) below) with a mean-reverting drift term. As always tends to return to a mean level between 0 and 1, the estimate never stays close to either or for long, leaving the first term of distinct from ideal trading indefinitely. This lasting deviation from the ideal can readily reduce investors’ wealth significantly. The mean-reverting property, on the other hand, dampens the oscillation of . The modest oscillation then keeps the second term of small, giving an inconsiderable effect on as a whole; see Section 4.2 for detailed discussions and numerical illustrations. In summary, for the scenario of a constant , the main culprit for systemic risk under partial information is the second term of ; for the scenario of an alternating , the main culprit shifts to the first term of .

The rest of the paper is organized as follows. Section 2 focuses on constant investment opportunities (i.e., is constant). For investors who consider a mean-variance objective with a relative performance criterion, we derive a Nash equilibrium under full information (Section 2.1) and one under partial information (Section 2.2). Section 3 focuses on alternating investment opportunities (i.e., is alternating), and a Nash equilibrium for the investors is again derived under full information (Section 3.1) and under partial information (Section 3.2). By comparing results under partial information with those under full information numerically, Section 4 finds that partial information can cause or aggravate systemic risk. Careful financial interpretations are made to explain how this happens in the two different scenarios of . The appendices collect proofs.

2 The Case of Constant Investment Opportunities

Let be a probability space equipped with a filtration satisfying the usual conditions. Suppose that a standard Brownian motion exists in the space. Consider a financial market with a riskfree rate and a stock price process given by

| (2.1) |

for any and , where and are fixed constants. Given a fixed time horizon , suppose that there are investors (e.g., fund managers) trading the stock . For each , the -th investor decides the amount of wealth to invest in at every time . We say is an admissible trading strategy if it is progressively measurable and satisfies We will denote by the collection of all admissible trading strategies.

2.1 Analysis under Full Information

Assume that the dynamics of in (2.1) (i.e., and ) is fully known. Hence, for any and , the wealth process of the -th investor at time is

| (2.2) |

For convenience, we will often write

By taking and , the average wealth satisfies

| (2.3) |

Suppose that each investor considers the mean-variance portfolio selection problem under a relative performance criterion. Specifically, in line with [10, 28], the -th investor, for all , is concerned about not only the terminal wealth but also how it compares relatively to the average wealth of all investors , thereby considering a mixed performance criterion

| (2.4) |

where is the weight for the relative component assigned by the -th investor.

Remark 2.1.

Now, for each , given the current time and wealth levels , as well as the trading strategies of the other investors (i.e., for all ), the -th investor looks for a trading strategy that maximizes the mean-variance objective

| (2.7) |

where the superscript “” denotes conditioning on and is the risk aversion parameter for the -th investor. We allow the possibility of two distinct weights for the relative component—one for the mean part and the other for the variance part.

Our goal is to find a Nash equilibrium for this -player game. Because a mean-variance objective is known to induce time inconsistency, how a Nash equilibrium should be defined requires a deeper thought. As elaborated in [24], in a dynamic game where players have time-inconsistent preferences, there are two intertwined levels of game-theoretic reasoning. At the inter-personal level, each player selects an action in response to other players’ chosen strategies. The selected action, importantly, has to be an equilibrium at the intra-personal level (i.e., among the player’s current and future selves), so as to resolve time inconsistency psychologically within the player. With this in mind, let us first introduce Markov trading strategies.

Definition 2.1.

We say is Markov for the -player game (2.7), if for any , there exists a Borel measurable such that for a.e. a.s. We will write and interchangeably.

Given two Markov for (2.7) and , we can define the concatenation of and at time , denoted by , as

| (2.8) |

Note that is Markov for (2.7) by construction.

Definition 2.2.

Condition (2.9) extends the standard definition of an intra-personal equilibrium for one single agent (see e.g., Björk et al. [3, 4]) to a setup with multiple agents. When the other players’ strategies are fixed, (2.9) states that at any time and state , as long as the -th investor’s future selves will employ the strategy , her current self cannot be better off by using any other strategy . That is, is an equilibrium intra-personally for the -th investor. A Nash equilibrium under Definition 2.2, as a result, stipulates that every investor achieves her own intra-personal equilibrium simultaneously, given the other players’ strategies. This corresponds precisely to the notion “soft inter-personal equilibrium” in [24, Definition 2.3].

There is a stronger notion of a Nash equilibrium, called “sharp inter-personal equilibrium” in [24, Definition 2.6], for a game where players have time-inconsistent preferences. It requires every player to attain her optimal intra-personal equilibrium (instead of an arbitrary one, as is required by a soft inter-personal equilibrium) simultaneously. In [24], a sharp inter-personal equilibrium is shown to exist in a Dynkin game, relying on the precise definition and characterization of an optimal intra-personal equilibrium under optimal stopping in [22, 23, 21]. For mean-variance portfolio selection, there is no consensus on how to compare different intra-personal equilibria and define an optimal one accordingly. We therefore stay with the notion “soft inter-personal equilibrium” in Definition 2.2.

To precisely characterize a Nash equilibrium as in Definition 2.2, we consider the constants

| (2.10) |

| (2.11) |

Theorem 2.1.

Remark 2.2.

When (i.e., disregarding relative performance), in (2.12) reduces to the Merton ratio , i.e., becomes the solution to the classical mean-variance problem of one single agent. In a sense, in (2.12) is a generalized Merton ratio with replaced by a linear combination of , where the involved coefficients depend on and .

2.2 Analysis under Partial Information

In practice, while investors observe the evolution of in (2.1), they rarely know its precise dynamics. As a concrete illustration, we assume that there are two possible values and (with ) for the expected return in (2.1) and investors do not know which one is the true value. The volatility coefficient in (2.1), on the other hand, is assumed to be known to all investors.111It is not unrealistic to assume that is known but is uncertain. As explained in [26, footnote 2], high-frequency data readily give good estimators for , while estimating is much more challenging statistically. Our setup is particularly suitable for modeling companies with unreported innovation. Even when it is known that an innovation can improve a company’s expected return from to , investors usually have no idea the progress of the innovation or whether the company has taken the initiative at all. Indeed, more than half of the NYSE-listed firms do not report any information on research and development [27], and European firms file patents for less than 36% of product innovations and less than 25% of process innovations [1].

As the true value of is unknown, the Nash equilibrium formula in Theorem 2.1 is no longer of use. To overcome this, we consider, for any time , the posterior probability

| (2.15) |

Lemma 2.1.

If , then as . If , then as .

By Lemma 2.1 (whose proof is relegated to Section A.1), the true value of can be learned from the long-time limit of . When one is restricted to a finite time horizon , the long-time limit is not necessarily available. It is then important to study the actual evolution of over time. In fact, can be characterized as the unique strong solution to a stochastic differential equation (SDE), as shown in the next result (whose proof is relegated to Section A.2).

Lemma 2.2.

Fix any .

-

(i)

Let be any standard Brownian motion. For any , the SDE

(2.16) has a unique strong solution, which satisfies for all a.s.

- (ii)

The expression (2.19) is important: in (2.1), which involves the unknown , is now expressed alternatively in terms of the known constants , , and the observable process . When investors view the stock as (2.19), their wealth processes can also be expressed in terms of in (2.18) and in (2.17), such that the dynamics of every process involved is fully observable. Specifically, for any and , the wealth process (2.2) of the -th investor can be equivalently expressed as

| (2.20) |

where is the unique strong solution to (2.18). The average wealth in (2.3) consequently takes the form

| (2.21) |

In line with (2.7), for each , given the current time , wealth levels , and posterior probability of the event , as well as the trading strategies of the other investors (i.e., for all ), the -th investor looks for a trading strategy that maximizes the mean-variance objective

| (2.22) |

where the superscript “” denotes conditioning on and .

Due to the additional state process , Markov trading strategies (Definition 2.1) need to be modified accordingly.

Definition 2.3.

We say is Markov for the -player game (2.22), if for any , there exists a Borel measurable such that for a.e. a.s. We will write and interchangeably.

Similarly to (2.8), given two Markov for (2.22) and , we can define the concatenation of and at time , denoted by , as

Note that is Markov for (2.22) by construction. We now define a Nash equilibrium for (2.22) in line with Definition 2.2.

Definition 2.4.

To precisely state a Nash equilibrium in Theorem 2.2 below, we need to introduce a set of two Cauchy problems, one depending on the other. To this end, define by

| (2.24) |

Given , recall defined in (2.10). Now, by setting , we consider, for any , the first Cauchy problem

| (2.25) |

As is not bounded away from 0 on , (2.25) is degenerate, i.e., the uniform ellipticity condition fails. As a result, standard results of parabolic equations (e.g., [16, Chapter 1] and [17, Chapter 6]) cannot be applied to the present case. Our strategy is to approximate (2.25) by a sequence of uniformly elliptic equations, each of which admits a classical solution by the standard results, and show that the limiting solution fulfills (2.25) by an analytic argument. Thanks to probabilistic arguments that involve taking derivatives of stochastic processes (see Remark 2.4), we can further obtain concrete stochastic representations of and its derivative . All this brings about the following result, whose proof is relegated to Section A.3.

Lemma 2.3.

Suppose that is Lipschitz and for any and ,

| (2.26) |

has a unique strong solution with for all a.s. Consider the probability measure on defined by

| (2.27) |

with

| (2.28) |

as well as the process

| (2.29) |

Then, for any ,

- (i)

- (ii)

Remark 2.3.

In Lemma 2.3, the condition “ for all ” ensures that is a bounded process, such that in (2.28) is a strictly positive martingale (by Novikov’s condition). Hence, in (2.27) is a well-defined probability measure equivalent to . Moreover, by Girsanov’s theorem (see e.g., [25, Theorem 3.5.1]), in (2.29) is a Brownian motion (adapted to the same filtration ) under .

Remark 2.4.

Given the solution to (2.25) for every , denoted by , we further consider the second Cauchy problem

| (2.34) |

where is given by

| (2.35) |

Despite the complexity of , it is bounded thanks to the boundedness of in Lemma 2.3. This allows us to establish in the next result the existence of a unique solution to (2.34), following similar arguments in the proof of Lemma 2.3; see Section A.4 for details.

Corollary 2.1.

Suppose that the conditions of Lemma 2.3 hold. For any , let denote the unique solution to (2.25) obtained in Lemma 2.3. Then, the Cauchy problem (2.34) has a unique solution that is continuous up to the boundary . The solution is bounded and admits the stochastic representation

| (2.36) |

where is the unique strong solution to (2.26).

Based on the solutions to the Cauchy problems (2.25) and (2.34), the next result presents a Nash equilibrium as in Definition 2.4. The proof is relegated to Section B.2.

Theorem 2.2.

Recall (2.10), (2.11), and (2.24). A Nash equilibrium for the -player game (2.22), subject to the wealth dynamics (2.20), is given by

| (2.37) |

where is the unique solution to the Cauchy problem (2.25), with therein, obtained in Lemma 2.3 and we use the notation . Moreover, the value function under the Nash equilibrium is

| (2.38) |

where is the unique solution to the Cauchy problem (2.34), with therein, obtained in Corollary 2.1.

Observe that the first term in (2.37) is of the exact form of (2.12). That is, under partial information, investors still wish to trade according to (2.12): they simply replace the unknown by the estimate in (2.24), which is the average of and (the two possible values of ) based on the current judgement in (2.15) at time . The second term in (2.37) comes into play to adjust the first term, based on (i) the current judgement per se and (ii) the precision of judgements over time222We use “precision” as in the usual context of “accuracy versus precision” in taking measurements. Specifically, “precision” means how close the measurements (i.e., posterior probabilities at different times) are to each other. (under an equivalent measure ).

Specifically, in (2.37) controls the level of adjustment through our current judgement . When is close to 1 (resp. 0), we are quite confident of (resp. ) at time . In addition, thanks to (2.24), is close to (resp. ), the likely true value of . As is likely close to , the first term in (2.37) should readily well approximate (2.12). Hence, little adjustment is needed, corresponding to a small . When is far away from 1 and 0 (i.e., near ), as now stands halfway between and , the first term in (2.37) clearly differs from (2.12). Stronger adjustment is then required, corresponding to a larger .

Our judgements, however, can vary wildly over time: by Lemma 2.2, starting with at time , evolves continuously according to SDE (2.18). If our judgements over time are “imprecise,” in the sense that will oscillate wildly on , our present action based on (i.e., the first term in (2.37)) should be modified significantly. If our judgements over time are “precise” (i.e., will stay near on ), our present action based on should be upheld generally. Such nuances are materialized through in the second term of (2.37).

By (2.32), is determined by in (2.33) and on , under a measure equivalent to . As is the stochastic exponential of , it takes values on the entire half line . By contrast, lies within and can take negative values if . Now, given , consider and observe that for any ,

| (2.39) |

where the first equality is due to Remark 2.4 and the second equality stems from the time-homogeneity and uniqueness of strong solutions of in (2.18). Since as , measures the rate of change of at time (under ), capturing how intensely will move away from its current value (under ). Hence, if is “precise” under (i.e., is small for all ), will be small by (2.32). This shrinks the second term of (2.37), leaving the first term to take command. If is “imprecise” under (i.e., is large for some ), can be large. In some cases, this can significantly inflate the second term of (2.37), which alters the first term drastically; see Section 4.1 for concrete illustrations.

Remark 2.5.

If , , for some in , (2.37) simplifies to

with , , and . Note that is now independent of other investors, relying on only the -th investor’s risk aversion coefficient .

Remark 2.6.

If for , then (2.22) becomes

i.e., investors consider a relative criterion for only expected wealth, but not the variance of wealth. In this case, (2.37) reduces to

| (2.40) |

While a relative criterion is still in place (for expected wealth), no longer depends on other investors: and in (2.40) only depend on the -th investor’s parameters , , and .

3 The Case of Alternating Investment Opportunities

In this section, we assume that the expected return of the stock alternates between and (with ). Let be a continuous-time Markov chain taking values in with a generator given by

where are given constants. We then modify the stock dynamics (2.1) to

| (3.1) |

where is defined by and . Furthermore, we assume that the processes and are independent.

The regime-switching feature encoded in (3.1), borrowed from Dai et al. [9], admits a concrete financial interpretation: “” represents the good state (i.e., a bull market) where is expected to grow at the larger rate , while “” represents the bad state (i.e., a bear market) where is expected to grow at the smaller rate .

3.1 Analysis under Full Information

Assume that the dynamics of in (3.1) is fully known; in particular, investors observe the process , i.e., know precisely the present market state. As a result, for any and , the wealth process of the -th investor at time is

| (3.2) |

which is simply (2.2) with therein replaced by . Similarly, the average wealth and the average wealth excluding the -th investor are given by (2.3) and (2.6), respectively, with therein replaced by . For each , at any current time , wealth levels , and market state , given the trading strategies of the other investors (i.e., for all ), the -th investor, in line with (2.7), looks for a trading strategy that maximizes the mean-variance objective

| (3.3) |

where the superscript “” denotes conditioning on and .

Due to the additional state process , Markov trading strategies (Definition 2.1) need to be modified accordingly.

Definition 3.1.

We say is Markov for the -player game (3.3), if for any , there exists a Borel measurable such that for a.e. a.s. We will write and interchangeably.

Similarly to (2.8), given two Markov for the game (3.3) and , we can define the concatenation of and at time , denoted by , as

Note that is Markov for the game (3.3) by construction. We now define a Nash equilibrium for (3.3) in line with Definition 2.2.

Definition 3.2.

Such a Nash equilibrium is presented in the next result, whose proof is relegated to Section C.

3.2 Analysis under Partial Information

In practice, when investors see the evolution of a stock, they rarely know the underlying market state precisely. Accordingly, we assume that investors see the realization of in (3.1) and also know the volatility coefficient (as in Section 2.2), but do not observe the continuous-time Markov chain .

As the present market state is unknown, the Nash equilibrium formula in Theorem 3.1 is no longer of use. As in (2.15), we consider for any time the posterior probability

| (3.9) |

Similarly to in (2.15), can be characterized as the unique strong solution to an SDE, as shown in the next result (whose proof is relegated to Section A.5).

Lemma 3.1.

Fix any .

-

(i)

Let be any standard Brownian motion. For any , the SDE

(3.10) has a unique strong solution, which satisfies for all a.s.

- (ii)

The importance of (3.13) is that it rewrites in (3.1), which involves the unknown , in terms of the known constants , , , and the observable process . When investors view the stock as (3.13), their wealth processes can also be expressed in terms of in (3.12) and in (3.11), such that the dynamics of every process involved is fully observable. Specifically, for any and , the wealth process (3.2) of the -th investor can be equivalently expressed as

| (3.14) |

where is the unique strong solution to (3.12). This is simply (2.20), with and therein replaced by the unique strong solution to (3.12) and , respectively. For each , given the current time , wealth levels , and posterior probability of the event , as well as the trading strategies of the other investors (i.e., for all ), the -th investor looks for a trading strategy that maximizes the mean-variance objective (2.22), with therein being the unique strong solution to (3.12). Our goal is to find a Nash equilibrium for this -player game defined as below.

Definition 3.3.

Theorem 3.2.

Recall (2.10), (2.11), and (2.24). A Nash equilibrium for the -player game (2.22), subject to the wealth dynamics (3.14), is given by (2.37), where is the unique solution to the Cauchy problem (2.25) obtained in Lemma 2.3, with therein taken to be

| (3.16) |

Also, the value function under the Nash equilibrium is given by (2.38), where is the unique solution to the Cauchy problem (2.34) obtained in Corollary 2.1, with therein taken to be (3.16).

The proof of Theorem 3.2 is relegated to Section B.3. Let us stress that the interpretations of the first and second terms of (2.37), discussed in detail below Theorem 2.2, still hold in the present setting, once we replace and SDE (2.18) therein by and SDE (3.12), respectively. Similarly, Remarks 2.5 and 2.6 also hold in the current setting of Theorem 3.2.

4 Discussion: How Partial Information Breeds Systemic Risk

4.1 The Case of Constant Investment Opportunities

When is a fixed unknown constant, Theorem 2.2 stipulates trading according to in (2.37). Both terms in (2.37) can in fact aggravate systemic risk, but in different ways.

As explained below Theorem 2.2, investors wish to trade according to (2.12), but can only approximate it by the first term of (2.37)—or, more precisely, approximate in (2.12) by in (2.37). By Lemmas 2.1 and 2.2, in (2.15) satisfies SDE (2.18), which can oscillate wildly between 0 and 1 before converging to one of them eventually. As a result, can drift far away from the true value of , such that the first term of (2.37) deviates from the ideal trading level (2.12), for quite some time. This can curtail, or even reverse, the growth of wealth.

Take the case for example. As it takes time for to move near , the first term of (2.37) specifies markedly less stock holding than (2.12) for some while. With a positive risk premium , when one takes in (2.2) to be the first term of (2.37), rather than (2.12), the momentum for wealth accumulation (resulting from in (2.2)) weakens. The situation gets worse if we also have . When drifts near , the first term in (2.37) becomes negative, such that in (2.2) actually reduces wealth.

The first plot in Figure 1(c) shows that in (2.15) oscillates wildly before converging to 1 after . Accordingly, the first term of (2.37) (the second plot, Figure 1(b)) deviates from (2.12) (the last plot, Figure 1(b)) for . This deviation, while visible, is generally small. The resulting wealth processes (the last two plots, Figure 1(a)) are therefore quite similar. Indeed, while oscillates forcefully, it generally moves in the right direction: it rises above 0.8 quickly after time 1 and stay within afterwards. This allows to stay near after , such that the first term of (2.37) and (2.12) remain close for most of the time.

It is in fact the second term of (2.37) that drastically turns the trading strategy away from the ideal level (2.12), as shown in the first plot of Figure 1(b). In particular, the most radical behavior takes place during , when previous stock holding is changed to heavy shortselling. This severely impacts the wealth processes of investors, many of which fall below the default level (the first plot, Figure 1(a)). Such a radical change demands further explanations.

Suppose that has gone a long way to reach , very close to 1, such that investors tend to believe . Now, recall the measure in (2.27). By Lemma 2.1 and the equivalence of and , we have (resp. 0) if (resp. ), under both and . In view of this, if will be stable on under , it will likely converge to 1 eventually, which reinforces the belief . As is already close to , the probable true value of , the first term of (2.37) is likely close to (2.12) and little adjustment is needed. Indeed, as explained below (2.39), when is stable (or “precise”) on under , is close to 0, which diminishes the second term of (2.37). If, on the other hand, will oscillate wildly on under , it can potentially drift away from 1, which weakens the belief . The stronger oscillation of is expected in the near future, the more concerned investors become about whether is a misbelief, and ultimately, the more severe change from holding to shortselling the stock (in view of the risk premiums and ), in order to compensate for previous trading under the misbelief. Indeed, as explained below (2.39), when is volatile (or “imprecise”) on under and its current value is close to 1, can take huge values. This can significantly inflate the second term of (2.37), which alters the first term drastically.

In summary, for the case of a constant , while both terms of (2.37) can contribute to systemic risk, the second term plays a dominant role, driving the trading strategy far away from the ideal level (2.12) for quite some time. This results from the strong oscillation (or “impreciseness”) of the posterior probability , from which investors cannot quickly read the true value of . As mentioned above, one specific realization of wealth processes (the first plot, Figure 1(a)) shows that wealth accumulation is significantly curtailed, compared with the full-information scenario (the last plot, Figure 1(a)). By simulating 100 realizations of the wealth processes , , we obtain the empirical loss distributions (the second plot, Figure 1(c)). It shows no default under full information, while partial information triggers defaults constantly and they tend to happen together (e.g., the probability that all 10 investors default is about 35%).

4.2 The Case of Alternating Investment Opportunities

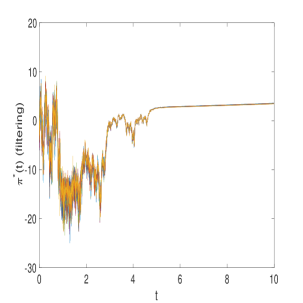

When alternates between and behind the scenes, Theorem 3.2 stipulates trading according to in (2.37), with “” therein replaced by (3.16). By the same reasoning in Section 4.1, both terms in (2.37) can aggravate systemic risk. As to which term takes command, a different story unfolds.

By Lemma 3.1, in (3.9) satisfies SDE (3.12). Let us compare SDEs (3.12) and (2.18) (the one under a fixed ) closely. As (2.18) involves only the Brownian motion term, it can oscillate wildly between 0 and 1, despite the ultimate convergence to either 0 or 1 (by Lemma 2.1). By contrast, the drift term of (3.12) makes the process mean-reverting. As (3.12) always tends to return to the mean level , its oscillation between 0 and 1 is dampened. In other words, with (2.18), investors’ judgment of changes widely over time, but a firm clear opinion will take shape eventually; with (3.12), investors’ judgment is stable over time but remains vague throughout.

This lasting vagueness keeps the first term of (2.37) away from the ideal trading level (3.5) perpetually. Indeed, as in (3.12) never stays near 0 or 1 for long, is constantly far away from and , whence from . In the first plot of Figure 2(c), we see oscillate around , taking values mostly within . Accordingly, never gets close to , leaving the first term of (2.37) distinct from (3.5) perpetually (the last two plots, Figure 2(b)). The resulting wealth processes (the last two plots, Figure 2(a)) then differ substantially: trading according to the first term of (2.37) severely reduces wealth, causing many defaults.

Interestingly, the second term of (2.37) does not play a significant role, as opposed to the case of a constant in Section 4.1. Under the measure in (2.27), in (3.12) becomes (2.31), with therein given by (3.16). By the definitions of and (in (3.16) and (2.24)), the mean-reverting effect remains dominant whenever moves near 0 or 1 under . As is made more stable (or, more “precise”) on under by this mean-reverting effect, the arguments below (2.39) imply that tend to be closer to 0, which diminishes the size of the second term of (2.37). Indeed, as shown in the first two plots of Figure 2(b), adding the second term of (2.37) does not change the trading strategies much (except reducing stock holding very slightly). The resulting wealth processes (the first two plots, Figure 2(a)) are therefore similar, with wealth reduced only slightly when the second term of (2.37) is added.

In summary, for the case of an alternating , while both terms of (2.37) can contribute to systemic risk, the first term plays a dominant role, driving the trading strategy far away from the ideal level (3.5) perpetually. This results from the mean-reverting feature of the posterior probability , from which investors never learn the true state of . As mentioned above, one specific realization of wealth processes (the first plot, Figure 2(a)) shows that wealth accumulation is significantly curtailed, compared with the full-information scenario (the last plot, Figure 2(a)). By simulating 100 realizations of the wealth processes , , we obtain the empirical loss distributions (the second plot, Figure 2(c)). In particular, it shows that when we change from the case of full information to that of partial information, the no-default probability drops by more than 10% while the probability that all investors default climbs by more than 10%.

Remark 4.1.

Appendix A Proofs of Auxiliary Results

A.1 Proof of Lemma 2.1

A.2 Proof of Lemma 2.2

(i) By [25, Theorem 5.5.15], there exists a weak solution to (2.16) up to a possibly finite explosion time beyond the interval , which is defined by

| (A.3) |

With no drift term in (2.16), the corresponding scale function (see e.g., [25, eqn. (5.5.42)]) simplifies to for some . Hence, the function in [25, eqn. (5.5.65)] takes the form

For any , observe that

which implies . For any , note that

which implies . Hence, by Feller’s test for explosion (see e.g., [25, Proposition 5.5.32]), . That is, never leaves the interval a.s. and is thus a genuine weak solution to (2.16). Now, as the map is locally Lipschitz on , the uniqueness of strong solutions to (2.16) holds (see [25, Theorem 5.2.5]), which in turn implies that pathwise uniqueness holds for weak solutions to (2.16) (see [25, Remark 5.3.3]). Thanks to the existence of a weak solution and pathwise uniquessness, we conclude from [25, Corollary 5.3.23] that a unique strong solution to (2.16) exists. As argued above, this solution must lie within a.s.

(ii) Let us write in (2.1) as , with for . As and , we deduce from (2.17) that

which is a standard Brownian motion w.r.t. thanks to [30, Lemma 11.3]. By Wonham [35, eqn. (12)], satisfies

| (A.4) |

To simplify this, we apply Itô’s formula to (2.17) and get

| (A.5) |

As , we have

| (A.6) |

where the second equality follows from (A.5). Plugging this into (A.4) yields . By taking in part (i), we conclude that is the unique strong solution to (2.18). Finally, since (A.5) can be rearranged as , we obtain (2.19).

A.3 Proof of Lemma 2.3

(i) For any and , recall the Hölder norm and its weighted version defined in [29, pp. 46-47] for all ; in particular, we say if . Now, for any , define and denote by the parabolic boundary of . Consider the equation

| (A.7) |

As is bounded away from 0 on , (A.7) is uniformly elliptic. Moreover, by (2.24), the maps , , and are Lipschitz on . Hence, we conclude from [29, Theorem 5.9] that there exists a classical solution to (A.7).

Given any compact subset of , we can take large enough such that . Note that by construction, , for any , is a solution to the equation

| (A.8) |

As argued above, this equation is uniformly elliptic and its coefficients are Lipschitz on . Hence, by [29, Theorem 4.9], there exists , depending on only and the coefficients of (A.8) (particularly, independent of ), such that

| (A.9) |

Now, by the definition of the weighted norm and the fact that is compactly embedded in , there exists (independent of ) such that

| (A.10) |

Recall from Remark 2.3 that the measure in (2.27) is equivalent to and in (2.29) is a Brownian motion (adapted to the same filtration ) under . It follows that the unique strong solution to (2.26) (under ) becomes a strong solution to (2.31) (under ), which satisfies for -a.s. (as is equivalent to ). Because the coefficients of (2.31), i.e., and , are locally Lipschitz, this strong solution to (2.31) is in fact the unique one; see e.g., [25, Theorem 5.2.5]. For each , since is a classical solution to (A.7), by applying Itô’s formula to under , we obtain the probabilistic representation

| (A.11) | ||||

| (A.12) |

where is the unique strong solution to (2.31) and the inequality follows from the definition of in (2.24) and for -a.s.

Now, combining (A.9), (A.10), and (A.12), we obtain

By the Arzela-Ascoli theorem, this implies that and its derivatives , , and converge uniformly (up to a subsequence) on to some and its derivatives , , and , respectively. Hence, fulfills (A.8) in . As the compact subset of is arbitrary, is in fact of and satisfies (A.8) in . Finally, as , by and a.s. (due to for -a.s.), we deduce from (A.11) and the dominated convergence theorem that

| (A.13) |

which implies

Hence, given , for any such that , we have . As a result, by setting for all , we see that is continuous up to the boundary and the stochastic representation of in (A.13) can be extended to include . As is bounded, the Feynman-Kac representation theorem (see e.g., [25, Theorem 5.7.6]) asserts that is the unique solution to (2.25) among functions in that are continuous up to .

(ii) As and are Lipschitz on , we denote by their Lipschitz constant. By definition, and are bounded by on . For any , thanks to the boundedness of and , the SDE with random coefficients (2.33) satisfies [32, conditions (1.14)-(1.16)]. Hence, by [32, Theorem 1.3.15], (2.33) admits a unique strong solution and there exists , depending only on and , such that

| (A.14) |

Now, we write for to stress the initial condition in (2.31). By [17, Theorem 5.3], for any , in as . We then deduce from (2.30) that

| (A.15) |

where the second equality stems from the definition of in (2.24) and Fubini’s theorem. By [31, Lemma 3.1], there exists , depending only on and , such that for all and . Thus, for all and . This allows the use of the dominated convergence theorem to exchange the limit and the integral in (A.15). By doing so and recalling in (and thus in ), we conclude from (A.15) that

| (A.16) |

where the last line follows from Fubini’s theorem. As for -a.s., is a bounded process by the definition of in (2.24). Also, in view of (2.33), is a nonnegative process. Hence, we conclude from (A.3) and (A.14) that is bounded on .

A.4 Proof of Corollary 2.1

The desired results follow from the same arguments in the proof of Lemma 2.3 (i) (see Section A.3), with and replaced by and , and the unique strong solution to (2.31) (under ) replaced by that to (2.26) (under ). In particular, as is bounded for all (by Lemma 2.3 (ii)), we see immediately that is bounded for all . Hence, when and in (A.13) is replaced by and , respecticely, the arguments below (A.13) still hold.

A.5 Proof of Lemma 3.1

(i) By [25, Theorem 5.5.15], there exists a weak solution to (3.10) up to a possibly finite explosion time beyond the interval , defined as in (A.3). In view of the dynamics in (3.10), for any , the corresponding scale function (see e.g., [25, eqn. (5.5.42)]) takes the form

| (A.17) |

where denotes a generic constant that depends only on , , and and may change from line to line. For , we deduce from the above and for all that

| (A.18) |

Hence, we get . For , a similar calculation shows that the above inequality “” turns into “”, which then implies . We therefore conclude from [25, Problem 5.5.27] and Feller’s test for explosion (see e.g., [25, Theorem 5.5.29]) that . That is, never leaves the interval a.s. and is thus a genuine weak solution to (2.16). Now, as the maps and are locally Lipschitz, we can argue as in the last five lines of the proof of Lemma 2.2 (i) (see Section A.3) that a unique strong solution to (2.16) exists and it lies in a.s.

(ii) Let us write in (3.1) as , with for . As and , (3.11) becomes

which is a standard Brownian motion w.r.t. thanks to [30, Lemma 11.3].333While [30, Lemma 11.3] is stated for diffusion processes, the arguments in its proof still hold when applied to , a continuous-time Markov chain. By Wonham [35, eqn. (21)], satisfies

| (A.19) |

To simplify this, we apply Itô’s formula to (3.11) and get (A.5), with and therein replaced by and , respectively. It follows that the dynamics of in (A.6) still holds, with and in place of and . Plugging this into (A.19) yields . By taking in part (i), we conclude that is the unique strong solution to (3.12). Finally, since rearranging (A.5), with and in place of and , gives , we obtain (3.13).

Appendix B Proofs of Theorems 2.1, 2.2, and 3.2

As we will see in this section, the proofs of Theorems 2.1, 2.2, and 3.2 share a similar structure. This is because the state processes involved, i.e., and , always change continuously as solutions to SDEs. By contrast, the proof of Theorem 3.1 (postponed to Section C) requires a different derivation to accommodate the state process , which jumps between two distinct states.

Section B.1 below derives the extended Hamilton-Jacobi-Bellman (HJB) equation for the problem (2.22), which is a coupled system of partial differential equations (PDEs)—two PDEs for each investor. By solving the extended HJB equation semi-explicitly (in terms of the solutions to the Cauchy problems (2.25) and (2.34)), we will construct the Nash equilibria stated in Theorems 2.2 and 3.2; see Sections B.2 and B.3. Theorem 2.1 will follow as a special case; see Section B.4.

B.1 Preparation: Deriving the Extended HJB Equations

Let be a standard Brownian motion. Consider the problem (2.22), subject to the wealth dynamics

| (B.1) |

where is the unique strong solution to

| (B.2) |

For the case , (B.1) corresponds to the wealth dynamics (2.2) in Section 2.1; moreover, as there is no longer -dependence in the wealth dynamics, the problem (2.22) reduces to (2.7). For the case , by taking , (B.1) corresponds to the wealth dynamics (2.20) in Section 2.2; by taking as in (3.16), (B.1) represents the wealth dynamics (3.14) in Section 3.2.

For each , by recalling the formulations in Remark 2.1, we rewrite (2.22) as

where

Following the derivation in Björk et al. [3, Section 10], the extended HJB equation for a Nash equilibrium and the corresponding equilibrium value functions takes the form: for any ,

| (B.3) |

with the terminal condition , where the function satisfies

| (B.4) | |||||

with the terminal condition .

B.2 Proof of Theorem 2.2

As the wealth dynamics (2.20) corresponds to (B.1)-(B.2) with , we take in the derivation in Section B.1. By solving for the maximizer of the supremum in (B.6), we find that a Nash equilibrium needs to satisfy

| (B.8) |

In addition, for (B.6)-(B.7) to hold for all , it is necessary that the coefficients of and the coefficients of sum up to 0, respectively. This leads to the ordinary differential equations (ODEs)

Solving the ODEs gives

| (B.9) |

and

| (B.10) |

By inserting (B.9) and (B.10) back into (B.8), we get

| (B.11) |

where the second equality follows from the definition of in (2.10). Recall that . It follows that

| (B.12) |

where the second equality follows from (B.11). Summing this up over all then gives

| (B.13) |

with and defined as in (2.11) and . Plugging this back into (B.12) leads to the formula of in (2.37).

In (B.7), with the coefficients of and those of both summing up to 0, the remaining terms should also sum up to 0. By plugging (B.10) into the remaining terms and using the relation (B.12), we find that needs to solve the Cauchy problem (2.25), with therein. Hence, we take to be the unique solution in to such a Cauchy problem, obtained in Lemma 2.3. Similarly, in (B.6), with the coefficients of and those of both summing up to 0, the remaining terms should also sum up to 0. By plugging (B.9) and (B.10) into the remaining terms and using the relation (B.12) and (B.13), we find that needs to solve the Cauchy problem (2.34), with therein. Hence, we take to be the unique solution in to such a Cauchy problem, obtained in Corollary 2.1.

All the above shows that for all , the extended HJB equation (B.3)-(B.4) has a solution of the form (B.5), with and as in (B.9), and as in (B.10), the unique solution to (2.25), and the unique solution to (2.34). Moreover, the maximizer of the supremum in (B.3) is given by (2.37). Using the explicit forms of , , and , we conclude directly from [4, Theorem 5.2] that satisfies (3.15). As this holds for all , is a Nash equilibrium for the -player game (2.22), subject to the wealth dynamics (2.20).

B.3 Proof of Theorem 3.2

B.4 Proof of Theorem 2.1

When deriving the extended HJB equation as in Section B.1, as there is no dependence in the present case, we obtain a simplified version of (B.3)-(B.4), where is replaced by and every term with a derivative in disappears. By plugging the ansatz (B.5) into this simplified extended HJB equation, we get and as in (B.9), and as in (B.10), and

with given as in (2.14). This in turn implies that the maximizer of the supremum in the simplified (B.3) takes the form (2.12). Using the explicit forms of , , and , we conclude directly from [4, Theorem 5.2] that satisfies (2.9). As this holds for all , is a Nash equilibrium for the -player game (2.7), subject to the wealth dynamics (2.2).

Appendix C Proof of Theorem 3.1

In the following, we derive the extended HJB equation following Björk et al. [3, Section 10], but in a regime-switching model similar to [36]. For the problem (3.3), subject to the wealth dynamics (3.2), the extended HJB equation for a Nash equilibrium and the corresponding equilibrium value functions , , takes the form: for any ,

| (C.1) | |||||

and

| (C.2) | |||||

with the terminal condition , where the functions and satisfy

| (C.3) | |||

| (C.4) |

with the terminal condition . By plugging the ansatz

| (C.5) |

into (C.1)-(C.4), we find that the coefficients of , the coefficients of , and the remaining terms should all sum up to 0. By a detailed calculation, this directly yields and as in (B.9), and as in (B.10), and as in (3.7)-(3.8), as well as

| (C.6) | |||||

| (C.7) | |||||

That is, for all , the extended HJB equation (C.1)-(C.4) has a solution , , of the form (C.5), with , , , , , and specified above. This in turn implies that the maximizer of the supremum in (C.1) (resp. (C.2)) is given by (3.5) with (resp. ). Using the explicit forms of , , and , we can follow the arguments in [4, Theorem 5.2] to show that satisfies (3.4). As this holds for all , is a Nash equilibrium for the -player game (3.3), subject to the wealth dynamics (3.2).

References

- [1] A. Arundel and I. Kabla, What percentage of innovations are patented? empirical estimates for european firms, Research Policy, 27 (1998), pp. 127–141.

- [2] F. Biagini, A. Mazzon, and T. Meyer-Brandis, Financial asset bubbles in banking networks, SIAM Journal on Financial Mathematics, 10 (2019), pp. 430–465.

- [3] T. Björk, K. Khapko, and A. Murgoci, On time-inconsistent stochastic control in continuous time: theory and examples, arXiv:1612.03650, (2016).

- [4] , On time-inconsistent stochastic control in continuous time, Finance and Stochastics, 21 (2017), pp. 331–360.

- [5] A. Capponi, X. Sun, and D. D. Yao, A dynamic network model of interbank lending, Mathematics of Operations Research, 45 (2020), pp. 1–26.

- [6] R. Carmona, J. P. Fouque, M. Mousafa, and L.-H. Sun, Systemic risk and stochastic games with delay, Journal of Optimization Theory and Applications, 179 (2018), pp. 366–399.

- [7] R. Carmona, J. P. Fouque, and L.-H. Sun, Mean field games and systemic risk, Communications in Mathematical Sciences, 13 (2015), pp. 911–933.

- [8] X. Chen, Y.-J. Huang, Q. Song, and C. Zhu, The stochastic solution to a Cauchy problem for degenerate parabolic equations, J. Math. Anal. Appl., 451 (2017), pp. 448–472.

- [9] M. Dai, Q. Zhang, and Q. J. Zhu, Trend following trading under a regime switching model, SIAM Journal on Financial Mathematics, 1 (2010), pp. 780–810.

- [10] G.-E. Espinosa and N. Touzi, Optimal investment under relative performance concerns, Mathematical Finance, 25 (2015), pp. 221–257.

- [11] F. Fang, Y. Sun, and K. Spiliopoulous, On the effect of heterogeneity on flocking behavior and systemic risk, Statistics & Risk Modeling, 34 (2017), pp. 144–155.

- [12] Z. Feinstein and A. Sojmark, A dynamic default contagion model: from Eisenberg-Noe to the mean field, arXiv:1912.08695, (2019).

- [13] J. P. Fouque and T. Ichiba, Stability in a model of inter-bank lending, SIAM Journal on Financial Mathematics, 4 (2013), pp. 784–803.

- [14] J.-P. Fouque and J. Langsam, Handbook on Systemic Risk, Cambridge University Press, 2013.

- [15] J.-P. Fouque and L.-H. Sun, Systemic risk illustrated, Handbook on Systemic Risk, Eds J.-P. Fouque and J. Langsam, (2013), pp. 444–452.

- [16] A. Friedman, Partial differential equations of parabolic type, Prentice-Hall, Inc., Englewood Cliffs, NJ, 1964.

- [17] , Stochastic differential equations and applications. Vol. 1, vol. Vol. 28 of Probability and Mathematical Statistics, Academic Press [Harcourt Brace Jovanovich, Publishers], New York-London, 1975.

- [18] J. Garnier, G. Papanicolaou, and T.-W. Yang, Diversification in financial networks may increase systemic risk, Handbook on Systemic Risk, Eds J.-P. Fouque and J. Langsam, (2013), pp. 432–443.

- [19] , Large deviations for a mean field model of systemic risk, SIAM Journal on Financial Mathematics, 4 (2013), pp. 151–184.

- [20] , A risk analysis for a system stabilized by a central agent, Risk and Decision Analysis, 6 (2017), pp. 97–120.

- [21] Y.-J. Huang and Z. Wang, Optimal equilibria for multidimensional time-inconsistent stopping problems, SIAM J. Control Optim., 59 (2021), pp. 1705–1729.

- [22] Y.-J. Huang and Z. Zhou, The optimal equilibrium for time-inconsistent stopping problems–the discrete-time case, SIAM Journal on Control and Optimization, 57 (2019), pp. 590–609.

- [23] , Optimal equilibria for time-inconsistent stopping problems in continuous time, Mathematical Finance, 30 (2020), pp. 1103–1134.

- [24] , A time-inconsistent Dynkin game: from intra-personal to inter-personal equilibria, Finance Stoch., 26 (2022), pp. 301–334.

- [25] I. Karatzas and S. E. Shreve, Brownian Motion and Stochastic Calculus Second Edition, Springer-Verlag New York, Springer Science+Business Media New York, 1991.

- [26] C. Kardaras and S. Robertson, Robust maximization of asymptotic growth, Ann. Appl. Probab., 22 (2012), pp. 1576–1610.

- [27] P.-S. Koh and D. Reeb, Missing R&D, Journal of Accounting and Economics, 60 (2015), pp. 73–94.

- [28] D. Lacker and T. Zariphopoulou, Mean field and n-agent games for optimal investment under relative performance criteria, Mathematical Finance, 29 (2019), pp. 1003–1038.

- [29] G. M. Lieberman, Second order parabolic differential equations, World Scientific Publishing Co., Inc., River Edge, NJ, 1996.

- [30] R. S. Liptser and A. N. Shiryaev, Statistics of random processes II: Applications, volume 6, Springer-Verlag New York, Springer Science+Business Media New York, 2013.

- [31] H. Pham, Optimal stopping of controlled jump diffusion processes: a viscosity solution approach, J. Math. Systems Estim. Control, 8 (1998), pp. 1–27.

- [32] , Continuous-time stochastic control and optimization with financial applications, vol. 61 of Stochastic Modelling and Applied Probability, Springer-Verlag, Berlin, 2009.

- [33] L.-H. Sun, Systemic risk and interbank lending, Journal of Optimization Theory and Applications, 179 (2018), pp. 400–424.

- [34] , Mean field games with heterogeneous groups: application to banking systems, Journal of Optimization Theory and Applications, 192 (2022), pp. 130–167.

- [35] W. M. Wonham, Some applications of stochastic differential equations to optimal nonlinear filtering, SIAM Journal on Control and Optimization, 2 (1965), pp. 347–369.

- [36] X. Y. Zhou and G. Yin, Markowitz’s mean-variance portfolio selection with regime switching: a continuous-time model, SIAM Journal on Control and Optimization, 42 (2003), pp. 1466–1482.