Almost Dominance: Inference and Application††thanks: The authors are grateful to all the seminar and conference participants for their insightful comments.

Abstract

This paper proposes a general framework for inference on three types of almost dominances: Almost Lorenz dominance, almost inverse stochastic dominance, and almost stochastic dominance. We first generalize almost Lorenz dominance to almost upward and downward Lorenz dominances. We then provide a bootstrap inference procedure for the Lorenz dominance coefficients, which measure the degrees of almost Lorenz dominances. Furthermore, we propose almost upward and downward inverse stochastic dominances and provide inference on the inverse stochastic dominance coefficients. We also show that our results can easily be extended to almost stochastic dominance. Simulation studies demonstrate the finite sample properties of the proposed estimators and the bootstrap confidence intervals. We apply our methods to the inequality growth in the United Kingdom and find evidence for almost upward inverse stochastic dominance.

Keywords: Almost Lorenz dominance, almost inverse stochastic dominance, almost stochastic dominance, estimation and inference, bootstrap confidence intervals

1 Introduction

Suppose that there are two arbitrary cumulative distribution functions (CDFs) and of two income (or wealth, etc.) distributions in two populations. As introduced in atkinson1970measurement, a Lorenz curve is a function that graphs the cumulative proportion of total income received by the bottom population. The distribution (weakly) Lorenz dominates if the Lorenz curve associated with is everywhere above the Lorenz curve associated with . Such Lorenz dominance implies that the wealth is distributed more equally in population compared to . Statistical tests of Lorenz dominance can be found in, for example, mcfadden1989testing, bishop1991international, bishop1991lorenz, dardanoni1999inference, davidson2000statistical, barrett2003consistent, BDB14, and Beare2017improved.

zheng2018almost introduces the notion of almost Lorenz dominance: When two Lorenz curves cross, almost Lorenz dominates if is above almost everywhere. The degree of almost Lorenz dominance can be measured by a coefficient, Lorenz dominance coefficient (LDC). The LDC was first proposed in zheng2018almost,111The original definition of LDC in zheng2018almost is slightly different from the proposed one in this paper. which is similar to the violation ratio in huang2021estimating. zheng2018almost shows that almost Lorenz dominance is highly related to Gini-type measures. Based on the seminal work of aaberge2009ranking, we generalize almost Lorenz dominance to almost upward Lorenz dominance and almost downward Lorenz dominance. We relate the generalized LDCs to a class of inequality measures. It is straightforward to show that the smaller LDCs are, the more inequality measures demonstrate higher distribution equality in the dominant population. Thus, LDCs are of interest to us when we compare distributions in terms of distribution inequality. We then provide estimators for LDCs and establish the asymptotic properties of the estimators.222The proposed estimators are also different from that proposed by zheng2018almost since the definitions of the proposed LDCs are different. Based on the asymptotic distributions, we construct bootstrap confidence intervals (CIs) for LDCs. LDCs are nonlinear transformations of the difference functions of two Lorenz curves. We show that this map is Hadamard directionally differentiable, and then we apply the bootstrap method of fang2014inference to approximate the asymptotic distributions of the estimators and obtain the confidence intervals.333For more discussions on Hadamard directional differentiability and its applications, see dumbgen1993nondifferentiable, andrews2000inconsistency, bickel2012resampling, hirano2012impossibility, beare2015nonparametric, Beare2016global, hansen2017regression, Seo2016tests, Beare2015improved, chen2019improved, Beare2017improved, and sun2018ivvalidity.

The second degree inverse stochastic dominance (atkinson1970measurement), also known as the generalized Lorenz dominance, is widely used for ranking distribution functions according to social welfare. However, as pointed out by aaberge2021ranking, when the distribution functions intersect, the second degree inverse dominance criterion may have limitations to attain an unambiguous ranking (davies1995making; atkinson2008more). aaberge2021ranking propose an approach for comparing intersecting distribution functions based on high-degree upward and downward inverse stochastic dominance criteria. They provide equivalence results between inverse stochastic dominance and the ranks of social welfare functions. Based on the framework of aaberge2021ranking, we introduce the notions of almost upward inverse stochastic dominance and almost downward inverse stochastic dominance. We then show that these types of almost dominances are also related to the ranks of social welfare functions. Similar to LDCs, the degree of almost inverse stochastic dominance can be measured by the inverse stochastic dominance coefficients (ISDCs). The smaller ISDCs are, the more social planner preference functions show higher social welfare for the dominant distribution. We provide inference and construct bootstrap confidence intervals for ISDCs.

Almost Lorenz dominance can be viewed as a special but nontrivial case of almost stochastic dominance which was first introduced by leshno2002preferred. Almost stochastic dominance has been extensively studied by guo2013note, tzeng2013revisiting, denuit2014almost, guo2014moment, tsetlin2015generalized, guo2016almost, and huang2021estimating.444See a comprehensive review on stochastic dominance in whang2019econometric. We show that our method on almost Lorenz dominance can easily be generalized to almost stochastic dominance and provide bootstrap confidence intervals for the stochastic dominance coefficients (SDCs).

We study the inequality growth in the United Kingdom as an empirical example in the paper. We find that the estimated upward inverse stochastic dominance coefficients are small and the bootstrap confidence intervals are narrow, which implies that there may exist almost inverse stochastic dominance between the years considered in this example.

For simplicity of exposition, we focus on the almost Lorenz dominances in the main text. The results for other types of almost dominances are provided in the supplementary appendix. The organization of the paper is as follows. Section 2 introduces the notions of Lorenz dominance coefficients, provides the properties of these coefficients, and relates them to measures of inequality. Section 2.3 proposes estimators for LDCs and establishes the asymptotic distributions of the estimators. We then construct the confidence intervals for LDCs based on these asymptotic distributions. Section 3 provides simulation evidence for the finite sample properties of the proposed method. In Section 4, we apply our methods to the empirical application. In the supplementary appendix, Sections A and B extend the results to almost inverse stochastic dominance and almost stochastic dominance. Section C provides additional simulation results. Section D contains the proofs of the results in the paper.

Notation (Beare2017improved): Throughout the paper, all the random elements are defined on a probability space . For an arbitrary set , let be the set of bounded real-valued functions on equipped with the supremum norm such that for every . For a subset of a metric space, let be the set of continuous real-valued functions on . Let denote the weak convergence defined in van1996weak. We follow the convention in folland2013real and define

| (1.1) |

2 Almost Lorenz Dominance

We suppose that the CDFs and satisfy the following regularity conditions which guarantee the weak convergence of the estimated quantile functions (K17; Beare2017improved).

Assumption 2.1

For , and is continuously differentiable on the interior of its support with for all . In addition, has finite th absolute moment for some .

With Assumption 2.1, we introduce the Lorenz curves. Let and denote the quantile functions corresponding to and , respectively, that is,

| (2.1) |

When has finite first moment as implied by Assumption 2.1, the quantile function is integrable with . Under Assumption 2.1 with , the Lorenz curve corresponding to can then be defined as

| (2.2) |

We say (weakly) Lorenz dominates if for all . We now follow zheng2018almost and introduce the notion of almost Lorenz dominance. For all arbitrary CDFs and such that the corresponding Lorenz curves exist, define

Definition 2.1

For every , the CDF -almost Lorenz dominates the CDF ( -ALD ), if

| (2.3) |

Remark 2.1

Lemma 2.1

For every , -ALD if and only if there is such that

| (2.4) |

We define the distance function of the two Lorenz curves by

| (2.5) |

Based on the equality in (2.4), we follow zheng2018almost and define the - Lorenz Dominance Coefficient as follows.555In Section 2.3 of zheng2018almost, the Lorenz dominance coefficient is defined in a slightly different way.

Definition 2.2

Suppose that there are two Lorenz curves and corresponding to the CDFs and , respectively. The - Lorenz dominance coefficient (- LDC), denoted by , is defined as

| (2.6) |

The following lemma summarizes the properties of the LDC .

Lemma 2.2

According to Lemma 2.2, -ALD for all if . On the other hand, implies that -ALD for all . Thus, presents the almost Lorenz dominance relationship between and , and provides all for which -ALD holds.

When and cross, given some , one interesting hypothesis is

Lemma 2.2 shows that it is equivalent to test the following hypothesis on :

The LDC provided in Definition 2.2 is closely related to Gini-type measures that are weighted averages of the area between the diagonal line and Lorenz curves. Following shorrocks2002approximating, for every possible weighting function , a Gini-type measure for distribution can be defined as

| (2.8) |

where denotes the Lorenz curve associated with the distribution .

We follow zheng2018almost and denote the set of all Gini-type measures for all possible weighting functions . Define

for every possible weighting function . It then follows that

For every , we define

| (2.9) |

As discussed in zheng2018almost, the condition in (2.9) basically requires that the largest weight in weighting the distance can not be larger than times the smallest weight.

Proposition 1 of zheng2018almost shows that for every , -ALD if and only if for all . According to Lemma 2.2, for every with , -ALD and thus for all . Therefore, we have the following proposition.

Proposition 2.1

If , it follows that for all .666Note that by definition. If , it follows that .

Proposition 2.1 shows the importance of LDC concerning Gini-type measures. The smaller the LDC is, the more Gini-type measures show higher equality in the distribution compared to . With the knowledge of , we can infer the relationship between and based on a class of Gini-type measures.

Following aaberge2009ranking, we introduce the family of rank-dependent measures of inequality:

| (2.10) |

where is the Lorenz curve of the distribution with mean and the weighting function is the derivative of a continuous, differentiable, and concave function such that , , and . As demonstrated by yaari1988controversial and aaberge2001axiomatic, can be interpreted as a preference function of a social decision maker, which assigns weights to the incomes of individuals in accordance with their rank in the income distribution, and measures the extent of inequality in an income distribution with Lorenz curve . We formally define the set of preference functions by

2.1 Almost Upward Lorenz Dominance and Inequality Measure

To unify notation, we let for . For , define function

aaberge2009ranking introduces the th-degree upward Lorenz dominance for as illustrated in the following.

Definition 2.3

A distribution th-degree upward Lorenz dominates a distribution if for all .

We generalize upward Lorenz dominance in aaberge2009ranking to almost upward Lorenz dominance.

Definition 2.4

For every , the CDF -almost th-degree upward Lorenz dominates the CDF ( -AULD ), if

| (2.11) |

Remark 2.2

In Definition 2.4, if , then th-degree upward Lorenz dominates .

For every , we define two sets of preference functions

and

The following proposition relates almost upward Lorenz dominance to the inequality measures in (2.10).

Proposition 2.2

For every , if -AULD , then for every . If -AULD and for all , then for every .

For , following Lemma 2.1, it is straightforward to show that -AULD if and only if there is such that

Similar to (2.6), we define the th-degree upward Lorenz dominance coefficient , where the superscript “” represents “upward”.

Definition 2.5

For , the - th-degree upward Lorenz dominance coefficient (- ULDC) is defined as

| (2.12) |

For , define the difference function

The following lemma summarizes the properties of the ULDC .

Lemma 2.3

According to Lemma 2.3, -AULD for all if . On the other hand, implies that -AULD for all . Thus, presents the degree of almost upward Lorenz dominance relationship between and , and provides all such that the -AULD holds.

Proposition 2.3

If , it then follows that for all . If, in addition, for all , then for all .

Similar to Proposition 2.1, Proposition 2.3 shows the importance of ULDC concerning inequality measures . The smaller the ULDC is, the more inequality measures show higher equality in the distribution compared to . With the knowledge of , we can infer the relationship between and based on a class of inequality measures.

2.2 Almost Downward Lorenz Dominance and Inequality Measure

Define function

and for ,

aaberge2009ranking introduces the th-degree downward Lorenz dominance for as illustrated in the following.

Definition 2.6

A distribution th-degree downward Lorenz dominates a distribution if for all .

We generalize downward Lorenz dominance in aaberge2009ranking to almost downward Lorenz dominance.

Definition 2.7

For every , the CDF -almost th-degree downward Lorenz dominates the CDF ( -ADLD ), if

| (2.14) |

Remark 2.3

In Definition 2.7, if , then th-degree downward Lorenz dominates .

For every , we define

and

The following proposition relates almost downward Lorenz dominance to the inequality measures in (2.10).

Proposition 2.4

For every , if -ADLD , then for every . If -ADLD and for all , then for every .

For , following Lemma 2.1, it is straightforward to show that -ADLD if and only if there is such that

Similar to (2.6), we now define the th-degree downward Lorenz dominance coefficient , where the superscript “” represents “downward”.

Definition 2.8

For , the - th-degree downward Lorenz dominance coefficient (- DLDC) is defined as

| (2.15) |

For , we define the difference function

The following lemma summarizes the properties of the DLDC .

Lemma 2.4

According to Lemma 2.4, -ADLD for all if . On the other hand, implies that -ADLD for all . Thus, presents the degree of almost downward Lorenz dominance relationship between and , and provides all such that the -ADLD holds.

Proposition 2.5

If , it then follows that for all . If, in addition, for all , then for all .

Similar to Proposition 2.1, Proposition 2.5 shows the importance of DLDC concerning inequality measures . The smaller the DLDC is, the more inequality measures show higher equality in the distribution compared to . With the knowledge of , we can infer the relationship between and based on a class of inequality measures.

2.3 Estimation and Inference

As discussed in the previous sections, LDCs play an important role in comparing the equality of income (or wealth) distributions in two populations. In this section, we consider the estimation and the inference of LDCs.

2.3.1 Sampling Frameworks

Following BDB14 and Beare2017improved, we consider two alternative frameworks for sampling from and . From and , we draw identically and independently distributed (iid) samples () that satisfy the following assumption.

Assumption 2.2

(BDB14; Beare2017improved) The iid samples and drawn from and satisfy one of the following conditions.

-

(i)

Independent samples: and are mutually independent, and the sample sizes and are treated as functions of an underlying index such that as ,

(2.17) -

(ii)

Matched pairs: The sample sizes and satisfy , the pairs are iid, and the bivariate copula for those pairs has maximal correlation strictly less than one (see, e.g., beare2010copulas, Definition 3.2).

2.3.2 Construction of Estimator

We define maps , , and by

| (2.18) |

To unify notation, for , we let and defined in (2.5) and (2.6), respectively. Clearly, for , we have by (2.7), (2.3), and (2.4). Following BDB14 and Beare2017improved, for , define the empirical CDF

| (2.19) |

the empirical quantile function

| (2.20) |

and the empirical Lorenz curve

where is the sample mean of . Let . For , define

Define

The difference function between empirical Lorenz curves is defined by

For , let for unified notation. For , define

The estimator of is given by .

2.3.3 Asymptotic Analysis

We now establish the consistency of and derive the asymptotic distribution of

| (2.21) |

for all and , where . We follow fang2014inference and introduce the following definition of Hadamard directional differentiability.

Definition 2.9

Let and be normed spaces. A map is said to be Hadamard directionally differentiable at tangentially to if there is a continuous map such that

| (2.22) |

for all sequences and such that and .

For every , define

| (2.23) |

Here, is the contact set we need to estimate later. For more discussions on the estimation of contact sets, see, for example, linton2010improved for an improved bootstrap test of stochastic dominance and lee2018testing for testing functional inequalities. By Lemma S.4.5 of fang2014inference, we have that and are both Hadamard directionally differentiable at tangentially to with

and

for all .

Following Beare2017improved, we let be a centered Gaussian random element in with covariance kernel

where under Assumption 2.2(i) and is the unique copula function for the pair under Assumption 2.2(ii). Let and be the centered Gaussian random elements in such that and . Under Assumptions 2.1 and 2.2, Beare2017improved show that

| (2.24) |

in for some random element , where is a centered random element of given by

| (2.25) |

Beare2017improved show that

| (2.26) |

for every . We follow Beare2017improved and provide the following lemma.

Lemma 2.5

For all , it follows that

where for and ,

For and , define such that

To unify notation, we let such that for . Then we obtain the following lemma.

Lemma 2.6

We then introduce the following proposition for the asymptotic properties of the estimator . Recall that for , ; for all , and .

Proposition 2.6

Proposition 2.6 provides the asymptotic distribution of when for some . We next construct a bootstrap confidence interval for based on this asymptotic distribution.

2.3.4 Bootstrap Confidence Interval

Since the distribution of in (2.30) is unknown and depends on the underlying DGPs, we use the bootstrap method to approximate this distribution. Because is nonlinear, the standard bootstrap method may not consistently approximate the distribution of (andrews2000inconsistency; bickel2012resampling; fang2014inference). We next employ the bootstrap method of fang2014inference to obtain a consistent approximation of the asymptotic distribution and construct valid critical values. By Lemma 2.5, for and , the estimator for , denoted by , is defined as the sample covariance of the two samples

Let . By Lemma 2.5, for independent samples, we estimate by

| (2.31) |

and for matched pairs, we estimate by

| (2.32) |

We let for all , and for , we let . Based on (2.6) and (2.6) with the estimates in (2.31) and (2.3.4), for , we estimate and by

| (2.33) |

and

| (2.34) |

respectively. Following Beare2017improved, we construct the estimators of , , and by

where is some tuning parameter such that and as and is a small trimming parameter that bounds away from zero. In our simulations and application, is set to . We then construct the estimators of and by

for every . The estimator of is defined by

for every .

For independent samples, we draw bootstrap samples independently with replacement from for , and is jointly independent of . For matched pairs, we draw a bootstrap sample independently with replacement from . Then following BDB14 and Beare2017improved, for , we define the bootstrap empirical CDF

the bootstrap empirical quantile function

| (2.35) |

and the bootstrap empirical Lorenz curve

where is the sample mean of . Let . For , define

Define

and for ,

The bootstrap approximation of is defined by

For , let . For , define

We define the bootstrap approximation of by

| (2.36) |

For every , let denote the quantile of the distribution of . We construct the bootstrap approximation of by

| (2.37) |

In practice, we approximate by computing the quantile of the independently generated , where is chosen as large as is computationally convenient.

For a nominal significance level , we construct the bootstrap confidence interval of by

| (2.38) |

Proposition 2.7

Proposition 2.7 provides the two-sided confidence interval for . It is straightforward to extend the result to one-sided confidence intervals.

3 Simulation Evidence

We run Monte Carlo simulations to provide evidence for the finite sample properties of the estimators and the bootstrap confidence intervals. In this section, we focus on the Lorenz dominance coefficient. Additional simulations are provided in Section C in the appendix. The number of bootstrap samples is . The number of Monte Carlo iterations is . The nominal significance level is set to . We present the mean (Mean), the bias (Bias), the standard error (SE), and the root mean square error (RMSE) of the estimators, and present the coverage rate (CR) of the bootstrap confidence intervals in iterations.

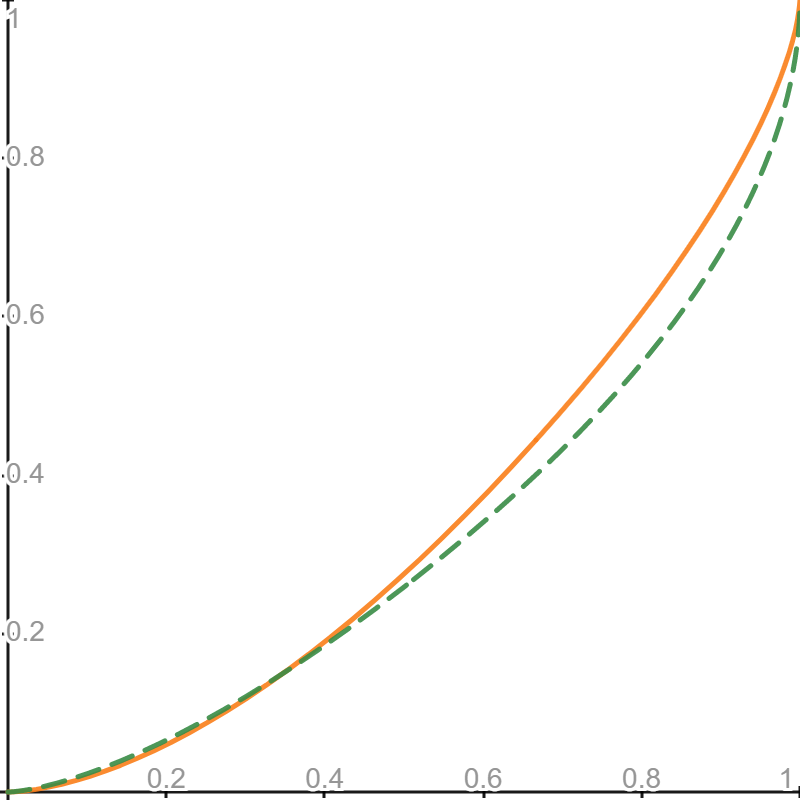

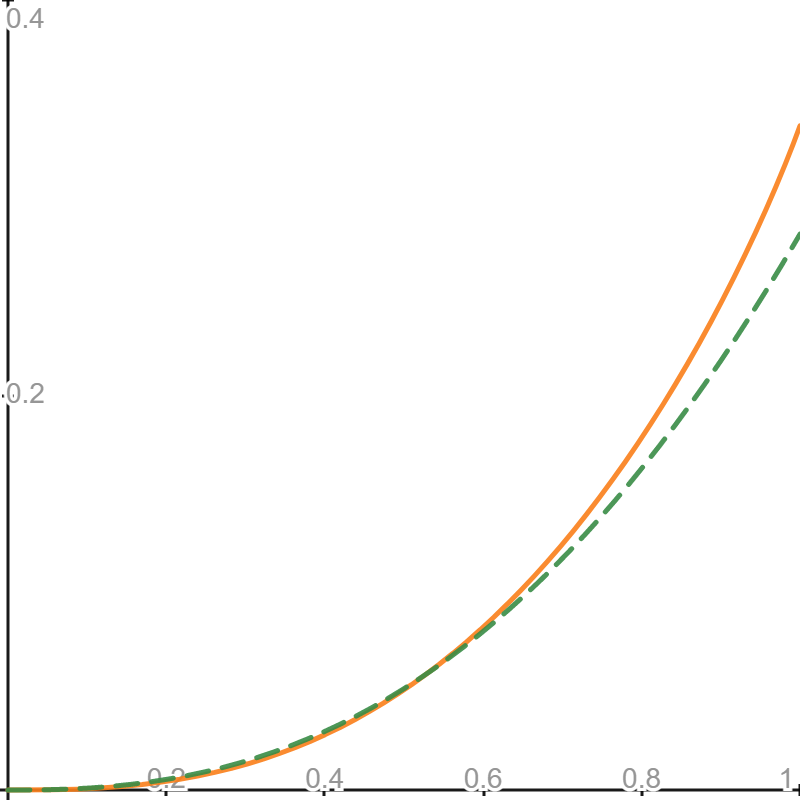

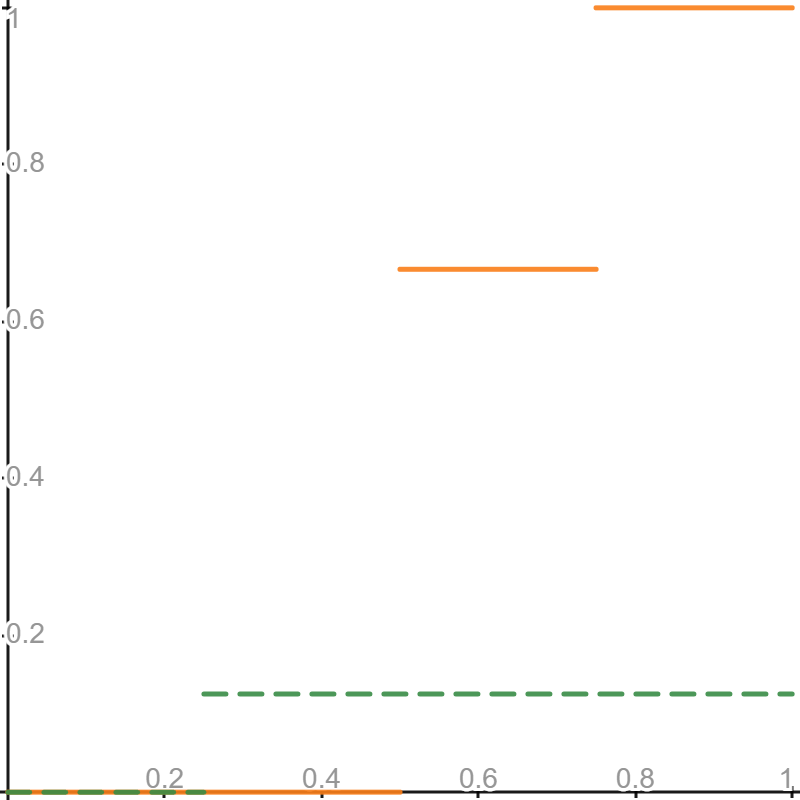

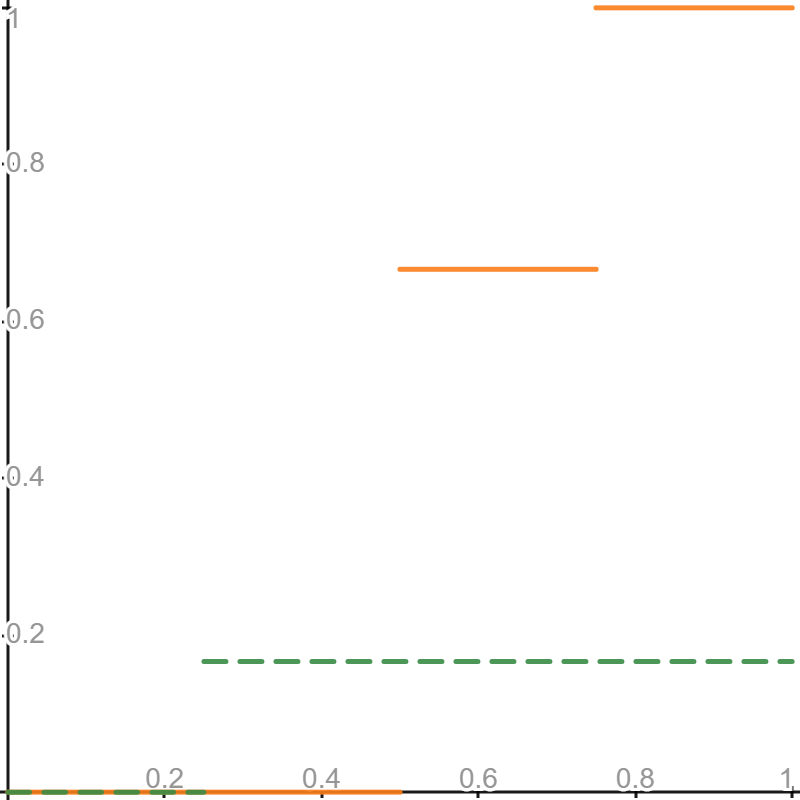

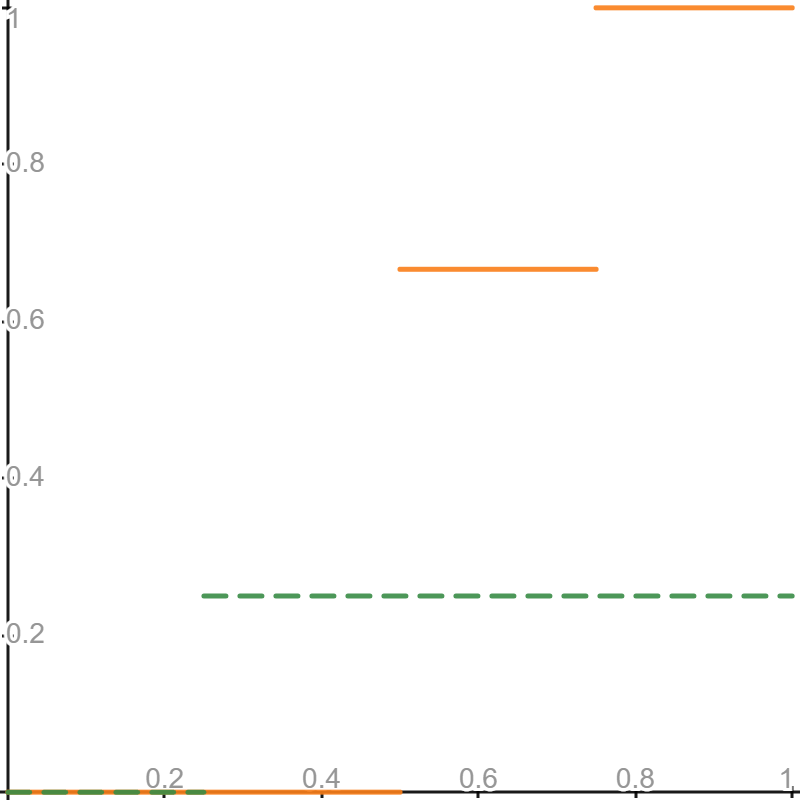

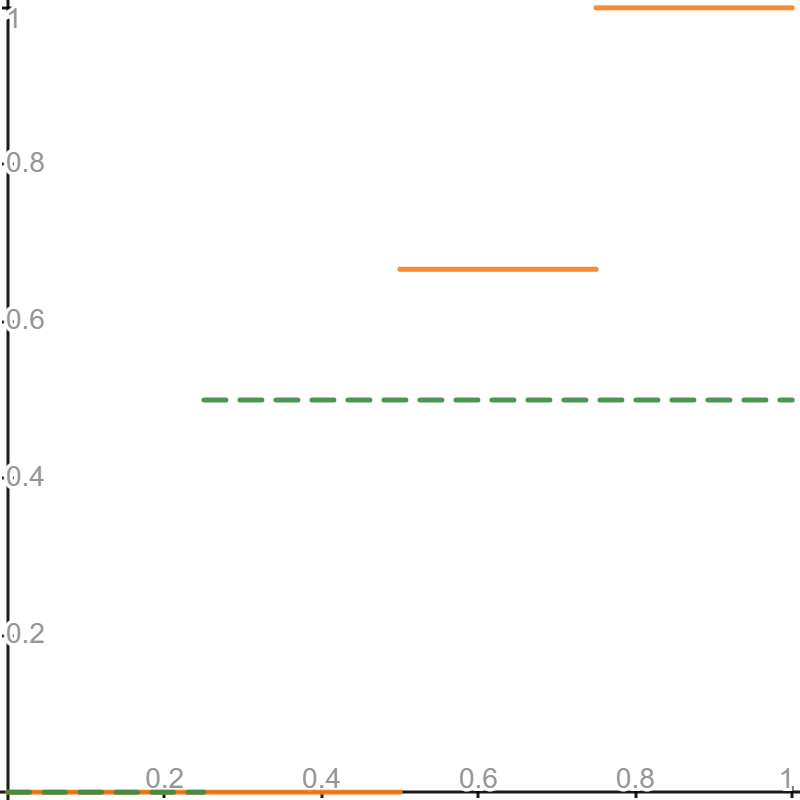

As discussed in Beare2017improved, reed2001pareto; reed2003pareto and toda2012double show that income distributions can be well approximated by members of the double Pareto parametric family. We use distributions from this family to construct the simulations. The density function for the double Pareto family is

where is a scale parameter. For , we write to denote that the random variable has the double Pareto distribution with normalized to one and shape parameters . Assumption 2.1 is satisfied when . We let and with . Figure 3.1 displays the Lorenz curves and corresponding to the above DGPs. The LDC , , , and , respectively, for , , , and . We choose the tuning parameter from . In Section C.3, we show how to choose empirically to construct the bootstrap confidence intervals. For independent samples, we let

For matched pairs, we let

Tables 3.1 and 3.2 show the simulation results for independent samples and matched pairs. For all the DGPs, as and increase, Mean gets close to , Bias decreases to , and both SE and RMSE decrease; under appropriate choices of , CR approaches to .

| DGP | Mean | Bias | SE | RMSE | CR | ||||

|---|---|---|---|---|---|---|---|---|---|

| (a) | 0.04703 | 200 | 200 | 0.2305 | 0.1834 | 0.3088 | 0.3592 | 0.001 | 0.7040 |

| 200 | 500 | 0.1529 | 0.1058 | 0.2420 | 0.2641 | 0.001 | 0.7270 | ||

| 200 | 1000 | 0.1258 | 0.0788 | 0.2144 | 0.2284 | 0.001 | 0.7200 | ||

| 1000 | 2000 | 0.0733 | 0.0263 | 0.0754 | 0.0798 | 0.001 | 0.8630 | ||

| 10000 | 10000 | 0.0523 | 0.0053 | 0.0233 | 0.0239 | 0.001 | 0.9330 | ||

| (b) | 0.31489 | 200 | 200 | 0.4753 | 0.1604 | 0.3341 | 0.3706 | 0.001 | 0.6970 |

| 200 | 500 | 0.3986 | 0.0837 | 0.2865 | 0.2985 | 0.001 | 0.7840 | ||

| 200 | 1000 | 0.3695 | 0.0546 | 0.2650 | 0.2706 | 0.001 | 0.7900 | ||

| 1000 | 2000 | 0.3515 | 0.0366 | 0.1612 | 0.1653 | 0.001 | 0.9140 | ||

| 10000 | 10000 | 0.3260 | 0.0111 | 0.0718 | 0.0727 | 0.001 | 0.9330 | ||

| (c) | 0.45198 | 200 | 200 | 0.5680 | 0.1160 | 0.3182 | 0.3387 | 0.001 | 0.6720 |

| 200 | 500 | 0.5056 | 0.0537 | 0.2770 | 0.2821 | 0.001 | 0.7800 | ||

| 200 | 1000 | 0.4811 | 0.0292 | 0.2574 | 0.2590 | 0.001 | 0.7940 | ||

| 1000 | 2000 | 0.4804 | 0.0284 | 0.1678 | 0.1702 | 0.001 | 0.9100 | ||

| 10000 | 10000 | 0.4619 | 0.0099 | 0.0799 | 0.0805 | 0.001 | 0.9260 | ||

| (d) | 0.51960 | 200 | 200 | 0.6114 | 0.0918 | 0.3060 | 0.3195 | 0.001 | 0.6690 |

| 200 | 500 | 0.5575 | 0.0379 | 0.2674 | 0.2701 | 0.001 | 0.7740 | ||

| 200 | 1000 | 0.5360 | 0.0164 | 0.2484 | 0.2489 | 0.001 | 0.7850 | ||

| 1000 | 2000 | 0.5427 | 0.0231 | 0.1655 | 0.1671 | 0.001 | 0.9030 | ||

| 10000 | 10000 | 0.5283 | 0.0087 | 0.0806 | 0.0811 | 0.001 | 0.9280 |

| DGP | Mean | Bias | SE | RMSE | CR | ||||

|---|---|---|---|---|---|---|---|---|---|

| (a) | 0.04703 | 200 | 200 | 0.1733 | 0.1262 | 0.2616 | 0.2904 | 0.001 | 0.7330 |

| 500 | 500 | 0.1173 | 0.0703 | 0.1783 | 0.1917 | 0.001 | 0.8280 | ||

| 1000 | 1000 | 0.0914 | 0.0444 | 0.1004 | 0.1097 | 0.001 | 0.9010 | ||

| 2000 | 2000 | 0.0692 | 0.0222 | 0.0585 | 0.0626 | 0.001 | 0.9070 | ||

| 10000 | 10000 | 0.0491 | 0.0021 | 0.0179 | 0.0181 | 1.0 | 0.9380 | ||

| (b) | 0.31489 | 200 | 200 | 0.4158 | 0.1009 | 0.3068 | 0.3230 | 0.001 | 0.7560 |

| 500 | 500 | 0.4162 | 0.1013 | 0.2334 | 0.2544 | 0.001 | 0.8590 | ||

| 1000 | 1000 | 0.3907 | 0.0758 | 0.1808 | 0.1961 | 0.001 | 0.9060 | ||

| 2000 | 2000 | 0.3568 | 0.0419 | 0.1434 | 0.1494 | 0.001 | 0.9170 | ||

| 10000 | 10000 | 0.3196 | 0.0047 | 0.0602 | 0.0604 | 7.7 | 0.9500 | ||

| (c) | 0.45198 | 200 | 200 | 0.5185 | 0.0665 | 0.2986 | 0.3059 | 0.001 | 0.7560 |

| 500 | 500 | 0.5473 | 0.0953 | 0.2249 | 0.2443 | 0.001 | 0.8590 | ||

| 1000 | 1000 | 0.5168 | 0.0648 | 0.1811 | 0.1923 | 0.001 | 0.9060 | ||

| 2000 | 2000 | 0.4903 | 0.0383 | 0.1546 | 0.1593 | 0.001 | 0.9170 | ||

| 10000 | 10000 | 0.4561 | 0.0041 | 0.0686 | 0.0687 | 4.4 | 0.9500 | ||

| (d) | 0.51960 | 200 | 200 | 0.5682 | 0.0486 | 0.2898 | 0.2938 | 0.001 | 0.7520 |

| 500 | 500 | 0.6094 | 0.0898 | 0.2144 | 0.2325 | 0.001 | 0.8510 | ||

| 1000 | 1000 | 0.5752 | 0.0556 | 0.1760 | 0.1845 | 0.001 | 0.9000 | ||

| 2000 | 2000 | 0.5547 | 0.0351 | 0.1549 | 0.1589 | 0.001 | 0.9060 | ||

| 10000 | 10000 | 0.5232 | 0.0036 | 0.0700 | 0.0701 | 3.5 | 0.9500 |

4 Empirical Application

In this section, we revisit the example of aaberge2021ranking about the inequality growth in the United Kingdom over the past few decades which may be related to the business cycle (blundell2010consumption). We use the replication data of aaberge2021ranking, which originally came from the European Community Household Panel (ECHP) for 1995–2001, and from the European Union Statistics on Income and Living Conditions (EU-SILC) for 2005–2010. In each year, the sample was restricted to households with a male aged 25–64. We follow aaberge2021ranking and focus on the distribution of individual equivalent income adjusted for inflation and differences in household size and composition.

Tables 3 and 4 of aaberge2021ranking report the successful rankings based on the 3rd-degree upward and downward inverse stochastic dominances. They show that the 3rd-degree upward inverse stochastic dominance does not provide a complete ranking for several years. We apply the proposed method to estimate the upward inverse stochastic dominance coefficients (UISDCs) and construct the confidence intervals of these coefficients for some of these years.777See theoretical and simulation results for upward and downward inverse stochastic dominance coefficients in Sections A and C in the appendix. We compare the latter years () with the former years () shown in Table 4.1, and find that all the estimated UISDCs are small. Furthermore, the bootstrap confidence intervals are narrow. These facts provide evidence that the income distributions of the latter years may almost upward inverse stochastically dominate the income distributions of the former years, which complements the results of aaberge2021ranking.

| Year | UISDC | CI | Year | UISDC | CI |

|---|---|---|---|---|---|

| 94–98 | 3.2067e-08 | [0, 3.0653e-07] | 96–98 | 2.9089e-06 | [0, 1.6521e-05] |

| 94–99 | 1.287e-07 | [0, 8.9855e-07] | 96–99 | 5.9121e-06 | [0, 3.0879e-05] |

| 94–00 | 3.0482e-07 | [0, 1.7727e-06] | 96–00 | 3.8907e-06 | [0, 1.6773e-05] |

| 94–01 | 3.9715e-07 | [0, 2.5549e-06] | 96–01 | 1.2211e-05 | [0, 5.0282e-05] |

| 95–98 | 1.0184e-07 | [0, 8.0492e-07] | 97–98 | 0.0063743 | [0, 0.056701] |

| 95–99 | 3.6099e-07 | [0, 2.5261e-06] | 97–99 | 0.0091885 | [0, 0.069839] |

| 95–00 | 6.5108e-07 | [0, 3.5034e-06] | 97–00 | 8.1315e-05 | [0, 0.0004528] |

| 95–01 | 1.7317e-06 | [0, 9.5748e-06] | 97–01 | 0.00027027 | [0, 0.0011134] |

References

Almost Dominance: Inference and Application

Online Supplementary Appendix

Xiaojun Song Zhenting Sun

[sections] \printcontents[sections]l1

Appendix A Almost Inverse Stochastic Dominance

Following leshno2002preferred, zheng2018almost, and aaberge2021ranking, in this section, we propose almost inverse stochastic dominances, define the inverse stochastic dominance coefficients, and establish an inference procedure for these coefficients. Let and be two distributions that satisfy Assumption 2.1. Define

Let denote the social planner’s preference function. As pointed out by yaari1988controversial and aaberge2021ranking, the social welfare functions are consistent with the condition of second-degree stochastic dominance if and only if and . We follow aaberge2021ranking and define the set of social planner’s preference functions

We then define the welfare functions such that for every and every CDF ,

Theorem 1 of aaberge2001axiomatic demonstrates that a person who supports Axioms 1–4 in aaberge2001axiomatic ranks Lorenz curves according to the criterion .

Remark A.1

aaberge2021ranking discuss the relationship between the inequality measure defined in (2.10) and the social welfare measure . ebert1987size shows that for every preference function and every distribution function that satisfies Assumption 2.1, , where denotes the population mean for and denotes the Lorenz curve corresponding to . As pointed out by aaberge2021ranking, the product presents the loss in social welfare due to inequality in the distribution.

A.1 Almost Upward Inverse Stochastic Dominance and Social Welfare

For , define

aaberge2021ranking introduce the th-degree upward inverse stochastic dominance for .

Definition A.1

A distribution th-degree upward inverse stochastically dominates a distribution if for all .

When , the upward inverse stochastic dominance is the generalized Lorenz dominance. We generalize the upward inverse stochastic dominance in aaberge2021ranking to almost upward inverse stochastic dominance.

Definition A.2

For every , the CDF -almost th-degree upward inverse stochastically dominates the CDF ( -AUISD ), if

| (A.1) |

For every , we define

and

Then the following proposition links AUISD to the social welfare function with from and .

Proposition A.1

For every , if -AUISD , then for every . If -AUISD and for all , then for every .

For , following Lemma 2.1, it is straightforward to show that -AUISD if and only if there is such that

We now define the upward inverse stochastic dominance coefficient as follows.

Definition A.3

For , the - th-degree upward inverse stochastic dominance coefficient (- UISDC), denoted by , is defined as

| (A.2) |

We define the difference function

| (A.3) |

The following lemma summarizes the properties of the UISDC .

Lemma A.1

According to Lemma A.1, -AUISD for all if . On the other hand, implies that -AUISD for all . Thus, presents the degree of almost upward inverse stochastic dominance relationship between and , and provides all such that the -AUISD holds.

Proposition A.2

If , it then follows that . If, in addition, for all , it follows that for every .

Similar to Proposition 2.1, Proposition A.2 shows the importance of UISDC concerning welfare functions . The smaller the UISDC is, the more welfare functions show higher welfare for the distribution compared to . With the knowledge of , we can infer the relationship between and based on a class of welfare functions.

A.2 Almost Downward Inverse Stochastic Dominance and Social Welfare

aaberge2021ranking introduce the th-degree downward inverse stochastic dominance for . For , define

For , define

Definition A.4

A distribution th-degree downward inverse stochastically dominates a distribution if for all .

We generalize the downward inverse stochastic dominance in aaberge2021ranking to almost downward inverse stochastic dominance.

Definition A.5

For every , the CDF -almost th-degree downward inverse stochastically dominates the CDF ( -ADISD ), if

For every , we define

and

Then the following proposition links ADISD to the social welfare function with from and .

Proposition A.3

For every , if -ADISD , then for every . If -ADISD and for all , then for every .

For , following Lemma 2.1, it is straightforward to show that -ADISD if and only if there is such that

We now define the downward inverse stochastic dominance coefficient as follows.

Definition A.6

For , the - th-degree downward inverse stochastic dominance coefficient (- DISDC), denoted by , is defined as

| (A.5) |

We define the difference function

| (A.6) |

The following lemma summarizes the properties of the DISDC .

Lemma A.2

According to Lemma A.2, -ADISD for all if . On the other hand, implies that -ADISD for all . Thus, presents the degree of almost downward inverse stochastic dominance relationship between and , and provides all such that the -ADISD holds.

Proposition A.4

If , it then follows that for all . If, in addition, for all , then for every .

Similar to Proposition 2.1, Proposition A.4 shows the importance of DISDC concerning welfare functions . The smaller the DISDC is, the more welfare functions show higher welfare for the distribution compared to . With the knowledge of , we can infer the relationship between and based on a class of welfare functions.

A.3 Estimation and Inference

Let , , and be defined as in (2.3.2), (2.19), and (2.20). Let and be the centered Gaussian random elements in defined in Section 2.3.3. It is straightforward to show that (see the proof of Lemma B.2)

in . Beare2017improved show that under Assumptions 2.1 and 2.2, we can apply the results of K17 and obtain

in . Recall that for all , and we estimate by . As shown in jiang2023nonparametric, by continuous mapping theorem,

| (A.10) |

where . By continuous mapping theorem again, it follows that

where and for all ,

By Lemma 3.1 of jiang2023nonparametric, for and , we have that

| (A.11) |

For , , and , define

and

For , define the empirical difference functions

The estimator for can be constructed by

Similar to Proposition 2.6, we can show that is Hadamard directionally differentiable at defined in (A.3) and (A.6) such that for every ,

where

and

with and defined in (2.23).

Proposition A.5

Let . For and , by (A.11), we estimate by which is defined as the sample covariance of the two samples

For independent samples, we estimate by

For matched pairs,

We then estimate the variance by

and

for .

A.3.1 Bootstrap Confidence Intervals for UISDC and DISDC

Similar to Section 2.3.4, for and , we construct the estimators of , , and by

where and as . We then construct the estimator of and by

for every . The estimator of is defined by

for every .

As discussed in Section 2.3.4, for independent samples, we draw bootstrap samples identically and independently from for , where is jointly independent of . For matched pairs, we draw a bootstrap sample identically and independently from . Let be defined as in (2.35). For , , and , define

and

Define the bootstrap difference functions

For , we define the bootstrap estimation of by

| (A.12) |

For every , let denote the quantile of the distribution of . We construct the bootstrap approximation of by

| (A.13) |

Empirically, we approximate by computing the quantile of the independently generated , where is chosen as large as is computationally convenient.

For a nominal significance level , we construct the confidence interval by

| (A.14) |

Appendix B Almost Stochastic Dominance

In this section, we extend our results to almost stochastic dominance. We follow tsetlin2015generalized and let be a decision maker’s utility function and the th derivative of . Let and be CDFs that are restricted on the support such that and . For and , we define

with for all . To fix the idea, we first consider almost first-degree stochastic dominance. Define

The original definition of almost first-degree stochastic dominance provided by leshno2002preferred is as follows.

Definition B.1

For every , -almost first-degree stochastically dominates ( -AFSD ) if

| (B.1) |

For every , define the utility function class

leshno2002preferred associate -AFSD with the class by showing that for every , -AFSD if and only if for all , where denotes the expectation for . As pointed out by tsetlin2015generalized, -AFSD is a weaker version of first-degree stochastic dominance (FSD): -AFSD requires that the ratio of the area between and for which (i.e., ) to the total area between and (i.e., ) is less than or equal to ; FSD requires that this ratio is zero, i.e., . It is interesting to figure out the smallest value of such that (B.1) holds. If we denote this value by , then it is easy to show (by proof similar to that of Lemma 2.2) that for all . We now consider general -almost th-degree stochastic dominance. We follow tsetlin2015generalized and define

Definition B.2

For every , -almost th-degree stochastically dominates ( -ASD ) if

| (B.2) |

For every , define the utility function class

Theorem 4 of tsetlin2015generalized shows that for all if and only if -ASD and for all . Similarly, we are interested in finding the smallest such that (B.2) holds. We propose the th-degree stochastic dominance coefficient as follows for all .

Definition B.3

The - th-degree stochastic dominance coefficient (- SDC), denoted by , is defined as

| (B.3) |

We define the difference function

The following lemma summarizes the properties of the SDC .

Lemma B.1

According to Lemma B.1, -ASD for all if . On the other hand, implies that -ASD for all . Thus, presents the degree of almost stochastic dominance relationship between and , and provides all such that the -ASD holds.

Proposition B.1

If and for all , it then follows that for all .

Similar to Proposition 2.1, Proposition B.1 shows the importance of SDC concerning utility functions. The smaller the SDC is, the more utility functions show higher expected utility for the distribution compared to . With the knowledge of , we can infer the relationship between and based on a class of utility functions.

B.1 Estimation and Inference

Next, we provide an approach of estimating and conducting inference on it.

Assumption B.1

Let random variables and have the joint CDF with marginal CDFs and , respectively. The mean vector is finite and has a finite covariance matrix.

Similar to Sections 2 and A, we define maps , , and by

| (B.5) |

Given the sample as in Assumption 2.2, let () be defined as in (2.19) for . For matched pairs, define the empirical joint CDF

| (B.6) |

For , define

with for all . Define

| (B.7) |

for every measurable function . For , define the empirical version of by

The estimator for can be constructed by

For every , define

Proposition B.2

Let . With (B.2), for independent samples, we estimate by

for all . For matched pairs, we estimate by

for all . We then estimate the variance by

for every .

B.1.1 Bootstrap Confidence Interval

Following Section 2.3.4, we construct the estimators of , , and by

where and as . We then construct the estimator of and by

for every . The estimator of is defined by

for every .

As discussed in Section 2.3.4, for independent samples, we draw bootstrap samples identically and independently from for , where is jointly independent of . For matched pairs, we draw a bootstrap sample identically and independently from . Let be defined as in Section 2.3.4 for . Then we define the bootstrap version of by

We define the bootstrap approximation of by

| (B.10) |

For every , let denote the quantile of the distribution of . We construct the bootstrap approximation of by

| (B.11) |

Empirically, we approximate by computing the quantile of the independently generated , where is chosen as large as is computationally convenient.

For a nominal significance level , we construct the confidence interval by

| (B.12) |

Proposition B.3

Suppose that Assumption 2.2 holds. If and the CDF of is continuous and increasing at and , then it follows that

| (B.13) |

Appendix C Additional Simulation Evidence

In this section, we provide additional simulation results for ISDCs and SDCs.

C.1 Inverse Stochastic Dominance Coefficient

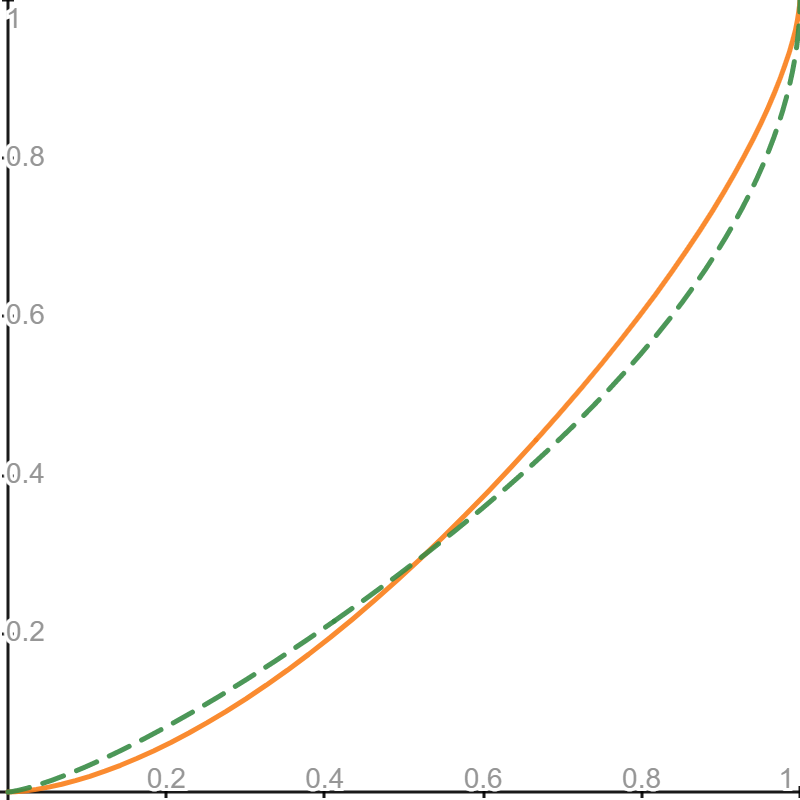

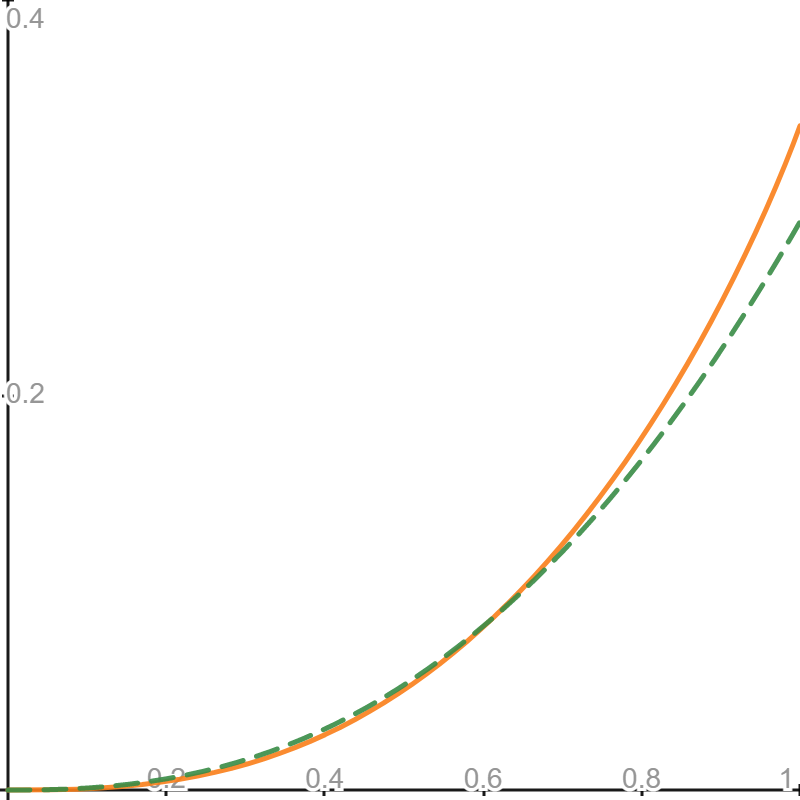

We consider simulations for UISDC. In each iteration of the simulations for UISDC, the data are generated independently from , and the data are generated independently from , whose law is parametrized by . We let . Figure C.1 displays the curves and corresponding to the above DGPs. The UISDC , , , and , respectively, for , , , and . We choose the tuning parameter from . For independent samples, we let

For matched pairs, we let

Tables C.1 and C.2 show the simulation results for independent samples and matched pairs. For all the DGPs, as and increase, Mean gets close to , Bias decreases to , and both SE and RMSE decrease; under appropriate choices of , CR approaches to .

| DGP | Mean | Bias | SE | RMSE | CR | ||||

|---|---|---|---|---|---|---|---|---|---|

| (a) | 0.06229 | 200 | 200 | 0.1736 | 0.1113 | 0.2474 | 0.2713 | 0.001 | 0.6980 |

| 200 | 500 | 0.1339 | 0.0716 | 0.2040 | 0.2162 | 0.001 | 0.7190 | ||

| 200 | 1000 | 0.1127 | 0.0504 | 0.1797 | 0.1866 | 0.001 | 0.6960 | ||

| 1000 | 2000 | 0.0777 | 0.0154 | 0.0762 | 0.0778 | 0.001 | 0.8430 | ||

| 10000 | 10000 | 0.0633 | 0.0010 | 0.0219 | 0.0219 | 0.001 | 0.9220 | ||

| (b) | 0.14052 | 200 | 200 | 0.2546 | 0.1141 | 0.2916 | 0.3131 | 0.001 | 0.6850 |

| 200 | 500 | 0.2130 | 0.0725 | 0.2566 | 0.2666 | 0.001 | 0.7210 | ||

| 200 | 1000 | 0.1882 | 0.0476 | 0.2351 | 0.2398 | 0.001 | 0.7080 | ||

| 1000 | 2000 | 0.1577 | 0.0172 | 0.1206 | 0.1218 | 0.001 | 0.8510 | ||

| 10000 | 10000 | 0.1404 | -0.0001 | 0.0406 | 0.0406 | 0.001 | 0.9190 | ||

| (c) | 0.26581 | 200 | 200 | 0.3461 | 0.0803 | 0.3231 | 0.3329 | 0.001 | 0.6680 |

| 200 | 500 | 0.3077 | 0.0419 | 0.2961 | 0.2990 | 0.001 | 0.7140 | ||

| 200 | 1000 | 0.2819 | 0.0161 | 0.2801 | 0.2806 | 0.001 | 0.7030 | ||

| 1000 | 2000 | 0.2735 | 0.0076 | 0.1630 | 0.1631 | 0.001 | 0.8620 | ||

| 10000 | 10000 | 0.2617 | -0.0041 | 0.0616 | 0.0618 | 0.001 | 0.9200 | ||

| (d) | 0.42840 | 200 | 200 | 0.4418 | 0.0134 | 0.3389 | 0.3392 | 0.001 | 0.6690 |

| 200 | 500 | 0.4117 | -0.0167 | 0.3174 | 0.3178 | 0.001 | 0.7010 | ||

| 200 | 1000 | 0.3868 | -0.0416 | 0.3086 | 0.3114 | 0.001 | 0.6970 | ||

| 1000 | 2000 | 0.4139 | -0.0145 | 0.1899 | 0.1905 | 0.001 | 0.8660 | ||

| 10000 | 10000 | 0.4177 | -0.0107 | 0.0761 | 0.0768 | 0.001 | 0.9210 |

| DGP | Mean | Bias | SE | RMSE | CR | ||||

|---|---|---|---|---|---|---|---|---|---|

| (a) | 0.06229 | 200 | 200 | 0.1212 | 0.0589 | 0.1711 | 0.1809 | 0.001 | 0.7690 |

| 500 | 500 | 0.1386 | 0.0764 | 0.1308 | 0.1515 | 0.001 | 0.9320 | ||

| 1000 | 1000 | 0.0912 | 0.0289 | 0.0732 | 0.0787 | 0.001 | 0.9430 | ||

| 2000 | 2000 | 0.0709 | 0.0086 | 0.0422 | 0.0431 | 0.001 | 0.9350 | ||

| 10000 | 10000 | 0.0642 | 0.0019 | 0.0166 | 0.0167 | 2.4 | 0.9510 | ||

| (b) | 0.14052 | 200 | 200 | 0.1998 | 0.0593 | 0.2236 | 0.2313 | 0.001 | 0.7930 |

| 500 | 500 | 0.2453 | 0.1048 | 0.1785 | 0.2070 | 0.001 | 0.9400 | ||

| 1000 | 1000 | 0.1863 | 0.0458 | 0.1180 | 0.1266 | 0.001 | 0.9490 | ||

| 2000 | 2000 | 0.1519 | 0.0114 | 0.0729 | 0.0738 | 0.001 | 0.9510 | ||

| 10000 | 10000 | 0.1423 | 0.0018 | 0.0305 | 0.0306 | 3.7 | 0.9510 | ||

| (c) | 0.26581 | 200 | 200 | 0.2972 | 0.0314 | 0.2656 | 0.2674 | 0.001 | 0.8020 |

| 500 | 500 | 0.3783 | 0.1125 | 0.2106 | 0.2388 | 0.001 | 0.9180 | ||

| 1000 | 1000 | 0.3221 | 0.0563 | 0.1576 | 0.1674 | 0.001 | 0.9480 | ||

| 2000 | 2000 | 0.2756 | 0.0098 | 0.1046 | 0.1050 | 1 | 0.9380 | ||

| 10000 | 10000 | 0.2655 | -0.0004 | 0.0462 | 0.0462 | 6.7 | 0.9500 | ||

| (d) | 0.42840 | 200 | 200 | 0.4061 | -0.0223 | 0.2900 | 0.2909 | 0.001 | 0.8030 |

| 500 | 500 | 0.5203 | 0.0919 | 0.2186 | 0.2371 | 0.001 | 0.8990 | ||

| 1000 | 1000 | 0.4810 | 0.0526 | 0.1761 | 0.1838 | 0.001 | 0.9320 | ||

| 2000 | 2000 | 0.4305 | 0.0021 | 0.1244 | 0.1244 | 1.5 | 0.9500 | ||

| 10000 | 10000 | 0.4236 | -0.0048 | 0.0567 | 0.0569 | 15.6 | 0.9550 |

C.2 Stochastic Dominance Coefficient

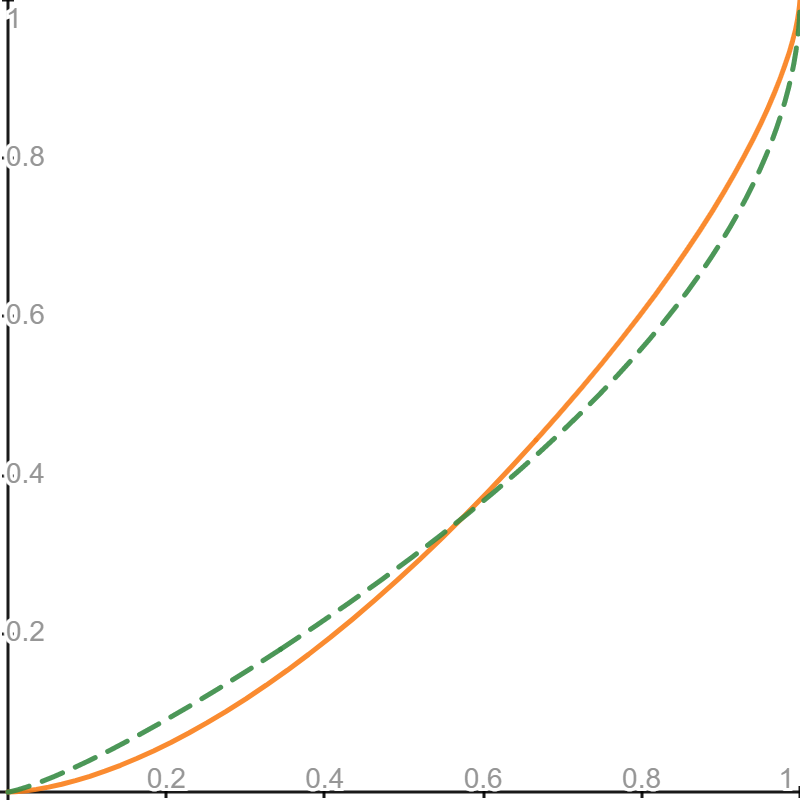

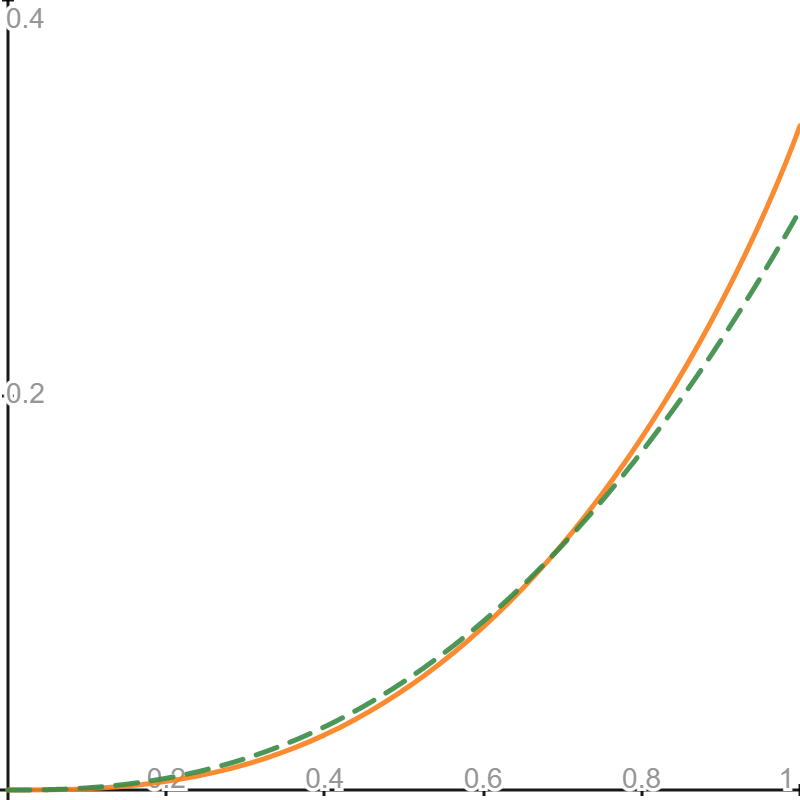

We let and be random variables such that

with . Figure C.2 displays the CDF curves and corresponding to the above DGPs. The SDC , , , and , respectively for , , , and . We choose the tuning parameter from . For independent samples, we let

For matched pairs, we let

Tables C.3 and C.4 show the simulation results for independent samples and matched pairs which are similar to those in Tables 3.1 and 3.2. For all DGPs, as and increase, Mean gets close to , Bias decreases to , and both SE and RMSE decrease; under appropriate choices of , CR approaches to .

| DGP | Mean | Bias | SE | RMSE | CR | ||||

|---|---|---|---|---|---|---|---|---|---|

| (a) | 0.08108 | 100 | 100 | 0.0826 | 0.0016 | 0.0241 | 0.0241 | 0.001 | 0.9380 |

| 100 | 200 | 0.0823 | 0.0012 | 0.0236 | 0.0236 | 0.001 | 0.9350 | ||

| 100 | 500 | 0.0812 | 0.0002 | 0.0229 | 0.0229 | 0.001 | 0.9330 | ||

| 200 | 500 | 0.0819 | 0.0009 | 0.0171 | 0.0171 | 0.001 | 0.9270 | ||

| 1000 | 1000 | 0.0812 | 0.0001 | 0.0073 | 0.0073 | 0.001 | 0.9490 | ||

| (b) | 0.11111 | 100 | 100 | 0.1130 | 0.0019 | 0.0290 | 0.0290 | 0.001 | 0.9410 |

| 100 | 200 | 0.1114 | 0.0003 | 0.0276 | 0.0276 | 0.001 | 0.9450 | ||

| 100 | 500 | 0.1119 | 0.0008 | 0.0269 | 0.0269 | 0.001 | 0.9540 | ||

| 200 | 500 | 0.1115 | 0.0004 | 0.0196 | 0.0196 | 0.001 | 0.9440 | ||

| 1000 | 1000 | 0.1111 | 0.0000 | 0.0086 | 0.0086 | 0.001 | 0.9500 | ||

| (c) | 0.17647 | 100 | 100 | 0.1804 | 0.0039 | 0.0386 | 0.0388 | 2.7 | 0.9470 |

| 100 | 200 | 0.1781 | 0.0016 | 0.0370 | 0.0371 | 3.0 | 0.9390 | ||

| 100 | 500 | 0.1766 | 0.0001 | 0.0361 | 0.0361 | 3.9 | 0.9490 | ||

| 200 | 500 | 0.1774 | 0.0010 | 0.0251 | 0.0251 | 5.8 | 0.9510 | ||

| 1000 | 1000 | 0.1767 | 0.0002 | 0.0113 | 0.0113 | 12.0 | 0.9510 | ||

| (d) | 0.42857 | 100 | 100 | 0.4326 | 0.0040 | 0.0652 | 0.0653 | 0.001 | 0.9470 |

| 100 | 200 | 0.4355 | 0.0069 | 0.0657 | 0.0660 | 0.001 | 0.9390 | ||

| 100 | 500 | 0.4317 | 0.0032 | 0.0634 | 0.0635 | 0.001 | 0.9410 | ||

| 200 | 500 | 0.4302 | 0.0016 | 0.0443 | 0.0443 | 0.001 | 0.9450 | ||

| 1000 | 1000 | 0.4284 | -0.0002 | 0.0209 | 0.0209 | 5.0 | 0.9500 |

| DGP | Mean | Bias | SE | RMSE | CR | ||||

|---|---|---|---|---|---|---|---|---|---|

| (a) | 0.08108 | 100 | 100 | 0.0824 | 0.0013 | 0.0233 | 0.0234 | 0.001 | 0.9450 |

| 200 | 200 | 0.0817 | 0.0006 | 0.0164 | 0.0164 | 0.001 | 0.9450 | ||

| 300 | 300 | 0.0816 | 0.0006 | 0.0138 | 0.0138 | 0.001 | 0.9410 | ||

| 500 | 500 | 0.0815 | 0.0004 | 0.0101 | 0.0101 | 7.3 | 0.9520 | ||

| 1000 | 1000 | 0.0815 | 0.0004 | 0.0077 | 0.0077 | 7.3 | 0.9390 | ||

| (b) | 0.11111 | 100 | 100 | 0.1126 | 0.0015 | 0.0278 | 0.0278 | 3.3 | 0.9530 |

| 200 | 200 | 0.1113 | 0.0002 | 0.0190 | 0.0190 | 3.3 | 0.9470 | ||

| 300 | 300 | 0.1111 | 0.0000 | 0.0158 | 0.0158 | 6.4 | 0.9510 | ||

| 500 | 500 | 0.1116 | 0.0005 | 0.0114 | 0.0115 | 9.0 | 0.9510 | ||

| 1000 | 1000 | 0.1117 | 0.0006 | 0.0089 | 0.0089 | 9.0 | 0.9490 | ||

| (c) | 0.17647 | 100 | 100 | 0.1796 | 0.0031 | 0.0359 | 0.0361 | 4.6 | 0.9480 |

| 200 | 200 | 0.1768 | 0.0003 | 0.0248 | 0.0248 | 6.9 | 0.9490 | ||

| 300 | 300 | 0.1766 | 0.0001 | 0.0203 | 0.0203 | 8.7 | 0.9530 | ||

| 500 | 500 | 0.1768 | 0.0003 | 0.0152 | 0.0152 | 11.7 | 0.9510 | ||

| 1000 | 1000 | 0.1769 | 0.0004 | 0.0110 | 0.0110 | 16.9 | 0.9500 | ||

| (d) | 0.42857 | 100 | 100 | 0.4298 | 0.0012 | 0.0519 | 0.0519 | 4.9 | 0.9490 |

| 200 | 200 | 0.4299 | 0.0013 | 0.0371 | 0.0371 | 6.5 | 0.9550 | ||

| 300 | 300 | 0.4294 | 0.0009 | 0.0292 | 0.0292 | 7.9 | 0.9460 | ||

| 500 | 500 | 0.4289 | 0.0004 | 0.0229 | 0.0229 | 10.0 | 0.9480 | ||

| 1000 | 1000 | 0.4299 | 0.0014 | 0.0156 | 0.0157 | 13.9 | 0.9510 |

C.3 Tuning Parameter Selection

In the above simulations, we compute the confidence intervals for all from some prespecified set and display the values that yield the best results. We now propose an empirical way of selecting in practice. Let be selected from a set which is sufficiently large. Suppose that we observe the data and . We then take the empirical distributions of and as the DGP to generate the data in the simulations and compute the dominance coefficient based on the empirical distributions of and . We take this as the true value of the coefficient we are interested in. Then we follow the previous simulation procedure to compute the bootstrap confidence intervals for every value of . Finally, we pick the value which yields the coverage rate that is closest to , and use this value to construct the bootstrap confidence intervals in the application.

Appendix D Proofs

D.1 Proofs for Section 2

Proof of Lemma 2.1. If (2.4) holds with some for some , then clearly -ALD by definition. If -ALD for some , then we can find

that satisfies (2.4).

Proof of Lemma 2.2. Suppose that

then there is some such that

For all with

we have that . It then follows that

for all such that , which contradicts the definition of . Thus, we have

If there is some other such that and

then the definition of is contradicted. Thus, is the smallest such that (2.3) holds. If , then . By (1.1), (2.7) holds. If , then and clearly . Then (2.7) holds since is the smallest such that (2.3) holds.

If , then which implies that Lorenz dominates . If Lorenz dominates , then and thus . If , then which implies that Lorenz dominates .

Proof of Proposition 2.1. For every , by Lemma 2.2 and Proposition 1 of zheng2018almost, -ALD for every and for all . If , then by Lemma 2.2, Lorenz dominates and the claim is clearly true.

Proof of Proposition 2.2. The proof closely follows the strategies of the proofs of Theorem 1 of leshno2002preferred and Theorem 3.1A of aaberge2009ranking. Using integration by parts, we can show that for every ,

If , then . For every , let and . Also, let . It then follows that

With , we have

which implies .

If for all , then for every , we have that and the result follows.

Proof of Proposition 2.4. The proof closely follows the strategies of the proofs of Theorem 1 of leshno2002preferred and Theorem 3.1B of aaberge2009ranking. Clearly, for , we have that . Also,

and it follows that . Then we have that for every ,

If , then . Let and . Also, let . It then follows that

With , we have

which implies .

If for all , then for every , and the result follows.

Lemma D.1

Let be a normed space. Suppose that and such that and are both Hadamard directionally differentiable at tangentially to some with the derivatives and . Then we have the following results:

-

(i)

The summation is Hadamard directionally differentiable at such that

-

(ii)

The multiplication is Hadamard directionally differentiable at such that

-

(iii)

If , then the inverse is Hadamard directionally differentiable at such that

Proof of Lemma D.1. Let and such that .

(i). By definition, it is easy to show that

(ii). First, we have that

Then, by the continuity of ( is directionally differentiable), we can show that

and

(iii). We first write

Then, by the continuity of ( is directionally differentiable), we can show that

Proof of Lemma 2.5. We closely follow the proofs of Lemma A.1 of Beare2017improved and Lemma 3.1 of jiang2023nonparametric. First, we have that

For , , and , define

Note that the almost sure integrability of follows from the weak convergence of in established by K17. Then we can show that defined in (2.25) satisfies that

Define

For and , by Fubini’s theorem,

Let be a pair of random variables with joint CDF given by the copula in Assumption 2.2(ii). For and , . By Theorem 3.1 of lo2017functional (see also cuadras2002covariance and beare2009generalization),

Then it follows that

For , . By Theorem 3.1 of lo2017functional again,

Then it follows that

Proof of Lemma 2.6. The results follow from the continuous mapping theorem and Fubini’s theorem (see, for example, Theorem 2.37 of folland2013real).

Proof of Proposition 2.6. For simplicity of notation, we focus on the case where . The proof of general results for and is similar. We first show the Hadamard differentiability of . Because and are continuous in , if for some , then . By Lemma D.1, we have that

| (D.1) |

This implies the continuity of . By Lemma 3 of BDB14, we have a.s. With (2.24) and (D.1), by Theorem 2.1 of fang2014inference, (2.30) holds.

Proof of Proposition 2.7. For simplicity of notation, we focus on the case where . The proof of general results for and is similar. Since , and . Let and denote the Lebesgue measure in the following. First, we have that

Since , then by Example 1.4.7 (Slutsky’s lemma) and Theorem 1.3.6 (continuous mapping) of van1996weak,

Then by Theorem 1.3.4(iii) of van1996weak, .

By Lemma 3 of BDB14, a.s. For simplicity of notation, let denote in the following. In the proof of Lemma A.2 of Beare2017improved, it is shown that is bounded by some a.s. Define

where the subscript denotes that the random elements are fixed at . Then . Consider

For every fixed , we have that

where

For every such that , since , then when is large enough, . Since is uniformly bounded and , we have that ( is fixed) for every fixed ,

Thus, by the dominated convergence theorem ( is fixed),

This implies that for every ,

Then by the dominated convergence theorem again,

Similarly, we can show that

In addition,

Also, we have that

Then by similar arguments, we have that

It is easy to show that is Lipschitz continuous, because

Similarly, we can show that is Lipschitz continuous. For every ,

Similarly, we can show that

Next, since a.s. by BDB14, we have that for some ,

Also, since and for every , then we have . By Remark 3.4 of fang2014inference, Assumption 4 of fang2014inference holds.

By a proof similar to that of Theorem S.1.1 in fang2014inference, we can show that

By Proposition 2.6 in the paper and Example 1.4.7 (Slutsky’s lemma), Theorem 1.3.6 (continuous mapping), and Theorem 1.3.4(vi) of van1996weak,

and

which imply that

or equivalently

D.2 Proofs for Section A

Proof of Proposition A.1. The proof closely follows the strategies of the proofs of Theorem 1 of leshno2002preferred and Theorem 2.3 of aaberge2021ranking. We can show that

The remaining of the proof is similar to that of Proposition 2.2.

Proof of Proposition A.3. The proof closely follows the strategies of the proofs of Theorem 1 of leshno2002preferred and Theorem 2.4 of aaberge2021ranking. By definition, for , we have that

which implies . Also, we have that

By a strategy similar to that of the proof of Proposition A.1, we can show that

The remaining of the proof is similar to that of Proposition 2.4.

D.3 Proofs for Section B

Proof of Proposition B.1. The results directly follow from Lemma B.1 and Theorem 4 of tsetlin2015generalized.

Proof of Lemma B.2. The proof for independent samples is trivial and is omitted. For matched pairs, let , , and . Define

for every . Since and are both Donsker classes, by Example 2.10.7 of van1996weak, in for some zero-mean Gaussian process . Define a map such that for every and every ,

Then by continuous mapping theorem,

where for every ,

By continuous mapping theorem again, we obtain that

where for every ,

with . Then it is easy to show that for all ,