DeFi Security: Turning The Weakest Link Into The Strongest Attraction

Ravi Kashyap (ravi.kashyap@stern.nyu.edu)111 Numerous seminar participants, particularly at a few meetings of the econometric society and various finance organizations, provided suggestions to improve the paper. The following individuals have been a constant source of inputs and encouragement: Dr. Yong Wang, Dr. Isabel Yan, Dr. Vikas Kakkar, Dr. Fred Kwan, Dr. Costel Daniel Andonie, Dr. Guangwu Liu, Dr. Jeff Hong, Dr. Humphrey Tung and Dr. Xu Han at the City University of Hong Kong. The views and opinions expressed in this article, along with any mistakes, are mine alone and do not necessarily reflect the official policy or position of either of my affiliations or any other agency.

Estonian Business School / City University of Hong Kong

February 27, 2024

Keywords: DeFi; Security; Blockchain; OTNTP - One Time Next Time Password; Safe-House; Investment Fund; UnAuthorized Access; Hack

Association for Computing Machinery Classification System: K.6.5: Security and Protection; D.4.6: Security and Protection; D.2.11: Software Architectures; B.8.2: Performance Analysis and Design Aids; I.2.8: Problem Solving; H.1.1: Systems and Information Theory

Journal of Economic Literature Codes: O3 Innovation • Research and Development • Technological Change • Intellectual Property Rights; D81 Criteria for Decision-Making under Risk and Uncertainty; C63 Computational Techniques; O31 Innovation and Invention: Processes and Incentives

Mathematics Subject Classification Codes: 94A62: Authentication and secret sharing; 93A14 Decentralized systems; 94A60: Cryptography; 91G45 Financial networks; 97U70 Technological tools

1 Abstract

The primary innovation we pioneer - focused on blockchain information security- is called the Safe-House. The Safe-House is badly needed since there are many ongoing hacks and security concerns in the DeFi space right now. The Safe-House is a piece of engineering sophistication that utilizes existing blockchain principles to bring about greater security when customer assets are moved around. The Safe-House logic is easily implemented as smart contracts on any decentralized system. The amount of funds at risk from both internal and external parties - and hence the maximum one time loss - is guaranteed to stay within the specified limits based on cryptographic fundamentals.

The Safe-House provides a first level of security that caters to, a significant extent, the enhanced fund movement needs for today’s DeFi protocols and blockchain investment funds. To improve the safety of the Safe-House even further, we adapt the one time password (OPT) concept to operate using blockchain technology. Well suited to blockchain cryptographic nuances, our secondary advancement can be termed the one time next time password (OTNTP) mechanism. The OTNTP is designed to complement the Safe-House making it even more safe.

We provide a detailed threat assessment model - discussing the risks faced by DeFi protocols and the specific risks that apply to blockchain fund management - and give technical arguments regarding how these threats can be overcome in a robust manner. We discuss how the Safe-House can participate with other external yield generation protocols in a secure way. We provide reasons for why the Safe-House increases safety without sacrificing the efficiency of operation. We start with a high level intuitive description of the landscape, the corresponding problems and our solutions. We then supplement this overview with detailed discussions including the corresponding mathematical formulations and pointers for technological implementation.This approach ensures that the article is accessible to a broad audience.

Investors are currently wary of putting their trust - and wealth - in the hands of financial intermediaries when they cannot be held fully accountable in an industry that still requires much closer scrutiny and regulation. Our innovations will ensure that losses can be attributed - mostly - to oversights - or any fraudulent intentions - of fund representatives who are accepting money from others and hence are taking on fiduciary responsibility. Such accountability - and transparency - will bring greater interest - and involvement - from many who are still on the fringes - or even far away from the reach - of blockchain technology. Incorporating the best practices we have introduced should aid in the wider adoption of blockchain technologies and in particular assuage the concerns of those who are disturbed by the increasing number of crimes in this space.

When investors are assured about the safety of their funds, it will provide much needed impetus - in terms of financing, by allowing many superior risk mitigation techniques from traditional finance to be applied to blockchain portfolios - to several upcoming projects by enhancing trust between financial market participants and intermediaries operating in a decentralized environment. We have reviewed around 240 papers spanning both technology and financial topics - artificial as these topical distinctions can be at times, we have strived to ensure that the paper can be useful for both technologists and financial specialists - and linked the insights towards creating a secure wealth management system that can be accessible by everyone.

The Safe-House - and related components - have been successfully deployed for commercial use on multiple platforms - Ethereum, Binance and Polygon - and hundreds of transactions have been performed satisfactorily.

2 Introduction: DeFi Defense Dilemmas

The invention of Bitcoin is transforming all aspects of business and human interactions (Nakamoto 2008; Narayanan & Clark 2017; Chen 2018; Monrat, et al. 2019; End-note 1). This seminal event - a landmark permanently etched in the history of technological change - has opened the floodgates for innovations seeking to add different aspects of human experiences onto the blockchain (Karamitsos et al., 2018; Zhang et al., 2018; Alladi et al., 2019; Kuo et al., 2019; Lu 2019; Whitaker 2019; Bumblauskas et al., 2020; Gatteschi et al., 2020; Hunhevicz & Hall 2020; Prewett et al., 2020; Brophy 2020). The rest, as they say, is history.

Most blockchain services have a financial component embedded within them as part of the overall offering. Almost all decentralized projects - even those which do not directly cater to a financial need - create blockchain based tokens - which are termed as cryptocurrencies - to facilitate transactions for their customers. The collection of these financial services using decentralized ledger technology can be denoted by the term decentralized finance (DeFi: Zetzsche, Arner & Buckley 2020; Werner et al., 2021; Grassi et al., 2022; End-note 4).

DeFi applications are bringing many traditional financial utilities - and wealth generation techniques - onto the decentralized realm. The rapid growth of this sector is bound to continue since new blockchain projects will focus on rolling out various products, which become investment opportunities. As newer blockchain platforms develop - and seek financing - investors will look to diversify their risks by spread out their investments across different networks. To continually monitor the risk and return profiles of such a portfolio spread across multiple networks - and tweak the holdings to suit risk preferences based on market conditions - would be an extremely arduous task - almost impossible for non-sophisticated investors (De Bondt 1998; Elton et al., 2009; Fuertes et al., 2014; Torre & Rudd 2004).

The complexity of managing wealth - and risks - across several platforms will give rise to specialized blockchain wealth managers. Such blockchain investment vehicles are actively trying to solve investment problems - more relevant to blockchain - by adapting many best practices from traditional finance for the blockchain realm (Cai 2018; Peterson 2018; Arshadi 2019; Schär 2021; Kareem 2021-II; 2022; Dos Santos et al., 2022). These blockchain-funds will collect money from several investors and invest in several assets across different networks. Decentralized financial services - which are accessible to everyone - providing sophisticated money management to the masses can now become a reality.

A tragic trend in this remarkable technological saga is the narrative of hacks, security vulnerabilities and related exploits - leading to significant loss of funds for several participants. We can broadly categorize the fundamental reasons for blockchain vulnerabilities into three groups: 1) information management issues - related to misuse of passwords, cryptographic keys and abuse of trust; 2) technical issues - server or infrastructure breaches, coding logic or smart contract bugs, cloud platform issues; and 3) economic incentives being misused or flaws in the financial principles used.

Chia et al., 2018; Zamani et al., (2020); Guo & Yu (2022); survey several blockchain security lapses seeking to identify the root cause of these issues, which can provide lessons for other participants to bolster their security. Wang et al., 2021; Werapun et al., (2022) look at how flash loans can be used to steal funds from DeFi protocols. Lee et al., 2022; Uhlig (2022); Briola et al., (2023) is an account of market failure related to the implosion of a DeFi project.

Li et al., (2022); Li et al., (2022) provide a systematic summary of DeFi security incidents and systematically analyze the vulnerabilities. Zhou et al., (2022) construct a DeFi reference frame that categorizes 77 academic papers, 30 audit reports, and 181 incidents, which reveals the differences in how academia and the practitioners’ community defend and inspect incidents - including both attacks and accidents. Wang et al., (2022) propose a deep-learning-based attack detection system to characterize DeFi attacks.

Chaliasos et al., (2023) investigate the effectiveness of automated security tools in identifying vulnerabilities that can lead to attacks. Their findings reveal that automated tools could have prevented a mere 8% of the attacks in which amounts to $149 million out of the $2.3 billion in losses across the 127 attacks they evaluated.

Liu et al., (2022) propose a semi-centralized trust management architcture that can identify and mitigate malicious influences. Liu et al., (2022) propose a blockchain-empowered federated learning framework for healthcare-based cyber physical systems (Pokhrel & Choi 2020; End-note 2). Tian et al., (2019) propose a secure digital evidence framework using blockchain with a loose coupling structure in which the evidence and the evidence information are maintained separately. Liu et al., (2022) propose the design of a blockchain-enabled reputation system - in which the ratings’ privacy is strongly preserved in the processes of transmission and storage - by especially considering the rating privacy issue.

Other than the immediate loss of funds, thefts and security incidents lead to loss of confidence for participants and increase volatility in the markets. Grobys (2021); Chen et al., (2023) investigate hacking incidents in the Bitcoin market and find that the volatility increases significantly. Corbet et al., (2020) find indications that blockchain crime can result in substantial loss of confidence in the cryptocurrency market. Moore & Christin (2013) find that - not surprisingly - the more successful blockchain projects are likely to attract hackers and experience a breach.

Investors are currently wary of putting their trust - and wealth - in the hands of financial intermediaries when they cannot be held fully accountable in an industry that still requires much closer scrutiny and regulation (Guo & Liang 2016; Yeoh 2017; Girasa 2018; Yeung 2019; Shanaev et al., 2020; Yadav et al., 2022). Our innovations will ensure that losses can be attributed - mostly - to oversights - or any fraudulent intentions - of fund representatives who are accepting money from others and hence are taking on fiduciary responsibility. Such accountability - and transparency - will bring greater interest - and involvement - from many who are still on the fringes - or even far away from the reach - of blockchain technology.

2.1 Enter The Safe-House: With An OTNTP (One-Time Next-Time Password)

A common requirement for all blockchain based wealth management protocols will be to utilize the principles of investing to accomplish better risk mitigation. Along with financial risk mitigation, having proper safety mechanisms in place - to prevent thefts and other security incidents - will be extremely crucial requirement. As discussed earlier: several technical enhancements, software architectural designs and elaborate powerful tools are being created to remedy blockchain related security issues. Improved economic incentives and risk mechanisms are being insituted within projects based on an understanding of previous failures. These intricate improvements will no doubt serve to better the infrastructure for blockchain transactions.

What is lacking is a security architecture - and software design - that caters to the fund movement requirements of blockchain wealth management protocols. In this paper we discuss what we consider to be the foremost priority for all organizations engaged in decentralized finance endeavors. What DeFi badly needs is a strengthened security blueprint. DeFi Protocols need to add protective shields against internal theft and external intrusion. The security related features have to be an intrinsic part of the design of distributed applications and deeply embedded within the software architecture.

The innovation we pioneer - focused on blockchain security - is called the Safe-House. The Safe-House is badly needed since there are many ongoing hacks and security concerns in the DeFi space right now. The Safe-House is a piece of engineering sophistication that utilizes existing blockchain principles to bring about greater security when customer assets are moved around. The Safe-House logic is easily implemented as smart contracts on any decentralized system (Wang et al., 2018; Mohanta et al., 2018; Zou et al., 2019; Zheng et al., 2020; End-note 8). The amount of funds at risk from both internal and external parties - and hence the maximum one time loss - is guaranteed to stay within the specified limits based on cryptographic fundamentals.

The Safe-House provides a first level of security that caters to a significant extent the enhanced fund movement needs for today’s DeFi protocols. To improve upon this further, we adapt the one time password - (OTP: Haller et al., 1998; Goyal et al., 2005; M’Raihi et al., 2011; Aravindhan & Karthiga 2013; Erdem & Sandıkkaya 2018; End-note 9) - concept to operate within the constraints of blockchain technology tightly embedded within the working of the safe-house. Well suited to blockchain cryptographic nuances, our secondary advancement, termed the one time next time password (OTNTP) mechanism, is designed to complement the Safe-House making it even more safe. We provide a detailed discussion - including the corresponding mathematical formulations and pointers for technological implementation.

Necessity is the mother of all invention - or creation / innovation - but the often forgotten father is frustration.

The enhanced security features we describe here are - no doubt - very necessary. But the essence of the security innovations we are creating are borne out of the numerous troubles - frustrations - several (all?) protocols are encountering due to unauthorized parties trying to access their funds. The same - frustration being the motivation - could be said about the rest of the investment vehicles discussed in Kasaliya (2022). These innovations are very necessary. But the key motivation for these mechanisms - and architectural designs - are due to the main issues that one encounters while trying to obtain: 1) unencumbered access to decent investment opportunities in the traditional financial world; and 2) peace of mind while investing in crypto assets.

We start with a high level intuitive description of the landscape, the corresponding problems and our solutions. We then supplement this overview with detailed discussions including the corresponding mathematical formulations and pointers for technological implementation.This approach ensures that the article is accessible to a broad audience. We have reviewed around 240 papers spanning both technology and financial topics - artificial as these topical distinctions can be at times, we have strived to ensure that the paper can be useful for both technologists and financial specialists - and linked the insights towards creating a secure wealth management system that can be accessible by everyone.

Incorporating the best practices we have introduced should aid in the wider adoption of blockchain technologies and in particular assuage the concerns of those who are disturbed by the increasing number of crimes in this space. When investors are assured about the safety of their funds, it will provide much needed impetus - in terms of financing, by allowing many superior risk mitigation techniques from traditional finance to be applied to blockchain portfolios - to several upcoming projects by enhancing trust between financial market participants and intermediaries operating in a decentralized environment.

2.2 Outline of the Sections Arranged Inline

Section (2) - which we have already seen - provides an introductory overview emphasizing the importance of information security in decentralized platforms. It summarizes our contributions to increasing DeFi security through the design of a novel software architecture suited for fund movements in the blockchain realm. Section (2.1) - which we have also already seen - summarizes the novel contributions we are making to DeFi wealth management security improvements.

Section (3) gives a high level intuitive description of our innovations to strengthen blockchain security using a novel paradigm we have created - termed the Safe-House - including a discussion of how the Safe-House functions. Section (3.1) gives a summary of the One Time Password (OPT) technique that has become quite prevalent in identity management and fraud prevention. Section (3.2) gives the rationale for why the Safe-House increases safety without sacrificing the efficiency of operation. Section (3.3) gives an intuitive analogy to describe why strengthening security can make DeFi an extremely attractive proposition for participants and providers alike.

A detailed threat assessment model - discussing the risks faced by DeFi protocols and the specific risks that apply to blockchain fund management - is outlined in Section (4). Section (4.1) describes the main components of any blockchain fund management system. Section (4.2) chronicles the various means through which investment funds - with many general concepts applicable outside blockchain, but with various pointers specific to decentralized systems - can face losses and even result in liquidation. Section (4.3) gives a broad set of different approaches to address blockchain fund movement security concerns.

Section (5) is a discussion of the specifics related to the Safe-House - with mathematical formulations and detailed explanations - that can be helpful for actual software implementations. Here we give detailed technical arguments regarding how the threats discussed in Section (4) can be overcome in a robust manner. Section (5.1) gives the architectural diagram for blockchain fund management using the Safe-House and our other innovations. Section (5.2) gives the detailed - step by step - methodology that brings greater security to decentralized investing. Section (5.3) is a formal discussion of the one time next time password (OTNTP) concept that we have advanced to complement the Safe-House. Section (5.4) considers the problem of transferring funds to external yield enhancement protocols and our solution to securely accomplish this goal.

3 The Safe-House: DeFinitely Strengthens DeFi Security Infinitely

In today’s blockchain environment, many protocols are constantly under threat wherein their assets can be taken out or withdrawn by unlicensed external actors. The problem is compounded since internal parties that can access organizational technology assets - for fund management and operational purposes or software development and maintenance - might try to steal funds that are not meant for their use or utilize blockchain resources to devise schemes to dupe investors (Bartoletti et al., 2020; Grobys 2021; Trozze, Kleinberg & Davies 2021; Li et al., 2022; Trozze et al., 2022; Kaur et al., 2023; Wang et al., 2021). Cryptographic methods used in blockchain protocols do provide a certain amount of security. But most projects are still vulnerable either when cryptographic keys - corresponding to fund movements - are compromised or when internal parties - who have access to the keys - have the intention of misappropriating investor funds.

The extent of the perils are magnified in the blockchain environment - since a few parties with malicious intent can reach numerous victims - given the distributed nature of this technology. This adds to the perception that security dangers are commonplace and that hackers are ruling the roost. The many security related incidents stand in the way of the mass adoption of blockchain technology, which otherwise has the potential to transform all human interactions. We wish to do our part to grow this ecosystem by mitigating the harmful influences and restoring the balance of power to groups that are actively trying to develop this landscape.

To counter these hazards, we are introducing several new innovations that will increase the overall defense mechanisms of any blockchain fund management protocol. The novel security innovations - which we are developing - are to ensure that a DeFi investment fund cannot be compromised by either internal or external actors. Our multi-pronged protection scheme refines the existing cryptographic cover by adding extra layers of protective shields. By making these upgrades, we are converting one of the major drawbacks of the DeFi space to one of the major strengths of any protocol.

The central element of our security innovations is the creation of a safe house - which will be guarded by private-public key cryptographic methods (Bernstein & Lange 2017; Kaushik et al., 2017; Puthal et al., 2018; Stephen & Alex 2018; McBee & Wilcox 2020; Pal et al., 2021; End-note 10) - to store all blockchain financial assets. As an additional measure to enhance the security, access to the safe house will be provided only upon verification of the identity of the person requesting the permission. Our identity verification methodology is above and beyond the security provided by existing blockchain public-private key cryptographic methods.

We call our authentication technique the One Time Next Time Password (OTNTP). The OTNTP concept will be used to verify the identity of the portfolio manager - trying to take out funds - and to allow Safe-House access for making withdrawals. Our modified authentication mechanism - OTNTP - should help with password protection in decentralized environments where all transaction information has to be made public for verification purposes.

3.1 Staying on TOP of The OTP (One Time Password)

The OTNTP - the novel technique we advance for blockchain systems - is a modification of the One Time Password (OTP) mechanism. The OTP approach that has become quite prevalent in identity management and fraud prevention. As the name suggests - One Time Passwords - are valid only once. Aravindhan & Karthiga (2013) provide a survey of the OTP mechanism. Using OTPs provides a greater level of security to information systems - that require passwords to gain access - since a new password is needed each time. Information systems that have static passwords - that do not change for prolonged periods - are compromised - guessed or stolen - by increasingly sophisticated hackers.

Originating with the proposal made by Lamport (1981), OTPs have found many use cases for financial activity and identity verification purposes. Several improvements and refinements have been made to the OTP concept. Groza & Petrica (2005) suggest the use of functions on groups of composite integers instead of one way hash functions (Naor & Yung 1989; Merkle 1990; End-note 11; 12). Goyal et al., (2005) suggest a way to reduce client computational requirements - associated with the OTP - without a significant increase in the server computational requirements. M’Raihi et al., (2011) outline a time-based variant of the OTP algorithm that provides short-lived OTP values, which are desirable for enhanced security. Erdem & Sandıkkaya (2018) describe an architecture to outsource the OTP verification to cloud computing platforms, which should ease adoption usage both for users and service providers (Ray 2017; End-note 13).

3.2 Safe-House Safety Without Sacrificing Efficiency

The safe house has also been designed to detect and neutralize dangers such as attempts to withdraw by players without the right credentials. If a real threat is determined, the safe house will go into a locked state. It will not allow anyone to take out any assets or funds from it until the severity of the danger has been assessed and it is deemed safe to resume further operations. It would be helpful to keep a detailed history of all the transactions - facilitated by decentralized ledger technology - linked to specific internal staff responsible for fund movements and trade execution. Needless to say, an extra layer of protection will be provided if the personnel involved in the process are fully KYC’ed (Know Your Customer or Client, or in this case KYE’ed, Know Your Employees: Bilali 2011; Chen 2020; Ostern & Riedel 2021; Malhotra, Saini & Singh 2022; End-note 14).

In the event of an extreme situation - such as a malicious party breaching the safe house - the extent of damage will be limited due to numerous safeguards on the mobility of funds. This scenario can occur if an internal member - or an employee - decides to turn rogue. In such a case, the identity of the person who stole the funds would be established with certainty, due to the incorporation of appropriate identity verification methodologies and the amount lost would be minimal. Even if the missing amount is very small, further action can be taken to recover the lost funds since the identity of the individual - who took the funds - will be known.

While building the new security features mentioned above, the overriding challenge will be to ensure that the improved safety procedures will not become too cumbersome. The objective is to be able to accommodate more security guidelines and yet operate quickly - and effectively - to take advantage of market conditions. This can be accomplished by matching fund flows - which are governed by Safe-House security parameters - to asset management principles and requirements. A detailed discussion of our trade execution related innovations given in Kareem (2021-I) demonstrate that funds movements have to happen in batches - which requires large fund movement requirements to be split into many smaller transfers - since that is the way to minimize trading transaction costs and related issues. To summarize, the result is a system that will protect investor assets and yet allow smooth functioning of the investment machinery.

3.3 Tall Towers and Weak Links

We give an intuitive analogy to describe why strengthening security can make DeFi an extremely attractive proposition for participants and providers alike. This justification appears in the title of the paper.

Any tall tower has to withstand a lot of wind resistance (Nagase, Hisatoku & Yamazaki 1993; Simiu & Scanlan 1996; Deng et al., 2019; Gu 2010; Li et al., 2020). The taller a structure the stronger the wind forces that it has to overcome. Hence, the height of the tall tower becomes its weakest aspect. But if this weakness is addressed properly, and enough safety mechanisms are incorporated in the design, the height of the tower becomes its greatest attraction. People flock to the top to marvel at the views and to admire the accomplishment of having created such a safe and tall structure. Clearly, the importance of having a solid foundation for a tall structure cannot be overlooked.

Likewise, security is the biggest threat - or the weakest link - in DeFi right now. DeFi is nothing but the movement of funds seeking profits. The more the funds move, the greater the security vulnerability. But if the security concerns are adequately addressed - and appropriate features are designed to make DeFi investing more safe - this very weakness can be turned into the greatest attraction. The captivating fascination will then be the generation of significant wealth for all participants. The solid foundation - in our case - is the rigorous risk management that has to be an intrinsic part of the DeFi framework (Kasaliya 2022).

4 Threat Assessment Model for DeFi Wealth Management

4.1 Components of Blockchain Wealth Management Platforms

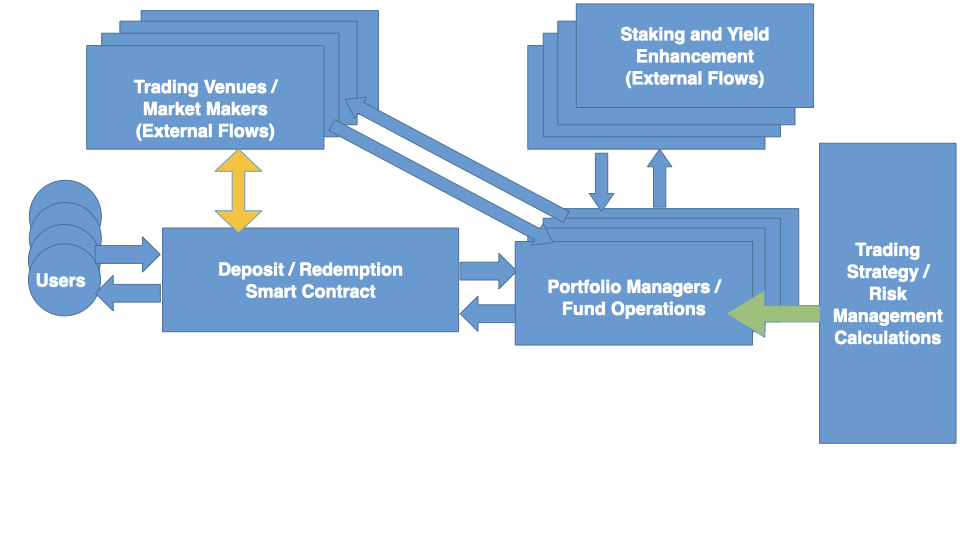

Figure (1) illustrates some common scenarios regarding how fund flows need to happen for wealth management in a decentralized environment. The blue arrows indicate fund flows in Figure (1). We can understand the diagram in Figure (1) by looking at the following components - and steps - of the architecture.

- 1.

-

2.

Similar to Point (1) investors can exit the fund by sending in their fund tokens and getting stable tokens back in exchange. A detailed description of how cryptocurrencies other than stable tokens can be deposited - or redeemed - to participate in - or exit - any investment fund is given in Kasaliya (2022).

-

3.

Investors authorize transactions using a blockchain wallet that manages their keys - and blockchain addresses - to send and receive tokens (He et al., 2018; Karantias 2020; Suratkar et al., 2020; Houy et al., 2023; End-note 17). Deposits and Redemptions happen by interacting with a smart contract - part of the fund infrastructure - that performs the calculations and authentication related to ensuring that tokens transfers happen according to fund prices and investor addresses.

-

4.

The price of the fund - or the exchange rate that determines how many fund tokens will be received in return for the stable tokens deposited - will depend on the holdings within the fund and the current market price of the assets held in the fund. The fund price will change as the portfolio positions are rebalanced to meet risk and return objectives and as the prices of the assets in the portfolio change. The nuances of rebalancing crypto portfolios while responding to risk mitigation needs are discussed in Kareem (2021-I); Kareem (2021-II); Kasaliya (2022).

-

5.

Portfolio managers - and others personnel responsible for operating the fund - use the collected stable coin proceeds to purchase other crypto-assets using Automated Markets Makers or centralized exchanges or other trading venues (End-notes 3b; 6; 5).

Fund personnel will need to have access to the smart contract keys to be able to withdraw funds to buy or sell assets. It would be extremely difficult to put the functionality to interface with external trading venues into the smart contract that collects funds from investors. This tenuous possibility is indicated by the yellow arrow in Figure (1). This issue is due to the difficulty regarding deploying new versions of smart contracts and making changes to blockchain infrastructure (Zou et al., 2019; Chen et al., 2021). If a new trading venue becomes available up - or if any changes are made to the application programming interface (API) of an existing venue - it will require deploying a new version of the smart contracts (Meng et al., 2018; Ofoeda et al., 2019; End-note 7).

It is possible to have an additional smart contract that keeps changing - as the interface to external venues change or a component that changes as the world changes while the rest of the infrastructure can remain relatively unaffected - and connect this external interface smart contract to the smart contract that manages investor deposits, redemptions and holds funds. But even in this case - even if the issue of external connections is resolved with a changing interface - trading personnel will need to be able to access the funds to make the necessary fund movements.

-

6.

The assets held in the portfolio can be utilized towards yield enhancement services to generate additional returns for the fund investors (Xu & Feng 2022; End-note 3). Similar to Point (5), fund personnel need to have the keys to be able access portfolio assets to delegate them to external yield providers.

-

7.

Even though all the transactions happen on the blockchain, a large off-chain software infrastructure - that reads information from the blockchain transaction record - can be useful to provide inputs to portfolio managers - and risk personnel - in terms of trading strategy signals and risk metrics. This receipt of information is indicated by the green arrow in Figure (1).

4.2 Fund Loss Categories

The main - and only - threat for any DeFi protocol is simply the loss of funds. The complications are of course the many ways in which this loss can happen. We initially broadly outline the fundamental reasons for why - and how - funds can be lost. We then zoom into our specific system components and consider the ways an attack can happen.

We can categorize deficiencies in software wealth management - not limited to blockchain alone - that can lead to loss of funds into three categories: 1) Economic Principles; 2) Software Malfunctions; 3) Unlicensed Access.

-

1.

Loss of funds due to limitations in the economic, financial and risk mitigation principles - used to build the corresponding software system - can occur in several ways.

-

(a)

A classic example of this type of catastrophe is the LUNA / UST failure on the Terra protocol (Lee et al., 2022; Uhlig 2022; Briola et al., 2023; End-note 18). The blowup of this network happened due to failure of the arbitrage arguments in the stable coin algorithm - which assume that participants will step in to correct the price of the stable coin using the protocol token when there would be a deviation in the peg of the stable coin (Kereiakes et al., 2019; Brown & Werner 1995; Shleifer, A., & Vishny 1997; End-note 20).

-

(b)

While it is easy to point out such mistakes after they have occurred - perfect vision in hindsight - these anomalies are hard to detect. Even if the designers of the system might be aware of these limitations, such issues are especially obscured from the view of the users - or investors - of the system. The failure of long term capital management is another example when liquidity of the financial instruments - held in the portfolio - dried up leading to a collapse of the fund (Lowenstein 2001; Edwards 1999; Jorion 2000; MacKenzie 2003; End-note 19).

-

(c)

Methods to bolster risk mitigation approaches are outlined in Kasaliya (2022). While the intuition behind the economic concepts can seem straightforward, these issues keep repeating themselves time and again due to several fundamental advancements that are needed in understanding the nature of uncertainty and human decision making (Reinhart & Rogoff 2009; Karbeer 2016). Kashyap (2024) has specific guidelines for risk mitigation in a cryptocurrency setting based on several situations - and corresponding lessons - from traditional wealth management.

-

(a)

-

2.

Software and technical glitches can be a lot more complicated to uncover due to the concealed nature of several system components. The principles of thorough software development, testing and maintenance have to be utilised. For the sake of brevity, we have focused on the central elements of our technique in Section (5). The actual technical implementation will have to cover several specialized scenarios, nuances or other constraints. Additional checks pertaining to division by zero and other such cases need to be considered in the software (End-note 21).

-

(a)

The tools we have outlined in Section (2) should help with identifying blockchain specific code deficiencies. The creation of better software development environments - and utilities - for the blockchain space comparable to other software areas should help immensely - including customized IDEs for blockchain software development (Marchesi et al., 2018; Bosu et al., 2019; End-note 22).

Chakraborty et al., (2018) find that standard software engineering methods including testing and security best practices need to be adapted with more seriousness to address unique characteristics of blockchain and mitigate potential threats. Vacca et al., (2021) present solutions to tackle software engineering-specific challenges related to the development, test, and security assessment of blockchain-oriented software. Qiu et al., (2019) propose a novel cloud-based solution, namely ChainIDE, for the development of blockchain-based smart contracts on multiple kinds of blockchain systems.

-

(b)

Interestingly - but not surprisingly - blockchain systems can be used to improve the software development life-cycle. Yilmaz et al., (2019) consider most software failures as Byzantine failures and propose a test-driven incentive mechanism - based on a blockchain concept - to orchestrate the software development process where production is controlled based on the working principles of blockchain. Farooq et al., (2022) address ways to overcome the major issues of transparency, trust, security, traceability, coordination, and communication in Distributed Agile Software Development (DASD) by utilizing blockchain technology (End-note 23).

-

(c)

Human errors - both, while creating and using the software system - can be considered as a subcategory within this group (Norman 1983; Huang et al., 2012; Huang & Bin 2017).

-

(d)

Logical errors in the software code can also be viewed as falling under this category (Nakashima et al., 1999; Engler et al., 2001; Holzmann 2002). Clearly human errors in designing the system can contribute to bugs in the code.

-

(e)

Losses when transferring funds via blockchain bridges also can be categorized as software related (Belchior et al., 2021; Hafid et al., 2020; Zhou et al., 2020; Stone 2021; Li et al., 2022; End-note 24). Here we are restricting bridge transfer failures to be errors in the functioning of the software that connects different blockchain networks. Many bridge transfer issues happen due to authentication related issues - or failures related to key management - pertaining to the operators of the bridge. The unlicensed access issues we discuss next are limited to the operation of the investment fund alone, without considering unlicensed access to funds - being transferred on a bridge - that are dependent on the keys for operating the bridge getting compromised. Kashyap (2023) gives some suggestions on how to minimize fund transfer needs in the current environment of severe bridge bottlenecks.

-

(a)

-

3.

Zooming into DeFi wealth management, all the funds - assets and tokens in the portfolio - will be maintained on a decentralized system - either a smart contract or wallet - at all times. This provides cryptographic assurance - based on public / private key principles - that no one can take the funds unless they have the keys to access the funds.

Hence, - in addition to the two categories of losses that we have outlined above and even if due care is taken to ensure that proper economic principles and software procedures are used - the most troubling type of losses can occur due to unlicensed withdrawal of funds. This presents a huge risk to blockchain funds - and the growth of decentralized wealth management - wherein the entirely of the funds being managed can be lost.

There are three main types of threats a blockchain investment fund will face in this scenario:

-

(a)

Withdrawal of funds by someone not authorized to access the system. The several ways in which fraudulent activity happens in traditional finance - or other digital arenas - can happen with respect to blockchain systems. This essentially boils down to trying and figuring out someone’s password - or dupe them to reveal it - for any information technology system (Chiew et al., 2018; Alabdan 2020; Desolda et al., 2021; End-note 26).

In the blockchain realm, wallet applications have a password and once that is divulged, the private keys saved in the wallet are compromised (Andryukhin 2019; Pillai et al., 2019; Chen et al., 2020). Barkadehi et al., (2018) identify different types of authentication systems and provide information in terms of how such systems work, their usability and drawbacks. Halgamuge (2022) develops a probabilistic model to estimate the success probability of a malicious attacker. Huang et al., (2011) propose a service to use one-time passwords to prevent password phishing attacks. Kirda & Kruegel (2006); Purkait (2012) discuss how to protect users against phishing attacks. Wu et al., (2020) propose an approach to detect phishing scams on Ethereum by mining its transaction records (End-note 25).

In a blockchain setting, fund personnel can make this excuse that their computer - or other devices - got hacked and the unauthorized withdrawals were a result of the corresponding incident.

-

(b)

Withdrawal of funds by someone who is authorized to access the system, but the amount withdrawn is larger than the amount authorized. As discussed in Section (4.1: Points 5; 6) fund personnel will need to have access to smart contract keys to be able to transfer funds - to trade or participate in yield enhancement platforms. Numerous instances of abuse of authority - violation of risk limits - in extremely fortified financial institutions - despite the many rigorous security procedures that these organizations followed - are documented in Greener (2006); Krawiec (2000; 2009; 2021); Ouriemmi & Gérard (2023). In particular, most funds have strict limits on the size of trades, positions and the corresponding fund flows. There are several well chronicled accounts of employees - turning rogue - having traded several multiples of the dollar values they are authorized to trade, resulting in significant losses and sometimes even causing entire organizational blowups.

-

(c)

Withdrawal of funds by someone who is authorized to access the system, but the time of withdrawal is not when withdrawals are authorized. This happens when personnel - with access to smart contract keys - trade using fund money at other times when their trades are not necessarily the result of official portfolio management objectives - but perhaps to take advantage of some fancy schemes, that have not been approved, the traders or portfolio manager come up with. This is similar to the case discussed above (Point 3b) about withdrawals being larger than permitted limits. Over a period of time, such trades can end up being large positions leading to huge losses for the fund. Several examples are given in the references listed under Point (3b).

-

(a)

4.3 Centralization and Rogue Risk Mitigation: Watching Whales and Wallet Withdrawals

As discussed in Section (4.2), the central fund repository - wallet or smart contract - might get hacked when someone external to the organization either gets access to the keys or figures out a way to steal funds when funds are required to be moved to external venues or yield enhancement platforms by fund personnel. The other possibility is that someone internal to the organization might have turned rogue.

There are two types of legitimate withdrawals that can happen:

-

1.

The first is by someone who has invested money into the investment fund and is withdrawing the tokens that rightfully belongs to them.

Investors can get tricked to revealing their keys as discussed in Section (4.2). Another possibility is that investors can get duped into believing that fake tokens are indeed the authentic tokens issued by the fund - and even entire distributed applications and platforms are real - and hence lose their investment.

Chen et al., (2019) develop a method to automatically detect inconsistent behaviors resulting from tokens deployed in Ethereum by comparing information from three different sources, including the manipulations of core data structures, the actions indicated by standard interfaces, and the behaviors suggested by standard events.Gao et al., (2020) have identified 2, 117 counterfeit tokens that target 94 of the 100 most popular cryptocurrencies by analyzing over 190,000 tokens (or cryptocurrencies) on Ethereum. Zheng et al., (2022) propose a fake-token detection algorithm to identify tokens generated by fake users or fake transactions and analyze their corresponding manipulation behaviors.

Xia et al., (2020) characterize several cryptocurrency exchange scams by identifying over 1,500 scam domains and over 300 fake apps. Fake accounts creating fake transactions to create the aura of authenticity is also a real possibility (Huang et al., 2020; Rabieinejad et al., 2023) including exchanges that fake trading volume to gain greater credibility (Chen et al., 2022). This is despite the possibility that blockchain services can serve to provide reliable methods of detecting and preventing fake documentation - and other digital content such as news - since information is made public and is accessible by anyone (Hammi et al., 2021; Qayyum et al., 2019; Sayed 2019; Fraga-Lamas & Fernandez-Carames 2020).

-

2.

The second type of authorized withdrawal happens when assets are added or removed from the wallet - using the amount invested by investors or to redeem investors - for trading them or to to delegate them to external yield enhancement platforms.

These withdrawals involve interacting with other smart contracts such as: constant market maker liquidity pools (LPs: Xu et al., 2021; Mohan 2022; End-note 3). Centralized exchange APIs might also fall under this category, but it would be helpful to distinguish them from LPs and further technical research should present ways of doing this.

We would like to put in place mechanisms that can mitigate the risk of having one central wallet that holds the invested funds. Any additional security measures need to ensure that the above two categories of legitimate transactions - Points (1; 2) - are not duly inconvenienced. Otherwise, it would be hard to ensure that portfolio management can happen seamlessly on blockchain. Hence, we wish to prevent unauthorized withdrawals without introducing additional constraints - and causing inefficiencies - for participants. We discuss four broad mechanisms below to handle the risk of unauthorized withdrawals.

-

1.

Quite simply we could have multiple wallets storing the portfolio funds. Spreading the funds - and hence the keys - would make it slightly harder for hackers to empty out all the fund storage pools. But, if fund personnel have all the keys - corresponding to different storage wallets or smart contracts - bundled together in the same wallet on the same device, it would take the same amount of efforts for hackers to steal funds in this case. Hence, the drawback in this scenario is that fund personnel need to have different devices - to hold different keys - to manage different storage mediums.

Another related possibility here is for wallet management software to require different password for keys corresponding to different addresses - which would then reduce the need to have multiple devices. But this would still require fund personnel to juggle multiple accounts and passwords. Also, if one device gets compromised it is possible that all the passwords on that device can be leaked and hence it is safer to use multiple computing devices to access multiple accounts.

-

2.

Having a Multiple-Signature wallet - (multi-sig: Bellare & Neven 2007; Aggarwal & Kumar 2021; Han et al., 2021; Zhang et al., 2022; Goel et al., 2023; End-note 27), which requires every withdrawal transaction from the wallet to be signed by multiple parties - will remedy unauthorized withdrawal risk to a great extent. The tradeoff is that it is expensive in terms of the gas fees to have every transaction being signed by many signatories.

This step also slows down the overall system - by creating dependencies on multiple parties - since buying and selling of assets will not happen quickly. Pending fund transfers could get stuck for long time periods when the required signatures are not obtained in a timely manner. This can be extremely costly from a risk management point of view, especially when assets need to be sold depending on negative sentiment that can cause drastic - and rapid - drops in prices. A similar situation affects assets buys and though this does not create losses for the portfolio, it will affect fund returns when timely buy trades are not made.

To remedy the timeliness aspect, we can necessitate that only withdrawals above a certain amount require multi-sign functionality before they are authorized. This is discussed further in Point (4). But clearly this additional check introduces limitations that can be exploited by making multiple smaller withdrawals. This approach would also be highly restrictive in terms of having multiple parties required to periodically check the withdraw queue to perform the necessary approvals.

-

3.

A white list - or an approved safe address list - such that withdrawals can only be made to the addresses on this list can be helpful (Banerjee et al., 2018; Laurent et al., 2018; Alam et al., 2022; End-note 28). Usage of white lists is a common practice in many blockchain systems especially when it comes to issuing new tokens or coins (Feng et al., 2019). The white list scheme is also used in many software systems to detect - and neutralize - phishing attacks (Jain & Gupta 2016; Varshney et al., 2016; Zaimi et al., 2020; Azeez et al., 2021).

Clearly the situation we are concerned with are write transactions - which happen when funds are withdrawn - that change the state of the decentralized ledger as opposed to read transactions which simply check the state of the ledger (Weber et al., 2017; Baliga et al., 2018; Abdella et al., 2021; Thakkar et al., 2018). All smart contracts and addresses - that the fund wallet interacts with - need to be pre-approved and present on the white list. Essentially a smart contract can also be viewed as an address on blockchain. So when a new set of addresses have to be added to the whitelist, multiple signatures are needed to approve their inclusion into the whitelist.

Investor address inclusion in the white list can also be made automatically - without the multi-sign feature - by adding any addresses that deposits money to the fund wallet to the whitelist programmatically. In this case, a rogue could deposit a small amount to get his - her / its - address added to the white list and withdraw a large amount. We articulate one method to handle this issue in Point (4).

In addition a time lock can be added on the white list such that changes to the list cannot be made for a certain number of hours after any new addresses are added or removed (Lai et al., 2021; Bacis et al., 2021; Mohanty & Tripathy 2022; End-note 30). And an additional condition - utilizing time locks - can be that once an address is included, withdrawals cannot be made to that new address until a certain amount of time has elapsed. This is to ensure that hackers cannot get onto the white-list and immediately withdraw funds. If sometime has to be elapse - between inclusion of an address to the whitelist and subsequent withdrawal to that address - and there is more opportunity that the new addresses will get noticed and appropriate action will be taken.

-

4.

We can set rules in the smart contract such that withdrawals from any one address above a certain amount, USD, within a certain time, minutes, will be flagged for greater scrutiny. This additional step - when a transaction is flagged - might be the use of multiple signatures to allow the withdrawal from proceeding further. A clever hacker might withdraw to several addresses and still take a large sum of money within a short span of time.

Hence we need to set a pre condition that the net deposits from an address have to be above a certain amount, USD, otherwise the withdrawal to that address will be flagged for additional scrutiny. Once the total deposits from an address are above USD, then the next condition - withdrawal above a certain amount, USD, within a certain time, minutes - will kick in and select transactions for closer inspection.

Having these rules are also helpful to ensure that the protocol will not suddenly have a bank run type of situation (Uhlig 2010; Calvo 2012; Brown et al., 2017; Dijk 2017; End-note 31). These rules are also helpful to ensure that huge withdraw requests - being watchful of investors holding large positions, also known as whales (Herremans & Low 2022; Manahov 2022; End-note 32) - do not lead to the need to liquidate large portions of the fund rapidly. Such large withdraw requests can cause both existing investors and the exiting investors to suffer losses due to the fall in prices that happen when quick sales are made. Rules for an orderly mechanism to handle outflow requests - and to ensure prices do not collapse abruptly - are detailed further in Kareem (2021-II). Handling both the inflow and outflow of funds with some type of queuing - so that the need to make a lot of trades in a short amount of time is reduced - is beneficial since it reduces implementation shortfall or slippage (Perold 1988; Bertsimas & Lo 1998; Karastilo 2020; End-note 33).

This mechanism can also be provided additional protection by combining it with the white list feature. This would mean that any changes - especially addition of new addresses - to the withdraw white list will require multiple signatures before it can be approved. If an address is not in the white list, no withdraw will happen. Only if an address is in the white list, the additional checks mentioned in this point will kick in providing greater security.

Clearly, several of the above features can be combined in different ways depending on the specifics of the system we are interested in creating. A mechanism that combines features of both multiple signatures and using other rules - including a type of password protection - is described next in Sections (5; 5.3).

5 The Safe-House Safety Combination

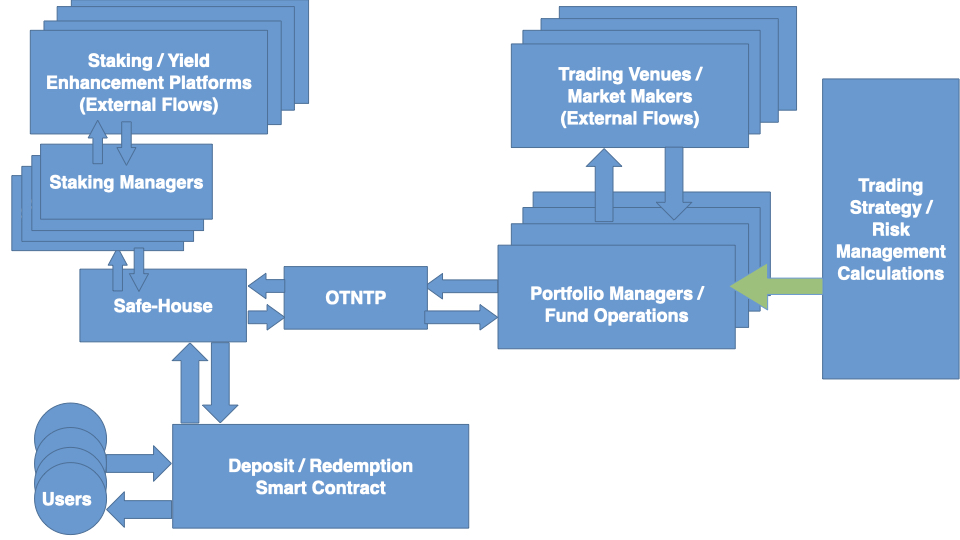

5.1 The Safe-House Architecture

The additional components in Figure (2) - compared to Figure (1) which has the basic components for blockchain wealth management - are briefly described below. Later sections have detailed explanations regarding how each of these additional components function.

-

1.

The safe-house is an additional smart contract that interacts with the smart contract that interfaces with investors to accepts deposits and perform redemptions. The Safe-House enforces additional rules when funds are transferred and this is discussed in detail below.

-

2.

The One-Time-Next-Time-Password (OTNTP) portion - explained in Section (5.3) - sits between the Safe-House and the Portfolio Mangers and performs identity verification.

-

3.

The Staking Manager - which connects to the Safe-House is elaborated in Section (5.4) - will be used to delegate assets to external yield enhancement platforms.

5.2 Multiple Signatures, Encrypted Password Withdrawal and Counter Deposit Criteria

In this section - and later sub-sections - we describe a methodology that brings greater security to the protocol by combining: multiple signature functionality for governance changes, encrypted password authentications for each withdrawal and a counter deposit of equivalent value to be made after each withdrawal - or after withdrawals reach a maximum limit.

Algorithm 1.

The following points - and corresponding steps with explanations - capture the methodology that will be required to significantly enhance the overall security of the overall investment fund using the additional components in Figure (2).

-

1.

The smooth functioning of any strategy will rely on two main roles: Owners and Managers.

-

(a)

Owners are responsible for all aspects of the fund and hence they have the main fiduciary responsibility in terms of accepting money from investors. The owners will own all the smart contracts and also make changes to the key governing parameters. The owners will also make the necessary changes to the governing parameters using multi-sig wallets. An example is given in Point (7). Clearly, the greater the number of owners, the more secure the fund. But the greater the number of owners - and hence the number of signatures needed to make critical changes - the greater the time delays or other corresponding inefficiencies.

-

(b)

Managers will do the day to day operational duties of the fund. Managers will ensure that the smart contracts are operating properly, there are enough funds to redeem investors and also invest the collected funds into various assets. The main tasks and responsibilities of managers are elaborated in Kareem (2021-II). We could have different managers for different strategies - or sub-funds - within the overall fund. The architecture given in Figure (2) can be replicated across the different sub-units to obtain greater security.

-

(a)

-

2.

The main smart contract, , of each strategy will receive funds from investors for investment and it will also redeem investors when they exit the strategy.

-

(a)

The smart contract, , will periodically move all funds received to a safe house, , which could be a wallet address or another smart contract.

-

(b)

The smart contract, , will also take funds from the safe house - or will be sent funds by a manager through the Safe-House or otherwise - , to redeem investors as necessary.

-

(c)

The subscript denotes the state or address of the corresponding component at time when there is no ambiguity.

-

(d)

The state of the at any time will be either or .

-

(a)

-

3.

The manager, , will access funds - stable coins or other tokens - from the , using a password unique to the manager at time .

-

(a)

The password, , will be stored in - or accessible to - the safe house, , in an encrypted manner.

-

(b)

To make a withdraw of funds or assets, , will enter the password, , using an internal only application component or user interface.

-

(c)

When the Safe-House is able to match the entered password to its encrypted counterpart - stored in the Safe-House - only then the Safe-House will open and allow funds to be taken by the manager. The manager will then invest the funds in various assets, which are then sent back directly to the .

-

(d)

A certain nuance that arises here - specific to blockchain and decentralization - is that the password sent to verify the identify of the manager will be recorded as part of the transaction input and stored on the ledger. This is necessary since the input sent to any smart contract function to change the state of the system needs to be stored so that the state change effected by that transaction can be verified by anyone. This being the core requirement of blockchain - so that there is transparency - gives way to the necessity to store the data that effects state changes and make it publicly available. Hence, the password sent by the manager has to be different each time since it will become publicly known after a transaction is validated and the corresponding information becomes public. A simple workaround can achieve the desired result using a scheme we call the One-Time-Next-Time-Password, which is discussed in Section (5.3).

-

(e)

Using the encrypted password protection scheme, it can be verified with certainty who made the withdraw since the password used to make the withdraw will be recorded. Hence if any manager turns rogue, they can be identified and suitable measures can be initiated. To ensure greater security and to prevent the additional costs, hassles and publicity that might come with pursuing a rogue scandal, we can limit the amount of funds or assets that can be taken in any one particular transaction. This also ensures that the maximum damage that can be done by rogue actions is minimized. In this case, we set a maximum amount that can be taken out in one particular withdraw transaction, .

-

(a)

-

4.

In addition, after a withdraw is made for any particular amount - less than the maximum permissible amount - a counter deposit has to be made that is comparable in value to the amount withdrawn, , by the manager at time .

-

(a)

This counter deposit has to be made from time - when the withdraw is made - until a certain time period after time, - that is .

-

(b)

Here denotes a time period measured in seconds. The cumulative value of the counter deposits made during the interval from to is denoted by . Clearly, for simplicity, can be a running time counter starting from time until a later time. The absence of one clock - or a standard time counter - for everyone is a limitation that is still being overcome in the decentralized realm. Even though, getting the same time for everyone is still hard to accomplish for all participants, several alternatives are being pursued. One approach is to use the time to validate blocks or the block-time as a reasonably proxy (Swan 2016; Zhang et al., 2019; Ladleif & Weske 2020; End-note 34).

-

(c)

represents the deposit made at time by address . If the difference between the withdrawal made at time , , and the cumulative value of the counter deposits till a time after , , - is less than a certain threshold, , the safe house will remain closed for all further withdraws. The is best represented as a percentage figure and converted to a notional value by multiplication with the withdraw amounts. Once the Safe-House is closed after a withdraw and the necessary amount of counter deposits have not been received - to open it again - intervention by the owners of the Safe-House using multiple signatures will be required.

-

(d)

It needs to be ensured that the withdraws made by the smart contract, , to redeem investors are not counted. Hence the withdraws that matter are the ones from addresses other than the . Clearly withdraws from addresses that hold the manager - or owner - role are the only ones that will be allowed to access the . It also needs to be checked that the counter deposits are not funds received from investors through the smart contract, . Hence the counter deposits have to be received from addresses other than the . This feature can also be implemented by having different functions in the Safe-House to interact with investors and managers.

-

(a)

-

5.

All of the above conditions are captured - using the notation developed thus far in Point (4) - more formally below:

Criterion 1.

The following inequalities and equations encapsulate the essence of the Safe-House,

(1) The Safe-House state will be closed, , after a withdraw at time as long the following condition holds,

(2) (3) Note that with a slight abuse of notation, we do not include a separate summation across all the managers and owners represented by the indices .

-

6.

Criterion 2.

A simpler alternative to the above - Criterion (5) - would be to view withdraws as being allowed up to a certain maximum limit.

-

•

When a withdraw a made, we deduct from the maximum limit and when a deposit is made we add to the maximum limit. The maximum limit will be the amount, .

-

•

The sum of the deposits can be less than the withdraws by a certain tolerance amount. The tolerance amount is obtained by using the - which is best represented as a percentage figure - and converting the percentage figure to a notional value by multiplication with the withdraw amounts.

-

•

We define a starting time to be when the safe house is opened for the first time after being closed.Hence the difference of the cumulative withdraws and deposits from any starting time, to any future time, has to be lesser than the maximum limit adjusted by the tolerance amount. Clearly we can start the counters from the time the safe house is established and opened for business, so that

-

•

A starting time is when the safe house is opened for the first time after being closed. The Safe-House state will stay open, , after a starting time, until the time, , as long the following condition holds,

(4) -

•

Note that with a slightly abuse of notation, we do not include a separate summation across all the managers and owners represented by the indices .

-

•

-

7.

Any changes to the governance parameters - or strategic parameters - will require authentication with multiple signatures from multiple parties - or owners. Examples for this are:

Condition 1.

To set someone with a manager role. Once someone has been given a manager role, they need to set a password for themselves in the safe-house and confirm it again.

Condition 2.

To revoke someone from a manager role, any of the multiple signature owners can do it without approval from others. This is to ensure timely intervention when necessary.

Condition 3.

To change parameters such as the , and . We outline some guidelines for setting these variables.

-

•

The will be related to the slippage tolerance discussed in Kareem (2021-II).

-

•

An insurance - or risk reserve - will be maintained as part of the fund treasury to finance various risk limits. The will need to be set as part of this risk reserve.

-

•

The will depend on how long the off chain risk and portfolio management infrastructure - scripts and other calculations with trader / portfolio manager oversight - take to complete.

Condition 4.

There are many other operational parameters that the manager might need to be able to update at times. These are related to various fees the fund needs to collects when deposits and redemptions happen (Kareem 2021-II). It is very important to be able to distinguish between governance and operational parameters and decide who - managers or owners - has responsibility to change those. If necessary, a detailed discussion of operational tasks - and related parameters - is available separately in Kareem (2021-II).

-

•

-

8.

The critical aspect with the counter deposit criteria is the verification of the value of the counter deposits, .

-

(a)

The counter deposit has to be made using only assets that have been included in a pre-approved list. This is to ensure that counter deposits are made with assets that satisfy due diligence requirements - as mandated by the fund strategies - and the Safe-House cannot be simply stuffed with junk assets to satisfy the corresponding criteria. The pre-approved list of assets can be the list of assets included in the portfolio of the corresponding strategy.

-

(b)

A very reliable price provider has to be used for the counter deposit value calculations. Oracles are a solution for smart contracts to obtain inputs from the outside world (Beniiche 2020; Pasdar et al., 2021; Lys & Potop-Butucaru 2022; Pierro et al., 2020; 2022; Caldarelli 2022; Pasdar et al., 2023). Price oracles on several platforms aggregate prices from various sources and provide values that cannot be easily manipulated (End-note 35). That said, oracle price related hacks are possible attack vectors in DeFi (Al-Breiki et al., 2020; Caldarelli 2020; Oosthoek 2021; Caldarelli & Ellul 2021) and hence this particular component needs additional attention when the systems are running.

-

(c)

A safety measure involves setting a reference price for each asset in the Safe-House. When withdraws - or deposits - are being made using external prices that are significantly different from this reference price, movement of those assets can be frozen until someone can investigate this matter further. The reference price should only be updated by owners and this is another example of a governance parameter. The list of approved assets and their latest reference price must be reviewed regularly - daily or even multiple times a day - by portfolio managers, risk personnel and even the owners of the fund.

Criterion 3.

Using this condition the deposit made to the Safe-House can be written as

(5) Here is the number of assets approved for manager - or owner - , . and represent the asset price and asset quantity being deposited into the Safe-House at time . Note that with a slight abuse of notation, we do not include a separate summation across all the managers and owners represented by the indices . This summation of deposits across all owners and managers gives the total counter deposit value, .

Criterion 4.

Withdraws can also be represented using a similar condition,

(6) -

(d)

Portfolio assets will be staked in various farms, pools or yield generating devices. The confirmation for staking in any farm or pool - which are usually liquidity pool (LP) tokens - can be sent to the . The verification of value of these LP tokens can be a challenge, but are being done currently by many tools - such as Nansen.AI (Moro-Visconti et al., 2023; Zhu et al., 2023; End-note 40) - across various networks.

The value of the LP tokens can also be obtained from the yield enhancement platform itself by invoking suitable functions- since essentially the automated market maker can provide a reference price. But changes to the API will involve quite a bit of maintenance for the fund technologists. Also it is easy to manipulate the price of a single market maker.

The discussion in Section (5.4) - using the Staking Manager - is an alternative to do yield enhancement that bypasses the withdraw and counter-deposit criteria. This would mean that LP tokens as confirmation for staking will be sent directly to - and from - the Safe-House without having to go through the withdraw - and deposit - aggregation.

-

(e)

The Safe-House contracts have been successfully deployed for commercial use on multiple platforms - Ethereum, Binance and Polygon - and hundreds of transactions have been performed without any issues. The use of price oracles for counter deposit value verification - including the use of a default reference price - has also been tested satisfactorily.

-

(a)

5.3 OTNTP: The One-Time-Next-Time-Password

The One-Time-Next-Time-Password (OTNTP) concept will be used to verify the identity of the manager and to allow Safe-House access for making withdrawals. It is important to note that the OTNPT is an additional layer or protection and is not a substitute for the private keys being used by fund personnel. This modified OTNPT scheme should help with password protection in decentralized environments where all transaction information has to be made public for verification purposes.

The internal application or component that will be used to access funds from the Safe-House, , will be called the administrative GUI (Graphical User Interface) or admin GUI for short. To access this internal application - which will perform various investment duties by interacting with the various smart contracts including the Safe-House, - another administration password will be required. We refer to this password for the admin GUI as the admin password.

We denote the admin password for manager at time , , as, . The One-Time-Next-Time-Password for manager at time will be denoted as .

Algorithm 2.

The main steps to implement The One-Time-Next-Time-Password (OTNTP) are:

-

1.

To access the funds - or assets - in the Safe-House, , the using the admin GUI will need to send the raw form or plain text version of the CURRENT One-Time-Next-Time-Password corresponding to him, that is needed for the current access.

-

(a)

When sending the raw form of the current , the admin GUI of the will create the NEXT One-Time-Next-Time-Password, , encrypt it and send it to the Safe-House, .

-

(b)

The encrypted form of will be saved in the Safe-House so that it can be used to access the Safe-House, the next time by the .

-

(a)

-

2.

The raw form of the next One-Time-Next-Time-Password, can be saved on the computing device of the manager, in a protected file, .

-

(a)

The password to access the contents of the protected file, is the for manager, .

-

(b)

Clearly, the can also be stored on external devices inside password protected files and access to this protected file, will require knowing the for manager, .

-

(c)

Hence, even if the wallet of the gets hacked, without knowing the or the of the manager access to the for withdrawals is not possible.

-

(a)

-

3.

The One-Time-Next-Time-Password, , can simply be a random number of sufficient length so that the number of tries for someone trying to force access to the is probabilistically very small.

-

(a)

This also means that after a few number of wrong attempts using the incorrect One-Time-Next-Time-Password, , the will go into the state for everyone.

-

(b)

Further intervention will be necessary from the owners using multi-sign transactions to restore the state of for normal operation and to be able to go back to the state.

-

(c)

Having non-numeric characters is helpful to decrease the probability of someone guessing the password.

-

(a)

-

4.

The scenario we have discussed above is for the regular operation of the using the One-Time-Next-Time-Password, or for system when it has been operational for sometime.

-

(a)

To start the operation of the system, the owners will need to seed the encrypted form of the into the .

-

(b)

A simpler and more practical alternative would be for the manager himself to seed the with the encrypted version of the first One-Time-Next-Time-Password, and then use this for the first withdrawal that follows.

-

(c)

When the manager will seed the Safe-House for the first time, multiple signature verification can also be enforced for increased security.

-

(d)

The same seeding mechanism can be used to restore the state of for normal operation and to be able to go back to the state, after it gets due to multiple incorrect attempts.

-

(a)

-

5.

To obtain access to the would require gaining control of the wallet of the manager and also hack his computing device - and knowing his - to obtain the contents of the - which is the OTNTP.

-

(a)

This OTNTP feature combined with the counter deposit requirement ensures that the effort to compromise the is significant in comparison to the reward that can be obtained - which is the maximum amount that can be taken from the Safe-House, without counter deposit verification. To steal assets above the maximum Safe-House amount will require a lot of additional resources to manipulate price oracles or other price feeds.

-

(a)

5.4 The Staking Manager: Yield Enhancement Through Third Party Delegation of Assets

If we need to delegate assets from the Safe-House to third party yield enhancement platforms, we will need a Staking Manager (SM) contract. The main purpose of the SM is to handle the specifics of token management with respect to the protocol - or DeFi platform - that is being used for the yield enhancement. The reason for having a separate SM is because third party platforms change their smart contract versions through which they provide yield enhancement services.

In addition, we will be seeking new yield enhancement platforms as and when they arise. When such external interface changes are necessary, we eliminate the need to modify and re-deploy the Safe-House. This becomes possible since the SM contract can be modified to deal with the changes and it can be deployed again and connected to the Safe-House. Hence the SM will change as the external world changes but its connection to the fund - that is to the Safe-House - will remain the same. By linking different SMs that provide these external connections we can retain the same Safe-House without any changes to it.

For now, we will consider the following three types of yield enhancement services (Kiong 2021; Xu & Feng 2022; Cousaert, Xu & Matsui 2022; End-note 3): AMM Liquidity Pairs (AMM LPs), LP Token Staking and Single Sided Staking. Other types of yield generation protocols can be handled in a similar manner (End-notes 41; 42; 43). Examples of Single sided staking are CAKE and BSW. Examples of AMM LPs are ETH-LINK, SOL-ETH on Uniswap and ADA-BNB, DOT-BNB on Pancake swap (End-notes 38; 39). Once we deposit the two tokens corresponding to an AMM LP pair, we get the relevant LP token. This LP token can then be staked in the corresponding staking pool to earn the platform rewards such as Pancake swap tokens.

The Safe-House needs to have the following functions which can be invoked for any asset or pair of assets. The following functions can also support more than two assets by designing the function interface such that an array of assets can be passed to the function as an input. The quantity - or number of tokens - also needs to be passed along. Along with the list of assets and quantities, an instruction ID will have to be passed to the function being invoked in the Safe-House. The instruction ID can be an integer. The functions needed in the Safe-House are:

-

1.

Add Liquidity

-

2.

Remove Liquidity

-

3.

Stake

-

4.

Un-Stake

-

5.

Claim Rewards