Disaggregating Time-Series with Many Indicators: An Overview of the DisaggregateTS Package

Abstract

Low-frequency time-series (e.g., quarterly data) are often treated as benchmarks for interpolating to higher frequencies, since they generally exhibit greater precision and accuracy in contrast to their high-frequency counterparts (e.g., monthly data) reported by governmental bodies. An array of regression-based methods have been proposed in the literature which aim to estimate a target high-frequency series using higher frequency indicators. However, in the era of big data and with the prevalence of large volume of administrative data-sources there is a need to extend traditional methods to work in high-dimensional settings, i.e. where the number of indicators is similar or larger than the number of low-frequency samples. The package DisaggregateTS includes both classical regressions-based disaggregation methods alongside recent extensions to high-dimensional settings, c.f. Mosley et al., (2022). This paper provides guidance on how to implement these methods via the package in R, and demonstrates their use in an application to disaggregating CO2 emissions.

1 Introduction

Economic and administrative data, such as recorded surveys and consensus, are often disseminated by international governmental agencies at low or inconsistent frequencies, or irregularly-spaced intervals. To aid the forecasting of the evolution of the dynamics of these macroeconomic and socioeconomic indicators, as well as their comparison with higher resolution indicators provided by international agencies, statistical agencies rely on signal extraction, interpolation and temporal distribution adjustments of the low-frequency data to provide high precision and uninterrupted historical data. Although, temporal distribution, interpolation and benchmarking are closely associated with one another, this article and its respective package (DisaggregateTS), expend particular attention to interpolation and temporal distribution (disaggregation) techniques, where the latter is predicated on regression-based methods111See Dagum and Cholette, (2006) for an overview of benchmarking, interpolation, temporal distribution and calendarization techniques.. These regression-based temporal distribution techniques rely on high-frequency indicators to estimate (relatively) accurate high-frequency data points. With the prevalence of large volume of high-frequency administrative data, a great body of literature pertaining to statistical and machine learning methods has been dedicated to taking advantage of these additional resources for forecasting purposes (see Fuleky, (2019) for an overview of macroeconomic forecasting in the presence of big data). Additionally, one may wish to utilize these abundant indicators to generate high-frequency estimates of low-frequency time-series with greater precision. However, in high-dimensional linear regression models where the number of dimensions surpass that of the observations, consistent estimates of the parameters is not possible without imposing additional structure (see Wainwright, (2019)). Hence, this article and the package DisaggregateTS adapt recent contributions in high-dimensional temporal disaggregation (see Mosley et al., (2022)) to extend previous work within this domain (see the package Sax et al., (2016) and its corresponding article Sax and Steiner, (2013)) to high-dimensional settings.

As noted by Dagum and Cholette, (2006), time-series data reported by most governmental and administrative agencies tend to be of low-frequency and precise, but not particularly timely, whereas their high-frequency counterparts seldom uphold the same degree of precision.The aim of temporal distribution techniques is to generate high-frequency estimates that can track shorter term movements, than directly observable with the direct low-frequency observations. While interpolation problems are generally encountered in the context of stock series, where say, the quarterly value of the low-frequency series must coincide with the value of third month of the high-frequency data (of the same quarter), temporal distribution problems often concern flow series, where instead the value of the low-frequency quarterly series must agree with the sum (or weighted combination) of the values of the high-frequency months in that quarter. The latter approach is generally accomplished by identifying and taking advantage of a number of high-frequency indicators which are deemed to behave in a similar manner to the low-frequency series, and by estimating the high-frequency series through a linear combination of such indicators.

In the last few decades, a significant number of articles have been published within this domain—see Dagum and Cholette, (2006) for a detailed review of these techniques. Notable studies within this context include the additive regression-based benchmarking methods of Denton, (1971) and Chow and Lin, (1971, 1976), as well as those proposed by Fernandez, (1981) and Litterman, (1983) in the presence of highly persistent error processes. More recently these methods have been extended to the high-dimensional setting by Mosley et al., (2022), where prior information on the structure on the linear regression model is used to enable estimation, and better condition the regression problem. Specifically, this is accomplished by “least absolute shrinkage and selection operator” (LASSO hereafter) proposed by Tibshirani, (1996), which in principle selects an appropriate model by penalizing the coefficients (in scale) of the high-dimensional regression, in effect discarding the irrelevant indicators from the model. In what follows, we demonstrate how to apply these methods using DisaggregateTS to easily estimate high-frequency series of interest.

The remainder of the paper is organized as follows: Section 2 introduces the methodologies underlining noteworthy temporal disaggregation techniques that have been included in the DisaggregateTS package, as well as their extensions to high-dimensional settings. Section 3 introduces the DisaggregateTS package and some of its useful functions. Moreover, examples predicated both on simulations (using a function provided in the package that generates synthetic data) and empirical data are explored to familiarize the reader with the package and its functionality. Finally, the paper is concluded in Section 4.

2 Sparse temporal disaggregation

2.1 Classical regression-based techniques

Suppose we observe a low-frequency series, say, quarterly GDP, encoded as the vector , containing quarterly observations. We desire to disaggregate this series to higher frequencies (say monthly), where the disaggregated series is denoted , with . Furthermore, we wish that the disaggregated series be temporally consistent without exhibiting any jumps between quarters (see Section 3.4 of Dagum and Cholette, (2006) for examples of such inconsistencies between the periods). The challenge is to identify an approach that distributes the variation between each observed quarterly point to the monthly level. A method that has been extensively studied in the literature concerns finding high-frequency (e.g., monthly) indicator series that are thought to exhibit similar inter-quarterly movements as the low-frequency variable of interest. Let us denote a set of observations from these indicators as the matrix . A classical approach to provide high-frequency estimates is the regression-based temporal disaggregation technique proposed by Chow and Lin, (1971) whereby the unobserved monthly series are assumed to follow the regression:

| (2.1) |

where is a vector of regression coefficients to be estimated (noting that may contain deterministic terms) and is a vector of residuals. Chow and Lin, (1971) assume that follows as AR(1) process of the form with and . The assumption of stationary residuals allows for a cointegrating relationship between and when they are integrated of the same order. Thus, the covariance matrix has a well-known Toeplitz structure as follows:

| (2.2) |

where and are unknown parameters that need to be estimated. The dependent variable in (2.1) is unobserved, hence the regression is premultiplied by the aggregation matrix , where:

| (2.3) | ||||

where the vector of ones in (2.3) is used for flow data (e.g., GDP), such that the sum of the monthly GDPs coincides with its quarterly counterpart222For alternative aggregations see Quilis, (2018) and Sax et al., (2016). For instance, if quarterly values correspond to averages of monthly values, then the vector in equation (2.3) assumes the form .. The premultiplication yields the quarterly counterpart of (2.1):

| (2.4) |

The GLS estimator for is thus expressed as follows:

| (2.5) | ||||

| (2.6) |

where , and . Note that estimating requires the knowledge of the unknown parameters and in which are unknown. We employ the profile-likelihood maximization technique of Bournay and Laroque, (1979) which entails first estimating and and subsequently conducting a grid-search over the range for the autoregressive parameter. Chow and Lin, (1976) show the optimal solution is obtained by:

| (2.7) |

where is the conditional expectation of given and the estimate of the monthly residuals are obtained by disaggregating the quarterly residuals to attain temporal consistency between and .

Other variants of the regression-based techniques include those proposed by Denton, (1971), Dagum and Cholette, (2006), Fernandez, (1981) and Litterman, (1983). The latter two consider scenarios where and are not cointegrated. Although, these traditional techniques are included in the DisaggregateTS package, for an overview of different temporal disaggregarion techniques and distribution matrices, we divert the attention of the reader to Table 2 in Sax and Steiner, (2013).

2.2 Extension to high-dimensional settings

The shortcoming of Chow and Lin, (1971) becomes evident in data-rich environments, where the number of indicators surpass that of the time-stamps for the low-frequency data. Let us once again recall the GLS estimator (2.6). When and the columns of are independent, the estimator is well-defined. However, when , the matrix is rank-deficient - i.e., , the matrix has linearly dependent columns, and thus is not invertible. In moderate dimensions, where , has eigenvalues close to zero, leading to high variance estimates of . Mosley et al., (2022) resolve this problem by adding a regularising penalty (e.g., regulariser) onto the GLS cost function (2.5):

| (2.8) |

Unlike the GLS estimator (2.6), the regularised estimator corresponding to the cost function (2.8) is a function of and the autoregressive parameter . Henceforth, it is important to nominate the most suitable and to correctly recover the parameters. In (2.8), we denote the estimator as to highlight that the solution paths of the estimator for different values of , say, are generated for (i.e. conditional on) a fixed . The solution paths are obtained using the LARS algorithm proposed Efron et al., (2004), the benefits of which have been extensively discussed in Mosley et al., (2022).

LASSO estimators inherently exhibit a small bias, such that , where denotes the true coefficient vector. To alleviate this issue, Mosley et al., (2022) further follow Belloni and Chernozhukov, (2013), by performing a refitting procedure using least squares re-estimation. The latter entails generating a new sub-matrix , where from the original matrix , with corresponding to the columns of supported by , for solutions obtained from the LARS algorithm333noting the LARS algorithm produces solutions evaluated at a series of points.. We then perform a usual least squares estimation on to obtain debiased solution paths for each .

Finally, Mosley et al., (2022) choose the optimal estimate from using the Bayesian Information Criterion (BIC hereafter) proposed by Schwarz, (1978). The motivation for nominating this statistic over resampling methods, such as cross-validation or bootstrapping techniques, stems from the small sample size in the low frequency observations. The optimal regularisation is chosen conditional on according to

| (2.9) |

where is the degrees of freedom and is the log-likelihood function of the GLS regression (2.6),

which in the presence of Gaussian errors, is given by:

| (2.10) |

where is the determinant of the Toeplitz matrix depending on , such that .

3 The “DisaggregateTS” package

In this Section, we showcase the main functions that has been included in the DisaggregateTS package. Following Sax et al., (2016), we first introduce the main function of the package and it its features, and subsequently we will showcase other functions that allow the practitioner to conducting simulations and analyses.

3.1 Functions

The main function of the package which performs the sparse temporal disaggregation method proposed by Mosley et al., (2022) is disaggregate(). This function is of the following form:

> disaggregate(Y, X, aggMat, aggRatio, method, ...) where the first argument of the function, Y, corresponds to the vector of low-frequency series that we wish to disaggregate, and the second argument, X, is the matrix of high-frequency indicator series . In the event that there is no input X, the disaggregation matrix is replaced with an vector of ones.

The argument aggMat coincides with the aggregation matrix in (2.3), and it has been set to "sum" by default, rendering it suitable for flow data. Alternative options include "first", "last" and "average". The aggregation (distribution) matrices that are utilised in this function are summarized in table 2 of Sax et al., (2016). The argument aggRatio has been set to 4 by default, which represents the ratio of annual to quarterly data. In general, this argument should be set to the ratio of the high-frequency to low-frequency series. For instance, in the examples considered in the preceding Sections, we had considered quarterly data as the low-frequency series, and monthly data as its high-frequency counterpart. Thus, in this setting aggRatio = 3. At first glance, the presence of the aggRatio argument may seem redundant. However, if , then extrapolation is done up to .

Finally, the argument method refers to the method of disaggregation under consideration. This argument has been set to "Chow-lin" method by default, which is the classical regression-based disaggregation technique introduced in Section 2.1. Other classical low-dimensional options include "Denton", "Denton-Cholette", "Fernandez", and "litterman", where these techniques have been extensively discussed in Dagum and Cholette, (2006) and Sax and Steiner, (2013). The main contribution of this package stem from the "spTD" and "adaptive-spTD" options pertaining to sparse temporal disaggregation and adaptive sparse temporal disaggregation, which are Mosley et al., (2022)’s high-dimensional extension of the regression-based techniques proposed by Chow and Lin, (1971). In a high-dimensional regression, the adaptive LASSO is relevant when, for instance, the columns of the design matrix exhibit multicollinearity, and the Irrepresentability Condition (IC hereafter) is violated (see Zou, (2006) for details). In such settings, the regularization parameter does not satisfy the oracle property, which can lead to inconsistent variable selection. The adaptive counterpart of the the regularized GLS cost function (2.8), can be expressed as follows:

| (3.1) |

where is an initial estimator, predicated on from the regularized (LASSO) temporal disaggregation. See Mosley et al., (2022), for the details of the proposed methodology, and Zou, (2006) and Van de Geer et al., (2011) to yield variable selection consistency using the OLS estimator and LASSO as when the IC condition is violated.

The second main function of the “DisaggregateTS” package is TempDisaggDGP(), which generates synthetic data that can be used for conducting simulations using the disaggregate() function. The main arguments of this function are as follows:

> TempDisaggDGP(n_l, n, aggRatio, p, beta, sparsity, method, aggMat, rho, ...) where the first argument corresponds to the size of low-frequency series and n to that of the high-frequency series. Moreover, aggRatio and aggMat are defined as before, in turn representing the ratio of the high-frequency to low-frequency series, as well as the aggregation matrix (2.3). A minor difference in the DGP function is that if , then the last columns of the aggregation matrix are set to zero, such that is observed only up to . Argument p sets the dimensionality of high-frequency series (set to by default), beta which has been set to by default is the positive and negative elements of the coefficient vector, sparsity is the sparsity percentage of the coefficient vector, and rho is the autocorrelation of the error terms, which has been set to by default. Finally, the method argument determines the data generating process of the error terms, corresponding to methods discussed earlier in this Section.

A number of optional arguments included in the function determine the mean vector and the standard deviation of the design matrix, as well as options such a setting seed for running the simulations, where the design matrix and the coefficient vectors are fixed.

In what follows, we showcase a simple example of the function and its respective outputs:

> # Load the DisaggregateTS library> library(DisaggregateTS)> # Generate low-frequency quarterly series and its high-frequency monthly counterpart> SynthethicData <- TempDisaggDGP(n_l = 2, n = 6, aggRatio = 3,+ p = 6, beta = 0.5, sparsity = 0.5, method = ’Chow-Lin’, rho = 0.5) In the example above, we generate low-frequency series corresponding to two quarters, and consequently, its high-frequency monthly counterpart . It is further assumed that the data is generated using six monthly indicators - i.e., , with a coefficient vector , where . Since, the sparsity argument is set to , only half of ’s elements are non-zero. Finally, the error vector is assumed to follow the structure AR() structure of Chow and Lin, (1971), with an autocorrelation parameter of .

3.2 Simulations

In this Section, we show a simulation exercise to demonstrate the implementation of the temporal disaggregation method via the DisaggregateTS package.

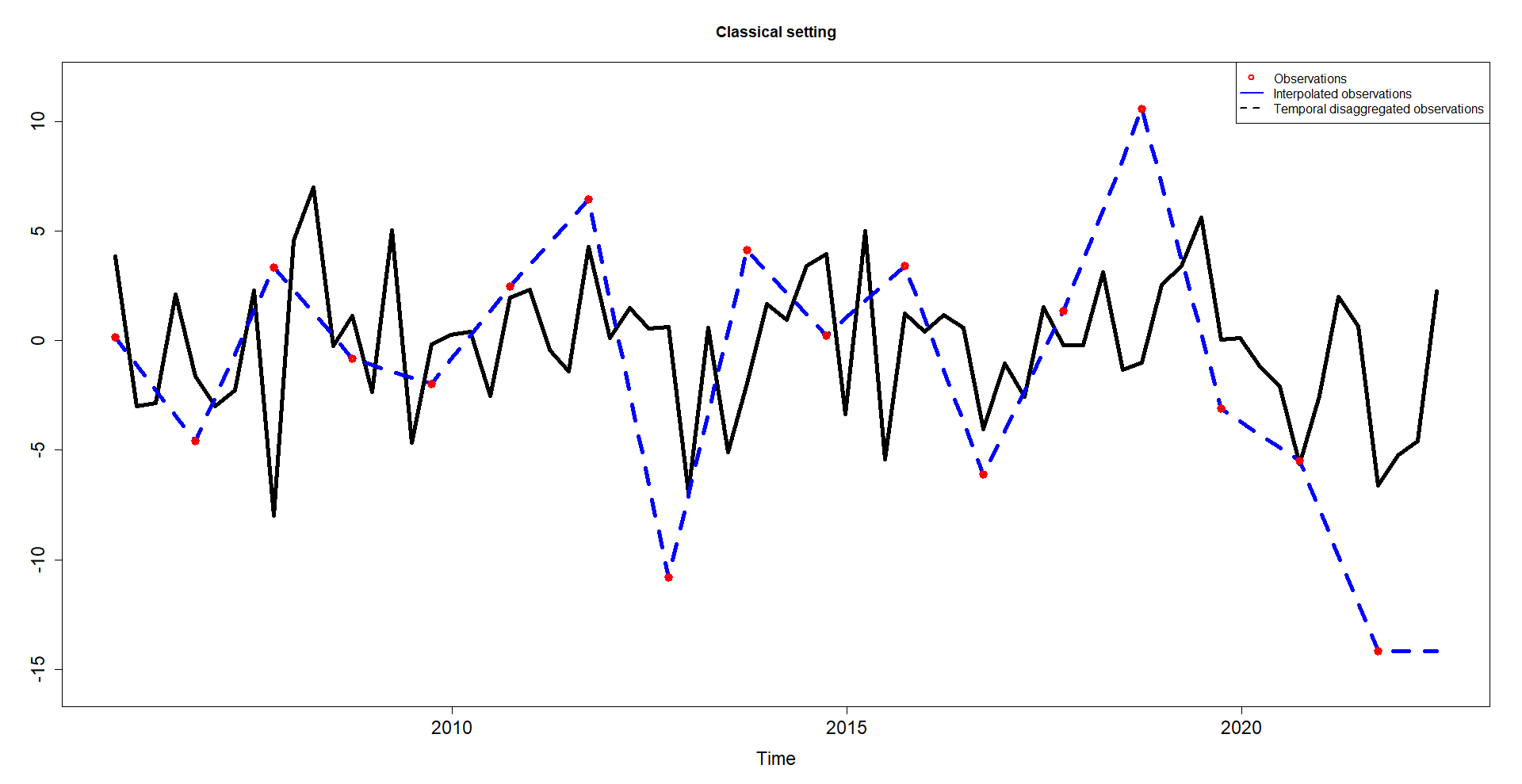

Classic setting

We start by simulating the dependent variable and the set of high-frequency exogenous variables by using the command:

> # Load the DisaggregateTS library> library(DisaggregateTS)> # Generate low-frequency yearly series and its high-frequency quarterly counterpart> n_l = 17 # The number of low-frequency data points> - annual> n = 68 # The number of high-frequency (quarterly) data points.> p_sim = 5 # The number of the high-frequency exogenous variables.> rho_sim = 0.8 # autocorrelation parameter> Sim_data <- TempDisaggDGP(n_l, n, aggRatio = 4, p = p_sim, rho = rho_sim)> Y_sim <- matrix(Sim_data$Y_Gen) # Extract the simulated dependent low-frequency variable> X_sim <- Sim_data$X_Gen # Extract the simulated exogenous high-frequency variables

In this example, we are generating a set of low-frequency data, i.e. 17 annual datapoints and a set of high-frequency (quarterly) exogenous variables that we want to use to infer the high-frequency counterpart of the low-frequency data. We now want to temporally disaggregate the low-frequency time series by using the information encapsulated in the high-frequency time series. In this case, since the number of time observations is larger than the number of exogenous variables, we can use standard methodologies to estimate the temporal disaggregation model. To do so, we use the disaggregate function setting method="Chow-Lin". The code is as follows:

> C_sparse_SIM <- disaggregate(Y_sim, X_sim, aggMat = "sum",+ aggRatio = 4, method = "Chow-Lin")> C_sparse_SIM$beta_Est> Y_HF_SIM = C_sparse_SIM$y_Est[ ,1] # Extract the temporal disaggregated> # dependent variable estimated through the function disaggregate()

We show in Figure 3 the results, where we depict the original (low-frequency) time series together with the high-frequency counterpart computed via standard interpolation and estimated through the Chow-Lin temporal disaggregation method.

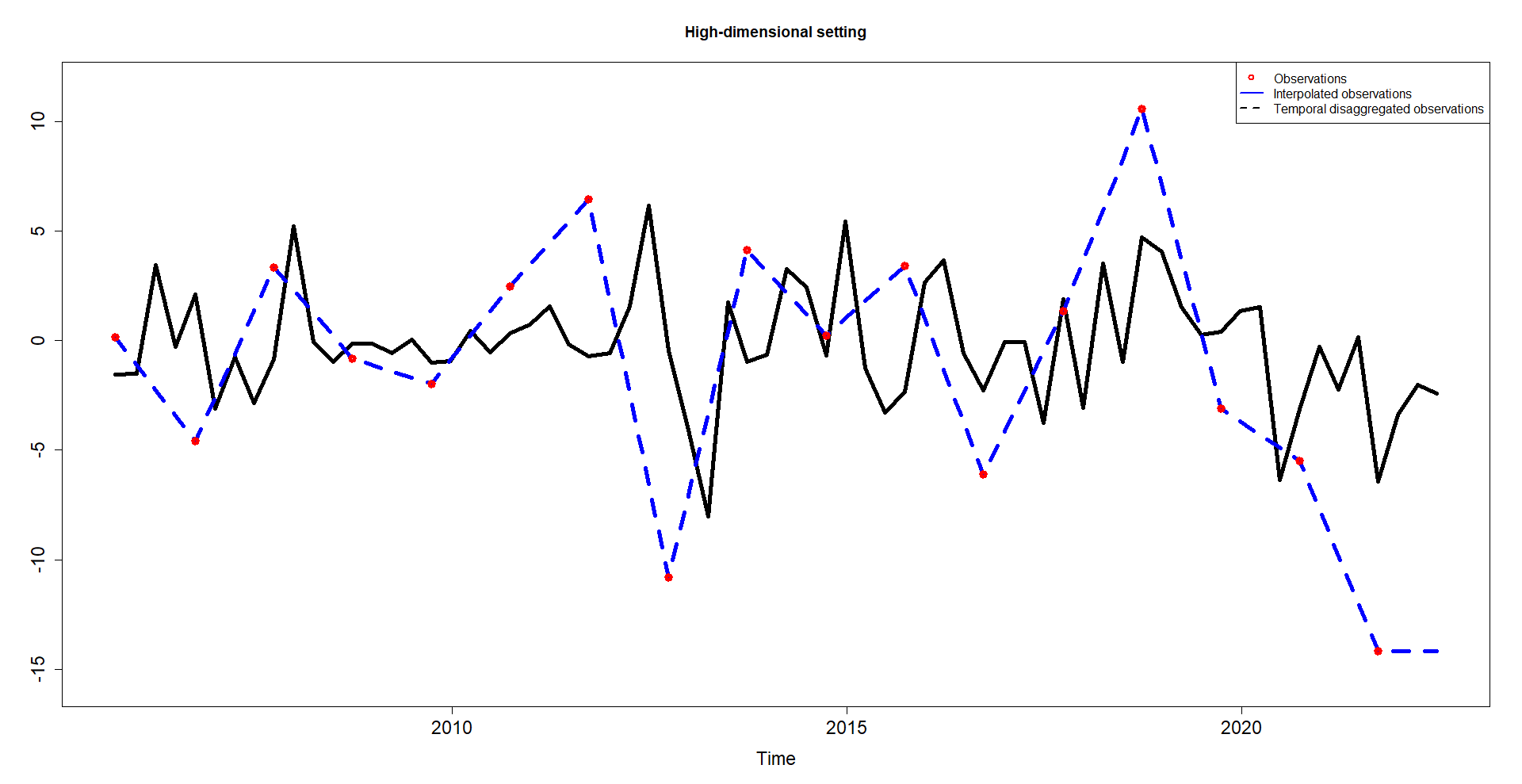

High-dimensional setting

We now repeat the simulation experiment in a high-dimensional setting, where the number of temporal observations is lower than the number of exogenous variables. In this case, standard methods like Chow-Lin cannot be applied. To do so, we simulate the dependent variable as before, but now the set of high-frequency exogenous variables is of dimension . Similarly, as before, we can use the following command:

> # Load the DisaggregateTS library> library(DisaggregateTS)> # Generate low-frequency yearly series and its high-frequency quarterly counterpart> n_l = 17 # The number of low-frequency data points - annual> n=68 # The number of high-frequency data points 0 quarterly> p_sim = 100 # The number of the high-frequency exogenous variables.> rho_sim = 0.8 # autocorrelation parameter> Sim_data <- TempDisaggDGP(n_l, n, aggRatio = 4,p = p_sim, rho = rho_sim)> Y_sim <- matrix(Sim_data$Y_Gen) #Extract the simulated dependent> # (low-frequency) variable> X_sim <- Sim_data$X_Gen #Extract the simulated exogenous variables - high-frequency In this case, we cannot use a standard technique, and we need to estimate a sparse model to overcome the curse of dimensionality. The disaggregate function can handle the high-dimensional setting by choosing the method to be spTD or adaptive-spTD. In the following example, we use the latter:

> C_sparse_SIM = disaggregate(Y_sim, X_sim, aggMat = "sum",+ aggRatio = 4, method = "adaptive-spTD")> C_sparse_SIM$beta_Est> Y_HF_SIM = C_sparse_SIM$y_Est[ ,1] # Extract the temporal disaggregated> # dependent variable estimated through the function disaggregate()

Figure 4 below shows the results.

3.3 Empirical application: Carbon intensity

In this Section, we show how temporal disaggregation can be used in a real-world problem.

The urgent need to address climate change has propelled the scientific community to explore innovative approaches to quantify and manage greenhouse gas (GHG) emissions. Carbon intensity, a crucial metric that measures the amount of carbon dioxide equivalent emitted per unit of economic activity (e.g. sales), plays a pivotal role in assessing the environmental sustainability of industries, countries, and global economies. Accurate and timely carbon accounting and the development of robust measurement frameworks are essential for effective emission reduction strategies and the pursuit of sustainable development goals.

While carbon accounting frameworks offer valuable insights into emissions quantification, they are not without limitations. One of those limitations is the frequency with which this information is released, generally at an annual frequency, while most companies’ economic indicators are made public on a quarterly basis.

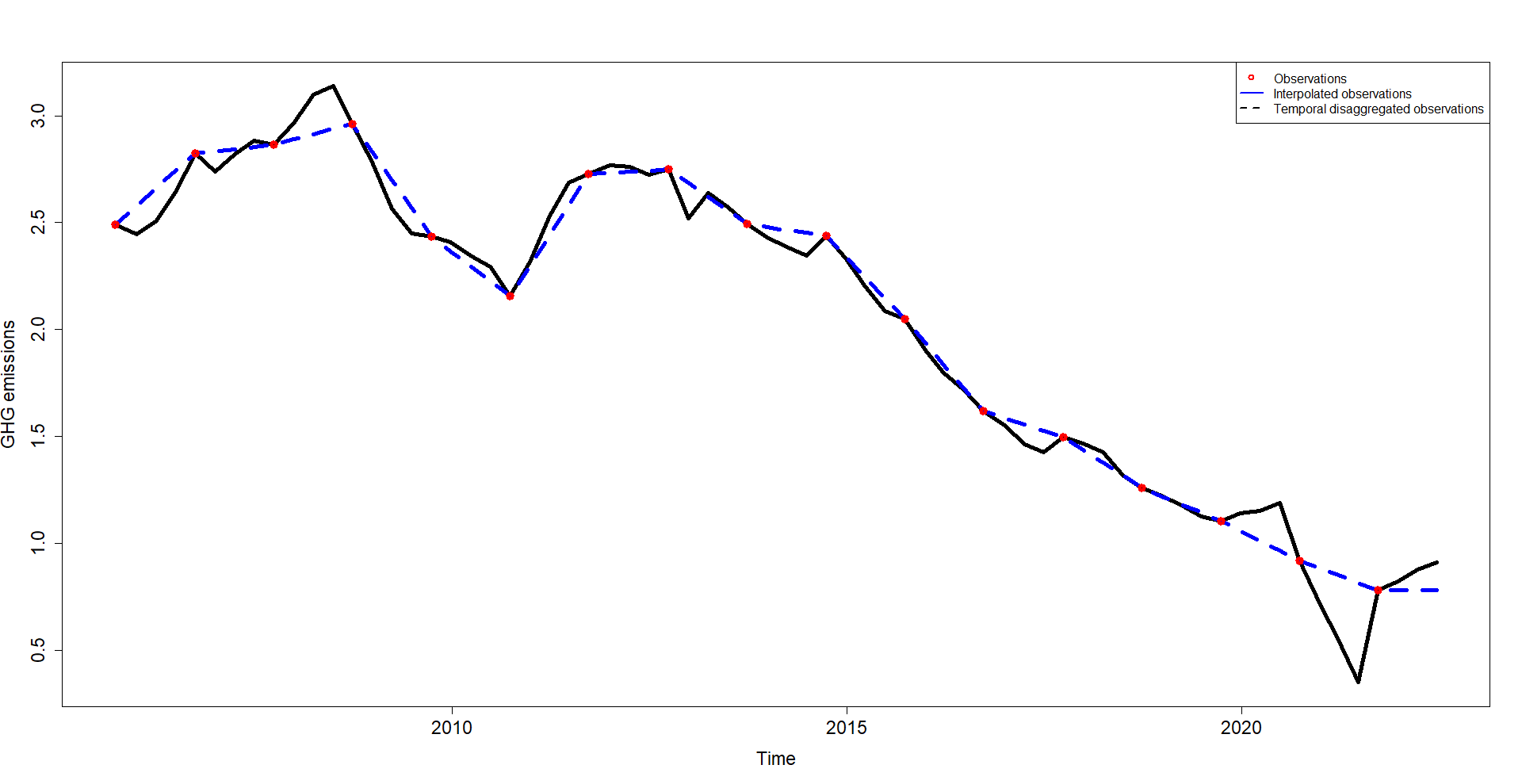

This is a perfect example in which temporal disaggregation can be used to bridge the gap between data availability and prompt economic and financial analyses. In this application, the variable of interest is the GHG emissions for IBM between Q3 2005 and Q3 2021, at annual frequency, resulting in 17 datapoints, i.e. . For the high-frequency data, we used the balance sheet, income statement, and cash flow statement quarterly data between Q3 2005 and Q3 2021, resulting in 68 datapoints for the 128 variables. We remove variables that have a pairwise correlation higher than 0.99, resulting in a filtered dataset with 112 variables, i.e. .

In this example, we employed the adaptive LASSO method, resulting in only two non-zero coefficients, which are the 12 months trailing sales and the total company capital. Trailing sales and total company capital are indeed relevant predictors of emissions because they reflect a company’s economic activity, operational intensity, and commitment to sustainability. We show the results in Figure 5 alongside a linear interpolation method.

As it is possible to observe from the plot, the interpolated data do not fluctuate as we would expect from real GHG emissions, as the method is not conditional on the variability of the high-frequency variables. In this respect, the temporal disaggregated observations show a remarkably truthful dynamics. This result can then be used to compute the GHG intensity, computing the ratio between GHG emissions and the sales for the corresponding quarter.

4 Summary

In this paper, we demonstrated how the DisaggregateTS package can be used and what are its potential use in climate finance and economics. The data-generating processes encoded within the model allow for efficient synthetic evaluation of disaggregation procedures.

References

- Belloni and Chernozhukov, (2013) Belloni, A. and Chernozhukov, V. (2013). Least squares after model selection in high-dimensional sparse models.

- Bournay and Laroque, (1979) Bournay, J. and Laroque, G. (1979). Réflexions sur la méthode d’elaboration des comptes trimestriels. In Annales de l’INSEE, pages 3–30. JSTOR.

- Chow and Lin, (1971) Chow, G. C. and Lin, A.-l. (1971). Best linear unbiased interpolation, distribution, and extrapolation of time series by related series. The review of Economics and Statistics, pages 372–375.

- Chow and Lin, (1976) Chow, G. C. and Lin, A.-L. (1976). Best linear unbiased estimation of missing observations in an economic time series. Journal of the American Statistical Association, 71(355):719–721.

- Dagum and Cholette, (2006) Dagum, E. B. and Cholette, P. A. (2006). Benchmarking, temporal distribution, and reconciliation methods for time series.

- Denton, (1971) Denton, F. T. (1971). Adjustment of monthly or quarterly series to annual totals: an approach based on quadratic minimization. Journal of the american statistical association, 66(333):99–102.

- Efron et al., (2004) Efron, B., Hastie, T., Johnstone, I., and Tibshirani, R. (2004). Least angle regression.

- Fernandez, (1981) Fernandez, R. B. (1981). A methodological note on the estimation of time series. The Review of Economics and Statistics, 63(3):471–476.

- Fuleky, (2019) Fuleky, P. (2019). Macroeconomic forecasting in the era of big data: Theory and practice, volume 52. Springer.

- Litterman, (1983) Litterman, R. B. (1983). A random walk, markov model for the distribution of time series. Journal of Business & Economic Statistics, 1(2):169–173.

- Mosley et al., (2022) Mosley, L., Eckley, I. A., and Gibberd, A. (2022). Sparse Temporal Disaggregation. Journal of the Royal Statistical Society Series A: Statistics in Society, 185(4):2203–2233.

- Mosley and S. Nobari, (2022) Mosley, L. and S. Nobari, K. (2022). DisaggregateTS: High-Dimensional Temporal Disaggregation. R package version 2.0.0.

- Quilis, (2018) Quilis, E. M. (2018). Temporal disaggregation of economic time series: The view from the trenches. Statistica Neerlandica, 72(4):447–470.

- Sax and Steiner, (2013) Sax, C. and Steiner, P. (2013). Temporal disaggregation of time series.

- Sax et al., (2016) Sax, C., Steiner, P., Di Fonzo, T., and Sax, M. C. (2016). Package ‘tempdisagg’.

- Schwarz, (1978) Schwarz, G. (1978). Estimating the dimension of a model the annals of statistics 6 (2), 461–464. URL: http://dx. doi. org/10.1214/aos/1176344136.

- Tibshirani, (1996) Tibshirani, R. (1996). Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society: Series B (Methodological), 58(1):267–288.

- Van de Geer et al., (2011) Van de Geer, S., Bühlmann, P., and Zhou, S. (2011). The adaptive and the thresholded lasso for potentially misspecified models (and a lower bound for the lasso).

- Wainwright, (2019) Wainwright, M. J. (2019). High-dimensional statistics: A non-asymptotic viewpoint, volume 48. Cambridge university press.

- Zou, (2006) Zou, H. (2006). The adaptive lasso and its oracle properties. Journal of the American statistical association, 101(476):1418–1429.