More is Better in Modern Machine Learning: when Infinite Overparameterization is Optimal

and Overfitting is Obligatory

Abstract

In our era of enormous neural networks, empirical progress has been driven by the philosophy that more is better. Recent deep learning practice has found repeatedly that larger model size, more data, and more computation (resulting in lower training loss) improves performance. In this paper, we give theoretical backing to these empirical observations by showing that these three properties hold in random feature (RF) regression, a class of models equivalent to shallow networks with only the last layer trained.

Concretely, we first show that the test risk of RF regression decreases monotonically with both the number of features and the number of samples, provided the ridge penalty is tuned optimally. In particular, this implies that infinite width RF architectures are preferable to those of any finite width. We then proceed to demonstrate that, for a large class of tasks characterized by powerlaw eigenstructure, training to near-zero training loss is obligatory: near-optimal performance can only be achieved when the training error is much smaller than the test error. Grounding our theory in real-world data, we find empirically that standard computer vision tasks with convolutional neural tangent kernels clearly fall into this class. Taken together, our results tell a simple, testable story of the benefits of overparameterization, overfitting, and more data in random feature models.

1 Introduction

It is an empirical fact that more is better in modern machine learning. State-of-the-art models are commonly trained with as many parameters and for as many iterations as compute budgets allow, often with little regularization. This ethos of enormous, underregularized models contrasts sharply with the received wisdom of classical statistics, which suggests small, parsimonious models and strong regularization to make training and test losses similar. The development of new theoretical results consistent with the success of overparameterized, underregularized modern machine learning has been a central goal of the field for some years.

How might such theoretical results look? Consider the well-tested observation that wider networks virtually always achieve better performance, so long as they are properly tuned (Kaplan et al., 2020; Hoffmann et al., 2022; Yang et al., 2022). Let denote the expected test error of a network with width and training hyperparameters when trained on samples from an arbitrary distribution. A satisfactory explanation for this observation might be a hypothetical theorem which states the following:

Such a result would do much to bring deep learning theory up to date with practice. In this work, we take a first step towards this general result by proving it in the special case of RF regression — that is, for shallow networks with only the second layer trained. Our Theorem 1 states that, for RF regression, more features (as well as more data) is better, and thus infinite width is best. To our knowledge, this is the first analysis directly showing that for arbitrary tasks, wider is better for networks of a certain architecture.

How might a comparable result for overfitting look? It is by now established wisdom that optimal performance in many domains is achieved when training deep networks to nearly the point of interpolation (i.e. zero training error), with train error many times smaller than test error ( Neyshabur et al. (2015); Zhang et al. (2017); Belkin et al. (2018), Appendix F of Hui & Belkin (2020)). However, unlike the statement “wider is better,” the statement “interpolation is optimal” cannot be true for generic task distributions: we can see this a priori by noting that any fitting at all can only harm us if the task is pure noise and the optimal predictor is zero. Indeed Nakkiran & Bansal (2020); Mallinar et al. (2022) empirically observe that training to interpolation harms the performance of real deep networks on sufficiently noisy tasks. This suggests that we instead ought to seek an appropriate class of model-task pairs — ideally general enough to include realistic tasks — such that a hypothetical statement of the following form is true:

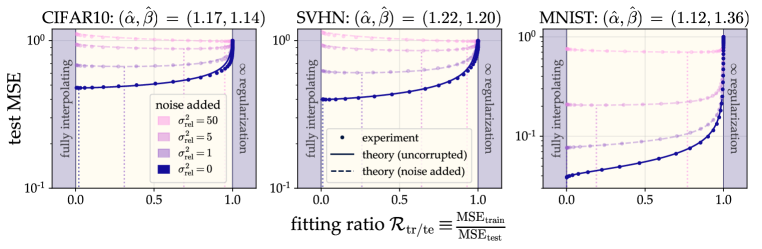

Here we have defined the fitting ratio to be the ratio of train error and test error and we have suppressed the arguments of and for the sake of generality. We take a step towards this general result, too, by proving a sharp statement to this effect for kernel ridge regression (KRR), including infinite-feature RF regression and infinite-width neural networks of any depth in the kernel regime (Jacot et al., 2018; Lee et al., 2019). Letting be the set of tasks with powerlaw eigenstructure (Definition 2), our Theorem 2 states that under mild conditions on the powerlaw exponents, not only is at optimal regularization, but in fact this overfitting is obligatory: attaining near-optimal test error requires that .111This is in contrast with the proposed phenomenon of “benign overfitting” (Bartlett et al., 2020; Tsigler & Bartlett, 2023) in which interpolation (i.e. training to zero train loss) is merely harmless, incurring only a sub-leading-order cost relative to optimal regularization. In our “obligatory overfitting” regime, interpolation is necessary, and not interpolating incurs a leading-order cost. Crucially, we put our proposed explanation to the experimental test: we clearly find that the eigenstructure of standard computer vision tasks with convolutional neural kernels displays powerlaw decay in satisfaction of our “obligatory overfitting” criteria, and indeed optimality occurs at for these tasks (Figure 2).

All our main results rely on closed form estimates for the train and test error of RF regression and KRR in terms of task eigenstructure. We derive such an estimate for RF regression, and our “more is better” conclusion (Theorem 1) follows quickly from this general result. This estimate relies on a Gaussian universality ansatz (which we validate empirically) and becomes exact in an appropriate asymptotic limit, though we see excellent agreement with experiment even at modest size. When we study overfitting in KRR, which is the infinite-feature limit of RF regression, we use the infinite-feature limit of our eigenframework, which recovers a well-known risk estimate for (kernel) ridge regression extensively investigated in the recent literature (Sollich, 2001; Bordelon et al., 2020; Jacot et al., 2020a; Dobriban & Wager, 2018; Hastie et al., 2020). We solve this eigenframework for powerlaw task eigenstructure, obtaining an expression for test error in terms of the powerlaw exponents and the fitting ratio (Lemma 10), and our “obligatory overfitting” conclusion (Theorems 2 and 1) follows from this general result. Remarkably, we find that real datasets match our proposed powerlaw structure so well that we can closely predict test error as a function of purely from experimentally extracted values of the powerlaw exponents (Figure 2). To conclude, we return to the question of how one ought to view modern machine learning, suggesting some intuitions consistent with our findings.

Concretely, our contributions are as follows:

-

•

We obtain general closed-form estimates for the test risk of RF regression in terms of task eigenstructure (Section 4.1).

-

•

We conclude that, at optimal ridge parameter, more features and more data are strictly beneficial (Theorem 1).

-

•

We study KRR for tasks with powerlaw eigenstructure, finding that for a subset of such tasks, overfitting is obligatory: optimal performance is only achieved at small or zero regularization (Theorem 2).

-

•

We demonstrate that standard image datasets with convolutional kernels satisfy our criteria for obligatory overfitting (Figure 2).

2 Related work

The benefits of overparameterization. Much theoretical work has aimed to explain the benefits of overparameterization. Belkin et al. (2019) identify a “double-descent” phenomenon in which, for certain underregularized learning rules, increasing overparameterization improves performance. Ghosh & Belkin (2022) show that only highly overparameterized models can both interpolate noisy data and generalize well. Roberts et al. (2022); Atanasov et al. (2022); Bordelon & Pehlevan (2023) show that neural networks of finite width can be viewed as (biased) noisy approximations to their infinite-width counterparts, with the noise decreasing as width grows, which is consistent with our conclusion that wider is better for RF regression. Nakkiran et al. (2021) prove that more features benefits RF regression in the special case of isotropic covariates; our Theorem 1 extends their results to the general case, resolving a conjecture of theirs. Concurrent work (Patil & Du, 2023) also resolves this conjecture, showing sample-wise monotonicity for ridge regression. Yang & Suzuki (2023) also show that sample-wise monotonicity holds for isotropic linear regression given optimal dropout regularization. It has also been argued that overparameterization provides benefits in terms of allowing efficient optimization (Jacot et al., 2018; Liu et al., 2022), network expressivity (Cybenko, 1989; Lu et al., 2017), and adversarial robustness (Bubeck & Sellke, 2021).

The generalization of RF regression. RF (ridge) regression was first proposed by Rahimi & Recht (2007) as a cheap approximation to KRR. Its generalization was first studied using classical capacity-based bounds Rahimi & Recht (2008); Rudi & Rosasco (2017). In the modern era, RF regression has seen renewed theoretical attention due to its analytical tractability and variable parameter count. Gerace et al. (2020) find closed-form equations for the test error of RF regression with a fixed projection matrix. Jacot et al. (2020b) show that the average RF predictor for a given dataset resembles a KRR predictor with greater ridge parameter. Mei & Montanari (2019); Mei et al. (2022) find closed-form equations for the average-case test error of RF regression in the special case of high-dimensional isotropic covariates. Maloney et al. (2022) find equations for the average test error of a general model of RF regression under a special “teacher equals student” condition on the task eigenstructure, and Bach (2023) similarly solved RF regression for the case of zero ridge. We report a general RF eigenframework that subsumes many of these closed-form solutions as special cases (see Appendix F). Our eigenframework can also be extracted, with some algebra, from replica calculations reported by Atanasov et al. (2022) (Section D.5.2) and Zavatone-Veth & Pehlevan (2023) (Proposition 3.1).

Interpolation is optimal. Many recent works have aimed to identify settings in which optimal generalization on noisy data may be achieved by interpolating methods, including local interpolating schemes (Belkin et al., 2018) and ridge regression (Liang & Rakhlin, 2020; Muthukumar et al., 2020; Koehler et al., 2021; Bartlett et al., 2020; Tsigler & Bartlett, 2023; Zhou et al., 2023). However, it is not usually the case in these works that (near-)interpolation is required to generalize optimally, as seen in practice. We argue that this is because these works focus entirely on the model, whereas one must also identify suitable conditions on the task being learned in order to make such a claim. Several papers have described ridge regression settings in which a negative ridge parameter is in fact optimal (Kobak et al., 2020; Wu & Xu, 2020; Tsigler & Bartlett, 2023). We consider only nonnegative ridge in this work to align with deep learning, but our findings are consistent with the task criterion found by Wu & Xu (2020).222Some of our results — for example, Corollary 1 — give inequalities which, if satisfied, imply that zero ridge is optimal. It is generally the case that, when such an inequality is satisfied strictly (i.e. we do not have equality), a negative ridge would have been optimal had we allowed it. In a similar spirit, Cheng et al. (2022) prove in a Bayesian linear regression setting that for low noise, algorithms must fit substantially below the noise floor to avoid being suboptimal.

3 Preliminaries

We will work in a standard supervised setting: our dataset consists of samples sampled i.i.d. from a measure over . We wish to learn a target function (which we assume to be square-integrable with respect to ), and are provided noisy training labels where with noise level . Once a learning rule returns a predicted function , we evaluate its train and test mean-squared error, given by and respectively.

RF regression is a learning rule defined by the following procedure. First, we sample weight vectors i.i.d. from some measure over . We then define the featurization transformation , where is a feature function which is square-integrable with respect to and . Finally, we perform standard linear ridge regression over the featurized data: that is, we output the function , where the weights are given by with and a ridge parameter. If the feature function has the form with and some nonlinearity , then this model is precisely a shallow neural network with only the second layer trained.

RF regression is equivalent to kernel ridge regression

| (1) |

where the vector and matrix contain evaluations of the (stochastic) random feature kernel . Note that as , the kernel converges in probability to its expectation and RF regression converges to KRR with the deterministic kernel .

3.1 Spectral decomposition of and the Gaussian universality ansatz

Here we say what we mean by “task eigenstructure” in RF regression. Consider the bounded linear operator defined as

The operator is a Hilbert-Schmidt operator to which the singular value decomposition can be applied to (Kato, 2013). That is, there is an orthonormal basis of and an orthonormal basis of such that . Here are the non-negative eigenvalues indexed in decreasing order and are the corresponding eigenfunctions of the integral operator given by

If we denote as the adjoint of , then . Moreover, the feature function admits the decomposition , where the convergence is in . The decomposition of the deterministic kernel is given by

Note that the learning problem is specified entirely by , .

The functions , viewed as random variables induced by and respectively can have a complicated distribution. However, since the functions form orthonormal bases, we know that the random variables are uncorrelated and have second moments equal to one — that is, . To make progress, throughout the text we will use the following Gaussian universality ansatz and assume that the distributions may be treated as uncorrelated Gaussians:

Assumption A (Gaussian universality ansatz).

The expected train and test error are unchanged if we replace , by random Gaussian functions , . By this, we mean that when sampling the values are i.i.d. samples from , and likewise for and .

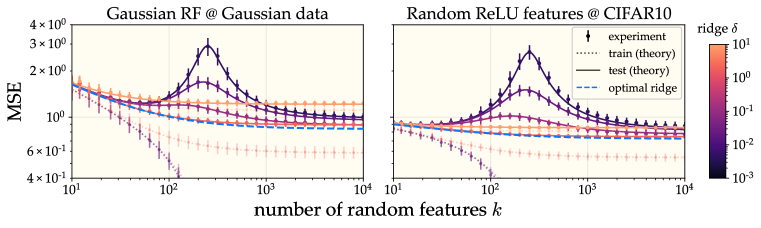

A seems strong at first glance. It is made plausible by many comparable universality results in random matrix theory which state that, when computing certain scalar quantities derived from large random matrices, only the first two moments of the elementwise distribution matter (up to some technical conditions), and the elements can thus be replaced by Gaussians for more convenient analysis (Davidson & Szarek, 2001; Tao, 2023). A holds provably for RF regression in certain asymptotic settings — see, for example, (Mei & Montanari, 2019; Mei et al., 2022). Most encouragingly, recent results for the test error of KRR derived using a comparable condition show excellent agreement with the test error computed on real data at moderate sample size (Sollich, 2001; Bordelon et al., 2020; Jacot et al., 2020a; Simon et al., 2021; Loureiro et al., 2021; Wei et al., 2022), so we might expect to observe a similar universality in RF regression. Indeed, we will shortly validate A empirically, demonstrating excellent agreement between predictions for Gaussian statistics and RF experiments with real data (Figure 1). Given that our ultimate goal is to understand learning from real data, this empirical agreement is reassuring.

Under this universality ansatz, the statistics of the eigenfunctions may be neglected, and the learning task is specified entirely by the remaining variables . We will now give a set of closed-form equations which estimate train and test error in terms of these quantities.

4 More data and features are better in RF regression

4.1 The omniscient risk estimate for RF regression

In this section, we will first state our risk estimate for RF regression, which will enable us to conclude that more data and features are better.

Let be the unique nonnegative scalars such that (2) Let and . The test and train error of RF regression are given approximately by (3) (4)

Following Breiman & Freedman (1983); Wei et al. (2022), we refer to Equation 3 as the omniscient risk estimate for RF regression because it relies on ground-truth information about the task (i.e., the true eigenvalues and target eigencoefficients ). We refer to the boxed equations, together with estimates for the bias, variance, and expectation of given in Section E.5, as the RF eigenframework. Several comments are now in order.

Like the framework of Bach (2023), our RF eigenframework is expected to become exact (with the error hidden by the “” going to zero) in a proportional limit where , , and the number of eigenvalues diverge together. 333More precisely: in this limit, one can consider taking , , and duplicating each eigenmode times for an integer , and then taking . Alternatively, new eigenmodes can be sampled from a fixed spectral distribution. However, we will soon see that it agrees well with experiment even at modest .

This eigenframework generalizes and unifies several known results. In particular, we recover the established KRR eigenframework when , we recover the ridgeless RF risk estimate of Bach (2023) when ,444We note the technicality that our equations Equation 2 have no solutions when and , and one should instead take . we recover the RF risk estimate of Maloney et al. (2022) when and , and we recover the main result of Mei et al. (2022) for high-dimensional RF regression by inserting an appropriate gapped eigenspectrum. We work out these and other limits in Appendix F.

Deriving the omniscient risk estimate for RF regression. We give a complete derivation of our RF eigenframework in Appendix E and give a brief sketch here. It is obtained from the fact that RF regression is KRR (c.f. Equation 1) with a stochastic kernel. As discussed in the introduction, many recent works have converged on an omniscient risk estimate for KRR under the universality ansatz, and if we knew certain eigenstatistics of the stochastic RF kernel , we could simply insert them into this known estimate for KRR and be done. Our main effort is in estimating these eigenstatistics using a handful of random matrix theory facts, after which we may read off the omniscient risk estimate for RF regression. Our derivation is nonrigorous, but we conjecture that it can be made rigorous with explicit error bounds decaying with as in Cheng & Montanari (2022).

Plan of attack. Our approach for the rest of the paper will be to rigorously prove facts about the deterministic quantities and given by our omniscient risk estimates in Equations 3 and 4.

4.2 The “more is better” property of RF regression

We now state the main result of this section.

Theorem 1 (More is better for RF regression).

Let denote with samples, features, and ridge with any task eigenstructure .

Let and .

It holds that

(5)

with strict inequality so long as and (i.e., the target has nonzero learnable component).

The proof, given in Appendix G, is elementary and follows directly from Equation 3. Theorem 1 states that the addition of either more data or more random features can only improve generalization error so long as we are free to choose the ridge parameter . It is counterintuitive from the perspective of classical statistics, which warns against overparameterization: by contrast, we see that performance increases with additional overparameterization, with the limiting KRR predictor being the optimal learning rule. However, this is sensible if one views RF regression as a stochastic approximation to KRR: the more features, the better the approximation to the ideal limiting process. This interpretation lines up nicely with recent theoretical intuitions viewing infinite-width deep networks as noiseless limiting processes (Bahri et al., 2021; Atanasov et al., 2022; Yang et al., 2022).

More prosaically, since additional i.i.d. features and samples simply provide a model with more information from which to generate predictions, one might have the intuitive hope that a “reasonable” learning rule should strictly benefit from more of either. Theorem 1 states that this hope is indeed borne out for RF regression so long as one regularizes correctly.

4.3 Experiments: validating the RF eigenframework

We perform RF regression experiments using real and synthetic data. Synthetic experiments use Gaussian data with and simple projection features with Gaussian weights . Experiments with real datasets use random ReLU features with Gaussian weights ; the corresponding theoretical predictions use task eigenstructure extracted numerically from the full dataset. The results, shown in Figure 1 and elaborated in Appendix A, show excellent agreement between measured test and train errors and our theoretical predictions. The good match to real data justifies the Gaussian universality ansatz used to derive the framework (A).

5 Overfitting is obligatory for KRR with powerlaw eigenstructure

Having established that more data and more features are better for RF regression, we now seek an explanation for why “more fitting” — that is, little to no regularization — is also often optimal. As we now know that infinite-feature models are always best, in our quest for optimality we simply take for the remainder of the paper and study the KRR limit. When , our RF eigenframework reduces to the well-established omniscient risk estimate for KRR, which we write explicitly in Section I.1. We will demonstrate that overfitting is obligatory for a class of tasks with powerlaw eigenstructure.

Defining “overfitting.” How should one quantify the notion of “overfitting”? In some sense, we mean that the optimal ridge parameter which minimizes test error is “small.” However, will usually decay with , so it is unclear how to define “small.” In this work, we define overfitting via the fitting ratio , which has the advantage of remaining order unity even as diverges. The fitting ratio is a strictly increasing function of the ridge , with when and as . Therefore, rather than minimizing with respect to , we can equivalently minimize with respect to . We will take the term “overfitting” to mean that .

Definition 1 (Optimal ridge, test error, and fitting ratio).

The optimal ridge , optimal test error , and optimal fitting ratio are equal to the values of these quantities at the ridge that minimizes test error. That is,

| (6) |

If the optimal fitting ratio is small — that is, if — we may say that overfitting is optimal. If it is also true that any gives higher test error, we say that overfitting is obligatory.

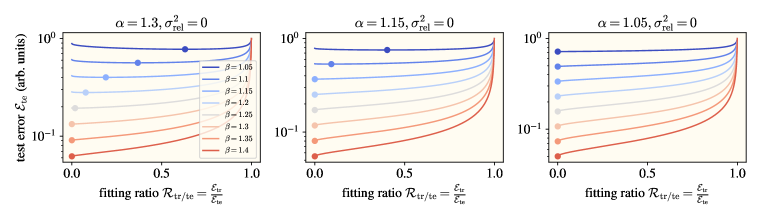

In this section, we will describe a class of tasks with powerlaw eigenstructure for which overfitting is provably obligatory. For all powerlaw tasks, we will find that is bounded away from (Theorem 2). Given an additional condition — namely, noise not too big, and an inequality satisfied by the exponents — we find that (Corollary 1). Remarkably, when we examine real learning tasks with convolutional kernels, we will observe powerlaw structure in satisfaction of this obligatory overfitting condition, and indeed we will see that .

Definition 2 ( powerlaw eigenstructure).

A KRR task has powerlaw eigenstructure for exponents if there exists an integer such that, for all , the task eigenvalues and eigencoeffients obey and .

In words, a task has powerlaw eigenstructure if the task eigenvalues and squared eigencoefficients have powerlaw tails with exponents . The technical condition needed for our proofs is mild, and we will find it is comfortably satisfied in practice.

Target noise. We will permit tasks to have nonzero noise. However, we must be mindful of a subtle but crucial point: we do not want to take a fixed noise variance , independent of . The reason is that the unlearned part of the signal will decay with , so if does not decay, the noise will eventually overwhelm the uncaptured signal. At this point, we might as well be training on pure noise. In this case, maximal regularization is optimal, and the model cannot possibly benefit from overfitting, as discussed in Section 1. We give a careful justification of this key point and compare with the benign overfitting literature in Appendix H.

We instead consider the setting where the noise scales down in proportion to the uncaptured signal To do so, we set

| (7) |

where is the relative noise level and is the test error at zero noise and zero ridge. This scaling also has the happy benefit of simplifying many of our final expressions. (We note that this question of noise scaling will ultimately prove purely academic — when we turn to real datasets, we will find that all are very well described with identically zero.)

We now state our main results.

Theorem 2.

Consider a KRR task with powerlaw eigenstructure.

Let the optimal fitting ratio and optimal test risk be given by Definition 1.

At optimal ridge, the fitting ratio is

(8)

where is either the unique solution to

(9)

over or else zero if no such solution exists,

and .

Furthermore, this fitting ratio is the unique optimum (up to error decaying in ) in the sense that

(10)

where .

The first part of Theorem 2 gives an equation whose solution is the optimal fitting ratio under powerlaw eigenstructure. The second part is a strong-convexity-style guarantee that, unless we are indeed tuned near , we will obtain test error worse than optimal by a constant factor greater than one.

The proof of Theorem 2 consists of direct computation of at large , together with the observation that . The difficulty lies largely in the technical task of bounding error terms. We give the proof in Appendix I.

The optimal fitting ratio given by Theorem 2 will always be bounded away from . This implies that some overfitting will always be obligatory in order to reach near-optimal test error. The following corollary, which follows immediately from Theorem 2, gives a necessary and sufficient condition under which and interpolation (i.e. zero ridge) is obligatory.

Corollary 1.

Consider a KRR task with powerlaw eigenstructure.

The optimal fitting ratio vanishes — that is, — if and only if

(11)

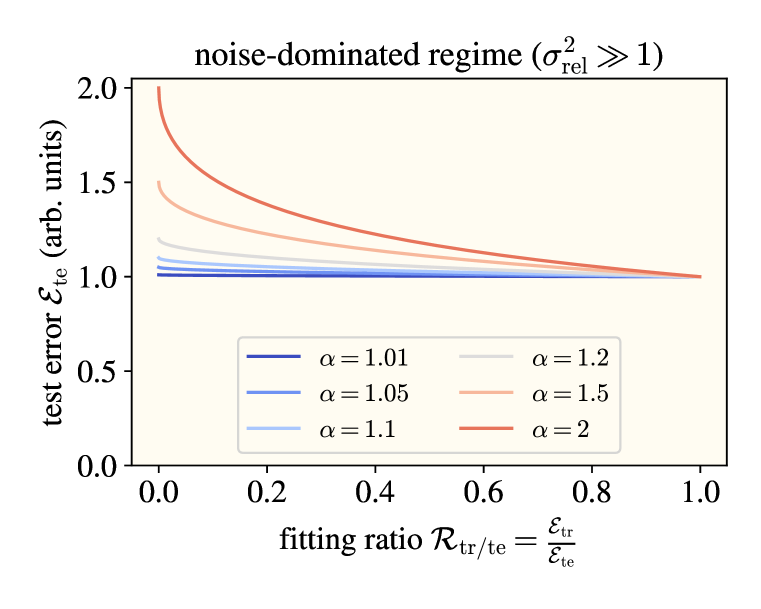

Corollary 1 gives an elegant picture of what makes a task interpolation-friendly. First, we must have ; otherwise, the RHS of Equation 11 is negative. Larger means that the error decays faster with (Cui et al., 2021), so amounts to a requirement that the task is sufficiently easy.555More precisely, since a larger corresponds to stronger inductive biases, means that in some sense “the task is no harder than the model anticipated.” Second, we must have sufficiently small noise relative to the uncaptured signal . More noise is permissible when the difference is greater, which is sensible since noise serves to make a task harder. The fact that zero regularization can be the unique optimum even with nonzero label noise is surprising from the perspective of classical statistics, which cautions against fitting below the noise level.

With zero noise, Theorem 2 simplifies to the following corollary for the optimal fitting ratio:

Corollary 2.

Consider a KRR task with powerlaw eigenstructure.

When , the optimal fitting ratio at large converges to

(12)

Corollary 2 implies in particular that even if is slightly smaller than , we will still find that .

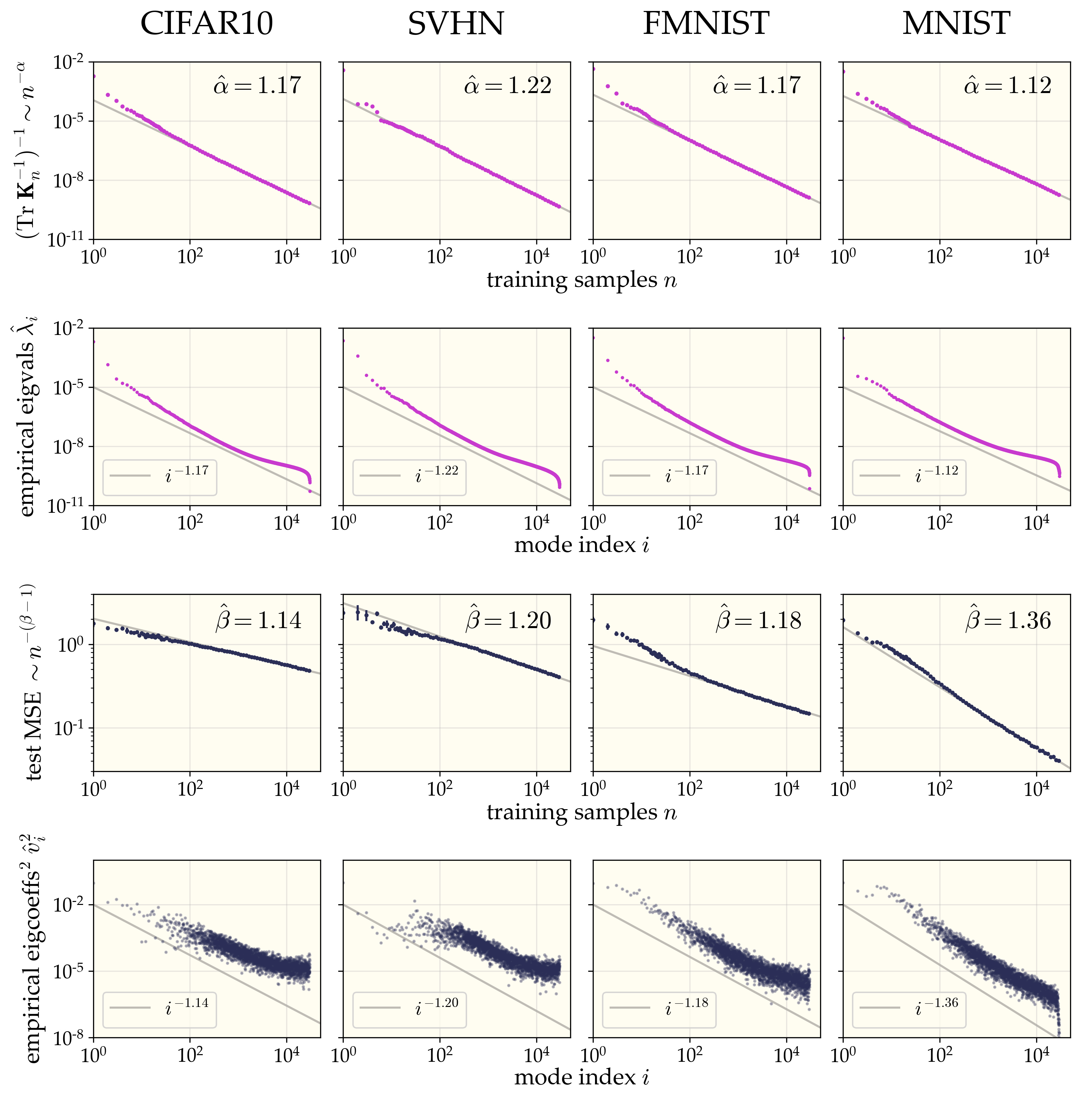

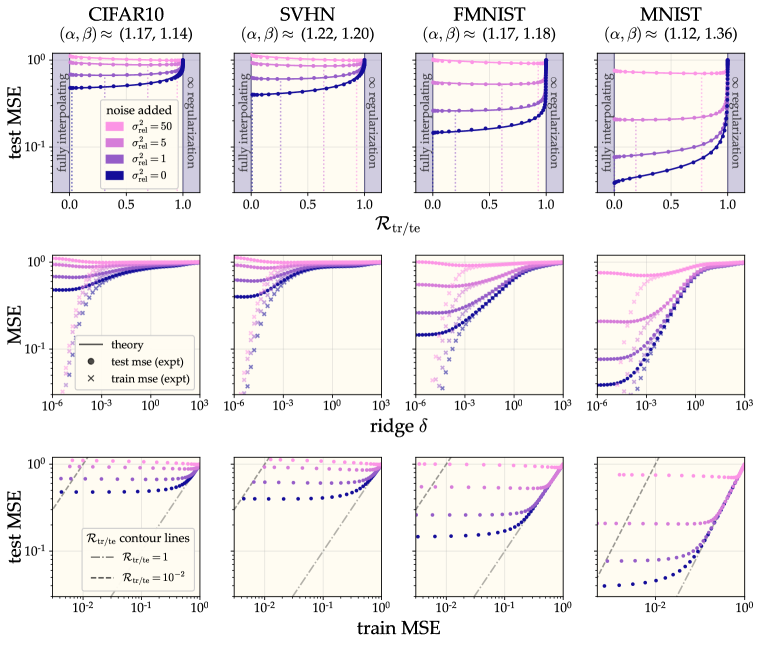

5.1 Experiments: overfitting is obligatory for MNIST, SVHN and CIFAR10 image datasets

We ultimately set out to understand an empirical phenomenon: the optimality of interpolation in many deep learning tasks. Having proposed a model for this phenomenon, is crucial that we now turn back to experiment and put it to the empirical test. We do so now with standard image datasets learned by convolutional neural tangent kernels. Running KRR with varying amounts of regularization, we observe that and (near-)interpolation is indeed obligatory for all three datasets (Figure 2). This is due to both favorable task structure and low intrinsic noise: as we add artificial label noise, is no longer zero, in accordance with Corollary 1.

We also find that adding label noise increases in accordance with our theory.

Even more remarkably, we find an excellent quantitative fit to our Lemma 10, which predicts as a function of up to a multiplicative constant. This surprising agreement attests that, insofar as the effect of regularization is concerned, the relevant structure of these datasets can be summarized by just the two scalars . These experiments resoundingly validate our theoretical picture for the examined tasks.

Measuring the exponents . We examine three standard image datasets — MNIST, SVHN, and CIFAR10 — and run KRR with the Myrtle convolutional neural tangent kernel (Shankar et al., 2020). We also report results for F-MNIST in Appendix D. We wish to check for powerlaw decay and and estimate the exponents .

We measure using the method of Wei et al. (2022). Assuming , it is easily shown that at zero ridge, the implicit regularization constant in the eigenframework decays with as (see e.g. our Lemma 2). Wei et al. (2022) show, theoretically under Gaussian universality and empirically for real data, that is well approximated by where is the empirical kernel matrix on samples. An estimate of the true exponent may thus be extracted by plotting many points on a log-log plot and fitting a line.

To measure , we make use of the eigenframework prediction that, with samples, zero ridge, and zero noise, the test risk decays as (see e.g. Cui et al. (2021) or our Lemma 3). Like with , we can thus extract an estimate of the true exponent by plotting many points on a log-log plot and fitting a line. We find a good linear fit here, which suggests that : if noise were significant, we instead expect to find instead that with some noise floor , but we find this noise floor is not necessary to achieve a good fit in the datasets we examine.

An alternative means of estimating is to simply diagonalize the kernel matrix evaluated on the full dataset and directly fit powerlaws to the resulting eigenvalues and coefficients (Spigler et al., 2020; Lee et al., 2020; Bahri et al., 2021). However, we found that this more direct method suffers from finite-sample-size effects which lead to significant error in measured exponents and which are avoided by instead fitting to the proxy metrics and . We give a clear illustration of this in Appendix C, where we construct a synthetic powerlaw task and find that this naive method fails to give good estimates of the ground-truth while our proxy measurements succeed in doing so.

6 Discussion

The present work is part of the research program aiming to understand the shortcomings of classical learning theory and to develop analyses suitable to machine learning as it exists today. We have presented two tractable models capturing the “more is better” spirit of deep learning, but we cannot consider this quest done until we have not only transparent models but also coherent new intuitions to take the place of appealing but outdated classical ones. To that end, we propose a few here.

One once-well-believed classical nugget of wisdom is the following: Overparameterization is harmful because it permits models to express complicated, poorly-generalizing solutions. Taking inspiration from our RF models, perhaps we ought instead to believe the following: Overparameterization is desirable because bigger models more closely approximate an ideal limiting process with infinitely many parameters. Overparameterization does permit a model to express complicated, poorly-generalizing solutions, but it does not mean that it will actually learn such a thing: models are simple creatures and tend not to learn unnecessarily complication without a good reason to.

Another classical view is that interpolation is undesirable because if a model interpolates, it has fit the noise, and so will generalize poorly. Our story with KRR suggests that perhaps we should instead hold the following belief: So long as the inductive bias of the model is a good match for the task and the noise is not too large, additional regularization is unnecessary, and it is optimal to fit with train error much less than test error.

What lessons might we take away for future deep learning theory? Any progress made in this paper relied entirely on closed-form average case estimates of risk. Unlike the bounds of classical learning theory, our risk estimates directly resolve interesting factors, and we were not left wondering how tight final bounds were. We simply studied the model’s behavior (namely, its train and test error) in the typical case. This approach is consistent with that of notable recent successes in deep learning theory, including the “neural tangent kernel” (Jacot et al., 2018) and “-parameterization” (Yang & Hu, 2021) avenues of study, both of which rely on exact descriptions of model behavior in regimes in which it concentrates about its mean. As we develop theory for deep learning, then, perhaps we ought to stop fretting about our models’ capacity to fail us and instead study the behavior they actually display.

Our study of overfitting differs from other recent works in its use of a theoretical model for the data. While this may at first seem like a weakness restricting the generality of our results, it ultimately proves a strength in that the predictions it furnishes are in excellent agreement with experiment. In other words, it is an assumption, but it appears to be a good assumption in the cases tested. An important auxiliary advantage of such a model is that it gives a new lens into the structure of the data: for example, we find that the tasks we study can be characterized by two powerlaw exponents of similar value, and that these tasks have negligible intrinsic noise, a conclusion which is difficult to draw without such a model. As we advance our understanding of deep learning, we advocate further use of phenomenological models aiming to capture statistical features of natural tasks.

Acknowledgements

JS thanks Alex Maloney, Alex Wei, Ben Adlam, Berfin Şimşek, Blake Bordelon, Jacob Zavatone-Veth, Francis Bach, Michael DeWeese, and Theo Misiakiewicz for useful discussions on the generalization of RF regression, as well as Roman Novak and Song Mei for useful discussions on the eigenstructure of image tasks early in the development of our empirical measurements. JS used Zymbolic for rapid math typesetting. JS gratefully acknowledges support from the National Science Foundation Graduate Fellow Research Program (NSF-GRFP) under grant DGE 1752814. MB acknowledges support from National Science Foundation (NSF) and the Simons Foundation for the Collaboration on the Theoretical Foundations of Deep Learning (https://deepfoundations.ai/) through awards DMS-2031883 and #814639 and the TILOS institute (NSF CCF-2112665). This work used the programs (1) XSEDE (Extreme science and engineering discovery environment) which is supported by NSF grant numbers ACI-1548562, and (2) ACCESS (Advanced cyberinfrastructure coordination ecosystem: services & support) which is supported by NSF grants numbers #2138259, #2138286, #2138307, #2137603, and #2138296. Specifically, we used the resources from SDSC Expanse GPU compute nodes, and NCSA Delta system, via allocations TG-CIS220009.

Summary of contributions

JS developed the main theoretical results, wrote the manuscript, and led the team logistically. DK developed and performed all experiments and assisted in writing. NG aided in framing the overall narrative, assisted in writing, and provided key technical insights during the development of the theory. MB proposed this line of study and provided overarching guidance throughout the project.

References

- Atanasov et al. (2022) Alexander Atanasov, Blake Bordelon, Sabarish Sainathan, and Cengiz Pehlevan. The onset of variance-limited behavior for networks in the lazy and rich regimes. arXiv preprint arXiv:2212.12147, 2022.

- Bach (2023) Francis Bach. High-dimensional analysis of double descent for linear regression with random projections. arXiv preprint arXiv:2303.01372, 2023.

- Bahri et al. (2021) Yasaman Bahri, Ethan Dyer, Jared Kaplan, Jaehoon Lee, and Utkarsh Sharma. Explaining neural scaling laws. arXiv preprint arXiv:2102.06701, 2021.

- Bartlett et al. (2020) Peter L Bartlett, Philip M Long, Gábor Lugosi, and Alexander Tsigler. Benign overfitting in linear regression. Proceedings of the National Academy of Sciences, 117(48):30063–30070, 2020.

- Belkin et al. (2018) Mikhail Belkin, Daniel Hsu, and Partha Mitra. Overfitting or perfect fitting? risk bounds for classification and regression rules that interpolate. arXiv preprint arXiv:1806.05161, 2018.

- Belkin et al. (2019) Mikhail Belkin, Daniel Hsu, Siyuan Ma, and Soumik Mandal. Reconciling modern machine-learning practice and the classical bias–variance trade-off. Proceedings of the National Academy of Sciences, 116(32):15849–15854, 2019.

- Bordelon & Pehlevan (2023) Blake Bordelon and Cengiz Pehlevan. Dynamics of finite width kernel and prediction fluctuations in mean field neural networks. arXiv preprint arXiv:2304.03408, 2023.

- Bordelon et al. (2020) Blake Bordelon, Abdulkadir Canatar, and Cengiz Pehlevan. Spectrum dependent learning curves in kernel regression and wide neural networks. In International Conference on Machine Learning, pp. 1024–1034. PMLR, 2020.

- Breiman & Freedman (1983) Leo Breiman and David Freedman. How many variables should be entered in a regression equation? Journal of the American Statistical Association, 78(381):131–136, 1983.

- Bubeck & Sellke (2021) Sébastien Bubeck and Mark Sellke. A universal law of robustness via isoperimetry. Advances in Neural Information Processing Systems, 34:28811–28822, 2021.

- Canatar et al. (2021) Abdulkadir Canatar, Blake Bordelon, and Cengiz Pehlevan. Spectral bias and task-model alignment explain generalization in kernel regression and infinitely wide neural networks. Nature communications, 12(1):1–12, 2021.

- Cheng & Montanari (2022) Chen Cheng and Andrea Montanari. Dimension free ridge regression. arXiv preprint arXiv:2210.08571, 2022.

- Cheng et al. (2022) Chen Cheng, John Duchi, and Rohith Kuditipudi. Memorize to generalize: on the necessity of interpolation in high dimensional linear regression. In Conference on Learning Theory, pp. 5528–5560. PMLR, 2022.

- Cui et al. (2021) Hugo Cui, Bruno Loureiro, Florent Krzakala, and Lenka Zdeborová. Generalization error rates in kernel regression: The crossover from the noiseless to noisy regime. Advances in Neural Information Processing Systems, 34:10131–10143, 2021.

- Cybenko (1989) George Cybenko. Approximation by superpositions of a sigmoidal function. Mathematics of control, signals and systems, 2(4):303–314, 1989.

- Davidson & Szarek (2001) Kenneth R. Davidson and Stanislaw J. Szarek. Chapter 8 - local operator theory, random matrices and banach spaces. In Handbook of the Geometry of Banach Spaces, volume 1 of Handbook of the Geometry of Banach Spaces, pp. 317–366. Elsevier Science B.V., 2001.

- Dobriban & Wager (2018) Edgar Dobriban and Stefan Wager. High-dimensional asymptotics of predictions: Ridge regression and classification. The Annals of Statistics, 46(1):247–279, 2018.

- Gerace et al. (2020) Federica Gerace, Bruno Loureiro, Florent Krzakala, Marc Mézard, and Lenka Zdeborová. Generalisation error in learning with random features and the hidden manifold model. In International Conference on Machine Learning, pp. 3452–3462. PMLR, 2020.

- Ghosh & Belkin (2022) Nikhil Ghosh and Mikhail Belkin. A universal trade-off between the model size, test loss, and training loss of linear predictors. arXiv preprint arXiv:2207.11621, 2022.

- Hastie et al. (2020) Trevor Hastie, Andrea Montanari, Saharon Rosset, and Ryan J. Tibshirani. Surprises in high-dimensional ridgeless least squares interpolation, 2020.

- Hoffmann et al. (2022) Jordan Hoffmann, Sebastian Borgeaud, Arthur Mensch, Elena Buchatskaya, Trevor Cai, Eliza Rutherford, Diego de Las Casas, Lisa Anne Hendricks, Johannes Welbl, Aidan Clark, et al. Training compute-optimal large language models. arXiv preprint arXiv:2203.15556, 2022.

- Hui & Belkin (2020) Like Hui and Mikhail Belkin. Evaluation of neural architectures trained with square loss vs cross-entropy in classification tasks. arXiv preprint arXiv:2006.07322, 2020.

- Jacot et al. (2018) Arthur Jacot, Clément Hongler, and Franck Gabriel. Neural tangent kernel: Convergence and generalization in neural networks. In Advances in Neural Information Processing Systems (NeurIPS), 2018.

- Jacot et al. (2020a) Arthur Jacot, Berfin Şimşek, Francesco Spadaro, Clément Hongler, and Franck Gabriel. Kernel alignment risk estimator: risk prediction from training data. arXiv preprint arXiv:2006.09796, 2020a.

- Jacot et al. (2020b) Arthur Jacot, Berfin Simsek, Francesco Spadaro, Clément Hongler, and Franck Gabriel. Implicit regularization of random feature models. In International Conference on Machine Learning, pp. 4631–4640. PMLR, 2020b.

- Kaplan et al. (2020) Jared Kaplan, Sam McCandlish, Tom Henighan, Tom B Brown, Benjamin Chess, Rewon Child, Scott Gray, Alec Radford, Jeffrey Wu, and Dario Amodei. Scaling laws for neural language models. arXiv preprint arXiv:2001.08361, 2020.

- Kato (2013) Tosio Kato. Perturbation theory for linear operators, volume 132. Springer Science & Business Media, 2013.

- Kobak et al. (2020) Dmitry Kobak, Jonathan Lomond, and Benoit Sanchez. The optimal ridge penalty for real-world high-dimensional data can be zero or negative due to the implicit ridge regularization. The Journal of Machine Learning Research, 21(1):6863–6878, 2020.

- Koehler et al. (2021) Frederic Koehler, Lijia Zhou, Danica J Sutherland, and Nathan Srebro. Uniform convergence of interpolators: Gaussian width, norm bounds and benign overfitting. Advances in Neural Information Processing Systems, 34:20657–20668, 2021.

- Lee et al. (2018) Jaehoon Lee, Yasaman Bahri, Roman Novak, Samuel S. Schoenholz, Jeffrey Pennington, and Jascha Sohl-Dickstein. Deep neural networks as gaussian processes. In International Conference on Learning Representations (ICLR), 2018.

- Lee et al. (2019) Jaehoon Lee, Lechao Xiao, Samuel S. Schoenholz, Yasaman Bahri, Roman Novak, Jascha Sohl-Dickstein, and Jeffrey Pennington. Wide neural networks of any depth evolve as linear models under gradient descent. In Advances in Neural Information Processing Systems (NeurIPS), 2019.

- Lee et al. (2020) Jaehoon Lee, Samuel S. Schoenholz, Jeffrey Pennington, Ben Adlam, Lechao Xiao, Roman Novak, and Jascha Sohl-Dickstein. Finite versus infinite neural networks: an empirical study. In Advances in Neural Information Processing Systems (NeurIPS), 2020.

- Liang & Rakhlin (2020) Tengyuan Liang and Alexander Rakhlin. Just interpolate: Kernel “ridgeless” regression can generalize. The Annals of Statistics, 48(3):1329–1347, 2020.

- Liu et al. (2022) Chaoyue Liu, Libin Zhu, and Mikhail Belkin. Loss landscapes and optimization in over-parameterized non-linear systems and neural networks. Applied and Computational Harmonic Analysis, 59:85–116, 2022.

- Loureiro et al. (2021) Bruno Loureiro, Cedric Gerbelot, Hugo Cui, Sebastian Goldt, Florent Krzakala, Marc Mezard, and Lenka Zdeborová. Learning curves of generic features maps for realistic datasets with a teacher-student model. Advances in Neural Information Processing Systems, 34:18137–18151, 2021.

- Lu et al. (2017) Zhou Lu, Hongming Pu, Feicheng Wang, Zhiqiang Hu, and Liwei Wang. The expressive power of neural networks: A view from the width. Advances in neural information processing systems, 30, 2017.

- Mallinar et al. (2022) Neil Mallinar, James B Simon, Amirhesam Abedsoltan, Parthe Pandit, Mikhail Belkin, and Preetum Nakkiran. Benign, tempered, or catastrophic: A taxonomy of overfitting. arXiv preprint arXiv:2207.06569, 2022.

- Maloney et al. (2022) Alexander Maloney, Daniel A Roberts, and James Sully. A solvable model of neural scaling laws. arXiv preprint arXiv:2210.16859, 2022.

- Mei & Montanari (2019) Song Mei and Andrea Montanari. The generalization error of random features regression: Precise asymptotics and the double descent curve. Communications on Pure and Applied Mathematics, 2019.

- Mei et al. (2022) Song Mei, Theodor Misiakiewicz, and Andrea Montanari. Generalization error of random feature and kernel methods: Hypercontractivity and kernel matrix concentration. Applied and Computational Harmonic Analysis, 59:3–84, 2022.

- Muthukumar et al. (2020) Vidya Muthukumar, Kailas Vodrahalli, Vignesh Subramanian, and Anant Sahai. Harmless interpolation of noisy data in regression. IEEE Journal on Selected Areas in Information Theory, 1(1):67–83, 2020.

- Nakkiran & Bansal (2020) Preetum Nakkiran and Yamini Bansal. Distributional generalization: A new kind of generalization. arXiv preprint arXiv:2009.08092, 2020.

- Nakkiran et al. (2021) Preetum Nakkiran, Prayaag Venkat, Sham M. Kakade, and Tengyu Ma. Optimal regularization can mitigate double descent. In International Conference on Learning Representations, ICLR, 2021.

- Neal (1996) Radford M Neal. Priors for infinite networks. In Bayesian Learning for Neural Networks, pp. 29–53. Springer, 1996.

- Neyshabur et al. (2015) Behnam Neyshabur, Ryota Tomioka, and Nathan Srebro. In search of the real inductive bias: On the role of implicit regularization in deep learning. In International Conference on Learning Representations, 2015.

- Novak et al. (2020) Roman Novak, Lechao Xiao, Jiri Hron, Jaehoon Lee, Alexander A. Alemi, Jascha Sohl-Dickstein, and Samuel S. Schoenholz. Neural tangents: Fast and easy infinite neural networks in python. In International Conference on Learning Representations, 2020.

- Patil & Du (2023) Pratik Patil and Jin-Hong Du. Generalized equivalences between subsampling and ridge regularization. arXiv preprint arXiv:2305.18496, 2023.

- Rahimi & Recht (2007) Ali Rahimi and Recht. Random features for large-scale kernel machines. In Advances in Neural Information Processing Systems (NeurIPS), volume 3, pp. 5, 2007.

- Rahimi & Recht (2008) Ali Rahimi and Benjamin Recht. Weighted sums of random kitchen sinks: Replacing minimization with randomization in learning. In Advances in Neural Information Processing Systems (NeurIPS), pp. 1313–1320. Curran Associates, Inc., 2008.

- Richards et al. (2021) Dominic Richards, Jaouad Mourtada, and Lorenzo Rosasco. Asymptotics of ridge (less) regression under general source condition. In International Conference on Artificial Intelligence and Statistics, pp. 3889–3897. PMLR, 2021.

- Roberts et al. (2022) Daniel A. Roberts, Sho Yaida, and Boris Hanin. Frontmatter. Cambridge University Press, 2022.

- Rudi & Rosasco (2017) Alessandro Rudi and Lorenzo Rosasco. Generalization properties of learning with random features. Advances in neural information processing systems, 30, 2017.

- Shankar et al. (2020) Vaishaal Shankar, Alex Fang, Wenshuo Guo, Sara Fridovich-Keil, Jonathan Ragan-Kelley, Ludwig Schmidt, and Benjamin Recht. Neural kernels without tangents. In International Conference on Machine Learning (ICML), volume 119 of Proceedings of Machine Learning Research, pp. 8614–8623. PMLR, 2020.

- Simon et al. (2021) James B Simon, Madeline Dickens, Dhruva Karkada, and Michael R DeWeese. The eigenlearning framework: A conservation law perspective on kernel ridge regression and wide neural networks. arXiv preprint arXiv:2110.03922, 2021.

- Sollich (2001) Peter Sollich. Gaussian process regression with mismatched models. In Advances in Neural Information Processing Systems, pp. 519–526. MIT Press, 2001.

- Spigler et al. (2020) Stefano Spigler, Mario Geiger, and Matthieu Wyart. Asymptotic learning curves of kernel methods: empirical data versus teacher–student paradigm. Journal of Statistical Mechanics: Theory and Experiment, 2020(12):124001, 2020.

- Tao (2023) Terence Tao. Topics in random matrix theory, volume 132. American Mathematical Society, 2023.

- Tsigler & Bartlett (2023) Alexander Tsigler and Peter L Bartlett. Benign overfitting in ridge regression. J. Mach. Learn. Res., 24:123–1, 2023.

- Vyas et al. (2023) Nikhil Vyas, Alexander Atanasov, Blake Bordelon, Depen Morwani, Sabarish Sainathan, and Cengiz Pehlevan. Feature-learning networks are consistent across widths at realistic scales. arXiv preprint arXiv:2305.18411, 2023.

- Wei et al. (2022) Alexander Wei, Wei Hu, and Jacob Steinhardt. More than a toy: Random matrix models predict how real-world neural representations generalize. In International Conference on Machine Learning, Proceedings of Machine Learning Research, 2022.

- Wu & Xu (2020) Denny Wu and Ji Xu. On the optimal weighted regularization in overparameterized linear regression. Advances in Neural Information Processing Systems, 33:10112–10123, 2020.

- Yang & Hu (2021) Greg Yang and Edward J Hu. Tensor programs iv: Feature learning in infinite-width neural networks. In International Conference on Machine Learning, pp. 11727–11737. PMLR, 2021.

- Yang et al. (2022) Greg Yang, Edward J Hu, Igor Babuschkin, Szymon Sidor, Xiaodong Liu, David Farhi, Nick Ryder, Jakub Pachocki, Weizhu Chen, and Jianfeng Gao. Tensor programs v: Tuning large neural networks via zero-shot hyperparameter transfer. arXiv preprint arXiv:2203.03466, 2022.

- Yang & Suzuki (2023) Tian-Le Yang and Joe Suzuki. Dropout drops double descent. arXiv preprint arXiv:2305.16179, 2023.

- Zavatone-Veth & Pehlevan (2023) Jacob A Zavatone-Veth and Cengiz Pehlevan. Learning curves for deep structured gaussian feature models. arXiv preprint arXiv:2303.00564, 2023.

- Zhang et al. (2017) Chiyuan Zhang, Samy Bengio, Moritz Hardt, Benjamin Recht, and Oriol Vinyals. Understanding deep learning requires rethinking generalization. In International Conference on Learning Representations (ICLR). OpenReview.net, 2017.

- Zhou et al. (2023) Lijia Zhou, James B Simon, Gal Vardi, and Nathan Srebro. An agnostic view on the cost of overfitting in (kernel) ridge regression. arXiv preprint arXiv:2306.13185, 2023.

Appendix A Experimental validation of our eigenframework for RF regression

We validate our RF eigenframework by comparing its predictions against two examples of random feature model:

Random Gaussian projections. We draw latent data vectors from an isotropic Gaussian in a high dimensional ambient space (dimension ).666In the main text, we purported to draw the data anisotropically as . For our explanation here, we introduce at the random projection stage, which amounts to the same thing. The target function is linear as , where the target coefficients follow a powerlaw with , and is Gaussian label noise with .

We construct random features as . Here, has elements drawn i.i.d. from . is a diagonal matrix of kernel eigenvalues, with . With this construction, the full-featured kernel matrix is (in expectation over the features) , with .

Random ReLU features. CIFAR10 input images are normalized to global mean 0 and standard deviation 1. The labels are binarized (with ) into two classes: things one can ride (airplane, automobile, horse, ship, truck) and things one ought not to ride (bird, cat, deer, dog, frog). Thus the target function is scalar.

The features are given by where has elements drawn i.i.d. from , with . With this construction, the limiting infinite-feature kernel is in fact the “NNGP kernel” of an infinite-width 1-hidden-layer ReLU network (Neal, 1996; Lee et al., 2018).

Theoretical predictions. The RF framework is an omniscient risk estimate, so to use it, we must have on hand the eigenvalues of the infinite-feature kernel and the eigencoefficients of the target function w.r.t to . For the synthetic data, we dictate the eigenstructure by construction: and . For random ReLU features, we use the neural tangents library (Novak et al. (2020)) to compute the NNGP kernel matrix of CIFAR10, and then diagonalize it to extract the eigenstructure. (We diagonalize an subset of the kernel matrix since this is the largest matrix we can diagonalize on a single A100 GPU without resorting to distributed eigensolvers.)

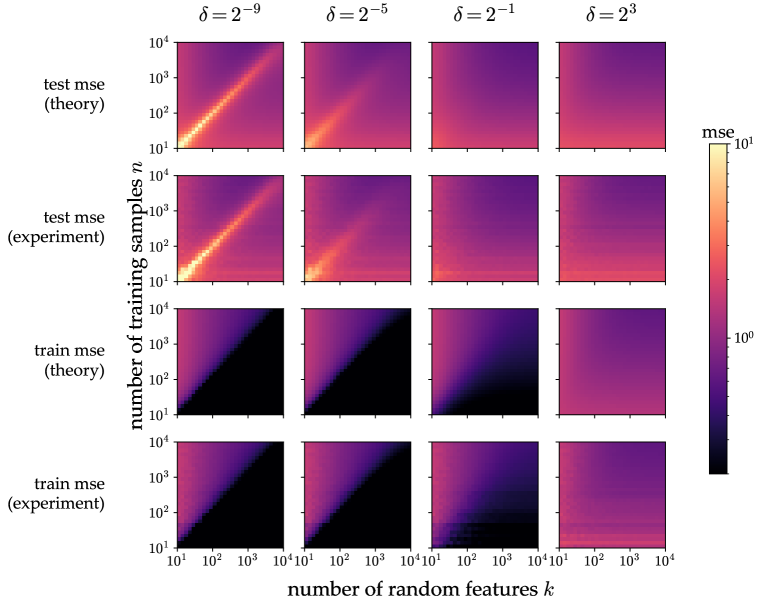

When evaluating our eigenframework, we numerically solve Equation 2 for and . This can prove a slightly finicky process. We use an inner-loop outer-loop routine as follows. In the inner loop, is fixed, we solve for such that , and we return the error signal , equal to the discrepancy in the other equation. In the outer loop, we optimize to drive that error signal to zero.

Experimental details. We vary , , . We perform 45 trials of each experimental run at a given (, , ); however, in each trial we fix the size- dataset as we vary the random features.

Additional plots. We report additional comparisons between RF experiments and our theory in Figures 3 and 4.

Code availability. Code to reproduce all experiments is available at https://github.com/dkarkada/more-is-better.

Appendix B Techniques for measuring powerlaw exponents in KRR tasks

Our analysis of overfitting in kernel regression relies on an assumption of “powerlaw eigenstructure” (Definition 2) characterized by two exponents . Here we describe our procedures for measuring for real datasets.

Extracting from the effective regularization .

The KRR eigenframework on which our results are based entails the computation of an intermediate quantity which serves as an “effective regularization constant” (Simon et al., 2021; Bordelon et al., 2020; Jacot et al., 2020a; Wei et al., 2022). This quantity decreases as more data are added: writing as a function of , one usually finds decay as .777Mallinar et al. (2022) find that can in fact be off of by log factors for certain exotic “benign overfitting” spectra, but this is beyond our scope here. In our case, if indeed we have for large , then we expect that .

Fortunately, Wei et al. (2022) describe a method by which may be experimentally measured. Under a reasonable Gaussian universality assumption, they find that , where is an empirical kernel matrix computed from samples. When we plot points on a log-log plot for many values of for the four datasets we study, we indeed see a clear linear tail indicative of powerlaw decay of and whose slope we can easily extract after performing a linear fit. We show these linear fits in Figure 5.

Extracting from the test error .

As discussed in the main text, we generally expect true risk at zero ridge and zero noise to decay proportionally to the uncaptured signal as . For the four datasets we study, we indeed see a linear decay when we plot points on a log-log plot. We fit a line and extract as the slope. We show these plots and linear fits in Figure 5.

Intuitions about powerlaw eigenstructure. Having measured powerlaw structure in several image datasets, we now give some informal discussion of how this structure might be interpreted. Informally, powerlaw eigenstructure describes the structure of natural data in two ways:

-

•

The eigenvalues of the kernel roughly decay as a powerlaw: . (Equivalently, the spectrum of the covariance matrix of the data distribution in the kernel’s feature space decay as a powerlaw.) Since represents a kernel’s “willingness” to learn eigenmode , we may interpret as representing the kernel’s parsimony: in modeling the data, a kernel with large tends to overattribute explanatory power to its top eigenmodes, confidently neglecting its tail eigenmodes.

-

•

The target function, expressed as a vector in the kernel’s eigenbasis, has components whose squares roughly decay as a powerlaw: Since larger implies a greater proportion of total task power in the top eigenmodes, we may interpret as representing the target function’s comprehensibility (to the kernel learner): targets with large are easier to learn.

These informal interpretations suggest that a kernel is well-suited to learn a task if is sufficiently small compared to . Otherwise, the kernel is simply too parochial to learn the intricacies of the target function; such a kernel will generalize poorly in the absence of regularization. This intuition is made precise in Corollary 1.

Remark. Powerlaw eigenstructure is a remarkable constraint. There is no clear reason why arbitrary data distributions and target functions should have this structure, and yet we observe that natural data do. This fact is both a miracle and a blessing for theorists, as it strongly restricts the class of data distributions we need concern ourselves with to explain the behavior of deep neural networks. It remains a major open question to fully explain and characterize the powerlaw structure of natural data with respect to neural kernels.

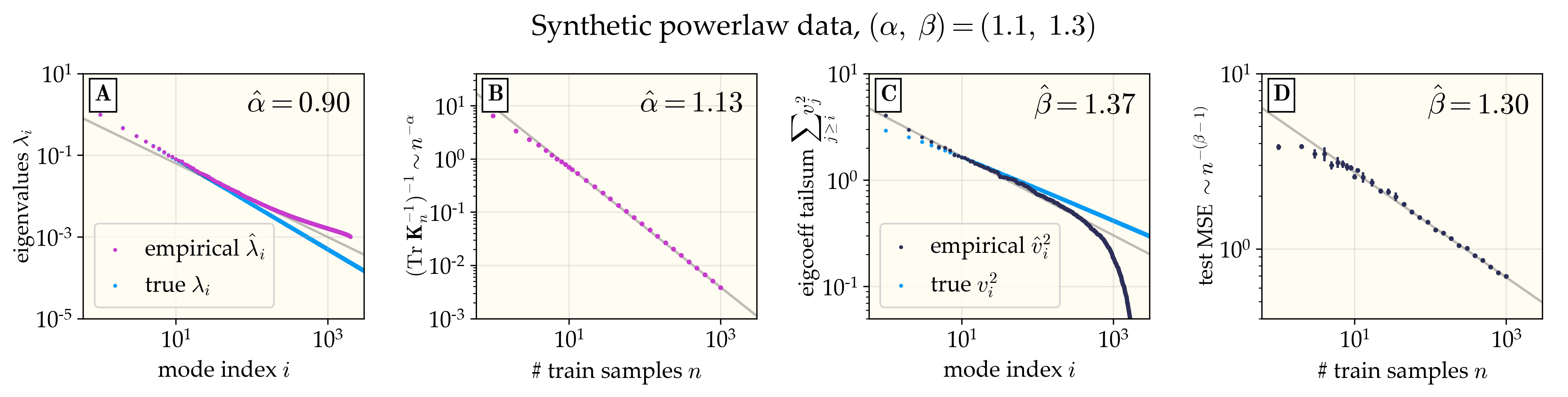

Appendix C Comparison: proxy measurements of recover true exponents more accurately than more direct measurements

Our theory for overfitting relies on the ansatz of powerlaw task eigenstructure that, at large , task eigenvalues and eigencoefficients decay as and . Prior works, including Spigler et al. (2020); Lee et al. (2020); Bahri et al. (2021), extracted the exponents from direct measurements of and for full datasets. However, as detailed in Appendix B, we instead extract more indirectly from the proxy quantities and . The purpose of this appendix is to explain a flaw in the direct method and thereby motivate this proxy method.

We begin by describing the direct method. First, one computes an empirical kernel matrix on a dataset of size . Since is real symmetric, we may numerically diagonalize it as , where and is a diagonal matrix of estimated eigenvalues. One then projects the labels onto the kernel eigenvectors to find the target eigencoefficient vector . Finally, one plots the computed eigenvalues and target eigencoefficients (or a tailsum thereof) on a log-log plot and performs linear fits, extracting powerlaw exponents from the slopes.

The essential problem with the direct method is finite-sample-size effects resulting from the finiteness of . For example, the extracted eigenvalues may be viewed as an estimation of the first ground-truth eigenvalues , but one generally expects this estimation to be accurate only for indices . In practice, we find it is often unclear for what range of indices we may say that “” and that we may therefore trust our estimated eigenvalues. This is not a trivial problem: we find that the error and ambiguity thereby induced can be quite large!

This is best illustrated with an example. To compare the accuracy of direct and proxy methods for exponent measurement, we construct a synthetic task with Gaussian data with powerlaw eigenstructure with and and try out both methods for recovering these exponents. The results are illustrated in Figure 6. For eigenvalues, we find that only the first few eigenvalues are recovered accurately, and attempted fits to the middle or tail of the spectrum yield large measurement errors. This is important because, in practice, the first few eigenvalues typically do not follow the powerlaw of the tail, leaving the experimenter with few or no clean power eigenvalues to which to fit a line. However, our proxy measurement recovers a decent approximation to the true . For eigencoefficients, since individual eigencofficients generally look noisy and require smoothing to see a powerlaw, we follow Spigler et al. (2020) and plot the tailsum as a function of , which is expected to decay as , the same exponent as that of test error. Here, too, we observe significant finite-size effects and are unable to observe the ground-truth powerlaw, but we recover the true with excellent accuracy from a plot of error vs. sample size.

Appendix D Experimental validation of theory for powerlaw tasks

We compute neural tangent kernel matrices for the Myrtle-10 convolutional architecture on four standard computer vision datasets: CIFAR-10, Street View House Numbers, FashionMNIST, and MNIST. For each, we perform kernel regression varying the ridge and added label noise. We additionally measure the eigenstructure exponents and using the techniques described in Appendix B. We use these measurements to predict the train and test error of these kernel learners and find excellent match with experiment (Figure 7).

Experimental details. We use the neural tangents library (Novak et al. (2020)) to compute the convolutional NTK matrices (CNTKs). It takes about four A100 GPU-days to compute each CNTK. We normalize each dataset to have global mean 0 and standard deviation 1. We do not binarize the labels: the learning task is one-hot 10-class regression. For experiments with label noise, the added noise is a Gaussian vector whose norm has total variance (see Equation 7). After adding noise, we normalize all label vectors to have unit norm so that all curves in Figure 2 intersect at .

In Figure 2 and Figure 7, each theory curve is vertically shifted by a constant multiplicative prefactor which is chosen such that the theory curve agrees with the experimental data at . This post-hoc fit is required because the derivation of Lemma 10 assumes the eigencoefficients follow a powerlaw with prefactor unity (i.e., with ), while the true eigencoefficients will be scaled, i.e. for some which may not be easy to measure. For this reason, we choose to simply fit the prefactor. When looking at Figure 2, then, we get theory-experiment match at for free, and the interesting fact is that we also have agreement for .

Code availability. Code to reproduce all experiments is available at https://github.com/dkarkada/more-is-better.

Appendix E Derivation of the RF eigenframework

In this appendix, we give a derivation of the eigenframework giving the train and test risk of RF regression which we report in Section 4. Our plan of attack is as follows. First we will recall from the literature the comparable eigenframework for KRR, expressing it in a manner convenient for our task. We will then explicitly write RF regression as an instance of KRR with a stochastic kernel. This framing will make it clear that, if we could understand certain statistics of the (stochastic) eigenstructure of the RF regression kernel, we could directly plug them into the KRR eigenframework. We will then use a single asymptotic random matrix theory identity to compute the various desired statistics. Inserting them into the KRR eigenframework, we will arrive at our RF eigenframework.

Our derivation will be nonrigorous in that we will gloss over technical conditions for the applicability of the KRR eigenframework for the sake of simplicity. Nonetheless, we will have strong evidence that our final answer is correct by its recovery of known results in various limits of interest (Appendix F) and by its strong agreement with real data (Figure 1).

E.1 Recalling the KRR eigenframework.

We now state the omniscient risk estimate for KRR (or equivalently linear ridge regression) under Gaussian design which has been converged upon by many authors in recent years (Sollich, 2001; Bordelon et al., 2020; Jacot et al., 2020a; Simon et al., 2021; Loureiro et al., 2021; Dobriban & Wager, 2018; Wu & Xu, 2020; Hastie et al., 2020; Richards et al., 2021). We phrase the framework in a slightly different way than in Section I.1 which will be more suitable to our current agenda.

As in the main text, let the Mercer decomposition of the kernel be , where are a complete basis of eigenfunctions which are orthonormal with respect to the data measure . We still assume our Gaussian universality ansatz (A) over the eigenfunctions .

We will find it useful to pack the eigenvalues into the (infinite) matrix , the target eigencoefficients into the (infinite) vector , and the set of eigenfunctions evaluated on any given data point into the (infinite) vector . Using this notation, the kernel function is given by

| (13) |

The KRR eigenframework appearing in these prior works is as follows.888All the prior works cited at the start of the subsection find the same eigenframework. As of the time of writing, Cheng & Montanari (2022) give probably the most rigorous and general derivation for this eigenframework and could be taken as the canonical source if one is required. First, let be the unique nonnegative solution to the equation999For two commuting matrices , we will sometimes abuse notation slightly to write in place of .

| (14) |

Then test and train MSE are well-approximated by

| (15) | ||||

| (16) |

The “” in 15 can be given several meanings. Firstly, it becomes an equivalence in an asymptotic limit in which and the number of eigenmodes in a given eigenvalue range (or the number of duplicate copies of any given eignemode) both grow large proportionally (Hastie et al., 2020; Bach, 2023). This is often phrased as sampling a proportional number of new eigenmodes from a fixed measure. Secondly, with fixed task eigenstructure, the error incurred can be bounded by a decaying function of (Cheng & Montanari, 2022). Thirdly, numerical experiments find small error even at quite modest (Canatar et al., 2021; Simon et al., 2021). For the purposes of this derivation, we will simply treat it as an equivalence.

E.2 Reframing RF regression as KRR with stochastic eigenstructure.

We now turn to RF regression. Recall from the main text that RF regression is equivalent to KRR with the random feature kernel

| (17) |

with sampled i.i.d. from some measure . Recall also that there exists a spectral decomposition

| (18) |

where and are sets of eigenfunctions which are orthonormal over and , respectively, and are a decreasing sequence of nonnegative scalars. Note that the limiting kernel as is in probability, from which we see that we are indeed justified in reusing the notation from the previous subsection.

Note that we can write this kernel as

| (19) | ||||

| (20) |

where we define the projection matrix . Comparing with Equation 13 and examining our KRR eigenframework, we see that, under A, we can predict the risk of RF regression as follows.

First, define (21) Then, let be the unique nonnegative solution to the equation (22) Then test and train MSE will be well-approximated by (23) (24)

We refer to this boxed set of equations as the partially-evaluated RF eigenframework because they are written in terms of the random projection , which we still have to deal with.

E.3 Building up some useful statistics of

The problem with the partially-evaluated RF eigenframework is of course that we do not know the stochastic eigenstructure matrix . To make progress, we again turn to our Gaussian universality ansatz (A). Under this assumption, we may replace the columns of with i.i.d. isotropic Gaussian vectors, which amounts to replacing the whole of with i.i.d. samples from .

We now leverage a basic random matrix theory fact for such Gaussian matrices leveraged in many recent analyses of ridge regression with random design (Jacot et al., 2020a; Simon et al., 2021; Bach, 2023). First, let be the unique nonnegative solution to

| (25) |

The final term is instead of simply as might be expected from the form of this fact in other works because of the factor of in Equation 21. Then, under the Gaussian design assumption on , we have that

| (26) |

This equation is useful because it reduces a statistic of the stochastic eigenstructure matrix into a function of the known eigenvalue matrix .

The meaning of “.” The “” in Equation 26 can be given various technical interpretations. It generally becomes an equivalence the proportional limit described in the following sense: consider fixing an integer and increasing , , and also duplicating each eigenmode times. As , we reach the proportional limit. For the purposes of this derivation, we will simply treat it as an equivalence.

We now bootstrap this relation to obtain four more relations. We state these relations and then justify them.

| (27) | ||||

| (28) | ||||

| (29) | ||||

| (30) |

Taking a derivative of Equation 25 and performing some algebra, we have that

| (31) |

We obtain Equation 27 by simply subtracting both sides of Equation 26 from the identity matrix . We obtain Equation 29 by taking a derivative of Equation 26 with respect to . We obtain Equation 30 by taking a derivative of Equation 27 with respect to . Finally, we obtain Equation 28 from the identity .

E.4 Inserting identities into the partially-evaluated RF eigenframework.

We are now in a position to insert Equations 26-30 into the partially-evaluated RF eigenframework to get closed-form results. We will generally trust that scalar quantities concentrate — that is, for some matrix and vector of interest, we will have that and , with small enough error that we can neglect it.

We start with Equation 22 defining . Inserting Equation 26 into the trace, it becomes

| (32) |

Inserting Equations 30 and 28 into Equation 23, we get that

| (33) |

Inserting Equation 31 for and simplifying with the definitions and and the fact that as per Equation 25, we arrive at the RF eigenframework we report in the main text.

Remark on implicit constants. The KRR eigenframework we started with had only one implicit constant , which could be understood two ways. First, it is given by the inverse of the trace of the inverse of the empirical kernel matrix: Wei et al. (2022). Second, it acts as an eigenvalue threshold: modes with are learned, and modes with are not. In the RF eigenframework, we have two implicit constants, and . This new still serves the first role: . However, it is now that acts as the learnability threshold for eigenvalues.

E.5 Additional estimates: bias, variance, and mean predictor

Test mean squared error is canonically split into a bias term (equal to the error of the “average” predictor) and a variance term (equal to the rest of the error). In the case of RF regression, a subtle question is: the average with respect to what? We could consider an average with respect to only random datasets, only random feature sets, or both at the same time. Jacot et al. (2020b) take a features-only average. Here we will take the other two.

In the main text, we denote the random dataset by . Let us also denote the random RF weights as . We then denote the data-averaged bias and variance to be

| (34) | ||||

| (35) |

Similarly, we let the data-and-feature-averaged bias and variance to be

| (36) | ||||

| (37) |

Fortunately, the KRR eigenframework gives us an equation for the data-averaged bias and variance: the data-averaged bias is the term in big parentheses in Equation 15, while the variance is the rest (see Simon et al. (2021)). This tells us that the data-averaged bias and variance are the following: (38) (39)

The more interesting case is perhaps the data-and-feature-averaged bias and variance. Jacot et al. (2020a); Canatar et al. (2021); Simon et al. (2021) found that the data-averaged predictor in the KRR case is simply , so in our case it will be

| (40) |

Taking the feature average, we conclude that

| (41) |

That is, . We thus conclude that the data-and-feature-averaged bias and variance are given as follows:

(42) (43)

E.6 Even at fixed ridge, more is better for bias terms

Increasing and (and keeping constant) strictly decreases both data-averaged and data-and-feature-averaged bias. To see this, we fist note the following proposition, which follows from Equation 2:

Proposition 1 (Derivatives of implicit constants).

Let . Then we have that

| (44) | ||||

| (45) | ||||

| (46) | ||||

| (47) |

In particular, note that when we increase , we decrease both constants.101010For this informal discussion, we will be a little fast and loose with terminology: when , we will find that these partial derivatives may be zero instead of strictly negative, and so when we say e.g. that a derived quantity increases with or , at zero ridge we really mean that it increases or remains the same. When we increase , we decrease but increase .

It is immediate from Equations 38 and 42 that increasing decreases both and . It is immediate also that increasing decreases , but since increasing decreases , it is not apparent that also decreases. However, we do not need to show this: it is apparent from Equation 68 that the bias of KRR is sample-wise monotonic in this sense for any task eigenstructure, and so RF regression (being simply a special case of KRR with stochastic task eigenstructure) will simply inherit this property. All together, we see that increasing either or will decrease both and . Any region of increasing error one encounters when increasing or — for example, at a double-descent peak — can thus be pinned on (one or another notion of) the variance.

Appendix F Taking limits of the RF eigenframework

In Section 4, we report an omniscient risk estimator giving the expected test risk of RF regression in terms of task eigenstructure. Here we demonstrate that, by taking certain limits, we can recover several previously-reported results from our general framework. For easier reference, we repeat Equations 2 here:

| (48) | ||||

| (49) |

F.1 The limit of large : recovering the KRR eigenframework

RF regression converges to ordinary KRR in the limit of large , and so we expect to recover the known KRR eigenframework. As , we find that . Therefore we can discard Equation 49 and find that simply satisfies as we get in the case of KRR.

Equation 3 reduces to

| (50) |

which is precisely the omniscient risk estimator for KRR (compare with e.g. Simon et al. (2021)).

F.2 The limit of zero ridge: recovering the ridgeless framework of Bach (2023)

Bach (2023) report an omniscient risk estimator for ridgeless RF regression. We should recover this result from our framework when we take . (Note that we cannot simply set as Equations 48 and 49 do not always have solutions, but we will have no trouble taking the limit .) Like Bach (2023), we will handle this in two cases.

Case 1: . When , we will still have even as . Observe that is determined by the constraint that . Plugging into Equation 48 gives us that

| (51) | ||||

| (52) |

Sticking in these substitutions into Equation 3 and simplifying substantially, we find that

| (53) |

which matches the result of Bach (2023).

Case 2: . When , we have that as . Therefore is determined by the constraint that . We also have that . Inserting these facts into Equation 3, we find that

| (54) |

This also matches the result of Bach (2023).

Remark. We can observe the following proposition from the above liimt of the RF eigenframework:

Proposition 2 (Monotonic improvement after the double-descent peak).

With , we have that

-

•

when ,

-

•

when .

Proof. First, let us take . From our discussion of “Case 1,” we see that further increasing will leave unchanged, which leaves unchanged. The only effect is thus to decrease the prefactor of the second term of Equation 53, which decreases .

Now let us take . From our discussion of “Case 2,” we see that further increasing leaves unchanged. It is similarly immediate from Equation 54 that the result is to decrease . ∎

Proposition 2 states that, at zero, ridge, increasing the larger of further can only improve test performance. Phrased another way, it’s all downhill after the double-descent peak. Though this fact is elementary, we do not know of any existing proof in the literature.

F.3 Student equals teacher: recovering the RF risk estimator of Maloney et al. (2022)

Maloney et al. (2022) work out a risk estimator for ridgeless RF regression under the “student equals teacher” condition that and . Inserting these into Equations 53 and 54 and exploiting the fact that when to simplify the resulting expressions, we find that

| (55) |

Again using the fact that , these can be further unified (using the notation of Maloney et al. (2022)) as

| (56) |

where is the unique nonnegative solution to with . This is the main result of Maloney et al. (2022).

F.4 High-dimensional isotropic asymptotics: the setting of Mei & Montanari (2019)

Here we compute the predictions of our framework in the setting of Mei & Montanari (2019), who study RF regression with isotropic covariates on the high-dimensional hypersphere. The essential feature of their setting is that task eigenvalues group into degenerate sets: we first have one eigenvalue of size , then eigenvalues of size , then eigenvalues of size , and so on. We take with with . In this setting, we expect to perfectly learn the 0th-order modes, partially learn the 1st-order modes, and completely fail to learn the higher-order modes.

Let denote the set of eigenvalue indices corresponding to degenerate level . Let be the total kernel power in level and to denote . Let be the total target power in level and to denote . Let us write etc. to denote the value of the degenerate eigenvalue at level .

In this setting, we will find that . Equation 2 simplify in this setting to

| (57) |

Here the hides terms that asymptotically vanish. These equations can be solved analytically or numerically for . Note that if one wishes to work in the large- limit, one might prefer to solve for and as follows:

| (58) |

The advantage of the above equations is that all quantities are after one replaces with the appropriate ratios.

One then has and . Let and . Equation 3 then reduces to

| (59) |

We expect this is equivalent to the risk estimate of Mei & Montanari (2019)’s Definition 1, as they solve the same problem, but we have not directly confirmed equivalence.

F.5 High-dimensional isotropic asymptotics: the setting of Mei et al. (2022)