Personalized Incentives with Constrained Regulator’s Budget

Abstract

We consider a regulator driving individual choices towards increasing social welfare by providing personal incentives. We formalize and solve this problem by maximizing social welfare under a budget constraint. The personalized incentives depend on the alternatives available to each individual and on her preferences. A polynomial time approximation algorithm computes a policy within few seconds. We analytically prove that it is boundedly close to the optimum. We efficiently calculate the Maximum Social Welfare Curve to achieve for a range of incentive budgets. This curve provides the right incentive budget to invest. We extend our formulation to enforcement, taxation and non-personalized-incentive policies. We analytically show that our personalized-incentive policy is also optimal within this class of policies and construct close-to-optimal enforcement and proportional tax-subsidy policies. We then compare analytically and numerically our policy with other state-of-the-art policies. Finally, we simulate a large-scale application to mode choice to reduce CO2 emissions.

keywords:

Personalized incentives; Knapsack problem; Tax policy; CO2 emissions; Modal shiftC61, H2, Q58, R41

This is an original manuscript of an article published by Taylor & Francis in Transportmetrica A: Transport Science on 23 Nov 2023, available at: https://doi.org/10.1080/23249935.2023.2284353.

1 Introduction

Taxes and subsidies in transportation are often perceived by the population as unfair, since they neglect the alternatives actually available to each individual and the individual preferences.111A preliminary version of this work was presented at the 2022 IEEE 25th International Conference on Intelligent Transportation Systems (ITSC), and a conference paper appears in the proceedings of that conference (Javaudin, Araldo, and de Palma 2022). On the other hand, with the increase in information available to governments (Clarke and Margetts 2014), economic policies can be improved to consider the peculiarities of each individual. Customized policies could be used to align the individual cost with the social cost in the individuals’ decisions, without penalizing anyone. We do not discuss here the legal dimension of such policies (which should be debated in the political arena).

We propose a policy of personalized incentives in a framework where individuals choose between multiple alternatives (or options). A benevolent regulator has a limited budget that he can use to propose monetary incentives, with the goal to induce individuals to change their choice toward socially-better ones. The policy we present is fair in the sense that no individual increases or decreases her utility. This is a clear advantage over road pricing, the most deployed demand management scheme, which usually decreases the utility of some individuals.

Consider a regulator aiming to induce car buyers to choose more environmentally-friendly car models. Suppose that two buyers, A and B, both consider buying a car with high CO2 emissions and suppose that buyer A (resp. buyer B) can be convinced to buy instead a car with low CO2 emissions if she gets a discount of $] (resp. of $]). With the policy of personalized incentives envisaged in this paper, the regulator could give $] (resp. $]) to buyer A (resp. to buyer B) if she accepts to buy the low-emission car. In this simple example, the regulator could convince the two buyers to choose the low-emission car for only $] ($] to buyer A and $] to buyer B), while, with a non-personalized subsidy policy, the regulator would need to spend at least $] to convince both buyers (each buyer receives $]). Hence, a personalized-incentive policy allows to reduce the average CO2 emissions by the same amount than a non-personalized policy, while spending less.

We define the optimal personalized-incentive policy as the allocation of incentives that maximizes social welfare (defined as the reduction of CO2 emissions in the example above), for a given budget. With two cars and two buyers, the optimal policy is easy to compute by simple enumeration. However, the problem is combinatorial so, with a large number of heterogeneous buyers and a large number of car models to choose from, we need more sophisticated methods.

We formalize the problem of finding a personalized-incentive policy maximizing social welfare under the regulator’s budget constraint and show that it reduces to the well-known Multiple-Choice Knapsack Problem (MCKP – see Section 3). The MCKP consists in packing ‘items’ of different ‘classes’ into a knapsack of a certain ‘capacity’. We show that the MCKP provides a natural formalization of an optimal incentive policy, where a class is an individual, an item is an alternative and the knapsack capacity is the budget of incentives. To approximate the optimal policy in polynomial time, we adapt a greedy algorithm from the Operations Research literature and we analyse some of its analytical (e.g., suboptimality gap bound) and economic (e.g., diminishing returns) properties (Section 4).

We then frame personalized-incentive policies into a larger family of demand management policies, including enforcement, tax and non-personalized-incentives (Section 5). These policies aim to maximize social welfare subject to a disutility constraint, where the disutility is the total loss of surplus for both the regulator and the individuals. We find that personalized-incentive policies are optimal within this larger family of policies. Moreover, they are ‘fair’, since they guarantee that the utility of each individual remains unchanged, and thus no one is penalized. We also compute a theoretical lower bound on the gap between state-of-the-art incentive policies, which are not personalized, and our personalized-incentive policy. Furthermore, we show that our greedy algorithm can not only construct incentive policies, but also enforcement and proportional tax-subsidy policies. We show that also in this case, the social welfare is boundedly close to the theoretical optimum. While in most of the paper we assume that the regulator knows exactly the preferences of each individual, we also study the case of imperfect information (Section 6).

Using data from the French census, we evaluate the CO2 reduction achieved via the policy computed with our algorithm in a large-scale use-case, where individuals are incentivized to shift toward greener transportation modes for their commute to work, at the scale of a French department (Section 7). The results confirm the theoretical findings, showing in particular that our personalized incentives achieve the same CO2 reduction as flat subsidies, but with a considerably smaller amount of incentives spent. Our code is available as open source.222https://github.com/LucasJavaudin/individualized-incentives-algorithm

Even though the case study is about modal shift, the proposed methods can be applied in various contexts. For example, consider the marketing department of a large firm selling mutually exclusive goods. To increase the profits of the firm, the marketing department could use its budget to propose price discounts to some consumers in order to convince them to shift to goods with higher margins. Another potential example of application is in the telecommunications management context. In recent years, governments are planning to subsidize local organizations to improve the access of rural population to the Internet (France alone will spend 3 billions euros in 10 years, Arcep 2021). With our methods, governments could allocate optimally these subsidies.

2 Related Work

We first discuss the literature on incentive policies (Section 2.1), in particular in transportation, which is the main application domain we envision. We then review the applications of the Multiple Choice Knapsack Problem, on which our optimization is based, in economics and transportation (Section 2.2) and, finally, in other domains (Section 2.3).

2.1 Incentive Policies in Transportation

Earlier studies of welfare analysis in a discrete-choice framework have been conducted by Small and Rosen (1981) and Anderson, de Palma, and Thisse (1992). De Borger (2001) studies the optimal taxation in a discrete-choice framework with externalities. His model is close to ours but he does not consider incentive policies. Some papers conduct an empirical study of an incentive policy in the transportation context (e.g., Merugu, Prabhakar, and Rama 2009, Ettema, Knockaert, and Verhoef 2010, Yue et al. 2015, Hu, Chiu, and Zhu 2015) but they do not carry out a theoretical study of the optimal policy.

Incentives are a promising tool for policy makers to trigger a transition toward greener transportation. Mirhedayatian and Yan (2018) model the reaction of a single logistics company to several incentives for buying and adopting electric vehicles. We are interested instead in calculating optimal incentives for a large plethora of individuals. A vast literature exists on time-varying incentives and/or surcharges to shift departure times, in order to reduce congestion. To this aim, Sun et al. (2020) adopt a bottleneck model of a road segment. Tang et al. (2020) propose an optimization model to calculate transit surcharges and incentives, during peak and off-peak, respectively, to avoid over-crowding. In the two aforementioned works, the incentives are not personalized, in that they do not depend on the individual’s profile and all the individuals go from the same origin to the same destination. We instead consider a large set of individuals, each with a different set of alternatives, resulting in different contributions to the social welfare and individual perceived utility. Our incentives are personalized, in that we encourage social-welfare maximizing alternatives with an incentive that compensate for the reduction in individual utility loss, which changes from an individual to another.

Closer to our work, Araldo et al. (2019) devise Tripod, a simulation-based optimization method to calculate incentives to encourage energy efficient transportation alternatives. However, the incentives do not depend on individual specificities. Indeed, the system computes a unique ‘Token Energy Efficiency’ (TEE) value, and computes the incentive for each alternative by simply multiplying the TEE by the estimated energy savings achieved with that alternative. Such approach is pertinent when the regulator has no information on the individual preferences. However, when perfect information is available, our approach is able to achieve the same social welfare of Tripod with less incentives spent or, equivalently, to achieve a larger social welfare with the same incentives spent. We show these findings both analytically (Section 5.2.3) and numerically (Section 7.6).

2.2 Multiple Choice Knapsack Problem in Economics and Transportation

The Multiple Choice Knapsack Problem (MCKP – Kellerer et al. 2004, chap. 11) can be used to model a decision maker willing to optimally invest a limited budget in order to increase an objective function. The possible investments options are divided into separate groups, and the decision maker has to choose at most one option for each group.

We now review the few examples of applications of MCKP in Economics and Transportation. Zhong and Young (2010) study the decision of a transportation planner willing to select a subset of candidate projects for funding. They do not propose any resolution algorithm and solve the problem in an exact way using a solver. Later, Colorni et al. (2017) use MCKP as a subroutine of a more general multi-criteria project-selection problem. Since the problem is NP hard (Kellerer et al. 2004, chap. 11), the aforementioned exact approach would require an unfeasibly large computation time in the large-scale applications we target. For this reason, we resort instead to a polynomial time approximation algorithm. Zoltners, Sinha, and Chong (1979, Sec. 6 and 7) use MCKP as a subroutine for a problem where a sales representative with a finite time-budget has to optimally allocate a call frequency to each accounts. They solve such a subroutine with an algorithm similar in spirit to our Algorithm 1, but in a more complicated setting, due to iterating decisions over multiple time-slots.

2.3 Multiple Choice Knapsack Problem in Computer Science and other Domains

MKCP is widely adopted in the Computer Science community, where a certain resource must be allocated among different entities. In the work of Cao, Brahma, and Varshney (2015), a central information aggregator receives information from several selfish sensors, which can transmit it at several precision levels: the more the precision level the higher the sensor cost in terms of energy. The aggregator needs to select one precision level (or none) per sensor and compensates the corresponding loss of energy of each sensor via payments. In Fielder et al. (2016), a manager of an information system invests in security controls. Per each control, it has to select a certain ‘level’: the higher the level, the higher the protection of the organization, but also the higher the investment. Araldo, Di Stefano, and Di Stefano (2020) allocate computational resources among different service providers; the owner of the resources selects one configuration for each of them in order to increase the overall system utility. To this aim, they use Multi-Dimensional Multiple-Node MCKP. Mohammadivojdan and Geunes (2018) solve the problem of a seller, who needs to decide the amount of product to buy from several providers, each proposing a different pricing scheme, in order to maximize its overall utility.

2.4 Position with respect to the Related Work

To the best of our knowledge, we are the first to formalize the problem of computing optimal personalized-incentives with MCKP. By finding the assumptions that enable such a formalization, we show in this paper that MCKP describes naturally such a problem, since it manages to represent the different alternatives of each individual. The adoption of MCKP also allows us to devise an efficient algorithm for large-scale applications, adapting existing solutions from Operations Research.

3 Framework and Personalized-Incentive Policy

In this section, we first formalize the model studied and present the underlying assumptions (Section 3.1). We also characterize the personalized-incentive policy that will be studied throughout this paper (Section 3.2). We then present the Maximum Social Welfare Problem, which consists in finding the optimal incentive policy under a budget constraint (Section 3.3). Finally, we present the Maximum Social Welfare Curve problem, which solves the previous problem for a range of budget values (Section 3.4).

The notations used throughout this paper are summarized in Table 1. All the proofs are relegated to Appendix B.

| Index to denote an individual | |

| Index to denote an alternative | |

| Alternative of individual | |

| , | Set of individuals and number of individuals |

| Set of alternatives available to individual | |

| Intrinsic utility of individual when choosing alternative | |

| Social indicator of alternative of individual | |

| Monetary transfer received (or paid) by individual when choosing alternative | |

| General policy (set of monetary transfers) | |

| Personalized incentive proposed to individual , conditional on choosing alternative | |

| Personalized-incentive policy (set of incentives) | |

| Set of all personalized-incentive policies | |

| Utility of individual when choosing alternative , given policy (1) | |

| Alternative chosen by individual , given policy | |

| Default alternative, i.e., alternative chosen by individual , in the absence of policy (5) | |

| Weight of alternative of individual , equation (8) | |

| Efficiency of alternative of individual (Definition 4.1) | |

| Maximum budget available to the regulator | |

| Budget actually spent by the policy computed by Algorithm 1 | |

| Maximum social welfare reachable with a personalized-incentive policy, | |

| with a total incentive expenditure of | |

| Social welfare obtained with the personalized-incentive policy produced by our algorithm, | |

| with a total incentive expenditure of | |

| Social welfare achieved with a policy , equation (2) | |

| Expenses of the regulator for a policy , equation (3) | |

| Total variation in individual utility of a policy , equation (18) | |

| Disutility of policy , equation (19) | |

| , | Set of LP-extremes alternatives of individual , and its cardinality |

| Incremental social indicator of the alternative of individual | |

| Incremental incentive of the alternative of individual | |

| Incremental efficiency of the alternative of individual | |

| Incremental efficiency of the split item (Algorithm 1) | |

| Iteration index of Algorithm 1 | |

| Overall and incremental efficiency of Algorithm 1 at iteration (Definition 4.6) | |

| Tax level (Section 5.2.2) | |

| Baseline social-indicator of individual (Section 5.2.2) |

3.1 Model and Assumptions

We consider a population of individuals. Each individual chooses an alternative among an individual-specific choice-set . For example, we can consider individuals choosing a mode of transportation to commute to their work. In this case, the choice set could be . The choice set can be individual-specific so that if individual owns a car but individual does not, we could have and . The mode-choice example is studied extensively in Section 7. As another example, could be a set of individuals purchasing a car. In this case, the set of alternatives of individual would include the models of cars available in the market.

Let be a monetary transfer, from the regulator to individual , induced when she chooses alternative . This monetary transfer can be an incentive, if positive, or a tax, if negative. Any policy can thus be described by a set of monetary transfers proposed to all the individuals for any of their alternatives, which we compactly denote with .

A policy influences the individual choice since the proposed monetary transfers change her utilities.

The utility of individual when choosing alternative is given by

| (1) |

where is the intrinsic utility (in the absence of policy). We implicitly assumed that utility is quasi-linear with respect to income, which means that both and are expressed in the same unit as income and that has an additive effect on utility, hence equation (1).

Given a policy , each individual chooses an alternative which maximizes her utility:

We consider a regulator aiming to maximize a social welfare indicator, whose value depends on the individuals’ choices. More formally, each alternative of individual is characterized by a social indicator . In the mode-choice example, the social indicator could be the opposite of CO2 emissions induced by the commutes.

The goal of the regulator is to find a policy which maximizes the global social indicator, or social welfare indicator, defined by

| (2) |

i.e., the sum of the social indicators of the alternatives chosen by the individuals. Intuitively, a policy which maximizes welfare could be

which is equivalent to a ban of all alternatives that do not maximize the social indicator for each individual. However, in practice, the regulator is affected by some political constraints and such extreme policy is not feasible.

Definition 3.1 (Expenses).

For any policy , we define the expenses of the regulator (or his revenues ) as

| (3) |

i.e., the sum of the monetary transfers paid or received for the alternative chosen by each individual .

The following assumptions are made. First, we assume that individuals cannot affect each other’s intrinsic utility.

Assumption 3.2 (Independent intrinsic utilities).

Given a policy , for each individual and each alternative , the intrinsic utility is independent of the alternative chosen by any other individual .

Similarly, we assume that the social indicator of the alternatives is independent of the choices of the individuals.

Assumption 3.3 (Independent social indicators).

Given a policy , for each individual and each alternative , the social indicator is independent of the alternative chosen by any other individual .

Note that Assumptions 3.2 and 3.3 hold in many practical situations. For instance, in the numerical scenario on transport mode choice (Section 7), we achieve relevant social welfare improvement (CO2 reduction), while inducing only few individuals to change their modes, with a negligible impact on the utilities of the other individuals.

We further assume that the utilities and social indicators are known to the regulator.

Assumption 3.4 (Perfect information).

The regulator has perfect information: it knows exactly the intrinsic utilities and social indicators of all the alternatives, for all the individuals.

In Sections 6 and 7 we discuss the implications of assumption 3.4 in the context of mode choice and we show how to relax it by more realistically assuming that the intrinsic utilities are imperfectly known to the regulator. Developing our theoretical framework under Assumption 3.4 allows us to develop optimization algorithms that can then be applied, mutatis mutandis, also to the realistic case when Assumption 3.4 does not hold, as we show in Section 7.7.

With no loss of generality, we rule out identical alternatives.

Assumption 3.5 (No identical alternatives).

We assume that, for any individual , there are no identical alternatives , i.e., such that and .

We need to characterize more precisely the behaviour of individuals when multiple alternatives maximize their utility.

Assumption 3.6 (Tie-breaking rule).

For any policy , if the set contains more than one alternative, individual chooses the alternative with the largest social indicator, i.e.,

| (4) |

The previous assumption is merely a technical assumption that could be relaxed by proposing incentives infinitesimally larger to ensure that the set is always a singleton.

The alternative chosen by each individual in the absence of policy (i.e., where , ) is called default alternative, and denoted . Under Assumption 3.6, the default alternative is given by

| (5) |

3.2 Personalized-Incentive Policies

We assume that the space of policies available to the regulator is limited to policies such that , for each alternative and individual . In other words, the regulator never taxes alternatives, for some political reasons. Note that we allow the regulator to give different monetary transfers to different individuals for the same alternative (e.g., some individuals might receive $] for commuting by foot, while others may only receive $]). Hence, this space of policies is referred to as the set of personalized-incentive policies, denoted . To distinguish personalized-incentive policies from more general policies, we denote them with , where is the incentive given to individual , conditional on her choosing alternative , and thus,

The incentive reduces the budget of the regulator only if individual chooses alternative . Therefore, if the regulator wants to spend at most a budget , the budget constraint can be written as

where is the alternative chosen by individual under the personalized-incentive policy .

In the rest of this subsection, we characterize more precisely the set of policies we consider, discarding ‘inefficient’ policies.

Proposition 3.7.

The regulator can induce any individual to shift from her default alternative to any alternative , with a higher social indicator (i.e., ), by proposing the following incentives

| (6) |

Additionally, , defined above, is the minimum incentive required to induce individual to shift to alternative .

Such a proposition tells us that it suffices to incentivize only one alternative per individual and no more than that. Therefore, we can limit the space of the studied personalized-incentive policies as in the following assumption, with no loss of generality.

Assumption 3.8.

We only study in this paper personalized-incentive policies that propose incentives in the form of (6), i.e., only one alternative per individual is incentivized, with an incentive equal to .

Remark 1.

With no loss of generality, we can remove from any individual choice-set the alternatives that are never chosen, as the ones defined below.

Proposition 3.9 (Pareto-dominance).

Let us consider individual facing two alternatives . Alternative is said to be Pareto-dominated by if and . Alternative is Pareto-dominated, if it is Pareto-dominated by some other alternative.

A personalized-incentive policy that incentivizes a Pareto-dominated alternative can be discarded, since there always exists another policy that obtains at least the same social welfare, by spending less budget.

We thus exclude Pareto-dominated alternatives from the choice-set of each individual , as they would never be chosen by individuals, under the considered policies.

Assumption 3.10 (No Pareto-dominated alternatives).

For any individual , there are no Pareto-dominated alternatives in her set of alternatives .

3.3 Maximum Social Welfare Problem

We can now formally define the optimization problem of the regulator, who chooses the personalized-incentive policy which maximizes social welfare under his budget constraint. We refer to this problem as Maximum Social Welfare Problem:

| (7) |

Definition 3.11 (Optimal personalized-incentive policy).

An optimal personalized-incentive policy , for a budget , is a solution of Problem 7.

We denote with a chosen-alternative set, where denotes the alternative chosen by individual . According to Proposition 3.7, the regulator can induce any chosen-alternative set by proposing to any individual the incentives and , for any . Thanks to the same proposition, the regulator cannot induce this set of alternatives by spending less. Therefore, the optimization problem of the regulator (7) amounts to finding the chosen-alternative set which maximizes social welfare , subject to the constraint that the corresponding spendings must not exceed the budget .

Such a problem can be expressed as an Integer Linear Program (ILP). In order to do so, we introduce a weight for any alternative of individual . The weight is defined as the incentive amount that would be proposed to individual if the regulator were to induce her to choose alternative , which is, according to Proposition 3.7,

| (8) |

Note that is a fixed value that we used to compute the optimal policy, while represents the incentive amount chosen by the regulator. The personalized-incentive policy is such that , if individual is induced to choose alternative , and otherwise.

We introduce the binary decision variable that is equal to if the regulator wants to make individual choose alternative , and that is equal to otherwise, with the natural constraint that (only one alternative is chosen). The Maximum Social Welfare problem (7) can be written as

| (9) |

which is a Multiple-Choice Knapsack Problem (MCKP) with weights and profits (Kellerer et al. 2004, chap. 11).

Observe that the solution of problem (9) corresponds to the personalized-incentive policy , solution of (7), where

For any budget , we indicate with the maximum of the social welfare, solution of problem (9).

3.4 Maximum Social Welfare Curve Problem

Suppose now that the regulator is endowed with a maximum budget and that he can spend any budget in the interval . To decide the exact amount of budget that is convenient to spend, it is useful to obtain the Maximum Social Welfare Curve , representing the maximum social welfare reachable, , for any budget , i.e.

| (10) |

The Maximum Social Welfare Curve Problem consists in finding the curve , for a given maximum budget . It is easy to show that it is monotone non-decreasing (the larger the budget spent, the larger the social welfare reached). Observe that, although a maximum budget is available, the regulator may not want to indiscriminately spend it all, but may choose the actual budget to invest in incentives, based on several criteria. For instance, the regulator may use the above curve to find the minimum budget needed to reach a certain social-welfare target. Moreover, in many practical cases, the social welfare is converted into money metric. The coefficient of conversion is usually fixed based on political considerations. For instance, in our numerical results (Section 7), we convert CO2 emission reduction into money, using the cost of 100 euros per ton of CO2. After converting social welfare in money metric, the regulator may choose to invest an incentive budget such that the gain of social welfare equals the incentive spent. Such a value can be found on the Maximum Social Welfare Curve.

4 Approximation Algorithm

Kellerer et al. (2004) shows that the MCKP problem, and thus the Maximum Social Welfare problem (9), is NP-hard. Therefore, for large instances of such problems, finding the optimal solution is unfeasible and we need to resort to heuristics. We provide in this section a polynomial time algorithm based on greedy algorithms from the Operations Research literature, which gives us solutions boundedly close to the optimum. We then discuss some relevant properties of such an algorithm, e.g., its diminishing returns behaviour and the fact that it is an anytime algorithm (explained in Remark 2).

In the following subsection, we introduce some preliminary mathematical concepts.

4.1 Preliminary Steps

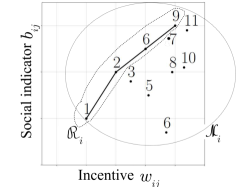

Before presenting the proposed algorithm, we need to ‘clean’ the input of the problem, removing some irrelevant alternatives from the set of the alternatives of any individual . In broad terms, irrelevant alternatives are the ones that do not provide enough social indicator compared to the incentive amount needed to induce them. We call LP-extremes the alternatives remaining after the cleaning, and we denote them with . The name LP-extremes is borrowed from Kellerer et al. (2004, Section 11.2.1).

The process of constructing the set is called concavization and is described in detail in Appendix A. Here we just give the reader an intuition of it via Figure 1, which represent the incentive amount and social indicator for a set of alternatives , of an individual . In the figure, alternative is irrelevant since provides a larger social indicator, while requiring less incentive. Alternative is irrelevant since it requires to spend more incentive than , for a negligible gain in the social indicator. It is much more convenient to make a slightly bigger investment to induce alternative , which provides a significant social indicator improvement with respect to . More formally, we say that is LP-dominated by and (see Appendix A for more details).

We follow the Operations Research literature in the slight abuse of notation of denoting with the incentive to be provided to the -th alternative in , where this is not ambiguous. With no loss of generality, we can assume the ordering

| (11) |

in the set , where is its cardinality. The default alternative of any individual is neither dominated nor LP-dominated, since it requires no incentive (). Therefore, the default alternative is the first alternative in the set and .

Definition 4.1 (Efficiency and incremental efficiency).

We define the efficiency of an alternative of individual as

i.e., the gain in social indicator that we can gain via a unit of incentive allocated to that alternative. We define the incremental social indicator and the incremental incentive required for each alternative as

| (12) |

The incremental efficiency is then defined as

| (13) |

The incremental efficiency can be interpreted as the increase in social welfare for each monetary unit spent, when individual shifts from alternative to alternative .

4.2 Greedy Algorithm

We want to find a curve that approximates the Maximum Social Welfare Curve (10), i.e., such that is close to for any value of budget .

Very efficient algorithms, like the Dyer-Zemel algorithm (Kellerer et al. 2004, Section 11.2.1) are known to solve problem (9), i.e., to approximate the maximum social welfare for a fixed single value of budget . However, to apply them to the Maximum Social Welfare Curve problem, in which we want to find the maximum social welfare for a range of budget values , instead of just one, we would have to run those algorithms from scratch for every single value of budget. For this reason, we build our solutions upon a simpler greedy algorithm (Kellerer et al. 2004, Figure 11.2), which is less efficient to solve the Maximum Social Welfare problem (although still polynomial in time complexity), but easily extendable to also solve the Maximum Social Welfare Curve problem. The other advantage deriving from such choice is that this greedy algorithm has interesting properties that increase its practical application and economic interpretability, as discussed in Section 4.3.

The pseudocode of the algorithm is in Algorithm 1. The notation stands for ‘-th alternative of individual ’. The idea of the algorithm is simple. First, the algorithm finds all the LP-extremes alternatives and sorts them by order of decreasing incremental efficiency. Then, at each iteration, the next pair of individual and alternative with the highest incremental efficiency is picked (line 1). The alternative induced to is set to (line 1) and the budget is reduced by the amount of the incremental weight (equation (14)). An additional piece of the approximation of the social welfare curve is computed (equation (16)). The algorithm stops when the maximum budget is depleted and it returns a policy , which is such that any individual , for whom the algorithm selected an alternative , effectively chooses this alternative .

| (14) | |||||

| (15) | |||||

| (16) | |||||

Observe that the curve given as output by the algorithm is an approximation of the solution of the Maximum Social Welfare Curve Problem (Section 3.4). Moreover, given any maximum budget , the algorithm returns an approximation to the solution of the Maximum Social Welfare Problem (9). Note that, in order to achieve , the policy issued by the algorithm does not spend the entire maximum budget , but only .

The algorithm also gives as output the incremental efficiency of the ‘split item’, denoted with , useful to compute the optimality gap of the algorithm (Theorem 4.2 below). The name split item, which we borrow from Kellerer et al. (2004), reminds of the fact that, when we allocate the budget , we add to the solution all the LP-extreme alternatives, in decreasing order of incremental efficiency, up to . In other words, such alternative splits the set of all the LP-extremes in two parts: the first part consists of the alternatives we include in our solution, while we do not include the LP-extremes from the second part.

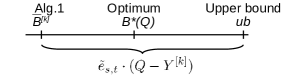

The distance to the optimum, in terms of social welfare, is bounded from above.

Theorem 4.2 (Upper bound).

Corollary 4.3.

The next corollary says that, for any budget , the curve returned by Algorithm 1 and the Maximum Social Welfare Curve ‘touch each other’. This ensures that the allocation computed by Algorithm 1 at every iteration is optimal. It is a direct consequence of Theorem 4.2.

Corollary 4.4.

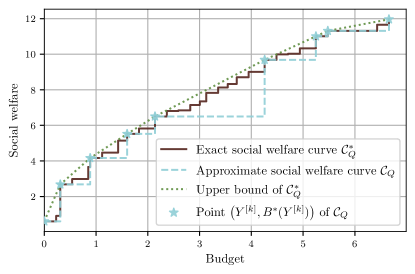

Figure 2 illustrates this property. The continuous curve represents the Maximum Social Welfare Curve and the dashed curve represents the curve obtained via Algorithm 1. These two curves are step-functions because of the discreteness of the problem. From Corollary 4.4, the curve intersects the curve at each iteration of the algorithm (represented by the stars). The dotted curve represents the upper bound of , computed from Theorem 4.2.

4.3 Useful Properties for Large-Scale Applications

Our aim is to compute a personalized-incentive policy in large scenarios in a small amount of time. It is therefore crucial to show that our algorithm is computationally efficient.

Proposition 4.5.

The computational complexity of Algorithm 1 is , where is the number of individuals, is the number of alternatives of individual , is the number of LP-extremes of individual and .

Note that, since the alternatives of each individual are independent of the others, the sets can be computed in parallel, thus reducing even further the computation time.

Despite our algorithm being computationally efficient, there might be cases in which it is desirable to stop it prematurely, without waiting for it to completely terminate. This can be the case when a personalized-incentive policy must be computed on-the-fly, within tight time-constraints. The following properties ensure that our algorithm is suitable to this situation, which eases its practical adoption.

Remark 2 (Anytime algorithm).

Algorithm 1 is anytime: if we stop it prematurely at any iteration , we get a valid solution for the Maximum Social Welfare and the Maximum Social Welfare Curve problems, with budget .

Remark 3 (Incremental use).

Another desirable property of Algorithm 1 is that we can build on a previously computed incentive allocation whenever new available budget becomes available, instead of recomputing the entire allocation from scratch. To explain this, let us suppose that we have a certain budget and the algorithm returns the allocation , spending the corresponding incentive amount . Suppose now that the available budget increases to . In this case, in order to exploit the new additional budget, we can simply resume the algorithm from its last iteration and continue up to the furthest iteration such that . This is, per-se, a computational advantage with respect to algorithms that need to run from scratch every time new resources (budget) are available.

In order to describe the diminishing return property of Algorithm 1, we need the following definition.

Definition 4.6 (Incremental and overall efficiency).

The incremental efficiency provided by the algorithm at iteration is , defined in equation (15). We define the overall efficiency of a personalized-incentive policy spending budget and achieving social welfare as . We denote with the overall efficiency of the policy obtained by stopping Algorithm 1 at iteration , i.e., .

The following proposition illustrates that, by spending more and more budget and allocating it as the algorithm dictates, we increase social welfare, but the marginal gain per unit of budget spent decreases.

Proposition 4.7 (Diminishing returns).

The incremental efficiency and the overall efficiency of the alternative added by Algorithm 1 at every iteration are both monotonically non-increasing.

The following corollary is a consequence of Proposition 4.7.

Corollary 4.8.

At any iteration , we can compute an upper bound to the social welfare we would get if we continue the algorithm until the end. Such an upper bound is .

Therefore, if we notice that is already sufficiently close to , then it is not worth continuing the algorithm, as we would not get much additional social welfare. In this case, we can safely stop the algorithm, without waiting for it to end, thus saving time.

In some cases, the regulator would be willing to maximize social welfare under the constraints that the overall inverse efficiency is below a certain target. For instance, in Section 7.5 the regulator does not want to spend more than 100 euros per ton of CO2 saved, which is considered to be the carbon price. In such cases, it is useful to observe that, thanks to Proposition 4.7, is non-decreasing. Therefore, the regulator could run the algorithm and stop at the iteration where goes above the target inverse efficiency.

We close this section with a definition that will be useful in Section 5.

Definition 4.9 (Maximum Step Size and Characteristic Incremental Efficiency).

Let us run Algorithm 1 with a certain budget and record the values calculated therein, as well as the incremental efficiency of the split item . The maximum step size is defined as . The characteristic incremental efficiency of budget is defined as .

The properties presented in this section have shown that the proposed Algorithm 1 is computationally efficient and able to return an allocation providing a welfare close to the optimum. Moreover, it has some features that make its adoption easier in practical large-scale scenarios.

5 Comparison with Other Policies

So far, we have considered that the regulator uses personalized incentives to increase social welfare. In particular, the policy proposed is such that the loss in individual utility, due to the shift to another alternative, is compensated exactly by the incentive. In this section, to frame our proposed personalized-incentive policy into a more general set of feasible policies, we generalize the formulation to include not only personalized incentives, but also enforcement policies, taxation, and non-personalized-incentive policies. In Section 5.1, we show that any optimal personalized-incentive policy (Definition 3.11) is optimal in this more general class of policies. In Section 5.2, we show that Algorithm 1 can be used to compute an enforcement policy and a proportional tax-subsidy policy, which are both boundedly close to the optimal general policy. We finally analytically show that non-personalized-incentive policies, like Tripod (Araldo et al. 2019), achieve by construction less social welfare than our personalized-incentive policy, and we provide a lower bound to this social welfare gap.

5.1 Optimality of Personalized-Incentives Policies among General Policies

We now consider a more general space of policies, including incentives, enforcement and taxation policies, and we define a criteria of optimality in this space. In order to do so, we need to define some new quantities.

The total loss in individual utility, of a policy , is

| (18) |

With a taxation policy, i.e., a policy such that , , the loss in individual utility is non-negative, i.e., . With an incentive policy, i.e., a policy such that , , the loss in individual utility is non-positive, i.e., . In particular, in any personalized-incentive policy obeying to Proposition 3.7, the individuals are perfectly compensated for their loss in utility, and thus , in accordance with Remark 1. Keeping everything else fixed, it is obvious that, the smaller , the better.

The disutility, or cost, of a policy is measured by combining the loss in individual utilities and the expenses for the regulator, defined in equation (3).

Definition 5.1 (Disutility).

The disutility of a policy is defined as the expenses of the regulator plus the total loss in individual utilities , i.e.,

| (19) |

The following proposition shows that the disutility of a policy is always non-negative, which means that it is not possible that both the individuals increase their utility and the regulator collects revenues. It also shows that, if two policies imply the same alternatives chosen, then they have the same disutility.

Proposition 5.2.

Every policy has a non-negative disutility that only depends on the alternative chosen by the individuals, rather than the actual incentive or taxation proposed. In particular:

We can now define an optimal general policy, whose definition includes incentive, taxation and enforcement policies.

Definition 5.3 (Optimal General Policy).

An optimal general policy with disutility threshold is the solution of the following problem:

| (20) |

Note that, problem (20) is a generalization of (7). Indeed, we obtain the latter from the former by (i) constraining the policy to be a personalized-incentive policy, i.e., and (ii) imposing no change in individual utility, i.e., .

The two next propositions characterize the optimal general policy. The first one implies that finding an optimal general policy is equivalent to finding a chosen-alternative set which maximizes social welfare, subject to a disutility constraint.

Proposition 5.4.

Let be an optimal general policy with disutility threshold . Any other policy inducing the same alternatives is also an optimal general policy, independent of the actual value of the single incentives or taxes proposed.

The following proposition shows that the personalized-incentive policy, considered previously, is still relevant in this more general framework. The proposition states that, for any disutility threshold , it is possible to find an optimal policy which is a personalized-incentive policy.

Proposition 5.5.

The following corollary states that the social welfare bound for personalized-incentive policies (Theorem 4.2) is equivalent for general policies.

Corollary 5.6.

Let us run Algorithm 1 with budget to construct a personalized-incentive policy. The social welfare we obtain is boundedly close to the optimum , obtainable with an optimal general policy with disutiliy threshold . In particular,

5.2 Computing Optimal Enforcement and Proportional Tax-Subsidy Policy

In this section, we show how Algorithm 1 can be used, in conjunction with Propositions 5.5 and Corollary 5.6, to compute an enforcement policy and a proportional tax-subsidy policy boundedly close to the optimum.

We provide a numerical comparison between these policies in Section 7.6.

5.2.1 Enforcement Policy

With enforcement policies, the regulator constrains the individuals to choose an alternative among a subset of their choice set. In the most extreme case, the individuals can choose only one alternative.

Let be the personalized-incentive policy returned by Algorithm 1, for a budget . Consider now a policy enforcing the individual to choose the same alternative that they would choose under the policy , i.e.,

Proposition 5.7.

The enforcement policy constructed above is boundedly close to an optimal general policy with disutility constraint . The bound is the same as Corollary 5.6.

5.2.2 Proportional Tax-Subsidy Policy

We consider here policies for which the monetary transfers are proportional to the social indicator of the alternatives, that is

| (21) |

where is the tax-subsidy level and is an individual-specific baseline social-indicator, set by the regulator. We call these policies proportional tax-subsidy policies. Observe that, for any individual , her alternatives such that the social indicator is below the baseline are taxed (i.e., ). Conversely, alternatives having social indicator above the baseline are subsidized (i.e., ). The baseline social-indicators can vary from individual to individual. However, we impose that the tax-subsidy level is the same for everyone. In this sense, we consider that these policies are not personalized.

Observe from equations (1) and (21) that, considering any individual , if we vary the baseline the variation of the utility is the same for all alternatives . Hence, the value of does not impact the choice of . It simply represents a monetary transfer between the individual and the regulator. More precisely, setting low favours transfers from the regulator to individuals, thus increasing individual utilities, to the detriment of the regulator. On the other hand, setting high , favours the revenue of the regulator, to the detriment of the utility of the individuals.

Note that, if represents a negative externality (as in Section 7), then the tax-subsidy policy defined above is equivalent to a Pigouvian tax if is set to be equal to the external marginal cost of the externalities and . For instance, it has been estimated (Quinet et al. 2009), that the social cost of 1 ton of CO2 is 100 euros. Then, if represents CO2 emissions (in tons), the Pigouvian tax would be a proportional tax-subsidy policy with euros.

The following theorem shows that we can use Algorithm 1 to compute a proportional tax-subsidy policy that is boundedly close to the theoretical optimum.

Theorem 5.8.

We can construct a proportional tax-subsidy under a certain disutility threshold as follows. Run Algorithm 1 with budget constraint and let be the incremental efficiency of the split item given as output.

5.2.3 Comparison with Proportional-Incentive Policy and Tripod

A proportional-incentive policy is a proportional tax-subsidy policy, as in (21) where only subsidies and not taxes are distributed, i.e.

| (23) |

An example of proportional-incentive policy is Tripod (Araldo et al. 2019).

In this section we show that proportional-incentive policies are inefficient incentive policies, in the sense that, to achieve a certain social welfare level, they spend more incentives than needed. We call ‘inefficiency gap’ this additional incentive spent and we compute a lower bound for it in the following proposition.

Proposition 5.9.

Consider a proportional-incentive policy as before. There always exists a personalized-incentive policy that is able to achieve at least the same social welfare and provides the following savings in the amount of incentive spent:

where is defined as efficiency loss, . The quantity defined above is a lower bound for the inefficiency gap.

Note that the efficiency loss quantifies the fact that proportional-incentive policies are not able to exploit the inherent efficiency (see Definition 4.1) of the incentivized alternative. Indeed, instead of using such an alternative-dependent efficiency, they use a single value .

We compute in the following proposition a lower bound on the suboptimality gap of proportional-incentive policies.

Proposition 5.10.

Let us consider a proportional-incentive policy , achieving a social welfare and spending an incentive amount . Let us denote with the maximum social welfare achievable by an optimal personalized-incentive policy with that incentive amount. The following lower bound holds on the suboptimality gap:

where and are the maximum step size and the characteristic incremental efficiency, as defined in Definition 4.9.

We now draw an interesting parallel with Tripod, a proportional incentive policy described in Araldo et al. (2019). In Tripod, social welfare is represented, in particular, by energy reduction. While our formulation is general and can encompass any type of social welfare (provided that the assumptions of Section 3 are valid) in our case study (Section 7) we consider CO2 reduction. In both our case study and Tripod, individuals are travellers and alternatives are modal choices. An important aspect of Tripod is that it is dynamic, i.e., time is slotted and, in each time slot, the incentives for the individuals happening to depart in that time slot are calculated. With the Tripod policy, that we denote , the incentives proposed to individuals are proportional to the gain in the social indicator with respect to the default alternative, i.e.

where the constant is called Token Energy Efficiency and is fixed by the regulator in every time slot . In Tripod, the incentives are distributed to individuals under a First-Come First-Served discipline, until a certain budget is depleted. Therefore, out of the entire population of individuals departing at time slot only a subset actually receive an incentive. In Araldo et al. (2019), the value of is fixed empirically, with a grid search, trying several values of in simulation and choosing the one with maximum social welfare. The calculation is based on a Model-Predictive Control (MPC) setting, where at every time slot the value of is calculated taking into account not only the current time slot, but also a prediction of the system state (congestion, individual arrival) in the subsequent time-slots, which are called optimization horizon. Note that the MPC setting of Tripod allows to take into account the impact of the incentive policies on congestion, which we instead neglect, based on Assumptions 3.2 and 3.3. Therefore, for adopting our policy to a real scenario, care should be taken in checking that such Assumptions are reasonable, as we do in our case study.

Within our framework, Tripod can be defined as a proportional-incentive policy, with and , applied to population .

As a consequence of Proposition 5.9, Tripod is an inefficient incentive policy, under the assumptions of Section 3.1. In Corollary 5.11, we lower-bound the additional incentive spent with respect to the theoretical best incentive policy.

Corollary 5.11.

For any Tripod incentive policy , there always exists a personalized-incentive policy that is able to achieve at least the same social welfare while spending less incentives. The saving in the incentives is:

where is defined as efficiency loss, and is the set of individuals getting incentives in Tripod in time-slot .

Corollary 5.11 shows that Tripod is far from minimizing the incentives needed to obtain a certain social welfare, while the policy issued by Algorithm 1 is generally close to using minimal incentives. This is confirmed by our numerical results in Section 7.6. An interpretation of the inefficiency suffered by Tripod follows.

Remark 4.

Tripod uses a single value to compute incentives for all alternatives of all users and gets additional units of social welfare per additional unit of incentive spent. The only incentivized alternatives are the ones for which (otherwise the proposed incentive would not be accepted by the individual). In other words, Tripod gets always an efficiency (unit of social welfare improvement over unit of incentive spend) that is lower than the intrinsic efficiency of the incentivized alternatives. By contrast, our personalized policy always entirely exploits the intrinsic efficiency of the incentivized alternatives.

Since Tripod is a proportional-incentive policy, the same lower bound on the suboptimality gap as in Proposition 5.10 also holds, which we do not write for the sake of space.

6 Imperfect Information

The assumption that the regulator knows perfectly the utility of the individuals may seem restrictive. In this section, we show that the algorithm is still relevant when the utility is imperfectly known. From discrete-choice theory (Anderson, de Palma, and Thisse 1992), we assume that intrinsic utility of alternative of individual is composed of a deterministic part and a random part :

We assume that the regulator knows the deterministic part of the utility but not the random part .

Under this assumption, the regulator cannot compute the minimum incentive amount needed to induce individual to shift from her default alternative to another alternative , using directly equation (6). A heuristic solution would be to set the incentive amount equal to the expectation of the utility difference between the two alternatives, given that is the default alternative chosen when there is no incentive. In this case, the incentives proposed by the regulator to individual , to convince her to shift to alternative , are such that , for any , and

| (24) |

where is the difference in the deterministic part of the utility, known to the regulator.

Given an individual and an alternative , if the regulator proposes the incentive , as defined by equation (24), then individual has a positive probability to refuse the incentive. Hence, the expenses of the regulator may be smaller than the total incentive amount proposed.

Algorithm 1 can be used to compute a personalized-incentive policy under imperfect information, by defining new weights

At each iteration of the algorithm, the regulator proposes the incentive to individual for alternative , where is the pair of individual and alternative selected by the algorithm. The regulator observes the response of the individual to the incentive. If the individual accepts the incentive, it decreases the budget by the incentive amount. The regulator keeps proposing incentives one by one until his budget is depleted.

Note that, if an individual accepts an incentive for alternative , the regulator can still propose her, later, an incentive for another alternative . If the individual refuses the second incentive , she still receives the first incentive .

In Section 7.7, we apply the policy presented above to our case study and compare it to the case with perfect information, assuming that random terms are Gumbel-distributed. The following proposition gives the exact expression of the incentives (24), in case of Gumbel-distributed random terms.

Proposition 6.1.

Let us assume that the random terms are i.i.d. and follow a Gumbel distribution with scale parameter (i.e., follows a standard Gumbel distribution). Then, the incentive amount from equation (24) can be written as

7 Numerical Results in an Application to Mode Choice

In this section, we simulate an application of our personalized incentive policy to a scenario related to mode choice of individuals commuting to their workplace. We consider a regulator willing to employ a limited monetary budget in order to promote eco-friendly modes of transportation. The goal of the regulator is to reduce CO2 emissions. We compute the reduction in CO2 emissions achieved via the personalized-incentive policy of Algorithm 1 and compare it with enforcement, proportional taxation and non-personalized-incentive policies.

Our approach is as follows. After describing the census data used to build the simulation scenario (Section 7.1), we estimate a Multinomial Logit model for mode choice (Section 7.2). Then, using the previous estimates, we simulate the utility of a home-work trip for a group of individuals, for all the modes of transportation considered (Section 7.3). We then approximate the CO2 emissions for these same trips (Section 7.4) and approximate the optimal personalized-incentive policy using Algorithm 1 (Section 7.5). We then study the modal shifts induced by such policy and the gain in CO2 emissions achieved. We conclude the numerical results by comparing our personalized incentive policy with other policies (enforcement, taxation, flat incentives – Section 7.6) and by evaluating its performance in case of imperfect information (Section 7.7).

7.1 Data

We use census data from the French statistics institute INSEE, regarding households surveyed between 2015 and 2019. We restrict the dataset to households whose home and workplace are in the Rhône department, which includes Lyon and its suburbs (about households in total). Observed variables include city- or district-level home and work location, main mode of transportation used for commuting, and some socio-demographic variables. The modes of transportation are divided in five categories: car, public transit, walking, cycling and motorcycle. Appendix C provides a detailed description of the data.

7.2 Multinomial Logit Model

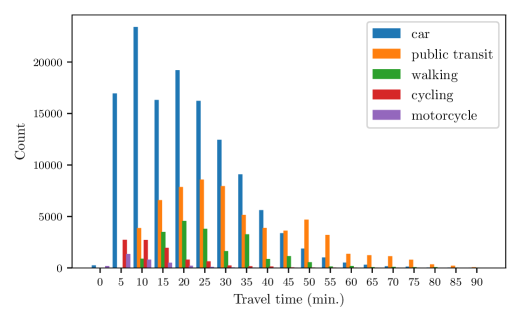

Using the census data, we estimate a Multinomial Logit model for the mode choice of the individuals. We consider five exogenous variables specific to the individual (age, sex, number of cars owned per employee in the household and professional occupation) and one exogenous variable which is specific to both the mode of transportation and the individual (travel time). The number of cars owned is supposed to only impact the utility of commuting by car. Following Inoa, Picard, and de Palma (2015), we also include interaction variables between travel time and socio-demographic variables. Details on how travel time is computed are provided on Appendix D. To estimate the utility of the round trip to work, travel times are doubled (we assume that the modes of transportation for the trip back and forth are the same).

Note that public transit is excluded from the choice set of the individuals whose commute to work cannot be performed by public transit ( individuals, see Appendix D for more details).

The four other modes of transportation (car, walking, cycling and motorcycle) are assumed to be in the choice set of all the individuals. This is a strong assumption. A regulator willing to deploy the personalized-incentive policy in practice could improve the precision of the model by using individual-specific data for vehicle ownership in order to remove some modes of transportation from the choice set of an individual, if she does not own the corresponding vehicle.

Table 2 provides the results of the Multinomial Logit model, estimated with the R package mlogit. The most frequent categories are used as reference category (car for the mode of transportation, man for the sex and employee for the occupation).

| (1) | (2) | (3) | (4) | (5) | |

|---|---|---|---|---|---|

| car | public_transit | walking | cycling | motorcycle | |

| constant | 2.7709*** | 2.8659*** | 1.1340*** | -0.7284*** | |

| (0.0395) | (0.0488) | (0.0509) | (0.0773) | ||

| age | -0.0150*** | -0.0026*** | -0.0139*** | -0.0019 | |

| (0.0008) | (0.0009) | (0.0010) | (0.0015) | ||

| woman | 0.5349*** | 0.4361*** | -0.3882*** | -1.6909*** | |

| (0.0194) | (0.0248) | (0.0242) | (0.0527) | ||

| car_per_indiv | 1.2138*** | ||||

| (0.0161) | |||||

| car_per_indiv0 | 1.5604*** | ||||

| (0.0245) | |||||

| occupation: farmer | -3.9054*** | -1.0434*** | -2.3653*** | -0.8798** | |

| (0.4140) | (0.2012) | (0.5073) | (0.4400) | ||

| occupation: artisan | -1.7023*** | -1.2153*** | -0.7848*** | -0.2261*** | |

| (0.0525) | (0.0566) | (0.0651) | (0.0841) | ||

| occupation: executive | 0.1522*** | 0.2031*** | 1.1710*** | 0.2986*** | |

| (0.0255) | (0.0327) | (0.0337) | (0.0575) | ||

| occupation: intermediate | -0.2283*** | -0.1447*** | 0.4259*** | -0.0060 | |

| (0.0242) | (0.0311) | (0.0349) | (0.0584) | ||

| occupation: blue-collar | -0.7579*** | -0.9691*** | -0.4808*** | -0.0259 | |

| (0.0318) | (0.0413) | (0.0467) | (0.0616) | ||

| travel_time | -1.6281*** | -1.1746*** | -2.1032*** | -2.8474*** | -3.2075*** |

| (0.0530) | (0.0480) | (0.0492) | (0.0581) | (0.0968) | |

| travel_time age | -0.0026** | ||||

| (0.0010) | |||||

| travel_time woman | -0.1134*** | ||||

| (0.0266) | |||||

| travel_time occupation: farmer | 1.1027*** | ||||

| (0.3621) | |||||

| travel_time occupation: artisan | -0.0763 | ||||

| (0.0918) | |||||

| travel_time occupation: executive | -0.3671*** | ||||

| (0.0354) | |||||

| travel_time occupation: intermediate | -0.1986*** | ||||

| (0.0330) | |||||

| travel_time occupation: blue-collar | 0.2623*** | ||||

| (0.0403) | |||||

| Reference category is male employee | |||||

| Travel time is expressed in hours | |||||

| Standard errors are reported in parentheses | |||||

| *** p0.01, ** p0.05, * p0.1 | |||||

The results are consistent with the literature on commute mode choice. For example, we find that being young and male increases the probability to commute by cycling, consistently with the literature review of cycling mode choice from Muñoz, Monzon, and Daziano (2016). We also find that the coefficient of travel time is larger for public transit than for car which suggests that the value of time for commutes by public transit is slightly smaller than for commutes by car. This is coherent with the meta-analysis on the value of travel-time in France from Wardman et al. (2012).

7.3 Simulating Utilities

We consider a regulator whose goal is to reduce the CO2 emissions due to commute trips, by distributing incentives to the population described in the data (about individuals).

To apply Algorithm 1, the regulator needs to know the utility and the CO2 emissions of each individual, for each mode of transportation. We describe in this subsection how we estimate them. Note that our estimations are individual specific.

Remark 5.

Recall that Assumption 3.2 implies that the utility of an individual when commuting by car or public transit does not depend on how many other individuals commute by car or by public transit. Such an assumption is reasonable when the congestion on the road and transit occupation rate are approximately exogenous, i.e., they do not depend on the incentive policy. This approximation is legitimate if the number of modal shifts induced by the policy is low, so that their impact on congestion and occupation is negligible. A posteriori, we check that this latter assumption is verified in our case, since less than % of individuals shifted mode due to the personalized-incentive policy.

Following the Multinomial Logit theory, we assume that utility of alternative of individual is composed of a deterministic part and a random part :

| (25) |

The deterministic part of the utility can be computed using the estimates from Table 2. As for the random part, we simulate random draws from a random variable with standard Gumbel distribution (see Appendix E). In accordance with Assumption 3.4, the regulator is assumed to know perfectly both the estimates and the draws and thus the utilities. We relax this assumption in Section 7.7, where we provide results where the random draws are unknown to the regulator.

To normalize the utility in monetary units, we compare the value of travel time by car from our regression (expressed in utility units) with the value of travel time by car in France from the literature (expressed in euros). We compute the value of travel time by taking the opposite of the average marginal effect on utility of increasing the travel time of the individuals by one hour.333For example, referring to the coefficients of Table 2, for a 40-year old male employee, the value of travel time by car is We find an average value of time of utility units per hour.

Previous studies (Wardman et al. 2012) have shown that the value of travel time, for car commuters, in France, is about euros per hour. This would imply that, in our estimates, one utility unit corresponds to euros. In the following, we assume that the utility is normalized in monetary units, i.e., the values in equation (25) are multiplied by . Note that it implies that the random variables follows a Gumbel distribution with scale parameter .

7.4 Computing the Social Indicator

The regulator wants to reduce greenhouse gas emissions. The social indicator associated to the mode of transportation of individual is the reduction in CO2 equivalent of greenhouse gas emissions generated during the trip of performed with mode , with respect to the emissions of the default mode. To compute CO2 emissions for each individual and each mode of transportation, we take the distance of the fastest path between the individual’s home and workplace and we multiply this distance with the CO2 emissions equivalent per kilometre for the mode of transportation, using open-sourced data from the French agency ADEME (Agence de l’Environnement et de la Maîtrise de l’Énergie).444https://www.bilans-ges.ademe.fr/en/

For car, we use the CO2 emissions of a passenger car with average motorization ( kilogram of CO2 per kilometre). That is, we assume that the CO2 emissions per kilometre are the same for everyone. We pinpoint that this assumption may lead to some imprecision in the calculation of the actual CO2 reduction. The application could be improved by using detailed data on the characteristics of the vehicle used by each individual.

For Assumption 3.3 to be valid, CO2 emissions due to the commuting trip of an individual must be independent from the mode of transportation chosen by the other commuters. For the same argument of Remark 5, we can claim that this approximately holds true in the scenario.

As Chester, Horvath, and Madanat (2010), we adopt a disaggregated view of CO2 emissions from public transit. We consider that the overall CO2 generated by transit vehicles is shared among all travellers making trips within transit, proportionally to the kilometres travelled. In other words, each trip on transit produces a quantity of CO2 emissions equal to the number of kilometres travelled multiplied by the average CO2 emissions per kilometre per passenger, assuming average and constant occupancy rate. Observe that it is reasonable to assume an average occupancy rate that is constant over time from the argument of Remark 5. The average CO2 emissions per kilometre per passenger vary according to the mode of transportation used (e.g., bus, tramway or metro). The mode of transportation taken for the fastest path are used to compute CO2 emissions. For multi-modal public-transit trips (e.g., bus then tramway), the CO2 emissions are computed according to the distance travelled by each mode of transportation.

CO2 emissions for walking and cycling trips are set to zero. Hence, for each individual, the two alternatives corresponding to walking and cycling differ only in the intrinsic utility. As a consequence, the alternative with smaller intrinsic utility can be neglected, thanks to Proposition 3.9.

| Daily CO2 emissions (all home-work and work-home trips) | tons of CO2 |

|---|---|

| Total CO2 emissions in one year (200 working days) | tons of CO2 |

| Average yearly individual CO2 emissions | 0.54 tons of CO2 |

Recall that Assumption 3.4 implies that the regulator knows perfectly the CO2 emissions of the trips. This is more realistic than for utility. In any case, measurement errors for CO2 emissions are not as worrying as measurement errors for utility as we can assume that, if such errors are unbiased, they cancel out. We will observe in Section 7.7 that the errors are much more severe when utilities are imperfectly known, as some individuals might reject the incentives, which leads to a suboptimal allocation.

Under the previous assumptions, we calculate the CO2 emissions reported in Table 3, which results in 0.54 ton of CO2 yearly per individual in the Rhône department. This number is close to the publicly known estimation for the entire France: in 2007, the average French worker emitted 0.64 ton per year because of his/her home-work trips (Levy and Le Jeannic 2011).

7.5 Calculation of the Personalized-Incentive Policy

We consider a large-scale scenario with more than 200 thousands individuals and over 1 million alternatives (Appendix C). We consider a policy in which the regulator proposes, each day, incentives to the individuals before their home-work trip. The incentives are given conditional on the mode of transportation chosen for the round trip to work, thus the social indicator of an alternative is the reduction in CO2 emissions for the trip back and forth, with respect to the default alternative. The budget represents the daily amount available to the regulator for incentives.

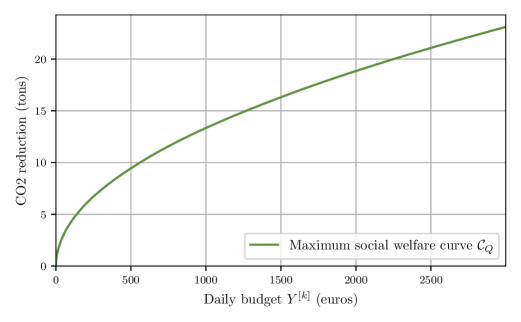

First, we run Algorithm 1 with a daily budget of euros and we plot the maximum social welfare curve (see Figure 3). The maximum social welfare curve is an increasing step function (steps are small and thus not visible). Consistently with Proposition 4.7, the slope of each step is non-increasing, which gives the curve a concave curvature.

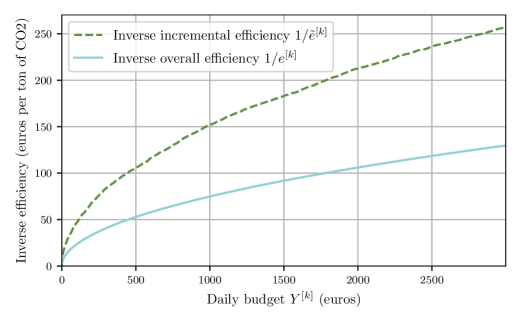

Quinet et al. (2009) predict that the carbon price in France would be of 100 euros per ton of CO2 in 2030. It is thus reasonable to assume the regulator is interested in finding an incentive policy such that, for every 100 euros spent in incentives, pollution is reduced by at least a ton of CO2. To this aim, the regulator can observe the curves of Figure 4, which plots the inverse of the incremental and overall efficiency (the and of Definition 4.6), with respect to the budget allocated by the algorithm at each iteration . Thanks to Proposition 4.7, and increase with , as we proceed with the iterations of the algorithm. Thanks to this monotonicity, the regulator can apply one of the following two criteria to fix the budget to invest. It could run Algorithm 4 and stop it when equals 100 euros per ton of CO2. Alternatively, it can stop the Algorithm when equals 100 euros per ton of CO2. From Figure 4, we observe that with the first criterion the regulator would need to invest about 1800 euros per day, and about 500 euros with the second criterion. In our opinion, both criteria would make sense, and the preference over one of them is a political choice.

We now set the budget of the regulator to euros. Running Algorithm 1 with this budget required about iterations and took about 6 seconds (with Python, on a computer with an Intel i5-8350U 1.7GHz and 24GB of memory). The algorithm allocates practically all the budget ( euros). We find that % of individuals received incentives and changed transportation mode, which results in a reduction of CO2 emission by tons of CO2 per day ( of total CO2 emissions). Thus, this policy would cost on average euros for each ton of CO2 prevented.

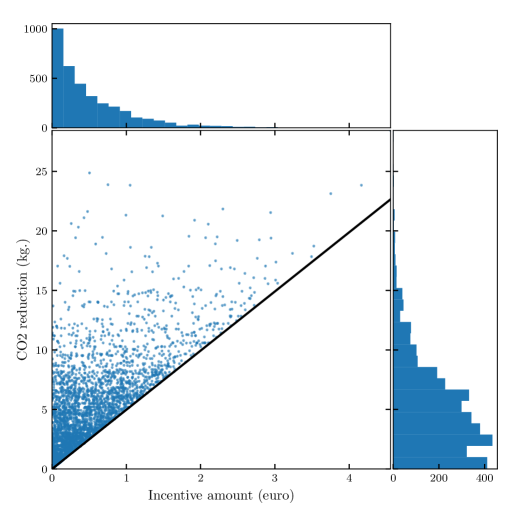

Despite the small incentives, the reduction in CO2 emissions is considerable. Indeed, among the individuals who received incentives, the average amount of incentives is euros per individual, for an average daily reduction in CO2 emissions of kilograms. Recall that alternatives providing a large reduction in CO2, while requiring small incentive, have a high efficiency. Hence, the algorithm selects first shifts achievable with a small incentive, i.e., where the individual is almost indifferent between the two alternatives, which however have a large difference in CO2. Figure 5 shows the distribution of the incentive amount and the CO2 reduction for the incentivized individuals. For most incentives, the amount proposed to individuals is below euro (incentives with a larger amount are not efficient enough, unless the CO2 reduction is very high).

The slope of the black line represents the incremental efficiency of the split item returned by the algorithm, tons of CO2 / euro. Note that all points are above the line because their incremental efficiency is larger. The histogram above represents the distribution of the incentive amounts. The histogram on the right represents the distribution of the CO2 reduction for the incentives.

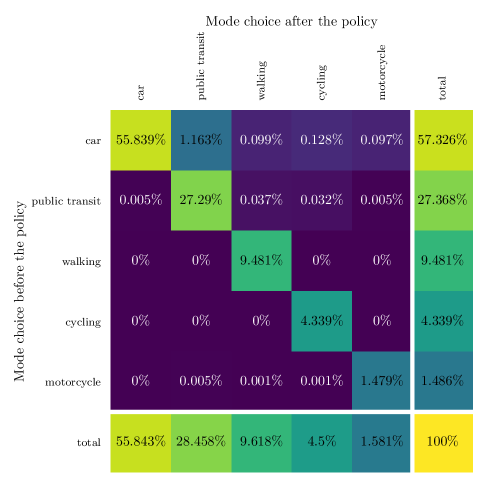

Figure 6 compares mode share before and after the policy. Most individuals who received incentives are individuals who commuted by car and were induced to commute by public transit (% of all individuals, % of individuals who received incentives). The share of individuals commuting by car decreased by 2.4%, while public transit ridership increased by %.

We now compute a bound of the optimality gap, i.e., the maximum additional CO2 savings we would achieve if we could use a theoretical optimal policy instead of resorting to Algorithm 1. To do so, we apply Theorem 4.2. Since the incremental efficiency of the split item returned by the algorithm is kilograms of CO2 per euro and the unused budget is euros, an optimal policy would reduce just kilograms more than Algorithm 1, which is negligible compared to the total CO2 emissions reduction of tons provided overall.

7.6 Comparison with Other Policies

In Section 7.5, we evaluated the performance of the personalized incentive policy calculated by Algorithm 1, which we denote with . We now compare it with three other policies from Section 5.2: an enforcement policy, a proportional taxation system and the Tripod incentive system from Araldo et al. (2019).

Aggregate results for these policies are provided in Table 4. The policies are defined so that they induce the same choices for the individuals, using results from Section 3. Therefore, they provide the same reduction in CO2 emissions and, from Proposition 5.2, they have the same disutility. However, they differ in their cost for the regulator and the variation in individual utilities implied. It should be noted that the best policy to implement depends on social, political or juridical constraints.

In these results, we fix the disutility threshold to euros, which corresponds to the incentive actually spent by Algorithm 1 when we set the budget to euros. This means that if we run the algorithm setting a budget of euros, it spends it all and, thanks to Corollary 5.6, the resulting policy is optimal under a budget constraint of euros.

| Policy | Expenses (euros) | Ind. utility (euros) | Disutility (euros) | CO2 reduction (tons) |

|---|---|---|---|---|

| Personalized incentives | 0 | |||

| Enforcement | 0 | |||

| Proportional tax | ||||

| Tripod incentives |

Enforcement policy

Thanks to Proposition 5.7, the regulator can compute an enforcement policy that is optimal for a disutility threshold of euros, by simply ‘imitating’ the personalized incentive policy , i.e., by inducing the same alternatives as . In order to do so, the regulator bans all the other alternatives, i.e., any alternative such that is banned. Obviously, it is not necessary to ban any alternative if is preferred to , in absence of policy, i.e., . Therefore, only the individuals receiving incentives under policy suffer bans with , which correspond to only 1.57% of the population.

Contrarily to the personalized-incentive policy, the enforcement policy does not cost any money to the regulator (apart from eventual transaction costs) but it decreases individual utilities by euros. Moreover, the % of individuals impacted by the ban may perceive that they are inequitably penalized with respect to the others. Hence, the enforcement policy might be less accepted by the population. Still, this policy is well adapted to the context of imperfect information as it ensures that the individuals always choose the alternative wanted by the regulator.

Proportional tax

The proportional tax policy is computed from equation (21), using the tax level given by equation (22) (Theorem 5.8). For each individual , the baseline social-indicators is set to the CO2 emissions of the default transportation mode, so that is equal to the opposite of the CO2 emissions of transportation mode .

Since the taxation provides revenues, the regulator is not constrained by his budget anymore. However, taxation negatively impacts the utilities of the individuals, and is thus limited by political constraints, which we model by imposing that the disutility of the policy must be below a threshold euros.