Optimal retirement choice under age-dependent force of mortality

Abstract.

This paper examines the retirement decision, optimal investment, and consumption strategies under an age-dependent force of mortality. We formulate the optimization problem as a combined stochastic control and optimal stopping problem with a random time horizon, featuring three state variables: wealth, labor income, and force of mortality. To address this problem, we transform it into its dual form, which is a finite time horizon, three-dimensional degenerate optimal stopping problem with interconnected dynamics. We establish the existence of an optimal retirement boundary that splits the state space into continuation and stopping regions. Regularity of the optimal stopping value function is derived and the boundary is proved to be Lipschitz continuous, and it is characterized as the unique solution to a nonlinear integral equation, which we compute numerically. In the original coordinates, the agent thus retires whenever her wealth exceeds an age-, labor income- and mortality-dependent transformed version of the optimal stopping boundary. We also provide numerical illustrations of the optimal strategies, including the sensitivities of the optimal retirement boundary concerning the relevant model’s parameters.

Keywords: Optimal retirement time; Optimal consumption; Optimal portfolio choice; Duality; Optimal stopping; Free boundary; Stochastic control.

MSC Classification: 91B70, 93E20, 60G40.

JEL Classification: G11, E21, I13.

1. Introduction

The timing of retirement is a crucial financial decision that individuals must face as they approach later stages of life. However, determining the appropriate moment to retire is a complex undertaking, as it is influenced by numerous factors. One of the most prominent and evident predictors of retirement decisions is an individual’s chronological age, as highlighted in empirical studies such as Wang and Shi [37]. Additionally, research indicates that individuals typically postpone retirement until they possess the necessary financial means to do so, with retirement timing being linked to both wealth and labor income, as explored in Honig [21]. In line with rational decision-making principles and the life-cycle model in economics, subjective life expectancy (how long one expects to live or expected mortality) also plays a significant role in retirement timing. Szinovacz et al. [36] used data from the Health and Retirement Study and found that expected mortality risk influenced retirement plans, and the effects were especially strong for expectations to work beyond age 65. Furthermore, factors like health status and familiar caregiving responsibilities contribute to the complexity of retirement decision-making. For a comprehensive examination of these factors, please refer to Fisher et al. [17]’s insightful review.

In addition to the aforementioned empirical studies, the field of optimal retirement time decision-making has been enriched by various theoretical models from a financial perspective. The historical origins of the optimal retirement time problem can be traced back to seminal works such as Jin Choi and Shim [26], Farhi and Panageas [16], Choi et al. [7], Dybvig and Liu [14], and Dybvig and Liu [15]. These foundational contributions paved the way for investigating the optimal investment and consumption behavior of individuals facing retirement decisions, resulting in significant advancements across various contexts. Notable advancements include the introduction of features like mandatory retirement dates and early retirement options Yang and Koo [38], the consideration of consumption ratcheting Jeon and Park [25], the exploration of partial information Chen et al. [6], the incorporation of habit persistence Chen et al. [5], Guan et al. [20], the examination of return ambiguity in risky asset prices Park and Wong [32], the analysis of non-Markovian environments Yang et al. [39], and the study of heterogeneous consumption patterns involving basic and luxury goods Jang et al. [23].

However, an important characteristic shared by much of the existing literature is the absence of consideration for mortality risk or the assumption of a constant force of mortality. This requirement, although common, can impose significant restrictions on the modeling framework. In reality, mortality has long been studied in the fields of mathematics and demography. Abraham De Moivre, in 1725, proposed perhaps the earliest mathematical mortality model, suggesting that the probability of surviving from birth to age follows a linear function of age. Moreover, the most successful and influential mortality law is known as Gompertz’s law, formulated by Gompertz [19]. This law describes a function with exponentially increasing mortality rates and has found application in insurance economics as well (see, e.g., Milevsky and Young [30] and De Angelis and Stabile [13] for the optimal annuitization problem with a Gompertz force of mortality).

In this paper, we aim to quantitatively examine the interplay between age, wealth, labor income, and mortality on the optimal retirement time. We extend the existing model by incorporating an age-dependent force of mortality, specifically the Gompertz model, to comprehensively analyze these influences. Our study focuses on an individual who confronts a mandatory retirement date but possesses the option to retire earlier, assuming irreversibility in retirement decisions. The individual can allocate her wealth to consumption and invest in a risky asset. Additionally, the labor income of the individual is stochastic until retirement, and post-retirement utility increases due to the availability of more leisure time.

As highlighted by Chen et al. [4], “the optimal retirement problem of a sophisticated individual with an age-dependent force of mortality has not been solved analytically.” Consequently, the primary objectives of our paper are twofold: first, to determine optimal consumption and portfolio-choice strategies considering realistic longevity risks stemming from an age-dependent force of mortality, and second, to fully characterize the optimal retirement time. By addressing these objectives, our study intends to fill the existing gap in the literature.

Notably, our findings, which are collected in Section 5 and Section 6, are somewhat intuitively convincing. For example, we show that it is optimal to retire when the agent’s wealth first reaches an endogenously determined boundary surface, which depends on the agent’s age, labor income and mortality. Intuitively, if the agent is sufficiently rich (her wealth exceeds the corresponding boundary), then retirement should be performed immediately; otherwise, it is optimal to wait for an increase of the wealth. Moreover, we show that both consumption and portfolio choices jump at the endogenous retirement time, which is consistent with Dybvig and Liu [14] and Chen et al. [5]. We also provide some interesting economic implications of the optimal retirement boundary through a numerical study in Section 6.

1.1. Overview of the mathematical analysis

From a mathematical point of view, we model the previous problem as a random time horizon, three-dimensional stochastic control problem with discretionary stopping. The three coordinates of the state process are the wealth process , the force of mortality process , and the stochastic labor income . The dominant feature of the wealth process is that it is not the same before and after the retirement time . The agent’s aim is to choose consumption rate , portfolio , and the retirement time in order to maximize the total expected utility of consumption , up to the random death time .

In the literature, the derivation of the Hamilton-Jacobi-Bellman (HJB) equation is a frequently employed approach when analyzing stochastic optimization problem with Markovian processes. In our specific case, the corresponding HJB equation (cf. (A.7)) turns out to be an involved combination of an HJB-type equation (reflecting the investment and consumption optimization) with a variational inequality (reflecting the retirement optimization). However, studying the properties of the value function and the optimal strategies, particularly the optimal stopping boundary, proves to be challenging when directly studying the equation. This difficulty arises due to the presence of a three-dimensional state process, rendering the classical “guess and verify” method ineffective.

In order to tame the intricate mathematical structure of our problem, where the consumption and portfolio choices nontrivially interact with the retirement decision, we combine a duality and a free-boundary approach, and proceed in our analysis as it follows.

Step 1. First, we conduct successive transformations (see Section 3) that connect the original stochastic control-stopping problem (with value function ) with its dual problem (with value function ) by martingale and duality methods (similar to Karatzas and Wang [29] or Yang and Koo [38]). The dual problem (with value function ) is a finite time-horizon, three-dimensional optimal stopping problem with interconnected dynamics, which is difficult to tackle directly. Due to the intrinsic homogeneous structure of the considered power utility function, we reduce the dimensionality by applying a measure change method, and reach a reduced-version dual stopping problem (with value function ).

Step 2. We then study the reduced-version dual problem, which is a finite time-horizon, two-dimensional optimal stopping problem with interconnected dynamics. The newly introduced state variable (depending on the dual process and the labour income process ) evolves as a geometric Brownian motion, where the drift depends on the mortality force . The coupling between the two components of the state process makes the optimal stopping problem quite intricate.

It is also worth pointing out that the force of mortality process does not possess any diffusive term, which leads to a novel analysis of the regularity of (given by the difference of and the smooth payoff of immediate stopping; see (4.12)). As a matter of fact, the process () is a degenerate diffusion process (in the sense that the differential operator of () is a degenerate parabolic operator) so that the study of the regularity of in the interior of its continuation region cannot hinge on classical results for parabolic PDEs (see, e.g., Friedman [18]).

Additional technical difficulties arise when trying to infer properties of the optimal stopping boundary . In fact, since the regularity of in the interior of its continuation region cannot be established a priori via classical PDE results, we were unable to establish continuity for the mapping , even if monotonicity properties of the latter could be easily proved. It is indeed well known in optimal stopping and free-boundary theory that interior regularity of in together with the monotonicity of are the key ingredients for a rigorous study of the continuity of the boundary (for a deeper discussion please refer to De Angelis [10]).

We overcome those major technical hurdles by proving that the optimal boundary is in fact a locally Lipschitz-continuous function of time and force of mortality , without employing neither monotonicity of the boundary nor classical results on interior regularity for parabolic PDEs. In order to achieve this goal, we rely only upon probabilistic methods borrowed from De Angelis and Stabile [12], which are then specifically adjusted to tackle our problem.

As a matter of fact, we first prove that is locally Lipschitz continuous and obtain probabilistic representations of its weak-derivatives (cf. De Angelis and Stabile [12]). Then, through a suitable application of the method developed in De Angelis and Stabile [13], by means of a version of the implicit function theorem for Lipschitz mappings (cf. Papi [31]), we can show that the free boundary surface is locally-Lipschitz continuous. This enables us to prove that the optimal stopping time is continuous, which in turn gives that is a continuously differentiable functions of its three variables. Being that the process is the only diffusive one, the -property of implies that admits a continuous extension to the closure of the continuation region. Notice that it is in fact this regularity that could had not been derived from standard results on PDEs nor from Peskir [34], and it is in fact this regularity that allows (via an application of a weak version of Dynkin’s formula) to derive an integral equation which is uniquely solved by the free boundary.

Step 3. After proving the strict convexity of , we can come back to the original coordinates’ system and via the duality relations we obtain the optimal consumption and portfolio policies, as well as the optimal retirement time, in terms of the optimal stopping boundary and value function (cf. Section 5).

Overall, we believe that the contributions of this paper are the following. As we discussed before, even though the literature on optimal retirement time problems is extensive from different perspectives, the introduction of the age-dependent force of mortality constitutes a novelty. From a mathematical point of view, we provide a rigorous theoretical analysis of the optimal retirement time in terms of the optimal boundary . To the best of our knowledge, ours is the first work providing a complete analytical characterization of the value function and of the optimal strategies in the optimal retirement time problem with age-dependent force of morality. Furthermore, we believe that the dual optimal stopping problem with the degenerate parabolic operator, studied as a device to characterize the optimal solution of the optimal retirement time problem, is of interest of its own. By performing a thorough analysis on the regularity of (a transformed version of the dual value function) and of the free boundary, we are able to provide a complete characterization of the optimal retirement time strategy through a nonlinear integral equation. The analysis in this paper is completed by solving numerically the integral equation and studying its sensitivity to variations in the model’s parameters, thus extending the results of the related optimal retirement time model.

1.2. Organization of the paper

The rest of the paper is organized as follows. In Section 2, we introduce the optimal retirement time decision model with an age-dependent force of mortality. We transform the original stochastic control-stopping problem into a pure stopping problem in Section 3, while in Section 4 we study the optimal stopping problem. In Section 5, we provide the optimal retirement time boundary, optimal consumption plan and optimal portfolio in primal variables, and in Section 6 we present a numerical study and provide some economic implications. Appendix A collects the proofs of some results of Sections 4 and 5, whereas Appendix B includes some auxiliary results needed in the paper. In Appendix C, we give the details of the numerical method used in Section 6.

2. Setting and problem formulation

2.1. The age-dependent mortality rate

Let be a complete probability space, endowed with a filtration satisfying the usual conditions, where is a fixed initial time. The remaining lifetime of an agent is an exogenous non-negative continuous random variable and is independent of . Moreover, has the cumulative distribution function , density function , so that, for any ,

is the probability that the agent is living at least another years. The force of mortality (also called the hazard function) represents the instantaneous death rate for the agent surviving to time , and it is defined by

Then the force of mortality is expressed by

which means that , for .

Consider an agent whose force of mortality rate evolves according to the standard Gompertz model (see, e.g., Gompertz [19]). The process thus follows the dynamics

| (2.1) |

with . Notice that the usual form for the Gompertz model is , hence we are using and . Here, denotes the agent’s age at initial time , is called the modal value, and is the dispersion coefficient for the Gompertz model. This model is simple, and takes advantage of a long experience of calibration to real populations.

2.2. The financial market and labour income

We assume that the agent invests in a financial market with two assets. One of them is a risk-free bond, whose price evolves as

where is a constant risk-free rate. The second one is a stock, whose price is denoted by and it satisfies the stochastic differential equation

where and are given constants. Here, is an -adapted standard Brownian motion under .

For the agent, there is a mandatory retirement time . Let be an -stopping time representing the time at which the agent chooses to retire. The agent receives a stochastic labor income as long as she is not retired. We assume the labor income to be spanned by the market and that we can express it as a geometric Brownian motion, similar to e.g. Bodie et al. [3] and Dybvig and Liu [14],

| (2.2) |

with for . Here and are constants, representing the instantaneous growth rate and the volatility of the labor income, respectively.

We define the market price of risk and the state-price-density process . Since the market is complete and the labor income is perfectly correlated with the market, the present value of the future labour income at time (also called “human capital” as in Dybvig and Liu [14]), under the assumption that the agent does not choose early retirement and the agent is always alive, is given by

| (2.3) |

where is the effective discount rate for labor income, which is assumed to be positive (see also Dybvig and Liu [15] and Guan et al. [20] for a similar requirement). Then, for , we define

so that .

The agent also consumes from her wealth, while investing in the financial market. Denoting by the amount of wealth invested in the stock at time , the agent then also chooses the rate of spending in consumption at time . Therefore, the agent’s wealth evolves as

| (2.4) |

In the following, we shall simply write to denote , where needed.

2.3. The optimization problem

Here and in the sequel, we write , and , with . We denote by the class of -stopping times for , and let . Then we introduce the set of admissible strategies as it follows.

Definition 2.1.

Let be given and fixed. The triplet of choices is called an admissible strategy for , and we write , if it satisfies the following conditions:

-

(i)

and are progressively measurable with respect to , ;

-

(ii)

for all and -a.s., for any ;

-

(iii)

for all , where is defined in (2.2) if and if .

Condition (iii) means that the agent is allowed to borrow money and hold a negative wealth level, while the amount of money she borrows cannot exceed the total value of future labour income. Once the agent retires, she is prohibited from any borrowing.

The preferences of the agent are described through a power utility function. Due to a larger amount of free time when retired, the agent assigns a higher utility value to consumption during retirement, represented by a constant weighting . The utility of the agent for consumption at time is

Specifically, we call the utility function before retirement, i.e., for ,

on the other hand, we call the utility function after retirement, i.e., for ,

From the perspective of time , the agent’s aim is then to maximize over all the expected intertemporal utility functional

where is a constant representing the discount rate. Thanks to Fubini’s Theorem and independence between and , we can disentangle the market risk and mortality risk and write

Hence, given the Markovian setting, the agent aims at determining

| (2.5) |

where denote the expectation under conditioned on and . In the rest of the paper, we shall focus on (2.5).

3. From control-stopping to pure stopping

3.1. The static budget constraint

An application of Itô’s formula yields

| (3.1) |

and

| (3.2) |

Since for any , we can deduce that for any from the continuity of . For an admissible plan , the left-hand side of (3.1) is nonnegative for , so that the Itô’s integral on the right-side is not only a continuous -local martingale, but it is also a supermartingale by Fatou’s Lemma. Thus, recalling that , the optional sampling theorem implies the so-called budget constraint:

| (3.3) |

By similar arguments on we also have

| (3.4) |

3.2. The agent’s optimization problem after retirement

In this subsection we will consider the agent’s optimization problem after retirement, and over this time period only consumption and portfolio choice have to be determined. Formally, the model in the previous section accommodates this case if we let , where is the fixed starting time. That is, the agent chooses immediate retirement. Then, letting where the subscript indicates that the retirement time is equal to , the agent’s value function after retirement is

| (3.5) |

where as defined in (2.1) and denotes the expectation conditioned on and .

From the budget constraint (3.4), recalling that and for a Lagrange multiplier , we have for any

| (3.6) |

where

| (3.7) |

Let then . By Itô’s formula, we obtain that the dual variable satisfies

| (3.8) |

and we set

| (3.9) |

Assumption 3.1.

We assume throughout the paper.

Proposition 3.1.

is independent of time , it is finite, and one has Moreover, satisfies

| (3.10) |

where

Proof.

First, we compute the convex dual of in (3.7); that is,

From (2.1), we have

| (3.11) |

Given that is time-independent, with a slight abuse of notation in the sequel we then simply write . It is possible to deduce properties of through those of by the following duality relation.

Theorem 3.1.

The following dual relations holds:

Proof.

Since is arbitrary, taking the supremum over on the left-hand side in (3.2) and recalling (3.5), we get, for any ,

and thus

For the reverse inequalities, observe that the equality in (3.2) holds if and only if

| (3.13) |

and

| (3.14) |

where we denote by the inverse of the marginal utility function

Then, assuming (3.14) (we will prove its validity later), we define

and notice that (3.2), (3.13) and (3.14) yield

where the last inequality is due to . The last display inequality thus provides

It thus remains only to show that equality (3.14) indeed holds. As a matter of fact, Lemma B.1 guarantees the existence of a candidate optimal portfolio process such that and (3.14) holds, where is a candidate optimal consumption process. By Theorem 3.6.3 in Karatzas and Shreve [28] or Lemma 6.2 in Karatzas and Wang [29], one can then show that is indeed optimal for the optimization problem . ∎

From Theorem 3.1 we see that is time-independent, so that in the following, with a slight abuse of notation, we simply write .

3.3. The pure optimal stopping problem

From the agent’s problem in (2.5), by the dynamic programming principle we can deduce that for any ,

| (3.15) |

Now, for any and Lagrange multiplier , from the budget constraint (3.3) and (3.15), recalling in (3.7), we have

| (3.16) |

where is defined in (3.8) and

| (3.17) |

Hence, defining

| (3.18) |

we have

| (3.19) |

In the following sections, we perform a detailed probabilistic study of (3.18). Before doing that, we have the following theorem that establishes a dual relation between the original problem (2.5) and the optimal stopping problem (3.18).

Theorem 3.2.

The following duality relations holds:

Proof.

Since is arbitrary, taking the supremum over on the left-hand side of (3.19), we get, for any ,

so that and .

For the reverse inequality, observe that equality holds in (3.19) if and only if (see also (3.3))

and

| (3.20) |

where denotes the inverse of the marginal utility function From Lemma B.2, we know that there exists a portfolio process such that (3.20) holds. From Theorem 3.1, we also know that . Next we define

and

Then by (3.19) and (3.20) we have

where the last inequality is due to . This in turn gives

which completes the proof.

∎

4. Study of the dual optimal stopping problem

4.1. Dimensionality reduction

Notice that the dual optimal stopping problem in has three state variables and a finite time-horizon. However, due to the homogeneous structure of the utility function , we can apply a measure change method to reduce the dimensionality of the problem from three state variables to two state variables .

Lemma 4.1.

Proof.

First, from (3.17) and (3.7) we compute the convex dual functions and :

| (4.3) |

Plugging into (3.9) we have

and

| (4.4) |

Direct calculations (cf. (3.8) and (2.2)) show

| (4.5) |

Then, by the continuous-time Bayes’ rule (cf. Lemma 3.5.3 in Karatzas and Shreve [27]), we have for any fixed , and for ,

| (4.6) |

where we have used (4.1), the definition of and (4.1). Based on the same arguments, we also have for

| (4.7) |

due to . Here and in the sequel, denotes the expectation under conditioned on and . Combining (4.1) and (4.1), together with (3.18), we have with

∎

Before closing this subsection, we introduce the dynamic equation of defined in Lemma 4.1. By Itô’s formula and Girsanov’s Theorem, under the new measure evolves as

| (4.8) |

where with , and is a standard Brownian motion under the measure . Then, the solution to (4.8) may be expressed as

so that depends on both initial values and .

For future frequent use, we also introduce here the new probability measure on such that

| (4.9) |

and notice that

| (4.10) |

where

| (4.11) |

By Girsanov’s Theorem, the process is a new standard Brownian motion under the measure . Moreover, it is easy to check that is uniformly bounded in time, i.e., there exist such that . In fact, is continuously differentiable in .

4.2. Preliminary properties of the value function

To study the optimal stopping problem (4.2), we find it convenient to introduce the function

| (4.12) |

with

| (4.13) |

Applying Itô’s formula to , and taking conditional expectations we have

where, for any , the second order differential operator is such that

Combining (4.2), (4.12) and (4.13), we have

| (4.14) |

where we have used the fact that

Indeed, arguing similarly to the proof of Lemma 4.1 (cf. (4.1) and (4.1)), one finds (recalling that )

| (4.15) |

and . Moreover, .

Notice now that the process is time-homogeneous, so that

Let be the expectation under conditional on . Hence, from (4.2),

| (4.16) |

As usual in optimal stopping theory, we let

| (4.17) |

be the so-called continuation (waiting) and stopping (retiring) regions, respectively. We denote by the boundary of the set

Since, for any stopping time , the mapping is continuous, is lower-semicontinuous on . Hence, is open, is closed, and introducing the stopping time

with , one has that is optimal for (see e.g. Corollary I.2.9 in Peskir and Shiryaev [35]).

Proposition 4.1.

The value function is such that for all and it satisfies the following properties:

-

(i)

When , is non-decreasing for all ; when , is non-increasing for all ;

-

(ii)

is non-increasing for all ;

-

(iii)

is non-decreasing for all

Proof.

The proof is given in Appendix A.1. ∎

The next lemma shows that as in (4.17) is nonempty.

Lemma 4.2.

One has .

Proof.

Suppose that , then for all we have

However, when , taking , the term converges monotonically to , leading to a contraction. Similarly, when , taking , the term converges monotonically to , which brings to a contradiction again. ∎

The next technical result states some properties of that will be useful in the study of the regularity of the boundary .

Proposition 4.2.

Recall , (4.9) and (4.11). The function is locally Lipschitz-continuous on and for a.e. we have the following probabilistic representation formulae:

| (4.18) |

| (4.19) |

Moreover, there exists a constant , independent of , such that

| (4.20) |

where is the optimal stopping time for the problem with initial data .

We conclude with asymptotic limits of .

Proposition 4.3.

When we have

When we have

4.3. Properties of the optimal boundary

In this section, we show that the boundary can be represented by a function . We establish connectedness of the sets and with respect to the -variable and give some preliminary properties of the optimal boundary.

For our subsequent analysis, it is convenient to introduce the auxiliary infinite time-horizon optimal stopping problem

Lemma 4.3.

When , then there exists a function , such that

| (4.21) |

Moreover, the function has following properties:

-

(i)

is non-decreasing for any

-

(ii)

is non-increasing for any ;

-

(iii)

one has .

When , then there exists a function , such that

| (4.22) |

Moreover, the function has following properties:

-

(i)

is non-increasing for any ;

-

(ii)

is non-decreasing for any ;

-

(iii)

one has , where , with being non-decreasing.

Proof.

The proof is given in Appendix A.4. ∎

The local Lipschitz-continuity of the boundary that we prove in the next theorem has important consequences regarding the regularity of the value function , as we will see in Proposition 4.5 below.

Theorem 4.1.

The free boundary is locally Lipschitz-continuous on .

4.4. Characterization of the free boundary and the value function

Assumption 4.1.

The model’s parameters are such that .

This assumption is sufficient to ensure the validity of the next lemma, which, given that is locally-Lipschitz, is proven through a suitable application of the law of the iterated logarithm.

Lemma 4.4.

When , let and set

Then a.s., where . Similarly, when , let and set

Then a.s., where .

The previous lemma in turn yields the following continuity property of , which will then be fundamental in the proof of Proposition 4.5 below.

Proposition 4.4.

One has that is continuous.

Proof.

Proposition 4.5.

The value function and solves the boundary value problem

Proof.

First we show that the function is continuously differentiable over . From the representations of and in Proposition 4.2, and the continuity of (cf. Proposition 4.4), we conclude that those weak derivatives are in fact continuous and therefore that , where denotes the interior of . In particular, on . It thus remains to analyze the regularity of across .

Fix a point and take a sequence with as Continuity of implies that -a.s. as Again, from Proposition 4.2, dominated convergence yields that and . Since and the sequence were arbitrary, we get .

Let us now turn to study the regularity of in . First of all notice that, because the solution to (4.8) is linear with respect to the initial datum , we then have that is convex, being from (4.3) clearly convex. This fact implies that is convex, as is strictly convex. Hence, is convex. In particular, by Alexandrov’s Theorem, admits second order derivatives with respect to in a dense subset of . Further, since is with respect to , we know that admits second order derivatives with respect to in a dense subset of (cf. (4.12) and (4.13)).

By Corollary 6 in Peskir [34], we also know that solves in the sense of distributions

| (4.23) |

and it is such that

By writing (4.23) as

we then see that admits a continuous extension to , that we denote Then, by taking arbitrary we can write

and the latter yields that is continuous for any such that . Since we already know that , we conclude that .

∎

Corollary 4.1.

Recall (4.12). The function and solves the boundary value problem

Remark 4.1.

It is worth noting that standard PDE arguments typically require uniform ellipticity of the underlying second-order differential operator and thus could not be directly applied in the proof of Proposition 4.5, due to the fully degenerate diffusion process . Therefore, we had to hinge on a novel series of intermediate results. First, we find the locally Lipschitz continuity of (cf. Proposition 4.2) and then establish the locally-Lipschitz continuity of free boundary without relying upon the continuity of and (cf. Theorem 4.1). Finally, we upgrade the regularity of using the continuity of the optimal stopping time (cf. Propositions 4.4 and 4.5).

We are now in the conditions of determining a nonlinear integral equation that characterizes uniquely the free boundary. Such a characterization results from an integral representation of the value function . This is accomplished by the next theorem, which exploits the regularity properties of proved so far.

Theorem 4.2.

If , from (4.16) has the representation

| (4.24) |

Moreover, recalling , the optimal boundary is the unique continuous solution bounded from above by to the following nonlinear integral equation: For all ,

| (4.25) |

with .

If , from (4.16) has the representation

| (4.26) |

Moreover, the optimal boundary is the unique continuous solution bounded from below by to the following nonlinear integral equation: For all ,

| (4.27) |

with .

Proof.

Step 1. In this step, we only need to prove (4.24), since the derivation in the case of is similar. Let be given and fixed, let be a sequence of compact sets increasing to and define

Since , , and for all , we can apply a weak version of Dynkin’s formula (see, e.g., Bensoussan and Lions [2], Lemma 8.1 and Th. 8.5, pp. 183-186) so to obtain

Therefore, using (4.23), we also find

where we have used again that .

Finally, we take , apply the dominated convergence theorem, and use that and (cf. Proposition 4.5) to obtain (4.24).

Step 2. Next, for , we find the limit value of when . The argument is inspired by the proof of Proposition 4.10 in De Angelis and Stabile [13]. The case of can be treated similarly and we thus omit it. Firstly, the limit exists, since is monotone on . Notice that for all (cf. Lemma 4.3) and therefore . Arguing by contradiction, we assume Then we pick such that and such that . Let with such that Recall (4.2) and define . Now, denoting by the adjoint of the operator , where . Therefore, we have on . Further,

since and for any when . From the above, we also deduce that is continuous up to ; thus there exists such that for and we obtain

since and for . This is a contradiction.

Step 3. Given that (4.24) holds for any , we can take in (4.24), which leads to (4.25), upon using that (cf. Proposition 4.5). The fact that is the unique continuous solution to (4.25) bounded from above (resp. below) by can be proved by following the four-step procedure from the proof of uniqueness provided in Theorem 3.1 of Peskir [33]. Since the present setting does not create additional difficulties we omit further details.

∎

5. Optimal boundaries and strategies in terms of primal variables

In the previous section, we studied the properties of the dual value function and used where denotes time, denotes marginal utility, denotes the force of mortality and denotes the labour income as the coordinate system for the study. In this section we will come back to study the value function in the original coordinate system , where denotes the wealth of the agent.

Proposition 5.1.

The function in (3.18) is strictly decreasing and strictly convex with respect to .

Proof.

The proof is inspired by Lemma 8.1 in Karatzas and Wang [29]. Firstly, defining

| (5.1) |

we have . From (3.2), it is easy to check that is strictly convex and strictly decreasing with respect to . Moreover, is strictly convex and strictly decreasing with respect to (cf. (4.3)). Therefore, is strictly convex and strictly decreasing with respect to . We denote by the set of stopping times that attain the supremum in (5.1) for every given . For any , and , we have

where are optimal stopping times. Further we have

which completes the proof. ∎

From Theorem 3.2, for any , we know that . Since is strictly convex (cf. Proposition 5.1), then there exists an unique such that

| (5.2) |

where , with being the inverse function of . Moreover, and, for any , is strictly decreasing with respect to . Hence, for any , is a bijection and therefore has an inverse function , which is continuous, strictly decreasing, and maps to .

Let us now define

| (5.3) |

Then, by Lemma 4.3 we have

| (5.4) |

so that we can express the optimal retirement time in terms of the initial coordinates as:

| (5.5) |

Theorem 5.1.

Let and recall that denotes the inverse of . Then

define the optimal feedback maps, while

is the optimal retirement time. Hence, and -a.s., provide an optimal control triple, where is assumed as a strong solution to SDE (2.4), after substituting for . Further, we have , where is the solution of Equation (3.8) with the initial condition .

Proof.

The proof is given in Appendix A.7. ∎

Thanks to (5.3) and Theorem 5.1 we can finally express the optimal retirement threshold and the optimal portfolio in terms of and , respectively.

Proposition 5.2.

One has that

for any , and

with .

6. Numerical Study

In this section, we present numerical illustrations of optimal strategies. Firstly, we show the retirement boundary in the dual and primal variables, as described in Theorem 4.2 and Proposition 5.2, respectively. Moreover, we investigate the sensitivity of the optimal retirement boundaries with respect to the relevant parameters and analyze the consequent economic meaning. We use a recursive iteration method proposed by Huang et al. [22] in order to solve the integral equation (4.27) and provide a detailed explanation of the method in Appendix C. The numerics was performed using Mathematica 13.1.

| 0.08 | 0.2 | 0.04 | 0.01 | 3 | 0.01 | 0.05 | 1/10.5 | 10 | 2 |

The basic parameters are listed in Table 1111We just consider the case in the numerical study, the case can be treated using the same method.. Here, for the age-dependent force of mortality of -year old individual, we use the Gompertz-Makeham model from Milevsky and Young [30]: , with corresponding modal value , scale parameter . We then consider an agent who is years old at the initial time () and the mandatory retirement time is 65 years old (), hence

6.1. Optimal retirement boundaries and sensitive analysis

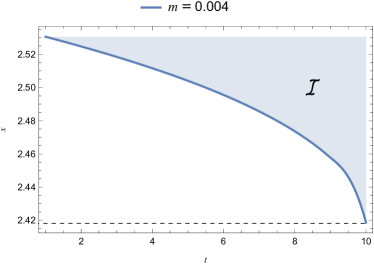

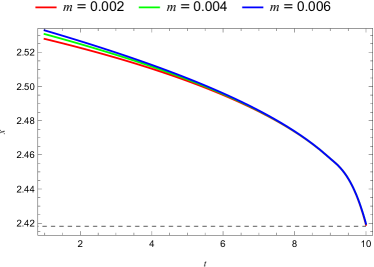

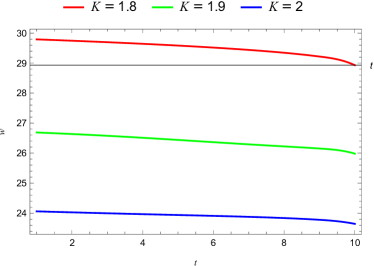

The retirement boundary of Theorem 4.2 is illustrated in Figure 2. As it has been proven in Lemma 4.3, we can observe that is a decreasing function of time . Intuitively, an elder agent will be more likely to retire and the retirement region expands with time. The dotted line represents , such that . Moreover, from Figure 2, we find that an increasing of induces larger , which is also consistent with the theoretical results provided in Lemma 4.3.

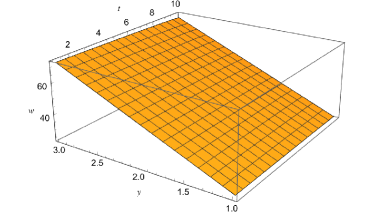

Next, fixing , we illustrate retirement boundary in the primal variables , which is displayed in Figure 3. Above the surface is the stopping region , which is defined in (5.4). Then we will study the sensitivity of with respect to some of the model’s parameters.

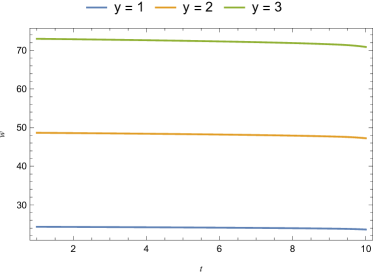

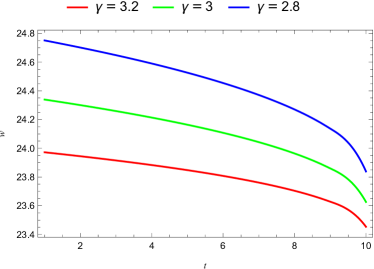

In Figure 5 we can observe the sensitivity of the optimal retirement boundary with respect to the initial labor income. Since an increase in implies higher human capital (the present value of future labor income (cf. (2.2)), the agent delays her decision to retire. As time goes by, the agent is expected to receive more future labour income. Figure 5 shows that if the risk aversion level is larger, the agent is more likely to retire later. This is an intuitive result, since a more risk averse agent invests less in the stock market, thus relies more on the income from labor and needs to work longer to accumulate enough wealth to be able to finance her retirement.

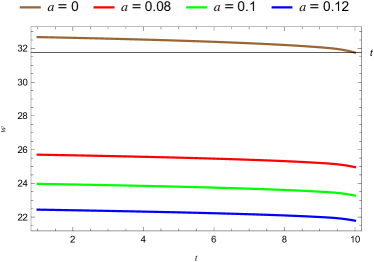

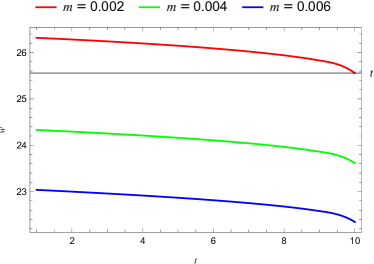

Figure 7 shows the effect of a change in on the boundary. If increases, growth rate of the agent’s force of mortality becomes larger. Thus, the agent is willing to retire earlier. If we consider a constant force of mortality (i.e., ) as that in existing literature, we will get a higher retirement boundary. It means the agent will retire later because the age-dependent force of mortality is ignored. Similarly, increasing the initial force of mortality , makes the agent retire earlier in order to profit earlier from the leisure. This is shown in Figure 7.

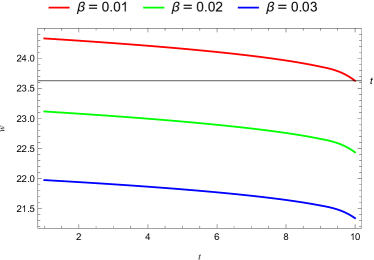

Figure 9 illustrates that as the discount rate becomes larger, the boundary becomes lower. As can be interpreted as the subjective impatience of the agent, increasing the value of makes the agent more impatient, with the result of an heavier discount of future utility. Consequently, the agent is willing to retire earlier. Figure 9 shows the effect of a change in on the boundary . It is clear that if is larger, the agent assigns higher utility value to consumption during retirement, so that the agent will choose to retire earlier.

6.2. Optimal consumption and portfolio

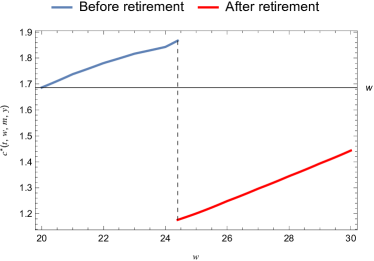

Figure 11 illustrates the optimal consumption . We find that the consumption jumps down at retirement if the relative risk aversion coefficient is greater than 1, where the dotted line is the critical wealth level for retirement. This is the so-called retirement consumption puzzle, which states that consumption drops at retirement (cf. Banks et al. [1]). Similar to Dybvig and Liu [14], consumption jumps on the retirement date because the marginal utility per unit of consumption changes after retirement.

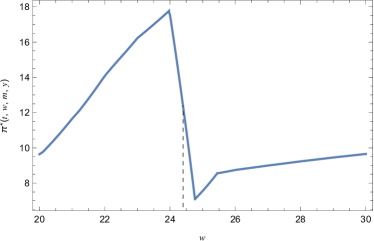

Figure 11 shows the optimal proportion of risky investment . We observe a substantial decline of proportion in stock, as it is observed by the empirical evidence in Coile and Milligan [9]. Hence, people tend to withdraw their investment in risky asset upon retirement in order to hedge the risk of unemployment; this is the so-called “saving for retirement”.

Appendix A Proofs

A.1. Proof of Proposition 4.1

Proof.

Finiteness. It is clear that for all . For , we have , so that

Monotonicity in . When , we find that and . Therefore, is non-decreasing for all . Analogously, when , and . Therefore, is non-increasing for all .

Monotonicity in . Monotonicity in is a trivial consequence of the fact that the is independent of .

Monotonicity in . When , we find that , thus is increasing -a.s. for all by uniqueness of the trajectories. As a consequence, is non-decreasing for all

When , we find that , thus is decreasing -a.s. for all by uniqueness of the trajectories, and is therefore non-decreasing for all

∎

A.2. Proof of Proposition 4.2

Proof.

The proof is divided into two steps.

Step 1: Here we show that is locally-Lipschitz and (4.19) holds for a.e. and each given (with the null set where is not differentiable being a priori dependent on ). Similar arguments, that we omit for brevity, also show that is locally Lipschitz in .

First we obtain bounds for the left and right derivatives of . Fix , pick , and notice that is suboptimal for (and independent of ). Then, recalling (4.10) and (4.11) we obtain

| (A.1) |

for some , where the last step has used the mean value theorem. Dividing (A.2) by and taking limits as gives

Since symmetric arguments applied to lead to the reverse inequality, we obtain

It now remains to show that is locally Lipschitz, so that a.e. is a point of differentiability. With the same notation as above, let be optimal for the problem with initial data . By arguments analogous to those used previously we find

| (A.2) |

Then, by the Hölder inequality, we can write from (A.2)

| (A.3) |

Clearly, , and because is continuously differentiable (cf. (4.11)), there exists a positive function such that, for any , .

Therefore, from (A.2) we have

The estimate in (A.2) implies , for some other constant which can be taken uniform over compact sets. Symmetric arguments allow also to prove that Therefore, is locally-Lipschitz and (4.19) holds for almost all .

Step 2: We borrow arguments from the proof of Proposition 3.4 in De Angelis and Stabile [13]. From the monotonicity of in (cf. Proposition 4.2), we know that , for all such that . Next we show that for all and any , we have

| (A.4) |

for some only depending on , and for all . Let be optimal in and define for . Since is admissible and suboptimal for , we get

| (A.5) |

for , as we have used the mean value theorem in the last equality. Furthermore,

with a uniform constant , and

Hence, exploiting the last two display equations in (A.2), one obtains the bound

In conclusion, noticing that , and recalling (4.9), (4.10) and (4.11) we have

| (A.6) |

for a different constant since is bounded (cf. (4.11)). Using the Markov inequality, we obtain

which plugged back into (A.2) give

| (A.7) |

Equation (A.7) implies (A.4) and, moreover, allow us to conclude that is locally Lipschitz a.e. in . Let be a point of differentiability of . Dividing (A.7) by and letting , we obtain the lower bound in (4.20).

∎

A.3. Proof of Proposition 4.3

Proof.

Taking for any we have,

On the other hand, we have from Proposition 4.1. Hence, overall,

Then, recalling that (cf. (4.3)), we have

and

Next we prove when . The proof of when is similar, and we thus omit it. We notice that exists a.s. by monotonicity of , which is inherited by that of . We want to show that a.s., which then implies . By arguing by contradiction, suppose that has positive probability. Let . Then, if , by dominated convergence

But (cf. Proposition 4.1), therefore it must be a.s. We then have when .

∎

A.4. Proof of Lemma 4.3

Proof.

Step 1: Here we prove (4.21). Equation (4.22) can be proved by similar arguments. Since is non-decreasing by Proposition 4.1, we can define (with the convention ), so that . Notice that actually on since by Lemma 4.2.

Step 2: Here we prove the property (i) for the case . Analogous considerations allow to prove it when . We know that is non-increasing by Proposition 4.1. Therefore, for , we have

Step 3: Here we prove property (ii), again only in the case . Since is non-decreasing by Proposition 4.1, for , we have

which implies that is non-increasing when .

Step 4: Here we provide the proof of property (iii), i.e., the bounds of the boundary. Noticing that, due to (4.16),

we have

| (A.8) |

Because (cf. (4.21)), (A.8) and the latter equation imply

Analogous arguments, now using , allow to obtain

To prove that when , we observe that

due to . Moreover, is non-decreasing because is non-decreasing. Given that is non-decreasing, in order to show that for all we proceed as follows. Suppose that such that . Then, by monotonicity of on . That is, such that we have and no-stopping is optimal; that is,

which is equivalent to

However, taking the right-hand side of the previous inequalities converges monotonically to . Hence, a contradiction. ∎

A.5. Proof of Theorem 4.1

Proof.

The proof is organized in five steps.

Step 1. For , define the function

Let now , (possibly depending on ), and, for , denote by . Since is locally-Lipschitz continuous in (cf. Proposition 4.2), if the following conditions are satisfied

-

(i)

;

-

(ii)

;

-

(iii)

and ,

then a version of the implicit function theorem (see, e.g., the Corollary at p.256 in Clarke [8] or Theorem 3.1 in Papi [31]) implies that, for suitable , there exists a unique continuous function such that

and also

| (A.9) | ||||

According to Proposition 4.2, when we have for a.e. inside . Then, by Propositions 4.1 and 4.3 it clearly follows that such a above indeed exists, and also . When we have for a.e. inside . Then, by Propositions 4.1 and 4.3 it clearly follows that such a above indeed exists, and also .

Moreover, when the family decreases as , so that its limit exists. Such a limit is such that the mapping is upper semicontinuous, as decreasing limit of continuous functions, and . Since , it is clear that taking limits as , we get by continuity of (cf. Proposition 4.2), and therefore due to the definition of the stopping region in (4.21). Hence,

| (A.10) |

Arguing symmetrically, we also have that (A.10) holds true for .

Step 2. We here prove that is bounded uniformly in . Clearly, we can restrict the attention to for some . From Lemma 4.3, we know that, when , we have . Since now (cf. (A.10)), we thus have that , which provides the desired uniform bound. When , we have . Hence, similarly, we have that , which provides the desired uniform bound.

Step 3. Here we show that is locally-Lipshitz continuous in , uniformly with respect to .

Step 3-(a). Here we determine an upper bound for . Recalling as in Proposition 4.2, by Proposition 4.1 we have

where . Then,

| (A.11) |

Step 3-(b). Here we determine a lower bound for . From (4.18), we have

| (A.12) |

so that from (A.12) we obtain

| (A.13) |

Step 3-(c). From (A.9) (with ), (A.5) and (A.13) we conclude that when the family of weak derivatives is uniformly bounded; i.e.,

| (A.14) |

Similarly, when the family of weak derivatives is uniformly bounded; i.e.,

| (A.15) |

since by Step 2.

Step 4. We show that is locally-Lipschitz continuous in , uniformly with respect to .

Step 4-(a). Here we find an upper bound for . Recalling that

by (4.20), one has

| (A.16) |

In the sequel a change of probability measures through a Girsanov argument will be needed in order to take care of the expectation on the right-hand side of (A.16). To this end, recall the probability measure on defined as

| (A.17) |

Then, by Girsanov’s Theorem, the process is a standard Brownian motion under the new measure .

Step 4-(b). We here determine another lower bound for . From (A.13) and recalling that , we have by a change of measure (cf. (A.17))

| (A.18) |

where .

Step 4-(c). Our aim here is to find a bound of , uniformly with respect to when . This term arises from the ratio of the two expectations in (A.16) and (A.5).

Since the dynamics of under are

those become under (remember that )

Now, if on we define

and , then we see that

where . Moreover, by the comparison principles for SDEs, we have that -a.s., for all since , and, therefore, we have -a.s., and

| (A.19) |

Step 4-(d). Our next task is to find a bound for the ratio , uniformly with respect to , when . The following proof arguments are borrowed from De Angelis and Stabile [13]. Due to Lemma 4.3, there exists such that , and we denote

For this part of the proof, it is convenient to think of as the canonical space of continuous paths and denote by the shifting operator . Moreover, we recall that and . With this notation, for fixed and any , we have and , because

Our first estimate gives (cf. (A.17))

| (A.21) |

for a suitable constant , independent of . Next we obtain

| (A.22) |

The last term can be further estimated via

| (A.23) |

where we have used that under . The last term in the above expression may be controlled by using iterated conditioning and the strong Markov property as

| (A.24) |

where

Notice that the strictly positivity of may be verified by using the known joint law of the Brownian motion and its running supremum. Indeed, recalling that , we have

Hence, overall, from (A.5), (A.5), (A.5), we obtain

where . Now we plug the latter into (A.5) and get

If we now let , we have

| (A.25) |

which gives the required uniform bound.

Step 5. Combining the findings of the previous steps, by (A.9) we have that is locally-Lipschitz continuous, with Lipschitz constants that are independent of (see (A.5), (A.13) and (A.5)). Furthermore, the family is also uniformly bounded (cf. Step 2).

Hence, by Ascoli-Arzelà theorem we can extract a subsequence such that uniformly, with being Lipschitz continuous with the same Lipschitz constant of . However, converges to (cf. Step 1), which, by uniqueness of the limit, is then locally-Lipschitz continuous.

∎

A.6. Proof of Lemma 4.4

Proof.

It is easy to check that by their definitions. In order to show the reverse inequality, the rest of the proof is organized in two steps.

Step 1. We claim that

due to the Lipschitz continuity of and the law of the iterated logarithm of Brownian motion. As a matter of fact, we fix a point and take a sequence with as We also fix , with , and assume that . Now we need to distinguish two cases: and .

Step 1-(a). We start with the case . The equality is trivial for such that , hence we fix with in the subsequent proof. Then, if on , for any we have,

Upon using that is Lipschitz continuous (cf. Theorem 4.1), we let and obtain

| (A.26) |

However, from (A.5) and (A.5) we have

which used in (A.6) give

where and Since , using the explicit representation for we find

| (A.27) |

By the law of the iterated logarithm (cf. Theorem 9.23 in Karatzas and Shreve [27]), for all we have (along a sequence of times converging to zero)

which combined with (A.27) yields (with due to and Assumption 4.1)

On the other hand, since when , the last display equation implies (for small enough) that

which simplified gives

| (A.28) |

Then dividing by and letting , we obtain that the left hand-side of the inequality in (A.6) is (since for ), but the right hand-side of the inequality in (A.6) is the constant . Thus, we reach a contradiction and -a.s.

Step 1-(b). Now we consider the case . The equality is trivial for such that , hence we fix with in the subsequent proof. Then we have

Upon using that is Lipschitz continuous (cf. Theorem 4.1), we let and obtain

| (A.29) |

However, from (A.15) and (A.5) we have

which used in (A.6) give

where we have used the monotonicity of in Lemma 4.3, and . Since , then we have

| (A.30) |

By the law of the iterated logarithm (cf. Theorem 9.23 in Karatzas and Shreve [27]), for all we have (along a sequence of times converging to zero)

which combined with (A.6) yields (with due to and Assumption 4.1)

On the other hand, since when , the last display equation implies (for small enough) that

which simplified gives

| (A.31) |

Then dividing by and letting , we obtain that the left hand-side of the inequality in (A.6) is (since for ), but the right hand-side of the inequality in (A.6) is the constant . Thus, we reach a contradiction and -a.s.

Step 2. In order to prove that one can finally use arguments as in the proof of Lemma 5.1 in De Angelis and Ekström [11].

∎

A.7. Proof of Theorem 5.1

Proof.

The proof is organized in two steps.

Step 1: We show that and and is a solution in the a.e. sense to the HJB equation

| (A.32) |

Step 1-(a): Firstly we show the regularity of . From (4.1) we know that . Therefore,

| (A.33) |

Then we conclude that with due to Corollary 4.1.

Step 1-(b): Now we show the regularity of . From (5.2), using that and , one has

| (A.34) | ||||

The proof is then completed due to Step 1-(a).

Step 1-(c): Now we characterize the optimal retirement time in the primal variables and show that is a solution in the a.e. sense to the HJB equation. Define . Recalling that on by (3.18), we notice that if , then the function attains its minimum value at Hence,

This means that is a stationary point of the convex function , so that

Combining these two arguments we have that

where . This, together with (5.4), leads to express the optimal retirement time in the original coordinates as

Due to the regularity of and the dual relations between and (cf. Step 1-(b)), from Corollary 4.1 we then find that is a solution in the a.e. sense to the HJB equation.

Step 2: Assuming that there exists a unique strong solution to the SDE (2.4), when and are replaced by and , respectively. From (5.2) we have , where is the solution to Equation (3.8) with the initial condition . Since by Proposition 5.1, it is easy to verify that , in particular, . Finally, a standard verification argument leads to the result. ∎

Appendix B Two auxiliary results

Lemma B.1.

Let be given, let be a consumption process satisfying

Then, there exists a portfolio process such that the pair is admissible and

Proof.

The proof is similar to Theorem 3.3.5 in Karatzas and Shreve [28], and we thus omit details.

∎

Lemma B.2.

For any , let be given, let be a consumption process. For any -measurable random variable with such that

there exists a portfolio process such that the pair is admissible and

Appendix C Recursive integration method

The numerical method is inspired by Huang et al. [22] and Jeon et al. [24]. Here we only consider the case . We rewrite (4.27) as

| (C.1) |

where . Now we compute the expectation inside the integral in the right-hand side of (C.1),

By direct computations we have

where

with being the cumulative distribution function of a standard normal random variable. Then the integral equation (C.1) can be converted to

Letting and , we can show that satisfies the following integral equation:

| (C.2) |

where

In order to solve the above integral equation (C.2), the recursive iteration method proceeds as follows.

We divide the interval into subintervals with end points where and . Let denote the numerical approximation to . For , by the trapezoidal rule, integral equation (C.2) is approximated by

| (C.3) |

Since , the only unknown in (C.3) is . We can solve the algebraic equation (C.3) by applying the bisection method. Similarly, for , we have

| (C.4) |

Since is known from previous step, equation (C.4) can be solved for by the same procedure. Hence, for , we can obtain recursively as the solution of the following algebraic equation,

Now from the values of , in (4.26) can be approximated by

As shown by Huang et al. [22], for sufficiently large number of subintervals , the approximated free boundary converges to , and therefore, converges to as well.

Acknowledgments

Funded by the Deutsche Forschungsgemeinschaft (DFG, German Research Foundation) – Project-ID 317210226 – SFB 1283. The work of Shihao Zhu was also supported by the program of China Scholarships Council.

References

- Banks et al. [1998] Banks J, Blundell R, Tanner S (1998) Is there a retirement-savings puzzle? American Economic Review 769–788.

- Bensoussan and Lions [1982] Bensoussan A, Lions JL (1982) Applications of variational inequalities in stochastic control (NorthHolland (Amsterdam)).

- Bodie et al. [2004] Bodie Z, Detemple JB, Otruba S, Walter S (2004) Optimal consumption–portfolio choices and retirement planning. Journal of Economic Dynamics and Control 28(6):1115–1148.

- Chen et al. [2021] Chen A, Hentschel F, Steffensen M (2021) On retirement time decision making. Insurance: Mathematics and Economics 100:107–129.

- Chen et al. [2018] Chen A, Hentschel F, Xu X (2018) Optimal retirement time under habit persistence: what makes individuals retire early? Scandinavian Actuarial Journal 2018(3):225–249.

- Chen et al. [2022] Chen K, Jeon J, Wong HY (2022) Optimal retirement under partial information. Mathematics of Operations Research 47(3):1802–1832.

- Choi et al. [2008] Choi KJ, Shim G, Shin YH (2008) Optimal portfolio, consumption-leisure and retirement choice problem with CES utility. Mathematical Finance 18(3):445–472.

- Clarke [1990] Clarke FH (1990) Optimization and nonsmooth analysis (SIAM, Philadelphia, PA).

- Coile and Milligan [2009] Coile C, Milligan K (2009) How household portfolios evolve after retirement: The effect of aging and health shocks. Review of Income and Wealth 55(2):226–248.

- De Angelis [2015] De Angelis T (2015) A note on the continuity of free-boundaries in finite-horizon optimal stopping problems for one-dimensional diffusions. SIAM Journal on Control and Optimization 53(1):167–184.

- De Angelis and Ekström [2017] De Angelis T, Ekström E (2017) The dividend problem with a finite horizon. The Annals of Applied Probability 27(6):3525–3546.

- De Angelis and Stabile [2019a] De Angelis T, Stabile G (2019a) On Lipschitz continuous optimal stopping boundaries. SIAM Journal on Control and Optimization 57(1):402–436.

- De Angelis and Stabile [2019b] De Angelis T, Stabile G (2019b) On the free boundary of an annuity purchase. Finance and Stochastics 23(1):97–137.

- Dybvig and Liu [2010] Dybvig PH, Liu H (2010) Lifetime consumption and investment: retirement and constrained borrowing. Journal of Economic Theory 145(3):885–907.

- Dybvig and Liu [2011] Dybvig PH, Liu H (2011) Verification theorems for models of optimal consumption and investment with retirement and constrained borrowing. Mathematics of Operations Research 36(4):620–635.

- Farhi and Panageas [2007] Farhi E, Panageas S (2007) Saving and investing for early retirement: A theoretical analysis. Journal of Financial Economics 83(1):87–121.

- Fisher et al. [2016] Fisher GG, Chaffee DS, Sonnega A (2016) Retirement timing: A review and recommendations for future research. Work, Aging and Retirement 2(2):230–261.

- Friedman [1982] Friedman A (1982) Variational principle and free boundary problems, 1982. John wiley & Sons 1026:149–192.

- Gompertz [1825] Gompertz B (1825) On the nature of the function expressive of the law of human mortality, and on a new mode of determining the value of life contingencies. Philos. Trans. Roy. Soc. London 115:513–585.

- Guan et al. [2020] Guan G, Liang Z, Yuan F (2020) Retirement decision and optimal consumption-investment under addictive habit persistence. arXiv preprint arXiv:2011.10166 .

- Honig [1998] Honig M (1998) Married women’s retirement expectations: Do pensions and social security matter? The American Economic Review 88(2):202–206.

- Huang et al. [1996] Huang Jz, Subrahmanyam MG, Yu GG (1996) Pricing and hedging American options: a recursive integration method. The Review of Financial Studies 9(1):277–300.

- Jang et al. [2022] Jang HJ, Xu ZQ, Zheng H (2022) Optimal investment, heterogeneous consumption, and best time for retirement. Operations Research .

- Jeon et al. [2018] Jeon J, Koo HK, Shin YH (2018) Portfolio selection with consumption ratcheting. Journal of Economic Dynamics and Control 92:153–182.

- Jeon and Park [2020] Jeon J, Park K (2020) Optimal retirement and portfolio selection with consumption ratcheting. Mathematics and Financial Economics 14(3):353–397.

- Jin Choi and Shim [2006] Jin Choi K, Shim G (2006) Disutility, optimal retirement, and portfolio selection. Mathematical Finance 16(2):443–467.

- Karatzas and Shreve [1998a] Karatzas I, Shreve S (1998a) Brownian motion and stochastic calculus, volume 113 (Springer Science & Business Media).

- Karatzas and Shreve [1998b] Karatzas I, Shreve SE (1998b) Methods of mathematical finance, volume 39 (Springer).

- Karatzas and Wang [2000] Karatzas I, Wang H (2000) Utility maximization with discretionary stopping. SIAM Journal on Control and Optimization 39(1):306–329.

- Milevsky and Young [2007] Milevsky MA, Young VR (2007) Annuitization and asset allocation. Journal of Economic Dynamics and Control 31(9):3138–3177.

- Papi [2005] Papi M (2005) On the domain of the implicit function and applications. Journal of Inequalities and Applications 2005(3):1–14.

- Park and Wong [2023] Park K, Wong HY (2023) Robust retirement with return ambiguity: Optimal G-stopping time in dual space. SIAM Journal on Control and Optimization 61(3):1009–1037.

- Peskir [2005] Peskir G (2005) On the American option problem. Mathematical Finance 15(1):169–181.

- Peskir [2022] Peskir G (2022) Weak solutions in the sense of Schwartz to Dynkin’s characteristic operator equation. Research report.

- Peskir and Shiryaev [2006] Peskir G, Shiryaev A (2006) Optimal stopping and free-boundary problems (Springer).

- Szinovacz et al. [2014] Szinovacz ME, Martin L, Davey A (2014) Recession and expected retirement age: Another look at the evidence. The Gerontologist 54(2):245–257.

- Wang and Shi [2014] Wang M, Shi J (2014) Psychological research on retirement. Annual review of psychology 65:209–233.

- Yang and Koo [2018] Yang Z, Koo HK (2018) Optimal consumption and portfolio selection with early retirement option. Mathematics of Operations Research 43(4):1378–1404.

- Yang et al. [2021] Yang Z, Koo HK, Shin YH (2021) Optimal retirement in a general market environment. Applied Mathematics & Optimization 84(1):1083–1130.