Self-interacting approximation

to McKean–Vlasov long-time limit:

a Markov chain Monte Carlo method

Abstract

For a certain class of McKean–Vlasov processes, we introduce proxy processes that substitute the mean-field interaction with self-interaction, employing a weighted occupation measure. Our study encompasses two key achievements. First, we demonstrate the ergodicity of the self-interacting dynamics, under broad conditions, by applying the reflection coupling method. Second, in scenarios where the drifts are negative intrinsic gradients of convex mean-field potential functionals, we use entropy and functional inequalities to demonstrate that the stationary measures of the self-interacting processes approximate the invariant measures of the corresponding McKean–Vlasov processes. As an application, we show how to learn the optimal weights of a two-layer neural network by training a single neuron.

1 Introduction

In this paper we develop a novel method to approximate the invariant measure of the non-degenerate McKean–Vlasov dynamics

| (1) |

where is a standard Brownian motion in . The McKean–Vlasov dynamics characterize the mean field limit of interacting particles, and they have widespread applications, encompassing fields such as granular materials [3, 6, 8], mathematical biology [27], statistical mechanics [31], and synchronization of oscillators [28]. More recently, there has been a growing interest in the role of such dynamics in the context of mean field optimization for training neural networks [32, 11, 26, 34, 33, 10, 13].

In order to simulate the invariant measure of (1), we turn to the corresponding -particle approximation, i.e., the dynamics

| (2) |

where are independent Brownian motions. It is expected that the empirical measure of the -particle system can approximate the McKean–Vlasov long-time limit when and are both large enough. For fixed , to ensure control over the distance between the McKean–Vlasov dynamics in (1) and the -particle system in (2), throughout the entire time horizon, the literature has proposed various uniform-in-time propagation of chaos results under different scenarios, see for example, [24, 20, 15, 29, 9].

When the drift does not depend on the marginal law , the diffusion process is Markovian. Under general conditions, we can leverage Birkhoff’s ergodic theorem [4] to approximate its invariant measure using the occupation measure

as . In scenarios where the drift takes the form of gradient , this ergodic property of the Markov diffusion lays the groundwork for various Markov chain Monte Carlo methods, such as Metropolis adjusted Langevin algorithm [37, 36] and unadjusted Langevin algorithm [21]. Motivated by the Markovian ergodicity, the recent paper [18] studied the following self-interacting process:

| (3) |

where the dependence on the marginal distribution in McKean-Vlasov diffusion (1) is replaced by the occupation measure, that is, the empirical mean of the trajectory . In [18], the authors successfully demonstrated that, in the regime of weak interaction, where the dependence on the marginal distribution is sufficiently small, the occupation measures of the self-interacting process (3) also converge towards the invariant measure of (1) as . Remarkably, from a practical point of view, simulating the occupation measure of the self-interacting process (3) only requires a single particle, which distinguishes it from the conventional -particle approximation (2). It is worth noting that the investigation into the long-time behavior of the self-interacting diffusions can be traced back to [14, 35, 2].

Building upon the discovery in [18], this paper ventures into uncharted territory, where the mean field interaction need not to be inherently weak. We propose to study the self-interacting particle with exponential decaying dependence on its trajectory:

| (4) | ||||

for a constant . Integrating the second equation of (4), we find

that is to say, the measure is an exponentially weighted occupation measure with emphasis on the recent past. As , the measure approaches the uniformly weighted occupation measure . Therefore for small the measure is heuristically anticipated to become almost deterministic when as implied by ergodic theorems. Furthermore, if converges to some probability measure , according to the equation (4), the measure must be an invariant measure to the McKean–Vlasov dynamics (1). At the same time we intuitively expect to converge to the same limit as , that is . The heuristic insight above suggests that the weighted self-interacting dynamics (4) has the potential to approximate the invariant measure of the initial McKean-Vlasov equation (1).

While our investigation into the dynamics (4) was initially inspired by the work in [18], our results and methodologies significantly diverge from theirs, comprising two essential components. In the first part, we employ a probabilistic approach involving reflection coupling to demonstrate that the dynamics (4) exhibits Wasserstein contraction under a semi-monotonicity condition. Importantly, this condition does not ensure the uniqueness of the stationary measure to (1). (See Example 3 for a counter-example.) This is a notable departure from the “weak interaction” regime implied by [18, Assumption 1.1], where the invariant measure is both unique and globally attractive. The second facet of our research centers on the study of the stationary measure to the self-interacting process (4), in the context where the drift term is the intrinsic gradient of a “finite-dimensional” and convex mean field functional . In this scenario, we are able to provide quantitative upper bounds of the distance between and , and demonstrate this distance converges to zero as tends to zero. Here, represents the unique invariant measure of the McKean–Vlasov dynamics (1), with its uniqueness being ensured by the convexity of the functional . Notably, the “finite dimensionality” of plays a pivotal role in our analyses, see Remark 3 for more details. By amalgamating the results derived from the two parts, we ultimately construct an annealing scheme, characterized by a piecewise constant that diminishes as approaches infinity. This scheme ensures the convergence of towards .

As a final note on the terminology, although the words “stationary” and “invariant” have almost identical meanings in the context of stochastic process, we always say “invariant measure” when referring to the McKean–Vlasov process (1), and “stationary measure” when referring to the self-interacting process (4). We hope this artificial distinction would reduce possible confusions for the readers.

The rest of the paper is organized as follows. The main results are stated in Section 2. Before proving the main theorems, we apply our results to the training of a two-layer neural network in Section 3. The proofs for the reflection coupling results are given in Section 4, these for the results in the gradient case in Section 5, and the proof for the convergence of the discrete annealing scheme is given in Section 6. Finally, some technical results and proofs, and the numerical algorithm are included in the appendices.

2 Main results

We state and discuss our main results in this section. First, we study the contractivity of the self-interacting process (4), and in particular, the exponential convergence to its unique stationary measure is obtained. Then, focusing on the gradient case, we quantify the distance between the self-interacting stationary measure and the corresponding McKean–Vlasov invariant measure. Finally, applying both the results, we propose an annealing scheme so that the self-interacting dynamics converges to the McKean–Vlasov invariant measure.

To avoid extra assumptions on the drift functional , for most results of the paper, we assume the existence and the uniqueness of strong solution to the self-interacting process (4).

Assumption 1.

Given any filtered probability space supporting a Brownian motion and satisfying the usual conditions, for any initial conditions measurable to the initial -algebra and taking value in , there exists a unique adapted stochastic process such that for all ,

One may easily find various sufficient conditions for Assumption 1. For example, if is -Lipschitz continuous in measure and Lipschitz continuous in space, then by Cauchy–Lipschitz arguments, we know that the assumption is satisfied.

2.1 Contractivity of the self-interacting diffusion

We first present the results on the contractivity of the self-interacting dynamics (4), from which follows the convergence to its unique stationary measure. We start with two basic definitions. First, we define moduli of continuity.

Definition 1 (Modulus of continuity).

We say that is a modulus of continuity if it satisfies the following properties:

-

•

;

-

•

is continuous and non-decreasing;

-

•

for all , , we have .

We also introduce the notion of semi-monotonicity following Eberle [22].

Definition 2 (Semi-monotonicity).

We say that is a semi-monotonicity function for a vector field if

holds for every , with . We say is a uniform semi-monotonicity function of a family of vector fields if it is a semi-monotonicity function of each member.

In this subsection, we impose the following assumption on the drift of the McKean–Vlasov dynamics (1).

Assumption 2.

The drift satisfies the following conditions:

-

1.

For different , the vector field is uniformly equicontinuous and has a uniform semi-monotonicity function , given by for some and .

-

2.

There exist a Banach space , a Borel mapping preserving convex combinations, that is,

for all , and all , as well as a constant and a bounded modulus of continuity , for some , such that

for every , and every , .

Using reflection coupling, we derive the following result.

Theorem 1.

Suppose Assumptions 1 and 2 hold. Let , be two processes following the dynamics (4) for some such that the first marginals of their initial values , have finite first moments. Define the following metric on :

and denote the corresponding Wasserstein distance on by . Denote and . Then, we have

where the constants , are given by

for and .

Remark 1 (On Assumption 2).

Upon defining and , the first condition of Assumption 2 is equivalent to

and this holds true when in particular.

The second condition implies

where is the Wasserstein distance:

Per Lemma 11 in Appendix A, we know that the distance induces the topology of weak convergence on , so the mapping is continuous. Thus, it is redundant in Assumption 2 to suppose its Borel measurability.

Conversely, given a bounded and non-zero modulus of continuity and a drift satisfying

we consider the following space of functions

The semi-norm becomes a real norm when we restrict to the subspace of functions with . Denoting the normed space by , we can verify that the -norm is actually complete, thus is a Banach space. Then, thanks to the Kantorovich duality in Lemma 11, we can construct a Banach space isomorphic to , and a mapping with . So the second condition of Assumption 2 is satisfied.

Remark 2 (Rate of convergence).

We discuss in this remark the estimate on the rate of convergence in Theorem 1 in three different cases. In the first scenario, when the drift is -strongly monotone for some , i.e., , and when there is no mean field interaction (), we observe that and . Consequently, we can infer that and . It is worth noting that under these conditions, the component exhibits exponential contraction with a rate of , while contracts at a rate no greater than . So our lower bound on the convergence rate, though not as favorable as the optimal rate , remains at least half of the optimal rate.

In the second scenario, when is small but non-zero (with self-interaction), we find that and . Again our lower bound on the convergence rate remains at least half of the optimal rate, which should be no greater than . It is important to note that our argument, illustrated in the proof of Theorem 1, offers flexibility in adjusting the lower bound to be arbitrarily close to the optimal rate by sacrificing other constants in the estimate.

Finally, in the regime where is large, our results give exponentially small rate of convergence and exponentially large , contrary to the intuition that larger should lead to stronger contraction. To obtain more reasonable contraction constants in this case, we need to study the alternative distance function before applying the concave transport cost of Eberle [22]. However, since the main interest of this work is the self-interacting dynamics (4) when , we do not elaborate on the better constants in the regime where is large.

Now we discuss a few examples satisfying Assumption 2.

Example 1 (Two-body interaction).

Consider , where

Suppose furthermore that

that is to say, the mapping is -bounded and -Lipschitz continuous for every . Then we take the Banach space to be the dual space and let be the natural injection from into . Thus, we have

Therefore Assumptions 1 and 2 are satisfied once is uniformly Lipschitz and has a semi-monotonicity function for some and .

We can generalize the example above to drifts that depend on the measure in a non-linear way.

Example 2 ( functional).

Suppose is differentiable in the sense that there exists a continuous and bounded mapping such that

for all , and . If is finite and the vector fields are uniformly Lipschitz and share a uniform semi-monotonicity function for some and , then we can take and by the same argument as in Example 1, Assumptions 1 and 2 are satisfied.

We now examine the stationary measure of the self-interacting process (4).

Definition 3.

We call a probability measure stationary to the self-interacting diffusion (4) if the stochastic process with initial value satisfies for all .

The definition above makes sense once Assumption 1 holds.

One consequence of Theorem 1 is the existence and uniqueness of stationary measure of the self-interacting process (4).

Theorem 2.

The proof of Theorem 2 is based on the contraction result in Theorem 1 together with the Banach fixed-point theorem. Nevertheless, we still need to handle some technical issues and will report its proof in Appendix A.

Finally, we note that although Theorem 1, along with Theorem 2, implies that the self-interacting process (4) converges to its stationary measure exponentially, its assumptions are not sufficient to establish the uniqueness of invariant measure of the McKean–Vlasov process (1), as illustrated by the following example. So in general, there is no hope that the self-interacting stationary measure approximates the McKean–Vlasov invariant measure.

Example 3 (Curie–Weiss).

In the following, we present a Curie–Weiss model, i.e., a mean field model of ferromagnets, which has multiple invariant measures. Consider the McKean–Vlasov drift

where is a smooth, odd, increasing function in . Then, Assumption 2 can be verified by taking the Banach space , and the mapping to be . If , then by the result of [39], we already know that the McKean–Vlasov dynamics (1) has a unique invariant measure, which is the centered Gaussian of variance , i.e., . In the general case where is not restricted, the invariant measures of (1) correspond to the fix points of the one-dimensional mapping , given by

That is to say, if satisfies , then the Gaussian measure is invariant to (1); and vice versa. Since , we know that is always invariant. Taking the derivative of , we obtain

and if , since , by the intermediate value theorem, we have and for some . So there exists at least three invariant measures, two of which are, in physicists’ language, “symmetry-breaking” phases, and the centered Gaussian measure is the “symmetry-preserving” phase.

2.2 Stationary measure in the gradient case

In this subsection, we study the stationary measure of the self-interacting dynamics (4), provided that the drift is the negative intrinsic gradient of a convex and finite-dimensional mean field functional, whose precise meaning will be explained in the following. In particular, we aim at proving that, in this case, the stationary measure of (4) provides an approximation to the invariant measure of the McKean–Vlasov dynamics (1). We fix a positive in this subsection.

Assumption 3.

There exists a function whose gradient is of at most linear growth, and a convex function whose Hessian is bounded such that the drift term reads

In other words, for the convex mean field functional defined by

the drift is the negative intrinsic derivative:

We shall assume that there exists a stationary measure of the self-interacting dynamics (4) in this subsection.

Assumption 4.

We shall also impose the following conditions on and .

Assumption 5 (Uniform LSI).

The probability measures on determined by

are well defined and satisfy a uniform -logarithmic Sobolev inequality for some .

Assumption 6 (Bound).

The following quantity is finite:

Under all the assumptions above, it is known in the literature that there exists a unique invariant measure of the McKean–Vlasov dynamics (1) by [9, Proposition 4.4 and Corollary 4.8], and the convergence to the invariant measure is exponentially fast [9, Theorem 2.1]. The main discovery of this paper is that the stationary measure of the self-interacting dynamics (4) is close to in the following sense.

Theorem 3.

Let Assumptions 1, 3, 4, 5 and 6 hold true. Let be a stationary measure of the self-interacting process (4) and let be a random variable distributed as . Denote by and the probability distributions of the random variables and respectively. Denote also by the unique invariant measure of the McKean–Vlasov dynamics (1). Define

Then, for , we have

and

If additionally,

then the three inequalities above hold also for all , with replaced by

The proof of Theorem 3 is postponed to Section 5. As we will demonstrate in the forthcoming proof, Theorem 3 can be more readily established when the additional condition is imposed. Nevertheless, we are committed to work without this assumption, allowing the simple Gaussian case in Example 4, which we present after some discussions on the results and conditions of the theorem, to be included.

Remark 3 (Dependence on the dimension ).

Readers may have observed that, in our framework, the value of the functional may only depend on the -dimensional vector , and this corresponds to “cylindrical functions” considered in [1, Definition 5.1.11]. Given a continuous functional on , for every compact subset , we can construct, according to the Stone–Weierstrass theorem, a sequence of functions and such that the cylindrical functionals approach in the uniform topology of (see [23, Lemma 2] for example). However, the dimension may tend to infinity when . Since all the upper bounds in Theorem 3 depend on the dimension linearly, our analysis and findings cannot be directly applied to more general functionals on .

Remark 4 (Meaning of and ).

The second-order functional derivative of reads

and by the positivity of , satisfies the Cauchy–Schwarz inequality:

Similarly, the second-order intrinsic derivative satisfies

Moreover, by taking in the inequalities above, we find that and are the respective suprema of the second-order flat and intrinsic derivatives of the functional .

We illustrate in the following example that the order of when for the variance of under in Theorem 3 (i.e., the first claim) is optimal.

Example 4 (Optimality of the order of ).

Consider the mean field functional given by

The corresponding gradient dynamics (1) is then characterized by the drift

and its unique invariant measure is . The corresponding self-interacting process (4) reads

| and has a unique strong solution by Cauchy–Lipschitz arguments. Upon defining , the process has the finite-dimensional projection: | ||||

The finite-dimensional dynamics has a unique invariant measure that is a centered Gaussian with the following covariance structure:

Hence, the exact distances, or bounds thereof, read

where the last mutual bound is due to [16, Theorem 1.1]. By the Kolmogorov extension theorem, we can construct a stationary Markov process , defined on the whole real line, such that for all . Then, by defining

we recover the solution to the original infinite-dimensional dynamics. By construction, is stationary and has finite fourth moments. The rest of the assumptions of Theorem 3 can be satisfied in the following way: take , , , and the constants are given by and . By the theorem, we get

for . So the results of Theorem 3 give the optimal order of when for the variance of the variable, but possibly sub-optimal ones for the Wasserstein and total-variation distances in the direction.

2.3 Discrete annealing

In this subsection, we first introduce a dynamics which allows arbitrarily large interactions. Then, using the results from the two previous parts, we demonstrate that under a discrete annealing scheme, the solution of the self-interacting particle process (4) converges to the McKean–Vlasov invariant measure.

Assumption 7.

The functions , , satisfy the following conditions:

-

•

the function is continuous with bounded hessian, i.e., , and its gradient admits a semi-monotonicity function for some and .

-

•

the probability measure , with , is well defined in , and satisfies a -logarithmic Sobolev inequality.

-

•

the function is -strongly convex for some and belongs to .

-

•

the function belongs to .

Under Assumption 7, we consider the McKean–Vlasov (1) and the self-interacting particle (4) with the following drift:

| (5) |

Moreover, we modify the dynamics (4) so that its parameter becomes variable:

| (6) | ||||

for a function to be determined. We call the dynamics above an annealing scheme for the self-interacting particle. Our main result is the following.

Theorem 4 (Discrete annealing).

Let Assumption 7 hold and let the drift in the McKean–Vlasov (1) and the annealing self-interacting process (6) be determined by (5). Then, the invariant measure to the McKean–Vlasov process exists and is unique, and we can find a piecewise constant function such that the solution to the annealing process satisfies

for large enough.

3 Numerical application to training two-layer neural networks

Let us recall the structure of two-layer neural networks and introduce the mean field model for it. Consider an activation function satisfying

Define , where the neurons take values. For each neuron we define the feature map:

where is a truncation function with the truncation threshold . The two-layer neural network is nothing but the averaged feature map parameterized by neurons :

| (7) |

The training of neural network aims to minimize the distance between the averaged output (7) for data points and their labels , that is, the objective function of the minimization reads

| (8) |

This objective function is of high dimension and non-convex, and this difficulty motivates the recent studies, see for example [32, 12, 26] among others, to lift the finite-dimensional optimization (8) to the space of probability measures and to consider the following mean field optimization:

The mean field loss functional is apparently convex. Given that the activation and truncation functions , have bounded derivatives of up to fourth order, it has been proved in [9, Proposition 4.4] that the minimum of the entropy-regularized mean field optimization problem

can be attained by the invariant measure of the mean field Langevin dynamics:

| (9) |

where the mean field potential functional reads

By defining

we note that the mean field potential functional is of the form:

as in the gradient case investigated in Sections 2.2 and 2.3.

In order to simulate the invariant measure of the mean field Langevin dynamics (9), one usually turns to the corresponding -particle system:

| (10) |

The uniform-in-time propagation of chaos results obtained in [9, 38] ensure that the marginal distributions of the -particle system are close to those of the mean field Langevin dynamics uniformly on the whole time horizon, and can efficiently approximate mean field invariant measure provided that and are both large enough.

Note that the -particle system (10) is nothing but a regularized and noised gradient descent flow for neurons. In contrast, the self-interacting diffusion

| (11) | ||||

introduces an innovative alternative algorithm for training two-layer neural networks, in which the algorithm iterations impact only a single neuron.

Setup.

We aim to train a neural network to approximate the non-linear elementary function . We draw points sampled according to the uniform distribution on and compute the corresponding labels to form our training data . We fix the truncation function by and the sigmoid activation function by . The Brownian noise has volatility such that , and the regularization constant is fixed at in the experiment. The initial value , taking values in , is sampled from the normal distribution in four dimensions. To observe the impact of the self-interacting coefficient , we run the simulation of (11) for different equal to for . Furthermore, to compare with these results with fixed , we choose the non-increasing piecewise constant function such that on successive intervals of length , for , and train the neural network along the annealing scheme:

| (12) | ||||

We simulate both the constant and dynamic- self-interacting diffusions (11), (12) by the Euler scheme, as described in Appendix C, on a long time horizon till the terminal time , with the discrete time step .

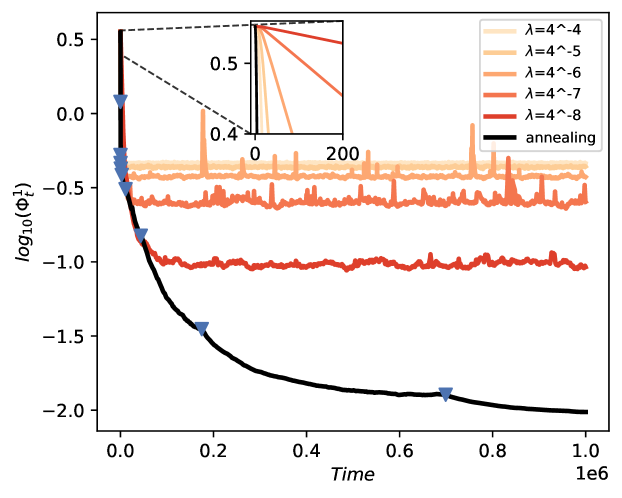

Results and discussions.

We repeat the simulations mentioned above for fixed ’s and dynamic all for times and compute the averaged loss at each time and plot its evolution in Figure 1. On the annealing scheme curve, we include triangles to visually indicate the points at which there are changes on the values of . We observe that the value of first decays exponentially, and the speed of initial decay depending on the value of . More precisely, the bigger is the value of , the faster is the initial decay. In particular, this remains true for the annealed process as it starts from a bigger value . We notice that such phenomenon is in line with our theoretical results in Theorem 1. In the long run, when fixing , the value of stabilizes at a level sensible with respect to the value of . We notice that the smaller is the value of , the better is the final performance. These facts are in line with our discovery in Theorems 1 and 3. Finally, the training exhibits the best performance when implementing the discrete annealing. The loss continues decreasing as the value of diminishes, which confirms the result in Theorem 4.

4 Proof of Theorem 1

Proof of Theorem 1.

We first note that, as pointed out in Remark 1, the mapping is continuous. Therefore, the separability of implies the separability of as a subset of the Banach space . This is sufficient to avoid the measurability issues for Banach-valued random variables and we refer readers to [30, Chapter 2] for details.

Denote , . Then the self-interacting dynamics (4) writes

| (13) | ||||

and similarly for the other dynamics driven by another Brownian motion . Note that takes value in and takes value in the Banach space . Fix . Let be a Lipschitz continuous function such that is also Lipschitz continuous and

We couple the two dynamics , by

where , are independent Brownian motions and is the -dimensional vector defined by

Subtracting the dynamical equations of , and denoting , , we obtain

where and is a one-dimensional Brownian motion by Lévy’s characterization. The absolute value of the semimartingale admits the decomposition with

| The Banach-norm process is absolutely continuous and satisfies | ||||

Hence the process

admits the decomposition with

Let be a function and define . Then, the process admits the decomposition with

for the function defined by

Thus, we have shown

Following Du et al. [19], we choose the function by requiring

and . The function is indeed continuous, and, according to [19, Lemma 5.1], it is also concave and satisfies

and

for all . Plugging in the expression for , we obtain

Thus, if , then , and

Otherwise, , and denoting by the uniform modulus of equicontinuity of the vector fields , we have

where the terms may change from line to line, but all tend to when . Then, combining the two cases above, we obtain, by Grönwall’s lemma,

for , and we conclude by taking the limit . ∎

5 Proof of Theorem 3

In this section we establish several intermediate results before giving the proof of Theorem 3.

We first note that the stationary measure, which exists according to Assumption 4, solves a partial differential equation in the following weak sense.

Proposition 5.

We omit the proof of the proposition, which follows directly from developing the difference by Itō-type calculus.

The infinite-dimensional nature of the PDE above makes its analysis difficult, and in the following we approach the problem by studying a finite-dimensional projection of it. Under Assumption 3, define the functions

They verify . Note that, if is a measure satisfying , then we have

Let be distributed as the stationary measure in Assumption 4. Setting and applying Proposition 5 to functionals of the following form:

where , we get that the joint distribution satisfies the static degenerate Fokker–Planck equation

| (14) |

in the sense of distributions. The fact that has finite fourth moment implies that its projection satisfies the following moment condition:

| (15) |

In the following, we will denote the first and second marginal distributions of by , respectively, and the conditional distributions to the second variable by . Define

| (16) |

for . Recall that is the probability measure on that satisfies a uniform LSI according to Assumption 5.

From the Fokker–Planck equation (14), we get the following result.

Proof of Lemma 6.

Then, by studying the more carefully the Fokker–Planck equation (14), we can control the relative entropy between and , the latter being introduced in (16).

Proposition 7.

In the following, we denote

| (17) |

so the result of the proposition reads

Proof of Proposition 7.

Let be the Gaussian kernel in dimensions:

We define the partial convolution , and according to (14), it solves the non-degenerate elliptic equation

| (18) |

where is defined by

Indeed, we have

Thus, . By [5, Lemma 3.1.1], we have . Then we can apply [5, Theorem 3.1.2] to (18) and obtain that and satisfies

As the function depends only on the argument, for the second term we have

where the first equality is due to Fubini and the second to the fact that . For the last term, similarly, since the function , we have and therefore,

That is to say, we have established

| (19) |

This equality implies a uniform-in- bound on by Cauchy–Schwarz. Using a sequence of functions in approaching in (14), we also get

| (20) |

The second term of (20) is upper bounded by

where the second inequality is due to (19). Using the uniform-in- bound of , we obtain that the second term of (20) converges to when . The third term of (20) satisfies

when . Hence, by (19) and (20), we have

where the last equality is due to the fact that

and

when by previous arguments and [5, Lemma 3.1.1]. We also have

when . Finally, by Lemma 6 for the function , we have

where the last equality is exactly the definition (17) of . Thus, we have shown

| (21) |

The uniform LSI for implies

Hence,

Taking into account of the lower semi-continuity of relative entropy under the weak convergence, and the weak convergences , , we take the limit in the inequality above to conclude. ∎

Remark 5.

If we formally integrate the static Fokker–Planck equation (14) with and integrate by parts, we obtain

| (22) |

However, the equality must be false. Indeed, if one artificially increases the dimension of and by defining the new functions

the right hand side of (22) increases while the left hand side stays unchanged. This phenomenon is caused by the fact that the equation (14) is degenerate elliptic and lacks Laplacian in the directions. To illustrate this effect, consider the first-order equation

in dimensions. This equation has a probability solution , the Dirac mass at the origin. Formally integrating the equation with and integrating by parts, we have

which is absurd.

We establish in the following upper bounds for the integral .

Proposition 8.

Under Assumptions 3, 4 and 5, the integral in (17) satisfies the upper bound:

| (23) |

where is the first component of the random variable following the stationary distribution , and is the unique invariant measure of the McKean–Vlasov process (1). If additionally the quantity

is finite, then we have the alternative upper bound:

| (24) |

Proof of Proposition 8.

First let us treat the simpler case where . By applying Lemma 6 to the function , we get

So the second claim of the proposition is proved.

Without the assumption , we note that, for the second-order functional derivative

we have

where is a random variable following the stationary distribution , and has the distribution . We observe

Then, by applying Lemma 12 in Appendix B to a sequence of functions approaching , we get

Let be the functional defined by

We consider the sequence of “soft cut-offs” of class approaching :

Then, by applying the sequence to Proposition 5 of stationary measure and taking the limit , we get

Thus, we have derived

and it remains to find an upper bound for . Note that, using the definition of Wasserstein distance and the triangle inequality, and letting be distributed as , we get

while the variance of is upper bounded by the Poincaré inequality:

We then conclude by combining the three inequalities above. ∎

Before moving on to the proof of Theorem 3, we need to introduce another probability measure on characterized by the following formula:

| (25) |

for all bounded and measurable . By taking depending only on the variable, we first realize that the second marginals of and agree, that is,

In addition, we show the following important properties of .

Proposition 9.

Proof of Proposition 9.

Consider the functional

where and . Then its linear functional derivative reads

so belongs to the class. Then, applying Proposition 5 to the functional , we get

By approximation, the equality above holds for and for all -continuous with the following growth bounds:

that is to say, we have

where, as before, . Specializing to , we obtain

where the last equality is due to Lemma 6, as for , we have . So the first claim is proved. Taking , for , yields the second claim.

For the last claim, we take for of linear growth in the defining equation (25) of . Then, we get

The desired property follows from the arbitrariness of . ∎

Proof of Theorem 3.

The proof consists of five steps.

Step 1: Control of the symmetrized entropy. We aim at controlling the symmetrized entropy

in this step. First observe

| (26) |

In order to control the right hand side above, we turn to the probability measure introduced in (25). Recall that is the invariant measure of the McKean–Vlasov (1), and . The convexity of implies the convexity of as a functional, and as a result, for -a.s. , we have the tangent inequalities

| (27) |

Thanks to the last claim of Proposition 9, the leftmost term satisfies, for -a.s. ,

Hence, integrating the tangent inequalities (27) above by , we get

| (28) |

Using and applying Proposition 9 to , we know that the left hand side of (28) satisfies

The right hand side of (28) satisfies

where the third equality is due to the last claim of Proposition 9. Thus, we have derived

| (29) |

Therefore, to dominate the right hand side of (26), it remains to control the following term. Using the Kantorovich duality, we get

where, by Assumption 6, for all , , and is the quantity to be controlled in the first claim of the theorem. The uniform LSI for implies a uniform Talagrand’s transport inequality, from which we obtain

Combining the two inequalities above with (26) and (29), we obtain

| (30) |

Step 2: Control of the conditional Wasserstein distance. Now, using again the Talagrand’s transport inequality for and (note that for ), we get

while the triangle inequality and the transport inequality imply

So, combining the three inequalities above and integrating with , we find

| (31) |

Step 3: Control of by . Applying Proposition 9 to the function , where, as we recall, , we get

where the last equality is due to the last claim of Proposition 9. In other words, we have

and this implies, by Cauchy–Schwarz,

As for all and , we have, by the Kantorovich duality,

| (32) |

Thus, using the fact that and the inequality (31), we obtain

Introduce the “adimensionalized” variable

Then the inequality above reads

Hence, we get

| (33) |

Step 4: Control of Wasserstein and TV distances by . By inserting (33) into (31), and noting, by the definition of the Wasserstein distance,

we get

| (34) |

For the total variation distance, we observe that the Csiszár–Kullback–Pinsker lity implies

By the triangle and Jensen’s inequalities, we get

Then, by inserting (33) into (30), we get

| (35) |

6 Proof of Theorem 4

Before proving Theorem 4, we first explain how to apply the results in Theorems 1, 2, 3 to get error bounds on the self-interacting process (4) with constant .

Lemma 10.

Let . Under Assumption 7, the McKean–Vlasov dynamics (1) corresponding to the drift (5) has a unique invariant measure . Moreover, if we let be the a solution to the self-interacting SDE (4) of finite first moment and with the same drift (5), then, denoting

| (36) |

we have

for some , , depending only on , and .

Proof of Lemma 10.

First, as the drift has derivative

we have

for every and every . Then the dynamics falls into the class considered in Example 2, and Theorems 1 and 2 apply. In particular, we know that the stationary measure of the self-interacting particle (4) exists and is unique. Moreover, letting be distributed as , and denoting , , we have

| (37) |

for some , independent of , according to the discussion in Remark 2.

Then, to apply the result in the gradient case in Theorem 3, we introduce the functions , defined respectively by

In this way, the drift reads

so Assumption 3 is satisfied. Now we show the stationary measure of the dynamics (4) has finite fourth moment. Consider the “energy” functional

Along the self-interacting dynamics (4), we have, by Itō’s formula,

As the vector field has weak monotonicity function , we have

for every , for some . Then, the energy functional verifies the Lyapunov condition as well:

for some , . Thus, the unique stationary measure of finite first moment must have finite fourth moment and Assumption 4 is satisfied. Since

with , by the Holley–Stroock perturbation argument [25], we know that the measure verifies a uniform -LSI with

so Assumption 5 is satisfied. The constants , in Theorem 3 and Assumption 6 are finite as

Hence, all the assumptions are satisfied and Theorem 3 implies, for some ,

where and . Combining the inequality above with (37) concludes. ∎

Proof of Theorem 4.

We prove the theorem in two steps. First, we choose the function and show the first claim on the convergence of . Second, using the first claim, we apply reflection coupling again, to demonstrate the convergence of , which is the second claim.

Step 1: Choice of and convergence of . We choose

where are given by the recursive relation

for to be determined in the following. Following the definition (36) for the constant case, we define

| (38) |

Denote and . Noting that on the interval , the dynamics (6) is nothing but the self-interacting process (4) with constant , and the distance is nothing but the corresponding , we can apply Lemma 10 to get

where , are the constants of the lemma. Take such that , i.e.,

Then, from the inequality above, we deduce

Consequently, we get

and therefore, for , we have, again according to Lemma 10,

By definition,

where the symbol means equivalence up to multiplicative constants for sufficiently large . Thus, we have and , for . Hence, we have shown the first claim:

Step 2: Convergence of by reflection coupling. Now we construct again a reflection coupling to show the second claim. Let be the solution of the SDE

with initial condition and , and being a Brownian motion to be determined below. Since is invariant to the McKean–Vlasov diffusion (1), we know that . Fix . Let be a Lipschitz continuous function such that is also Lipschitz continuous and

We couple the two dynamics , by

where , are independent Brownian motions and is the -dimensional vector defined by

Define . As in the proof of Theorem 1, the norm process admits the decomposition with

where and is a one-dimensional Brownian. Recalling that is increasing, we choose the concave function by

and . The function solves

and, according to the computations in the proof of Theorem 1, we have

Thus, when , the process satisfies

In the contrary case where , we have

where the term tends to when . Using Grönwall’s lemma, we obtain

The integral over the interval , for some large enough, is upper bounded, up to a multiplicative constant, by

Here the symbol means the term on the left is upper bounded by the term on the right, up to multiplicative constants, for large enough. Note that the final term on the right also dominates the exponential decay for sufficiently large . So taking the limit , we get

and this concludes. ∎

Appendix A Proof of Theorem 2

We first study the space of probability measures metrized by Wasserstein distances induced by a bounded modulus of continuity.

Lemma 11.

Let be a bounded modulus of continuity. Then the space of probabilities , endowed with the Wasserstein distance

is a complete and separable metric space, which induces the topology of weak convergence on . Moreover, we have the Kantorovich duality:

where the norm of the function is defined by

Proof of Lemma 11.

It suffices to consider the alternative distance

on and apply standard results about Wasserstein distances on metric spaces (see for example [7, Section 5.1]). ∎

Before moving on to the proof of the theorem, let us first explain the main technical issue in applying the Banach fixed-point theorem. The problem is that the contraction result in Theorem 1 is not stated for the solution of the original process (4), but rather for a projection of it. In particular, the projection mapping may fail to be injective and some information about the variable is lost. Quite surprisingly, this issue can be solved by augmenting the Banach space in a way that preserves Assumption 2.

Proof of Theorem 2.

We divide the proof into several steps.

Step 1: Augmentation to the Banach space. Let Assumption 2 hold. Define and let be the mapping defined by

where is the natural injection. We define the new modulus of continuity by

Since we can take as the upper bound for , by the same argument as in Examples 1 and 2, we know that the Banach space , the mapping , the same constant and the modulus of continuity satisfy Assumption 2.

Step 2: Uniqueness. Let and be two random variables distributed as two stationary measures , respectively. By applying Theorem 1 to the augmented construction , we have

This implies that for every , we have

This property extends to every continuous bounded by density and hence,

That is to say the stationary measure is unique.

Step 3: Existence. Since the augmented mapping is injective by construction, one can define the following distance on :

As pointed out in Remark 1, we have the mutual bound

Then, by applying Lemma 11, we get that is a complete metric space and induces the topology of weak convergence. In the following, we will always equip with the distance .

Denote by the semi-group of operators acting on probability measures on the product metric space . That is to say, for , we construct a stochastic process solving (4) according to Assumption 1, and set

for all . By the discussion in the paragraph above, the product metric space is complete and separable, and therefore, , equipped with the -distance, is also complete and separable. Using the continuity of the trajectory and the dominated convergence theorem, we get that the mapping is continuous with respect to the distance, i.e., the semi-group is -continuous. Applying Theorem 1 to the augmented construction , we get that there exists a such that for every , the operator is a contraction on with respect to the distance. The Banach fixed-point theorem then assures the existence of a unique fixed point of in for such . Denote in this case the fixed point by . Let , be rational to each other, i.e., . We can find that is a integer multiple of both and , and therefore,

The uniqueness of fixed point of implies . Similarly, we have , and consequently, . By the density of rationals in and -continuity of the semi-group , we find for all , , and we denote . Finally, by the semi-group property, for every , we have

and this concludes the proof of the existence. ∎

Remark 6.

For the existence part of the proof above, we could also show that the Markov semi-group is Feller by synchronous coupling. Then together with tightness, we could get the existence of a stationary measure by the Krylov–Bogoliubov theorem [17, Theorem 12.3.2]. However, it seems difficult to apply general results on Markov chains to get the uniqueness of stationary measure without the contraction in Theorem 1. In particular, since the diffusion in the self-interacting process (4) is highly degenerate, we do not expect the strong Feller property to hold.

Appendix B A lemma on Wasserstein duality

Lemma 12.

Let be a function such that the Euclidean operator norm of satisfies

for all and . Then, for all , and , , we have

Proof of Lemma 12.

Let be the -optimal transport plan between and , and be that between and . Construct the random variable distributed as . Then, we have

Therefore, taking absolute values, we get

which concludes the proof. ∎

Appendix C Algorithm

Acknowledgements.

The authors would like to thank Fan Chen for his help in the numerical implementation.

Funding.

The first author’s research is supported by the National Natural Science Foundation of China (No. 12222103), and by the National Key R&D Program of China (No. 2022ZD0116401). The second author’s research is supported by Finance For Energy Market Research Centre. The third author’s research is supported by the European Union’s Horizon 2020 research and innovation programme under the Marie Skłodowska-Curie grant agreement No. 945332.

References

- [1] Luigi Ambrosio, Nicola Gigli, and Giuseppe Savaré. Gradient flows in metric spaces and in the space of probability measures. Basel: Birkhäuser, 2005.

- [2] Michel Benaïm, Michel Ledoux, and Olivier Raimond. Self-interacting diffusions. Probab. Theory Relat. Fields, 122(1):1–41, 2002.

- [3] Dario Benedetto, Emanuele Caglioti, José A. Carrillo, and Mario Pulvirenti. A non-Maxwellian steady distribution for one-dimensional granular media. J. Stat. Phys., 91(5-6):979–990, 1998.

- [4] George D. Birkhoff. Proof of the ergodic theorem. Proc. Natl. Acad. Sci. USA, 17:656–660, 1931.

- [5] Vladimir I. Bogachev, Nicolai V. Krylov, Michael Röckner, and Stanislav V. Shaposhnikov. Fokker–Planck–Kolmogorov equations, volume 207 of Math. Surv. Monogr. Providence, RI: American Mathematical Society (AMS), 2015.

- [6] François Bolley, Ivan Gentil, and Arnaud Guillin. Uniform convergence to equilibrium for granular media. Arch. Ration. Mech. Anal., 208(2):429–445, 2013.

- [7] René Carmona and François Delarue. Probabilistic theory of mean field games with applications I. Mean field FBSDEs, control, and games, volume 83 of Probab. Theory Stoch. Model. Cham: Springer, 2018.

- [8] José A. Carrillo, Robert J. McCann, and Cédric Villani. Kinetic equilibration rates for granular media and related equations: entropy dissipation and mass transportation estimates. Rev. Mat. Iberoam., 19(3):971–1018, 2003.

- [9] Fan Chen, Zhenjie Ren, and Songbo Wang. Uniform-in-time propagation of chaos for mean field Langevin dynamics. arXiv preprint arXiv:2212.03050, 2022.

- [10] Lénaïc Chizat. Mean-field Langevin dynamics : Exponential convergence and annealing. Transactions on Machine Learning Research, 2022.

- [11] Lénaïc Chizat and Francis Bach. On the global convergence of gradient descent for over-parameterized models using optimal transport. In S. Bengio, H. Wallach, H. Larochelle, K. Grauman, N. Cesa-Bianchi, and R. Garnett, editors, Advances in Neural Information Processing Systems, volume 31. Curran Associates, Inc., 2018.

- [12] Lénaïc Chizat and Francis Bach. On the global convergence of gradient descent for over-parameterized models using optimal transport. In S. Bengio, H. Wallach, H. Larochelle, K. Grauman, N. Cesa-Bianchi, and R. Garnett, editors, Advances in Neural Information Processing Systems, volume 31. Curran Associates, Inc., 2018.

- [13] Giovanni Conforti, Anna Kazeykina, and Zhenjie Ren. Game on random environment, mean-field Langevin system, and neural networks. Mathematics of Operations Research, 48(1):78–99, 2023.

- [14] Michael Cranston and Yves Le Jan. Self attracting diffusions: Two case studies. Math. Ann., 303(1):87–93, 1995.

- [15] François Delarue and Alvin Tse. Uniform in time weak propagation of chaos on the torus. arXiv preprint arXiv:2104.14973, 2021.

- [16] Luc Devroye, Abbas Mehrabian, and Tommy Reddad. The total variation distance between high-dimensional Gaussians with the same mean. arXiv preprint arXiv:1810.08693, 2018.

- [17] Randal Douc, Éric Moulines, Pierre Priouret, and Philippe Soulier. Markov chains. Springer Ser. Oper. Res. Financ. Eng. Cham: Springer, 2018.

- [18] Kai Du, Yifan Jiang, and Jinfeng Li. Empirical approximation to invariant measures for McKean–Vlasov processes: mean-field interaction vs self-interaction. Bernoulli, 29(3):2492–2518, 2023.

- [19] Kai Du, Yifan Jiang, and Xiaochen Li. Sequential propagation of chaos. arXiv preprint arXiv:2301.09913, 2023.

- [20] Alain Durmus, Andreas Eberle, Arnaud Guillin, and Raphael Zimmer. An elementary approach to uniform in time propagation of chaos. Proc. Am. Math. Soc., 148(12):5387–5398, 2020.

- [21] Alain Durmus and Éric Moulines. Nonasymptotic convergence analysis for the unadjusted Langevin algorithm. Ann. Appl. Probab., 27(3):1551–1587, 2017.

- [22] Andreas Eberle. Reflection couplings and contraction rates for diffusions. Probab. Theory Relat. Fields, 166(3-4):851–886, 2016.

- [23] Wendell H. Fleming and Michel Viot. Some measure-valued Markov processes in population genetics theory. Indiana Univ. Math. J., 28:817–843, 1979.

- [24] Arnaud Guillin and Pierre Monmarché. Uniform long-time and propagation of chaos estimates for mean field kinetic particles in non-convex landscapes. J. Stat. Phys., 185(2):20, 2021. Id/No 15.

- [25] Richard Holley and Daniel Stroock. Logarithmic Sobolev inequalities and stochastic Ising models. J. Stat. Phys., 46(5-6):1159–1194, 1987.

- [26] Kaitong Hu, Zhenjie Ren, David Šiška, and Łukasz Szpruch. Mean-field Langevin dynamics and energy landscape of neural networks. Ann. Inst. Henri Poincaré, Probab. Stat., 57(4):2043–2065, 2021.

- [27] Evelyn F. Keller and Lee A. Segel. Model for chemotaxis. J. Theor. Biol., 30(2):225–234, 1971.

- [28] Yoshiki Kuramoto. Rhythms and turbulence in populations of chemical oscillators. Physica A: Statistical Mechanics and its Applications, 106(1):128–143, 1981.

- [29] Daniel Lacker and Luc Le Flem. Sharp uniform-in-time propagation of chaos. Probab. Theory Relat. Fields, 187(1-2):443–480, 2023.

- [30] Michel Ledoux and Michel Talagrand. Probability in Banach spaces. Isoperimetry and processes, volume 23 of Ergeb. Math. Grenzgeb., 3. Folge. Berlin etc.: Springer-Verlag, 1991.

- [31] Nicolas Martzel and Claude Aslangul. Mean-field treatment of the many-body Fokker-Planck equation. J. Phys. A, Math. Gen., 34(50):11225–11240, 2001.

- [32] Song Mei, Andrea Montanari, and Phan-Minh Nguyen. A mean field view of the landscape of two-layer neural networks. Proc. Natl. Acad. Sci. USA, 115(33):e7665–e7671, 2018.

- [33] Atsushi Nitanda, Denny Wu, and Taiji Suzuki. Convex analysis of the mean field Langevin dynamics. In Gustau Camps-Valls, Francisco J. R. Ruiz, and Isabel Valera, editors, Proceedings of The 25th International Conference on Artificial Intelligence and Statistics, volume 151 of Proceedings of Machine Learning Research, pages 9741–9757. PMLR, 28–30 Mar 2022.

- [34] Atsushi Nitanda, Denny Wu, and Taiji Suzuki. Particle dual averaging: optimization of mean field neural network with global convergence rate analysis. J. Stat. Mech. Theory Exp., 2022(11):51, 2022. Id/No 114010.

- [35] Olivier Raimond. Self-attracting diffusions: Case of the constant interaction. Probab. Theory Relat. Fields, 107(2):177–196, 1997.

- [36] Gareth O. Roberts and Jeffrey S. Rosenthal. Optimal scaling of discrete approximations to Langevin diffusions. J. R. Stat. Soc., Ser. B, Stat. Methodol., 60(1):255–268, 1998.

- [37] Gareth O. Roberts and Richard L. Tweedie. Exponential convergence of Langevin distributions and their discrete approximations. Bernoulli, 2(4):341–363, 1996.

- [38] Taiji Suzuki, Atsushi Nitanda, and Denny Wu. Uniform-in-time propagation of chaos for the mean-field gradient Langevin dynamics. In The Eleventh International Conference on Learning Representations, 2023.

- [39] Feng-Yu Wang. Distribution dependent SDEs for Landau type equations. Stochastic Processes Appl., 128(2):595–621, 2018.