2021

1]\orgdivDepartment of Mathematics and Statistics, \orgnameUniversity of Nevada, Reno, \orgaddress1664 \streetN. Virginia Street, \cityReno, \postcode89557, \stateNevada, \countryUSA

Withdrawal Success Optimization

Abstract

For assets and discrete-time rebalancing, the probability to complete a given schedule of investments and withdrawals is maximized over progressively measurable portfolio weight functions. Applications consider two assets, namely the S&P Composite Index and an inflation-protected bond. The maximum probability and optimal portfolio weight functions are computed for annually rebalanced schedules involving an arbitrary initial investment and then equal annual withdrawals over the remainder of the time period. Applications also consider annually rebalanced schedules that start with dollar cost averaging (equal annual investments) and then shift to equal annual withdrawals. Results indicate noticeable improvements in the probability to complete a given schedule when optimal portfolio weights are used instead of constant portfolio weights like the standard of keeping 90% in the S&P Composite Index and 10% in inflation-protected bonds.

keywords:

Dollar cost averaging, Terminal wealth, Standard and Poor, Lévy alpha-stable, Withdrawals1 Introduction

Suppose an investor wishes to make a particular schedule of investments and withdrawals. Assume the number of investments and withdrawals are finite and completely determined at time . Given assets available for investment, the goal is to maximize the probability to complete the schedule, with the maximization occurring over time-adapted portfolio weights. Assume the set of rebalancing times is finite and contains the set of investment and withdrawal times.

Theoretical results present a recursive formula that computes this maximum probability, providing the optimal time-adapted portfolio weights along the way. The recursive formula is also generalized to incorporate a mortality distribution. In this case, the goal is to maximize the probability of completing just the scheduled investments and withdrawals that occur while the investor is alive.

Applications focus on two assets: the S&P Composite Index and an inflation protected bond. This combination offers a good balance of high risk - high return and low risk - low return. In particular, the risk and return of the portfolio is increased (decreased) by raising (lowering) the proportion of wealth invested in the S&P Composite Index. Consequently, the optimal portfolio weights indicate the best time-adapted balance of high risk - high return and low risk - low return for the given schedule of investments and withdrawals.

Two general investment schedules are considered in applications. There is the schedule that starts with a lump sum investment and then has equal withdrawals for a specified length of time or until death. There is also the schedule that starts with dollar cost averaging (DCA) and then has equal withdrawals for a specified length of time or until death. Note that in DCA, equal amounts are invested at equidistant times. In applications, all investments and withdrawals are executed on an annual basis. Rebalancing occurs whenever an investment or withdrawal is made.

The maximum probability to complete the schedule is compared to the probability resulting from portfolio weights that are constant over time. Special attention is given to the portfolios with , where of wealth is invested in the S&P Composite Index and of wealth is invested in the inflation protected bond. generally gives a probability that is closest to the maximum probability; however, the difference can be several tenths (note that probability is measured here on a scale from 0 to 1).

The following results from applications demonstrate the advantage in using optimal portfolio weights versus constant portfolio weights. Consider the schedule having an initial lump sum investment and then equal annual withdrawals. Suppose the initial investment is 30 times the withdrawal amount. Then an investor can make 50 annual withdrawals with 95% confidence, and a 60 year old can make annual withdrawals until death with 99% confidence. Note that only investing in the S&P Composite Index would result in 90.9% and 97.3% confidence, respectively. Next consider the schedule that starts with DCA and then has equal annual withdrawals. Suppose .5 times the withdrawal amount is invested annually for 30 years. Then the investor can make 50 years of withdrawals with 95% confidence; only investing in the S&P Composite Index would result in 92.4% confidence. Suppose .95 times the withdrawal amount is invested annually for 20 years, starting at age 20. Then starting at age 40, the investor can make annual withdrawals until death, with 95% confidence; only investing in the S&P Composite Index would result in 93% confidence.

1.1 Literature Review

Maximizing the probability that an outcome lies above a particular value is known as the safety first principle, originally considered by Roy (1952). Here, the outcome in question is the terminal wealth resulting from a given schedule of investments and withdrawals. Under the setup detailed in section 2, a given schedule of investments and withdrawals is successfully executed if and only if terminal wealth is non-negative. Thus, the goal is to maximize the probability that terminal wealth is non-negative. In the parlance of Roy (1952), the disaster level here is 0. The theory presented here also handles other disaster levels, but the primary focus is on 0.

To account for nuances of individual choice that safety first misses, Levy and Levy (2009) proposed the expected utility - safety first (EU-SF) model. In particular, the EU - SF model takes a continuous utility function and seeks to maximize the weighted average of that utility and the probability for the outcome to be greater than or equal to some disaster level. Recently, the EU - SF model has been extended to support a probability distortion function, which addresses further nuances of individual choice like the overestimation of low probability events and underestimation of high probability events (Li and Mi, 2021). Since successful execution of a given schedule of investments and withdrawals is fully characterized by the safety first principle with disaster level 0, there is no need to consider these more complicated extensions here.

The discrete-time portfolio optimization problem is considered in Phelps (1962), with the goal being to maximize the expected lifetime utility of consumption. The focus is on lifetime utility functions of the form

where is the amount consumed at the beginning of period and is bounded, strictly increasing, strictly concave and continuously differentiable. In words, this lifetime utility function is the separable sum of each period’s discounted utility of consumption. Expexted lifetime utility of consumption is maximized when there is investment in just one asset that has iid return over each period. The return distribution is assumed to be discrete with a finite number of outcomes. This optimization is generalized in Hakansson (1975) to the multi-asset case with bounded, possibly non-discrete, return distributions. Special attention is given the infinite period case and utilities with constant relative or absolute risk aversion index.

The portfolio optimization problem can also be approached from the continuous angle, where stock prices follow stochastic differential equations and portfolios are rebalanced continuously in time. In Karatzas et al (1987), the goal is to maximize expected discounted utility of consumption and terminal wealth over a continuously rebalanced portfolio. The effect of various wealth-based constraints on the maximization of expected utility of terminal wealth is considered in Basak and Shapiro (2001) and Kraft and Steffensen (2013). Here, stock price processes can be generated by stochastic differential equations, but the portfolios are not rebalanced continuously in time. It is advantageous to consider discrete-time rebalancing, since there can be significant error in results when a strategy that involves continuous rebalancing is discretized for applications.

For a portfolio consisting of the S&P 500 index and US Treasury Bills, Musumeci and Musumeci (1999) use dynamic programming to compute the optimal portfolio weights for an investor looking to maximize his expected utility of wealth , where and are constants. Results only account for an initial investment that is rebalanced periodically. Additional investments and withdrawals are not considered in the dynamic programming formulation. Here, applications focus on the effect of periodic investments and withdrawals on the optimal portfolio weights, with the goal being to maximize the safety first utility with disaster level 0. Furthermore, this safety first utility is easily understood as the probability to complete a given schedule of investments and withdrawals.

In Bertsekas and Shreve (1996), the discrete-time stochastic dynamic programming problem is generalized to the Borel setting where results are carefully treated with measure theory. Theoretical results presented here follow a similar framework. However, the formulation is slightly different. Here, asset prices and portfolio weights are progressively measurable with respect to a filtration that represents the evolution of information over time.

Results presented here are meant to serve individual investors, ultimately providing an idea of how much retirement income can be reliably generated by an individual account. Maintaining an individual account during retirement can be advantageous because the investor maintains unconditional control over his wealth. Annuities can offer good deals on retirement income, but the purchaser must surrender some control over his wealth. Annuities are also focused on seniors, with many having minimum age requirements that leave out younger investors. Since the results presented here use an individual account, they are more accessible, giving younger investors an annuity-like alternative. For examples of research that considers annuities in the problem of optimizing retirement income, see Antolín et al (2010), Butt and Khemka (2015) and the references therein.

1.2 Organization

Section 2 provides the problem set-up. Theoretical results are given in section 3, with their proofs in Appendix A. Section 4 provides applications of theoretical results using data. Data is described in section 4.1. Closing remarks and a discussion of related future research ideas are given in section 5.

2 Preliminaries

Introduce the filtered probability space , where denotes a filtration of and , . Consider assets available for investment, each denoted by an index from 1 to . For each , let be an -adapted process. When convenient, write in place of , understanding that is an -measurable function on . In this setting, denotes the value of asset at time .

Let be an increasing sequence in with . Require that for each and , is independent of . Suppose is invested or withdrawn at each time step . Positive indicate investments, and negative indicate withdrawals. No other investments or withdrawals are made. Further suppose that rebalancing occurs only at those times . Note that in this set-up, rebalancing can occur at time with .

After accounting for , denote the wealth available for investment at time with . At each time , rebalance according to the -measurable portfolio weight vector , where . When convenient, write , understanding that and each is an -measurable function on . In particular, at each time , invest in asset for each .

To simplify notation, let for and . When convenient, write . Let for . Then the wealth at time step is given by , where the are computed recursively via

| (1) |

Again, note that wealth at time step is computed after accounting for the invesment or withdrawal of at time step . Furthermore, observe that each , and is an -measurable function on . Figure 1 illustrates (1) in the context of a decision tree.

Some additional conditions must be placed on the in order for to make sense. In particular, will make sense if implies for each . This guarantees that a failure to execute a schedule of investments and withdrawals up to time , indicated by , will be carried over to time and indicated by . To achieve such propagation of negativity in the , it suffices to require that implies for . Observe that if , then for all . On the other hand, if at least one of the in is negative, then this requirement makes negative, in which case implies for each .

Observe that is a function of each for . The notation

is used to denote the supremum of over all -measurable portfolio weight vectors , where . This kind of abbreviation is used in similar situations where there is a -like function that is constructed using the -measurable .

Use to denote the expectation with respect to . Use to denote , the expectation conditioned on the -algebra generated by . Use to denote the real numbers. Given and , use to denote . Given sets , and , use to denote the pointwise supremum of the , meaning for each , . Let denote the -dimensional vector of 1s, and use to indicate the dot product. For a vector , use to denote the -th component of . Let denote the indicator function of .

Lemma 1 (proposition 2.13 of De Saporta and Zili (2021)).

Let and be -measurable functions, a sub--algebra of and a Borel measurable function such that is integrable. If is independent from and is -measurable, then

with for all .

Lemma 2 (lemma 1.13 of Kallenberg (2019)).

Fix two measurable functions and from into some measurable spaces and , where the former is Borel. Then is -measurable iff there exists some measurable mapping with .

3 Theoretical Results

For a given non-negative constant and positive integer , the goal is to find the supremum of over the portfolio vectors , where . That goal is expressed in (2).

| (2) |

It is unreasonable to compute (2) by testing all possible portfolio vectors , where . Instead, a recursive method is presented that allows more reasonable computation of (2).

Before presenting the recursive method used to compute (2), a simpler method is presented that allows computation of for given portfolio vectors . This method is useful in applications because it fascilitates comparisons between (2) and the resulting from given portfolio vectors .

3.1 Computing for given

The simpler recursive method arises after expressing in terms of conditional expectations. Define the Borel measurable function such that

| (3) |

Using lemma 2, let , , denote the Borel measurable functions satisfying

| (4) |

Note that integrability of follows from induction and the fact that is bounded. Furthermore, is -measurable and is a sub -algebra of , so the conditional expectation in (4) is a well-defined -measurable function. Next observe that

| (5) |

By (4) and the law of total expectation,

| (6) |

Since is deterministic, . It follows from (5) and (6) that

| (7) |

If the are -measurable for , then by lemma 2, there exist Borel measurable such that for each . In this situation, can be computed recursively using (4) and the following. Recall from (1) that . If for each , it follows from lemma 1 that there is an with such that for each ,

| (8) |

For simplicity, compute using for all . Next, the above recursion is modified to incorporate the supremum in (2).

3.2 Computing (2)

First define the non-decreasing upper semicontinuous function such that

| (9) |

Let , , denote the non-decreasing upper semicontinuous functions satisfying

| (10) |

Moreover, (2) is given by , which can be computed recursively, starting with (9) and then using (10). Proofs of the previous statements are given in sections A.3 and A.4 of the appendix.

3.3 Computing (2) with stock-bond portfolios

Fix and . Let denote the value of the stock at time . Assume the are continuous in the sense that for each and . Let , meaning denotes the value of the bond, with interest , at time . Let be the natural filtration generated by . Let , and for , let

| (11) |

If , then only investing in the bond would yield . So the case where is not worth studying. Hence, require that each () is positive.

Under the above set-up, each () is continuous over and right continuous at . When ,

For ,

| (12) |

where . See section A.5 in the appendex for proofs of the previous three statements.

3.4 Extension to a mortality distribution

Let the Borel measurable function denote the investor’s time of death. Require that is independent of for every and . Assume is a continuous random variable so that borderline cases where death occurs at time is not an issue. Let be such that implies . By the law of total probability,

| (14) |

If the are -measurable, then is independent to each and

| (15) |

Moreover, each in (15) can be computed using section 3.1 or direct simulation of the .

Now it is tempting to maximize (14) over . First set up the recursion

| (16) |

Observe that

| (17) |

which implies

| (18) |

If , then (18) and (14) coincide. Otherwise, can be chosen large enough such that (18) approximates (14). So for sufficiently large,

| (19) |

There is also the inequality

| (20) |

which holds for any . Notice the similarity between (2) and the right side of (19). This similarity is taken advantage of to obtain the following result.

Let be independent random variables for , where . Additionally require that each is -measurable and independent of for every and . Define such that for each and ,

Let , where is as in (9). For , let denote the non-decreasing upper semicontinuous functions satisfying

| (21) |

Then the right side of (19) is given by , which can be computed recursively, starting with (9) (since ) and using (21) after that. Proof of the previous statements are given in section A.6 of the appendix.

4 Applications

Theoretical results are applied to portfolios consisting of the S&P Composite Index and an inflation-protected bond. Applications use a mortality distribution that is based on the 2017 per-age death rates of the US Social Security area population. Section 4.1 describes the S&P Composite Index data and the mortality distribution data. Section 4.2 justifies the treatment of S&P returns as iid and details the set-up needed to apply theoretical results. Algorithms used in applications are described in section 4.2. Results of applications are given in section 4.3.

4.1 Data

Annual data from the S&P Composite Index and Comsumer Price Index is taken from http://www.econ.yale.edu/~shiller/data.htm, collected for easy access at https://github.com/HaydenBrown/Investing. The data spans 1871 to 2020 and is described in table 1. Note that S&P Composite Index refers to Cowles and Associates from 1871 to 1926, Standard & Poor 90 from 1926 to 1957 and Standard & Poor 500 from 1957 to 2020. Cowles and Associates and the S&P 90 are used here as backward extensions of the S&P 500.

The data is transformed so that annual returns incorporate dividends and are adjusted for inflation. In particular, returns are computed using the consumer price index, the S&P Composite Index price and the S&P Composite Index dividend. Use the subscript to denote the th year of , and from Table 1. The return for year is computed as .

| Notation | Description |

|---|---|

| I | Average monthly close of the S&P composite index |

| D | Dividend per share of the S&P composite index |

| C | January consumer price index |

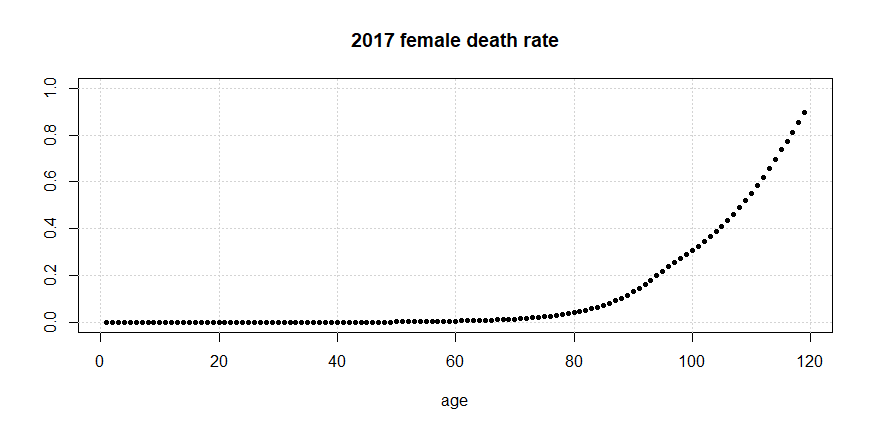

Death rates are taken from https://www.ssa.gov, the official website of the Social Security Administration. In particular, the female per-age death rates of the US Social Security area population are taken from the 2017 period life table. Female death rates are used because they are generally lower than male death rates. The female death rates are illustrated in figure 2.

Let denote the 2017 female death rate for age , and let denote the starting age for a given schedule of investments and withdrawals. Applications use and

4.2 Set-up

In order to apply theoretical results, , , for , and need to be specified. Set and . Let denote the inflation-adjusted value of the S&P Composite Index at time , and let , meaning denotes the inflation-adjusted value of an inflation-protected bond, with interest , at time . Set for . When no mortality distribution is present, let be the natural filtration generated by . When a mortality distribution is present, adjust the previous as follows

Since and are inflation-adjusted, it follows that the and are also inflation-adjusted. For example, if and inflation is 5% from time 0 to time , then the actual amount withdrawn at time is . In other words, 2 is the inflation-adjusted amount withdrawn, and is the actual amount withdrawn.

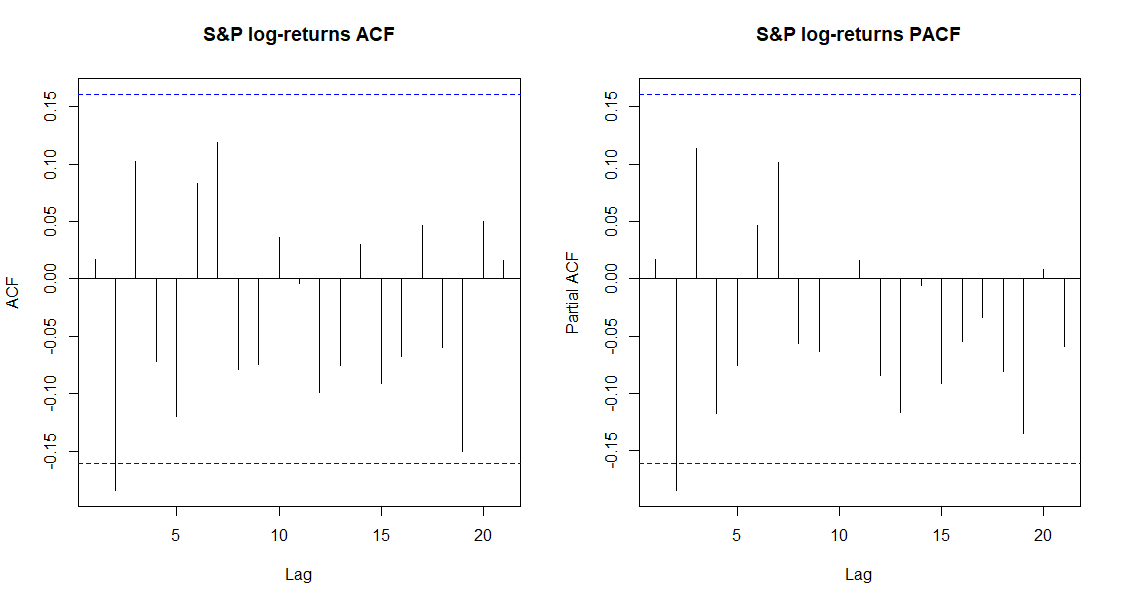

Theoretical results also require the to be independent of . It suffices to have iid . Observing that is deterministic, it suffices to justify the assumption that annual S&P returns are iid. Table 2 provides p-values from the Ljung-Box test on returns, log-returns and the absolute value of annual log-returns. The p-value of .078 is slightly concerning, but not enough to reject independence with the usual 95% confidence. The autocorrelation and partial autocorrelation functions of annual log-returns are given in figure 3. Overall, the assumption that annual S&P returns are independent appears to be supported by the data. Next, the distribution of the annual returns is fitted.

| returns | log-returns | absolute log-returns | |

|---|---|---|---|

| lag = 1 | .928 | .833 | .555 |

| lag = 5 | .113 | .078 | .975 |

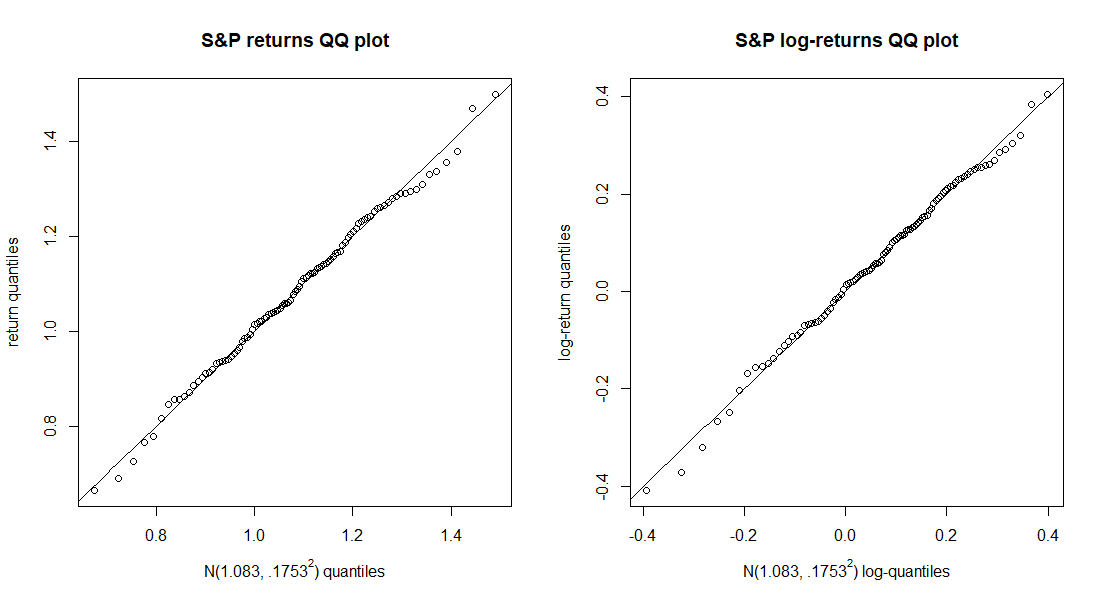

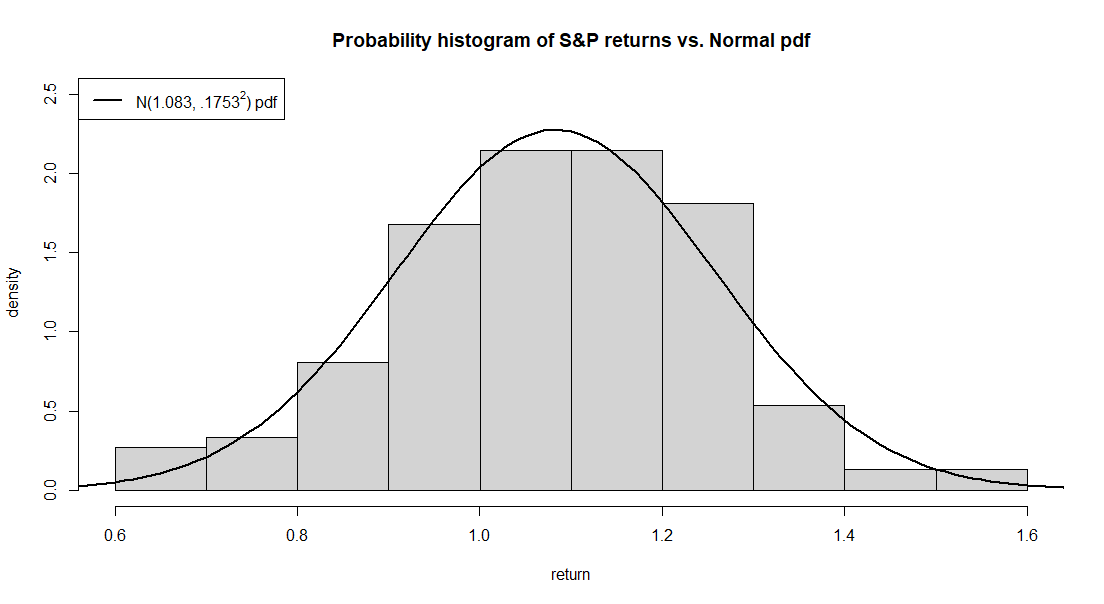

A simple and effective option is to fit returns to a Normal distribution with mean and standard deviation equal to their corresponding sample values (see figures 4 and 5). This fit works especially well because the mean and standard deviation of its logarithm are approximately equal to their corresponding sample values as well. In particular, if , then the mean and standard deviation of are approximately equal to the sample mean (.06578) and standard deviation (.1690) of annual S&P log-returns. The mean (.06534) and standard deviation (.1680) of were computed as the sample mean and standard deviation of 100,000 samples of . Note that under this fitted distribution, it is possible to realize a negative return. However, the probability of realizing a negative return is so small (on the order of ), that it is negligible here.

Now fix and require that for , where is as in section 3.3.

4.2.1 Simulating and

Algorithms 1 and 2 compute and , respectively, via simulation. Both algorithms use that are defined using Borel measurable . In particular, algorithm 1 uses

and algorithm 2 uses

In algorithm 1, realizations of are simulated, and then is computed as the number of realizations greater than or equal to , divided by . Likewise, in algorithm 2, realizations of are simulated, and then is computed as the number of realizations greater than or equal to , divided by .

4.2.2 Computing

Let be a sufficiently large postive integer. In algorithm 3, is computed recursively for , where

The following elaborates on the details behind algorithm 3.

Recall that is given by (9). Observe that the set-up detailed at the top of section 4.2 aligns with that of section 3.3. So for and . Furthermore, is given by (13) for .

Denote the pdf and cdf of the iid with and , respectively. Then (12) implies that for each , is the maximum of and

| (23) |

where indicates the proportion invested in the stock at time and

Transforming the integral in (23) with the substitution

yields

| (24) |

Summarizing,

| (25) |

Let . Algorithm 3 first computes , which is needed in (25). If , then , and it follows that . If , then a lower bound of is given by . If , then a lower bound of is given by , where is the closest lesser element in to . If , then .

| (26) |

Note that the fraction in (26) approximates the expectation of given , where has pdf

Furthermore, .

The maximum over in (25) is computed with an iterated grid search, where the grid is refined at each iteration. In particular, the first grid tests in . Let denote the in that produces the maximum of . The next grid is . Let denote the in that produces the maximum of . The last grid is . Let denote the in that produces the maximum of . From here, algorithm 3 uses the approximation

4.2.3 Computing

4.2.4 Simulating (2) and the right side of (19)

4.3 Results

First consider the case where a mortality distribution is not present, and a constant annual withdrawal of 1 unit is made for years, after an initial investment ( and for ).

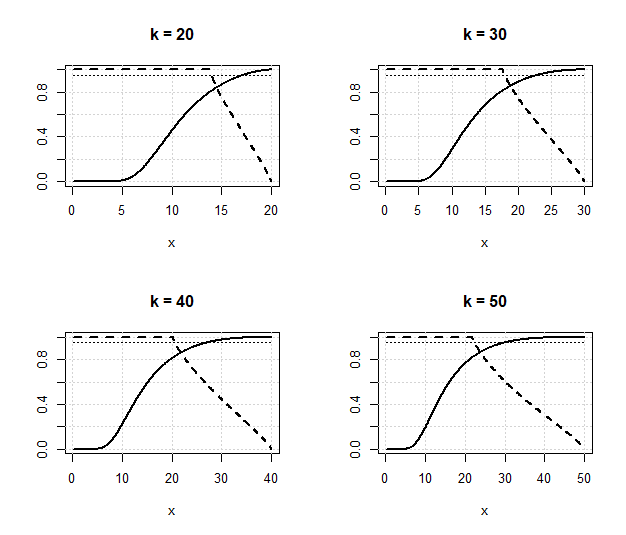

Figure 6 illustrates the and returned from algorithm 3 for various . In general, is decreasing over , indicating that the optimal proportion invested in the S&P Composite Index decreases as increases.

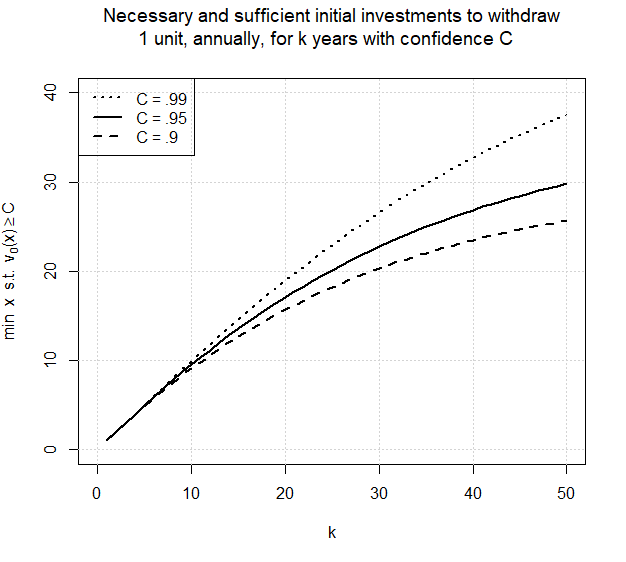

Figure 7 illustrates the minimum such that for various and . Of note, an initial investment of (or ) units allows an investor to make (or ) annual withdrawals of unit with 95% confidence.

Figure 8 shows that the returned from algorithm 3 are reproducable via the Monte Carlo simulation described in section 4.2.4. Furthermore, the optimal portfolio weights coming from algorithm 3 offer a noticeable improvement to over constant portfolio weights.

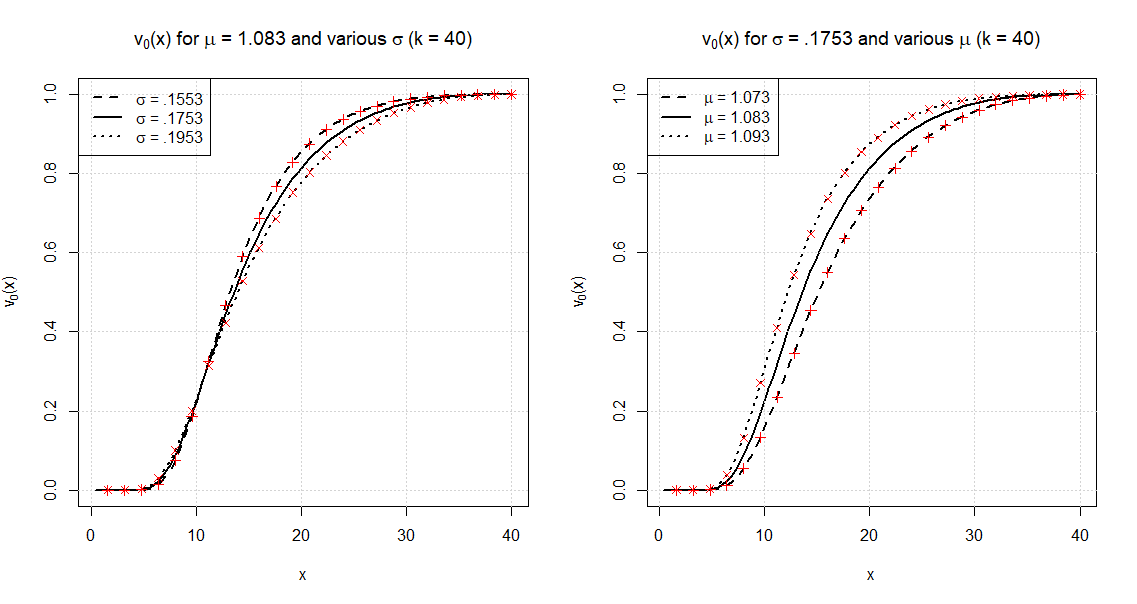

Figure 9 shows how is affected by and when . In general, small changes to and result in noticeable changes to . Let denote the returned from algorithm 3 using . Interestingly, the returned from algorithm 1 with and are very close to the that use . In other words, the optimal portfolio weights returned from algorithm 3 with can serve as the optimal portfolio weights when instead , provided and are close to and , respectively.

Next consider the case where a mortality distribution is not present, and a constant annual withdrawal of 1 unit is made for years, after executing DCA for years ( and for ). Table 3 shows the DCA investment amount () that supports execution of the years of withdrawals with 95% confidence. For comparison, the numbers in parenthesis indicate () when for , in which case the portfolio is always fully invested in the S&P Composite Index. In general, the advantage of using optimal portfolio weights instead of decreases as and increase. For the and considered in Table 3, the improvement in resulting from using optimal portfolio weights ranges from to .

| Years of Withdrawals | |||||

|---|---|---|---|---|---|

| Years of DCA | 30 | 40 | 50 | 60 | 70 |

| 10 | 1.89 (.896) | 2.21 (.906) | 2.44 (.913) | 2.60 (.919) | 2.70 (.922) |

| 20 | .76 (.906) | .89 (.916) | .97 (.921) | 1.03 (.924) | |

| 30 | .39 (.911) | .46 (.921) | .50 (.924) | ||

| 40 | .23 (.922) | .26 (.924) | |||

| 50 | .14 (.930) | ||||

Next consider the case where a mortality distribution is present, and a constant annual withdrawal of 1 unit is made until death, after executing DCA for years ( and for ). Table 4 shows the DCA investment amount () that supports execution of the withdrawals until death with 95% confidence. For comparison, the numbers in parenthesis indicate when for all , in which case the portfolio is always fully invested in the S&P Composite Index. In general, the advantage of using optimal portfolio weights instead of decreases as the starting age and increase. For the starting ages and considered in Table 4, the improvement in resulting from using optimal portfolio weights ranges from to .

| Starting age | |||||

|---|---|---|---|---|---|

| Years of DCA | 20 | 30 | 40 | 50 | 60 |

| 10 | 2.58 (.929) | 2.42 (.928) | 2.19 (.929) | 1.91 (.932) | 1.54 (.938) |

| 20 | .95 (.930) | .86 (.931) | .75 (.934) | .60 (.940) | |

| 30 | .45 (.936) | .38 (.936) | .30 (.939) | ||

| 40 | .22 (.941) | .17 (.942) | |||

| 50 | .10 (.945) | ||||

Last consider the case where a mortality distribution is present, and a constant annual withdrawal of 1 unit is made until death, after an initial investment ( and for ).

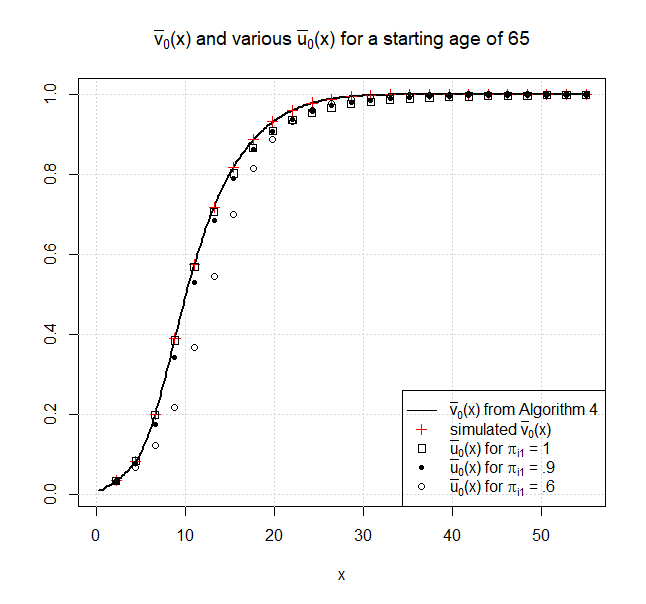

Figure 10 shows that the returned from algorithm 4 are reproducable via the Monte Carlo simulation described in section 4.2.4. For between and , the optimal portfolio weights coming from algorithm 4 offer a small, but noticeable, improvement to over constant portfolio weights. For other , the improvement is hardly distinguishable.

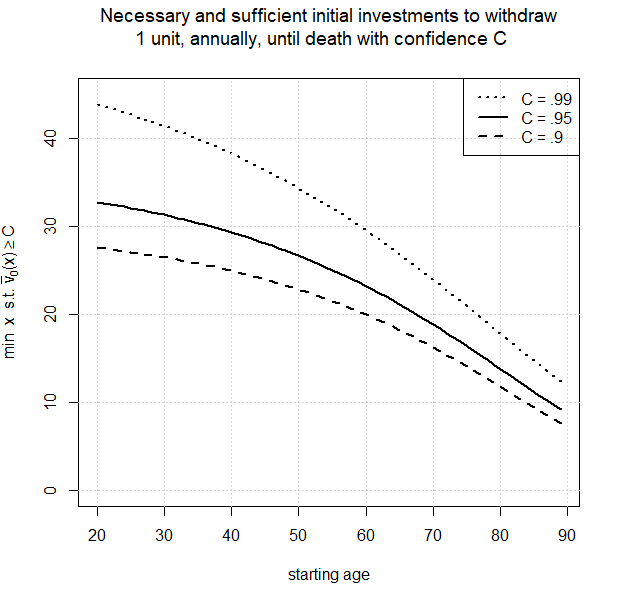

Figure 11 illustrates the minimum such that for various . Of note, an initial investment of (or ) units at age 60 allows an investor to make annual withdrawals of unit until death with 99% (or 90%) confidence.

5 Conclusion

In general, maximization of and over the offers a noticeable, but sometimes small, improvement over the and produced when the are constant over . Of the constant portfolio weights, appears to produce and that are closest to their maximum versions; however, the difference can be several tenths. So optimal portfolio weights can offer investors a worthwhile improvement in their probability to complete a given schedule of investments and withdrawals.

This kind of optimization can also be used in the context of a guaranteed lifetime withdrawal benefit (GLWB) rider on a variable annuity. In particular, the GLWB rider that precludes any withdrawals outside of the pre-determined () can be priced as follows. Consider the recursion

Compute as

Provided enough customers, a price of will let the insurance company generate a profit of approximately at time , where is the number of customers. Moreover, if indicates year for , then the annual withdrawal percentage of the GLWB is given by . Typically, variable annuities do not offer this sort of optimized investment, but it could offer customers a noticeable price reduction without changing the annual withdrawal amount. Performing this optimization in the inflation-adjusted setting is especially appealing, since then withdrawals and expected profits will be inflation adjusted. Fortunately, this scheme is easily modified to accommodate a guaranteed death benefit (GDB) rider. If the guaranteed death benefit is then the expected profit per customer (at time ) for the variable annuity with GLWB and GDB riders is . The author plans to investigate this optimization and compare the resulting prices with current variable annuity prices.

Future research could consider investment and withdrawal amounts that are not pre-determined constants at time 0. At the very least, each would need to be -measurable. On its own, this basic measurability condition leads to trivial optimization. The optimization is more interesting under the following scheme. Fix and . At each time , compute such that , where is computed using for . Set to be the least such that . If there is no such , set . In words this scheme starts with an initial investment of , and then the are non-positive for , with each being adapted in time to maximize the probability (given the information up to time ) of withdrawing at each time . It would be interesting to investigate the distribution of these adapted , meaning look at for a desirable withdrawal amount . Ideally, the should be greater than or equal to some threshold . Ultimately, the goal of this scheme would be to achieve increased at the cost of having variable withdrawal amounts.

Appendix A Proofs

A.1 Additional notation and definitions

A.2 Additional lemmas

Lemma 3 (simplified version of proposition 7.30 from Bertsekas and Shreve (1996)).

Let and be separable metrizable spaces and let be a Borel probability measure on the Borel -algebra of . If is bounded and continuous, then the function defined by

is continuous.

Lemma 4 (simplified version of proposition 7.31 from Bertsekas and Shreve (1996)).

Let and be separable metrizable spaces, let be a Borel probability measure on the Borel -algebra of , and let be Borel measurable. If is upper semicontinuous and bounded above, the so is the function defined by

Lemma 5 (proposition 7.33 of Bertsekas and Shreve (1996)).

Let be a metrizable space, a compact metrizable space, a closed subset of , and let be upper semicontinuous. Let be given by

Then is closed in , is upper semicontinuous, and there exists a Borel measurable function such that and

A.3 Proof that are well-defined

Obviously, is well-defined. It remains to be seen whether the are well-defined for . To begin, is given in another representation that (10) will be shown to satisfy. Let , , denote the non-decreasing upper semicontinuous functions satisfying

| (27) |

Note that the supremum in (27) indicates the supremum over all -measurable portfolio weight functions .

In order for the recursion given by (27) to make sense, the need to be well-defined. This is shown via induction. Suppose that is well-defined. The goal from here is to show that is well-defined.

Observe that is -measurable and integrable because is bounded and Borel measurable, and is -measurable. So is well-defined.

Since , a property of conditional expectation gives

| (28) |

Recall from Section 2 and (1) that . Observe that and are both -measurable, and is independent of . By lemma 1,

| (29) |

where

| (30) |

for each and . It follows from (28) and (29) that

| (31) |

The next goal is to show that

| (32) |

Observe that

for each -measurable portfolio weight function . It follows that

So (32) holds when is replaced with . To show that (32) holds when is replaced with , first observe that

| (33) |

where the supremum is taken over the Borel measurable functions . Because of (33), it suffices to show

| (34) |

This is done by showing

| (35) |

and

| (36) |

The in (35) are -measurable. Since , it follows that (35) holds when is replaced with . To show that (35) holds when is replaced with , observe that for almost every ,

| (37) |

Moreover, it is now clear from (37) that

| (38) |

To show (36), it suffices to show that the right side of (36) is -measurable. Let be such that

Observe that is continuous. Since is upper semicontinuous, it follows that is upper semicontinuous. Applying lemma 4 reveals that is upper semicontinuous. To see this, let , and in lemma 4 be , and , respectively. Next, applying lemma 5 reveals that is upper semicontinuous over , and there is a Borel measurable function such that

| (39) |

Therefore is Borel measurable over , which implies is -measurable. Applying (38), the right side of (36) is -measurable. Now it follows from (27), (31), (32), (34), (38) and (39) that

| (40) |

Looking at (30), it is not hard to see that is non-decreasing over . Furthermore, the fact that maps to implies also maps to . It is now clear that the as given in (10) are well-defined and satisfy (27).

A.4 Proof that (2) is given by

Observe that

| (41) |

By the law of total expectation, for each ,

| (42) |

A.5 Proofs for stock-bond portfolios

Observe that is the indicator function of , so is continuous over and right continuous at . Now proceed by induction. Suppose is continuous over and right continuous at . Further suppose that for , and if , suppose that for .

For and , let . Using the notation of section A.3, observe that

Under the setting outlined at the beginning of section 3.3, for . Therefore

when . By assumption, is continuous over . Also recall from section A.3 that is continuous. Therefore is continuous over

It follows from lemma 3 that is continuous over . To see that is continuous at any point , simply take advantage of the uniform continuity of over .

Observe that

Since for , it follows that for . Recall that maps to and for each . Therefore for .

The next goal is to show for , provided . Since , it follows from the assumption in the first paragraph of this section that for . Additionally having implies that for each and , . Thus, for .

A.6 Proof that the right side of (19) is given by

This proof is very similar to that of sections A.3 and A.4, so only an outline with the key differences is presented. First introduce the additional recursion

| (50) |

Next observe that for ,

Therefore

| (51) |

Like in section A.3, is given first in another representation that (21) will be shown to satisfy. Let be such that , where . For , let denote the functions satisfying

| (52) |

with

-

•

upper semicontinuous w.r.t. for each ,

-

•

for and ,

-

•

non-decreasing and for .

Suppose that is well-defined. The goal from here is to show that is well-defined. Observe that

| (53) |

Since , a property of conditional expectation gives

| (54) |

It follows from (53) and lemma 1 that

| (55) |

where

for each , and . By the independence of to each , it follows that

By the induction assumption, and for and . Therefore

It follows from (54) and (55) that

| (56) |

Paralleling the logic of section A.3, the following result is eventually achieved. is upper semicontinuous over for each , and there is a Borel measurable function such that

Moreover, a satisfactory is given by

is well-defined because is a well-defined mapping to and

-

•

is upper semicontinuous w.r.t. for each ,

-

•

for and ,

-

•

is non-decreasing and for .

Likewise, is well-defined because is a well-defined mapping to and

-

•

is upper semicontinuous w.r.t. ,

-

•

is non-decreasing w.r.t. .

From here, this proof mimics that of section A.4 after making the following changes. Except for , replace each instance of , , , and with , , , and , respectively, for . Replace each instance of with . The final result is

References

- \bibcommenthead

- Antolín et al (2010) Antolín P, Payet S, Yermo J (2010) Assessing default investment strategies in defined contribution pension plans. OECD Journal: Financial Market Trends 2010(1):87–115

- Basak and Shapiro (2001) Basak S, Shapiro A (2001) Value-at-risk-based risk management: optimal policies and asset prices. The review of financial studies 14(2):371–405

- Bertsekas and Shreve (1996) Bertsekas D, Shreve SE (1996) Stochastic optimal control: the discrete-time case, vol 5. Athena Scientific

- Butt and Khemka (2015) Butt A, Khemka G (2015) The effect of objective formulation on retirement decision making. Insurance: Mathematics and Economics 64:385–395

- De Saporta and Zili (2021) De Saporta B, Zili M (2021) Martingales and Financial Mathematics in Discrete Time. John Wiley & Sons

- Hakansson (1975) Hakansson NH (1975) Optimal investment and consumption strategies under risk for a class of utility functions. In: Stochastic Optimization Models in Finance. Elsevier, p 525–545

- Kallenberg (2019) Kallenberg O (2019) Foundations of Modern Probability. Probability and its applications, Springer

- Karatzas et al (1987) Karatzas I, Lehoczky JP, Shreve SE (1987) Optimal portfolio and consumption decisions for a “small investor” on a finite horizon. SIAM journal on control and optimization 25(6):1557–1586

- Kraft and Steffensen (2013) Kraft H, Steffensen M (2013) A dynamic programming approach to constrained portfolios. European Journal of Operational Research 229(2):453–461

- Levy and Levy (2009) Levy H, Levy M (2009) The safety first expected utility model: Experimental evidence and economic implications. Journal of Banking & Finance 33(8):1494–1506

- Li and Mi (2021) Li Y, Mi H (2021) Portfolio optimization under safety first expected utility with nonlinear probability distortion. Chaos, Solitons & Fractals 147:110,917

- Musumeci and Musumeci (1999) Musumeci J, Musumeci J (1999) A dynamic-programming approach to multiperiod asset allocation. Journal of Financial Services Research 15(1):5–21

- Phelps (1962) Phelps ES (1962) The accumulation of risky capital: A sequential utility analysis. Econometrica: Journal of the Econometric Society pp 729–743

- Roy (1952) Roy AD (1952) Safety first and the holding of assets. Econometrica: Journal of the econometric society pp 431–449