Nonequilibrium statistical mechanics of money/energy exchange models

Abstract

Many-body dynamical models in which Boltzmann statistics can be derived directly from the underlying dynamical laws without invoking the fundamental postulates of statistical mechanics are scarce. Interestingly, one such model is found in econophysics and in chemistry classrooms: the money game, in which players exchange money randomly in a process that resembles elastic intermolecular collisions in a gas, giving rise to the Boltzmann distribution of money owned by each player. Although this model offers a pedagogical example that demonstrates the origins of Boltzmann statistics, such demonstrations usually rely on computer simulations – a proof of the exponential steady-state distribution in this model has only become available in recent years. Here, we study this random money/energy exchange model, and its extensions, using a simple mean-field-type approach that examines the properties of the one-dimensional random walk performed by one of its participants. We give a simple derivation of the Boltzmann steady-state distribution in this model. Breaking the time-reversal symmetry of the game by modifying its rules results in non-Boltzmann steady-state statistics. In particular, introducing “unfair” exchange rules in which a poorer player is more likely to give money to a richer player than to receive money from that richer player, results in an analytically provable Pareto-type power-law distribution of the money in the limit where the number of players is infinite, with a finite fraction of players in the “ground state” (i.e., with zero money). For a finite number of players, however, the game may give rise to a bimodal distribution of money and to bistable dynamics, in which a participant’s wealth jumps between poor and rich states. The latter corresponds to a scenario where the player accumulates nearly all the available money in the game. The time evolution of a player’s wealth in this case can be thought of as a “chemical reaction”, where a transition between “reactants” (rich state) and “products” (poor state) involves crossing a large free energy barrier. We thus analyze the trajectories generated from the game using ideas from the theory of transition paths, and highlight non-Markovian effects in the barrier crossing dynamics.

I Introduction

Simple asset exchange games have been used as models of wealth distribution in econophysics Angle (1986); Greenberg and Gao (2023); Yakovenko and Rosser (2009); Dragulescu and Yakovenko (2000); Patriarca and Chakraborti (2013); Banerjee and Yakovenko (2010); Bennati (1988, 1993); Ispolatov et al. (1998); Klein et al. (2021); Liu et al. (2021); Drăgulescu and Yakovenko (2001); Silva and Yakovenko (2004); Banerjee et al. (2006). Such models are also of interest as relatively simple many-body systems whose time evolution can be shown, explicitly and without resorting to the fundamental postulates of statistical mechanics, to give rise to the Boltzmann distribution Scalas et al. (2006); Lanchier (2017); Lanchier and Reed (2018, 2019, 2022). Indeed, microscopic models where fundamental laws of statistical mechanics can be proven without invoking statistical assumptions are scarce, and such proofs are often complex – see, e.g., Balint et al. (2021); Simányi (2003, 2009).

In contrast, the onset of the Boltzmann distribution in the simple game where players exchange a fixed amount of money in a random direction can be understood using simple arguments. In this game, which is known in econophysics as the Bennati-Dregulescu-Yakovenko game Dragulescu and Yakovenko (2000); Yakovenko and Rosser (2009), and which is also used by physical chemistry teachers to illustrate various concepts of statistical mechanics Michalek and Hanson (2006), a randomly selected pair of players exchange a single money unit in a random direction. A physical counterpart of this game corresponds to “molecules” with (quantum) harmonic oscillator energy spectra, and with pairs of oscillators exchanging one quantum of energy at random such that the total energy is conserved. The “fair” version of this game corresponds to time-reversible exchange dynamics where the random exchange direction is unbiased, leading to a Boltzmann distribution of money/energy Dragulescu and Yakovenko (2000); Scalas et al. (2006). In contrast, “unfair” versions of the game with a bias in the exchange direction give rise to interesting scenarios with non-Boltzmann money statistics Cao and Motsch (2023); Scafetta et al. (2002, 2004).

Here, we present analytical results for a class of exchange games, where “unfair” exchange rules correspond to broken time-reversal symmetry. We start with an elementary derivation of the Boltzmann distribution as the steady-state result of the fair exchange game with players. We note that another derivation of this distribution was recently provided in Lanchier (2017); Lanchier and Reed (2018, 2019). We then introduce “unfair” versions of the game, where money exchange, while still probabilistic, is biased to increase or decrease the wealth of the richer or poorer players (we call them rich-biased and poor-biased games, as in Cao and Motsch (2023)). A key feature of these games is that they violate time-reversal symmetry, leading to nonequilibrium dynamics with dissipative cycles. As a result, the steady-state probability of the money belonging to a player no longer has an exponential dependence on predicted by the Boltzmann law.

The -dependence of is qualitatively different depending on whether the game is poor-biased or rich-biased. In the former case, we find a bell-shaped distribution centered around the mean. The latter case is more interesting. In the limit where both the number of players and the average amount of money per player approach infinity, the function is a power law, while in the limit with fixed, the distribution follows a power law at intermediate values of (where this distribution turns out to be independent of the value of ) and becomes exponential in the limit . Another interesting feature of this regime is that the fraction of players with zero money (or, equivalently, the fraction of particles in the ground state) always remains finite. For finite (in the rich-biased case) we find that finite-size effects dominate the dynamics, resulting in a bimodal wealth distribution, with the money belonging to each player undergoing non-Markovian bistable dynamics switching between poor and rich states, and with the rich state occurring when the player accumulates nearly the entire money in the system.

This paper is organized as follows: In Section II we describe details of the model. Section III discusses the “fair game” case and gives simple arguments explaining the Boltzmann distribution of money in this case. Unfair exchange games are introduced in Section IV, where the connection between unfairness and time-reversal symmetry breaking is shown. The general mean-field solution to such games is introduced in Section V. Section VI reports on analytical results for the case of a rich-biased game in the limit of infinite number of players, while Sections VII - IX discuss finite-size effects in this game using both simulations and analytic theory. Section X discusses the timescales to reach the steady state, and Section XI concludes by highlighting the most important findings of this work. Supplementary Material provides further details of the analytical theory used to predict the wealth distribution in the case of a finite number of players.

II Model

The model studied here is described, more precisely, as follows: Each of the players (molecules) has money (or energy) units, where the index enumerates the players. The total amount of money,

| (1) |

is conserved and fixed by the initial conditions. At every step, a pair, say and , is selected at random; If and , then these players/molecules exchange money/energy,

| (2) |

with the signs “+” and “-” determining which player receives the money selected according to certain probabilistic rules to be specified below. When only one direction of exchange is possible, the exchange becomes deterministic. For example, if and , the result of the exchange is , . If and , then no exchange takes place, , . We note that these rules may be viewed as unrealistic from an economics perspective: for example, it could be more realistic to assume that a player reaching the zero-money state leaves the game Ispolatov et al. (1998). But since we are more interested in molecular consequences than economic implications of the model here, the assumption of conservation of the number of particles/players is more natural.

We are interested in the steady-state probability that a player has money units, particularly in the limit,

| (3) |

with the average amount of money per player being a given parameter specified by the initial conditions.

III Fair exchange leads to Boltzmann distribution

In the fair game, when both directions of exchange (i.e. both signs in Eq. (2)) are possible, they are chosen with equal probabilities. Note that the dynamics under the fair game rules is time-reversible - see Section IV.

We now give a simple physical explanation why fair exchange rules lead to the Boltzmann distribution in the steady-state. Focus on a single participant of the game, and consider the evolution of the amount of money owned by this player. This quantity undergoes a one-dimensional random walk, as shown in Fig. 1. Let and be the conditional probability that a player with amount will increase/decrease its amount by (see Fig. 1) such that the walker steps right/left. Given the fairness of the game, is equally likely to increase/decrease upon encountering another player with a nonzero amount of money. When encountering a player with zero amount of money, however, our participant cannot receive money and must lose money instead (assuming ). The probability that the player encountered is broke is , and the probability that this player is not ; therefore we have

| (4) |

Similarly, we find

| (5) |

For we obviously have , as cannot become negative. To find we note that the walker takes a step to the right ( increases) provided that the player encountered is not broke (with probability ) or remains unchanged otherwise (with probability ). Thus, . Finally, if a player with no money encounters another player that is broke, the probability of such an encounter is (Fig. 1).

The steady-state probabilities must satisfy the detailed balance condition, i.e.,

| (6) |

from which we find:

| (7) |

This is the Boltzmann distribution, with exponentially decaying with increasing . Importantly, the probabilities satisfying Eq. (7) automatically satisfy the normalization condition

| (8) |

The value of , then, must be determined by the initial amount of money in the system

| (9) |

In combination with Eq. (7), this gives

| (10) |

or

| (11) |

The occupancy of the zero-money state (i.e. of the single-molecule “ground state”) is thus a monotonically decreasing function of the average money per player. In the limit , Eq. (11) gives , and Eq. (7) can be written, approximately, as

| (12) |

with

| (13) |

As expected, the “temperature” of the Boltzmann distribution is, in this limit, equal to the average money/energy per player/molecule.

In the opposite limit of ”scarce resources”, , we find from Eq. (11),

We note that, for a finite number of players , Eq. (7) is not exact: Indeed, in contradiction to this equation, the probability must be equal to zero for . This case can be analyzed, systematically, using a local equilibrium approximation described in Section VIII and in the Supplementary Material. In practice, however, assuming , the probability predicted by Eq. (7) is vanishingly small for any such that . In other words, our theory works under the assumption that each player can only amass a vanishingly small (comparable to ) fraction of the total money pool , which is true for . As will be seen below, however, this assumption is not necessarily satisfied when the rules of the game are changed to be unfair and when is finite.

Finally, let us point out another important feature of Eqs. (12)-(13) (but not of Eq. (7)): The distribution of money is independent of certain details of the game. More precisely, recall that, the “unit” of money in our game is the same as the amount of money exchanged in each encounter between players. Let be the actual exchanged money, say, in dollars or cents, and let be the money owned by a player. Then it follows from Eqs. (12)-(13) that the probability density of the wealth , measured at a sufficiently low resolution such that the discreteness of is irrelevant, is given by the exponential law:

| (16) |

which is independent of the money exchanged (). In other words, regardless of whether players exchange dollars or cents, their wealth distribution will be the same as long as the average wealth per player is the same. In general, this is not the case (e.g. for the more general result of Eq. (7)).

IV Unfair exchange implies broken time reversal symmetry

We now introduce a class of “unfair” exchange models, in which the direction of exchange between two players with amounts of money and depends on and . Specifically, let be the (conditional) probability that a player with money units will accept money upon encountering a player with money units. Assuming , the probability that this player will give money to the other player is, then, , and, by symmetry, we also have . In what follows, we will focus on a particular example of such a model, where the exchange probabilities are determined by the sign of the difference . Specifically:

| (17) |

The quantity is the probability that a wealthier player encountering a poorer one (but still with nonzero money) will receive money from the latter. Thus, it is a measure of unfairness of the game, with corresponding to the fair game discussed in the preceding Section. When , the game will tend to equalize the wealth of the players. When , it will increase inequality. Intuitively, time reversible exchange dynamics should correspond to the fair game case: for example, if we replace players with colliding molecules and money with their energies, then a trajectory of two colliding trajectories and its time-reverse result in the same amount of energy being exchanged in the opposite directions.

To quantify the above statement more precisely, note that the time evolution of the state vector of the system is described by a discrete-time master equation, with transition probabilities specified by Eq. (17) multiplied by the probability that two specific players meet. As an example, a kinetic scheme describing this system is shown in Fig. 2 for the case . Importantly, the dynamics satisfies detailed balance and is time-reversible only for the fair game with . Indeed, according to Kolmogorov’s cycle criterion Kelly (2011); Kolmogoroff (1936), detailed balance is violated if there is a cyclic sequence of microscopic states such that the product of the transition probabilities in the clockwise direction is different from that taken in the counterclockwise direction. Examples of such cycles, for , are highlighted in Fig. 2. And since any -player game can be embedded in a game with players, the example in Fig. 2 suffices to prove that detailed-balance is broken when .

Various other ”unfair” exchange models have been studied in the literature Cao and Motsch (2023); Scafetta et al. (2002, 2004). In Cao and Motsch (2023), the exchange direction is always set from a “giver” to a “receiver”, and the bias is introduced in the probability of selecting a “giver” and a “receiver”, which depends on the amount of money each person has (see Fig. 1 in Cao and Motsch (2023)). In Scafetta et al. (2002, 2004) the bias in the exchange direction does not only depend on the sign difference of (as we have here), but also on the magnitude of the difference (see i.e., Eq. (16) in Scafetta et al. (2004)). The latter, however, reduces the analytical tractably of the model.

V Mean-field theory: evolution of wealth as a Markovian random walk

Consider the one-dimensional random walk shown in Fig. 1. Within mean-field theory, the transition probabilities of stepping right and left are computed as weighted averages of the microscopic transition probabilities,

| (18) |

For the model specified by Eq. (17), then, we can write

| (19) |

In writing Eq. (19) it was assumed that the probabilities decay to zero, as , fast enough that the upper summation limit can be extended to infinity; this assumption allows us to disregard large values of where, for example, the money owned by another player cannot be greater than if .

Introducing now

| (20) |

we can rewrite Eq. (19) as:

| (21) |

Similarly, we have

| (22) |

Using detailed balance, given by Eq. (6), the steady-state probabilities can now be determined, starting from , by iterating the following map:

| (23) | ||||

| (24) |

which holds for . Note that Eq. (23) contains both on the RHS and LHS - each iteration, then, involves solving a quadratic equation for .

Eqs. (23) and (24) are not valid for ; writing the detailed balance condition between states with and , we obtain the first step of the map (cf. Fig. 1):

| (25) |

or, using ,

| (26) |

Again, Eq. (26) results in a quadratic equation that allows one to determine starting from .

It is worth noting that the use of the detailed balance condition, given by Eq. (6), is justified even when the system, viewed microscopically, is in a nonequilibrium steady state rather than in equilibrium, as is the case for (see the previous Section). Indeed, the linear kinetic scheme of Fig. 1 always obeys detailed balance. This scheme describes a projection of nonequilibrium dynamics in a -dimensional space onto a single degree of freedom , where - as is often the case for projected dynamics (see, e.g., Godec and Makarov (2023); Blom et al. (2023); Hartich and Godec (2021); Harunari et al. (2022); Meer et al. (2022)) - the nonequilibrium character of the underlying process is hidden, although it affects the distribution .

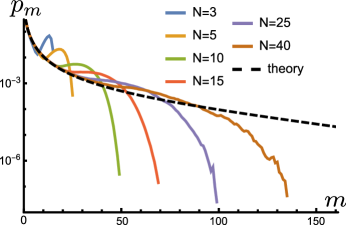

Figure 3 illustrates the performance of our theory in comparison with Monte Carlo simulations of money exchange. For , the theory is identical to that of Section III leading to a probability distribution described by Eq. (7). For , the money exchange is more likely to proceed in the direction from a wealthier player to the poorer one; as a result, the distribution has a peak centered around the average amount , which was also observed in Scafetta et al. (2002, 2004). This qualitative property of the distribution is captured by the theory, which becomes increasingly more accurate as increases. For , the situation is more complicated. As will be seen in Section VII, if is large enough, then the distribution becomes bimodal, a qualitative feature not captured by our theory. The parameters in Fig. 3 are chosen such that this is not the case. See Section VII for a further discussion.

VI The , case

The most interesting regime is , where money transfer from poorer players to wealthier ones is favored. We start with considering the behavior of satisfying Eq. (23) in the limit . Since the distribution is normalized, we must have

Moreover, we have

Inserting the above two relations into Eq. (23), we see that the ratio approaches a constant for ,

| (27) |

On the other hand, can only vanish in the limit if . It then follows from Eq. (27) that a normalized steady-state solution exists only if

| (28) |

Hence, for we find . In other words, in the rich-biased game, the fraction of players with zero money remains finite regardless of the total pool of money in the game.

What happens when approaches the minimum possible value from above? To answer this question, let us write the map of Eq. (23) in the following form,

| (29) |

where

and

For , we have , and thus in order to study the tails of the distribution we have to consider two small parameters, , and . Depending on the relationship between the two, there are two cases:

Case A: . Eq. (29) can then be approximated by

| (30) |

leading to an exponential tail for the distribution ,

| (31) |

Case B: . Eq. (29) can now be rewritten as

| (32) |

Treating as a continuous variable, we can further approximate the above equation by

or

| (33) |

Guessing the solution of this integro-differential in the form of a power law, we find:

| (34) |

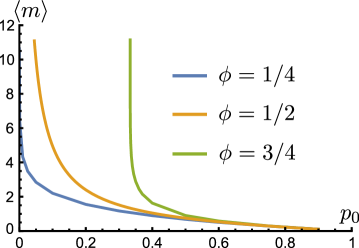

For a nonzero (but sufficiently small) , therefore, the shape of the curve vs. includes an exponential tail at and an intermediate power-law regime (Fig. 4). When () the exponential tail disappears, and the power law of Eq. (34) holds even in the limit . Such a power law for the tail of the wealth distribution is an example of Pareto’s law Pareto et al. (1964); Montroll and Shlesinger (1982), which has been confirmed empirically in various settings Drăgulescu and Yakovenko (2001); Chakrabarti et al. (2013). In this case, the first moment of the distribution (as well as its higher moments) diverges, since . More generally, as shown in Fig. 5, increases and diverges as approaches the critical value from Eq. (28). In contrast, for , diverges as approaches zero (Fig. 5).

Remarkably, the intermediate power law predicted by Eq. (34) is independent of the value of , or, equivalently, of the average amount of money per player, and is only a function of the ”inequality” parameter . This prediction is confirmed by the numerical results for shown in Fig. 4.

Recall that our unit of money here is the amount of money exchanged in each transaction. It is instructive to rewrite our result using more natural units, where the amount exchanged is and a player’s wealth is (see Section III). In this case we find, for the probability density of (treating, again, as continuous),

| (35) |

Unlike Eq. (16), this result depends, explicitly, on the amount of money exchanged in each transaction, and the average properties, such as the average wealth , are insufficient for determining the wealth distribution in this case. For example, if we ask how many individuals have wealth below some predefined value , the answer will depend, explicitly, on , not just on . The proportionality of the power-law probability distribution of Eq. (35) to also follows from dimensional arguments: Since is the only characteristic money scale of the power-law distribution (for which ), the only way the power-law dependence of the probability density on , , can be reconciled with its units of inverse money is that it is also proportional to .

VII The , finite case: breakdown of mean-field theory, bimodality of the wealth distribution and the winner-takes-all scenario

For , the difference between the case of a finite number of players and the limit is not merely quantitative: unlike the case, where the shape of the dependence of on remains the same regardless of (cf. Fig. 3), the distribution may become bimodal (see Fig. 6). Importantly, the location of the rightmost peak of the distribution is comparable to , the total amount of money in the system. Thus, the assumption that is vanishingly small for is violated. As increases, the right distribution peak is shifted to the right, and the probability distribution converges towards the result predicted by mean-field theory (Fig. 6).

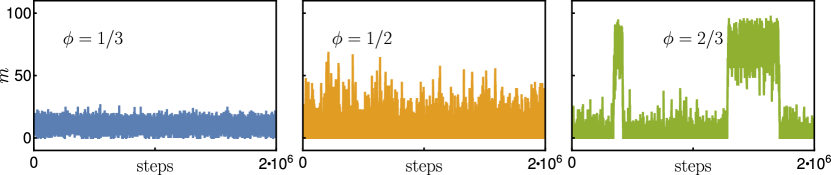

In what follows, it will be shown that this second peak accounts for the possibility that a single player accumulates nearly all the money in the game, thus necessarily forcing the rest of the players into a “poor” state. Indeed, once a player happens to accumulate more than half of the total money, , the rest of the players have less than . Under the rules of the game with , the “rich” player will be more likely to gain rather than lose money in subsequent exchanges. This leads to a “winner-takes-all” scenario until an improbable sequence of money exchanges causes the lucky winner to lose enough money that reverts this player to poverty. For a sufficiently long game, this will happen, occasionally, to every player. This is illustrated in Fig. 7, where the amount of money belonging to a selected player exhibits bistable behavior for (right panel in Fig. 7). In contrast, for , no extreme values of close to occur with significant probability (left and middle panels in Fig. 7).

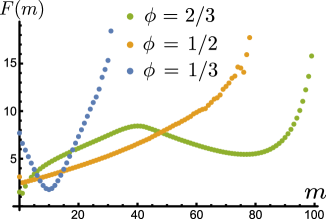

The above points become even more clear when the probability distribution is considered. Equivalently, Fig. 8 shows the “free energy”, defined as

| (36) |

as a function . Introduction of the free energy offers a convenient physical picture of the evolution of money as motion on a free energy surface , which will be explored further below.

For , the free energy has a single minimum. For (the Boltzmann case) this minimum is located at , with the probability decaying exponentially (and thus increasing linearly) as increases. Thus, the probability of large values of is exponentially small. For the single minimum is, roughly, comparable with . Again, the probability decays quickly to the right of this maximum, making states with improbable. But the case is qualitatively different, with a second free energy minimum (i.e., probability maximum) corresponding to the player being in a “rich” state.

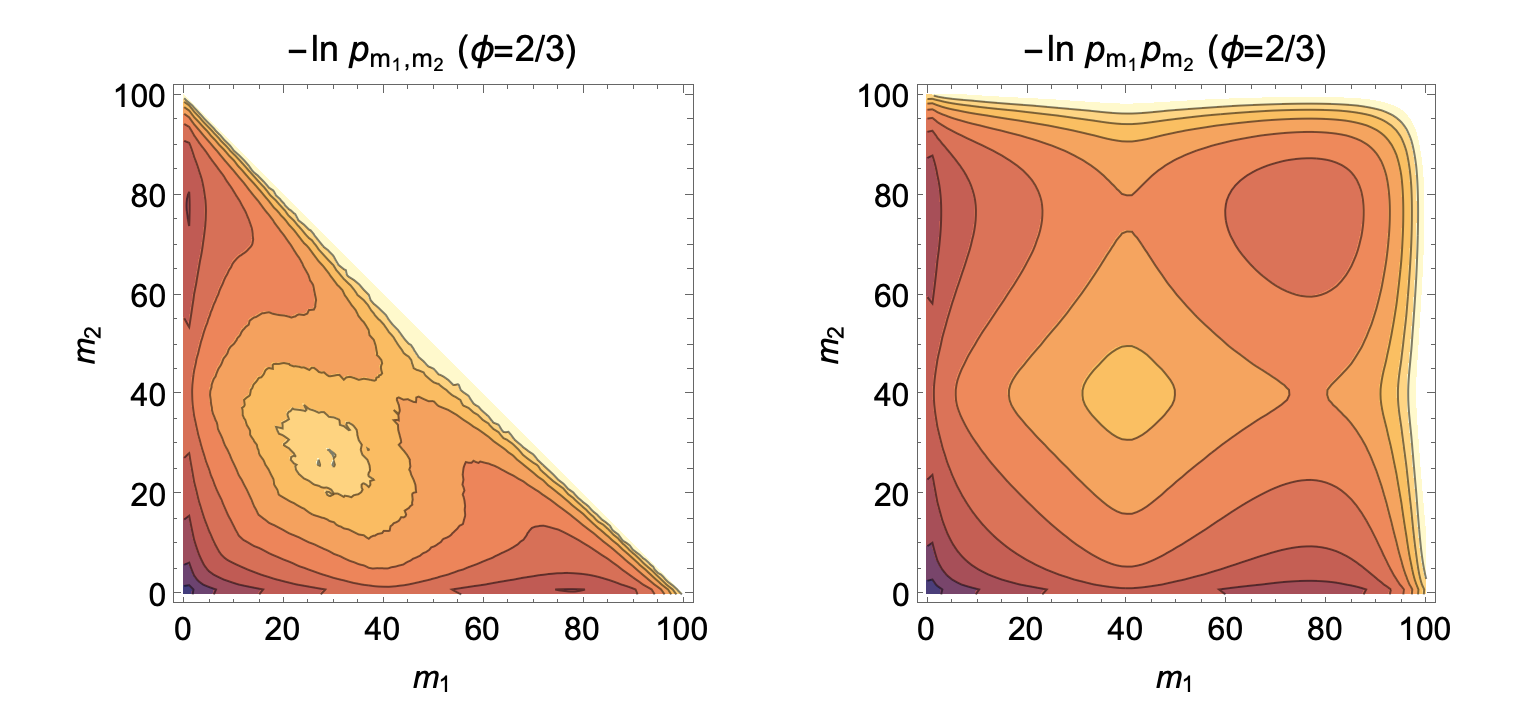

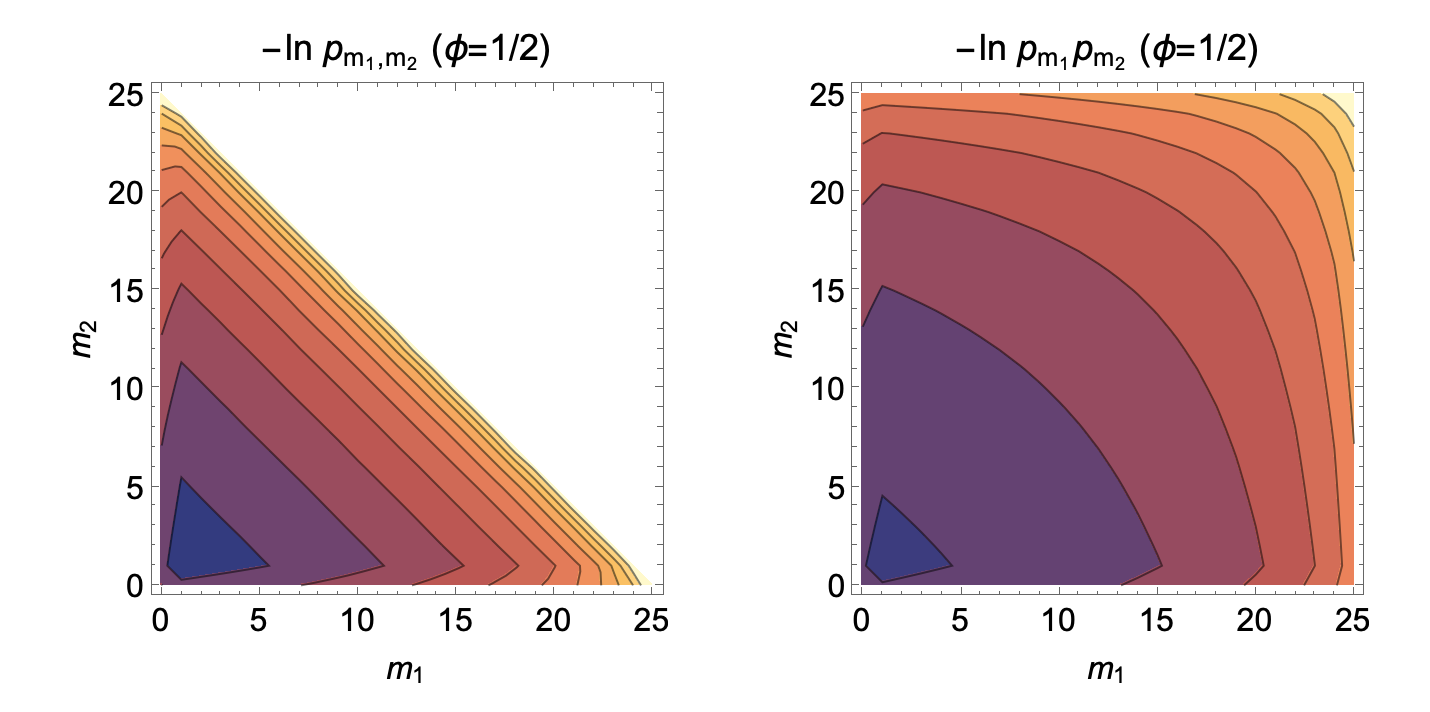

Since the total amount of the game’s money, , is conserved, the existence of a super-rich player (say ) that accumulates more than half of the total money () will subjugate the rest of the players to the poor state with . This means that the trajectories of two different players, and , must be coupled. The lack of statistical independence of and implies violation of the assumptions of the mean-field theory – and, indeed, mean-field theory predicts a monotonic rather than bimodal distribution .

The coupling between and can be further examined by comparing their joint distribution with the product of single-player distributions . Such a comparison is given in Fig. 9.

If the moneys belonging to players 1 and 2 are statistically uncoupled, then their joint distribution is the product of the single-player distributions. The simulation results, however, show this is not the case, with qualitatively different from for (Fig. 9). In particular, the product has an impossible local minimum at , where the money belonging to the two players exceeds the total amount of money in the game.

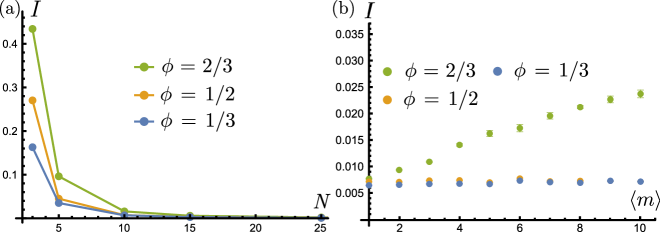

To examine, more systematically, how the coupling among players depends on the total number of players, the value of , and on the amount of money in the game, we quantify the coupling between players and () using the mutual information defined as Stone (2015):

| (37) |

If and are statistically independent then , and so =0; non-zero values of mutual information indicate coupling between and . Of course, since all players are equivalent, is independent of and .

As seen from Fig. 10a and, especially, Fig. 10b, the mutual information between pairs of players is significantly greater in the rich-biased games (), as compared to the fair and poor-biased game, given the same number of players. This mutual information further shows significant dependence on the average amount of money accumulated by a player for , but not for (Fig. 10b), in accord with the above qualitative argument suggesting strong coupling in this case. In all cases, the mutual information decreases with the number of players (given a fixed average amount of money per player). This, again, is consistent with the expectation that the mean-field theory prediction should be recovered for .

VIII The finite case: local equilibrium approximation

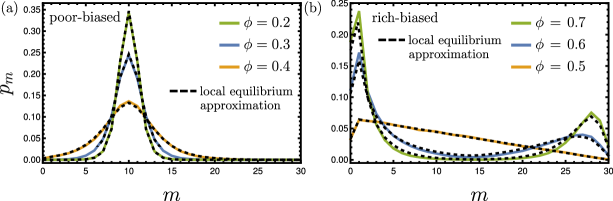

The mean field theory-type approximation described above works in the limit and cannot explain, even qualitatively, the bistable dynamics and the winner-takes-all scenario occurring in the rich-biased game when the number of players is finite. To account for such finite-size effects, we developed a local equilibrium approximation, which assumes that the dynamics of, for example, player (with money ) takes place in an equilibrated pool of players with total amount of money . In contrast to the mean field approximation, the local equilibrium approximation explicitly accounts for a finite , and therefore the pool of players does not effectively have infinite money. Similarly to the mean field approximation, the local equilibrium approximation describes the time evolution of the money owned by any given player as a one-dimensional random walk (Fig. 1), where the effective transition rates are determined by the steady-state probabilities of the -player game. An explicit expression for the transition rates and steady-state probabilities in the local equilibrium approximation are given in the Supplementary Material. Comparison of the local equilibrium approximation with simulations shows nearly perfect agreement (Fig. 11). In particular, the local equilibrium approximation captures the bimodal distribution of money for (Fig. 11b).

IX The , finite case: non-Markov effects in barrier crossing dynamics

The theory described in Section V projects -dimensional dynamics onto a single degree of freedom and considers a one-dimensional random walk performed by the money owned by a single player. Importantly, despite the nonequilibrium character of the -dimensional dynamics (when ), the corresponding one-dimensional random walk always obeys detailed balance. The nonequilibrium character of the underlying dynamics is therefore not directly observable in the trajectories , even though it is indirectly reflected in the probability distributions or, equivalently, in the effective free energies, Fig. 8. The one-dimensional dynamics can, in this case, be viewed as one-dimensional random walk/diffusion in the presence of the effective potential .

The situation is different at finite values of , particularly in the case (considered in Section VII) where the potential is bistable. Qualitatively, we can still think of the dynamics along as a one-dimensional random walk governed by the bistable potential . But because of the coupling between different random walkers, as discussed in Section VII, each individual random walk no longer has the Markov property.

To illustrate this non-Markov behavior, here we analyze the transition paths between the poor and rich states. A transition path Makarov (2015); Elber et al. (2020) is defined as a segment of a single-player trajectory that enters a “transition region” between the poor and rich states, i.e. a segment , through its “poor” boundary and stays continuously inside this region until exiting through the “rich” boundary . Analyzing transition paths informs one, for example, whether the ”mechanism” of getting rich is the same as that of getting poor: if this is the case, then the ensemble of rich-to-poor transition paths is statistically the same as the ensemble of time-reversed poor to rich transition paths. As a result, then, the mean transition path time (i.e. the mean temporal duration of the transition path) would be the same for the forward and backward transition path, which is often taken as one of the fingerprints of time reversal symmetry.

For a Markovian one-dimensional random walk this forward-backward symmetry always holds because, as noted above, such a random walk always satisfies detailed balance and thus has time-reversal symmetry Kolmogoroff (1936). But for a non-Markovian random walk, such symmetry may be violated Berezhkovskii and Makarov (2019). In all the simulations reported here, we have not be able to find any difference between the mean forward and backward transition path times, to within simulation errors. This, of course, should not be taken as a proof of the time reversal symmetry of the random walk.

Another property of the transition path ensemble can be used as a test of Markovianity of the process : consider the probability that a point , , belongs to a transition path from the rich to the poor state (as opposed to a trajectory that enters and exits the transition region through the same boundary): for Markovian dynamics this probability attains a maximum value of corresponding to a committor-one-half point where the trajectory starting from is equally likely to reach either transition-region boundary 111Strictly speaking, this is exactly true only when is a continuous variable. For non-Markov dynamics we expect Berezhkovskii and Makarov (2018) , and, indeed, this is what we observe in Fig. 12 which shows the non-Markov character of the bistable dynamics observed for .

X Equilibration times

Finally, another interesting dynamical property of our model is the time it takes for the steady-state distribution to set in, particularly in the limit. We set the time between the money exchanges carried out by a single player as the unit of time; this choice is physically sensible, as a ”microscopic” time unit is independent of the ensemble size. With this choice, time effectively corresponds to the number of steps performed by the random walker shown in Fig. 1.

Consider first the specific scenario where each player starts with money units: the initial distribution (measured across the ensemble of players) is infinitely narrow. As this distribution spreads toward the broader equilibrium distribution, each player will, typically, have to travel a distance along the coordinate that is comparable to the standard deviation of the equilibrium distribution,

| (38) |

Given the diffusive dynamics along , and assuming a constant diffusivity , the time to attain the equilibrium distribution should be comparable to

| (39) |

Although this estimate ignores the possible dependence of the diffusivity on , as well as the fact that diffusion is not free but biased, it highlights an important observation that is insensitive to the above assumptions: if diverges, then some of the players will have to travel infinitely far from their starting point , which will take infinite time, and so we expect the equilibration time to diverge 222Note that the diffusion coefficient remains finite in this case, given the discrete time unit adopted here.

In particular, for the Boltzmann distribution, Eqs. (12) and (13), the standard deviation is given by

| (40) |

Therefore, we expect the relaxation time to diverge in the limit . Similarly, the power law distribution of Eq. (34) has infinite variance, and thus the relaxation time should become infinite for for any value of the unfairness parameter that exceeds 1/2. The case is different: using Eqs. (23)-(26), it can be shown that the equilibrium distribution (cf. Fig. 3) has a finite width. Thus, we expect the equilibration time to be finite even in the limit.

To study the relaxation timescales of the money game more quantitatively, let us first consider the relaxation dynamics for the single-player variable , as revealed by its equilibrium autocorrelation function

| (41) |

Here is the propagator, i.e., the joint probability to find the player with money units at (discrete) time given that this player had money units initially. In the matrix form, the one-step propagator is given by , where

| (42) |

is the matrix of transition probabilities corresponding to the kinetic scheme of Fig. 1. Similarly, we have

Using Eq. (41) now, we conclude that the autocorrelation function has a spectral expansion of the general form

| (43) |

where , , , … are the positive eigenvalues of T arranged in descending order. Unless the coefficient happens to be identically equal to zero, the long-time decay of the correlation function is dominated by , and thus we take

| (44) |

to be the characteristic relaxation time of .

To study global relaxation dynamics of the entire system, one needs to introduce a global order parameter that describes the system’s dynamics. If is a linear combination of single-player variables ’s or, more generally, some function of the form 333For example, one could use the variance as one such global parameter

then, taking into account the statistical independence of and for , it is easy to see that

and thus the autocorrelation function of has a spectral expansion of the same form as Eq. (43). Therefore, we take Eq. (44) as a measure of both projected and global relaxation dynamics.

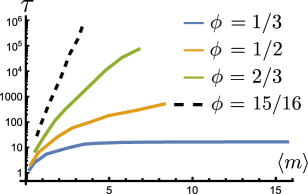

Figure 13 shows the relaxation times given by Eq. (44) as a function of the average amount of money per player. Consistent with the arguments above, this time grows indefinitely as for but approaches a plateau for .

XI Concluding remarks

In the money exchange model studied here, the Boltzmann distribution could be derived directly as the steady-state distribution corresponding to the kinetic laws governing the system in the thermodynamic limit (). It is instructive to consider how the same result can be obtained using conventional statistical mechanics arguments. As the microscopic kinetics of the model is a random walk on a connected graph that is not bipartite, the system is ergodic Norris and Norris (1997). In the case of a “fair” game (), for most connected pairs of microscopic states (namely, those with nonzero money) (cf. Fig. 2) detailed balance leads to equally populated states. Therefore, the principle of equiprobability of the microstates holds. We can think of the microscopic description of the game as leading to the microcanonical ensemble. Now, if we view an individual player as a small subsystem exchanging money/energy with the large “reservoir” formed by the remaining players, then the Boltzmann distribution of this player’s money can be deduced using the usual arguments of statistical mechanics Khinchin and Gamow (2014); Landau and Lifshitz (1980); Kardar (2020).

For , time-reversal symmetry and detailed balance are broken, and the microstates of the system are no longer equally populated – a microcanonical ensemble description is no longer applicable. As a result, the distribution of an individual player’s wealth is no longer exponential. The poor-biased () and rich-biased () cases turn out to be qualitatively different. The former leads to a bell-shaped distribution of money centered around the mean, which is attained over a finite equilibration time, even when . The latter leads, in the limit, to a broad distribution with a Pareto-type power-law intermediate regime and an exponential tail, such that the first moment of the distribution remains finite. As increases, the range of values of for which the power law holds becomes broader, with the exponential tail shifting toward large values of . Remarkably, the probability distribution of money in the power-law regime is independent of the total average wealth of a player, and thus of the total amount of money in the game – that is, the wealth of those “moderately successful players” is unaffected by the total wealth. At the same time, the fraction of players in the “ground state” with exactly zero money remains finite regardless of the value of , and it cannot be lower than a certain critical value . In the limit the power law holds even for , and the distribution’s first moment diverges accordingly. The equilibration time also diverges in this case.

For a finite number of players , the rich-biased game has an interesting regime with bistable dynamics, with each player hopping between a “super-rich” state in which they accumulate nearly the entire money pool and a “poor” state. This bistability can be captured within the local equilibrium approximation discussed in Section VIII.

Finally, we note that the time evolution of the money belonging to a single player (or, analogously, the energy of a single particle exchanging energy with other particles), can be viewed as a projection of a highly multidimensional process (in full state space, as in Fig. 2) onto a single degree of freedom. Such projected dynamics is generally expected to be a non-Markov process Zwanzig (2001). But for our system, non-Markov effects are only significant for intermediate values of , particularly in the non-equilibrium case of a rich-biased game, where the winner-takes-all scenario leads to coupling between players. Indeed, such coupling only exists at finite values of where the total amount of money in the game is finite (Section VII); on the other hand, for the dynamics of the money belonging to each player is strictly Markovian, as the conservation of money, , necessitates that both and are one-dimensional, Markovian random walks (see the Supplementary Material).

Acknowledgement

Discussions with Cai Dieball, Irene Gamba, Aljaž Godec, Hagen Hofmann, Matthias Krüger, Peter Sollich, and John Stanton are gratefully acknowledged. This work was supported by the Robert A. Welch Foundation (Grant No. F- 1514 to DEM), the National Science Foundation (Grant No. CHE 1955552 to DEM), and the Alexander von Humboldt Foundation.

References

- Angle (1986) J. Angle, Social Forces 65, 293 (1986), URL http://www.jstor.org/stable/2578675.

- Greenberg and Gao (2023) M. Greenberg and H. O. Gao, Twenty-five years of random asset exchange modeling (2023), eprint 2309.12418, URL https://arxiv.org/abs/2309.12418.

- Yakovenko and Rosser (2009) V. M. Yakovenko and J. B. Rosser, Rev. Mod. Phys. 81, 1703 (2009), URL https://link.aps.org/doi/10.1103/RevModPhys.81.1703.

- Dragulescu and Yakovenko (2000) A. Dragulescu and V. M. Yakovenko, Eur. Phys. J. B 17, 723 (2000), URL https://doi.org/10.1007/s100510070114.

- Patriarca and Chakraborti (2013) M. Patriarca and A. Chakraborti, Am. J. Phys. 81, 618 (2013), ISSN 0002-9505, URL https://doi.org/10.1119/1.4807852.

- Banerjee and Yakovenko (2010) A. Banerjee and V. M. Yakovenko, New J. Phys. 12, 075032 (2010), URL https://dx.doi.org/10.1088/1367-2630/12/7/075032.

- Bennati (1988) E. Bennati, Rivista Internazionale di Scienze Economiche e Commerciali 35, 735 (1988).

- Bennati (1993) E. Bennati, Rassegna di Lavori dell’ISCO (Istituto Nazionale per lo Studio della Congiuntura) 10, 31 (1993).

- Ispolatov et al. (1998) S. Ispolatov, P. L. Krapivsky, and S. Redner, The European Physical Journal B-Condensed Matter and Complex Systems 2, 267 (1998), URL https://doi.org/10.1007/s100510050249.

- Klein et al. (2021) W. Klein, N. Lubbers, K. K. L. Liu, T. Khouw, and H. Gould, Phys. Rev. E 104, 014151 (2021), URL https://link.aps.org/doi/10.1103/PhysRevE.104.014151.

- Liu et al. (2021) K. K. L. Liu, N. Lubbers, W. Klein, J. Tobochnik, B. M. Boghosian, and H. Gould, Phys. Rev. E 104, 014150 (2021), URL https://link.aps.org/doi/10.1103/PhysRevE.104.014150.

- Drăgulescu and Yakovenko (2001) A. Drăgulescu and V. M. Yakovenko, Physica A 299, 213 (2001), ISSN 0378-4371, application of Physics in Economic Modelling, URL https://www.sciencedirect.com/science/article/pii/S0378437101002989.

- Silva and Yakovenko (2004) A. C. Silva and V. M. Yakovenko, Europhys. Lett. 69, 304 (2004), URL https://dx.doi.org/10.1209/epl/i2004-10330-3.

- Banerjee et al. (2006) A. Banerjee, V. M. Yakovenko, and T. Di Matteo, Physica A 370, 54 (2006), ISSN 0378-4371, econophysics Colloquium, URL https://www.sciencedirect.com/science/article/pii/S0378437106004353.

- Scalas et al. (2006) E. Scalas, U. Garibaldi, and S. Donadio, Eur. Phys. J. B 53, 267 (2006), URL https://doi.org/10.1140/epjb/e2006-00355-x.

- Lanchier (2017) N. Lanchier, J. Stat. Phys. 167, 160 (2017), URL https://doi.org/10.1007/s10955-017-1744-8.

- Lanchier and Reed (2018) N. Lanchier and S. Reed, J. Stat. Phys. 171, 727 (2018), URL https://doi.org/10.1007/s10955-018-2024-y.

- Lanchier and Reed (2019) N. Lanchier and S. Reed, J. Stat. Phys. 176, 1115 (2019), URL https://doi.org/10.1007/s10955-019-02334-z.

- Lanchier and Reed (2022) N. Lanchier and S. Reed, Distribution of money on connected graphs with multiple banks (2022), eprint 2201.11930, URL https://arxiv.org/abs/2201.11930.

- Balint et al. (2021) P. Balint, T. Gilbert, D. Szasz, and I. P. Toth, Pure and Applied Functional Analysis 1, 1 (2021).

- Simányi (2003) N. Simányi, Inventiones Mathematicae 154, 123 (2003), URL https://doi.org/10.1007/s00222-003-0304-9.

- Simányi (2009) N. Simányi, Inventiones mathematicae 177, 381 (2009), URL https://doi.org/10.1007/s00222-009-0182-x.

- Michalek and Hanson (2006) B. Michalek and R. M. Hanson, J. Chem. Educ. 83, 581 (2006), URL https://doi.org/10.1021/ed083p581.

- Cao and Motsch (2023) F. Cao and S. Motsch, Kinetic and Related Models 16, 764 (2023), ISSN 1937-5093, URL https://www.aimsciences.org/article/id/63ff170498611f40362f13e0.

- Scafetta et al. (2002) N. Scafetta, S. Picozzi, and B. J. West, Pareto’s law: a model of human sharing and creativity (2002), eprint cond-mat/0209373, URL https://arxiv.org/abs/cond-mat/0209373.

- Scafetta et al. (2004) N. Scafetta, S. Picozzi, and B. J. West, Physica D: Nonlinear Phenomena 193, 338 (2004), ISSN 0167-2789, anomalous distributions, nonlinear dynamics, and nonextensivity, URL https://www.sciencedirect.com/science/article/pii/S0167278904000624.

- Kelly (2011) F. P. Kelly, Reversibility and stochastic networks (Cambridge University Press, 2011).

- Kolmogoroff (1936) A. Kolmogoroff, Mathematische Annalen 112, 155 (1936), URL https://doi.org/10.1007/BF01565412.

- Godec and Makarov (2023) A. Godec and D. E. Makarov, J Phys Chem Lett 14, 49 (2023), ISSN 1948-7185 (Electronic) 1948-7185 (Linking), URL https://www.ncbi.nlm.nih.gov/pubmed/36566432.

- Blom et al. (2023) K. Blom, K. Song, E. Vouga, A. Godec, and D. E. Makarov, preprint (2023).

- Hartich and Godec (2021) D. Hartich and A. Godec, Phys. Rev. X 11, 041047 (2021).

- Harunari et al. (2022) P. E. Harunari, A. Dutta, M. Polettini, and E. Roldan, Physical Review X 12, 041026 (2022), URL https://doi.org/10.1103/PhysRevX.12.041026.

- Meer et al. (2022) J. v. d. Meer, B. Ertel, and U. Seifert, Phys. Rev. X 12, 031025 (2022), URL https://doi.org/10.48550/arXiv.2203.12020.

- Pareto et al. (1964) V. Pareto, G.-H. Bousquet, and G. Busino, Cours d’économique politique (Droz, 1964).

- Montroll and Shlesinger (1982) E. W. Montroll and M. F. Shlesinger, Proc. Natl. Acad. Sci. U.S.A. 79, 3380 (1982), URL https://www.pnas.org/doi/abs/10.1073/pnas.79.10.3380.

- Chakrabarti et al. (2013) B. K. Chakrabarti, A. Chakraborti, S. R. Chakravarty, and A. Chatterjee, Econophysics of income and wealth distributions (Cambridge University Press, 2013).

- Stone (2015) J. V. Stone, Information theory: A Tutorial Introduction (Sebtel Press, 2015).

- Makarov (2015) D. E. Makarov, Single Molecule Science: Physical Principles and Models (CRC Press, Taylor and Francis Group, Boca Raton, 2015).

- Elber et al. (2020) R. Elber, D. E. Makarov, and H. Orland, Molecular Kinetics in Condense Phases: Theory, Simulation, and Analysis (Wiley and Sons, 2020).

- Berezhkovskii and Makarov (2019) A. Berezhkovskii and D. E. Makarov, Journal of Chemical Physics 151, 065102 (2019).

- Berezhkovskii and Makarov (2018) A. M. Berezhkovskii and D. E. Makarov, J Phys Chem Lett 9, 2190 (2018), ISSN 1948-7185 (Electronic) 1948-7185 (Linking), URL https://www.ncbi.nlm.nih.gov/pubmed/29642698.

- Norris and Norris (1997) J. R. Norris and J. R. Norris, Markov chains (Cambridge University Press, 1997).

- Khinchin and Gamow (2014) A. Khinchin and G. Gamow, Mathematical Foundations of Statistical Mechanics (Martino Publishing, 2014).

- Landau and Lifshitz (1980) L. Landau and E. Lifshitz, Statistical Physics, vol. 5 of Course of Theoretical Physics (Butterworth-Heinemann, 1980).

- Kardar (2020) M. Kardar, Statistical physics of particles (Cambridge University Press, 2020).

- Zwanzig (2001) R. Zwanzig, Nonequilibrium Statistical Mechanics (Oxford University Press, 2001).