A Bayesian Markov-switching SAR model for time-varying cross-price spillovers

Abstract

The spatial autoregressive (SAR) model is extended by introducing a Markov switching dynamics for the weight matrix and spatial autoregressive parameter. The framework enables the identification of regime-specific connectivity patterns and strengths and the study of the spatiotemporal propagation of shocks in a system with a time-varying spatial multiplier matrix. The proposed model is applied to disaggregated CPI data from 15 EU countries to examine cross-price dependencies. The analysis identifies distinct connectivity structures and spatial weights across the states, which capture shifts in consumer behaviour, with marked cross-country differences in the spillover from one price category to another.

Keywords: Bayesian inference; Markov switching; Random spatial weights; Spatial autoregressive model; Time-varying network.

JEL-Codes: C23; C33; C34; E31

1 Introduction

A cornerstone model within the spatial econometrics literature is the spatial autoregressive (SAR) model, which exploits a weight matrix to introduce spatial dependence among the observations. Empirical practise typically relies on the fundamental assumption of an exogenously given spatial weight matrix, whose entries are known and based on a neighbourhood concept between any two (spatial) observations, such as geographic proximity (LeSage and Pace, 2009). For a given definition of distance, the associated spatial matrix can be interpreted as representing the connectivity pattern (or network) according to that criterion.

Spatial autoregressive (SAR) models have been applied in statistics and econometrics to investigate diverse problems, including the measurement of sovereign risk spillovers (Debarsy et al., 2018), regional economic dynamics (Basile et al., 2014), and firm-level productivity spillovers (Baltagi et al., 2016). The importance of accounting for spatial dependence goes beyond linear conditional mean models. In particular, Taşpınar et al. (2021) recently defined a spatial autoregressive stochastic volatility model to investigate volatility clustering in spatial data, while Doğan and Taşpinar (2018) introduced spatial dependence in a sample selection model. In addition, Badinger and Egger (2010) applied an extension of the SAR model to disentangle the horizontal (demand for final products) and vertical (demand for intermediate products) interdependence in multinational enterprise activity.

Several attempts have been made to relax the crucial assumption in the baseline SAR model of an exogenously fixed spatial weight matrix. For instance, Qu and Lee (2015) proposed a framework where the spatial weight is assumed to depend on an observable random variable and inferred by means of a generalised method of moments estimator, whereas Qu et al. (2021) utilised a two-stage estimation approach. Instead, Krisztin and Piribauer (2022) design a fully Bayesian approach to learn the unknown spatial weight matrix, thus allowing for uncertainty quantification on the dependence structure. An alternative statistical approach consists of estimating SAR models using different types of spatial weight matrices and then applying model averaging procedures to address model uncertainty regarding selecting the best matrix (Zhang and Yu, 2018; Debarsy and LeSage, 2022).

Over the last decades, the use of weight matrices based solely on the geographical neighbourhood has been criticised (Corrado and Fingleton, 2012) due to the application of spatial regression models to contexts where the geographical location of the observations is not fundamental in driving capturing their connectivity structures, such as in trade, migration, and social networks (for a thorough discussion, see Allen and Arkolakis, 2023). It follows that the results and interpretation of a SAR model might vary significantly according to the chosen concept of spatial proximity. Moreover, as selecting an appropriate definition that accounts for the key interconnections in the data is often challenging, pinning the model to a single spatial weight matrix may be misleading. To address this issue, recent contributions to the literature have focused on the uncertainty associated with the choice of neighbourhood structures by selecting or combining alternative weight matrices (e.g., see Piribauer and Crespo Cuaresma, 2016; Debarsy and LeSage, 2018).

Only recently, attention has moved towards spatial models with an unknown weight matrix to be estimated from the data. The main advantage is that the results do not depend on arbitrary distance or neighbour concepts specified a priori; conversely, the inferred matrix would encode the connectivity structure that better explains the relationships in the data. However, this comes at the cost of high dimensional parameter space since the number of free elements in a spatial weight matrix scales quadratically in the length of the cross-section. Consequently, this new strand of literature builds heavily on statistical techniques for high-dimensional models, such as penalised likelihood approaches (Lam and Souza, 2020) or shrinkage priors in a Bayesian setting (Krisztin and Piribauer, 2022; Piribauer et al., 2023).

Together with the spatial dependence of unknown form, economic and financial data repeatedly observed displays non-negligible temporal dependence over time. An important implication of this stylised fact is that the data might not support the assumption of time-invariant connectivity patterns and strength. Consequently, to account for the dynamics of the unknown dependence structure, we relax this assumption and allow both the weight matrix and the degree of spatial autocorrelation to evolve over time.

This article extends the Bayesian SAR panel model along two important dimensions. First, we relax the typical assumption of an exogenously given spatial weight matrix to make inferences about connectivity patterns. Based on work by Krisztin and Piribauer (2022) and Piribauer et al. (2023), we employ a shrinkage prior to tackling the dimensionality issue and recovering the strongest dependence relationships. Second, we relax the assumption of time-invariant connectivity and degree of spatial autocorrelation. We rely on the features of the multi-sector prices data investigated in the empirical application to design an appropriate mechanism driving the time variation. Distinctive features of many economic and financial data are the cyclical behaviour of the economy at a country-specific level and sporadic abrupt structural changes, which are usually associated with dramatic events, such as financial crises or the propagation of epidemics (e.g., see Billio et al., 2016; Huber and Fischer, 2018). Motivated by these discontinuities in the time series, we propose a Bayesian Markov-switching spatial autoregressive (MS-SAR) panel model to study the impact of covariates and spillover propagation in the different connectivity regimes.

In an empirical application, based on the theoretical framework by Glocker and Piribauer (2023), we use the proposed MS-SAR panel model along with monthly data on (three-digit) consumer price index (CPI) subindices for 15 euro-zone countries to estimate the role of consumer preferences in shaping demand-driven cross-price dependencies. The analysis identifies distinct states corresponding to significant economic events and consumer behaviour shifts with marked cross-country variation in spillover dynamics. States characterised by a high network density and widespread inflation spillovers appear particularly during economic transitions, most notably the recent energy price shocks.

2 Model

We are interested in investigating the direct and indirect propagation of shocks (i.e., spillovers) in a system of interconnected countries. A standard approach to study these phenomena is a spatial autoregressive (SAR) model (e.g., see Anselin, 1988) with exogenous covariates of the form:

| (1) |

where denotes an -dimensional vector of country-specific response variables, is a full-rank matrix of covariates, with an associated vector of coefficients . The square matrix denotes a spatial weight matrix encoding the contemporaneous connections among the responses, and is a spatial dependence parameter.

Most of the literature in spatial statistics considers a time-invariant weight matrix, as in eq. (1), which is an appropriate assumption for all those settings where represents geographical borders or spatial distance concepts. Conversely, time-invariance is likely violated when the weight matrix is unknown and subject to estimation or summarises a more abstract notion of distance between pairs of subjects, such as in economic and financial applications. For instance, the Euclidean distance between two collections of economic indicators might be considered a proxy for economic similarity or (inverse) distance between two countries. In cases like this, the temporal evolution of the underlying indicators induces a variation over time in their (economic) distance. Moreover, when distance metrics other than geographical proximity are considered, little guidance is often provided to the researcher about which criterion best captures the connections among a set of country-level variables. A more agnostic, data-based approach would be a desirable solution to this issue.

Motivated by these key facts, we propose a new model that allows us to infer directly from the data the contemporaneous connectivity structure (or network) among the response variables. Furthermore, to capture the discontinuities in economic and financial time series and account for their time-varying and connectivity structure with persistent links, we introduce a finite state Markov chain driving the dynamics of the pair in eq. (1).

Following Krisztin and Piribauer (2022), we assume that each entry of the time-varying spatial weight matrix is obtained from a hidden spatial binary adjacency matrix with typical element , that is . The choice of the linking function is guided by the restrictions commonly imposed on the weight matrix in static SAR models. First, is non-negative with if variable is connected (or neighbour) to in state , and otherwise. Second, to avoid self-loops, that is, to prevent a variable from being connected to itself. Third, is row-stochastic, meaning that each row sums to unity. This leads us to the following specification of the link function :

| (2) |

The evolution of and are then modelled using a Markov switching process. Specifically, we assume that and each entry are driven by a common -state hidden Markov chain , that is and at each time , where , with , are state-specific parameters. This specification assumes the existence of states of the world such that at each time , the matrix (and ) and the dependence parameter equal one of different values. Finally, by linking the probabilities of connecting any pair of variables over time, this construction is able to capture the persistence in the dynamics of the adjacency matrices and . This is achieved by means of a time-invariant transition matrix , where each row is a probability vector and is the transition probability from state to state . The resulting Markov switching spatial autoregressive (MS-SAR) model is:

| (3) |

Following Debarsy and LeSage (2022), let , then denote with the block-diagonal matrix whose -th block is the matrix . Moreover, define , , , and . The conditional likelihood can thus be written as:

| (4) |

where is the Jacobian of the transformation that depends on the parameters . Let count the transitions from state to state , that is , with denoting the cardinality of a set. Thus, the complete-data likelihood is:

| (5) |

3 Bayesian Estimation

3.1 Prior specification

In the following, we describe the prior distributions for the state-specific parameters for each state . Let where is the prior probability of a link between and in state . We assume the following hierarchical prior distribution for the latent binary spatial matrix :

| (6) | ||||

| (7) |

The spatial dependence parameter in the MS-SAR model in eq. (3) has a key role in determining the overall strength of the spatial relationships. However, unlike traditional SAR models with known spatial weight matrices, identification issues arise when both the spatial matrix and dependence parameters are inferred from data. For SAR models with row-standardised known spatial matrix, , a sufficient condition to ensure spatial stationarity of the model is (LeSage and Pace, 2009). A more relaxed condition is found in Sun et al. (1999, Lemma 2), which show that is sufficient, where denote the minimum and maximum eigenvalues of . Hereinafter, inspired by the common practice, we impose , meaning that only positive spatial autocorrelation is allowed, which is a typical assumption for empirical applications. The most commonly used restriction for known is . However, we rule out due to the identification issue that arises in this case when the spatial matrix is inferred from data. Therefore, we choose a Beta prior for the spatial dependence parameter:

| (8) |

Finally, a symmetric Dirichlet prior distribution is assumed for each row of the transition matrix:

| (9) |

Concerning the remaining non-switching parameters, we assume a Gaussian prior distribution for the coefficient vector and an inverse Gamma prior distribution for the innovation variance:

| (10) |

One may also use an improper prior for and , that is , as the resulting posteriors would be proper (e.g., see Debarsy and LeSage, 2022).

3.2 Posterior sampling

To make inferences on the model parameters, we design an efficient Gibbs sampler targeting the joint posterior distribution that cycles over the following steps:111We refer to the Supplement for the derivation of the full conditional posterior distributions.

-

1.

Draw the path of the latent states from using a forward-filtering backward-sampling (FFBS) algorithm.

-

2.

Draw the spatial dependence parameters from using a Griddy-Gibbs algorithm.

-

3.

Draw the entries of the latent binary matrix from .

-

4.

Draw the probability of each link in from

(11) -

5.

Draw the rows of the transition matrix from

(12) -

6.

Draw the covariates’ coefficients from

(13) -

7.

Draw the structural innovations variance from

(14)

Steps 4-5-6-7 are standard, and we refer to the Supplement for full computational details. The entire path of the latent states is sampled in Step 1 by using a forward-filtering backward-sampling (FFBS) algorithm (Frühwirth-Schnatter, 2006). This algorithm consists of a forward pass to compute the filtered probabilities of each state and a backward pass to compute the smoothed probabilities and simulate the entire trajectory of jointly, which is more efficient than drawing each from its full conditional distribution.

The dependence parameter has a complex full conditional distribution due to the complex way it enters the likelihood, for which no conjugate prior is available. However, since is a scalar parameter distributed on a bounded support, several methods for approximating its posterior distribution are available. In particular, as in LeSage and Pace (2009), we rely on the Griddy-Gibbs algorithm (Ritter and Tanner, 1992) that consists in discretising the support of , and sampling from the re-normalised approximated discrete distribution.

Finally, Step 3 samples the entries of the latent binary matrix relying on the efficient algorithm proposed in Krisztin and Piribauer (2022). Denoting with the observations allocated to the th state and with all the elements of except , the not normalised posterior full conditional probabilities are given by

where and are obtained from by modifying the spatial weight matrix via setting and , respectively. Therefore, each element has a Bernoulli posterior full conditional distribution , where .

4 Empirical application

Based on theoretical underpinnings in Glocker and Piribauer (2023), we apply the proposed MS-SAR model to illustrate the role of consumer preferences in shaping demand-driven cross-price dependencies by using monthly data on three-digit CPI subindices for 15 euro-zone countries.

4.1 Preferences, demand and cross price dependencies

Cross-demand describes the relationship between the change in demand for a good or service in response to a change in the price of a related good or service. An important aspect of this theory is that a change in the price of good will, in turn, shift the demand curve, causing both the demand for good and its price to change. Therefore, given either a substitutability or complementarity relationship, a change in the price of good will not only change the demand for good but also the price of good . Thus, changes in the price of one good can affect the prices of other goods through the demand system.

Glocker and Piribauer (2023) establish a relationship between demand-driven cross-price dependencies and the consumer price index (CPI, ), and hence the CPI inflation rate (). In what follows, we briefly discuss this. Consider goods and let be the Marshallian demand function of good as a function of its own price , the vector of the prices of all other goods , and income . We collect the corresponding inverse demand functions in the -dimensional vector-valued function . Assuming perfectly competitive markets and price inelastic supply, the vector represents equilibrium prices. Computing the total differential, the change implies that

| (15) |

where the vector which captures income-demand effects. Most importantly, is a Jacobian matrix of first derivatives, that is , which contains cross-price interdependencies , with (and zeros on the main diagonal). The cross-price dependencies measure the extent to which the price of good changes as a result of a change in the price of good within the demand system. Since cross-price effects arise due to the substitutability or complementarity of goods (and services), cross-demand, and hence the non-zero entries in the Jacobian matrix , can be either positive or negative.

To obtain a relationship between the Jacobian matrix and the CPI inflation rate222We approximate the geometric mean, as used to construct the CPI, by the arithmetic mean., let the CPI be given by , where the -dimensional column vector contains the weights (expenditure shares) of each good. Using this expression, if the weights are fixed at some constant level, then the change in the CPI is given by and the CPI inflation rate is given by the relative change in the CPI . Substituting eq. (15) into the latter expression yields the following relationship between prices shape the CPI inflation rate:

| (16) |

where . For example, if the Jacobian is the null matrix, then the effect of a shock to a single price on the CPI inflation rate is equal to that price’s weight times the shock’s size. Instead, in the presence of cross-price dependencies, the Jacobian is nonzero, implying that a shock to price can affect the CPI inflation rate both directly, via the price and indirectly, via the spillover effects arising from the cross-price dependencies.

To keep the exercise tractable, we restrict the analysis to non-negative entries in the Jacobian matrix, thus implying that all links between prices arise from complementarities between goods (and services). While this is a strong assumption and is likely to overestimate the impact of an exogenous shock to a given price on CPI inflation, it is justified by the fact that Regmi and Seale (2010) and Glocker and Piribauer (2023), for example, emphasise the dominance of complementarity over substitution relationships.

4.2 The data

The goods and services in the CPI basket are classified by purpose into consumption groups (COICOP) at different levels of (dis)aggregation called level of structure (two-digit, three-digit, etc.). We use the three-digit COICOP structure of the CPI, which consists of 44 different monthly price sub-indices. We exclude sub-indices for which the sample does not extend back to at least 2002. These are the price sub-indices related to educational goods and services (cp_101 to cp_105), leaving a total of sub-indices and their respective basket weights.333Weights have been adjusted to take account of the omission of five sub-indices. Details of the sub-indices are given in the Supplement. We collect data for 15 euro-zone countries (Austria, Belgium, Cyprus, Estonia, Finland, France, Germany, Greece, Ireland, Italy, Latvia, Lithuania, the Netherlands, Portugal and Spain).

For each country in our sample, we consider the monthly relative year-over-year changes from January 2002 to June 2023, resulting in time observations. Besides these CPI-based data and additional monthly variables as control variables, explained in detail below, we also use the weights () for each price sub-index of the three-digit COICOP structure for the subsequent analysis.

4.3 From theory to an econometric specification

We apply the proposed MS-SAR model to investigate the cross-dependencies between the aforementioned CPI-based price sub-indices at the 3-digit level. In this context, we aim to estimate a version of equation (15). We apply the MS-SAR panel model in eq. (3) where the dependent variable is an -dimensional vector comprising monthly information on the price sub-indices and expressed as year-over-year (relative) change. The MS-SAR model is applied individually to all countries in our sample. Therefore, the spatial element refers only to the individual price sub-indices and not to geographical regions. We include item-fixed effects in each country model to control for item-specific heterogeneity.

Significantly, changes in consumer behaviour can affect cross-price dependencies along two dimensions. The first concerns the amount of nonzero elements in and, hence, the amount of other goods’ prices being affected once the price of a particular good changes. We control for this effect by considering a state-dependency in the matrix, . The second concerns the extent of inertia. Once a price shock propagates through the demand system, its effect could either abate quickly or not. We consider a state-dependency in the scalar, , to account for this matter. In both cases, the state-dependency represents changes in consumer preferences and, hence, consumer behaviour.

The explanatory variables, , include several producer price sub-indices444This serves to identify demand and hence to solve the endogeneity problem related to estimating demand and supply functions. We can isolate the demand-driven cross-price interdependencies within the matrix by controlling for these supply-side factors. (e.g., food, textiles, energy), administered price measures, the nominal effective exchange rate, and global indicators such as shipping costs (Carrière-Swallow et al., 2023), Brent crude oil prices, and natural gas prices (Dutch TTF). In addition, we include the overall CPI inflation rate as a control variable. This choice is based on the common industry practice of adjusting prices based on past CPI inflation rates (inflation indexation of prices). These variables are used for each country in our analysis.

4.4 Results

Given the abundance of empirical output, we organise our discussion as follows: Section 4.4.1 provides country-specific evidence, focusing on two specific countries to illustrate how the model works in the context of their unique characteristics. Section 4.4.2 provides consolidated statistics and discussion, where we attempt to synthesise the results from all countries in our sample.

To analyse the impact of demand shocks on CPI inflation, it is helpful to rewrite the model in its reduced form

| (17) |

where the matrix is commonly referred to as the spatial multiplier matrix. It describes the transmission of demand shocks (and thus of the elements in ) in the system of cross-price dependencies. The elements on the diagonal of the spatial multiplier matrix , called direct effects in the spatial econometrics literature (e.g., see LeSage and Pace, 2009), contain information about the impact of a shock on the price sub-index , namely the own-price effect. The Neumann series expansion of the spatial multiplier matrix shows that these main diagonal elements already contain feedback effects due to cross-price dependencies. The off-diagonal elements in comprise the indirect (or spillover) effects and capture the impact of a shock on other price sub-indices , .

Motivated by the interest in analysing the impact of shocks on the overall CPI inflation rate , we exploit eq. (16) to relate the direct and indirect effects of shocks on particular price sub-indices to the overall CPI inflation rate. Let us first define the -dimensional vector , which collects the direct effects on the CPI inflation rate at time , as

| (18) |

where the -th element captures the direct effect of a shock to the -th price subindex on the CPI inflation rate and denotes the diagonal matrix operator such that represents an diagonal matrix. Instead, the contribution of the spillover (or indirect) effects to the CPI inflation rate is given by the off-diagonal elements of the spatial multiplier

| (19) |

Indirect effects measure the impact of shocks to a particular price sub-index on the CPI inflation rate resulting only from the interaction with other price sub-indexes. Finally, the total effect combines both direct and spillover effects and is given by . In the following, we will focus on the extent to which direct and indirect effects vary across countries and, most importantly, across the states of the world as captured by the Markov chain.

4.4.1 Country-specific results

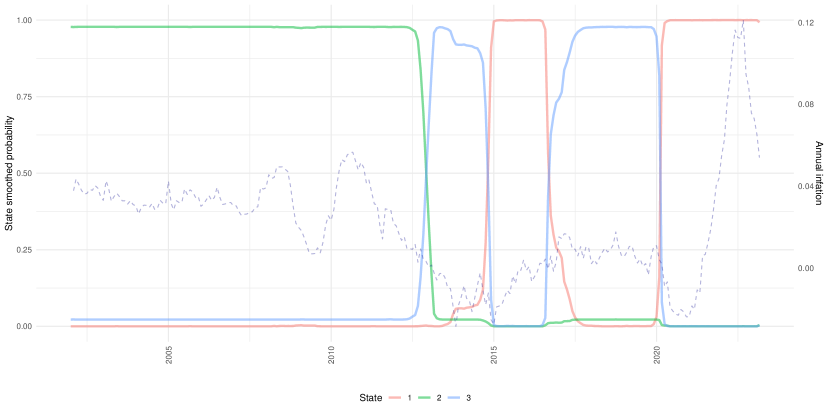

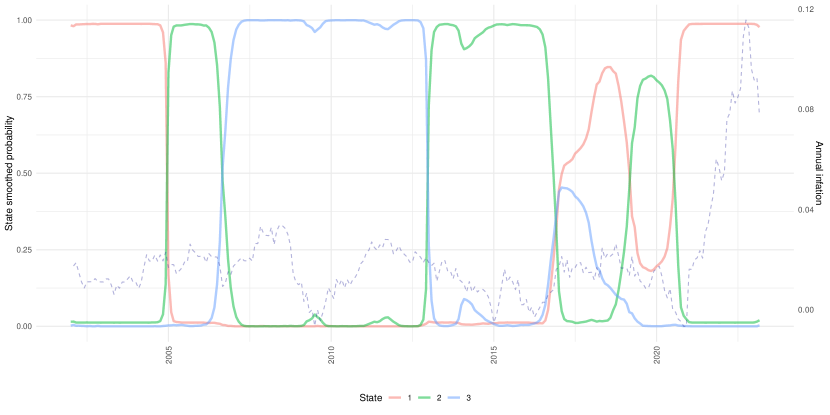

We present a detailed analysis of Greece (EL) and Germany (DE), chosen for their interesting patterns, which provide valuable insights into the functioning and understanding of our empirical model.555The results of other countries in the sample are too numerous to be included here, but are available upon request to the authors. We use the DIC criterion to determine the number of hidden states of the Markov chain, resulting in for both countries. The two panels in Figure 1 report the posterior estimate of the (smoothed) state probabilities for Greece (upper panel) and Germany (lower panel). In each case, we compare the time trajectory of the (smoothed) state probabilities to the overall CPI inflation rate (dashed line in the panels).

The results show several state transitions for Greece. From a macroeconomic perspective, the first coincides with the Greek debt crisis in 2012. The subsequent state transitions resemble significant energy price changes, the first of which occurred in 2014/2015 with a considerable drop in oil prices, followed by a subsequent increase in 2017. The final state transition coincides with the outbreak of the COVID-19 pandemic in early 2020. Regarding Germany, it is noteworthy that the state transitions reflect either economic crises or their recovery. For example, the first (2004/2005) corresponds to a country-specific episode of economic slack, while the second (2007) corresponds to the subsequent recovery. The third (2013) corresponds to the recovery from the European debt crisis, while the last partly reflects the energy price hike and, thus, the recovery from the COVID-19 recession. Between 2017 and 2020, the smoothed probabilities are very close to each other, thus suggesting no clear evidence in favour of any particular state.

Given our focus on estimating (inverse) consumer demand functions, the evolution in state probabilities indicates changes in consumer preferences and, hence in the composition of household expenditure, which in turn leads to changes in cross-price dependencies. This adjustment is particularly pronounced during switches of economic conditions, from boom to bust and vice versa, indicating sudden and dramatic changes in demand and, hence in cross-price dependencies. This phenomenon was particularly evident during the COVID-19 pandemic and may have been exacerbated by policy-related closure measures: the enforced closure of physical retail outlets led to a significant shift towards online shopping. Gorodnichenko and Talavera (2017) and Gorodnichenko et al. (2018) underline that the shift to online retailing had a significant impact on price dynamics, ultimately leading to changes in demand-driven cross-price dependencies and hence the overall CPI inflation rate.666As the matrix represents a directed weighted network, the presence of cycles between nodes can be important. A cycle involving only two nodes (i.e., a directed link from node to and another from to ) can have a large overall effect even though there are no other edges in the network. We refer the interested reader to Fan et al. (2021) and Glocker and Piribauer (2023) for further discussion.

State No.1 State No.2 State No.3 DE EL DE EL DE EL Network statistics Link density (in %) 3.10 3.24 1.48 2.70 1.21 2.02 Network density () 1.00 1.17 0.59 0.98 0.51 0.84 Network density () 0.47 0.70 0.19 0.33 0.09 0.25 Spatial auto-regressive parameter post. mean 0.47 0.60 0.33 0.34 0.18 0.29 post. std. dev. 0.03 0.02 0.03 0.01 0.02 0.02 The values in the table are multiplied by 100 in each case. The link density is the ratio between the number of links (edges) and the maximum possible number of links in the network. The network density is the average value of the size of the existing links. It extends the link density by considering the numerical value associated with each link (in a weighted network). Hence, the network density measures the strength effect for a given link density.

The changes of states, the switch in the probability of a particular state relative to the others, also lead to significant changes in the structure of demand-driven cross-price dependencies. Details are provided in Table 1 using two commonly used measures of network topology: link density (Newman, 2010) and network density (Horvath, 2011). The former is the ratio between the number of links and the maximum possible number of links in the network. The network density, defined as the average value of the size of the existing links, extends the link density by accounting for the weight associated with each link in a weighted network; as such, it measures the average strength of the links. Both connectedness measures quantify the spillover effects of shocks to individual price sub-indices. In computing these network statistics, only those entries in the matrix whose posterior inclusion probabilities exceed a value of are considered; those with a value below this threshold are set to zero.777This choice is motivated by the fact that the proposed model can shrink the entries of toward zero but does not allow for exact zeros. Therefore, we follow common practice in Bayesian shrinkage estimation and set a hard threshold to obtain zeros in the estimated adjacency matrices.

In both countries under scrutiny, state is characterised by the most significant number of links with a concomitantly high overall network density. In contrast, state is associated with the lowest degree of interconnectedness. Looking at the estimated path of the state probabilities, we find the transition to state in conjunction with dramatic changes in the overall CPI inflation rate resulting from changes in (aggregate) demand. Since state reflects a situation of high linkage and network density, small shocks to the demand for particular goods (i.e., individual price sub-indices) quickly spill over to many other prices, eventually leading to a broad-based price (and hence inflationary) impact. Given that we consider a framework where all the links are positive-valued, any additional link exacerbates the transmission mechanism of shocks, thus increasing the likelihood of the previously mentioned phenomenon being particularly pronounced.

It is noteworthy that the estimated spatial weight parameter significantly differ across the states, as shown in the bottom panel of Table 1. The posterior mean is highest in state 1 and lowest in state 3, reinforcing the previous claim that these states represent periods of strong and weak spatial dependence, respectively. Instead, the posterior standard deviation is small and similar across all the states. These findings support the claim that both the structure of the spatial relationships and their strength vary over time, which is the key motivation underlying the Markov-switching specification for the pair in model (3). Interestingly, our results confirm the claim recently made by Scidá (2023), which performed a rolling window analysis of a SAR model with time invariant parameters. In contrast, the proposed MS-SAR model is explicitly designed to capture the switching values of the parameter and network structure.

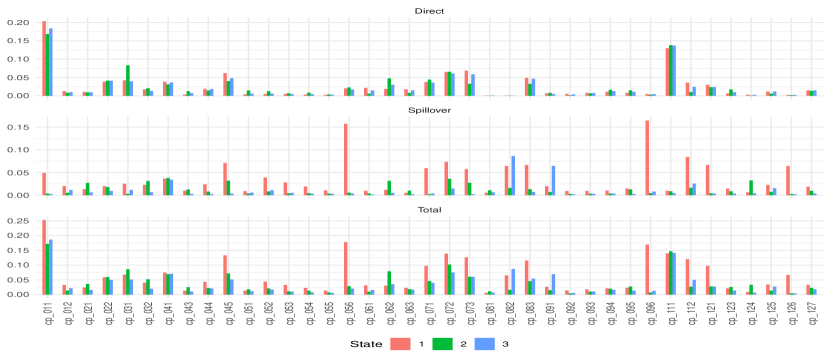

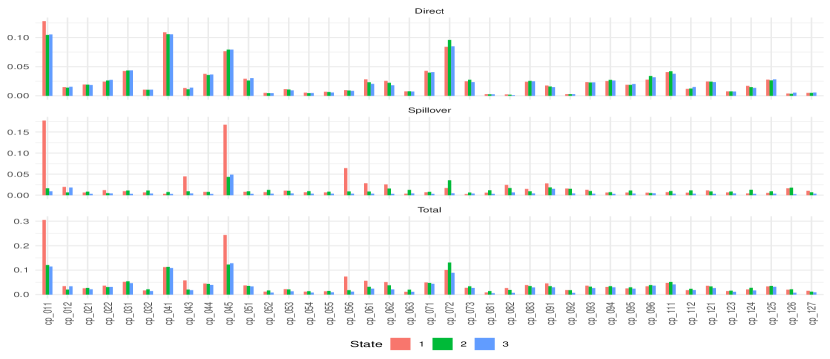

The dominance of state is also apparent when considering the effects of shocks to individual price sub-indices on the CPI inflation rate. To this end, we now consider the decomposition of the impact of a shock to each single price sub-index on the CPI inflation rate into direct and indirect effects, as motivated by eq. (18) and (19). The two panels in Figure 2 show the results for each price sub-index across all identified states for both countries. The calculations are based on the average over time of the weights . Specifically, we first compute the posterior mean of each state-specific spatial multiplier matrix . For each period where the posterior inclusion probability of state was greater than , we then calculate the direct, indirect, and total effects using the corresponding weights . Finally, we average these effects over time.

The results for both countries suggest that, in many cases, the most considerable spillovers (middle sub-panel) are associated with state 1 (red bar). In contrast, the other two states are associated with significantly smaller spillovers in magnitude. Another interesting result in this context concerns the importance of certain price sub-indices in shaping the overall CPI inflation rate.

For instance, the results for Greece show that, in some cases, a large overall effect is due solely to strong direct effects (e.g., for the categories “food” and “restaurant services”); that is, the corresponding price indices have a large (average) weight in the CPI, while in other cases a large overall effect is due to significant spillover effects (e.g., for the categories “Package holidays” and “Telephone and Telefax Equipment”). A similar pattern is observable for Germany, though the price sub-indices shaping the spillover effects most considerable in size are instead “Electricity, Gas and Other Fuels” and “Goods and Services for Routine Household Maintenance” apart from the category “Food” whose large total effect is established by both large direct and spillover effects.

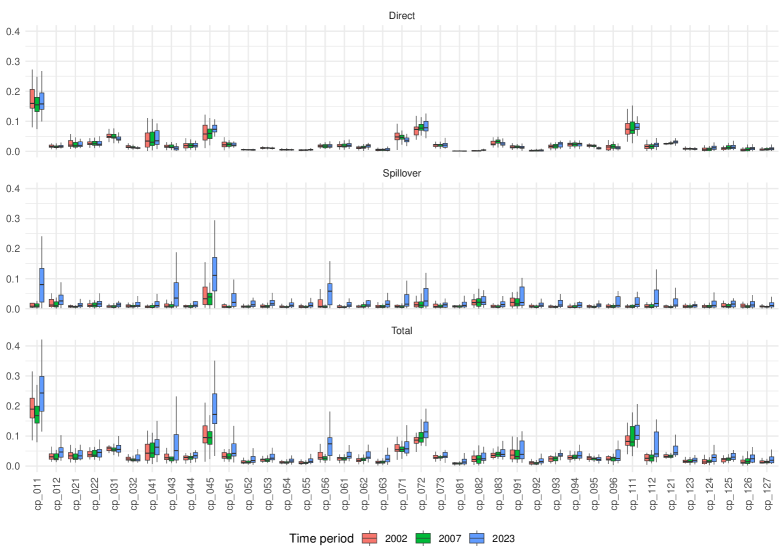

4.4.2 Evidence across countries

As the previous country-specific results highlight some form of country heterogeneity, we now examine the cross-country variation in more detail, using all 15 countries in the sample. Figure 3 provides a comprehensive overview of the effects of different price sub-indices on the CPI inflation rate for three selected years, which represent different phases that are essentially common to all countries in our sample: the beginning of an expansionary period (2002), the end of a boom (2007), and the peak of the energy crisis in 2022/2023 (2023). The figure breaks down the impacts along three dimensions: (i) direct, (ii) indirect, and (iii) total impacts and the bars measure the extent of country variation along these three dimensions for each of the selected years.

One striking result is the significant cross-country variation in some price sub-categories, such as “Electricity, Gas & Other Fuels”, “Operation of Personal Transport Equipment”, and “Other Recreational Items & Equipment, Gardens & Pets”. In each case, the total effects show considerable cross-country variation, mainly due to cross-country differences in spillover effects. On the other hand, the direct effects are relatively similar in size across countries, implying small bars on average.

Interestingly, the estimated direct effects are relatively constant between 2002 and 2007, whereas the spillover effects show more time variation. However, in 2023, the time variation becomes more pronounced compared to the other years. This dramatic change goes beyond energy-related prices and is particularly pronounced in categories such as “Accommodation Services” and “Goods & Services for Routine Household Maintenance”. Crucially, the variation in total effects in 2023 compared with 2002 and 2007 is mainly due to changes in spillovers rather than weight changes. The slight change of direct impacts over time is primarily because the weights of the price sub-indices in the CPI are only marginally adjusted. The comparatively high importance of spillovers thus underlines the importance of changing consumer preferences in this respect, which play a crucial role in shaping demand-driven cross-price dependencies and, consequently, changes in spillovers that shape the transmission of shocks to individual prices to the CPI inflation rate.

5 Conclusions

The article introduces a novel Markov-switching spatial autoregressive (SAR) model with an unknown time-varying weight matrix and presents a Bayesian approach to statistical inference. The model aims to study the time-varying shocks’ direct and indirect propagation in a system of interconnected variables (nodes). Using an unknown weight matrix allows more flexibility in capturing the connectivity patterns, while the temporal variation accounts for the cyclical behaviour and abrupt structural changes in the data. A Markov switching process drives the time variation of two main components of the SAR model: the elements of the weight matrix and, hence, the connectivity pattern among the response variables, and the spatial autocorrelation, which governs the speed of decay of a shock propagating through the system.

We illustrate the model’s performance in an empirical application that examines consumer preferences’ role in shaping demand-driven cross-price dependencies. The analysis identifies distinct states corresponding to significant economic events and shifts in consumer behaviour, with marked cross-country variation in the spillover from one price category to another. Overall, the proposed model provides a valuable framework for studying spillovers and understanding the links between economic variables and their variation over time.

There are various possible extensions to our proposed setup. For instance, the increasing use of stochastic-block models motivates a refinement of the time-varying element to particular blocks within the weight matrix (Holland et al., 1983). Related to this, an extension could then also be considered for community detection (Fortunato, 2010). Another possible direction for future research is to investigate different types of nonlinear spillover effects in the system, such as those incorporating threshold effects. Overall, these potential extensions and future research directions can further enhance our understanding of the spatiotemporal propagation of shocks and the dynamics of spatial dependence in interconnected economic systems.

Another interesting avenue for future research would be to extend the proposed Markov switching approach to the dynamic spatial autoregressive framework (e.g., see Baltagi et al., 2014; Yang and Lee, 2021; Billé and Rogna, 2022) to account for potential breaks in both the temporal and spatial dependence structures and strengths.

References

- Allen and Arkolakis (2023) Allen, T. and C. Arkolakis (2023). Economic activity across space. The Journal of Economic Perspectives 37(2), 3–28.

- Anselin (1988) Anselin, L. (1988). Spatial econometrics: Methods and models, Volume 4. Springer Science & Business Media.

- Badinger and Egger (2010) Badinger, H. and P. Egger (2010). Horizontal vs. vertical interdependence in multinational activity. Oxford Bulletin of Economics and Statistics 72(6), 744–768.

- Baltagi et al. (2016) Baltagi, B. H., P. H. Egger, and M. Kesina (2016). Firm-level productivity spillovers in China’s chemical industry: A spatial Hausman-Taylor approach. Journal of Applied Econometrics 31(1), 214–248.

- Baltagi et al. (2014) Baltagi, B. H., B. Fingleton, and A. Pirotte (2014). Estimating and forecasting with a dynamic spatial panel data model. Oxford Bulletin of Economics and Statistics 76(1), 112–138.

- Basile et al. (2014) Basile, R., M. Durbán, R. Mínguez, J. M. Montero, and J. Mur (2014). Modeling regional economic dynamics: Spatial dependence, spatial heterogeneity and nonlinearities. Journal of Economic Dynamics and Control 48, 229–245.

- Billé and Rogna (2022) Billé, A. G. and M. Rogna (2022). The effect of weather conditions on fertilizer applications: A spatial dynamic panel data analysis. Journal of the Royal Statistical Society Series A: Statistics in Society 185(1), 3–36.

- Billio et al. (2016) Billio, M., R. Casarin, F. Ravazzolo, and H. K. Van Dijk (2016). Interconnections between eurozone and us booms and busts using a Bayesian panel Markov-switching VAR model. Journal of Applied Econometrics 31(7), 1352–1370.

- Carrière-Swallow et al. (2023) Carrière-Swallow, Y., P. Deb, D. Furceri, D. Jiménez, and J. D. Ostry (2023). Shipping costs and inflation. Journal of International Money and Finance 130, 102771.

- Celeux et al. (2006) Celeux, G., F. Forbes, C. Robert, and D. Titterington (2006). Deviance information criteria for missing data models. Bayesian Analysis 1(4), 651–674.

- Corrado and Fingleton (2012) Corrado, L. and B. Fingleton (2012). Where is the economics in spatial econometrics? Journal of Regional Science 52(2), 210–239.

- Debarsy et al. (2018) Debarsy, N., C. Dossougoin, C. Ertur, and J.-Y. Gnabo (2018). Measuring sovereign risk spillovers and assessing the role of transmission channels: A spatial econometrics approach. Journal of Economic Dynamics and Control 87, 21–45.

- Debarsy and LeSage (2018) Debarsy, N. and J. LeSage (2018). Flexible dependence modeling using convex combinations of different types of connectivity structures. Regional Science and Urban Economics 69, 48–68.

- Debarsy and LeSage (2022) Debarsy, N. and J. P. LeSage (2022). Bayesian model averaging for spatial autoregressive models based on convex combinations of different types of connectivity matrices. Journal of Business & Economic Statistics 40(2), 547–558.

- Doğan and Taşpinar (2018) Doğan, O. and S. Taşpinar (2018). Bayesian inference in spatial sample selection models. Oxford Bulletin of Economics and Statistics 80(1), 90–121.

- Fan et al. (2021) Fan, T., L. Lü, D. Shi, and T. Zhou (2021). Characterizing cycle structure in complex networks. Communications Physics 4(272), 1–9.

- Fortunato (2010) Fortunato, S. (2010). Community detection in graphs. Physics Reports 486(3), 75–174.

- Frühwirth-Schnatter (2006) Frühwirth-Schnatter, S. (2006). Finite mixture and Markov switching models. Springer.

- Glocker and Piribauer (2023) Glocker, C. and P. Piribauer (2023). Propagation of Price Shocks to CPI Inflation: The role of Cross-Demand Dependencies. Wifi working paper 663, Austrian Institute of Economic Research.

- Gorodnichenko et al. (2018) Gorodnichenko, Y., V. Sheremirov, and O. Talavera (2018). Price setting in online markets: Does it click? Journal of the European Economic Association 16(6), 1764–1811.

- Gorodnichenko and Talavera (2017) Gorodnichenko, Y. and O. Talavera (2017). Price setting in online markets: Basic facts, international comparisons, and cross-border integration. American Economic Review 107(1), 249–282.

- Holland et al. (1983) Holland, P. W., K. Blackmond Laskey, and S. Leinhardt (1983). Stochastic block models: First steps. Social Networks 5(2), 109–137.

- Horvath (2011) Horvath, S. (2011). Weighted Network Analysis: Applications in Genomics and Systems Biology. SpringerLink : Bücher. Springer New York.

- Huber and Fischer (2018) Huber, F. and M. M. Fischer (2018). A Markov switching factor-augmented VAR model for analyzing US business cycles and monetary policy. Oxford Bulletin of Economics and Statistics 80(3), 575–604.

- Krisztin and Piribauer (2022) Krisztin, T. and P. Piribauer (2022). A Bayesian approach for the estimation of weight matrices in spatial autoregressive models. Spatial Economic Analysis, 1–20.

- Lam and Souza (2020) Lam, C. and P. C. Souza (2020). Estimation and selection of spatial weight matrix in a spatial lag model. Journal of Business & Economic Statistics 38(3), 693–710.

- LeSage and Pace (2009) LeSage, J. and R. K. Pace (2009). Introduction to spatial econometrics. Chapman and Hall/CRC.

- Newman (2010) Newman, M. E. J. (2010). Networks: An introduction. Oxford; New York: Oxford University Press.

- Piribauer and Crespo Cuaresma (2016) Piribauer, P. and J. Crespo Cuaresma (2016). Bayesian variable selection in spatial autoregressive models. Spatial Economic Analysis 11(4), 457–479.

- Piribauer et al. (2023) Piribauer, P., C. Glocker, and T. Krisztin (2023). Beyond distance: The spatial relationships of european regional economic growth. Journal of Economic Dynamics and Control 155, 104735.

- Qu and Lee (2015) Qu, X. and L.-f. Lee (2015). Estimating a spatial autoregressive model with an endogenous spatial weight matrix. Journal of Econometrics 184(2), 209–232.

- Qu et al. (2021) Qu, X., L.-f. Lee, and C. Yang (2021). Estimation of a SAR model with endogenous spatial weights constructed by bilateral variables. Journal of Econometrics 221(1), 180–197.

- Regmi and Seale (2010) Regmi, A. and J. L. Seale (2010). Cross-price elasticities of demand across 114 countries. Technical Bulletins 59870, United States Department of Agriculture, Economic Research Service.

- Ritter and Tanner (1992) Ritter, C. and M. A. Tanner (1992). Facilitating the Gibbs sampler: The Gibbs stopper and the griddy-Gibbs sampler. Journal of the American Statistical Association 87(419), 861–868.

- Scidá (2023) Scidá, D. (2023). Structural VAR and financial networks: A minimum distance approach to spatial modeling. Journal of Applied Econometrics 38(1), 49–68.

- Spiegelhalter et al. (2002) Spiegelhalter, D. J., N. G. Best, B. P. Carlin, and A. Van Der Linde (2002). Bayesian measures of model complexity and fit. Journal of the Royal Statistical Society Series B: Statistical Methodology 64(4), 583–639.

- Sun et al. (1999) Sun, D., R. K. Tsutakawa, and P. L. Speckman (1999). Posterior distribution of hierarchical models using CAR(1) distributions. Biometrika 86(2), 341–350.

- Taşpınar et al. (2021) Taşpınar, S., O. DoĞan, J. Chae, and A. K. Bera (2021). Bayesian inference in spatial stochastic volatility models: An application to house price returns in Chicago. Oxford Bulletin of Economics and Statistics 83(5), 1243–1272.

- Yang and Lee (2021) Yang, K. and L.-f. Lee (2021). Estimation of dynamic panel spatial vector autoregression: Stability and spatial multivariate cointegration. Journal of Econometrics 221(2), 337–367.

- Zhang and Yu (2018) Zhang, X. and J. Yu (2018). Spatial weights matrix selection and model averaging for spatial autoregressive models. Journal of Econometrics 203(1), 1–18.