Who Benefits from a Multi-Cloud Market? A Trading Networks Based Analysis

Abstract

In enterprise cloud computing, there is a big and increasing investment to move to multi-cloud computing, which allows enterprises to seamlessly utilize IT resources from multiple cloud providers, so as to take advantage of different cloud providers’ capabilities and costs. This investment raises several key questions: Will multi-cloud always be more beneficial to the cloud users? How will this impact the cloud providers? Is it possible to create a multi-cloud market that is beneficial to all participants?

In this work, we begin addressing these questions by using the game theoretic model of trading networks and formally compare between the single and multi-cloud markets. This comparison a) provides a sufficient condition under which the multi-cloud network can be considered more efficient than the single cloud one in the sense that a centralized coordinator having full information can impose an outcome that is strongly Pareto-dominant for all players and b) shows a surprising result that without centralized coordination, settings are possible in which even the cloud buyers’ utilities may decrease when moving from a single cloud to a multi-cloud network. As these two results emphasize the need for centralized coordination to ensure a Pareto-dominant outcome and as the aforementioned Pareto-dominant result requires truthful revelation of participant’s private information, we provide an automated mechanism design (AMD) approach, which, in the Bayesian setting, finds mechanisms which result in expectation in such Pareto-dominant outcomes, and in which truthful revelation of the parties’ private information is the dominant strategy. We also provide empirical analysis to show the validity of our AMD approach.

1 Introduction

In the enterprise cloud computing market, there is an increasing trend to move to multi-cloud computing, in which enterprises can seamlessly distribute their computational tasks among multiple cloud providers, so as to take advantage of the different capabilities and costs of these providers. Such a multi-cloud market intuitively seems to benefit the cloud users while being detrimental to existing large cloud providers. As most of today’s cloud resources are provided by such large providers, it will be difficult to realize the multi-cloud vision without their support. Therefore, in order to understand, from an economic standpoint, the benefits and pitfalls of the multi-cloud market, there is a need to formally analyze, exactly who, and under which conditions, will benefit or lose from moving to a multi-cloud market. In addition we would like to understand whether a multi-cloud market is possible that is beneficial to all participants.

To carry out this analysis requires formally modeling and comparing between the existing single cloud market and desired multi-cloud one. As cloud markets are two sided markets between the cloud users (or buyers) and the cloud providers, between which there are contracts, a model is required which captures the need for the buyers and providers to agree on the prices paid for the IT infrastructure. Therefore, rather then modeling this as a normal form game, which has been the approach taken in many previous applications of game theory to cloud computing, we model these markets as trading networks (Hatfield et al., 2013), which model the outcome of a game as a set of contracts, and in which the accepted solution concept is a stable outcome, which requires joint agreement between the parties on the set of preferred contracts (a formal definition of stable outcomes appear in the sequel). To the best of our knowledge, this is the first usage of trading networks in the context of cloud computing

Using the trading networks model, we carry out a comparative analysis of the two markets. Our first result formalizes the intuition that a multi-cloud market is more efficient than a single cloud one, by showing that there is a formal sufficient condition such that, whenever this condition holds, a centralized coordinator that has access to the parties’ private information can create an outcome that is strongly Pareto-dominant for all cloud users and providers. However, our analysis also shows the more surprising result that in the absence of such centralized coordination, not only are such Pareto-Dominant outcomes not guaranteed, but that there are cases in which even the cloud buyers utilities’ may decrease when moving to a multi-cloud setting.

The fact that cloud users’ utilities may decrease when moving to the multi-cloud market strengthens the need for a centralized market coordinator. However, the constructive proof used to create the Pareto-dominant multi-cloud outcome requires both cloud users and cloud providers to reveal their information technology (IT) infrastructure costs, which are typically proprietary information. Moreover (see Osogami, Wasserkrug, and Shamash (2023)), in trading network settings, parties are often incentivized to be untruthful about such costs, and even when adding a centralized coordinator, such that all contracts and payments go though that coordinator, it is impossible to design a priori even for simple trading networks a mechanism which is ex-post a) efficient, b) one in which the dominant strategy for all participants is to be truthful (formally called dominant strategy incentive compatible or DSIC), c) the coordinator’s utility from participating in the network is not negative (formally, weakly budget balanced or WBB) and d) that the utility of all parties is non-negative (formally, individually rational or IR - which is a special case of Pareto-dominance). Therefore, we build upon Automated Mechanism Design (AMD) work in Osogami, Wasserkrug, and Shamash (2023) to show how mechanisms can be created, for some distributions of cost functions, which are ex-post DSIC and efficient, ex-ante WBB, and Pareto-dominant in expectation.

To summarize our contributions: we model both the single cloud and multi cloud market using the trading network model, formally show that the multi-cloud market is more efficient given a centralized coordinator and that without such coordination, there are settings in which the cloud users’ utilities may decrease when moving to a multi-cloud environment. Furthermore, we provide an AMD approach which, for many IT cost distributions, results, in expectation, in a strongly Pareto-dominant market and in which truthful participation for all parties is the dominant strategy. Finally, we provide empirical analysis which demonstrates the validity of our AMD approach.

2 Related Work

The potential benefits of moving to the multi-cloud market, as well as the technical capabilities required for this move, appear in many works (Keahey et al., 2009; Jia et al., 2015). Kash et al. (2016) discuss at a high level the economics of multi-cloud for both buyers and providers. Chasins et al. (2022) provide a contemporary and comprehensive view on multi-cloud, called Sky Computing, and suggest implementing software components called brokers for the distribution across multiple clouds. This work also recognizes the possible opposition of cloud providers. However, none of the above works carry out a formal market analysis or design.

A large body of previous works exists on the application of game theory to cloud computing. This includes: pricing schemes for selling cloud services (Abhishek, Kash, and Key, 2012; Kash, Key, and Suksompong, 2019), truthful online scheduling (Babaioff et al., 2022), analysis of ad services and resulting network effects (Nair, Subramanian, and Wierman, 2018), spot pricing of cloud instances (Li et al., 2016), a game theoretic analysis of the benefits of cloud computing (Künsemöller and Karl, 2012) and a mean field analysis of cloud resource sharing (Hanif et al., 2016). However, none of these works have a formal analysis and comparison of the single and multi-cloud market, nor suggest any approach of moving from one market to another while increasing the utilities of all participants. Moreover, none of these works use trading networks to model the cloud settings.

Trading networks, the formal framework we use to analyze the two cloud markets, along with associated models, have been covered extensively in a large body of work (Ostrovsky, 2008; Hatfield and Kominers, 2011, 2012; Hatfield et al., 2013, 2015).

AMD (Conitzer and Sandholm, 2002; Sandholm, 2003) is a class of optimization and machine learning based approaches to create use case specific mechanisms in cases in which manual mechanism design face challenges. AMD approaches generate mechanisms for specific players’ types distributions, that satisfy desired properties such as DSIC, efficiency, IR and WBB. Most previous works on AMD such as Rahme, Jelassi, and Weinberg (2021); Curry and Reusche (2022); Duetting et al. (2019); Manisha, Jawahar, and Gujar (2018) focus on combinatorial auctions. A work which does address AMD in trading networks is Osogami, Wasserkrug, and Shamash (2023). We build upon this work to define an AMD approach to create a Pareto-dominant multi-cloud market.

3 Trading Networks

In this section, we briefly summarize the trading network model as presented in Hatfield et al. (2013) and the stable outcome solution concept.

A trading network is a tuple , where is a set of players (or firms), is a set of bi-lateral trades such that each has a buyer and a seller , and , where each is the value player associates with any set of trades. The set of trades defines a set of possible contracts , where is of the form , where and is the price paid by to for the trade . An outcome in a trading network is a set of feasible contracts where is feasible if it does not contain two contracts in which the same trade appears. The utility of for a set of contracts is defined by

| (1) |

where is the set of trades in , is the subset of contracts in in which is a seller and is the subset of contracts in in which is a buyer.

The standard solution concept in trading networks is the stable outcome. Similar to Nash Equlibria, a stable outcome is a state from which players do not wish to deviate. Stable outcomes are defined based on the notion of choice correspondence (Hatfield et al., 2013) which, for each agent and set of contracts , are the subsets of contracts in , that maximize ’s utility:

A stable outcome is then defined as:

Definition 3.1 (Stability (from Hatfield et al. (2013))).

An outcome is stable if it is:

-

1.

Individually rational: for all ;

-

2.

Unblocked: There does not exist a nonempty blocking set such that

-

(a)

, and

-

(b)

for every for every , we have , where is the set of trades in that involve as the buyer or seller.

-

(a)

Intuitively, this means that when presented with a stable outcome , one cannot propose a new set of contracts such that all the agents involved in the new contracts would strictly prefer forming all of them (and possible dropping some of existing contracts in ) to sticking with .

4 Modeling Cloud Computing

4.1 The Cloud Market

A cloud market has a set of cloud buyers which are the potential users of the cloud resources, and which we denote by , such that each cloud buyer has a set of computational workflows they need to run, where each workflow of buyer is composed of a set of tasks . An example of such a workflow is a machine learning workflow, which could be composed of a data extraction task and a machine learning task that uses deep neural networks. Each such task requires a set of resources. In this machine learning workflow, the data extraction task requires access to the database where the data resides, and the deep neural network machine learning task will require access to GPUs.

In a cloud market, there is also a set of cloud providers . Each provider has a set of computational resources such as storage, GPUs and software services, which can be provided to buyers to fulfill their tasks. In our model, for any buyer , we assume that each of the tasks of can be implemented either on computational resources provided by one of the providers , or on internal computational infrastructure owned and operated by . Buyers pay the providers for providers’ computational resources they use, and have costs associated with the internal computational resources. Formally, we will model the cost of a buyer for the internal computational resources for a subset of tasks by a function , and the cost of provider for providing set of computational resources for a subset of tasks by a function (these different functions encapsulate the cost and capabilities differences between providers). For simplicity of exposition, we assume that , , , i.e., the cost of not providing any resources for the providers or using any internal resources for the buyers is zero333In practice, cloud providers have infrastructure in place which results in costs, even if this infrastructure is not used. It is easy to incorporate such costs, for example, by ensuring that is negative for . However, for the remainder of this work, we ignore these costs and assume that , .. Finally, we assume that for each , there is a value for for running the tasks , such that .

To model both a single cloud and multi-cloud market, we define a trading network where:

-

•

The agents are the set 444While not detailed in this work, the trading networks model and our major results also cover more complex cloud markets such as ones including organizations that provide higher level cloud services to buyers on top of other cloud providers’ infrastructure (Anselmi et al. (2017) and Zheng et al. (2016)), i.e., organizations which are both buyers and sellers..

-

•

The set of possible trades is , i.e., there is a trade for each combination of provider, buyer, and subset of tasks for that specific buyer.

-

•

where , is such that where is the set of tasks in for which is a seller. I.e., is ’s cost for providing the resources required by all tasks appearing in the trades . Note that we assume that if cannot provide the resources for , then .

The above definitions are common for both single cloud and multi-cloud networks. The differences between the two settings is captured by the valuation function of the buyers as follows

-

•

In the single provider setting, the value of selecting resources from more than one provider is . Formally, if and such that for some task both and (we call this Condition 1), then .

-

•

In the multi-cloud setting, or in the single provider setting where Condition 1 does not hold, where . Note that is the cost for buyer of implementing internally the tasks that are not fulfilled by trades in .

Given the above, and an outcome defined by a set of contracts , we define the utility of each agent from according to Equation (1), i.e.:

-

•

For each buyer ,

-

•

For each provider , .

Comment: The above model assumes that a provider can provide the same infrastructure to different buyers at different prices. While this may not hold in the consumer market, it does apply in the enterprise market, where confidential contracts can be agreed between providers and buyers, based on, for example, volume discounts.

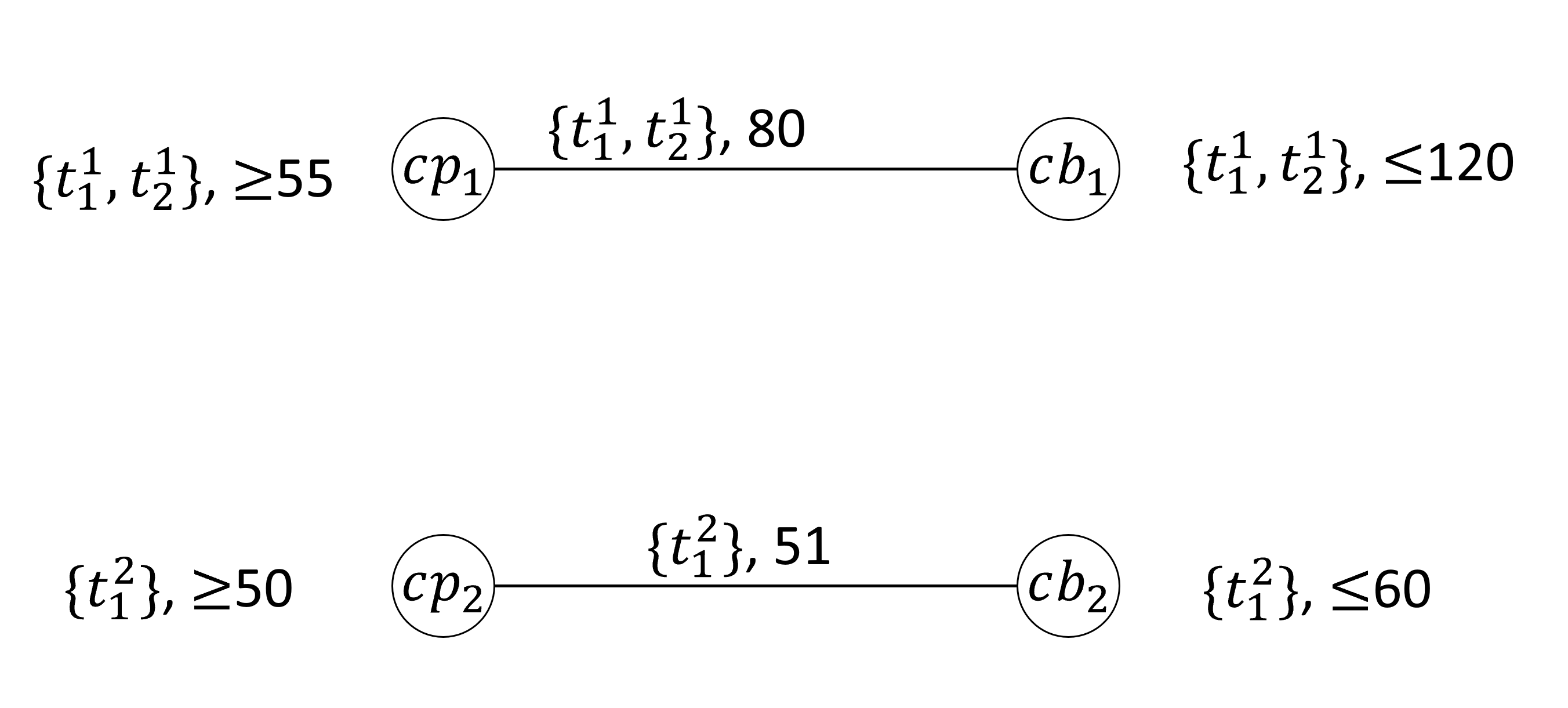

Example 1. describes a concrete example of a cloud trading network.

Example 1.

There are two cloud buyers, and two cloud providers . The buyers have the following tasks: , . ’s costs and values are: , and . ’s costs and values are: and . ’s costs are: and , i.e., can provide resources for and either or at a cost of 55, but not simultaneously for and . ’s cost is and is for any other nonempty subset of tasks, i.e., can provide resources for either task or but not both or any other tasks.

The set of trades are . A feasible contract set is the set consisting of a single contract , i.e., that uses ’s cloud resources for both its tasks for a price of 60, and only uses internal computational resources. For this set of contracts, and . As there are no contracts in in which or participate, we have that and .

In the remainder of this work, we will use the following notation: given a trading network in the single cloud setting, we will denote the corresponding network in the multi-cloud setting by , i.e. the trading network with the same buyers, providers and trades (which encapsulate the same set of tasks), with the difference in the value functions of the buyers between the two networks.

5 Comparing the two cloud markets

Modeling the respective cloud markets as trading networks allows us to formalize the intuition that the multi-cloud market is more efficient than the single cloud market. From the above model it is clear that, for every set of feasible contracts in the single cloud trading network , there is a feasible set of contracts in the corresponding multi-cloud trading network such that:

| (2) |

Indeed, this holds trivially for as, according to the respective definitions of and :

-

•

Every feasible set of contracts in is feasible in , i.e. (where is the set of all possible contracts in , and is the set of all possible contracts in ).

-

•

By definition of the value functions , , (where are the set of trades), and hence for every set of contracts , .

However, we can also show a stronger result as follows:

Theorem 5.1.

If

| (3) |

then for every set of feasible contracts in the single cloud trading network there is a set of trades and a set of payments , , such that

| (4) |

The significance of this theorem is the following: By definition of the value functions , for any set of trades the sum is directly proportional to the sum of the costs of the computational infrastructure for all buyers and providers. Therefore, when Equation (3) holds, it means that a set of trades can be found in the multi-cloud network in which the sum of all computational resource costs for all network participants is strictly lower than the sum of all costs for any set of trades in the corresponding single cloud network. What this theorem then states is that when the multi cloud network is more efficient in the sense of Equation (3), for any set of contracts in the single cloud setting, there can be found a set of trades in the corresponding multi-cloud setting with (possibly negative) payments , such that when the total payment is made to , ’s utility Pareto dominates , i.e., all parties can benefit from this higher efficiency of the multi cloud. In addition, as , the payments can be viewed as total payments between the cloud providers and cloud buyers, i.e., no additional payments need to be added from an external source. Such payments could be distributed, through, for example, a centralized coordinator, which collects all payments from the cloud buyers and providers and distributes all positive payments.

Proof Sketch of Theorem 5.1 (full proof appears in the technical appendix): a key observation is that in any trading networks, the sum of the valuations over a set of trades is equal to the sum of utilities over any set of contracts over these trades, i.e. , . Therefore, when Equation (3) holds, there is a positive difference between the maximum sum of utilities in the multi-cloud setting and the sum of the utilities for any contract set . Consequently, given a set of trades which maximizes the sum of valuations in the multi-cloud setting (which also maximizes the utilities), a centralized coordinator through which all payments flow can take this positive difference in the multi-cloud setting and distribute it so that each party gets a higher utility than in the single cloud one.

Thus, with a centralized coordinator, the multi-cloud network can be more beneficial to everyone in the sense of Theorem 5.1. The question is what would be the outcome of moving to a multi cloud market without such a centralized coordination (in which case we would expect the trading network to settle on a stable outcome as defined in Definition 3.1).

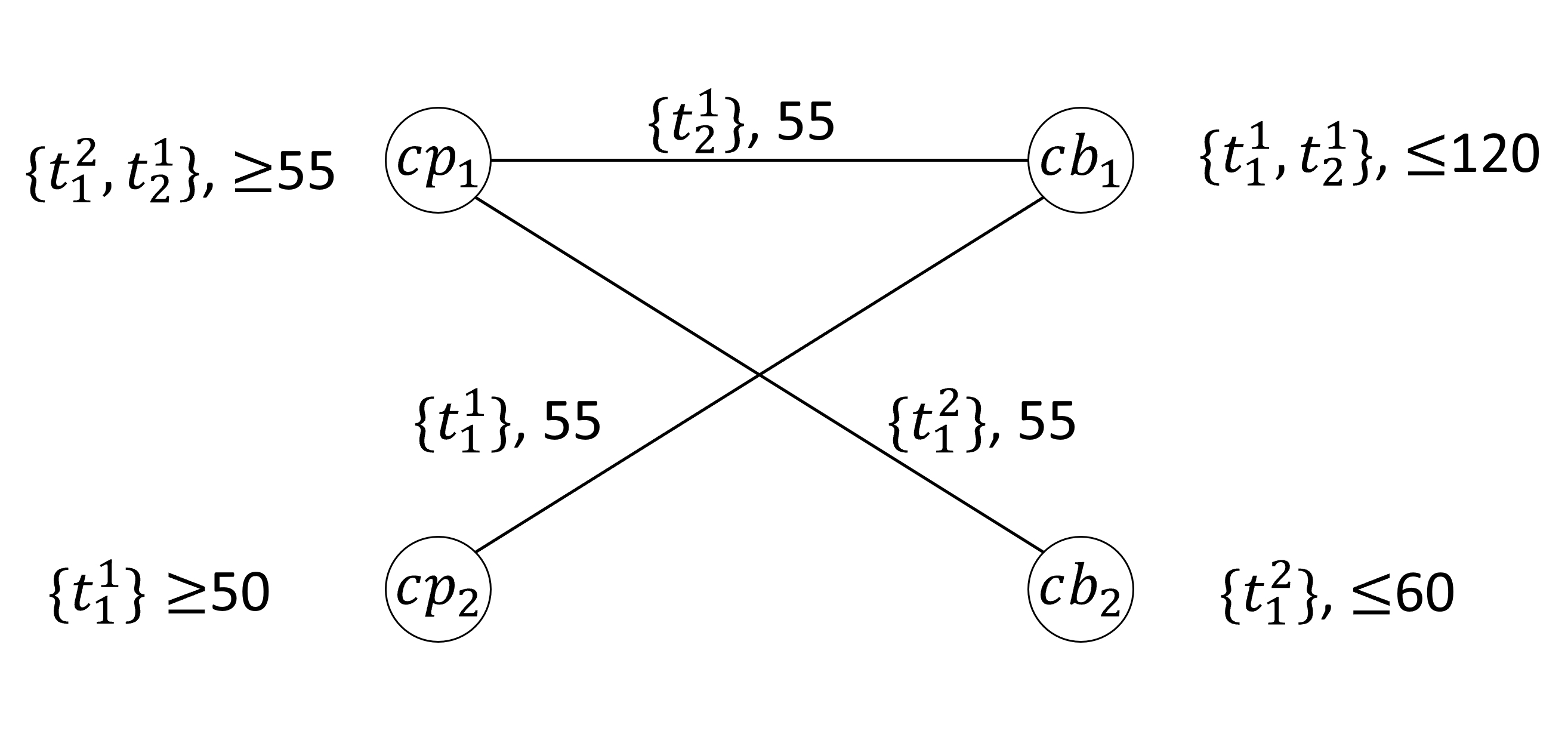

(a) Single cloud

(b) Multi-cloud

It turns out that without centralized coordination, the multi-cloud stable outcomes do not Pareto-dominate the single cloud stable outcomes even for the buyers. Consider Example 1: Figure (1) shows a stable outcome where pays to for and pays 51 for in the single cloud case (Figure (1a)). In Figure (1b) there is a multi cloud stable outcome where ’s tasks are split between and for a total cost of , and pays for it’s task, so that both buyers pay more than in the single cloud stable outcome (a proof showing that these outcomes are indeed stable appears in the technical appendix).

6 Pareto Dominant Multi-Cloud Mechanism

While the multi-cloud stable outcomes do not dominate the single cloud stable outcomes, whenever Equation (3) holds, it is possible to create a centralized multi-cloud market which strongly Pareto-dominates the single cloud one. However, the constructive proof used to obtain such a set of payments requires full knowledge of the valuation functions (which, in the case of the cloud market corresponds to the values and functions of the buyers, and the functions of the providers). As these quantities include the IT costs of the cloud providers and buyers, this information is expected to be highly proprietary and confidential. Moreover, in centralized mechanism settings, trading network participants are often incentivized not to be truthful about their valuations (see Osogami, Wasserkrug, and Shamash (2023)). We therefore describe how to create a centralized mechanism (which we will call a broker as in Keahey et al. (2009)) which is Pareto-dominant and in which truthful revelation of one’s costs is the dominant strategy.

Formally, we would like a mechanism that, given a set of contracts in a single cloud market and a set of valuation functions such that is the valuation function declared by , results in a set of trades and (possibly negative) payments from to the broker in the multi cloud market such that:

-

•

(5) i.e., is a set of trades for which the sum of utilities is maximized (as maximizing the sum of ’s maximizes the sum of utilities).

-

•

The mechanism is Dominant Strategy Incentive Compatible (DSIC),

(6) where and are the actual and reported valuation function of respectively and are the valuation functions reported by all players other than . This means that all players are incentivized to truthfully reveal their valuation functions irrespective of the behavior of the other players as a player never get a higher utility from revealing false valuations.

-

•

-Pareto-dominating the existing set of contracts, , in the single cloud setting,

(7) where are the actual valuation functions of all parties and . Namely, each participant’s utility increases by at least when moving from a single cloud to a multi cloud setting.

- •

However, as Osogami, Wasserkrug, and Shamash (2023) show, it is impossible to create such a mechanism that fulfills Equations (5)-(8) for all possible valuation functions even for a very simple trading network with a single provider and customer, and even for the special case when and in Equation (7) 555In this special case, the -Pareto-dominant requirement is identical to the traditional IR requirement.. Therefore, following the approach in Osogami, Wasserkrug, and Shamash (2023), we will address the Bayesian setting where there is a finite set of possible sets of valuations (also known as type spaces for the players and a common knowledge prior distribution666While the assumption of a common knowledge prior may seem to be overly restrictive, there are many public sources of information from which such a prior could be obtained, including the typical types of cloud workloads and their resource requirements (contributing to the buyers value), IT hardware, software and maintenance costs, and published prices by cloud providers, all contributing to the and cost functions. over these valuations).

In this Bayesian setting, and building upon the approach in Osogami, Wasserkrug, and Shamash (2023), we look for a mechanisms that finds a set of trades and a set of payments such that:

- •

-

•

Equation (8) is relaxed to:

(9) where denotes the expectation with respect to the distribution of ., i.e., the broker is profitable on average over the possible valuations.

We similarly relax Equation (7) to:

| (10) |

where denotes i.e., the expectation of ’s utility when conditioned on its true valuation . Equation (10) requires that the expectation of ’s utility when conditioned on its true valuation is at least as high as ’s utility in the single cloud setting777We condition on ’s true valuation as we assume that each participant will know what their true valuation is.. However, Equation (10) raises another issue that each agent is required to reveal their true utility . As we cannot assume that revealing the true single cloud valuation is a dominant strategy, we will assume that, rather, what is available to the broker is knowledge of the mechanism by which prices are determined in the single cloud market, such as accepted bargaining processes. Formally, we assume that is a mechanism known to the broker that, given a set of valuations , can calculate the utility for all in the single cloud trading trading network under . Assuming this, we relax Equation (7) to:

| (11) |

which specifies that, conditioned on the true valuation function , the expected utility in the multi-cloud case is higher than the expected utility in the single cloud case given mechanism .

To summarize, given a specific distribution over possible valuations (which are the providers’ and buyers’ cost), and a single cloud mechanism, , which determines the outcome for any specific set of valuations , we wish to design a mechanism specific to and that maximizes the sum of valuations, is DSIC, and satisfies Equations (9) and (11).

To construct such a mechanism, following again the approach outlined in Osogami, Wasserkrug, and Shamash (2023), we utilize an optimization problem formulation to find a Groves mechanism (Groves, 1973) that fulfills the above requirements. A Groves mechanism is any mechanism that, given a set of reported valuations , induces a set of trades and payments such that:

| (12) | |||

| (13) |

where does not depend on ’s valuation, . A Groves mechanism is always ex-post efficient and DSIC. Note that a first step towards implementing a Groves mechanism requires finding an optimal set of trades that satisfies Equation (12). We discuss how to find a set of trades in the sequel. Now, as Osogami, Wasserkrug, and Shamash (2023) show, given such an optimal set of trades, if , we can search for a set of functions that satisfy Equations (9) and (11) by solving the following optimization problem:

| (14) | ||||

| s.t. | (15) | |||

| (16) |

Here Constraint (15) enforces that the broker does not have to invest in participating, and Constraint (16) enforces Equation (11) when . To require that Equation (11) holds, we can therefore modify Constraint (16), to the following:

| (17) |

To summarize, given as input a mechanism , a set of cloud buyers , a set of cloud providers and a set of tasks for each , the following steps are carried out to find a desired mechanism:

-

1.

A distribution over possible sets of valuation functions (defined by , ) e.g. based on publicly available information).

-

2.

For each valuation function , an optimal set of trades, is calculated.

-

3.

The optimization problem defined by Equations (14), (15) and (17) is solved, using appropriate values 888The specified optimization problem objective minimizes the payments from the parties in to the broker, thereby distributing as much value as possible between the participants. Alternatively, we can set the objective to maximize the broker’s utility..

6.1 Finding an optimal set of trades

Implementing our AMD approach requires finding an optimal set of trades defined by Equation (5). Such a set of trades can be found by solving the 0-1 integer linear programming problem defined by Equations (18)-(20) 999For trading networks which are fully substitutable more efficient algorithms exist for finding an optimal set of trades. (see, e.g., Candogan, Epitropou, and Vohra (2021)). However, a multi-cloud trading network is not necessarily fully substitutable (see technical appendix)..

| (18) | ||||

| s.t. | (19) | |||

| (20) |

where indicates that the set of trades is selected, and .

Note that this is an integer program with a large number of variables. Since every can have a trade for every subset of , and each such trade can potentially have each as a seller, we have . Therefore, the number of variables as defined above is . Recall, however, that the valuation functions for is a function only of the set of tasks assigned to each party. Therefore, all cases in which the tasks are partitioned identically between the parties result in the same value for all valuations. Due to this, we can restrict the search for an optimal set of trades over subsets of trades where each partitions their tasks across the provider and itself. For each , the number of such possible partitions is where is the 2nd Stirling number. Therefore, multiplying this across the buyers, gives us a total of subsets of trades (which we denote by ), such that at least one such subset is optimal. This results in an optimization problem with variables, which is a much smaller number of variables:

| (21) | ||||

| s.t. | (22) | |||

| (23) |

where is one of the partitions of tasks.

6.2 Testing the validity of the AMD approach

To demonstrate that our approach can indeed find an -Pareto-dominating multi-cloud setting in many networks, we tried it out on many instances of networks, so as to seek, for each instance, a setting with the desired properties101010While we have open sourced the code, we have not included the link here so as to maintain anonymity. We will include the link in the final version.. In all network instances, we consider a network where a single cloud buyer (player 0) has two tasks (task 0 and 1) to be processed, and there are three providers (player 1, 2, and 3) who can process those tasks. The network instances differed in the possible set of valuations, , as described below.

To calculate the utility in the single cloud case, we assume that results in the two tasks being covered by the provider who has the minimum total cost (when multiple providers have the minimal total cost, we assume that the provider with the smallest index process the two tasks). The buyer (player 0) then makes payment to the provider who processes those tasks. The utility of the buyer is then , where is the amount of payment. The utility of the provider who processes the two tasks is , where is the total cost of processing the two tasks. The utilities of the other providers are 0.

In the multiple provider case, we compute the mechanism that guarantees all of the desired properties by implementing and solving the linear program (LP) specified by Equations (14), (15) and (17) (we solved the LP by using the CPLEX® optimization engine).

In our experiments, the possible valuation functions, , are defined as follows: We assume that player 1 and player 2 can have one of multiple types and study two type spaces: and . Let , where and can take any of the four values and are the respective costs of players 1 and 2. Let , where and (the respective costs of players 1 and 2) can take one of the two values . For example, type means that the resource cost for task 0 is Low, and for task 1 is High; type means that the cost is High for both tasks; other types are defined analogously. We assume that the types of player 0 (the buyer) and player 3 (the third provider) are fixed. Let be the type of player 0, who has Very high cost of computational resources for either task, and let be the type of player 3, who has Medium cost for either task. Let the low cost be and the very high cost be . We consider all of the combinations of the medium cost and high cost such that and .

We carried out the above experiment for a variety of random instances and studied how often we can find desirable mechanisms (indicated by having a feasible solution to the optimization problem). We consider the amount of payment in the single provider case to be in . For each of the 360 combinations of , we generate 100 prior distributions over types uniformly at random, resulting in 36,000 random instances for each of the two type spaces, and . Table 1 summarizes the results of the experiment. As shown in Table 1, for , our method has found a desirable mechanism for all of the 36,000 random instances. For , while we found that the desired Grove mechanisms do not always exist, our approach found desirable mechanisms for a slim majority (52%) of the instances. This shows that overall, in most cases of our generated networks, a desirable mechanism can be found.

| Type space | ||

|---|---|---|

| % feasible instances | 52 | 100 |

7 Summary and Future Work

Using the trading networks model, we have analyzed and compared between the single cloud and multi-cloud markets. Our model and analysis showed that the multi-cloud market is more efficient than the single cloud one, provided a characterization of when the multi-cloud market can be made strictly more efficient, and showed that without centralized coordinators, stable outcomes for the multi-cloud market do not Pareto-dominate the single cloud ones, even for the buyers. Finally, we have provided an AMD based approach for creating a multi-cloud market which is strongly Pareto-dominant in expectation for all participants and in which the dominant strategy is for each party to truthfully reveal their private information. We have also provided an empirical analysis, showing that for many cases, such a Pareto-dominant market can indeed be found by our method. To the best of our knowledge, ours is the first work to provide a game theoretic comparison of the two cloud markets and an approach for designing a desired multi-cloud market.

An important direction for future work is enhancing the AMD approach to enable finding desired mechanisms for more instances, by, for example, weakening the DSIC requirement to Bayesian Nash incentive compatibility. Another important enhancement is to increase the computational efficiency of the AMD approach, possibly by not requiring efficiency and focusing on Pareto-dominance.

References

- Abhishek, Kash, and Key (2012) Abhishek, V.; Kash, I. A.; and Key, P. 2012. Fixed and market pricing for cloud services. In 2012 Proceedings IEEE INFOCOM Workshops, 157–162.

- Anselmi et al. (2017) Anselmi, J.; Ardagna, D.; Lui, J. C. S.; Wierman, A.; Xu, Y.; and Yang, Z. 2017. The Economics of the Cloud. ACM Trans. Model. Perform. Eval. Comput. Syst., 2(4).

- Babaioff et al. (2022) Babaioff, M.; Lempel, R.; Lucier, B.; Menache, I.; Slivkins, A.; and Wong, S. C.-w. 2022. Truthful Online Scheduling of Cloud Workloads under Uncertainty. In Proceedings of the ACM Web Conference 2022, WWW ’22, 151–161. New York, NY, USA: Association for Computing Machinery. ISBN 9781450390965.

- Candogan, Epitropou, and Vohra (2021) Candogan, O.; Epitropou, M.; and Vohra, R. V. 2021. Competitive Equilibrium and Trading Networks: A Network Flow Approach. Operations Research, 69(1): 114–147.

- Chasins et al. (2022) Chasins, S.; Cheung, A.; Crooks, N.; Ghodsi, A.; Goldberg, K.; Gonzalez, J. E.; Hellerstein, J. M.; Jordan, M. I.; Joseph, A. D.; Mahoney, M. W.; Parameswaran, A.; Patterson, D.; Popa, R. A.; Sen, K.; Shenker, S.; Song, D.; and Stoica, I. 2022. The Sky Above The Clouds.

- Conitzer and Sandholm (2002) Conitzer, V.; and Sandholm, T. 2002. Complexity of Mechanism Design. In Proceedings of the Eighteenth Conference on Uncertainty in Artificial Intelligence, UAI’02, 103–110. San Francisco, CA, USA: Morgan Kaufmann Publishers Inc. ISBN 1558608974.

- Curry and Reusche (2022) Curry, M. J.; and Reusche, D. 2022. “Auction Learning as a Two Player Game”: GANs (?) for Mechanism Design. In ICLR Blog Track. Https://iclr-blog-track.github.io/2022/03/25/two-player-auction-learning/.

- Duetting et al. (2019) Duetting, P.; Feng, Z.; Narasimhan, H.; Parkes, D.; and Ravindranath, S. S. 2019. Optimal Auctions through Deep Learning. In Chaudhuri, K.; and Salakhutdinov, R., eds., Proceedings of the 36th International Conference on Machine Learning, volume 97 of Proceedings of Machine Learning Research, 1706–1715. PMLR.

- Groves (1973) Groves, T. 1973. Incentives in Teams. Econometrica, 41(4): 617–631.

- Hanif et al. (2016) Hanif, A. F.; Tembine, H.; Assaad, M.; and Zeghlache, D. 2016. Mean-Field Games for Resource Sharing in Cloud-Based Networks. IEEE/ACM Transactions on Networking, 24(1): 624–637.

- Hatfield and Kominers (2011) Hatfield, J. W.; and Kominers, S. D. 2011. Stability and competitive equilibrium in matching markets with transfers. ACM SIGecom Exchanges, 10(3): 29–34.

- Hatfield and Kominers (2012) Hatfield, J. W.; and Kominers, S. D. 2012. Matching in networks with bilateral contracts. American Economic Journal: Microeconomics, 4(1): 176–208.

- Hatfield et al. (2013) Hatfield, J. W.; Kominers, S. D.; Nichifor, A.; Ostrovsky, M.; and Westkamp, A. 2013. Stability and competitive equilibrium in trading networks. Journal of Political Economy, 121(5): 966–1005.

- Hatfield et al. (2015) Hatfield, J. W.; Kominers, S. D.; Nichifor, A.; Ostrovsky, M.; and Westkamp, A. 2015. Chain stability in trading networks. Available at SSRN 3180740.

- Jia et al. (2015) Jia, Q.; Shen, Z.; Song, W.; Van Renesse, R.; and Weatherspoon, H. 2015. Supercloud: Opportunities and challenges. ACM SIGOPS Operating Systems Review, 49(1): 137–141.

- Kash et al. (2016) Kash, I.; Jia, Q.; Shen, Z.; Song, W.; van Renesse, R.; and Weatherspoon, H. 2016. Economics of a Supercloud. In Proceedings of the 3rd Workshop on CrossCloud Infrastructures & Platforms, CrossCloud ’16. New York, NY, USA: Association for Computing Machinery. ISBN 9781450342940.

- Kash, Key, and Suksompong (2019) Kash, I. A.; Key, P.; and Suksompong, W. 2019. Simple Pricing Schemes for the Cloud. ACM Trans. Econ. Comput., 7(2).

- Keahey et al. (2009) Keahey, K.; Tsugawa, M.; Matsunaga, A.; and Fortes, J. 2009. Sky computing. IEEE Internet Computing, 13(5): 43–51.

- Künsemöller and Karl (2012) Künsemöller, J.; and Karl, H. 2012. A Game-Theoretical Approach to the Benefits of Cloud Computing. In Vanmechelen, K.; Altmann, J.; and Rana, O. F., eds., Economics of Grids, Clouds, Systems, and Services, 148–160. Berlin, Heidelberg: Springer Berlin Heidelberg. ISBN 978-3-642-28675-9.

- Li et al. (2016) Li, Z.; Zhang, H.; O’Brien, L.; Jiang, S.; Zhou, Y.; Kihl, M.; and Ranjan, R. 2016. Spot pricing in the Cloud ecosystem: A comparative investigation. Journal of Systems and Software, 114: 1–19.

- Manisha, Jawahar, and Gujar (2018) Manisha, P.; Jawahar, C. V.; and Gujar, S. 2018. Learning Optimal Redistribution Mechanisms Through Neural Networks. In Proceedings of the 17th International Conference on Autonomous Agents and MultiAgent Systems, 345–353.

- Nair, Subramanian, and Wierman (2018) Nair, J.; Subramanian, V.; and Wierman, A. 2018. Provisioning of ad-supported cloud services: The role of competition. Performance Evaluation, 120: 36–48.

- Osogami, Wasserkrug, and Shamash (2023) Osogami, T.; Wasserkrug, S.; and Shamash, E. S. 2023. Learning Efficient Truthful Mechanisms for Trading Networks. In Elkind, E., ed., Proceedings of the Thirty-Second International Joint Conference on Artificial Intelligence, IJCAI-23, 2862–2869. International Joint Conferences on Artificial Intelligence Organization. Main Track.

- Ostrovsky (2008) Ostrovsky, M. 2008. Stability in supply chain networks. American Economic Review, 98(3): 897–923.

- Rahme, Jelassi, and Weinberg (2021) Rahme, J.; Jelassi, S.; and Weinberg, S. M. 2021. Auction Learning as a Two-Player Game. In International Conference on Learning Representations.

- Sandholm (2003) Sandholm, T. 2003. Automated Mechanism Design: A New Application Area for Search Algorithms. In Proceedings of the 9th International Conference on Principles and Practice of Constraint Programming, CP’03, 19–36. Berlin, Heidelberg: Springer-Verlag. ISBN 9783540202028.

- Zheng et al. (2016) Zheng, L.; Joe-Wong, C.; Brinton, C. G.; Tan, C. W.; Ha, S.; and Chiang, M. 2016. On the Viability of a Cloud Virtual Service Provider. SIGMETRICS Perform. Eval. Rev., 44(1): 235–248.

Appendix A Proof of Theorem 5.1

A key observation is that in any trading network , for all (with being the set of all possible contracts), we have that:

| (24) |

This is as all payments between the parties cancel each other out. Now let

| (25) |

Then, for any feasible contracts , we have

| (26) | ||||

where the strict inequality follows from the assumption of the theorem.

Appendix B The outcomes in Figure (1) are stable

Figure (1a) is stable as:

-

•

will not be willing to pay more than to for .

-

•

will not be willing to accept or less, as doing so will requires to pay more then for so that gets a higher utility and strictly prefers these contracts.

-

•

However, for to have the same utility, will need to pay less than for , which will not be willing to accept, as this reduces ’s current utility.

Therefore, there are no sets of contracts strictly preferred by all parties involved.

Figure (1b) is stable as neither nor will agree to a set of contracts in which they earn less, and neither buyer will be willing to pay more than they currently do.

Appendix C The Multi-Cloud Trading Network is not Fully Substitutable

Definition C.1 (MFS from Definition 3 of (Hatfield et al., 2013)).

The preferences of agent are matching-theory fully subsitutable (MFS) if:

-

1.

for all sets of contracts such that and , and for each , there exists a set such that and ;

-

2.

for all sets of contract such that and , and for each , there exists a set such that and

Now consider the network with a single cloud buyer and a single cloud provider such that , m. This results in , , .

Now consider the two contract sets:

and

Therefore and .

However, and so but , so , which is a contradiction of 1 above

Appendix D Experimental Details

All of the experiments were run on a cloud instance with one CPU core with 4 GB memory. For each of the 360 configurations of , the run on 100 random instances was completed within one second, where the -th random instance was generated with random seed for .

Table 1 in the main paper shows that 52 percent of the instances are feasible when the type space is . Here, we investigate what instances tend to be feasible. Figure 2 shows the fraction of feasible instances against the medium cost, , when the type space is . Note that, for each value of , there are multiple instances with varying values of the high cost, , and the amount of payment, . Nevertheless, each value of has a single value of the fraction of feasible instances. This means that the value of determines the fraction of feasible instances regardless of the values of and in the settings under consideration. Overall, the instances tend to be more feasible when is high.