Trimmed Mean Group Estimation of Average Treatment Effects in Ultra Short Panels under Correlated Heterogeneity††thanks: We are grateful to Cheng Hsiao, Ron Smith and Hayun Song for helpful comments and discussions. The research on this paper was completed when Liying Yang was a Ph.D. student at the Department of Economics, University of Southern California.

Abstract

Under correlated heterogeneity, the commonly used two-way fixed effects estimator is biased and can lead to misleading inference. This paper proposes a new trimmed mean group (TMG) estimator which is consistent at the irregular rate of even if the time dimension of the panel is as small as the number of its regressors. Extensions to panels with time effects are provided, and a Hausman-type test of correlated heterogeneity is proposed. Small sample properties of the TMG estimator (with and without time effects) are investigated by Monte Carlo experiments and shown to be satisfactory and perform better than other trimmed estimators proposed in the literature. The proposed test of correlated heterogeneity is also shown to have the correct size and satisfactory power. The utility of the TMG approach is illustrated with an empirical application.

Keywords: Correlated heterogeneity, irregular estimators, two-way fixed effects, FE-TE, tests of correlated heterogeneity, calorie demand

JEL Classification: C21, C23

1 Introduction

Fixed effects estimation of average treatment effects has been predominantly utilized for program and policy evaluation. For static panel data models where slope heterogeneity is uncorrelated with treatment effects, standard fixed and time effects (FE-TE) estimators are consistent and if used in conjunction with robust standard errors lead to valid inference in short (time dimension) panels when the number of cross sections () is sufficiently large. However, when the slope heterogeneity is correlated with the treatment and/or control variables the FE-TE estimators (also known as two-way fixed effects) become inconsistent even if both and .111The concept of the correlated random coefficient model is due to Heckman and Vytlacil (1998). Wooldridge (2005) shows that FE-TE estimators continue to be consistent if slope heterogeneity is mean-independent of all the de-trended covariates. See also condition (2.19) given below. Such correlated heterogeneity arises endogenously in the case of dynamic panel data models considered by Pesaran and Smith (1995) even if the slope heterogeneity itself is purely random.

In the case of static panels, correlated heterogeneity could arise when treatment effects are correlated with the treatment itself and/or the control variables. For example, in estimation of returns to education, the choice of educational level is likely to be correlated with expected returns to education. In a review of active policies in labor markets, Crépon and Van Den Berg (2016) emphasize that when estimating the average impacts on workers’ productivity and earnings, correlated heterogeneity should be accounted for, to better encourage enrollment in training programs. Banerjee et al. (2015) also consider identification and estimation of heterogeneous treatment effects in the case of micro-credit evaluation programs, and Bastagli et al. (2019) consider similar issues in studies of anti-poverty cash transfer programs.222Reviews of recent advances in econometric methods for heterogeneous treatment effects of binary variables can be found in Athey and Imbens (2017) and Abadie and Cattaneo (2018). In a recent survey de Chaisemartin and D’Haultfoeuille (2023) highlight the importance of allowing for correlated heterogeneity and draw attention to the misleading inferences that can result when FE-TE estimates are used in the case of heterogeneous policy effects.

Pesaran and Smith (1995) proposed mean group (MG) estimation for dynamic heterogeneous panel data models, where by construction represent examples of correlated heterogeneity. It was later shown that for panels with strictly exogenous regressors, the MG estimator is -consistent in the presence of correlated heterogeneity even if is fixed as , so long as is sufficiently large such that at least second order moment of the MG estimator exists. However, when is ultra short such that is close to the number of regressors, , the MG estimator could fail. As shown by Chamberlain (1992) one needs to be strictly larger than for regular identification of average effects under correlated heterogeneity.333An unknown parameter, , is said to be regularly identified if there exists an estimator that converges to in probability at the rate of . Any estimator that converges to its true value at a rate slower than is said to be irregularly identified. Chamberlain (1992) calculated efficiency bounds for models defined by conditional moment restrictions with a nonparametric component, and proposed a -consistent Generalized Method of Moments (GMM) estimator for the mean of correlated random coefficients in panel data models provided that certain rank and moment conditions hold.444The GMM estimator proposed by Chamberlain (1992) turns out to be the same as the MG estimator. See equation (4.8b) in Chamberlain (1992). See also Bonhomme (2012) and Arellano and Bonhomme (2012). Assuming the errors follow autoregressive moving average processes, Arellano and Bonhomme (2012) provide rank conditions under which the GMM estimators they propose for variances and densities of correlated random coefficients can be regularly identified.

The above papers adopt the GMM approach to address identification and estimation of average treatment effects. Some researchers consider other regular estimators by imposing additional restrictions on the correlation between heterogeneous coefficients and regressors. Wooldridge (2005) proposes an alternative estimator for models with nonlinear individual-specific unobserved effects, where he imposes a condition that random coefficients are mean independent of the idiosyncratic deviations in regressors. To estimate the average effects of binary treatment variables for the sub-population with no time variations in treatment status, Verdier (2020) explicitly models selection into treatment. Assuming random coefficients are independent of regressors, Lee and Sul (2022) apply a double-sided trimming scheme to the MG estimators for static panels with common correlated effects developed by Chudik and Pesaran (2015), so as to eliminate effects of outlying individual estimates with too small or too large regressor sample variances.

This paper considers identification and estimation of average treatment effects in ultra short linear panel data models with continuous covariates, where could be as small as . Building on the pioneering work of Chamberlain (1992), Graham and Powell (2012) focus on panels with , where identification issues of time effects and the mean coefficients arise especially when there are insufficient within-individual variations for some regressors. They derive an irregular estimator of the mean coefficients by excluding individual estimates from the estimation of the average treatment effects if the sample variance of regressor in question is smaller than a given threshold.555The trimming idea of Graham and Powell has also been used recently by de Chaisemartin et al. (2023) for identification of the average slopes of switchers’ potential outcomes with many “near stayers”. Exploiting the sub-population of “stayers”with no time variations in regressors, they then propose an estimator of time effects.666Graham and Powell (2012) establish identification results based on moment equations conditional on the sub-population of “stayers”, namely individuals with no time variations in their realized covariates. But in estimation, a sub-sample of “near stayers”is used instead. More recently Sasaki and Ura (2021) propose an alternative procedure to deal with the possibility of many stayers and/or slow movers in the panel. They consider various distributions of within-variations and use local polynomial regressions to provide robust inference.

In this paper, we first derive asymptotic properties of MG and FE estimators in large and short heterogeneous static panel data models, and provide sufficient conditions under which MG and FE estimators are regular, in the sense that they are -consistent. In cases where these conditions are not met, we propose a new trimmed mean group (TMG) estimator which makes use of additional information on trimmed units not exploited by Graham and Powell (2012). In effect, information on all units (whether subject to trimming or not) are included in the computation of the average treatment effect. Following the literature, the decision on whether a unit is subject to trimming is made with respect to the determinant of the sample covariance matrix of the regressors, denoted by , and the individual estimates for unit are trimmed uniformly if , where , and measures the rate of trade-off between bias and variance of TMG. Our asymptotic derivations suggest setting close to . Also noting that is scale free, our choice of trimming threshold, , does not involve any other tuning parameters.

We also consider heterogeneous panels with time effects and develop two new estimators of the average treatment effects in two-way fixed effects regressions, which we denote by TMG-TE and TMG-C, corresponding to cases where and , respectively. The TMG-TE estimator is based on joint estimation of time and average effects, whilst the TMG-C estimator follows Chamberlain (1992) and eliminates the time effects before estimating the average treatments, which is possible only if . We derive the asymptotic distributions of TMG-TE and TMG-C estimators under fairly general assumptions but require the identifying condition that the non-zero dependence between heterogeneous slope coefficients and the regressors is time-invariant. Note that this condition trivially holds in the case of FE-TE estimators whose validity requires zero dependence between the slope coefficients and the regressors.

As noted above the presence of heterogeneity by itself does not invalidate the use of the FE-TE estimator which continues to have the regular convergence rate of . The problem arises when slope heterogeneity is correlated with the covariates, such as the treatment variable. It is, therefore, important that before using the FE-TE estimator the assumption of uncorrelated heterogeneity is tested. To this end, we also propose Hausman-type tests of correlated heterogeneity by comparing the FE and FE-TE estimators with the associated TMG estimators, and derive their asymptotic distributions under fairly general conditions. The earlier Hausman tests of slope homogeneity developed by Pesaran et al. (1996) and Pesaran and Yamagata (2008) are based on the difference between FE and MG estimators and do not apply when is ultra short.

We also carry out an extensive set of Monte Carlo (MC) simulations to investigate the small sample properties of the TMG, TMG-TE and TMG-C estimators and how they compare with other estimators, including the trimmed estimators proposed by Graham and Powell (GP) and Sasaki and Ura (SU). The MC evidence on the size and empirical power of the Hausman-type tests of correlated heterogeneity in panel data models without and with time effects is provided, and the sensitivity of estimation results to the choice of the trimming threshold parameter, , is also investigated. The MC and theoretical results of the paper are all in agreement. The TMG and TMG-TE estimators not only have the correct size but also achieve better finite sample properties compared with other trimmed estimators across a number of experiments with different data generating processes, allowing for heteroskedasticity (random and correlated), error serial correlations, and regressors with heterogeneous dynamics and interactive effects. The simulation results also confirm that the Hausman-type tests based on the difference between FE (FE-TE) and TMG (TMG-TE) estimators have the correct size and power against the alternative of correlated heterogeneity.

As an empirical illustration, we re-visit the example considered by GP who provide estimates of the average effect of household expenditures on calorie demand using a balanced panel of households in poor rural communities in Nicaragua over the years 2001–2002 and 2000–2002 . Comparing the FE and TMG estimates, for panels with and without time effects, we find that the Hausman tests reject the null of uncorrelated heterogeneity, thus shedding doubt on the use of FE or FE-TE estimates for this application. For the ultra short panel with , the FE and TMG estimates of the average treatment effects are and . The figures in brackets are standard errors. Given the result of the Hausman test, most likely the FE estimate is biased upward, with a much lower standard error. These results do not change if we allow for time effects. Turning to the other trimmed estimators, the GP and SU estimates, and , respectively, are wide apart, and both have larger standard errors as compared to the TMG estimate. Again these estimates are not much affected by allowing for time effects. But once we consider the panel with the TMG and GP estimates (with or without time effects) become very similar, although the TMG estimates continue to be more precisely estimated. The gap between FE and TMG estimates also becomes closer but remains statistically highly significant.

The rest of the paper is organized as follows. Section 2 sets out the heterogeneous panel data model and investigates the asymptotic properties of the MG and FE estimators. Section 3 considers ultra short panels and discusses the need for trimming as suggested by GP. The proposed TMG estimator is introduced in Section 4, and its asymptotic properties are established in Section 5. Section 6 extends the TMG estimation to ultra short panel data models with time effects, distinguishing between cases where and . Section 7 sets out the Hausman-type test of correlated heterogeneous slope coefficients. Section 8 describes the Monte Carlo experiments and reports the simulation results. Section 9 presents the empirical illustration. Section 10 concludes. The online supplement develops the test of correlated heterogeneity for panels with time effects, and provides supplementary information on Monte Carlo designs and additional Monte Carlo evidence.

2 Heterogeneous linear panel data models

Consider the panel data model where the outcome variable for unit at time is explained linearly in terms of the vector of covariates

| (2.1) |

where is a vector of unknown unit-specific coefficients and is the error terms. Stacking by time we have

| (2.2) |

where , , and . The parameter of interest is the vector of average treatment effects, , defined by

| (2.3) |

When , can be estimated by the mean group estimator, , computed as a simple average of the least squares estimates of , namely (see Pesaran and Smith (1995))

| (2.4) |

where

| (2.5) |

To investigate the asymptotic properties of the MG estimator when is short and , we make the following assumptions:

Assumption 1 (Errors)

Conditional on , (a) the errors, , in (2.1) are cross-sectionally independent, (b) , for and (c) , where is a bounded matrix with .

Assumption 2 (Regression coefficients)

The vector of coefficients, , is allowed to depend on the distribution of with . This dependence could be (a) deterministic with fixed and bounded or (b) stochastic, with jointly determined with .

-

(a)

are deterministic with for , such that , with

-

(b)

are independent draws from a distribution with and bounded variances for , where , and .

Remark 1

Under Assumption 1, the vector of covariates, , for are strictly exogenous, but it allows the conditional variance of to depend on , and for the errors, , to be serially (over time ) correlated.

Remark 2

Part (c) of Assumption 1 rules out the possibility of unbounded random variations in , but can be relaxed if instead it is assumed that , with higher order moment conditions on and .

Remark 3

2.1 Properties of mean group estimator in short T panels

Substituting (2.2) in (2.5) we have

| (2.6) |

where

| (2.7) |

and . Averaging both sides of (2.6) over , we have

| (2.8) |

where

| (2.9) |

Then under Assumption 1, , and hence . Then using (2.8) namely is an unbiased estimator of irrespective of the possible dependence of on . However, the MG estimator is likely to have a large variance when is too small. This arises, for example, when the variance of does not exist or is very large. The conditions under which converges to at the regular rate are given in the following proposition:

Proposition 1 (Sufficient conditions for -consistency of )

For a proof see A.2.1 in the Appendix.

Example 1

In the simple case where , , and . Suppose for and with , then the individual OLS estimator of the slope coefficient, has first and second order moments if and where , , and . In the case where are Gaussian distributed with mean zeros and a finite variance, , it follows that , where is a Chi-squared variable with degrees of freedom. Hence, exists if or if . For panels with , the MG estimator would be irregular when first and/or second order moments of some individual estimates do not exist.

2.2 A comparison of MG and FE estimators

Consider a panel data model with individual fixed effects, , and heterogeneous slope coefficients, ,

| (2.11) |

where is a vector of regressors ). In matrix notations

| (2.12) |

where . The FE and MG estimators of are given by

| (2.13) |

and

| (2.14) |

where In this setting the parameter of interest is given by . One of the main advantages of the estimator is its robustness to the dependence between and the regressors. is also well defined even if so long as the following standard assumption is met:

Assumption 3 (Data pooling assumption)

Let , where

For there exists such that for all , is positive definite,

| (2.15) |

and

| (2.16) |

2.2.1 Conditions for consistency of FE estimator

Under the heterogeneous specification (2.11) and noting that , we have

| (2.17) |

Then by Assumption 1, , and hence . Under Assumptions 1, 2 and 3,

where , and is a consistent estimator of the average treatment effect, , if

| (2.18) |

This condition is clearly met if

| (2.19) |

for all , and has been already derived by Wooldridge (2005).777See equation (12) on page 387 of Wooldridge (2005). But it is too restrictive, since it is possible for the average condition in (2.18) to hold even though condition (2.19) is violated for some units as . What is required is that a sufficiently large number of units satisfy the condition (2.19). Specifically, denote the number of units that do not satisfy (2.19) by and note that , and condition (2.18) is met if . But for to be a regular -consistent estimator of a much more restrictive condition on is required. Using (2.17) note that

and if . The bias term can be written as

The first term tends to zero in probability if are weakly cross-correlated over . For the second term to tend to zero we must have , or if .

Proposition 2 (Condition for consistency of the FE estimator)

Suppose that for and are generated by the heterogeneous panel data model (2.12), and Assumptions 1, 2 and 3 hold. Then the FE estimator given by (2.13) is -consistent if

| (2.20) |

and this condition is met if , with defined by , where denotes the number of units that are subject to correlated heterogeneity.

2.2.2 Relative efficiency of FE and MG estimators

Suppose now that conditions (2.20) and (2.10) hold and both FE and MG estimators are -consistent. The choice between the two estimators will then depend on their relative efficiency, which we measure in terms of their asymptotic covariances, given by

and

where , , , and as before , and Hence

| (2.21) |

where

| (2.22) |

and

| (2.23) |

and capture the effects of two different types of heterogeneity, namely slope heterogeneity and regressors/errors heterogeneity. The superiority of the FE over MG is readily established when the slope coefficients and error variances are homogeneous across , and the errors are serially uncorrelated, namely if and for all . In this case , and we have

which is the difference between the harmonic mean of and the inverse of its arithmetic mean, which is a non-negative definite matrix.888For a proof see the Appendix to Pesaran et al. (1996). However, this result may be reversed when we allow for heterogeneous , and/or if . The following proposition summarizes the results of the comparison between the FE and MG estimators.

Proposition 3 (Relative efficiency of MG and FE estimators)

Suppose that for

and are generated by the heterogeneous panel data model (2.12), and Assumptions 1, 2 and 3 hold, and the uncorrelated heterogeneity condition (2.20) is met. Then where and are given by (2.22) and (2.23), respectively. is a non-positive definite matrix, and the sign of is indeterminate. Under uncorrelated heterogeneity, the FE estimator, , is asymptotically more efficient than the MG estimator if the benefit from pooling (i.e. when ) outweighs the loss in efficiency due to slope heterogeneity (since ).

For a proof see Section A.2.2 of the Appendix.

Example 2

Consider a simple case where , and are scalars, and suppose that then

where . In this simple case the MG estimator is more efficient than the FE estimator even if .

In general, with uncorrelated heterogeneous coefficients, the relative efficiency of the MG and FE estimators depends on the relative magnitude of the two components in (2.21). Since , the outcome depends on the sign and the magnitude of , which in turn depends on the heterogeneity of error variances, ) and over .

3 Irregular mean group estimators

So far we have argued that the MG estimator is robust to correlated heterogeneity, and its performance is comparable to the FE estimator even under uncorrelated heterogeneity. However, since the MG estimator is based on the individual estimates, for , its optimality and robustness critically depend on how well the individual coefficients can be estimated. This is particularly important when is ultra short, which is the primary concern of this paper. In cases where is small and/or the observations on are highly correlated, or are slowly moving, is likely to be close to zero in finite samples for a large number of units . As a result, is likely to be a poor estimate of for some , and including it in could be problematic, rendering the MG estimator inefficient and unreliable.

However, as discussed above, continues to be an unbiased estimator of , even if are correlated with so long as the stochastic component of is strictly exogenous with respect to . By averaging over for , as , the MG estimator converges to if is sufficiently large such that have at least second order moments for all . The existence of first order moments of is required for the MG estimator to be unbiased, and we need to have second order moments for -consistent estimation and valid inference about the average effects, . Accordingly, we need to distinguish between cases where have first and second order moments for all , as compared to cases where some may not even have first order moments. We refer to the MG estimator based on individual estimates without first or second order moments as the “irregular MG estimator”, which is the focus of our analysis. We consider the irregular MG estimator both for models with and without time effects and show how our proposed estimator relates to the literature.

3.1 Graham and Powell estimator

For panels with , Graham and Powell (2012) propose a trimmed GMM estimator (denoted as “GP”) whereby individual estimates with smaller than a given threshold value, , are omitted from the estimation of . For now, abstracting from time effects, the GP estimator can be viewed as a trimmed MG estimator given by

| (3.1) |

In the special case where , , and the trimming procedure based on is algebraically the same as the one used in (3.1). GP show that to correctly center the limiting distribution of , must be set such that , as . For example, for the choice of it is required that .999See Section 2 of GP and page 2125 where the use of is recommended. The GP approach can be viewed as trimming by exclusion and overlooks the information that might be contained in when . In what follows we propose an alternative trimmed MG (TMG) estimator that makes use of this information.

4 Trimmed mean group estimators

To motivate the TMG estimator we first introduce the following trimmed estimator of ,

where as before , , and

| (4.1) |

with and bounded in . The choice of and will be discussed below. Written more compactly, we have

| (4.2) |

where is given by

| (4.3) |

We considered two versions of TMG estimators depending on how individual trimmed estimators, , are combined. An obvious choice was to use a simple average of , namely

| (4.4) |

which can also be viewed as a weighted average estimator with the weights . But it is easily seen that these weights do not add up to unity, and it might be desirable to use the scaled weights , where . Using these modified weights we consider

| (4.5) |

Although the difference between the two TMG estimators is small for sufficiently large , it turns out that behaves much better in small samples and will be the focus of this paper.

To relate to the GP estimator given by (3.1), using the above results we note that

| (4.6) |

where is the fraction of the estimates being trimmed

| (4.7) |

Compared to , the GP estimator ignores the second term in (4.6), and hence places zero weights on the estimates with . In contrast, both and hence place non-zero weights on all the individual estimates, .

5 Asymptotic properties of the TMG estimator

To investigate the asymptotic properties of the TMG estimator, , we introduce the following additional assumptions:

Assumption 4

For , denote by where is the matrix of observations on in the heterogeneous panel data model (2.2). , , and , where is the adjoint of .

Assumption 5 (Distribution of )

For , are random draws from the probability distribution function, , with the continuously differentiable density function, , over , such that , , and where is the first derivative of evaluated at .

Assumption 6 (Characterization of correlation between and )

For , the dependence of on is characterized by (a):

| (5.1) |

where , and . (b): Denote

| (5.2) |

and

| (5.3) |

where and for are bounded and continuously differentiable functions of on , and are bounded matrices of fixed constants with . (c) are distributed independently over .

Remark 4

Remark 5

Remark 6

Under Assumption 6, can be written as

| (5.4) |

where represents the part of the heterogeneity of that is correlated with , and represents random or idiosyncratic heterogeneity which is distributed independently of , with , for all .

Remark 7

Remark 8

Under Assumption 6, it also follows that are distributed independently over , although in general .

Using (2.6) and (5.2) in (4.2) we have , where , and defined by (4.5) can be written as

| (5.5) |

where . (5.5) can be written equivalently as

| (5.6) |

where

| (5.7) |

with

| (5.8) |

Under Assumptions 4, 5 and 6 and are distributed independently over with zero means and bounded variances, and we have

Furthermore by Lemma A.1, , , and it follows that

| (5.9) |

and

| (5.10) |

Also conditional on , are distributed independently with mean zeros, and since where , using results in Lemma A.2 we have and

Hence, . Using these results in (5.6) we have

| (5.11) |

Hence asymptotically converges to , so long as as . The convergence rate of to will depend on the trade-off between the asymptotic bias and variance of . Though it is possible to reduce the bias of by choosing a value of close to unity, it will be at the expense of a large variance. In what follows we shed light on the choice of by considering the conditions under which the asymptotic distribution of is centered around so that also tends to zero at a reasonably fast rate.

5.1 The choice of the trimming threshold

We begin by assuming that the rate at which converges to is given by , where is set in relation to . Given the irregular nature of the individual estimators of when is ultra short (for example ), we expect the rate, , to be below the standard rate of .101010This issue has also been addressed by Graham and Powell (2012) and Sasaki and Ura (2021). Using (5.6) and (5.10) and noting that (with equality holding only under regular convergence), we have

| (5.12) |

To ensure that the asymptotic distribution of is correctly centered, we must have as . Since , this condition is ensured if Turning to the second term of the above, we also note that to obtain a non-degenerate distribution we also need to set . Combining these two requirements yields

| (5.13) |

which implies that at most the convergence rate of can be , well below the standard convergence rate, , which is achieved only if individual estimators of have at least second order moments for all . In practice, we suggest setting at the boundary value of or just above , which yields the familiar non-parametric convergent rate of .

5.2 Trimming condition

The condition whilst necessary, it is not sufficient. It is also required that the asymptotic variance of tends to a positive definite matrix. To this end, setting we first write (5.12) as

where , and . Recall also that which becomes negligible since , and under Assumption 6, are cross-sectionally independent and we have . Since , it follows that at the rate of as , and hence

The first term can be written as . By (A.1.14) of Lemma A.2 and recalling that , we have

, and the asymptotic distribution of is determined by that of . Under Assumption 1, conditional on , are independently distributed over with zero means and tends to a normal distribution if is a positive definite matrix. Using (A.1.13) of Lemma A.2 we note that

| (5.14) | |||||

which can be written equivalently as

| (5.15) | |||||

By (A.1.15) in Lemma A.2 , and since it then follows that (recall that )

To establish conditions under which , note that a symmetric matrix is positive definite if , for all non-zero vectors . Accordingly, consider

for some such that . Note that

and since , then

But by assumption , and (see Assumptions 1 and 4). Hence, a necessary and sufficient condition for to tend to a positive definite matrix is given by

| (5.16) |

Assumption 7 (Trimming condition)

and are jointly distributed such that

| (5.17) |

where , for and .

5.3 Robust estimation of the covariance matrix of the trimmed MG estimator

As with standard MG estimation, consistent estimation of using (5.19) requires knowledge of which cannot be estimated consistently when is short. Here we follow the literature and propose a robust covariance estimator of which is asymptotically unbiased for a wide class of error variances, , thus allowing for serially correlated and conditionally heteroskedastic errors. The main result is summarized in the following theorem.

Theorem 2 (Robust covariance matrix of TMG estimator)

See Section A.2.3 of the Appendix for a proof.

Remark 9

Following the literature on MG estimation here we also consider the following bias-adjusted and scaled version

| (5.21) |

The above results can be readily extended to panel data models with time effects.

6 Ultra short panels with time effects

Allowing for time effects the panel data model (2.11) can be written as

| (6.1) |

where for are the time effects. Without loss of generality we adopt the normalization ,111111Graham and Powell (2012) use the normalization . The choice of normalization is innocuous for the estimation of the average treatment effects, . where , and make the following additional assumption:

Assumption 8

| (6.2) |

where , and .

Remark 10

Assumption 8 allows for dependence between and , but requires this dependence to be time-invariant.

Remark 11

The irregular identification of when in Graham and Powell (2012) is based on moments conditional on the sub-population of “stayers”. Under Assumption 4 for all , i.e., there are no “stayers”in the population, this identification strategy cannot be used. Moreover, GP assume that the joint distribution of given does not depend on , which is similar to Assumption 8. See interpretations of Assumption 1.1 part (ii) on page 2111 in Graham and Powell (2012).

To estimate , initially we suppose is known. Let

| (6.3) |

Then the trimmed estimator of is given by and the associated TMG-TE estimator of follows as

where is given by (4.5), and

| (6.4) |

From our earlier analysis, it is clear that for a known , has the same asymptotic distribution as with replaced by . We first propose an estimator of for the case where , and then following Chamberlain (1992) we consider an alternative estimator of with better small sample properties when .

6.1 TMG-TE estimator with

Averaging (6.1) over ,

| (6.5) |

where , , , , and . Averaging over , under the normalization ,

| (6.6) |

where , and . Subtracting (6.6) from (6.5), yields (noting that )

| (6.7) |

where . Under Assumptions 1, 6 and 8, ,121212For a proof see Lemma A.3. which suggests the following estimator of

| (6.8) |

where

| (6.9) |

Stacking the equations in (6.8) over we have

| (6.10) |

where , , and. The above system of equations can now be solved in terms of if is non-singular. Under this condition we have

| (6.11) |

and substituting from (6.10) in (6.9) we have

| (6.12) |

Remark 12

Note that and have the same () non-zero eigenvalues, , and if is invertible so will .

The following theorem provides a summary of the results for estimation of and , and their asymptotic distributions.

Theorem 3 (Asymptotic distribution of and the time effects when )

Suppose that for and , are generated by (6.1), , Assumptions 1-8 hold, and is invertible where is given by (6.4), and . Then as , for ,

| (6.13) |

where is given by (6.12),

, and . Also

-

(a)

If , we have

(6.14) where , , and .

-

(b)

If , for , we have

(6.15) where .

A proof is given in Section A.3 of the Appendix. Using results similar to the ones employed to establish Theorem 2, robust covariance matrices for and are given by (A.3.4) and (A.3.7), respectively, in Section A.3 of the Appendix. In particular, the asymptotic covariance of is applicable to both cases (a) and (b) of Theorem 3, and does not require knowing if , or not.

Example 3

As an example of case (a) in Theorem 3, suppose , where are distributed independently over with zero means. Then , and we have . An example of case (b) arises when contains an interactive effect, namely . In this case where , and it follows that which is non-zero if varies over time and , namely at least one of the factors has loadings with non-zero means.

6.2 TMG-C estimator when

When , we can follow Chamberlain (1992) and eliminate the time effects by the de-meaning transformation . Under the normalization , , and we have . Then , and averaging over we obtain

| (6.16) |

Hence, can be estimated if is a positive definite matrix, without knowing . This requires , since is singular if . Therefore, to implement the Chamberlain estimation approach we require the following additional assumption:

Assumption 9

For , where

Under this Assumption can be estimated by

| (6.17) |

and its asymptotic distribution follows straightforwardly. Specifically, using (6.16) we have

| (6.18) |

and where

Since can be consistently estimated by

| (6.19) |

Using , the TMG-C estimator of is now given by

| (6.20) |

Also since , the asymptotic variance of can be consistently estimated by

| (6.21) |

where and .

7 A Hausman-type test of the validity of the FE estimator

As summarized by Proposition 2, the validity of the FE estimator depends on the independence of slope heterogeneity, , from the covariates, . Here we propose a Hausman-type test of this condition when is ultra short, under the null hypothesis

| (7.1) |

It is clear that the homogeneous alternative, , for all , and the uncorrelated alternative, , for all , are both implied by . But a less restrictive null can also be entertained by allowing , for , so long as , namely the number of violations of the null over the units is relatively few. This is in line with condition (2.20) that requires , which is the implicit null of the Hausman-type test. But to simplify the derivations we derive the tests under .

Consider the FE and TMG estimators defined by (2.13) and (4.5) respectively. Then a Hausman-type test of can be constructed based on the difference . Such a test has been considered by Pesaran et al. (1996) and Pesaran and Yamagata (2008), assuming the MG estimator has at least the second order moment.131313See pages 160–162 of Pesaran et al. (1996), and page 53 of Pesaran and Yamagata (2008). Here we extend this test to cover cases when is ultra short. Also, the earlier tests were derived under the null of homogeneity (namely , for all ), whilst the null that we are considering is more general and covers the null of homogeneity as a special case.

First recall from (2.17) and (4.5) that and , where , is given by (4.3), and . Also by Assumption 3, and . Using these results it follows that

where . Under and Assumption 1, for all and , and since by Assumptions 1 and part (c) of Assumption 6 and are cross-sectionally independent, then conditional on are also cross-sectionally independent and we have as , so long as

where , and . Hence where is a chi-squared distribution with degree of freedom. Note that can be written equivalently as where and is the column of . For fixed , a consistent estimator of , which is robust to the choices of and , can be obtained given by where , , with being the column of given by

| (7.2) |

Using the above estimator of , the Hausman-type test statistic for correlated slope heterogeneity is given by

| (7.3) |

Under the alternative hypothesis that , , as , and the test is consistent. The extension of the test to panel data models with time effects are provided in Section S.2 of the online supplement.

8 Monte Carlo evidence on small sample properties

Using Monte Carlo (MC) techniques, we now consider the small-sample properties of the TMG estimator and compare its performance with the FE, MG and GP estimators, as well as the recent estimator proposed by Sasaki and Ura (SU).141414Perhaps it should be noted that the SU estimator is intended for a more general setup that allows for many stayers (units with for some ) which we do not allow in our analysis. We are grateful to Sasaki and Ura for providing us with their codes written specifically for the case when . We also provide MC evidence on the estimation of panels with time effects. The finite-sample performance of the Hausman-type test of correlated slope heterogeneity is also examined.

8.1 Monte Carlo designs

8.1.1 Data generating processes (DGP)

The outcome variable, , is generated as

| (8.1) |

where we allow for heteroskedastic and serially correlated errors. We generate as first order autoregressive (AR(1)) processes

| (8.2) |

and consider two scenarios for , namely Gaussian , and chi-squared, . We also allow the shocks in the outcome equation, denoted by , to be cross-sectionally heteroskedastic. In the baseline model we generate for all where with . We also consider the robustness of the MC results to cases where also varies with , as detailed below in Section 8.1.3.

The regressors, are generated as factor-augmented AR processes

| (8.3) |

where , for , and . We generate the individual effects in , , as , with , , and . When time effects are included in the model, we set , for , and , so that .

8.1.2 Generation of the heterogeneous coefficients

We consider both correlated and uncorrelated effects specifications and generate as

| (8.4) |

where with and . To generate correlated effects we set to be a function of the innovations to the process:

| (8.5) |

Since , it follows that is .151515In Section S.3.1 of the online supplement, we show that when is serially independent with no interactive effects ( and ), then can be written as a standardized version of The random components of , namely , are generated independently of , as where . Namely,

The degree of correlated heterogeneity is determined by , and it is zero if . Also will be non-zero when both and are non-zero. Specifically , , and . Therefore, the correlation coefficients of and are given by , and

| (8.6) |

Solving the above equations for and , we have

| (8.7) |

Also recall that , and then , and . Hence, the key drivers of heterogeneity are , , , and . The scaling parameter in (8.1) is set to achieve a given level of overall fit, , given by (S.3.3) in Section S.3.2 of the online supplement.

Section 8.1.3 summarizes parameters and details of the baseline model and the other experiments where we allow for heterogeneity in the autoregressive processes assumed for and . We also consider cases where is generated with and without an interactive factor.161616When there are feedbacks, we generate or for , then drop the first observations. All estimations are based on simulated observations , for and .

8.1.3 Baseline and other experiments

For all experiments we set , , and , with , and experiment with two levels of fit: and . We also consider two options when generating , the shocks to the process, namely Gaussian, , and uniformly distributed errors, with .

For the baseline experiments, we set , generate the errors in the outcome equation as chi-squared without serial correlation ( in (8.2)). For we allow for heterogeneous serial correlation, with , but did not include the interactive effects in (setting in (8.3)). We consider both uncorrelated and correlated heterogeneity and set , defined by (8.6), to (a) zero correlation, , (b) a medium level of correlation, , and (c) a high level of correlation, . For each choice of , the scalar variable, , in the outcome equation, (8.1), is set such that , on average. This is achieved by stochastic simulation for each , as described in Section S.3.2 of the online supplement.

To check the robustness of the TMG estimator, the following variations in the DGP of the errors and regressors are considered. When the errors in are serially correlated, we generate , and for all . When there is an interactive effect in , and , for , where , with .

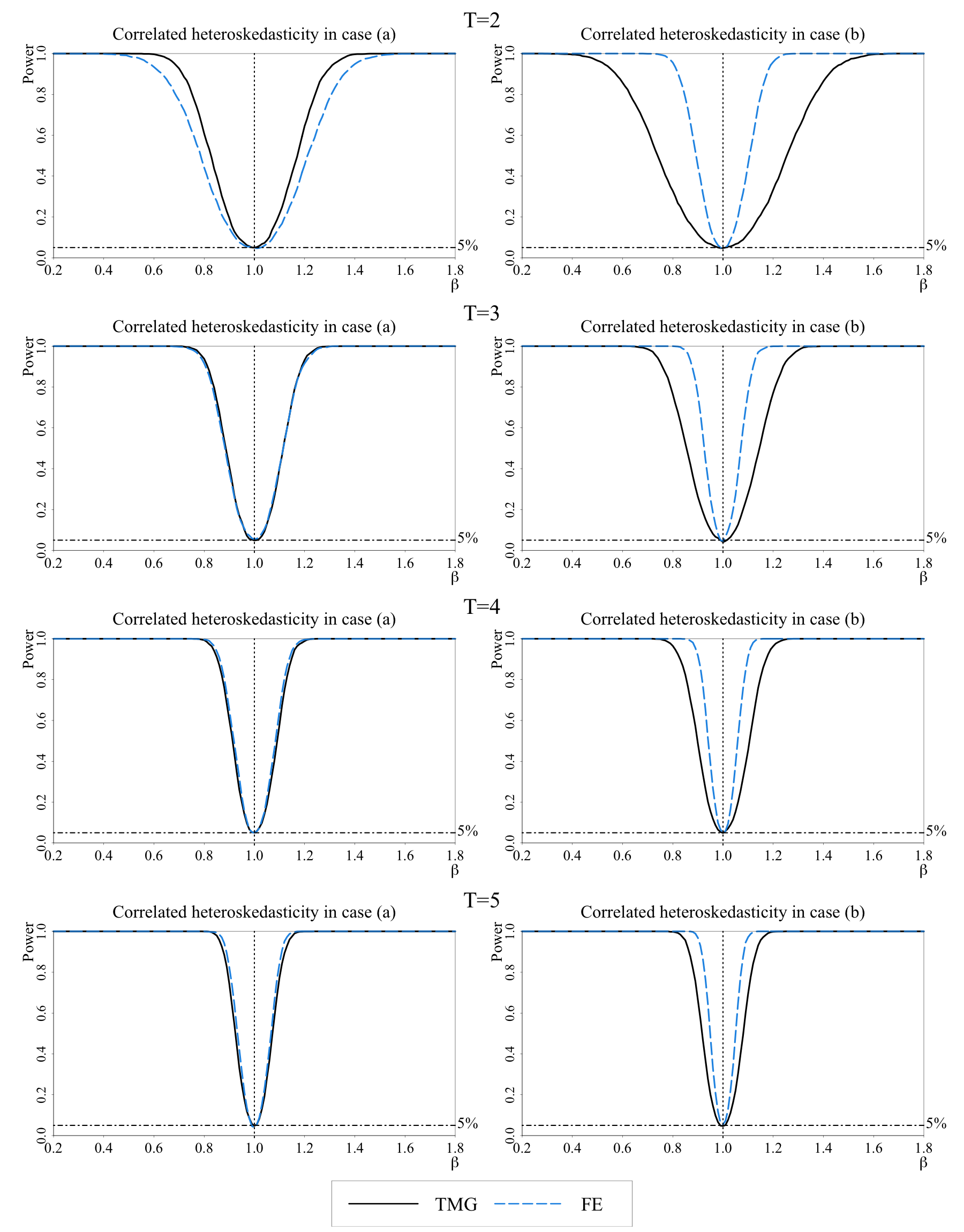

To examine the relative efficiency of TMG and FE estimators, we set (uncorrelated heterogeneity) but allow for error heteroskedasticity to be correlated with the processes generating . We consider the following two scenarios: (a) cross-sectional heteroskedasticity, , for all and , where is given by (8.5); and (b) cross-sectional and time series heteroskedasticity, , for all and , where is the innovation to the process. In both cases we have , which match the case of randomly generated heteroskedasticity.

To investigate the small sample properties of the Hausman-type test, we allow individual effects, , to be correlated with , irrespective of whether and are correlated. Recall that FE and MG estimators are both robust to the correlation of and . The focus of the Hausman-type test is on the degree of heterogeneity of and the nature of correlation between and . We carry out replications for all experiments.

8.2 Monte Carlo findings

8.2.1 Comparison of TMG, FE, and MG estimators

We first compare the performance of the TMG estimator with FE and MG estimators under both uncorrelated and correlated heterogeneity for the sample size combinations , and . The TMG estimator depends on the indicator, , where . In view of the discussion in Section 5.1 on the choice of , we consider the values of and , and set , where . This choice of ensures that the value of is unaffected by the scale of . In what follows we report the results for the TMG estimator with , but discuss the sensitivity of the TMG estimator to the choice of in sub-section 8.2.4.

Table 1 reports bias, root mean squared errors (RMSE) and size for estimation of . The first column of the table gives estimates of the fraction of individual estimates being trimmed as defined by (4.7). The left panel gives the estimates under uncorrelated heterogeneity, with , and the right panel reports the results for the case of correlated heterogeneity, with . The estimates of tend to be quite large for the case of ultra short but fall quite rapidly as is increased. For example, for and as many as per cent of the individual estimates are trimmed when computing the TMG estimates, but it falls to per cent when is increased to . However, recall that the TMG estimator continues to make use of the trimmed estimates, as can be seen from (4.6), and the TMG estimator shows little bias compared to the untrimmed MG estimator. The TMG and MG estimators converge as is increased and they are almost identical for the panels with . The results in Table 1 clearly show the effectiveness of trimming in dealing with outlying individual estimates.

| Uncorrelated heterogeneity: , | Correlated heterogeneity: , | ||||||||||||||||||||||||||

| Bias | RMSE | Size | Bias | RMSE | Size | ||||||||||||||||||||||

| TMG | FE | MG | TMG | FE | MG | TMG | FE | MG | TMG | TMG | FE | MG | TMG | FE | MG | TMG | FE | MG | TMG | ||||||||

| 2 | 31.2 | -0.004 | -7.325 | -0.002 | 0.17 | 353.13 | 0.33 | 5.0 | 2.1 | 4.7 | 31.2 | 0.444 | -7.714 | 0.048 | 0.48 | 371.86 | 0.35 | 66.6 | 2.1 | 4.9 | |||||||

| 3 | 16.5 | 0.001 | -0.011 | -0.002 | 0.11 | 0.57 | 0.19 | 4.9 | 4.0 | 4.7 | 16.5 | 0.322 | -0.011 | 0.023 | 0.34 | 0.60 | 0.20 | 74.1 | 4.2 | 5.2 | |||||||

| 4 | 10.4 | -0.002 | -0.001 | -0.002 | 0.09 | 0.21 | 0.14 | 4.8 | 5.1 | 5.5 | 10.4 | 0.265 | 0.000 | 0.013 | 0.28 | 0.22 | 0.15 | 76.7 | 5.3 | 5.2 | |||||||

| 5 | 7.1 | -0.002 | -0.001 | 0.000 | 0.08 | 0.13 | 0.11 | 5.6 | 4.0 | 3.6 | 7.1 | 0.230 | 0.000 | 0.009 | 0.25 | 0.14 | 0.12 | 77.5 | 4.2 | 4.0 | |||||||

| 6 | 5.2 | 0.002 | 0.000 | 0.001 | 0.07 | 0.11 | 0.10 | 4.5 | 4.5 | 4.7 | 5.2 | 0.211 | 0.000 | 0.008 | 0.22 | 0.11 | 0.10 | 80.0 | 4.8 | 5.1 | |||||||

| 8 | 3.2 | 0.002 | 0.000 | 0.000 | 0.06 | 0.08 | 0.08 | 4.9 | 4.6 | 4.6 | 3.2 | 0.179 | 0.000 | 0.003 | 0.19 | 0.08 | 0.08 | 80.0 | 4.6 | 4.5 | |||||||

| 2 | 28.5 | -0.005 | -2.398 | -0.001 | 0.12 | 149.72 | 0.26 | 4.6 | 2.0 | 5.5 | 28.5 | 0.445 | -2.525 | 0.044 | 0.46 | 157.67 | 0.27 | 90.8 | 2.0 | 5.3 | |||||||

| 3 | 14.1 | 0.002 | 0.007 | -0.002 | 0.08 | 0.44 | 0.15 | 4.9 | 4.3 | 5.6 | 14.1 | 0.323 | 0.007 | 0.018 | 0.34 | 0.46 | 0.16 | 95.2 | 4.5 | 5.4 | |||||||

| 4 | 8.4 | 0.000 | -0.003 | -0.003 | 0.07 | 0.15 | 0.11 | 4.9 | 4.3 | 4.4 | 8.4 | 0.266 | -0.003 | 0.008 | 0.27 | 0.15 | 0.11 | 95.7 | 4.8 | 4.7 | |||||||

| 5 | 5.6 | 0.001 | -0.004 | -0.001 | 0.06 | 0.10 | 0.09 | 5.6 | 5.1 | 5.1 | 5.6 | 0.233 | -0.004 | 0.006 | 0.24 | 0.11 | 0.09 | 96.3 | 5.2 | 5.1 | |||||||

| 6 | 4.0 | 0.000 | -0.001 | -0.001 | 0.05 | 0.08 | 0.07 | 3.8 | 4.2 | 4.3 | 4.0 | 0.208 | -0.001 | 0.004 | 0.21 | 0.08 | 0.07 | 97.4 | 4.0 | 4.4 | |||||||

| 8 | 2.4 | 0.000 | 0.000 | 0.000 | 0.04 | 0.06 | 0.06 | 4.2 | 5.0 | 4.6 | 2.4 | 0.178 | 0.000 | 0.003 | 0.18 | 0.06 | 0.06 | 97.4 | 4.7 | 4.8 | |||||||

| 2 | 24.7 | 0.002 | -4.275 | 0.000 | 0.08 | 426.12 | 0.17 | 5.1 | 1.8 | 4.3 | 24.7 | 0.452 | -4.502 | 0.037 | 0.46 | 448.73 | 0.18 | 100.0 | 1.8 | 4.7 | |||||||

| 3 | 10.8 | 0.001 | -0.006 | 0.000 | 0.05 | 0.28 | 0.10 | 4.3 | 4.7 | 4.8 | 10.8 | 0.323 | -0.006 | 0.016 | 0.33 | 0.29 | 0.11 | 100.0 | 4.7 | 5.3 | |||||||

| 4 | 5.8 | 0.001 | 0.000 | 0.000 | 0.04 | 0.10 | 0.07 | 5.1 | 4.9 | 5.7 | 5.8 | 0.265 | 0.000 | 0.008 | 0.27 | 0.10 | 0.08 | 100.0 | 5.3 | 5.6 | |||||||

| 5 | 3.5 | 0.000 | -0.001 | 0.000 | 0.04 | 0.07 | 0.06 | 5.1 | 4.6 | 4.0 | 3.5 | 0.231 | -0.001 | 0.004 | 0.23 | 0.07 | 0.06 | 100.0 | 4.3 | 4.0 | |||||||

| 6 | 2.3 | -0.001 | 0.000 | 0.000 | 0.03 | 0.05 | 0.05 | 4.7 | 5.1 | 5.2 | 2.3 | 0.207 | 0.000 | 0.003 | 0.21 | 0.06 | 0.05 | 100.0 | 5.1 | 5.4 | |||||||

| 8 | 1.2 | 0.000 | 0.000 | 0.000 | 0.03 | 0.04 | 0.04 | 5.2 | 5.0 | 5.1 | 1.2 | 0.178 | 0.000 | 0.001 | 0.18 | 0.04 | 0.04 | 100.0 | 5.1 | 5.1 | |||||||

| 2 | 22.1 | -0.001 | -1.536 | -0.004 | 0.05 | 175.33 | 0.13 | 5.3 | 2.2 | 4.7 | 22.1 | 0.449 | -1.617 | 0.029 | 0.45 | 184.63 | 0.14 | 100.0 | 2.2 | 5.6 | |||||||

| 3 | 8.8 | -0.002 | 0.004 | 0.000 | 0.04 | 0.19 | 0.07 | 5.1 | 4.2 | 4.9 | 8.8 | 0.321 | 0.004 | 0.013 | 0.32 | 0.20 | 0.08 | 100.0 | 4.3 | 5.3 | |||||||

| 4 | 4.4 | 0.000 | 0.000 | 0.001 | 0.03 | 0.07 | 0.05 | 4.6 | 4.6 | 4.6 | 4.4 | 0.265 | 0.000 | 0.007 | 0.27 | 0.07 | 0.05 | 100.0 | 4.7 | 4.4 | |||||||

| 5 | 2.5 | 0.000 | -0.001 | -0.001 | 0.03 | 0.05 | 0.04 | 4.5 | 4.4 | 4.6 | 2.5 | 0.231 | -0.001 | 0.002 | 0.23 | 0.05 | 0.04 | 100.0 | 4.7 | 4.7 | |||||||

| 6 | 1.6 | 0.000 | 0.000 | 0.000 | 0.02 | 0.04 | 0.03 | 5.6 | 4.2 | 4.0 | 1.6 | 0.208 | 0.000 | 0.002 | 0.21 | 0.04 | 0.04 | 100.0 | 4.4 | 4.1 | |||||||

| 8 | 0.8 | 0.000 | 0.000 | 0.001 | 0.02 | 0.03 | 0.03 | 5.1 | 4.9 | 4.8 | 0.8 | 0.177 | 0.000 | 0.001 | 0.18 | 0.03 | 0.03 | 100.0 | 4.8 | 4.7 | |||||||

Notes: (i) The baseline model is generated as , where the errors processes for and equations are chi-squared and Gaussian, respectively, are generated as heterogeneous AR(1) processes, and (the degree of correlated heterogeneity) is defined by (8.6). For further details see Section 8.1.3. (ii) FE and MG estimators are given by (2.13) and (2.4). The trimmed mean group (TMG) estimator and its asymptotic variance are given by (4.5) and (5.21), respectively. (iii) The trimming threshold for the TMG estimator is given by , where , , and . is set to . is the simulated fraction of individual estimates being trimmed, defined by (4.7).

Comparing TMG and FE estimators, we first note that in line with the theory, the FE estimator performs very well under uncorrelated heterogeneity but is badly biased when heterogeneity is correlated, and this bias does not diminish if and are increased. When heterogeneity is correlated, the FE estimator also exhibits substantial size distortions which tend to get accentuated as is increased for a given . In contrast, the TMG estimator is robust to the correlation between and , and delivers size around the 5 per cent nominal level in all cases.171717Increasing from to does not affect the bias and RMSE of the FE estimator, but results in a higher degree of size distortion under correlated heterogeneity. Compare the results summarized in the right panel of Table 1 and Table S.4, respectively, in the online supplement.

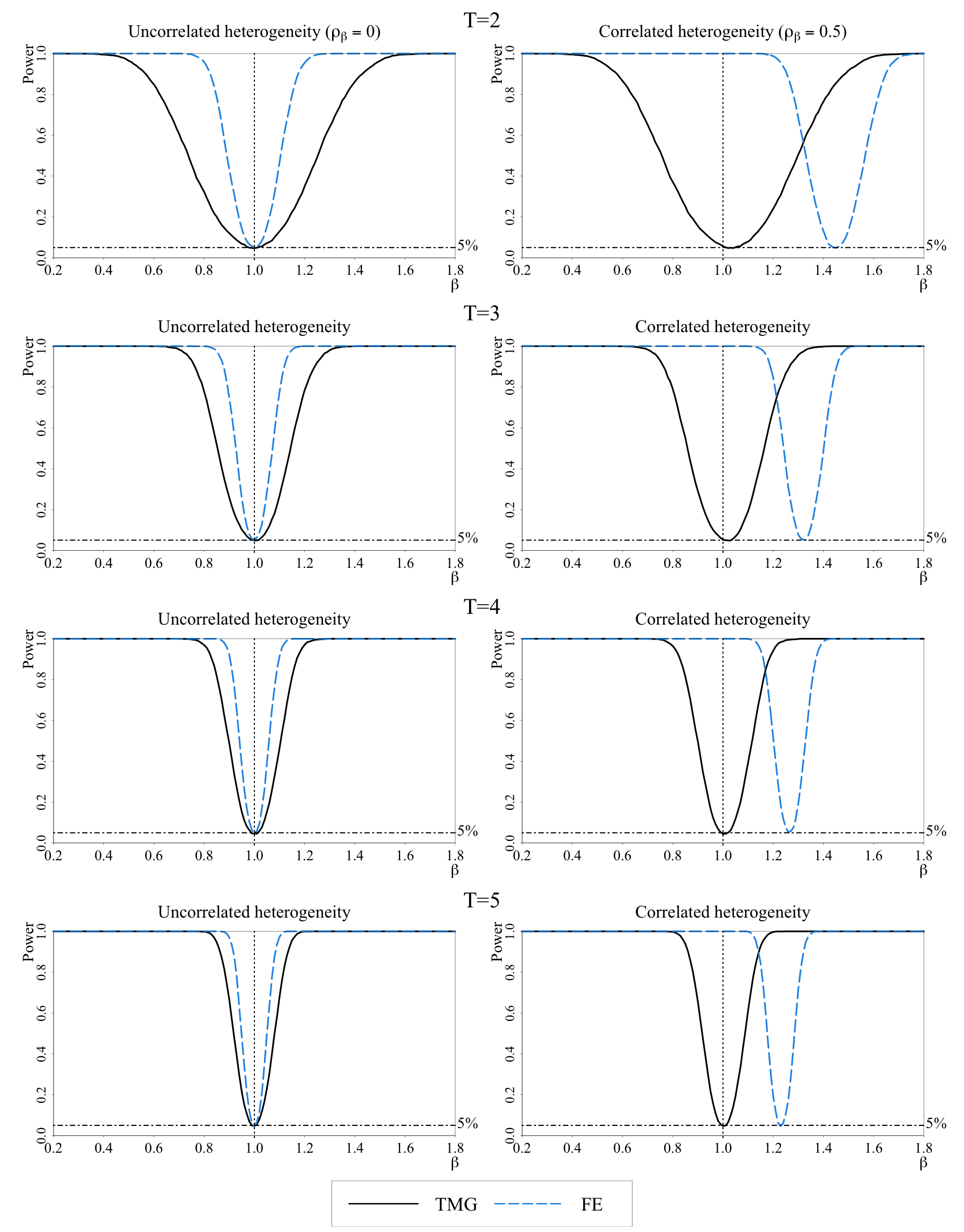

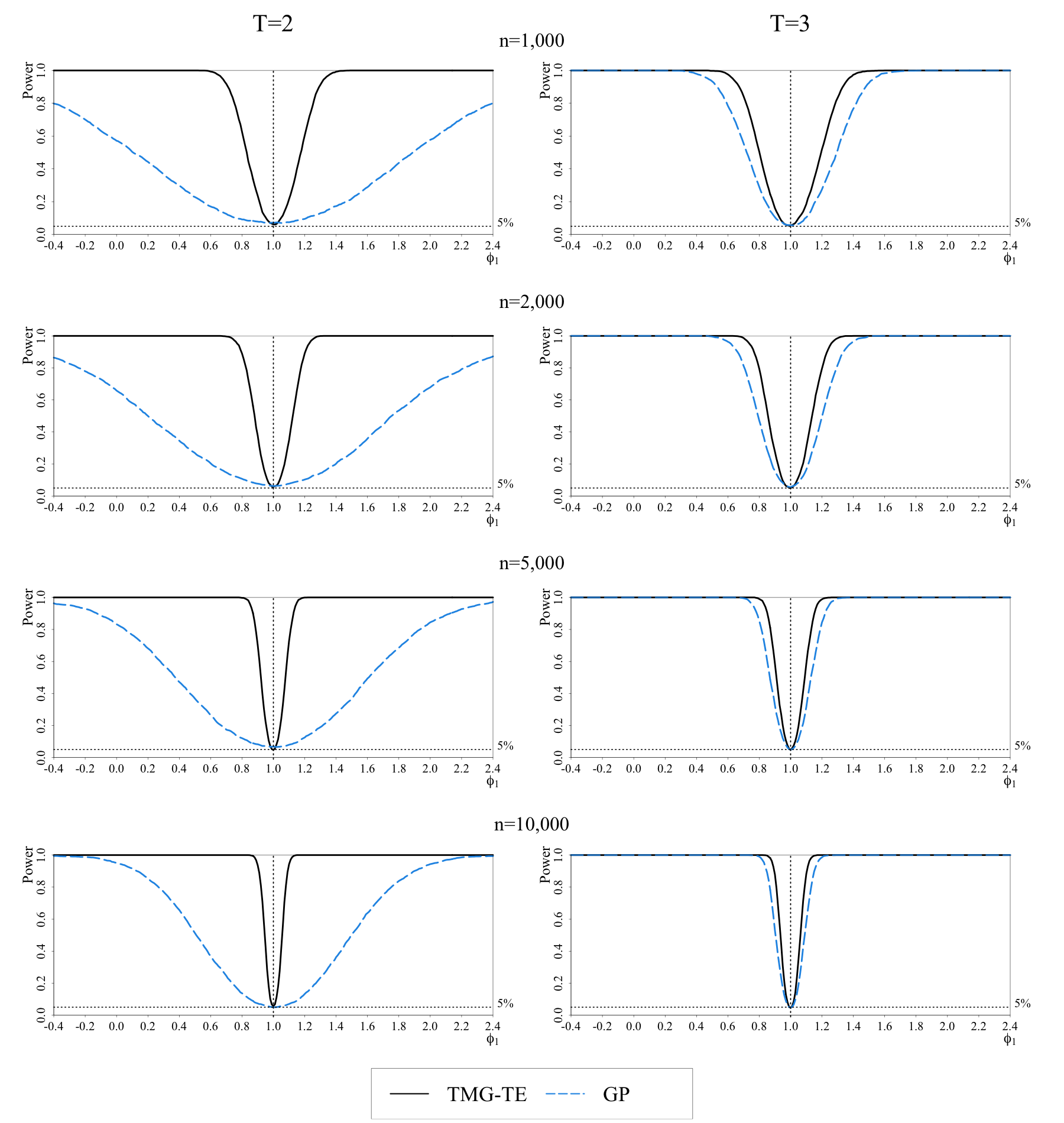

Figure 1 shows the plots of the empirical power functions for TMG and FE estimators for and and . The left panel gives the power functions for the case of uncorrelated heterogeneity (), and as can be seen, both estimators are centered correctly around , with the FE estimator having better power properties. But the differences between the power of FE and TMG estimators shrink rapidly and become negligible as is increased from to .181818But see the left panel of Table S.3 and Figure S.1 in the online supplement where it is shown that it does not necessarily follow that the FE estimator will dominate the TMG estimator in terms of efficiency even when is ultra short. The right panel of the figure provides the same results but under correlated heterogeneity with . In this case, the empirical power functions of the FE estimator now shift dramatically to the right, away from the true value, an outcome that becomes more concentrated as is increased. In contrast, the empirical power functions for the TMG estimator tend to be reasonably robust to the choice of .

To summarize, in the case of uncorrelated heterogeneity, the FE estimator performs well despite of the heterogeneity and is more efficient than the TMG estimator in the case of baseline model used in our MCs, but in general the relative efficiency of TMG and FE estimators depends on the underlying DGP. The situation is markedly different when heterogeneity is correlated, and the FE estimator can be badly biased, leading to incorrect inference, whilst the TMG estimator provides valid inference with size around the nominal five per cent level and reasonable power, irrespective of whether is correlated with or not.

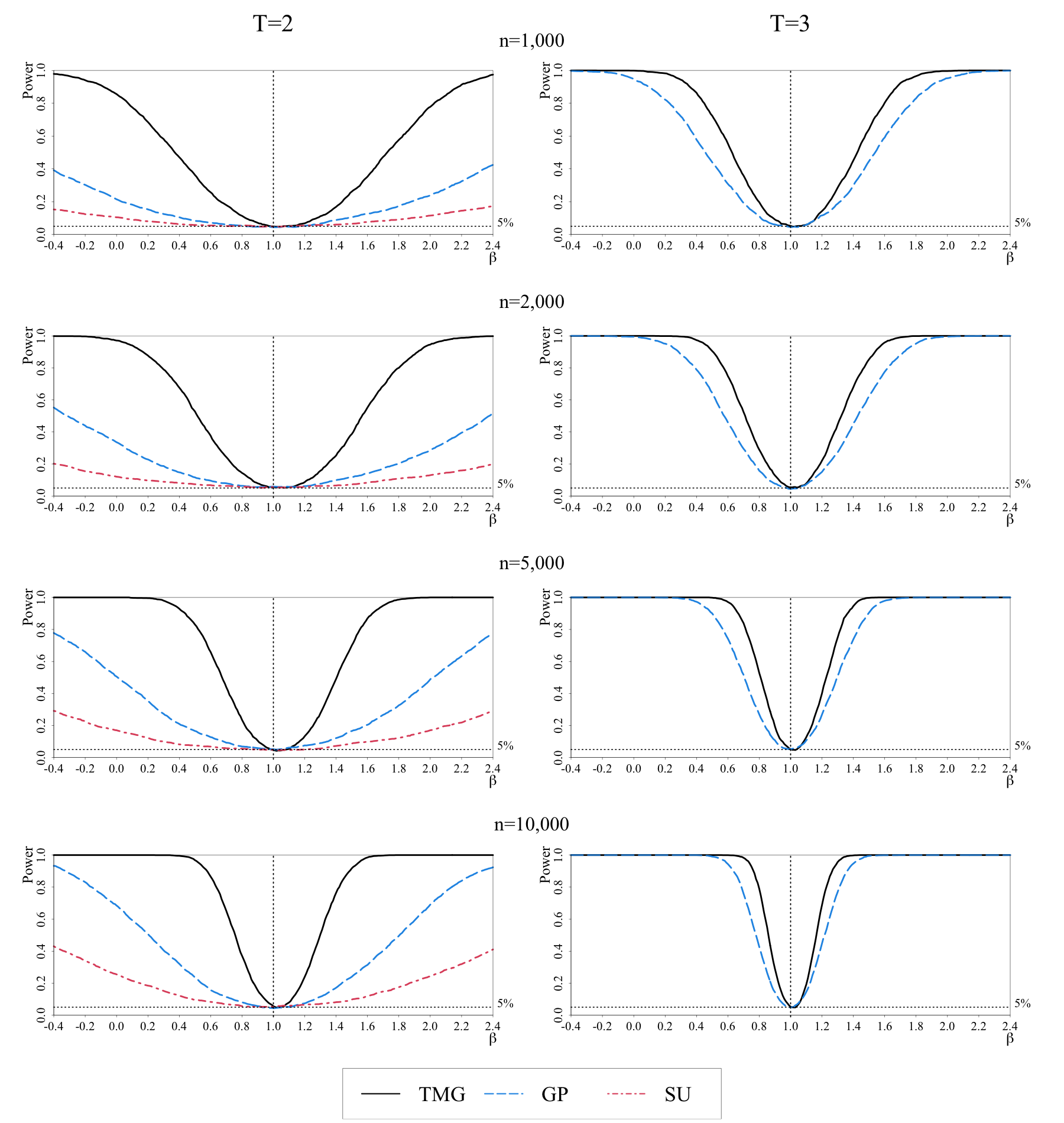

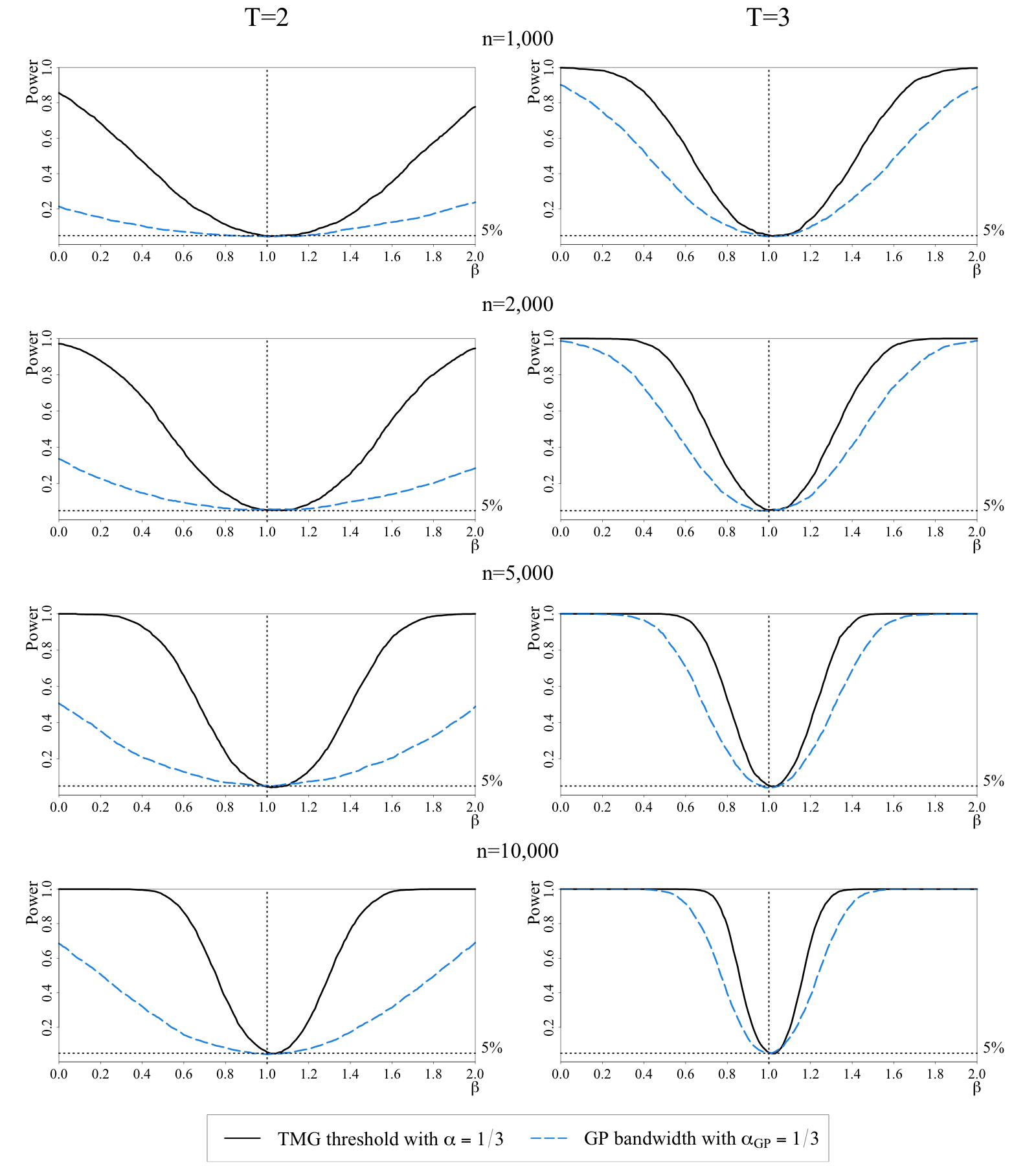

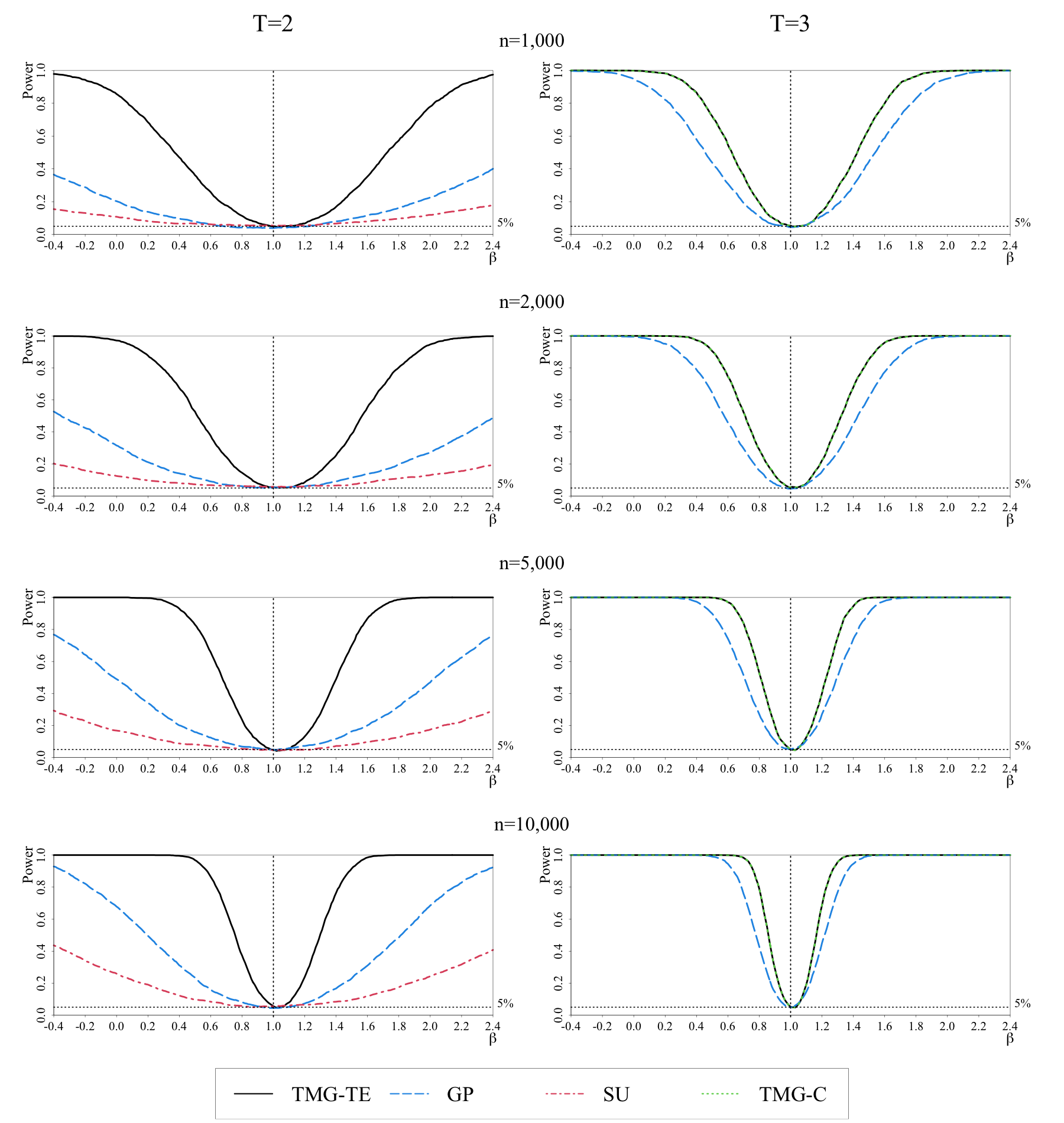

8.2.2 Comparison of TMG, GP, and SU estimators

Focusing on the case of correlated heterogeneity, we now compare the performance of the TMG estimator with GP and SU estimators. To implement the GP estimator, defined by (3.1), for we follow GP and set , with , and , where and are the respective sample standard deviation and interquartile range of . See page 2138 in Graham and Powell (2012).191919However, GP seem to be using the larger scaling value of , when they generate the histograms in Figure 1, on page 2137. There is no clear guidance in GP as to the choice of when .202020For , GP do not use the bandwidth parameter, , but directly select the “percent trimmed”, . In their empirical application for they report estimates with 4 per cent being trimmed. See the last column of Table 3 on page 2136 of GP. For consistency, for GP estimates we continue to use their bandwidth, with , but set and trim if . The sensitivity of the results to the other choices of is considered below. For SU we use the code made available to us by the authors, which is applicable only when .

The bias, RMSE and size for all three estimators are summarized in Table 2 for , and . For the results are provided for TMG and GP estimators only. The associated empirical power functions are provided in Figure 2.

| Size | Size | |||||||||

| Estimator | Bias | RMSE | Bias | RMSE | ||||||

| TMG | 31.2 | 0.048 | 0.35 | 4.9 | 16.5 | 0.023 | 0.20 | 5.2 | ||

| GP | 4.2 | -0.029 | 0.83 | 4.5 | 2.0 | -0.002 | 0.27 | 4.6 | ||

| SU | 4.2 | -0.045 | 1.62 | 4.9 | … | … | … | … | ||

| TMG | 28.5 | 0.044 | 0.27 | 5.3 | 14.1 | 0.018 | 0.16 | 5.4 | ||

| GP | 3.4 | 0.031 | 0.70 | 5.8 | 1.3 | 0.003 | 0.22 | 4.4 | ||

| SU | 3.4 | 0.008 | 1.39 | 5.5 | … | … | … | … | ||

| TMG | 24.7 | 0.037 | 0.18 | 4.7 | 10.8 | 0.016 | 0.11 | 5.3 | ||

| GP | 2.5 | 0.009 | 0.52 | 5.2 | 0.7 | -0.001 | 0.15 | 5.2 | ||

| SU | 2.5 | 0.003 | 1.01 | 4.9 | … | … | … | … | ||

| TMG | 22.1 | 0.029 | 0.14 | 5.6 | 8.8 | 0.013 | 0.08 | 5.3 | ||

| GP | 2.0 | 0.002 | 0.41 | 4.3 | 0.5 | -0.002 | 0.11 | 4.9 | ||

| SU | 2.0 | 0.007 | 0.82 | 5.2 | … | … | … | … | ||

Notes: (i) GP and SU estimators are proposed by Graham and Powell (2012) and Sasaki and Ura (2021), respectively. The GP estimator is given by (3.1). For , GP compare with the bandwidth . is set to 1/3. , where and are the respective sample standard deviation and interquartile range of . For , we continue using the bandwidth with . See Section 8.2.2 for details. When , the SU estimator uses the same bandwidth as GP. (ii) For details of the baseline model without time effects, see footnote (i) to Table 1. For the TMG estimator and its trimming threshold, see footnotes (ii) and (iii) to Table 1. is the simulated fraction of individual estimates being trimmed, defined by (4.7). The estimation algorithm for the SU estimator is not available for , denoted by “…”.

The fraction of the trimmed estimates, , defined by (4.7), for the TMG estimator is quite high when , but declines markedly when is raised to and to a lesser extent as is increased. This is not the case for the other two estimators. For example, when and , the fraction of trimmed estimates for the TMG estimator is around per cent as compared to per cent for GP and SU estimators, and falls to per cent as is increased to . Increasing from to with reduces this fraction to per cent as compared to per cent for the GP estimator.212121Recall that the codes released by SU do not allow us to compute their estimator when The heavy trimming causes the TMG estimator to have a much larger bias than GP and SU estimators, particularly when and is sufficiently large. However, the TMG estimator continues to have better overall small sample performance due to its higher efficiency. Recall that the TMG estimator makes use of the trimmed estimates, as set out in the second term of (4.6), but the trimmed estimates are not used in the GP estimator. This difference in the way trimmed estimates are treated is reflected in the lower RMSE of the TMG estimator as compared to the other two estimators for all and combinations. For example, when and , the RMSE of the TMG is as compared to and for GP and SU estimators. The relative advantage of the TMG estimator continues when is increased from to , but its relative advantage declines. For , the RMSE of the TMG estimator stands at compared to for the GP estimator. The larger the value of , the less important the trimming becomes.

The empirical power functions for all three estimators are shown in Figure 2. As can be seen, the TMG estimator is uniformly more powerful than the GP estimator and the GP estimator is more powerful than the SU estimator.

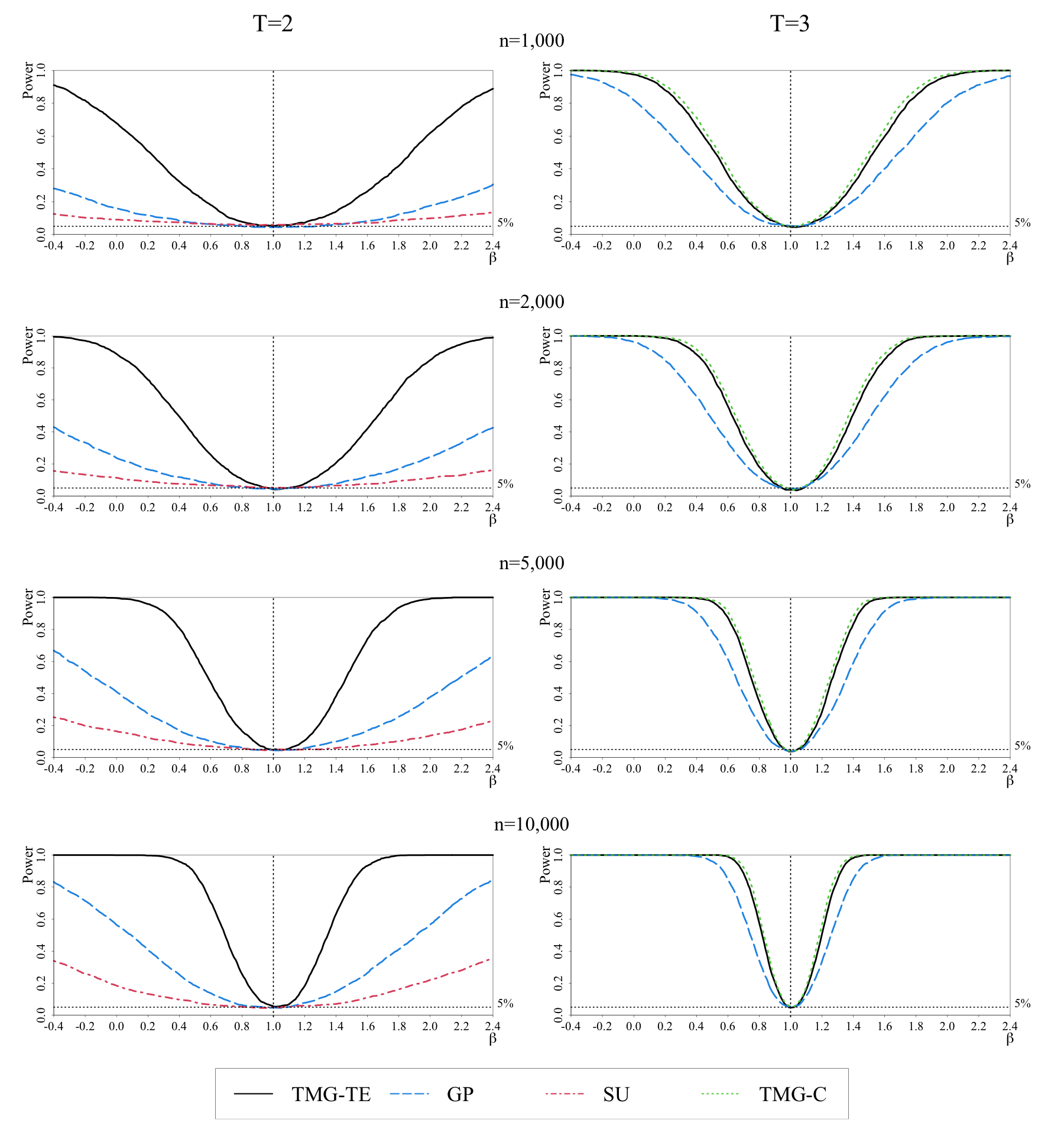

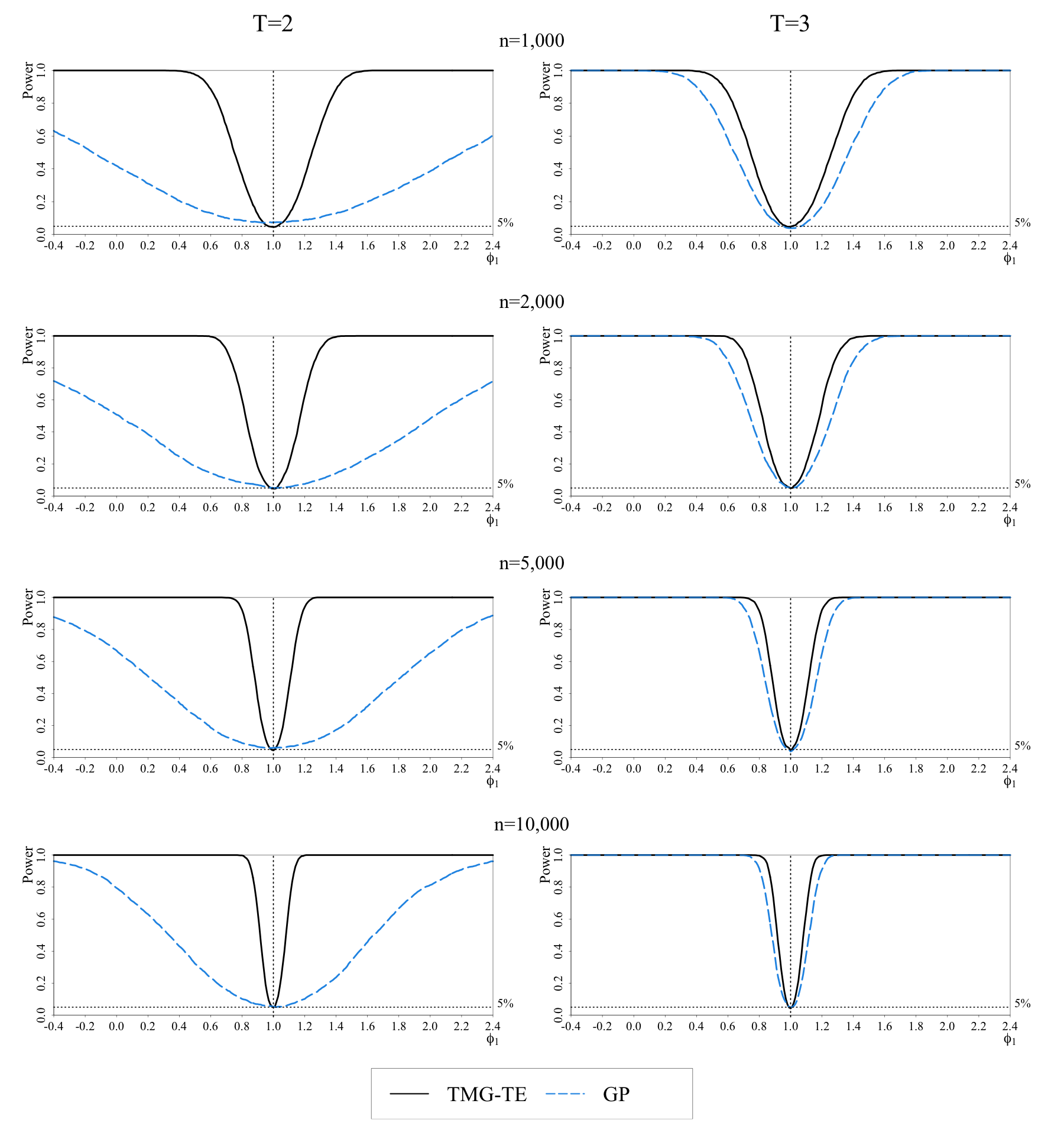

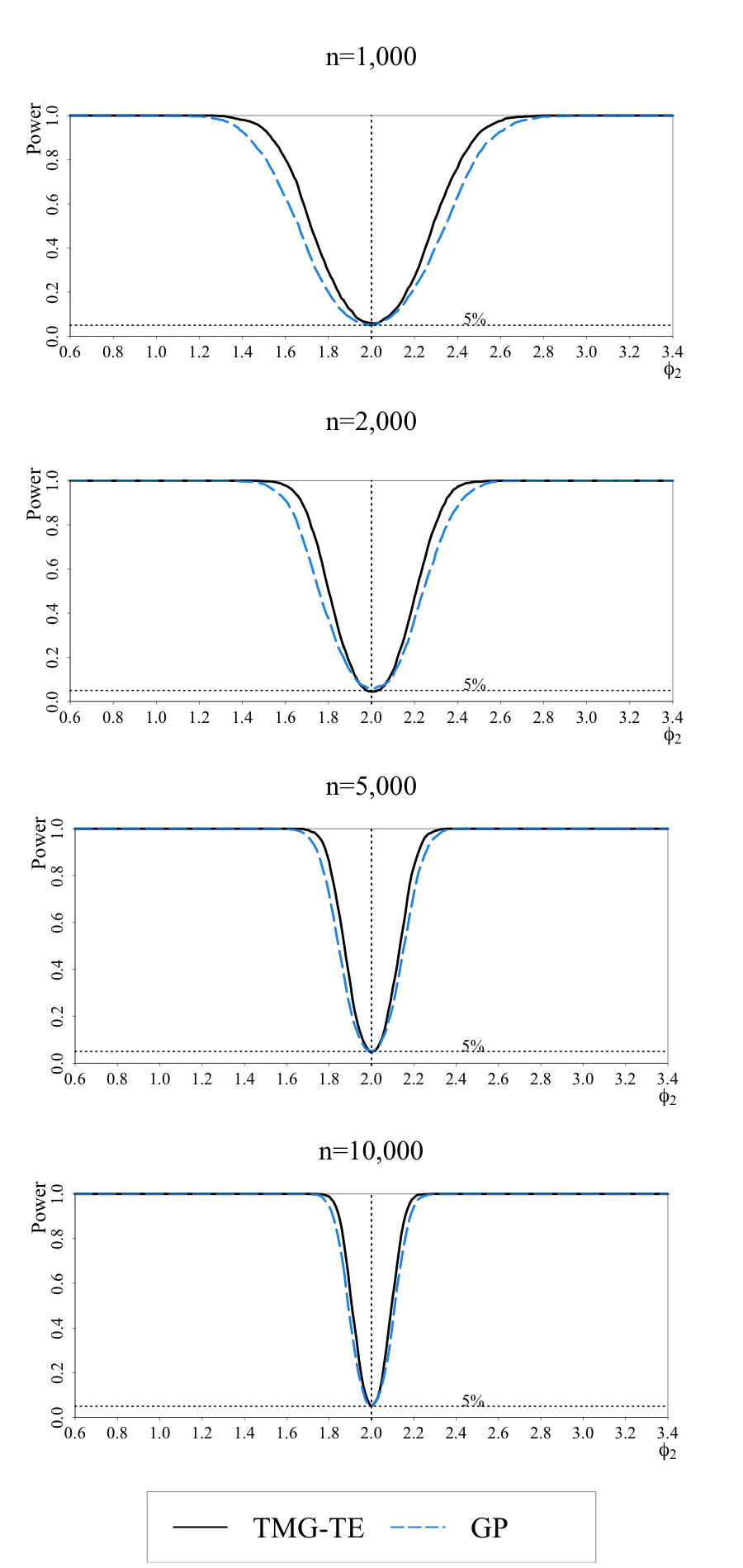

8.2.3 Models with time effects

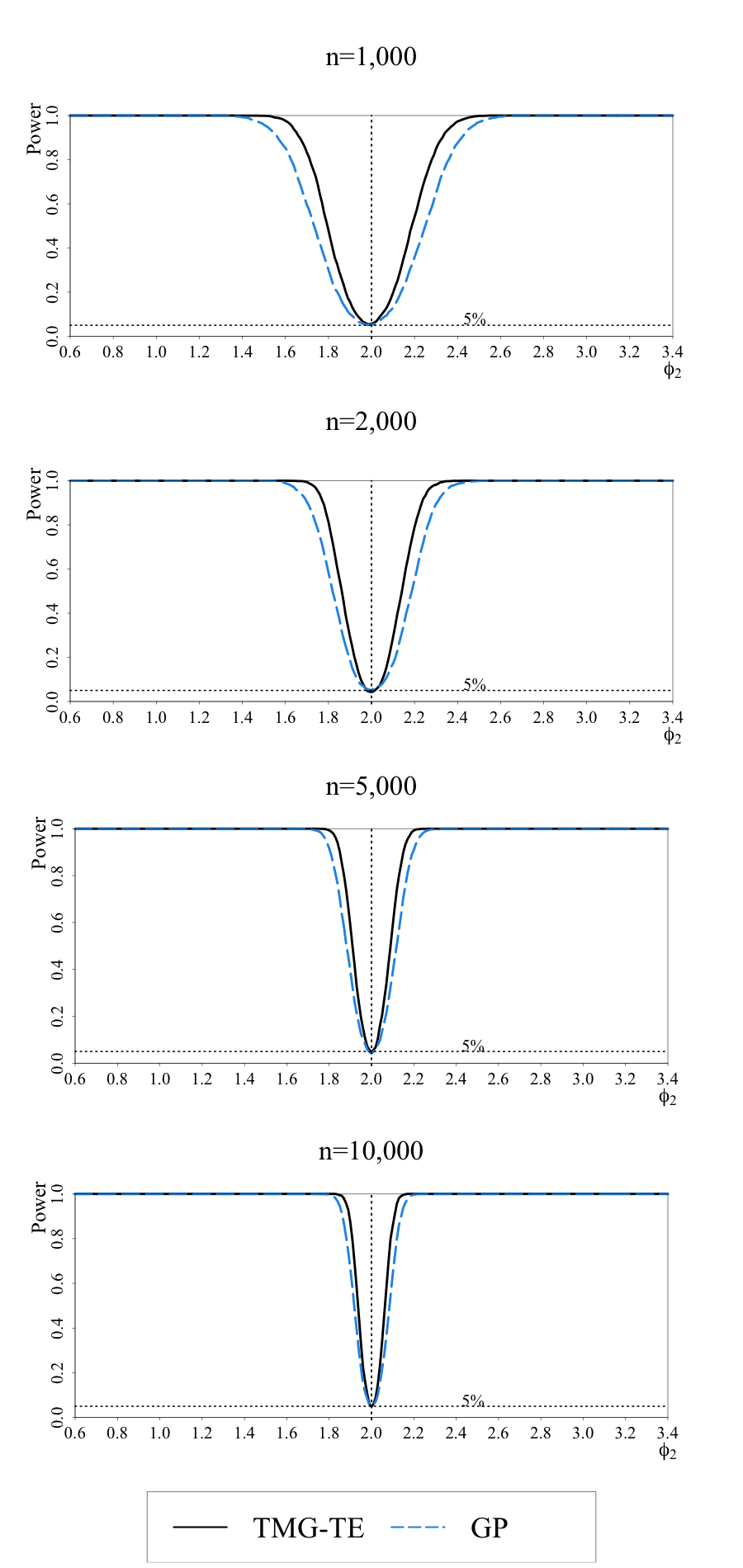

Adding time effects to the panel regressions does not alter the above conclusions. The MC results for estimation of and the time effects are summarized in Tables 3 and 4, respectively. The small sample properties of the TMG-TE estimator of are very close to those reported for the TMG estimator in Table 2. Interestingly, there are also little differences between TMG-TE and TMG-C estimators of when , as can be seen from the right panel of Table 3. Also, the time effects are precisely estimated. Bias, RMSE and size for TMG-TE and GP estimators of are summarized in Table 4. The bias of TMG-TE and GP estimators of are similar, but the TMG-TE estimator has much lower RMSEs and higher power when . A comparison of the empirical powers of these two estimators is given in Figures S.9–S.11 in the online supplement.

| Size | Size | |||||||||

| Estimator | Bias | RMSE | Bias | RMSE | ||||||

| TMG-TE | 31.2 | 0.048 | 0.35 | 5.0 | 16.5 | 0.023 | 0.20 | 5.4 | ||

| TMG-C | … | … | … | … | 16.5 | 0.023 | 0.20 | 5.2 | ||

| GP | 4.2 | -0.034 | 0.84 | 3.9 | 2.0 | -0.002 | 0.27 | 4.6 | ||

| SU | 4.2 | -0.052 | 1.67 | 5.3 | … | … | … | … | ||

| TMG-TE | 28.5 | 0.044 | 0.27 | 5.6 | 14.1 | 0.018 | 0.16 | 5.5 | ||

| TMG-C | … | … | … | … | 14.1 | 0.018 | 0.16 | 5.6 | ||

| GP | 3.4 | 0.032 | 0.71 | 5.2 | 1.3 | 0.003 | 0.22 | 4.6 | ||

| SU | 3.4 | 0.012 | 1.40 | 5.8 | … | … | … | … | ||

| TMG-TE | 24.7 | 0.037 | 0.18 | 4.7 | 10.8 | 0.016 | 0.11 | 5.3 | ||

| TMG-C | … | … | … | … | 10.8 | 0.016 | 0.11 | 5.3 | ||

| GP | 2.5 | 0.008 | 0.53 | 5.0 | 0.7 | -0.001 | 0.15 | 5.1 | ||

| SU | 2.5 | 0.006 | 1.02 | 4.7 | … | … | … | … | ||

| TMG-TE | 22.1 | 0.028 | 0.14 | 5.7 | 8.8 | 0.013 | 0.08 | 5.3 | ||

| TMG-C | … | … | … | … | 8.8 | 0.013 | 0.08 | 5.3 | ||

| GP | 2.0 | 0.003 | 0.41 | 4.4 | 0.5 | -0.002 | 0.11 | 5.0 | ||

| SU | 2.0 | 0.011 | 0.82 | 5.5 | … | … | … | … | ||

Notes: (i) The baseline model is generated as , with time effects given by for , and . The errors processes for and equations are chi-squared and Gaussian, respectively, are generated as heterogeneous AR(1) processes, and (the degree of correlated heterogeneity) is defined by (8.6). For further details see Section 8.1.3. (ii) The TMG-TE estimators of and are given by (6.9) and (6.11), respectively, and their asymptotic variances are estimated by (A.3.4) and (A.3.7), respectively, in the Appendix. The TMG-C estimators of and are given by (6.20) and (6.17), respectively, and their asymptotic variances are estimated by (6.21) and (6.19), respectively. For the trimming threshold, see footnote (iii) to Table 1. (iii) For GP and SU estimators, see footnote (i) to Table 2. is the simulated fraction of individual estimates being trimmed, defined by (4.7). “…” denotes the estimation algorithms are not available or not applicable.

| Estimator | Bias | RMSE | Size | Bias | RMSE | Size | ||||

| TMG-TE | 0.002 | 0.09 | 6.1 | -0.001 | 0.04 | 4.8 | ||||

| GP | 0.001 | 0.54 | 7.1 | -0.008 | 0.35 | 6.9 | ||||

| TMG-TE | -0.002 | 0.10 | 5.6 | 0.001 | 0.05 | 4.9 | ||||

| GP | 0.004 | 0.15 | 5.7 | 0.001 | 0.07 | 5.0 | ||||

| TMG-TE | -0.006 | 0.10 | 5.7 | 0.000 | 0.05 | 4.9 | ||||

| GP | -0.010 | 0.13 | 5.3 | 0.000 | 0.06 | 4.2 | ||||

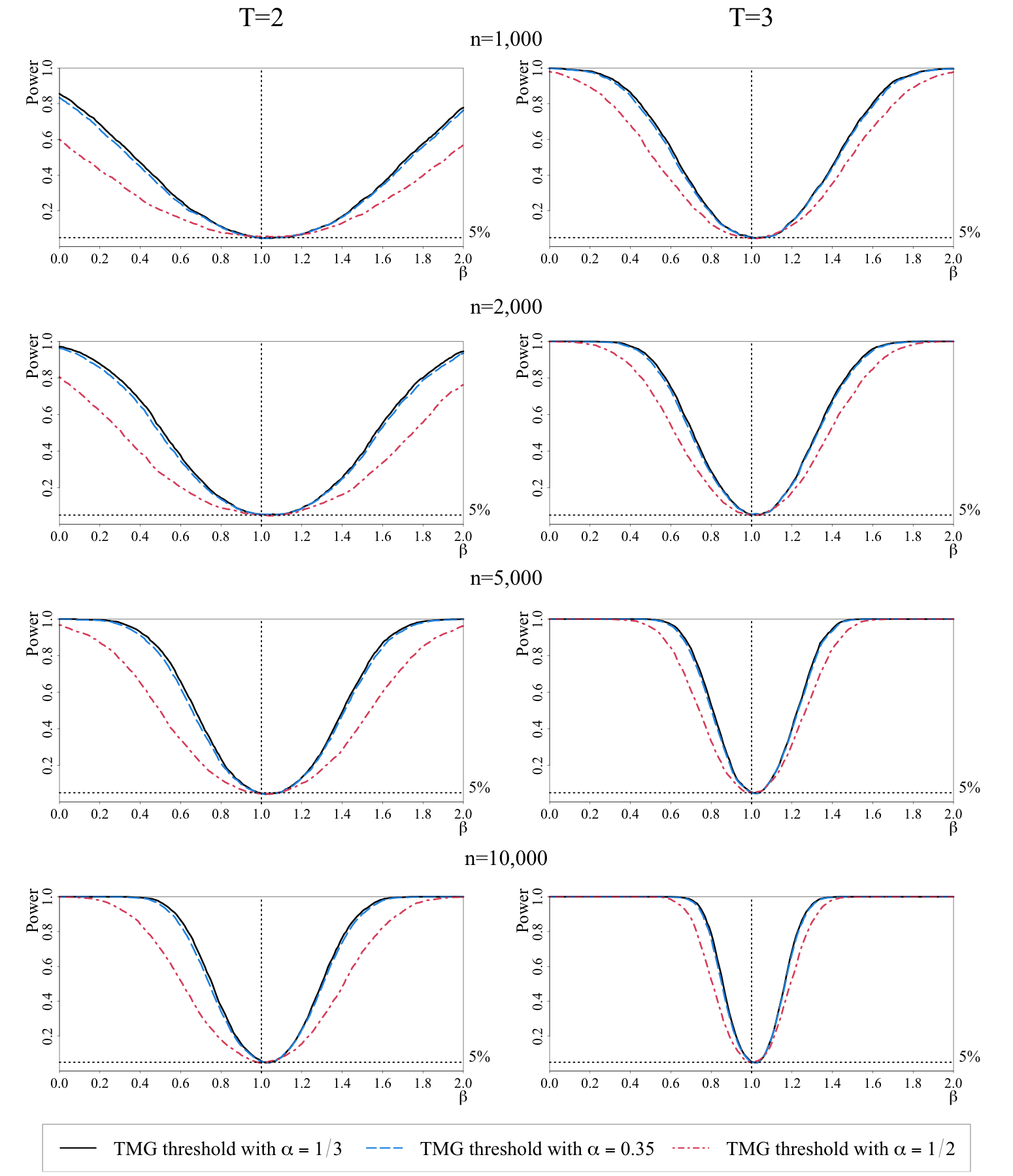

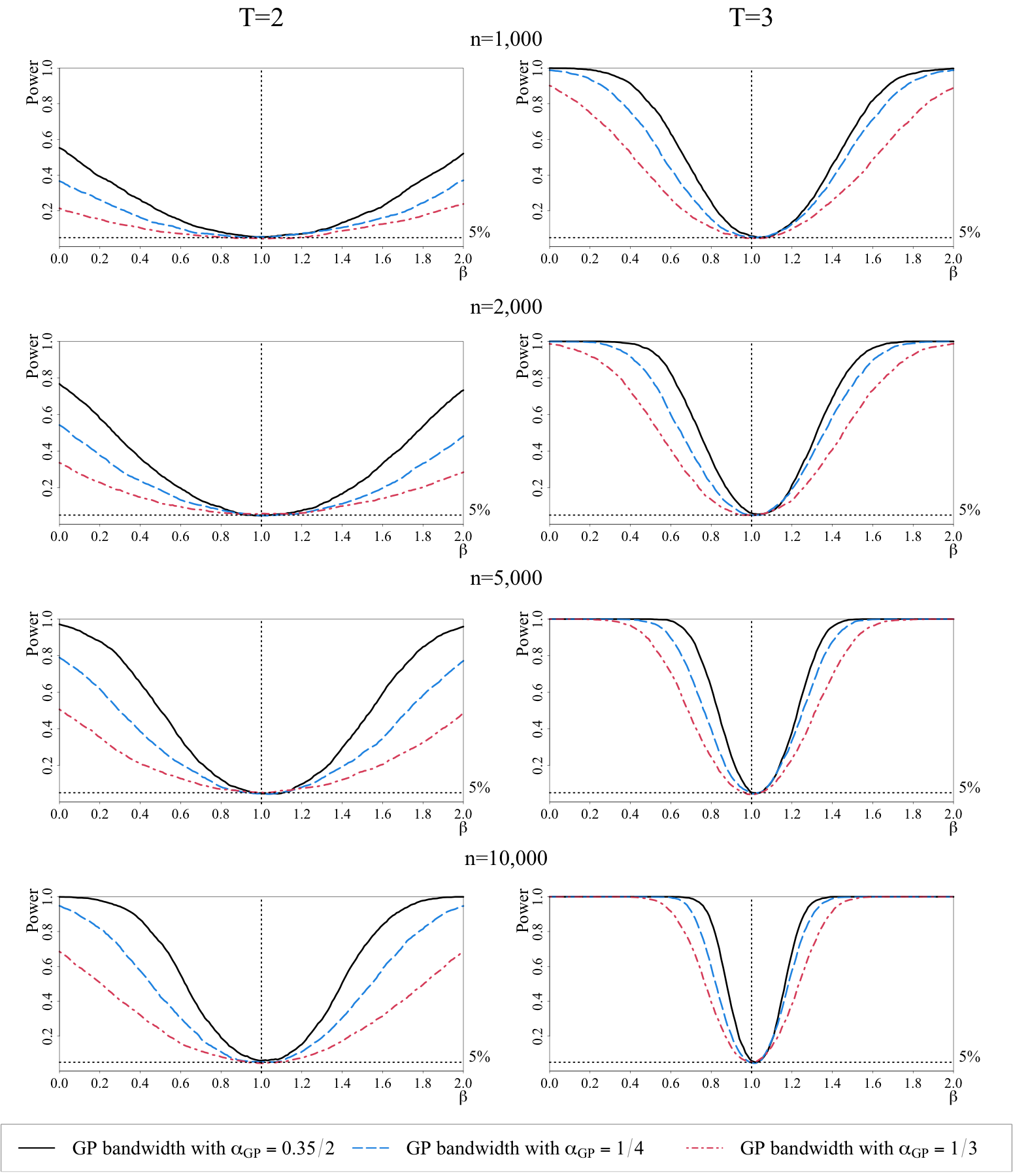

8.2.4 Sensitivity of TMG and GP estimators to the choice of the threshold values

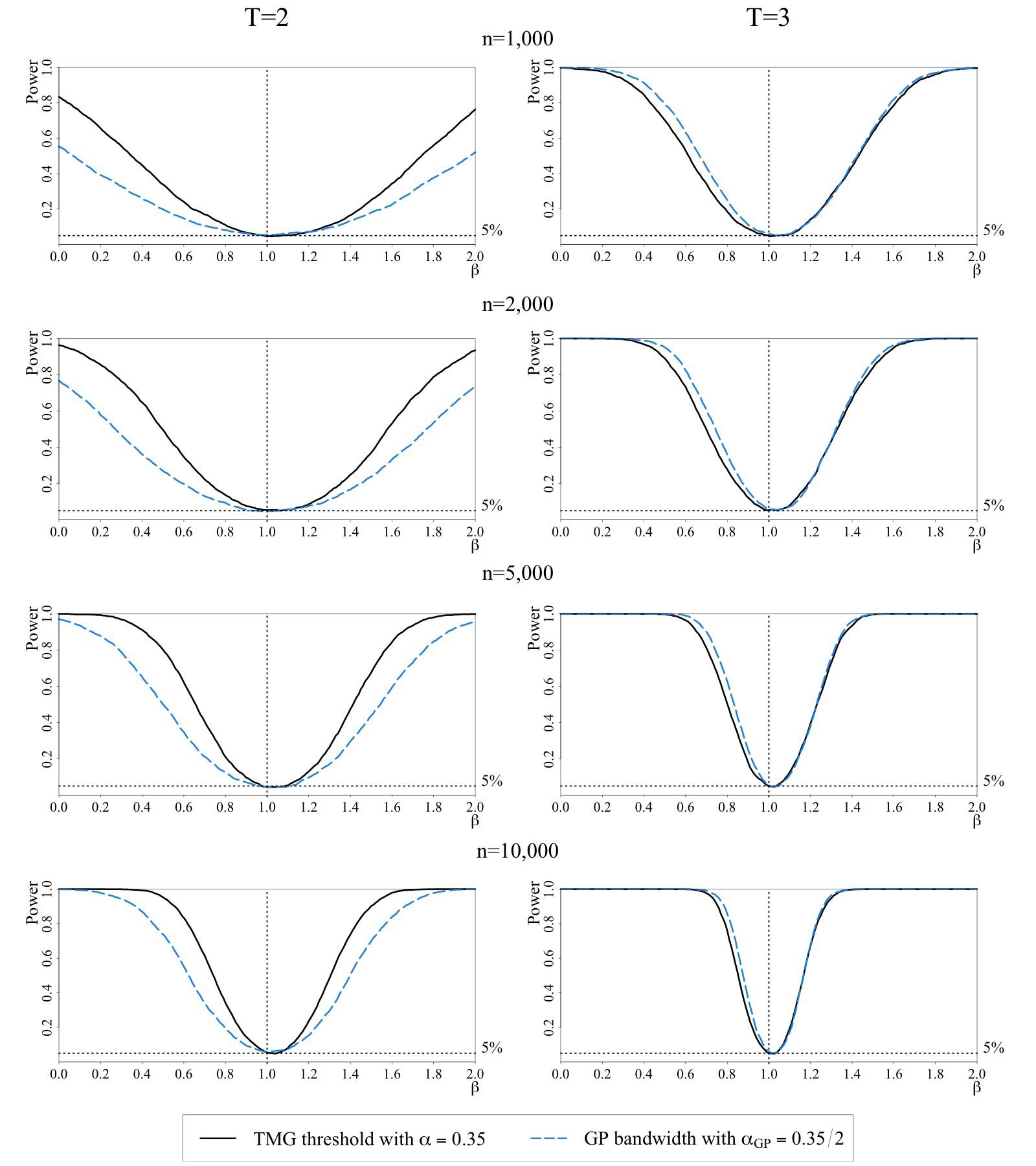

Finally, we consider the sensitivity of TMG and GP estimators to the choice of threshold values. The baseline value of the threshold value for the GP estimator, as recommended by GP.222222See equation (3.1) and the related discussion for the implementation of the GP estimator in sub-section 8.2.2. But for the purpose of comparison with the TMG estimator computed for and , we also consider and . Recall that the bandwidth, , used by GP corresponds to used in the specification of TMG. Hence, corresponds to . For comparability, we decided to consider values of below required by GP’s theory. This allows us to compare GP and TMG focusing on the utility of including both trimmed and untrimmed estimates of in estimation of average treatment effects.

The results are summarized in Section S.4.2 of the online supplement. As can be seen from Table S.5 there is a clear trade-off between bias and variance as and are increased. For , the TMG estimator is biased when (as predicted by the theory), but has a lower variance with its RMSE declining as is increased from to . This trade-off is less consequential when is increased to . The same is also true for the GP estimator. But for all choices of and the TMG performs better in terms of RMSE when . For , TMG and GP estimators share the same trimming threshold when , resulting in identical trimmed fractions for . While RMSEs are similar, the GP estimator exhibits significantly higher bias than the TMG estimator as observations of the trimmed units are not exploited by the GP estimator.

Figure S.2 compares power functions of TMG and GP estimators with . For , a higher trimmed fraction results in a steeper power function for the TMG estimator as compared to that of the GP estimator. When , with the same trimmed fraction, the power function of the GP estimator shifts to the right, away from the true value. The substantial differences in power performance of the TMG estimator with and the GP estimator with are also illustrated in Figure S.3.

The power comparisons of TMG and GP estimators for different values of and are given in Figures S.4 and S.5, respectively, and convey the same message, suggesting that for the TMG estimator the boundary choice of tends to produce the best bias-variance trade-off. Increasing reduces the bias but increases the variance, and the boundary value derived theoretically seems to strike a sensible balance and is recommended.

8.2.5 MC evidence on the Hausman-type test of correlated heterogeneity

| Under | Under | ||||||||||||||

| Homogeneity: | Uncorrelated hetro.: , | Correlated hetro.: , | |||||||||||||

| 1,000 | 2,000 | 5,000 | 10,000 | 1,000 | 2,000 | 5,000 | 10,000 | 1,000 | 2,000 | 5,000 | 10,000 | ||||

| 2 | 4.1 | 4.4 | 5.3 | 5.5 | 5.6 | 5.5 | 4.8 | 5.9 | 26.0 | 39.0 | 69.8 | 90.8 | |||

| 3 | 4.5 | 5.7 | 5.8 | 4.8 | 5.3 | 4.5 | 5.7 | 4.7 | 41.0 | 61.5 | 91.3 | 99.6 | |||

| 4 | 4.9 | 5.7 | 5.6 | 4.9 | 4.8 | 4.5 | 5.5 | 4.7 | 53.5 | 77.2 | 97.8 | 100.0 | |||

| 5 | 5.3 | 4.6 | 4.9 | 5.2 | 4.3 | 4.6 | 4.4 | 4.3 | 63.5 | 86.1 | 99.5 | 100.0 | |||

| 6 | 4.8 | 5.2 | 5.5 | 5.3 | 5.2 | 4.4 | 4.6 | 4.4 | 72.0 | 91.7 | 100.0 | 100.0 | |||

| 8 | 5.0 | 4.8 | 5.0 | 5.3 | 4.6 | 4.9 | 6.0 | 5.7 | 81.1 | 96.2 | 100.0 | 100.0 | |||

Notes: (i) The baseline model for the Hausman-type test is generated as , with correlated with under both the null and alternative hypotheses. The errors processes for and equations are chi-squared and Gaussian, respectively, and are generated as heterogeneous AR(1) processes. For further details see Section 8.1.3. (ii) The null hypothesis is given by (7.1), including the case of homoegenity with and the case of uncorrelated heterogeneity with (the degree of correlated heterogeneity defined by (8.6) and . The alternative of correlated heterogeneity is generated with and . (iii) The test statistic is calculated based on the difference between FE and TMG estimators, given by (7.3). Under , the test statistic is asymptotically distributed as as . For the FE estimator, see footnote (ii) to Table 1. For the TMG estimator, see footnotes (ii) and (iii) to Table 1. Size and power are in per cent.

Table 5 reports empirical size and power of the Hausman-type test of correlated heterogeneity given by (7.3). The left, middle and right panels report the results under homogeneity, uncorrelated heterogeneity and correlated heterogeneity in slope coefficients. In the left and middle panels, the size of the test is around the nominal level of 5 per cent. As shown in the paper, when is strictly exogenous and is mean independent of , FE, MG and TMG estimators are all consistent under homogeneity and uncorrelated heterogeneity, and in this case the Hausman-type test does not have power against uncorrelated heterogeneity. However, in the case where slope coefficients are heterogeneous and correlated with the regressors, the MG and TMG estimators are consistent when they have at least finite second moments, while the FE estimator is biased for all . In this case, we would expect the proposed test to have power, and this is indeed evident in the right panel of Table 5. Also the power of the test rises with increases in even when , illustrating the (ultra) small consistency of the proposed test.

The MC evidence on the performance of our proposed test of correlated heterogeneity in the case of panels with time effects is given in Table S.15 of the online supplement. We consider two versions of the test, depending on how time effects are filtered out, namely TMG-TE and TMG-C estimators (see equations (S.2.15) and (S.2.21)).232323For further details, see Section S.2 in the online supplement. The empirical size and power of these two test statistics are comparable for . More importantly, allowing for time effects has negligible effects on the small sample performance of the test, while the power of the test is slightly lower than the power reported in Table 5 for models without time effects. Increases in and/or result in a rapid rise in power, illustrating the consistent property of the proposed test.

9 Empirical illustration

In this section, we re-visit the empirical application in Graham and Powell (2012) who provide estimates of the average effect of household expenditures on calorie demand, based on a sample of households from poor rural communities in Nicaragua that participated in a conditional cash transfer program Red de Proteccion Social (RPS). The data set is a balanced panel with households observed from 2000 to 2002. We present estimates of the average treatment effects using the following panel data model with time effects:

| (9.1) |

where denotes the logarithm of household calorie availability per capita in year of household , and denotes the logarithm of real household expenditures per capita (in thousands of 2001 cordobas) of household in year . The parameter of interest is the average treatment effect defined by , allowing for possible dependence between and . Correlated heterogeneity could arise for a number of reasons, such as model misspecification, individuals responding strategically to treatments, and common factors that simultaneously affect and the treatment, . It is, therefore, prudent to first test for correlated heterogeneity before estimating by fixed effects, which is the standard approach when is ultra short. We provide test statistics and estimates of for the panels of 2001–2002 and 2000–2002 with and without time effects.

Table 6 reports results of the Hausman-type test of correlated heterogeneity in the effects of household expenditures on calorie demand. The null hypothesis is rejected for both panels covering the periods 2001–2002 and 2000–2002, and irrespective of whether time effects are allowed. As shown in the Monte Carlo experiments, the test only has power against the alternative of correlated heterogeneity. Therefore, these results provide strong evidence of heterogeneity in the treatment effects that are correlated with the level of household expenditures, which in turn sheds doubt on the validity of the FE estimation of the average treatment effect for this application.

| Without time effects | With time effects | |||||||

| 2001–2002 | 2000–2002 | 2001–2002 | 2000–2002 | |||||

| TMG-TE | TMG-TE | TMG-C | ||||||

| Statistics | 5.918 | 7.626 | 5.959 | 6.772 | 7.653 | |||

| -value | 0.015 | 0.006 | 0.015 | 0.009 | 0.006 | |||

| 2 | 3 | 2 | 3 | 3 | ||||

Notes: The test is applied to the average effect in the model (9.1) based on the RPS panel of households. The test statistic for panels without time effects is described in footnote (iii) to Table 5. The test statistics for panels with time effects are based on the difference between the FE-TE and TMG-TE estimators given by (S.2.15) with , and the difference between the FE-TE and TMG-C estimators given by (S.2.21) with . For further details see Section S.2 in the online supplement.

| Without time effects | With time effects | ||||||||

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | ||

| FE | GP | SU | TMG | FE-TE | GP | SU | TMG-TE | ||

| 0.6568 | 0.4549 | 0.6974 | 0.5623 | 0.6554 | 0.4629 | 0.6952 | 0.5612 | ||

| (0.0287) | (0.1003) | (0.1689) | (0.0425) | (0.0284) | (0.1025) | (0.1650) | (0.0424) | ||

| … | … | … | … | 0.0172 | -0.0181 | … | 0.0178 | ||

| … | … | … | … | (0.0063) | (0.0296) | … | (0.0064) | ||

| … | 3.8 | 3.8 | 27.1 | … | 3.8 | 3.8 | 27.1 | ||

Notes: The estimates of and in the model (9.1) are based on the RPS panel of households. The FE estimator is described in the footnote (ii) to Table 1. GP and SU estimators are described in footnote (i) to Table 2. The TMG estimator is described in footnotes (ii) and (iii) to Table 1. The FE-TE estimator is the two-way fixed effects estimator given by (S.2.1) in the online supplement. TMG-TE and TMG-C estimators are described in footnote (ii) to Table 3. is the estimated fraction of individual estimates being trimmed, defined by (4.7). The numbers in brackets are standard errors. “…” denotes the estimation algorithms are not available or not applicable.

Table 7 presents the estimates of based on the panel of 2001–2002 (with ) without time effects (left panel), and with time effects (right panel). The estimates are not affected by the inclusion of time effects but differ considerably across different methods.242424When , is not significant, and adding time effects does not change the estimated average effect. Based on the test results reported in Table 6, the FE estimates are most likely biased. Turning to the trimmed estimators, we find that only the TMG estimator is heavily trimmed with 27.1 per cent of the estimates being trimmed, whilst the rate of trimming is only around 3.8 per cent for GP and SU estimators.252525For the 2001–2002 panel, of the GP estimator is identical to the one reported in Table 3 of Graham and Powell (2012). Graham and Powell (2012) estimated a model with time-varying coefficients, , where are identified by stayers but estimated by near stayers. While is not included in (9.1), the GP estimates we compute are close to the trimmed estimates in Table 3 of Graham and Powell (2012). Focussing on the estimates without time effects, we find the FE estimate, 0.6568 (0.0287), is much larger and more precisely estimated than either the GP or TMG estimates, given by 0.4549 (0.1003) and 0.5623 (0.0425), respectively.262626The bracketed figures are standard errors. Judging by the standard errors, it is also noticeable that the TMG is more precisely estimated than the GP estimate and lies somewhere between the FE and GP estimates. In contrast, the SU estimate of 0.6974 (0.1689) is close to the FE estimate but with a much larger degree of uncertainty. These estimates are in line with the MC results reported in the previous section, where we found that in the presence of correlated heterogeneity FE estimates are biased with smaller standard errors (thus leading to incorrect inference), whilst GP and TMG estimators are correctly centered with the TMG estimator being more efficient.

| Without time effects | With time effects | |||||||

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | ||

| FE | GP | TMG | FE-TE | GP | TMG-TE | TMG-C | ||

| 0.6588 | 0.6034 | 0.5900 | 0.6968 | 0.6448 | 0.6370 | 0.6338 | ||

| (0.0233) | (0.0350) | (0.0284) | (0.0211) | (0.0330) | (0.0263) | (0.0261) | ||

| … | … | … | 0.0727 | 0.0682 | 0.0708 | 0.0682 | ||

| … | … | … | (0.0087) | (0.0123) | (0.0088) | (0.0123) | ||

| … | … | … | 0.1066 | 0.0954 | 0.1054 | 0.0682 | ||

| … | … | … | (0.0080) | (0.0108) | (0.0080) | (0.0123) | ||

| … | 1.2 | 10.9 | … | 1.2 | 10.9 | 10.9 | ||

Table 8 gives the estimates of for the extended panel, 2000–2002 (with ), both with and without time effects. When time effects are included we provide two versions of the TMG estimates (TMG-TE and TMG-C), depending on how time effects are estimated. As in the case of the 2001–2002 panel, the FE estimates are larger than the GP and TMG estimates, but these differences are reduced somewhat, particularly when time effects are included in the panel regressions. Further, as expected, increasing reduces the rate of trimming and brings the GP and TMG estimators closer to one another. The trimming rate for the GP estimator is very small indeed (only 1.2 per cent), as compared to around 11 per cent for the TMG estimator in the case of the 2000–2002 panel. The TMG-TE and TMG-C estimates of the time effects ( and ) are quite close and are both highly statistically significant and positive, capturing the upward trend in the calorie intake.

10 Conclusions

This paper studies estimation of average treatment effects in panel data models with possibly correlated heterogeneous coefficients, when the number of cross-sectional units is large, but the number of time periods can be as small as the number of regressors. We recall that the FE estimator is inconsistent under correlated heterogeneity, and the MG estimator can have unbounded first or second moments when applied to ultra short panels. Thus, the TMG estimator is proposed, where the trimming process is derived by a careful examination of the bias/efficiency trade-off in the asymptotic distribution. Conditions under which the TMG estimator is consistent and asymptotically normally distributed are provided. We also propose new estimators for ultra short panel data models with time effects, distinguishing between cases where and , and derive their asymptotic distributions under the identifying condition that the dependence between heterogeneous slope coefficients and the regressors is time-invariant. Moreover, based on differences between the TMG and FE estimators (without and with time effects), we propose Hausman-type tests of correlated slope heterogeneity which must be applied before using FE or FE-TE estimators in practice.

Using Monte Carlo experiments, we highlight the bias and size distortion properties of the FE and FE-TE estimators under correlated heterogeneity. In contrast, the TMG and TMG-TE estimators are shown to have desirable finite sample performance under a number of different MC designs, allowing for Gaussian and non-Gaussian heteroskedastic error processes, dynamic heterogeneity and interactive time effects in the covariates, and different choices of the trimming threshold parameter, . In particular, since the TMG and TMG-TE estimators exploit information on untrimmed and trimmed estimates alike, they have the smallest RMSE, and tests based on them have the correct size and are more powerful compared with the other trimmed estimators currently proposed in the literature.

The Hausman-type tests based on TMG and TMG-TE estimators are also shown to have very good small sample properties, with their size controlled and their power rising strongly with even when . It is hoped that the new Hausman test provides empirical investigators with a diagnostic test that can be used before the application of the FE-TE estimators that are commonly used in the empirical literature. It is hoped that the use of this diagnostic test can help researchers in avoiding biased estimates and possibly misleading inferences. When the TMG and TMG-TE estimators and the Hausman-type tests of correlated heterogeneity are applied to a panel of households in poor rural communities in Nicaragua, the results provide clear evidence of correlated heterogeneity in the average effect of household expenditures on calorie demand, which sheds doubt on the application of FE-TE estimators to this data set.

Finally, we would like to end by acknowledging that, similarly to the FE-TE estimators, the validity of the TMG-TE and TMG-C estimators requires the so-called parallel trends assumption where time effects are assumed to have homogeneous effects across all individual units in the panel. Relaxing the parallel trends assumption in short panels has been an important area of active research, but most of these contributions either assume homogeneous slopes or restricted forms of slope heterogeneity, or place restrictions on the time effects. The development of techniques for estimation and inference in ultra short panels with correlated heterogeneous slopes and interactive effects is a topic for future research.

References