Hamiltonian Dynamics of Bayesian Inference

Formalised by Arc Hamiltonian Systems

Supplemental Material for ‘Hamiltonian Dynamics of Bayesian Inference Formalised by Arc Hamiltonian Systems’

Abstract

This paper advances theoretical understanding of infinite-dimensional geometrical properties associated with Bayesian inference. First, we introduce a novel class of infinite-dimensional Hamiltonian systems for saddle Hamiltonian functions whose domains are metric spaces. A flow of this system is generated by a Hamiltonian arc field, an analogue of Hamiltonian vector fields formulated based on (i) the first variation of Hamiltonian functions and (ii) the notion of arc fields that extends vector fields to metric spaces. We establish that this system obeys the conservation of energy. We derive a condition for the existence of the flow, which reduces to local Lipschitz continuity of the first variation under sufficient regularity. Second, we present a system of a Hamiltonian function, called the minimum free energy, whose domain is a metric space of negative log-likelihoods and probability measures. The difference of the posterior and the prior of Bayesian inference is characterised as the first variation of the minimum free energy. Our result shows that a transition from the prior to the posterior defines an arc field on a space of probability measures, which forms a Hamiltonian arc field together with another corresponding arc field on a space of negative log-likelihoods. This reveals the underlying invariance of the free energy behind the arc field.

1 Introduction

In Bayesian inference, statisticians elicit a prior distribution over a parameter space of a model that reflects their belief in an appropriate model to describe a phenomenon of interest. Observing data realised from the phenomenon, they update the prior distribution to the posterior distribution by Bayes’ rule. Denote the negative log-likelihood by , making the associated model and data implicit111If the model and data are explicit, we have . Since we assume no specific form of the model and input, we denote the negative log-likelihood simply by .. Most generally, the posterior is a measure absolutely continuous to that has the Radon–Nikodym derivative

| (1) |

If the prior admits a probability density , the posterior can be expressed as a probability density as usual. The measure of the form (1) is also known as a Gibbs measure for a potential with a reference measure (Georgii, 2011).

The posterior, or the Gibbs measure, has a variational characterisation whose origin may be traced back to Gibbs (1902). It is a unique solution of the following variational problem:

| (2) |

where denotes a set of all probability measures on and denotes the relative entropy of from . The functional is called the free energy222More precisely, Jordan, Kinderlehrer and Otto (1997) called the ‘generalised’ free energy in a sense that a reference measure is used, where the (Helmholtz) free energy is recovered when is the Lebesgue measure. in light of the thermodynamical significance. This characterisation has been long known as the Gibbs variational principle (Ellis, 2006) mainly in the context of statistical mechanics (Ruelle, 1967, 1969) and large deviation theory (Dembo and Zeitouni, 2009; Dupuis and Ellis, 2011). Later, it was repeatedly rediscovered and has played a pivotal role in several recent advances of Bayesian inference, such as variational Bayes methods (Attias, 1999; Blei, Kucukelbir and McAuliffe, 2017), PAC-Bayes analysis (Catoni, 2007; Guedj, 2019), and generalised Bayesian inference (Bissiri, Holmes and Walker, 2016). This paper establishes (i) a further variational characterisation of the posterior and (ii) its Hamiltonian dynamical interpretation.

Hamiltonian systems are a fundamental description of dynamical phenomena that obey the law of conservation of energy (Goldstein, Poole and Safko, 2002). A flow of a Hamiltonian system is generated by the Hamiltonian vector field determined by the gradient of a Hamiltonian function. Under sufficient regularity, the value of the Hamiltonian function remains invariant along the flow (Abraham and Marsden, 1987). While Hamiltonian systems are well-established for finite-dimensional topological spaces (Arnold, 1978), this work deals with saddle (i.e. concave-convex) Hamiltonian functions whose domains are infinite-dimensional metric spaces. A chief challenge in formulating Hamiltonian systems in such a setting is to have (a) an appropriate notion that acts as a gradient in an infinite-dimensional domain and (b) the well-defined evolution of a system in a metric topology. To date, Hamiltonian systems have been extended to Banach spaces—or symplectic manifolds built on smooth Banach manifolds (Lang, 1985) more generally—by works of Chernoff and Marsden (1974); Marsden and Hughes (1983). A formulation based on a norm topology is however not suitable for our main application involving dynamics of measures, as illustrated in Section 2. This motivates the development of a novel class of Hamiltonian systems, termed arc Hamiltonian systems, using (a) the first variation of Hamiltonian functions and (b) the notion of arc fields (Calcaterra and Bleecker, 2000) that extends vector fields to metric spaces. A flow of an arc Hamiltonian system is generated by the Hamiltonian arc field determined by the first variation of a Hamiltonian function. We provide a condition for the existence of the flow over , and prove that this system obeys the conservation of energy.

We use arc Hamiltonian systems to study an infinite-dimensional geometrical property associated with Bayesian inference. Denote for simpler presentation. We shall see that the difference of the posterior and the prior is characterised as the first variation of the minimum free energy with respect to :

| (3) |

where the first variation here, formally defined in Section 3, is similar to one often considered in the context of gradient flows (Santambrogio, 2015). We shall show that the first variation , coupled with the negative of the other first variation with respect to , defines an arc Hamiltonian field on a metric space of negative log-likelihoods and probability measures . It generates a flow of the system that follows the first-order approximation similar to Hamilton’s equations in vector spaces:

| (4) |

Our formulation capitalises on a property that the right-hand side stays within the domain of the energy for all , due to the form of the first variations. In such cases, the first-order approximation (4) can determines a flow in a metric topology.

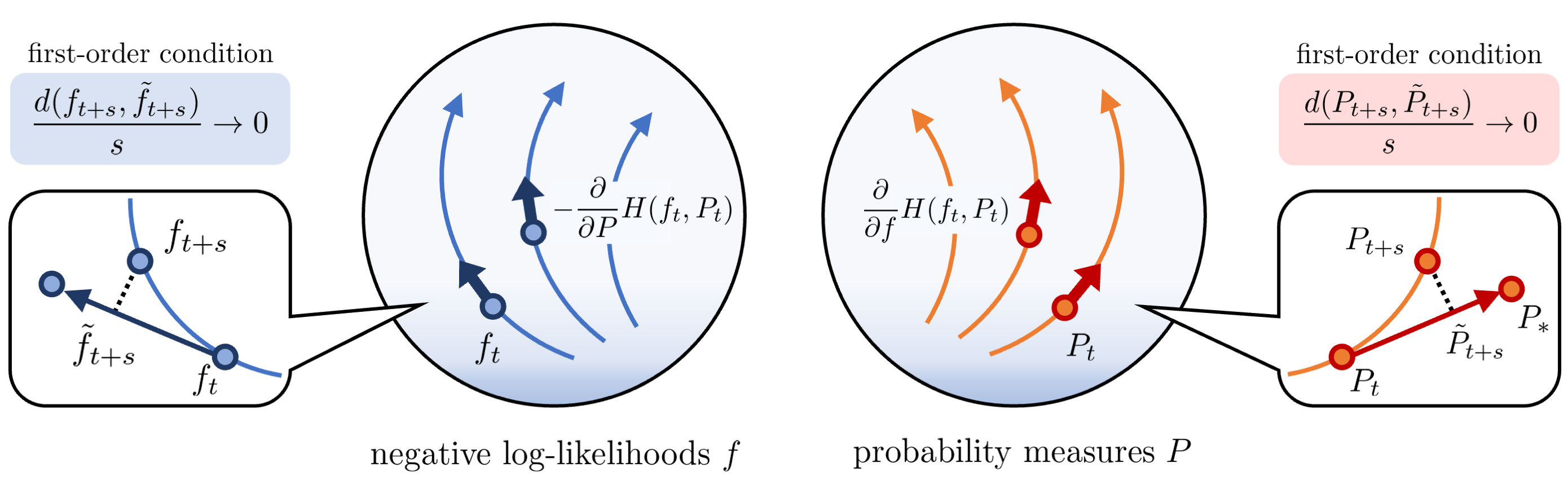

The first-order approximation (4) of driven by the first variation is a transition from to over in the mixture geodesic , where the posterior is defined for . By the belief updating mechanism of Bayesian inference, we can assign this transition over to every probability measure . Our result confers the geometrical significance of such an assignment at every as a Hamiltonian arc field, by introducing another transition driven by the other first variation . In particular, this reveals an underlying invariance of the minimum free energy behind the arc field induced by the belief updating mechanism. See Figure 1 for illustration of this dynamics.

Certainly, there can exist various geodesics to define a transition from to . Finally, it is intriguing to highlight a contrast with a Wasserstein gradient flow of the free energy (Jordan, Kinderlehrer and Otto, 1997). The Wasserstein dynamics describes the evolution of a probability measure over time that minimises the free energy for a fixed potential with reference measure . We have the same Wasserstein dynamics for a class of free energies of potentials up to a constant 333This is because the minimiser is invariant to any constant term of the potential due to the normalisation that cancels out the constant as follows: .. We suppose that the free energy is defined with a ‘mean-zero’ potential with . The minimum free energy equals to the free energy at the minimiser :

where this equality is known as the Gibbs or Donsker-Varadhan variational formula (Dupuis and Ellis, 2011). In contrast to the Wasserstein dynamics that minimises the free energy , our result reveals the existence of the dynamics of the potential and reference measure that keeps the minimised free energy constant.

The rest of the paper is structured as follows. Section 2 introduces basic notations and useful preliminaries for the development of arc Hamiltonian systems. In Section 3, we establish the framework of arc Hamiltonian systems, providing the theory on the existence and the energy-conserving invariance of their flow. The general framework of arc Hamiltonian systems may be of independent interest in many fields, such as convex analysis, information theory, and statistical physics. In Section 4, we present the system of the minimum free energy formalised by arc Hamiltonian systems. We draw our conclusion in Section 5.

2 Background

We provide useful preliminaries to develop arc Hamiltonian systems. Section 2.1 introduces a set of basic notations and terminologies. Section 2.2 briefly recaps a standard Hamiltonian system in the Euclidean space , illustrating a few limitations of an infinite-dimensional extension based on a norm topology for our application. Finally, Section 2.3 recaps the notion of arc fields established by Calcaterra and Bleecker (2000), which we capitalise on to formulate the evolution of an arc Hamiltonian system in a metric topology.

2.1 Notations and Terminologies

We introduce basic notations and terminologies.

Functional-Analytic

By a “curve”, we mean a map from a time interval to a metric space, where it can be equivalently thought of as a time-dependent variable in a metric space. We use subscripts to indicate the time argument of a curve; for example denotes a curve. A curve is said continuous if it is a continuous map. We denote by the limit with respect to a scalar approaching to from the right. For any metric space , we denote by an open ball in around a point with a radius . For any map defined for a set and the time interval , we use subscripts to indicate the time argument of , that is, denotes the value at .

Measure-Theoretic

Let be a separable completely metrizable space (i.e. a Polish space). By a “measure”, we mean a non-negative Borel measure on . By a “signed measure”, we mean a signed Borel measure on . Any signed measure admits the Jordan decomposition by two uniquely associated (non-negative) measures and . For each signed measure , we define a measure —often referred to as the variation of — by . This means that for any Borel set . A signed measure is said finite if and only if the measure is finite. If a measure admits the Radon-Nikodym derivative with respect to a measure , we indicate the relationship by for better presentation. Denote by , , and a set of all finite signed measures, all finite measures, and all probability measures.

2.2 Hamiltonian Systems

Hamiltonian systems have an extensive history of the development; we refer readers to Goldstein, Poole and Safko (2002) for a detailed introduction of classical mechanics and to Arnold (1978) for the rigorous mathematical foundation. Hamiltonian systems enable us to describe the evolution of the objects through the first-order evolution equation, by introducing a variable called the momentum. For illustration, consider an object moving in whose location at time is denoted . The momentum, denoted , can be associated with a physical quantity calculated by the product of the mass and velocity at time . A Hamiltonian function corresponds to the total energy that the system has at each state . How the pair of the location and momentum evolves over time is determined through Hamilton’s equation:

| (5) |

where and denote the gradient operator with respect to the first and second argument. Hamilton’s equation (5) is a differential equation driven by the Hamiltonian vector field , which can be solved as an initial value problem. Under sufficient regularity, it generates a unique solution flow from any initial state in the domain . In particular, any flow generated by the Hamiltonian vector field conserves the energy, meaning that the value of the Hamiltonian function remains constant along the flow. Figure 2 illustrates a Hamiltonian system of a simple pendulum; it can be observed that the values of the Hamiltonian function remain constant along every generated flow.

Chernoff and Marsden (1974)—and later Marsden and Hughes (1983) for application to mechanics of elastic materials—established an infinite-dimensional extension of Hamiltonian systems to Banach spaces and, more generally, to symplectic manifolds built on smooth Banach manifolds. Here, we do not consider the case of Banach manifolds. As Kriegl and Michor (1997) and Schmeding (2022) pointed out, there are known limitations of Banach manifolds. For example, Eells and Elworthy (1970) proved that an infinite-dimensional smooth Banach manifold is smoothly embedded as an open set in a Banach space used to define the atlas444Although an atlas of a Banach manifold can be defined using multiple Banach spaces in principle, the Banach spaces turn out to be all isomorphic in most cases to guarantee Fréchet-differentiability. This means that it suffices to use one Banach space to define an atlas of a Banach manifold (see Lang, 1985, p.22).. Analysis on smooth Banach manifolds then reduces to that on Banach spaces.

Consider a setting where an object of interest belongs to a Banach space . In the extended Hamiltonian system, the evolution of the system is governed by an evolution equation driven by a map which depends on the gradient of the Hamiltonian function analogous to (5) but taken in a sense of the Fréchet derivative under appropriate conditions of and . By the Cauchy-Lipschitz theorem (e.g. Brezis, 2011), the evolution equation admits a unique solution from any initial state if the map is Lipschitz continuous in . However, this formulation based on a norm topology is not suitable for dynamics involving the set of measures . In a Banach space of signed measures under e.g. the total variation norm (Cohn, 2013), it is easy to prove that the subset has no interior point. That is, if we use the norm topology on , no open set can be defined inside to use important topological notions—such as the Fréchet derivative or local Lipschitz continuity—of functions defined only on . One trivial approach to define open sets inside is to use a metric topology on instead of the norm topology introduced to the vector space . For example, the set will be a metric space under the total variation metric on defined by restricting the norm distance to . This motivates us to introduce a metric on the domain of interest and define the evolution within the metric space. To achieve this, we capitalise on the notion of arc fields (Calcaterra and Bleecker, 2000) recapped next.

2.3 Arc Fields

The notion of arc fields (Calcaterra and Bleecker, 2000), that extends vector fields to metric spaces, is used to formulate an analogue of Hamiltonian vector fields and Hamilton’s equation in metric spaces. The underlying idea behind arc fields has a close connection to mutational equations (Aubin, 1999; Lorenz, 2010) whose common application includes the evolution of set-valued objects and objects that belongs to complicated regions of vector spaces (Aubin, 1993). To illustrate the idea, consider a vector field in a Banach space and a solution curve of the corresponding evolution equation . At each , define a curve over time . Informally, the evolution equation can be thought of as the first-order approximation of the solution curve at each over small , specified by the curve :

A key observation is that the vector-space structure of the set —where the curve belongs—is not essential in this formulation. In the above condition, consider that the vector space is replaced with any set, such as , and the norm is replaced with a metric on the replaced set . The above condition can be still well-defined if we have a premise that the curve stays within the set over all in some interval. This observation leads to the extension of vector fields to metric spaces.

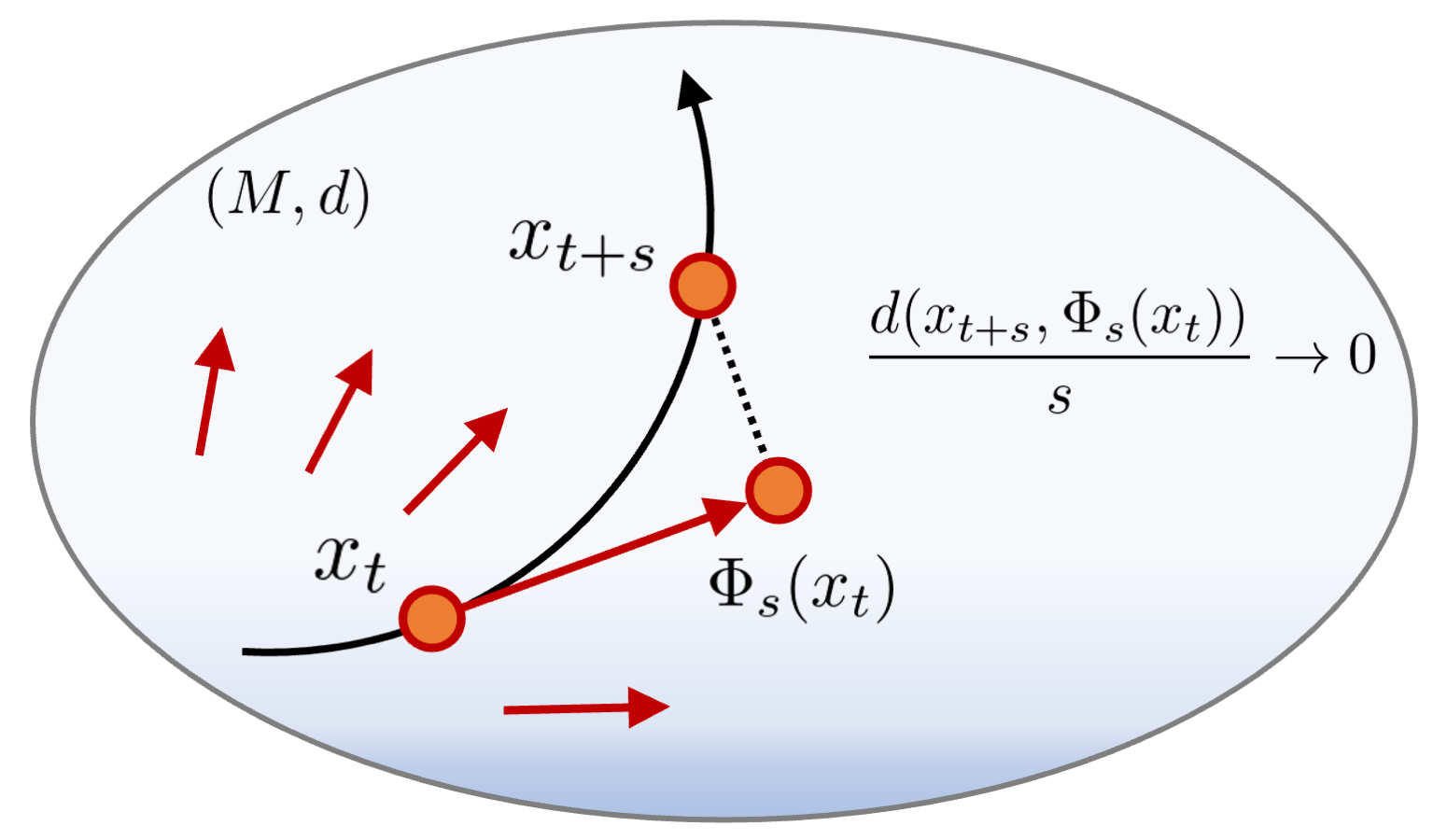

Given a metric space , consider a map that satisfies for all , where we recall that denotes the value of at . To each point , this map is considered to assign a curve over in that starts from . Calcaterra and Bleecker (2000) was concerned with the existence of a curve in that satisfies the following first-order approximation at each :

| (6) |

To study the existence, Calcaterra and Bleecker (2000) focused on a class of sufficiently regular maps , called arc fields, that satisfies a continuity condition in (7) below. A curve in from some initial point that satisfies the condition (6) of an arc field over some interval is then called a solution of the arc field .

Definition 1 (Arc Field).

An arc field on a metric space is a map that satisfies that for all and that

| (7) |

at each for sufficiently small.

See Figure 3 for illustration of a solution of an arc field . See Appendix A for a summary of the theoretical results of Calcaterra and Bleecker (2000) relevant to the development of arc Hamiltonian systems. A flow of an arc Hamiltonian system is formulated as a unique continuous solution of the Hamiltonian arc field associated with the system.

3 Arc Hamiltonian Systems

Extending Hamiltonian systems to infinite-dimensional metric spaces may open up a new horizon for formulating the dynamics of intriguing phenomena. A focus in this work is on saddle Hamiltonian functions whose domains are equipped with metrics. This section will establish the general framework of arc Hamiltonian systems. The first variation (c.f. Section 3.1) of a Hamiltonian function determines an arc field, called Hamiltonian arc field (c.f. Section 3.2), that generates a flow of the system in the metric space. It will be shown that the generated flow obeys the conservation of energy.

In Section 3.1, we present the definition of the first variation based on a convex-analytic formulation. In Section 3.2, we provide the rigorous construction of arc Hamiltonian systems. Section 3.3 shows the existence of a flow generated by a Hamiltonian arc field, followed by Section 3.4 establishing the conservation of energy by the generated flow. Under sufficient regularity, a condition of the existence of the energy-conserving flow reduces to local Lipschitz continuity of the first variation of a Hamiltonian function. Before moving on to the first subsection, we introduce convex-analytic preliminaries below.

Convex-Analytic Preliminaries

Define the extended real number . It is standard convention in convex analysis to consider extended-valued functions from a vector space to . We denote by a subset of where an extended-valued function takes a finite value in . An extended-valued function is said convex if (i) is a non-empty convex set and (ii) holds for any and . An extended-valued function is said concave if (i) is convex. Any function defined on a subset of can be identified as an extended-valued function by setting for all .

3.1 First Variations

The gradient of functions in a general topological space is characterised as an element of the topological dual. For example, the topological dual of is identical to itself and hence the gradient of functions in belongs to . First, we recap definition of dual pair (Aliprantis and Border, 2006, Section 5.14) that plays a fundamental role in defining a gradient in infinite-dimensional convex analysis.

Definition 2 (Dual Pair).

A dual pair, denoted , is a pair of vector spaces and together with a bilinear functional that satisfies

-

•

if for each , then ;

-

•

if for each , then .

The bilinear functional is called the duality of the dual pair .

A dual pair equips each and with topologies—called the weak and weak∗ topologies, respectively—that turn and into the topological dual of each other. A large class of vector spaces can be coupled as the mutual topological dual through an appropriate dual pair; see (Aliprantis and Border, 2006, Section 5.14) for examples of common dual pairs. A dual pair we consider in Section 4 is one for functions and measures in whose duality is given by (e.g. Müller, 1997).

In the rest of Section 3, let be an arbitrary dual pair. It suffices to consider convex or concave functions to define a gradient we use for saddle Hamiltonian function. The directional derivative of at in direction is defined by

| (8) |

One of the most common notions of gradients in infinite-dimensional convex analysis is the Gâteaux gradient555The Gâteaux gradient may be called by a different terminology in other literatures. For example, Rockafellar (1974) simply called it the gradient and Ekeland and Témam (1999) called it the Gâteaux-differential.. If there exists a unique element s.t. the limit of (8) satisfies

| (9) |

the unique element is called the Gâteaux gradient of at . The linear functional is called the Gâteaux derivative of at . A gradient we use is a weaker version of the Gâteaux gradient that requires the equality (9) to hold only for directions s.t. stays within over all . This ensures that the value of in the directional derivative (8) is finite for all small to take the limit in . Such a version is often used and called first variation in the context of Wasserstein gradient flows (e.g. Santambrogio, 2015, Chapter 7.2) for functions whose domain is a set of probability measures in the vector space of the signed measures . What first variation refers to may differ in each field. Now, we introduce our definition of first variation.

Definition 3 (First Variation).

Given a convex or concave function , let denote a set at each . If there exists a unique element s.t. the directional derivative of at in (8) satisfies that

| (10) |

we call the unique element the first variation of at . We refer the function to as the variational derivative of at .

Note that, if , we have for all because is expressed as a convex combination in the convex set . Note also that the set is never empty; given any , a point is a trivial element of . If , the first variation coincides with the Gâteaux gradient by definition.

Remark 1.

The first variation are immediately defined for convex or concave functions in the other space by interchanging the symbols and throughout Definition 3 and replacing with in (10).

3.2 Definition of Arc Hamiltonian Systems

Hamiltonian systems describe the dynamics of a paired variable in some space. We consider a setting where the variable belongs to a subset in the product space . A Hamiltonian function on is regarded as an extended-valued function in convex-analytic manner.

The framework of arc Hamiltonian systems is developed for saddle Hamiltonian functions. An extended-valued function is said saddle if, at each ,

-

•

for fixed , the function is concave;

-

•

for fixed , the function is convex.

Denote by the first variation of the concave function at . Denote by the first variation of the convex function at . It is convenient to introduce a condition, compatibility, of a saddle function to be used in arc Hamiltonian systems. In what follows, the duplet is referred to as the symplectic variation666It is possible to define the symplectic variation as alternatively. of a saddle function .

Definition 4 (Compatibility).

A saddle function is said compatible if, at each , the symplectic variation exists and satisfies for all .

We then equip the domain with a metric to define the Hamiltonian arc field associated with the compatible Hamiltonian function .

Definition 5 (Hamiltonian Arc Field).

Given a compatible function and a metric on the domain , a map defined by

is called the Hamiltonian arc field on if it is an arc field on .

The Hamiltonian arc field acts as an analogue of a Hamiltonian vector field in the metric space . We will see in Section 3.4 that a solution of the Hamiltonian arc field —i.e., a curve that satisfies the condition (6) of —is an energy-conserving flow in . We refer the condition (6) of the Hamiltonian arc field to as the arc Hamilton equation.

Definition 6 (Arc Hamiltonian System).

Let be compatible and let be a metric on the domain . We call the tuple an arc Hamiltonian system if the Hamiltonian arc field on exists. Given an initial state , if there exists a unique continuous solution that satisfies the arc Hamilton equation

| (11) |

from in some interval , the solution is called a flow of the system from . The flow is said global if .

One of our main contributions is this rigorous formulation of the novel class of Hamiltonian systems in infinite-dimensional metric spaces. We briefly discuss a numerical discretisation scheme of the arc Hamilton equation (11). One of the most straightforward approaches is the first-order discretisation scheme. Given a small , a flow generated by the system is approximated by the following recursive formula starting from :

| (12) |

Next, we turn our attention to the condition under which there exists a global flow generated by a Hamiltonian arc field from any point in the domain .

3.3 Existence of Flows

By definition, a flow of an arc Hamiltonian system is a unique continuous solution of the Hamilton arc field from a given initial state. Calcaterra and Bleecker (2000) established a condition of a general arc field , under which a unique solution of the arc field exists from any initial state. First, we adapt their result to arc Hamilton fields to provide general conditions of the existence of global flows. Second, we consider a convenient setting where a metric on has an extension to a norm-induced metric on . In this setting, we can reduce the general condition provided first to local Lipschitz continuity of the map from to .

In the rest of Section 3, let be a complete metric space s.t. . Let be a compatible function s.t. . Let be a map defined by at each and .

Our first theorem shows the existence of global flows of the system. We adapt the result in Calcaterra and Bleecker (2000) by relaxing their original condition; see Appendix A for a summary of their result and the relaxation of the original condition. Recall from Section 2.1 that denotes an open ball in .

Assumption 1.

For some and , at each there exist a radius and a length s.t.

-

1.

, and is upper bounded, for all and all ;

-

2.

, and is upper bounded, for all and all .

Assumption 2.

For the following function

at each there exist a radius and two constants s.t. we have for all .

Theorem 1 (Existence of Global Flow).

Proof of Theorem 1.

See Section B.1. ∎

We define to simplify the notation hereafter in Section 3. The condition in Assumptions 1–2 is stated in a highly general form. Nonetheless, our second theorem shows that the condition reduces to local Lipschitz continuity of the map when the metric on admits an extension to a norm-induced metric on . Clearly, a metric , that is defined by restricting some norm on to , immediately admits an extension to a norm-induced metric of on . Such metrics are common in spaces of measures; for example see (Müller, 1997) for integral probability metrics.

Assumption 3.

The following conditions hold:

-

1.

there exists a norm-induced metric on , to which the metric on can be extended;

-

2.

the map is locally Lipschitz continuous from to , that is, at each there exist a radius and a constant s.t.

(13) holds for all .

Proof of Theorem 2.

See Section B.2. ∎

Remark 2.

While the metric space is supposed to be complete, the metric space does not need to be complete. Consider the space of measures for example. There are many common metrics on that can be extended to norm-induced metrics on the vector space of signed measures (e.g. Müller, 1997). However, the resulting norm space may no longer be complete; see (Bogachev, 2006, p.192) for the case of the Kantorovich–Rubinstein metric. 3 is applicable without completeness of .

By Theorems 1–2, local Lipschitz continuity of the map implies the existence of a global flow of the system from any initial state. It gives a metric-space analogue of the Cauchy-Lipschitz theorem (Brezis, 2011). The analogy was discussed in Calcaterra and Bleecker (2000) for an evolution equation in a Banach space defined by a Lipschitz continuous vector field. Our result demonstrates the analogy for a metric space using only local Lipschitz continuity of the map .

3.4 Conservation of Energy

An important property of regular Hamiltonian systems is that they obey the law of conservation of energy, meaning that the value of a Hamiltonian function remains constant along any flow of the system. Now we shall establish that arc Hamiltonian systems are endowed with this invariance to obey the law of conservation of energy. This can be shown under the following continuity conditions of .

Assumption 4.

The following conditions hold:

-

1.

the function is locally Lipschitz continuous in , that is, at each there exists a radius and a constant s.t.

(14) holds for all .

-

2.

convergence in implies that (i) for each and (ii) for each .

Theorem 3 (Conservation of Energy).

Suppose the tuple is an arc Hamiltonian system. Under 4, if a flow of the system exists in some interval , the value of the Hamiltonian function along the flow is constant in .

Proof of Theorem 3.

See Section B.3. ∎

Note that Theorem 3 holds for any length including . Combining Theorem 1 with Theorem 3 establishes the fact that the arc Hamiltonian system generates energy-conserving flows in everywhere in the metric space .

Finally, we revisit the convenient setting of 3. In this setting, 4 reduces to local Lipschitz continuity of the map if we impose an additional regularity on the metric on as in 5. The following theorem combines Theorems 1–3 under this setting. It provides a sufficient condition for the existence of energy-conserving flows, which is easy to verify for our application presented in the next section.

Assumption 5.

There exists a norm on and a norm on that satisfy for any . The norm-induced metric on in 3 is defined as .

Theorem 4.

Proof of Theorem 4.

See Section B.4. ∎

This completes the construction and theoretical development of arc Hamiltonian systems.

4 Hamiltonian Dynamics of Bayesian Inference

We shall present an arc Hamiltonian system of the minimum free energy defined in a metric space of negative log-likelihoods and probability measures on . We derive the symplectic variation of the minimum free energy . It determines the Hamiltonian arc field on that generates flows of negative log-likelihoods and probability measures . We reveal the underlying invariance to conserve the free energy.

Recall that the main components to construct an arc Hamiltonian system are:

-

1.

a dual pair that contains a domain of interest;

-

2.

a domain and metric to constitute a complete metric space ;

-

3.

a compatible Hamiltonian function over the domain .

In Section 4.1, we define a dual pair used throughout this section. In Section 4.2, we detail a metric space of negative log-likelihoods and probability measures , in which the minimum free energy is defined. In Section 4.3, we show the compatibility of the minimum free energy and the generation of the energy-conserving flows in the metric space . Finally, Section 4.4 provides a visual illustration of the generated flow.

Remark 3.

Recall from Section 2.1 that the only assumption of the space , on which functions and measures are defined, is to be separable and complete metrizable. Hence, all the results in this section hold regardless of whether is finite or infinite dimensional. Note that we assume no specific form of probability models of negative log-likelihoods , where they are simply viewed as functions on . Functions to be contained in the domain will be specified by their tail-growth condition. Hence, the ‘posterior’ of the form (1) in our result includes general Gibbs measures or pseudo-posteriors.

4.1 Dual Pair

First, we define a dual pair consisting of a vector space of functions and a vector space of signed measures on . A common condition to construct such a dual pair is the growth-rate condition of functions and the moment condition of signed measures . The following spaces and are often referred to as a weighted function space and a weighted measure space (Kolokoltsov, 2019), where a given weight function specifies the maximum growth-rate of functions.

Definition 7 (Weighted Spaces).

Given a continuous function that is lower bounded as over ,

-

•

let be a vector space of all measurable functions s.t. ;

-

•

let be a vector space of all signed measures s.t. .

Define a bilinear functional by the integral

| (15) |

under which the pair of the vector spaces and constitutes a dual pair .

The proof that the vector spaces and form a dual pair under the duality (15) can be found in (Müller, 1997, Lemma 2.1). For example, if setting for some when , the space represents all measurable functions up to the -th order polynomial growth; the space represents all signed measures endowed with the -th moment condition. A choice of the weight function is arbitrary for all the results in this work.

4.2 Domain of Minimum Free Energy

In the rest of Section 4, let be the dual pair in Definition 7. The minimum free energy is defined on a metric space of functions in and measures in . We specify the condition of the domain as follows.

Assumption 6.

Let be a set of all s.t.

-

•

is a continuous function that satisfies ;

-

•

is a probability measure.

Since due to c.f. Definition 7, the above condition on can be understood as (i) grows faster than and (ii) is lower bounded by . These two conditions are not restrictive for most negative log-likelihoods:

-

•

The growth of in the condition (i) is slower than any small -th order polynomial () if the weight function is of any -th polynomial order ()777For illustration, consider only in . If , we have . It is easy to verify—e.g., by L’Hôpital’s rule—that grows slower than any -th order polynomial..

-

•

It it natural to assume that a negative log-likelihood has some lower bound because it outght to be minimisable if the maximum likelihood estimator exists. We suppose in the condition (ii) without loss of generality. For a negative log-likelihood whose value may fall below , we can consider a version shifted by a large constant . The minimum free energy is invariant to any constant term of because it is defined with a ‘mean-zero’ transform that cancels the constant :

For example, consider a normal location model in , whose negative log-likelihood is given by for any datum . This negative log-likelihood is contained in if we set for any .

We specify a metric on the domain that determines convergence of a flow evolving in the domain . We use the product metric of the weighted uniform metric for the functions and the weight total variation metric for the measures as below.

Assumption 7.

The weighted uniform metric is a natural choice that allows functions to grow up to the rate of the weight function . The weighted total variation metric is topologically stronger than most of the other common metrics for measures . It controls the standard total variation metric and the Kantorovich–Rubinstein metric. It also controls the Wasserstein metric given an appropriate weight function (Villani, 2009). If a flow of an arc Hamilton system exists under some metric , the flow exists under any other metric weaker than . This is because the convergence in (11) under the metric immediately implies the convergence under any other weaker metric. Therefore, the existence of a flow under 7 is sufficient for the existence in any other weaker metrics.

Finally, we show that the metric space is complete.

Proof of Proposition 1.

See Section C.1. ∎

This completes specification of the domain of the minimum free energy.

4.3 System of Minimum Free Energy

We shall derive the first variation of the minimum free energy. We then show the generation of the energy-conserving flows by the corresponding Hamiltonian arc field. First, we provide a formal definition of the minimum free energy.

Assumption 8.

All the values of outside the domain are set to in convex-analytic manner. It takes a finite value in inside the domain , where the integral inside the logarithm function is positive and finite because is non-negative and is a probability measure. The next proposition confirms that the minimum free energy is saddle.

Proposition 2.

Suppose 8. The function is saddle.

Proof of Proposition 2.

See Section C.2. ∎

We derive a form of the symplectic variation of the minimum free energy . In addition, we confirm that is compatible (c.f. Definition 4). Recall from Section 2.1 that, if a measure admits the Radon-Nikodym derivative with respect to a measure , we use a notation for better presentation.

Theorem 5.

Proof of Theorem 5.

See Appendix D. ∎

Proposition 3.

Suppose 8. The function is compatible.

Proof of Proposition 3.

See Section C.3. ∎

This result establishes the characterisation of the difference of the posterior and the prior as the first variation . Now, we have the domain , the metric , and the compatible Hamiltonian function to construct the arc Hamiltonian system of the minimum free energy. We arrive at a main result on the generation of the flow everywhere in that obeys the invariance to conserve the minimum free energy.

Theorem 6.

Proof of Theorem 6.

See Section C.4. ∎

This result provides a fruitful insight into infinite-dimensional geometrical properties associated with Bayesian inference. By Theorem 5, the Hamiltonian arc field is given by

The Hamiltonian arc field consists of the arc field on the space of negative log-likelihood and the arc field on the space of probability measures.

Remark 4.

Our result confers a geometrical significance of the transition from the prior to the posterior in the mixture geodesic over . Assignment of this transition to every probability measures acts as a certain field on the space of probability measures. That field is the arc field driven by the first variation of the minimum free energy. It forms the Hamiltonian arc field with another arc field driven by the other first variation . Our result reveals the underlying invariance of the conservation of the minimum free energy. Figure 1 illustrates this dynamics.

Remark 5.

As aforementioned in Section 1, the minimum free energy equals to the free energy at the minimiser for the mean-zero potential . Our result formalises the dynamics of the potential and reference probability measure of the Gibbs measure that conserves the value of the free energy over time .

4.4 Illustration of Generated Flows

While our results are all theoretical, we can approximately visualise a flow of the system of the minimum free energy. We first consider two discrete cases where the parameter space is (i) a set and (ii) a set , so that the flow and the simplectic variation can be visualised in the Euclidean space. We then consider a continuous case , where we visualise approximated trajectories of the infinite-dimensional flow from two different initial state .

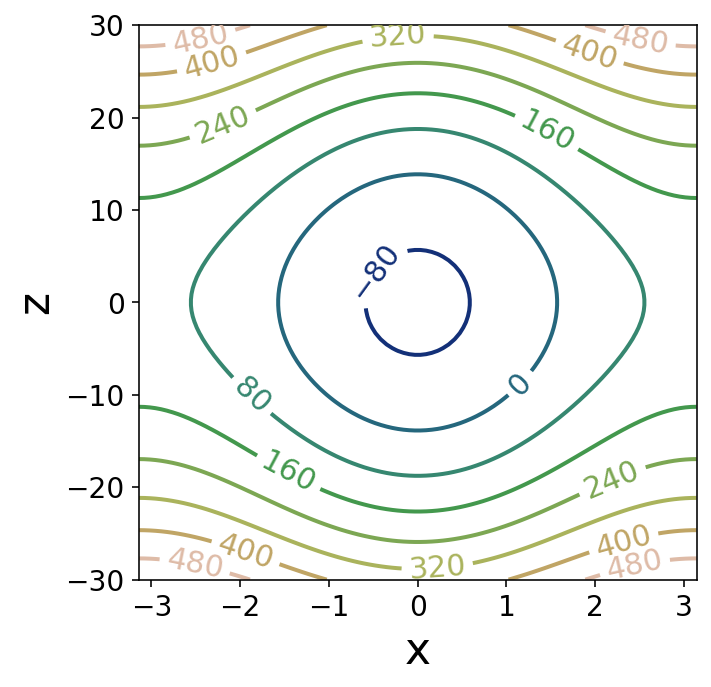

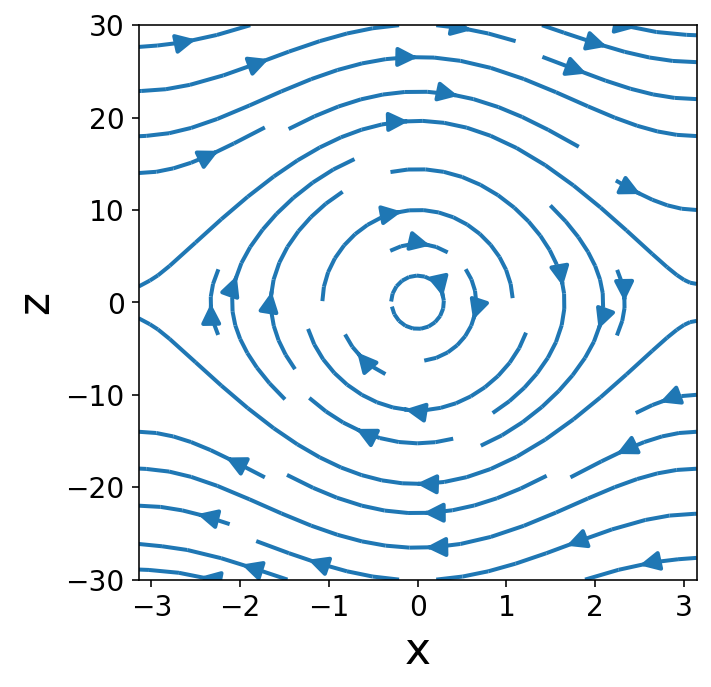

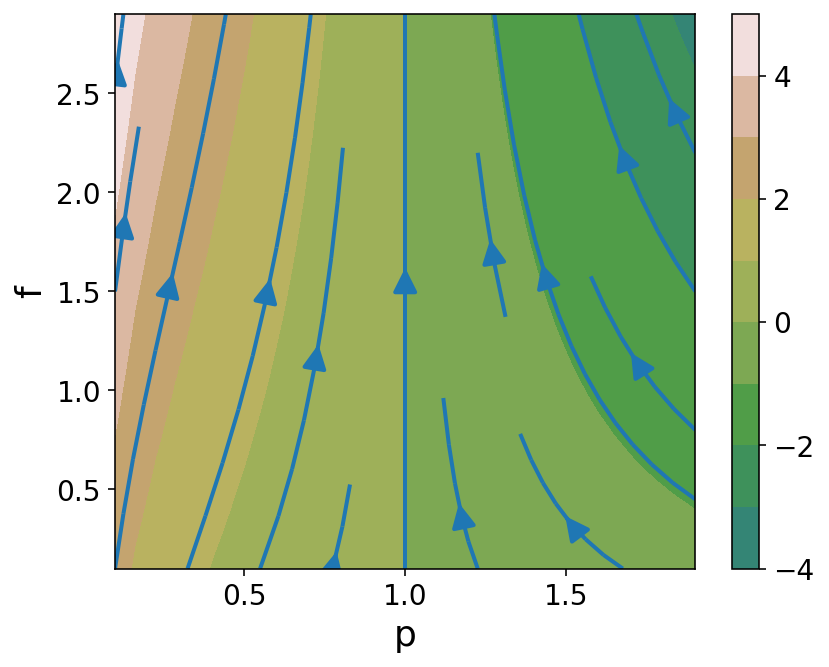

In the first discrete case , functions and probability measures on are identified as scalars in the Euclidean space . Here, probability measures on all reduce to ; for visualisation purpose we extend the minimum free energy to non-probability measures , so that we can plot the value and the flow of the minimum free energy over a two-dimensional domain . Figure 4 shows the flows driven by the simplectic variation and the value of the extended minimum free energy on . It can be observed that all flows run along the contour line where is constant, and that the flow in the domain where is the probability measure, i.e. , stays within the domain.

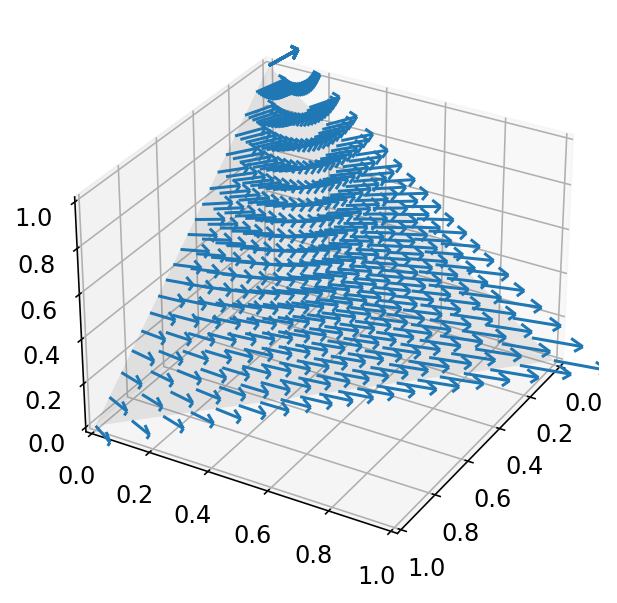

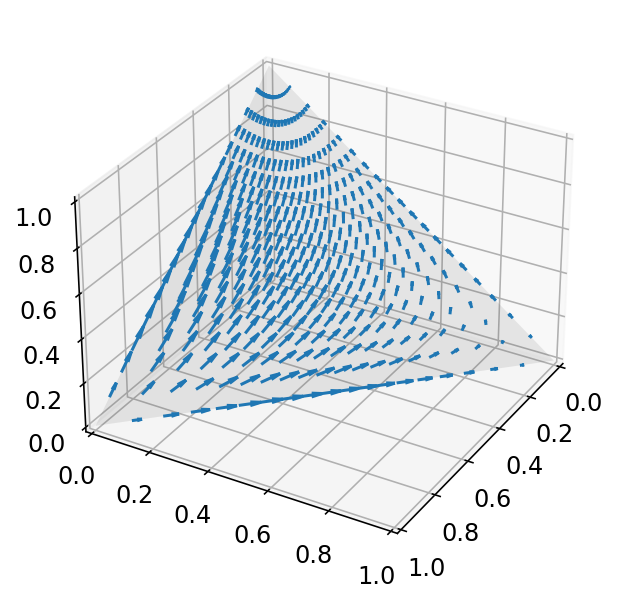

In the second discrete case , functions and probability measures on are identified as vectors in the Euclidean space . We visualise the first variation and the other first variation as three-dimensional vectors. Let be a function s.t. . Figure 5 (b) visualises the first variation at the fixed and each point in the probability simplex in . This illustrates what field on a space of probability measures is induced by the first variation assigned at every . Let be a probability measure s.t. . Figure 5 (a) visualises the first variation at the fixed and each point , again, in the probability simplex in . Here, we take each from the probability simplex for visualisation, but the first variation can be defined for all non-negative functions .

Next, we illustrate an infinite-dimensional flow in the continuous case . We approximate a flow from to by the discretisation scheme in (12):

where we use . By Theorem 5, the symplectic variation of the minimum free energy at each is given by with

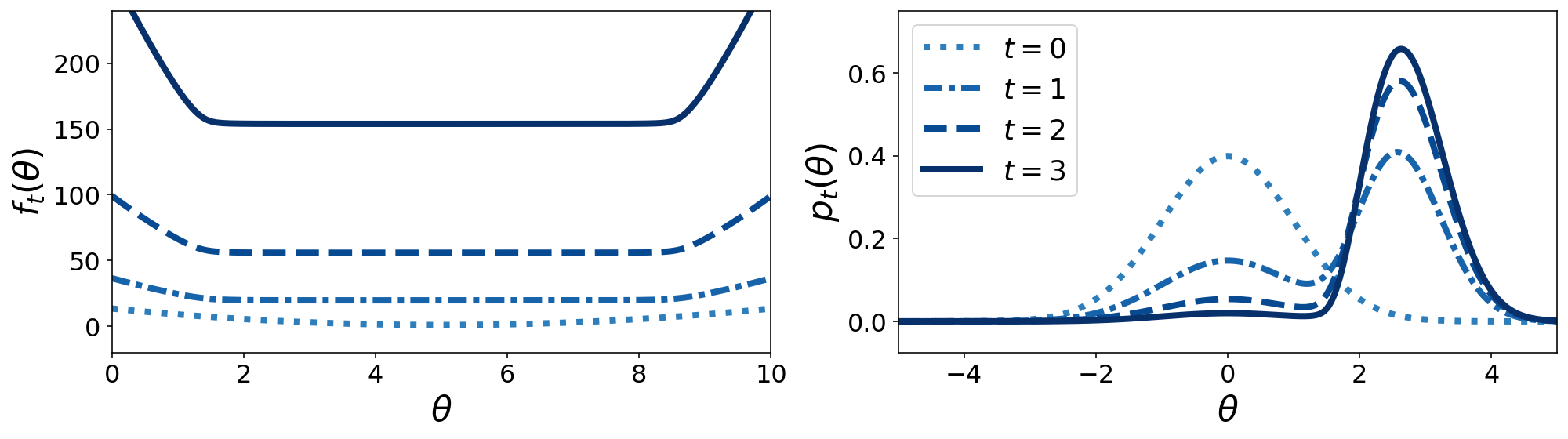

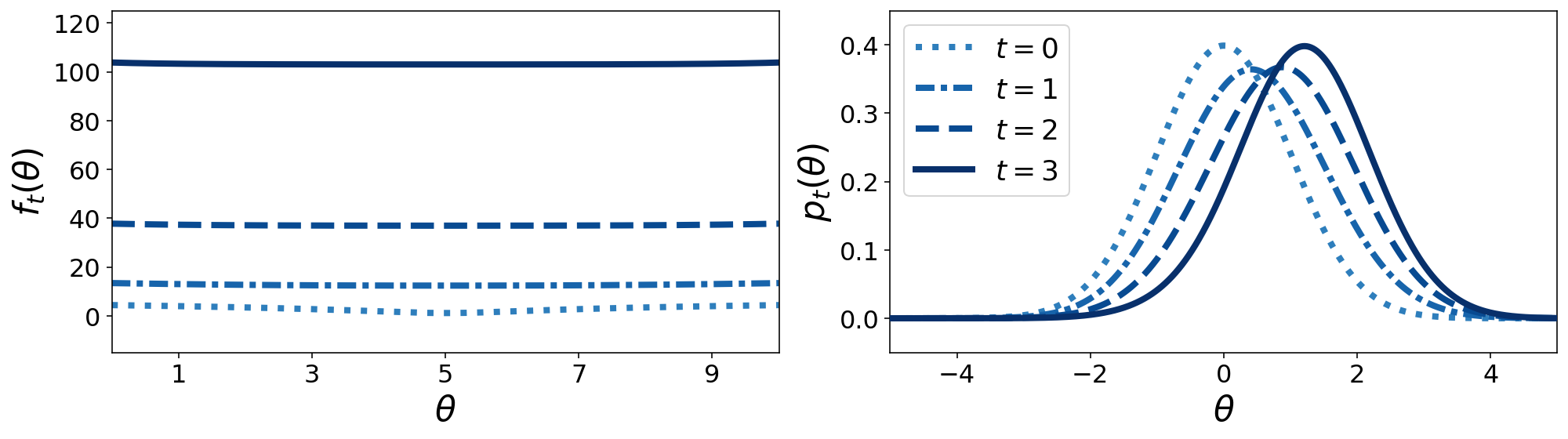

At any time in , the integral in the definition of and is numerically computed by the left-endpoint rule using grid points over . We identify the measure with the density with respect to the Lebesgue measure in . We compute the approximated flow at each time , from two different initial states . Consider a normal location model over data domain with mean parameter and scale . The first initial state is defined by the negative log-likelihood of the normal location model for datum and the density . Consider a Cauchy location model over data domain with mean parameter and scale . The second initial state is defined by the negative log-likelihood of the Cauchy location model for datum and the same density as above. Figures 7 and 7 show the approximated flow from each initial state.

5 Conclusion

This paper made two theoretical contributions. First, we established the framework of arc Hamiltonian systems for saddle Hamiltonian functions whose domains are infinite-dimensional metric spaces. We derived the general condition, under which a Hamiltonian arc field generates energy-conserving flows everywhere in a metric space. We showed that the general condition reduces to local Lipschitz continuity of the first variation of the Hamiltonian function when the metric on has an extension to a norm-induced metric on . Second, we presented the arc Hamiltonian system of the minimum free energy, in which the difference of the posterior and the prior of Bayesian inference is characterised as the first variation of the minimum free energy with respect to . Pairing this first variation with the other first variation with respect to , we revealed the underlying Hamiltonian arc field behind the transition from the prior and the posterior, as highlighted in Remark 4. The invariance of the conservation of the minimum free energy was established.

In this work, convexity of saddle Hamiltonian functions plays a vital role in the construction of our energy-conserving systems. Arc Hamiltonian systems satisfy the conservation of energy, using only a topologically weak notion of derivative and gradient, i.e., the variational derivative and the first variation. In contrast to the Fréchet derivative, weak notions of derivative, such as the Gâteaux derivative, no longer satisfy the chain rule in general (Yamamuro, 1974). Nonetheless, convexity acts in place of the chain rule to guarantee the energy-conserving property of arc Hamiltonian systems. We focused on saddle Hamiltonian functions that are independent of time . Relaxing time-independence of saddle Hamiltonian functions represents one of natural directions for future work. An extension of arc fields to time-dependent cases was considered in Kim and Masmoudi (2013). In this paper, we applied the framework of arc Hamiltonian systems to formalise the infinite-dimensional geometrical property associated with Bayesian inference. Apart from our application, there may be other intriguing dynamical phenomena or optimisation methodologies that benefit from infinite-dimensional Hamiltonian systems in metric spaces. The general framework of arc Hamiltonian systems can naturally lead to the development of further applications.

Supplementary Material for ‘Hamiltonian Dynamics of Bayesian Inference Formalised by Arc Hamiltonian Systems’ \sdescriptionThe supplementary material contains proofs for all the theoretical results in the main text.

References

- Abraham and Marsden (1987) {bbook}[author] \bauthor\bsnmAbraham, \bfnmRalph\binitsR. and \bauthor\bsnmMarsden, \bfnmJerrold E.\binitsJ. E. (\byear1987). \btitleFoundations of Mechanics, \bedition2nd edition ed. \bpublisherAddison-Wesley Publishing Company, Inc. \endbibitem

- Aliprantis and Border (2006) {bbook}[author] \bauthor\bsnmAliprantis, \bfnmCharalambos D.\binitsC. D. and \bauthor\bsnmBorder, \bfnmKim C.\binitsK. C. (\byear2006). \btitleInfinite Dimensional Analysis: A Hitchhiker’s Guide. \bpublisherSpringer. \endbibitem

- Arnold (1978) {bbook}[author] \bauthor\bsnmArnold, \bfnmV. I.\binitsV. I. (\byear1978). \btitleMathematical Methods of Classical Mechanics. \bpublisherSpringer. \endbibitem

- Attias (1999) {binproceedings}[author] \bauthor\bsnmAttias, \bfnmHagai\binitsH. (\byear1999). \btitleA variational Baysian framework for graphical models. In \bbooktitleAdvances in Neural Information Processing Systems \bvolume12. \endbibitem

- Aubin (1993) {barticle}[author] \bauthor\bsnmAubin, \bfnmJean-Pierre\binitsJ.-P. (\byear1993). \btitleMutational equations in metric spaces. \bjournalSet-Valued Analysis \bvolume1 \bpages3–46. \endbibitem

- Aubin (1999) {bbook}[author] \bauthor\bsnmAubin, \bfnmJean-Pierre\binitsJ.-P. (\byear1999). \btitleMutational and Morphological Analysis. \bpublisherSpringer. \endbibitem

- Bissiri, Holmes and Walker (2016) {barticle}[author] \bauthor\bsnmBissiri, \bfnmP. G.\binitsP. G., \bauthor\bsnmHolmes, \bfnmC. C.\binitsC. C. and \bauthor\bsnmWalker, \bfnmS. G.\binitsS. G. (\byear2016). \btitleA general framework for updating belief distributions. \bjournalJournal of the Royal Statistical Society Series B: Statistical Methodology \bvolume78 \bpages1103-1130. \endbibitem

- Blei, Kucukelbir and McAuliffe (2017) {barticle}[author] \bauthor\bsnmBlei, \bfnmDavid M.\binitsD. M., \bauthor\bsnmKucukelbir, \bfnmAlp\binitsA. and \bauthor\bsnmMcAuliffe, \bfnmJon D.\binitsJ. D. (\byear2017). \btitleVariational inference: a review for statisticians. \bjournalJournal of the American Statistical Association \bvolume112 \bpages859-877. \endbibitem

- Bogachev (2006) {bbook}[author] \bauthor\bsnmBogachev, \bfnmVladimir I.\binitsV. I. (\byear2006). \btitleMeasure Theory. \bpublisherSpringer. \endbibitem

- Brezis (2011) {bbook}[author] \bauthor\bsnmBrezis, \bfnmHaim\binitsH. (\byear2011). \btitleFunctional Analysis, Sobolev Spaces and Partial Differential Equations. \bpublisherSpringer. \endbibitem

- Calcaterra and Bleecker (2000) {barticle}[author] \bauthor\bsnmCalcaterra, \bfnmCraig\binitsC. and \bauthor\bsnmBleecker, \bfnmDavid\binitsD. (\byear2000). \btitleGenerating flows on metric spaces. \bjournalJournal of Mathematical Analysis and Applications \bvolume248 \bpages645-677. \endbibitem

- Catoni (2007) {barticle}[author] \bauthor\bsnmCatoni, \bfnmOlivier\binitsO. (\byear2007). \btitlePac-Bayesian supervised classification: the thermodynamics of statistical learning. \bjournalIMS Lecture Notes Monograph Series \bvolume56 \bpages1–-163. \endbibitem

- Chernoff and Marsden (1974) {bbook}[author] \bauthor\bsnmChernoff, \bfnmPaul Robert\binitsP. R. and \bauthor\bsnmMarsden, \bfnmJerrold Eldon\binitsJ. E. (\byear1974). \btitleProperties of Infinite Dimensional Hamiltonian Systems. \bpublisherSpringer. \endbibitem

- Cohn (2013) {bbook}[author] \bauthor\bsnmCohn, \bfnmDonald L.\binitsD. L. (\byear2013). \btitleMeasure Theory. \bpublisherSpringer. \endbibitem

- Dembo and Zeitouni (2009) {bbook}[author] \bauthor\bsnmDembo, \bfnmAmir\binitsA. and \bauthor\bsnmZeitouni, \bfnmOfer\binitsO. (\byear2009). \btitleLarge Deviations Techniques and Applications. \bpublisherSpringer. \endbibitem

- Dupuis and Ellis (2011) {bbook}[author] \bauthor\bsnmDupuis, \bfnmPaul\binitsP. and \bauthor\bsnmEllis, \bfnmRichard S\binitsR. S. (\byear2011). \btitleA Weak Convergence Approach to the Theory of Large Deviations. \bpublisherWiley. \endbibitem

- Eells and Elworthy (1970) {barticle}[author] \bauthor\bsnmEells, \bfnmJ.\binitsJ. and \bauthor\bsnmElworthy, \bfnmK. D.\binitsK. D. (\byear1970). \btitleOpen embeddings of certain Banach manifolds. \bjournalAnnals of Mathematics \bvolume91 \bpages465–485. \endbibitem

- Ekeland and Témam (1999) {bbook}[author] \bauthor\bsnmEkeland, \bfnmIvar\binitsI. and \bauthor\bsnmTémam, \bfnmRoger\binitsR. (\byear1999). \btitleConvex Analysis and Variational Problems. \bpublisherSociety for Industrial and Applied Mathematics. \endbibitem

- Ellis (2006) {bbook}[author] \bauthor\bsnmEllis, \bfnmRichard S.\binitsR. S. (\byear2006). \btitleEntropy, large deviations, and statistical mechanics. \bpublisherSpringer. \endbibitem

- Georgii (2011) {bbook}[author] \bauthor\bsnmGeorgii, \bfnmHans-Otto\binitsH.-O. (\byear2011). \btitleGibbs Measures and Phase Transitions, \bedition2nd edition ed. \bpublisherDe Gruyter. \endbibitem

- Gibbs (1902) {bbook}[author] \bauthor\bsnmGibbs, \bfnmJosiah Willard\binitsJ. W. (\byear1902). \btitleElementary Principles in Statistical Mechanics. \bpublisherCharles Scribner’s Sons. \endbibitem

- Goldstein, Poole and Safko (2002) {bbook}[author] \bauthor\bsnmGoldstein, \bfnmHerbert\binitsH., \bauthor\bsnmPoole, \bfnmCharles\binitsC. and \bauthor\bsnmSafko, \bfnmJohn\binitsJ. (\byear2002). \btitleClassical mechanics. \bpublisherAmerican Association of Physics Teachers. \endbibitem

- Guedj (2019) {barticle}[author] \bauthor\bsnmGuedj, \bfnmBenjamin\binitsB. (\byear2019). \btitleA primer on PAC-Bayesian learning. \bjournalarXiv:1901.05353. \endbibitem

- Jordan, Kinderlehrer and Otto (1997) {barticle}[author] \bauthor\bsnmJordan, \bfnmRichard\binitsR., \bauthor\bsnmKinderlehrer, \bfnmDavid\binitsD. and \bauthor\bsnmOtto, \bfnmFelix\binitsF. (\byear1997). \btitleFree energy and the Fokker-Planck equation. \bjournalPhysica D: Nonlinear Phenomena \bvolume107 \bpages265-271. \endbibitem

- Kim and Masmoudi (2013) {barticle}[author] \bauthor\bsnmKim, \bfnmH. K.\binitsH. K. and \bauthor\bsnmMasmoudi, \bfnmN.\binitsN. (\byear2013). \btitleGenerating and adding flows on locally complete metric spaces. \bjournalJournal of Dynamics and Differential Equations \bvolume25 \bpages231–-256. \endbibitem

- Kolokoltsov (2019) {bbook}[author] \bauthor\bsnmKolokoltsov, \bfnmVassili\binitsV. (\byear2019). \btitleDifferential Equations on Measures and Functional Spaces. \bpublisherSpringer. \endbibitem

- Kriegl and Michor (1997) {bbook}[author] \bauthor\bsnmKriegl, \bfnmAndreas\binitsA. and \bauthor\bsnmMichor, \bfnmPeter\binitsP. (\byear1997). \btitleThe Convenient Setting of Global Analysis. \bseriesMathematical Surveys and Monographs \bvolume53. \bpublisherAmerican Mathematical Society. \endbibitem

- Lang (1985) {bbook}[author] \bauthor\bsnmLang, \bfnmSerge\binitsS. (\byear1985). \btitleDifferential Manifolds. \bpublisherSpringer. \endbibitem

- Lorenz (2010) {bbook}[author] \bauthor\bsnmLorenz, \bfnmThomas\binitsT. (\byear2010). \btitleMutational analysis. A joint framework for Cauchy problems in and beyond vector spaces. \bpublisherSpringer. \endbibitem

- Marsden and Hughes (1983) {bbook}[author] \bauthor\bsnmMarsden, \bfnmJ. E.\binitsJ. E. and \bauthor\bsnmHughes, \bfnmT. J. R.\binitsT. J. R. (\byear1983). \btitleMathematical Foundations of Elasticity. \bpublisherEnglewood Cliffs. \endbibitem

- Müller (1997) {barticle}[author] \bauthor\bsnmMüller, \bfnmAlfred\binitsA. (\byear1997). \btitleIntegral probability metrics and their generating classes of functions. \bjournalAdvances in Applied Probability \bvolume29 \bpages429–443. \endbibitem

- Rockafellar (1974) {bbook}[author] \bauthor\bsnmRockafellar, \bfnmTyrrell R\binitsT. R. (\byear1974). \btitleConjugate Duality and Optimization. \bpublisherSIAM. \endbibitem

- Ruelle (1967) {barticle}[author] \bauthor\bsnmRuelle, \bfnmD.\binitsD. (\byear1967). \btitleA variational formulation of equilibrium statistical mechanics and the Gibbs phase rule. \bjournalCommunications in Mathematical Physics \bvolume5 \bpages324–329. \endbibitem

- Ruelle (1969) {bbook}[author] \bauthor\bsnmRuelle, \bfnmDavid.\binitsD. (\byear1969). \btitleStatistical Mechanics: Rigorous Results. \bpublisherW. A. Benjamin. \endbibitem

- Santambrogio (2015) {bbook}[author] \bauthor\bsnmSantambrogio, \bfnmFilippo\binitsF. (\byear2015). \btitleOptimal Transport for Applied Mathematicians Calculus of Variations, PDEs, and Modeling. \bpublisherSpringer. \endbibitem

- Schmeding (2022) {bbook}[author] \bauthor\bsnmSchmeding, \bfnmAlexander\binitsA. (\byear2022). \btitleAn Introduction to Infinite-Dimensional Differential Geometry. \bpublisherCambridge University Press. \endbibitem

- Villani (2009) {bbook}[author] \bauthor\bsnmVillani, \bfnmCédric\binitsC. (\byear2009). \btitleOptimal Transport: Old and New. \bpublisherSpringer. \endbibitem

- Yamamuro (1974) {bbook}[author] \bauthor\bsnmYamamuro, \bfnmSadayuki\binitsS. (\byear1974). \btitleDifferential Calculus in Topological Linear Spaces. \bpublisherSpringer. \endbibitem

This supplementary material contains proofs of all the theoretical results presented in the main text. Appendix A provides a concise summary of the theoretical results in Calcaterra and Bleecker (2000) relevant to the theoretical development of arc Hamiltonian systems. It also shows that a part of the original conditions can be relaxed. Appendix B contains proofs of all the theoretical results presented in Section 3. Appendix C contains proofs of all the theoretical results presented in Section 4 apart from the derivation of the first variation. The derivation of the first variation in Section 4 is summarised in Appendix D. Finally, Appendix E presents proofs of three intermediate lemmas used in the proof of Theorem 6.

A The Theory of Arc Fields and The Relaxation of The Condition

Let be an arbitrary complete metric space and let be an arbitrary map s.t. throughout Appendix A. Recall that the map is called an arc field if it satisfies the condition in Definition 1. Calcaterra and Bleecker (2000) were concerned with a curve in that satisfies the following condition at each time :

| (S1) |

They established conditions for the map , under which a unique solution of (S1) from exists in the infinite interval for every starting point .

In Section A.1, we provide a brief recap of their results relevant to the theoretical development of arc Hamiltonian systems. We restate their results using our notation, remarking corresponding statements of Calcaterra and Bleecker (2000) in each statement provided in Section A.1. We prefix ‘CB-’ to statements of Calcaterra and Bleecker (2000) refered here—e.g., CB-Definition 2.1—for simpler citation. In Section A.2, we show that a part of their original conditions can be relaxed. Section A.3 contains the proof of the relaxation.

A.1 The Theory of Arc Fields

First, they studied under what condition a unique solution of (S1) exists at least in some finite interval at each starting point. They provided the following two fundamental conditions.

Assumption 9 (CB-Condition AL).

For some function , at each there exist a radius and a length s.t.

and is upper bounded for all and .

Assumption 10 (CB-Condition BL).

For some function , at each there exist a radius and a length s.t.

and is upper bounded for all and .

Originally, the above inequality in CB-Condition BL was stated in a form

using some function . However, CB-Remark 2.1 highlighted that it suffices to set in CB-Condition BL. We hence use as our default choice in 10 by combining CB-Condition BL and CB-Remark 2.1.

By CB-Definition 4.1, an arc field is said to have unique solutions for short time if there exists an interval at each point , in which a unique solution of (S1) exists from . This means that, if two non-unique solutions of (S1) exist from in some interval larger than , they must equal to each other at least in the interval . Then they showed in CB-Proposition 4.2 that, if an arc field has unique solutions for short time, a maximal solution (i.e. the longest solution that can exist) at each point is, in fact, unique. In other words, any solution of (S1), shown to exists in some interval, turns out to be a part of the underlying longest unique solution. CB-Proposition 4.2 formalised this intuition.

Proposition 4 (CB-Proposition 4.2).

They concisely summarised in CB-Corollary 4.3 that an arc field has unique solutions for short time under CB-Condition AL and CB-Condition BL.

Corollary 1 (CB-Corollary 4.3).

In CB-Corollary 4.3, the interval in which each unique maximal solution exists was implicit. They next studied under what additional condition each unique maximal solution exists globally in the infinite interval . For simplicity, we drop the term ‘maximal’ for any unique solution in , because a unique solution in is trivially the longest solution. They used a condition, termed linear speed growth, and showed the existence of a unique solution in the infinite interval in CB-Theorem 4.4.

Definition 8 (CB-Definition 4.2).

An arc field is said to have linear speed growth if there exists a point and some constant dependent only on s.t.

holds for all , where is defined in Definition 1.

Theorem 7 (CB-Theorem 4.4).

Note that each unique solution above is continuous while this was implicit in CB-Theorem 4.4. Continuity of each solution is made explicit in our statement in Section A.2. We move on to Section A.2, where we weaken CB-Definition 4.2 and reproduce CB-Theorem 4.4.

A.2 The Relaxation of The Condition

The condition of CB-Definition 4.2 for an arc field requires that the inequality holds for all radius in . This is in contrast to the inequalities in Assumptions 9–10 that need to hold only for all radius smaller than some constant at each point . The condition of CB-Definition 4.2 may be restrictive for some application; in the theory of arc Hamiltonian systems, we use local Lipschitz continuity of the first variation of a Hamiltonian function to show the existence of a flow. We conclude Appendix A by showing that the condition of CB-Definition 4.2 can be relaxed in a manner that an analogous inequality holds only for all radius smaller than some constant at each point . The function in 11 is defined in Definition 1.

Assumption 11.

At each , there exist a radius s.t.

holds for all , where are constants dependent only on .

Here, we note that a map that satisfies 11 is in fact an arc field.

Lemma 1.

A map that satisfies 11 is an arc field on .

Proof.

Recall from Definition 1 that . It follows from 11 that each there exist a radius s.t. it holds for all that

where the last inequality is immediate from and . Since for all at each , we conclude that satisfies Definition 1 and is an arc field. ∎

Now, we reproduce CB-Theorem 4.4 under 11 without using the condition of CB-Definition 4.2. Continuity of each solution is made explicit in the following Theorem 8.

Theorem 8.

The proof of Theorem 8 is provided in Section A.3. Theorem 8 is the main result that directly used in the theoretical development of arc Hamiltonian systems. This completes the brief recap of the theory of arc fields and the relaxation of the condition.

A.3 Proof of Theorem 8

We introduce an intermediate lemma used in the main proof.

Lemma 2.

Suppose that for a point an arc field has a unique solution from in some interval. Given any radius , there exists some length s.t. the unique solution from satisfies for all .

Proof of Lemma 2.

Denote by the interval in which a unique solution from is supposed to exist. Let be an arbitrary point in and let be any variable in , where we have . By the triangle inequality, we have

In the above inequality, we plug the following trivial inequality

where is the function defined in Definition 1. We take the limit to see that

We have by the condition (S1) and have by Definition 1. We set to see that . By definition of convergence, for any value , we can take some value so that holds for all . ∎

Now, we present the main proof of Theorem 8.

Proof of Theorem 1.

By Lemma 1, the map is an arc field under 11. Let be an arbitrary point in . Let be the radius that the inequality in 11 holds at . By Corollary 1, the arc field has unique solutions for short time. Hence a unique solution from exists in some interval. By Lemma 2, there exists some s.t. the solution from satisfies for all .

Our aim is to show that the unique solution in can be uniquely and indefinitely extended to , by the same argument in the proof of CB-Theorem 4.4. Let be a Cauchy sequence in s.t. . A key part of the proof is to show that

the solution sequence from is Cauchy.

If item holds, the solution from converges to some point as . This implies that, at , the solution connects to the other unique solution running from in some interval . Since we show item for arbitrary , the other solution from is also Cauchy and converges to some point as . By repeating this process, the original solution from can be continued over . By Proposition 4, the continued solution in is unique, which concludes the existence of a unique solution in . Continuity of the solution is clarified in the end of this proof.

It suffices to prove item . We repeat the argument in the proof of CB-Theorem 4.4 for item , using only 11. Let for any where . For any and , it follows from the reverse triangle inequality that

It further follows from the triangle inequality that

Dividing both the side by and taking the limit in , we have

where due to the condition (S1). Recall that holds for all , where . Since is the radius under which the inequality in 11 holds at , we can apply the inequality of for all , that is,

| (S2) |

This inequality (S2) implies a bound . To verify this, we set and calculate its right-derivative

where the right-hand side is non-positive because of the inequality (S2). Since the right-derivative is non-positive, decreases over and hence , which leads to

where we used . Rearranging the term confirms that we have the intended bound . Since , we arrive at a main bound:

| (S3) |

Let be an arbitrary point in . Define for any , where . We aim to derive an upper bound of similar to (S3). The above argument for depends only on the condition . If a corresponding condition holds for some constants and , we have

| (S4) |

In fact, the required condition holds for and because

where the first inequality follows from the inequality in 11 and the last inequaliy follows from the triangle inequality. Applying (S3) for in the constant , we further have . We plug these constants and in (S4) to see that

Since the mean value theorem implies for any , we have, for arbitrary and , that

Since the metric are symmetric, we can rewrite this inequality as

| (S5) |

for any . This inequality implies Lipschitz continuity of the solution in . We conclude that the solution sequence is Cauchy as intended, because we have whenever due to (S5).

Finally, we make explicit continuity of the continued solution in . As aforementioned, a solution from in converges to some point at and connects to the other solution from in . Since is arbitrary in this proof, both the solution from and the solution from satisfy Lipschitz continuity (S5). Thus, the connected solution over is continuous if it is continuous at . It is trivially continuous at since the two solutions are concatenated at . By repeating this process, the solution from continues over continuously. ∎

B Proofs for Results in Section 3

B.1 Proof of Theorem 1

Theorem 4.4 of Calcaterra and Bleecker (2000) established conditions for an arbitrary arc field , under which a unique solution of the associated condition (6) exists in from any initial point in . See Section A.1 for a summary of their results. We established in Theorem 8 in Section A.2 that a part of their original assumptions can be relaxed. Theorem 1 is a direct application of Theorem 8 stated under the relaxed assumptions suitable for our theoretical development.

Proof.

By definition, a global flow of the system from a point is a unique continuous solution of the arc Hamilton equation (11) from in the infinite interval . Theorem 8 shows that a unique continuous solution of the condition (6) exists in the infinite interval from every initial point in if the associated map satisfies Assumptions 9–11. For the arc Hamilton equation (11), 1 restates Assumptions 9–10 combined together and 2 restates 11. ∎

B.2 Proof of Theorem 2

In Section B.2, let be the norm on that induces the metric on in 3 item (1). Since is an extension of from to , we have everywhere in . We introduce an intermediate lemma used in the main proof.

Lemma 3.

Proof of Lemma 3.

The first equality is immediate from

For any , we apply the triangle inequality to see that

where the last inequality follows from local Lipschitz continuity (13). ∎

Now, we provide the main proof of Theorem 2.

Proof of Theorem 2.

First, we specify the functions and , for which 1 is shown to hold:

Here, we verify and are well-defined at each point. If , the value of at each point is finite because . Even if , the value of is finite because local Lipschitz continuity (13) implies that, for all ,

| (S6) |

at each point . Therefore, is well-defined at each point, so does .

In what follows, let be an arbitrary point in . Let be the radius that local Lipschitz continuity (13) in 3 holds at . Let be arbitrary points in an open ball for a given radius . Let be arbitrary points in an interval for a given length . First, we show that there exist some radius and length s.t. 1 items (1)–(2) hold.

1 item (1): It follows from the triangle inequality that

Since everywhere in , we have

If are contained in , the term is bounded by as established in (S6). Selecting any and concludes 1 item (1).

1 item (2): Denote to see

Since by Lemma 3, it follows from definition of that

We can conclude 1 item (2) if there exist some and s.t. is bounded for all and all . Since by definition we have , we will upper bound each component and . If we have , Lemma 3 shows that . It thus suffices to take any to upper bound the second component. It is established in (S6) that if both and are contained in . In fact, if we have , there exists s.t. for all . To verify this, see that Lemma 3 implies . By definition of convergence, for any given there exists some s.t. for all . That is, given the radius , there exists some s.t. is contained in for all . Clearly, the open ball around is further contained in the open ball around if we have . This means that, if we take any , then and are both contained in for all . Therefore, selecting any and guarantees that is bounded.

We complete the proof by showing 2.

B.3 Proof of Theorem 3

If a convex function admits the first variation at , the following inequality holds for any :

| (S8) |

The first equality follows from definition of the first variation, where is a trivial element of . The last inequality follows from convexity . If is a concave function, we have the inequality with the less-than sign flipped

| (S9) |

Note that the essentially same inequalities hold for a convex or concave function in . We introduce a lemma that applies (S8) and (S9) for a saddle function .

Lemma 4.

Suppose that a saddle function has the first variations and everywhere in . For any ,

Proof of Lemma 4.

Let be arbitrary points in . Denote for fixed and for fixed , where is concave and is convex. By definition, the first variation of at is , and the first variation of at is . We apply (S9) for both (i) and (ii) to see that

| (i) | |||

| (ii) |

We multiply both sides of the inequality (ii) by to have that

| (S10) |

Similarly, we apply (S8) for both (iii) and (iv) to see that

| (iii) | |||

| (iv) |

We multiply both sides of the inequality (iv) by to have that

| (S11) |

Now we present the main proof of Theorem 3.

Proof of Theorem 3.

It suffices to show that (i) is continuous in and (ii) the right derivative equals to zero everywhere in . First of all, item (i) immediately holds by combining local Lipschitz continuity (14)

with continuity of the flow, that is, for any with the edge case . For item (ii), by definition of the right derivative,

In the remainder, let be arbitrary fixed time in , and we show that both the term and equal to zero. This in turn concludes that item (ii) holds as intended.

Term : Let be the radius that local Lipschitz continuity (14) in 4 holds at the point . We verify that and are contained in for all sufficiently small. It is trivial that for all sufficiently small by continuity of the flow. It also holds that for all sufficiently small, because it follows from the triangle inequality that

where the first term is by continuity of the flow and the condition (11) is strong enough to imply that the second term is . Thus, by local Lipschitz continuity (14), we have

where the last equality holds by the condition (11). Thus the term equals to .

Term : For better presentation, denote simply by since is a fixed time. Denote to rewrite the term as

We shall derive upper and lower bounds of the term inside the limit, showing that the bounds both converge to in the limit. We begin with the lower bound. It follows from Lemma 4 that

We then plug and in, to see that

Here, it is clear that we have in in the limit . It then follows from 4 item (2) that we have for any . By applying this convergence with , we have

We move on to the upper bound. It follows from Lemma 4 that

Here, it is clear that we have in in the limit . We apply the essentially same argument as above for the terms and to see that

Therefore, we have , which concludes that the term equals to since the upper and lower bounds both converge to . ∎

B.4 Proof of Theorem 4

Proof of Theorem 4.

It follows from Theorem 2 that 3 implies Assumptions 1–2. Then, by Theorem 1, there exists a global flow of the system from any initial state in . We complete the proof by showing that the value of the Hamiltonian function along the flow is constant everywhere in .

Our aim is to show that Theorem 3 holds. To this end, we show that 4 item (1)–(2) are each implied by 3 item (2) under 5. Recall that, under 5, the metric is defined as and we have the inequality . In what follows, let be an arbitrary point in . Let be the radius that local Lipschitz continuity (13) in 3 holds at . Let be arbitrary points in the open ball . For better presentation, we show 4 item (2) first and item (1) next.

4 item (2): First, we show part (i) in 4 item (2). By 5.

holds for any . It is trivial that from definition of . We apply this bound to see that

Then, local Lipschitz continuity in 3 item (2) implies that the right-hand side converges to whenever in . This concludes part (i) of 4 item (2). The essentially same argument holds for part (ii) of 4 item (2).

4 item (1): By Lemma 4, we have where

By the inequality in 5, we further have

For any , the following inequality is trivial by definition of :

If , it follows from local Lipschitz continuity (13) around that

where the first last inequality follows from the triangle inequality. Note that is a constant dependent only on . Hence, for any , we have

| (S12) |

We aim to apply this bound (S12) for all the terms , , , and used in the bound and . To do so, we need to verify that each point —at which the above terms are evaluated—is contained in . It is trivial that since we let at first. It can be further verified that because

Therefore, by applying (S12) for all the terms, we upper bound and as follows:

By taking the absolute value of all the side of , we have

This bound holds for all , where depends only on . Setting and concludes 4 item (1). ∎

C Proofs for Results in Section 4

C.1 Proof of Proposition 1

Proof of Proposition 1.

Let be a set of all continuous functions that satisfies . Let be a set of all signed measures that satisfies . Given the metrics and in (16), the metric spaces and are complete if is continuous and strictly positive (Kolokoltsov, 2019, p.4). The product metric space s.t. and is then complete. Here is a metric subspace of because and is the restriction of to by definition. By a standard fact on complete metric spaces (Aliprantis and Border, 2006, p.74), the metric subspace is complete if is closed in .

The set is closed in if any convergent sequence of taken in has its limit within . Let be an arbitrary convergent sequence of taken in , whose limit is denoted . Our aim is to show that . Since the limit is at least an element of , it suffices to verify that the limit satisfies the condition: (i) satisfies and (ii) is a probability measure.

Condition (i): First, we have at all because . The uniform convergence in implies the pointwise convergence . At each , we take the limit of in the both side of to see that

The function of the limit thus satisfies the condition (i).

Condition (ii): Note that convergence of in the metric implies that

because due to . The measure is non-negative because is non-negative for all and we have . Similarly, the measure satisfies because for all and we have . The measure thus satisfies the condition (ii). ∎

C.2 Proof of Proposition 2

For in 6, define by

| (S13) |

for all and by for all . It is easy to verify that and satisfies an equality relation for each because

| (S14) |

We introduce an intermediate lemma used in the main proof.

Lemma 5.

The function in (S13) is saddle.

Proof of Lemma 5.

Let be arbitrary. Define and . It is clear that and are convex from definition of . We show that (i) is concave over and (ii) is convex over . Then is saddle since is arbitrary.

Item (i): We show that holds for any and any . Since the edge case or is trivial, it suffices to consider without loss of generality. First of all, we have

It then follows from Hölder’s inequality with and that

where we note that and are positive everywhere in .

Item (ii): We show that holds for any and any . Again, since the edge case or is trivial, it suffices to consider without loss of generality. First of all, we have

Because the negative logarithm is convex in , we complete the proof. ∎

Now we move on to the main proof.

Proof of Proposition 2.

C.3 Proof of Proposition 3

Proof of Proposition 3.

It follows from Theorem 5 that at each . The function is compatible if, at each , we have for all (c.f. Definition 4). We verify that and satisfy the condition of for all . First, since by 6 and by definition, we have

where the last inequality holds by the condition of by 6 again. Second, since and are both probability measures, we have

We therefore conclude that for all . ∎

C.4 Proof of Theorem 6

We introduce three intermediate lemmas whose proofs are deferred to Appendix E for better presentation. Denote .

Lemma 6.

Lemma 7.

Lemma 8.

The proofs are each contained in Sections E.1, E.2 and E.3. We move on to the main proof.

Proof of Theorem 6.

The metric space is complete by Proposition 1. Theorem 6 follows from Theorem 4 and we hence verify Assumptions 3 and 5. We begin with verifying 3 item (1) and 5. Define a norm on and a norm on . It is clear that and in (16) are norm-induced metrics and by definition. Thus, the metric on defined in 7 has an extension to a norm-induced metric on . This confirms 3 item (1). Furthermore, by definition of and , we have

for any , which confirms 5.

We complete the proof by verifying 3 items (2). By Theorem 5, at each we have where

In what follows, let be an arbitrary point in . Let be an arbitrary radius in . Let be arbitrary points in the open ball . Our aim is to find a constant dependent only on s.t. we have for . By the triangle inequality, we have

| (S15) |

It hence suffices to find a constant s.t. we have for , by which the proof is completed with .

We upper bound in the remainder. By definition of , we have

Due to (c.f. Definition 7) and Lemma 8, the first term is bounded by

| (S16) |

For the second term , we first decompose the term as follows:

By the triangle inequality, the second term is then bounded as

We bound the term . For the numerator, we have because by the condition of . For the denominator, Lemma 7 shows that . This implies that . The term is bounded as by Lemma 6. Finally, it follows from Lemma 8 that . By applying these upper bounds, we have

| (S17) |

where we applied a trivial inequality for the last inequality, which follows from definition of . Combining each bound (S16) and (S17), we arrive at

| (S18) |

where we set which is dependent only on . Since this argument holds for the arbitrary , we conclude 3 item (2). ∎

D Derivation of The First Variations in Section 4

Appendix D derives the first variations of the minimum free energy in Theorem 5. For the function , at each denote by the variational derivative of the function at . The first variation is a unique element in s.t.

| (S19) |

Similarly, at each denote by the variational derivative of the function at . The first variation is a unique element in s.t.

| (S20) |

The first variations and can be found by deriving an explicit form of the variational derivative and that satisfies (S19) and (S20).

First, we introduce two intermediate lemmas: the first one in Section D.1 and the second one in Section D.2. We then provide the main proof of Theorem 5 in Section D.3.

D.1 The First Lemma for Theorem 5