[name=Theorem, sibling=theorem]rThm \declaretheorem[name=Lemma, sibling=theorem]rLem \declaretheorem[name=Observation, sibling=theorem]rObs \declaretheorem[name=Corollary, sibling=theorem]rCor \declaretheorem[name=Proposition, sibling=theorem]rPro \addauthorebblue \addauthorczred \addauthorvgpurple \addauthorxtcyan

Online Mechanism Design with Predictions††thanks: All four authors were supported by NSF grant CCF-2210502. Eric Balkanski was also supported by NSF grant IIS-2147361.

Abstract

Aiming to overcome some of the limitations of worst-case analysis, the recently proposed framework of “algorithms with predictions” allows algorithms to be augmented with a (possibly erroneous) machine-learned prediction that they can use as a guide. In this framework, the goal is to obtain improved guarantees when the prediction is correct, which is called consistency, while simultaneously guaranteeing some worst-case bounds even when the prediction is arbitrarily wrong, which is called robustness. The vast majority of the work on this framework has focused on a refined analysis of online algorithms augmented with predictions regarding the future input. A subsequent line of work has also successfully adapted this framework to mechanism design, where the prediction is regarding the private information of strategic agents. In this paper, we initiate the study of online mechanism design with predictions, which combines the challenges of online algorithms with predictions and mechanism design with predictions.

We consider the well-studied problem of designing a revenue-maximizing auction to sell a single item to strategic bidders who arrive and depart over time, each with an unknown, private, value for the item. We study the learning-augmented version of this problem where the auction designer is given a prediction regarding the maximum value over all agents. Our main result is a strategyproof mechanism whose revenue guarantees are -consistent with respect to the highest value and -robust with respect to the second-highest value, for . We show that this tradeoff is optimal within a broad and natural family of auctions, meaning that any -consistent mechanism in that family has robustness at most . Finally, we extend our mechanism to also obtain expected revenue that is proportional to the prediction quality.

1 Introduction

One of the well-established shortcomings of worst-case analysis is that it often leads to overly pessimistic conclusions. On the other hand, any non-trivial performance guarantee that can be established through worst-case analysis is very robust, since it holds no matter what the input may be. In an attempt to overcome the limitations of worst-case analysis without compromising its robustness, the recently proposed framework of “algorithms with predictions” allows algorithms to be augmented with a machine-learned prediction that they can use as a guide [28]. Crucially, this prediction may be highly inaccurate, so depending too heavily on it can lead to very poor performance in the worst case. Therefore, the goal in this framework is to use such a prediction so that a strong performance can be guaranteed whenever the prediction is accurate (known as the consistency guarantee), while simultaneously maintaining non-trivial worst-case guarantees even if the prediction is inaccurate (known as the robustness guarantee).

During the last five years since this framework was introduced, a surge of work has utilized it toward a refined analysis of algorithms, data structures, and mechanisms (see [25] for a frequently updated list of papers in this rapidly growing literature). The vast majority of this work has focused on the design and analysis of online algorithms, i.e., algorithms that need to process their input piece-by-piece and make irrevocable decisions without knowing the whole input. Learning-augmented online algorithms are enhanced with a prediction regarding the future input, which they can potentially use to make more informed decisions, while carefully managing the risk of being misguided by it. An even more recent line of work has successfully adapted this framework for the design and analysis of mechanisms interacting with strategic bidders [1, 34]. One of the canonical problems in mechanism design is the design of auctions for selling goods to a group of strategic bidders, aiming to maximize the revenue. The main obstacle in achieving this goal is the fact that the amount that each bidder is willing to pay is private information that the designer needs to carefully elicit. Learning-augmented mechanisms are therefore enhanced with predictions regarding the value of this private information, which can potentially overcome these obstacles.

In this work, we initiate the study of online mechanism design with predictions, bringing together the two lines of work on online algorithms with predictions and mechanism design with predictions. Specifically, we consider the problem of selling goods to strategic bidders that arrive and depart over time. This problem combines the challenges of both lines of work since the designer needs to carefully elicit the unknown, private, value of each bidder, while also not knowing (and being unable to elicit) the values of the bidders who have not yet arrived. In fact, designing an auction for such dynamic settings can be more demanding because, apart from the combined information limitations that the designer faces, the bidders may not only strategically misreport their value for the good(s) beings sold, but they may also strategically misrepresent their arrival and departure times.

The study of online mechanism design (without predictions) has previously received a lot of attention, given the many important applications that involve dynamic settings with bidders that arrive and depart over time [32]. For example the sale of airplane and theater seats or the sale of cars usually takes place over a period of time, during which interested buyers join the market and depart from it. As this happens, the seller may gradually adjust the prices of the goods being sold aiming to maximize the revenue. These adjustments can be a function of the demand that the seller observes over time, but it is quite natural to assume that the designer may also have access to some prediction regarding this demand, e.g., using historical data. Our goal in this paper is to design online auctions enhanced with such a prediction and to evaluate the extent to which they can yield strong performance guarantees in terms of consistency and robustness.

1.1 Our results

Our main goal is to evaluate the potential impact of the learning-augmented model on the performance of auctions in dynamic environments. To achieve this goal, we revisit the well-studied model of online mechanism design, where the bidders arrive and depart over time [32, 20]. This model poses several realistic and non-trivial obstacles for the auction designer: 1) the bidders can lie about their value for the good(s) being sold (the standard obstacle in mechanism design), 2) during the execution of the auction, the auctioneer has no information regarding bidders who have not yet arrived (the standard obstacle in online problems), and 3) the bidders can also lie regarding their arrival and departure times (an obstacle that is specific to the online mechanism design setting).

Within this model, we focus on the problem of selling a single item aiming to maximize revenue. Each bidder has a value for the item being sold and this value is the largest amount she would be willing to pay for it. In the absence of any predictions, the best revenue that one can guarantee, even in an offline setting, is equal to the second-highest value over all bidders.111This can be achieved by the classic Vickrey (second-price) auction. Using this as a benchmark, prior work proposed an online single-item auction that guarantees revenue at least of the second-highest value [20]. Aiming to refine this result and achieve stronger guarantees, we adopt the learning-augmented framework and consider the design of online auctions that are enhanced with a (possibly very inaccurate) prediction regarding the highest value over all bidders. The goal is to guarantee more revenue whenever the prediction is accurate (the consistency guarantee), while also achieving some non-trivial revenue guarantee even if the prediction is highly inaccurate (the robustness guarantee, which is equivalent to the worst-case guarantee studied in prior work).

Targeting a more ambitious benchmark, we use the highest value over all bidders (the first-best revenue) as a benchmark for our consistency guarantee, while maintaining the second-highest value (the second-best revenue) as the benchmark for robustness (as in prior work).

The Three-Phase learning-augmented online auction.

Our first main result is the Three-Phase auction: a learning-augmented online auction parameterized by some value , which takes place in three phases. During the first phase, the auction observes the values of the first departing bidders in order to “learn” an estimate regarding what an appropriate price may be. In the second phase, the auction “tests the prediction” by giving each active bidder the opportunity to clinch the item if their value is at least as high as the prediction. After more bidders have departed, if the item remains unsold the auction enters the third and last phase. During this phase, any active bidder is given the opportunity to clinch the item at a price equal to the maximum value observed during the first two phases. This learning-augmented online auction achieves the following trade-off between consistency and robustness.

Theorem.

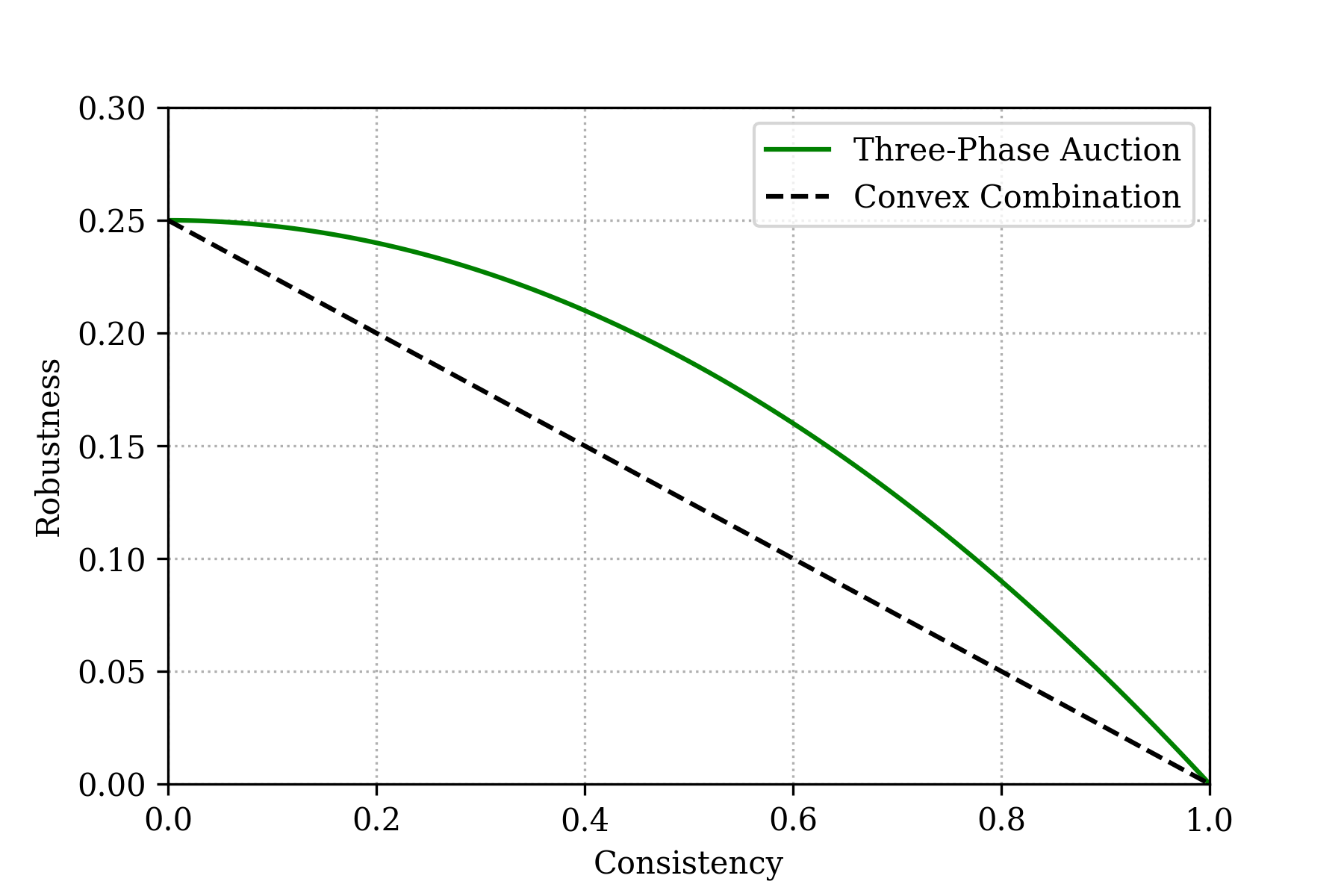

The Three-Phase learning-augmented online auction is deterministic, strategyproof, and for any such that its revenue guarantees -consistency with respect to the first-best revenue benchmark and -robustness with respect to the second-best revenue benchmark.

Note that, although we focus on revenue maximization throughout this paper, as a corollary of our analysis, we also obtain a social welfare guarantee that is also -consistent and -robust, where consistency and robustness are both with respect to the highest value.

If we let our auction retrieves the robustness guarantee of that was achieved in prior work, but provides no consistency guarantees. On the other extreme, if we let then we get a perfect consistency of (since our auction reduces to a posted price auction that offers a price equal to the prediction to every bidder, if the prediction is correct it extracts the first-best revenue) but without any robustness guarantees. Figure 1 exhibits the convex combination of these two extreme solutions, as well as the improved tradeoff achieved by the Three-Phase auction.

A tight impossibility result.

Our other main result is an impossibility result proving the optimality of our Three-Phase auction within a broad and natural family of learning-augmented online auctions called PAF auctions (Prediction or Any-so-Far auctions). Having no information regarding the bidders’ values beyond the observed values of previous bidders and the prediction, online auctions are limited in terms of what is a “reasonable” price for them to offer. The PAF class contains all auctions such that the prices offered are equal to any value of previous bidders or the prediction (see Definition 10). Although one could technically define auctions outside this class (e.g., auctions that just post an arbitrary price outside this set), PAF captures the Three-Phase auction, existing auctions from previous work [20, 14].

Theorem.

For any , there is no PAF auction that is -consistent with respect to the first-best revenue benchmark and -robust with respect to the second-best revenue benchmark.

Note that optimality results for secretary and online auction problems are often obtained through LP duality arguments [15, 14, 2]. The LP formulations for these problems rely on strong history-independence properties. In our problem, these history-independence properties do not hold because, for example, the probability of a bidder accepting a price equal to the prediction crucially depends on how many bidders have previously rejected an offered price equal to the prediction. Such dependencies make it challenging to give an LP formulation of our problem. Instead, we use an interchange argument to show that, for any there exists an -consistent PMF auction that achieves an optimal robustness and satisfies a three-phase structure identical to our auction. We then optimize for the optimal time thresholds for auctions that satisfy this three-phase structure.

1.2 Related work

Online mechanism design.

Due to the many applications with strategic agents who arrive in an online fashion, online mechanism design is an important subfield of mechanism design (see Chapter 16 by Parkes [32] of the Algorithmic Game Theory textbook [31] for an overview). The problem of online auctions with bidders who arrive dynamically and might misreport their arrival and departure times was introduced by Hajiaghayi et al. [20]. For revenue maximization, their main results are a -competitive strategyproof mechanism and a impossibility result in the single item setting, and a constant factor competitive strategyproof mechanism for the -item setting. Since then, different variations of the problem have been considered. Buchbinder et al. [14] examine agents with private arrival times and values, along with an unrestricted strategy space, and propose a strategyproof auction that achieves a competitive ratio of in terms of revenue. Krysta and Telelis [24] improve the -item competitive ratio of [20] to for the special case where the active times of bidders do not overlap. Additional related models for online mechanism design include unlimited supply, digital goods [9, 11, 10, 23]; two-sided auctions with both buyers and sellers online [13, 12]; and interdependent value environments [16].

Online algorithms with predictions.

The line of work on algorithms with predictions, also called learning-augmented algorithms, is an exciting emerging literature (see [29] for a survey of early contributions and [25] for an updated list of papers in this field). Numerous classic online algorithm design problems have been revisited, including online paging [26], scheduling [33], optimization problems involving covering [7] and knapsack constraints [21], as well as Nash social welfare maximization [8], the secretary problem [2, 17, 18], and a range of graph-related challenges [3]. Among these previous works, the most closely related to our setting is by Antoniadis et al. [2], who consider the value-maximizing secretary problem augmented with a prediction regarding the maximum value of the agents. In fact, their proposed learning-augmented algorithm follows a three-phase structure which is similar to the one used in our auction. However, our setting and our proposed solution, differ in several significant ways. The most significant one is the fact that just focusing on the online aspect of the problem, we need to deal with the important additional obstacle that the agents are strategic and can misreport their value, as well as their arrival and departure time. Furthermore, our goal is to maximize revenue whereas the goal in the secretary problem is to choose the agent with maximum value. Finally, our setting does not assume that each agent departs before the arrival of the next one, like the secretary setting does; this makes the problem of designing strategyproof mechanisms significantly more delicate. To achieve strategyproofness, our auction must very carefully determine the time at which the item is allocated, the bidder who receives the item, and the item’s price in order to handle bidders who might be active during multiple phases, which is the main technical (and novel) challenge in our setting.

Mechanism design with predictions.

Mechanism design with predictions regarding the private information of bidders is an even more recent line of work that was initiated by [1] and [34]. It includes strategic facility location [1, 34, 22], price of anarchy of cost-sharing protocols [19], strategic scheduling [34, 6], auctions [27, 34], and bicriteria (social welfare and revenue) mechanism design [4]. We refer to [5] for a reading list of this line of work.

2 Preliminaries

We consider the problem of designing an auction to sell a single item to a set of bidders who arrive and depart over time. Each bidder arrives at some time , departs at some time , and has value for the item being sold. We refer to the interval as the active time for bidder . For simplicity, we assume that the bidders are indexed based on their order of departure (i.e., bidder is the -th bidder to depart). We also let be an arbitrary total order over the set of bidders, which we use for tie-breaking, and let denote the fact that is ranked before bidder according to . Our objective is to maximize the revenue from the sale.

The main obstacle is that all the relevant information of each bidder , i.e., their “type” , is private information that is unknown to the auction designer, so the auction needs to elicit it from each bidder. However, the bidders can misreport their types and the auction needs to be designed to ensure that they cannot benefit by doing so. Specifically, apart from misreporting her value for the item (which is the standard type of manipulation considered in mechanism design), a bidder can also misreport her arrival and departure times: adopting the original model introduced by Hajiaghayi et al. [20], we assume that each bidder can delay the announcement of her arrival (essentially reporting a delayed arrival time ), and she can report a false departure time (either earlier or later than her true departure time, ). Upon arrival, each bidder declares a type (potentially different than ) and the auction needs to determine who the winner is (i.e., which bidder will be allocated the item), at what time the item should be allocated to the winner, as well as the amount that the winner should pay.

Apart from the information limitations that the auction faces due to the private nature of the bidders’ types, the auction also needs to be implemented in an online fashion. This means that if it decides to allocate the item at some time , then this decision is irrevocable, and both this allocation decision and the payment amount requested from the winner can depend only on information regarding bidders with arrival time . In other words, the allocation and payment cannot in any way depend on the types of bidders that have not yet arrived.

If the auction allocates the item to some bidder at some time for a price of , then this bidder’s utility is equal to , as long as , i.e., as long as is active at time . Otherwise, if is allocated the item outside her (real) active time, then she receives no value from it, and her utility is . All other bidders receive no item and contribute no payment, so their utility is . A auction is strategyproof if for every bidder , truthfully reporting her type is a dominant strategy. This means that no matter what types the other bidders report, the utility of bidder is maximized if she reports her true type, . To emphasize the added difficulty for achieving strategyproofness in online auctions, relative to static ones, prior work often distinguishes between value-strategyproofness, which ensures that bidders will not want to misreport their value, and time-strategyproofness, which is the additional requirement to ensure that bidders cannot benefit by misrepresenting their arrival or departure times either.

To evaluate the performance of online auctions with respect to the revenue they extract, prior work focused on a model where a set of arrival-departure intervals and a set of values are generated adversarially, and the values of are then matched to arrival-departure intervals from uniformly at random. Note that, if the intervals are all non-overlapping, this reduces to the classic random ordering model, where the values of the bidders are determined adversarially and the order of their arrival is random. Therefore, our setting generalizes the classic setting of the “secretary problem”. We let denote the random matching of values to intervals and denote the expected revenue of an auction with respect to this random matching. Also, let and denote the highest and second-highest values in , which are important benchmarks since the former is the highest feasible revenue (no bidder would pay more than that) and the latter is the “offline Vickrey” benchmark (this corressponds to the amount of revenue that is actually achievable via the classic Vickrey auction in offline settings).

In this work we adopt the learning-augmented framework and study online auctions that are also equipped with a (potentially very inaccurate) prediction regarding the highest value, , in . We denote the expected revenue of a auction, , as and we evaluate the performance of using its consistency and robustness. Consistency refers to the competitive ratio of the expected revenue achieved by the algorithm when the prediction it is provided with is accurate, i.e., whenever . The benchmark we use for consistency is the highest value in , often referred to as the first-best revenue. Formally:

Robustness refers to the competitive ratio of the expected revenue given an adversarially chosen, inaccurate, prediction. The benchmark we use for robustness is the best revenue achievable via any (offline) strategyproof auction, i.e., the second highest value , often referred to as the second-best revenue. Formally:

3 The Three-Phase Auction

We propose the Three-Phase auction, which is parameterized by a value , with greater values corresponding to higher confidence in the accuracy of the prediction. Our main result in this section shows that for any choice of this auction achieves -consistency and -robustness, while simultaneously guaranteeing both value-strategyproofness and time-strategyproofness.

The Three-Phase auction considers the bidders based on the order of their departure (i.e., the order of their indices) and comprises three separate phases.

-

1.

During the first phase, the auction observes the values of the first bidders to depart (without allocating the item to any of them), aiming to “learn” an estimate regarding what a reasonable price for the item may be. If, during this first phase, the auction observes a value that exceeds the predicted maximum, (implying that the prediction is inaccurate), then, after the first phase is complete, the auction essentially skips the second phase and moves directly onto the third phase. If, on the other hand, the first phase does not prove the prediction to be inaccurate, then the auction proceeds to the second phase.

-

2.

During the second phase, the auction “tests” the prediction. Specifically, during this phase (which terminates after more bidders have departed) it asks all active bidders whether they would be willing to pay a price equal to the prediction. If any active bidder is willing to pay this price, then they secure the item and they are guaranteed to pay a price no more than that. The exact payment of bidders who secure the item during the second phase, however, may need to be lower than that to guarantee strategyproofnes; we discuss this important subtlety later on. Finally, if none of the bidders is willing to pay a price equal to the prediction during the second phase, then the auction enters its third phase.

-

3.

During the third phase, the auction offers a take-it-or-leave-it price equal to the highest value observed over all the bidders that have previously departed, and any active bidder can claim the item at that price.

Before going into more detail regarding each of the phases, we note that the auction has a simple description for the special case where no two bidders have overlap with respect to their active intervals (i.e., there is just one active bidder at a time). In this case, the auction is a posted price mechanism that posts price to the first bidders, then posts price to the next bidders and, finally, if the item remains unsold, it posts price to the remaining bidders, where is the maximum value of bidders who have previously departed. We note that the allocation rule induced by these posted prices is a generalization of the threshold-based algorithm for the classic secretary problem.

The main challenge, and the main technical portion of our auction, is to handle the cases where there is an overlap between bidders. The time at which the item is allocated, the bidder who receives the item, and the item’s price must all be carefully designed to handle bidders who might be active during multiple phases (in particular the second and third phases) and are competing against other bidders. Irrespective of the stage of the auction where the winner is determined, the item is allocated to at the time of her (reported) departure, , to guarantee time-strategyproofness. If the winner is determined during the third phase, then her final price is the take-it-or-leave-it price that they accepted during this phase. If, on the other hand, the winner is determined during the second phase, the final price needs to be carefully determined in order to guarantee the strategyproofness of the auction. Specifically, if the winner remains active after the transition into the third phase and no other bidder would have claimed the item during the second phase, then the Three-Phase auction may need to reduce the winner’s payment to be equal to the take-it-or-leave-it price that would have been offered during the third phase if we were to remove and simulate the outcome of the auction without them.

For clarity, we formally present the allocation and the payment rule of the auction separately:

-

•

Process 1 is the execution of the allocation rule, i.e., it determines who should receive the item. This process maintains a value , corresponding to the maximum value observed among the bidders that have departed so far, and a threshold value . If any active bidder has value at least , then they can secure the item (tie-breaking using if there are multiple such active bidders). The threshold is during the first phase, then during the second phase, and finally during the third phase. This process returns the winner , if any, and the threshold at which secured the item. Furthermore, to make the formal definition of the payment rule easier, we also let this process return a Boolean variable, “active-winner,” which is true only if secured the item right after the transition between two phases. Specifically, this Boolean variable is set to true if the item was secured after a departure of an agent rather than an arrival of one, which implies that the departure caused the transition from one phase to another, leading to a drop in the threshold value, , and the winner was already active.

-

•

Process 2 is the execution of the payment rule, i.e., it determines how much the winner, if any, should pay for the item. The price is initially set to be equal to the threshold at which the item was secured and the final price will be no more than that. However, under some circumstances, the price is reduced to guarantee strategyproofness. Specifically, if the winner secured the item during the second phase and remains active during the third phase, they may receive a lower price. In this case, the price is determined by simulating the allocation process without the winning bidder, . If the new winner , in the absence of , either i) is not active during the transition into the third phase or ii) loses to in tie-breaking, then the price is lowered to the threshold at which would have secured the item. Intuitively, if neither of these two conditions hold and we did not offer the reduced price, then could report a value of instead of her true value and secure the item at that lower price right after the transition into the third phase.

Observation 1.

The Three-Phase auction can be implemented in an online fashion.

Proof.

It is easy to verify that the allocation rule is online implementable, since the auction maintains a threshold at any point and decides the winner when some active bidder’s value is above the threshold; this requires no future information. We now argue that the payment rule is online implementable as well. Crucially, note that the winner is allocated the item at the time of their departure, so all we need to argue is that the price that they need to pay can be determined at that point. To verify this fact, note that if is not active during the transition from the second phase to the third phase, then her price is just . If, on the other hand, is active during that transition, then the auction can also check the value of any other bidder that is also active up to that transition to determine and active-winner′, without needing to simulate any portion of the allocation rule beyond the departure of . ∎

Our main result in this section shows that the Three-Phase not only guarantees value- and time-strategyproofness, but it also achieve a non-trivial tradeoff between robustness and consistency.

Theorem 2.

Three-Phase is a value-strategyproof and time-strategyproof online auction that, given any parameter , simultaneously guarantees -consistency and -robustness.

In Section 3.1, we prove the consistency and robustness guarantees achieved by our auction. In Section 3.2, we show that it is strategyproof. Finally, in Section 3.3, we give an extension of our auction that achieves revenue guarantees as a function of the prediction quality. For presentation purposes we use to denote and to denote in the following analysis.

3.1 Revenue Guarantees

In this section we analyze the performance of our auction in terms of consistency and robustness. We focus on the values of in the set which make and (the number of bidder departures in the first two phases) are integral.

Lemma 3.

For any , Three-Phase is -consistent.

Proof.

Assume that the prediction is correct, i.e., . First, observe that for all , so during Phase 2, and no one would be above the threshold besides the highest value bidder. Additionally, note that no bidder is allocated the item in the first phase. Then the auction would be able to extract revenue if the highest value bidder is allocated the item during Phase 2 and pays the price . Let be the bidder with the highest value; it is sufficient to guarantee the aforementioned outcome if the departure time is between the -th departure and the -th departure, i.e., , which, based on our random-ordering assumption, occurs with a probability of . ∎

Lemma 4.

For any , Three-Phase is -robust.

Proof.

Recall that robustness is measured relative to . We now consider the cases where we under-predict and over-predict separately.

Case one: . Since for any bidder , we have that bidders can only be above the threshold in phase 3. In this case, by the payment rule, it is sufficient to extract if , which requires the second highest bidder to be amongst the first bidders to depart and bidders with the highest value are amongst the last to depart. Then with probability , revenue is extracted.

Case two: . Observe that in the under-predicted case, the prices in phases 2 and 3 are guaranteed to fall in the range if the second highest bidder is amongst the first bidders to depart. Bidders with the highest value may be allocated the item if they are present at any point in phases 2 and 3, meaning they are amongst the last to depart. Then with probability , revenue is extracted. ∎

3.2 Strategyproofness

In this section we show our auction is both value-strategyproof and time-strategyproof. All the missing proofs are deferred to Appendix A. We first show that the bidders with the first departure times have no incentive to misreport.

Lemma 5.

Consider some bidder and any . If bidder ’s true departure time is in the first , then bidder has no incentive to misreport her type .

Proof.

First note that if such bidder reports her type truthfully, she won’t receive the item since before the departure of the -th bidder. Let be the reported departure time of the -th bidder based on the departure schedule. The only way for bidder to possibly obtain the item is to report a later departure time, denoted as , such that . However, the auction allocates at her reported departure time , which falls outside her active time. Based on our assumption, she receives no value from the item. Such bidder therefore has no incentive to change her type to obtain the item. ∎

We now make the following observation: if there exists a value in the first bidders that is weakly more than the prediction, then the price the winner pays is fixed. {rObs}[] Let be the maximum value of the first departed bidders. If in Line 1, , then the price winners pays is .

We refer to the above scenario as the single-threshold case since is effectively only updated once (from to ), analogously, we refer to the other scenario as the two-threshold case. We note that only the first bidders can define therefore they (together with the prediction) decide which case the rest of the bidders are in. We first show that the rest of the bidders have no incentive to lie in the single-threshold case. The next two lemmas focus on bidders with true value below and above the threshold, respectively. {rLem}[] Consider some bidder , and any that results in the single-threshold case and let be the thresholds defined in Line 1. If bidder has a value , she has no incentive to misreport her type . {rLem}[] Consider some bidder , and any that results in the single-threshold case and let be the thresholds defined in Line 1. If bidder has a value , she has no incentive to misreport her type . We now discuss the more involved case, the two-threshold case. For the ease of presentation, we will denote the threshold defined in Line 1 as and the threshold defined in Line 1 as . Note that ( is equivalent to the single-threshold case). We first show that winners in this case can’t manipulate the price via misreporting.

Lemma 6.

Consider some bidder , and any that results in the two-threshold case. If is the winner with her true type , then bidder has no incentive to misreport her type .

Proof.

Consider the two possible prices the bidder is paying, and . If bidder wins and pays (the cheaper one), she has no incentive to deviate as it is the best outcome. Consider the cases where bidder wins with price . By the payment rule, she either left before the update (she is ranked before with respect to departure time) or there must exist a bidder that wins in Line 2 of the payment rule. Consider the three possible cases below:

Case one: . In this case the bidder departs before the threshold drops to . To possibly get the lower price, she has to report a departure time . However, the auction allocates at her reported departure time which falls outside her active time. Based on our assumption, she receives no utility from the item.

Case two: . This means that some other bidder is above the threshold before it drops. In this case, the winner can’t reduce the price since the existence of such a bidder is independent of her report.

Case three: and . This case happens when becomes available right after the threshold drops to . Since both the tie-breaking rule and the existence of bidder are independent of bidder ’s report, bidder can’t get a better price via misreporting. ∎

We now demonstrate that the losing bidders cannot benefit from misreporting as well. The next lemma shows that bidders with values below have no incentive to lie. The proof is almost identical to the proof of Lemma 5.

[] Consider some bidder , and any that results in the two-threshold case and let and be the thresholds defined in Line 1 and Line 1 respectively. If bidder has a value , she has no incentive to misreport her type .

The next lemma shows that the losing bidder with values above has no incentive to lie. The proof is almost identical to the proof of Lemma 5 regrading the losing bidders. {rLem}[] Consider some bidder , and any that results in the two-threshold case and let and be the thresholds defined in Line 1 and Line 1 respectively. If bidder has a value and she is not the winner, she has no incentive to misreport her type . The next lemma shows that bidders with value in between the two threshold have no incentive to lie.

Lemma 7.

Proof.

Consider a bidder with a value such that who is not the winner. The only outcome that is strictly better for her is winning the item with a price of . For the rest of the proof we show that such outcome is not obtainable by such bidders through misreporting. Since is not the winner, there must be another bidder who either has a value above the threshold before or is above the threshold at the same time as but . Since ’s value is less than , she can only be above the threshold after the departure of the -th bidder if she reports her true type.

Case one: If bidder is above the threshold before bidder , two scenarios are possible. First, bidder is above the threshold before the arrival time of bidder , in which case there is no way bidder can misreport and win the item, as we assume bidders cannot report an arrival time earlier than their actual arrival time. If bidder ’s value is not above the threshold before bidder ’s arrival time but is earlier than when is above the threshold, it must be that bidder ’s arrival time is before the threshold drops to , and bidder is above the threshold . In this case, bidder indeed can report a value to win the item. However, due to the presence of bidder , the price she needs to pay is by Line 2 of the payment subroutine, implying that bidder would reduce her utility by misreporting in this way.

Case two: If bidder loses to bidder in the tie-breaking, this can only occur when the threshold drops to 222In all of the cases, we consider the bidders with respect to some ordering even if they arrive at the same time.. The only way for bidder to win the item is if she has an arrival time before the threshold drop and reports a value to avoid the tie-breaking. However, due to the presence of bidder , we would get and , making . Even if bidder obtains the item, her utility is non-positive. ∎

We are now ready to show the main Lemma of the subsection

Lemma 8.

Three-Phase is both value-strategyproof and time-strategyproof.

3.3 The Error-Tolerant Auction

We now show that our auction can be easily extended to achieve an improved revenue guarantee not only when the prediction is perfectly accurate, but even when it is approximately accurate. Given a prediction regarding the maximum bidder value , we use , or just , to capture the prediction quality, defined as the relative under- or over-prediction:

Note that and that higher values of correspond to better predictions.

We start by describing the Error-Tolerant auction, which is an extension of the Three-Phase auction. This auction takes as input an additional parameter called the error-tolerance parameter and whose value is chosen by the auction designer. The only change from Three-Phase to Error-Tolerant is that Line 1 is changed from to . The main result for the Error-Tolerant auction is that when the prediction quality is at least the error-tolerance , then the auction achieves a revenue guarantee of . Thus, in that case, a competitive ratio of is guaranteed against the first-best revenue benchmark , even if the prediction is not exactly correct. In addition, a competitive ratio of against the second-best revenue benchmark is always maintained. We defer the proof to Appendix B. {rThm}[] Error-Tolerant is a value-strategyproof and time-strategyproof online auction that, given any parameter , , and the actual quality of the prediction, achieves expected revenue at least

4 A Tight Impossibility Result

In this section, we show that the tradeoff achieved by our auction is optimal for a natural family of auctions. To define this family of auctions, we first need to define the family of instances , called the no-overlap instances. A no-overlap instance is such that at each time step , there is a single active bidder such that (the values can be arbitrary). For the remainder of this section, we implicitly assume that we are only considering no-overlap instances and show that the tight impossibility result holds on this restricted family of instances. We refer to bidder as the bidder who arrives and departs at time The analysis of the impossibility result considers two nested families of auctions. The first is called the family of Prediction or Maximum-so-Far (PMF) auctions.

Definition 9.

Consider the following three allocation rules: never allocates the item to bidder , allocates to if , and allocates to if . An auction is in the family of Prediction or Maximum-so-Far (PMF) auctions if, for every bidder , there is an allocation rule such that, for all no-overlap instances , if the item is not allocated to a bidder then allocates to according to .

It is easy to verify that our auction, as well as online auctions in previous work that are without predictions [20, 14], are PMF auctions. Our impossibility result holds for a family of auctions that generalizes PMF auctions. In a Prediction or Any-so-Far (PAF) auction , the allocation rules can depend on the highest value seen so far , for any .

Definition 10.

Consider the following allocation rules for bidder :

-

•

never allocates the item to bidder ,

-

•

for all , allocates to if , and

-

•

for all , allocates to if .

Let . An auction is in the family of Prediction or Any-so-Far (PAF) auctions if, for every bidder , there is an allocation rule such that, if the item is not allocated to a bidder , allocates to according to for all no-overlap instances .

Observe that .

The main result in this section is the following.

Theorem 11.

For any , there is no auction in the PAF family of auctions that is -consistent and -robust.

We conjecture that the above result also holds for all strategyproof auctions. Note that, even without predictions, there is still a gap between the best-known -competitive auction and the impossibility result of [20]. Thus, showing that Theorem 11 holds for all strategyproof auctions would also close the gap for the setting without predictions.

Overview of the proof.

By Myerson’s Lemma [30], we have that for any PAF auction and bidder , there is a price such that, if the item is not allocated to a bidder , posts price to bidder for all no-overlap instances . We say that an -consistent auction is robustness-optimal among if and there is no -consistent auction that achieves strictly better robustness than .

-

1.

We first show that, for any PAF auction , there exists a PMF auction that achieves consistency and robustness that are no worse than those achieve by (Section 4.1). Thus, impossibility results for PMF auctions extend to PAF auctions.

-

2.

We then show that, for any , there exist and an -consistent, robustness-optimal auction among auctions in that posts price at each time , then price at each time , and finally price at each time (Section 4.2). This is the main part of the proof.

-

3.

Finally we show that, for the auction structure described in the second step, the optimal thresholds for maximizing robustness are and , achieving robustness at most (Section 4.3).

4.1 The reduction from PAF to PMF auctions

We start by giving a simple formula for the consistency and robustness of auctions in over the family of instances . Observe that for instances in , the random matching of values to intervals is equivalent to drawing a random permutation that maps the values to indices . Let be the set of all permutations over the bidders. Given a permutation , we define as the rank of the ith arriving bidder. In particular, if bidder is the bidder with the highest value. If multiple bidders have equal value, we break ties arbitrarily and consistently. Then we have that denotes the position of the th highest ranked bidder. For , we let and .

Lemma 12.

Consider an auction . Over the family of no-overlap instances , its consistency is and its robustness is .

Proof.

Observe that for each , the auction achieves revenue when the prediction is correct. In addition, for each , the auction achieves revenue , even when the prediction is incorrect. Then consistency and robustness are lower bounded by the probability of drawing and respectively from , which are precisely and .

To show that consistency is at most , it suffices to find a single instance where equality holds. Consider the instance where the values are and prediction (we will denote this ). Observe from our definition of PAF auctions, the only (noninfinite) prices that can be posted to bidder are in the set . For this instance, only two of these may be nonzero, or if the highest bidder arrives at step bidder. In the first case, the only bidder who can accept this price is the highest bidder, and revenue of is extracted. In the second case, we know the highest bidder has already departed, so bidder must have value and no revenue can be gained. Thus the only way revenue is gained in this instance is by posting to the highest bidder at step , and the revenue is precisely , so consistency is exactly .

Similarly, for robustness consider the instance where the values are for some and the prediction is (we will denote this ). No revenue is gained by posting since no bidder would accept that price. The only other positive prices that can be posted to bidder are if the highest bidder arrives at step or if the second highest bidder arrives at step . The first case is the same as above. As for , the only bidder who can accept this price is the highest bidder, and revenue of is gained. Thus the only way revenue is gained in this instance is by posting price to the highest bidder at step , and the revenue is precisely , so robustness is . ∎

Lemma 13.

For every , there exists some such that

Proof.

We will construct from as follows. We determine the allocation rule uses for bidder :

Note that and allocate the item to bidder i if is at least and respectively.

Next, we show that . First, we have that by Lemma 12, so it is sufficient to show that . Consider any with . Observe that if does not allocate the item prior to step , neither does because at any , posts to a price at least as high as the price posts to . Since price is posted by to , we know that , and subsequently , so also posts price to . Thus , and therefore .

Similarly, we show that by proving that . Consider any with . By the same argument as above, if does not allocate the item prior to step neither does . Since posts price to , there are two cases for . Case 1 is if . Note that we know because must be seen at time i. Then and also posts to bidder . Case 2 is , and by the same reasoning. Then and again posts to bidder . Thus and . ∎

By Lemma 13, impossibility results for extend to .

4.2 The main lemma for the impossibility result

The main lemma for the impossibility result shows that there exists an -consistent auction that is robustness-optimal among auctions in and has, on no-overlap instances, a three-phase structure (as our auction).

Lemma 14.

There exists an -consistent auction that is robustness-optimal among auctions in and satisfies the following structure: it posts price at each time , then price at each time , and finally price at each time .

Overview of the proof of Lemma 14.

The proof follows an interchange argument that shows that if an auction does not post prices in the order specified by Lemma 14, then there are two positions and that violate this order and the prices posted at these time steps can be swapped without decreasing and , and therefore without decreasing consistency and robustness. There are three potential violations of the ordering specified by Lemma 14. In Lemma 16, we consider the case where is posted to bidder and to bidder , in Lemma 17 the case where is posted to bidder and to bidder , and in Lemma 18 the case where to bidder and to bidder .

We now define the interchange function . For fixed index and any permutation , let

which is a bijective function that swaps the values of the ith and (i+1)th bidders. We first state a trivial fact regarding the revenue achieved from the first bidders for two auctions that are identical up to step . This fact will be repeatedly used in the proof of the next lemmas.

Lemma 15.

Consider two auctions that are identical for steps up to . Then under order and under order gain the same revenue before step .

Proof.

Observe that does not affect the values that appear before . Then sees the same ranks before under as does under , and since they follow the same rules the revenue gained at each step before is the same. ∎

The first potential violation of the ordering specified by Lemma 14 is when is posted to bidder and to bidder .

Lemma 16.

Consider an auction that posts price at some step and at step . Let be the same auction as except that it posts price at step and at step . Then, and .

Proof.

First we show that if , then , meaning . Since is a bijective function, consequently . Assume that . Consider any , then is posted to the highest ranked bidder who arrives at step . Observe that to prove , it is sufficient to show that price is posted to bidder , or that revenue is extracted by under ordering . There are three cases.

First, if , observe that there is no difference between and before step . Then it follows from Lemma 15 that since extracts revenue at step , extracts the same revenue under before step .

The second case is if . Recall that implies that price is posted to bidder . Then since posts to bidder , is the only possibility, and indeed posts to . Now we must show that posts price to . By our definition of the interchange function, , so . Note that if reaches step , then does as well. Then since posts price at step , then .

The third and last case is if . Observe that it is sufficient to show that under , bidders and do not receive the item because at steps after , the auctions see the same order of bidders and make the same posts. Clearly if under bidder does not accept its posted-price , ie , then under , bidder with value will not accept its posted price . Now we consider bidder under . If we let be the value of the highest ranked bidder seen before step given ordering , we can see that . Then if bidder does not accept the price posted under , ie , then and under bidder also does not accept its posted price .

Next, to show the second part of lemma, we show that . If is true, then is posted to the bidder at step . Similar to the consistency proof, to prove , it is sufficient to show that price is posted to bidder , or that revenue is extracted by under ordering (for any value of ). Cases 1 and 3 are exactly the same as for consistency. Then consider .

If , then under price is posted to and rejected by bidder , so is the only possibility. Indeed, price may be posted to if the second highest bidder arrives before . After the interchange, bidder is offered price under and they reject it. Observe that if , then . Then under , bidder sees price .

Now if , then there are two scenarios. First, consider , then since posts at we know that . Observe that since the highest two bidders arrive by step , then . Under , bidder has value . Then when posts to bidder price , it is rejected. then posts price , which is exactly because bidder has value below , to the bidder with rank . If instead , then it is impossible for bidder to have the second highest value or else they would accept their price . Then for to hold, the second highest bidder must arrive before and . Thus under , price is posted at step to the bidder with rank .

Observe that if , given that , selling by posting and both result in at least revenue, so swapping these two prices does not lower robustness. ∎

The second potential violation of the ordering specified by Lemma 14 is when is posted to bidder and to bidder .

Lemma 17.

Consider an auction that posts price at some step and at step . Let be the same auction at except that it posts price at step and at step . Then, and .

Proof.

We first show that by proving that . Let . Consider any , so is posted to bidder . There are again three cases. The first case, , is as in Lemma 16. The second case is . Observe that it is impossible to post to bidder by posting or . This is because . The third and last case is . It is sufficient to show that does not sell the item at time or . Clearly the former is true because is posted to . Since fails to sell the item at step by posting price , we know that . Then under , the price is posted to bidder with value , so the item is not sold to bidder under .

For the second part of the lemma, we show for any . If is true, then is posted to the bidder at step . Similar to the consistency proof, to prove , it is sufficient to show that price is posted to bidder , or that revenue is extracted by under ordering (for any value of ). Once again, cases one and three are the same. Now consider . Since bidder never accepts , this means that . posts price to bidder , so . Observe that . First posts at step , and then , which equals since the highest bidder cannot be at step under . Then is posted to bidder . ∎

The third and last potential violation of the ordering specified by Lemma 14 is when to bidder and to bidder .

Lemma 18.

Consider an auction that posts price at some step and at step . Let be the same auction at except that it posts price at step and at step . Then, and .

Proof.

We again first show that by proving that . Let . Consider any , so is posted to bidder . The first case, , is as in Lemma 16. The second case is . Since auction posts to , is the only possibility, and indeed is posted at . First observe that if reaches step , then does as well. subsequently posts to bidder , effectively skipping them. We know that . Then when under auction posts at step , it is to the highest bidder. The third and last case is . Use the same argument as in Lemma 17 except instead of being rejected by bidder under and under , here is being rejected by bidder under and under .

For the second part of the lemma, we show that for . If is true, then is posted to the bidder at step . Similar to the consistency proof, to prove , it is sufficient to show that price is posted to bidder , or that revenue is extracted by under ordering (for any value of ). Observe that the proofs for cases 1 and 3 are the same as above. Case two is impossible if because no bidder accepts prices or . Then if , we have , as auction posts to bidder . In order for value at least (but below ) to be posted at step by , we need , so it is sufficient for the second highest bidder to arrive before and therefore . Observe that . Under , is posted to bidder , and then is posted to bidder . We know that by the same reasoning as in Lemma 17. Then posts to bidder with the highest value. ∎

We are now ready to prove Lemma 14.

Proof of Lemma 14. Consider an -consistent robustness-optimal auction . If it does not satisfy the structure specified by Lemma 14, then there exist time steps and such that either posts prices and , or prices and , or prices and to and . Lemma 16, Lemma 17, and Lemma 18 show that for each of these cases, the two prices can be swapped without decreasing and . By repeating this swapping process, we obtain an auction such that and .

4.3 The optimal thresholds

For auctions in constructed as in Lemma 14, the time thresholds and set to and achieve -consistency and -robustness. We show that for , no other thresholds lead to a better robustness, which then shows the impossibility result for PAF auctions. We note that our auction also use these same thresholds.

Proof of Theorem 11. Let us first introduce some notation. Let be the event that step is reached under auction and let be the event that is posted at step under auction . For a fixed , consider an -consistent auction that is optimal with respect to robustness and is structured as in Lemma 14 with time thresholds and . Observe that if , then the consistency achieved by is

where the first equality is because is posted only at steps and the highest ranking bidder is equally likely to be at any step. The second equality holds because posting up to step and bidders within failing to accept price . Thus, achieves -consistency if .

In our auction, we use and , and we show no other pair can improve robustness. Recall from Lemma 12 that the robustness of is precisely . We consider two cases. The first is if . Observe that if , and letting being a uniformly random permutation in , then we have that

where the first equality is by definition of and the second by definition of . The third equality is since we need to not post to , so that is posted to , and to not sell to and reach . Differentiating with respect to , we get , which is positive for . Then since , we get that the robustness of is .

The second case is if . Since , then . Observe that if , and letting being a uniformly random permutation in , then we have that

where the second equality is since we need to not post or to , so that is posted to , and to not sell to and reach . Differentiating with respect to , we get , which is negative for . Since , we obtained that the robustness achieved by is .

References

- Agrawal et al. [2022] P. Agrawal, E. Balkanski, V. Gkatzelis, T. Ou, and X. Tan. Learning-augmented mechanism design: Leveraging predictions for facility location. In EC ’22: The 23rd ACM Conference on Economics and Computation, Boulder, CO, USA, July 11 - 15, 2022, pages 497–528. ACM, 2022.

- Antoniadis et al. [2023] A. Antoniadis, T. Gouleakis, P. Kleer, and P. Kolev. Secretary and online matching problems with machine learned advice. Discret. Optim., 48(Part 2):100778, 2023.

- Azar et al. [2022] Y. Azar, D. Panigrahi, and N. Touitou. Online graph algorithms with predictions. Proceedings of the Thirty-Third Annual ACM-SIAM Symposium on Discrete Algorithms, 2022.

- Balcan et al. [2023] M. Balcan, S. Prasad, and T. Sandholm. Bicriteria multidimensional mechanism design with side information. CoRR, abs/2302.14234, 2023. doi: 10.48550/arXiv.2302.14234. URL https://doi.org/10.48550/arXiv.2302.14234.

- Balkanksi et al. [2023] E. Balkanksi, V. Gkatzelis, and X. Tan. Mechanism design with predictions: An annotated reading list. SIGecom Exchanges, 21(1):54–57, 2023.

- Balkanski et al. [2023] E. Balkanski, V. Gkatzelis, and X. Tan. Strategyproof scheduling with predictions. In Y. T. Kalai, editor, 14th Innovations in Theoretical Computer Science Conference, ITCS 2023, January 10-13, 2023, MIT, Cambridge, Massachusetts, USA, volume 251 of LIPIcs, pages 11:1–11:22. Schloss Dagstuhl - Leibniz-Zentrum für Informatik, 2023. doi: 10.4230/LIPIcs.ITCS.2023.11. URL https://doi.org/10.4230/LIPIcs.ITCS.2023.11.

- Bamas et al. [2020] É. Bamas, A. Maggiori, and O. Svensson. The primal-dual method for learning augmented algorithms. In Advances in Neural Information Processing Systems 33: Annual Conference on Neural Information Processing Systems 2020, NeurIPS 2020, December 6-12, 2020, virtual, 2020.

- Banerjee et al. [2022] S. Banerjee, V. Gkatzelis, A. Gorokh, and B. Jin. Online nash social welfare maximization with predictions. In Proceedings of the 2022 ACM-SIAM Symposium on Discrete Algorithms, SODA 2022. SIAM, 2022.

- Bar-Yossef et al. [2002] Z. Bar-Yossef, K. Hildrum, and F. Wu. Incentive-compatible online auctions for digital goods. In D. Eppstein, editor, Proceedings of the Thirteenth Annual ACM-SIAM Symposium on Discrete Algorithms, January 6-8, 2002, San Francisco, CA, USA, pages 964–970. ACM/SIAM, 2002. URL http://dl.acm.org/citation.cfm?id=545381.545506.

- Blum and Hartline [2005] A. Blum and J. D. Hartline. Near-optimal online auctions. In Proceedings of the Sixteenth Annual ACM-SIAM Symposium on Discrete Algorithms, SODA 2005, Vancouver, British Columbia, Canada, January 23-25, 2005, pages 1156–1163. SIAM, 2005. URL http://dl.acm.org/citation.cfm?id=1070432.1070597.

- Blum et al. [2003] A. Blum, V. Kumar, A. Rudra, and F. Wu. Online learning in online auctions. In Proceedings of the Fourteenth Annual ACM-SIAM Symposium on Discrete Algorithms, January 12-14, 2003, Baltimore, Maryland, USA, pages 202–204. ACM/SIAM, 2003. URL http://dl.acm.org/citation.cfm?id=644108.644143.

- Blum et al. [2006] A. Blum, T. Sandholm, and M. Zinkevich. Online algorithms for market clearing. J. ACM, 53(5):845–879, 2006. doi: 10.1145/1183907.1183913. URL https://doi.org/10.1145/1183907.1183913.

- Bredin and Parkes [2012] J. Bredin and D. C. Parkes. Models for truthful online double auctions. CoRR, abs/1207.1360, 2012. URL http://arxiv.org/abs/1207.1360.

- Buchbinder et al. [2010] N. Buchbinder, K. Jain, and M. Singh. Incentives in online auctions via linear programming. In International Workshop on Internet and Network Economics, pages 106–117. Springer, 2010.

- Buchbinder et al. [2014] N. Buchbinder, K. Jain, and M. Singh. Secretary problems via linear programming. Mathematics of Operations Research, 39(1):190–206, 2014. URL http://www.jstor.org/stable/24540892.

- Constantin et al. [2007] F. Constantin, T. Ito, and D. C. Parkes. Online auctions for bidders with interdependent values. In E. H. Durfee, M. Yokoo, M. N. Huhns, and O. Shehory, editors, 6th International Joint Conference on Autonomous Agents and Multiagent Systems (AAMAS 2007), Honolulu, Hawaii, USA, May 14-18, 2007, page 110. IFAAMAS, 2007. doi: 10.1145/1329125.1329260. URL https://doi.org/10.1145/1329125.1329260.

- Dütting et al. [2021] P. Dütting, S. Lattanzi, R. P. Leme, and S. Vassilvitskii. Secretaries with advice. In P. Biró, S. Chawla, and F. Echenique, editors, EC ’21: The 22nd ACM Conference on Economics and Computation, Budapest, Hungary, July 18-23, 2021, pages 409–429. ACM, 2021.

- Fujii and Yoshida [2023] K. Fujii and Y. Yoshida. The secretary problem with predictions. CoRR, abs/2306.08340, 2023.

- Gkatzelis et al. [2022] V. Gkatzelis, K. Kollias, A. Sgouritsa, and X. Tan. Improved price of anarchy via predictions. In Proceedings of the 23rd ACM Conference on Economics and Computation, pages 529–557, 2022.

- Hajiaghayi et al. [2004] M. T. Hajiaghayi, R. Kleinberg, and D. C. Parkes. Adaptive limited-supply online auctions. In Proceedings of the 5th ACM Conference on Electronic Commerce, pages 71–80, 2004.

- Im et al. [2021] S. Im, R. Kumar, M. M. Qaem, and M. Purohit. Online knapsack with frequency predictions. In Advances in Neural Information Processing Systems 34: Annual Conference on Neural Information Processing Systems 2021, NeurIPS 2021, December 6-14, 2021, virtual, pages 2733–2743, 2021.

- Istrate and Bonchis [2022] G. Istrate and C. Bonchis. Mechanism design with predictions for obnoxious facility location. CoRR, abs/2212.09521, 2022.

- Koutsoupias and Pierrakos [2013] E. Koutsoupias and G. Pierrakos. On the competitive ratio of online sampling auctions. ACM Transactions on Economics and Computation (TEAC), 1(2):1–10, 2013.

- Krysta and Telelis [2012] P. Krysta and O. Telelis. Limited supply online auctions for revenue maximization. In International Workshop on Internet and Network Economics, pages 519–525. Springer, 2012.

- [25] A. Lindermayr and N. Megow. Alps. URL https://algorithms-with-predictions.github.io/.

- Lykouris and Vassilvtiskii [2018] T. Lykouris and S. Vassilvtiskii. Competitive caching with machine learned advice. In International Conference on Machine Learning, pages 3296–3305. PMLR, 2018.

- Medina and Vassilvitskii [2017] A. M. Medina and S. Vassilvitskii. Revenue optimization with approximate bid predictions. In I. Guyon, U. von Luxburg, S. Bengio, H. M. Wallach, R. Fergus, S. V. N. Vishwanathan, and R. Garnett, editors, Advances in Neural Information Processing Systems 30: Annual Conference on Neural Information Processing Systems 2017, December 4-9, 2017, Long Beach, CA, USA, pages 1858–1866, 2017. URL https://proceedings.neurips.cc/paper/2017/hash/884d79963bd8bc0ae9b13a1aa71add73-Abstract.html.

- Mitzenmacher and Vassilvitskii [2021] M. Mitzenmacher and S. Vassilvitskii. Algorithms with predictions. In T. Roughgarden, editor, Beyond the Worst-Case Analysis of Algorithms, page 646–662. Cambridge University Press, 2021. doi: 10.1017/9781108637435.037.

- Mitzenmacher and Vassilvitskii [2022] M. Mitzenmacher and S. Vassilvitskii. Algorithms with predictions. Commun. ACM, 65(7):33–35, 2022.

- Myerson [1981] R. B. Myerson. Optimal auction design. Mathematics of operations research, 6(1):58–73, 1981.

- Nisan et al. [2007] N. Nisan, T. Roughgarden, E. Tardos, and V. V. Vazirani. Algorithmic Game Theory. Cambridge University Press, New York, NY, USA, 2007.

- Parkes [2007] D. C. Parkes. Online mechanisms. In N. Nisan, T. Roughgarden, E. Tardos, and V. V. Vazirani, editors, Algorithmic Game Theory, page 411–440. Cambridge University Press, 2007. doi: 10.1017/CBO9780511800481.018.

- Purohit et al. [2018] M. Purohit, Z. Svitkina, and R. Kumar. Improving online algorithms via ML predictions. In Advances in Neural Information Processing Systems 31: Annual Conference on Neural Information Processing Systems 2018, NeurIPS 2018, December 3-8, 2018, Montréal, Canada, pages 9684–9693, 2018.

- Xu and Lu [2022] C. Xu and P. Lu. Mechanism design with predictions. In L. D. Raedt, editor, Proceedings of the Thirty-First International Joint Conference on Artificial Intelligence, IJCAI 2022, Vienna, Austria, 23-29 July 2022, pages 571–577. ijcai.org, 2022.

Appendix A Missing proofs from Section 3.2

See 5

Proof.

If in Line 1, it means that . First note that will never equal to , implying . Consider the case where the winner is above the threshold before the -th bidder departs, then the allocation is terminated before the possible update of , making . Consider the case where the winner, denoted as is above the threshold after the departure of the -th bidder, then , since there are no bidder with value higher than before bidder , in this case the payment is also . ∎

See 5

Proof.

First, note that if such a bidder, denoted as , reports her type truthfully, she won’t receive the item. The only way she can possibly win the item is by reporting a value . However, since, as observed in Observation 5, in the case of a single threshold, the price , bidder would incur non-positive utility if she were to obtain the item. ∎

See 5

Proof.

By Lemma 5, we already have that the bidders with the first departures has no incentive to misreport. Note that the threshold , and therefore the payment , is independent of the rest of the bidders’ reports. First if bidder , with her true type, wins the auction, then she has no incentive to misreport since the price is independent of her report. We now consider some bidder with but bidder is not the winner. This can only result from one of the following two scenarios: 1. Some other bidder is above the threshold before bidder is above the threshold. 2. bidder and some bidder are above the threshold at the same time, but bidder loses in tie-breaking. We will now address these two cases separately.

Case one: Since in the single-threshold case is not updated after Line 1, it means that bidder is above the threshold before the arrival time of bidder . For bidder to claim the item, she would need to report an earlier arrival time to be above the threshold weakly earlier than bidder . However, this is not a feasible outcome since we assume bidders cannot report .

Case two: First, note that by the definition of our auction and the fact that , the only possible tie-breaking happens at Line 1 after changes from to . Since the tie-breaking rules are independent of bidders’ reports, there is no way for bidder to change the results of the tie-breaking. Additionally, since the threshold is before this point, there is also no way for bidder to misreport her type to win the item. ∎

See 6

Proof.

First, note that if such a bidder, denoted as , reports her type truthfully, she won’t receive the item. The only way she can possibly win the item is by reporting a value . However, since the price , bidder would incur negative utility if she were to obtain the item. ∎

See 6

Proof.

Consider some bidder with but bidder is not the winner. First note that if by Lemma 5 she has no incentive to misreport. Consider any but is not the winner. Then it can only result from one of the following two scenarios: 1. Some other bidder is above the threshold before bidder is above the threshold. 2. bidder and some bidder are above the threshold at the same time, but bidder loses in tie-breaking. We will now address these two cases separately.

Case one: Since , it means that bidder is above the threshold before the arrival time of bidder . For bidder to claim the item, she would need to report an earlier arrival time to be above the threshold weakly earlier than bidder . However, this is not a feasible outcome since we assume bidders cannot report .

Case two: First, note that by the definition of our auction and the fact that , the only possible tie-breaking happens at Line 1 after changes from to . Since the tie-breaking rules are independent of bidders’ reports, there is no way for bidder to change the results of the tie-breaking. Additionally, since the threshold is before this point, there is also no way for bidder to misreport her arrival as earlier to win the item. ∎

Appendix B Missing Proofs from Section 3.3

See 3.3

Proof.

We first prove that the worst case expected revenue is always bounded by . The argument is identical to the proof of Lemma 4, but changing the case conditions from and to and , respectively.

We now prove the bound when the prediction is relatively accurate, i.e., . First by the definition of we have . Suppose , then . Consider the same instance we consider in Lemma 3, where the highest value agent , i.e., agent in the second phase. First note that she will get the item and pay , since and . In addition, the threshold . In this case the revenue achieved is at least

Since such instance happens with probability . We therefore have that the expected revenue is at least when .

Lastly, we note that the strategyproof argument for auction Error-Tolerant is identical to that for auction Three-Phase. ∎