Stable Estimation of Survival Causal Effects

Abstract

We study the problem of estimating survival causal effects, where the aim is to characterize the impact of an intervention on survival times, i.e., how long it takes for an event to occur. Applications include determining if a drug reduces the time to ICU discharge or if an advertising campaign increases customer dwell time. Historically, the most popular estimates have been based on parametric or semiparametric (e.g. proportional hazards) models; however, these methods suffer from problematic levels of bias. Recently debiased machine learning approaches are becoming increasingly popular, especially in applications to large datasets. However, despite their appealing theoretical properties, these estimators tend to be unstable because the debiasing step involves the use of the inverses of small estimated probabilities—small errors in the estimated probabilities can result in huge changes in their inverses and therefore the resulting estimator. This problem is exacerbated in survival settings where probabilities are a product of treatment assignment and censoring probabilities. We propose a covariate balancing approach to estimating these inverses directly, sidestepping this problem. The result is an estimator that is stable in practice and enjoys many of the same theoretical properties. In particular, under overlap and asymptotic equicontinuity conditions, our estimator is asymptotically normal with negligible bias and optimal variance. Our experiments on synthetic and semi-synthetic data demonstrate that our method has competitive bias and smaller variance than debiased machine learning approaches.

1 Introduction

The estimation of the impact of interventions on survival times is a key objective in numerous studies. This analytical approach is important in various domains, including drug efficacy’s evaluation at ICU stay duration and assessment of advertising campaigns’ effects on customer dwell time.

The predominant approach for assessing the impact of interventions on survival times is to employ the Cox proportional hazards model (CoxPH) [Cox, 1972, Andersen and Gill, 1982]. This model estimates conditional hazard ratios, which serve as a measure of survival causal effects. However, the causal interpretation of conditional hazard ratios within the CoxPH model can be complex [Martinussen, 2022, Vansteelandt et al., 2022]. Hence, there has been a growing interest in directly estimating counterfactual survival curves and consequently deriving survival causal effects from these estimates [Westling et al., 2023] such as the average survival effect, the residual average survival effect, and the survival quantile effect [Mansourvar et al., 2016, Mao et al., 2018]. A counterfactual survival curve represents the probability of an event occurring at a specific point in time, if contrary to fact, the entire population had undergone a specific intervention, given that the event of interest has not yet occurred.

Traditional approaches for estimating counterfactual curves in survival analysis have relied on conditional parametric or semiparametric regression models [Kleinbaum and Klein, 2012, Cox, 1972], or weighted methods based on inverse probability of censoring and treatment weighting (IPW) [Robins and Rotnitzky, 1992]. However, both approaches can suffer from model misspecification i.e. the model does not contain the truth. Weighted methods are also susceptible to extreme inversions [Kang et al., 2007, Kallus and Santacatterina, 2022, Kallus, 2021]. In recent years, debiased machine learning approaches have gained popularity due to their appealing double robustness property which deals with model misspecification in addition to being semiparametric efficient [Kennedy, 2022]. Specifically, double robustness implies that even if only certain models that need to be estimated are correctly specified, these approaches remain consistent, ie., asymptotycally unbiased. Semiparametric efficiency refers to the ability of an estimator or estimation method to achieve the smallest possible asymptotic variance among a class of semiparametric estimators. Despite their desirable theoretical properties, debiased machine learning methods still face challenges associated with extreme inversions because they are necessarily characterized by inverse probability weights [Chernozhukov et al., 2022a].

Covariate balancing methods have been proposed as a solution to the issue of extreme weights encountered in other approaches [Ben-Michael et al., 2021]. Instead of directly incorporating inverse probabilities, these methods employ a weight-learning process that yields more stable estimates while preserving crucial properties like semiparametric efficiency. However, the application of these methods to estimate survival causal effects has been significantly limited [Xue et al., 2023, Wong and Chan, 2017, Abraich et al., 2022, Johansson et al., 2022, Santacatterina, 2023, Kallus and Santacatterina, 2021, Yiu and Su, 2022], with none of them providing results on asymptotic normality. Asymptotic normality is crucial for statistical inference, hypothesis testing, and the construction of confidence intervals, highlighting a current gap in the literature.

We contribute to the literature of survival causal effects estimation by presenting a novel approach based on covariate balancing techniques. Our proposed method offers stability in practical applications, and when certain conditions such as overlap and asymptotic equicontinuity are met, it demonstrates asymptotic normality with minimal bias and optimal variance, ie., statistically efficiency. We substantiate these claims both theoretically and through experiments conducted on synthetic data. Proofs, additional experiments and some technical details are deferred to appendices.

2 Setting

In this section, we review the notations and main quantities in standard discrete survival analysis (Section 2.1). We refer interested readers to e.g. Chapter 16 of Crowder [2012] for further details. We then introduce counterfactual survival analysis including the causal parameter of interest and identification assumptions using the Neyman-Rubin potential outcome framework [Neyman, 1923, Rubin, 1974] (Section 2.2). Finally, some useful notations are introduced in Section 2.3.

2.1 Discrete Survival Analysis

Data structure.

We define an observable survival data unit as the set of random variables where is the covariate recorded prior to the beginning of the study. To define and , let be the time-to-event and the time-to-censoring (censor time), where means that the event has not happened during the study time window . In a clinical study, can be the patient’s time from their entry to the study until their death - the event of interest. The events may not happen during the study’s time or the patients drop out before the end of the study, therefore a censoring time is introduced. Define the right-censored time and the event indicator. If , the event is observed and occurs at time , otherwise, the event has not happened or is censored at time . We assume discrete , and , so that zero times are ruled out. Denote the total number of time points and the number of time points less than or equal to . may be chosen by the user, or as a result of administrative censoring .

The marginal and sub-survival functions.

We seek to recover the distributions of latent time from the observable and . Define the marginal-hazard, the marginal-survival function of and the marginal-censoring function of as follows:

| (1) |

These definitions imply a one-to-one relationship between and : letting ,

| (2) |

For observable data, define the sub-hazard and sub-survival function as:

| (3) |

When and are conditionally independent given , the following lemma relates the sub-distributions and the marginal-distributions:

Proposition 2.1.

If then: , therefore:

| (4) |

Additionally, the sub-survival function decomposes into a product of the marginal-survival functions of the event and censoring:

We provide a proof in Appendix B. This equivalence enables the estimation of all identities defined up to now from observable data. From here on, we will use term hazard to refer to the sub-hazard.

2.2 Counterfactual Survival Analysis

Data structure.

We define the ideal data unit in counterfactual survival analysis as , where is a binary random variable indicating e.g. whether or not a patient receives the treatment, is the event time of interest under and similarly for . With the introduction of , we define and , therefore the observable time and event indicator are defined as before. The observable data unit is now . In this context, we will talk about the treatment-specific hazard and survival function, and , characterized as in Section 2.1 in terms of the conditional distribution given treatment . With Lemma 2.1, we then define,

| (5) |

Survival causal parameter of interest: the counterfactual survival function.

We will focus mainly on the counterfactual survival function at time and treatment : . Other commonly encountered parameters can be built from it such as the average survival effect at time : and the treatment-specific mean survival time as well as its average effect counterpart. Where convenient, we will write in place of , letting the treatment and time of interest be inferred from context.

Identification

To identify the counterfactual survival function using the observable data, similar to Hubbard et al. [2000], Bai et al. [2013, 2017], Westling et al. [2023], Díaz [2019], Cai and van der Laan [2020], we require the following testable and untestable assumptions:

-

•

(A1) for each .

-

•

(A2) for each .

-

•

(A3) almost surely.

-

•

(A4) positivity (censoring),

Proposition 2.2.

When Assumptions (A1)-(A4) hold, can be computed by observable quantities

| (6) |

The proof, along with a discussion of the assumptions, appears in Appendix B.

2.3 Notation for our proposed approach

In the next section, it will be useful to think of the hazard at time , , as where

| (7) | ||||||

Furthermore, we’ll think of the functions as the components of a vector-valued function with Note that this vector-valued function has the property that its th component depends on only through the indicator ; we will call the space of vector-valued functions with this property the ’hazard-like functions’ . And we will think of our estimand , as identified in Proposition 6, as a functional on this space evaluated at :

| (8) |

We’ve written things in these terms to emphasize the analogy between our estimation problem and the problem of estimating a functional of a conditional expectation function considered in Hirshberg and Wager [2021] and Chernozhukov et al. [2022b]. What we are estimating is a functional of a vector-valued function that is, in each component, the conditional expectation function of an observed outcome given observed conditioning variable . We will work with an inner product on this space defined in terms of a random variable with the same distribution as .111Note that this is an average over only. If and are random variables, will be the random variable . We will do this conditioning implicitly throughout. Letting here and below,

| (9) |

While we cannot evaluate the functional or the inner product exactly because we do not know the distribution of , natural sample-average approximations are available.

| (10) |

3 Approach

3.1 A first-order approximation and the derivative’s Riesz representer

Given an estimate of the hazard , which we can get e.g. by using a machine-learning method of our choice to regress on at each timestep , the ‘plug-in estimate’ is a natural estimate of . But we can improve on this using a first-order correction. Consider the first-order Taylor expansion of around . In terms of its derivative at in the direction ,

| (11) |

Taking , the difference between our actual hazard and our estimate, we get a first-order approximation to our estimand . Our main concern will therefore be the estimation of this derivative term where, as established in Lemma C.2 in the appendix,

| (12) |

While and are known quantities, derived from our hazard estimate , we will need to substitute something for the actual hazard . For this purpose, is a natural proxy, as its conditional mean is the hazard at the observed levels of the conditioning variables ; our challenge is make this speak to its value at often-unobserved levels of those variables. To this end, we observe that the Riesz representation theorem guarantees that, for the space , there exists a unique element that acts (via an inner product) on the function like the functional derivative does, i.e., one satisfying

| (13) |

and, in particular, taking ,

| (14) |

We call the Riesz representer of . Substituting for gives us an equivalent expression for our derivative term. By the law of iterated expectations,

| (15) | ||||

So, supposing that we have an estimator for our Riesz representer, we obtain the following estimator for by replacing expectations with sample averages as in Equation (10).

| (16) |

3.2 Estimating the Riesz Representer

can be characterized in terms of inverse probability weights. The explicit solution to the set of equations defining the Riesz representer (Equation 13) is

| (17) | ||||

One approach is to estimate the functions and appearing in Equation (LABEL:eq:riesz-rep-explicit) and assemble them into an estimate of the Riesz representer . Taking this approach yields ‘one-step’ estimator discussed in Section 4 below. However, this solution suffers from instability, common in all inverse weight-based estimators. When the ground truth functions and are very small at some observations, naturally their estimators tends to be very small, hence, slight errors in estimating them can result in large errors in the estimation of their inverses (i.e. ). Thus, lack of overlap in the data means that such estimators will be unstable, with very large sample sizes needed to get estimates of and accurate enough to tolerate inversion. Moreover, even when when overlap in the data is not poor, moderate-sized errors in the estimation of and that occur at smaller sample sizes results in similar issues. It is common practice to clip these weights to a reasonable range before using them, but ad-hoc clipping often results in problematic levels of bias. In short, we lack practical and theoretically sound methods to make this inversion step work reliably.

Our approach, which avoids this problematic inversion, focuses not on the analytic form of the Riesz representer but on what it does, i.e., on the equivalence of the inner product to the derivative evaluation . As we lack the ability to analytically evaluate the expectations involved in both, we will use the sample average approximations of these quantities: (defined above) and . Inspired by the explicit characterization in Equation (LABEL:eq:riesz-rep-explicit), taking to have a functional form (for weights ) , we ask that, for a set of functions ,

| (18) |

In the simpler setting considered in Hirshberg and Wager [2021], this approximation has meaning beyond that, suggested by its relationship to the population analog Equation (13). The quality of the in-sample approximation described by Equation (18) for the specific function is, along with the accuracy of the estimator and therefore of the linear approximation in Equation (12), one of two essential determinants of the estimator’s bias. See Appendix C.2, where we include an informative decomposition of our estimator’s error and further discussion.

In light of that, we generalize the approach of Hirshberg and Wager [2021] for estimating by ensuring that Equation (18) holds for a set of hazard-like functions , which we deem as a model for function . In particular, we ask for weights that are (i) not too large, to control our estimator’s variance, and (ii) ensure the approximation in Equation (18) is accurate uniformly over model . This modeling task is somewhat simplified by the observation that we only need a model for , as the presence of the indicator on the right side of Equation (18) justifies the substitution of for . Thus, choosing a norm and taking the set of vector-valued functions with as our model for , we choose weights by solving the following optimization problem

| (19) | ||||

What remains is to choose this norm with the intention is small for all . If our model is correct in the sense that , then times the maximal approximation error bounds the approximation error in Equation (18).

As usual, there is a natural trade-off in choosing this model—if we take it to be too small, will be large or even infinite; on the other hand if we take it to be too large, we will be unable to find weights for which the approximation Equation (18) is highly accurate for all functions in the model. Choosing a norm with a unit ball that is a Donsker class, e.g. a Reproducing Kernel Hilbert Space (RKHS) norm like the one we use in our experiments, is a reasonable trade-off that is common in the literature on minimax and augmented minimax estimation of treatment effects [e.g., Hirshberg et al., 2019, Kallus, 2016]. When we do this, our estimator will be asymptotically efficient, i.e. asymptotically normal with negligible bias and optimal variance, if the hazard functions are in this class and we estimate them via empirical risk minimization with appropriate regularization. We discuss the computational aspects of this problem in Appendix A.2.

3.3 Asymptotic Efficiency

In this section, we will discuss the asymptotic behavior of our estimator, giving sufficient conditions for it to be asymptotically efficient. Throughout, we will assume is cross-fit, i.e., fit on an auxilliary sample independent of and distributed like our sample.

Our first condition is that it converges faster than fourth-root rate. This ensures the error of our first-order approximation Equation (11), quadratic in the error , is asymptotically negligible.

Assumption 3.1.

for all .

Our second condition is that its error is bounded in the norm used to define our model. This ensures that the bound on achieved via the optimization in Equation (19) implies a comparable bound on the error of the derivative approximation in Equation (18) for the relevant perturbation .

Assumption 3.2.

for all .

If our model is correctly specified in the sense that for , a sensibly tuned -penalized estimator of will have these two properties [see, e.g., Hirshberg and Wager, 2021, Remark 2].

Our third condition is that we have a sufficient degree of overlap.

Assumption 3.3.

This is a substantially weakened version of the often-assumed ‘strong overlap’ condition that is bounded away from zero, allowing this probability to approach zero for some as long as it is ‘typically’ elsewhere.

Our final condition is, for the most part, a constraint on the complexity of our model.

Assumption 3.4.

The unit ball is Donsker and uniformly bounded in the sense that . Furthermore, is Donsker for all .

The ‘furthermore’ clause here is implied by the first clause if strong overlap holds, as multiplication by the inverse probability weight will not problematically increase the complexity of the set of functions if those weights are bounded.

We are now ready to state our main theoretical result, which involves the efficient influence function for estimating ,

| (20) | ||||

Theorem 3.5.

Suppose is a hazard estimator fit on an auxiliary sample and Assumptions 3.1-3.4 are satisfied. Then the estimator described in Equation (16), using the Riesz Representer estimate obtained by solving Equation (19) for any fixed , is asymptotically linear with influence function . That is, it has the asymptotic approximation .

It follows, via the central limit theorem, that under these conditions is asymptotically normal with mean zero and variance . This justifies a standard approach to inference based on this asymptotic approximation, i.e., based on the t-statistic being approximately standard normal if is a consistent estimator of this variance .

As usual for estimators involving cross-fitting, working with multiple folds and averaging will yield an estimator with the same characterization without an auxiliary sample [e.g., Chernozhukov et al., 2018]. The resulting estimator is asymptotically linear on the whole sample and, having the efficient influence function , is asymptotically efficient.222There are many equivalent formal descriptions of what asymptotic efficiency means [e.g.,in Van der Vaart, 2000, Chapter 25]. In essence, it implies that no estimator can be reliably perform better in asymptotic terms, either in terms of criteria for point estimation like mean squared error or in terms of inferential behavior like the power of tests against local alternatives.

4 Related work

Outcome regression and inverse probability weighting estimators.

Based on Proposition 6, the outcome regression approach [Makuch, 1982] estimates is by directly estimating the conditional event survival given the treatment and covariates. Parametric and semi-parametric models such as the Cox proportional hazard (CoxPH) model [Cox, 1972, Andersen and Gill, 1982] in addition to deep learning techniques [Zhu et al., 2016, Katzman et al., 2018, Faraggi and Simon, 1995, Wang et al., 2021, Ching et al., 2018, Sun et al., 2020, Zhong et al., 2022, Nagpal et al., 2021, Meixide et al., 2022, Lv et al., 2022, Tibshirani, 1997, Biganzoli et al., 1998, Liestbl et al., 1994, Zhao and Feng, 2020, 2019, Hu et al., 2021, Luck et al., 2017, Yousefi et al., 2017, Lv et al., 2022] have been proposed to estimate . A popular alternative to outcome regression is the inverse probability of censoring and treatment weighting estimator (IPW) [Robins and Rotnitzky, 1992] defined as . In the past, model misspecification is a problem for both approaches. Modern machine learning methods can readily alleviate this, but they are data hungry, which motivates the use of semi-parametric efficient estimators [Chernozhukov et al., 2017].

Semi-parametric efficient estimators.

The recent wake of big data and machine learning attracts renewed attention for the field of semi-parametric efficient estimation, with numerous notable contributions focusing on causal inference, such as Díaz [2020], Chernozhukov et al. [2017, 2022a], Robins and Rotnitzky [1992], Tsiatis [2006]. One starts from the efficient influence function (EIF), which determines the fastest rate of any regular estimators [Van der Vaart, 2000], and construct efficient estimators e.g. the one-step estimator [Kennedy, 2022]. Similar EIFs to LABEL:eq:eif but with different parameterization are found in e.g. Díaz [2019], Cai and van der Laan [2020], Hubbard et al. [2000], Bai et al. [2013, 2017], Westling et al. [2023]. All semi-parametric efficient estimators are the same asymptotically [Van der Vaart, 2000], whose asymptotic variances are determined by the EIF, similar to Theorem 3.5; this key property shows that our estimator is asymptotically as good as other semi-parametric efficient ones. It does not, however, characterize an estimator’s finite-sample behavior.

Covariate balancing.

Numerous covariate balancing methods have been developed for estimating the effect of binary/continuous treatments on continuous outcomes including [Kallus and Santacatterina, 2021, 2022, Kallus, 2021, Hirshberg et al., 2019, Hirshberg and Wager, 2021, Zhao and Percival, 2017, Zhao et al., 2019, Wong and Chan, 2017, Visconti and Zubizarreta, 2018, Zubizarreta et al., 2014, Li et al., 2018, King et al., 2017, Josey et al., 2020, Yiu and Su, 2018, Hainmueller, 2012, Imai and Ratkovic, 2014, Zubizarreta, 2015, among others]. There is however limited body of research on covariate balance in the context of survival data [Xue et al., 2023, Abraich et al., 2022, Leete et al., 2019, Santacatterina, 2023, Yiu and Su, 2022, Kallus and Santacatterina, 2021]. Perhaps the most similar to our work and motivation is Xue et al. [2023], which is a covariate-balancing extension of Xie and Liu [2005]. Unfortunately, they assume independent censoring ( and are independent unconditionally of ) and their estimator is inefficient. None of the mentioned covariate-balancing methods in survival context provide results on asymptotic normality like ours, which allows for statistical inference, hypothesis testing, and the construction of confidence intervals.

5 Experiments

We now describe the experimental evidence concerning our estimator. As noted by, e.g., Curth et al. [2021], ground truth is almost never available in causal inference, so synthetic or semi-synthetic data (i.e. synthesized data based on real data) is the standard. We focus on the experiments that provide the most insight into the behavior of our estimator and its competitors; additional experiments and metrics along with implementation details are included in Appendix A.

5.1 Baselines, Metrics and datasets

We compare our balancing estimator (Balance) with the outcome regression estimator (OR) and the doubly-robust estimator (DR). We include 2 implementation of DR, one with clipping the weight’s denominator to be at least and one without.

We report the average survival effect at time t: . Our key error metrics are (1) the relative root-mean-squared-error (Relative RMSE), defined as the RSME of an estimator divided by the RMSE of the OR estimator, which we take to be the baseline, and (2) the Bias over Standard Error ratio (Bias/StdE). Let be our estimates over simulations and the ground truth, The RSME, Bias, and Standard Error are defined as , respectively.

We use the two datasets from Curth et al. [2021] with slight modifications; note that they are concerned with the heterogeneous treatment effect and thus incomparable in our context. For the first dataset Synthetic, we modified the assignment distribution to where is a sample of a 10-dimensional multivariate normal, so that controls the lack of overlap from propensity (the higher the less overlap as Sigmoid saturates quicker). The default value of is . We refer readers to the authors’ exposition of the different biases arising from censoring and assignment in this dataset. The second dataset Twins is a semi-synthetic dataset based on the Twins dataset [Louizos et al., 2017]. For both, we set . We use 200 and 500 observations for Synthetic and Twins, respectively, for each simulations of each experiment. We provide the full data generating process in A.1, A.3.

5.2 Discussion of results

Poor overlap can effect estimators in 2 ways (1) make naive outcome regression estimators biased and (2) lead to extreme numerical inverses in inverse-weight-based estimators. We illustrate this with 2 experiments for censoring bias/poor overlap in time and treatment bias/poor overlap in propensity.

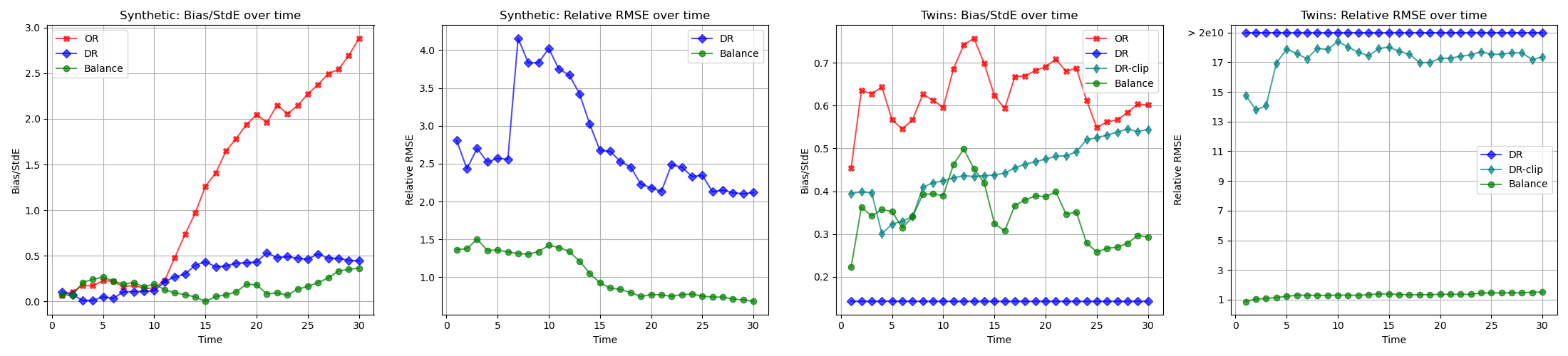

Metrics over time.

From Figure 1, in both datasets, Balance is both accurate and inferentially useful i.e. we can construct meaningful confidence interval, without suffering from the poor overlap at higher times. Balance has comparable RMSE to OR, where DR and DR-clip are much worse; in Twins, DR clearly runs into large numerical inverses, and DR-clip, despite its improvements, is still far from Balance. Yet, Bias/StdE plots show that OR has serious bias issue that is exacerbated by censoring bias at higher times. This bias is extremely problematic for inference: an Bias/StdE of at time in Synthetic means that a nominal 95% confidence interval contains the truth only 74.5% of the time. In contrast, this number is always above 92% for DR and Balance (), but of course, as seen from Relative RMSE plots, DR and DR-clip have very high standard error that push their RMSE up and thus highly inaccurate.

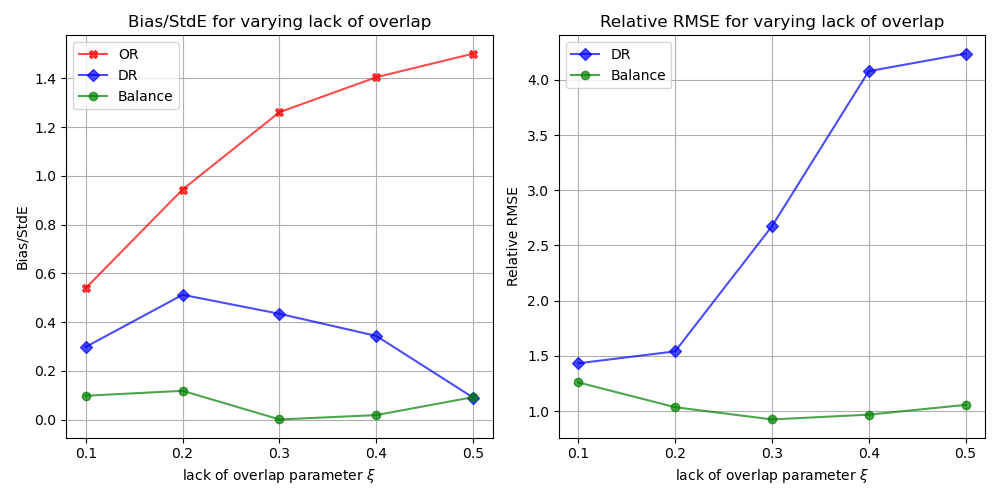

Metrics over varying propensity.

In Figure 2, we re-run Synthetic for and report the metrics at to see how poor overlap from extreme propensities influence our estimators. We observe similar behavior of estimators as seen in the first experiment. As overlap decreases, we see that both OR’s Bias/StdE and DR’s Relative RMSE increase. DR-clip was omitted in Synthetic plots as the estimates here are much less extreme and not truncated. Despite that, because of small sample sizes, we still see the same large errors in DR. In contrast, Balance is very stable across degrees of overlap, again proving its capability to fix DR’s accuracy problem while being less biased than OR, which was also shown in our semi-parametric efficiency theory.

References

- Abraich et al. [2022] Ayoub Abraich, Agathe Guilloux, and Blaise Hanczar. Survcaus: Representation balancing for survival causal inference. arXiv preprint arXiv:2203.15672, 2022.

- Andersen and Gill [1982] Per Kragh Andersen and Richard D Gill. Cox’s regression model for counting processes: a large sample study. Annals of Statistics, 10(4):1100–1120, 1982.

- Bai et al. [2013] Xiaofei Bai, Anastasios A Tsiatis, and Sean M O’Brien. Doubly-robust estimators of treatment-specific survival distributions in observational studies with stratified sampling. Biometrics, 69(4):830–839, 2013.

- Bai et al. [2017] Xiaofei Bai, Anastasios A Tsiatis, Wenbin Lu, and Rui Song. Optimal treatment regimes for survival endpoints using a locally-efficient doubly-robust estimator from a classification perspective. Lifetime data analysis, 23:585–604, 2017.

- Ben-Michael et al. [2021] Eli Ben-Michael, Avi Feller, David A Hirshberg, and José R Zubizarreta. The balancing act in causal inference. arXiv preprint arXiv:2110.14831, 2021.

- Biganzoli et al. [1998] Elia Biganzoli, Patrizia Boracchi, Luigi Mariani, and Ettore Marubini. Feed forward neural networks for the analysis of censored survival data: a partial logistic regression approach. Statistics in medicine, 17(10):1169–1186, 1998.

- Cai and van der Laan [2020] Weixin Cai and Mark J van der Laan. One-step targeted maximum likelihood estimation for time-to-event outcomes. Biometrics, 76(3):722–733, 2020.

- Chernozhukov et al. [2017] Victor Chernozhukov, Denis Chetverikov, Mert Demirer, Esther Duflo, Christian Hansen, and Whitney Newey. Double/debiased/neyman machine learning of treatment effects. American Economic Review, 107(5):261–65, 2017.

- Chernozhukov et al. [2018] Victor Chernozhukov, Denis Chetverikov, Mert Demirer, Esther Duflo, Christian Hansen, Whitney Newey, and James Robins. Double/debiased machine learning for treatment and structural parameters, 2018.

- Chernozhukov et al. [2022a] Victor Chernozhukov, Whitney Newey, Victor M Quintas-Martinez, and Vasilis Syrgkanis. Riesznet and forestriesz: Automatic debiased machine learning with neural nets and random forests. In International Conference on Machine Learning, pages 3901–3914. PMLR, 2022a.

- Chernozhukov et al. [2022b] Victor Chernozhukov, Whitney K Newey, and Rahul Singh. Debiased machine learning of global and local parameters using regularized riesz representers. The Econometrics Journal, 25(3):576–601, 2022b.

- Ching et al. [2018] Travers Ching, Xun Zhu, and Lana X Garmire. Cox-nnet: an artificial neural network method for prognosis prediction of high-throughput omics data. PLoS Computational Biology, 14(4):e1006076, 2018.

- Cox [1972] David R Cox. Regression models and life-tables. Journal of the Royal Statistical Society: Series B (Methodological), 34(2):187–202, 1972.

- Crowder [2012] Martin J Crowder. Multivariate survival analysis and competing risks. CRC Press, 2012.

- Curth et al. [2021] Alicia Curth, Changhee Lee, and Mihaela van der Schaar. Survite: learning heterogeneous treatment effects from time-to-event data. Advances in Neural Information Processing Systems, 34:26740–26753, 2021.

- Díaz [2019] Iván Díaz. Statistical inference for data-adaptive doubly robust estimators with survival outcomes. Statistics in medicine, 38(15):2735–2748, 2019.

- Díaz [2020] Iván Díaz. Machine learning in the estimation of causal effects: targeted minimum loss-based estimation and double/debiased machine learning. Biostatistics, 21(2):353–358, 2020.

- Faraggi and Simon [1995] David Faraggi and Richard Simon. A neural network model for survival data. Statistics in medicine, 14(1):73–82, 1995.

- Hainmueller [2012] Jens Hainmueller. Entropy balancing for causal effects: A multivariate reweighting method to produce balanced samples in observational studies. Political Analysis, 20(1):25–46, 2012.

- Hirshberg and Wager [2021] David A Hirshberg and Stefan Wager. Augmented minimax linear estimation. The Annals of Statistics, 49(6):3206–3227, 2021.

- Hirshberg et al. [2019] David A Hirshberg, Arian Maleki, and Jose Zubizarreta. Minimax linear estimation of the retargeted mean. arXiv preprint arXiv:1901.10296, 2019.

- Hu et al. [2021] Shi Hu, Egill Fridgeirsson, Guido van Wingen, and Max Welling. Transformer-based deep survival analysis. In Survival Prediction-Algorithms, Challenges and Applications, pages 132–148. PMLR, 2021.

- Hubbard et al. [2000] Alan E Hubbard, Mark J Van Der Laan, and James M Robins. Nonparametric locally efficient estimation of the treatment specific survival distribution with right censored data and covariates in observational studies. In Statistical Models in Epidemiology, the Environment, and Clinical Trials, pages 135–177. Springer, 2000.

- Imai and Ratkovic [2014] Kosuke Imai and Marc Ratkovic. Covariate balancing propensity score. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 76(1):243–263, 2014.

- Imbens and Rubin [2015] Guido W Imbens and Donald B Rubin. Causal inference in statistics, social, and biomedical sciences. Cambridge University Press, 2015.

- Johansson et al. [2022] Fredrik D Johansson, Uri Shalit, Nathan Kallus, and David Sontag. Generalization bounds and representation learning for estimation of potential outcomes and causal effects. The Journal of Machine Learning Research, 23(1):7489–7538, 2022.

- Josey et al. [2020] Kevin P Josey, Elizabeth Juarez-Colunga, Fan Yang, and Debashis Ghosh. A framework for covariate balance using bregman distances. Scandinavian Journal of Statistics, 2020.

- Kallus [2016] Nathan Kallus. Generalized optimal matching methods for causal inference. arXiv preprint arXiv:1612.08321, 2016.

- Kallus [2021] Nathan Kallus. More efficient policy learning via optimal retargeting. Journal of the American Statistical Association, 116(534):646–658, 2021.

- Kallus and Santacatterina [2021] Nathan Kallus and Michele Santacatterina. Optimal balancing of time-dependent confounders for marginal structural models. Journal of Causal Inference, 9(1):345–369, 2021.

- Kallus and Santacatterina [2022] Nathan Kallus and Michele Santacatterina. Optimal weighting for estimating generalized average treatment effects. Journal of Causal Inference, 10(1):123–140, 2022.

- Kang et al. [2007] Joseph DY Kang, Joseph L Schafer, et al. Demystifying double robustness: A comparison of alternative strategies for estimating a population mean from incomplete data. Statistical science, 22(4):523–539, 2007.

- Katzman et al. [2018] Jared L Katzman, Uri Shaham, Alexander Cloninger, Jonathan Bates, Tingting Jiang, and Yuval Kluger. DeepSurv: Personalized treatment recommender system using a Cox proportional hazards deep neural network. BMC medical research methodology, 18(1):24, 2018.

- Kennedy [2022] Edward H Kennedy. Semiparametric doubly robust targeted double machine learning: a review. arXiv preprint arXiv:2203.06469, 2022.

- King et al. [2017] Gary King, Christopher Lucas, and Richard A Nielsen. The balance-sample size frontier in matching methods for causal inference. American Journal of Political Science, 61(2):473–489, 2017.

- Kleinbaum and Klein [2012] David G. Kleinbaum and Mitchel Klein. Parametric Survival Models, pages 289–361. Springer New York, 2012.

- Kvamme and Borgan [2019] Håvard Kvamme and Ørnulf Borgan. Continuous and discrete-time survival prediction with neural networks. arXiv preprint arXiv:1910.06724, 2019.

- Leete et al. [2019] Owen E Leete, Nathan Kallus, Michael G Hudgens, Sonia Napravnik, and Michael R Kosorok. Balanced policy evaluation and learning for right censored data. arXiv preprint arXiv:1911.05728, 2019.

- Li et al. [2018] Fan Li, Kari Lock Morgan, and Alan M Zaslavsky. Balancing covariates via propensity score weighting. Journal of the American Statistical Association, 113(521):390–400, 2018.

- Liestbl et al. [1994] Knut Liestbl, Per Kragh Andersen, and Ulrich Andersen. Survival analysis and neural nets. Statistics in medicine, 13(12):1189–1200, 1994.

- Louizos et al. [2017] Christos Louizos, Uri Shalit, Joris M Mooij, David Sontag, Richard Zemel, and Max Welling. Causal effect inference with deep latent-variable models. Advances in neural information processing systems, 30, 2017.

- Luck et al. [2017] Margaux Luck, Tristan Sylvain, Héloïse Cardinal, Andrea Lodi, and Yoshua Bengio. Deep learning for patient-specific kidney graft survival analysis. arXiv preprint arXiv:1705.10245, 2017.

- Lv et al. [2022] Zhilong Lv, Yuexiao Lin, Rui Yan, Ying Wang, and Fa Zhang. TransSurv: Transformer-based survival analysis model integrating histopathological images and genomic Data for colorectal cancer. IEEE/ACM Transactions on Computational Biology and Bioinformatics, pages 1–10, 2022. doi: 10.1109/TCBB.2022.3199244.

- Makuch [1982] Robert W Makuch. Adjusted survival curve estimation using covariates. Journal of chronic diseases, 35(6):437–443, 1982.

- Mansourvar et al. [2016] Zahra Mansourvar, Torben Martinussen, and Thomas H Scheike. An additive–multiplicative restricted mean residual life model. Scandinavian Journal of Statistics, 43(2):487–504, 2016.

- Mao et al. [2018] Huzhang Mao, Liang Li, Wei Yang, and Yu Shen. On the propensity score weighting analysis with survival outcome: Estimands, estimation, and inference. Statistics in medicine, 37(26):3745–3763, 2018.

- Martinussen [2022] Torben Martinussen. Causality and the cox regression model. Annual Review of Statistics and Its Application, 9:249–259, 2022.

- Meixide et al. [2022] Carlos García Meixide, Marcos Matabuena, and Michael R. Kosorok. Neural interval-censored cox regression with feature selection. https://doi.org/10.48550/arXiv.2206.06885, 2022. Accessed 2022-09-20.

- Nagpal et al. [2021] Chirag Nagpal, Steve Yadlowsky, Negar Rostamzadeh, and Katherine Heller. Deep Cox mixtures for survival regression. In Ken Jung, Serena Yeung, Mark Sendak, Michael Sjoding, and Rajesh Ranganath, editors, Proceedings of the 6th Machine Learning for Healthcare Conference, volume 149 of Proceedings of Machine Learning Research, pages 674–708, 2021.

- Neyman [1923] Jerzy Neyman. On the application of probability theory to agricultural experiments. essay on principles. Ann. Agricultural Sciences, pages 1–51, 1923.

- Robins and Rotnitzky [1992] James M Robins and Andrea Rotnitzky. Recovery of information and adjustment for dependent censoring using surrogate markers. AIDS epidemiology: methodological issues, pages 297–331, 1992.

- Rubin [1974] Donald B Rubin. Estimating causal effects of treatments in randomized and nonrandomized studies. Journal of educational Psychology, 66(5):688, 1974.

- Santacatterina [2023] Michele Santacatterina. Robust weights that optimally balance confounders for estimating marginal hazard ratios. Statistical Methods in Medical Research, 2023.

- Sun et al. [2020] Tao Sun, Yue Wei, Wei Chen, and Ying Ding. Genome-wide association study-based deep learning for survival prediction. Statistics in Medicine, 39(30):4605–4620, 2020.

- Tibshirani [1997] Robert Tibshirani. The lasso method for variable selection in the Cox model. Statistics in Medicine, 16(4):385–395, 1997.

- Tsiatis [2006] Anastasios A Tsiatis. Semiparametric theory and missing data. 2006.

- Van der Vaart [2000] Aad W Van der Vaart. Asymptotic statistics, volume 3. Cambridge university press, 2000.

- Vansteelandt et al. [2022] Stijn Vansteelandt, Oliver Dukes, Kelly Van Lancker, and Torben Martinussen. Assumption-lean cox regression. Journal of the American Statistical Association, pages 1–10, 2022.

- Visconti and Zubizarreta [2018] Giancarlo Visconti and José R Zubizarreta. Handling limited overlap in observational studies with cardinality matching. Observational Studies, 4:217–249, 2018.

- Wang et al. [2021] Di Wang, Zheng Jing, Kevin He, and Lana X Garmire. Cox-nnet v2.0: improved neural-network-based survival prediction extended to large-scale EMR data. Bioinformatics, 37(17):2772–2774, 2021.

- Westling et al. [2023] Ted Westling, Alex Luedtke, Peter B Gilbert, and Marco Carone. Inference for treatment-specific survival curves using machine learning. Journal of the American Statistical Association, (just-accepted):1–26, 2023.

- Wong and Chan [2017] Raymond KW Wong and Kwun Chuen Gary Chan. Kernel-based covariate functional balancing for observational studies. Biometrika, 105(1):199–213, 2017.

- Xie and Liu [2005] Jun Xie and Chaofeng Liu. Adjusted kaplan–meier estimator and log-rank test with inverse probability of treatment weighting for survival data. Statistics in medicine, 24(20):3089–3110, 2005.

- Xue et al. [2023] Wu Xue, Xiaoke Zhang, Kwun Chuen Gary Chan, and Raymond KW Wong. Rkhs-based covariate balancing for survival causal effect estimation. Lifetime Data Analysis, pages 1–25, 2023.

- Yiu and Su [2018] Sean Yiu and Li Su. Covariate association eliminating weights: a unified weighting framework for causal effect estimation. Biometrika, 105(3):709–722, 2018.

- Yiu and Su [2022] Sean Yiu and Li Su. Joint calibrated estimation of inverse probability of treatment and censoring weights for marginal structural models. Biometrics, 78(1):115–127, 2022.

- Yoon et al. [2018] Jinsung Yoon, James Jordon, and Mihaela Van Der Schaar. Ganite: Estimation of individualized treatment effects using generative adversarial nets. In International Conference on Learning Representations, 2018.

- Yousefi et al. [2017] Safoora Yousefi, Fatemeh Amrollahi, Mohamed Amgad, Chengliang Dong, Joshua E Lewis, Congzheng Song, David A Gutman, Sameer H Halani, Jose Enrique Velazquez Vega, Daniel J Brat, et al. Predicting clinical outcomes from large scale cancer genomic profiles with deep survival models. Scientific reports, 7(1):11707, 2017.

- Zhao and Feng [2019] Lili Zhao and Dai Feng. Dnnsurv: Deep neural networks for survival analysis using pseudo values. arXiv preprint arXiv:1908.02337, 2019.

- Zhao and Feng [2020] Lili Zhao and Dai Feng. Deep neural networks for survival analysis using pseudo values. IEEE journal of biomedical and health informatics, 24(11):3308–3314, 2020.

- Zhao and Percival [2017] Qingyuan Zhao and Daniel Percival. Entropy balancing is doubly robust. Journal of Causal Inference, 5(1), 2017.

- Zhao et al. [2019] Qingyuan Zhao et al. Covariate balancing propensity score by tailored loss functions. The Annals of Statistics, 47(2):965–993, 2019.

- Zhong et al. [2022] Qixian Zhong, Jonas Mueller, and Jane-Ling Wang. Deep learning for the partially linear Cox model. Annals of Statistics, 50(3):1348–1375, 2022.

- Zhu et al. [2016] Xinliang Zhu, Jiawen Yao, and Junzhou Huang. Deep convolutional neural network for survival analysis with pathological images. In 2016 IEEE International Conference on Bioinformatics and Biomedicine (BIBM), pages 544–547. IEEE, 2016.

- Zubizarreta [2015] José R Zubizarreta. Stable weights that balance covariates for estimation with incomplete outcome data. Journal of the American Statistical Association, 110(511):910–922, 2015.

- Zubizarreta et al. [2014] José R Zubizarreta, Ricardo D Paredes, Paul R Rosenbaum, et al. Matching for balance, pairing for heterogeneity in an observational study of the effectiveness of for-profit and not-for-profit high schools in chile. The Annals of Applied Statistics, 8(1):204–231, 2014.

Appendix A Description of implementation, datasets and additional results

A.1 Implementation

Throughout, we use the RBF kernel with length scale 10. For all methods considered, we need to train a hazard estimator for time-to-event (the survival function can then be constructed from the hazard). We use the discrete logistic-hazard model [Kvamme and Borgan, 2019] with the mean negative log-likelihood loss parameterized by the hazard function as:

where . This loss breaks down into independent binary cross-entropy losses for each and :

Therefore, we can fit independent hazard models using kernel logistic regression.

Covariate-balancing

The hazard estimate must be fit on a separate split of the data, therefore we divide the data into 2 folds. For each fold, we fit the hazard estimator on the other fold, then estimate the Riesz representer using the just obtained hazard estimate on the canonical fold. The result is one causal parameter estimate of the canonical fold, by solving the optimization problem 19. This gives us the time-to-event hazard and the riesz estimates which we use to estimate the causal parameter of this canonical fold, using Equation (16). Lastly, we obtain the final estimate by averaging the estimates across 2 folds.

Double robust estimation

We need to train a hazard estimator for time-to-censoring, which can be done similarly to the time-to-event case (but with events flipped), and a propensity estimator, for which we use a simple linear logistic regression (correctly specified in both datasets). We use cross-fitting [Chernozhukov et al., 2018], where we randomly divide the dataset into K folds (we used K=5 in our experiments). For each fold, we fit the time-to-event/censoring hazard and propensity estimators on the remaining folds and obtain their estimates on the canonical fold. Using the time-to-censoring and the propensity estimates we obtain the riesz estimate using Equation (LABEL:eq:riesz-rep-explicit). Lastly we obtain the causal parameter estimate using Equation (16).

A.2 The weight optimization problem

We start by observing that we do not need to solve the optimization Equation (19) all at once. It decomposes into separate optimizations over timestep-specific weights specific to a single timestep.

Lemma A.1.

If the weights solve Equation (19), the timestep--specific subset satisfy the following one.

| (21) | ||||

In the case that is the norm of an RKHS, we can use the representer theorem to further simplify this optimization. The representer theorem implies that it is sufficient to maximize over that can be written as where is our space’s kernel. Making this substitution, we get the following characterization in terms of the kernel matrix satisfying .

where are vectors in and , and is the element-wise product. The maximum is achieved at and is:

Replacing into the outer minimization problem:

This quadratic-programming problem can be solved efficiently by most convex solvers, in particular we chose cvxpy. Now we show why we can decompose the original problem this way.

Proof of theorem A.1.

Let be defined as follows.

In terms of this function,

The last equality is due to Cauchy-Schwarz inequality, with equality achievable by setting proportional to . If we substitute this expression into our original optimization Equation (19), we get:

as each term in the sum over is a function of an individual , we can therefore solve a separate minimization sub-problem for each :

proving our claim. ∎

A.3 Datasets

We use both datasets from Curth et al. [2021] with modifications to the assignment distribution and censoring distribution to exacerbate the overlap problem.

Synthetic Data.

where is a sigmoid function, is an identity matrix of size 10, is a matrix of all ones, and is the sum of all covariates of . All time after is censored so we set .

Semi-synthetic Data.

We preprocess the Twins dataset similar to Curth et al. [2021], Yoon et al. [2018]. The time-to-event outcome is the time-to-mortality of each twin. Each observation has 30 covariates and we do not encode the categorical features. We are interested in the survival in the first 30 days, therefore . We also create artificial treatment and censoring:

treatment decides which twin outcome is observed. Here being continuous does not affect the discrete event time. We standardize covariate for training and only after creating the datasets.

A.4 Additional Result for Synthetic Data.

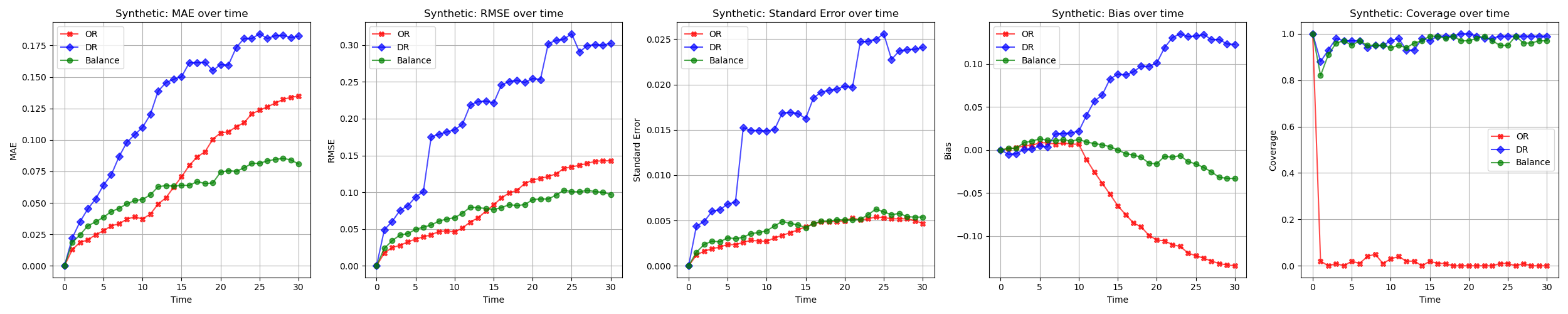

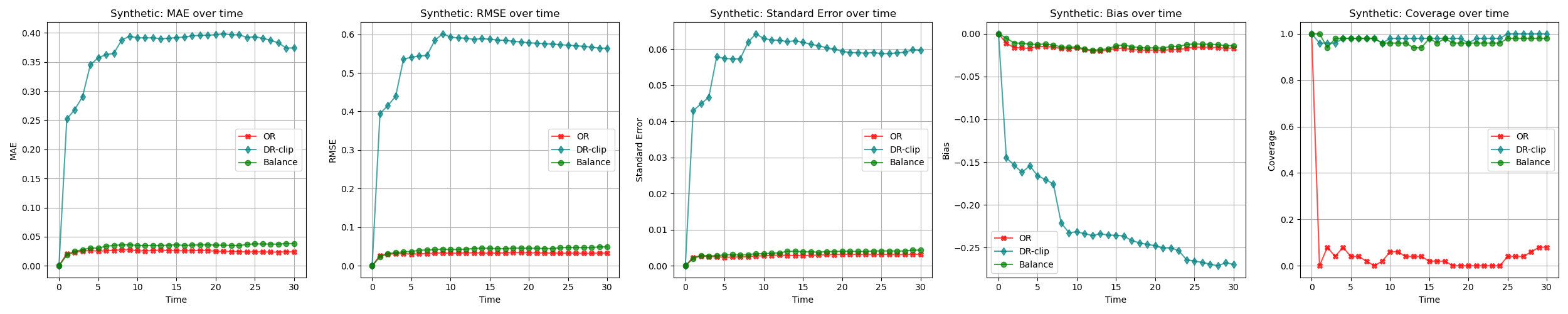

We add 5 more metrics: MAE, MSE, Bias, Standard Error and Coverage for both datasets in figure 3 and 4. Overall, we see that Balance is competitive in all metrics. More specifically, it consistently has the lowest bias, its MAE and MSE are competitive to OR while not suffering from poor overlap at higher times in Synthetic. It also has consistently high coverage similar to DR, but does not suffer from high standard errors and therefore low accuracy. Both DR and OR suffer from poor overlap, but DR is the most susceptible, which shows that all the benefit of semi-parametric efficiency is lost to extreme inversions.

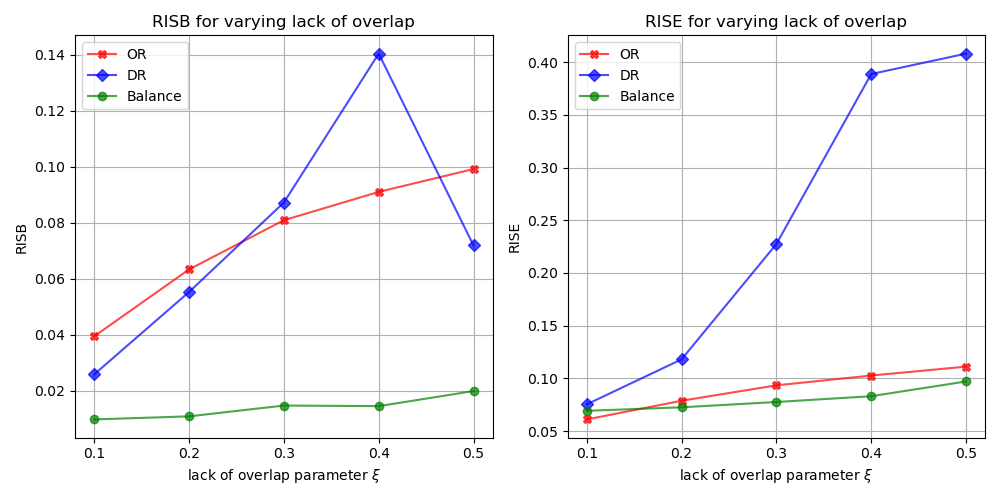

In our experiment on varying degree of overlap in Synthetic, instead of a fixed time , we use 2 more metrics that summarize all time points: the Root Mean Squared Bias (RISB) and Root Mean Squared Error (RISE) [Xue et al., 2023], defined as and respectively. Once again, we see that Balance is best among all methods across all degree of overlap (see figure 5).

Appendix B Identification and Proof of Supporting Lemmas

Proof of Lemma 2.1.

and ∎

Identification

To identify the counterfactual survival function using the observable data, similar to Hubbard et al. [2000], Bai et al. [2013, 2017], Westling et al. [2023], Díaz [2019], Cai and van der Laan [2020], we require the following testable and untestable assumptions:

-

1.

(A1) for each ().

-

2.

(A2) for each .

-

3.

(A3) almost surely.

-

4.

(A4) positivity (censoring),

in addition to consistency (A5) and non-interference (A6) Imbens and Rubin [2015]. (A1), also referred to as no unmeasured confounders, selection on observables, exogeneity, and conditional independence, asserts that the potential outcomes/potential censoring times, and treatment assignment are independent given confounders. This assumption implies that all relevant information regarding treatment assignment and follow-up censoring times is captured in the available data. (A2) states that the potential follow-up and censoring times are independent given the treatment and confounders. (A3) and (A4) assert that the probability of receiving or not receiving treatment, as well as the probability of censoring, given confounders, is greater than zero. Finally, (A6) and (A7) state that the observed treatment corresponds to the actual treatment received, ensuring consistency between the observed and true treatment assignments.

Appendix C Proof of theorem 3.5

We first recall and introduce additional notations for this section. Denote the conditioning structure of the hazard function . As and are functions of , we use and as functions of to denote the estimator counterparts. We drop the superscripts of since they are not relevant in the proof. We use for the parameter of interest , for the sample analog . As and are one-to-one, would be . We use to denote our estimator, i.e.,

| (22) |

Let’s start by recalling what we are proving.

| (23) |

To do this, we will work with this error decomposition.

| (24) | ||||

We prove Equation (23) in three steps. Throughout, we will work conditionally on the auxilliary sample used to estimate , so we can act as if it is a deterministic function. This will imply that our claim holds where refers to probability conditional on the auxilliary sample and therefore also that it holds where refers to unconditional probability.

Step 1.

The third term in this decomposition, the error of our linearization of around , is . Lemma C.2 below shows that this is implied by our assumption that converges at faster-than-fourth-root rate.

Step 2.

Lemma C.4 below concludes that the second term in our decomposition has the following asymptotic approximation.

Step 3.

The sum of the first term in our decomposition and the non-negligible part of the second is

| (25) | ||||

To complete our proof of the claim Equation (23), we show

Because this is an average of independent and identically distributed terms with mean zero, its mean square is times the variance of an individual term; thus, all we have to do is show that the variance of goes to zero. In Lemma C.5 below, we show that this is a consequence of the convergence of .

We conclude by stating and proving our lemmas.

Lemma C.1.

For all ,

Furthermore,

Lemma C.2.

Let and be two hazards and and the associated survival functions. Then the functional evaluated at has the following expansion:

| (26) | ||||

Remark C.3.

Lemma C.4.

Lemma C.5.

Suppose our overlap assumption, Assumption 3.3, is satisfied. Then the influence function is mean-square continuous as a function of , i.e.,

satisfies if and are two hazards, with corresponding survival curves and and ratios and , that converge in the sense that .

C.1 Lemma Proofs

Proof of Lemma C.1.

For all

| (27) | ||||

therefore

since . ∎

Proof of Lemma C.2.

We expand each term of the decomposition in Lemma C.1 around the approximation ,

therefore

| (28) | ||||

Proof of Lemma C.4.

We will establish this result timestep-by-timestep. That is, we will show that for all ,

| (29) | ||||

It’s sufficient to show that this holds for a version in which the expectation is replaced by a sample average, as the variance of the difference is . This follows from the consistency of and the boundedness of .333We can treat as deterministic here, avoiding empirical process arguments, because is cross-fit.

To do this, we will start with the result of Lemma A.1, which characterizes the weights as the solution to an optimization problem equivalent to the following one.

| (30) | ||||

This differs from the characterization from Lemma A.1 in two ways. First, we do not restrict the parametric form of the weights to be . Second, we write the class of functions we’re maximizing over as functions of instead of functions of alone. However, as argued in Hirshberg et al. [2019, Proposition 7], the solution must satisfy unless and , as to do otherwise would increase the objective function. Thus, we may impose this restriction on and therefore reduce our maximization to one over without changing the solution . Reparameterizing in terms of yields the equivalent problem described in Lemma A.1. The benefit of the formulation we use here is that it’s recognizable as an instance of the problem used to estimate weights in Hirshberg and Wager [2021].

Under our assumptions, Hirshberg and Wager [2021, Theorem 1] establishes this claim, i.e. the sample-average-replacing-expectation version of Equation (29). Almost. It does so for a fixed function ; because ours varies with sample size we would need a triangular-array version. However, such a version follows from the proof used to derive Hirshberg and Wager [2021, Theorem 1] from a finite sample result [Hirshberg and Wager, 2021, Theorem 2]. In particular, the finite sample result shows that the approximation we’ve claimed holds with error that’s bounded in terms of certain Rademacher complexity fixed points, and the proof of Hirshberg and Wager [2021, Theorem 1] shows that the Donsker conditions assumed there ensure that these bounds are . Following the same argument, the Donsker conditions we’ve assumed here, in conjunction with the uniform-in-n boundedness of and the contraction principle for Rademacher complexity, imply the same. ∎

Proof of Lemma C.5.

For simplicity, we drop the when writing functions , and .

We first consider the term . From Lemma C.1, we can write

It is obvious that . Applying Holder’s inequality and the given condition , we can imply that .

Since and are continuous functions of and , respectively, and as shown above, . Then for the last term of the , we can continue applying Holder’s inequality and further conclude that . ∎

C.2 A Sketch of Theorem 3.5

Our proof of Theorem 3.5 uses results from Hirshberg and Wager [2021] to do some heavy lifting. For the sake of self-containedness, we will sketch the main ideas of the argument we’d use to prove it from scratch. We use a more detailed decomposition of the error as follows:

| (31) | ||||

We sketch the analysis of each of the 4 terms above:

-

1.

The first term converges to the influence function of the estimator because and are convergent. That the latter converges to the population Riesz representer is a consequence of the analysis of the imbalance in the 2nd term below.

- 2.

-

3.

The 3rd term is the difference of the sample-average derivative and its expectation, can be shown to be because each term of the mean has mean 0 and variance as consequence of the convergence of .

-

4.

The 4th term is the 2nd-order remainder as before and is .

Overall, we see again that .