2021

These authors contributed equally to this work.

These authors contributed equally to this work.

[2]\fnmShashi \surJain \equalcontThese authors contributed equally to this work.

1]\orgdivDepartment of Mathematics, \orgnameIndian Institute of Science, \orgaddress\cityBangalore, \postcode560012, \countryIndia

2]\orgdivDepartment of Management Studies, \orgnameIndian Institute of Science, \orgaddress\cityBangalore, \postcode560012, \countryIndia

Multi-period static hedging of European options

Abstract

We consider the hedging of European options when the price of the underlying asset follows a single-factor Markovian framework. By working in such a setting, Carr and Wu carr2014static derived a spanning relation between a given option and a continuum of shorter-term options written on the same asset. In this paper, we have extended their approach to simultaneously include options over multiple short maturities. We then show a practical implementation of this with a finite set of shorter-term options to determine the hedging error using a Gaussian Quadrature method. We perform a wide range of experiments for both the Black-Scholes and Merton Jump Diffusion models, illustrating the comparative performance of the two methods.

keywords:

Multi-period static hedging, short-term options, Carr Wu, Gauss Hermite, Gaussian Quadrature, Gauss Laguerre, European options, Black Scholes, Merton Jump Diffusion, Markovian models.1 Introduction

Financial crises over the past few decades have highlighted the growing importance of static and semi-static hedging strategies. More recently, the widespread COVID-19 pandemic emphasized the well-known phenomenon that every major financial crisis is always accompanied by numerous mini-crises. These crises cause asset prices to behave in an unpredictable fashion, triggering circuit breakers, trading halts, and increased risk aversion among investors. All of these factors contribute to the drying up of liquidity in the market, making the application of dynamic hedging strategies difficult and often faulty. Consequently, static and semi-static hedging strategies offer an attractive alternative.

One of the pioneering works in this regard was by Breeden and Litzenberger breeden1978prices . They proved that for a given portfolio, the price of a claim received at a future date provided the portfolio’s value is between two specified levels on that date, can be obtained explicitly from a second partial derivative of its call option pricing function. This was further elaborated by Green and Jarrow () green1987spanning and Nachman nachman1988spanning , who show that a path-independent payoff can be hedged using a portfolio of standard options maturing with the claim. In spite of the strategy being robust to model misspecification, the class of claims that this static hedging strategy can hedge is fairly narrow.

In their paper, Carr and Chou () carr1997hedging propose static replications of barrier options using vanilla options under the Black and Scholes () black1973valuation environment. The necessity of continuous trading of the underlying is replaced by the necessity of trading options with a continuum of different strikes and is restricted to the Black Scholes () model.

In the recent past, Carr and Wu () carr2014static extend the strategy to obtain an exact static hedging relation to hedge a long-term option with a continuum of short-term options, all sharing a common maturity. This theoretical result, when discretized using their approach, to include finitely many shorter-term options, results in strike points that are too widespread. The static hedging approach in Carr and Wu carr2014static is restricted to a single maturity for the shorter-term options and they recommend the short-term maturity to be close to the target option’s maturity. The practical problem occurs when the target maturity is considerably long, resulting in the short-term options with maturity closest to the target option being mostly illiquid. Hence, it is always desirable to include multiple short maturities in the hedging portfolio to provide more liquidity, while retaining the efficiency by including maturities closest to the target option.

In this paper, we extend the theoretical spanning relation obtained in Carr and Wu () carr2014static . We address the problem of static hedging of European options with maturity, . The hedging portfolio constitutes short-term options, all written over the same underlying asset as for the target option and with multiple choices for the shorter maturities. We obtain an exact theoretical spanning relation for the hedge portfolio in this case. This relation is then discretized using a Gaussian Quadrature approach to include short-term options with bounded strike ranges. Further, the portfolio is not just restricted to short-maturity call options but can include liquid put options.111This work is also supported by the DST FIST program- 2021[TPN - 700661]

To summarise, the main contributions of our paper are as follows:

-

1.

Extend the exact theoretical spanning relation in carr2014static to include options not restricted to a common short maturity.

-

2.

Discretize the spanning relation using a Gaussian Quadrature () algorithm, for practical application of our method to construct hedge portfolios with a finite number of options, over multiple short maturities.

-

3.

Perform a comparative analysis of the performance of our method with the one in carr2014static , in each of the cases when the number of quadrature points, the short maturities, and the available liquid strike intervals are varied for the model.

-

4.

Study the performance of our method and the method in carr2014static , in comparison to a Delta Hedging algorithm, throughout the duration of the hedge, until the expiry of the short maturity options, using simulated stock paths, in the model.

-

5.

Perform a comparative analysis of the performance of our method with the one in carr2014static , in each of the cases when the number of quadrature points, the short maturities, the available liquid strike intervals, and the parameters governing the distribution of the stock price jumps are varied for the Merton Jump Diffusion () model.

In related literature, Bakshi, Cao, and Chen () bakshi1997empirical , Bakshi and Kapadia () bakshi2003delta , and Dumas, Fleming and Whaley () dumas1998implied use hedging performance to test different option pricing models. Bakshi and Madan () bakshi2000spanning propose a general option-valuation strategy based on effective spanning using basic characteristic securities. Renault and Touzi () renault1996option consider optimal hedging under a stochastic volatility model. Hutchinson, Lo and Poggio () hutchinson1994nonparametric propose to estimate the hedging ratio empirically using a nonparametric approach based on historical data. He et al.()he2006calibration and Kennedy, Forsyth, and Vetzal () kennedy2009dynamic set up a dynamic programming problem in minimizing the hedging errors under jump-diffusion frameworks and in the presence of transaction cost. Their method applied to only jump-diffusion frameworks and provided better performance than the standard dynamic hedging approach in the presence of transaction costs. Branger and Mahayni () branger2006tractable branger2011tractable propose robust dynamic hedges in pure diffusion models when the hedger knows only the range of the volatility levels but not the exact volatility dynamics.

For static payoff matching strategies, Balder and Mahayani () balder2006robust consider discretization strategies for the theoretical spanning relation in Carr and Wu () carr2014static when the strikes of the hedging options are pre-specified and the underlying price dynamics are unknown to the hedger. Wu and Zhu () wu2016simple propose an option hedging strategy that is based on the approximate matching of contract characteristics. The portfolio constructed using their approach required expanding along contract characteristics instead of focusing on risk. Hedging instruments close in characteristics to the target contract must be chosen to minimize the expansion errors on characteristic differences. The portfolio includes a total of three short-maturity options over two short maturities and with the added assumptions that at all strikes and expiries, the calendar spreads and butterfly spreads are strictly positive, such that the Dupire () dupire1994pricing local volatility is well-defined and strictly positive.

Among the most recent works, Bossu et.al () bossu2021functional propose a functional analysis approach using spectral decomposition techniques to show that exact payoff replication may be achieved with a discrete portfolio of special options. They discuss applications for fast pricing of vanilla options that may be suitable for large option books or high-frequency option trading, and for model pricing when the characteristic function of the underlying asset price is known. In their paper, Lokeshwar et.al () lokeshwar2022explainable develop neural networks for a regress-later-based Monte Carlo approach for pricing multi-asset discretely-monitored contingent claims. Their work demonstrates that any discretely monitored contingent claim- possibly high-dimensional and path-dependent— under Markovian and no-arbitrage assumptions, can be semi-statically hedged using a portfolio of short-maturity options.

The layout of the paper is as follows: Section 2 provides a detailed explanation of the exact spanning relation as well as the discretization scheme given by carr2014static . In Section 3 we propose an exact multi-period static hedging relation to hedge a European call/put option using a continuum of options with finitely many different short maturities and discretize the approach by applying a method of Gaussian Quadrature to generate the optimal strikes and associated weights of the short-maturity options constituting the hedge portfolio. In Section 4 we perform a series of numerical experiments for the and models to provide a comparative analysis of the efficiency of our approach with carr2014static . Section 5 gives the conclusion and certain mathematical derivations for the theoretical results have been provided in Appendix.

2 Hedging using a continuum of short maturity options

We restrict our attention to a continuous-time one-factor Markovian setting and show how one can approximately hedge the risk of a European option by holding a finite number of shorter-term European options, all having a common maturity, as proved in carr2014static . We begin by stating the assumptions and notations that we shall use throughout this paper, followed by some of the theoretical results that one can apply to approximate the static hedge using a finite number of shorter-term options. The results that are presented here can be readily extended to the case of a European put option via put-call parity.

2.1 Assumptions and Notations

We assume the markets to be frictionless and have no-arbitrage. We use the standard notation of to denote the spot price of an underlying asset( for example, a stock or stock index), at time . To be consistent with the assumptions as well as notations in carr2014static , we further assume that the owners of this asset enjoy limited liability, which implies that at all times and the continuously compounded risk-free rate is a constant, and a constant dividend yield, . Our analysis is also restricted to the class of models for which the risk-neutral evolution of the stock price is Markov in the stock price and the calendar time .

We shall use to denote the time- value of a call option with strike price and expiry . The probability density function of the asset price under the risk-neutral measure , evaluated at the future price level and the future time , conditional on the stock price starting at level at an earlier time , is denoted by .

One then obtains, as shown by Breeden and Litzenberger () breeden1978prices , that the risk-neutral density is related to the second strike derivative of the call pricing function as follows,

| (1) |

This yields the fundamental result derived in carr2014static .

Theorem 2.1.

Under no-arbitrage and the Markovian assumption, the time- value of a European call option maturing at a fixed time relates to the time- value of a continuum of European call options of shorter maturity by

| (2) |

for all possible non-negative values of and at all times . The weighting function is given by,

| (3) |

The static nature of the spanning relation (2) is attributed to the fact that the option weights are independent of and . Hence, under the assumption of no-arbitrage, once the spanning portfolio is formed at the initial time , no further re-balancing needs to be done until the maturity date of the options in the constructed hedge portfolio. The practical implication of Theorem 2.1 is that an investor can hedge the risk associated with taking a short position on a given option, by taking a static position in a continuum of shorter-term options.

It should also be observed that the weight associated with the call option with maturity and strike , is proportional to the gamma that the target call option shall have at time , provided the underlying asset price is at that time point. Hence, as explained in carr2014static , the bell-shaped curve, centered near the call option’s strike price, that is projected by the gamma of a call option, implies that the highest weight is attributed to the options whose strikes are close to that of the target option. Moreover, as the common short maturity of the hedging portfolio approaches the target call option’s maturity , the underlying gamma becomes more concentrated around the strike price, . So, taking the limit , the entire weight is found to be concentrated on the call option of strike .

2.2 Finite approximation using Gauss Hermite Quadrature

The result in (2) shows that a European call option can be hedged using a continuum of short maturity calls. However, in practice, investors cannot form a static portfolio involving a continuum of securities. Therefore, the integral in (2) is approximated using a finite sum carr2014static , where the number of call options thereby used to construct the hedging portfolio is chosen in order to balance the cost from the hedging error with the cost from transacting in these options.

As mentioned in carr2014static , the integral in (2) is approximated by a weighted sum of a finite number of call options at strikes as follows,

| (4) |

where the strike points, , and their corresponding weights are chosen based on the Gauss-Hermite quadrature rule.

As described in their paper, a map is constructed in order to relate the quadrature nodes and weights to the corresponding choice of option strikes, and the portfolio weights, . The mapping function between the strikes and the quadrature nodes is given by,

| (5) |

and the gamma weighting function under the Black-Scholes model is as follows,

where denotes the pdf of a standard normal random variable and is given by,

Finally, using the Gauss-Hermite quadrature and the map (5), one obtains the respective strike points, and the associated portfolio weights are given by,

| (6) |

2.2.1 Implication of the hedging approach

In order to signify the practical utility of this static hedging approach using a portfolio of shorter maturity options, one can consider the following situation at time , where there are no liquid call options of maturity available in the market but it is known to the investors that such a call shall be available in the market under consideration, by a future date . In such a scenario, an options trading desk might very well consider writing such a call option of strike and maturity to a customer, thereby receiving a premium for the transaction. Then, given the validity of the underlying Markov assumption, the options trading desk can hedge away the risk exposure that arises from writing the call option over the time period by utilizing a static position in the available shorter-term options. However, the maturity of the shorter-term options should then be equal to or longer than , with the portfolio weights being given by (6). The validity of the Markov condition would then imply that at date , the options trading desk can use the proceeds that can be obtained by closing the position, in order to purchase the maturity call. For a detailed explanation, the reader can refer to carr2014static .

3 Multi-period static hedging approach

In this section, we modify equation (2) to obtain an exact spanning relation using options with multiple short maturities, over bounded strike ranges. The corresponding finite-sum approximations of the hedging integrals are then obtained by the application of Gaussian and Gauss-Laguerre Quadrature rules. The point of contrast between the Gauss Hermite and the Gaussian Quadrature rule lies in the fact that while the former is a finite approximation method for an integral on an infinite domain, the latter serves as an approximation for a definite integral on a bounded interval.

Our first job now is to define the Gaussian Quadrature rule for our hedging problem and then apply it accordingly for our numerical experiments. A detailed explanation of the Gaussian Quadrature rule has been provided in the Appendix and davis2007methods .

3.1 Hedging using options with multiple short maturities

In practice, there are few liquid options with maturity , which have strikes in the range and equation (2) is essentially approximated as follows,

| (7) |

where ’s are the strikes corresponding to the liquid options with maturity and ’s are the corresponding weights of the short-term options that one needs to hold in their portfolio. These are obtained by a direct application of the Gaussian Quadrature rule to the integral given in equation (7).

As a practical problem, at any given time , prior to the maturity of the target option, liquid options with multiple shorter maturities are available. Further, the approximation in (7) excludes a wide range of strike points, while only targeting liquid options that are available with maturity , within the range .This entails an error when compared to the original formula (2)

However, there would be liquid options of other multiple short maturities that may be available at time . So, it would be beneficial if these options could be included in the hedge portfolio. This would further partially compensate for the error incurred by only using options over a restricted strike range .

We illustrate the procedure for including options of maturities , where and formulate a hedging scheme that gives a better approximation than the one involving a single maturity . We begin by rewriting equation (2)as follows,

| (8) | ||||

Now, changing the order of integration in (9) yields,

We are now ready to state the main result of this paper.

Theorem 3.1.

Under no-arbitrage and the Markovian assumption, the time- value of a European call option maturing at a fixed time relates to the time- value of a continuum of European call options having shorter maturities by,

| (10) | ||||

with weights,

| (11) |

| (12) |

where,

and, , denotes the range of liquid strikes available at initial time , corresponding to the options with maturity .

Iterating the whole procedure yields the following Corollary for including any finite number of short maturities.

Corollary 3.2.

Under no-arbitrage and the Markovian assumption, the time- value of a European call option maturing at a fixed time relates to the time- value of a continuum of European call options having shorter maturities by,

with,

and

where, , denotes the range of liquid strikes available at initial time , corresponding to the options with maturity .

Remark.

In a real-world scenario, liquid options with maturity would be available for strikes over a bounded interval , with . Taking this into account, one obtains the final expression of the hedging portfolio as,

| (13) | ||||

where,

denotes the approximation error.

Remark.

As time evolves and options of short maturities become available, at some time with , one can easily incorporate that and rebalance their portfolio using our approach.

3.1.1 Application of Gaussian Quadrature and Gauss Laguerre to construct the hedging portfolio

As mentioned earlier, trading takes place only over finite strike points and hence, the hedge portfolio thereby constructed has to be a finite sum instead of a continuum of short maturity calls. Therefore, to construct an equivalent hedging portfolio, each of the two integrals in (10) needs to be discretized to a finite sum, as done in carr2014static . The corresponding expression for the first integral is then given by,

where, the weights, ’s and the corresponding strikes, ’s are computed using the Gaussian Quadrature scheme as discussed in Appendix 6.

The associated approximation error is,

for some .

For approximating the first integral in (12), one needs to perform Gaussian Quadrature twice, the inner one to compute the integral with respect to , over the interval , which once obtained, is used to calculate the outer integral over , over the bounded interval .

For the computation of the second integral in (12), one needs to approximate the inner integral over using a shifted Gauss-Laguerre integration and perform Gaussian Quadrature for the outer integral over .

Similar to the method of Gauss-Hermite quadrature, the Gauss-Laguerre quadrature method is used to approximate integrals of the form , for a sufficiently smooth function . For a given target function , the Gauss-Laguerre quadrature rule generates a set of weights and nodes , , that are defined by

for some .

A shifted Laguerre method approximates an integral , where , for a sufficiently smooth function , by performing a change of variable to to the above integral to obtain the following approximation,

| (14) |

for some . The reader can refer to the Appendix 6 for a detailed outline of the Gauss-Laguerre method performed for our integral at hand and refer to davis2007methods for a detailed description of the Gauss-Hermite, Gauss-Laguerre as well as Gaussian Quadrature methods.

3.2 Black-Scholes model

Consider the model where, under the risk-neutral framework, the stock price follows a Geometric Brownian Motion () given by,

| (15) |

where, denotes the standard Wiener process.

Equation (11) for obtaining the weights associated to the options with short maturity under the model translates to,

| (16) |

with

and,

with

where denotes the cdf of a standard normal random variable.

Under the model, the modified weight , given by equation (12) and associated with options with short maturity , would then be obtained by substituting,

| (17) |

with

3.3 Merton Jump Diffusion model

The Merton Jump-diffusion () model is a Markovian model where the movements of the underlying asset price are modeled by,

| (18) |

with denoting a compound Poisson jump with intensity .

Conditional on a jump occurring, the log price follows a normal distribution with mean and variance , while the mean percentage price change is given by .

In the dynamics, the price of a European call option can be expressed as a weighted average of the call pricing functions, with the weights being given by the Poisson distribution,

where refers to the probability mass function of a Poisson distribution and is given by,

The function is defined as,

with,

In the model, the delta and the strike weighting functions corresponding to the first short maturity are given by

The strike points based on Gauss-Hermite quadrature , as defined in carr2014static , are,

where,

is the annualized variance of the asset return under the measure . The corresponding portfolio weights are given by carr2014static ,

3.4 Application of Gaussian Quadrature to the MJD model

The integrals in equation (8) can be computed for the model in an analogous manner as in model, to obtain the modified weight (12) using,

| (19) |

and,

| (20) |

with,

and,

Here, and correspond to the strike points obtained by application of the Gaussian Quadrature over the intervals and respectively.

4 Numerical results

In this section, we apply the Gaussian Quadrature method, discussed in detail in Section 3.3, for hedging a European call option and use calls with both one as well as two short maturities to construct the hedge. The key assumption is that the liquid options corresponding to the short maturities and are available in the ranges and respectively.

Throughout the rest of the paper, we shall use the notations and to denote the Gaussian Quadrature hedges obtained using options with one and two short maturities respectively. The first part of this section is dedicated to a detailed analysis of the performance of the Gaussian Quadrature methods, and along with the Carr-Wu method carr2014static , at initial time , for the and models. The experiments have been designed to depict the efficiency of our method when compared to the Carr-Wu method carr2014static and thereby, highlight their practical significance.

The only restriction that we impose while applying the Carr-Wu method carr2014static for the purpose of our numerical experiments throughout this paper is that the strike points in the expression (4) are restricted to be in the interval , as done for our Gaussian Quadrature () method. We apply the Carr-Wu method in two ways to construct the hedge:

-

1.

denotes the application of the method with the number of quadrature points, being chosen such that the corresponding strike points , all lie in the interval

-

2.

denotes the application of the method with the number of quadrature points, , being chosen to be the same as for and the strike points falling outside the interval are dropped.

For the second part of the numerical results, we present the performance of these methods at an intermediate time, under the model, using simulated stock paths. We report the following statistics: the th percentile, th percentile, root mean squared error (), mean, mean absolute error (), minimum (Min), maximum (Max), skewness and kurtosis, when applied to and Delta Hedging (). The choice of including the Delta Hedging approach as a benchmark is due to the fact that it allows traders to hedge the risk of constant price fluctuations in a portfolio and has been one of the most popular methods for hedging over the past decades.

For simplicity of notations, we assume a zero dividend rate in all our experiments for the model. The Delta Hedging is then performed using the following method:

If denotes the initial value of the hedge, then by the self-financing condition we have,

We then divide the time interval into finite number of equi-spaced time-points , such that , .

Then, by the Delta Hedging argument, the value of the hedge portfolio at each time step , , is given by,

where denotes the Greek delta of the call option at time .

4.1 Black-Scholes Model:

4.1.1 Effect of number of quadrature points

In the first experiment, we list the results obtained by hedging using the Carr-Wu method and the Gaussian Quadrature method, involving both one and two short maturities, as we keep varying the number of quadrature points for both methods.

For the first experiment, we do not include the options of shorter maturity since the errors for , as seen in Table 1 are already low, so an introduction of a second short maturity is not necessary and would not affect the results.

Table 1 reports the expected discounted loss () of the hedge at initial time when the hedge is constructed. The formula for the expected discounted loss is,

| (21) | ||||

The reason behind the terminology of is that it represents the portion of the risk that cannot be hedged at the initial time by the constructed hedging portfolio.

The parameters used are: .The value of the target call option is

Since there are around trading days each year, we have expressed the short maturities as a fraction of the year. Thus, denotes a maturity after trading days starting from the initial time . Further the number in the brackets for indicates the number of quadrature points falling in the range .

| 2 | 0.9464 | 50 | -0.00065(28) | -0.00067 |

| 2 | 0.9464 | 25 | 3.2(15) | -0.00067 |

| 2 | 0.9464 | 15 | 0.00167(9) | -0.00067 |

| 2 | 0.9464 | 10 | -0.01357(6) | -0.00625 |

| 2 | 0.9464 | 8 | -0.01556(5) | -0.05559 |

| 2 | 0.9464 | 6 | -0.00568(4) | -0.28426 |

In Table 1, denotes the number of quadrature points used for applying and denotes the number of quadrature points used for and methods. For the given choice of parameter values, is restricted to since for higher values, some strike points lie outside the interval .

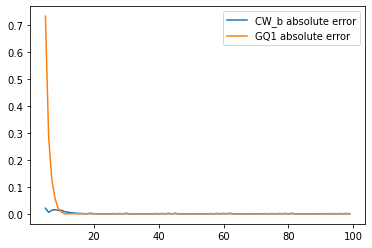

From the results listed in Table 1 and Figure 1, one can observe that the performance of improves as we keep increasing the number of quadrature points, up to a certain value of , after which the performance becomes stable. Contrary to this, the performance of fluctuates, sometimes to a large extent, depending on the strike points that fall in the range and their associated weights.

This highlights the advantage of our Gaussian Quadrature hedging approach in obtaining a static hedge that is stable as we keep increasing the number of options that are used in constructing the hedge portfolio. Whereas ’s performance would fluctuate in such a scenario.

An investor needs to choose the number of options in constructing his hedge portfolio, depending on the liquidity in the market. If his hedge performance fluctuates with respect to the number of options chosen, then it would be difficult to buy/sell the exact number of options that would be required in order to ensure the efficient performance of his hedging algorithm.

To ensure simplicity of notations, for all future experiments, we use the same number of quadrature points () for both the short maturities and . For calculating the modified weight (12), we use and quadrature points for the application of the Gaussian Quadrature and Gauss Laguerre methods respectively, which have been explained in detail in subsection 3.1.1.

4.1.2 Effect of the range of strike intervals

In this subsection we examine the effect of the restriction of the range of strike points, on the performance of the hedge, keeping the number of quadrature points to be fixed.

In an ideal scenario, when an investor has enough liquidity in the market, where a large range of liquid strikes are available, he can easily use either the Carr-Wu method or the Gaussian Quadrature method to construct his hedge portfolio and thereby, hedge the risk that he incurs from short-selling the target call option.

The problem arises when the markets experience extreme situations and the strike range for liquid options for a given maturity is then quite restricted. Therefore, one has very few liquid options at their disposal to construct their hedge portfolio.

To illustrate this effect we restrict the range of strikes for the two short-maturities and . Further, our portfolio constitutes only options for and , and additional options with short maturity , for the method.

Table 2 lists the of the , and methods. The strike points are restricted to the mentioned intervals. The strike points for and have been restricted over the interval and the number of quadrature points used for and the actual number of strike points for that fall in the strike interval have been mentioned in the brackets.

The inclusion of the second short maturity, assuming that the liquid strikes for the second short maturity are in mentioned strike intervals ends up improving the hedging performance of the Gaussian Quadrature method as denoted by the percentage decrease in loss (). The is calculated by the following formula, The parameters used for the following experiment are : . The value of the target call option is

From Table 2 one can notice that in certain cases holding the or hedge would provide better risk-exposure than . It should be noted that one can further optimize the risk exposure using by including options with shorter maturities, (say), with .

Further, in the case of the and methods, the results would be highly dependent on the number of quadrature points used, as explained in the previous experiment. The Gaussian Quadrature, on the other hand, would provide stable results even in restricted strike intervals, after a certain number of quadrature points.

Table 2 also highlights an important fact that a slight increase in the range of liquid strikes corresponding to the second short maturity can have a substantial positive impact on the performance of the hedge. This is relevant since more liquidity would be expected for options as the short maturities keeps decreasing. This performance can be improved by the addition of further liquid short maturities by application of Corollary 3.2.

| -3.8(1) | -13.0(1) | -8.9 | -8.3 | 6.7% | ||

| -3.8(1) | -13.0(1) | -8.9 | -7.2 | 19.5 % | ||

| -3.8(1) | -13.0(1) | -8.9 | 1.6 | 82.2% | ||

| -3.8(1) | -2.7(1) | -2.1 | -1.7 | 20.0% | ||

| -3.8(1) | -2.7(1) | -7.1 | -6.5 | 9.4% | ||

| -3.8(1) | -2.7(1) | -1.0 | -0.9 | 6.7% | ||

| -3.8(1) | -2.7(1) | -1.0 | -0.9 | 4.7% |

4.1.3 Effect of the spacing between the target and the short maturities

Let us consider the problem faced by the writer of a call option that matures in one year and is written at-the-money, as assumed in our previous example. The writer intends to hold this short position for an optimal time , after which the option position will be closed. During this time, the writer has the option of hedging their market risk using various exchange-traded liquid assets such as the underlying stock, futures, and/or options on the same stock. In the case that the writer decides to hedge their position using options on the same stock, it is of utmost interest to compute the effect of the short maturities, , on the performance of the hedge and accordingly minimize their risk exposure.

Assuming enough liquidity in the market, we use quadrature points for computing the hedge portfolios for both and the methods and quadrature points for the method. Further, we restrict the strike interval to a more realistic range to indicate the fact that liquid short maturity options have strikes close to the target option’s strike. The parameters are: . The value of the target call option is

Table 3 reports the of the , , and methods as we vary the short maturity , while keeping the second short maturity fixed at .

| 21/252 | 1 | -4.2 | -10.6(2) | -9.6 | -2.0 | 78.6% |

|---|---|---|---|---|---|---|

| 40/252 | 1 | -3.8 | -10.2(2) | -8.9 | -2.5 | 72.3% |

| 80/252 | 1 | -2.8 | -9.6(2) | -7.5 | -2.4 | 67.3% |

| 160/252 | 1 | -1.3 | -3.6(3) | -3.8 | -1.4 | 63.6% |

.

It can be inferred from Table 3 that for an investor with a very restricted range of liquid strikes at their disposal, the method would serve as a better method for minimizing their risk exposure.

It should also be noted from the last two rows of Table 3 that even though gives a comparable performance to in the case when is closer to the target maturity , with only one strike point being used for , the results would vary considerably if the actual strike in the mentioned range is quite far away from the strike point given by . While for we have distinct choices of strike points in each of the intervals and , so the actual strike points would be close to strike points.

One can further increase the quadrature points in to ensure that the actual strike points are very close to quadrature points (without impacting the results, owing to the stability of the method with increasing quadrature points, after a certain number of quadrature points) as shown in the first experiment, which is not the case for or .

If, on the other hand, the range of liquid strikes corresponding to the first short maturity is wide as given by the parameters: , then, choosing the same number of quadrature points for , and , as done in Table 3, one would obtain the results listed in Table 4. On observing the results in both Tables 3 and 4, it can be concluded that the performance of the hedge improves as we keep increasing the short maturity , keeping everything else fixed.

| 21/252 | 2 | 1.27 | -0.96(4) | -2.36 | -2.36 | 0.1% |

|---|---|---|---|---|---|---|

| 40/252 | 2 | 0.94 | -0.96(4) | -1.91 | -1.63 | 14.6% |

| 80/252 | 2 | 0.52 | -0.92(4) | -1.11 | -0.85 | 23.3% |

| 160/252 | 2 | 0.11 | -0.31(5) | -0.27 | -0.06 | 76.6% |

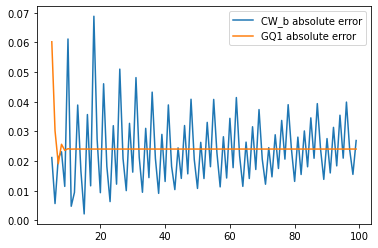

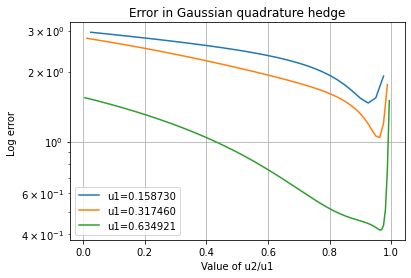

Figure 2 displays the error in the hedge for three different choices of the first short maturity , while increasing the short maturity to approach for each such choice. It can be concluded from Figure 2 that the error in the hedge decreases as the second short maturity approaches , with a sudden jump as gets extremely close to . The jump arises due to the discontinuity in the call option pay-off at time , owing to a factor of in the denominator for obtaining the modified weight given by equation (12), associated with options with maturity .

From a practical viewpoint, this implies that an investor should accumulate options of short maturities, with maturity dates close to each other to obtain significant improvements in the performance of his hedge, rather than just using one short maturity.

One should also note that, even if the short maturities are not close to each other, the resultant hedge with options (say), would always have a better performance than that of the hedge constructed with only options. So, from an investor’s perspective, it is always beneficial to include options of multiple short maturities in his hedge portfolio.

4.1.4 Simulation based comparison with Delta Hedging

Following the series of experiments that have been done at the initial time , the most natural thing to study would be to analyze the performance of the hedge until the expiry of the short maturity options.

Since the hedge constitutes options with two short maturities, , we incorporate the fact that at short maturity , the payoff corresponding to the options with short maturity is invested in a risk-free bank account and the corresponding interest earned from this at every time is also a part of our hedging portfolio value at time .

The of the hedges at time are denoted by . These are the approximation errors incurred due to the usage of a finite number of short-maturity options instead of the continuum of short-maturity options, given by the integrals in the corresponding hedge portfolios.

Depending on the sign, these errors are each invested in / borrowed from the money market at time and the interest incurred constitutes a part of the hedge portfolio error at each time , as done in carr2014static .

We construct the hedging portfolio using two short maturities, while also constructing the Delta Hedging portfolio simultaneously. The Delta Hedging portfolio is rebalanced at a certain number of equi-spaced time points over the interval . We report the corresponding statistics at the final time-point, which corresponds to the maturity date of the shorter maturity options.

For the Carr-Wu hedge portfolio, we only include the options with short maturity , to emphasize the effect of the exclusion of shorter maturity on the performance of the hedge.

Tables 5 and 6 report the of the , and methods with the strike points being restricted to the mentioned strike interval . To obtain the results, we simulate stock paths, each at equi-spaced time-points , and report the at the date for the three schemes.

The parameters used for Tables 5 and 6 are: , with the only difference being the strike range corresponding to the options with short maturity , which are taken to be and , respectively.

For the delta hedge, we perform a daily rebalancing of the portfolio and therefore the portfolio is rebalanced times our experiments since the short maturity is taken as trading days. The modified weight (12) associated with options with short maturity is estimated using and quadrature points respectively.

It can be concluded from Table 5 that the performance of the obtained by the daily rebalancing of the portfolio is far superior to the and methods under the model but the expense of rebalancing the portfolio daily could be high owing to liquidity constraints.

Further, as explained through numerical experiments in carr2014static for the case of the model, the Delta Hedging breaks down completely and is not adapted to tackle jumps in the stock price process.

| Statistics | |||||

|---|---|---|---|---|---|

| No. of quad points | 1 | 15(2) | 15 | 15 | |

| th percentile | 0.294 | 4.237 | 5.788 | 4.658 | 3.405 |

| th percentile | -0.293 | -3.569 | -6.425 | -5.391 | -3.609 |

| RMSE | 0.175 | 2.422 | 3.716 | 3.102 | 2.137 |

| Mean | 0.007 | 0.037 | -0.010 | -0.012 | 0.037 |

| MAE | 0.142 | 2.044 | 2.943 | 2.467 | 1.695 |

| Min | -0.554 | -4.027 | -15.647 | -14.058 | -7.731 |

| Max | 0.427 | 6.159 | 9.235 | 7.921 | 6.409 |

| Skewness | -0.262 | 0.251 | -0.332 | -0.369 | -0.267 |

| Kurtosis | -0.168 | -0.894 | 0.055 | 0.245 | 0.248 |

| Statistics | |||||

|---|---|---|---|---|---|

| No. of quad points | 1 | 15(2) | 15 | 15 | |

| th percentile | 0.183 | 3.062 | 3.979 | 3.328 | 0.650 |

| th percentile | -0.209 | -1.698 | -4.791 | -3.995 | -0.773 |

| RMSE | 0.123 | 1.563 | 2.705 | 2.266 | 0.440 |

| Mean | 0.001 | 0.033 | -0.073 | -0.061 | -0.011 |

| MAE | 0.098 | 1.302 | 2.155 | 1.804 | 0.351 |

| Min | -0.498 | -1.712 | -9.242 | -8.033 | -1.585 |

| Max | 0.303 | 4.906 | 7.626 | 6.387 | 1.305 |

| Skewness | -0.516 | 0.798 | -0.304 | -0.325 | -0.291 |

| Kurtosis | 0.522 | -0.265 | -0.010 | 0.048 | 0.029 |

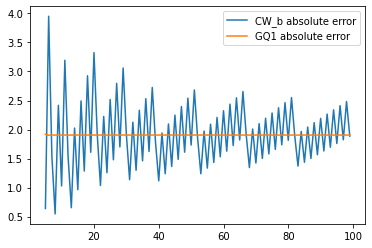

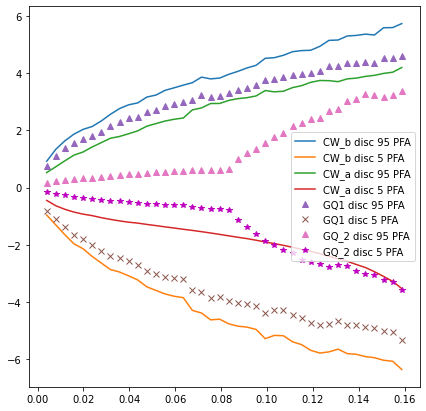

Figure 3 displays the corresponding discounted th and th potential future exposures of the and methods for the parameters used in Table 5. It can be observed from Figure 3 that the discounted s of are significantly lower than the corresponding s of and up to the second short maturity , indicating better hedging of the investor’s risk exposure up to time on including the options with short maturity , which was the desirable motivation behind including such options.

Figure 3 highlights an important factor. Over the time period , if the investor invests the proceeds earned at the expiry of the options corresponding to short-maturity in a bank account, the hedge portfolio would still perform better overall compared to , and portfolios. While the discounted -th percentile for the method, given by the red line, is lower than the corresponding -th percentile for the hedge, it is highly sensitive to the available strike points in the strike range , as explained earlier.

The investor can also choose to partially rebalance their portfolio at time . By applying our algorithm, they can include liquid options available at time , with maturity in the interval , along with their already existing portfolio of options with short-maturity . This would help them obtain a significant reduction in the hedging error.

4.2 Merton Jump Diffusion model

For the model we shall repeat the similar sequence of experiments as done for the model and report the corresponding results.

Since the results obtained in the case of the models are similar in nature to the ones obtained for the model, we exclude the simulation experiments for dynamics.

4.2.1 Effect of the number of quadrature points

Table 7 presents the results obtained at initial time when the number of quadrature points is varied for and while restricting the strike points of to be in the range . Since for , some of the strike points obtained using lie outside , we exclude such strike points.

The parameters used are: . The value of the target call option is

| 3 | 1.47 | 5 | -0.80(4) | 6.27 |

| 3 | -2.24 | 10 | -0.04(7) | -0.34 |

| 3 | -2.24 | 15 | 0.04(10) | 0.01 |

| 3 | -2.24 | 25 | 0.01(16) | 1.67 |

| 3 | -2.24 | 50 | 1.19(29) | -8.98 |

| 3 | -2.24 | 100 | -6.82(56) | -8.98 |

From Table 7 one can observe similar results as for the model, where the Gaussian Quadrature method’s performance is stable with respect to increasing quadrature points (after a certain number of points).

4.2.2 Effect of strike range

Table 8 lists the absolute errors at time for both the , and methods, as the strike ranges are varied while keeping the number of quadrature points to be fixed. The actual number of strike points for which fall in the strike interval has been mentioned in brackets. For we restrict ourselves to include only the strike points which fall in the range .

The parameters used for Table 8 are: .The value of the target call option is

| 1 | -2.54 | 20 | -6.33(2) | -6.80 | -6.52 | 4.10% | ||

| 1 | -2.54 | 20 | -6.33(2) | -6.80 | -4.86 | 28.5% | ||

| 1 | -2.54 | 20 | -6.33(2) | -6.80 | -1.21 | 82.21% | ||

| 1 | -2.54 | 20 | -6.33(2) | -4.64 | -4.37 | 14.49% | ||

| 1 | -2.54 | 20 | -0.20(4) | -0.61 | -0.52 | 14.49% | ||

| 1 | -2.54 | 20 | -0.20(4) | -0.20 | -0.19 | 7.44% | ||

| 1 | -2.54 | 20 | -0.20(4) | -0.20 | -0.19 | 6.09% |

On observing Table 8 one can draw similar conclusions as for the model that if the strike range corresponding to the first short maturity is wide enough, with enough liquid options at his disposal, the investor can choose either or to construct his hedge.

The addition of the options with the second short maturity, , always leads to a reduction in the hedging error, with the most significant decrease being when the strike range, corresponding to the short maturity is wider than for .

4.2.3 Effect of the spacing between the target and the short maturities

Table 8 lists the absolute errors at time for both the , and methods, as the short maturity are varied while keeping everything else fixed.

The actual number of strike points for which fall in the strike interval have been mentioned in brackets. For we restrict ourselves to include only the strike points which fall in the range .

The parameters used for Table 9 are : . The value of the target call option is

| 21/252 | 1 | -3.18 | -6.63(2) | -7.47 |

|---|---|---|---|---|

| 40/252 | 1 | -2.54 | -6.33(2) | -6.80 |

| 80/252 | 1 | -1.29 | -5.73(3) | -5.22 |

| 160/252 | 2 | 0.14 | -0.89(4) | -1.65 |

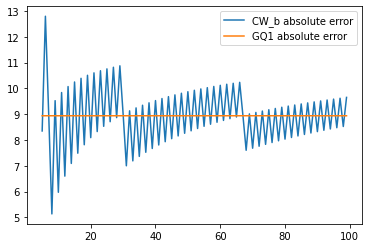

Figure 4 plots the error in hedge as the second short-maturity approaches the first short maturity , while keeping the other parameters fixed at : .

From Table 9 and Figure 4, we arrive at similar conclusions that the errors in the hedge are a monotonically decreasing function in short maturity . In the case of , the errors decrease until a certain time point close to the short maturity , attain a minimum, and rapidly increase beyond that owing to the discontinuity, as in the case of the Black-Scholes model.

The value of at which the minimum is attained, for a given choice of parameters, can be easily obtained applying a simple bisection method.

4.2.4 Effect of distribution of jumps

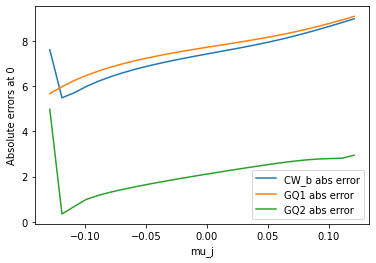

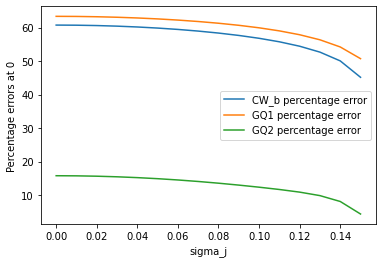

In this section we would like to analyse the effect of changes in values of and on the performance of the and hedges while keeping the annualized variance to be fixed at .

The reason for this study is to analyze the effect that the distribution of the jumps in the stock process would have on the hedging performance.

Effect of change in and : We study the effect of change in and thereby, , while keeping the other parameters fixed. The values of are chosen such that .

| 0.02 | 0.2690 | 20 | 0.8117 | 20 | 1.5985 |

| 0.1 | 0.2649 | 20 | 0.7796 | 20 | 1.5529 |

| 0.5 | 0.2438 | 20 | 0.6239 | 20 | 1.3332 |

| 1 | 0.2144 | 20 | 0.4435 | 20 | 1.0500 |

Based on the results obtained, it can be concluded that over a restricted strike interval, the absolute error (at time ) of the hedge is a monotonically decreasing function of , provided we change , while keeping the other parameters fixed.

Effect of change in and : We study the effect of change in and thereby, , while keeping the other parameters fixed. The values of are chosen such that .

The parameters used for Figure 6 are: .

On observing Figure 6 one can conclude that the absolute error (at time ) of the monotonically increases with an increase in the mean of the jump size , provided we adjust , while the other parameters are constant.

Effect of change in and : We study the effect of change in and thereby, , while keeping the other parameters fixed. The values of are chosen such that .

The parameters used for Figure 7 are: .

On observing Figure 7 one can conclude that the absolute error (at time ) of the monotonically decreases with an increase in the variance of the jump size , provided we adjust , while the other parameters are kept constant.

5 Conclusion

In this paper we have extended the theoretical spanning relation in carr2014static to include options with multiple shorter maturities through Theorem 3.1 and Corollary 3.2. An approximation of the exact spanning relation is then obtained by an application of the Gaussian Quadrature rule, as explained in detail in Section 3.3 and Appendix 6. Numerical experiments are then performed in Section 4 for the and models lead to the following conclusions:

-

1.

The efficiency of the and methods can be increased as one keeps increasing the number of options held in the hedging portfolio, up to a threshold, after which the performance stabilizes. ’s performance would fluctuate in such a scenario.

-

2.

In case of restricted liquid strikes, the inclusion of the second short maturity , by application of the method improves the hedging performance, when compared to both and or . This improvement is substantial when the range of liquid strikes available for the short-maturity is wider than that for the first short-maturity .

-

3.

As observed for the Carr-Wu method, the closer the short-maturities are to the target option’s maturity, , the better the performance is for both the and methods. Further, the performance of the hedge improves as the spacing between the shorter maturities and keeps reducing.

-

4.

On the expiry of the options corresponding to the second short-maturity , the investor has two choices at hand- They can invest their earnings from the sale of these options in a bank account and continue with the initial portfolio corresponding to the options with short-maturity . They can choose to reinvest their earnings from this sale to buy liquid options of other shorter maturities. The initial portfolio corresponding to the options with short-maturity can either be kept intact or an entire rebalancing of the hedge portfolio can also be done.

In either case, the overall performance of the would be better than both the and methods.

-

5.

The Gaussian Quadrature method would also allow the investor to include available liquid options into their existing hedge portfolio at any time prior to the short maturity or set up a completely new hedge at the expiry .

While the results obtained in this paper illustrate the utility of our method from a hedging perspective, it is restricted to Markovian dynamics. Hence, as a natural extension of this work, extending this result for non-Markovian settings would serve as an important problem.

References

- \bibcommenthead

- (1) Carr, P., Wu, L.: Static hedging of standard options. Journal of Financial Econometrics 12(1), 3–46 (2014)

- (2) Breeden, D.T., Litzenberger, R.H.: Prices of state-contingent claims implicit in option prices. Journal of business, 621–651 (1978)

- (3) Green, R.C., Jarrow, R.A.: Spanning and completeness in markets with contingent claims. Journal of Economic Theory 41(1), 202–210 (1987)

- (4) Nachman, D.C.: Spanning and completeness with options. The review of financial studies 1(3), 311–328 (1988)

- (5) Carr, P., Chou, A.: Hedging complex barrier options. Risk (1997)

- (6) Black, F., Scholes, M.: The valuation of options and corporate liabilities. Journal of political economy 81(3), 637–654 (1973)

- (7) Bakshi, G., Cao, C., Chen, Z.: Empirical performance of alternative option pricing models. The Journal of finance 52(5), 2003–2049 (1997)

- (8) Bakshi, G., Kapadia, N.: Delta-hedged gains and the negative market volatility risk premium. The Review of Financial Studies 16(2), 527–566 (2003)

- (9) Dumas, B., Fleming, J., Whaley, R.E.: Implied volatility functions: Empirical tests. The Journal of Finance 53(6), 2059–2106 (1998)

- (10) Bakshi, G., Madan, D.: Spanning and derivative-security valuation. Journal of financial economics 55(2), 205–238 (2000)

- (11) Renault, E., Touzi, N.: Option hedging and implied volatilities in a stochastic volatility model 1. Mathematical Finance 6(3), 279–302 (1996)

- (12) Hutchinson, J.M., Lo, A.W., Poggio, T.: A nonparametric approach to pricing and hedging derivative securities via learning networks. The journal of Finance 49(3), 851–889 (1994)

- (13) He, C., Kennedy, J.S., Coleman, T.F., Forsyth, P.A., Li, Y., Vetzal, K.R.: Calibration and hedging under jump diffusion. Review of Derivatives Research 9, 1–35 (2006)

- (14) Kennedy, J.S., Forsyth, P.A., Vetzal, K.R.: Dynamic hedging under jump diffusion with transaction costs. Operations Research 57(3), 541–559 (2009)

- (15) Branger, N., Mahayni, A.: Tractable hedging: An implementation of robust hedging strategies. Journal of Economic Dynamics and Control 30(11), 1937–1962 (2006)

- (16) Branger, N., Mahayni, A.: Tractable hedging with additional hedge instruments. Review of Derivatives Research 14, 85–114 (2011)

- (17) Balder, S., Mahayni, A.: Robust hedging with short-term options. Wilmott Magazine 9, 72–78 (2006)

- (18) Wu, L., Zhu, J.: Simple robust hedging with nearby contracts. Journal of Financial Econometrics 15(1), 1–35 (2016)

- (19) Dupire, B., et al.: Pricing with a smile. Risk 7(1), 18–20 (1994)

- (20) Bossu, S., Carr, P., Papanicolaou, A.: A functional analysis approach to the static replication of european options. Quantitative Finance 21(4), 637–655 (2021)

- (21) Lokeshwar, V., Bharadwaj, V., Jain, S.: Explainable neural network for pricing and universal static hedging of contingent claims. Applied Mathematics and Computation 417, 126775 (2022)

- (22) Davis, P.J., Rabinowitz, P.: Methods of numerical integration (2007)

6 Appendix

6.1 Approximation of an integral using Gaussian Quadrature rule

There are various numerical schemes ranging from the Trapezoidal and Simpson’s rule to more sophisticated ones over the recent past, for approximation of integrals over a bounded interval. While these numerical schemes have subtle differences among themselves, the general form of these approximation schemes is given as follows,

where,

While in the Trapezoidal and Simpson’s rules, the approach is to fix the nodes ’s, using which the weights ’s are found, the Gaussian Quadrature rule allows us to estimate both ’s and ’s, as dependent variables. The idea behind this approach is to choose ’s and ’s in a manner such that,

| (88) |

where, denotes the vector space of polynomials of degree , where , which denotes the degree of precision of the method, can be taken as large as possible.

The first observation that needs to be made in this regard is that for (88) to hold, it is enough to show that the same holds for the basis functions: , of the space .

This results in a set of equations which need to be solved for unknowns, ’s and ’s, , such that , which is simply the consistency condition.

In order to explain the idea better, let us first consider an example in the space . We wish to approximate the following integral,

| (89) |

Hence, our task is now to check that (89) holds for . An extremely useful formula in this regard is as follows,

On substituting in (89) and utilising the above result we obtain the following system of equations,

This system can be easily solved to obtain the following values,

If on the other hand, one wishes to approximate the following integral,

then the desired nodes ’s and weights ’s in the interval can be obtained from the above obtained nodes, ’s and the corresponding weights ’s on ,using the following linear transformations,

The most interesting fact about this approach is that the nodes lie in symmetric positions around the centre of the interval and correspondingly the weights assigned for each pair of symmetric points are the same, as can be seen in the example above.