COMPARATIVE ANALYSIS OF TECHNICAL AND LEGAL FRAMEWORKS OF VARIOUS NATIONAL DIGITAL IDENTITY SOLUTIONS

Abstract

National digital identity systems have become a key requirement for easy access to online public services, specially during Covid-19. While many countries have adopted a national digital identity system, many are still in the process of establishing one. Through a comparative analysis of the technological and legal dimensions of a few selected national digital identity solutions currently being used in different countries, we highlight the diversity of technologies and architectures and the key role of the legal framework of a given digital identity solution. We also present several key issues related to the implementation of these solutions, how to ensure the State sovereignty over them, and how to strike the right balance between private sector and public sector needs. This position paper aims to help policy makers, software developers and concerned users understand the challenges of designing, implementing and using a national digital identity management system and establishing a legal framework for digital identity management, including personal data protection measures. The authors of this paper have a favorable position111The positions in this paper are those of the authors and are not these of any of the organizations that the authors are affiliated to. for self-sovereign identity management systems that are based on Blockchain technology, and we believe they are the most suitable for national digital identity systems.

Keywords Digital identity management National digital identity systems Legal frameworks for digital identity systems Personal data protection Self-sovereign identity Blockchain eIDAS regulation GDPR

1 Introduction

National digital identity systems are solutions endorsed by public authorities to provide digital identity attributes and/or digital identity documents, in order to identify and authenticate residents and citizens before accessing online public services. Some of the national digital identity solutions are also accepted by private sector to identify and authenticate their clients online.

A national digital identity solution is either created by the State, or created by private partners and backed and recognized by the State.

The emerging national digital identity solutions have opened up many discussions about the assurance level of online identity transactions because no in-person verification can be made between the service provider and the requester. Moreover, electronic trust services related to digital identity, such as electronic signatures and seals, are also made possible in most national identity solutions, opening the door for more online business transactions and bigger need for verifiability and accountability.

However, the legal recognition of these transactions must be addressed. Electronic trust services and online identity-related transactions are only as valuable and genuine as the legal framework that provides them with relevant purpose and validity. These legal frameworks also subject their associated digital identity solutions to data protection legislation, because of the sensitive nature of identity management data.

This means that studying a national identity solution requires studying the associated legal framework and personal data protection legislation.

There are multiple research questions to cover within the theme of national digital identity systems. These are solutions that require a high level of availability, resilience and security. They are destined to be used by public authorities, citizens and residents, and allow access for sensitive and critical services. Liability (legal responsibility) of all involved entities requires legal recognition of the solution and of the transactions it allows for. This makes the legal frameworks associated to these solutions a crucial element.

Via comparison and study of different models and deployed solutions, we try to answer the following questions:

(Q1) What are the architectural, technological, functional and governance choices that need to be made when designing and deploying a national digital identity solution?

(Q2) What are the key elements that need to be addressed in the legal framework of a given deployed technological solution? And how do legal framework and the technical solution affect each other? And what are the data protection measures these legal frameworks establish?

(Q3) What is the best identity model and infrastructure for a national digital identity system that ensures State sovereignty and empowers its users? How do we imagine this solution in terms of governance and ecosystem? And how can it benefit users, the public and the private sector?

To answer these questions, we organize this paper as follows. The first section is a Background section where we present key definitions and technical overview of identity management models. The second section about National Digital Identity Solutions is dedicated to studying some digital identity solutions provided by public authorities in different countries, grouped by their identity management model of choice (to answer Q1). In the section Legal Frameworks for National Digital Identity Solutions, we are interested in two main legislation types: legislation that makes a digital identity official, i.e. recognized as legal by public authorities, and personal data protection legislation. These legislations are made to protect the online privacy of users and cover national digital identity solutions due to the sensitive nature of identity management data. The legal frameworks studied are the ones associated to the technical solutions presented in the section that precedes this (to answer Q2). By studying and analysing the solutions, along with their legal frameworks, their governance and the different configurations such as the ecosystem and stakeholders, we can highlight the problems and issues facing any solution. It also enables us to point out the conditions for a solution’s success. We set out these conclusions and our own position as researchers in the field of identity and access management, law and privacy in the Authors’ Position section. Our recommendations for the design and implementation of a national digital identity solution, as well as other considerations for protecting user privacy, ensuring state sovereignty over this digital governance instrument, and striking the right balance between public and private sector needs are also detailed in this section (in response to Q3). Finally, we conclude our paper.

2 Background

Identity management data and attributes have evolved over the years from simply coupling identifiers like usernames and emails with to-know authentication factors like passwords, to whole profiles characterized by an online presence, activities, content and other forms that help express and define “self-hood” [1]. This eventually meant the collection and processing of more personal data. Technologies and legislation regarding how these data are used, processed, and stored are also evolving.

However, the Internet was created without any standards for identifying users. As a matter of fact, anonymity is an important feature of the Internet, and it is what made online communities succeed as an alternative space capable of providing a multitude of identities, even fictive ones. It is important to preserve this kind of freedom over the internet. In recent years, Internet freedom has become a major concern for users. A wide range of legislation worldwide reflect these concerns by providing a legal framework and directives for the processing, sharing, and storage of personal data by service providers.

Legal frameworks for online identity should preserve privacy, while allowing a form of accountability to prevent cyber-crime (e.g. fraud, hate speech, cyber-terrorism). Technological choices for building online identity solutions must align with legal frameworks. The same logic applies to national digital identity solutions, where users are provisioned with trusted digital identity attributes that can be used to perform the needed online transactions in a secure and private way, allowing user control, pseudonymity, and even anonymity in certain use-cases such as in health care.

2.1 Definitions

2.1.1 Identity Management Data

Identity management data, for a natural person (also referred to as a physical person or a data subject), are the multitude of data that are declared, computed, collected or issued across different online platforms that are directly or indirectly linked to a natural person, and used to manage their identity (identify, authenticate and authorize). Identity management data range from identifiers, attributes and credentials that are self-certified or issued by a trusted party (public authority, university …), to social media and online community profiles data, biometric data, identifiers created by or for the user and data resulted from internet activities. Identity management data also include authentication factors used by a user to prove that they are indeed the user described by these data, such as to-know factors (e.g., passwords and patterns), to-own factors (e.g., private keys, tokens, and physical objects), and to-be factors (e.g., fingerprints, facial recognition, and voice).

2.1.2 Personal Data

Personal data is defined as any information related to an identified or identifiable person222Article 4-1, GDPR.. This includes direct identifiers like the name, identification numbers and online identifiers, biometric data, social identity etc. It also includes any data that can be used to identify the person behind even indirectly. In other legal frameworks, it is referred to as Personal Information or Personally Identifiable Information (PII)333OMB M-10-23 (Guidance for Agency Use of Third-Party Website and Applications), Appendix.

eIDAS regulation defines Person Identification Data (PID) as a set of data enabling the identification of a natural or legal person444 Article 3-3, eIDAS regulation.. PID and any other data that can be used to identify a person directly or indirectly, mainly identity management data defined above, are considered personal data.

2.1.3 Electronic Trust Services

Electronic trust services are electronic services related to the verification, creation and preservation of electronic signatures, seals, website certifications, electronic timestamps, and other similar services. The term was coined by the European parliament and the European Council first in the Electronic Signatures Directive 1999/93/EC555The term was initially Certification Service Provider and later in the eIDAS regulation666Article 3-16, eIDAS regulation.. The eIDAS regulation calls the provider of these electronic trust services a Trust Service Provider (TSP). If these electronic trust services meet additional eIDAS regulation requirements777Annexes I, II and III, eIDAS regulation., they are known as Qualified Trust Services888Article 3-17, eIDAS regulation., and the provider is knows as a qualified trust service provider (QTSP).

2.1.4 Level of Assurance

The Level of Assurance (LoA) is the degree of confidence in a claimed digital identity or the certainty with which a claim to a particular identity during authentication can be trusted. eIDAS regulation defines 3 levels of assurance for electronic identification: low, substantial and high999Chapter 2, Article 8-2, eIDAS regulation.. LoA is also known as IAL for Identity Assurance Level in other frameworks of reference. The US National Institute of Standards and Technologies (NIST), for example, defines different IAL for identity proofing, authentication, and federation [2]. Different LoA levels are required according to the variety of use cases.

2.2 Identity Management Models

An identity-management model is a set of architectural and functional choices for managing identities in a given identity-management system. Traditionally, service providers used a siloed identity management model to identify and authenticate their users. Users have to sign up and sign in for each service separately and are obliged to keep their authentication information. From their end, service providers have to retain the identity management data and credentials of users. This means a more fragmented digital identity for users and an overhead for service providers tasked with the storage and security of their users’ data. Businesses have no way to obtain or share user credentials between them.

The federated identity management model solves this problem by centralizing most identity management data and credentials to be stored and managed by an identity provider (IdP) that connects the user directly with any service provider. Federated identity management is convenient for service providers, as it offloads the identity management tasks and costs, and it is also convenient for users who do not have to deal with scattered identity credentials and authentication material. However, the model presents a strong centralization and dependence on identity providers.

The user-centric model changes the game by placing the user at the center of the interaction between an identity provider and service providers. In [3], Kim Cameron et al. define the user-centric approach as “structured so as to allow users to conceptualize, enumerate and control their relationships with other parties, including the flow of information.”

Users are responsible for storing their identity management data and have the freedom to share them when needed with the service providers.

The user-centric approach raises concerns regarding possible correlations and tracing of a user’s activities, as the IdP and service providers can collude to correlate users’ activities. Although it enables the user to give consent and control who should share their identity management data, the user-centric model still relies on an identity provider to enroll the user and provide them with identifiers. The level of user autonomy is still weak.

The self-sovereign identity model (SSI) solves the autonomy and centralization problems of the typical user-centric model. Instead of relying on a centralized source of trust to authenticate users and on an identity provider to enroll and register them, the SSI model enables users to register themselves directly as many times as they wish on a decentralized platform like Blockchain, and enables them to contact and demand different issuers for different credentials and attestations/attributes to be linked to whatever identifier they want. Moreover, the SSI model enables users to create these credentials themselves, where they can self-assert claims and relationships about themselves and other users, such as club and group membership, personal capabilities, and other relevant claims. In general, SSI systems rely on open standards developed by different communities and work groups, like the Decentralized IDentifier (DID) and Verifiable Credentials (VC) standards and DID-Auth for authentication. Users interact with the SSI issuers and verifiers through an application called a wallet. Wallets allow users to request, obtain, store credentials they get from issuers and present them to verifiers. Wallets can also integrate other services like digital signatures, key and identifier generation and even the capacity to create credentials that are either self-issued or issued by the users to other users, and the capacity to verify presented credentials. Wallet applications are not a compulsory component for an SSI system, since we can still have verifiable documents over a decentralized ledger similar to the Public Key Infrastructure (PKI) certificates model. In a matter of fact, issuers can still issue credentials that are rooted in Blockchain networks, and that are verifiable, and can simply transfer them to users by different means without relying on wallets. Users from their end can choose how to store and present their credentials. However, the process seems more complicated without a wallet application that provides such functionalities in a more secure way.

Table 1 compares the above four models on the basis of different features and security and privacy aspects.

| Siloed | Federated | User-centric | SSI | |

| Interoperability1 | Low to None | Medium2 | High | High |

| Control over identity management data and credentials | Service providers | Identity providers | Users | Users |

| Registration Authorities | Applications | Identity providers | Identity providers | Autonomous registration |

| Privacy3 | High (identity management data specific to each silo which mitigates correlations) | Low (high risk of correlation across Service Providers) | Medium (correlation still possible when IdPs and SPs collude) | High (multiple identifiers, identity management data created, stored and controlled by users) |

| Decentralization | No | Yes but there is still a degree of centralization (limited number of IdPs per federation) | Yes | Yes, strong decentralization |

| Service availability4 | Medium (relies on the availability of the silo) | Medium (relies on the availability of the IdP) | High | High (relies on the availability of the distributed ledger) |

| Common standards and protocols | TLS/SSL, HTTPS | SAML, OAuth, OpenID Connect | OpenID, SpaceCard | DID, DID-Auth, VC, DID-Communication, Blockchain |

| User Autonomy | Low (identity management data provided and managed by the silo) | Low (identity management data provided and managed by IdPs) | Medium (identity management data provided by IdPs but controlled by users) | High (the users generate, publish and manage their own identity management data) |

| Architecture |

![[Uncaptioned image]](/html/2310.01006/assets/Figures/siloed.png)

|

![[Uncaptioned image]](/html/2310.01006/assets/Figures/federated.png)

|

![[Uncaptioned image]](/html/2310.01006/assets/Figures/user-centric.png)

|

![[Uncaptioned image]](/html/2310.01006/assets/Figures/ssi.png)

|

-

1

Use of identity attributes across different systems

-

2

Only between federation members

-

3

Measured according to the level of possible correlations among entities to link identity management data, and the number of entities able to link them

-

4

Availability of the identity and access management service

3 National Digital Identity Solutions

Digital identity systems vary from one State to another, from Single Sign-On (SSO) authentication systems that enable citizens to identify and authenticate themselves with different online public services, to fully mobile wallets containing digital versions of official credentials - issued by public authorities or on behalf of public authorities.

The different design choices on one hand, coupled with governance choices, are what makes national digital identity solutions very different in terms of capabilities, levels of assurance in the user’s identity, what services they allow their users to access and how much do they appeal to public use or adoption by the private sector. We proceed by studying a few examples of these solutions grouped by their identity management model that we presented in the previous section.

3.1 Federated Identity Management Solutions

Multiple national digital identity solutions around the world follow a federated identity model. Notably, two solutions that are notified within the "electronic Identification, Authentication, and trust services" (eIDAS regulation) regulation and are the French FranceConnect/FranceConnect+101010To the moment of writing this article, only FranceConnect is rolled out and currently being used. Thus we focus on FranceConnect. and the British UK Verify - at least before Brexit. Both solutions follow a federated identity management model and are used by users to access online public services. However, while FranceConnect has over 30M users by October 2021 [4] and is still operational, UK Verify failed to attract British users, gaining only about 3.6M users at its peak [5] and was eventually decommissioned by 2020, only to be extended during Covid-19. Differences in business logic, technologies, and legal frameworks between the two States may explain these different outcomes.

For instance, the manner in which identity providers (IdPs) are designated and chosen for each solution is a major difference. France relied on its own public authorities to work as IdPs for FranceConnect since most of them already have an identity solution - e.g. the ministry of finance (impots.gouv), the French Social security (Ameli), the French post office (Identité Numérique La Poste) and "France Identité" as an IdP provided by the ministry of interior, ministry of justice and other public authorities.

On the other hand, the UK has relied exclusively on private sector companies as identity providers, mainly Experian, Verizon, Barclays, GB Group Digidentity and Post Office [6]. Currently, all have withdrawn, except for the Post Office and Digidentity. This had major drawbacks on the solution. For example, Experian alone had around 2M registered users, it was the biggest IdP for Verify, and when Experian opted out from their role in the UK Verify, they simply asked their users to re-register with another IdP, with a total lack of interoperability and availability.

While FranceConnect only offers access to online public services, UK Verify enables using services from private sector entities using Open Identity Exchange (OIX)111111 Most IdPs for UK Verify are members of the OIX, mainly Barclays, Experian, GBG and Digidentity [7]. However, it is planned that FranceConnect+ will enable such services.

Another major difference between FranceConnect and UK Verify is that FranceConnect had no competitors supported by the public administrations. Although public administrations had their own digital identity solutions and identity management data, they came together within FranceConnect as identity providers for the federated solution. That was not the case for UK Verify, which competitor - “Gateway Connect” developed by HM Revenue and Customs (HMRC) - gained over 16M users121212Gateway Connect is based on the Government Connect solution that was supposed to be replaced with UK Verify. Instead, HMRC developed its own solution that uses the existing Government Gateway identifiers., and already enabled users having an account to authenticate themselves and access around 123 online public services, a number far greater than the public services that UK Verify enables users to access.

Moreover, HMRC refused to integrate UK Verify as an authentication method for their services [8]. This was also the case in the National Health Service (NHS) of England, who found that UK Verify was not suitable from a security and privacy perspective for authenticating patients and allowing them to access health data. NHS patients who have tested the solution were highly skeptical of banks and private entities providing their identities and intervening in their health data [9].

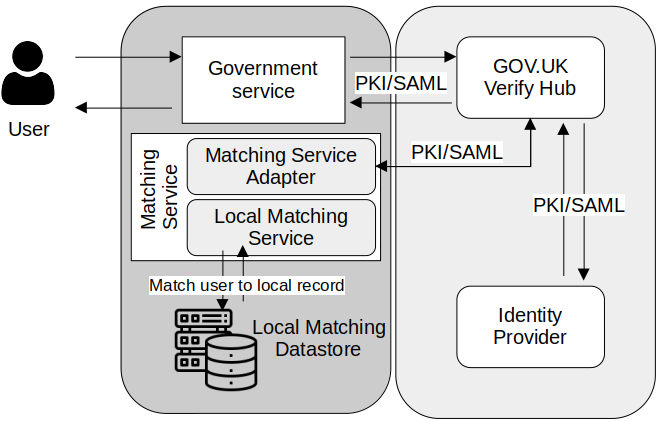

Even from legal and social points of view, the grounds for a digital identity system differ between the two countries. France still has national identity cards and centralized databases containing the identity management data of natural persons residing in France (RNIPP), which facilitate the identification and authentication of individuals. For example, the RNIPP database was consulted to authenticate the presented identity management data and to remove redundant identity profiles from FranceConnect. On the other hand, the UK does not have national identity cards or centralized identity databases, as data are fragmented across different agencies and authority branches, making it harder to authenticate and de-duplicate identity management data at the national level. That is why, as depicted in Figure 1, the UK Verify solution uses a Local Matching Service that is hosted on the organization’s infrastructure (for example, each public authority should have its own identity database) and it only provides a Matching Service Adapter to help match identity management data provided by an IdP to locally existing data records. The matching policy is also left to the discretion of organizations which can deal with single, multiple or no matches.

On a technical level, the two solutions integrate different identity federation protocols even though they follow the same identity model. FranceConnect uses the Open ID Connect (OIDC) protocol, which is more recent than the SAML protocol used by UK Verify. In matter of fact, OIDC is the third generation of the Open ID protocol, and was published in 2014, while the latest version of SAML, SAML 2.0, dates back to 2005.

OIDC uses JSON over the RESTful API to transfer identity management data between IdPs and service providers, whereas SAML uses XML over HTTP and SOAP to transfer identity management data. Communication between IdPs and service providers in SAML is secured using encrypted, digitally signed certificates, whereas in OIDC, encrypted, digitally signed tokens are used.

OIDC is easier to consume and lighter to use with APIs, whereas SAML does not work well with APIs and is too heavy. Moreover, OIDC can also be used for mobile applications, unlike SAML, because its reliance on XML is difficult to integrate into the mobile world. These fundamental differences between the chosen protocols were also inherited by the two solutions, and may explain, among other factors mentioned above, why FranceConnect was more successful than UK Verify and why it is more appealing to users.

3.2 User-Centric Solutions

User-centric national identity solutions usually revolve around an official digital identity document or identifiers held on a mobile application or a physical card equipped with a smart chip used via a card-reader or a compatible equipment, which the user employs with various service providers both online and offline public services, and other private sector services that accept a State-authenticated digital identity.

India’s Aadhaar, Estonia’s e-ID and Singapore’s Singpass are examples of user-centric national identity solutions. Although all three solutions follow the same identity model at an architectural level, there are significant differences. For example, Aadhaar and Singpass are highly centralized in terms of registration. The only identity provider is the State, and registrars are either public authorities or third parties working on their behalf. The acquired identity management data are held by the public authorities in a centralized way. On the other hand, Estonia’s e-ID handles identity management data in a decentralized way using the X-Road platform and a Blockchain platform.

3.2.1 India’s Aadhaar

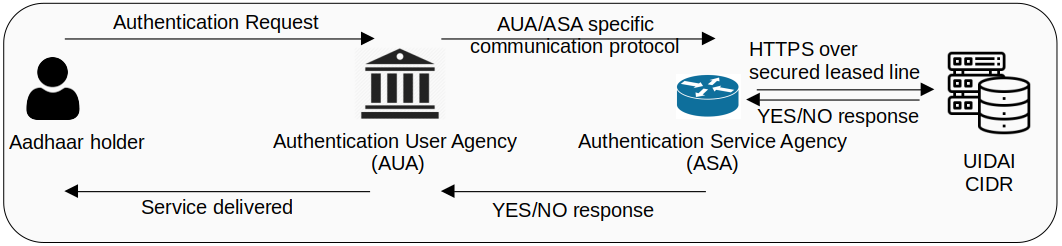

For Aadhaar, India has enrollment centers responsible for obtaining the biometric and demographic data of an individual and enrolling it in the system by providing a unique permanent 12-digit identifier. The system has already issued 1.3 billion identifiers to users131313As of March 2021 according to Unique Identification Authority of India (UIDAI) Annual Report 2020-21 where each user has one unique identifier, and the deduplication process - which is the removal of redundant identifiers or the detection of subjects having more than one identifier - is done by consulting a biometric database called the Central Identities Data Repository (CIDR) owned and centralized by the public authorities. Three Automatic Biometric Identification System (ABIS) from three different vendors are used to detect redundant biometrics by comparing incoming CIDR reference and anonymized biometrics to their own [11]. Aadhaar identifiers and cards allow holders to identify and authenticate themselves to access online and offline services such as banking, sim cards, social pensions and rations, and other online public services. Aadhaar also enables digital signatures with the same legal value as handwritten signatures.

However, the world’s largest digital identity solution has significant privacy and accuracy concerns. For example, relying on a biometric database to deduplicate identifiers is problematic and cannot guarantee the correct deduplication. Between 2010 and 2019, 475,000 identifiers were canceled, with an average of approximately 145 duplicate identifiers per day [12]. In addition to the issues of proper operation, Aadhaar has several privacy and confidentiality issues. For instance, having a unique global identifier using the same identifier for all online transactions means that the CIDR can correlate the user’s activity and has a complete history of who accessed what.

Privacy International published a very critical report of Aadhaar [13], and cited the impossibility of making efficient comparisons to deduplicate identifiers from a biometric database of the size of the Indian population (approximately 1.4 billion). The report also notes data breaches and leaks in the system. There are also important violations of user consent, where the user is obliged - in practice - to enroll and have an identifier even if it is not legally mandatory. Aadhaar identifiers are also linked to bank accounts and health records, further compounding the problems and compromising solutions.

As Figure 2 shows, the Aadhaar system relies heavily on the CIDR biometric database, which calls into question the performance and accuracy of the system as a whole because the verification method, that is, comparing the submitted data with the CIDR data, is not reliable in itself. The heavy reliance on the CIDR database and biometric and demographic data for deduplication makes it mandatory for users to give up their biometric data during enrollment to be issued an Aadhaar identifier. This technical obligation to collect biometrics for correct functioning exerts a heavy toll on the Aadhaar solution because of the sensitivity of the data, extra security measures, and overhead needed to store and transport them.

Aadhaar also raised transparency issues as no public consultations took place during the design of the solution. Moreover, unlike all the solutions analyzed in this section, Aadhaar is a proprietary solution that is not open-source.

3.2.2 Singapore’s Singpass

Singapore’s Singpass is also based on a authority-owned biometric database. It uses an API called "Identiface" to authenticate users through online facial recognition and allows them to access online public and private sector services, as well as electronic signatures. Singpass comes with a mobile app in the form of a wallet storing digital identity documents, such as drivers’ licenses, national ID cards, diplomas, etc. These digital documents are in the form of digital certificates issued by the National Certification Authority of Singapore. The solution relies on a PKI for digital signatures and digital certificates issued to users mainly by the centralized national registration identity card (NRIC) of Singapore.

Singpass provides two main services for citizens and businesses: MyInfo which uses the latest data on individuals and businesses from various public authorities to automatically fill out forms and exchange these data between the involved parties, and Verify which is used to verify the data without any physical documents. 4.5 million persons use the Singpass system (around 82% of the Singaporean population and 97% of citizens and residents above 15 years old) [14], and about 78% use the Singpass mobile application.

Like Aadhaar, Singpass is government-owned, managed, and maintained by the Government Technology Agency GovTech, but it is an open source solution [15] and has received less criticism about transparency and openness.

The use of facial verification API in a national identity scheme is the first, which comes with privacy concerns, fear of mass surveillance, and intrusiveness. Users consent to the use of their biometric data for authentication. The use of mobile applications and mobile identity documents is optional because users can use Singpass as a website to access services using their physical identity documents and the identifiers present on them. Providing many alternatives to access online services is always crucial for digital identity schemes because if a national identity scheme is left to be the only way a user can access services, it is no longer an optional solution, even if it is stated to be one, which is the case with Aadhaar.

3.2.3 Estonia’s e-ID

In terms of digital identity infrastructure, Estonia is arguably the most developed national digital identity system. Estonia launched e-governance and e-banking services in 1996, an e-tax for online tax payments in 2000, and the national digital identity program e-ID in 2002. The national identity card is mandatory in Estonia from the age of 15; 99% of Estonians have national ID cards, that are equipped with an electronic chip.

Estonia uses a PKI system to power the e-ID infrastructure: a private key is generated and stored on the card’s electronic chip, the identifier on the card is used as the public key, and the public key can be retrieved using LDAP from the public directories. The card and the associated software called “DigiDoc” can be used to authenticate the cardholder online using PIN1, to electronically sign documents using PIN2, to encrypt data and exchange them using the keys associated with the card, and to access public and private online services.

The Police and Border Guard Board (PBGB) is the authority responsible for the creation and supervision of both physical and digital identity documents to Estonians.

The shortcomings of e-ID cards are that users need a card reader to use their identity cards with their computers. Estonia launched its Mobile ID program in 2007 with the country’s major mobile operators. Today, approximately 19% of Estonians use Mobile ID, which is a special SIM card equipped with applications for digital signatures and authentication and private keys stored on the chips, enabling the same functionalities of an Estonian e-ID card without relying on a card reader.

To ensure the availability, confidentiality, and integrity of citizens’ identity management data, Estonia uses a Keyless Signature Infrastructure called the KSI Blockchain [16]. The KSI Blockchain is used as part of a data exchange layer to timestamp transactions via an X-road platform, which is used by both public and private entities in Estonia to exchange data. In addition, Estonia has “Data Embassies,” the first of which is in Luxembourg. These embassies are data centers, servers, and cloud instances capable of running all online services and providing backup data in any situation to ensure service continuity. This solution is crucial to ensure availability because Estonia has a paperless policy and heavily relies on a digital infrastructure that was attacked on several occasions, the most critical of which was in 2007 [17].

Despite being advanced and well established, the Estonian national digital identity scheme experienced several troubles. For example, in 2011, faulty cards were delivered to users, and it took the Estonian authorities over nine months to publicly and transparently address the incidents. A similar problem occurred in 2017, where the same private key was stored on multiple cards by a private contractor [18]. The latter incident was immediately communicated by the public authorities, but it took time to find and resolve the problems, which involved approximately 750,000 cards at the time.

Estonia contracts private companies to build various technological components of its digital identity infrastructure, which means an extra layer of abstraction between the public authorities and the digital identity services it provides. This extra layer can prevent public authorities from overseeing the services correctly and efficiently.

The digital identity layer is a pillar of e-governance. It enables all public and private services and allows secure data and document exchanges between all involved parties, as depicted in Figure 3.

3.2.4 Summary of user-centric solutions

User-centric identity solutions still present privacy issues, and even if users control their identity management data, identity and service providers can still correlate user’s activities and relationships. The centralized sources of truth – for authentication and deduplication – on which these solutions rely, such as centralized or decentralized databases held by the public authorities or identity providers, still introduce design flaws and opportunities for hackers to target these databases, thereby threatening data confidentiality and integrity.

In matter of fact, both user-centric and federated identities have conceptual drawbacks. Both models rely on identity providers, and whether the identity provider is from the private or public sector, the immense levels of power that the provider has over the user’s identity make the relationship completely asymmetric. This is inappropriate for the users, since IdPs can revoke identities, delete identity management data, or simply stop maintaining the systems, as was the case with UK Verify.

Rethinking how digital identity should be designed has become crucial, as it is a way to empower individuals instead of aggravating mass-surveillance and allowing private organizations to merchandise personal data.

3.3 Self-Sovereign Identity Solutions

Powered by a distributed ledger, generally a Blockchain, Self-Sovereign Identity (SSI) systems are increasingly being adopted in identity systems that require a high level of decentralization, interoperability, and shared governance. Companies such as Evernym and organizations such as Sovrin are already providing Blockchain-based digital identity infrastructures and services for various use cases [20] centered on verifiable credentials and their exchange.

The European Self-Sovereign Identity Framework (ESSIF)141414Note: while ESSIF itself is a framework and not a single monolithic solution, for simplicity we refer to it as one. is perhaps one of the most interesting, promising and challenging implementations of the SSI model on a big scale.

The ESSIF aspires to provide a technical framework in which different actors work together to solve one of Europe’s digital challenges: a digital identity solution that is in accordance with the legal framework defined by eIDAS regulation - which is currently being discussed and evolving to eIDAS 2.0, refer to eIDAS regulation (EU) in the next section about legal frameworks - and trusted in the European Union.

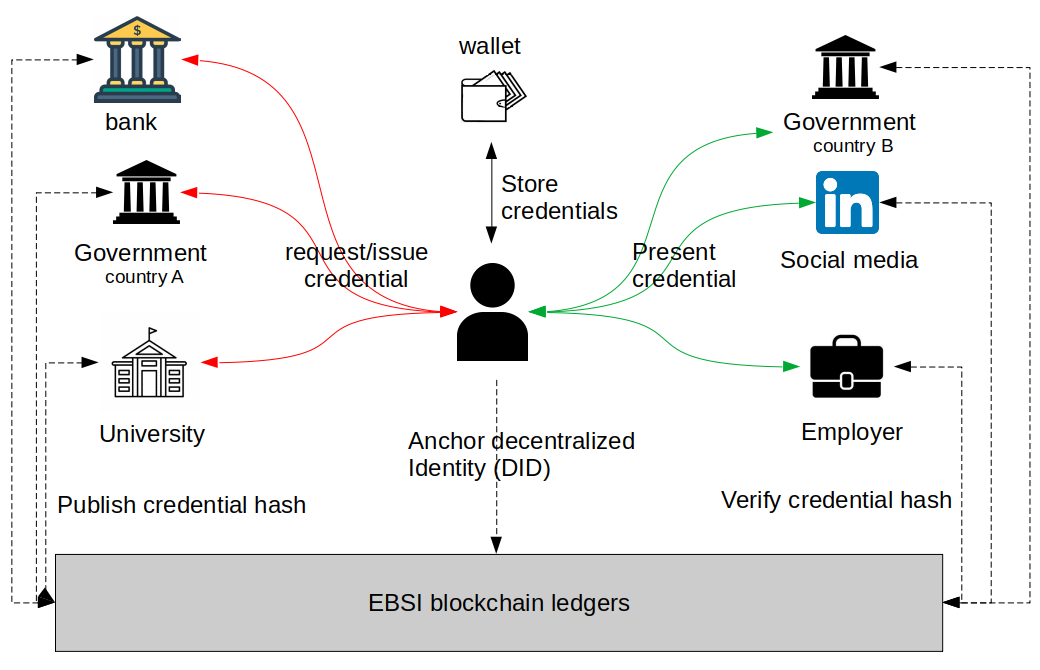

The EU identity program consists of three major building blocks: the European Blockchain Services Infrastructure (EBSI) providing a consortium Blockchain between EU members; eIDAS nodes for interoperability between national infrastructures and administrations, including national identity infrastructures; and the ESSIF framework that provides users with an SSI application used for digital identity services. Figure 4 illustrates this.

3.3.1 ESSIF context and Scope

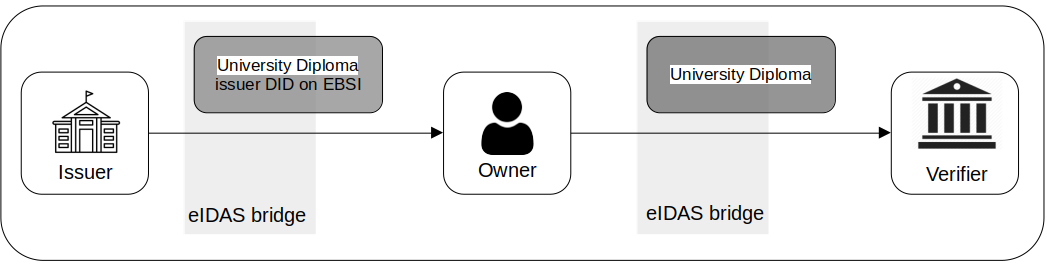

The ESSIF defines an ecosystem for the European SSI and a trust framework that allows natural persons to be identified, authenticated, and exchange verifiable credentials, which are digitally signed attestations of attributes about the subject issued by a trusted entity, such as a university or a public authority. These credentials are designed to be cryptographically verifiable in terms of ownership and authorship, and support different privacy enhancing techniques, such as zero-knowledge proofs and selective disclosure, to guarantee a high level of privacy. The first use case of ESSIF is to create digital diplomas as verifiable credentials issued by universities to their alumni. These credentials are to be verified by potential employers and stakeholders across the EU. Figure 5 is an overview of ESSIF that shows potential stakeholders and transactions between them.

3.3.2 ESSIF Governance and Ecosystem

For a project on this size to work, the ecosystem must be carefully defined. The ESSIF is designed as a large framework, where multiple SSI solutions and services are recognized cross-border between EU Member States. ESSIF is one of the first use cases of the EBSI Blockchain.

EBSI blockchain is specifically used by ESSIF for publishing decentralized identifiers, public keys and credential related metadata such as schemas and revocation status. In addition, the ESSIF maintains public lists for trusted issuers and trusted service providers to ensure greater trust in the framework. ESSIF does not aim to build or maintain a wallet for EU citizens but rather to define a solid framework for different wallet providers and electronic trust services to work within.

3.3.3 ESSIF/EU ID Wallet

The EBSI project includes a wallet, but only for testing purposes, and is not or intended to be publicly used. ESSIF, as a framework, as well as the work of the eIDAS Expert Group on EUDI wallet specifications [22], propose architectures, standards, and requirements for wallet applications, rather than providing one, because other actors, from both public and private, are supposed to provide their own wallet solutions to users.

These entities are called “wallet providers” and will be certified by a conformity assessment body and under the supervision of a supervisory body. Wallets can be both online and offline, with different requirements for each type, and must allow users to register themselves by publishing their DID on an EBSI ledger and to communicate with various issuers and trust service providers to obtain verifiable credentials and perform normal and qualified electronic signatures.

The capabilities and requirements of the wallets, as defined by the eIDAS Expert Group, go beyond the scope of ESSIF for some functionalities such as digital signatures and other electronic trust services, but in general align in terms of wallet identity requirements and standards, since ESSIF must align with and comply with the eIDAS regulation. Overall, although the EUDI wallet does not mention any standards to be used in terms of identifiers and credentials, the ESSIF does.

The ESSIF encourages the use of the DID standard as Blockchain identifiers and VC standard as credentials to be used by different interacting parties. EBSI even propose their own DID method called DID EBSI [23]. Users can register as many DIDs as they want and can use different DIDs to interact with different issuers that have different levels of assurance based on the type of VC they provide. Different VCs obtained from different issuers can be linked to different DIDs or the same DID depending on what the user wants and on the use-case.

After a DID is registered, the legal implication of using that identifier and the associated credentials are still in discussion since different EU Member States have different notions and laws regarding unique identifiers is and if a DID is considered a unique identifier in this context or not. However, a DID can be legally and officially linked to the identified subject when needed by having an authority to verify the legal identity of the subject and issue a credential linking that identity to the DID. Moreover, a VC may contain the digital signature or digital seal of a qualified trust service provider, which adds value and LoA to digital documents or claims issued in the form of a VC [24].

3.4 Section Summary

Implementing a national digital identity system presents challenges from one State to another. Some States that already have uniform (centralized or decentralized) databases of citizens and resident identities, such as France (RNIPP, INSEE registry), Estonia, Singapore, and India, have been more successful in implementing digital identity systems with higher levels of trust in the authenticated identity. In contrast, countries with more fragmented digital identity databases and without national identity schemes such as the national identity card, e.g. the United States and the United Kingdom, have had more difficulty implementing such systems. National digital identity projects follow different identity models, depending on legal frameworks and the ability of different existing identity infrastructures to coexist and be used in newer digital solutions, as summarized in Table 2.

On the other hand, we have SSI solutions emerging all over the world, such as in New South Wales (Australia) [25] and British Columbia (Canada) [26] and ESSIF.

ESSIF starts with a well-defined use case: the cross-border recognition of educational credentials such as diplomas and student IDs. This first use case will be used to prove that a European SSI platform is an essential step towards a single European market. Providing full administrative interoperability via a cross-border digital identity will enable European citizens to access services in all EU Member States in the same way as they do in their own country.

| FranceConnect | UK Verify | Aadhaar | eID Estonia | Singpass | ESSIF | |

| Decentralized identity database | No | Yes | No | Yes | No | Yes |

| Identity model | Federated | Federated | User-Centric | User-Centric | User-Centric | SSI |

| IdP | Public authorities, Private companies | Private companies | Public authorities | Public authorities | Public authorities | None |

| Services from private sector | No | Yes | Yes | Yes | Yes | Yes |

| Electronic signatures | No | No | Yes | Yes | Yes | Yes |

| Interoperability | Yes1 | Yes | No | Yes | No | Yes |

| Standards, protocols and technologies | OpenID, OAuth-2 | SAML, PKI | ABIS | KSI Blockchain, X-road, PKI, SIM cards, electronic chips | Facial recognition | DID, VC, Blockchain, DID Auth |

| Deduplication method | Cross-checking the RNIPP database | Local Matching | Biometrics | Not specified, but supervised by the PBGB | Biometrics | No single identifer |

| Legal framework | eIDAS regulation, GDPR, the decree of November’s 8th 2018 | eIDAS regulation, GDPR | Aadhaar Act 2016 | eIDAS regulation, GDPR, the Identity Documents Act | NDI2 initiative | eIDAS regulation, GDPR |

| Openness | Open source | Open source | Proprietary | Open source | Open source | Open source |

-

1

Via eIDAS node, the same goes for UK Verify, Estonia’s eID, ESSIF and any other European national identity scheme that is eIDAS notified.

-

2

National Digital Identity

From experience and by referring to different incidents, such as: (i) the scrapping of the ID Cards in the UK in 2011 (ii) the SAFARI affair in France in 1972-1974 where the public authorities attempted to interconnect identity files and data held in different French administrations and authorities using the INSEE number and (iii) the United States where President Bush’s attempt to create a national ID card failed for fear of a lack of transparency and abuse of the system in the absence of a clear legal framework, we can conclude that if a national digital identity system is to work, it must avoid repeating mistakes like lack of transparency and the absence of a legal framework that guarantees the proper use of personal data, privacy protection, and trust. In the next section, we conduct a comparative study of Legal frameworks related to the national digital identity solutions presented above.

4 Legal Frameworks for National Digital Identity Solutions and Personal Data Protection Legislation

Legal frameworks that are established to regulate how digital identity solutions and electronic trust services are deployed and used. They add legal recognition to identity-related transactions like electronic signatures and seals. These frameworks also include personal data protection measures.

4.1 Legal Frameworks For National Digital Identity Solutions

National identity solutions are often created or launched by legislation that makes them possible within a given legal framework. The legal framework defines governance for a solution by creating or designating a regulatory control body. The framework should also define how the data collected for these solutions are stored, processed, and used, especially personal data. Generally speaking, depending on the State, the framework either makes the solution subject to existing data protection legislation or establishes specific rules for personal data protection.

4.1.1 eIDAS regulation (EU)

The eIDAS regulation is a EU regulation adopted in 2014 and went into force in 2016. The regulation addresses the electronic identification cross-border between EU Member States, by virtue of mutual recognition of eIDAS notified digital identity schemes for high and substantial LoA. Private sector services can also make use of eIDAS notified schemes but they are not under any obligation. Overall, the regulation aims to harmonize and leverage standards for better interoperability between public digital infrastructures and services in the EU. The regulation currently has 5 electronic trust services in scope: electronic signatures, electronic seals, electronic time stamps, electronic registered delivery services and website authentication. The regulation differentiates between qualified and non-qualified trust services and trust service providers. A qualified trust service provider providing qualified electronic signatures or qualified digital certificates, for example, must comply with additional requirements in eIDAS regulation151515Article 24 and Annexes II,III,IV, eIDAS regulation..

There are several eIDAS-notified national digital identity schemes with different LoA, allowing for different use cases depending on the required LoA. While eIDAS regulation does not require States to have an eID solution or to notify one, it does require Member States to accept the notified eID schemes161616Article 6, eIDAS regulation. of other EU States for accessing public services if these schemes are of LoA substantial or high.

This cross-border recognition of eID enables EU citizens and residents to access public and private services of other Member States. EU-wide recognition of eIDAS notified solutions started in 2018.

The eIDAS Regulation also addresses personal data processing and protection, stating that it must be carried out in accordance with Directive 95/46/EC, which is now effectively replaced by the GDPR. Supervisory bodies are appointed by Member States to oversee the implementation of the regulation and cooperate with data protection authorities (required by the GDPR).

eIDAS regulation aims to be technology-neutral, leaving Member States free to choose whatever technology they wish, as long as the requirements of the regulation are met.

eIDAS nodes, also known as eIDAS bridges [27], is a technical solution which operate in Member States to ensure interoperability between national infrastructures and to ensure that authentication points in each Member State can recognize and verify presented electronic proofs of identity or identity-related transactions. Projects such as the ESSIF and EBSI are also based on this regulation, which means that eIDAS regulation is a very important legal framework for the European digital market.

According to an evaluation study of the eIDAS regulation published by the European Commission in 2019 [28], only 14% of key public-services are available cross-border via eIDAS notified solutions, while the majority of public service providers do not support cross-boarder authentication. This low performance compared to eIDAS aspirations have lead to the current eIDAS 2.0 discussions that aim to provide a EU digital identity wallet like the one discussed in ESSIF section previously. In matter of fact, eIDAS 2.0 have seen a paradigm shift compared to the previous version. In matter of fact, in 2021 the European Commission have proposed a framework for a European digital identity within eIDAS, based on an identity wallet [29]. This framework will amend eIDAS to eIDAS 2.0. The eIDAS 2.0 will make credential issued from a public authority issuer to holder wallet to have the same legal effects of a qualified certificate of attributes, among others.

4.1.2 The Decree of November’s 8th 2018 (France)

The French national digital identity scheme, FranceConnect, started in 2014 and was regulated in 2018 by the decree of November 8th. FranceConnect is the successor of “Idenum,” a project launched in 2009 with the goal of providing a digital identity infrastructure to facilitate access to online public services. Although Idenum’s initial work saw several organizations (SFR, La Poste ..) partnering, the stakeholders had their own digital identity projects in parallel. These competing solutions led to the failure of the Idenum initiative, especially because of the FranceConnect project that was launched in 2014 and promoted a single national information system to deliver public services based on August 2014 decree, No. 2014-879.

In 2016, the solution went alive, and in November 2018, a decree was published to provide it with a legal background and placing it under the supervison of interministerial digital management DINUM (Direction Interministérielle du NUMérique).

In 2021, FranceConnect was eIDAS-notified as the national identity system of France. In matter of fact, it was notified under the name "FranceConnect+" with La Poste as an identity provider under DINUM to have the LoA substantial.

The decree of 8 November 2018[30] defines the purpose, context, and scope of FranceConnect. The solution is described as a federated identity solution that is used to facilitate access to public services and online services provided by private organizations and to secure data exchange between public administrations. Because it is eIDAS notified, FranceConnect+ also permits users to access digital services in other EU Member States.

The decree also defines the personal data collected and processed for the legitimate operations of FranceConnect. Mandatory data include the last name, first name, date of birth, place of birth, email address, and other identifiers generated by the system. A unique technical alias is obtained from the hash of the personal data and used to de-duplicate identities with reference to the RNIPP. Optional data include the username and cell phone number of the user. Other data are collected for traceability, for example, IP addresses and ports, connection timestamps, and web tokens issued by identity providers.

Furthermore, the categories of data processing, the data controllers in charge of the data processing and the manner in which the data are stored and protected are specified. This includes defining recipients of personal data and for how long personal data can be stored. The text also addresses the right to access and the right to rectification and deletion. By the decree 2021-1538, users can consult and access personal data held by different public administrations. This can be done via a public service called MonFranceConnect (in Beta version so far). FranceConnect must also comply with a broader regulatory context, including the French Act 78-17 supervised by the CNIL (Commission Nationale de l’Informatique et des Libertés - National Commission for Information and Liberties), the GDPR, and the eIDAS regulation. Through the decree of November 8th, the legal aim and finality of FranceConnect, as well as the scope of use, are clearly defined and are intended to set limits of use to be respected by the public administrations. Another notable point is that the decree freezes the identity management model because it specifically references the federated identity solution.

4.1.3 Identity Related Legislation in the UK

Identity related legislation in the UK is a bit complex. For starters, the existence of national identity cards has been a subject of conflict since they were introduced by the Identity Document Act 2006 along with the National Identity Register that contains information about identities. This registry is similar to the French RNIPP discussed above in the comparison between UK Verify and FranceConnect. By 2010, the Act of 2006 was repealed by the Identity Document Act of 2010 that cancels ID cards and forces the destruction of all information recorded in the National Identity Register. UK Verify, started by the Government Digital Services (GDS) as early as 2011, was officially launched in 2016 and eIDAS notified in 2018, in the context of the GDS tasks of provision of online public services. The solution was recognized on a European level, but on the national level, other public authorities had their own solutions going without any attempts to unify the solutions or integrate the UK Verify within them.

The after-phase of UK Verify on the other hand seems more organized and defined: the UK has established the Office for Digital Identities and Attributes (ODIA) in 2022 to supervise security and privacy for digital ID solutions. Moreover, the new Data Protection and Digital Information (No. 2) Bill draft 2023 establishes in its second part "Digital Verification Services" a trust framework171717 Section 47, Data Protection and Digital Information Bill. along with other legal provisions for digital identity solutions. The draft is still in discussion so far, and it is expected to consolidate the existing unrelated political initiatives and systems like "One Login"181818Currently in Beta phase.. This consolidation is expected to come though the Information Gateway191919Section 54, Data Protection and Digital Information Bill. that will allow trusted organizations to verify user’s identity management data against the data held by public authorities. Coupling this with the ODIA and the certification processes for different organizations and digital ID solutions, the UK is getting closer to a national digital identity scheme.

4.1.4 Identity Documents Act (Estonia)

The Identity Documents Act of 1999 made it mandatory for all Estonian residents to have an identity document. Electronic identity documents are just as well accepted as physical documents under this Act. We also note that the Estonian physical ID cards are equipped with a smart chip that contains private keys and can be used for online identification and authentication and even issuance of digital signatures, which means that national identity in Estonia is already a mix of the physical and digital components that make up the citizen’s complete identity. The Identity Document Act covers the provisions for the creation of identity documents, both digital and physical, and the personal data to be collected to issue them.

The Ministry of the Interior and the Police and Border Guard Board is responsible for the interpretation and enforcement of the Act. Responsible authorities are left to decide the list of certificates, identification and authentication procedures, the nature of the identity document database, and its governance. Giving executives more freedom to interpret the Act has made the implementation of the digital identity infrastructure and services more flexible. However, the legitimate purpose of the Act is to identify and authenticate Estonian residents, which means that the executive authorities can use the digital identity infrastructure as they see fit, since the use cases of the Act and the derived identity documents are not specified.

The Identity Documents Act does not define the actors, but rather specifies the issuers of identity documents, such as the Police and Border Guard Board (PBGB), as the issuer of ID cards, which is also responsible for the legal identification of applicants and the management of the Identity Documents database. It is also important to mention that another Act, the Electronic Identification and Trust Services for Electronic Transactions Act, is more detailed and specific in defining ecosystem actors and trust lists, as well as policies for electronic identification and other electronic trust services such as digital signatures and seals.

Estonia is one of the most advanced countries in terms of experience with digital identity management, and beyond that, the digitization practices of public services. However, several major incidents have been reported in relation to Estonian digital identity solutions. Most significant is the 2017 Infineon incident, for which security flaws were detected in the chips of approximately 750,000 ID cards issued between 2014 and 2017 [31] although the chips were subjected to a certification process [32]. This unfortunate experience raises concerns about the security of the digital infrastructure and actors in the digital identity ecosystem in Estonia, especially because the majority of actors are private sector companies.

Finally, the Identity Documents Act does not limit the purpose and scope of digital identity solutions and associated private data, as explained above. Complementary legislation, such as the GDPR, the Estonian Personal Data Protection Act (PDPA Estonia), The Electronic Identification and Trust Services for Electronic Transactions Act of 2016 and eIDAS regulation, provide more specific legislative guidance regarding the establishment of digital identity documents, the privacy and security of associated personal data, and the governance of the infrastructure and its use cases.

4.1.5 Aadhaar Act (India)

The Targeted Delivery of Financial and Other Subsidies Benefits and Services (Aadhaar) Act was passed in 2016. It defines the legal framework for the Aadhaar identity program as an Act to provide effective, transparent, and targeted financial assistance and other services to individuals residing in India through the assignment of unique identity numbers. This identity program began in 2009 as a project to identify Indian residents.

Its adoption in 2016 was questionable. Indeed, the Aadhaar Act was adopted as a “money bill” as part of the budget presentation, with much criticism as it bypassed the upper house of parliament, since money bills must be passed only by the lower house. The identity project was also disputed in the Supreme Court, as the public authorities pushed for the use of the identifier in multiple use cases, in clear contradiction with the non-mandatory aspect of the Act [33].

Beyond the questionable process of passing the Act, the Aadhaar Act and Aadhaar itself are the subject of much criticism. Even in Indian popular culture, Aadhaar identifiers have been greeted with great caution and scepticism due to the fear of increased government control. This is reflected in the famous example of the movie “aadhaar” released in 2019. Moreover, the Aadhaar identity program, initially presented as optional, is finally made mandatory in practice. Indeed, Aadhaar IDs are required to access multiple subsidies and financial services, which are essential for the poor population. Enrolling a child into school also requires the provision of a child’s Aadhaar ID.

Although the technical solution predates the Act itself, the Aadhaar Act legalizes the personal data collected during the registration and use of the Aadhaar platform. The Act defines the demographic and biometric data required to enroll in the national identity system, including name, date of birth, home address, gender and fingerprint, iris scan, and a photograph (as face recognition is supported by the solution). This personal data are stored in a central database called the Central Identities Data Repository (CIDR) and maintained by the UIDAI.

The Act also defines how registration agencies carry out the enrollment process, which means that it covers what data are to be collected, how, and by whom. During the data collection process, subjects must be informed of how the collected data will be used, with whom it will be shared, and the right they have to access their data and how to access them. India has not yet implemented a data protection legislation, as the proposed 2019 bill has been withdrawn [34]. Although there is another act, the Information Technology Act [35], that addresses some aspects and rules for data processing, it is positive to see that the Aadhaar Act sets rules for consent and user awareness for the national identity system.

The authentication process is also defined in the Act, which means that the legal framework effectively technically limits how the architecture of the solution is designed and how the authentication flow, as well as the registration flow, is realized. This is understandable, since the legislation has given a legal context to a solution that already exists, but it severely limits the solution on the technical side; since then, the legislation must be amended when new changes are introduced or different technological choices are made. In the authentication process, the legislation also specifies that entities requesting the authentication of a user from the UIDAI must obtain user consent and inform the user of the purpose of the authentication, and the services and information the user will obtain after the authentication.

An authentication record, including the authentication time, requesting entity, and authentication response, is maintained by the UIDAI. This ensures a degree of accountability and traceability for the authenticating entities; however, it means that user activity can be easily traced, especially because the Aadhaar identifier is unique and persistent. The demographic and biometric data required for the generation of Aadhaar IDs and deduplication are protected by law. Basic biometric data cannot be shared with any other party for any reason, is classified as “sensitive personal data” and falls under the provisions of the Information Technology Act, 2000 (21 of 2000) [35].

The Act gives UIDAI responsibility for the Aadhaar identity system and assigns operational and security duties to this authority.

4.1.6 National Digital Identity Initiative Singapore

The National Digital Identity (NDI) is considered a digital enabler within the Digital Government Blueprint202020Addendum to Digital Government Blueprint - 47.c (updated in 2020) elaborated by the Government Technology Agency GovTech. The solution Singpass discussed above in the national digital identity solutions section is underpinned by the NDI. GovTech also appointed the National Certification Authority (mentioned when studying Singpass) and Assurity212121https://www.assurity.sg/. The first is responsible for the PKI and certificates behind Singpass, and the second provides different Singpass products like "Login" for onboarding Singpass users with high LoA. So overall, Singpass itself is not the result of a legislation but rather of a Digital Governance plan piloted by the Government Technology Agency of Singapore to provide reliable digital identity for both public and private sector. In terms of governance, the solution is maintained by GovTech and the entities it appoints like Assurity and the National Certification Authority. As for technical requirements and principles about personal data, it is GovTech that specifies those. For example, for private sector integration of Singpass products, technical requirements include the use of X.509 Public Key Certificates with RSA key sizes of 2048 bits and larger, provided by a compatible Certificate Authority222222Can be found here https://api.singpass.gov.sg/library/verify/developers/implementation-technical-requirements. As for personal data collection and processing requirements, the GovTech places personal data related to Singpass under the protection of the Personal Data Protection Act.

4.1.7 Comparing Legal Frameworks

As seen in the previous subsections, different legal frameworks have different legal purposes, requirements, and backgrounds for the solution, as depicted in Table 3. For example, some frameworks define limited use cases for their identity solutions (e.g., India, France), and others leave it open to interpretation by public authorities (e.g., Estonia). Some legal frameworks that contain certain technical specifications that influence how a solution is implemented (e.g., France and India) and others leave it up to the competent public authorities and entities to choose the technologies needed to implement the solution, as long as the legal requirements are met (e.g., Estonia and the eIDAS regulation).

| Legal Framework | Adopted in | Technical solution | Supervisory body | Year | Legal purposes | Technical requirements | Other applicable legislation |

| eIDAS regulation | EU Member States | eIDAS notified solutions1 | European Commission | 2016 | Harmonize digital identity standards and requirements and ensure interoperability between member States | None | GDPR |

| The decree of November’s 8th | France | FranceConnect | DINUM | 2018 | Unify the digital identity infrastructure to simplify online administrative procedures | Federated Identity model | GDPR, Law on IT and Liberties |

| Data Protection and Digital Information Bill2 | UK | Any solution trusted by the ODIA | ODIA | 2023 | Establish a legal framework for digital ID services and verification | None | Data Protection Act |

| Identity Documents Act | Estonia | eID Estonia | PBGB | 1999 | Identifying and authenticating residents | None | GDPR, PDPA Estonia, eIDAS regulation |

| Aadhaar Act | India | Aadhaar | UIDAI | 2016 | Delivery of subsidies and financial aid and services | Centralized authentication process based on a central database CIDR | Information Technology Act |

| National Digital Identity initiative | Singapore | Singpass | GovTech, NCA | 2003 | Provide reliable digital identity services for public and private sector | X509 Certificates, RSA public keys 2048 bits, specific TLS ciphers | Personal Data Protection Act |

-

1

A list of currently eIDAS notified solutions can be found here [36]

-

2

The Bill is still a draft during the writing of this paper.

4.2 Personal Data Protection Legislation

According to the United Nations, 137 countries already have data protection and privacy legislation in 2021. Including countries with a draft of such legislation, 80% of States have such legislation [37]. States without legislation and without any available data about such legislation sum up to 20%, including India that we have studied in previous sections. The definition of personal data and the policies in place to protect them, in addition to the various levels of regulation adoption, vary from State to State.

We explore a few examples of legislation in this subsection: the GDPR and its consequent implementations applied in the EU; the Law on IT and Liberties (1978) in France, the Data Protection Act (2018) and the Data Protection and Digital Information (No. 2) Bill (2023) in the UK, Estonia’s Personal Data Protection Act (2007/2018), The Personal Data Protection Act (2012) of Singapore and the California Consumer Protection Act (CCPA) (2018) as an example of personal data protection legislation in the United States. We compared the legislation based on the definition of personal data, the rights granted to users, the identity of the protected subjects, and the location where the law applies.

4.2.1 General Data Protection Regulation GDPR (EU)

The GDPR was published in the EU’s official journal in 2016 and entered into effect in 2018 replacing the Data Protection Directive 95/46/EC of 1995. The regulation harmonizes data protection laws of EU Member States. It aims to protect individuals in the EU by defining personal data and rules on how data are collected and processed by private and public sector organizations, regardless of whether the organization itself is established in the EU.

The GDPR defines personal data as any information relating directly or indirectly to an identified or identifiable natural person. It defines the legal grounds for personal data processing and collection and cases where the data subject’s consent must be obtained. In matter of fact, GDPR requires personal data controllers and processors to have consent explicitly as a clear affirmation from an informed data subject that agrees to their data being processed232323Article 4-11, GDPR. in multiple cases.

GDPR gives the data subjects multiple rights, such as transparency on the part of the controller/processor of personal data about how data will be processed, by whom and with whom it may be shared, access to consult their collected data and correct it, the right to restrict the processing of the data, or to delete that data. Users also have the right to claim compensation when an organization causes any material or non-material losses because of non-respect of the regulation242424Article 82, GDPR..

For their part, controllers and processors of personal data must comply with the GDPR principles such as fairness and transparency, purpose limitation, data minimization, accuracy, storage limitation and establishing measures to ensure the security, confidentiality, and integrity of personal data252525Article 5, GDPR.. Accountability is also a major principle, as controllers and processors of personal data must demonstrate compliance with the regulation, which legally require organizations to appoint a Data Protection Officer (DPO) if their primary activities include processing sensitive data on a large scale, although they may appoint a DPO voluntarily. The DPO’s role is to ensure that their organization(s) process personal data collected from employees, customers, and other possible data subjects in compliance with the GDPR and, potentially, other national laws dealing with data protection.

GDPR also requires each EU Member State to establish at least one Supervisory Authority to enforce GDPR262626Chapter VI - Article 51, GDPR.. These public independent authorities monitor the application of the regulation, and the application of other legislation derived from GDPR or based on it. In matter of fact, GDPR leaves to Member States certain flexibility in incorporating GDPR principles into their legal systems.

Given the size of the EU, with over 447 million people, and the extraterritorial nature of the GDPR, other States and organizations outside the EU have an interest to have GDPR-compliant legislation to stay in business with the vast European market[38]. Exporting data outside the EU is also possible but only to States with adequate levels of protection272727Article 45, GDPR.. The UK for example kept the GDPR in place after Brexit. Other States such as Canada, Japan, and Argentina have an adequate level of protection. Therefore, transferring data to these States is expressly permitted [39].

As part of the GDPR implementation, financial penalties of up to €20M are applied for non-compliance or incidents such as data breaches. These penalties account for up to 4% of the organization’s annual revenue if they exceed the €20M fine. The GDPR also explicitly requires organizations to report breaches to supervisory authorities within 72 hours of discovery, along with a justification for the delay. In terms of penalties, the GDPR is considered as very strict compared to other laws.

One of the strong aspects of GDPR is user awareness of the regulation, for both organizations that handle user personal data and users themselves. GDPR DPOs ensure the awareness of employees, and for the public, the survey requested by the European Commission about GDPR awareness [40] indicates that around 2/3 of EU residents have heard of the GDPR and 3/4 of them are aware of at least one right guaranteed by the regulation, with 1/3 of them aware of all rights.

4.2.2 Act 78-17 on Data Processing, Data Files and Individual Liberties (France)

The French Act 78-17 came as a response to the Safari affair mentioned above in the section summary of the National digital identity solutions. The attempt to use an unique identifier across public authorities and to inter-connect files held on individuals lead to the creation of a commission to provision measures and legislation to ensure the respect of private data and liberties. This later evolved to the CNIL that was established as an independent administrative authority by the Act 78-17 in the 6th of January 1978. This provided the ground for personal data protection in France. It was updated in 2004 to implement the 95/46/EC directive, and later updated in 2018 in the light of GDPR282828Act 2018-493, 20 June 2018. CNIL is designated as the personal data protection authority in France under GDPR. Act 78-17 and GDPR are complementary, like most EU member State implementations of GDPR on a State level. In matter of fact, GDPR has empowered the CNIL in terms of sanctions and supervision since it gives the possibility to apply harder financial sanctions.

4.2.3 The Data Protection Act and The Data Protection and Digital Information Bill (UK)

The Data Protection Act (DPA) of 2018, also called the UK GDPR, is the UK’s implementation of GDPR. DPA was passed to keep a GDPR-similar data protection legislation after the Brexit referendum of 2016. It retains GDPR notions and principles in the UK legal system with minor amendments for domestic context. In matter of fact, up until the end of 2020, all personal data collected and processed were under GDPR, since GDPR was part of the retained EU laws that were incorporated to the UK legal system by the European Union (Withdrawal) Act 2018292929An Act of the Parliament of the United Kingdom. Also known as the Great Repeal Act.. The DPA in its Part 5 - 114 and 115 - names The Information Commissioner as the UK’s independent supervisory authority responsible of the Act application, as required by the article 51 of GDPR. UK GDPR also have an extra-territorial scope, the same as GDPR.