Bayesian Design Principles for Frequentist Sequential Learning

Abstract

We develop a general theory to optimize the frequentist regret for sequential learning problems, where efficient bandit and reinforcement learning algorithms can be derived from unified Bayesian principles. We propose a novel optimization approach to generate “algorithmic beliefs” at each round, and use Bayesian posteriors to make decisions. The optimization objective to create “algorithmic beliefs,” which we term “Algorithmic Information Ratio,” represents an intrinsic complexity measure that effectively characterizes the frequentist regret of any algorithm. To the best of our knowledge, this is the first systematical approach to make Bayesian-type algorithms prior-free and applicable to adversarial settings, in a generic and optimal manner. Moreover, the algorithms are simple and often efficient to implement. As a major application, we present a novel algorithm for multi-armed bandits that achieves the “best-of-all-worlds” empirical performance in the stochastic, adversarial, and non-stationary environments. And we illustrate how these principles can be used in linear bandits, bandit convex optimization, and reinforcement learning.

1 Introduction

1.1 Background

We address a broad class of sequential learning problems in the presence of partial feedback, which arise in numerous application areas including personalized recommendation (Li et al., 2010), game playing (Silver et al., 2016) and control (Mnih et al., 2015). An agent sequentially chooses among a set of possible decisions to maximize the cumulative reward. By “partial feedback” we mean the agent is only able to observe the feedback of her chosen decision, but does not generally observe what the feedback would be if she had chosen a different decision. For example, in multi-armed bandits (MAB), the agent can only observe the reward of her chosen action, but does not observe the rewards of other actions. In reinforcement learning (RL), the agent is only able to observe her state insofar as the chosen action is concerned, while other possible outcomes are not observed and the underlying state transition dynamics are unknown. In this paper, we present a unified approach that applies to bandit problems, reinforcement learning, and beyond.

The central challenge for sequential learning with partial feedback is to determine the optimal trade-off between exploration and exploitation. That is, the agent needs to try different decisions to learn the environment; at the same time, she wants to focus on “good” decisions that maximize her payoff. There are two basic approaches to study such exploration-exploitation trade-off: frequentist and Bayesian. One of the most celebrated examples of the frequentist approach is the family of Upper Confidence Bound (UCB) algorithms (Lai and Robbins, 1985; Auer et al., 2002a). Here, the agent typically uses sample average or regression to estimate the mean rewards; and she optimizes the upper confidence bounds of the mean rewards to make decisions. Another widely used frequentist algorithm is EXP3 (Auer et al., 2002b) which was designed for adversarial bandits; it uses inverse probability weighting (IPW) to estimate the rewards, and then applies exponential weighting to construct decisions. One of the most celebrated examples of the Bayesian approach is Thompson Sampling (TS) with a pre-specifed, fixed prior (Thompson, 1933). Here, the agent updates the Bayesian posterior at each round to learn the environment, and she uses draws from that posterior to optimize decisions.

The advantage of the frequentist approach is that it does not require a priori knowledge of the environment. However, it heavily depends on a case-by-case analysis exploiting special structure of a particular problem. For example, regression-based approaches can not be easily extended to adversarial problems; and IPW-type estimators are only known for simple rewards/losses such as discrete and linear. The advantage of the Bayesian approach is that Bayesian posterior is a generic and often optimal estimator if the prior is known. However, the Bayesian approach requires knowing the prior at the inception, which may not be accessible in complex or adversarial environments. Moreover, maintaining posteriors is computationally expensive for most priors.

In essence, the frequentist approach requires less information, but is less principled, or more bottom-up. On the other hand, the Bayesian approach is more principled, or top-down, but requires stronger assumptions. In this paper we focus on the following research question:

Can we design principled Bayesian-type algorithms, that are prior-free, computationally efficient, and work well in both stochastic and adversarial/non-stationary environments?

1.2 Contributions

In this paper, we synergize frequentist and Bayesian approaches to successfully answer the above question, through a novel idea that creates “algorithmic beliefs” that are generated sequentially in each round, and uses Bayesian posteriors to make decisions. Our contributions encompass comprehensive theory, novel methodology, and applications thereby. We summarize the main contributions as follows.

Making Bayesian-type algorithms prior-free and applicable to adversarial settings.

To the best of our knowledge, we provide the first approach that allows Bayesian-type algorithms to operate without prior assumptions and hence also be applicable in adversarial settings, in a generic, optimal, and often computationally efficient manner. The regret bounds of our algorithms are no worse than the best theoretical guarantees known in the literature. In addition to its applicability in adversarial/non-stationary environments, our approach offers the advantages of being prior-free and often computationally manageable, which are typically not achievable by traditional Bayesian algorithms, except for simple model classes like discrete (Agrawal and Goyal, 2012) and linear (Agrawal and Goyal, 2013) rewards/losses. It is worth noting that the main ideas underlying our methodology and proofs are quite insightful and can be explained in a succinct manner.

General theory of “Algorithmic Information Ratio” (AIR).

We introduce intrinsic complexity measures that serve as objective functions in order to create “algorithmic beliefs” through round-dependent information. We refer to these measures as “Algorithmic Information Ratio” (AIR) types, including the adaption of “Model-index AIR” (MAIR) in the stochastic setting. Our approach always selects algorithmic beliefs by approximately maximizing AIR, and we show that AIR can bound the frequentist regret of any algorithm. We then show that AIR can be upper bounded by previously known complexity measures such as information ratio (IR) (Russo and Van Roy, 2016) and decision-estimation coefficient (DEC) (Foster et al., 2021). As an immediate consequence, our machinery converts existing regret upper bounds using information ratio and DEC, into simple frequentist algorithms with tight guarantees. And we provide methods and guarantees to approximately maximize AIR.

Novel algorithm for MAB with “best of all worlds” empirical performance.

As a major illustration, we propose a novel algorithm for Bernoulli multi-armed bandits (MAB) that achieves the “best-of-all-worlds” empirical performance in the stochastic, adversarial, and non-stationary environments. This algorithm is quite different from, and performs much better than, the traditional EXP3 algorithm, which has been the default choice for adversarial MAB for decades. At the same time, the algorithm outperforms UCB and is comparable to Thompson Sampling in the stochastic environment. Moreover, it outperforms Thompson Sampling and “clairvoyant” restarted algorithms in non-stationary environments.

Applications to linear bandits, bandit convex optimization, and reinforcement learning.

Our theory can be applied to various settings, including linear and convex bandits, and reinforcement learning, by the principle of approximately maximizing AIR. Specifically, for linear bandits, we derive a modified version of EXP2 based on our framework, which establishes a novel connection between inverse propensity weighting (IPW) and Bayesian posteriors. For bandit convex optimization, we propose the first algorithm that attains the best-known regret (Lattimore, 2020) with a finite running time. Lastly, in reinforcement learning, we provide simple algorithms that match the regret bounds proven in the early work Foster et al. (2021).

Combining estimation and decision-making.

Our approach jointly optimizes the belief of an environment and probability of decision. Most existing algorithms including UCB, EXP3, Estimation-to-Decision (E2D) (Foster et al., 2021), TS, and Information-Directed Sampling (IDS) (Russo and Van Roy, 2014) maintain a different viewpoint that separates algorithm design into a black-box estimation method (sample average, linear regression, IPW, Bayesian posterior…) and a decision-making rule that takes the estimate as an input to an optimization problem. In contrast, by optimizing AIR to generate new beliefs, our algorithm simultaneously deals with estimation and optimization. This viewpoint is quite powerful and broadens the general scope of bandit algorithms.

1.3 Related literature

The literature in the broad area of our research is vast. To maintain a streamlined and concise presentation, we focus solely on the most relevant works. Russo and Van Roy (2016, 2014) propose the concept of “information ratio” (IR) to analyze and design Bayesian bandit algorithms. Their work studies Bayesian regret with a known prior rather than the frequentist regret. Lattimore and Gyorgy (2021) proposes an algorithm called “Exploration by Optimization (EBO),” which is the first general frequentist algorithm that optimally bounds the frequentist regret of bandit problems and partial monitoring using information ratio. However, the EBO algorithm is more of a conceptual construct as it requires intractable optimization over the complete class of “functional estimators,” and hence may not be implementable in most settings of interest. Our algorithms are inspired by EBO, but are simpler in structure and run in decision and model spaces (rather than intractable functional spaces). In particular, our approach advances EBO by employing explicit construction of estimators, offering flexibility in selecting updating rules, and providing thorough design and computation guidelines that come with provable guarantees. Our work also builds upon the line of research initiated by Foster et al. (2021), which introduces the concept of the “decision-estimation coefficient” (DEC) as a general complexity measure for bandit and RL problems. Remarkably, DEC not only provides sufficient conditions but also offers the first necessary characterization (lower bounds) for interactive decision making, akin to the VC dimension and the Rademacher complexity in statistical learning. It is important to note that while DEC is tight for one part of the regret, as demonstrated in Foster et al. (2021) and Foster et al. (2023), the remaining “estimation complexity” term in the regret bound can be sub-optimal when the model class is large. The proposed E2D algorithm in Foster et al. (2021) separates the black-box estimation method from the decision-making rule. For this reason, E2D is often unable to achieve optimal regret, even for multi-armed bandits, when the size of the model class is redundant in terms of estimation complexity. Moreover, E2D only works for stochastic environments. Foster et al. (2021) also provides an adaptation of EBO from Lattimore and Gyorgy (2021) to improve estimation complexity, and the subsequent work Foster et al. (2022b) extends the theory of DEC to adversarial environments by adapting EBO. However, as adaptations of EBO, these algorithms present computational challenges, as discussed earlier.

2 Preliminaries and definition of AIR

2.1 Problem formulation

To state our results in the broadest manner, we adopt the general formulation of Adversarial Decision Making with Structured Observation (Adversarial DMSO). This setting extends the original Adversarial DMSO setup introduced in Foster et al. (2022b) by incorporating adversarial partial monitoring, where the reward may not be directly observable. The setting covers broad problems including bandit problems, reinforcement learning, partial monitoring, and beyond. For a locally compact metric space we denote by the set of Borel probability measures on that space. Let be a compact decision space. Let be a compact model class where each model is a mapping from the decision space to a locally compact observation space . A problem instance in this protocol can be described by the decision space and the model class . We define the mean reward function associated with model by .

Consider a round game played by a randomized player in an adversarial environment. At each round , the agent determines a probability over the decisions, and the environment selects a model . Then the decision is sampled and an observation is revealed to the agent. An admissible algorithm ALG can be described by a sequence of mappings where the th mapping maps the past decision and observation sequence to a probability over decisions. Throughout the paper we denote as the filtration where is the algebra generated by random variables , and use the notations for conditional expectation starting round .

The frequentist regret of the algorithm ALG against the usual target of single best decision in hindsight is defined as

where the expectation is taken with respect to the randomness in decisions and observations. There is a large literature that focuses on the so-called stochastic environment, where for all rounds, and the single best decision is the natural oracle. Regret bounds for adversarial sequential learning problems naturally apply to stochastic problems. We illustrate how the general formulation covers bandit problems, and leave the discussion of reinforcement learning to Section 7.

Example 1 (Bernoulli multi-armed bandits (MAB)).

We illustrate how the general formulation reduces to the basic MAB problem with Bernoulli reward. Let be a finite set of actions, and be the set of all possible mappings from to . Take as the induced model class, where each maps into the Bernoulli distribution . The mean reward function for model is itself. At each round , the environment selects a mean reward function , and the observation is the incurred reward .

Example 2 (Structured bandits).

We consider bandit problems with general structure of the mean reward function. Let be a dimensional action set, and be a function class that encodes the structure of the mean reward function. Take as the induced model class, where each maps to the Bernoulli distribution . The mean reward function for model is itself. For example, in dimensional linear bandits, the mean reward function is parametrized by some such that . And in bandit convex optimization, the mean reward (or loss) function class is the set of all concave (or convex) mappings from to .

2.2 Algorithmic Information Ratio

Let be a probability measure of the joint random variable , and be a distribution of another independent random variable . Given a probability measure , let

be the marginal distribution of . Viewing as a prior belief over , we define as the Bayesian posterior belief conditioned on the decision being and the observation (generated from the distribution ) being ; and we define the marginal posterior belief of conditioned on and as

where the subscript in is an index notation, whereas and in are random variables. For two probability measures and on a measurable space, the Kullback-Leibler (KL) divergence between and is defined by if the measure is absolutely continuous with respect to the measure , and otherwise.

Now we introduce a central definition in this paper—Algorithmic Information Ratio (AIR).

Definition 2.1 (Algorithmic Information Ratio).

Given a reference probability and learning rate , we define the “Algorithmic Information Ratio” (AIR) for probability of and belief of as

where the expectation is taken with .

The term “Algorithmic Information Ratio” was used to highlight the key difference between AIR and classical information ratio (IR) measures (to be presented shortly in (2.1)). Firstly, AIR incorporate a reference probability in its definition, while classical IR does not. This additional flexibility makes AIR useful for algorithm design and analysis. Secondly, AIR is defined in an offset form, whereas IR is defined in a ratio form. We choose the word “algorithmic” because AIR is particularly suited to designing constructive and efficient frequentist algorithms; we remain the term “ratio” as it is consistent with previous literature on the topic. The formulation of AIR is inspired by the optimization objectives in recent works Lattimore and Gyorgy (2021) on EBO and Foster et al. (2021) on DEC. There are various equivalences between different variants of AIR, DEC, EBO, and IR when considering minimax algorithms, worst-case environments, and choosing the appropriate index, divergence, and formulation (see the next two subsections for details). However, AIR crucially focuses on “algorithmic belief” rather than maximizing with respect to the worst-case deterministic model, providing algorithmic unity, interpretability, and flexibility.

Note that AIR is linear with respect to and concave with respect to , as conditional entropy is always concave with respect to the joint probability measure (see Lemma D.1). By the generalized Pythagorean theorem (Lemma D.7) for the KL divergence and the fact about posterior , we have the equality . Thus it will be illustrative to write AIR as the sum of three items:

where: the “expected regret” measures the difficulty of exploitation; the “information gain” is the amount of information gained about the marginal distribution of by observing the random variables and , and this in fact measures the degree of exploration; and the last “regularization” term forces the marginal distribution of to be “close” to the reference probability distribution . By maximizing AIR, we generate an “algorithmic belief” that simulates the worst-case environment. This algorithmic belief will automatically balance exploration and exploitation, as well as being close to the chosen reference belief (e.g., a standard reference is the posterior from previous round, as used in traditional Thompson Sampling).

2.3 Bounding AIR by IR and DEC

Notably, our framework allows for the utilization of essential all existing upper bounds for information ratio and DEC in practical applications, enabling the derivation of the sharpest regret bounds known, along with the development of constructive algorithms. In this subsection we demonstrate that AIR can be upper bounded by IR and DEC.

We present here the traditional definition of Bayesian information ratio (Russo and Van Roy, 2016). See Russo and Van Roy (2016, 2014); Lattimore and Szepesvári (2019, 2020); Hao and Lattimore (2022) for upper bounds of IR in bandit problems and structured RL problems.

Definition 2.2 (Information ratio).

Given belief of and decision probability of , the information ratio is defined as

| (2.1) |

Note that the traditional information ratio (2.1) does not involve any reference probability distribution (unlike AIR). By completing the square, it is easy to show that AIR can always be bounded by IR as follows.

Lemma 2.3 (Bounding AIR by IR).

For any , , belief , and , we have

The recent paper Foster et al. (2021) introduced the complexity measure DEC, with the aim of unifying bandits and many reinforcement learning problems of interest.

Definition 2.4 (Decision-estimation coefficient).

Given a model class , a nominal model and , we define the decision-estimation coefficient by

where is the squared Hellinger distance between two probability measures. And we define

| (2.2) |

DEC offers a unifying perspective on various existing structural conditions in the literature concerning RL. For comprehensive explanations on how DEC relates to and subsumes these structural conditions, such as Bellman rank (Jiang et al., 2017), Witness rank (Sun et al., 2019), (Bellman-) Eluder dimension (Russo and Van Roy, 2013; Wang et al., 2020; Jin et al., 2021), bilinear classes (Du et al., 2021), and linear function approximation (Dean et al., 2020; Yang and Wang, 2019; Jin et al., 2020), we encourage readers to consult Section 1 and Section 7 in Foster et al. (2021) and the references therein. Moreover, a slightly strengthened version of DEC, defined through the KL divergence instead of the squared Hellinger divergence,

can be upper bounded by the traditional information ratio. This result follows from Proposition 9.1 in Foster et al. (2021). Note that the convex hull feasible region for the reference model in the notation (2.2) is fundamental because the convex hull also appears in the lower bound, see the discussions in Foster et al. (2023) and Section 3.5.1 in Foster et al. (2021) for details.

We demonstrate in the following lemma that the worst-case value of AIR, when employing a “maximin” strategy for selecting , is equivalent to the KL version of DEC applied to the convex hull of the model class (see below). Consequently, it is bounded by the standard version of DEC using the squared Hellinger distance.

Lemma 2.5 (Bounding AIR by DEC).

Given model class and , we have

| (2.3) |

To prove Lemma 2.5, we can start by noting that the left-hand side of (2.3) is equivalent to the “parametric information ratio,” defined as

| (2.4) |

which was introduced in Foster et al. (2022b). This equivalence can be shown by using the concavity of AIR to exchange over and over . Furthermore, the equivalence between (2.4) and has been established by Theorem 3.1 in Foster et al. (2022b). Therefore, we obtain a proof of Lemma 2.5.

We conclude that AIR is the tightest complexity measure in the adversarial setting, with its maximin value equivalent with the EBO objective in Lattimore and Gyorgy (2021), the KL version of DEC, and the offset version of IR (2.4). Such tightness is established by Lemma 2.5 and the lower bounds in Foster et al. (2022b). However, for reinforcement learning problems in the stochastic setting, it is often desirable to remove the convex hull on the right-hand side of (2.3). To this end, we introduce a tighter version of AIR, called “Model-index AIR” (MAIR), which is upper bounded by the original version of DEC using model class rather than its convex hull (see Lemma 2.8 in the next subsection), and allows us to apply essentially all existing regret upper bounds using DEC to our framework.

2.4 Model-index AIR (MAIR) and DEC

Denote decision be the induced optimal decision of model . In the stochastic environment, where for all rounds, the benchmark policy in the definition of regret is the natural oracle . Unlike the adversarial setting, where algorithmic beliefs are formed over pairs of models and optimal decisions, in the stochastic setting, we only need to search for algorithmic beliefs regarding the underlying model. This distinction allows us to develop a strengthened version of AIR, which we call “Model-index AIR” (MAIR), particularly suited for studying reinforcement learning problems.

Definition 2.6 (Model-index AIR).

Denote be a reference distribution of models, and be a prior belief of models, we define the “Model-index Algorithmic Information Ratio” as

where is the Bayesian posterior belief of models induced by the prior belief .

By the data processing inequality (Lemma D.9), KL divergence between two model distributions will be no smaller than KL divergence between the two induced decision distributions. Thus we have the following Lemma.

Lemma 2.7 (Relationship of MAIR and AIR).

When is the decision distribution of induced by the model distribution , and is the distribution of induced by the model distribution , we have

Lemma 2.5 has shown that the worst-case value of AIR under the “maximin” strategy is smaller than DEC of the convex hull of . Now we demonstrate that the worst-case value of MAIR under a “maximin” strategy is smaller than DEC of the original model class , which does not use the convex hull in its argument. In fact, there is an exact equivalence between the worst-case value of MAIR and the KL version of DEC, as is the case in Lemma 2.5 for AIR.

Lemma 2.8 (Bounding MAIR by DEC).

Given model class and , we have

We conclude that lemma 2.8 enables our approach to match the tightest known regret upper bounds using DEC, and the tightness of MAIR follows from the lower bounds of DEC in Foster et al. (2021). In Section 7, we discuss how to derive principled algorithms using MAIR and application to reinforcement learning. In Section 7.1, we also discuss how the pursuit of MAIR comes at the cost of larger estimation complexity, explaining the trade-off between AIR and MAIR.

3 Algorithms

In this section we focus on the adversarial setting and leverage AIR to analyze regret and design algorithms. All the results are extended to leverage MAIR in the stochastic setting in Section 7. For the comparison between AIR and MAIR, we refer to the ending paragraphs of Section 3.3 and Section 7.1 for detailed discussion.

3.1 A generic regret bound leveraging AIR

Given an arbitrary admissible algorithm ALG (defined in Section 2.1), we can generate a sequence of algorithmic beliefs and a corresponding sequence of reference probabilities in a sequential manner as shown in Algorithm 1.

Input algorithm ALG and learning rate .

Initialize to be the uniform distribution over .

Maximizing AIR to create algorithmic beliefs is an alternative approach to traditional estimation procedures, as the resulting algorithmic beliefs will simulate the true or worst-case environment. In particular, this approach only stores a single distribution at round , which is the Bayesian posterior obtained from belief and observations , and it is made to forget all the rest information from the past. We should note that all values in the sequence will reside within the interior of . This is due to the fact that the (negative) AIR is a Legendre function concerning the marginal distribution .333We refer to Definition D.4 and Lemma D.5 for more details regarding the property that for all . Furthermore, it is worth emphasizing that AIR (and the negative KL divergence term) can be appropriately defined as negative infinity () when the reference probability resides on the boundary of and is not absolutely continuous with respect to . This is a direct result of the well-defined nature of the KL divergence. Such simple extension can provide an alternative solution to address any concerns related to boundary issues that may arise in the paper.

Based on these algorithmic beliefs, we can provide regret bound for an arbitrary algorithm. Here we assume to be finite (but potentially large) for simplicity; this assumption can be relaxed using standard discretization and covering arguments.

Theorem 3.1 (Generic regret bound for arbitrary learning algorithm).

Given a finite decision space , a compact model class , the regret of an arbitrary learning algorithm ALG is bounded as follows, for all ,

| (3.1) |

Note that Theorem 3.1 provides a powerful tool to study the regret of an arbitrary algorithm using the concept of AIR. Furthermore, it suggests that the algorithm should choose decision with probability according to the posterior . Building on this principle to generate algorithmic beliefs, we provide two concrete algorithms: “Adaptive Posterior Sampling” (APS) and “Adaptive Minimax Sampling” (AMS). Surprisingly, their regret bounds are as sharp as the best known regret bounds of existing Bayesian algorithms that require knowledge of a well-specified prior. An analogy of the theorem leveraging MAIR in the stochastic setting is presented as Theorem 7.1.

3.2 Adaptive Posterior Sampling (APS)

When the agent always selects to be equal to the posterior , and optimizes for algorithmic beliefs as in Algorithm 1, we call the resulting algorithm “Adaptive Posterior Sampling” (APS).

Input learning rate .

Initialize .

At round , APS inputs to the objective to optimize for the algorithmic belief ; and it sets to be the Bayesian posterior obtained from belief and observations . Unlike traditional TS, APS does not require knowing the prior or stochastic environment; instead, APS creates algorithmic beliefs “on the fly” to simulate the worst-case environment. We can prove the following theorem using the regret bound (3.1) in Theorem 3.1, and the upper bounds of AIR by IR and DEC established in Section 2.3.

Theorem 3.2 (Regret of APS).

Assume that for all and . The regret of Algorithm 2 with and all is bounded by

where is the maximal value of information ratio444For technical reason we use the squared Hellinger distance to define (instead of KL as in the definition (2.1) of IR). There is no essensial difference between the definitions of IR and in practical applications, since all currently known bounds on the information ratio hold for the stronger definition with added absolute constants. See Appendix A.8 for details. for Thompson Sampling. Moreover, the regret of Algorithm 2 with any is bounded as follows, for all

where is DEC of for the Thompson Sampling strategy .

For armed bandits, APS achieves the near-optimal regret because ; for dimensional linear bandits, APS recovers the optimal regret because . See Appendix A.8 for the proof of these information ratio bounds.

The main messages about APS and Theorem 3.2 are: 1) the regret bound of APS is no worse than the standard regret bound of TS (Russo and Van Roy, 2016), but in contrast to the latter, does not rely on any knowledge needed to specify a prior! 2) Because APS only keeps the marginal beliefs of but forgets beliefs of the models, it is robust to adversarial and non-stationary environments. And 3) Experimental results in Section 4 show that APS achieves “best-of-all-worlds” empirical performance for Bernoulli MAB in different environments.

3.3 Adaptive Minimax Sampling (AMS)

When the agent selects decision by solving the minimax problem

and optimizes for algorithmic beliefs as in Algorithm 1, we call the resulting algorithm “Adaptive Minimax Sampling” (AMS).

Input learning rate .

Initialize .

By the regret bound (3.1) in Theorem 3.1 and the upper bounds of AIR by DEC and IR established in Section 2.3, it is straightforward to prove the following theorem.

Theorem 3.3 (Regret of AMS).

Theorem 3.3 shows that the regret bound of AMS is always no worse than that of IDS (Russo and Van Roy, 2014). Algorithm 3 is implicitly equivalent with a much simplified implementation of the EBO algorithm from Lattimore and Gyorgy (2021), but this implementation runs in computationally tractable spaces (rather than intractable functional spaces) and does not require limit analysis. We propose the term “AMS” with the intention of describing the algorithmic idea broadly, encompassing its various variants, including the important one we will discuss shortly, Model-index AMS. Alternatively, the EBO perspective is convenient and essential when one wishes to establish connections with mirror descent and analyze general Bregman divergences, as we do in Appendix A.7.

In Section 7, we develop a model-index version of AMS in the stochastic setting, which we term “Model-index AMS” (MAMS) and introduce as Algorithm 6. Model-index AMS leverage MAIR as the optimization objective in the algorithmic belief generation. The regret of MAMS is always bounded by

| (3.3) |

Compared with the regret bound of AMS in (3.2), the regret bound (3.3) of MAMS uses DEC of the original model class rather than its convex hull ; on the other hand, the estimation complexity term in (3.3) is , which is larger than the term in (3.2). Furthermore, MAMS is only applicable to the stochastic environment, while AMS is applicable to the adversarial environment. We refer to Section 7.1 for a more detailed comparison between AIR and MAIR.

3.4 Using approximate maximizers

In Algorithm 1, we ask for the algorithmic beliefs to maximize AIR. In order to give computationally efficient algorithms in practical applications (MAB, linear bandits, RL, …), we will require the algorithmic beliefs to approximately maximize AIR. This argument is made rigorous in the following theorem, which uses the first-order optimization error of AIR to represent the regret bound.

Theorem 3.4 (Generic regret bound using approximate maximizers).

Given a finite , a compact , an arbitrary algorithm ALG that produces decision probability , and a sequence of beliefs where for all rounds, we have

Thus we give a concrete approach towards systematical algorithms with rigorous guarantees—by minimizing the gradient of AIR, we aim to approximately maximize AIR. This is an important factor upon which we advance the existing literature in EBO and DEC. We not only provide regret guarantees for “minimax algorithm” and “worst-case environment,” but also offer a comprehensive path for designing algorithms by leveraging the key idea of “algorithmic beliefs.” An analogy of this theorem leveraging MAIR in the stochastic setting is presented as Theorem 7.1 in Section 7.

4 Application to Bernoulli MAB

Our Bayesian design principles give rise to a novel algorithm for the Bernoulli multi-armed bandits (MAB) problem. It is well-known that every bounded-reward MAB problem can equivalently be reduced to the Bernoulli MAB problem, so our algorithm and experimental results actually apply to all bounded-reward MAB problems. The reduction is very simple: assuming the rewards are always bounded in , then after receiving at each round, the agent re-samples a binary reward so that .

4.1 Simplified APS for Bernoulli MAB

In Example 1, is a set of actions, and each model is a mapping from actions to Bernoulli distributions. Given belief , we introduce the following parameterization: ,

| (conditional mean reward) | ||||

| (marginal belief) | ||||

| (guarantees concavity) |

Then we have a concave parameterization of AIR by the dimensional vector :

where for all . By setting the gradients of AIR with respect to all coordinates in to be exactly zero, and choosing (which results in the gradient of AIR with respect to being suitably bounded), we are able to write down a simplified APS algorithm in closed form (see Algorithm 4). We apply Theorem 3.4 to show that the algorithm achieves optimal regret in the general adversarial setting.

Theorem 4.1 (Regret of Simplified APS for Bernoulli MAB).

The regret of Algorithm 4 with and is bounded by

Input learning rate .

Initialize .

At each round, Algorithm 4 increases the weight of the selected action if , and decreases the weight if . The algorithm also maintains the “relative weight” between all unchosen actions , allocating probabilities to these actions proportionally to . Algorithm 4 is clearly very different from the well-known EXP3 algorithm, which instead updates by the formula

In Section 6.2 we recover a modified version of EXP3 by Bayesian principle assuming the reward distribution is exponential or Gaussian. We conclude that Algorithm 2 uses a precise posterior for Bernoulli reward, while EXP3 estimates worst-case exponential or Gaussian reward. This may explain why Algorithm 4 performs much better in all of our experiments.

Reflection symmetry and mirror map:

We would like to highlight a notable property of our new algorithm: Algorithm 4 exhibits reflection symmetry (or reflection invariance), signifying that when we interchange the roles of reward and loss, the algorithm remains unchanged. The theoretical convergence of our algorithm is not contingent on any truncation. On the contrary, the traditional IPW estimator does not exhibit this property: the reward-based IPW and the loss-based IPW yield distinct algorithms. While the expected regret convergence of EXP3 with the loss-based estimator does not necessitate truncation, EXP3 with the reward-based estimator mandates truncation for convergence. (The original EXP3 algorithm from Auer et al. (2002b) is reward-based; we refer to §11.4 in Lattimore and Szepesvári (2020) for loss-based EXP3.)

We would also like to comment on the relationship between Algorithm 4 and mirror descent. Algorithm 4 is equivalent to running mirror descent (specifically exponential weight here) using the reward estimator:

| (4.1) |

From this perspective, Algorithm 4 can be understood as addressing a long-standing question: how to fix the issue of exploding variance in the IPW estimator and automatically find the optimal bias-variance trade-off. It is worth noting that the derivation of our algorithms reveals a deep connection between frequentist estimators and the natural parameters of exponential family distributions (see Appendix B.6 for details). We hope this framework can be applied to challenging problems where a more robust estimator than IPW is required, such as bandit convex optimization (Bubeck et al., 2017) and efficient linear bandits (Abernethy et al., 2008).

4.2 Numerical experiments

We implement Algorithm 4 (with the legend “APS” in the figures) and compare it with other algorithms across the stochastic, adversarial and non-stationary environments (code available here). We plot expected regret (average of 100 runs) for different choices of , and set a forced exploration rate in all experiments. We find APS 1) outperforms UCB and matches TS in the stochastic environment; 2) outperforms EXP3 in the adversarial environment; and 3) outperforms EXP3 and is comparable to the “clairvoyant” benchmarks (that have prior knowledge of the changes) in the non-stationary environment. For this reason we say Algorithm 4 (APS) achieves the “best-of-all-worlds” performance. We note that the optimized choice of in APS differ instance by instance, but by an initial tuning we typically see good results, whether we tune optimally or not optimally.

4.2.1 Stochastic Bernoulli MAB

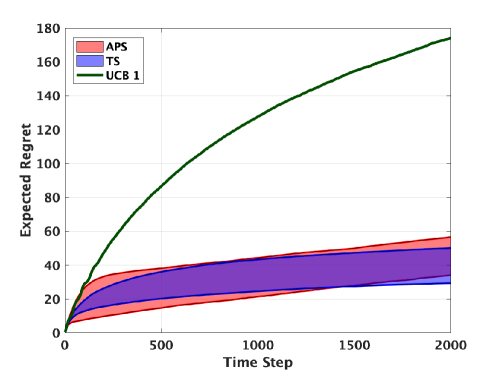

In Figure 1 we report the expected regret for APS with different choices of , TS with different Beta priors, and the UCB 1 algorithm, in a stochastic 16-armed Bernoulli bandit problem. We refer to this as “sensitivity analysis” because the red, semi-transparent, area reports the regret of APS when learning rates are chosen across a range of values drawn from the interval (the interval is specified by an initial tuning); and the priors of TS are chosen from Beta where . In particular, the bottom curve of the red (or blue) area is the regret curve of APS (or TS) using optimally tuned (respectively, prior). The conclusion is that APS outperforms UCB 1, and is comparable to TS in this stochastic environment.

4.2.2 Adversarial Bernoulli MAB

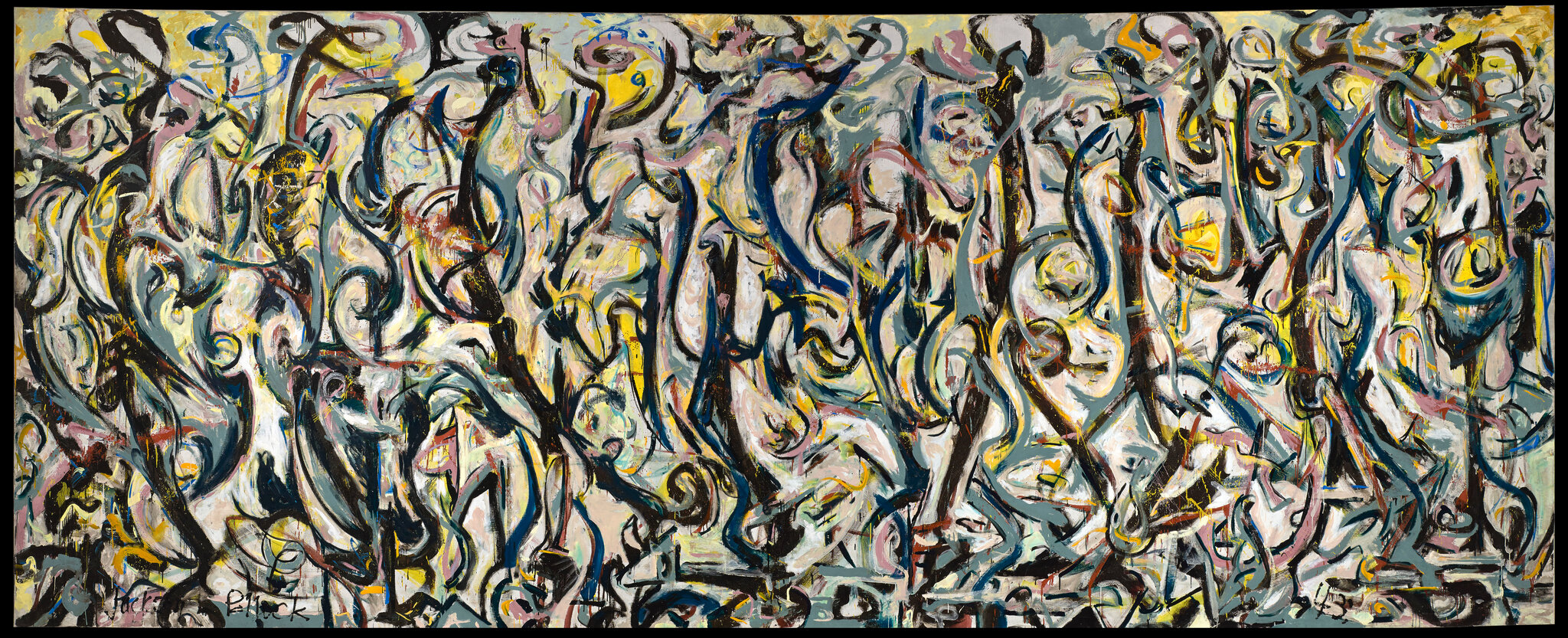

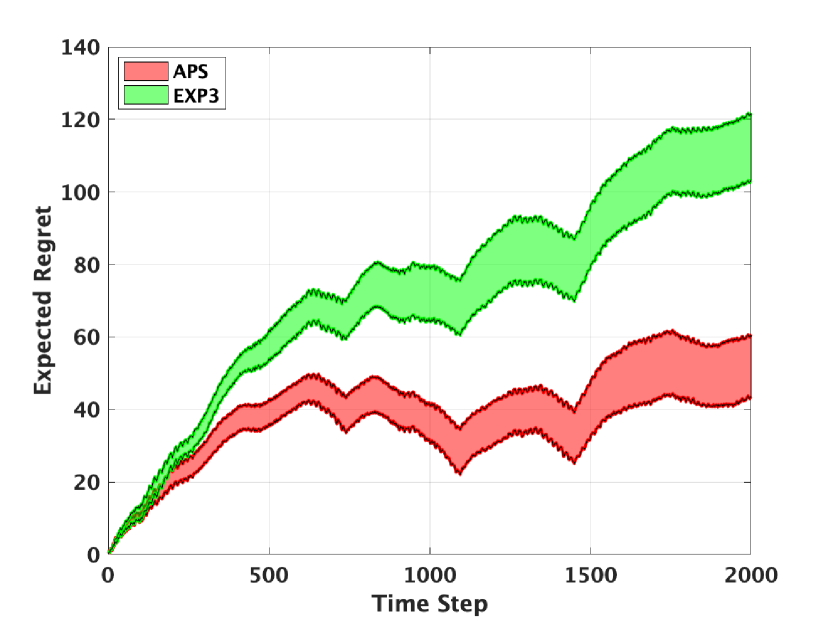

We equidistantly take 16 horizontal lines from an abstract art piece by Jackson Pollock to simulate the rewards (pre-specified) in an adversarial environment, and study this via a 16-armed bandit problem. To be more specific, we transform these 16 horizontal lines into grayscale values, resulting in each line becoming a sequence of 2000 values in the range [0, 1]. As depicted in Figure 3, it’s evident that the environment is inherently adversarial and lacks any statistical regularity. This is further confirmed by empirical findings that the best-in-hindsight arm changes over time. Figure 3 shows the sensitivity analysis for APS and EXP3 when both the learning rates are chosen from (the interval is specified by an initial tuning). In particular, the red and green lower curves compare the optimally tuned versions of APS and EXP3. The conclusion is that APS outperforms EXP3 whether is tuned optimally or not.

4.2.3 Non-stationary Bernoulli MAB (with change points)

“change points” environment.

restarted algorithms in a “change points”

environment.

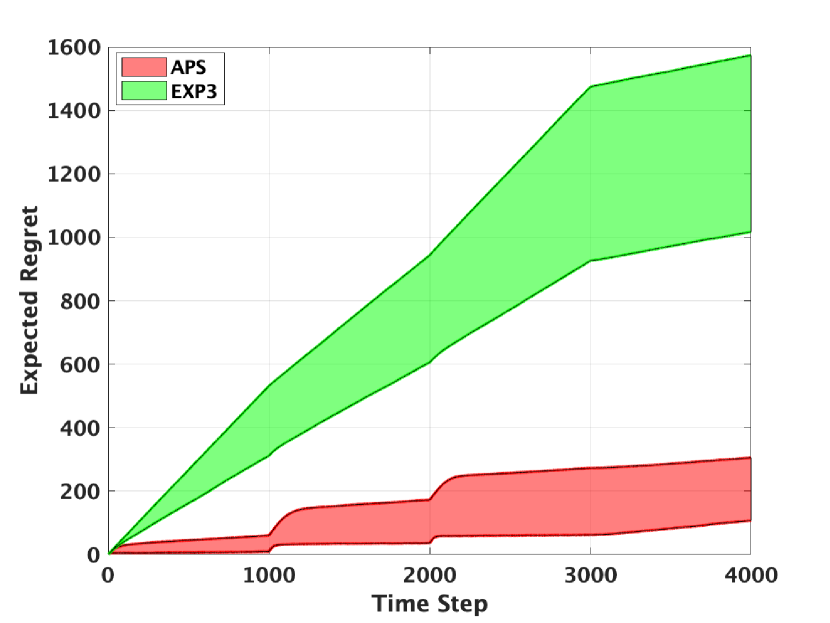

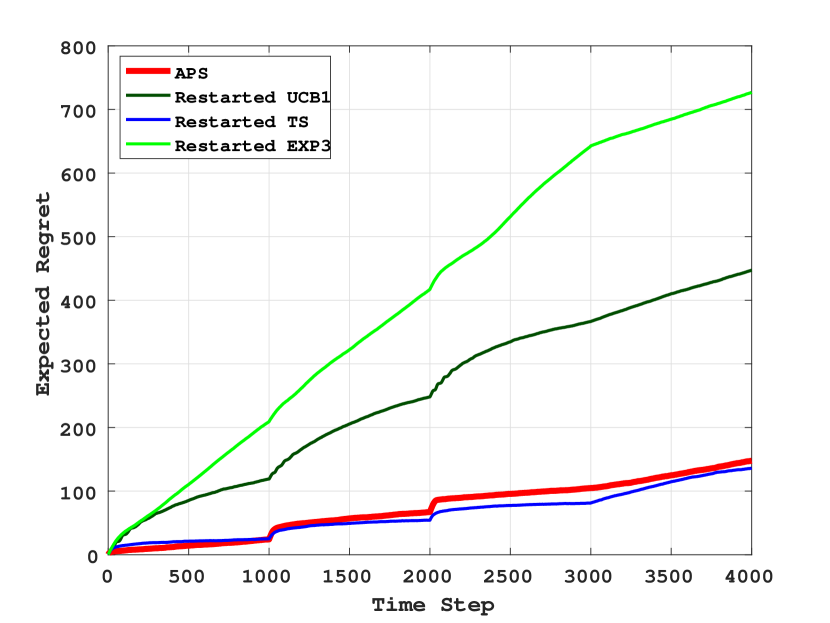

We study a 16-armed Bernoulli bandit problem in a non-stationary environment. We generate 4 batches of i.i.d. sequences, where the changes in the environment occur after round 1000, round 2000, and round 3000. We consider a stronger notion of regret known as the dynamic regret (Besbes et al., 2014), which compares the cumulative reward of an algorithm to the cumulative reward of the best non-stationary policy (rather than a single arm) in hindsight. In this particular setting, the benchmark is to select the best arm in all the 4 batches. In Figure 5 we perform sensitivity analysis for APS and EXP3, where the learning rates are chosen across . Since the agent will not know when and how the adversarial environment changes in general, it is most reasonable to compare APS with EXP3 without any knowledge of the environment as in Figure 5. We observe that APS dramatically improves the dynamic regret by several times.

In Figure 5, we compare APS to three “clairvoyant” restarted algorithms, which require knowing that the environment consists of 4 batches of i.i.d. sequences, as well as knowing the exact change points. We tune the parameters in these algorithms optimally. Without knowledge of the environment, APS performs better than restarted EXP3 and restarted UCB 1, and is comparable to restarted TS. (It is important to emphasize again that the latter algorithms are restarted based on foreknowledge of the change points.)

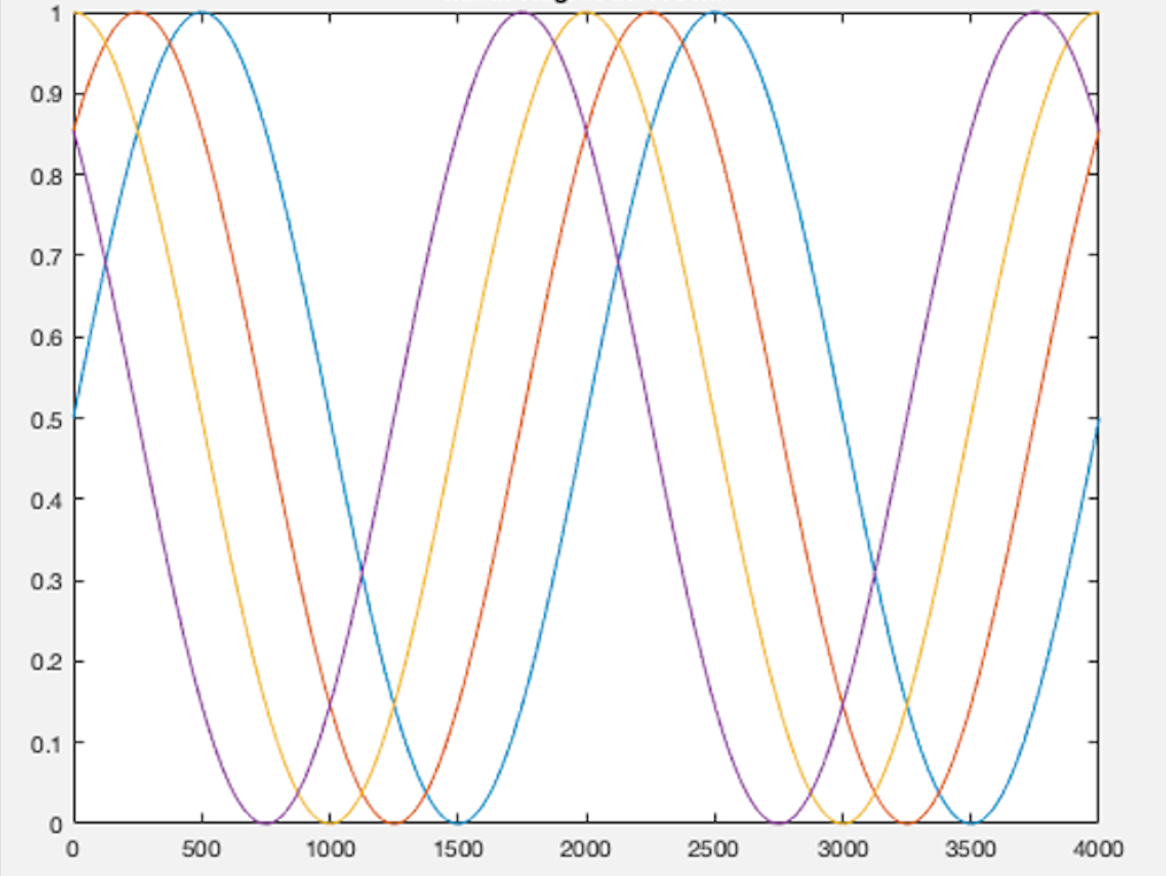

4.2.4 Non-stationary Bernoulli MAB (with “sine curve” reward sequences)

for 4 arms.

environment.

in a “sine curve” environment.

in a “sine curve” environment.

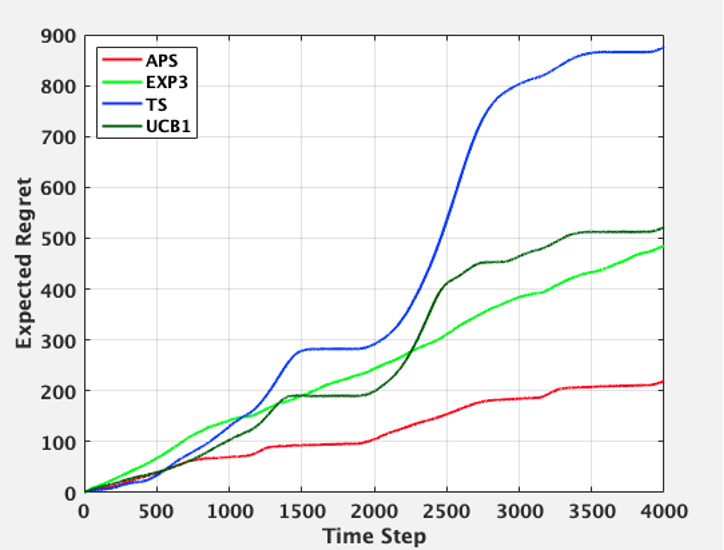

We generate a 4-armed bandit problem with the mean-reward structure shown in Figure 7. The four sine curves (with different colors) in Figure 7 represent the mean reward sequences of the 4 arms. We tune the parameters in all the algorithms to optimal and report their regret curves in Figure 7. As shown in Figure 7, APS achieves the best performance, while TS fails in this non-stationary environment. This experiment shows the vulnerability of TS if the environment is not stationary, such as the sine curve structure shown here.

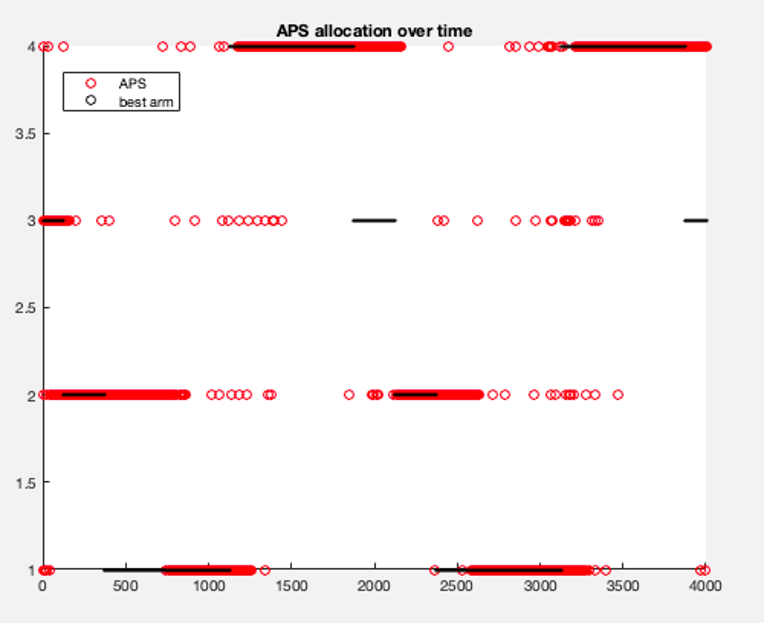

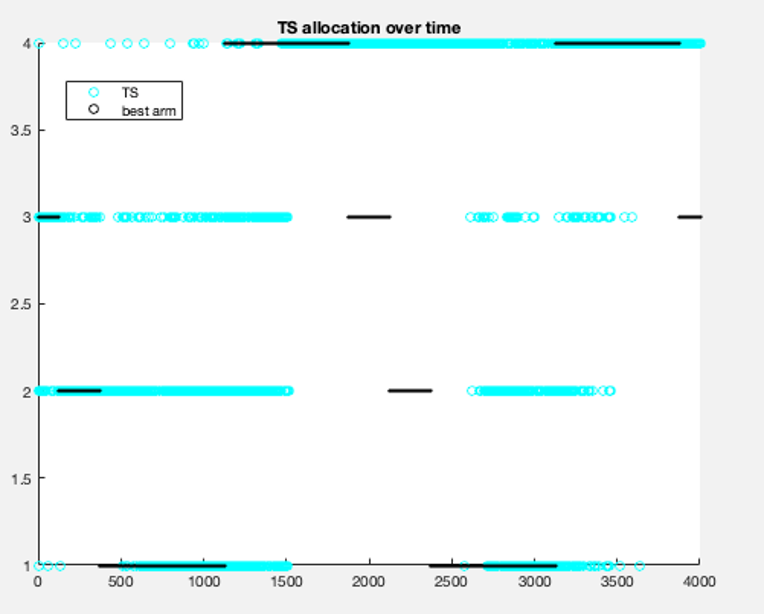

To better illustrate the smartness of APS compared with TS in the non-stationary environment, we track the selected arms and the best arms throughout the process. In Figure 9 and Figure 9, the horizontal line represents the 4000 rounds, and the vertical lines represent the 4 arms (indexed as 1, 2, 3, and 4). In Figure 9, the red points show the selected arms of APS, and the black points represent the best arms at each round in this “sine curve” non-stationary environment. In Figure 9, the blue points show the selected arms of TS. The more consistent the selected arms are with the best arms (black points), the better choices an algorithm makes. Comparing Figure 9 and Figure 9, we can see that APS is highly responsive to changes in the best arm, whereas TS is relatively sluggish in this regard. The implication of this experiment is that creating a new algorithmic belief at each round has the potential to significantly improve performance and be a game changer in many problem settings.

We conclude that these experiments provide some numerical evidence indicating that APS achieves the “best-of-all-worlds” across stochastic, adversarial, and non-stationary environments.

5 Key intuition and underlying theory

It is worth noting that the proofs of Theorem 3.1 and its generalizations are quite insightful and parsimonious. The two major steps in the proofs may be interesting on its own. The first step is a succinct analysis to bound the cumulative regret by sum of AIR (see Section 5.1); and the second step is to extend the classical minimax theory of “exchanging values” into a constructive approach to design minimax decisions (estimators, algorithms, etc.), which will be presented in Section 5.2. At the end, we also illustrate how such analysis generalizes to approximate algorithmic beliefs, as presented in Theorem 3.4 and Theorem 7.1.

5.1 Bounding regret by sum of AIR

For every , we have

| (5.1) |

Taking as in Algorithm 1, and taking conditional expectation on the left hand side of (5.1), we have

| (5.2) |

where the conditional expectation notation is introduced in Section 2.1. By subtracting the additive elements on the left-hand side of (5.2) (divided by ) from the per-round regrets against , we obtain

| (5.3) |

where the inequality is by taking supremum at each rounds; and the last equality in (5.3) is by Lemma 5.2, an important identity to be explained in Section 5.2, which is derived from the fact that the pair of maximizer and posterior functional is a Nash equilibrium of a convex-concave function. We note that the second-to-last formula is true without imposing any restrictions on ; only the last formula relies on the fact that maximizes AIR.

5.2 Duality theory: from value to construction

Consider a decision space , a space of the adversary’s outcome, and a convex-concave function defined in . The classical minimax theorem (Sion, 1958) says that, under regularity conditions, the minimax and maximin values of are equal:

We refer to as the set of “minimax decisions,” as they are optimal in the worst-case scenario. And we say is “maximin decision” if is “maximin adversary’s outcome.” One natural and important question is, when will the “maximin decision” also be a “minimax decision?” Making use of strong convexity, we extends the classical minimax theorem for values into the following theorem for constructive minimax solutions:

Lemma 5.1 (A constructive minimax theorem for minimax solutions).

Let and be convex and compact sets, and a function which for all is strongly convex and continuous in and for all is concave and continuous in . For each , let be the corresponding unique minimizer. Then, by maximizing the concave objective

we can establish that is a minimax solution of and is a Nash equilibrium.

The above lemma, although straightforward to prove through the classical minimax theorem, is conceptually interesting because it emphasizes the significance of strong convexity (often achieved through regularization). This strong convexity allows us to obtain “minimax solutions” by considering a “worst-case adversary” scenario, such as the least favorable Bayesian prior. This approach simplifies the construction of minimax estimators in classical decision theory, moving away from the need to consider “least favorable prior sequence” and specific losses by imposing regularization.

Applying Lemma 5.1 to our framework, we can show: 1) Bayesian posterior is the optimal functional to make decision under belief ; and 2) by choosing worst-case belief , we construct a Nash equilibrium. As a result, we can establish the following per-round identity, which leads to the key identity denoted as in (5.3). This identity plays a crucial role in the proof of Theorem 3.1.

Lemma 5.2 (Identity by Nash equilibrium).

Given , and , denote . Then we have

Furthermore, we establish the following lemma, demonstrating that the role of AIR and its derivatives is generic for any belief selected by the agent and any environment specified by nature. Recall that the second-to-last formula in (5.3) holds without imposing any restrictions on . Thus, Lemma 5.3 leads us to Theorem 3.4 and Theorem 7.1. This fact is proven through Danskin’s theorem (Bernhard and Rapaport, 1995) (Lemma D.3), which establishes equivalence between the gradient of the optimized objective and the partial derivative at the optimizer. The “identity” nature of Lemma 5.3 indicates that regret analysis using derivatives of AIR can be principled, precise, and reliable for arbitrary algorithmic beliefs (in addition to maximizers) and any type of environment.

Lemma 5.3 (Identity for arbitrary algorithmic belief and any environment).

Given , , and an arbitrary algorithmic belief selected by the agent and an arbitrary environment specified by the nature. Then we have

where is a vector in simplex where all the weights are given to .

In addition to their utility in upper bound analyses, we hope that the duality methodology presented in this section may also offer values for lower bound analyses. Furthermore, the derivation of our bandit and RL algorithms unveils a rich mathematical structure, which we will demonstrate in Appendix B and C for more details.

6 Applications to infinite-armed bandits

Our design principles can be applied in many sequential learning and decision making environments. In order to maximize AIR in practical applications, we parameterize the belief , and make the gradient of AIR with respect to such parameter small. We will present our results for linear bandits and bandit convex optimization in this section and present our results for reinforcement learning in Section 7. We give a high-level overview of the applications to linear bandits and bandit convex optimization here.

Application to linear bandits.

A classical algorithm for adversarial linear bandits (described in Example 2) is the EXP2 algorithm (Dani et al., 2007), which uses IPW for linear reward as a black-box estimation method, and combines it with continuous exponential weight. We derive a modified version of EXP2 from our framework, establishing interesting connection between IPW and Bayesian posteriors.

Application to bandit convex optimization.

Bandit convex optimization (described in Example 2) is a notoriously challenging problem, and much effort has been put to understanding its minimax regret and algorithm design (Bubeck and Eldan, 2016; Bubeck et al., 2017; Lattimore, 2020). The best known result, which is of order , is derived through the non-constructive information-ratio analysis in Lattimore (2020). As a corollary of Theorem 3.3, Adaptive Minimax Sampling (AMS) recovers the best known regret bound with a simple constructive algorithm, which can be computed in time. To the best of our knowledge, this is the first finite-running-time algorithm that attains the best known regret.

6.1 Maximization of AIR for structured bandits

Consider the structured bandit problems described in Example 2. We consider the computation complexity of the optimization problem

| (6.1) |

The computational complexity of (6.1) may be in the worst case as the size of . However, when the mean reward function class is a convex function class, the computational complexity will be which is efficient for armed bandits and is no more than in general (by standard discretization and covering arguments, we may assume to have finite cardinality for the simplicity of theoretical analysis). Moreover, we also give efficient algorithm for linear bandits with exponential-many actions. We refer to Appendix B.1 for the detailed discussion on the parameterization method and computational complexity.

6.2 Application to Gaussian linear bandits

We consider the adversarial linear bandit problem with Gaussian reward. In such a problem, is a convex action set with dimension . The model class can be parameterized by a dimensional vector that satisfies for all . Here we use the notations (as action set), (as action) and (as optimal action) to follow the tradition of literature about linear bandits. The reward for each action is drawn from a Gaussian distribution that has mean and variance . To facilitate the handling of mixture distributions, we introduce the “homogeneous noise” assumption as follows: for all actions , the reward of is denoted as , where is Gaussian noise that is identical across all actions (meaning all actions share the same randomness within the same rounds). This “homogeneous noise” simplifies our expression of AIR, and the resulting algorithms remain applicable to independent noise models and the broader sub-Gaussian setting.

As discussed in Section 6.1, we restrict our attention to sparse where for each there is only one model , which corresponds to the Gaussian distribution . We parameterize the prior by vectors and , where and . Note that AIR in this “homogeneous noise” setting can be expressed as

| (6.2) |

By setting the gradients of (6.2) with respect to to zero and the gradients with respect to to nearly zero, we obtain an approximate maximizer of AIR in (6.2). We calculate the Bayesian posterior, and find that the resulting algorithm is an exponential weight algorithm with a modified IPW estimator: at each round , the agent update by

where is the modified IPW estimator for linear reward,

| (6.3) |

Note that in order to avoid boundary conditions in our derivation, we require forced exploration to ensure . This can be done with the help of the volumetric spanners constructed in Hazan and Karnin (2016). The use of volumetric spanner makes our final proposed algorithm (Algorithm 5) to be slightly more involved, but we only use the volumetric spanner in a “black-box” manner.

Input learning rate , forced exploration rate , and action set .

Initialize .

We highlight that the algorithm is computationally efficient (even more efficient than traditional EXP2), because the reward estimator (6.3) is strongly concave so that one can apply log-concave sampling when executing exponential weighting. The additional “mean zero regularizer” term in (6.3) is ignorable from a regret analysis perspective, so the standard analysis for exponential weight algorithms applies to Algorithm 5 to establish the optimal regret bound. One may also analyze Algorithm 5 within our algorithmic belief framework through Theorem 3.4, as we did for Algorithm 4 in Section B.2; we omit the analysis here. Finally, we note that the algorithm reduces to a modified version of EXP3 for finite armed bandits, a connection we mentioned at the end of Section 4.1.

6.3 Application to bandit convex optimization

We consider the bandit convex optimization problem described in Example 2. In bandit convex optimization, is a dimensional action set whose diameter is bounded by , and the mean reward (or loss) function is required to be concave (respectively, convex) with respect to actions:

The problem is often formed with finite (but exponentially large) action set by standard discretization arguments (Lattimore, 2020). Bandit convex optimization is a notoriously challenging problem, and much effort has been put to understanding its minimax regret and algorithm design. The best known result, which is of order , is derived through the non-constructive information-ratio analysis in Lattimore (2020). By the information ratio upper bound for the non-constructive Bayesian IDS algorithm in Lattimore (2020), Lemma 2.3 that bounds AIR by IR, and Theorem 3.3 (regret of AMS), we immediately have that Algorithm 3 (AMS) with optimally tuned achieves

As a result, AMS recovers the best known regret with a constructive algorithm. By our discussion on the computational complexity in Appendix B.1, AMS solves convex optimization in a -dimensional space, so it can be computed in time for bandit convex optimization. To the best of our knowledge, this is the first algorithm with a finite running time that attains the best known regret. We note that the EBO algorithm in Lattimore and Gyorgy (2021) has given a constructive algorithm that achieves the same regret derived by Bayesian non-constructive analysis. However, EBO operates in an abstract functional space, so it is less clear how to execute the computation.

7 MAIR and application to RL

In the stochastic environment, where for all rounds, we only need to search for algorithmic beliefs regarding the underlying model to determine the best decision . This distinction allows us to introduce a strengthened version of AIR in Section 2.4, which we term “Model-index AIR” (MAIR), particularly suited for studying reinforcement learning problems in the stochastic setting.

Crucially, we can construct a generic and closed-form sequence of algorithmic beliefs that approximate the maximization of MAIR at each round. By leveraging these beliefs, we develop Model-index AMS and Model-index APS algorithms that achieves the sharpest known bounds for RL problems within the bilinear class (Du et al., 2021; Foster et al., 2021). Some of our algorithms feature a generic and closed-form updating rule, making them potentially well-suited for efficient implementation through efficient sampling oracles.

7.1 Generic analysis leveraging MAIR

In the stochastic setting, by leveraging MAIR, we can prove the following generic regret bound for arbitrary learning algorithm, and with arbitrarily chosen algorithmic belief sequence . This generic regret bound is an analogy of Theorem 3.4, which is not only applicable to any algorithm but also allows the algorithmic beliefs to be flexibly selected.

Theorem 7.1 (Generic regret bound for arbitrary learning algorithm leveraging MAIR).

In the stochastic setting, given a finite model class , the ground truth model , an arbitrary algorithm ALG that produces decision probability , and a sequence of beliefs where for all rounds, we have

where is the vector whose coordinate is but all other coordinates are .

An appealing aspect of Theorem 7.1 is that we only need to bound the gradient-based optimization error with respect to the same for all rounds. This property arises due to the stochastic environment.

Specifically, when the algorithmic beliefs exactly maximizes MAIR at each round (optimization errors equal to ), and when applying the minimax strategy in algorithm design, we propose Model-index Adaptive Minimax Sampling (MAMS), see Algorithm 6 below.

Input learning rate .

Initialize .

Because the minimax value of MAIR is always upper bounded by DEC, as illustrated in Lemma 2.8, it is straightforward to prove the following theorem.

Theorem 7.2 (Regret of MAMS).

For a finite and compact model class , the regret of Algorithm 6 with any is always bounded as follows, for all ,

This shows that the regret bound of MAMS is always no worse than the regret bound of the Estimation-to-Decision (E2D) algorithm in Foster et al. (2021).

Comparing AIR and MAIR.

We have seen from Lemma 2.5, Lemma 2.8, and Lemma 2.7 that 1) Maximin AIR can be bounded by DEC of the convex hull ; 2) Maximin MAIR can be bounded by DEC of the original class ; and 3) MAIR is “smaller” than AIR. However, as we have shown in Theorem 3.1 and Theorem 7.1, the regret bound using AIR scales with a term (estimation complexity of decision space), while the regret bound using MAIR scales with a bigger term (estimation complexity of model class). We explain their difference as follows.

When to use AIR versus MAIR? First, AIR is applicable to both stochastic and adversarial environments, whereas MAIR may only be applicable to stochastic environments. Second, when using AIR, an estimation complexity term of is introduced, whereas MAIR results in a larger estimation complexity term of . Therefore, AIR often yields tighter regret bounds for bandit problems. For instance, AIR provides optimal regret bounds for multi-armed bandits and achieves -type regret bounds for the challenging problem of bandit convex optimization, whereas MAIR may not attain these results. On the other hand, MAIR does achieve optimal regret bounds for stochastic linear bandits. Notably, MAIR also achieves optimal regret bounds for stochastic contextual bandits with general realizable function classes (Foster and Rakhlin, 2020; Simchi-Levi and Xu, 2022), including scenarios with potentially infinite actions (Xu and Zeevi, 2020b; Foster et al., 2020; Zhu et al., 2022). Moreover, MAIR is better suited than AIR for reinforcement learning problems in which taking the convex hull to the model class may significantly enhance its expressiveness. For instance, in RL problems, the model class, especially the state transition dynamics, often does not adhere to convexity assumptions. In general, AIR is more suitable for “infinite divisible” problems where taking the convex hull does not substantially increase the complexity of the model class. Conversely, MAIR is better suited for stochastic model-based bandit and RL problems in which avoiding convex hull operations is preferred.

7.2 Near-optimal algorithmic beliefs in closed form

For any fixed decision probability , it is illustrative to write MAIR as

| (7.1) |

where is the induced distribution of conditioned on , and the third equality is by property of mutual information. We would like to give a sequence of algorithmic beliefs that approximately maximize MAIR at each rounds, as well as have closed-form expression.

We consider the following algorithmic priors at each round:

| (7.2) |

where the adaptive algorithmic belief in (7.2) attempts to optimize the MAIR objective in (7.2), with approximates . The factor before the squared Hellinger distance is a technical consequence of the triangle-type inequality of the squared Hellinger distance, which has a factor rather than (see Lemma D.12). And we use their corresponding posteriors to update the sequence of reference probabilities:

This results in the following update of :

| (7.3) |

Input algorithm ALG and learning rate .

Initialize to be the uniform distribution over .

Using such algorithmic beliefs, the regret of an arbitrary algorithm can be bounded as follows.

Theorem 7.3 (Regret for arbitrary algorithm with closed-form beliefs).

Given a finite model class where the underlying true model is , and for every and . For an arbitrary algorithm ALG and any , the regret of algorithm ALG is bounded as follows, for all ,

where and are closed-form beliefs generated according the Algorithm 7.

By combining the belief generation process in Algorithm 7 as an estimation oracle to E2D (Foster et al., 2021), we can recover its regret bound using DEC, as we have demonstrated with MAMS in Theorem 7.2. Now, we have closed-form expressions for the near-optimal beliefs. Note that our reference probabilities (7.3) update both the log-likelihood term and an adaptive algorithmic belief term at each iteration. In contrast, most existing algorithms, whether optimistic or not, typically update only the log-likelihood term and rely on a fixed prior term. Furthermore, it’s worth highlighting that existing “optimistic” or “model-free” algorithms often employ a scaled version of the Bayesian posterior formula (Agarwal and Zhang, 2022; Foster et al., 2022a; Zhang, 2022; Chen et al., 2022). In contrast, we approach the problem using the original Bayesian posterior formula by incorporating adaptive beliefs. This approach may also have implications for fundamental problems like density estimation with proper estimators, as earlier methods have typically relied on the scaled version of posterior formulas (Zhang, 2006; Geer, 2000), rather than directly utilizing the original posterior formula as we do here.

In our applications, we often use a simple posterior sampling strategy for which we always induce the distribution of optimal decisions from the posterior distribution of models. We refer to the resulting algorithm, Algorithm 8, as “Model-index Adaptive Posterior Sampling” (MAPS).

Input learning rate .

Initialize to be the uniform distribution over .

MAPS draws inspiration from the optimistic posterior sampling algorithm proposed in Agarwal and Zhang (2022) (also referred to as feel-good Thompson sampling in Zhang (2022)). However, our approach incorporates adaptive algorithmic beliefs and the original Bayesian posterior formula, rather than using the fixed prior and the scaled posterior update formulas as in Agarwal and Zhang (2022); Zhang (2022).

For model class , a nominal model , and the posterior sampling strategy , we can define the Bayesian decision-estimation coefficient of Thompson Sampling by

| (7.4) |

This value is bigger than the minimax DEC in Definition 2.4, but often easier to use in RL problems.

Theorem 7.4 (Regret of Model-index Adaptive Posterior Sampling).

Given a finite model class where for every and . The regret of Algorithm 8 with is bounded as follows, for all ,

7.3 Application to reinforcement learning

By using MAMS (Algorithm 6), MAPS (Algorithm 8), and Algorithm 7 (closed-form algorithmic belief generation), we are able to recover several results in Foster et al. (2021) that bound the regret of RL by DEC and the estimation complexity of the model class. Note that MAPS (Algorithm 2) has the potential to be efficiently implemented through efficient sampling oracles, while the generic E2D algorithm in Foster et al. (2021) is not in closed form and requires minimax optimization, and the sharp regret bounds are proved through the non-constructive Bayesian Thompson Sampling. The paper also presents regret bounds for a constructive algorithm using the so-called “inverse gap weighting” updating rules (Foster and Rakhlin, 2020; Simchi-Levi and Xu, 2022), but that algorithm has worse regret bounds than those proved through the non-constructive approach (by a factor of the bilinear dimension). As a result, Algorithm 8 makes an improvement because its simplicity and achieving the sharpest regret bound proved in Foster et al. (2021) for RL problems in the bilinear class.

We illustrate how the general problem formulation in Section 2.1 covers RL problems as follows.

Example 3 (Reinforcement learning).

An episodic finite-horizon reinforcement learning problems is defined as follows. Let be the horizon and be a finite action set. Each model specifies a non-stationary Markov decision process (MDP) , where is the initial distribution over states; and for each layer , is a finite state space, is the probability transition kernel, and is the reward distribution. We allow the transition kernel and loss distribution to be different for different but assume to be fixed for simplicity. Let be the space of all deterministic non-stationary policies , where . Given an MDP and policy , the MDP evolves as follows: beginning from , at each layer , the action is sampled from , the loss is sampled from and the state is sampled from . Define to be the expected reward under MDP and policy . The general framework covers episodic reinforcement learning problems by taking the observation to be the trajectory and be a subspace of . While our framework and complexity measures allow for agnostic policy classes, recovering existing results often requires us to make realizability-type assumptions.

We now focus on a broad class of structured reinforcement learning problems called “bilinear class” (Du et al., 2021). The following definition of the bilinear class is from Foster et al. (2021).

Definition 7.5 (Bilinear class).

A model class is said to be bilinear relative to reference model if:

1. There exist functions , such that for all and ,

We assume that .

2. Let . There exists a collection of estimation policies and estimation functions such that for all and ,

If , we say that estimation is on-policy.

If is bilinear relative to all , we say that is a bilinear class. We let denote the minimal dimension for which the bilinear class property holds relative to , and define . We let denote any almost sure upper bound on under , and let .

For , let be the randomized policy that—for each —plays with probability and with probability . Combining the upper bounds of proved in Theorem 7.1 in Foster et al. (2021) with our Theorem 7.2 (regret of MAMS) and Theorem 7.4 (regret of MAPS), we can immediately obtain regret guarantees for RL problems in the bilinear class.

Theorem 7.6 (Regret of MAMS and MAPS for RL problems in the bilinear class).

In particular, as a closed-form algorithm that may be computed through sampling techniques, MAPS matches the sharp results for E2D, MAMS, and the non-constructive Bayesian Posterior Sampling algorithm used in the proof of Theorem 7.1 in Foster et al. (2021); and MAPS achieves better regret bounds than the closed-form “inverse gap weighting” algorithm provided in the same paper. Its regret bound for RL problems in the bilinear class also match the E2D algorithms in Foster et al. (2021, 2022a) that are not in closed-form and require more challenging minimax optimization.

Our results in this section apply to reinforcement learning problems where the DEC is easy to upper bound, but bounding the information ratio may be more challenging, particularly for complex RL problems where the model class may not be convex and the average of two MDPs may not belong to the model class. Specifically, we propose MAIR and provide a generic algorithm that uses DEC and the estimation complexity of the model class () to bound the regret. Another promising research direction is to extend our general results for AIR and the tools from Section 6.2 to reinforcement learning problems with suitably bounded information ratios, such as tabular MDPs and linear MDPs, as suggested in Hao and Lattimore (2022). We hope that our tools can pave the way for developing constructive algorithms that provide regret bounds scaling solely with the estimation complexity of the value function class, which is typically smaller than that of the model class.

8 Conclusion and future directions

In this work, we propose a novel approach to solve sequential learning problems by generating “algorithmic beliefs.” We optimize the Algorithmic Information Ratio (AIR) to generate these beliefs. Surprisingly, our algorithms achieve regret bounds that are as good as those assuming prior knowledge, even in the absence of such knowledge, which is often the case in adversarial or complex environments. Our approach results in simple and often efficient algorithms for various problems, such as multi-armed bandits, linear and convex bandits, and reinforcement learning.

Our work provides a new perspective on designing and analyzing bandit and reinforcement learning algorithms. Our theory applies to any algorithm through the notions of AIR and algorithmic beliefs, and it provides a simple and constructive understanding of the duality between frequentist regret and Bayesian regret in sequential learning. Optimizing AIR is a key principle to design effective and efficient bandit and RL algorithms. We demonstrate the effectiveness of our framework empirically via experiments on Bernoulli MAB and show that our derived algorithm achieves “best-of-all-worlds” empirical performance. Specifically, our algorithm outperforms UCB and is comparable to TS in stochastic bandits, outperforms EXP3 in adversarial bandits, and outperforms TS as well as clairvoyant restarted algorithms in non-stationary bandits.

Our study suggests several potential research directions, and we hope to see progress made by utilizing the methodology developed in this work. Firstly, an important task is to provide computational and representational guidelines for optimizing algorithmic beliefs, such as techniques for selecting belief parameterization and index representation (function class approximation). Secondly, a major goal is to achieve near-optimal regrets with efficient algorithms for challenging problems in infinite-armed bandits, contextual bandits, and reinforcement learning. An initial step involves exploring the Bayesian interpretation of existing frequentist approaches, including gaining a deeper understanding of IPW-type estimators and related computationally-efficient algorithms (Abernethy et al., 2008; Agarwal et al., 2014; Bubeck et al., 2017). Moreover, it is worth investigating whether our approach can facilitate the development of more precise regret bounds and principled algorithm design for reinforcement learning problems involving function approximation. Thirdly, an important direction is to leverage algorithmic beliefs to study adaptive and dynamic regrets in non-stationary environments and explore instance optimality (Wagenmaker and Foster, 2023) in stochastic environments. We note that we currently lack theoretical justification for our empirical “best-of-all-worlds” performance, and a comparison of our approach to earlier theoretical works on this topic (Bubeck and Slivkins, 2012; Wei and Luo, 2018). Fourthly, our paper introduces a novel framework for analyzing regret through AIR and offers a rich mathematical structure to explore and uncover, including the geometry of natural parameterization for maximizing AIR and its correspondence to the mirror space (see Appendix B for details). Fifthly, our aim is to comprehend alternative formulations of AIR, including the constrained formulation (drawing inspiration from the recent investigation of the constrained formulation of DEC in Foster et al. (2023)); connection may be made between regularization and the notion of localization (Xu and Zeevi, 2020a). Finally, we hope that the duality identities, which can accommodate arbitrary beliefs, algorithms, and any type of environment (as illustrated in Lemma 5.3), may offer values for lower bound analyses and information theory. We encourage exploration in these and all other relevant directions.

Acknowledgement.

We thank Yunzong Xu for valuable discussions.

References

- Abernethy et al. (2008) Jacob Abernethy, Elad Hazan, and Alexander Rakhlin. Competing in the dark: An efficient algorithm for bandit linear optimization. In 21st Annual Conference on Learning Theory, COLT 2008, 2008.

- Agarwal and Zhang (2022) Alekh Agarwal and Tong Zhang. Model-based RL with optimistic posterior sampling: Structural conditions and sample complexity. Advances in Neural Information Processing Systems, 35:35284–35297, 2022.

- Agarwal et al. (2014) Alekh Agarwal, Daniel Hsu, Satyen Kale, John Langford, Lihong Li, and Robert Schapire. Taming the monster: A fast and simple algorithm for contextual bandits. In International Conference on Machine Learning, pages 1638–1646, 2014.

- Agrawal and Goyal (2012) Shipra Agrawal and Navin Goyal. Analysis of thompson sampling for the multi-armed bandit problem. In Conference on Learning Theory, pages 39–1. JMLR Workshop and Conference Proceedings, 2012.

- Agrawal and Goyal (2013) Shipra Agrawal and Navin Goyal. Thompson sampling for contextual bandits with linear payoffs. In International Conference on Machine Learning, pages 127–135. PMLR, 2013.

- Auer et al. (2002a) Peter Auer, Nicolo Cesa-Bianchi, and Paul Fischer. Finite-time analysis of the multiarmed bandit problem. Machine Learning, 47(2):235–256, 2002a.

- Auer et al. (2002b) Peter Auer, Nicolo Cesa-Bianchi, Yoav Freund, and Robert E Schapire. The nonstochastic multiarmed bandit problem. SIAM Journal on Computing, 32(1):48–77, 2002b.

- Bernhard and Rapaport (1995) Pierre Bernhard and Alain Rapaport. On a theorem of Danskin with an application to a theorem of Von Neumann-Sion. Nonlinear Analysis: Theory, Methods & Applications, 24(8):1163–1181, 1995.

- Bertsekas (1999) Dimitri P Bertsekas. Nonlinear Programming. Athena Scientific, Belmont, MA, 1999.

- Besbes et al. (2014) Omar Besbes, Yonatan Gur, and Assaf Zeevi. Stochastic multi-armed-bandit problem with non-stationary rewards. Advances in Neural Information Processing Systems, 27, 2014.

- Bogachev and Ruas (2007) Vladimir Igorevich Bogachev and Maria Aparecida Soares Ruas. Measure Theory, volume 1. Springer, 2007.

- Bubeck and Eldan (2016) Sébastien Bubeck and Ronen Eldan. Multi-scale exploration of convex functions and bandit convex optimization. In Conference on Learning Theory, pages 583–589. PMLR, 2016.

- Bubeck and Slivkins (2012) Sébastien Bubeck and Aleksandrs Slivkins. The best of both worlds: Stochastic and adversarial bandits. In Conference on Learning Theory, pages 42–1. JMLR Workshop and Conference Proceedings, 2012.

- Bubeck et al. (2017) Sébastien Bubeck, Yin Tat Lee, and Ronen Eldan. Kernel-based methods for bandit convex optimization. In Proceedings of the 49th Annual ACM Symposium on Theory of Computing, pages 72–85, 2017.

- Chen et al. (2022) Fan Chen, Song Mei, and Yu Bai. Unified algorithms for RL with decision-estimation coefficients: No-regret, PAC, and reward-free learning. arXiv preprint arXiv:2209.11745, 2022.

- Dani et al. (2007) Varsha Dani, Sham M Kakade, and Thomas Hayes. The price of bandit information for online optimization. Advances in Neural Information Processing Systems, 20, 2007.

- Dean et al. (2020) Sarah Dean, Horia Mania, Nikolai Matni, Benjamin Recht, and Stephen Tu. On the sample complexity of the linear quadratic regulator. Foundations of Computational Mathematics, 20(4):633–679, 2020.

- Du et al. (2021) Simon Du, Sham Kakade, Jason Lee, Shachar Lovett, Gaurav Mahajan, Wen Sun, and Ruosong Wang. Bilinear classes: A structural framework for provable generalization in RL. In International Conference on Machine Learning, pages 2826–2836. PMLR, 2021.

- Foster and Rakhlin (2020) Dylan Foster and Alexander Rakhlin. Beyond ucb: Optimal and efficient contextual bandits with regression oracles. In International Conference on Machine Learning, pages 3199–3210. PMLR, 2020.

- Foster et al. (2020) Dylan J Foster, Claudio Gentile, Mehryar Mohri, and Julian Zimmert. Adapting to misspecification in contextual bandits. Advances in Neural Information Processing Systems, 33, 2020.

- Foster et al. (2021) Dylan J Foster, Sham M Kakade, Jian Qian, and Alexander Rakhlin. The statistical complexity of interactive decision making. arXiv preprint arXiv:2112.13487, 2021.

- Foster et al. (2022a) Dylan J Foster, Noah Golowich, Jian Qian, Alexander Rakhlin, and Ayush Sekhari. A note on model-free reinforcement learning with the decision-estimation coefficient. arXiv preprint arXiv:2211.14250, 2022a.

- Foster et al. (2022b) Dylan J Foster, Alexander Rakhlin, Ayush Sekhari, and Karthik Sridharan. On the complexity of adversarial decision making. Advances in Neural Information Processing Systems, 35:35404–35417, 2022b.

- Foster et al. (2023) Dylan J Foster, Noah Golowich, and Yanjun Han. Tight guarantees for interactive decision making with the decision-estimation coefficient. arXiv preprint arXiv:2301.08215, 2023.

- Geer (2000) Sara A Geer. Empirical Processes in M-estimation, volume 6. Cambridge University Press, 2000.

- Hao and Lattimore (2022) Botao Hao and Tor Lattimore. Regret bounds for information-directed reinforcement learning. Advances in Neural Information Processing Systems, 35:28575–28587, 2022.

- Hazan and Karnin (2016) Elad Hazan and Zohar Karnin. Volumetric spanners: an efficient exploration basis for learning. The Journal of Machine Learning Research, 17(1):4062–4095, 2016.