Double machine learning and design in batch adaptive experiments

Abstract

We consider an experiment with at least two stages or batches and subjects per batch. First, we propose a semiparametric treatment effect estimator that efficiently pools information across the batches, and show it asymptotically dominates alternatives that aggregate single batch estimates. Then, we consider the design problem of learning propensity scores for assigning treatment in the later batches of the experiment to maximize the asymptotic precision of this estimator. For two common causal estimands, we estimate this precision using observations from previous batches, and then solve a finite-dimensional concave maximization problem to adaptively learn flexible propensity scores that converge to suitably defined optima in each batch at rate . By extending the framework of double machine learning, we show this rate suffices for our pooled estimator to attain the targeted precision after each batch, as long as nuisance function estimates converge at rate . These relatively weak rate requirements enable the investigator to avoid the common practice of discretizing the covariate space for design and estimation in batch adaptive experiments while maintaining the advantages of pooling. Our numerical study shows that such discretization often leads to substantial asymptotic and finite sample precision losses outweighing any gains from design.

1 Introduction

In sequential experimentation, we can use earlier observations to adjust our treatment allocation policy for subsequent observations and thereby gain improved estimation of causal effects in the overall study. For instance, for an experiment with one treatment arm and one control arm, Neyman, (1934) showed that choosing the number of subjects in each arm to be proportional to the outcome standard deviation of that arm minimizes the variance of the treatment effect estimate based on the difference in means. While these standard deviations are unknown, they can be estimated using the initial data. Then the Neyman allocation can be approximated to improve the sample efficiency of the remainder of the experiment (Hahn et al.,, 2011; Blackwell et al.,, 2022; Zhao,, 2023; Dai et al.,, 2023).

We study a version of this design problem for an experiment divided into a small number of stages or batches. The design, or treatment assignment mechanism, can be updated adaptively for later batches based on the observations from earlier batches to improve the precision of the causal estimate computed at the end of the experiment. A salient feature of our setting is knowledge of pre-treatment covariates that can further improve precision. Thus, we conceptualize our design problem as choosing a propensity score for each batch. The propensity score specifies the probability that a subject receives treatment given their covariates (throughout, we consider the setting of a binary treatment). The propensity score is well known to be a key mathematical object to be estimated in the causal analysis of observational data (e.g. Rosenbaum and Rubin, (1983)). In a randomized experiment it is known and under the control of the investigator. Hence, it can be exploited for design.

Our specific design objective is to minimize an appropriate scalarization of the asymptotic covariance matrix of an estimator that efficiently pools information across all batches of the experiment. After describing our mathematical notation and setup in Section 2, we present and study an oracle version of this pooled estimator in Section 3. That oracle is given knowledge of some nuisance parameters, typically infinite-dimensional mean or variance functions. It pertains to a so-called “non-adaptive batch experiment” where treatment is assigned with possibly varying but nonrandom propensity scores across batches. In certain cases, our oracle pooled estimator asymptotically dominates the best possible alternative that aggregates single batch estimates, regardless of the per-batch propensities. This justifies designing for the pooled estimator instead of an aggregation-based alternative.

For such a design procedure to be useful, however, we must show that the targeted asymptotic precision of the oracle pooled estimator is in fact attainable in a batched experiment where the propensity scores used are adaptive (data-dependent) and the nuisance parameters need to be estimated. We address these challenges in Section 4 by extending the framework of double machine learning formalized by Chernozhukov et al., (2018), hereafter DML, to what we call a “convergent split batch adaptive experiment,” or CSBAE. In a CSBAE, observations in each batch are split into folds, and treatment is assigned in each fold according to an adaptive propensity score that only depends on observations from previous batches within the same fold. Within a given batch, the adaptive propensity scores are further required to converge to a common limit at rate in root mean square (RMS). Our DML extension then shows that by plugging in estimated nuisance functions, we can construct a feasible estimator in a CSBAE that is asymptotically equivalent to the oracle pooled estimator computed on the limiting non-adaptive batch experiment. The nuisance function estimates only need to converge at the rate .

Section 5 details a finite dimensional concave maximization procedure (Algorithm 1) that provably constructs a CSBAE for which the limiting propensities in each batch are sequentially optimal within a function class satisfying standard complexity conditions. Hence, we can effectively design for our pooled estimator in a batch adaptive experiment with theoretical guarantees that our final estimator will indeed attain the targeted optimal asymptotic precision, even with a fairly flexible propensity score learning method and nonparametric machine learning estimates for nuisance functions.

To the best of our knowledge, existing work either designs for a less efficient alternative to our pooled estimator, or discretizes the covariate space at the design and estimation stages to construct a feasible variant of the pooled estimator on a batch adaptive experiment. Our simulations in Section 6 suggest that the latter approach in particular can lead to substantial precision losses that swamp any gains from design, even with a moderate number of continuous covariates. Thus, for the practitioner, we provide an end-to-end design and estimation procedure to efficiently handle continuous covariates in a batched experiment.

1.1 Related work

There has been substantial research interest in adaptive experiment designs in recent years. In many applications, treatment assignments are updated in an attempt to maximize the (expected) response values of either those in the experiment, as in adaptive bandit algorithms (Russo et al.,, 2018; Hao et al.,, 2020), or those in the superpopulation from which the experimental subjects are assumed to arrive (Xu et al.,, 2018; Kasy and Sautmann,, 2021). Inference on data collected from these algorithms can be challenging since the treatment assignment rules often do not converge (Hadad et al.,, 2021; Zhang et al.,, 2020, 2021). By contrast, in our setting where the goal is purely statistical (maximizing asymptotic precision of the treatment estimate), the design objective is a static propensity score to be learned consistently. An interesting direction for further study would be to design for a mixture of both statistical and non-statistical objectives. For example, one might expand the literature on tie-breaker designs (Owen and Varian,, 2020; Morrison and Owen,, 2022; Li and Owen,, 2023; Kluger and Owen,, 2023)) to the setting of batched experiments.

The present work can be viewed as an extension of Hahn et al., (2011) in several directions. Those authors considered a two batch experiment to estimate the average treatment effect (ATE) as precisely as possible. Using data from the first batch to estimate variance functions, they estimate the asymptotic variance of a pooled version of the semiparametric efficient ATE estimator of Hirano et al., (2003) for a coarsely discretized covariate. Then, they learn a propensity score for the second batch that approximately minimizes this variance. The covariate discretization ensures nuisance functions and optimal propensities can be estimated at parametric rates without parametric assumptions. Consequently, a feasible version of the pooled estimator indeed attains the targeted asymptotic variance on the batch adaptive experiment. We generalize this pooling construction beyond the setting of ATE estimation and relax these rate requirements to those described in the previous section. This permits more efficient handling of continuous covariates through nonparametric nuisance function estimates and more flexible adaptive propensity scores.

Other approaches to extend the work of Hahn et al., (2011) include Kato et al., (2020), who consider an online setting where subjects from a stationary superpopulation enter one at a time, without batches. Similarly, the literature on covariate-adjusted response-adaptive (CARA) designs has focused on different but related objectives, both statistical and ethical (Zhang et al.,, 2007; Zhu and Zhu,, 2023). In the batched setting, Tabord-Meehan, (2022) proposes a method to learn a variance-minimizing stratification of the covariate space of fixed size, avoiding the need to discretize the space prior to observing the data as in Hahn et al., (2011). Cytrynbaum, (2021) showed that by performing a form of highly stratified treatment assignment called local randomization, consistent variance function estimates from the first batch make it possible to attain the semiparametric lower bound for ATE estimation in the second batch with optimal propensity score without having to estimate the conditional mean functions. Neither of these approaches, however, maintains the efficiency advantages of pooling. They also do not immediately extend beyond ATE estimation.

2 Setup and notation

Let be the number of batches in the experiment. Each subject in batch has observed covariates and potential outcomes . We place these in the vectors which are exogenous in our model. Let be the binary treatment indicator for this subject, which is controlled by the investigator. Under the usual stable unit value treatment assumption (SUTVA), the observed outcome is

| (1) |

Then the available data for the subject is . We assume that the vectors for and , for some distribution . Appendix A relaxes this assumption to permit certain forms of non-stationarity across batches, such as covariate shifts. It will be convenient to define the functions

| (2) |

for and . These expectations are taken under .

Let . Then as in Hahn et al., (2011), Che and Namkoong, (2023) and others, we consider a proportional asymptotic regime

| (3) |

as . In settings where the batch sizes are fully controlled by the experimenter, it may be theoretically preferable to make initial batch sample sizes a vanishing fraction of the total sample size (Zhao,, 2023). However, in many settings the batch sizes are exogenously constrained to satisfy (3) unless observations are discarded.

For various and probability measures on some space , it will be useful to consider function norms of the form

for . We will use propensity scores denoted by with various subscripts. A propensity score specifies , the probability of treatment conditional on covariates. We will typically require propensity scores to lie in , the set of all measurable functions on taking on values in the interval for some . We use to denote the square root of the sum of the squared entries of any vector, matrix, or tensor . For any integer , will denote the set of symmetric positive semidefinite real matrices, and will be the set of symmetric positive definite real matrices. Finally, for any real vector , we write .

We summarize the preceding requirements for the data generating process in Assumption 2.1. Assumption 2.1 does not impose any restrictions on the treatment assignment process, which will be discussed at length in subsequent sections.

Assumption 2.1 (Data generating process).

2.1 Estimands and score equations

Consider the setting where (so we can drop the batch subscript ), and the observations are i.i.d. Suppose additionally that (1) holds along with the unconfoundedness assumption

Then many popular causal estimands are identified by a score equation

In this score equation, is a vector of possibly infinite-dimensional nuisance parameters lying in a nuisance set , and is the propensity score. Following Section 3.1 of Chernozhukov et al., (2018), we will assume for simplicity that the score is linear in the sense that

| (4) |

for some , , and .

When , propensity scores may vary across batches by design or external constraints. For any propensity and integrable function , we use the subscripted notation where is the distribution of induced by and under the SUTVA assumption (1). Further let be the marginal distribution of under . Then we will require the following score equations to hold for some to identify the our causal estimand :

| (5) |

Note that (5) requires the score to have mean 0 when any propensity score is plugged in. This plug-in propensity may differ from the propensity used for treatment assignment in the experiment that generated the observations . Such a robustness property is satisfied by definition so long as the score is doubly robust. It is required to ensure the validity of the pooled estimator that we propose in Section 3. That estimator requires plugging in a mixture propensity score that averages propensities across all batches . While identification of within each batch is possible by only requiring (5) to hold when , this will not be sufficient to ensure validity of our pooled estimator. We formally restate our requirements on identification of the estimand in Assumption 2.2.

Assumption 2.2 (Estimand identification).

The first estimand we are motivated by is the ATE, given by in our notation. For an investigator interested in modeling how the treatment effect varies with , they may instead wish to estimate the regression parameter under a linear treatment effect assumption

| (6) |

See Robinson, (1988) for background on semiparametric estimation of under (6), which characterizes the well-known “partially linear model.” We show next that both and are identified by score functions that are linear in the sense of (4) and robust in the sense of (5), and hence identifiable according to Assumption 2.2.

Example 2.1 (ATE estimation).

Let be the estimand of interest. Now consider the augmented inverse propensity weighting (AIPW) score function

| (7) |

for nuisance parameter . For each , it is well known that for any in when lies in the nuisance set . Hence, satisfies the score equation (5). This score is also linear because for

which completes the task of showing that satisfies Assumption 2.2.

Example 2.2 (Partially linear model).

Suppose the linear treatment effect assumption (6) holds and is the estimand of interest. Now consider the weighted least squares score

| (8) |

for nonnegative weights

with nuisance parameter . Let be the set of all measurable functions . Then if lies in the nuisance set for some , we have for any in . Furthermore, is linear, because for

Thus, satisfies Assumption 2.2 with and the score . Note that the score equations (5) hold for any nonnegative weight functions , though the specific choice in is semiparametrically efficient (Chamberlain,, 1992; Ma et al.,, 2006).

3 Oracle pooled and aggregate estimation (non-adaptive)

Here we propose and analyze an oracle estimator of a generic estimand satisfying Assumption 2.2 with score . It is an oracle in the sense that it uses the unknown true value of the nuisance parameter from the score equations (5). We discuss feasible estimation of , including estimation of , in Section 4. The estimator pools observations across all batches . We then prove a central limit theorem (CLT) for it in the setting of a non-adaptive batch experiment where treatment in each batch is assigned according to a fixed (non-random) propensity score :

Definition 3.1 (Non-adaptive batch experiment).

A non-adaptive batch experiment has data generating process satisfying Assumption 2.1 and treatment assignments satisfying

for some nonrandom (i.e., non-adaptive) batch propensity scores and uniformly distributed random variables that are i.i.d. and independent of the vectors .

Next, we compare the pooled estimator to an alternative oracle that makes an optimal linear aggregation of per-batch estimates. It also satisfies a CLT, but we show that our pooling strategy dominates aggregation in terms of efficiency in the setting of Examples 2.1 and 2.2. We remark that some authors (e.g. Tabord-Meehan, (2022)) refer to this aggregation approach as pooling, but we reserve that term for pooling data, not estimators.

3.1 Pooled oracle estimator

The main idea behind the construction of our oracle estimator is as follows. After collecting the observations from all batches in a non-adaptive batch experiment, we ignore the batch structure and pool together the observations across batches. Now consider a random draw from these pooled observations . In the notation of Section 2, it is straightforward to show that the distribution of is , where is the mixture propensity score

| (9) |

It will also be helpful to define the limiting mixture propensity score under the proportional asymptotics (3):

| (10) |

When a particular set of nonrandom batch propensities is relevant, we omit an additional subscript by letting and . Using this notation, the oracle pooled estimator is derived by solving the sample analogue of the mixture score equations for :

| (11) |

This is only defined when the matrix inverse in (11) exists. That will be the case with probability tending to 1 so long as is invertible, which we will require in our theoretical results. One such result is a CLT for . The proofs of all our technical results are provided in Appendix C.

Proposition 3.1 (Oracle CLT).

Let be an estimand satisfying Assumption 2.2 for some , some score , and some nuisance parameters . Suppose observations are collected from a non-adaptive batch experiment with batch propensities , and define and as in (9) and (10), respectively. Further assume the following conditions hold:

-

1.

For some sequence , we have

-

2.

is invertible and .

-

3.

For some and we have for all sufficiently large .

Then with as defined in (11), we have

where

Proof.

See Appendix C.1. ∎

For the estimands and , following (11) we use the scores and , respectively to derive the oracle estimates

| (12) | ||||

| (13) |

We now specialize the generic oracle CLT of Proposition 3.1 to these two estimators under some regularity conditions.

Assumption 3.1.

[Regularity for estimating ] For some and , we have and for all and .

Assumption 3.2.

Corollary 3.1 (Oracle CLT for ).

Suppose Assumption 3.1 holds, and let be observations from a non-adaptive batch experiment with batch propensities for some . Then where

| (14) |

Proof.

See Appendix C.2. ∎

Corollary 3.2 (Oracle CLT for ).

Suppose Assumption 3.2 holds, and let be observations from a non-adaptive batch experiment with batch propensities , where . Then , where

| (15) |

Proof.

See Appendix C.3. ∎

3.2 The aggregated oracle estimator

When the covariate space is finite, the oracle pooled estimator is equivalent to an oracle variant of the estimator proposed by Hahn et al., (2011). The complexity of constructing a feasible pooled estimator for an adaptive experiment in more general settings has led other authors to instead consider single batch estimators that can lose considerable efficiency. For instance, Cytrynbaum, (2021) proposes simply discarding the first batch in a two-batch experiment when computing the final estimate, which is clearly inadmissible in our proportional asymptotic regime (46). Section 3.2 of Tabord-Meehan, (2022) suggests instead taking a linear aggregation of estimates computed separately on each batch, as described above. We will now show that even the best linearly aggregated oracle estimator is asymptotically dominated by our pooled estimators and . While Tabord-Meehan, (2022) hypothesized in their Appendix C.2 that this may be true for ATE estimation, they do not pursue this further as are unable to construct a feasible pooled estimator attaining the targeted oracle variance when batch propensities are chosen adaptively using their stratification trees. By contrast, our design approach will allow us to construct such an estimator using our extension of double machine learning in Section 4.

Fix a non-adaptive batch experiment with batch propensities . For each batch , consider an (oracle) estimator for computed by solving the empirical analogue of the score equations that averages only those observations in batch :

By applying Proposition 3.1 with a single batch, for each we obtain the CLT

where

Now, as stated in Slud et al., (2018), the asymptotically unbiased linear combination of with the smallest asymptotic covariance matrix with respect to the semidefinite ordering is the inverse covariance weighted estimator

This optimal linearly aggregated estimator satisfies the CLT

We can similarly define the linearly aggregated oracle estimator for based on combining per-batch estimates from the score , which satisfies a CLT . Here is given by replacing with , with , and with in the definition of . Our main result is then that regardless of the batch propensities, and are asymptotically dominated by our pooled estimators and , respectively. This motivates our work in Section 5 that designs for these estimators.

Theorem 3.1 (Pooling dominates linear aggregation).

Proof.

See Appendix C.4. ∎

4 Feasible pooled estimation in batch adaptive experiments

The oracle estimator of (11) depends on nuisance parameters that are unknown in practice. Additionally, recall that our CLT for (Proposition 3.1) holds for a non-adaptive batch experiment. Our goal is to choose propensities adaptively in each batch to improve precision. Therefore, we would like to develop a feasible estimator that attains the targeted asymptotic variance for experiments where treatment is assigned adaptively, even when the nuisance parameters must be estimated.

As mentioned above, our construction of such a feasible estimator is based on extending the double machine learning (DML) framework of Chernozhukov et al., (2018). The main requirements for to have the same asymptotic variance as the corresponding oracle are convergence rate guarantees for both nuisance parameter estimates and the adaptive propensities. Our DML extension ensures that these rate requirements can be made sub-parametric, enabling the use of somewhat flexible machine learning methods.

The typical DML setting assumes access to a single sample of i.i.d. observations. An example of this setting is a non-adaptive batch experiment with and propensity . Then a standard DML estimator is based on two ingredients: a Neyman orthogonal score and cross-fitting. Neyman orthogonality of the score at means a local insensitivity of the score equations to perturbations in in any direction:

It is well known that the scores and are Neyman orthogonal (Chernozhukov et al.,, 2018). Given a Neyman orthogonal score , DML proceeds by constructing an estimator by cross-fitting. In cross-fitting, the indices are partitioned into (roughly) equally sized folds . Then is computed as the solution to the empirical score equations , where for each , and are estimates of and , respectively. Each pair depends only on the observations outside fold . The sample splitting ensures that for each , the estimates are independent of the observations in fold . By the arguments of Chernozhukov et al., (2018), such independence is key to guarantee that the feasible estimator is equivalent (up to first order asymptotics) to the oracle solving (cf. (11)), even when the estimates converge at sub-parametric rates.

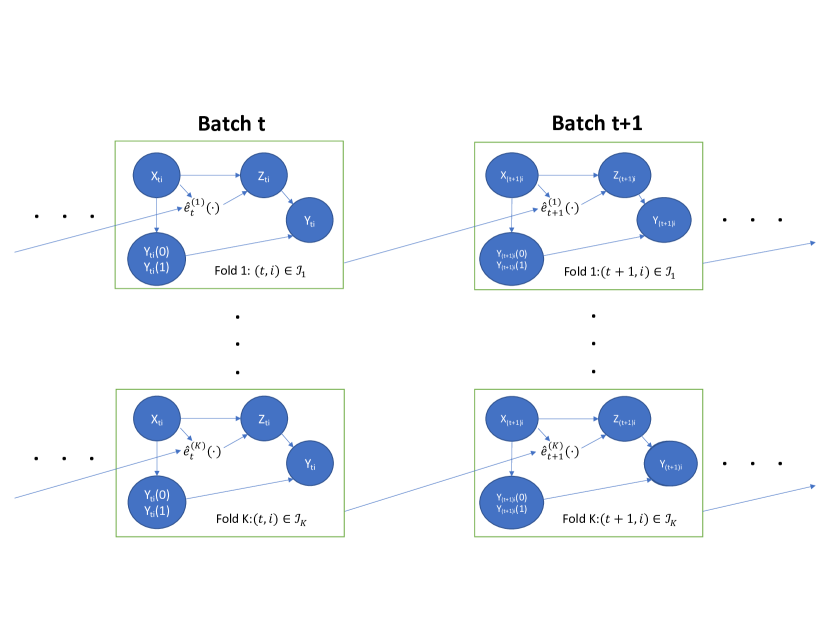

To maintain this independence in an adaptive batched experiment, we require sample splitting at the design stage, as illustrated in Figure 1, along with convergence of the adaptive propensity scores. Our notion of a convergent split batch adaptive experiment (CSBAE) in Definition 4.1 formalizes this. The main idea is to split the observations in every batch into folds. Re-using the notation above from the standard DML setting with , we let denote the set of batch and observation indices assigned to fold . Then the adaptive propensity used to assign treatment to a subject in batches is allowed to only depend on observations in previous batches from the same fold as this subject. To ensure that the adaptivity does not introduce any additional variability (up to first-order asymptotics) into the final estimator, a CSBAE requires these adaptive propensities to converge to nonrandom limits at RMS rate . While this convergence requirement may appear restrictive, in Section 5 we show how it can be ensured by design by solving an appropriate finite-dimensional concave maximization procedure. Moreover, the limiting propensity scores from this procedure will be provably optimal, in a sense we make more precise in Section 5.

Definition 4.1 (Convergent split batch adaptive experiment).

A convergent split batch adaptive experiment (CSBAE) is an experiment with data generating process satisfying Assumption 2.1 where each observation index is assigned to one of folds . The fold assignments are such that , the number of observations in batch assigned to fold , satisfies for all , . Now let be the empirical distribution on , the covariates in batch and fold , and define to be the -algebra generated by the covariates in batch and fold along with the observations in fold and any of the previous batches . We further require the following for each batch and fold :

-

1.

Treatment is assigned according to an adaptive propensity that is measurable with respect to . That is, the treatment indicators can be represented as

(16) where is a collection of i.i.d. uniformly distributed random variables independent of the vectors .

-

2.

For some nonrandom propensity , the adaptive propensity satisfies

(17)

Remark 4.1.

The left-hand side of equation (17) uses an norm on the empirical distribution of the covariates of the subjects that will be assigned treatment according to the learned propensity . These covariates will also be used to learn itself in our propensity learning procedure of Section 5. Thus, we can interpret (17) as a rate requirement on the “in-sample” convergence of .

Given a CSBAE, our feasible estimator is

| (18) |

As in the standard (single batch) DML setting, for each , and are estimates of the nuisance parameters and the mixture propensity defined in (9), respectively, that depend only on the observations outside fold . These observations are fully independent of the observations in fold (across all batches ) by the construction of a CSBAE. As in the single batch case, given convergence of the estimators to , this independence along with (17) enable a DML-style argument that is asymptotically equivalent to the oracle under (17) computed on a counterfactual non-adaptive batch experiment with propensities . This argument proceeds by coupling the treatment indicators in the CSBAE with counterfactual treatment indicators .

Assumption 4.1 (Score properties and convergence rates for estimating nuisance parameters and the mixture propensity in a CSBAE).

Observations are collected from a CSBAE with limiting batch propensities . Additionally, the estimand of interest is identified as in Assumption 2.2 by some score , nuisance parameters , and , such that the propensity collection contains . Defining for , the score has the following properties:

-

(a)

The matrix is invertible and .

-

(b)

The mapping is twice continuously differentiable on for each .

-

(c)

All propensities satisfy

(19) for all and .

Also, there exist estimators and of and the mixture propensity defined in (9), respectively, that depend only on the observations outside fold of the CSBAE. Next, there are nonrandom subsets containing , such that for all , as . The sets shrink quickly enough for the following to hold for all , all and all when is sufficiently large:

| (20) | ||||

| (21) | ||||

| (22) | ||||

| (23) | ||||

| (24) | ||||

| (25) |

Finally, letting be the -algebra generated by the observations outside fold across all batches 1 through , we require

| (26) |

where

Theorem 4.1 (Feasible CLT for a CSBAE).

Proof.

See Appendix C.5. ∎

In Assumption 4.1, the conditions (a) and (b) along with the inequalities (20) through (25) are direct extensions of Assumptions 3.1 and 3.2 in Chernozhukov et al., (2018) for ordinary DML (). The equations (19) and (26) are additional requirements that enable the dependence across batches in a CSBAE to be sufficiently weak so that computed on the CSBAE is asymptotically equivalent to a version of it computed on the limiting non-adaptive batch experiment.

We can show that Assumption 4.1 is satisfied for estimating and with and , respectively under simple rate conditions on nuisance parameter and propensity estimation rates that mirror those in Section 5 of Chernozhukov et al., (2018) for single-batch DML estimators. Then we apply Theorem 4.1 to construct feasible pooled estimators and as special cases of equation (18), which attain the oracle asymptotic variances and defined in (14) and (15), respectively.

Corollary 4.1 (Feasible pooled estimation of in a CSBAE).

Suppose observations are collected from a CSBAE for which the regularity conditions of Assumption 3.1 hold for some and and the limiting batch propensities are in for some . Additionally, for each , suppose we have estimates and of the mean function and mixture propensity , respectively, both depending only on the observations outside fold , such that the following are true:

-

1.

-

2.

-

3.

,

-

4.

with probability tending to 1.

Then .

Proof.

See Appendix C.6. ∎

Corollary 4.2 (Feasible estimation of in a CSBAE).

Suppose observations are collected from a CSBAE for which the regularity conditions of Assumption 3.2 hold for some and , and for which the limiting batch propensities are in with . For each , assume we have estimates , , and of the mean function , the variance function , and the mixture propensity , respectively, all depending only on the observations outside fold , such that the following are true:

-

1.

,

-

2.

,

-

3.

,

-

4.

-

5.

.

Then .

Proof.

See Appendix C.7. ∎

We now compare the rate requirements in Corollaries 4.1 and 4.2 with those needed to prove a feasible CLT for the linearly aggregated estimators discussed in Section 3. Consider a batch adaptive experiment without sample splitting, so that we assign treatment using the propensities where each is possibly random but can only depend on the observations in batches , and converges to some nonrandom at any rate; in particular, this rate may be slower than the rate of (17). Then the standard DML results in Section 5 of Chernozhukov et al., (2018) show that we can construct feasible estimators and that are asymptotically equivalent to the oracle single-batch estimators and in Section 3, so long as we plug in the true propensity score used to assign treatment and use cross-fitting at the estimation stage, even if all rates in Corollaries 4.1 and 4.2 are weakened to . Unfortunately, we cannot extend this construction to our pooled estimator when , since plugs in estimates of the mixture propensity , which does not correspond (in general) to a propensity actually used for treatment in any batch. Our numerical studies in Section 6 suggest, however, that the weaker rate requirements for a feasible CLT for the linearly aggregated estimators (compared to our pooled estimators) make little difference in practice. Indeed, there we also see finite sample advantages to pooling, beyond those predicted by the asymptotics.

5 Batch adaptive learning of the optimal propensity score

We now discuss how to learn adaptive propensity scores that satisfy (17) with limiting propensity scores that maximize asymptotic precision of the final estimators and constructed in the previous section, as measured by their asymptotic covariance matrices and . This generates a CSBAE on which, by Theorem 4.1, feasible estimators and achieve the targeted asymptotic variances and .

While is scalar and so there is no ambiguity in what it means to maximize asymptotic precision of , when is multivariate (), is a matrix. To handle the multivariate setting, we follow classical literature on experiment design in regression models by scalarizing an information matrix (typically an inverse covariance matrix) using an information function . See textbooks such as Atkinson et al., (2007); Pukelsheim, (2006) for more background. We generically write to emphasize that in our setting, will be indexed by a propensity score in some function class along with some unknown nuisance functions to be estimated. Then the design objective is to learn an optimal propensity , in the sense of maximizing :

| (27) |

The nuisance functions in the information matrix are distinct from the nuisance functions in the score function. Examples of for information matrices based on and are given in Section 5.2.

5.1 Generic convergence rates with concave maximization

We start by considering a feasible procedure to learn the propensity of (27) when the information matrix and the function class being optimized over generically satisfy Assumption 5.1 below. An explanation of how to apply this generic procedure to construct an appropriate CSBAE that designs for the estimators and is deferred to Section 5.2. Here we instead focus on a precise exposition of our propensity learning procedure and the technical assumptions needed to ensure convergence, without explicitly invoking any notation or setup from previous sections. We begin with some generic structure on the information matrix and the function class . Roughly, we require the information matrix to be strongly concave in and the function class to be not too complex. We also allow for interval constraints on the per-batch expected proportion of subjects treated.

Assumption 5.1 (Generic optimization setup).

The information matrix in (27) takes the form

| (28) |

where is a vector of possibly unknown functions taking values in some compact set , and is a covariate distribution from which i.i.d. observations are drawn. Additionally, the function appearing in (28) satisfies the following properties:

-

•

There exists an extension of with continuous second partial derivatives to an open neighborhood of r+1 containing for some .

-

•

For some we have

(29) where denotes the second partial derivative of with respect to the first argument, evaluated at .

Next, the collection of propensity scores to be optimized over takes the form , for some base propensity class and some known budget constraints with . The base propensity class is convex and closed in and additionally satisfies the following properties for all :

-

1.

There exists for which

(30) where is the metric entropy of the base propensity class in , as defined in Appendix B.1, and is the empirical distribution on the observations .

-

2.

Given any , there exists a convex set , possibly depending on , such that

-

•

For every , we must have , and

-

•

For every , there exists with for all .

-

•

-

3.

There exists such that for some .

-

4.

There exist such that and .

Remark 5.1.

If (29) only holds for in for some (instead of on all of ) and the base propensity class is chosen to lie within , then one can rewrite (28) as

where is an invertible linear mapping. Then the remainder of Assumption 5.1 holds as stated with replaced by and the base propensity class replaced by , and so all results below depending on Assumption 5.1 hold by considering optimization over instead of .

Similar to the idea of empirical risk minimization in supervised learning (ERM, e.g. Vapnik, (1991) and Montanari and Saeed, (2022)), when Assumption 5.1 is satisfied, our learning procedure replaces the unknown population expectation appearing in the objective (27) by a sample average over observations , where the generic sample size diverges. In our designed CSBAE, these observations will be the covariates of those subjects in a given batch of a CSBAE within a given fold , so will be identified with the quantity of Definition 4.1. The main computational procedure is then a finite dimensional optimization over the values of the propensity score at the points :

| (31) |

Here is an estimate of the nuisance function in (28), and the optimization set is defined by

| (32) |

where are budget constraints as in Assumption 5.1 and is as in the numbered condition 2 of that assumption.

We convert the vector in (31) to a propensity score by taking to be any member of the base propensity class of Assumption 5.1 with for each . The existence of such a propensity is guaranteed by the numbered condition 2 in Assumption 5.1. Then as in the ERM literature, we use empirical process arguments to guarantee the learned propensity converges to at rate under appropriate restrictions on the complexity of the base propensity class . Our main such restriction is the finite entropy integral requirement in (30). Examples of function classes satisfying this condition can be found in the literature on empirical processes. A sufficient condition is that for some , some , and all . Examples 5.1 through 5.4 below show that this requirement is loose enough to admit some relatively rich function classes.

Example 5.1 (Monotone).

Suppose and let be the set of nondecreasing functions in . By Lemma 9.11 of Kosorok, (2008), we know that for each and some positive universal constant .

Example 5.2 (Lipschitz).

Again suppose and let be the set of -Lipschitz functions in for some fixed . If is a bounded closed interval, then the discussion preceding Example 5.11 of Wainwright, (2019) shows that for each and some positive universal constant (which may depend on ).

Example 5.3.

(VC-subgraph class) Let be any subset of that is closed and convex in , and whose subgraphs are a Vapnik-Chervonenkis (VC) class, meaning they have a finite VC dimension . A special case is a fully parametric class like where is a known set of basis functions and . Then by Theorem 2.6.7 of van der Vaart and Wellner, (1996), for some universal depending on the VC dimension of the subgraphs. Note that may depend on .

Example 5.4.

(Symmetric convex hull of VC-subgraph class) Let be a VC-subgraph class of functions. The symmetric convex hull of is defined as

Now suppose is contained within , the pointwise closure of . Let be the VC dimension of the collection of subgraphs of functions in . Then by Theorem 2.6.9 of van der Vaart and Wellner, (1996) we have for all . For example, with we can take

| (33) |

where is any vector of real-valued basis functions, can be made arbitrarily large, and are arbitrary. This choice of is evidently a closed and convex subset of with . Note the collection is indeed a VC-subgraph class by Lemmas 2.6.15 and 2.6.17 of van der Vaart and Wellner, (1996), as each function in is the composition of the monotone function with the -dimensional vector space of functions .

Next, we construct sets that satisfy condition 2 of Assumption 5.1 for the base propensity classes in Examples 5.1 to 5.4. For the set of monotone functions in one dimension (Example 5.1) we can take

where is the inverse of the function that maps each to the rank of among (with any ties broken in some deterministic way). For the set of -Lipschitz functions (Example 5.2) we can take

For the parametric class in Example 5.3 we can take

Finally, for the class (33) in Example 5.4 we take

The convergence rates of to will be proven using strong concavity of the design objective (27) on the space . This is ensured by Assumption 5.1 along with the following conditions on the information function :

Assumption 5.2 (Information function regularity).

The information function is concave, continuous, and nondecreasing with respect to the semidefinite ordering on p×p and satisfies the following conditions:

-

(a)

For every , .

-

(b)

is twice continuously differentiable on , such that for all , there exists such that whenever and .

-

(c)

For every , implies for some .

-

(d)

For every and , there exists such that for all with , we have .

We can show that Assumption 5.2 is satisfied by two common information functions: the “-optimality” function with whenever is singular, and the “-optimality” function . The -optimality criterion corresponds to minimizing the average (asymptotic) variance of the components of the estimand, while -optimality corresponds to minimizing the volume of the ellipsoid spanned by the columns of the (asymptotic) covariance matrix.

Lemma 5.1.

The information functions and satisfy Assumption 5.2.

Proof.

See Appendix C.8. ∎

There are some common information functions that do not satisfy Assumption 5.2. For example, the “-optimality” function , where refers to the smallest eigenvalue of , is not differentiable. Similarly the function (for some fixed ), corresponding to “-optimality,” does not satisfy condition (c). We leave open the question of whether the convergence rate of to in Lemma 5.2 can be extended to these (and other) information functions using different techniques, and now prove this rate under Assumptions 5.1 and 5.2.

Lemma 5.2 (Convergence of generic concave maximization routine).

Suppose Assumption 5.1 holds for some information matrix of the form (28), covariate distribution , and budget constraints . Further assume that for some sequence , we have an estimate of satisfying

| (34) |

where is defined by by (28). Then for any information function satisfying Assumption 5.2, the following statements are true:

-

1.

There exists an optimal propensity function satisfying (27) which is unique -almost everywhere.

- 2.

-

3.

For any such optimal probabilities , there exists a propensity score for which for each . Any such function satisfies both and .

Proof.

See Appendix C.9. ∎

5.2 Convergence of batch adaptive designs

We now leverage Lemma 5.2 to develop a procedure (Algorithm 1) that can learn adaptive propensities with the convergence guarantees (17) so that when used for treatment assignment, they lead to a CSBAE with limiting propensities that optimize objectives of the form (27) with information matrices based on and . This shows we can effectively design for the estimators and .

For simplicity, we assume treatment in the first batch is assigned according to a non-random propensity for some . We let . Then for later batches , the target propensities are taken to be one of the following, for an information function satisfying Assumption 5.2:

| (35) |

Above, and are the asymptotic variances of the oracle pooled estimators and of (12) and (13), respectively, when computed using observations in a non-adaptive batch experiment with only batches and propensities . By (14) we can compute

| (36) |

where includes the components . Similarly, by (15) we have

| (37) |

where includes the components . In both of the preceding equations, the dependence on the batch propensity score is through the mixture given by

| (38) |

Finally, the optimization set in (35) is

| (39) |

which satisfies all the conditions in Assumption 5.1 with covariate distribution , budget constraints , and base propensity class .

We do not target the final covariances and in our discussion here since the sample sizes and budget constraints in future batches may not be known. If they are known in advance, then we can learn propensities for all future batches simultaneously at the time batch 2 covariates are observed, and indeed target or at that stage.

Now suppose we split our observations into folds as in a CSBAE, and for notational simplicity we re-index the covariates in each batch , fold as . Then following (31), we can estimate for each batch within each fold by computing

| (40) |

Here is defined as in (32), and the estimate of is given by

| (41) |

where each estimate of the variance function is computed using only the observations from batches within fold . Note that any plug-in estimate of and does not affect the optimization (40) and so can be omitted. The dependence of on the optimization variables is through the mixture quantities

| (42) |

where for , is the (possibly adaptive) propensity used to assign treatment in batch , fold . By comparing (42) and (38), we see that for each batch , is being used as a plug-in estimate of and the adaptive propensity score is used as a plug-in estimate of its limit . Finally, as in the conclusion of Lemma 5.2, the learned adaptive propensity to be used for treatment assignment in batch , fold is taken to be any choice in the predetermined base collection with for all .

Learning is exactly analogous; first we compute

| (43) |

where

| (44) | ||||

| (45) |

Then we assign treatment with any propensity in the base propensity class satisfying for all .

The main additional regularity condition required to ensure the adaptive propensities and above converge at the desired RMS rate to and of (35) is the same rate of convergence in the estimates and of the nuisance parameters and . We also strengthen the sample size asymptotics (3) by requiring

| (46) |

Theorem 5.1 (Convergence of Algorithm 1).

Suppose , fix a batch and suppose Assumption 2.1 holds along with (46). Further assume treatment in batches is assigned according to a CSBAE where the batch 1 propensities are for some , and that for each fold :

-

•

There exists an estimator of the variance function depending only on the observations in batches assigned to fold , such that for .

-

•

There are universal constants for which

-

•

The information function satisfies Assumption 5.2.

Let be any base propensity class satisfying the conditions of Assumption 5.1, and define to be the empirical distribution on the covariates in batch , fold . Then for any budget constraints and each fold , the following holds:

- 1.

If additionally, the linear treatment effect assumption (6) holds for some basis function containing an intercept, then:

- 2.

Proof.

See Appendix C.10. ∎

6 Numerical simulations

We implement Algorithm 1 to construct some synthetic CSBAE’s that illustrate the finite sample performance of our proposed methods. For simplicity we consider batches throughout. Our evaluation metric is the average mean squared error (AMSE) of the estimators and computed at the end of each CSBAE. As a baseline, we also compute feasible variants of the linearly aggregated estimators and computed on a “simple RCT”: that is, a non-adaptive batch experiment with a constant propensity score in each batch. We additionally consider the approach of Hahn et al., (2011) for design and estimation of . This is equivalent to using Algorithm 1 for design (without sample splitting, i.e. ) and using the pooled as the final estimator, but with the covariates replaced everywhere by a coarse discretization . As a hybrid we also consider using the discretized covariates for design but computing the final estimates and using the full original covariate . To separately attribute efficiency gains to design and pooling, we also consider the linearly aggregated estimators and when a modification of Algorithm 1 that targets and (the asymptotic variances of the estimators and given in Section 3, depending only on observations in batch 2) is used for design.

We consider four data generating processes (DGPs), distinguished by whether the covariate dimension is 1 or 10 and whether the conditional variance functions are homoskedastic (with for all ) or heteroskedastic (with . The scaling by the covariate dimension in the heteroskedastic variance functions ensures the variance in is independent of the covariate dimension . In all of the DGPs the covariates are i.i.d. spherical Gaussian, i.e. . The outcome mean functions are taken to be for . For estimating we use the basis functions where . Note . The potential outcomes are generated as follows:

For each DGP we run Algorithm 1 with folds, batch sample sizes , information function (corresponding to -optimality), and treatment fraction constraints for . In Appendix D, we present additional simulation results where remain at 0.2 but , so that the treatment budget for the second batch has increased. The initial propensity score is taken to be constant (i.e. for all ), and the base propensity class is the set of all -Lipschitz functions taking values in when (cf. Example 5.2). When , we take as in (33), with the collection of vectors with each coordinate and no more than two of the ’s nonzero.

The discretization used to implement the approach of Hahn et al., (2011) partitions d into four bins based on the quartiles of . Note that this partition is along the single dimension along which the variance functions vary in the heteroskedastic DGPs, so we would expect this to perform better than in practice, where the structure of the variance functions is not known (it could possibly be learned, as in Tabord-Meehan, (2022)). The choice of four bins is based on the experiments of Hahn et al., (2011), which find minimal performance difference between two and six bins for the DGP’s they consider. We denote their “binned” AIPW estimator by . Recall, as indicated above, that this is equivalent to when the only available covariate is the binned and no cross-fitting is used. For the conditional means are estimated nonparametrically by sample outcome means among all units with and in the appropriate batch(es) and fold(s). Similarly, the conditional variances are estimated by sample outcome variances.

For all simulations, the concave maximizations are performed using the CVXR software (Fu et al.,, 2017) and the MOSEK solver (MOSEK ApS,, 2022). All estimates of the mean function are computed by fitting a generalized additive model (GAM) to the outcomes and covariates from the observations with treatment indicators equal to in the appropriate fold(s) and batch(es). The GAMs use a thin-plate regression spline basis (Wood,, 2003) and the degrees of freedom are chosen using the generalized cross-validation procedure implemented in the mgcv package in R (Wood,, 2004). Variance function estimates are computed by first computing as above on the appropriate observations, then fitting a GAM on these same observations to predict the squared residuals from .

6.1 Average treatment effect

| DGP | Estimator | Design | Sim. rel. eff. (90% CI) | Asymp. rel. eff. |

|---|---|---|---|---|

| , Homoskedastic | Flexible | 0.989 (0.965, 1.013) | 1.000 | |

| Binned | 1.011 (0.977, 1.046) | 0.999 | ||

| Simple RCT | 1.016 (1.003, 1.029) | 1.000 | ||

| Flexible | 0.984 (0.971, 0.998) | 0.999 | ||

| Binned | 0.919 (0.877, 0.961) | 0.885 | ||

| , Heteroskedastic | Flexible | 1.016 (0.968, 1.064) | 1.048 | |

| Binned | 1.046 (0.997, 1.096) | 1.041 | ||

| Simple RCT | 0.997 (0.979, 1.016) | 1.000 | ||

| Flexible | 1.008 (0.971, 1.045) | 1.024 | ||

| Binned | 1.001 (0.946, 1.057) | 0.963 | ||

| , Homoskedastic | Flexible | 1.039 (0.990, 1.089) | 1.000 | |

| Binned | 1.011 (0.959, 1.065) | 1.000 | ||

| Simple RCT | 1.081 (1.052, 1.110) | 1.000 | ||

| Flexible | 1.047 (1.018, 1.077) | 1.000 | ||

| Binned | 0.477 (0.439, 0.519) | 0.417 | ||

| , Heteroskedastic | Flexible | 1.081 (1.023, 1.143) | 1.036 | |

| Binned | 1.050 (0.986, 1.117) | 1.000 | ||

| Simple RCT | 1.102 (1.070, 1.135) | 1.000 | ||

| Flexible | 0.991 (0.952, 1.030) | 1.024 | ||

| Binned | 0.651 (0.597, 0.708) | 0.595 |

Table 1 shows the performance of the various design and estimation procedures for that we consider. Each entry is a “relative efficiency”: that is, a ratio of the MSE of the baseline approach (which computes the linearly aggregated on a simple RCT) to the MSE of the relevant approach. The simulated relative efficiencies in the table estimate these MSE’s by averaging the squared error of each estimator over 1,000 simulations. The 90% confidence intervals for the true finite sample relative efficiency are computed using 10,000 bootstrap replications of these 1,000 simulations. Finally, the asymptotic relative efficiencies in Table 1 are computed by estimating the asymptotic variance of each estimator using the appropriate formula, i.e. for and for . The computation is based on a non-adaptive batch experiment with second batch propensity equal to the average of the learned propensities from the relevant approach across the 1,000 simulations, as a closed form solution for the limiting is not easily obtained in general. All expectations over the covariate distribution are computed using Monte Carlo integration.

For both of the homoskedastic DGPs, it is straightforward to show using Jensen’s inequality that for all . It can be further shown that the unpooled and pooled estimators are asymptotically equivalent. Thus, for the homoskedastic DGPs, there is no asymptotic efficiency gain to be had. With unequal budget constraints there is some asymptotic benefit to pooling with homoskedastic variance functions (Appendix D.1); however the optimal design will still be the simple RCT. Nonetheless, we do observe some finite sample benefits to pooling in Table 1. For example, the simulated relative efficiency of on the simple RCT is significantly larger than 1 for both and . We attribute this to improved nuisance estimates for the pooled estimator, as discussed further in Appendix D.2. As one might expect, this finite sample improvement from pooling is apparently offset by variance in both the flexible and binned design procedures. Still, in the homoskedastic DGPs, our adaptive approaches do not show significant finite sample performance decline relative to the baseline, which here is an oracle. With unequal treatment constraints, we further obtain asymptotic efficiency gains from pooling (Appendix D.1).

We notice that using the discretized covariate in place of for both design and estimation, as in Hahn et al., (2011), leads to a substantial loss of efficiency. Indeed, when the (asymptotic and simulated) variance of the estimator is more than double that of our baseline under the homoskedastic DGP, both asymptotically and in our finite sample simulations. This efficiency loss occurs because the discretized explains much less of the variation in the potential outcomes than the original . We expect greater precision losses from this discretization at the estimation stage when the variance functions vary substantially within the strata defined by .

For the heteroskedastic DGPs, we see modest asymptotic efficiency gains from both pooling and design. Design using the flexible base propensity class leads to about a 2.4% asymptotic efficiency gain for both and , while pooling provides an additional 1–2% gain. These small asymptotic gains appear to be largely canceled out at our sample sizes by the finite sample variability in learning propensity scores, limiting the net finite sample gains from design. Of course, with greater heteroskedasticity and/or differences between and , we would expect greater efficiency gains from design; in our simulations we have chosen to keep these differences within common ranges in social science studies as per Blackwell et al., (2022).

6.2 Partially linear model

Unlike for estimating , for estimating , we see clear efficiency gains over the baseline from design when (Table 2). For instance, the linearly aggregated estimator exhibits a 5.6% asymptotic efficiency gain as a result of the flexible design; replacing this with the pooled estimator then yields a total asymptotic gain of 10.0% over the baseline, even in the homoskedastic DGP. The analogous gains for the heteroskedastic DGP are slightly larger. We once again observe a substantial finite sample benefit to pooling, with the simulated relative efficiency of the approaches using the pooled tending to be larger than the asymptotic relative efficiency. We attribute this to both improved use of nuisance estimates by the pooled estimator (as in the ATE case) as well as a more fundamental finite sample efficiency boost due to the fact that the asymptotic variance is not exact for the oracle pooled in finite samples, whereas is exact for ; see Appendix D.2. When , design introduces some more salient finite sample variance from the errors in the concave maximization procedure. This is offset in both the homoskedastic and heteroskedastic DGPs by the asymptotic gains from the flexible design, so that when is used, the flexible design ultimately performs similarly to the simple RCT in finite samples.

Even if we use and hence the original covariate(s) in the final estimation step,

we see that the “binned” design which uses only for choosing the second batch propensity score

struggles to learn a substantially better propensity score than the simple RCT in all DGPs.

Indeed, in the heteroskedastic DGP with ,

we see a 2.1% asymptotic efficiency loss relative to the baseline from using the binned design.

By comparison, there is an 11.2% asymptotic efficiency gain from using the flexible design.

The efficiency loss can occur with the binned design because the objective in (27) changes when working in terms of the discretized covariate instead of .

In other words, even though the simple RCT propensity is within the class of propensities that can be chosen by the binned design,

it is worse according to the binned objective based on ,

but not according to the objective based on the original .

| DGP | Estimator | Design | Sim. rel. eff. (90% CI) | Asymp. rel. eff. |

|---|---|---|---|---|

| , Homoskedastic | Flexible | 1.150 (1.103, 1.198) | 1.100 | |

| Binned | 1.057 (1.009, 1.107) | 1.026 | ||

| Simple RCT | 1.038 (1.018, 1.058) | 1.000 | ||

| Flexible | 1.049 (1.016, 1.083) | 1.056 | ||

| , Heteroskedastic | Flexible | 1.310 (1.214, 1.412) | 1.112 | |

| Binned | 1.049 (0.972, 1.133) | 0.979 | ||

| Simple RCT | 1.084 (1.014, 1.159) | 1.000 | ||

| Flexible | 0.983 (0.880, 1.076) | 1.073 | ||

| , Homoskedastic | Flexible | 1.229 (1.203, 1.256) | 1.023 | |

| Binned | 1.177 (1.147, 1.206) | 1.000 | ||

| Simple RCT | 1.228 (1.204, 1.251) | 1.000 | ||

| Flexible | 1.023 (1.011, 1.035) | 1.019 | ||

| , Heteroskedastic | Flexible | 0.997 (0.963, 1.032) | 1.071 | |

| Binned | 0.932 (0.899, 0.965) | 1.002 | ||

| Simple RCT | 0.982 (0.952, 1.014) | 1.000 | ||

| Flexible | 0.969 (0.942, 0.996) | 1.060 |

7 Discussion

We view our primary technical contribution in this paper to be a careful extension of the double machine learning framework that enables both estimation and design in batched experiments based on pooled treatment effect estimators. This allows the investigator to take advantage of the efficiency gains from pooling and design without needing to make strong parametric assumptions or to discretize their covariates. As our numerical study in Section 6 shows, the latter can more than wipe out any efficiency gains from design.

Related to our work is the extensive literature on combining observational data with a (single batch) randomized experiment.

In that setting a primary concern is mitigating bias from unobserved confounders in the observational data (Rosenman and Owen,, 2021; Gagnon-Bartsch et al.,, 2023).

By contrast,

in our setting unconfoundedness holds by design in each batch of the experiment.

It would be useful to examine if the ideas from the present work can be extended to the observational setting where confounding bias is a concern.

Acknowledgments: The authors thank Stefan Wager, Lihua Lei, and Kevin Guo for comments that improved the content of this paper. H.L. was partially supported by the Stanford Interdisciplinary Graduate Fellowship (SIGF). This work was also supported by the NSF under grant DMS-2152780.

Appendix A Nonstationary batches

Assumption 2.1 in the main text supposes the distribution of the covariates and potential outcomes is stationary across batches . Here we relax that assumption. Let be the distribution of the vector in batch , now allowed to vary across batches (in the main text it is assumed that ). Then we have the following relaxation of Assumption 2.1:

Assumption A.1 (Relaxation of Assumption 2.1).

Now letting be the mixture distribution , we introduce the notation , which denotes an expectation under the distribution on induced by and for any propensity and . The notation refers to the corresponding marginal distribution of the covariates . Then the score equation (5) will be generalized to

| (47) |

which we will require to identify in each batch:

Assumption A.2 (Relaxation of Assumption 2.2).

Equation (47) encodes a requirement that the same parameters and satisfy the score equations for all batches ; to ensure this, we require those parameters to be stationary across batches. For instance, for ATE estimation with the score , we require the conditional mean functions to be stationary across batches. For estimation under the partially linear model with the score , we also require the outcome variance functions to remain stationary. However, in both cases the covariate distribution can otherwise vary arbitrarily across batches, as can higher moments of the conditional distributions of the potential outcomes given the covariates .

Due to the possibility of covariate shift, the relevant mixture propensity scores are now

| (48) |

These definitions generalize (9) and (10). Here denotes the marginal distribution of when . When there is no covariate shift, we have for all and we recover (9) and (10) in the main text. The expressions in (48) are derived using Bayes’ rule as the conditional probability that given when is drawn uniformly at random from the pooled collection of observations in a non-adaptive batch experiment with propensities .

Where indicated, we are able to generalize various results in Sections 3 and 4. The generalized results are as stated in the main text, if we make the following changes to the notation and assumptions:

- 1.

- 2.

-

3.

Any expectations of the form without subscripts are interpreted as being taken under the distribution on .

-

4.

Any expectations of the form are interpreted as being taken under the distribution on , and any expectations of the form are interpreted as being taken under the distribution on .

Appendix B Technical lemmas

Here we give some technical lemmas used in our proofs.

B.1 Asymptotics

Definition B.1.

For any sequence of random vectors and constants , we write if . We write if for every , .

Lemma B.1.

Let be a sequence of random vectors and be a sequence of -algebras such that . Then .

Proof of Lemma B.1.

Fixing , we have for all . Taking conditional expectations given on both sides we have

| (49) |

Thus if we have as well. But is uniformly bounded so its expectation converges to zero, i.e., . Since was arbitrary we conclude that . ∎

Lemma B.2.

if and only if for every sequence we have as .

Proof of Lemma B.2.

Fix and . If then there exists such that . Since eventually we conclude as well. With arbitrary, the result follows. Conversely now suppose we do not have . Then there exists such that for all . Defining , this ensures that for each , there exists so that . But then for , we have yet for all so does not converge to 0 as . ∎

We now state an important result in empirical process theory in our proof of Lemma 5.2 above. For a metric space , let be the -ball around . For any set , the covering number of is then defined as the smallest number of -balls in whose union contains . For a subset of the space of -square integrable real-valued functions on with , control over the logarithm of the covering numbers of (the metric entropy) over a variety of radii under the random metric given by implies control of the empirical process where for any measure on . Here is the empirical probability measure on observations . This result is due to a “chaining” argument of Dudley, (1967). We restate a more direct version of this result below, which is Lemma A.4 of Kitagawa and Tetenov, (2018).

Lemma B.3.

For a class of -measurable functions with , there exists a universal constant such that for the empirical distribution of ,

Remark B.1.

Often, control of the right-hand side in the previous display is shown by controlling

where the supremum is taken over all finitely supported probability measures . See Sections 2.5 and 2.6 of van der Vaart and Wellner, (1996) for further discussion.

We also make use of the following elementary results on covering numbers.

Lemma B.4.

Let be a collection of functions contained in the class . Let for some and with continuous on and for some , where denotes the partial derivative of with respect to the first argument. Then for all probability distributions on and , we have .

Proof of Lemma B.4.

Fix and a probability distribution on . For each let for each , so that . Suppose is an -cover of in the norm. WLOG we can assume that each is a member of . Then for each , by the uniform bound on we have

so that is a cover of in the norm. ∎

Lemma B.5.

Let be a collection of functions contained in the class . Define . Then for every and probability measure on we have

| (50) |

Proof.

Fix and a probability distribution on . Define the collection . Suppose is a cover of in the norm. Then the collection is a cover of in the norm, since for any there exist such that and so

showing that . But by applying Lemma B.4 with and (hence we can take ) we have for all . Chaining together the inequalities preceding two sentences establishes (50). ∎

B.2 Miscellaneous

Here we have some standalone technical lemmas. Their proofs do not depend on any of our other results.

Lemma B.6.

Suppose and are mean zero random vectors in p with finite second moments where has full rank. Then

Proof of Lemma B.6.

For any matrix we have , hence

Taking yields the desired result. ∎

Lemma B.7.

If is a random vector where are independent with mean 0 and finite second moments, then .

Proof of Lemma B.7.

By assumption we have for , so

∎

Appendix C Proofs

Here we collect proofs of the formal results stated in the main text; some are generalized to allow for some nonstationarities across batches, as described in Appendix A.

C.1 Proof of Proposition 3.1: CLT for oracle

The CLT of Proposition 3.1 for our oracle pooled estimator holds under the numbered generalizations in Appendix A without further restrictions; here we prove this more general proposition. It is helpful to begin by noting that , which shows, for instance, that for any -integrable function

By score linearity (4) we can write

| (51) |

whenever exists. Defining

we have from (3) and the law of large numbers that

| (52) |

Then the third equality follows because

by Lemma B.1 and condition 1 of the Proposition, noting that

for . Invertibility of from condition 2 ensures that is well-defined with probability tending to 1 by (52).

Next, we fix with and a batch . Define

where . Evidently the random variables are independent, with for all by (47), and . Furthermore we have

for all sufficiently large and some by condition 3. Then by the Lyapunov CLT we have

as . Therefore

and since was arbitrary,

With the left-hand side of the preceding display independent across batches , we have

| (53) |

With

C.2 Proof of Corollary 3.1: CLT for

Corollary 3.1, which applies Proposition 3.1 to prove a CLT for the oracle estimator of , holds under the numbered generalizations of Appendix A under one additional condition: that the mean functions are stationary, meaning for all , , and . This condition is needed to ensure Assumption A.2 holds, as discussed in Appendix A.

Our proof proceeds by showing that the conditions of the Corollary imply the conditions of generalized Proposition 3.1 proven in the previous section with and . That is, first we show Assumption A.2 is satisfied with and . Then we show the three numbered conditions in Proposition 3.1.

First, for brevity let , and note that for any , we have

using unconfoundedness and stationarity of the mean function. All the necessary expectations exist by our assumption that . Hence Assumption A.2 is satisfied. Next we show the conditions of Proposition 3.1:

-

1.

Trivially we have

Next we compute the following for each :

Plugging in gives, by Minkowski’s inequality, that

where

By an analogous computation

The result now follows because

and hence

This bound only uses the fact that propensities are bounded between 0 and 1, so

(54) -

2.

Evidently is invertible. Additionally for we have by the moment conditions in Assumption 3.1 so

Now is the sum of the following terms:

These are all square integrable, because , , and are all uniformly bounded.

-

3.

From for by Assumption 3.1, we have

Then each of

is at most and the desired condition holds by Minkowski’s inequality.

Now we can apply Proposition 3.1, to conclude where

The third equality in the preceding display follows by noting that the three cross terms in the expansion of the square have mean zero. The first two vanish by conditioning on and the third because .

C.3 Proof of Corollary 3.2: CLT for

Here we prove Corollary 3.2, the CLT for the partial linear estimator of the regression parameter under the linear treatment effect assumption (6). This Corollary holds under the numbered generalizations of Appendix A with the additional condition that the mean and variance functions are stationary. That is, we have and for all , , and . This condition is needed to ensure Assumption A.2 holds.

As in the proof of Corollary 3.1, we first show that Assumption A.2 holds with , estimand , score , and nuisance functions lying in the nuisance set . Then we show that the three numbered conditions in Proposition 3.1 hold.

Fix . For each ,

hold by the unconfoundedness and SUTVA assumptions. Hence by (6),

| (55) |

Thus for any ,

after conditioning on and applying (55). Integrability is not a concern because for . Thus Assumption A.2 is satisfied.

Now we consider the numbered conditions of Proposition 3.1 in turn.

- 1.

-

2.

For invertibility of , we compute

With positive definite by assumption, is strictly negative definite and hence invertible.

For boundedness of with , we compute

-

3.

For boundedness of with ,

where the final inequality follows from Minkowski’s inequality and Jensen’s inequality as below:

We now compute

and

Finally, we apply Proposition 3.1 to conclude where

C.4 Proof of Theorem 3.1: Pooling dominates linear aggregation

Here we prove that the oracle pooled estimators and dominate the best linearly aggregated estimators and for estimating and , respectively. For , Theorem 3.1 generalizes to nonstationary batches as described in Appendix A. But for , the Theorem does not necessarily hold under the nonstationarities of Appendix A. For example, suppose that , is uniform on , and is the distribution with density on with respect to Lebesgue measure. Let and suppose for each . Then . We can however generalize the ATE result to the case of a multivariate outcome variable, i.e., , where the conditional mean and variance functions and take values in q and , respectively.

We begin by showing the result for ATE estimation. We have where we compute

by applying Corollary 3.1 to the observations in each single batch . Letting

for each , we have

Thus, to prove the desired result, it suffices to show is a concave (matrix-valued) function on . To that end, fix and . It suffices to show that is concave on , i.e., that for each . Because is continuous on , we need only show that for each . Letting and , we obtain

| (57) |

for

To get this, we reversed the order of differentiation and expectation, which is justified by the regularity conditions in Assumption 3.1.

C.5 Proof of Theorem 4.1: CLT for feasible in a CSBAE

Here we prove the CLT for the feasible estimator in a CSBAE. It holds under the nonstationarity conditions described in Appendix A.

We begin by constructing the non-adaptive batch experiment in the statement of the theorem. Define the counterfactual treatment indicators via

for . Then the observations in the counterfactual non-adaptive batch experiment are the vectors , where

The corresponding oracle estimator from (11) is then

Because , conditions 1, 2, and 3 of Proposition 3.1 are satisfied for this counterfactual non-adaptive batch experiment by equations (22), (23), and (25) along with condition (a) of Assumption 4.1. Hence the oracle CLT holds with as in the conclusion of Proposition 3.1.

It remains to show that

where

as in (18). To do so, we show that the following intermediate quantity

satisfies both and .

C.5.1 Showing that

To show , for each fold let be the total number of observations in fold across all batches . Also define the quantity

where

For each , let be the event that . This is measurable and as by assumption. Then for all sufficiently large ,

by equation (22). The second inequality above uses the fact that , are nonrandom given , but the vectors in fold are independent of and i.i.d. from ; the third inequality follows because

| (58) |

for all by the definitions of and . Then by Lemma B.1. This immediately shows for all folds and so

| (59) |

too. Now recall the identity

| (60) |

for any invertible square matrices of the same size. By (52) we know that

| (61) |

and hence

are both . The preceding display along with (59) and (60) show .

Equations (59) and (61) immediately imply that , while (C.1) implies that . It remains to show . To that end we consider the quantity

where for each

To see that , we write

Now

is twice continuously differentiable on by regularity. Hence by Taylor’s theorem

| (62) |

By (21) we know that

With , by (20) and (62) we conclude that that

Recalling that , we have and

Using from (3) we have

as

| (63) |

Thus we have shown . Finally, for each batch , the quantity is a sum of random variables that are i.i.d. and mean 0 conditional on . Thus by Lemma B.7, we have

where for each such that we’ve defined

| (64) | ||||

and used the basic variance inequality

| (65) |

for any random vector and -algebra . Hence by (58), Minkowski’s inequality, and then (23), we have

Thus by Lemma B.1. With

we conclude that , as desired. This establishes that .

C.5.2 Showing that

To establish that , similar to above we write

where

We will show that , , , and . First we define

where the term for each fold is decomposed into a sum over batches :

Here

satisfies

by the Cauchy-Schwarz inequality. Recalling the -algebra in the definition of a CSBAE (Definition 4.1), we have

and so by (17)

Hence

by Lemma B.1. Next, for and , by Jensen’s inequality and (58) we have

by (25). By Markov’s inequality, for each batch and fold ,

holds for . Applying Minkowski’s inequality with the norm shows

We conclude , hence and as well. Now we recall

Then

as well. Thus we have both

| (66) |

Subtracting these two equations gives .

Next, equation (66) immediately provides , while as shown above. Thus it only remains to show that . We write

where

| and | ||||

It suffices to prove that for each , the terms , , and are all asymptotically negligible. First, we have

We briefly justify each of the equalities in the preceding display:

-

•

The first equality holds because given , the only randomness in for any is in , which is independent of , , and ; hence

(67) -

•

The second equality holds because the vectors are mutually independent (Assumption A.1).

-

•

The third equality follows directly from (19).

For batches , the vectors are conditionally independent given . Defining

and letting be the real solution to , we apply Lemma B.7 and Holder’s inequality to get

using the conditional independence in (67) once again. Then

We can assume WLOG that so that . Then with for all , we conclude

| (68) |

by (17). Next, from Jensen’s inequality

But by Minkowski’s inequality, (58), and (25), we see

We conclude by Markov’s inequality that

Along with (68) we can conclude that by Lemma B.1. Then also

Next, for define

so that . Then by the triangle inequality is no larger than

Taking conditional expectations of both sides yields

by Cauchy-Schwarz. We have by (17) that

Then by equation (26), we get for , and so as well.

Finally, we write

for

| where | ||||

For each , we have

| (69) |