On Deterministically Approximating Total Variation Distance

Abstract

Total variation distance (TV distance) is an important measure for the difference between two distributions. Recently, there has been progress in approximating the TV distance between product distributions: a deterministic algorithm for a restricted class of product distributions (Bhattacharyya, Gayen, Meel, Myrisiotis, Pavan and Vinodchandran 2023) and a randomized algorithm for general product distributions (Feng, Guo, Jerrum and Wang 2023). We give a deterministic fully polynomial-time approximation algorithm (FPTAS) for the TV distance between product distributions. Given two product distributions and over , our algorithm approximates their TV distance with relative error in time .

Our algorithm is built around two key concepts: 1) The likelihood ratio as a distribution, which captures sufficient information to compute the TV distance. 2) We introduce a metric between likelihood ratio distributions, called the minimum total variation distance. Our algorithm computes a sparsified likelihood ratio distribution that is close to the original one w.r.t. the new metric. The approximated TV distance can be computed from the sparsified likelihood ratio.

Our technique also implies deterministic FPTAS for the TV distance between Markov chains.

1 Introduction

The total variation distance (TV distance), which is also known as the statistical difference, is a fundamental metric for measuring the difference between two probability distributions. For two distributions and over the sample space , their TV distance is defined by

The TV distance is essentially the -norm of the difference, and can also be characterized as the discrepancy of the optimal coupling between and [MU17]. The TV distance connects to many statistical distances including the relative entropy and other well-studied divergences [PW22].

This paper studies the computational problem of TV distance. The problem is particularly interesting when both and are high-dimensional distributions that admit succinct descriptions. However, computing (even approximating with additive error) the TV distance is known to be hard for general distributions. The seminal work of Sahai and Vadhan [SV03] proved that deciding whether two distributions given by Boolean circuits are “close” or “far-apart” w.r.t. TV distance is a complete problem in SZK (Statistical Zero Knowledge). SZK-complete problems are often believed to be computationally hard [BCH+20]. Many works studied the complexity of computing the TV distance for specific classes of distributions [LP02, CMR07, Kie18, BGM+23]. One of the simplest situations is when and are both product distributions over the sample space , where is a finite domain and is the dimension. Recently, Bhattacharyya, Gayen, Meel, Myrisiotis, Pavan and Vinodchandran [BGM+23] proved a surprising result: the exact computing of the TV distance between two product distributions is -complete, even in the Boolean domain ().

The hardness result motivates the study of approximation algorithms for the total variation distance between two product distributions. The algorithm is required to estimate the TV distance within relative error. Previous works mainly focused on randomized approximation algorithms, which find a good estimation with probability at least . The first polynomial-time randomized approximation algorithm was given in the preprint version of [BGM+23], but it only works for a restricted class of product distributions. Later on, Feng, Guo, Jerrum and Wang [FGJW23] gave a randomized algorithm for general product distributions. The algorithm runs in time .

All algorithms mentioned above are based on the Monte Carlo method. One natural question is how to design deterministic approximation algorithms. Very recently, in the conference version111Link to the paper: https://www.cs.toronto.edu/~meel/Papers/ijcai23-bggmpv.pdf of [BGM+23], authors strengthened their randomized algorithm into a deterministic one. However, the algorithm still requires some restrictions on the input distributions, i.e., the domain needs to be Boolean and has a constant number of distinct marginals (e.g., can be the uniform distribution). The major open question is to give a deterministic approximation algorithm that works for general product distributions. We answered this question affirmatively.

Theorem 1 (TV distance between product distributions) There exists a deterministic algorithm such that given two product distributions over and , it outputs satisfying in time .

In the above theorem, both and are described by their marginal distributions and each marginal distribution is given in binary. We remark that the term in running time is always a polynomial with respect to the input size. Moreover, our algorithm is faster for product distributions with larger total variation distances. The approximated TV distance returned by our algorithm is always a lower bound of .

Our technique can be extended to more general high-dimensional distributions with “limited” dependency. One example is the distribution of the Markov chain trajectory. Let be the joint distribution of a random vector , where follows the initial distribution and each is generated based on a Markov kernel that specifies the distribution of conditional on . We call the distribution of an -step Markov chain222The Markov chain has the state space as each , but is a distribution over the sample space .. Given two -step Markov chains and , we can also approximate their TV distance in polynomial time.

Theorem 2 (TV distance between -step Markov chains) There exists a deterministic algorithm such that given two -step Markov chains in state space and , it outputs satisfying in time .

We remark that our algorithm estimates the TV distance between the joint distributions of and rather than the TV distance between the distributions of and . The latter is trivial because the marginal distribution of (also ) can be computed by simple matrix multiplications. But estimating is non-trivial because the sample space is exponentially large. Our result is related to the problem of comparing two labelled Markov chains. See Section 1.2 for a detailed discussion.

1.1 Technical Overview

Let be two distributions over a sample space , their total variation distance is well known to equal the maximal advantage of distinguishing between and . Say a distinguisher is given a sample from either or and is asked to guess which distribution is sampled from. The distinguisher can be formalized as a randomized algorithm (or a Markov kernel) from to . The probability that the distinguisher outputs 0 under hypothesis (resp. ) can be written as (resp. ). The difference between them is called the advantage. The maximal advantage equals the total variation distance

and the optimal distinguisher who maximizes the advantage, is the likelihood ratio test

where is called the likelihood ratio. The likelihood ratio is an important tool in information theory [PW22]. It is particularly useful when is sampled from or from .

In this paper, we formally define the likelihood ratio as a distribution, denoted by , such that . In other words, is the distribution of where .

As we will discussed in Section 3, the likelihood ratio distribution (or “ratio” in short) contains all the “useful” information about . For example, , so we can denote the distance by . For the task of computing the total variation distance, it suffices to compute .

Given two product distributions and , their ratio

is the distribution of , where are independent and . This suggests a naïve algorithm to compute the total variation distance.

-

•

Compute for each .

-

•

Compute .

-

•

Output .

Here denotes the distribution of where are independently sampled from . The naïve algorithm computes the exact value of total variation distance, but has exponential time and space complexity, because the support of can be exponentially large.

To contain the complexity blow-up, our actual algorithm computes an approximation of . The high-level framework of our algorithm looks as follows.

-

•

Compute for each .

-

•

Compute . Then sparsify it as .

-

•

Compute . Then sparsify it as .

-

-

•

Compute . Then sparsify it as .

-

•

Output as an approximation of .

In our algorithm, the sparsification subroutine plays a central role: a given complicated ratio is sparsified into a simpler one that is “close to” the given ratio. The closeness is formalized as a new metric. For the correctness of our algorithm, the metric should satisfy a few properties: i) triangle inequality, if and , then ; ii) if , then ; iii) if , then . Then correctness is guaranteed as follows:

then by triangle inequality, ; therefore .

We say two ratios are close, if there exist distributions satisfying , such that (resp. ) is close to (resp ) with respect to the TV distance. In such case, () must be close to () due to the triangle inequality of the TV distance. This inspires us to consider the minimum total variation distance,

In Section 3.1, we show that is a metric between ratios.

In the rest of this overview, we briefly describe how the sparsification subroutine works, and why the sparsified ratio is close to the original ratio with respect to the minimum total variation distance.

The sparsification subroutine takes a ratio as the input. The ratio can be represented by a table of entries , each entry represents . If the table has too many entries, then some of them must be close together. Say are very close together in the sense that , where is a sufficiently narrow interval. W.l.o.g., assume , and the case inside is symmetric. The sparsification subroutine “merges” these entries into one entry. The sparsified ratio is represented by table We claim that is close to with respect to the minimum total variation distance .

Define two distributions over sample space as

so that . Consider distribution that is the same as except

Then , this also ensures that is a valid ratio. By definition, . Since , we have being small for all . Quantitatively, say interval is sufficiently narrow means . Thus we have for all , and the error introduced by merging is bounded by .

The actual sparsification subroutine picks a collection of disjointed sufficiently narrow intervals333The last interval is not sufficiently narrow because its right endpoint is 1, and has to be analyzed separately. that jointly cover , then merges all the entries that lie in the same interval. The total error introduced by merging is bounded by

Symmetrically, the error introduced by merging within is also bounded by .

1.2 Related Works and Open Problems

The TV distance between two labelled Markov chains (LMC, a.k.a. hidden Markov chain) has been studied by previous works [LP02, CMR07, Kie18]. It was proved that for LMCs, computing TV distance within -additive error, where is given in binary, is #P-hard [Kie18]. The Markov chains we studied in Theorem 2 is not hidden, which is equivalent (by a polynomial-time reduction) to the deterministic acyclic LMCs in [Kie18]. Kiefer [Kie18, Theorem 10] gave a randomized algorithm that approximates the TV distance between (not necessarily deterministic) acyclic LCMs with additive-error , where the algorithm succeeds with probability at least and the running time is . Compared with our result, Kiefer’s algorithm works for more general distributions but for deterministic acyclic LMCs, our algorithm is deterministic and achieves stronger relative-error approximation.

Some works [CDKS18, BGMV20] studied the problem of computing TV distances for structured high-dimensional distributions, e.g. Bayesian networks, Ising models and multivariate Gaussian distributions. Some randomized approximation algorithms were discovered, but they only achieved an additive-error approximation. One open problem is to find efficient deterministic approximation (with additive or relative error) algorithms for those distributions. Our technique relies on a strong conditional independence property of the distribution. We wonder whether one can relax this restriction and make our technique work for more general graphical models.

Our technique for approximating the TV distance is different from the previous ones. Previous randomized algorithms [Kie18, CDKS18, BGMV20, FGJW23] are all based on the Monte Carlo method. For the deterministic approximation of the TV distance between two product distributions, the algorithm in [BGM+23] first reduces the problem to the approximate counting of knapsack solutions (#Knapsack) and then solves the #Knapsack by existing deterministic approximation algorithms [GKM10, SVV12]. We introduce a new sparsification technique together with a new metric called minimum total variation distance, which is of independent interest.

2 Notations

We use to denote the set for any positive integer . We use to indicate whether the condition (or event) holds.

We use to denote the infinity point, which is an extended real number. For any , let , and .

This paper only considers discrete distributions. Distributions are denoted by calligraphic letters (e.g., ). A discrete distribution over a sample space can be defined by its probability mass function . For each , the value is the probability that is sampled from . We use to denote the support of , which refers to . Let denote that random variable follows distribution . For each subset , we use the conventional notation to denote the probability that a sampling from falls in set . That is, .

For any two distributions , let (or ) denotes the distribution of , let denotes the distribution of , where are independent random variables satisfying respectively.

A Markov kernel from sample space to sample space is a function , such that for any , function is a distribution over . For any distribution over , let denote the distribution over that . Their semidirect product, denoted by or , is a distribution over that .

3 Likelihood Ratio as a Distribution

Given two distributions over a sample space , people call the likelihood ratio for . We introduce a notation for the distribution of the likelihood ratio.

Definition 1 (Ratio).

Let be two discrete distributions over a sample space . The likelihood ratio distribution (or ratio, in short) between , denoted by , is a distribution over .

Equivalently, the distribution can be defined as follows: sample random variable , define as the distribution of . Note that the denominator is always non-zero because is sampled from . In the paper, we typically denote the ratio distribution by .

Not every discrete distribution over is the ratio between some two discrete distributions. We say is a valid ratio if there exist two discrete distributions such that .

Proposition 2.

A discrete distribution over is a valid ratio if and only if .

Proof.

Suppose , then .

On the other hand, if , define distribution over as

| (1) |

It is easy to verify that is a distribution and . ∎

Definition 3 (Canonical Pair).

For any valid ratio , define its alternative ratio, denoted by , as the distribution in (1). We call the canonical pair of .

We can define another natural distribution of likelihood ratio

Its sample space has to be extended to , because the denominator can be zero. It is easy to verify that implies .

Proposition 4.

for any discrete distributions .

Proof.

Let . Define , then . Since are independent, are also independent. Define , then . ∎

The likelihood ratio is a well-studied concept. Almost all statistical distances and divergences between and can be derived from their ratio . The derivation of the total variation distance is shown in the following proposition. The cases of other distances and divergences can be found in most information theory textbooks (e.g. [PW22]).

Proposition 5.

Let , then , where

Proof.

∎

It comes as no surprise how ratio can derive these distances and divergences. In some sense, ratio is a complete characterization of the decision problem between and .

- Sufficient Statistic.

-

Say random variable is sampled from either or . Whether is sampled from or is the hidden parameter of the statistical model. Consider a statistic where . If the hidden parameter is , then ; otherwise, . That is, , . It is well known that is a sufficient statistic containing all the “useful” information of . There exists a Markov kernel who recovers the entire information of from , such that , . So the problem of distinguishing is equivalent to the problem of distinguishing .

- Equivalent Decision Problems.

-

In decision theory, the equivalence relationship between decision problems are formalized. Two decision problems and are called equivalent, if there exist Markov kernels such that [LC12]. It is easy to verify that they are equivalent if and only if . If direction: let , then both and equivalent to the canonical pair . Only if direction is ensured by a new metric defined in Section 3.1. Thus can represent the equivalence class where is.

The above discussion inspires us to consider the “data processing” relation. Say decision problem is stronger than , denoted by , if and only if there exists a Markov kernel such that , . This relation is almost an order relation [LC12], satisfying reflexivity, transitivity and antisymmetry w.r.t. the equivalence relation between decision problems

Therefore, it induce an order relation between ratios.

Definition 6.

For any two ratios , we say “ is stronger than ”, denoted by , or “ is weaker than ”, denoted by , if there exists distributions and a Markov kernel such that and .

It captures the “data processing”: is the process, are the post-processing distributions. Therefore, by the data processing inequality for TV distance, .

Proposition 7.

For any ratios satisfying , , it holds that .

Proof.

There exist distributions and Markov kernels such that and . Then and . So it suffices to find a Markov kernel such that , . The required Markov kernel is . ∎

3.1 Minimum Total Variation Distance

We introduce a metric between (valid) ratios, called the minimum total variation distance.

Definition 8 (MTV Distance).

For two valid ratios , the minimum total variation distance between them, denoted by , is defined as

We define as an infimum for safe. We cannot rule out the possibility that the minimum does not exist, unless the supports of and are finite (Lemma 9).

Lemma 9.

When the supports of ratios and are finite,

The lemma is proved by enforcing the search space of to be a tuple of distributions over a fixed finite domain. The proof is deferred to Appendix B.

The minimum total variance distance satisfies the following properties, as proved in Appendix B.

Lemma 10.

The minimum total variance distance is a metric.

Lemma 11.

For any two valid ratios , it holds that .

Lemma 12.

For any valid ratios ,

A very similar concept called Le Cam’s distance exists in decision theory. Here we present an equivalent definition restricting on the decision problems that has only two hypotheses.

Definition 13 (Deficiency and Le Cam’s Distance [LC12]).

For decision problems , the deficiency of with respect to is defined as

their Le Cam’s distance is .

Le Cam’s distance is a pseudo metric between decision problems. It is not hard to show that two decision problems have zero Le Cam’s distance if and only if . Therefore, Le Cam’s distance is a metric between ratios. We can similarly define deficiency between ratios.

For any two ratios , it holds that if and only if , and .

4 Sparsify the Likelihood Ratio

As discussed in Section 3, the ratio completely characterizes the problem of distinguishing and . Once the ratio is known, the distances between (including the TV distance) follow easily. The bottleneck is the complexity of computing and representing . We will store ratio as the table of values of its probability mass function, so the space complexity is proportional to the support size . When are described as product distributions, the size of can be exponentially large. Our solution is to simplify the ratio without introducing too much error. The process of simplification is called the sparsification of the ratio. The amount as error is measured by MTV distance (Definition 8).

Lemma 14 (Sparsification).

There exists a deterministic algorithm Sparsify as defined in (3). Given a valid ratio and two error bounds as inputs, it outputs a sparsified ratio in time , such that and .

The intuition behind the sparsification has been sketched in the technical overview (Section 1.1). We divide into a collection of disjointed intervals, then “merge” all the probability masses within one interval together. We formalized this process as SparsifyWrtIntervals (Algorithm 1). The support size of the sparsified ratio is no more than the number of disjoint intervals we choose. The running time equals the input ratio support size plus the number of intervals, assuming the ratio is presented by a sorted table and the intervals is also sorted.

As a warm-up, consider how does the sparsification process work on a single interval. Let be the canonical pair of , let be a sufficiently small interval. The sparsification of with respect to an interval works as follows:

If , the sparsification does nothing and . Otherwise, the sparsified ratio and its alternative are

where . Apparently .

To bound , consider the following two distributions

They satisfy . Therefore,

We should use the tighter one to bound .

Intuitively, is obtained by modifying at points ; is obtained by modifying at points . If the interval , then for all , thus modifying introduces less error, in other words, is a tighter bound of . Symmetrically, if the interval , is a tighter bound. This intuitive argument can be formalized by:

Consider the case , let be the endpoints of , so . Then can be upper bounded by one of the two following arguments:

-

•

If for all , then

By its similarity with , even if we sparsify the ratio with respect to many disjointed intervals, the total error is bounded by .

To ensure for all , the two endpoints should satisfy . Note that this cannot be satisfied if .

-

•

If for all , then

To ensure for all , the two endpoints should satisfy .

Based on the above observations, we choose the following partition of , which is a collection of disjoint intervals

in that order.

-

•

Let for every , where . Thus .

-

•

Let and let

(2) Thus .

Symmetrically, let for and let .

Putting the above intervals into SparsifyWrtIntervals (Algorithm 1) gives the Sparsify algorithm used in Lemma 14.

| (3) |

4.1 Proof of the Sparsification Lemma

This section proves the sparsification lemma (Lemma 14). The sparsified ratio for defined in Algorithm 1, thus . The support size of the sparsified ratio is no more than the number of intervals, which is . The running time is proportional to the number of intervals and the support size of the input ratio, which is . The rest of the section forces on bounding the error with respect to the minimum total variation distance.

For each , define as

Note that implies . Symmetrically, define as

The sparsified ratio and its alternative can be written as

To bound , consider the following two distributions, as inspired by the discussion of sparsification w.r.t. one interval,

Claim 15.

are well-defined distributions and .

Proof.

For each , . Thus

So is a distribution over . Symmetrically, , and is a distribution.

Say random variable ,

-

•

and .

-

•

and .

-

•

and .

Thus . ∎

Then is upper bounded by . Consider the two terms on the right hand side separately.

By how we choose the intervals, for each and any , we have

Therefore,

Symmetrically, for each and any , we have

due to the choice of intervals. Then can be upper bounded by

The last equality symbol relies on

As the conclusion, .

5 Estimate TV Distance between Product Distributions

The two product distributions of interest are and , where are distributions over sample space . We present a deterministic algorithm that estimates the TV distance between and . The intuition has be explained in the technical overview (Section 1.1).

Theorem 1.

There exists a deterministic algorithm (Algorithm 2). Given two product distributions over and , it outputs an estimation satisfying , in time .

The algorithm starts by computing a relatively tight lower bound of the .

Claim 16.

.

Proof.

for every , thus .

Let be independent and is the optimal coupling of . Hence,

The algorithm then iteratively computes for up to . is an approximation of the “actual” ratio .

Claim 17.

For each , it holds that and .

Proof.

It is proved by induction on . The base case is satisfied as .

For larger , the inductive assumption is and . By the data processing inequality for TV distance, . By the nature of the sparsification process (Lemma 14), the sparsified ratio and

| (4) |

Then the inductive proof is concluded by

In the end, the algorithm outputs as an estimation of the TV distance. Since , we have

In the meanwhile, implies

The running time of our algorithm is dominated by the main loop. The support size of is bounded by , by Lemma 14. The support size of is at most times larger. The time complexity of computing is , which is the complexity of merging sorted list, each list of length . The time complexity of computing from is smaller. Thus the time complexity of each iteration is dominated by computing , and the total time complexity is .

6 Estimate TV Distance between Markov Chains

A Markov chain over can be represented by its initial distribution and Markov kernels such that . In the Markov chain setting, we use the conventional notation to denote the Markov kernel . As the notation suggested, if ,

for all such that .

Similarly, another Markov chain is represented by its initial distribution and Markov kernels . We give a deterministic FPTAS for the TV distance between and .

Theorem 2.

There is a deterministic algorithm (Algorithm 3) such that given two Markov chains over and an error bound , it outputs satisfying in time .

To present our algorithm, we introduce a few more notations, in particular, the conditional ratio between Markov kernels, which plays the central role in our algorithm.

The conventional notation denotes a Markov kernel from to , is defined as

As the notation suggested, if ,

for all such that . We use and to denote the derived distributions and respectively. That is

They can be viewed as the conditional distributions of and .

Then we can consider the ratio between and , defined as

This implicitly defines a Markov kernel from to , as formalized below.

Definition 18 (Conditional Ratio between Markov kernels).

For two Markov kernels from to , the conditional ratio between them, denoted as , is a Markov kernel from to , such that, if letting , for every

A valid conditional ratio over is Markov kernel from to , such that is a valid ratio for every ,

Conditional ratio plays the central role in our algorithm, as presented in Algorithm 3. The core of the algorithm is an iterative process computing an approximation of the conditional ratio for each . In each iteration step, to compute an approximation of , the algorithm need an approximation of from last iteration, and distributions from the inputs. We call this subroutine Concatenate, and it is defined and analyzed in Section 6.1.

an error bound

That is, for each

6.1 The Concatenation of Conditional Ratios

Given and , to compute the ratio , the naïve solution is to first compute the two joint distributions . This section shows that there is an alternative approach: first compute , then

can be computed from , and .

Let and set

then . What is the distribution of conditioning on ? Let denote this conditional distribution. Then is the distribution of

| (5) |

where is sampled from the distribution of conditioning on . In other words, . In such case, the distribution of the second fraction in (5) is . Therefore, can be simply computed from , and the wanted ratio is a weighted average of .

If we let denote the distribution of when , the above analysis can be written as one formula.

| (6) |

Lemma 19 (Concatenation).

There is a deterministic algorithm Concatenate inspired by (6). Given distributions over and a conditional ratio over , the algorithm outputs such that

for any sample space and any Markov kernels to satisfying .

If the support size of is less than for every , the support size of is no more than , the time complexity of Concatenate is bounded by .

Proof.

The correctness is ensured by (6).

The complexity bottleneck is to merge sorted lists, each list has up to elements. ∎

The concatenation process has a few nice properties. In particular, concatenation preserves the order relation (Definition 6) and does not increase minimum total variation distance.

Lemma 20.

For any conditional ratios over such that for every , for any distributions over , it holds that

Proof.

Since for every , there exist a sample space , distributions over , and a Markov kernel from to such that

Define sample space , Markov kernels from to as

Then and . So the two sides of the wanted inequality equal and respectively.

Define a Markov kernel from to itself as

Intuitively, the distribution of conditioning on is to set and sample according to . It is easy to verify that and . Therefore,

6.2 A Lower Bound for TV Distance

Similar to the case of product distributions (Section 5), our algorithm approximating the TV distance between Markov chains needs a relative tight lower bound to start with.

Lemma 21.

There exists an deterministic algorithm such that given two Markov chains and over , it returns satisfying in time .

Proof.

Define . For each , define distribution .

Thus . By the triangle inequality,

For any , it holds that

Therefore, satisfies the requirement if it is defined as

Note that, can be computed in time because

and we can compute all in time. (Here denote the -th marginal distribution of , which can be recursively computed by .) ∎

6.3 Analysis of our Algorithm

First analyze the time complexity. Let denote an upper bound of the support size of every sparsified ratios generated by Sparsify. The support size of each concatenation ratio is bounded by . The complexity is dominated by calls to Sparsify and calls to Concatenate. Each Sparsify call takes at most time, each Concatenate call takes at most time. Thus the total time complexity is bound by .

Let , denote the actual ratio and conditional ratio

Our algorithm recursively computes a good approximation of for smaller and smaller . In the end, the our algorithm computes , which is an approximation of , satisfying and . Thus is a sufficiently good approximation of .

In the proof, we use the conventional notation to denote the marginal distribution of the -th coordinate of . It can be recursively defined by . The conventional notation is a Markov kernel specifying the distribution of the -th coordinate conditioning on the -th coordinate.

Claim 22.

For every , the conditional ratio satisfies for all . The ratio satisfies .

Proof.

There is an inductive proof from larger to smaller . The base case is when . The base case follows trivially from the fact that .

Claim 23.

The ratio in Algorithm 3 satisfies .

We present a rather intuitive proof here. A more formal proof is given in Appendix A.

Proof.

Image that there are hybrid worlds, numbered by . In the -th hybrid world, we modify how Algorithm 3 works.

- The -th hybrid world

-

consider a modified algorithm that skips the sparsification step in the main loop for every index . In other words, let for every . To avoid confusion, we use to denote this value for every , we use to denote the value of in the -th hybrid world.

The 1st hybrid world is identical to the real world, thus . The last hybrid world is “ideal” in the sense that there is no error introduced by sparsification, thus . To bound the MTV distance between and , it suffice to prove for every ,

Comparing the -th and -th hybrid worlds, the only difference is whether the sparsification step is skipped when . In the -th hybrid world, . In the -th hybrid world, is the sparsification of . By Lemma 14,

So there exist Markov kernels , , , from to a sample space satisfying

| (7) | |||

| (8) |

Inspired by these distributions, we define some extra artificial hybrid worlds:

- The * hybrid world

-

is a truncated version of the -th hybrid word. In this hybrid worlds, the algorithm sets according to (7) and the rest of the computation is the same as the -th hybrid word. In this hybrid world, the algorithm will also compute .

By its definition, the algorithm computes the exact ratio between

- The ** hybrid world

-

is a truncated version of the -th hybrid word. In this hybrid worlds, the algorithm sets according to (7) and the rest of the computation is the same as the -th hybrid word. In this hybrid world, the algorithm will also compute .

By its definition, the algorithm computes the exact ratio between

Therefore,

The right-hand side of the inequality is bounded by

The first inequality symbol follows from formula (8). The second inequality symbol relies on

Acknowledgement

Weiming Feng would like to thank Dr. Heng Guo for the helpful discussions. Tianren Liu would like to thank Prof. Yury Polyanskiy for introducing us to the concepts of deficiency and Le Cam’s distance.

References

- [BCH+20] Adam Bouland, Lijie Chen, Dhiraj Holden, Justin Thaler, and Prashant Nalini Vasudevan. On the power of statistical zero knowledge. SIAM J. Comput., 49(4), 2020.

- [BGM+23] Arnab Bhattacharyya, Sutanu Gayen, Kuldeep S. Meel, Dimitrios Myrisiotis, Aduri Pavan, and N. V. Vinodchandran. On approximating total variation distance. In IJCAI, 2023. (to appear, preprint version in arXiv abs/2206.07209).

- [BGMV20] Arnab Bhattacharyya, Sutanu Gayen, Kuldeep S. Meel, and N. V. Vinodchandran. Efficient distance approximation for structured high-dimensional distributions via learning. In NeurIPS, 2020.

- [CDKS18] Yu Cheng, Ilias Diakonikolas, Daniel Kane, and Alistair Stewart. Robust learning of fixed-structure bayesian networks. In NeurIPS, pages 10304–10316, 2018.

- [CMR07] Corinna Cortes, Mehryar Mohri, and Ashish Rastogi. L distance and equivalence of probabilistic automata. Int. J. Found. Comput. Sci., 18(4):761–779, 2007.

- [FGJW23] Weiming Feng, Heng Guo, Mark Jerrum, and Jiaheng Wang. A simple polynomial-time approximation algorithm for the total variation distance between two product distributions. TheoretiCS, 2, 2023.

- [GKM10] Parikshit Gopalan, Adam Klivans, and Raghu Meka. Polynomial-time approximation schemes for knapsack and related counting problems using branching programs. arXiv preprint arXiv:1008.3187, 2010.

- [Kie18] Stefan Kiefer. On computing the total variation distance of hidden markov models. In ICALP, volume 107 of LIPIcs, pages 130:1–130:13. Schloss Dagstuhl - Leibniz-Zentrum für Informatik, 2018.

- [LC12] Lucien Le Cam. Asymptotic methods in statistical decision theory. Springer Science & Business Media, 2012.

- [LP02] Rune B. Lyngsø and Christian N. S. Pedersen. The consensus string problem and the complexity of comparing hidden markov models. J. Comput. Syst. Sci., 65(3):545–569, 2002.

- [MU17] Michael Mitzenmacher and Eli Upfal. Probability and computing: Randomization and probabilistic techniques in algorithms and data analysis. Cambridge university press, 2017.

- [PW22] Yury Polyanskiy and Yihong Wu. Information Theory: From Coding to Learning. Book draft, 2022.

- [SV03] Amit Sahai and Salil P. Vadhan. A complete problem for statistical zero knowledge. J. ACM, 50(2):196–249, 2003.

- [SVV12] Daniel Stefankovic, Santosh S. Vempala, and Eric Vigoda. A deterministic polynomial-time approximation scheme for counting knapsack solutions. SIAM J. Comput., 41(2):356–366, 2012.

Appendix A Another Analysis of our Algorithm in the Markov Chain Setting

This section presents an alternative analysis for bounding the error of Algorithm 3. It starts by introducing a finer characterization of the “difference” between two ratios.

Definition 24 (Region).

For any two ratios , define the feasible region of TV distance pair (or “region”, in short) between , denoted by , as

Region has many nice properties. It is more expressive than the minimum total variation distance. The later can be defined as the -distance between and the region.

We remark that, the current definition of is not special. For example, consider an alternative distance

This alternative distance, which is the -distance from , also works well with the paper. An early draft of this paper uses to analyze our algorithms.

For this paper, it is sufficient to have the following property. The proof is deferred to Appendix B.

Lemma 25 (Triangle Inequality).

For any ratios such that and , it holds that .

The description of this lemma uses a convenient notation , defined as follows. For any two points , in the Euclidean plane, we say if and . Apparently, this defines an order relation. Let be a point set in the Euclidean plane, we say if there exists such that .

Using the new concept of region, we gives a fine characterization of how the error passes through the concatenation process.

Lemma 26.

Given conditional ratios over , for any mappings such that for every , for any distributions over , it holds that

Proof.

Since for every , there exist a sample space , Markov kernels from to such that

The two ratios in the wanted inequality equal and respectively. Therefore444The expectation in the 3rd line of the following formula is written using an inconsistent but intuitive notation . If using the same notation as the rest of the paper, it should be written as .

Now we are ready to present an alternative error analysis of Algorithm 3.

Claim 27.

For every , the intermediate conditional ratio satisfies

for all . The ratio satisfies .

Proof.

There is an inductive proof from larger to smaller . The base case is when . The base case follows trivially from the fact that .

For every smaller , by Lemma 14, the error introduced by sparsifying is bounded by

which means

Combining with the inductive hypothesis that bounds by

using the triangle inequality (Lemma 25)

| (9) |

Note that, in the above formula, is the degenerated distribution that only samples . Then the inductive step is concluded by Lemma 26

| (10) |

In the special case when , by the same analysis as the first half of the inductive step, formula (9) holds. Then by an argument mostly similar555The argument will be exactly the same, if we define degenerated distributions over a size-1 sample space and define Markov kernels such that as and . to (10),

For each , we have

Symmetrically, . Therefore,

Appendix B Deferred Proofs

Proof of Lemma 9.

The key step of the proof is to enforce the search space of to be finite-dimensional. Concretely, we construct a finite set such that we can assume w.l.o.g. that is the sample space of distributions . That is,

| (14) |

Assume that we have found such a finite set satisfying equation (14), then the infimum symbol can be replaced by minimum, because the search space is a compact set and the TV distance is a continuous function. Thus to finish the proof, it suffices to (explicitly) construct and show (14).

The sample space is defined as

The desired (14) is implied by the following statement: for any discrete distributions over any sample space such that and , there exists distributions over such that , and

| (15) |

The distributions are constructed as follows. Define mapping as

Let be the distributions of where . By the data-processing principle, (15) holds. Now the only remaining task is to show , . By symmetry, it suffices to prove one of them.

For each such that (which implies ),

For each

Thus . ∎

Proof of Lemma 10.

It is easy to verify that and .

Positivity: Next, we verify the positivity property: if . If have finite-size supports, the positivity property is very easy to prove. Here we briefly present a proof without assuming finite-size supports.

The proof requires some basic knowledge of decision theory. In the decision problem between two distribution and , a distinguisher is given a sample that is sampled from either or , and is supposed to guess which distribution is sampled from. The distinguisher can be formalized as a randomized algorithm from the sample space to . It is well-known that TV distance can be defined as

The Neyman-Pearson region of the decision problem, denoted by , is defined as

Every Neyman-Pearson region satisfies the following properties.

-

•

The region is close and convex.

-

•

The region contains and .

-

•

The region is centrally symmetric: if and only if .

-

•

The region is determined by the ratio, and vice verse. Thus we can define the Neyman-Pearson region of ratio , denoted by , so that as long as .

Given any two distinct ratios , we have . Assume w.l.o.g. that . Since is close, there exists a constant such that for any .

For any satisfying , since , there exists a distinguisher such that

For any satisfying , let

Then

Therefore .

Triangle inequality: We will prove that for any ratios ,

By the definition of MTV distance, there exist666For this paper, we can assume have finite-size supports, then such distributions are guaranteed to exist (Lemma 9). Otherwise, the proof need a small modification. distributions over sample space such that

Similarly, there exist distributions over sample space such that

We are going to construct distributions such that

| (21) |

Then the proof will be concluded by

Intuitively, the distribution samples a pair of dependent random variables , such that and the distribution conditional on is the same as the distribution of conditional on . To formalize the intuition, we define a joint distribution .

where are defined as

Note that the probability mass function of equals

Thus there are two other equivalent interpretations:

-

•

First sample . Conditioning on , the distribution of is the same as the distribution of conditional on .

-

•

First sample . Conditioning on , and are independent, and the conditional distribution of (resp. ) is the same as the distribution of (resp. ) conditional on (resp. ).

Similarly, we can define a joint distribution as

Note that, if letting be the canonical pair of , the probability mass function of equals

We can define the conditional distributions so that and . That is, for any

Moreover, for any , we have for some , then

Thus we can define them so that . Similarly, we can let .

-

•

Let , then . In the meanwhile,

Thus .

-

•

By the data processing inequality for TV distance (use it twice)

The rest of properties in (21) can be verified similarly. ∎

Proof of Lemma 11.

For any such that , , we have

by triangle inequality. Thus

Proof of Lemma 12.

Consider any distributions satisfying for all . By Proposition 4, and . Thus

By the the triangle inequality,

Similarly, . So

Since the inequality holds for any satisfying ,

Appendix C Visualize the Sparsification Process

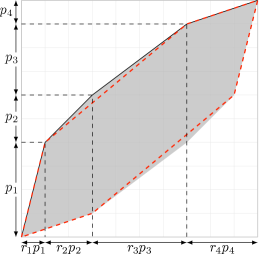

This section provides an informal intuitive visualization of the sparsification process. The Neyman-Pearson region of a decision problem is considered when proving the positivity of the minimum total variation distance (Lemma 10). In that proof, we claim that the Neyman-Pearson region contains exactly the same information as the ratio .

Say the ratio is represented by a sorted table , that is, and . By the Neyman-Pearson lemma, the (upper) boundary of the Neyman-Pearson region is the polygonal chain that connects

as illustrated in Figure 1. The -th direct segment in the polygonal chain is the vector . This also explains how the Neyman-Pearson region contains exactly the same information as the ratio.

The goal of our sparsification process is to find a simpler ratio (the sparsified ratio) that is close to the given ratio. From another point of view, the goal is to find a region with simpler boundary that is close to given Neyman-Pearson region.

If a few consecutive direct segments in the boundary have similar slopes, they can be replaced by a single direct segment, causing minor change on the shape of the region. This is exactly how our sparsification algorithm works: identifying a cluster of probability masses then merging them together.