Explosive growth from AI automation: A review of the arguments

Abstract

We examine whether substantial AI automation could accelerate global economic growth by about an order of magnitude, akin to the economic growth effects of the Industrial Revolution. We identify three primary drivers for such growth: 1) the scalability of an AI labor force restoring a regime of increasing returns to scale, 2) the rapid expansion of an AI labor force, and 3) a massive increase in output from rapid automation occurring over a brief period of time. Against this backdrop, we evaluate nine counterarguments, including regulatory hurdles, production bottlenecks, alignment issues, and the pace of automation. We tentatively assess these arguments, finding most are unlikely deciders. We conclude that explosive growth seems plausible with AI capable of broadly substituting for human labor, but high confidence in this claim seems currently unwarranted. Key questions remain about the intensity of regulatory responses to AI, physical bottlenecks in production, the economic value of superhuman abilities, and the rate at which AI automation could occur.††We thank Jaime Sevilla, Tom Davidson, Carl Shulman, Anson Ho, Matthew Barnett, Neil Thompson, Sam Manning, and Amelia Michael for helpful feedback and Maria de la Lama for the illustrations. We are grateful to Open Philanthropy for support for this project.

1 Introduction

Artificial intelligence (AI) possesses enormous potential to transform the economy by automating a large share of tasks performed by human labor. There has been growing interest in the possibility that advanced artificial intelligence (AI) systems could drive explosive economic growth, meaning growth an order of magnitude faster than current rates. ([10]) AI could rekindle the increasing returns dynamics that have historically led to super-exponential growth. This report aims to build on Davidson’s analysis by providing a comprehensive assessment of the key arguments for why AI that can meaningfully substitute for human labor may or may not produce an acceleration of economic growth by as much as we understand the Industrial Revolution as having done, a factor of ten or more.

The idea of AI’s potential to automate many or even all tasks presently undertaken by labor has drawn considerable interest from economists. Various mechanisms, through which this transformation may or may not happen, have been proposed (for a review, see [43]). While current scholarship provides valuable qualitative insights and intuitions about the limitations of accelerated economic growth due to AI (e.g. [1]), our work aims to extend this foundation by offering a more detailed quantitative analysis. We focus on identifying the specific conditions under which significant growth accelerations may or may not occur. For example, arguments involving economic bottlenecks, including so-called ‘Baumol effects’ that are invoked to suggest accelerations might be unlikely, often permit substantial level-effects from AI automation—effects which could easily produce accelerated growth if automation were to take place in a sufficiently short period of time. Our approach attempts to dig into the precise quantitative ranges of growth rates that might blocked by such previously identified mechanisms.

![[Uncaptioned image]](/html/2309.11690/assets/x1.png)

We take stock of some of the key arguments as to why or why not we might expect explosive growth from AI—growth an order of magnitude greater than is typical in today’s frontier economies. We spell out these arguments in detail and tentatively assess their force. We focus on providing a quantitative basis to key arguments (such as arguments involving bottlenecks to automation, preferences for human-produced outputs, technical and regulatory difficulties in automation, among others) to better understand the plausible range of growth rates.

We describe three related arguments in favor of explosive growth that rest on the idea that the development of AI offers an accumulable substitute to human labor—the first relying on increasing returns to scale due to technological progress, the second based on fast expansions on the amount of total effective labor force (including AI) and the third from transitory growth effects due to rapid automation.

The bulk of this work analyzes arguments against explosive growth from AI, which we articulate and tentatively assess (see Figure 1). Overall, our assessment highlights four themes:

Growth theory models predict explosive growth. Growth theory models often predict explosive growth by default when AI is able to substitute for human labor on most or all tasks in the economy. These predictions are quantitatively robust under various modeling assumptions, such as whether we assume increasing returns to scale or constant returns to scale and whether or not we consider delays to investment, if realistic parameter values are used.

Regulation could restrict AI-driven growth. Regulation of AI and various restraints (arising from political economy, or risk-related concerns) could be sufficient to keep growth from increasing by an order of magnitude. However, such paths generally require lasting global coordination and potentially exerting control over many distributed actors, which might be infeasible given both the strengths of relevant incentives to develop and deploy advanced AI and the falling costs of AI training stemming from algorithmic and hardware technology advances.

Many arguments against explosive growth lack quantitative specificity or are otherwise weak. There are numerous arguments against explosive growth from AI that falter in providing quantitative specifics. For instance, some posit that fundamental physical limits or non-accumulable factors of production will rapidly bottleneck growth post AI automation, yet they fall short in quantitatively bounding the growth accelerations permitted by such constraints in a compelling manner. Other objections, such as that humans might strongly disprefer consuming AI-produced goods or services, may also fail to thoroughly take seriously “good AI" that is actually able to flexibly substituting for human labor across a wide range of tasks.

It is difficult to rule out explosive growth from AI, but that this should happen is far from certain. We think that the odds of widespread automation and subsequent explosive growth by the end of this century are about even. Yet, high confidence in this claim seems unwarranted, given numerous plausible counterarguments and the fact that the prediction of explosive growth involves the extrapolation of models beyond the regime in which they have been observed to work.

![[Uncaptioned image]](/html/2309.11690/assets/x2.png)

In this work, we will refer to “explosive growth" as growth an order of magnitude greater than what is typical in today’s frontier economies. Specifically, we define this as annual real gross world product (GWP) exceeding of its maximum value over all previous years. This definition is consistent with prior definitions (e.g. [10]), and it precludes scenarios in which the level of GWP crashes (due to, e.g., some disaster) and then recovers quickly. Moreover, by economic output, we refer to the measured output figures produced by relevant statistical agencies operating in at least as favorable measurement conditions as those today in frontier economies, i.e. incorporating new product varieties and adequate sampling intervals, etc. at least as adequately as the Bureau of Labor Statistics (BLS), Office of National Statistics (ONS), and so on.

We analyze a dozen key arguments for and against explosive growth from AI capable of substantially automating economically valuable tasks. Each argument is first summarized concisely before a deeper examination aims to give a quantitative sense of how it might permit or rule out certain growth rates. After thoroughly assessing each argument, we evaluate its importance in assessing the probability of AI-induced explosive growth. To ground our quantitative estimates, appendices provide relevant economic growth models and data. We offer calibrated probability estimates for each argument being decisive in determining if explosive growth occurs. These judgments are based on a defined likelihood scale that we introduce in Appendix A.

It is worth noting a few key limitations upfront. This work is perhaps not very balanced in two ways. Firstly, we searched perhaps more thoroughly for reasons why substantial growth accelerations could not happen compared to arguments in favor. As a result, it contains a much larger treatment of all the ways in which explosive growth could not happen, relative to the ways in which it could. The fact that many such counterarguments are featured in our work might then inadvertently give the impression that there are many more plausible ways for the overall hypothesis to fail than to succeed. On the other hand, we have become more partial towards the idea that explosive growth looks highly plausible, likely more so than informal polls suggest economists are. Partly in light of this, our evaluation of some counterarguments may come across as succinct, reflecting our updated perspective on their relative merit.

2 Arguments in favor of the explosive growth hypothesis

In this section, we delve into three reasons to expect explosive economic growth driven by the advent of artificial general intelligence (AGI). Firstly, we demonstrate that increasing returns to scale in semi-endogenous growth models generally produces explosive growth when labor is accumulable (in the sense that the stock can be increased by reinvestment of production). Secondly, we extend our analysis to exogenous growth models, highlighting how explosive growth can emerge even without increasing returns to scale and while considering current hardware prices. Thirdly we argue substantial automation happening in a brief window in time could raise the level of output sufficiently high to give rise to explosive growth. All throughout, we emphasize that the rapid expansion of the total labor force, which encompasses human and AI workers, likely leads to explosive growth.

2.1 Increasing returns to scale in production gives rise to explosive growth

One argument for explosive growth from AI invokes the increasing-returns production implied by standard R&D-based growth models. In such models, when AI suitably substitutes for human labor, all factors of production become “accumulable" so that these can be increased through investment. Notably, this gives rise to a feedback mechanism where greater output gives rise to an increase in inputs that give rise to a greater-than-proportional increase in output. Hence, such models generically predict super-exponential growth conditional on AI that suitably substitutes for human labor. The striking feature of endogenous growth models to produce explosive growth was previously pointed out, by among others, [43].

If AI offers a suitable substitute for human labor, standard R&D-based growth models with increasing returns to scale predict super-exponential growth as long as the diminishing returns to R&D are not very steep. Consider a generalized version of R&D-based growth model, which— due to the nonrivalry of ideas—gives rise to increasing returns:

| (1) |

where represents total factor productivity and is the stock of capital (machines, computers, etc.). Capital accumulates in line with dedicated investment, as does total factor productivity. However, total factor productivity investment have diminishing marginal returns as ideas get “harder to find" (as is well-documented in, for example, [4]). Formally:

| (2) |

Standardly, motivated by the so-called “replication argument", we might suppose that . However, this assumption is not at all needed for our conclusion. Indeed, still produces increasing returns to scale as long as the returns to idea-production diminish sufficiently slowly.

In particular, we show that as long as , the economy exhibits increasing returns, which implies that such an economy will grow hyperbolically, i.e. as described by the differential equation , where is the returns to scale parameter (which is whenever ).

[4], which provides us perhaps with the best estimates of the extent to which ideas get “harder to find", we find that hyperbolic growth occurs with values of as low as 0.68. Hence, while standard economic arguments suggest we might expect , with highly conservative assumptions, hyperbolic growth with AI is predicted by R&D-based growth models. This point has been noted elsewhere, notably by [10]: avoiding increasing returns to scale is difficult to avoid even when ideas get “harder to find" over time. Indeed, this outcome is consistent with fairly conservative assumption on there being decreasing returns on inputs to final goods production.

Why might we take the conclusions from these models seriously? R&D-based growth models, and in particular, the semi-endogenous version, offer adequate explanations of recent and distant economic history, as has been noted in the literature. As such, the fact that it robustly predicts explosive growth from AI that suitably substitutes for human labor should be considered a relatively strong argument. Although obtaining high-quality empirical evidence to decide between competing growth theories remains challenging, the semi-endogenous account predicting explosive growth performs relatively well (see Table 1).

| Prediction | Explanation and References |

|---|---|

| Economic growth acceleration under Malthusian conditions | An acceleration of economic growth when the size of the population is limited by the available technology (see also [30]). This prediction is in line with the observed acceleration over recorded economic history, such as that of [5]. While there is reasonable debate about how closely models that predict gradual economic acceleration fit distant economic data, and the extent to which such data is reliable (see, e.g. [14, 39]), this model arguably captures key dynamics of the data. |

| Non-increasing growth in global output | Non-increasing growth in global output in the mid-20th century concurrent with the observed slowing rates of population growth in middle and high-income countries ([24]). The model predicts that slowing rates of population growth produce slowing rates of output growth, all things equal, and therefore does a decent job accounting for the general pattern of 20th-century growth. There is furthermore evidence that the semi-endogenous growth model fits recent empirical data on output, multifactor productivity, research intensity better than other models (see, e.g. [31, 18]). |

| Maximum observed rate of long-term economic growth | The maximum observed rate of long-term economic growth should be on the order of the maximum rate of population growth.111Assuming some dimensionless parameters such as the labor elasticity of output are close to , which in practice they appear to be. Semi-endogenous growth theory predicts that growth in output should be close to the rates of population growth (see Appendix C), and should therefore be on the order of 3% per year, which is consistent with historical data. |

There are alternative accounts of economic history that put more weight on culture and institutions compared to scale effects from population, capital, and ideas. We agree that these factors matter, but think they are best viewed as corrections on top of the semi-endogenous model. For instance, just as culture and institutions influenced which countries were the first to undergo the Industrial Revolution, we also believe that they will influence which countries will be the first ones to start experiencing explosive growth.

Nevertheless, it might still be appropriate to put some weight on such alternative explanations and appropriately be less confident that simply scaling the labor force will lead to explosive growth. However, the basic picture here still seems persuasive to us even if for some reason we believe this is not a good account of what happened in economic history, and so we still think this argument is strong in the absence of more specific critiques.

Semi-endogenous growth theory offers a comprehensive framework for understanding historical trends and patterns of economic growth. Although obtaining high-quality empirical evidence on growth theories remains challenging, the semi-endogenous account predicting explosive growth from AI systems that provide suitable substitutes for human labor presents moderately strong evidence supporting the explosive growth hypothesis. There is a possibility that current growth rates are shaped by additional bottlenecks beyond the fact that the current labor-stock is non-accumulable or that new bottlenecks may emerge shortly after AI substitutes for human labor. The exact nature of such a bottleneck remains uncertain, which warrants a cautious approach when evaluating future growth prospects (for a more in-depth discussion on this topic, see Section 3.2).

2.2 The stock of digital workers could grow fast

The stock of AI systems that substitute for human workers could grow very fast once such systems have become technically feasible, which by itself could potentially expand output massively. Relaxing our earlier assumption of increasing returns to scale, we can show that even a simple exogenous growth model predicts explosive growth from AI because the stock of AI systems performing tasks that human labor previously did could grow sufficiently rapidly. Consider an exogenous growth model without technological progress:

Here refers to workers: either digital workers in the form of AI systems or human workers. With the development of AI that presents a suitable substitute for human labor, we can suppose that the stocks of labor and capital grow as a result of investment:

| (3) |

where is the fraction of investment channelled towards AI, is the saving rate of the economy. denote the average dollar-costs (on compute and electricity) of building an AI system that performs the same amount of work as a human laborer. are the depreciation rates for the effective labor and capital stocks, respectively. Assuming that is constant, some algebra (see Appendix D) combined with the parametric assumptions presented in Table 2 reveals that the steady-state rate of growth in this model exceeds 30% per year if

| (4) |

| Parameter | Value |

|---|---|

| Value of US capital stock | $70T |

| US Labor Force | 165M |

| 0.7 | |

| 30% |

Hence if the cost of running an AI that substitutes for a human worker ( whose units are ) is sufficiently low, exogenous growth models predict that the effective labor stock should grow sufficiently fast to give rise to explosive growth. A similar argument to the effect that a rapidly expanding “digital workforce" can result in massive expansions in output has previously been made by [27].

We can provide a rough estimate of AGI runtime costs by relying on estimates of the cost of computation and the estimated cost of running the human brain. Right now, machine learning hardware costs around ,222The current flagship datacenter GPU, the H100, can perform around 4000 TeraFLOP/s in half-precision, and costs around $30,000. Conservatively assuming this is ran at 40% utilization for three years with a $30,000 energy bill, this amounts to . and [8] provides a best-guess estimate of for the rate of computation done by the human brain. Combining these two estimates suggests a value of around . In our model, this is consistent with explosive growth if

| (5) | ||||

| (6) | ||||

| (7) |

In other words, this would hold if savings rates are in line with saving rates that have been historically observed in Western countries and significantly lower than saving rates that have been observed in East Asian countries such as Japan, China, and Singapore. In addition, saving could be higher under AI-driven growth, given that AI could increase the productivity of capital investments, and result in concentrating wealth to those with a high propensity to save ([43]).

Overall, this calculation suggests even if we very conservatively assume that hardware technology stops improving, that we operate in a constant-returns to scale regime, and that AIs are only as productive as the average worker in the US, explosive growth is still a plausible outcome of labor becoming accumulable if our AGI software can match the performance of the human brain.

It should be noted that we assume that the depreciation rates of the stock of compute and capital ( and ) are assumed to be neglible compared to the growth rate (see table 2). If we were to relax this assumption then we need precise estimates of these numbers and in general need higher saving rates. However, even with depreciation rates , we only need to double the savings rate to to still get explosive growth, which has historically been observed in e.g. East Asian countries.

Moreover, we might need to account for the cost of robotic systems in addition to the computational costs of running the software. While state-of-the-art industrial robotic systems are currently, for e.g. spot welding, are on the order of $100k per unit ([42]), it is difficult to predict how much this would add to the cost basis, . This is because there could be substantial reductions in prices as we proceed along a learning curve as robotics usage expands ([29]).

While the model above is only a toy model, it nevertheless illustrates the key importance of the parameter or something else fulfilling the same role for any endogenous growth model involving AI-driven automation.

The preceding analysis relies on a static calculation that does not account for potential price effects. In other words, it overlooks how demand could influence the price of computation. Additionally, the model’s conclusions rest heavily on estimates of the computational requirements of the human brain, which are marked by considerable uncertainty. If we were to consider the higher-end estimates of the computation costs of running the human brain in [8] of , explosive growth looks unlikely with current prices.

Remarkably, this result holds even if we assume that there are delays to investment, in the sense that “realized investment" is an exponential moving average of past inputs to investment. In other words, we model investment to move more gradually, thereby avoiding short and perhaps unrealistic bursts of capital accumulation and output growth (see Appendix E).

However, it is important to note that hardware prices are expected to decrease considerably over time, with a current halving time of roughly 2.5 years ([19]). This indicates that the cost of running a human-equivalent AI is likely to become more affordable in the future. Therefore, the argument presented in the analysis becomes more persuasive if one anticipates that AGI will take around 10 to 20 years to develop, a period during which computer hardware could become one or two orders of magnitude more cost-effective. This dynamic could potentially amplify the economic growth impact of labor substitution by AI. In addition to this, it’s also plausible that is lower because AIs could be more capable than humans at runtime compute parity. Here are a few reasons why we might expect this to be the case:

-

1.

A single AI system trained only once can be deployed in many different settings in the economy given a sufficient runtime compute budget, while this is impossible to do for humans. In other words, it’s much easier to copy AI systems than it is to copy humans.

This has many beneficial effects. It allows us to amortize the cost of training large systems over a vast number of runtime instances, something impossible to do with human lifetime learning. In addition, it means we can pick the best-performing systems at a given runtime compute level and simply copy those, instead of sampling from a wide distribution of conscientiousness, intelligence, communication skills, etc. that we must do when the labor force is made up of humans.

-

2.

Software progress on AI capabilities might not stop at human levels. Indeed, there’s no particularly good reason to suppose that human brains are optimal from the point of view of converting runtime compute into capabilities, given that humans are evidence that previous species were not optimal. Even one or two orders of magnitude of decrease in from software progress would strengthen the argument in this section considerably.

An important criticism of this argument is that scaling GWP along the intensive margin and the extensive margin might be meaningfully different. For instance, it might very well be true that doubling the world population over a sufficiently long period of time leads to a doubling in gross world product, but without this increase in population leading to faster technological progress, per capita income would stay the same. If we do not count the consumption of AIs as part of GWP in our model, then our thesis is that increasing the number of AIs will lead to higher per capita consumption among humans, and perhaps it is more difficult to get explosive growth this way without being able to scale the quality of the services in the economy.

We think there is some kernel of truth in this argument, and we expect it to make explosive growth significantly more difficult in worlds where AI-driven automation is unable to meaningfully accelerate R&D, but some scaling along the intensive margin is possible even without technological advances. There are already substantial differences in personal income across the world, and even within rich countries. In most countries, simply raising the average standard of living in the country to the standards enjoyed by the wealthiest residents would lead to orders of magnitude increase in gross domestic product, and we know that if resource constraints are sufficiently loose, doing this requires no new technology. Resource constraints could of course pose obstacles, but those are no more binding when we’re talking about an increase along the intensive margin than they are when the increase happens along the extensive margin instead.

Even without the assumption of increasing returns to scale, standard economic growth models predict substantial acceleration in economic growth rates if we assume substitutes for human labor at realistic costs in the model. While we do not strongly endorse the conclusions of this calculation due to the many simplifications we make throughout, we think the argument still provides evidence that explosive growth is more likely than we might think, as it occurs even in the absence of endogenous technological progress and hardware efficiency growth.

2.3 AI automation could have massive transitory effects

In growth theory, there is an important qualitative distinction between growth effects and level effects ([33]). A growth effect is assumed to be either permanent or last for a long time (e.g. changes to the steady state or balanced growth path), while a level effect is a one-time, transitory increase in the level of economic output that does not translate into higher growth in the future.

It might be the case that even if AI fails to lead to a long-term growth effect, there might still be a level effect from human-level artificial intelligence being deployed throughout the economy, and a change in the level of gross world product that happens over a sufficiently short window of time could lead to transitory growth rates that clear the threshold of “explosive growth".

To quantify these effects, consider a toy model in which output is produced by a CES production function over a unit continuum of tasks:

| (8) |

where is a measure of productivity. We will not be explicit about what the inputs represent for the sake of generality, but we assume that there is some total stock of inputs available in the economy that can be allocated across different tasks. Moreover, so that tasks are complements, thereby giving rise to ‘bottlenecks’ in production: the larger negative values of , the more severe the bottlenecks.

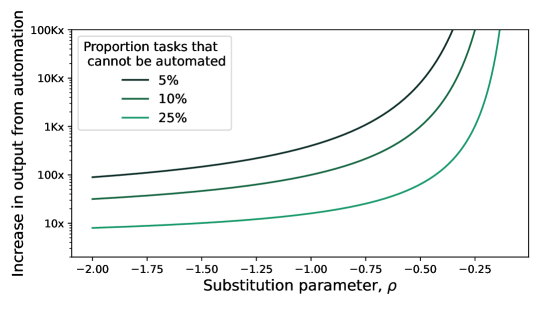

Let denote the fraction of tasks that cannot be cheaply automated. We show that when is relatively large (e.g. 10%), the level effect from AI automation is very substantial, even despite substantial bottlenecks in production.

Given that there is some total stock of inputs available in the economy that can be allocated across different tasks, we have the constraint:

| (9) |

When so that the tasks are complements, is optimized when for all and therefore .

To see the impact of automation, let’s suppose that for some , a fraction of tasks are “cheaply automated". In practice, this is likely to mean that we get many orders of magnitude more inputs on these tasks after the automation than before. When complementarity effects are strong (so when ) we can approximate by assuming infinite input on automated tasks instead, as this simplifies the calculation without making much of a difference to the final result. In this case, our optimization problem becomes

| (10) |

This problem, as before, is solved by setting the inputs of all tasks equal to each other: for all . In this case, we get that , so GWP is higher by a factor of . Figure 1 contains the values of this function evaluated at some plausible values of and .

Indeed, the level effects from partial AI automation is substantial, even when the assumptions are relatively pessimistic. For instance, [28] looks at the elasticity of substitution between capital and labor in the US economy and finds a plausible range from to , which corresponds to values of ranging from to . is perhaps below the standard range that is considered plausible, implying stronger complementarities between tasks than we currently believe exist between capital and labor.

Overall, even if the other arguments fail to go through and we cannot even attain AI that perfectly substitutes for humans across all tasks, there’s still room for explosive growth if AI can automate e.g. of tasks in the economy and it can do so in a period of less than years. We can relax these assumptions even further if we do not make the pessimistic assumption of .

The argument we present above can fail to hold for many different reasons:

-

1.

The approximation that AI will be infinitely productive on automated tasks makes the numbers look more impressive than they should when are close to zero. For instance, if we believe AI will only ever contribute nine times the input intensity on any automated task, the most we can get out of AI automation is an order of magnitude increase in gross world product, even assuming full automation.

Indeed, if we rely on our estimates of the computational cost of running the human brain from Section 2.2., we can estimate that all the computing hardware available in the world today can perhaps run 100 million simulated workers at most. If that’s the best we can do, human-level AI software will fall far short of increasing input intensities at all, let alone setting them to infinity. In the future, this can be overcome by manufacturing more chips, improving hardware efficiency, etc. but these are out of the scope of this argument.

-

2.

We do not have good information about what value for should be considered plausible. In a world where full automation is attained, we can turn our model into a coarse approximation and interpret as the fraction of tasks where running human-equivalent AIs is comparable to or more expensive than employing humans to perform the same tasks, but there’s no obvious reason within the framework of this argument why this quantity should be e.g. less than . Our previous calculations based on the cost of human brains are suggestive that this number should be small, but conditional on the increasing returns to scale and digital worker cost arguments failing, we might not want to put substantial weight on this argument either.

-

3.

Even if the argument gives us correct values for the factor increase in GWP we should expect, this increase can simply drag out over a sufficiently long period of time such that we do not get an explosive rate of growth at any point. We address some objections which argue for such a possibility Section 3, but our responses are not decisive and we have to concede that long delays are indeed possible.

This argument suggests that explosive growth remains possible even if AI does not result in full automation and even if humans continue to occupy roles in the economy that bottleneck production. As such, it’s a “worst case argument" which leads us to put some probability on explosive growth even in such worlds. However, we consider it to be on shakier ground than the other arguments we present for explosive growth, and recommend against taking this argument too seriously in worlds where our other arguments for explosive growth have failed.

3 Arguments against the explosive growth hypothesis

In this section, we provide accounts of arguments against AI-driven explosive growth. For each, we assess their plausibility and, where possible, attempt to estimate the permitted growth rates the argument implies. While several of the arguments initially seem concerning, upon closer analysis most do not appear decisive. However, a few remain non-trivial objections that could plausibly reduce the probability of explosive growth, especially in conjunction. We examine each argument in turn and aim to draw tentative conclusions about their effects on the likelihood of explosive growth.

3.1 Regulations can slow down the economic impact of AI

This objection states that the training or deployment of AI systems will be sufficiently impeded by regulation to reduce the economic growth effects of AI. The possibility of the growth effects from AI automation being curtailed by regulation features, for example, in [23, 45, 15]. Presumably, there are many reasons this might happen: generic fear or reluctance regarding powerful new technologies, concerns about privacy or intellectual property leading to a shortage of training data, unwillingness to let AI systems perform tasks that can be automated without human supervision due to concerns about legal liabilities, etc. Such regulations may very well be appropriate and prudent, and their negative growth effects could plausibly be outweighed by other considerations around safety and social welfare. The basic argument, though, is that even if AI would indeed produce explosive growth if this were allowed to happen by governments or relevant international bodies, this possibility may not be realized due to dedicated efforts coordinating to slow this process down.

Within the deep learning paradigm that has been dominant in AI research over the past decade, what seems to matter most for the performance of AI systems are the number of examples they see during training and the number of parameters they have – which is in turn dictated by the amount of compute developers have at their disposal. Quantitative support for this statement is provided by the growing literature on scaling laws, which describe the performance of a deep learning model in terms of a few macroscopic properties of the model such as the parameter count and the training dataset size. For more on this in the context of large language models, see [25] and [20].

In light of this, the regulation objection looks more plausible than it did a decade ago because it seems that AI development will be largely driven by access to vast amounts of data and computation. The large physical footprint of the computation capacity required for training and deploying advanced AI would likely make the process easier to regulate, and intellectual property laws can be a significant impediment to the data scaling part of the equation if they were to be interpreted in a manner unfavorable to AI labs. So we do not think we can rule out this scenario as it stands, especially if in the future there are large and visible alignment failures of AI systems that scare people into action.

However, there are effects pushing in the opposite direction. Insofar as being in possession of better AI systems becomes a matter of national security, we can expect any coordination by governments across the world to slow down AI development to be imperfect. Furthermore, the scale of the potential economic value that AGI can create is enormous: it’s orders of magnitude beyond any other recent innovation we can think of, mainly because of its credible potential to restore the historical trajectory of accelerating growth. These factors create strong incentives for governments to allow the widespread deployment of AGI systems.

We also have to consider algorithmic progress and improving hardware efficiency. While scaling laws give a good description of the performance of ML systems at a particular level of algorithmic efficiency, over time we develop better software and this means we need fewer resources to achieve the same level of performance. [17] estimates the pace of algorithmic efficiency improvements in computer vision as one doubling every 16 months and [12] estimates one doubling every 9 months, though with wide confidence intervals. If these rates of progress are at least within the right ballpark and hold up across many orders of magnitude of progress, eventually AGI systems could become quite cheap to train.

In addition, the falling price of computation over time due to hardware efficiency progress means this represents an increasingly smaller fraction of global spending on computation. To keep up with these two effects, increasingly strict regimes of surveillance could eventually be required. The theoretical lower bound on the resource needs of AGI set by the human brain should loom large in our thoughts here: the existence of the human brain means that in principle we do not need more energy or data than is used by a human to achieve human-level performance, and tracking every human born in the world would require a surveillance regime the likes of which we have never seen so far. We think the first AGI systems will require substantially more computation and data than the human brain does, but over time there’s no reason why these costs should not fall to the level of the human brain or even further below.

In light of the above discussion, we think our baseline scenario here for AI regulation should be more like nuclear arms control and less like the regulation of nuclear energy: coordination on nuclear arms control does happen, but it is quite imperfect and hasn’t stopped nuclear proliferation from taking place. This is because we think the incentives for AI adoption are more similar to the incentives for nuclear proliferation than the incentives for using nuclear energy, as the economic value that would be unlocked by AGI is far greater and this also has the potential to directly translate into overwhelming military advantage against adversaries.

Here are some concrete ways in which regulation could be used to slow down the economic impact of AI:

-

1.

Place restrictions or otherwise impose additional costs on large training runs, similar to the restrictions that now exist on nuclear power. The large resource footprint of training runs past the scale or so should make these enforceable for some time.

-

2.

Prohibit the use of AI for certain economic activities. For instance, laws could be created or interpreted to bar the use of AI in courtrooms or at hospitals without adequate human supervision. This would introduce an artificial bottleneck that would stop AI from fully automating some tasks.

-

3.

Use intellectual property laws to prevent the use of certain kinds of data for the training of AI systems. A sufficiently expansive interpretation of existing intellectual property legislation could prevent AI from being usefully monetized, reducing the incentive for private actors to invest resources into developing better AI systems.

While implementing such regulations may hinder the development or deployment of AI, the feasibility of enacting and enforcing them remains uncertain. Firstly, it is unclear whether such policies can reliably remain enforced over a sufficiently large, possibly global, jurisdiction for multiple decades or longer. The potential value of AI deployment could be immense, with the prospect of increasing output by several orders of magnitude. Consequently, this would likely create formidable disincentives for imposing restrictions, as well as powerful incentives for eliminating or bypassing any existing constraints. Secondly, the difficulties with enforcing such restrictions might become large as software improvements bring the capital costs of AI training down. Over time, enforcing such restrictions will require increasingly ubiquitous global surveillance.

The historical record of regulating technologies that could boost output tenfold is sparse because few, if any, such technologies have previously been developed. Perhaps the closest possible analogs are a cluster of agricultural technologies that were introduced during the Neolithic Revolution or the manufacturing technologies that contributed to the Industrial Revolution (the steam engine, the spinning jenny, cotton gin). While England attempted to forestall the diffusion of some key Industrial Revolution technologies by prohibiting the emigration of skilled workers and the export of machinery, these protectionist policies proved largely ineffective ([21]). From the 1780s to 1840s, skilled workers, machines, and blueprints were frequently smuggled out of the country despite the bans, and by the 1840s, with industrialization advancing rapidly, the policies were seen as futile and repealed (Ibid.). In summary, England failed to meaningfully slow the international diffusion of its industrial technologies. The experience highlights the challenges of restricting technologies that offer major economic gains.

As far as we can tell, there is no compelling evidence to suggest that technologies involved in prior shocks to production technologies could have been effectively regulated with the effect of not just delaying such shocks but also substantially dampening their growth effects.

Overall, we conclude that regulating the training and deployment of AI may delay its economic impact, but there is no compelling reason to be confident that its development and application would be sufficiently prolonged to maintain historical economic growth rates for an extended period of several decades. We do not rule out the possibility, but we would judge it to be unlikely that regulation of the training and deployment of AI will block explosive growth.

3.2 Output is bottlenecked by other non-accumulable factors of production

The endogenous growth theory argument for explosive growth from the Section 2.1 only implies that we should expect constant returns to scale on all physically embodied inputs jointly. Labor and capital are physically embodied inputs, but they might not be the only important ones: other inputs such as energy or land could be just as important, and if they cannot be accumulated through better technology, perhaps this means AGI-driven growth can get short-circuited by its dependence on these non-accumulable factors before reaching the threshold of “explosive growth". In addition, just like population, there might be intrinsic timescales that block currently accumulable inputs such as physical capital from being accumulated arbitrarily quickly. If true, this could be a strong objection against the explosive growth view.

Some version of this argument is certainly sound: there must eventually be some resource constraints that prevent output from growing arbitrarily large. The important question about this argument is not whether it holds eventually, but whether it holds quickly enough to preclude explosive growth.

We estimate that the diminishing returns structure on idea production implied by [4] means that we need the returns to scale on accumulable inputs to be at least around for explosive growth to occur (see Appendix B). Theoretically, we have reason to believe that (i.e. we have constant returns to scale) if we consider all physically embodied inputs. However, not all such inputs may be accumulable: as a naive example, if empty space becomes a valuable resource, then regardless of how much output we invest the speed at which we can grow our access to space might be bounded by the speed of light. There’s no a priori argument which can settle the question of the returns to scale on accumulable inputs, and we must also consider the possibility that there might be strong complementarity between presently accumulable inputs such as capital and non-accumulable inputs such as land or empty space. We must examine the argument in greater detail to make a judgment about its strength.

The outside view consideration is that economic growth has accelerated by many orders of magnitude in the past: indeed, this is the empirical regularity for which the semi-endogenous growth theory provides an explanation. Factors which bottleneck this acceleration do not seem commonplace. We might look at the order of magnitude increase in growth rates since the agricultural era as evidence that new bottlenecking factors such as population growth appear at a rate of roughly once every orders of magnitude of acceleration, suggesting a probability of using the time-invariant version of Laplace’s rule from [41] that one such bottleneck appears before world economic growth accelerates by one order of magnitude.

When we get down to specifics, the most plausible bottlenecking factors that we can think of are land, energy and capital. On the energy front; on average, W hit the Earth ([36]), while global yearly energy consumption is about W ([38]), suggesting that energy consumption could expand by 3 orders of magnitude. Similarly, only around 1.5m km2 out of the Earth’s 100m km2 of habitable land is urban and built-up land, which suggests that there are around 2 orders of magnitude of land that could be urbanized or built-up. Even if these are strong constraints that cannot be overcome, considering just these constraints, we have at least orders of magnitude of room to scale up gross world product. If we assume no improvements in efficiency, so that resource consumption needs to be scaled up proportionally to output, such constraints would still permit explosive growth if the transition to full automation took 20 years or less. Clearly, then such constraints do not block growth accelerations at least when AI automation occurs swiftly.

We examine the prospect that some form of physical capital could end up being a bottlenecking factor quantitatively and come to the conclusion that for the argument to block explosive growth, we need adjustments in investment to be significantly slower than the growth rate of the broader economy (see Appendix E). In particular, if we can double the worldwide stock of physical capital at a rate of , there’s no reason to suppose that explosive growth would be prevented due to investment delays or adjustment costs.

The assessment of the likelihood of physical capital becoming a bottlenecking factor, therefore, comes down to the quantitative question of how long we can expect fundamental delays to investment to be. The experience of Chinese catch-up growth shows that sustained growth rates on the order of and one-time growth rates on the order of have precedent in economic history. To reach the threshold of explosive growth, we only need a doubling of this final rate of increase in a world where AI will also be capable of assisting with the process of capital stock adjustment, which does not seem sufficiently far out of distribution for us to seriously doubt its feasibility.

Overall, the inside view here seems somewhat ambiguous and it’s difficult to know in which direction we should update given the above paragraph. The fact that the joint returns to scale on labor and capital right now seem to be well over the threshold of required for explosive growth is reasonably good evidence that we should expect at least some period of growth acceleration after full automation, but this period might be short and it might stop before we actually reach in gross world product growth rates.

Still, we think the threshold of might be really low, much lower than where existing empirical evidence places it (e.g. [26, 3]). In addition, even in a world where this objection is valid, the argument from accumulating digital workers from Section 2.2 could still produce explosive growth for some time as a consequence of the transition from human labor to AI labor. As a consequence, our estimate of the probability that this objection blocks explosive growth is substantially smaller than the naive outside view figure of .

Our final conclusion is that this argument is plausible on the outside view and the inside view evidence makes the argument seem somewhat less compelling, though is by no means sufficient to rule it out. Our final judgment is that it’s unlikely this objection blocks explosive growth.

3.3 Technological progress and task automation by AI will be slow

This argument posits that the requirements for automating different tasks in the economy span a wide range in computation, data or both. As these resources can only be accumulated in a gradual fashion, it will take a long time to get from the point where AI starts to have a large economic impact by automating tasks that are the easiest to automate to the point where AI is able to fully automate the economy, and this long waiting period will spread out the economic impact sufficiently that we end up not observing explosive growth.

The effect of this argument is similar to the argument from regulation, but the underlying driver is different. Here, the reason is a physical property of AI systems as such, and not a property of how human civilization will react to the prospect of full automation of the world economy by AI. In both cases, however, there is some force that causes the large impact of full automation to be spread out over a long period of time, and this is what precludes explosive growth.

This objection rests on an empirical claim about the relative difficulty and resource requirements of automating different tasks in the economy, specifically that the distribution of the amount of computation, data, etc. required to use AI to automate different tasks in the economy is wide and/or fat-tailed. In other words, we need some tasks to be easy and automated early on, and some tasks to be very difficult and to take many orders of magnitude more resources to automate.

If this objection holds, it could indeed be why explosive growth does not occur: a 4 order of magnitude ( hereafter) increase in gross world product spread out evenly over years would not produce explosive growth, for instance. A specific plausible story here is that “physically embodied" tasks such as general-purpose robotics will be quite difficult to automate – solving them will require large amounts of computation, data, and researcher effort.

This is among the more compelling reasons why we might not get explosive growth. However, on the inside view, it still seems rather unlikely to be correct. There are two main reasons for this:

-

1.

Slow deployments and automation require large gaps in compute and data requirements between the point where AI starts to accelerate economic growth and the point AI is able to fully automate the world economy. However, inside-view investigations into AI (such as [9, 11]) do not usually support such large gaps.

The largest plausible gap in training computation between AI starting to have a noticeable macroeconomic impact and full automation that has been suggested in such inside-view investigations is around 10 orders of magnitude, and even this gap would be crossed fairly quickly if we add up the effects of hardware scaling, improving hardware and software efficiency, etc. It’s implausible that we could get a delay that’s as long as 80 years, and delays on the order of 30-40 years seem like the slowest that takeoff could end up being.

-

2.

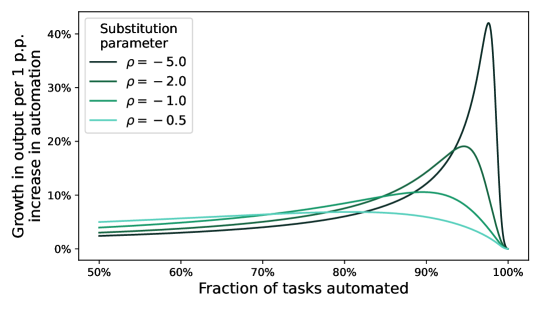

Even if the delay period is much longer than 40 years, in a straightforward constant elasticity of substitution (CES) world, where tasks performed in the economy are gross complements so that automated ‘outputs’ are imperfect substitutes for non-automated ‘outputs’, the final tasks to get automated are substantially more valuable than earlier tasks. This means that a constant rate of task automation (say, automate of tasks that humans can do in the year every year) leads to initially slow growth that becomes extremely fast towards the end, as can be seen in Figure 2. This intuition seems compelling: the final tasks to get automated remove the final bottlenecks in production, so if we believe full automation is actually possible it’s difficult to construct a scenario in which we do not get explosive growth here.

While we consider this objection unlikely to be correct, it’s internally coherent and more compelling compared to most of the other objections. We expect it to be unlikely that this objection blocks explosive growth.

3.4 Alignment difficulties could reduce the economic impact of AI

If AI alignment—the challenge of steering artificial intelligence (AI) systems to behave according to intended goals and avoid unintended harmful behaviors—turns out to be so difficult that it’s hard to get AI systems to reliably do what we want in real-world deployment, then aside from these systems being regulated more strictly, it could also simply not be in the private interest of any actor to deploy such systems at large scale. The capabilities of an AI system may seem impressive in the lab, but if private actors are unable to confidently align these systems to accomplish the tasks they want done safely, it’s hard to foresee such unaligned AI generating major economic impact before these alignment problems are solved.

It might also be challenging for AI systems to be deployed to perform certain tasks without human supervision. For instance, as outlined in [22], a common alignment problem of modern large language models is their tendency to hallucinate facts that are wrong: when asked to provide references for a claim they have made, they will often respond with references formatted according to the proper guidelines but referring to papers that do not exist. If the tendency for models to hallucinate facts cannot be entirely fixed, it might be necessary for a human in the loop to be present in any application where strict agreement with facts is highly important, which would mean there are limits to how far poorly aligned AI systems are able to automate such tasks.

There are many other paths to alignment problems leading to AI performing below the economic potential we might attribute to it based strictly on capabilities. As another example, if humans are concerned about misaligned AI systems having too much agency, they might deliberately try to engineer AI systems to be less independent in their decision-making than humans. This would then require humans to play critical decision-making roles in the economy, and then human decision-making capabilities could end up being a bottleneck in the way of explosive growth.

While the motivation behind the alignment difficulty argument is quite different from the other arguments we consider, formally its effects are likely going to be equivalent to limiting the fraction of tasks AIs are able to perform in the economy. For instance, if humans must occupy key decision-making roles in the economy, this means that effectively these tasks cannot be automated from an economic point of view. The effect of some tasks requiring human supervision to perform is similar.

This means our quantitative basis for assessing the above argument should be similar to what we outline in Section 2.3. If we think misalignment is likely to be so bad that e.g. of tasks are likely to remain unautomated, and the elasticity of substitution across tasks , then it’s quite plausible that this argument blocks explosive growth. However, as discussed in the aforementioned section; is a large fraction of the tasks in the economy, and is a high degree of complementarity across tasks. As before, we consider both of these parameter choices to be rather unfavorable, but the alignment difficulty argument pushes us to think that perhaps a lower bound on the fraction of unautomated tasks in the economy is not as implausible as it might seem.

It is rather unclear what probability distribution is implied by this argument over the parameter of tasks that AIs won’t be able to automate “early on". However, it seems likely to us that this distribution puts significant probability mass on values that are rather small and would block explosive growth even with moderate values of , with potentially long delays in the R&D process that would push this fraction down, echoing the arguments from the Section 3.2. Overall, our assessment is that this argument is most likely not going to block explosive growth, but its influence cannot be ruled out, especially in worlds where turns out to be smaller than we expect.

Overall, our conclusion is that alignment difficulties are unlikely to block explosive growth. Furthermore, this argument is in a family of arguments whose plausibility is correlated with one another due to the confounding influence of the elasticity of substitution parameter , and therefore it’s important to take care when aggregating the probabilities: the disjunction of these arguments is less likely than would be implied if we simply treated them as independent events and blithely multiplied their individual probabilities of not being blockers to get a final answer.

3.5 R&D may be harder than expected

One argument for why we might not see explosive growth is that R&D may be simply too hard. More precisely, the idea production function for total factor productivity (TFP) may have such unfavorable diminishing returns that it blocks the whole model from exhibiting explosive growth. As we have shown in Section 3.4, to make this work, the rate of the returns to R&D and the returns to scale in economic production jointly need to be small enough so that the the feedback between economic inputs and output is too decoupled to give rise to accelerating growth. If we take existing estimates of the returns to R&D in for US TFP, from [4], this argument works if the homogeneity of the production function for other non-idea outputs is no greater than .

We unfortunately do not have much evidence to evaluate how plausible the premise of this objection is. Although we have estimates related to for the advanced economies today, it is unclear how much these should inform us about the returns to scale in economies that are possibly bottlenecked by other factors of production. It is also appropriate to put some probability mass on the possibility that present estimates of the returns to R&D are too aggressive, or that returns might fall over time as we make more progress in R&D. However, even if we assume the premise that returns to R&D are less favorable than present estimates suggest, this argument isn’t sufficient to rule out explosive growth because of the argument based on the cost of computation we advance in the Section 2.2. Indeed, even in a world with exogenous technological progress and diminishing returns to scale on labor, explosive growth still remains a plausible outcome.

Because of the uncertainty about the premises of this argument and that it does not seem easy for this effect to block explosive growth even if the premises of the argument are assumed to be valid, this argument seems rather weak. We accordingly estimate a low probability that this argument is a decisive blocker. In light of the above assessment, we conclude that it is very unlikely that unexpected difficulties in R&D that result in stagnating TFP growth will end up blocking explosive growth.

3.6 AI automation will fail to show up in the productivity statistics

Even if substantial AI automation causes explosive growth in some intuitive sense, it is possible that economic measurement will be flawed in some respects and fail to capture a possible growth acceleration. Therefore, we could end up seeing a world of rapid economic transformation in which GDP growth statistics nevertheless fall far short of the threshold of we set for explosive growth.

There are at least two related arguments for why substantial AI automation will fail to show up in productivity. The first is that economic output will be inaccurately measured and that this measurement error will result in a downward bias in the estimated rate of economic growth. The second related objection is that there are well-known issues with measured growth in economic output failing to capture growth in consumer surplus, so even if the measurement of output was highly reliable, estimated economic growth would fall short of growth in consumer surplus. The second objection also contends that consumer surplus is, in some sense, the more important metric.

The first argument that economic growth will be imperfectly measured and suffer attenuation bias is indeed plausible. There are many reasons why this might happen, such as:

-

•

Lag in incorporating new product varieties: Official economic agencies often fail to promptly incorporate new types of products into their metrics. For instance, the advent of electric vehicles took years to be accurately reflected in GDP calculations.

-

•

Inadequate sampling intervals: Current sampling intervals may be too long to capture short bursts of rapid economic growth.

-

•

Random measurement errors: Factors like imperfect quality adjustments introduce random errors into growth estimates. Such error could introduce attenuation bias into the estimates of growth.

The first of these is in part the reason why the productivity effects in IT have been relatively meager (see, e.g. [6]), and the same measurement issues might similarly result in the underestimation of the effects of AI. On the other hand, the existing literature on the accuracy of GDP estimates suggests that these are not usually statistically biased. For example, the difference between preliminary estimates and later estimates derived from the comprehensive economic census tend not to be systematically different, at least in G7 countries ([44]) or in the US ([32, 34]). Moreover, using data from six comprehensive revisions—in 2009, 2003, 1999, 1995, 1991, and 1985, [13] finds that the size of BEA revisions of advance GDP estimates are not correlated much at all with preliminary GDP estimates. This suggests that historical growth accelerations are not likely to be systematically underestimated, at least in the United States.

This leaves us with conflicting insights regarding the economic implications of AI. On one hand, GDP estimates in leading economies have generally proven to be unbiased and reliable. On the other hand, the economic contributions of past technological innovations like IT have been historically under-reported due to measurement issues.

However, as discussed in Sections 2 and go on to discuss in 3.8, the economic impact of a technology that can widely substitute for human labor could far exceed that of past technological innovations like IT. Given this, it is reasonable to expect that statistical agencies, operating under conditions at least as favorable as today’s, will more accurately estimate the economic gains from AI, akin to how they track overall GDP. Relevant agencies might adapt to a faster rate of change. In an AI-automation world, agencies could face pressures to ensure that tracking and monitoring are commensurate with the pace of change. Their budgets are likely to expand in line broadly with the size of the economy, and relevant technologies used for monitoring with the sophistication of extant technology.

We think this argument is somewhat implausible, mostly because it relies strongly on the notion that output measurements will make predictable and large errors that we can anticipate but competent statistical agencies will predictably fail to address. Even with limited knowledge of these agencies’ operations, we find the assumption hard to believe.

A weaker version in which we do not claim to predict the sign of the error in advance is somewhat more convincing. In light of this objection, one’s expectations of growth rates under AI automation should be more spread out. The net effect of this is depends on one’s expectations of growth rates from AI automation: if one were confident in explosive growth, one should shade their probability estimates in light of additional noise. On the other hand, if one were confident that explosive growth would not occur, one should assign a greater credence to statistical agencies reporting 30% growth rates. In the end, we consider it unlikely that GDP measurements will make errors sufficiently large and systematic for their measures to not show explosive growth occurring.

The second argument is based on the recognition that there are well-known issues with measured growth in economic output failing to capture growth in consumer surplus, as the former fails to capture the value of ‘free’ IT goods, such as Wikipedia, Google search, OpenCourseWare, and so on. Perhaps, an AI-driven economy will produce a relatively larger share of goods that fail to show up on the usual output accounting.

Existing attempts to estimate the contributions from ‘free’ goods find the contribution of is relatively small, contributing roughly no more than one-tenth, in proportional terms, to GDP growth numbers. For example, [35] estimate that including ‘free’ content would raise U.S. GDP growth by about 0.03 percentage points per year from 1995 to 2014. Relative to the average GDP growth rate of 2.5% over that period, this would represent a very small margin of error. Other attempts at similar accounting of the contributions from ‘free’ content like Facebook likely find slightly larger contributions (e.g. [7]), but similarly suggest that this added growth adds on the order of tens of basis points to GDP growth, at least in the United States.

In addition, even if such errors did come to pass, at some level, we do not care about productivity statistics in any fundamental sense. They are simply a useful proxy for what we wish to discuss, and if they fail to be a good proxy in the future, that does not necessarily mean our thesis about explosive growth is mistaken or that we shouldn’t take action to prepare for a world in which explosive growth will occur. We find it exceptionally unlikely that this argument blocks explosive growth in a sense that we would care about, as opposed to e.g. being a measurement artifact.

3.7 Human preferences for human-produced goods will bottleneck growth

Humans may have a preference for human providers over AI counterparts even in economically significant service industries. Even if AI is physically capable of doing any task as well as a human can or better, there might be some tasks that are valued by humans only when they are performed by other humans. For example, we today have computer programs that can play chess better than any human player can, but top human chess players can still make money by winning tournaments. The fact that a tournament of computers would have a better quality of play is not important because part of what people want to watch is for humans to be playing the game.

Humans might prefer to interact with human therapists, teachers, or other service providers that involve high symbolic value and expression of identity ([16]). Although AI systems may one day replicate some social abilities of humans, people currently tend to prefer human interaction for certain services. If such intrinsic preferences apply to a sufficient range of tasks, full automation might be impossible simply because of human preferences and not because of any physical fact about what AIs can or cannot do. This would limit gross world product as long as humans remain the ultimate consumers in the world economy and therefore the prices of goods and services are set according to their marginal utility.

This objection could in principle work assuming that all prices in the economy are set by humans, but there are two main problems with it.

-

1.

While there might be good reasons to care about what happens to gross world product, we’re fundamentally more interested in questions about the ability to manipulate the physical world to get desirable outcomes. Importantly, scenarios in which AI poses a significant military risk or reshapes the physical environment around us in some substantial way can still be “explosive" in character even if humans are setting the prices of goods and services and therefore GWP ends up being bottlenecked by human preferences of one sort or another.

-

2.

Even on the argument’s own terms, the parameter values needed to make this story work seem quite implausible.

The first problem is relatively straightforward, so we focus on the second problem here. Suppose that consumer utility is some monotone transformation of the CES aggregator

| (11) |

over individual consumer goods . If markets clear in some underlying model such that goods prices are proportional to marginal utility, GDP growth would be given by

| (12) |

so that the expression for GDP growth simplifies to

| (13) |

This equation is solved by . Therefore, for this particular specification, GDP perfectly tracks consumer utility, and we can reason about GDP growth by using the growth of as a proxy for it.

If a fraction of tasks can only be done by humans by definition, and initially the are all equal, then setting the output tasks that cannot be done by humans to infinity should raise by at least a factor , and this factor would increase if we could explicitly take human labor reallocation from automated tasks to human-only tasks into account - if the technology converting human labor to output on individual tasks is constant returns to scale, for instance, then we can get this up to .

This is just the same expression that we dealt with in the Section 2.3. We present a range of parameter values to analyze the plausibility of the argument here in Table 3:

| 89 | |||

| 32 | |||

| 128 | 8 |

The value corresponds to an elasticity of substitution , which is conservative. Even under the pessimistic assumptions of and , AGI should produce at least increase in gross world product. If this happens in less than a decade, it would be sufficient to produce explosive growth.

We think this scenario is pessimistic because both parameter values seem unreasonable. We think to are more realistic values for the fraction of current economic tasks humans would only value if they were done by humans, and is a more realistic value for the elasticity of substitution in the human utility function. Combining these means we should expect around increase in GDP as a result of AGI even if we accept the argument that some tasks will not get automated as a result of human preferences for those tasks to be done by humans. This is, as mentioned previously, more than enough to produce explosive growth for an extended period of time.

As a reference point, note that likely matches how much gross world product has increased since the Industrial Revolution, and plenty of this came from increased task automation. So arguments based on intrinsic human preferences for some tasks being performed by humans seem like they would have made poor predictions if we had relied upon them in the past, and accordingly, we should be skeptical of them today as well.

We think that this argument will have some effect on economic growth, but do not consider it important for three main reasons:

-

1.

It’s not clear if all prices in the economy will actually be set by humans. If AIs can own property and are able to make consumption decisions as well, then gross world product would also take their preferences into account, and these preferences may not come with intrinsic demands that certain tasks must be performed by humans to be valuable.

-

2.

Quantitatively, the magnitude of the complementarity in the utility function and the mass of tasks that humans wish to be intrinsically done by other humans have to be quite large for this argument to block explosive growth.

-

3.

Even if explosive growth in gross world product is blocked, this does not necessarily mean that explosive growth is blocked in other physical variables that we might care about. These might include energy use, military strength, computer chip production, etc.

For all of these reasons, we consider this argument to be rather weak and do not think it should lead us to update our credence in explosive growth conditional on AGI downwards by a substantial amount. We consider it very unlikely that this argument blocks explosive growth.

3.8 Previous technological revolutions did not lead to growth acceleration

We have seen many other technological innovations in the past that changed how we live our lives: computers, electricity, cars, airplanes, etc. Nevertheless, while these technologies allowed the trend growth rate of around per year per person in the US and other developed economies to continue, they didn’t lead to any noticeable growth acceleration. If this is the relevant reference class for evaluating the plausibility of AI-driven explosive growth, we ought to assign a low prior chance to the possibility of explosive growth driven by AI.

Our view is that this argument is sound in general and gives us some uninformative prior over whether any new technology is likely to lead to explosive growth. The probability of this happening for a generic technology is, indeed, quite small: for instance, while fusion reactors would no doubt be economically valuable, we do not expect them to lead to explosive growth even if they became viable and cost-effective. However, the evidence that AI that can match human performance on most or all economic tasks is likely to lead to explosive growth is strong enough to overcome this general argument.

The key reason is that almost every model in endogenous growth theory makes the prediction that AI that’s capable of automating most or all economic tasks humans can perform at low cost (e.g. cost of human subsistence) has a substantial chance of leading to explosive growth. For some models, this prediction is robust to parameter choices; while in others it’s sensitive, but in either case we cannot rule out the possibility. For example, Section 2.1 predict explosive growth robustly conditional on full automation from AI, while, as we show in Section 2.2, constant returns to scale models make this prediction for a substantial fraction of plausible parameter values.

There is no comparable situation with most other technologies, and the reason is the important role played by labor in growth economics. Labor is unique in that it’s an input that’s both a key driver of economic production and growth and cannot be increased by reinvestment of economic output the same way capital, compute, energy etc. production can be. In other words, labor is non-accumulable, while other factors of production that are of comparable importance to labor are accumulable.

This means the potential economic benefits of a technology that can turn labor into an accumulable input are enormous: we turn the currently most important factor of production from something that is difficult to scale to something that is easy to scale. If we also assume that the cost of producing or maintaining this stock of accumulable labor inputs is not prohibitively expensive, almost all conventional growth models will predict explosive growth in this situation.

While the generic argument outlined in this section is convincing about most technologies, we believe that in the specific case of AI that’s capable of substituting for human workers, we have enough evidence to overcome the low prior that such an argument would assign to explosive growth conditional on AI. As a result, if the other objections to our argument (regulations, other bottlenecks, slow speed of automation, etc.) do not apply, we think this generic argument does not have any additional force. For this reason, we think it’s very unlikely that this argument blocks explosive growth.

3.9 Fundamental physical limits restrict economic growth

There might be fundamental physical limits to how much we can produce with a given amount of resources, or how quickly we can scale up production from current levels, regardless of how good our technology is. This objection may, for example, be found in ([1]). If these limits are sufficiently tight, they might prevent explosive growth. Some examples of such limits include the speed of light, conservation of energy, the Landauer limit for irreversible computing, the Bekenstein bound for energy density, Bremermann’s limit for reversible computing, Carnot’s theorem, etc.

In principle, this argument is valid: there will be fundamental physical limits that block economic growth at some point. Many, if not all, of the bounds listed above will be relevant in constraining growth in the far future. However, we find the argument unconvincing insofar as it’s meant to apply to explosive growth caused by AGI this century, because we’re simply too far from the relevant fundamental physical limits for the constraints imposed by them to be binding.

For instance, humans use around of the energy flux incident on Earth for production and consumption, and doing of computation on Earth alone seems feasible based only on fundamental physical limits, which at the cost of estimated in [8] for running the human brain would be sufficient to simulate virtual workers. This would be equivalent to scaling up the world population by 7 orders of magnitude. Even if every worker needs to be provided with amenities that match the current per capita energy consumption on the planet, there’s still room for a scaling up of 3 to 4 orders of magnitude.

We simply cannot come up with any plausible scenario in which economic growth is blocked early on as a result of a fundamental physical limit, as opposed to e.g. limitations of our engineering capabilities. As a result, we think this argument is rather weak. We think the chance that this argument blocks explosive growth conditional on AGI is small and conclude that it is very unlikely to block explosive growth.

4 Discussion