SupReferences

A Spike-and-Slab Prior for Dimension Selection in Generalized Linear Network Eigenmodels

Abstract

Latent space models (LSMs) are frequently used to model network data by embedding a network’s nodes into a low-dimensional latent space; however, choosing the dimension of this space remains a challenge. To this end, we begin by formalizing a class of LSMs we call generalized linear network eigenmodels (GLNEMs) that can model various edge types (binary, ordinal, non-negative continuous) found in scientific applications. This model class subsumes the traditional eigenmodel by embedding it in a generalized linear model with an exponential dispersion family random component and fixes identifiability issues that hindered interpretability. Next, we propose a Bayesian approach to dimension selection for GLNEMs based on an ordered spike-and-slab prior that provides improved dimension estimation and satisfies several appealing theoretical properties. In particular, we show that the model’s posterior concentrates on low-dimensional models near the truth. We demonstrate our approach’s consistent dimension selection on simulated networks. Lastly, we use GLNEMs to study the effect of covariates on the formation of networks from biology, ecology, and economics and the existence of residual latent structure.

Keywords: Generalized Linear Model; Model Selection; Network Latent Space Model; Statistical Network Analysis.

1 Introduction

Networks data is at the center of modern statistical applications in various fields, including sociology, biology, ecology, and economics. A network describes the relations, or edges, between pairs of entities, or nodes. This information is represented as an adjacency matrix with entries that quantify the relation between node and node . These edge variables can be binary with values in or weighted taking on any real value depending on the relation under study. For example, world trade is often studied as a network with weighted edge variables, , that represent the amount of bilateral trade in dollars between nations (Ward et al., 2013; Benedictis et al., 2014).

A fundamental goal in the analysis of network data is to understand the relationship between the edge variables and additional dyadic covariates . A popular approach focuses on estimating the regression function that relates the expected value of the edge variables to the dyadic covariates. Such a relationship is called assortative or dissassortative in the network literature depending on whether increasing a dyadic covariate increases or decreases the regression function. An example from economics is the gravity model, which models the expected bilateral trade between nations as a log-linear function of the nations’ gross domestic product and geographic distance (Tinbergen, 1962; Anderson, 1979), cf. Section 7. However, the assumption made by these traditional regression methods that the edge variables are independent conditional on the covariates is almost always invalidated by the presence of strong network dependencies such as degree, transitivity, and clustering effects (Kolaczyk, 2017; Hoff, 2021).

In the statistics literature, a solution is to introduce additional latent variables into the regression to capture the residual network dependencies, such that conditional on the latent variables the edge independence assumption holds. These latent variables usually take the form of latent variable network models including the -model (Graham, 2017; Yan et al., 2019; Stein and Leng, 2022), stochastic block models (Mariadassou et al., 2010; Huang et al., 2022), and latent space models (LSMs) (Hoff et al., 2002; Handcock et al., 2007; Krivitsky and Handcock, 2008; Ma et al., 2020). For a comprehensive overview of network models, see Goldenberg et al. (2010) and Kolaczyk (2017). In this work, we assume the latent variables take the form of a LSM which has garnered popularity due to its ability to capture various network structures while remaining amiable to interpretation and visualization. The key idea behind LSMs is that each node can be represented by a latent position in a low-dimensional () latent space, and nodes with similar latent positions will have a larger edge variable in expectation.

This paper tackles two problems in the Bayesian analysis of networks using LSMs: (1) Selecting the dimension of the latent space while also assessing its uncertainty, and (2) Accounting for this selection when assessing the covariate effects’ statistical uncertainty. The most popular approach to dimension selection minimizes a model selection criterion (Spiegelhalter et al., 2002; Watanabe, 2010; Sosa and Buitrago, 2021) or a metric calculated on data held out by a data splitting strategy such as cross-validation (Hoff, 2008; Chen and Lei, 2018; Li et al., 2020). For Bayesian LSMs, significant issues with these approaches are that they either are computationally intensive, lack theoretical support, or only apply to networks without covariates. As such, many Bayesian analyses forgo dimension selection altogether. Furthermore, any post-selection inference about the covariate effects will not account for the uncertainty induced by the dimension selection process.

Alternatively, a fully Bayesian solution places a prior over the latent space dimension and selects the dimension based on its posterior distribution. A difficulty with this approach is that most LSM likelihoods are invariant to the re-ordering of the latent space dimensions, so special priors are required to account for this non-identifiability. Early attempts used ordered shrinkage priors (Battacharya and Dunson, 2011; Durante and Dunson, 2014); however, these priors often induce undesirable overshrinkage due to their sensitivity to hyperparameter choice (Durante, 2017) and are unable to fully eliminate unnecessary dimensions from the model. As such, recent applications of the eigenmodel (Guhaniyogi and Rodriguez, 2020; Guha and Rodriguez, 2021) have employed spike-and-slab priors (Ishwaran and Rao, 2005) that penalize increasing model size. However, these priors share many weaknesses with the original ordered shrinkage priors because their increasing penalization only holds in expectation. Furthermore, all existing priors lack any theoretical guarantees that their penalization penetrates through to the posterior.

This work addresses these problems for a large class of models we call generalized linear network eigenmodels (GLNEMs), which are variants of the eigenmodel proposed by Hoff (2008, 2009). Traditionally, the eigenmodel relates a latent Gaussian edge variable to the regression function through a link function. The use of latent Gaussian random variables permits Bayesian inference over a variety of edge-types by facilitating a flexible Metropolis-within-Gibbs Markov chain Monte Carlo (MCMC) algorithm; however, it hinders the interpretation of the covariate effects since one must interpret them conditional on these latent variables. Instead, GLNEMs directly embed the eigenmodel in a generalized linear modeling framework with an exponential dispersion family random component and possibly non-canonical link functions. Importantly, under the GLNEM framework, we introduce new identifiability constraints on the latent positions that allow one to interpret the covariate effects as marginal effects independent of the latent variables.

The main thrust of this article is then the development of a computationally efficient and theoretically grounded Bayesian approach that can automatically identify the dimension of the latent space for GLNEMs. Our approach to dimension selection begins with a prior that induces posterior zeros with high probability. We introduce a novel spike-and-slab prior coupled with a non-homogeneous Indian buffet process prior (Griffiths and Ghahramani, 2011) that increasingly pulls coefficients to the spike at zero, which we call the truncated non-homogeneous spike-and-slab Indian buffet process. The advantages of this prior are three-fold: (1) we demonstrate that the prior induces a stochastic ordering that alleviates issues arising from the GLNEM likelihood’s invariance to the re-ordering of the latent space dimensions, (2) we provide a tail bound on the expected posterior latent space dimension that demonstrates concentration near the true number of dimensions, and (3) we identify hyperparameter values that are justified by our theoretical results. To the best of our knowledge, this is the first such theoretical guarantee for Bayesian LSMs.

Our final contribution addresses the challenge of designing an efficient MCMC algorithm that applies for all GLNEMs. This task’s difficulty is compounded by the fact that our proposed identifiability constraints require some parameters to lie on a sub-manifold of the Stiefel manifold. We address this issue by introducing a new parameter expanded prior based on the QR decomposition that is amiable to gradient based sampling methods. Under this prior, the target posterior distribution has marginal densities for the parameters of interest that satisfy the identifiability constraints. Furthermore, we use this prior to design a simple Metropolis-within-Gibbs sampler with efficient Hamiltonian Monte Carlo proposals (Neal, 2011; Hoffman and Gelman, 2014) that applies for any GLNEM.

The article is structured as follows. Section 2 introduces GLNEMs. Section 3 develops the truncated non-homogeneous spike-and-slab Indian buffet process and demonstrates properties sufficient for dimension selection. Section 4 provides a tail bound on the GLNEM’s posterior latent space dimension under the proposed prior. Section 5 describes our parameter expansion strategy and MCMC sampler. Section 6 investigates the proposed methods in a simulation study, and Section 7 applies them to networks from biology, ecology, and economics. Lastly, Section 8 contains a discussion.

2 Generalized Linear Network Eigenmodels

Here, we outline a class of latent space models for network data with dyadic covariates we call generalized linear network eigenmodels (GLNEMs). We start by fixing notation. Let refer to the set where is any indexed object. We denote the -dimensional vector of ones and zeros by and , respectively. We let represent the identity matrix. For a vector , we use to denote the diagonal matrix with the elements of on its diagonal. For a matrix , we denote the Frobenius norm as and the number of non-zero elements as . We denote the Stiefel manifold, which contains semi-orthogonal matrices, as . We use and to denote independently distributed and independent and identically distributed, respectively. Lastly, the proofs of all subsequent results can be found in Section A of the supplement.

2.1 Model Description

Suppose we observe an undirected network on a set of nodes, which is represented by an adjacency matrix with symmetric real-valued entries . For simplicity, we allow self-loops (i.e., diagonal entries) although these entries may be unobserved. We also observe additional -dimensional dyadic covariates for each pair of nodes and , denoted by . Let denote the matrix with the -th covariate of each dyad as entries, i.e., for .

In the tradition of generalized linear models (GLMs), an intuitive statistical model for the adjacency matrix specifies a systematic component that describes ’s expected value and a random component that categorizes its distribution. GLNEMs relate the adjacency matrix’s expected value to a linear function of the covariates and the latent space via a strictly increasing link function as follows:

| (1) |

where , is a real-valued diagonal matrix, is a matrix with the nodes’ latent positions as rows, and in a slight abuse of notation, is the link function applied element-wise to the matrix . The -th regression coefficient measures the extent of assortativity or disassortativity in the network attributed to the -th covariate depending on whether is positive or negative. The term captures latent low-rank residual network effects. This term takes the form of an eigen-decomposition, which motivates the eigenmodel name (Hoff, 2008). Similar to the regression coefficients, measures the amount of assortativity or disassortativity associated with the -th latent space dimension.

For the random component, we assume the edge variables are independent conditional on the dyad-wise covariates and the latent space:

| (2) |

where is a member of the exponential dispersion family with mean and known dispersion factor . That is, we assume that the edge variables are independently drawn from densities of the form

| (3) |

where is a natural parameter lying in , is a known dispersion factor, and and are known functions. Following the usual conventions for GLMs, we assume that the function is twice differentiable and strictly convex on so that the second derivate satisfies for every . It is easy to see that the expected value and variance of are and , respectively. The exponential dispersion family includes the Gaussian, binomial, Poisson, negative binomial, gamma, Tweedie, and beta distributions. Based on our choice of systematic component, we have

| (4) |

We refer to model (1) – (3) as a generalized linear network eigenmodel (GLNEM).

It is worth comparing the GLNEM framework to existing approaches. Unlike the eigenmodel proposed by Hoff (2008, 2009), which assumes , where , GLNEMs do not use latent Gaussian random variables. GLNEMs are also closely related to the generalized linear modeling framework for network data proposed by Wu et al. (2017), who replace with a general low-rank matrix. Unlike the model of Wu et al. (2017), GLNEMs allow for both dispersion and non-canonical link functions, which can provide a better fit to real-world networks as shown in Section 7. Next we present some concrete examples to demonstrate the utility of the GLNEM framework.

Example 1 (Binary Edges). For binary edge variables, an appropriate random component is a Bernoulli distribution. Setting , the cumulative distribution function of the standard normal distribution, one recovers the eigenmodel in Hoff (2008). Another common choice is the logistic link function. However, the GLNEM framework also includes the complementary log-log and log-log link functions, which have not appeared in the network literature.

Example 2 (Ordinal Edges). Ordinal edge variables are a common edge type, e.g., networks of counts. In this case, common choices for are the Poisson or negative binomial distribution. Often is used for both distributions despite being non-canonical for the latter. Furthermore, we found that the negative binomial model often results in lower-dimensional models when over-dispersion is present in the data, which often occurs in networks due to zero-inflation. See Section E of the supplement for details.

Example 3 (Non-Negative Continuous Edges). Edge variables are often non-negative continuous so that , e.g., world-trade networks. A solution proposed in the literature is the tobit model based on a latent Gaussian variable (Sewell and Chen, 2016); however, this model can be inappropriate for certain networks. For example, economists have scrutinized using the tobit model to model world trade due to the results depending on the units of measurement (Silva and Tenreyro, 2006), e.g., trade measured in dollars or billions of dollars. A solution under the GLNEM framework that has not appeared in the network literature is the Tweedie distribution (Jørgensen, 1987) with power parameter , which is invariant to the edge variables’ units. Furthermore, the Tweedie distribution is equivalent to a compound Poisson-gamma distribution, which is a reasonable data generating process for trade. See Section F of the supplement for more details.

2.2 Parameter Identifiability and Marginal Effect Interpretation

Identifiability of model (1) – (3) requires additional constraints on the model parameters. For and to be individually identifiable, we place a sum-to-zero constraint on ’s columns and require the node-averaged covariate matrix be non-singular. For the magnitude of to be identifiable, we must constrain the scale of . We adopt a constraint imposed by Hoff (2009) that requires to be a semi-orthogonal matrix. In summary, we make the following two assumptions:

Assumption A1.

, where .

Assumption A2.

.

Formally, we have the following proposition about the identifiability of the covariate effects.

Proposition 1 (Identifiability of Covariate Effects).

Importantly, the sum-to-zero constraint allows one to interpret ’s elements as marginal effects, which is usually not the case for LSMs (Minhas et al., 2018). Specifically, often one wants to quantify how the covariates affect the edge variables associated with a single node . It is natural to consider the average . In other words, the elements of represent the effect a covariate has on the average value of after marginalizing over the latent positions. For example, in the context of a Bernoulli GLNEM with a logistic link, is the marginal additive effect on the average log-odds ratio of forming an edge with node for a unit increase in feature , i.e., a unit increase in the average covariate increases the average log-odds of forming an edge with node by . Similarly, under a log link we can interpret as the marginal multiplicative effect on the geometric mean of the expected edge variables involving node . Note that we call these marginal effects because they are not conditional on keeping the latent positions fixed.

3 A Spike-and-Slab Prior for Dimension Selection

Now, we turn to the main contribution of this paper which is the development of a Bayesian procedure that can automatically identify the dimension of the latent space. In the context of GLNEMs, the dimension selection problem is equivalent to estimating , i.e., the number of non-zero diagonal elements of . As such our approach begins with a spike-and-slab prior on the diagonal elements of that induces posterior zeros with high probability. Furthermore, we expect additional dimensions to play a progressively less important role in describing the network structure. As a solution, we introduce a novel ordered spike-and-slab prior that induces a stochastic ordering of ’s elements and results in a posterior that asymptotically concentrates around the true dimension .

3.1 The Non-Homogeneous Spike-and-Slab Indian Buffet Process

To construct a prior with ordered shrinkage and dimension selection, we build upon the spike-and-slab priors (Ishwaran and Rao, 2005) and the Indian buffet process (Griffiths and Ghahramani, 2011). Specifically, let be a collection of random variables. We consider the following spike-and-slab prior on with a shrinking sequence of slab probabilities :

| (5) |

where , , and and are the distributions of the spike and slab components, respectively. Because our prior uses the stick-breaking construction of the Indian buffet process, we denote the prior in (5) as the non-homogeneous spike-and-slab Indian buffet process prior truncated at , or . The hyperparameters of this prior are determined by , , and the scalars and . We call this prior non-homogeneous because we draw from a two-parameter Beta distribution and the remaining parameters from a one-parameter Beta distribution. We will show that this non-homogeneous IBP is sufficient to obtain posterior concentration around the true dimension when used as a prior for in GLNEMs.

The ordering of the slab probabilities induces a stochastic ordering of the parameters under the prior, which is formalized in the following proposition.

Proposition 2 (SS-IBPs Induce a Stochastic Ordering).

For and fixed , let denote the -ball centered at . Under the , whenever .

Intuitively, for any that is favored by the spike distribution relative to the slab , the places more mass around as increases. We usually set , which implies the prior places more mass around zero as increases.

Next we turn to an important property of the prior’s tail behavior that is crucial for obtaining a posterior that is adaptive to the latent space dimension and may be of interest for applications outside GLNEMs. When is a point mass concentrated at zero, the prior induces an implicit prior on the number of non-zero elements of , that is, , that favors low-dimensions. Formally, the next theorem shows that this induced prior has exponentially decaying tails when we set and and appropriately.

Theorem 1 (The Prior on has Exponentially Decaying Tails).

If for , , and , then for any ,

| (6) |

It has been widely observed in the literature on posterior asymptotics that an exponentially decaying tail is an sufficient property for obtaining optimally behaving posteriors (Castillo and van der Vaart, 2012; Ročková and George, 2016). Note that Theorem 1 leaves the slab distribution unspecified; however, a sufficiently heavy-tailed slab is used in Theorem 2 to ensure property (6) transfers to the posterior.

3.2 An SS-IBP Prior for in GLNEMs

Now, we use the to construct a prior for that promotes sparsity and induces a soft identifiability constraint that counteracts the permutation invariance of the GLNEM’s likelihood. In particular, we use the following prior:

| (7) |

where denotes a Laplace distribution centered at the origin with scale .

The next corollary to Proposition 2 states that this prior induces a stochastic ordering on ’s diagonal elements, which counteracts the likelihood’s column permutation invariance.

Corollary 1.

If are drawn from the SS-IBP prior defined in (3.2), then, for any , , whenever .

This corollary follows immediately from the fact that the Laplace distribution puts greater mass around zero when the scale parameter is near zero. In particular, the condition ensures that the spike distribution is more concentrated around zero than the slab distribution. In the remainder of this article, we will set , which corresponds to using a discrete spike-and-slab prior with , a point mass concentrated at 0. We provide the more general result because setting can have computational advantages.

4 Theoretical Results on Dimension Selection

Next, we provide theoretical support for using the posterior distribution of to infer the dimension of the latent space for GLNEMs when an SS-IBP prior is placed on . Specifically, we consider the following model augmented with priors for the parameters:

where the edge variable’s distribution function is a member of the exponential dispersion family defined in (2), is any distribution fully supported on , , and . Because we will study the asymptotics of the posterior distribution as the number of nodes goes to infinity, we will denote the adjacency matrix by and the dyad-wise covariate matrices by for to make the dependence on apparent. We denote the posterior distribution as .

The goal of our analysis is to study the frequentist properties of the posterior distribution assuming the matrices are generated from model (1) – (3) with true non-zero latent space dimension and true parameters where , and . Let and denote the probability and expectation under this true data generating process. We consider the scenario that grows with while is fixed. As such, we must also increase the prior’s truncation level as increases. We find that the following conditions on the growth rate of are sufficient to obtain our results:

Condition C1 (Growth of with ).

for some .

Condition C2 (Bounded scale parameter).

For sufficiently large , for a constant independent of .

Condition C1 requires to grow as a fractional power of . Condition C2 constrains the scale of the Laplace slab. This condition holds when is a constant or grows as a fractional power (less than or equal to ) of , such as our choice of in the following sections.

Next, we make the following assumptions on the truth:

Assumption A3 (Growth of ).

as .

Assumption A4 (Bounded ).

for some .

Assumption A5 (Bounded latent space).

for some .

Assumption A6 (Bounded covariate effects).

for some .

Assumption A7 (Bounded covariates).

for some .

Assumption A3 sets the growth rate of the true latent space dimension relative to the truncation level , which trivially holds for the common assumption that is bounded due to Condition C1. Assumptions A4 – A7 are equivalent to bounding , which is common in the LSM literature (Wu et al., 2017; Ma et al., 2020). For a Bernoulli GLNEM, these bounds imply that the resulting networks are dense.

Finally, we need the following mild assumptions about the function and the link function . These conditions are satisfied by all GLNEMs in this work.

Assumption A8 (Bounded variance).

For any compact subset , there exists positive constants such that .

Assumption A9 (Inverse link has a bounded derivative).

The next theorem states that the average posterior probability that overshoots a constant multiple of the true latent space dimension goes to zero as the number of nodes and prior truncation level simultaneously increase.

Theorem 2 (The Posterior Concentrates on Low Dimensions in Expectation).

Practically, Theorem 2 justifies the following strategy for estimating . Without knowledge of , one would set the prior truncation level as large as possible with the hope that the shrinkage prior will select an appropriate dimension. An objection to this strategy is that employing too many latent dimensions may cause the posterior to over-estimate the dimension of the latent space due to over-fitting. Theorem 2 alleviates this concern by showing that the posterior will asymptotically concentrate on low-dimensional latent spaces near the true dimension .

5 Estimation

In this section, we develop a Markov chain Monte Carlo (MCMC) algorithm to sample from the GLNEM’s posterior. Due to the high-dimensionality of the latent variables and the necessity to provide an algorithm that applies over a wide range of random and systematic components, we use gradient-based sampling methods. Specifically, we propose a Metropolis-within-Gibbs sampler with Hamiltonian Monte Carlo (HMC) proposals. However, the requirement that must lie in poses a challenge for gradient-based samplers because they often require the parameters to lie in an unconstrained space. As such, we first propose various parameter expansion strategies that overcome this limitation.

5.1 A Prior Over

An explicit prior density over centered semi-orthogonal matrices is difficult to construct due to the constraints placed on these matrices. In fact, we are unaware of any explicit prior density over currently used for Bayesian inference. Instead, we use the following probabilistic construction based on the QR decomposition:

-

1.

Sample with entries independently drawn from a standard normal .

-

2.

Calculate the unique QR decomposition of , i.e., , where and is an upper-triangular matrix with positive elements on its diagonal.

-

3.

Set to the last columns of , i.e., .

This procedure generates a matrix since the columns of lie in the orthogonal complement of , where is the first column of . To make the dependence of on explicit, we denote as a matrix constructed in this fashion. Also, the following result holds.

Proposition 3.

The support of the probability distribution of equals .

This proposition states that the probability distribution induced by steps 1–3 assigns positive probability to all open neighborhoods of ’s elements, which makes the distribution suitable as a prior when performing posterior inference over parameters in . Lastly, since this procedure is differentiable with respect to (Walter et al., 2012), we can easily include it as a prior in gradient-based sampling methods such as the one we develop in Section 5.3.

5.2 Hierarchical Representation of the SS-IBP with a Laplace Slab

To improve the mixing of the MCMC algorithm, we use a hierarchical representation of the prior based on the exponential scale mixture representation of the Laplace distribution (Park and Casella, 2008). The slab probabilities come from (5); however, we introduce binary indicator variables, , such that for ,

Marginalizing over and recovers the original prior. To further improve mixing, we use a non-centered parameterization (Papaspiliopoulos et al., 2007) for , that is, we set , where for . We denote to make the dependence of on clear.

5.3 The Metropolis-within-Gibbs Sampler

Here we outline the MCMC algorithm that we use to sample from the GLNEM’s posterior. Let denote the collection of model parameters excluding the dimension indicator variables . Overall, the algorithm is a Gibbs sampler that alternates between sampling and from their full conditional distribution and , respectively. To sample from , we use Hamiltonian Monte Carlo (HMC) with adaptive tuning parameter selection (Neal, 2011; Hoffman and Gelman, 2014) as implemented in NumPyro (Phan et al., 2019; Bingham et al., 2019). To sample from using NumPyro’s HMC routine, we must provide the logarithm of this density up to an additive constant, which can be found in Section B of the supplementary material. The model parameters are initialized as detailed in Section C of the supplementary material. Algorithm 1 outlines the full Metropolis-within-Gibbs algorithm.

Up until now, we have made the unrealistic assumption that the dispersion parameter is known. In addition, the Tweedie distribution has an unknown power parameter . Under the proposed Bayesian inference scheme, we can infer these parameters by giving them priors and analyzing their posteriors. We place a half-Cauchy prior on and a uniform prior on , i.e., and . The truncation of the endpoints for avoids the multimodality of the Tweedie density. These parameters are then sampled as a part of step 1 in Algorithm 1. Because the normalizing constant for the Tweedie distribution is intractable, we approximate it using the series expansion proposed by Dunn and Smyth (2005).

Given the previous parameters and , update the current parameters as follows:

-

1.

Sample from defined in Equation (18) of the supplementary material using HMC with adaptive tuning.

-

2.

Let and set . For :

Note that denotes a different random permutation of at each iteration. Also, we use to indicate the collection of with the -th element removed, i.e., .

Although the prior places soft identifiability constraints on the parameters, the posterior remains invariant to signed-permutations of ’s columns. As such, we post-process the posterior samples by matching to some reference configuration based on the Frobenious norm. We take the maximum a posteriori (MAP) estimates as the reference. This matching is a linear assignment problem, which we solve with the Hungarian method (Kuhn, 1955). In addition, ’s posterior mean is not guaranteed to lie in . As such, we take a Bayesian decision theoretic approach and use ’s posterior Fréchet mean as a point estimate. See Section C of the supplementary material for details.

6 Simulation Studies

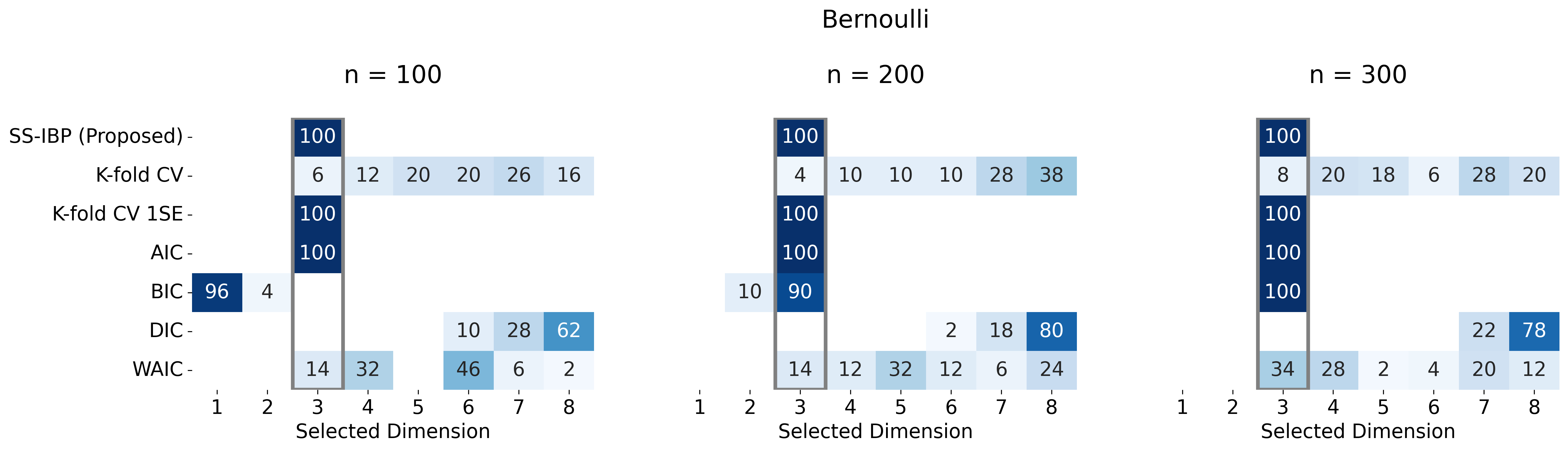

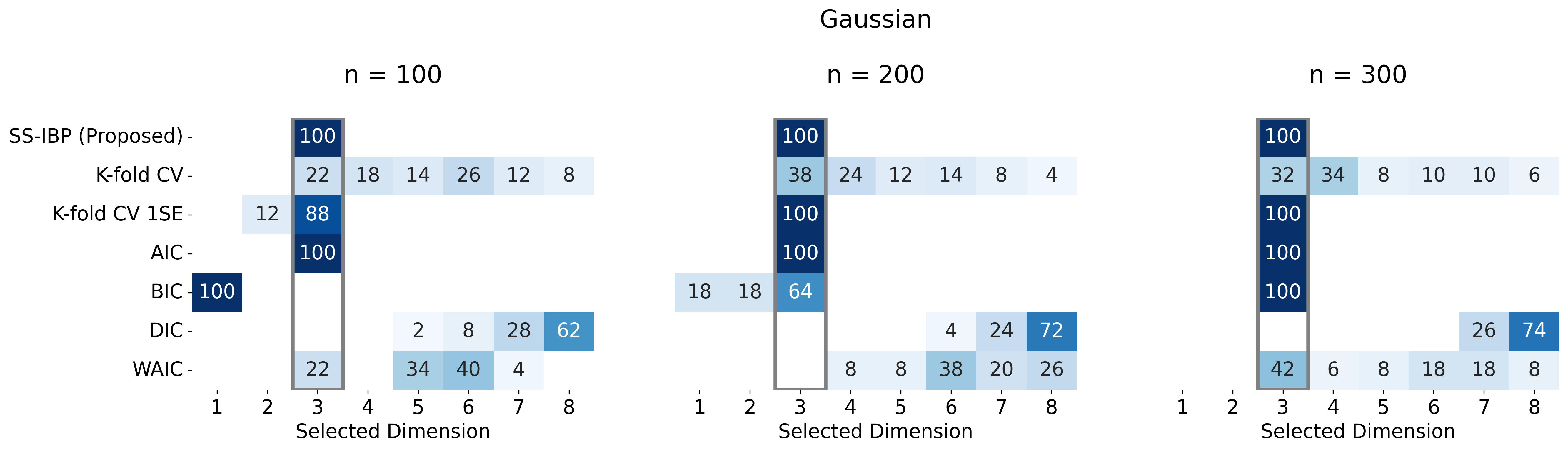

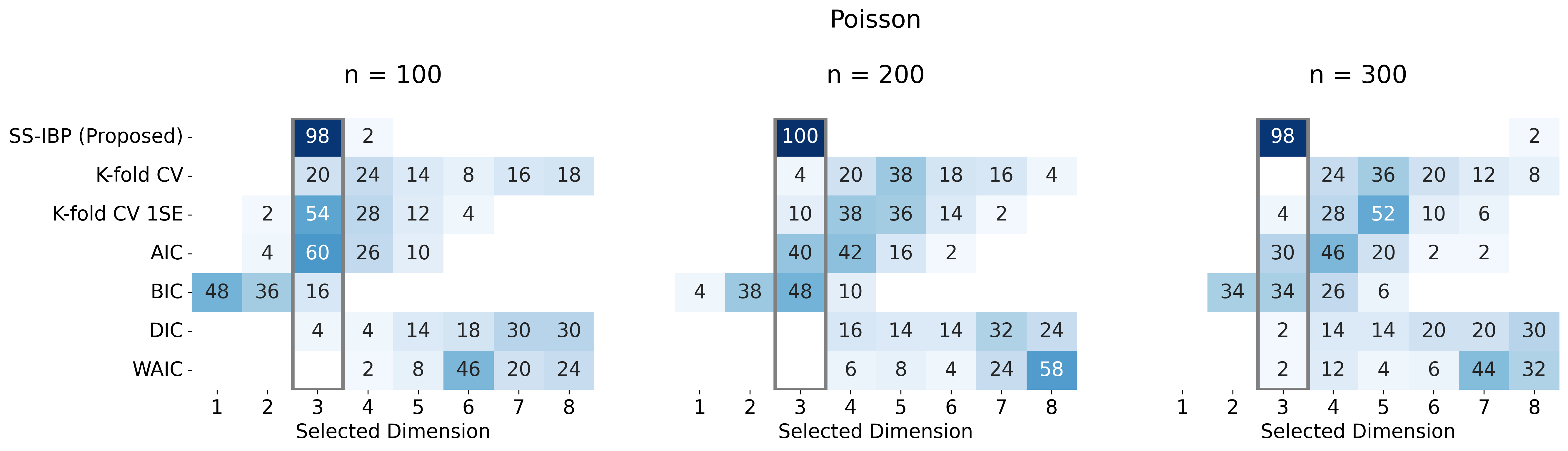

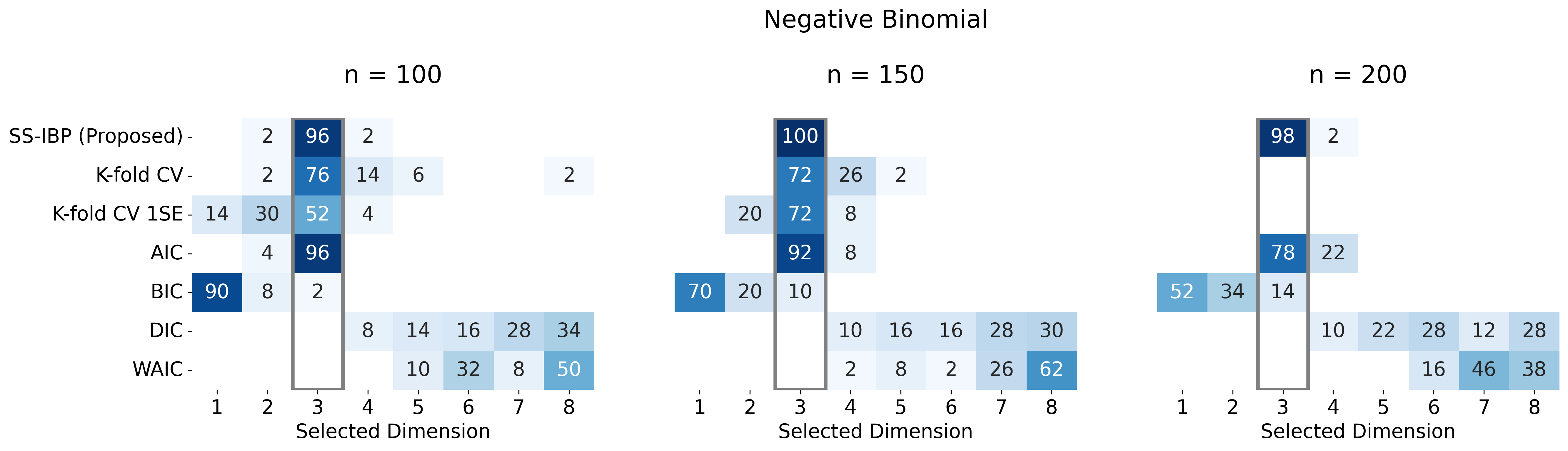

In this section, we present simulation studies that assessed different properties of the SS-IBP prior and our estimation method. We performed two studies that evaluated the following tasks: (1) the ability of the MCMC algorithm to recover the model parameters, and (2) the accuracy of the prior in recovering the true dimension of the latent space compared to existing methods. An assessment of the method’s sensitivity to model misspecification and zero-inflation is included in Section E of the supplement.

6.1 Simulation Setup and Competing Methods

For various values of , we generated 50 synthetic networks from the following five GLNEMs with parameters and true dimension : (1) Bernoulli with a logistic link, (2) Gaussian with an identity link and variance , (3) Poisson with a log link, (4) negative binomial with a log link and dispersion , and (5) Tweedie with a log link, dispersion , and power parameter . For each network, we sampled an initial latent position matrix by drawing , where . We set , where was constructed using the procedure described in Section 5.1. We sampled ’s diagonal elements from a Gaussian mixture for . We set for the Bernoulli and Gaussian models, for the Poisson and negative binomial models, and for the Tweedie model. We included five dyadic covariates. For each dyad, we set to account for an intercept and we drew for . We set . We set the intercept to for all models except the Gaussian model where we set it to to better match the positive values found in real data. We set in all simulations.

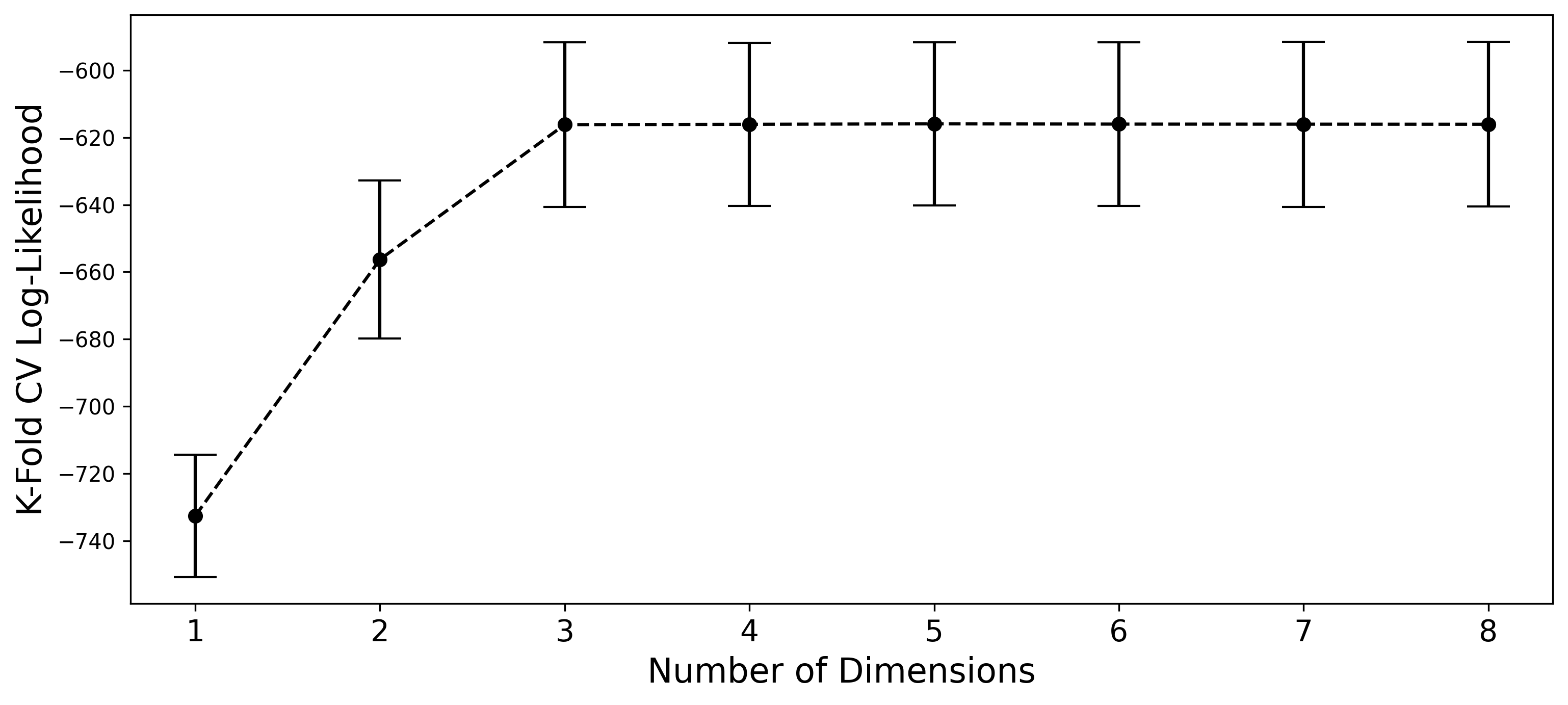

We compared our proposed SS-IBP prior with two alternative selection criteria commonly used in the latent space literature: minimization of information criteria and K-fold cross-validation. For the information criteria, we considered the Akaike information criterion (AIC), Bayesian information criterion (BIC), deviance information criterion (DIC), and the Watanabe-Akaike information criterion (WAIC). The K-fold cross-validation (K-fold CV) scheme used folds, where the folds defined a non-overlapping partition of the network’s dyads. We selected the dimension that maximized the held-out log-likelihood averaged across all folds. We found that the K-fold CV tended to overestimate the latent space dimension due to the held-out log-likelihood curves increasing drastically around the true dimension and slowly decreasing afterword. To compensate for this behavior, we included the one standard error rule, which selected the smallest model within one standard deviation of the best model (K-fold CV 1SE). The competing methods placed a prior on the diagonal of as in Hoff (2009). We estimated these models by running NumPyro’s HMC algorithm for 5,000 iterations after a burn-in of 5,000 iterations. Section D of the supplementary material has more details on the competing methods.

Lastly, we estimated the GLNEMs with SS-IBP priors by running the MCMC algorithm proposed in Section 5 for 5,000 iterations after a burn-in of 5,000 iterations. To match the theory developed in Section 4, we set and . Furthermore, we used a truncation level of in all simulations. For the remaining hyperparameters, we set and , which resulted in relatively broad priors.

6.2 Parameter Recovery

This section presents results that demonstrate the ability of the MCMC algorithm proposed in Section 5 to recover the model parameters as the number of nodes increases. To evaluate the estimators’ accuracy, we compared the top three dimensions ranked by their posterior inclusion probabilities, , to the ground truth. Our evaluation metrics included the trace correlation between the ground truth and estimated latent positions, i.e., , and the relative error with respect to the squared Frobenius norm between the true and estimated matrix and coefficients . We also include the relative error between the true and estimated matrix , which was estimated using all eight latent dimensions.

Table 1 displays the results. Note that the trace correlation ranges from to 1, with one indicating a perfect alignment of the subspaces spanned by and . For the relative errors, smaller is better. In all cases, the MCMC algorithm is able to recover the model’s parameters with high accuracy. Furthermore, the performance increases with the number of nodes. As such, we can conclude that the MCMC algorithm is successful in estimating the model parameters for a wide variety of GLNEMs.

| GLNEM | Trace Corr. | Rel. Error | Rel. Error | Rel. Error | |

|---|---|---|---|---|---|

| 100 | 0.909 (0.074) | 0.004043 (0.003925) | 0.156 (0.021) | 0.01157 (0.0084) | |

| Bernoulli | 200 | 0.965 (0.066) | 0.000909 (0.000826) | 0.078 (0.007) | 0.00313 (0.0018) |

| 300 | 0.977 (0.057) | 0.000380 (0.000337) | 0.052 (0.004) | 0.00102 (0.0011) | |

| 100 | 0.926 (0.067) | 0.002575 (0.002996) | 0.173 (0.027) | 0.01325 (0.0086) | |

| Gaussian | 200 | 0.960 (0.052) | 0.000581 (0.000524) | 0.086 (0.009) | 0.00389 (0.0025) |

| 300 | 0.975 (0.066) | 0.000179 (0.000195) | 0.058 (0.005) | 0.00138 (0.0012) | |

| 100 | 0.945 (0.052) | 0.001652 (0.002492) | 0.141 (0.051) | 0.00250 (0.0024) | |

| Poisson | 200 | 0.977 (0.040) | 0.000407 (0.000291) | 0.066 (0.015) | 0.00069 (0.0006) |

| 300 | 0.986 (0.141) | 0.000147 (0.313174) | 0.044 (0.167) | 0.00029 (0.0099) | |

| 100 | 0.924 (0.172) | 0.002722 (0.195986) | 0.199 (0.173) | 0.00521 (0.1216) | |

| Neg. Bin. | 150 | 0.951 (0.033) | 0.001147 (0.001195) | 0.132 (0.034) | 0.00217 (0.0017) |

| 200 | 0.965 (0.041) | 0.000599 (0.000543) | 0.100 (0.018) | 0.00139 (0.0008) | |

| 50 | 0.935 (0.079) | 0.009565 (0.008941) | 0.118 (0.026) | 0.17972 (0.0983) | |

| Tweedie | 100 | 0.969 (0.055) | 0.001007 (0.000831) | 0.043 (0.006) | 0.02304 (0.0157) |

| 150 | 0.982 (0.057) | 0.000313 (0.000257) | 0.027 (0.003) | 0.00990 (0.0060) |

6.3 Dimension Selection

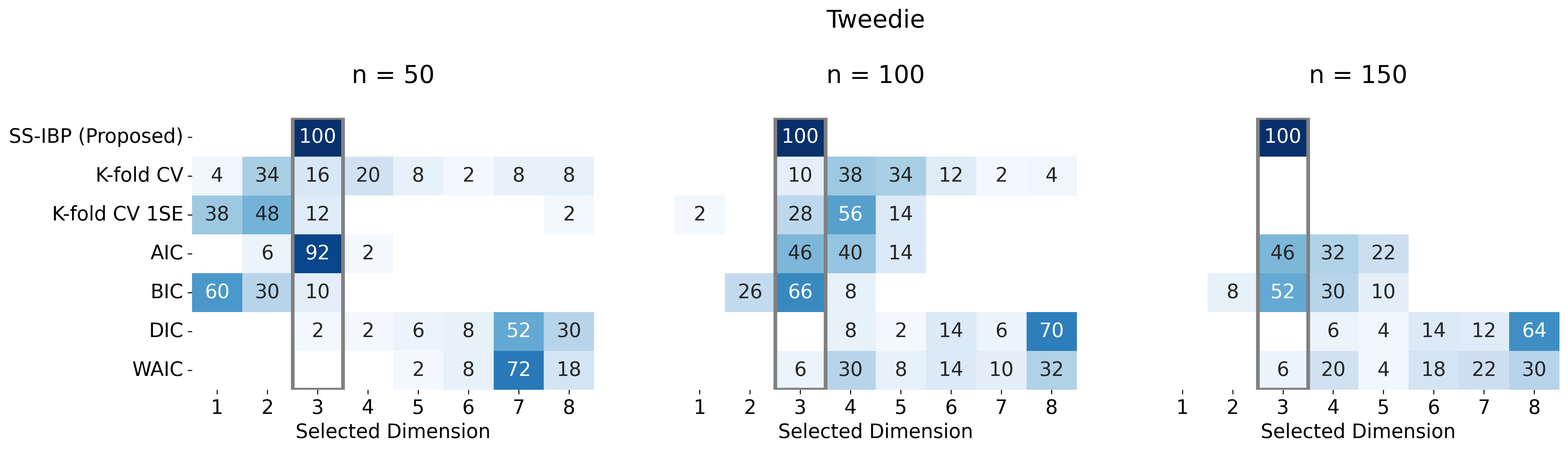

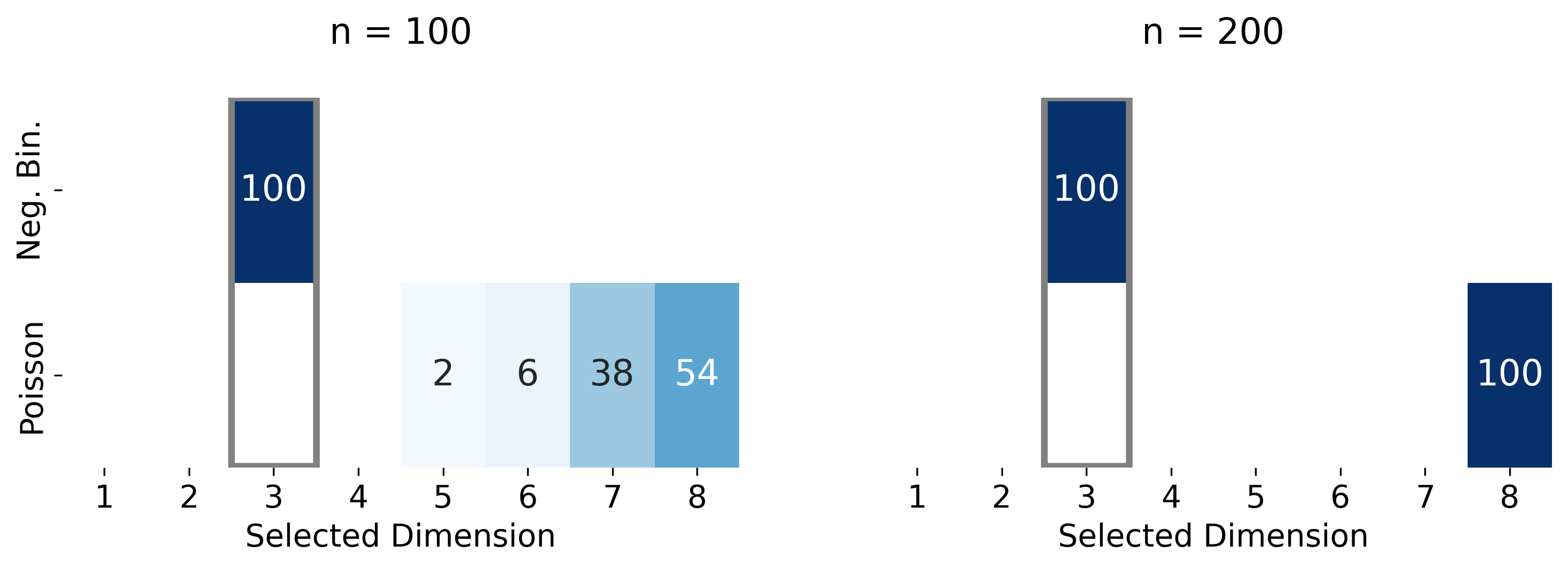

Here, we assess the ability of the proposed spike-and-slab prior to select the correct number of dimensions. We used the same simulation setup described in Section 6.1 with true latent space dimension . Figure 1 and Figure 2 display heatmaps of the percentage of times a dimension was selected by the proposed SS-IBP prior and its competitors over the 50 simulations for GLNEMs with canonical and non-canonical link functions, respectively. Note that the proposed SS-IBP estimates the latent space dimension based on the posterior mode, that is, . The proposed SS-IBP prior performed the best or equivalent to the best in all scenarios. In contrast, the DIC and WAIC estimators often overestimate the number of latent space dimensions. The BIC estimator often underestimated the latent space dimension except for the Bernoulli case where it has competitive performance for larger networks. The K-fold CV estimator performed poorly except for the negative binomial distribution. The ad-hoc K-fold CV 1SE performed well for the Bernoulli and Gaussian models, but poorly otherwise. Note that we did not compute the cross-validation estimators for the largest network sizes of the negative binomial and Tweedie models because they took more than a day to compute for a single simulation. Finally, the AIC estimator performed well for the Bernoulli, Gaussian, and negative binomial models, but performed poorly for the Poisson and Tweedie models. Overall, unlike the competing methods, the SS-IBP prior has excellent performance for a variety of GLNEMs. The SS-IBP prior is also less computationally intensive than the competitors because it requires only a single MCMC run. The SS-IBP prior also inherently accounts for the uncertainty due to the latent space dimension, unlike the competitors.

7 Real Data Applications

To illustrate the benefits of the proposed methodology, we used it to analyze networks arising from different scientific fields, namely biology, ecology, and economics. The first example studies a binary network of interactions between 270 proteins of E. coli. The second example investigates the similarities between 51 tree species based on a count network of shared fungal parasites. Finally, the third example analyzes trade in bananas between 75 nations based on a network with non-negative continuous edges. All GLNEMs were estimated using the same hyperparameter values outlined in the simulation studies.

7.1 Protein-Protein Interactions

Here, we re-analyze a binary network of protein-protein interaction data from Butland et al. (2005) that was introduced as a benchmark for the eigenmodel by Hoff (2009). Each node corresponds to an essential protein of E. coli with proteins overall. A binary edge () is recorded if protein and protein interact, otherwise .

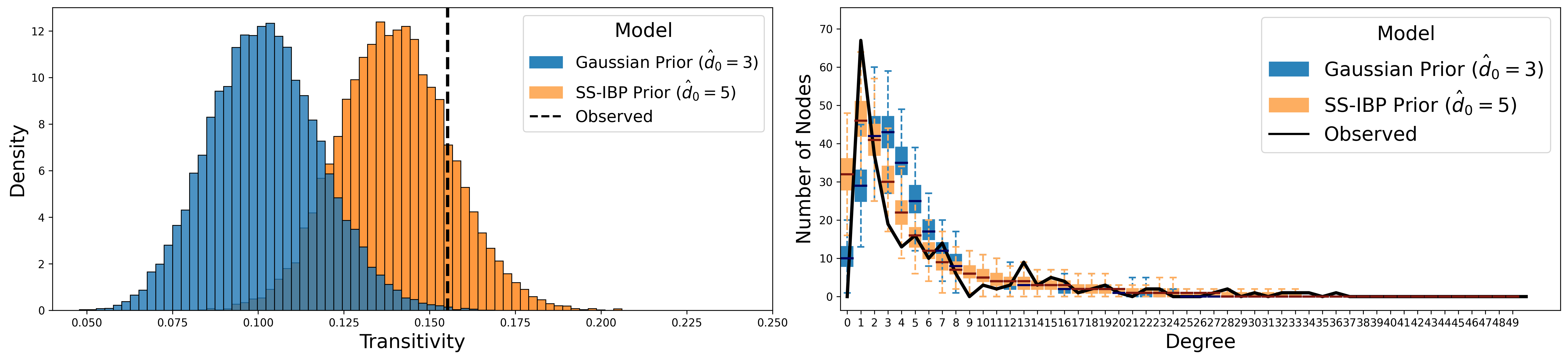

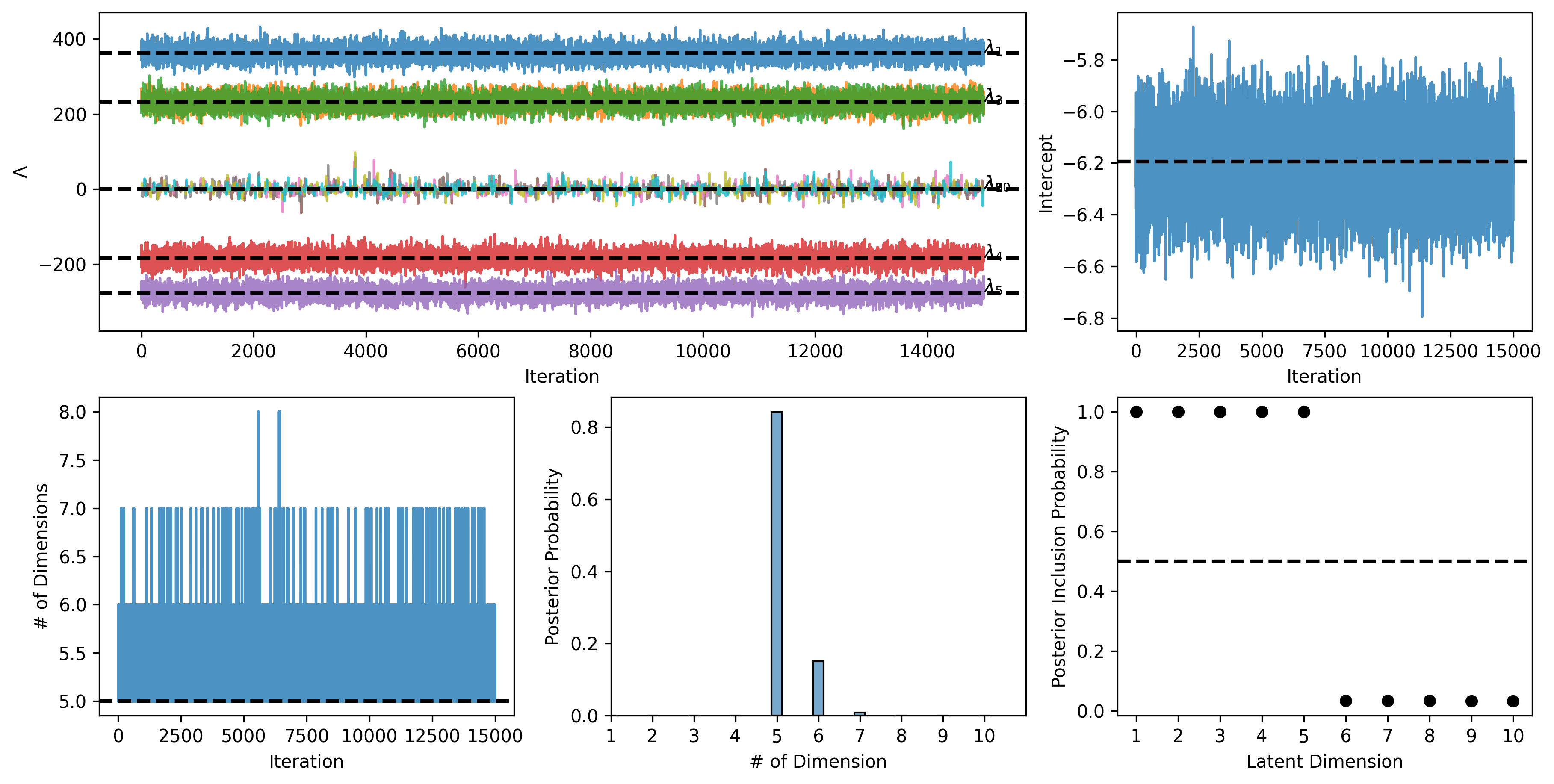

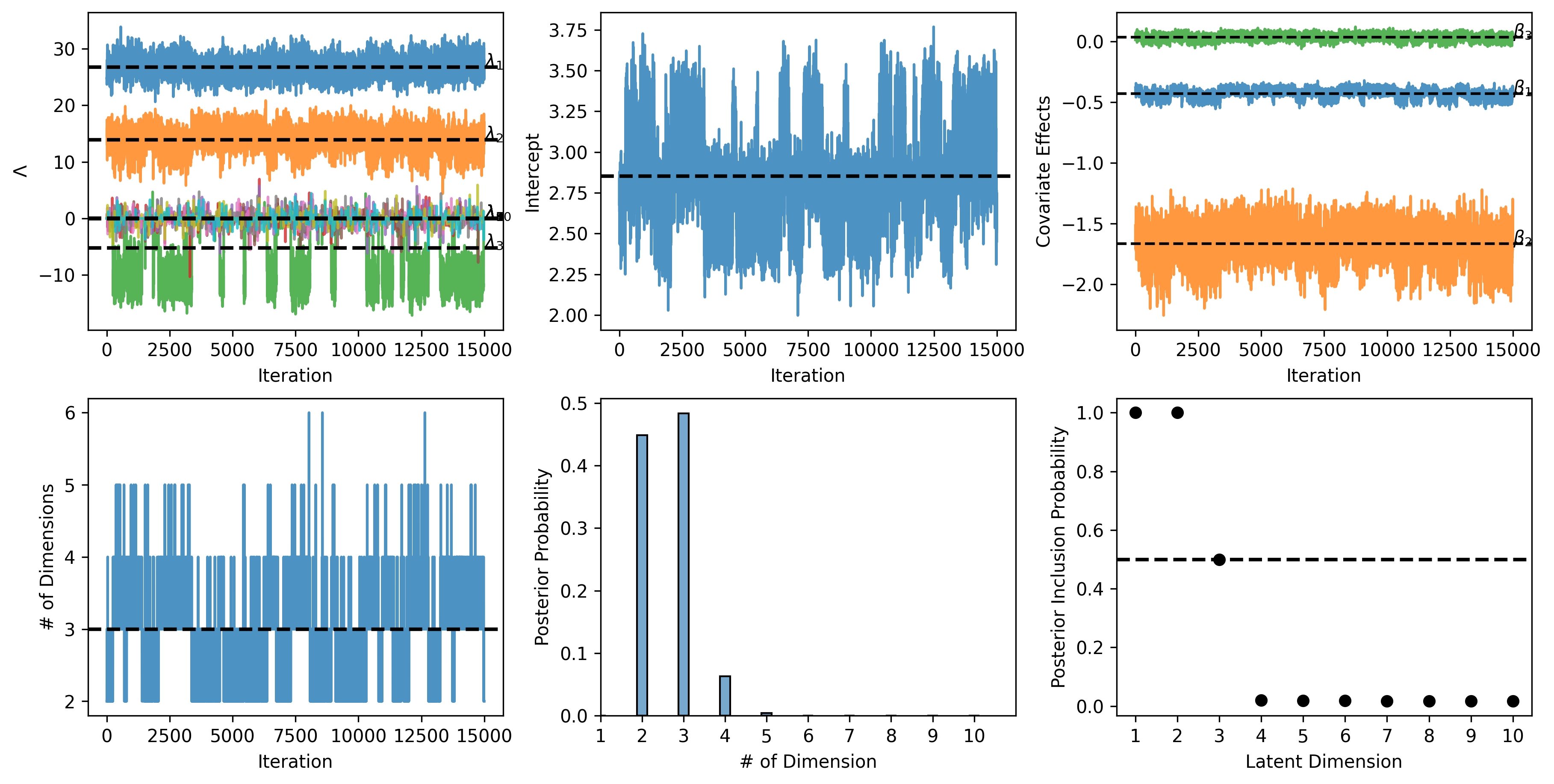

In this analysis, we demonstrate that the proposed SS-IBP prior selects a better fitting model than the K-fold cross-validation estimator used in previous analyses (Hoff, 2008, 2009; Jauch et al., 2021). Specifically, we estimated a Bernoulli GLNEM with a logistic link using both our proposed SS-IBP prior and the prior used in the original analysis. Note that the original analysis used a probit link; however, we use a common logistic link to focus on the differences due to model size. Since there are no dyadic covariates, the model only contains an intercept. We estimated both models by running the MCMC algorithms for 15,000 iterations after a burn-in of 7,500 iterations. The Gaussian model using the K-fold CV 1SE estimator with and estimated , which matches the original analysis. For the SS-IBP prior we set and made the same hyperparameter choices as described in Section 6.1. The posterior mode selected dimensions. See Figure 9 and Figure 10 in Section G of the supplement for summaries of these selection procedures.

A natural approach to comparing the goodness-of-fit of two network models is based on their predictions of observed quantities (Hunter et al., 2008). As such, we demonstrate that the proposed model better describes the data by comparing the two models’ posterior predictive distributions of the transitivity coefficient and the degree distribution. We chose to use the transitivity coefficient because latent space models are often used to explain the high levels of transitivity found in real-world networks. We included the degree distribution because the network science literature puts tremendous focus on this statistic. Figure 3 displays the results. The proposed model better fits the data based on both statistics. The three-dimensional model underestimates the transitivity, while the observed transitivity falls within the SS-IBP model’s posterior predictive distribution. Similarly, the degree distribution more closely matches the SS-IBP model, although both models underestimate the number of single degree nodes and overestimate the number of isolated nodes.

7.2 Host-Parasite Interactions Between Tree Species

In ecology, networks are often used to study the extent that species are related. Here, we consider an ordinal-valued network of tree species introduced by Vacher et al. (2008), where the edge variables represent the number of shared fungal parasites between tree species and . In addition, three dyadic covariates are measured that represent different distances between pairs of tree species: taxonomic (), geographic (), and genetic () distances. This network was previously analyzed using a Poisson stochastic block model with covariates in Mariadassou et al. (2010) and Donnet and Robin (2021).

Similar to Mariadassou et al. (2010), our goals are to understand how the covariates affect the number of shared fungal parasites and to describe any potential residual network structure after accounting for the covariates. We consider two models for networks with ordinal edge variables: A Poisson and negative binomial GLNEM both with a log link and an SS-IBP prior. We included the negative binomial model because the network is potentially zero-inflated with 46% of the edges equaling zero. We estimated the models by running the MCMC algorithm for 15,000 iterations after a burn-in of 7,500 iterations.

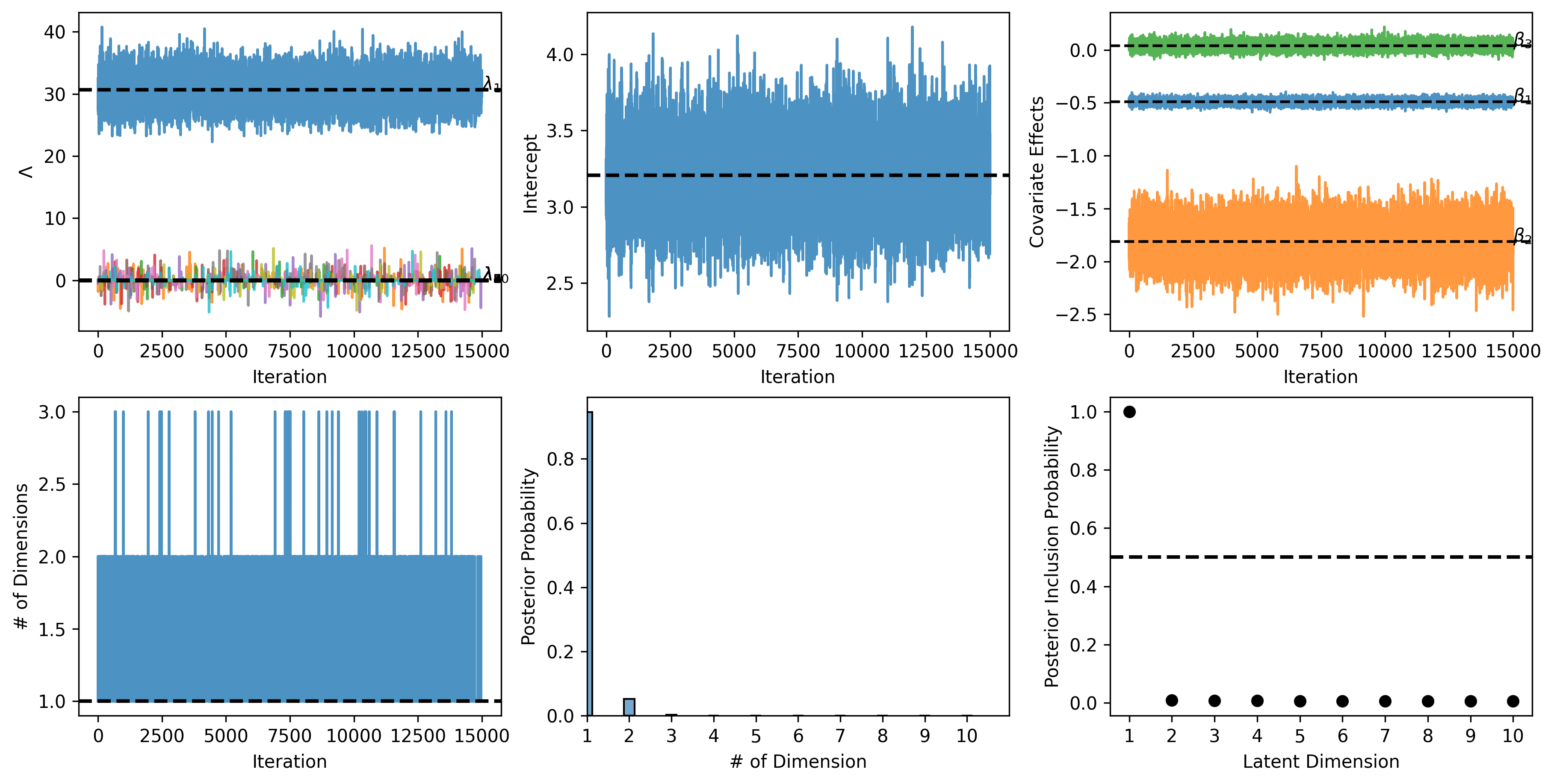

To choose between the models, we examined the dispersion parameter of the negative binomial GLNEM, which reduces to the Poisson GLNEM when is zero. The 95% credible interval for is (0.43, 0.62), which is well above zero and provides support for the negative binomial GLNEM. Furthermore, the WAIC of the Poisson and negative binomial models are 3957 and 3807, respectively, which also favors the negative binomial model. The negative binomial model also has a lower-dimensional latent space with the one-dimensional space receiving 95% of the posterior probability. On the other hand, the Poisson model was split between a latent space with two (posterior probability of ) and three (posterior probability of ) dimensions. See Figure 11 and Figure 12 in Section G of the supplement for posterior summaries. As demonstrated in the simulation study in Section E of the supplement, the negative binomial model’s lower dimension may be due to zero-inflation.

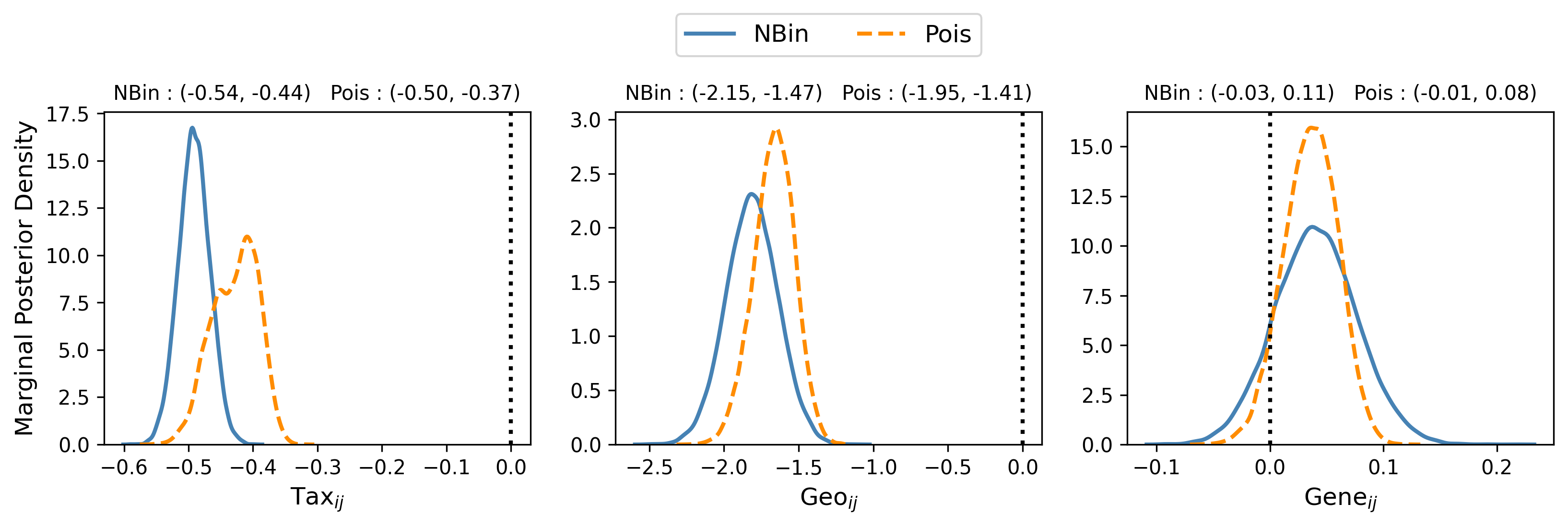

Despite the two models’ differences, Figure 4 demonstrates that their inferences about the covariates’ marginal effects are roughly the same. Both models indicate that increasing a tree’s average taxonomic or geographic distance to other trees in the network decreases the geometric mean of its expected number of shared parasites, while genetic distance is insignificant when these variables are in the model. These conclusions match the original analysis by Mariadassou et al. (2010); however, their results are conditional on the network structure. Also, note that under the Poisson GLNEM, the posterior density of ’s coefficient has two local modes due to the mixing of the two and three dimensional models.

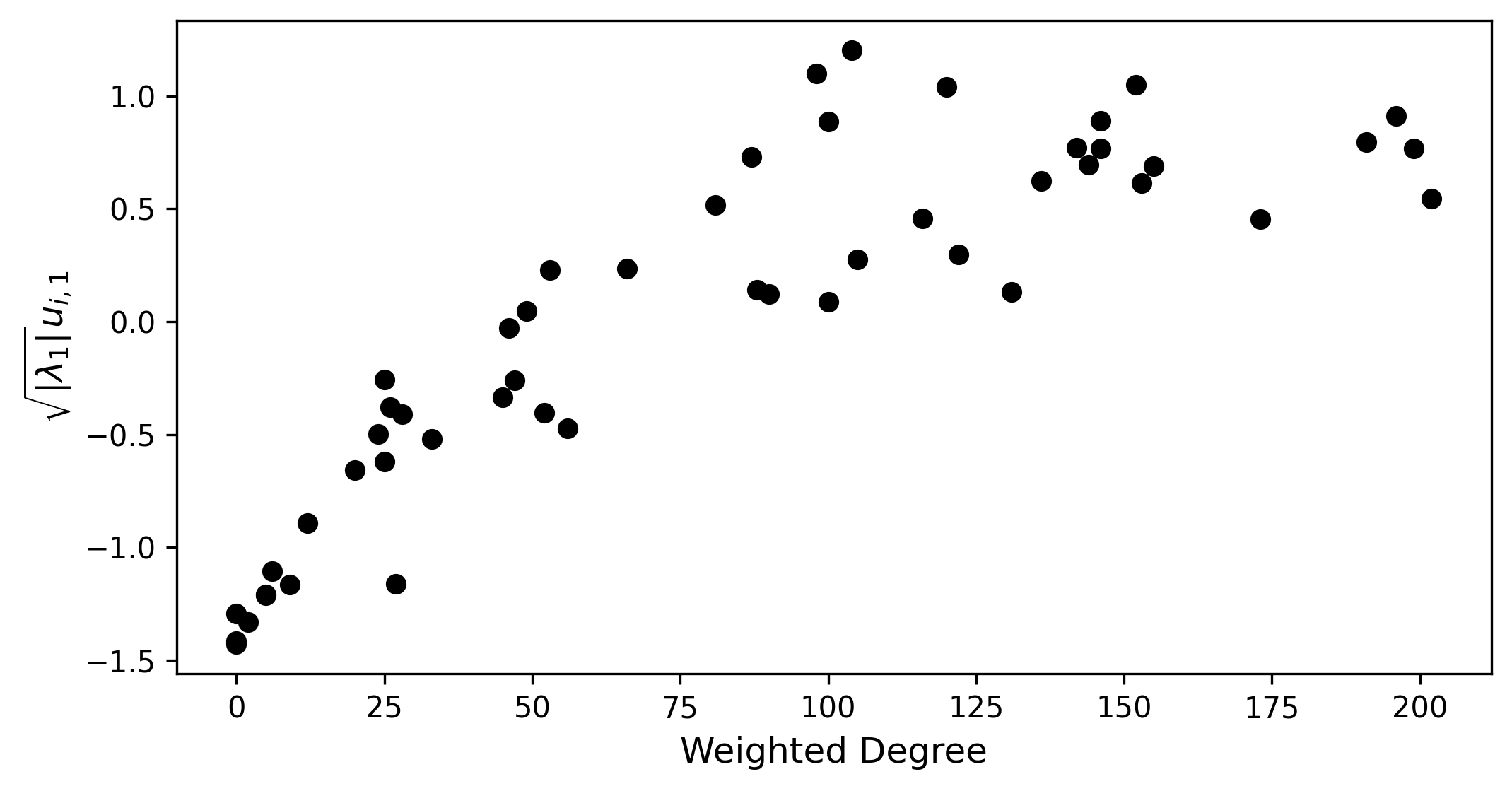

Next, we analyze the residual network structure captured by the one-dimensional latent space in the negative binomial model. The scatter plot in Figure 5 demonstrates that a node’s latent position is highly correlated with its weighted degree with a Pearson correlation equal to 0.86. The 95% credible interval for is (26.61, 34.42) indicating assortativity along this dimension. These observations suggest that the latent space acts as a degree correction in the model. In conclusion, the negative binomial GLNEM fits the network data better than the Poisson GLNEM and also has a simpler latent structure.

7.3 International Trade of Bananas in 2018

Lastly, we consider the international trade of bananas, which is a topic of academic research (Josling and Taylor, 2003) and listed as one of the Food and Agriculture Organization’s most important commodities for both consumption and trade (Benedictis et al., 2014). The data take the form of a non-negative continuous-valued network of nations where the edge variable is the amount of trade of bananas in thousands of U.S. Dollars between nation and nation in 2018. We only consider the top nations in terms of total trade volume, that is, their weighted degree. The network was constructed from the BACI database (Gaulier and Zignago, 2010), which is derived from the UN Comtrade database by the Centre d’Études Prospectives et d’Informations Internationales (CEPII).

Our goal is to quantify the effect of various dyadic covariates on the trade of bananas, while controlling for network effects. To develop an appropriate GLNEM, we start with a model for trade from economics known as the gravity model (Tinbergen, 1962; Anderson, 1979). In its simplest form, the gravity model states that the systematic component is

| (8) |

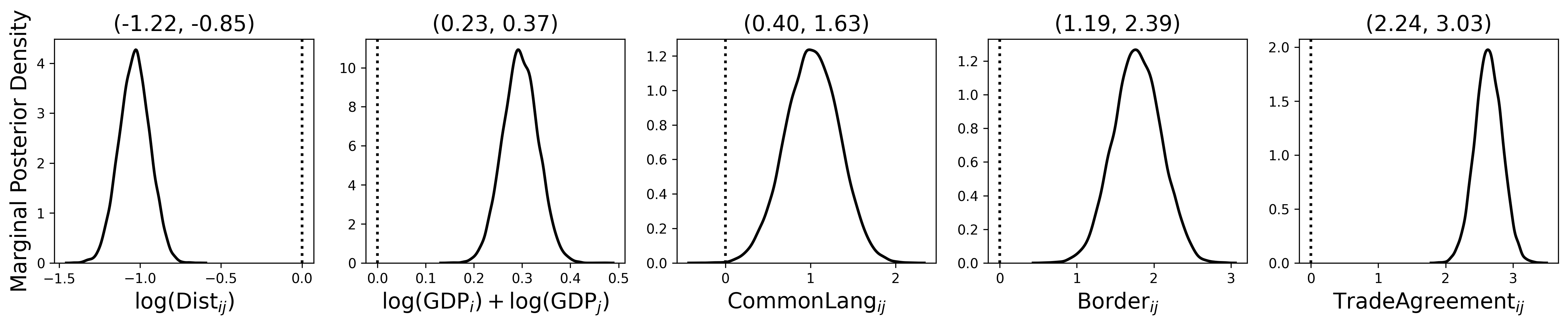

where is nation ’s GDP in thousands of U.S. Dollars, is the population weighted harmonic distance between nations and , and the ’s are any other relevant covariates. We included three additional binary indicator variables for shared language (), shared border (), and active trade agreement (). We obtained the dyadic covariates from the CEPII Gravity database (Conte et al., 2022).

For the random component, we propose to use the Tweedie distribution supported on the non-negative reals with power parameter , which has not appeared in the network latent space literature. This distribution has been recognized as a suitable distribution for trade data (Barabesi et al., 2016) because of its interpretation as a compound Poisson-gamma distribution and invariance to the edge variable’s unit of measurement. See Section F of the supplementary material for more details. We estimated a Tweedie GLNEM with a log link and by running the MCMC algorithm for 15,000 iterations after a burn-in of 7,500 iterations. The fraction of deviance explained (Hastie et al., 2015) of the model is 0.75, the AUC (area under the reciever operating characteristic curve) for classifying zero-valued edges is 0.853, and the fraction of variance explained for non-zero edges is 0.86. All values are close to one, which indicates a good fit to the trade network.

Figure 6 displays the posterior distributions of the covariate effects and their 95% credible intervals. According to the credible intervals, all covariates effects are significant. Furthermore, the sign of the coefficients for distance and GDP agree with those posited by economic theory, namely, that the amount of trade between nations decreases with distance and increases with GDP. The other coefficients indicate that sharing a language, a border, or entering into a trade agreement increases the volume of trade in bananas.

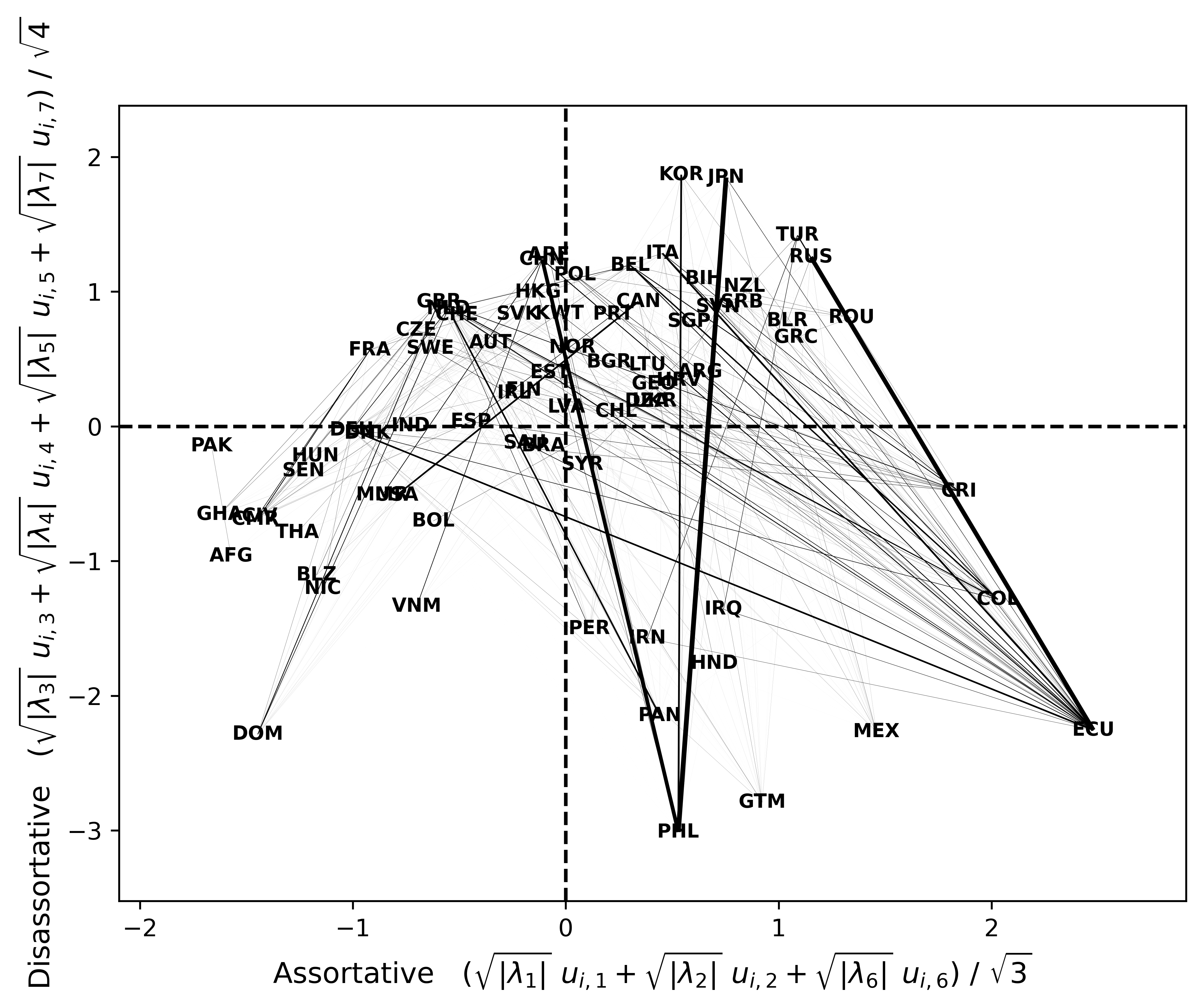

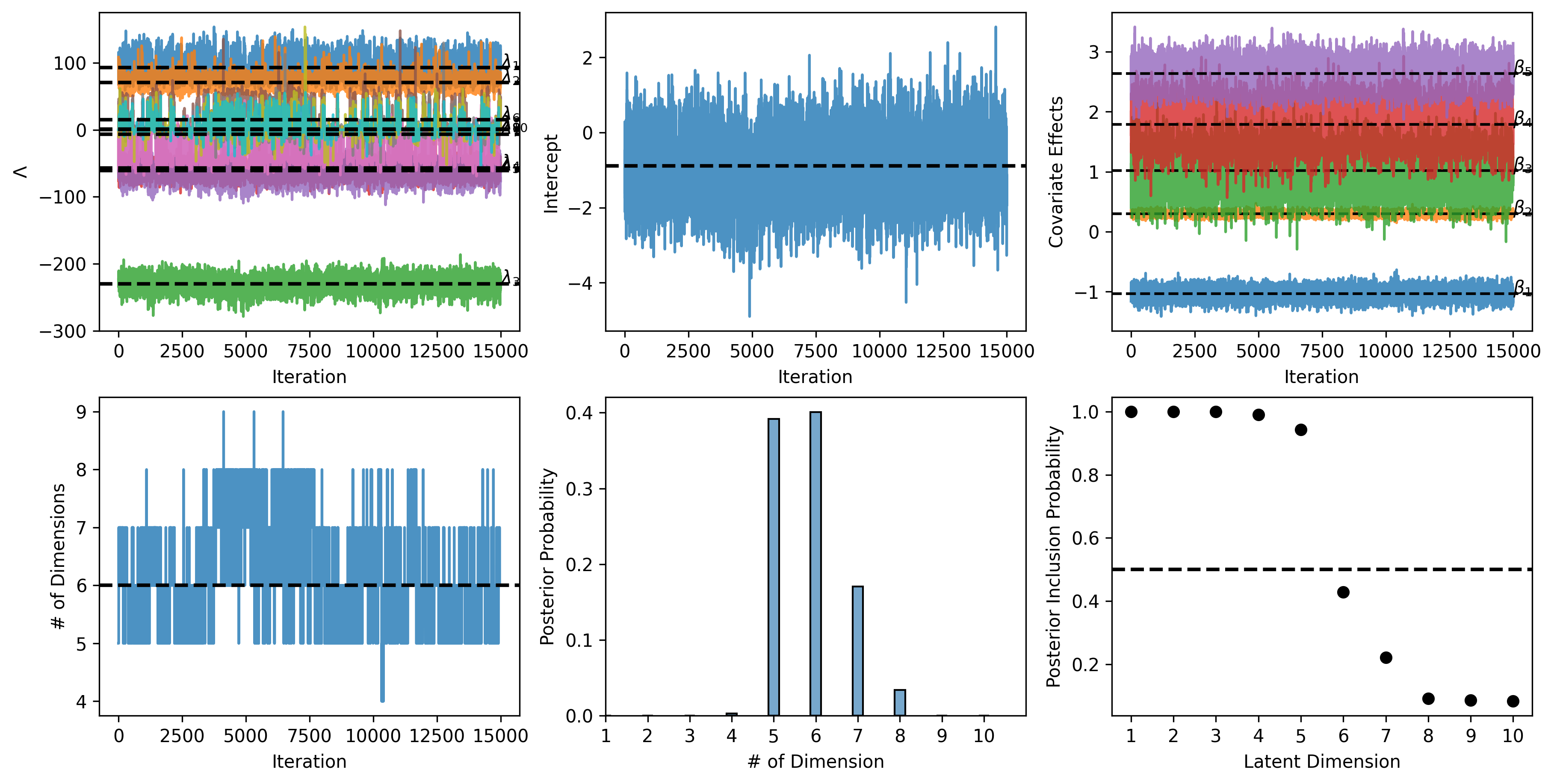

Next, we analyzed the residual network structure captured by the latent space. The dimension of the latent space was uncertain with the posterior consisting of a mixture of five (posterior probability 39%), six (posterior probability 40%), and seven (posterior probability 17%) dimensional latent spaces. Detailed summaries are in Section G of the supplement. Figure 7 shows a two-dimensional visualization of the seven-dimensional latent space obtained by separately combining the assortative and disassorative dimensions into single-feature summaries, that is, and . In this visualization, a nation tends to trade more with nations that they are closer to along the -axis (assortative) and further apart along the -axis (disassortative). The disassortative summary identifies a group of nations below the -axis that primary trade with nations above the -axis and do not trade with each other. These nations include the major global exporters of bananas such as Ecuador (ECU), the Philippines (PHL), and the Dominican Republic (DOM). The assortative summary encodes regional patterns in the trade relationships. For example, the Philippines primarily trade with nations in Asia such as Japan (JPN), South Korea (KOR), and China (CHN). In addition, the Dominican Republic focuses its trade with nations in the European Union such as the United Kingdom (GBR), the Netherlands (NLD), and Germany (DEU).

8 Discussion

In this article, we developed a theoretically supported Bayesian approach to dimension selection for a class of network models we called generalized linear network eigenmodels. This model class is very general and applicable to networks with edge variables drawn from any exponential-dispersion family and a systematic component using possibly non-canonical link functions. Furthermore, we introduced a new sum-to-zero identifiability constraint on the latent positions that allows one to interpret the effect of dyadic covariates as marginal effects. To enforce this constraint in a fully Bayesian way, we proposed a new prior for the latent positions based on the QR decomposition that has full support and easily integrates with gradient based sampling methods.

Next, we introduced a novel prior that addresses the important problem of automatically selecting the latent space dimension and assessing its uncertainty. We showed that this prior induces a stochastic ordering that counteracts certain identifiability issues in the model’s likelihood. In addition, we provided a posterior tail bound on the number of dimensions that reflects the true model’s underlying dimensionality. To the best of our knowledge, this is the first such theoretical result for Bayesian LSMs. Furthermore, this result is a first step toward establishing a posterior concentration rate for GLNEM estimation. Note that our theoretical results do not establish posterior dimension selection consistency, which would require a matching lower bound on the number of dimensions. Lastly, we developed a general Metropolis-within-Gibbs MCMC algorithm applicable to any GLNEM with SS-IBP priors, and showed the flexibility of our method by modeling three real-world networks from biology, ecology, and economics.

An interesting research direction is to extend our approach to directed networks. The typical eigenmodel for directed networks involves a decomposition based on the singular value decomposition: the latent space component, , becomes , where , , and the matrix of singular values has positive real-valued entries. The positivity of the singular values invalidates our use of a slab, so choosing an appropriate prior requires additional computational and theoretical care. Finally, while our approach to dimension selection is more computationally efficient than existing model selection criteria for Bayesian LSMs, our use of MCMC sampling is still computationally intensive for large networks. The exploration of an appropriate EM algorithm (Dempster et al., 1977) to estimate the posterior mode or a variational inference algorithm (Wainwright and Jordan, 2008) to approximate the posterior is an area of future research interest.

References

- Anderson (1979) Anderson, J. E. (1979), “A Theoretical Foundation for the Gravity Equation,” The American Economic Review, 69, 106–116.

- Barabesi et al. (2016) Barabesi, L., Cerasa, A., Perrotta, D., and Cerioli, A. (2016), “Modeling international trade data with the Tweedie distribution for anti-fraud and policy support,” European Journal of Operational Research, 248, 1031–1043.

- Battacharya and Dunson (2011) Battacharya, A. and Dunson, D. (2011), “Sparse Bayesian Infinite Factor Models,” Biometrika, 98, 291–306.

- Benedictis et al. (2014) Benedictis, L. D., Nenci, S., Santoni, G., Tajoli, L., and Vicarelli, C. (2014), “Network Analysis of World Trade using the BACI-CEPII Dataset,” Global Economy Journal, 14, 287–343.

- Bingham et al. (2019) Bingham, E., Chen, J. P., Jankowiak, M., Obermeyer, F., Pradhan, N., Karaletsos, T., Singh, R., Szerlip, P. A., Horsfall, P., and Goodman, N. D. (2019), “Pyro: Deep Universal Probabilistic Programming,” Journal of Machine Learning Research, 20, 1–6.

- Butland et al. (2005) Butland, G., Peregrín-Alvarez, J. M., Li, J., Yang, W., Yang, X., Candien, V., Starostine, A., Richards, D., Beattie, B., Krogan, N., Davey, M., Parkinson, J., Greenblatt, J., and Emili, A. (2005), “Interaction network containing conserved and essential protein complexes in Escherichia coli,” Nature, 433.

- Castillo and van der Vaart (2012) Castillo, I. and van der Vaart, A. (2012), “Needles and Straw in a Haystack: Posterior concentration for possible sparse sequences,” The Annals of Statistics, 4, 2069–2101.

- Chen and Lei (2018) Chen, K. and Lei, J. (2018), “Network Cross-Validation for Determining the Number of Communities in Network Data,” Journal of the American Statistical Association, 113, 241–251.

- Conte et al. (2022) Conte, M., Cotterlaz, P., and Mayer, T. (2022), “The CEPII Gravity Database,” Working Papers 2022-05, CEPII.

- Dempster et al. (1977) Dempster, A. P., Laird, N. M., and Rubin, D. B. (1977), “Maximum likelihood from incomplete data via the EM algorithm,” Journal of the Royal Statistical Society Series B, 39, 1–38.

- Donnet and Robin (2021) Donnet, S. and Robin, S. (2021), “Accelerating Bayesian Estimation for Network Poisson Models using Frequentist Variational Estimates,” Journal of the Royal Statistical Society Series C: Applied Statistics, 70, 858–885.

- Dunn and Smyth (2005) Dunn, P. K. and Smyth, G. K. (2005), “Series evaluation of Tweedie exponential dispersion model densities,” Statistics and Computing, 15, 267–280.

- Durante (2017) Durante, D. (2017), “A note on the multiplicative gamma process,” Statistics & Probability Letters, 122, 198–204.

- Durante and Dunson (2014) Durante, D. and Dunson, D. B. (2014), “Nonparametric Bayes Dynamic Modelling of Relational Data,” Biometrika, 101, 883–898.

- Gaulier and Zignago (2010) Gaulier, G. and Zignago, S. (2010), “BACI: International Trade Database at the Product-Level. The 1994-2007 Version,” Working Papers 2010-23, CEPII.

- Goldenberg et al. (2010) Goldenberg, A., Zheng, A. X., Fienberg, S. E., and Airoldi, E. M. (2010), “A Survey of Statistical Network Models,” Foundations and Trends in Machine Learning, 2, 129–233.

- Graham (2017) Graham, B. S. (2017), “An Econometric Model of Network Formation with Degree Heterogeneity,” Econometrica, 85, 1033–1063.

- Griffiths and Ghahramani (2011) Griffiths, T. L. and Ghahramani, Z. (2011), “The Indian Buffet Process: An Introduction and Review,” Journal of Machine Learning Research, 12, 1185–1224.

- Guha and Rodriguez (2021) Guha, S. and Rodriguez, A. (2021), “Bayesian regression with undirected network predictors with an application to brain connectome data,” Journal of the American Statistical Association, 116, 581–593.

- Guhaniyogi and Rodriguez (2020) Guhaniyogi, R. and Rodriguez, A. (2020), “Joint modeling of longitudinal relational data and exogenous variables,” Bayesian Analysis, 15, 477–503.

- Handcock et al. (2007) Handcock, M. S., Raftery, A. E., and Tantrum, J. M. (2007), “Model-Based Clustering of Social Networks,” Journal of the Royal Statistical Society - Series A, 170, 301–354.

- Hastie et al. (2015) Hastie, T., Tibshirani, R., and Wainwright, M. (2015), Statistical Learning with Sparsity: The Lasso and Generalizations, New York: Chapman and Hall/CRC.

- Hoff (2021) Hoff, P. (2021), “Additive and Multiplicative Effects Network Models,” Statistical Science, 36, 34–50.

- Hoff (2008) Hoff, P. D. (2008), “Modeling homophily and stochastic equivalence in symmetric relational data,” in Advances in Neural Information Processing Systems, pp. 657–664.

- Hoff (2009) — (2009), “Simulation of the Matrix Bingham-von Mises-Fisher Distribution, With Applications to Multivariate and Relational Data,” Journal of Computational and Graphical Statistics, 18, 438–456.

- Hoff et al. (2002) Hoff, P. D., Raftery, A. E., and Handcock, M. S. (2002), “Latent Space Approaches to Social Network Analysis,” Journal of the American Statistical Association, 97, 1090–1098.

- Hoffman and Gelman (2014) Hoffman, M. D. and Gelman, A. (2014), “The No-U-Turn Sampler: Adaptively Setting Path Length in Hamiltonian Monte Carlo,” Journal of Machine Learning Research, 15, 1593–1623.

- Huang et al. (2022) Huang, S., Sun, J., and Feng, Y. (2022), “Pairwise Covariates-Adjusted Block Model for Community Detection,” arXiv preprint arXiv:1807.03469v3.

- Hunter et al. (2008) Hunter, D. R., Goodreau, S. M., and Handcock, M. S. (2008), “Goodness of Fit of Social Network Models,” Journal of the American Statistical Association, 103, 248–258.

- Ishwaran and Rao (2005) Ishwaran, H. and Rao, J. S. (2005), “Spike and slab variable selection: Frequentist and Bayesian strategies,” Annals of Statistics, 33, 730–773.

- Jauch et al. (2021) Jauch, M., Hoff, P. D., and Dunson, D. B. (2021), “Monte Carlo Simulation on the Stiefel Manifold via Polar Expansion,” Journal of Computational and Graphical Statistics, 0, 1–10.

- Jørgensen (1987) Jørgensen, B. (1987), “Exponential Dispersion Models,” Journal of the Royal Statistical Society, Series B, 49, 127–162.

- Josling and Taylor (2003) Josling, T. and Taylor, T. (2003), Banana Wars: The Anatomy of a Trade Dispute, CABI Publishing.

- Kolaczyk (2017) Kolaczyk, E. D. (2017), Statistical Analysis of Network Data, Springer.

- Krivitsky and Handcock (2008) Krivitsky, P. N. and Handcock, M. S. (2008), “Fitting Latent Cluster Models for Networks with latentnet,” Journal of Statistical Software, 24, 1–23.

- Kuhn (1955) Kuhn, H. W. (1955), “The Hungarian method for the assignment problem,” Naval Research Logistics Quarterly, 2, 83–97.

- Li et al. (2020) Li, L., Levina, E., and Zhu, J. (2020), “Network cross-validation by edge sampling,” Biometrika, 107, 257–276.

- Ma et al. (2020) Ma, Z., Ma, Z., and Yuan, H. (2020), “Universal Latent Space Model Fitting for Large Networks with Edge Covariates,” Journal of Machine Learning Research, 21, 1–67.

- Mariadassou et al. (2010) Mariadassou, M., Robin, S., and corinne Vacher (2010), “Uncovering Latent Structure in Valued Graphs: A Variational Approach,” The Annals of Applied Statistics, 4, 715–742.

- Minhas et al. (2018) Minhas, S., Hoff, P. D., and Ward, M. D. (2018), “Inferential Approaches for Network Analysis: AMEN for Latent Factor Models,” Political Analysis, 27, 208–222.

- Neal (2011) Neal, R. M. (2011), “MCMC using Hamiltonian Dynamics,” in Handbook of Markov chain Monte Carlo, eds. Brooks, S., Gelman, A., Jones, G. I., and Meng, X.-L., Boca Raton, FL: CRC Press, chap. 5, pp. 113–162.

- Papaspiliopoulos et al. (2007) Papaspiliopoulos, O., Roberts, G. O., and Sköld, M. (2007), “A General Framework for the Parametrization of Hierarchical Models,” Statistical Science, 22, 59–73.

- Park and Casella (2008) Park, T. and Casella, G. (2008), “The Bayesian Lasso,” Journal of the American Statistical Association, 103, 681–686.

- Phan et al. (2019) Phan, D., Pradhan, N., and Jankowiak, M. (2019), “Composable Effects for Flexible and Accelerated Probabilistic Programming in NumPyro,” arXiv preprint arXiv:1912.11554.

- Ročková and George (2016) Ročková, V. and George, E. I. (2016), “Fast Bayesian Factor Analysis via Automatic Rotations to Sparsity,” Journal of the American Statistical Association, 111, 1608–1622.

- Sewell and Chen (2016) Sewell, D. K. and Chen, Y. (2016), “Latent Space Models for Dynamic Networks with Weighted Edges,” Social Networks, 44, 105–116.

- Silva and Tenreyro (2006) Silva, J. M. C. S. and Tenreyro, S. (2006), “The Log of Gravity,” The Review of Economics and Statistics, 88, 641–658.

- Sosa and Buitrago (2021) Sosa, J. and Buitrago, L. (2021), “A Review of Latent Space Models for Social Networks,” Revista Colombiana de Estdística, 44, 171–200.

- Spiegelhalter et al. (2002) Spiegelhalter, D. J., Best, N. G., Carlin, B. P., and Linde, A. V. D. (2002), “Bayesian measures of model complexity and fit,” Journal of the Royal statistical Society Series B, 64, 583–639.

- Stein and Leng (2022) Stein, S. and Leng, C. (2022), “A Sparse Beta Regression Model for Network Analysis,” arXiv preprint arXiv:2010.13604v2.

- Tinbergen (1962) Tinbergen, J. (1962), Shaping the World Economy - Suggestions for an International Economic Policy, New York: Twentieth Century Fund.

- Vacher et al. (2008) Vacher, C., Piou, D., and Desprez-Loustau, M.-L. (2008), “Architecture of an Antagonistic Tree/Fungus Network: The Asymmetric Influence of Past Evolutionary History,” PLOS ONE, 3, e1740.

- Wainwright and Jordan (2008) Wainwright, M. J. and Jordan, M. I. (2008), “Graphical Models, Exponential Families, and Variational Inference,” Foundations and Trends in Machine Learning, 1, 1–305.

- Walter et al. (2012) Walter, S. F., Lehmann, L., and Lamour, R. (2012), “On evaluating higher-order derivatives of the QR decomposition of tall matrices with full column rank in forward and reverse mode algorithmic differentiation,” Optimization Methods & Software, 27, 391–403.

- Ward et al. (2013) Ward, M. D., Ahlquist, J. S., and Rozenas, A. (2013), “Gravity’s Rainbow: A dynamic latent space model for the world trade network,” Network Science, 1, 95–118.

- Watanabe (2010) Watanabe, S. (2010), “Asymptotic Equivalence of Bayes Cross Validation and Widely Applicable Information Criterion in Singular Learning Theory,” Journal of Machine Learning Research, 11, 867–897.

- Wu et al. (2017) Wu, Y.-J., Levina, E., and Zhu, J. (2017), “Generalized linear models with low rank effects for network data,” arXiv preprint arXiv:1705.06772v1.

- Yan et al. (2019) Yan, T., Jiang, G., Fienberg, S. E., and Leng, C. (2019), “Statistical Inference in a Directed Network Model with Covariates,” Journal of the American Statistical Association, 114, 857–868.

Supplementary Material for

“A Spike-and-Slab Prior for Dimension Selection in Generalized Linear Network Eigenmodels”

Joshua Daniel Loyal and Yuguo Chen

Appendix A Proofs of Main Results

This section contains proofs of the various results found in the main text. Section A.1 contains proofs of the various propositions concerning the identifiability of GLNEMs and the proposed SS-IBP prior. Section A.2 contains proofs of the tail-bound of the SS-IBP prior and the GLNEM’s dimension under the posterior. Lastly, Section A.3 contains auxiliary lemmas necessary to prove the results in the previous two sections.

We use the following notation throughout this section. For two densities and , we let and denote the Kullback-Leibler (KL) divergence and second moment of the KL ball, respectively. For two positive sequences and , we write to denote . If , we write . We use to denote that for sufficiently large , there exists a constant independent of such that . For a vector , we let denote the , , and norm, respectively. For a matrix , we denote the Frobenius norm as . Last, for two real numbers , and .

A.1 Proofs of Propositions 1, 2, and 3

Proof of Proposition 1.

The condition that two probability distributions under two different parameterizations coincide implies that their moments must also coincide. This implies that the adjacency matrix’s expected value is identifiable. Furthermore, the condition that the link function is strictly increasing, thus invertible, implies that

| (9) |

Now, note that

| (10) |

Similarly, . Multiplying both sides of Equation (9) on the right by , applying Equation (10), and rearranging, we have

Next, multiplying both sides of the previous expression on the left by , we have

Since is full rank, we must have . From the previous equality, the fact that follows immediately from Equation (9). ∎

Proof of Proposition 2.

The proof proceeds directly:

Since is decreasing in , the result follows. ∎

Proof of Proposition 3.

Before proving the result, we need to formally define the support of a probability measure and prove a general measure theoretic lemma.

Definition 1.

Let be a probability measure on a measurable space , where is a topological space and is the associated Borel -algebra. The support of , denoted by , is the set of all such that every open neighborhood of has non-zero probability.

Lemma 1.

Let and be measurable spaces where and are topological spaces and and are their associated Borel -algebras. Also, let be a probability measure on and be a continuous, surjective function. If , then , the push-forward measure on associated with defined as for all , has .

Proof.

First note that the continuity of implies that is -measurable, so the statements made above are well defined. Now pick an arbitrary . Note that for any open neighborhood of , because is surjective. In addition, since is a non-empty open set in , it is also an open neighborhood of some point in . Therefore, for any by the assumption that has full support on . Since was arbitrary, this proves that has full support on . ∎

We are now ready to prove Proposition 3. First, we show that the function defined by steps 2 and 3 in Section 5.1 is surjective. Pick an arbitrary . Let , then so that and . Therefore, , which proves is surjective. Furthermore, is differentiable with respect to and thus continuous. The result follows from Lemma 1 with , , and the Gaussian measure on (that is, the elements of are independently drawn from a distribution) which has full support. ∎

A.2 Proof of Theorem 1 and Theorem 2

Recall that we model the observed edge variables using a GLNEM. In particular, we assume the edge variables, , are independently drawn from an exponential dispersion family with densities of the form:

where

| (11) |

for a strictly increasing link function . We will refer to the right hand side of the above equation as . We will also write , so that .

In addition, we assume that the matrices are generated from model (2) with true parameters , where , , , and . Furthermore, let

| (12) |

and . Let and denote the probability and expectation under this true data generating process. Finally, we denote the exponential dispersion family density under this true data generating process as

Our proofs of Theorem 1 and Theorem 2 make use of the theory developed by \citetSupgoshal2007 and \citetSupjeong2021 to demonstrate that the posterior concentrates around low-dimensional models for GLNEMs. Furthermore, we synthesize recent theoretical results for sparse Gaussian factor models \citepSuprockova2016, ohn2021 to derive our result on the prior’s ability to concentrate on low-dimensional models and derive our posterior concentration rates.

Proof of Theorem 1.

Since the inequality follows trivially when , we assume . Define the random variable . We bound as follows:

where . Conditioned on , is the sum of independent Bernoulli random variables with success probabilities

with the property by construction. In addition, on the event , we have , where we used the fact that for . As such, we can apply Lemma 4:

| (13) | ||||

where we used the fact that for any in the fifth line.

Now we bound , where with . Since , Gautschi’s inequality \citepSupgautschi1959 implies

The last line of the previous display used the fact that for , which follows from being monotonically decreasing on with . Then we have

where we used the fact that for and in the last line. Next, we note that by the assumption that and . It follows that the first term in the last line of the previous display is bounded above by 1, so that

| (14) |

Before proving Theorem 2 we need the following Lemma.

Lemma 2.

Suppose that the conditions of Theorem 2 hold. Then , where the set is

for

and some constant that only depends on .

Proof.

Denote the KL-neighborhood for the model parameters by

By Lemma 10 of \citetSupgoshal2007, we have for any ,

Therefore, it suffices to show that the prior probability for some constant . By Taylor expanding and , Lemma 1 of \citetSupjeong2021 established that

First, we show that is uniformly bounded above by a constant for all . Specifically, , since is continuous and strictly increasing and we used the parameter bounds in Assumptions A4 – A7. Coupled with Assumption A8, we have that is uniformly bounded above by a constant. Next, using the chain-rule, we have that , where we used the lower bound in Assumption A8 and Assumption A9. Therefore, both and can be bounded above by a constant multiple of for sufficiently large . Thus, we have for some constant and sufficiently large ,

where the last line follows from the triangle inequality and the fact that is independent of the remaining variables under our prior specification.

Let and denote the -th column of and , respectively. Furthermore, we define and such that and for and and for . In particular, this implies . Next, we have

Combining this with the previous inequality and use Assumptions A4 and A7, we have

| (15) |

where we used the fact that and are independent under the prior. Now we bound each term on the right hand side of (15) from below.

We start with the last term

| (16) |

We assert that . Indeed,

Therefore, the probability on the right hand side of (16) equals one for sufficiently large by Assumption A3.

Next, we apply Lemma 3 to bound the second term in (15) from below. Note that we satisfy the condition that for sufficiently large by Assumption A3, so the lemma implies that

for some constants and that depends on . In the third line of the previous display, we used the fact that for sufficiently large because . Also, we used Condition C2 in the last line of the previous display.

Lastly, we provide a lower bound for the first term in (15). First, we have that for some constant and sufficiently large. Thus,

For simplicity, let . Since the prior density on is bounded away from zero in a neighborhood of for , we have

where and is the lower bound on the Gaussian density in the neighborhood of . Combining this result with the previous expression, we have that there is a constant such that for large enough ,

for some constants and , where we used Condition C1 on the second to last line.

Combining the previous three bounds for the probabilities in (15) with gives the desired bound on . The result follows with . ∎

Proof of Theorem 2.

As in \citetSupjeong2021, we write the posterior as

| (17) |

where , , and denote the prior distributions for , and , respectively. Now, we introduce an event with large probability under the true data generating process. In particular, let , where is the rate in Lemma 2. If we decompose the probability in Equation (17) into the sum of two complementary conditional probabilities (conditioning on and its complement ), we can write:

On the event , is bounded below by . On the other hand, the expected value of the numerator can by bounded above by using Fubini’s theorem:

Therefore, we can use Lemma 2 to conclude that

In addition, for sufficiently large we have that , since by Condition C1, so we can apply Theorem 1 to bound the previous expression from above as

for large enough, which goes to zero as for .

∎

A.3 Auxiliary Lemmas

Lemma 3.

Let with , and . If has nonzero support on the first entries with , i.e., for and for , then for any ,

for some positive constant that only depends on . Moreover, if for some , , and , we have

for some positive constant that depends only on .

Proof.

Conditioned on , it follows from Lemma 6 that

where in the last line we used . Focusing on the terms involving , we have

so that

due to the independence of and the fact that are identically distributed. Since , , and , it follows that

for some depending only on , where the second inequality used the fact that for . Similarly we have

where the second line used the fact that . Combining these results, we recover the desired bound:

where is a positive constant that only depends on .

For the second assertion, note that implies

which completes the proof. ∎

Lemma 4.

Let be independent Bernoulli random variables with for , such that . Let and , then

for .

Proof.

The proof follows the derivation of a similar Chernoff bound found in \citetSuphagerup1990. For , we have that

where the last line follows from the ordering of the . For , this become

Note that

so that

Noting that gives the desired bound. ∎

Lemma 5.

Assume is distributed as for . Then for any and any ,

Proof.

Using the change-of-variables , we get

where are iid exponential random variables with scale . Recall that the sum of iid exponential random variables with scale follows a gamma distribution with shape and scale . Thus, we have

The fact that completes the proof. ∎

Lemma 6.

Assume is distributed as

for with for . Assume has nonzero support on the first entries, i.e., for and for . Then for any ,

Proof.

We start with the inequality

Note that . Also,

where denotes the probability measure under a density. Applying Lemma 5 completes the proof. ∎

Appendix B Full Conditional Distributions

In this section, we present the logarithm of the full conditional distribution used in the Hamiltonian Monte Carlo algorithm presented in Section 5.3 of the main text. First, we outline the change-of-variable transformations that we applied to the scalar parameters with a constrained domain. We applied a log-transformation to and a logistic transform to for . In particular, denote the unconstrained variables after the transformation as

Note that we correct these transformations with Jacobian adjustments to the full conditional distribution. The logarithm of up to an additive constant is

| (18) |

where

The term involving the logarithm of the Jacobian determinant is

where is the logistic function.

Appendix C MCMC Initialization and Post-Processing

This section provides additional information about the initialization of the MCMC algorithm proposed in Section 5 of the main text and the post-processing of its output.

C.1 Parameter Initialization

We can greatly reduce the number of iterations required to reach convergence by choosing good initial values for the model parameters. We initialize the parameters with the last sample from a short MCMC chain (500 iterations) targeting a model without dimension selection, that is, we repeat step one of Algorithm 1 for 500 iterations with for . We remove the dimension selection indicators to allow the sampler to initially freely explore the unconstrained parameter space before applying shrinkage. The initial parameters of this short chain are drawn randomly according to NumPyro’s recommended random initialization scheme, which draws the unconstrained variables uniformly from the interval \citepSupphan2019.

C.2 Post-Processing to Account for Posterior Invariances

Although our use of an prior places soft identifiability constraints on the parameters, the posterior remains invariant to signed-permutation of ’s columns, i.e., where and is a permutation matrix on elements. This can lead to inflated variance estimates without proper post-processing. As such, we post-process the results by matching each posterior draw to some reference . For convenience, we choose to be the maximum a posteriori (MAP) estimator.

Similar to Procrustes matching commonly employed in the latent space literature, which minimizes the Frobenius norm over rotation matrices, we solve

| (19) |

where is the set of permutation matrices on elements. We recognize the second expression as a linear assignment problem \citepSupgower2004 with a cost matrix with elements

where and are the -th and -th columns of and , respectively. Therefore, the solution to (19) can be efficiently found in time with algorithms such as the Hungarian method \citepSupkuhn1955. In summary, for each posterior draw, we solve the above linear assignment problem to obtain and set . Note that we also apply the permutation matrix to the diagonal elements of .

C.3 A Point Estimator for

Because the posterior mean of may not lie on the Stiefel manifold, it does not provide a meaningful point estimator for . To define a point estimator that lies on the Stiefel manifold, we take a Bayesian decision theoretic approach and minimize the following constrained Frobenius norm under the posterior:

If we view the Stiefel manifold as an embedded manifold of -dimensional Euclidean space, then the solution is the posterior Fréchet mean of . The above expression is minimized by the orthogonal component of the polar decomposition of \citepSupgower2004, i.e., where is the singular value decomposition (SVD) of .

Appendix D Definitions of Competing Model Selection Criteria