Stochastic Approximation MCMC, Online Inference, and Applications in Optimization of Queueing Systems

Abstract

Stochastic approximation Markov Chain Monte Carlo (SAMCMC) algorithms are a class of online algorithms having wide-ranging applications, particularly within Markovian systems. In this work, we study the optimization of steady-state queueing systems via the general perspective of SAMCMC. Under a practical and verifiable assumption framework motivated by queueing systems, we establish a key characteristic of SAMCMC, namely the Lipschitz continuity of the solution of Poisson equations. This property helps us derive a finite-step convergence rate and a regret bound for SAMCMC’s final output. Leveraging this rate, we lay the foundation for a functional central limit theory (FCLT) pertaining to the partial-sum process of the SAMCMC trajectory. This FCLT, in turn, inspires an online inference approach designed to furnish consistent confidence intervals for the true solution and to quantify the uncertainties surrounding SAMCMC outputs. To validate our methodologies, we conduct extensive numerical experiments on the efficient application of SAMCMC and its inference techniques in the optimization of GI/GI/1 queues in steady-state conditions.

1 Introduction

We investigate stochastic approximation (SA) methods for optimizing the steady-state performance of queueing systems. SA is a potent and efficient method for handling streaming data, adapting to dynamic environments, and offering significant computational efficiency through its iterative and incremental update process (Borkar, 2009; Benveniste et al., 2012; Kushner and Yin, 2003). Leveraging these benefits, the application of SA to queueing systems has a long history in the literature (Fu, 1990; Chong and Ramadge, 1994; L’Ecuyer and Glynn, 1994; L’Ecuyer et al., 1994). Recently, it was proven efficient in online learning (Chen et al., 2023) and Nash equilibrium solving tasks (Ravner and Snitkovsky, 2023) for queueing systems. In general, the goal of SA is to solve the following integral equation

| (1) |

where is the model parameter of the queueing system, represents the system state, and denotes the invariant measure or stationary distribution corresponding to a probability measure and is the steady-state distribution of the queueing system with model parameter . The function is decided according to concrete applications, for example, in a revenue optimization problem, is the gradient of long-run revenue rate with respect to parameter (Chen et al., 2023), while in a Nash equilibrium solving problem, it is defined by some fixed-point equation (Ravner and Snitkovsky, 2023). The function can be interpreted as an estimator of and is designed using gradient simulation methods. It has an explicit expression in terms of and so that it is tractable from observation or simulation data on the system state.

A key challenge when applying SA to the queueing setting is that due to the transient behavior in queueing dynamics, data on the system state do not follow exactly the steady-state distribution . As a consequence, there is a transient bias in the estimator . To effectively control such transient bias, previous works rely on a certain kind of batch-data approach to estimating the function . For example, Chen et al. (2023) suggested using a pre-determined batch size of order to estimate at iteration , while Ravner and Snitkovsky (2023) explored the regenerative structure of the queueing process and used the data over a complete regenerative cycle to estimate . Using such batch data, on the one hand, could provide more straightforward theoretic bounds on the transient bias and convergence guarantee for the SA algorithm, but on the other hand, could probably slow down the convergence rate as more data are needed in each iteration. The first question we want to answer is whether such batch-data designs are necessary for SA in queueing systems.

Furthermore, in the majority of prior research concerning SA for queueing systems, the theoretical analysis has primarily focused on establishing asymptotic or finite-step upper bounds for the SA estimation error. This error is defined as the disparity between the SA outcome and the true value . These bounds are crucial components of convergence analysis, furnishing valuable convergence guarantees and, on occasion, providing engineering guidance on choosing algorithm hyper-parameters. Nevertheless, they are often derived under somewhat conservative worst-case scenarios, and therefore, may not consistently provide precise estimates. As a consequence, they fall short of assisting decision-makers in quantifying the true quality or level of uncertainty associated with SA algorithm outcomes when applied to specific queueing models. This leads us to our second research question: Is it feasible to quantitatively measure the uncertainty in SA algorithm outcomes without incurring excessive computational costs?

In this paper, we resort to a stochastic approximation Markov Chain Monte Carlo (SAMCMC) algorithm (Andrieu and Moulines, 2006; Liang, 2010), giving rise to affirmative answers to the above two questions. We shall specifically study SAMCMC in the context of joint pricing and capacity sizing for a GI/GI/1 model. We believe our approach is applicable to other queueing models and even general stochastic models satisfying similar probabilistic properties, which we summarized in Remark 5 in Section 4.1.

Corresponding to our answer to the first question, in each SAMCMC iteration, the decision parameter and system state evolve jointly according to the following recursion

| (2) |

where represents the one-step transition of the queueing system under parameter , is the projection operator into the domain , and is the step size.

The key feature of the SAMCMC method, distinguishing from the conventional SA algorithms in the previous works, is that is estimated from the one-step transition under parameter with the previous state . In this light, SAMCMC can nicely incorporate many application settings, especially in online decision-making for stochastic systems where the parameter is updated earlier before the system converges to the stationary distribution. However, at the same time, this will introduce transient bias and sequentially dependent noises to the estimators , and thus make the convergence analysis much more challenging. We answer the first question by establishing a finite-step convergence rate result on SAMCMC in terms of the step size . In particular, we show that SAMCMC is “optimal” in the sense that obtains the same convergence rate (in the number of iterations) as the standard SA algorithm with an unbiased estimator for when the underlying Markovian system has nice ergodicity and continuity properties. Based on the finite-step convergence rate guarantee, we are able to provide a upper bound on the cumulated regret when SAMCMC is applied in an online fashion.

To answer the second question, we propose an online inference method for SAMCMC that can output consistent confidence intervals of the optimal value in real time. With this online inference method, service providers could quantify the uncertainty of the online learning result. To the best of our knowledge, we are the first to study online statistical inference in the optimization of queueing systems. The asymptotic consistency of the online inference method is built on a novel functional central limit theorem (FCLT) of the averaging SAMCMC trajectory, which we believe is of independent research interest.

At the technological level, the key idea in our theoretic analysis is to connect the transient errors across different iterations utilizing the Poisson equation to obtain a finer error bound. This approach is inspired by Benveniste et al. (2012) and has recently been used by Atchadé et al. (2017); Karimi et al. (2019); Li and Wai (2022) in finite-step convergence analysis for other variants of the SAMCMC algorithm. In particular, we validate that the Poisson equations corresponding to the queueing processes satisfy the desired properties which are usually assumed granted in SA literature (Polyak and Juditsky, 1992; Liang, 2010; Li et al., 2023b), via a careful analysis of the underlying dynamics. From this perspective, our analysis is applicable to SAMCMC on general stochastic systems where the Poisson equations can be proved to have similar properties. To the best of our knowledge, although asymptotic convergence of SAMCMC was proved (Liang, 2010), there is no existing result on finite-time convergence rates of SAMCMC that are directly applicable to our specific application in queueing systems.

Supplementing our theoretical results, we evaluate the practical effectiveness of SAMCMC and our online inference methods by conducting comprehensive numerical experiments on a concrete application setting of online SGD for steady-state optimization of queueing systems. It illustrates better sample complexity and cumulated regret compared to the batch-data-based algorithms proposed in the previous work. We also test the performance of our inference method via the empirical coverage rate. The numerical results show that the empirical coverage rate is quite close to the required significance level under moderately large iteration numbers.

The remainder of this paper is organized as follows. In Section 2, we review the related literature. In Section 3, we describe the queueing model and revenue management problem along with the key assumptions on the underlying Markov dynamics of the queueing system, and then give the SAMCMC algorithm. In Section 4, we present some auxiliary results and the convergence results. The inference methods along with the FCLT results are given in Section 5. In Section 6, we report the numerical results of SAMCMC and the online inference method in a variety of queueing models. Finally, we conclude our work in Section 7.

2 Related Literature

2.1 SGD for Queueing Systems

Our work is motivated by SGD methods for steady-state optimization for queueing systems. Application of SGD to queueing systems can be traced back to Suri and Zazanis (1988) for M/M/1 queues. Later, Fu (1990) extended the method to the GI/GI/1 queue utilizing its regenerative structure. Convergence properties of the SGD method for GI/GI/1 queues were given in L’Ecuyer and Glynn (1994) with different gradient estimators including IPA(infinitesimal perturbation analysis), finite-difference, and likelihood-ratio estimators. L’Ecuyer et al. (1994) reported detailed numerical studies on M/M/1 queues. Recently, Chen et al. (2023) applied SGD to online learning and optimization for GI/GI/1 queues and established a finite-step convergence rate result. Ravner and Snitkovsky (2023) developed a novel SGD-based algorithm to solve the Nash equilibrium of queueing games. In the previous works, to effectively bound the transient bias of the gradient estimator, the SGD algorithms were designed to use a batch of queueing data for computing a single gradient estimator in each iteration. For example, in L’Ecuyer and Glynn (1994) and Chen et al. (2023), the batch size for the IPA gradient estimator was pre-determined and sent to infinity as the SGD iteration goes on, while in Fu (1990) and Ravner and Snitkovsky (2023), the batch size was random corresponding to the length of a regenerative cycle. In addition to queueing models, SGD with batch data was also applied to steady-state optimization for inventory models (Huh et al., 2009; Yuan et al., 2021; Zhang et al., 2020). Different from the previous works, the SAMCMC algorithm we propose in this paper does not use batch data, and as a consequence, our proof approach is also different from those in the previous works which were based on the batch-data algorithm design.

2.2 SAMCMC Algorithm

A general theoretical framework of the SAMCMC algorithm was studied in Liang (2010) which is motivated by applications in statistics such as maximum likelihood estimation (Moyeed and Baddeley, 1991; Gu and Kong, 1998; Gu and Zhu, 2001), general stochastic simulation (Liang et al., 2007; Atchadé and Liu, 2010), and Bayesian posterior inference (Ma et al., 2015; Nemeth and Fearnhead, 2021). In particular, Liang (2010) established the asymptotic convergence of SAMCMC iteration and showed the asymptotic normality of the trajectory averaging estimator. The SAMCMC algorithm we propose here in the queueing context is slightly different from that in Liang (2010) and is easier to implement. In addition, we provide an explicit on the finite-step convergence rate of SAMCMC in terms of model and algorithm hyperparameters, and a functional-level CLT for the sequence of trajectory averaging estimators, which were not discussed in previous works on SAMCMC.

Recently, many optimization studies have proposed variants of the SAMCMC algorithm to tackle the optimization problems where the data is sampled from a state-dependent Markov chain . Such an optimization method prevails in reinforcement learning. Atchadé et al. (2017) explored a proximal SA algorithm with stochastic gradients computed on batch data. Karimi et al. (2019) conducted an analysis of the plain SAMCMC algorithm without projection, albeit with the assumption of uniformly bounded stochastic update . Analyzing the same algorithm, Li and Wai (2022) relaxed this boundedness assumption but introduced a uniformly Lipschitz and convex condition on the gradient function (see Remark 4 for details).

Though, in these works, finite-time convergence guarantees are provided following the spirit of (Benveniste et al., 2012) (including ours), there are several distinctions between our work and theirs. First, their studies rely on either hard-to-verify or more restrictive assumptions regarding the gradient function. These assumptions are not directly applicable or generally suitable to the queuing system we considered. Second, we investigate a projected SAMCMC algorithm, which enhances the stability of the optimization process. Lastly, their primary focus is on establishing finite-time convergence guarantees, whereas our work goes further by providing a regret analysis—a facet absent in all of their works.

2.3 Online Inference for Stochastic Approximation

Most online inference methods are based on the averaged SA iterates (e.g., SGD (Chen et al., 2020) or its variants (Toulis and Airoldi, 2017; Liang and Su, 2019)) and assume i.i.d. data. Under i.i.d. data, a traditional inference method to establish asymptotic normality first and then estimate the asymptotic variance matrix so as to construct an asymptotically valid confidence intervals (Chen et al., 2020; Zhu et al., 2021). However, efficient online estimation for the asymptotic variance matrix in the presence of Markovian data remains open in general for SA algorithms. Other works considering i.i.d. data depend on either bootstrapping (Li et al., 2018; Fang et al., 2018) or structural independence (Su and Zhu, 2023) to provide randomness quantification. The approach we employ for quantifying randomness in our paper, based on the FCLT, finds its origins in the work of Lee et al. (2022a). This approach has been extended to various domains, including federated learning (Li et al., 2022), reinforcement learning (Li et al., 2023b), gradient-free optimization (Chen et al., 2021), and quantile regression (Lee et al., 2022b; Liu et al., 2022).

For Markovian data, Ramprasad et al. (2021) built an online bootstrap-based inference method for linear problems assuming the availability of multiple simulation oracles that can evaluate the stochastic gradient simultaneously at different parameters using shared random numbers. As a consequence, this approach is not applicable to settings where data are observed sequentially from real system dynamics. To waive such restriction on the simulation oracles, Li et al. (2023a) proposed a novel family of asymptotic pivotal statistics leveraging the longitudinal dependence between consecutive iterates instead, and developed an efficient online computation algorithm for those statistics. The online inference method we develop here is inspired by Li et al. (2023a) but in a more complicated setting. In particular, in Li et al. (2023a), the distribution of Markovian data is not affected by the varying parameter , while in our setting, the distributions of the data and parameter are intertwined through the queueing dynamics. As a consequence, the algorithm and theory developed in Li et al. (2023a) is not directly applicable.

3 SAMCMC for GI/GI/1 Queue

In Section 3.1, we specify the queueing model and revenue management problem. In Section 3.2, we give a detailed description of the SAMCMC algorithm in the queueing context, especially the joint evolution of control parameters and system state.

3.1 Model and Problem Specification

We consider a concrete application of the SAMCMC algorithm in steady-state optimization of GI/GI/1 queue. The problem itself has a long history in the literature and is of independent research interest, see, for example, Chen et al. (2023) and references therein. This optimization problem is motivated by revenue management in a service system modeled by a GI/GI/1 Queue. In this system, customer arrivals are distributed according to a renewal process with generally distributed interarrival times (the first ). Their service times are independent and identically distributed (i.i.d.) following a general distribution (the second ), and a single server provides service under the first-in-first-out (FIFO) discipline.

The decision problem for the service provider is to decide the service price and service rate jointly. The actual service and interarrival times are subject to pricing and service capacity decisions. In detail, the interarrival and service times are driven by two scaled random sequences and , where and are two independent i.i.d. sequences of random variables having unit means, i.e., . Each customer upon joining the queue is charged by the service provider a fee . The demand arrival rate (per time unit) depends on the service fee and is denoted as . Then, the interarrival times under price decision become . Similarly, the service times under service rate are . To maintain a service rate , the service provider continuously incurs a staffing cost at a rate of per time unit. The goal of the service provider is to determine the optimal service fee and service capacity in the feasible set , with the objective of maximizing the steady-state expected profit rate, or equivalently, to minimizing the cost rate:

| (3) |

where is the steady-state mean queue length measuring the congestion level of the service system. We impose the following assumptions on the demand and cost functions and inter-arrival and service distributions.

Assumption 1.

Demand rate, staffing cost, and uniform stability

-

The arrival rate is continuously differentiable and non-increasing in .

-

The staffing cost is continuously differentiable and non-decreasing in .

-

The lower bounds and satisfy that so that the system is uniformly stable for all feasible choices of the pair .

Assumption 2.

Light-tailed service and inter-arrival times

There exists a sufficiently small constant such that the moment-generating functions

In addition, there exist constants , and such that

| (4) |

where and are the cumulant generating functions of and .

Let be the optimal solution of Problem (3) and . Let denote the gradient of the objective function and denote the Euclidean norm. To ensure convergence of our gradient-based algorithm, we also inquire about a certain convexity condition on the objective function.

Assumption 3.

Convexity and smoothness

There exist finite positive constants and such that for all

-

is an inner point of which is uniformly bounded by , i.e., ;

-

;

-

.

3.2 SAMCMC Algorithm and System Dynamics

We now treat as in Eqn. (1). Before giving the SAMCMC algorithm, we first need to specify a proper gradient estimator for . By Little’s law, the steady-state expectation

Hence, to estimate , it suffices to estimate the partial derivatives and . Applying the infinitesimal perturbation analysis (IPA) approach, derivatives of steady-state mean waiting time can be estimated using the so-called observed busy period.

In detail, for each , the observed busy period is the age of the server’s busy time observed by customer upon arrival. If an arriving customer finds the server idle, both the waiting time and observed busy time corresponding to this customer are equal to 0. Under a fixed pair of control parameter , evolves jointly with the waiting time according to the following recursion:

| (5) |

where and is the indicator function.

It is known that under the stability condition , the process has a unique stationary distribution. We denote by and the steady-state waiting time and observed busy period corresponding to control parameter . Then, the derivative of is connected to as follows.

Lemma 1 follows from Lemma 5 of Chen et al. (2023). As a result, one can construct an unbiased estimator for the gradient using samples from the steady-state distribution of .

However, as the control parameters keep evolving in the optimization procedure, it is infeasible to sample exactly from the steady-state distribution and obtain an unbiased gradient estimator. Instead, SAMCMC uses transient samples to approximate the gradient estimator. Below, we give a detailed description of SAMCMC in the context of steady-state optimization of GI/GI/1 queue in Algorithm 1. Following the convention in SAMCMC literature, we use to denote the system state including the waiting time and observed busy period.

Remark 2.

Remark 3.

Given the concrete setting of GI/GI/1 model, we explicitly specify the dynamic of system state by recursions in Algorithm 1. Following the general framework of SAMCMC, one can also write where is the transition kernel of under control parameter . In the rest of the paper, we shall use both representations of the system dynamics alternatively.

We close this section by showing that the gradient estimator is continuous in both parameter and system state data .

Proposition 1 (Continuity of ).

For the GI/GI/1 system described above, then there is a positive universal constant such that for any and ,

4 Convergence Rate and Regret Analysis

In this section, our focus is on the convergence rate of Algorithm 1. Based on the convergence rate, we are able to provide a regret bound when Algorithm 1 is applied in an online fashion. The convergence rate is derived on the basis of the Lipschitz continuity of a Poisson equation.

4.1 Continuity with the Solution of the Poisson Equation

Before presenting our convergence results, we first introduce the notion of a Poisson equation and study its continuity property. Under the uniform stability condition in Assumption 1 and Assumption 2, it is known that, for all , the queueing process with transition kernel converges exponentially fast to the stationary distribution (Lemma 2 of Chen et al., 2023). As a result, for a function (satisfying certain regularity conditions), there exists a unique bivariate function that solves the Poisson equation with respect to :

where and . The following Lemma 2 shows that in the setting of queue, the solution to the Poisson equation is continuous with respect to parameter .

Lemma 2.

To characterize the transient errors of the gradient estimator used in Algorithm 1, for each pair of , we denote by the solution to the following Poisson equation with respect to ,

Intuitively, can be interpreted as the cumulated transient bias of , namely,

Here we use subscript instead of previous to emphasize that is generated from , a transition kernel with a given parameter . The function plays a key role in both the proofs of the convergence rate and FCLT result to bound the transient error.

Note that the difference bound given in Lemma 2 is for fixed system state , while in the optimization procedure of SAMCMC, the system state is random and dynamic. Therefore, we also need to control the variability of the system state over the optimization procedure. In the queueing setting, we are able to bound such variability by controlling the tail of the queueing process.

Lemma 3.

The proofs of the two lemmas are given in Appendix B.1. They lead to the following proposition including the most crucial technical conditions, especially on , in the convergence rate proof.

Proposition 2 (Continuity and bounded moment).

Suppose we utilize the SAMCMC method to determine the optimal fee-capacity pair for the GI/GI/1 system, and represents the data we gather during this process. Then we can establish that:

-

For any and , .

-

For any and , .

-

There exist so that for any ,

-

There exist such that for any ,

Remark 5.

Proposition 2 along with Proposition 1 and Assumption 3 are common assumptions used in stochastic approximation literature to deal with trajectory averaging estimators (Polyak and Juditsky, 1992; Liang, 2010; Li et al., 2023b). Heuristically speaking, because the change in has the same order of and thus is very small, the continuity conditions (a) and (b) indicate that the gradient estimator and its transition error in SAMCMC will behave similarly as in the batch-sample case where is fixed for a multiple number of system state transitions. Therefore, one could expect that will still be a good approximation of as in the batch-sample case and the consequent convergence follows as well. In this light, the proof approach used in our paper for queues could be applied to other Markov systems as long as all conditions in Propositions 1 and 2 and Assumption 3 can be verified.

The detailed proof of Proposition 2 is available in Appendix B.1.3. Before delving into the subsequent sections on convergence and regret analysis, it is important to highlight that the proof of Proposition 2 is a non-trivial endeavor. In fact, we have established several intriguing properties of the GI/GI/1 system (refer to Lemmas 2 and 3), the proofs of which are deferred to Appendices B.1.1 and B.1.2, respectively. These properties not only provide substantial support for the proof of Proposition 2, but also possess potential for independent exploration.

4.2 Finite-step Convergence Rate

Utilizing the continuity conditions presented in the previous section, we establish convergence rate on the distance between and for the SAMCMC algorithm if the step size sequence satisfies the following conditions.

Assumption 4.

Remark 6.

Our assumption on the step size sequence , while seemingly stringent at first glance, is actually quite lenient in practice. It is satisfied when one choose with , or with . Actually, such kind of assumptions on the step size are commonly used in stochastic optimization literature, see for example (Moulines and Bach, 2011; Chen et al., 2020; Li et al., 2023a).

Given the step size sequence satisfying Assumption 4, our first main result is the following explicit finite-step upper bound on , i.e. the expected distance between and the optimal .

Theorem 1.

Remark 7.

As a direct consequence, when with , Algorithm 1 could achieve a convergence rate of order for , which has the same order as standard stochastic approximation schemes with unbiased sampling data (Theorem 2.1 in Chapter 10 of Kushner and Yin (2003)). In this sense, SAMCMC can achieve the optimal convergence rate in the GI/GI/1 setting. Compared to the batch-data method proposed in Chen et al. (2023), SAMCMC obtains improved sample complexity as it uses fewer data samples in a single round of gradient estimation. Finally, we would again point out that Theorem 1 gives an explicit non-asymptotic convergence bound on the finite-step convergence rate of SAMCMC, whereas Liang (2010) only considered the asymptotic convergence of SAMCMC.

The main step in our proof of Theorem 1 is to decompose into a martingale term and other terms that can be expressed as the difference of continuous functions evaluated at consequent parameter and (we call them finite difference terms for short), which relies on the solution to Poisson equation introduced in Section 4.1 and its continuity property established in Proposition 2. The martingale term then vanishes after taking expectation, while these finite difference terms can be shown to be of order . Using conditions on in Assumption 4, we can effectively bound the summation of those finite difference terms and finally arrive at the finite-step bound presented in Theorem 1. The complete proof of Theorem 1, along with the explicit expression of the two constants and , are given by (31) and (34) in Appendix B.2.1, respectively.

4.3 Regret Analysis

Based on the convergence rate result, we now carry out a regret analysis to measure the actual revenue performance of SAMCMC. Following the literature on online learning for queues (Chen et al., 2023; Jia et al., 2022), we define the cumulated regret of SAMCMC in the first iterations as the expected difference between the actually cost and the optimal long-run cost under the optimal policy . Note that the queueing system operates in continuous time, so we need to map the discrete iterations back to the real timeline to evaluate the actual revenue performance. Before introducing the formal definition of regret, we first describe the real-time dynamic of the queuing system.

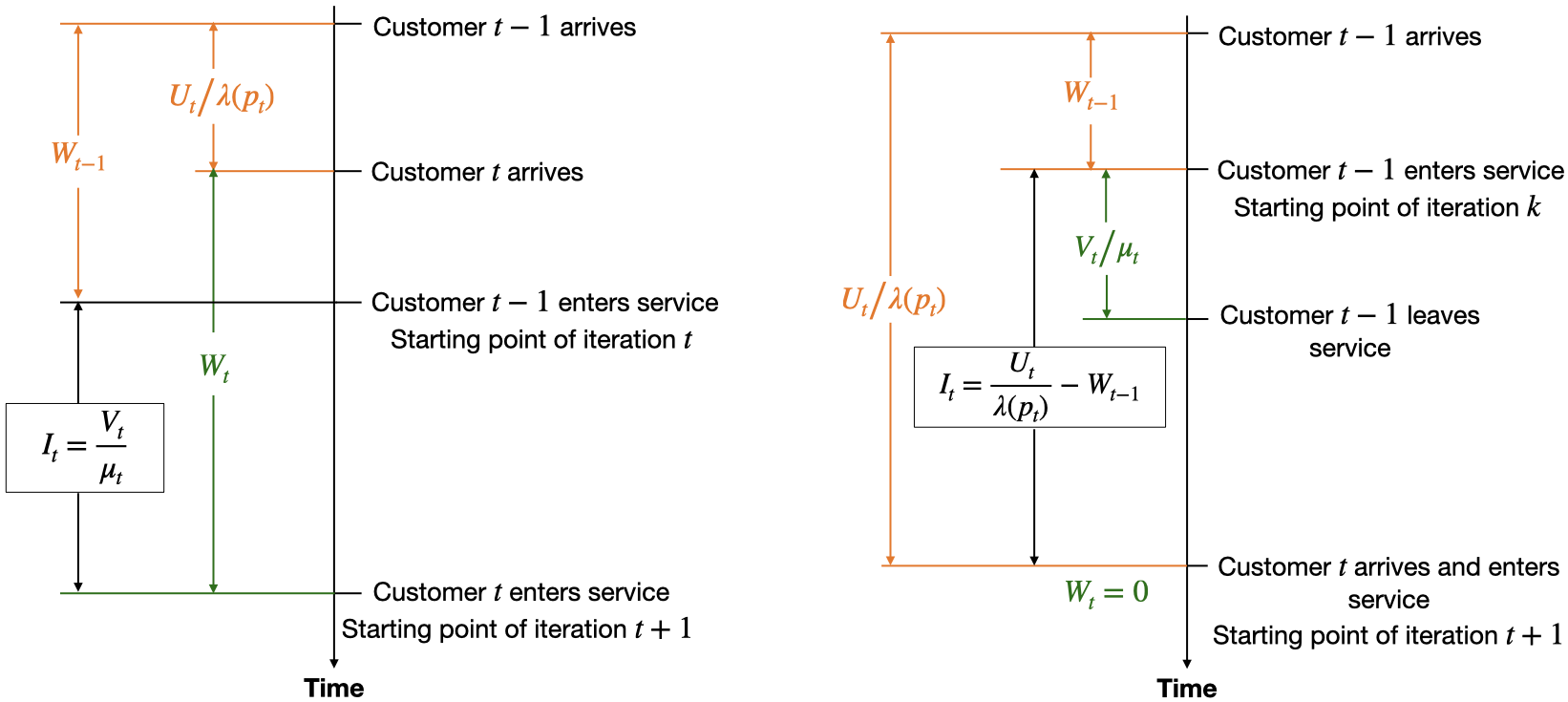

Figure 1 illustrates the dynamic of the queueing system at iteration . As the waiting times and observed busy periods are realized when customers enter service, we prescribe that each iteration starts when a customer enters the service and use to denote the time interval between the enter-service times of the consequent customer and . If the -th customer arrives before the -th customer leaves, then corresponds to the service time of customer , which equals to . If the -th customer arrives after the -th customer leaves, we then should take the idle time where no customer receives service into consideration and find that . In both cases, one can verify that

Then, the total time elapsed upon SAMCMC finishes iterations is and customer enters service then. As a result, the cumulated regret in iterations is

| (8) |

where is the service time of customer . For each , the term can be understood as the cost brought by customer to the system.

Similar to the regret analysis in (Chen et al., 2023), we decompose the regret into regret of nonstationarity and regret of suboptimality as follows

where is caused by the transient behavior of the queueing dynamic while is caused by the suboptimal choice of control parameters. Applying Theorem 1 that and Taylor’s expansion of around , one can check that, if ,

Next, we shall deal with the more challenging regret of nonstationary . The analysis approach for regret of nonstationary developed in Chen et al. (2023) highly depends on the batch-data structure of their algorithm. Roughly speaking, the key step in their analysis is to show that the last observed waiting time in batch is sufficiently close to , in expectation, when the batch size is large enough and keeps increasing. In our SAMCMC setting, the batch size is fixed to 1 and thus their analysis approach can not apply. Hopefully, similar to the proof of Lemma 2, by utilizing the continuity of the parameters with respect to the transition kernel, we are able to prove that, the mean difference between and is still sufficiently small even when the batch size is 1.

Lemma 4.

Remark 8.

Lemma 4 reflects a two-time-scale feature of the joint dynamics of under the SAMCMC algorithm. On the one hand, under Assumption 1, the queueing process converges exponentially fast to the stationary distribution for a fixed control parameter with the exponent uniformly bounded away from 0. On the other hand, the control parameter varies at a much smaller rate proportional to . As a consequence, one could expect that approximately follows the stationary distribution corresponding to in the spirit of the multiscale approximation of stochastic processes (Kurtz, 2005).

5 Online Statistical Inference

Based on the finite-step convergence rate result in the previous session, we are able to prove a functional central limit theorem for the averaging trajectory of SAMCMC in Section 5.1, which lays down the theoretic foundation for our inference method. In Section 5.2, we describe how to construct confidence intervals using the FCLT result. Finally, we present an efficient computation algorithm in Section 5.3 that produces confidence intervals efficiently from SAMCMC outputs in an online fashion.

5.1 Functional Central Limit Theorem

In order to establish the more general FCLT, additional regularity assumptions are introduced.

Assumption 5.

More regularity conditions for FCLT

We additionally assume that

-

(a)

There exists a positive definite matrix and constant such that

-

(b)

The step size satisfies both Assumption 4 and the following condition

(9)

Assumption 5 introduces two additional prerequisites. Condition (a) necessitates that the non-linear function demonstrates local linearity within the vicinity of the root . Essentially, this implies that the target gradient exhibits a linear behavior in close proximity to . Consequently, is differentiable at , with its derivative represented by the matrix . In other words, contains the curvature information of the target function at the root . Condition (b) places constraints on the decaying rate of the step size , thereby excluding the use of linearly scaled step sizes, such as , theoretically. In practice, a viable alternative is , where and . A straightforward verification confirms that this chosen step size satisfies both Assumption 4 and the relations given in Eqn. (9).

Before delving into the establishment of the FCLT for , it’s crucial to characterize another element: the limiting covariance matrix . Recall that the bi-variate function serves as the solution to the Poisson equation. To commence, we introduce a covariance matrix that employs this function, which is defined as follows:

Evidently, constitutes the matrix conditional covariance of , with the initiation point being , and a one-step transition conducted along the kernel . Consequently, this matrix depends not only on but also on . It encapsulates the discrepancy that the SAMCMC method may incur during the gradient estimation process . Based on existing assumptions, the following Proposition 3 tells us that the average of converges in probability towards a covariance matrix which is defined to be , whose proof is deferred to Appendix C.6.

Proposition 3 (Limiting Covariance Matrix).

Theorem 3.

With the same condition as in Proposition 3 we have that

within the topology which signifies the set of all càdlàg functions defined on equipped with the maximum norm . Here is the local linearity matrix defined in Assumption 5, is the limiting covariance matrix given in Proposition 3 and is a standard -dimension Brownian motion.

Theorem 3 shows both the cadlag constant function weakly converges to the rescaled Brownian motion . The scale is the nuisance parameter that involves both the local linearity coefficient and the covariance matrix .

Remark 9.

The proof of Theorem 3 follows the approach outlined in Li et al. (2023a). This proof method uses a so-called Martingale-residual-coboundary decomposition. By applying this approach, the centered gradient is partitioned into three distinct terms: a martingale term, a residual term, and a coboundary term. Leveraging the convergence rate established in Theorem 1, we can show that both the residual and coboundary terms exhibit higher-order convergence compared to the martingale term. This property facilitates the decomposition of the partial-sum process into two main components: a partial-sum process of martingale differences, and an additional higher-order reminder process. Classic results imply the former partial-sum process weakly converges to the scaled Brownian motion . The subsequent step involves establishing the convergence of the reminder process towards a zero process within the framework of the uniform topology. The detailed proof of this theorem can be found in Appendix C.1.

By invoking the continuous mapping theorem, we are able to derive Corollary 1. This corollary helps us to restore the asymptotic normality result documented in Liang (2010) simply by selecting as , resulting in Corollary 2.

Corollary 1.

Under the same condition in Theorem 3, for any continuous functional , it follows that as ,

Corollary 2.

Under the same condition in Theorem 3, setting ,

5.2 Construction of Confidence Intervals

Conventional wisdom in developing online inference methods entails estimating the asymptotic variance matrix, and plugging it into the asymptotic normality in Corollary 2 (Chen et al., 2020, 2021; Li et al., 2022). However, this endeavor is particularly formidable within our context, given its intricate connection to both the local linearity coefficient and the solution to the Poisson equation. The task of estimating this matrix remains an open challenge in the context of a SA procedure using Markovian data. On another note, even the estimation of and is attainable within our framework; the computation involving the matrix inversion and the multiplication , however, incurs a computational cost of up to , with the added need for memory to store intermediate outcomes. This conundrum leads us to explore the existence of an efficient online inference method that bypasses the need to estimate any matrix spanning between and while maintaining a computational expense of up to and a memory requirement of up to .

Fortunately, the FCLT offers a positive response to this query. Corollary 1 brings forth a pivotal insight: when exhibits scale-invariance - such that for any non-singular matrix and any cadlag process - the outcome is that

This implies that the distributional convergence of is towards a functional reliant on the standard Brownian motion, . Scrutinizing further, it’s apparent that represents a pivotal entity, solely entwined with collected data and the unknown root . Conversely, boasts a known distribution, rendering its quantiles computable through simulation. This dynamic facilitates the construction of asymptotic confidence intervals. Therefore, FCLT underpins the foundational rationale of our statistical inference approach. We make this point more precise in the following proposition.

Proposition 4.

Under the same condition in Theorem 3, given any unit vector and a continuous scale-invariant functional , it follows that when ,

where is the -level confidence set defined by

| (10) |

and is the critical value defined by

| (11) |

The feasibility of the aforementioned construction of confidence intervals hinges on the presence of an appropriate scale-invariant functional, denoted as . A typical choice in the literature is given in the following functional (Li et al., 2023a, b, 2022; Lee et al., 2022a, b)

| (12) |

One can show that this , as a one-dimensional functional, is not only scale-invariant so that for any non-negative but also symmetric in the sense that for any cadlag process . With this specific functional , this confidence interval (10) has a more concrete form as shown in the following corollary.

Corollary 3.

Under the same condition in Theorem 3, then as ,

| (13) |

where is the average of the first iterates and

is an approximation of the denominator .

Prior research has adopted two distinct strategies to compute the critical values for : stochastic simulation (Kiefer et al., 2000) and density approximation (Abadir and Paruolo, 1997). In our study, we employ the former approach and present our computed estimates in Table 1 for convenient reference.

Remark 10.

By the definition of , when for any , we have and then

which remains independent of the unknown root . This observation motivates us to use the rectangle rule to compute the integral , i.e.,

Numerical evidence in (Li et al., 2023a) confirms that this approximation exhibits high accuracy in practice and adequately delivers satisfactory performance.

As illustrated by the concrete example, the scale-invariant property is closely linked to the utilization of the entire trajectory iterates . This rationale underscores the necessity for a stronger FCLT outcome beyond the asymptotic normality of trajectory averages.

| -8.628 | -6.758 | -5.316 | -3.873 | 0.000 | 3.873 | 5.316 | 6.758 | 8.628 |

5.3 An Efficient Online Computation Algorithm

The remaining issue is how to compute the confidence interval (13) efficiently online. Actually, this work has already been done in previous works (Lee et al., 2022a; Li et al., 2022, 2023a). For completeness, we formally introduce this online computation algorithm, analyze its computation and memory cost, and present its extensions.

According to Corollary 3, we only need to identify an online incremental update for both and . On one hand, the moving average can be naturally computed online due to the relation . On the other hand, we note that , as the key component in , can be decomposed into the sum of three terms as follows

| (14) |

where we define the following notation for simplicity

Once is obtained, can be updated to using only computation for any . Indeed, it directly follows from the fact that

| (15a) | ||||

| (15b) | ||||

| (15c) | ||||

As a result, updating to requires only computations which happen in the evaluation of the inner product . Because we only need to maintain three one-dimensional sequences and the average , the memory cost is also , which scales linearly with the dimension .

We summarize this online computation algorithm in Algorithm 2.

Remark 11.

In a related study, Li et al. (2023a) introduced a family of scale-invariant functionals, expressed as , which encompasses the formulation in (12) as a special case. This framework provides a structured approach for different values of . For even values of , the denominator can be decomposed similarly to (5.3). Consequently, the computational complexity and memory requirements at each iteration remain at for online statistical inference. For the sake of simplicity and illustrative purposes, we focus on the case in (12).

6 Numerical Experiments

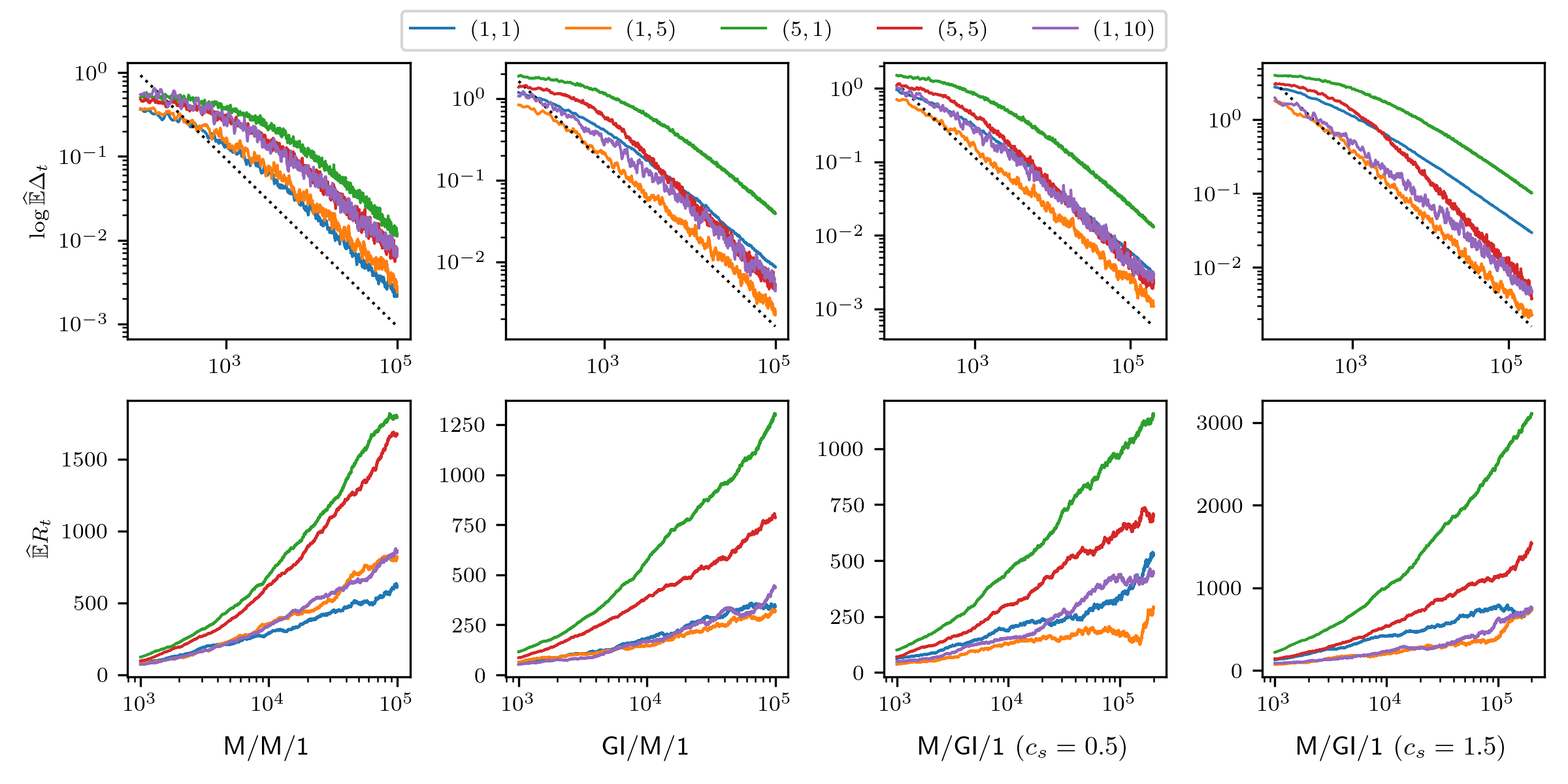

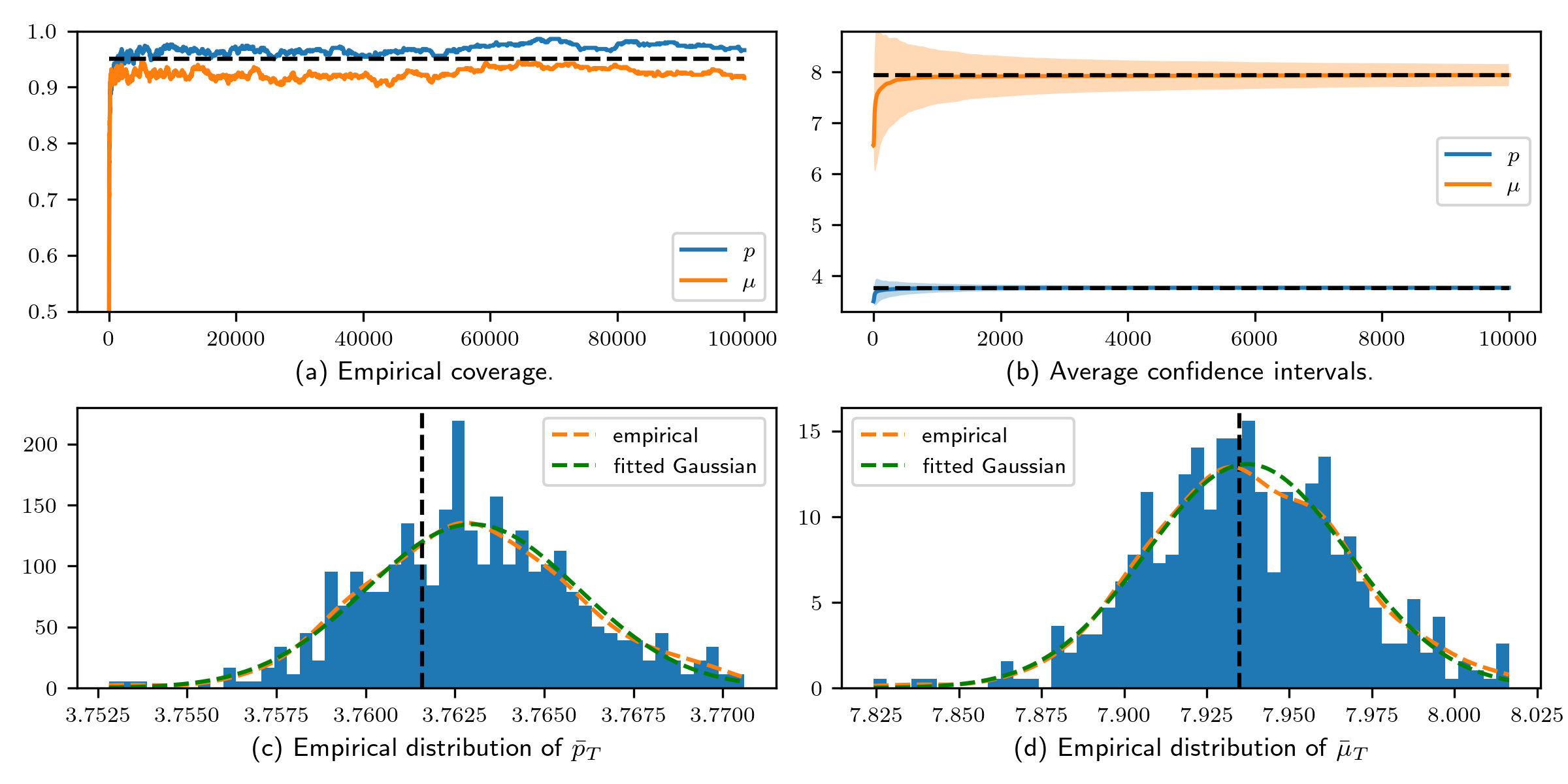

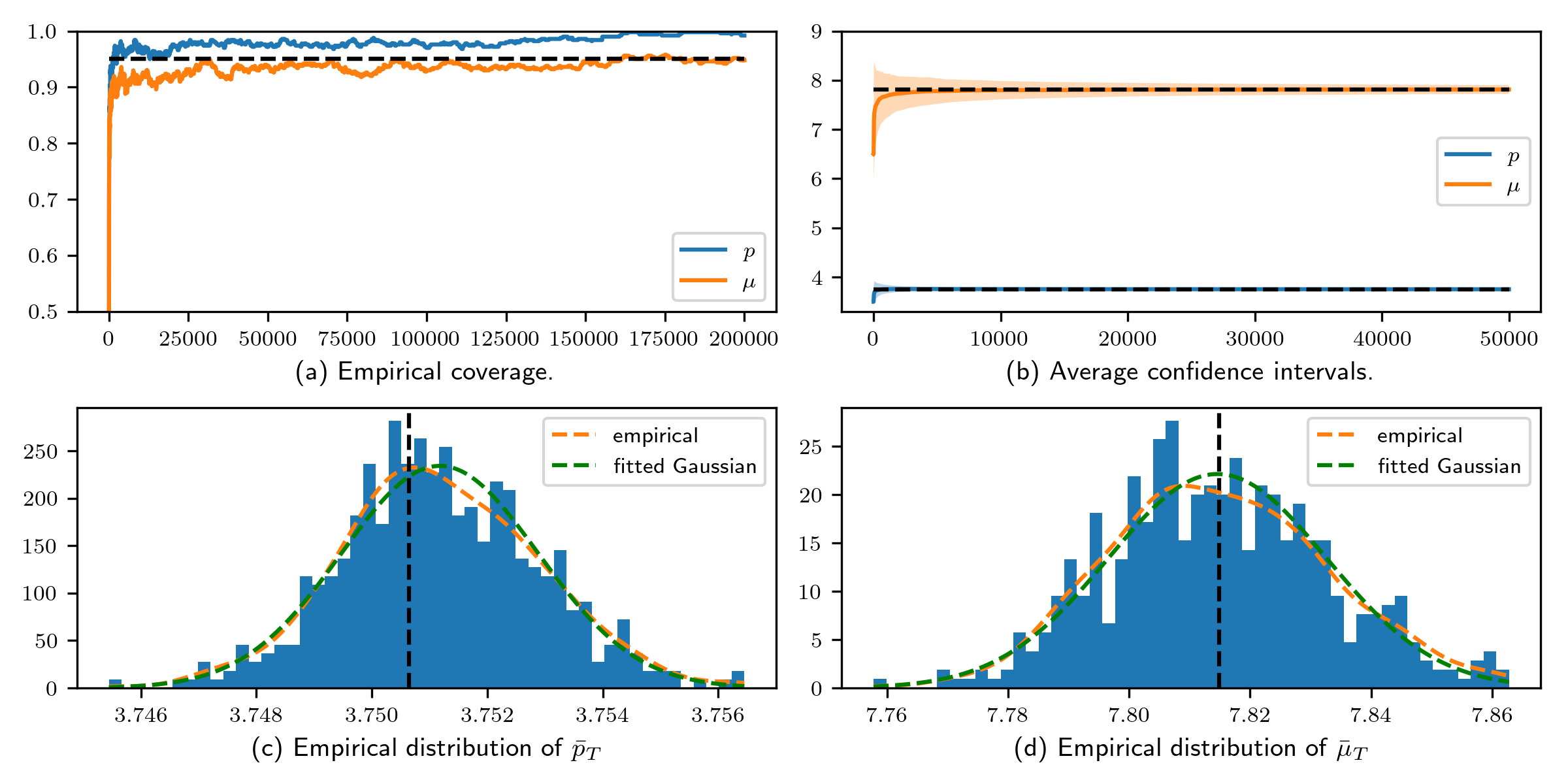

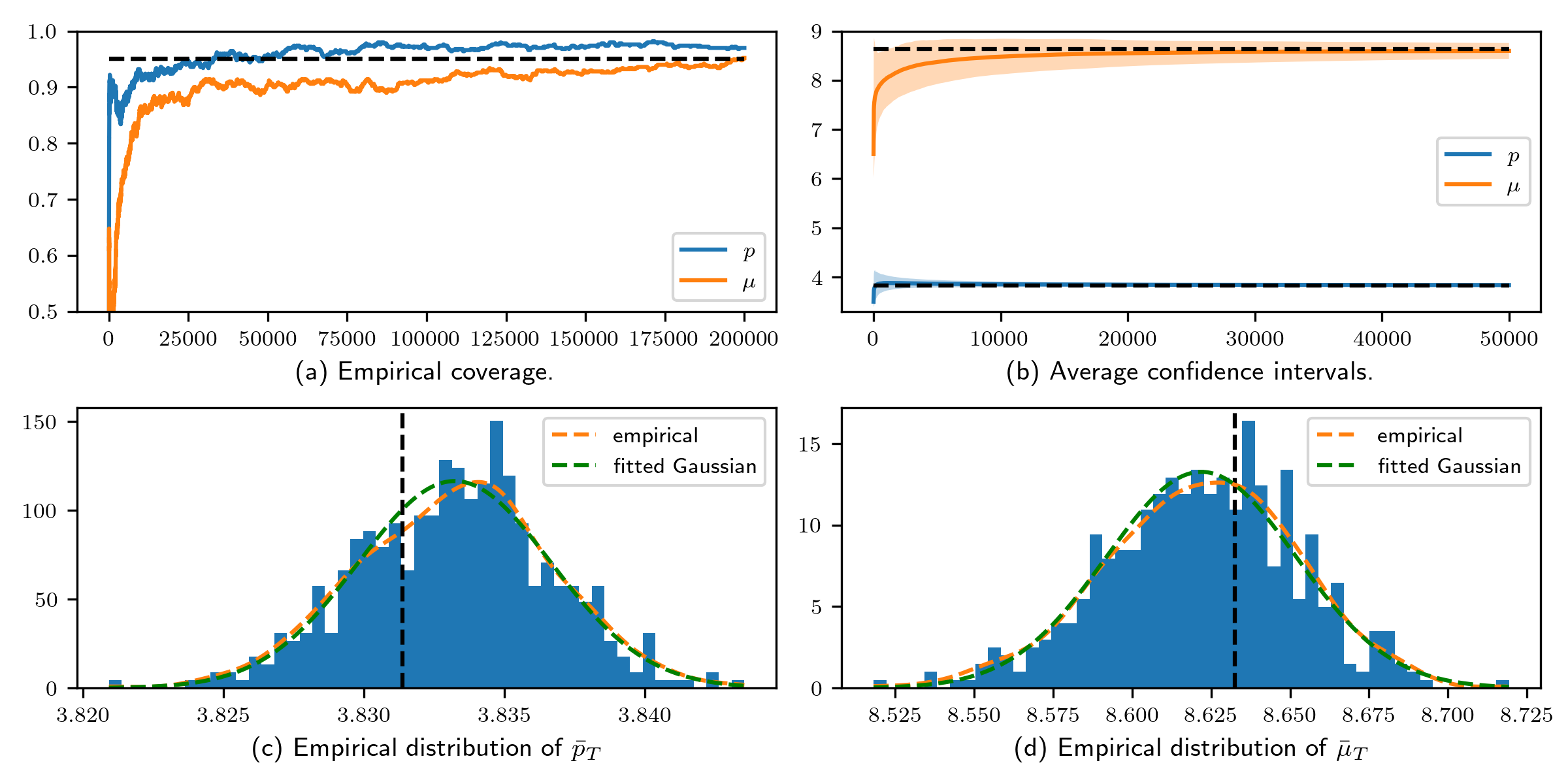

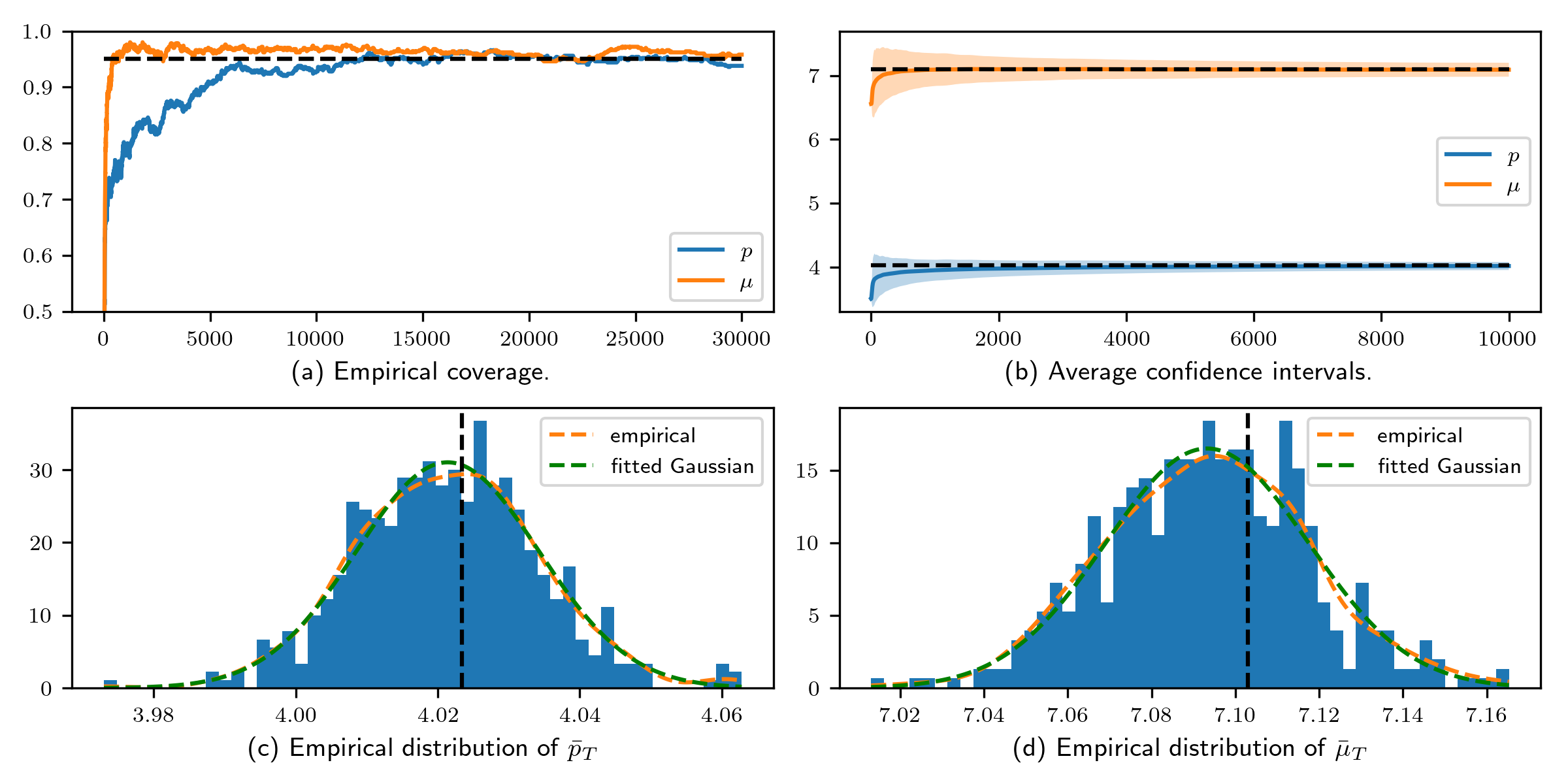

To test the actual performance of the SAMCMC algorithm and our online inference method, we conduct a series of numerical experiments on steady-state optimization of GI/GI/1 queue. In particular, to confirm the practical effectiveness of our online learning method, we conduct numerical experiments to visualize the algorithm convergence, and benchmark the outcomes with known exact optimal solutions, estimate the true regret, and compare it to the theoretical upper bounds. We also verify the asymptotic normality of SAMCMC and test the consistency of our online inference method in Section 6.4.

6.1 Experiment Setting

We implement SAMCMC on three GI/GI/1 models with different inter-arrival and service time distributions as considered in Chen et al. (2023). In all settings , we use a logistic demand function in the form of

| (16) |

where is interpreted as the market size. In the following experiments, we set , and the coefficient of holding cost in the objective function (3). Below, we specify the setting details of the three queueing models one by one.

M/M/1 Queue

The first example is the fundamental M/M/1 queue with Poisson arrivals and exponential service times. Following Chen et al. (2023), we consider a quadratic cost function for service rate

| (17) |

In this case, the objective function (3) has a closed-form expression as

from which the exact values of the optimal solutions and the corresponding objective value can be obtained via numerical methods. We set and , which results the optimal solution .

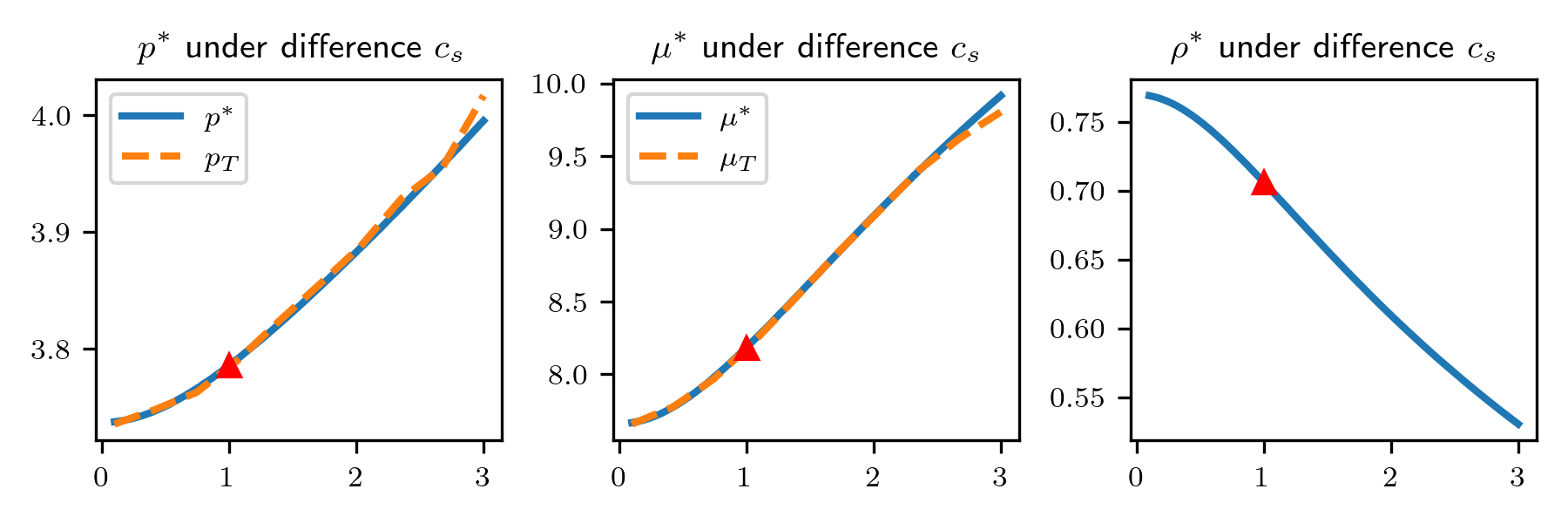

M/GI/1 Queue

The famous Pollaczek-Khinchine (PK) formula provides a closed-form expression for the steady-state average queue length the for M/GI/1 model:

| (18) |

where is the traffic intensity under the parameter and is the squared coefficient of variation (SCV) for the service time random variable .

To introduce an additional degree of flexibility for , we adopt the Erlang- distribution for the service-time distribution whose SCV equals . In the special case when , the Erlang-1 distribution is reduced to the Poisson distribution, and the corresponding M/GI/1 queue is reduced to an M/M/1 queue. For the M/GI/1 model, we consider a linear staffing cost function

| (19) |

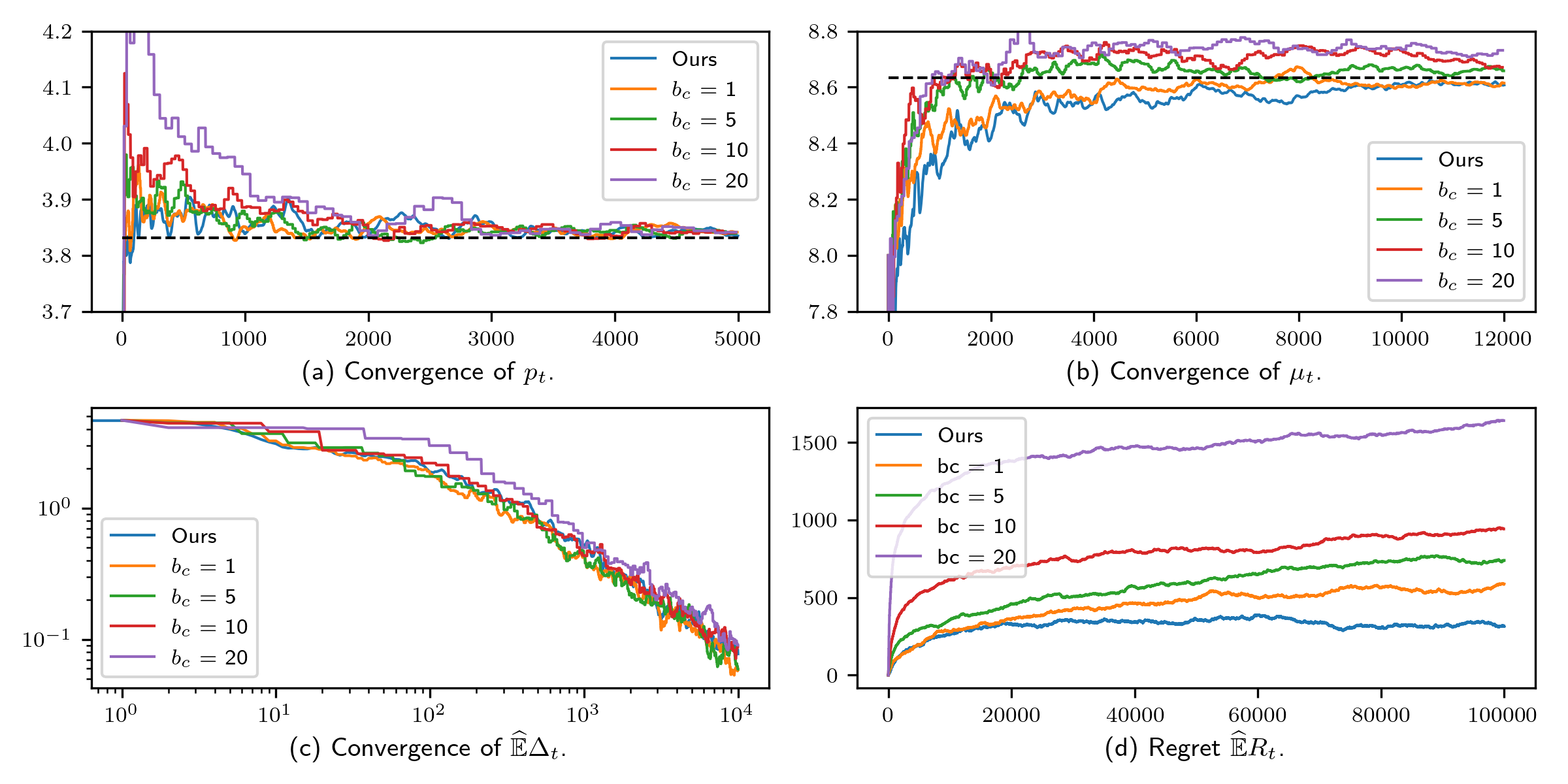

In our experiments, we fix and but vary to make range from to equidistantly, with a total of 200 different ’s. The optimal solutions and traffic intensity corresponding to different values of , together with the last-iterate performance of the SAMCMC algorithm, are reported in Figure 2. Noting that M/M/1 corresponds to the case where , we also examine two specific scenarios where for further case study.

GI/M/1 Queue

For the queueing model with general inter-arrival time distributions, we consider an /M/1 queue – a system characterized by Erlang-2 interarrival times and exponential service times. The main purpose for us to use this setting is that efficient numerical methods are available for computing the true value of the optimal and objective function, employing the matrix geometric approach.

In this experiment, we use linear staffing cost with and , which yields the optimal decision .

Benchmark algorithm

We select a simplified version of GOLiQ111For a fair comparison, we ignore the leftovers from previous cycles in our implementation of GOLiQ. proposed in Chen et al. (2023) as the benchmark algorithm as it provides explicit guidance on the choice of batch size and other algorithm parameters. GOLiQ differs from SAMCMC in estimating the gradient using an increasing number (or batch size) of samples collected under the current policy parameterized by . Following the guidance in Chen et al. (2023), we use different choices of batch size in the form of for the -th estimate of the gradient with to test the effect of batch sizes. Our SAMCMC algorithm corresponds to the case when .

We then implement SAMCMC and the benchmark GOLiQ on all three queuing settings and run 200 rounds of simulation. In all experiments, the initial value . The step size is fixed with for the update of and for the update of . Next, we compare their performance in terms of sample complexity and cumulated regret and test the robustness of SAMCMC with respect to the choice of step size .

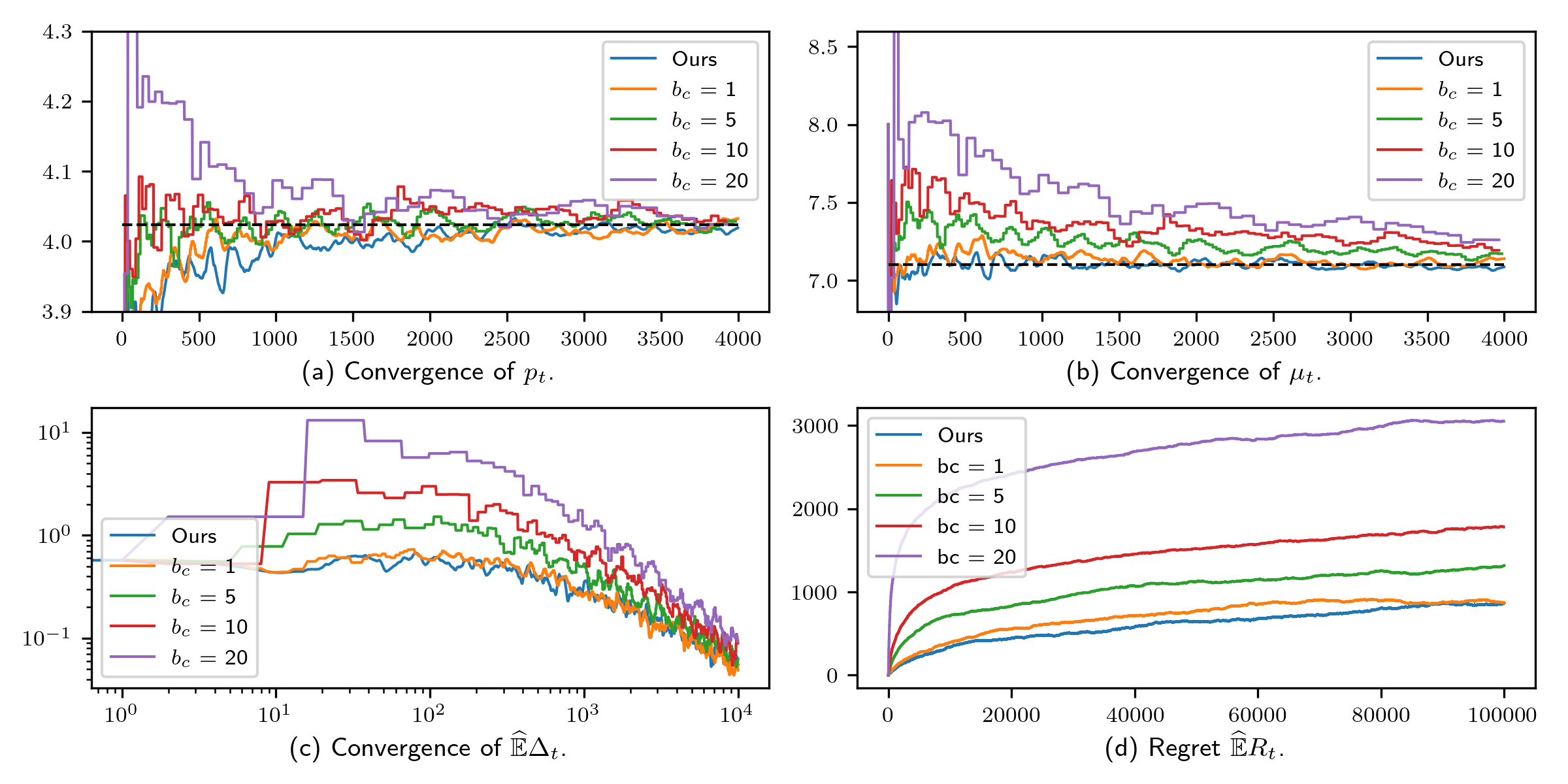

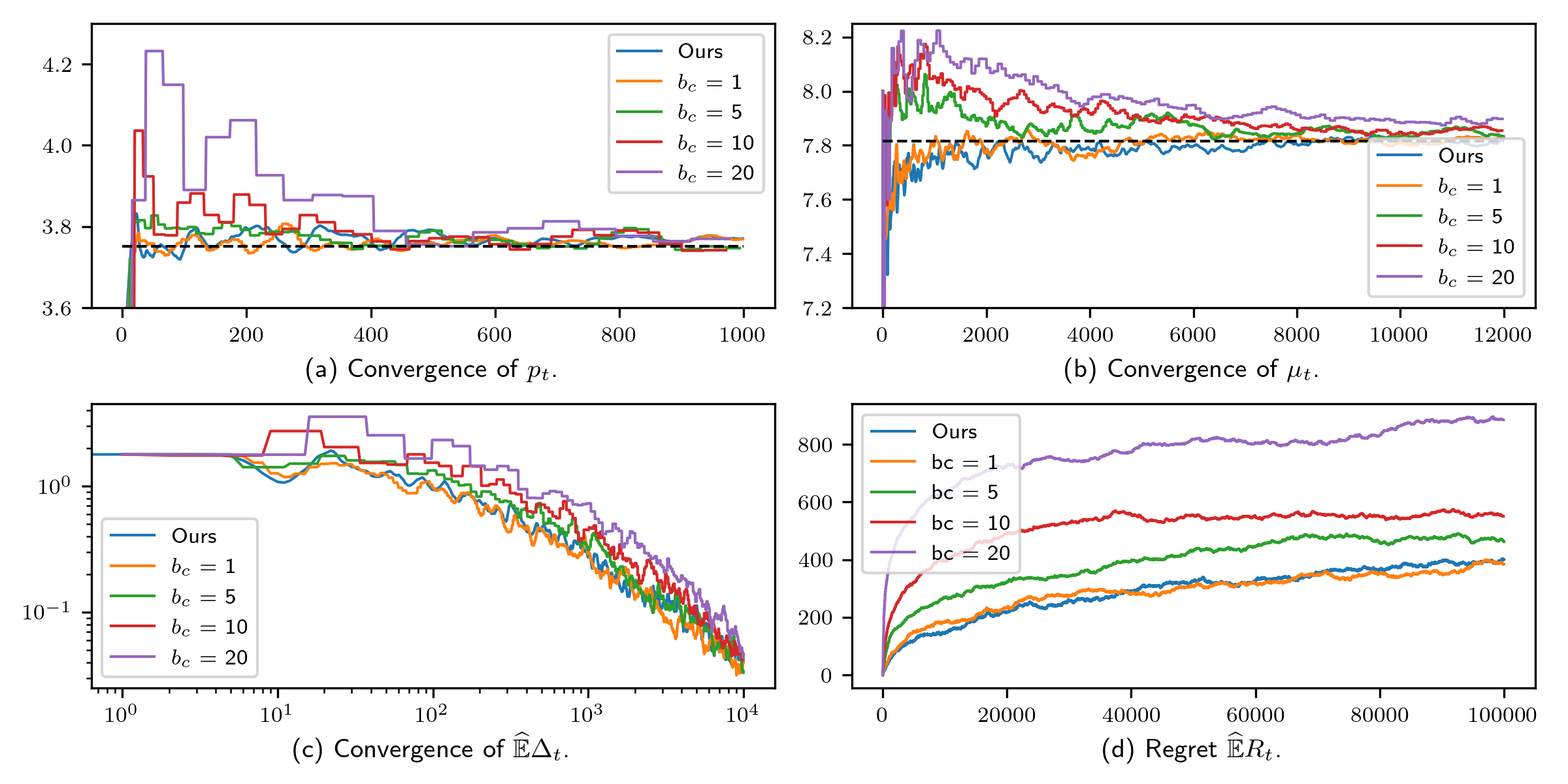

6.2 Convergence and Regret Results

The numerical results of SAMCMC and GOLiQ with different choices of are reported in Figures 3 to 5 corresponding to different queueing model settings. In each figure, the top two panels report the averaged trajectories of the control parameter and , respectively, while the left-bottom panel reports the average difference between and and the right-bottom one reports the average cumulated regret. The -axes denote the number of data samples, or equivalently, the number of customers served, in all panels.

Our first observation is that increasing batch size does not help either in improving the convergence rate or in reducing cumulated regret in all the queueing models. This encores our theoretic result that gradient estimation with a single data point is adequate for controlling transient bias and guaranteeing algorithm convergence. The difference between SAMCMC and GOLiQ is more significant when , which can be attributed to an overemphasis on gradient quantity at the expense of the optimization process itself, as an excessive number of samples are allocated to refining gradient estimates rather than advancing the optimization trajectory. When , the batch size is close to for small , as a consequence, we see that the two curves corresponding to SAMCMC and GOLiQ with are similar in the early iterations but gradually deviate from each other in the later iterations.

Comparing Figures 4, 3, and 5 corresponding to models with and , respectively, we find that the improvement of SAMCMC over GOLiQ seems more significant when there is more variability in the system dynamics, i.e. with larger value of . A more rigorous analysis of this phenomenon is left for future study.

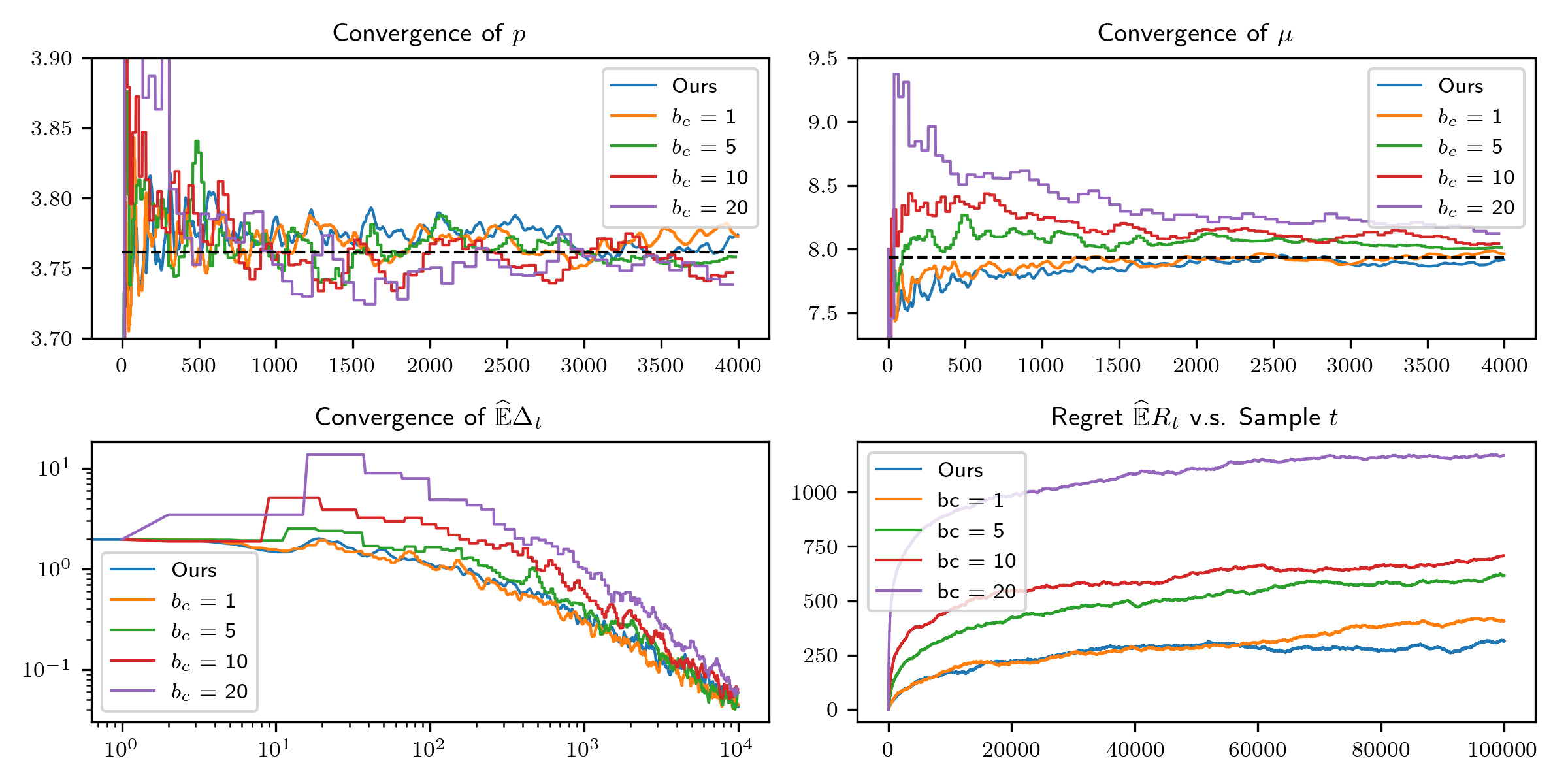

6.3 Robustness Check on the Step Sizes

While our theory uses the same step size , we experiment with different step sizes for different coordinates. From the theoretic aspect, this discrepancy does not pose a critical problem. An effective amendment is to substitute the standard Euclidean norm with a weighted one. Specifically, for any set of positive weights denoted as for , if we intend to implement a separate step size to update the -th coordinate, we could replace the inner product with a weighted counterpart in all our theoretical assumptions. This adaptation retains its efficacy as long as all the step sizes approach zero uniformly at the same rate. Under these new assumptions, the fundamental tenets of our theoretical framework remain preserved without changing the proof too much.

In addition to the above amendment to the convergence theory, we next test the robustness of the choice of step sizes numerically. Allowing the flexibility of employing distinct yet proportionate step sizes for different coordinates, we implement SAMCMC with a set of different step sizes in the form of for updating and for updates with .

In the top panel of Figure 7, we plot the logarithmic of the resulting difference versus the logarithmic of the number of data samples. We see that all the curves can be well fitted by some 45-degree line as depicted in the graphs, indicating that the convergence rate holds in all queueing settings with different choices of step size. In the bottom panel of Figure 7, we plot the cumulated regret versus the logarithmic of the number of data samples. Consistent with the theoretic regret bounds, in all settings, the curve of regret becomes close to a straight line, although with different slopes, in the later iterations. To this light, our numerical results illustrate the robustness of SAMCMC with respect to the choice of step sizes in both dimensions.

Another interesting observation is that step size combinations and perform slightly better than the coordinately equal step size . One possible explanation is that the objective function, along the dimension of staffing level , is flatter around the optimal solution, compared to that along the dimension of price (see figure 6 of Chen et al. (2023)). As a consequence, applying a larger step size to could help improve algorithm convergence.

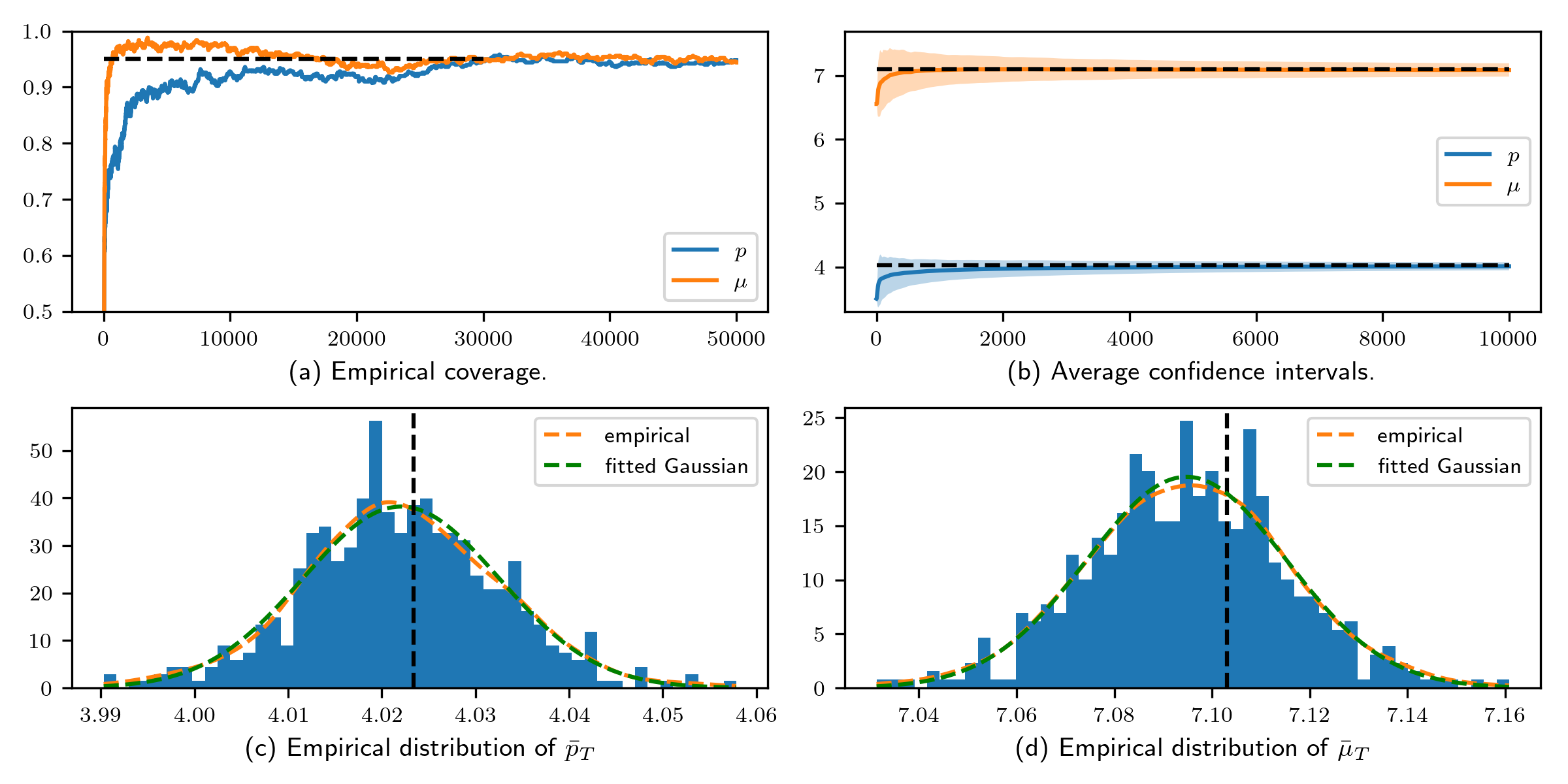

6.4 Numerical Performance of Online Inference Method

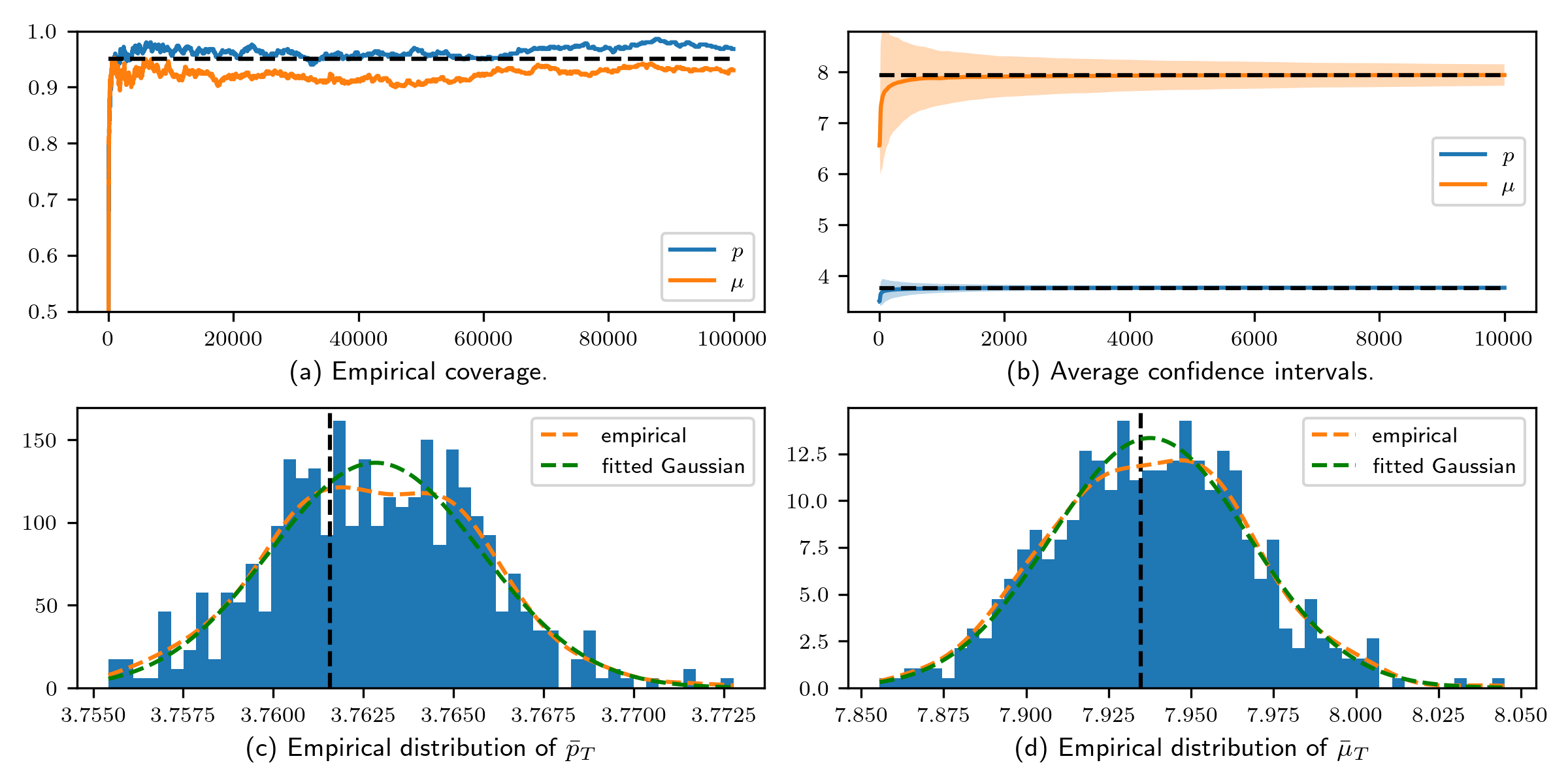

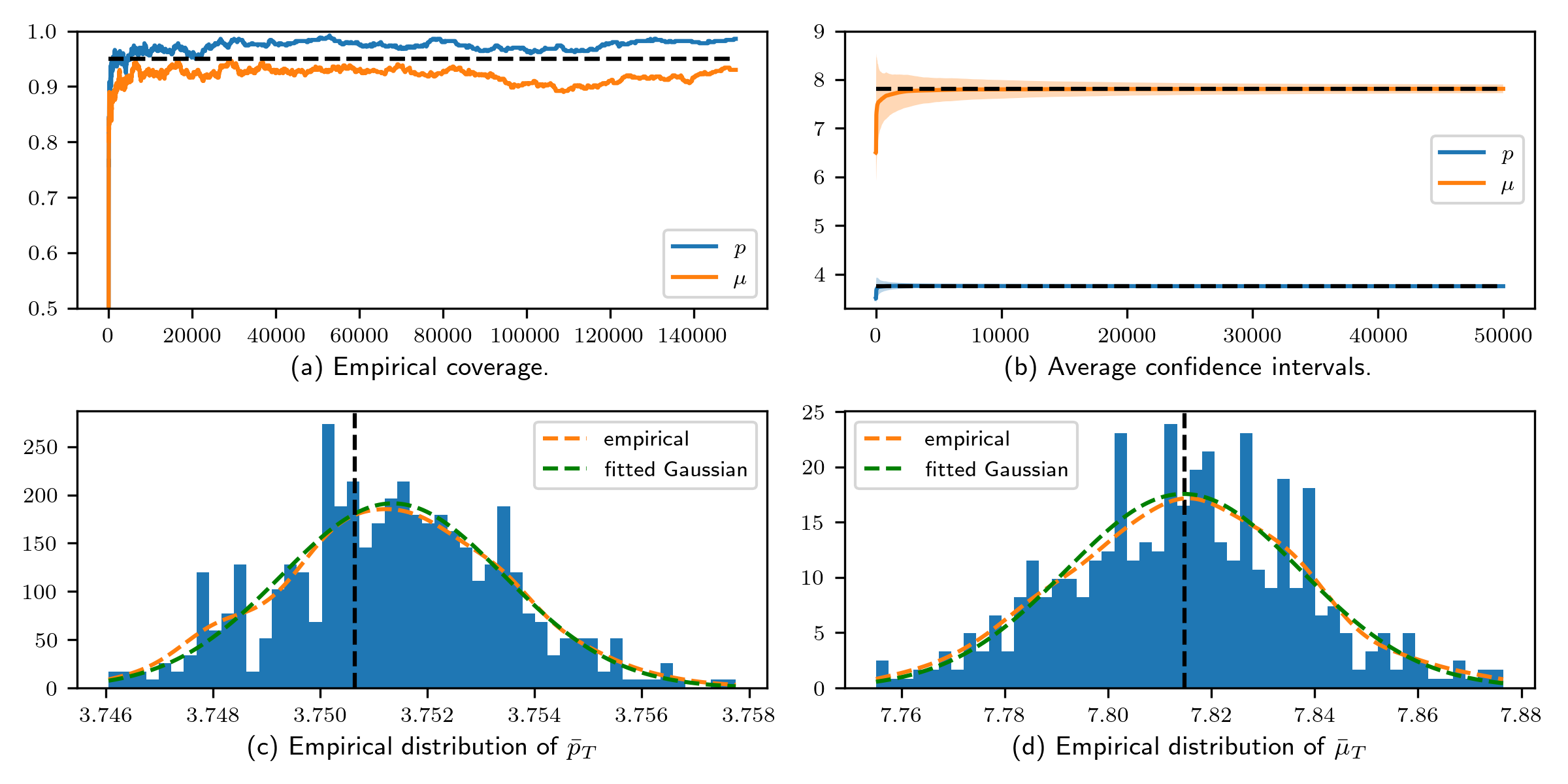

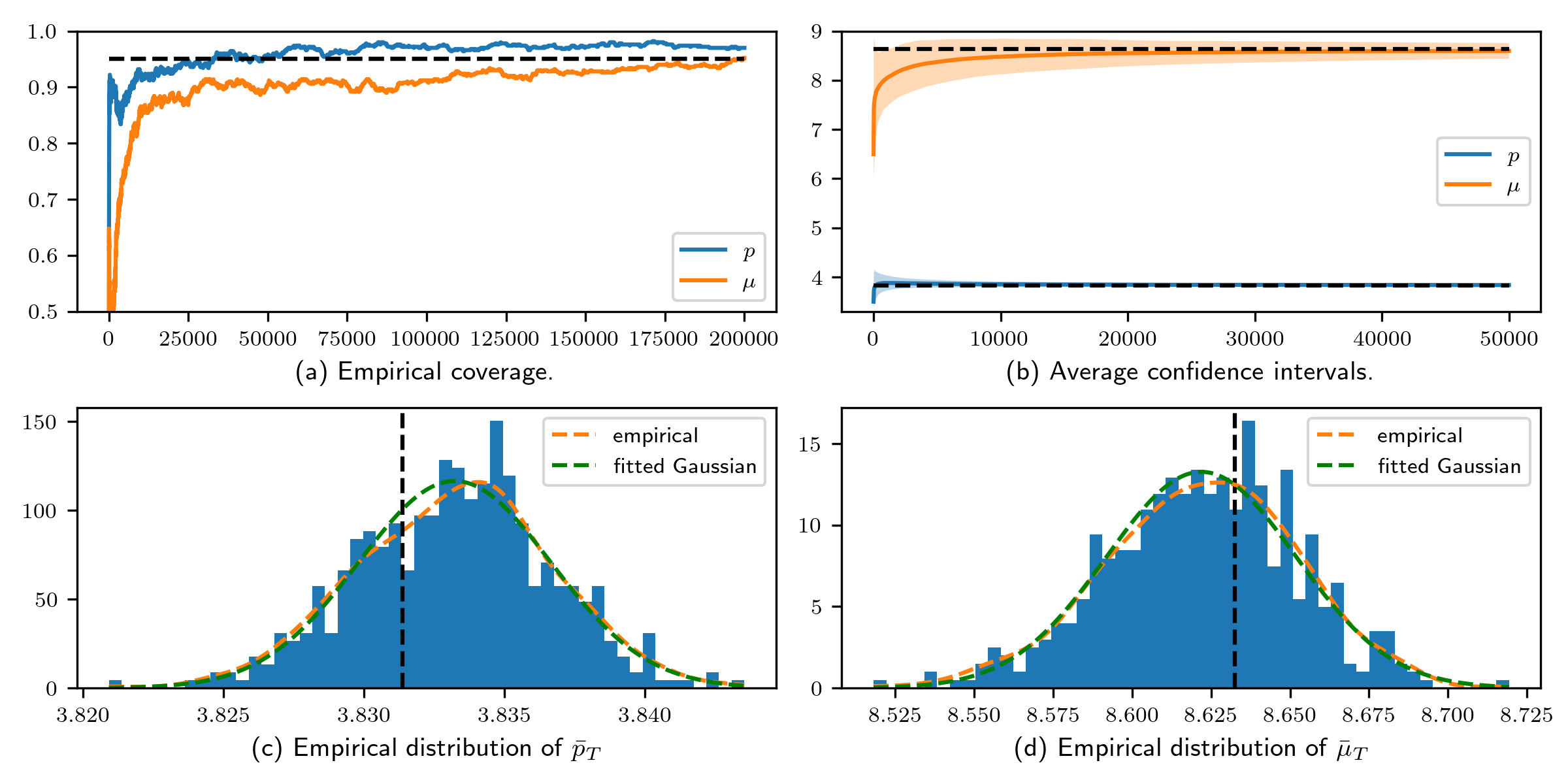

We retain the same three experimental setups introduced in Section 6.1. To ensure consistency with our theoretical framework, we adopt polynomial step sizes across all experiments detailed in this section. Specifically, we employ for updating the parameter , and for updating , where we set and . To provide a comprehensive overview, we also furnish results for the same step sizes with in the appendix. It is worth noting that similar performance trends have been observed under these conditions.

In each of Figures 8 to 11 below, we report (a) the empirical coverage rate across 500 repetitions and (b) visualization of averaged confidence intervals. To better depict the actual distribution of the averaged estimators and , we report their histograms across the 500 repeated experiments along with the fitted Gaussian distributions in panels (c) and (d), respectively. We also display the distributions fitted using Gaussian kernel density methods, denoted as “empirical”, as a nonparametric alternative to illustrate the empirical distribution.

Consistent with Corollary 3, the empirical coverage rate progressively increases as the iterations advance and the volume of received samples grows, as illustrated in panels (a). In addition, the empirical coverage rates converge around the intended coverage rate in all settings. Furthermore, in panel (b), we see that the averaged confidence intervals showcase a consistent tendency to cover the true parameters while gradually dwindling its confidence interval lengths.

The histograms of or are well approximated by the fitted Gaussian distributions, aligning with the expectations laid out in Corollary 2. It’s important to note that the perceived deviation of the true parameter (denoted by black dotted straight lines) from the centers of both empirical and fitted Gaussian distributions is misleading, primarily due to the diminutive scale of the -axis. For instance, in Figure 8, the mean of the estimated Gaussian distributions deviates from the true parameter by no more than 0.004 – an exceedingly minimal error.

7 Concluding Remarks

In this paper, we propose a stochastic approximation MCMC (SAMCMC) algorithm for steady-state optimization of queueing systems and develop a novel online inference method to quantify the uncertainty of the SAMCMC output. For theoretic verification of the efficiency of our proposed algorithms, we establish both a non-asymptotic convergence rate and regret bound for the final output of SAMCMC and derive the functional central limit theory for the averaging trajectory of the SAMCMC output sequence, which is of independent research interest. Our theoretical results are built on Propositions 1 to 2, which are commonly made as the assumptions in the stochastic approximation literature. Thus, if similar conditions are satisfied, we could apply our convergence results and inference methods to a general SAMCMC setting beyond the current queueing system. To the best of our knowledge, we are the first to explore the SAMCMC algorithm along with the online statistical inference for the GI/GI/1 queueing optimization.

There are several venues for future research. One natural extension would be to apply and analyze SAMCMC for steady-state optimization in other operations research problems such as inventory control. Another dimension would be developing sufficient conditions that ensure convergence in more general settings beyond queueing systems but are easier to validate, especially compared to the conditions in Assumption 1 and 2 that are expressed in terms of the solutions to Poisson equations.

References

- Abadir and Paruolo [1997] Karim M Abadir and Paolo Paruolo. Two mixed normal densities from cointegration analysis. Econometrica: Journal of the Econometric Society, pages 671–680, 1997.

- Andrieu and Moulines [2006] C. Andrieu and É. Moulines. On the ergodicity property of some adaptive MCMC algorithms. The annals of Applied Probability, 16:1462–1505, 2006.

- Atchadé and Liu [2010] Yves F Atchadé and Jun S Liu. The Wang-Landau algorithm in general state spaces: Applications and convergence analysis. Statistica Sinica, pages 209–233, 2010.

- Atchadé et al. [2017] Yves F Atchadé, Gersende Fort, and Eric Moulines. On perturbed proximal gradient algorithms. The Journal of Machine Learning Research, 18(1):310–342, 2017.

- Benveniste et al. [2012] Albert Benveniste, Michel Métivier, and Pierre Priouret. Adaptive algorithms and stochastic approximations, volume 22. Springer Science & Business Media, 2012.

- Borkar [2009] Vivek S Borkar. Stochastic approximation: A dynamical systems viewpoint, volume 48. Springer, 2009.

- Chen et al. [2020] Xi Chen, Jason D Lee, Xin T Tong, and Yichen Zhang. Statistical inference for model parameters in stochastic gradient descent. The Annals of Statistics, 48(1):251–273, 2020.

- Chen et al. [2021] Xi Chen, Zehua Lai, He Li, and Yichen Zhang. Online statistical inference for stochastic optimization via Kiefer-Wolfowitz methods. arXiv e-prints, pages arXiv–2102, 2021.

- Chen et al. [2023] Xinyun Chen, Yunan Liu, and Guiyu Hong. An online learning approach to dynamic pricing and capacity sizing in service systems. Operations Research, 2023.

- Chong and Ramadge [1994] E. K. P. Chong and P. J. Ramadge. Stochastic optimization of regenerative systems using infinitesimal perturbation analysis. IEEE Transactions on Automatic Control, 39:1400–1410, 1994.

- Durrett [2013] Rick Durrett. Probability: Theory and Examples (Edition 4.1). Cambridge University Press, 2013.

- Fang et al. [2018] Yixin Fang, Jinfeng Xu, and Lei Yang. Online bootstrap confidence intervals for the stochastic gradient descent estimator. The Journal of Machine Learning Research, 19(1):3053–3073, 2018.

- Fu [1990] M. C. Fu. Convergence of a stochastic approximation algorithm for the GI/G/1 queue using infinitesimal perturbation analysis. Journal of Optimization Theory and Applications, 65:149–160, 1990.

- Glynn and Meyn [1996] Peter W Glynn and Sean P Meyn. A liapounov bound for solutions of the poisson equation. The Annals of Probability, pages 916–931, 1996.

- Gu and Kong [1998] Ming Gao Gu and Fan Hui Kong. A stochastic approximation algorithm with Markov chain Monte-Carlo method for incomplete data estimation problems. Proceedings of the National Academy of Sciences, 95(13):7270–7274, 1998.

- Gu and Zhu [2001] Ming Gao Gu and Hong-Tu Zhu. Maximum likelihood estimation for spatial models by Markov chain Monte Carlo stochastic approximation. Journal of the Royal Statistical Society Series B: Statistical Methodology, 63(2):339–355, 2001.

- Hall and Heyde [2014] Peter Hall and Christopher C Heyde. Martingale limit theory and its application. Academic press, 2014.

- Huh et al. [2009] W. T. Huh, G. Janakiraman, J. A. Muckstadt, and P. Rusmevichientong. An adaptive algorithm for finding the optimal base-stock policy in lost sales inventory system with censored demand. Mathematics of Operations Research, 34(2):397–416, 2009.

- Jia et al. [2022] Huiwen Jia, Cong Shi, and Siqian Shen. Online learning and pricing for service systems with reusable resources. Operations Research, 0(0):null, 2022.

- Karimi et al. [2019] Belhal Karimi, Blazej Miasojedow, Eric Moulines, and Hoi-To Wai. Non-asymptotic analysis of biased stochastic approximation scheme. In Conference on Learning Theory, pages 1944–1974. PMLR, 2019.

- Kiefer et al. [2000] Nicholas M Kiefer, Timothy J Vogelsang, and Helle Bunzel. Simple robust testing of regression hypotheses. Econometrica, 68(3):695–714, 2000.

- Kurtz [2005] Thomas G Kurtz. Averaging for martingale problems and stochastic approximation. In Applied Stochastic Analysis: Proceedings of a US-French Workshop, Rutgers University, New Brunswick, NJ, April 29–May 2, 1991, pages 186–209. Springer, 2005.

- Kushner and Yin [2003] Harold Kushner and G George Yin. Stochastic approximation and recursive algorithms and applications, volume 35. Springer Science & Business Media, 2003.

- L’Ecuyer and Glynn [1994] P. L’Ecuyer and P. W. Glynn. Stochastic optimization by simulation: Convergence proofs for the GI/GI/1 queue in steady state. Management Science, 40(11):1562–1578, 1994.

- L’Ecuyer et al. [1994] P. L’Ecuyer, N. Giroux, and P. W. Glynn. Stochastic optimization by simulation: Numerical experiments with the M/M/1 queue in steady-state. Management Science, 40(10):1245–1261, 1994.

- Lee et al. [2022a] Sokbae Lee, Yuan Liao, Myung Hwan Seo, and Youngki Shin. Fast and robust online inference with stochastic gradient descent via random scaling. In the AAAI Conference on Artificial Intelligence, volume 36, pages 7381–7389, 2022a.

- Lee et al. [2022b] Sokbae Lee, Yuan Liao, Myung Hwan Seo, and Youngki Shin. Fast inference for quantile regression with tens of millions of observations. Available at SSRN 4263158, 2022b.

- Li and Wai [2022] Qiang Li and Hoi-To Wai. State dependent performative prediction with stochastic approximation. In International Conference on Artificial Intelligence and Statistics, pages 3164–3186. PMLR, 2022.

- Li et al. [2018] Tianyang Li, Liu Liu, Anastasios Kyrillidis, and Constantine Caramanis. Statistical inference using SGD. In the AAAI Conference on Artificial Intelligence, volume 32, 2018.

- Li et al. [2022] Xiang Li, Jiadong Liang, Xiangyu Chang, and Zhihua Zhang. Statistical estimation and online inference via Local SGD. In Po-Ling Loh and Maxim Raginsky, editors, Conference on Learning Theory, volume 178, pages 1613–1661. PMLR, 2022.

- Li et al. [2023a] Xiang Li, Jiadong Liang, and Zhihua Zhang. Online statistical inference for nonlinear stochastic approximation with markovian data. arXiv preprint arXiv:2302.07690, 2023a.

- Li et al. [2023b] Xiang Li, Wenhao Yang, Zhihua Zhang, and Michael I Jordan. A statistical analysis of Polyak-Ruppert averaged Q-Learning. In International Conference on Artificial Intelligence and Statistics, volume 206, 2023b.

- Liang [2010] Faming Liang. Trajectory averaging for stochastic approximation MCMC algorithms. The Annals of Statistics, 38(5):2823–2856, 2010.

- Liang et al. [2007] Faming Liang, Chuanhai Liu, and Raymond J Carroll. Stochastic approximation in Monte Carlo computation. Journal of the American Statistical Association, 102(477):305–320, 2007.

- Liang and Su [2019] Tengyuan Liang and Weijie J Su. Statistical inference for the population landscape via moment-adjusted stochastic gradients. Journal of the Royal Statistical Society, 2019.

- Liu et al. [2022] Yi Liu, Ke Sun, Bei Jiang, and Linglong Kong. Identification, amplification and measurement: A bridge to gaussian differential privacy. In Advances in Neural Information Processing Systems, volume 35, pages 11410–11422, 2022.

- Ma et al. [2015] Yi-An Ma, Tianqi Chen, and Emily Fox. A complete recipe for stochastic gradient MCMC. Advances in neural information processing systems, 28, 2015.

- Moulines and Bach [2011] Eric Moulines and Francis Bach. Non-asymptotic analysis of stochastic approximation algorithms for machine learning. Advances in neural information processing systems, 24, 2011.

- Moyeed and Baddeley [1991] RA Moyeed and Adrian J Baddeley. Stochastic approximation of the MLE for a spatial point pattern. Scandinavian Journal of Statistics, pages 39–50, 1991.

- Nemeth and Fearnhead [2021] Christopher Nemeth and Paul Fearnhead. Stochastic gradient Markov chain Monte Carlo. Journal of the American Statistical Association, 116(533):433–450, 2021.

- Polyak and Juditsky [1992] Boris T Polyak and Anatoli B Juditsky. Acceleration of stochastic approximation by averaging. SIAM journal on control and optimization, 30(4):838–855, 1992.

- Ramprasad et al. [2021] Pratik Ramprasad, Yuantong Li, Zhuoran Yang, Zhaoran Wang, Will Wei Sun, and Guang Cheng. Online bootstrap inference for policy evaluation in reinforcement learning. Journal of the American Statistical Association, 2021.

- Ravner and Snitkovsky [2023] Liron Ravner and Ran I. Snitkovsky. Stochastic approximation of symmetric Nash equilibria in queueing games. Operations Research, 0(0):null, 2023.

- Robbins and Siegmund [1971] Herbert Robbins and David Siegmund. A convergence theorem for non-negative almost supermartingales and some applications. In Optimizing methods in statistics, pages 233–257. Elsevier, 1971.

- Su and Zhu [2023] Weijie J Su and Yuancheng Zhu. Higrad: Uncertainty quantification for online learning and stochastic approximation. Journal of Machine Learning Research, 24(124):1–53, 2023.

- Suri and Zazanis [1988] Rajan Suri and Michael A Zazanis. Perturbation analysis gives strongly consistent sensitivity estimates for the M/G/1 queue. Management Science, 34(1):39–64, 1988.

- Toulis and Airoldi [2017] Panos Toulis and Edoardo M Airoldi. Asymptotic and finite-sample properties of estimators based on stochastic gradients. The Annals of Statistics, 45(4):1694–1727, 2017.

- Whitt [2007] Ward Whitt. Proofs of the martingale FCLT. Probability Surveys, 4:268–302, 2007.

- Yuan et al. [2021] Hao Yuan, Qi Luo, and Cong Shi. Marrying stochastic gradient descent with bandits: Learning algorithms for inventory systems with fixed costs. Management Science, 67(10):6089–6115, 2021.

- Zhang et al. [2020] Huanan Zhang, Xiuli Chao, and Cong Shi. Closing the gap: A learning algorithm for lost-sales inventory systems with lead times. Management Science, 66(5):1962–1980, 2020.

- Zhu et al. [2021] Wanrong Zhu, Xi Chen, and Wei Biao Wu. Online covariance matrix estimation in stochastic gradient descent. Journal of the American Statistical Association, pages 1–12, 2021.

Appendix A Proofs for Section 3

Proof of Proposition 1.

Now we are going to verify Proposition 1. Recall that the gradient estimator has the following closed form

On the one hand, for a fixed and different , the triangle inequality yields

On the other hand, for a fixed and different , a similar analysis follows

Due to Assumption 1, the absolute value part in every term above can be bounded by the difference of considered two parameters, that is, by , where is a constant depending on the smoothness of and problem-dependent constants including and . Putting everything together, we

Thus, Proposition 1 holds by taking . ∎

Appendix B Proofs for Section 4

B.1 Proofs for Continuity of the Poisson Equation’s Solution

Recall the definition of the waiting time sequence and the observed busy period sequence , both of which depend on the parameter . In this section, our primary aim is to establish the Lipschitz continuity of and with respect to the parameter .

B.1.1 Proof of Lemma 2

Proof of Lemma 2.

There is an equivalent characterization of the Poisson equation’s solution [Glynn and Meyn, 1996], that is,

| (20) |

where we denote for simplicity and denote an operator defined on the function space . Lemma 2 and Lemma 6 in [Chen et al., 2023] show that this infinite summation is well-defined when .

Now, we set a large number and consider a truncated version of :

It can be shown that

The remainder of the proof involves bounding for respectively. Without loss of generality, we assume that in the subsequent proof. Importantly, there are no technical difficulties if one wants to extend this analysis to the scenario where .

Step 1: Analysis on

In the following, for simplicity, we will employ the notation to denote that is smaller than by an absolute constant factor. According to the mechanism for generating and Lemma 5 and 6, we have

where for .

Next we plug the definition of into and . We assume . The other case where would be easier to analyze using the same argument. It then follows that

Taking these back into the bound for , we get that

We then start to analyze both and . One one hand,

For , we leverage the condition in the indicator function to get . For , we use . Here is a universal constant independent with and .

On the other hand, for , a similar argument yields that

Consequently, we obtain

Step 2: Bound for

For simplicity, we define an operator by . The analysis in Step 1 shows

We now consider every term in the double summation of , i.e.,

we will control this term according to the relative magnitude between and .

If , because is non-expansive, we can get

If , we apply synchronous coupling. To that end, we let be the zero hitting time of , i.e., . Then

By truncating each based on the condition , we can proceed with the second integration

Therefore, Bernstein’s inequality implies that

Here uses Lemma 3 when we perform the integration with respect to the measure .

Step 3: Bound for

We first simplify the expression of :

Therefore,

Due to the uniform ergodicity of GI/GI/1 system, we replace the stationary distribution by where we denote the initial state by and set sufficiently large number so that and for all . For simplicity, we set and consider

The definition of implies that

As for , it follows that

| (21) | ||||

Here holds because the Markovian operator is non-expansive, uses the bound of , which is discussed in the first step of this proof, with . Next, we are going to deal with the above expectations to be summed up. In fact, we may assume with defined in Lemma 3. Otherwise, by the positive homogeneity of , we have with . And note actually, we always have . Therefore,

Because of Lemma 3, the right hand of the inequality is upper bounded by up to some constants.

For the following two lemmas, we use subscript instead of previous to emphasize that is generated from , a transition kernel with a fixed parameter .

Lemma 5 (Lemma 2 in [Chen et al., 2023]).

Suppose two GI/GI/1 queues with parameter are synchronously coupled with initial waiting times and , respectively. Then, for the two positive constants and defined in Assumption 2 and any , we can find a , such that conditional on and

Lemma 6.

Suppose two GI/GI/1 queues with parameter are synchronously coupled with initial waiting time, observed busy period pairs and , respectively. Then under Assumption 2, for any , it holds that

Here is denoted as . Specifically, when , we can write the bound as follows:

where is an absolute constant and is only related to and .

B.1.2 Proof of Lemma 3

Proof of Lemma 3.

For simplicity, we assume the initial states . The proof for other initial states can be imitated similarly. We then introduce several notations which are also used in the proof of Lemma 6. We define the hitting time of reaches zero within the iteration , that is,

it is obvious that from this definition. We define

| (22a) | ||||

| (22b) | ||||

| (22c) | ||||

Clearly, is a zero mean i.i.d random sequence. An important observation is that

| (23) |

Sub-exponential of W

We first handle the bound of the waiting time . It follows that

Here uses Bernstein’s inequality and holds for .

Sub-exponential of Y

At a high level, the derivation for the bound of is similar, i.e., to consider the latest hitting time where reaches zero before . The difference is that here a more detailed analysis is required because the transition of is much involved. Defining , we then have

| (24) | ||||

When , we have

where holds due to Bernstein’s inequality and follow from the condition which implies .

When , we have

We redefine as so that we have

Plugging the above results into (24) yields

| (25) | ||||

The last inequality is derived by letting and . Here, we assume that is an integer. In cases where it is not, we can simply replace it with its floor or ceiling value. Based on the preceding proof above, our result remains valid with only a minor adjustment to the constants involved. ∎

B.1.3 Proof of Proposition 2

Proof of Proposition 2.

We verify and sequentially.

For , we first observe that both two coordinates of have the form , where are Lipschitz continuous (which are easy to check given the explicit expression in (7)). In fact, by the linearity of the operator (defined in (B.1.1)), it follows that

where . It’s clear that is -Lipschitz continuous. Combining the Lipschitz continuity of and Lemma 2 yields

We complete the proof for by noting that

Here can be defined by .

For and , it suffices to show

| (26) |

according to the form of and obtained above and the specific expression of functions and . Here, the sequence represents the sample sequence generated while the SAMCMC is in progress.

Unlike the case considered in Lemma 3, the parameter is no longer fixed here; it varies as we proceed with the SAMCMC. Nevertheless, Lemma 3 could serve as a bridge and help us to get (26) still. To see this, we introduce an auxiliary sequence that satisfies

This auxiliary sequence share the same randomness and initial state with the actual sequence . If we can show that

| (27) |

then the proof is completed by applying Lemma 3 directly which implies

In the following, we show that (27) is indeed true. We prove this by induction. When , the inequalities hold trivially. Suppose we’ve already had and . At the -iteration, noting that and using the monotonicity of and , we have

Hence, the two inequalities (27) hold at -iteration and thus hold at any time by induction.

∎

B.2 Proofs for Convergence Results

Proposition 2 shows that is -Lipschitz w.r.t. for any given data point . Similarly, the is average--Lipschitz at the parameter for any given data point . Note that the Lipschitz modules and are allowed to depend on the data rather than a universal constant in previous works [Li and Wai, 2022, Li et al., 2023a]. In order to ensure stability, we require both and are uniformly bounded. As a result, we have the following result

Lemma 7 implies that both the incremental update and the conditional functions have uniformly bounded second moments. The analysis of Lemma 7 heavily depends on the fact that all iterates locate in that is contained in a ball with radius . If we allow to be infinity, then we should force and to be constant again so as to ensure stability and convergence.

An important intermediate result is that all any polynomial functional of is bounded.

Lemma 8.

For any , there exists some problem-dependent constant such that

Proof of Lemma 8.

This lemma follows from Lemma 3 where we bound the tail distribution of both and , which exhibit subexponential behaviors. ∎

B.2.1 Proof of Theorem 1

In the following, we will establish Theorem 1 step by step. We first capture the one-step progress of our Markov SGD in Lemma 9.

Once is sufficiently small (e.g., ), we have . It implies that the first term in the r.h.s. of (28) is a contraction. To simplify notations, we introduce the scalar product , for , and if . Solving the recursion in (28) yields

| (29) | ||||

It can be shown that the first two terms in (60) are bounded by . Indeed, the first term would decay exponentially fast by using the numerical inequality . For the second term, by the following Lemma 20, we immediately know that , given the step size condition in Assumption 4.

Lemma 10.

Let and be a non-increasing sequence such that . If for any , then for any ,

In the following, we focus on analyzing the last term in (60) which we refer to as the cross term, and present the result in Lemma 11. When the samples are drawn according to , to bound the expectation of this cross term in Lemma 11, we make use of the Poison equation and decompose the gradient error into martingale and finite difference terms. This analysis approach is inspired by Benveniste et al. [2012] and has recently been used by Atchadé et al. [2017], Karimi et al. [2019], Li and Wai [2022] for the finite-time convergence analysis of their interested algorithms.

Lemma 11.

To proceed the proof, we substitute Lemma 11 and Lemma 20 into (60) and obtain

| (32) |

where we introduce constants for notation simplicity

| (33) |

Lemma 12.

Proving the above lemma requires one to establish the stability of the system (B.2.1), which demands a sufficiently small to control the remainder term . Our analysis relies on the special structure of this inequality system which is also used by Li and Wai [2022]. The convergence bound (35) follows from the boundedness of in (35). Applying Lemma 12 finishes the proof of Theorem 1.

B.2.2 Proof of Lemma 7

B.2.3 Proof of Lemma 9

Proof of Lemma 9.

Let be the -field generated by all randomness before iteration . Then . By the non-expansiveness of projections, it follows that

The inner product can be lower bounded as

| (36) |

where the last inequality is due to the -strong convexity of .

Furthermore, by Lemma 7,

Combing the bounds for and , we can get the desired inequality.

∎

B.2.4 Proof of Lemma 20

Proof of Lemma 20.

It follows that

∎

B.2.5 Proof of Lemma 11

Proof of Lemma 11.

Note that due to . By applying the Poisson equation, we can simplify the sum of inner products into

In the following, the key idea is to decompose

into four sub-terms which can be bounded using the smoothness assumption. In particular, we have

For , as , we get . Applying the smoothness condition of in , we have that

| (37) |

where (a) uses for any and (b) uses Lemma 7.

For , notice that and thus

Using this inequality, we have that

| (39) |

where the last inequality again uses Lemma 7.

Finally, for , we have

| (40) |

B.2.6 Proof of Lemma 12

Proof of Lemma 12.

Recall that the sequence satisfies the following inequality

| (B.2.1) |

The inequality in (B.2.1) is not easy to handle. We then introduce a non-negative auxiliary sequence that always serves as a valid upper bound of . This sequence is defined by the recursion: and

| (42) |

By induction, it is easy to see that for any .

Note that for any . Arrangement on (42) implies that

where the last inequality uses the inequalities on step sizes in Assumption 4, namely the following results

-

•

for all ;

-

•

.

Given the established inequality

| (43) |

we are ready to establish the lemma.

We first prove the part (i) of the lemma. Summing up the inequality (43) over to yields

Rearranging the last inequality give

where (a) uses , (b) uses , (c) uses , and (d) is due to repeatedly using (c) times

B.3 Proofs for Regret Analysis

B.3.1 Proof of Lemma 4

Proof of Lemma 4.

For any initial state and inital parameter , we let be the waiting time process follows the generating rule (5). By Lemma 5, for any , we have

According to Lemma 3, there is an independent of and such that is sub-exponential,i.e., . Without loss of generality, we may assume . Otherwise, by the positive homogeneity of , we have with a new . Plugging , the waiting time in -th cycle in SAMCMC, into the above inequality yields

When setting , we can get

Note that the same argument holds for any parameter . Especially, we have

Note the fact and the following decomposition

In the following, we are going to analyze any summand in this summation. To make use of the Lipschitz continuity of the waiting time , we introduce a new random variable to denote the next state obtained by starting from and following the generation rule (5). Here we assume the generation of shares the same randomness as that we used to generate from . As a result, it follows that