Weak Markovian Approximations of Rough Heston

Abstract.

The rough Heston model is a very popular recent model in mathematical finance; however, the lack of Markov and semimartingale properties poses significant challenges in both theory and practice. A way to resolve this problem is to use Markovian approximations of the model. Several previous works have shown that these approximations can be very accurate even when the number of additional factors is very low. Existing error analysis is largely based on the strong error, corresponding to the distance between the kernels. Extending earlier results by [Abi Jaber and El Euch, SIAM Journal on Financial Mathematics 10(2):309–349, 2019], we show that the weak error of the Markovian approximations can be bounded using the -error in the kernel approximation for general classes of payoff functions for European style options. Moreover, we give specific Markovian approximations which converge super-polynomially in the number of dimensions, and illustrate their numerical superiority in option pricing compared to previously existing approximations. The new approximations also work for the hyper-rough case .

Key words and phrases:

Rough Heston model, Markovian approximations, Weak error2020 Mathematics Subject Classification:

91G60, 91G201. Introduction

Rough volatility [Bay+23] is a now established paradigm for modeling of equity markets, which provides excellent fits to market data. However, theoretical analysis and numerical approximation typically becomes more challenging as rough volatility models are neither Markov processes nor semimartingales. Apart from the rough Bergomi model [BFG16], the workhorse model of rough volatility is the rough Heston model [EER19] given by

| (1.1) | ||||

| (1.2) |

where , , where is a two-dimensional standard Brownian motion and where is the fractional kernel given by

| (1.3) |

with Hurst parameter .

The kernel in (1.2) introduces a dependence of the volatility process on the past, ensuring that the volatility has memory. However, this also means that the process is neither a Markov process, nor a semi-martingale. Furthermore, the sample paths of are only -Hölder continuous, for all , where is the Hurst parameter in (1.3). This leads to significant problems of the rough Heston model both in terms of theoretical analysis, and for simulation of sample paths, and option pricing more generally. Note, however, that the rough Heston model is an affine Volterra process [AJLP19], and can be analyzed as such, implying weak existence and uniqueness as well as a semi-explicit formula for the characteristic function – in terms of a fractional Riccati equation.

One remedy for these challenging properties of the model is to use Markovian approximations of . More precisely, note that the kernel is completely monotone, and can thus be written as

| (1.4) |

for all , where is the gamma function.

Taking the special example of fractional Brownian motion (fBm) for a moment, we observe that

| (1.5) |

where is a Brownian motion, and where we used the stochastic Fubini theorem. Note that is an Ornstein-Uhlenbeck (OU) process driven by with mean-reversion rate . Indeed, in [CC98] it was shown that is an infinite-dimensional Markov process. Therefore, fBm is a linear functional of an infinite-dimensional Markov process.

The representation (1.5) indicates a natural way of approximating fBm by a finite-dimensional Markov process. We simply discretize the integral over in (1.5), to obtain an approximation of as a linear functional of a finite-dimensional OU (and hence Markov) process. Furthermore, it is easy to see that discretizing the integral in (1.5) is equivalent to discretizing the integral in (1.4), i.e. to approximating by a discrete sum of exponential functions given by

| (1.6) |

for some non-negative nodes and non-negative weights .

Furthermore, using the approximation of , we can define the approximation of by

It has been shown, e.g. in [AJEE19a] and in [AK21, Proposition 2.1], that is the solution to an -dimensional stochastic differential equation (SDE). The precise form of this SDE will however not be important for our purposes.

Given the Markovian approximation of , we are of course interested in proving error bounds and convergence rates as . Assuming Lipschitz-continuous coefficients and , [AK21] proved for general stochastic Volterra equations with Hurst parameter given by

| (1.7) |

the strong error bound

| (1.8) |

for some , where is again defined by replacing with in (1.7).

However, this bound is not directly applicable to the rough Heston model due to the singularity of the square root in . Moreover, the -error in can converge very slowly for small Hurst parameters . Indeed, since , the singularity at of is barely integrable, leading to slow convergence rates. For example, using Gaussian quadrature rules, it was shown in [BB23] that one can achieve a convergence rate of

| (1.9) |

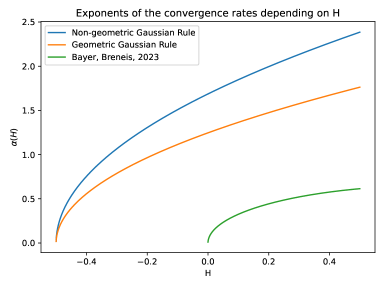

While this rate is superpolynomial, it is still very slow for small – ant not applicable at all in the hyper-rough case , see [JR20].

At the same time, a strong error bound as in (1.8) may be too stringent for many practical applications, where we are often satisfied with a weak error bound. Indeed, in [AJEE19a, Proposition 4.3] is was shown for the specific case of the call option in the rough Heston model with some strike price that we have the much better error bound

| (1.10) |

where . Using the -error instead of the -error in the kernel is a significant improvement, since has much better integrability properties at than . However, the authors of [AJEE19a] did not seem to proceed to prove the weak error bound (1.10) for more general payoff functions. Moreover, they proved (1.10) only under very strong assumptions on the approximating kernel . The first aim of this paper is hence to extend and greatly generalize the results of [AJEE19a]. More precisely, in Corollary 2.12 we prove that for every and for “nice” payoff functions , there exists a constant such that

| (1.11) |

Additionally, the approximating kernels only have to satisfy the rather mild Assumption 2.1.

Having proved the error bound (1.11), we want to find a good approximation of minimizing the -norm, and prove a convergence rate similar to (1.9). We give two slightly different versions in Theorems 3.9 and 3.16. In particular, in Theorem 3.16 we show that we can achieve the convergence rate

| (1.12) |

for any This is a much faster convergence rate than the one in (1.9), especially for tiny , and moreover, it is also valid for negative .

The paper is structured as follows. In Section 2, we prove (1.11), i.e. that the weak error of the Markovian approximations of the rough Heston model can be bounded by the -error in the kernel. Next, in Section 3 we give two separate (but similar) approaches for achieving small -errors in the kernel . Especially the first approach using geometric Gaussian rules in Section 3.1 resembles the approach in [BB23], except that we refine their results in several ways. The second approach in Section 3.2 using non-geometric Gaussian rules is essentially an improvement of the first approach, yielding the rate in (1.12). We decided to give both methods, since the geometric rules are simpler and easier to understand, and since the majority of the proof for the geometric rules can be transferred to the non-geometric rules. Next, in Section 4, we show that by optimizing the -error we can indeed achieve very fast convergence rates and achieve small errors even for small values of the approximating dimension . We also illustrate that minimizing the -error leads to much faster convergence rates in the weak errors than minimizing the -error. Finally, some technical results and some of the algorithms used in Section 4 are delegated to the appendices.

2. Weak error of Markovian approximations

Throughout this section, we will work under the following assumption.

Assumption 2.1.

Assume that are chosen such that

and that there exists a constant such that for all and , we have

| (2.1) |

We remark that sequences of such nodes and weights satisfying Assumption 2.1 have been given in many previous works, among others in [AJEE19a, AK21, BB23, Har19] (although (2.1) is usually not verified in these references, it is merely a rather weak and technical assumption). Also, as in [AJEE19a, Theorem 3.1], we have strong existence and uniqueness of the process , and non-negativity of .

We now recall some basic definitions and facts from [AJEE19a]. First, we define the characteristic function of the log-stock price as

Moreover, we note that can be given in semi-closed form as

| (2.2) |

where is defined by

| (2.3) |

and where is the solution to the fractional Riccati equation

| (2.4) |

with

By replacing the kernel with and defining and as in (2.3) and (2.4), respectively, we obtain a formula similar to (2.2) for the characteristic function of the log-stock price .

Our ultimate goal will be to prove a bound in terms of for the weak error of approximating by . To this end, we will first prove a local Lipschitz error bound for the characteristic function in terms of in Section 2.1. Then, in Section 2.2, we will use this error bound on to prove a weak error bound of .

2.1. Error bound for the characteristic function

The goal of this subsection is to prove the following theorem under Assumption 2.1.

Theorem 2.2.

For all there exists a constant such that for all and with and satisfying

| (2.5) |

we have

From here on, the values of the constant may change from line to line, but it is always independent of . Furthermore, for a complex number , we write for .

First, under Assumption 2.1, we have the following two propositions, similar to [AJEE19a, Theorem 4.1] and [AJEE19a, Proposition 5.4]. We remark that while [AJEE19a] uses much more restrictive assumptions than Assumption 2.1, it is not difficult to verify that their proves still go through with only minor adaptations.

Proposition 2.3.

There exists a constant such that for all and with and ,

Proposition 2.4.

There exists a constant such that for all and with and ,

Proposition 2.3 already suggests that the Markovian approximations might converge weakly at the same speed as , as in Theorem 2.2. To prove this theorem, we need some intermediary lemmas.

Lemma 2.5.

For all there exists a constant such that for all and with and satisfying

we have

Proof.

Since is a quadratic polynomial in the second variable, Proposition 2.3 and inequality (2.6) imply that also

Denote by the integral inside the exponential function. Since can be bounded on finite intervals,

| (2.7) |

We take , where is the final constant in (2.7). Since ,

Lemma 2.6.

For all there exists a constant such that for all and with and satisfying

we have

Proof.

The proof of this lemma is similar to the proof of Lemma 2.5. ∎

We can now proceed with the proof of Theorem 2.2.

2.2. Weak error bound for the log-stock price

We have proved that the error in the characteristic function can be bounded using . The next step will be to extend this result to the weak error in . To this end, let us introduce some notation related to the Fourier transform.

Given a function , we denote its generalized Fourier transform by

for all for which the above integral is well-defined. Furthermore, for , we define the damped function

Define the sets

| (2.8) |

where denotes the set of -functions that are bounded and continuous. We remark that we have Then, for each , we have the Fourier pricing formula

| (2.9) |

see e.g. [EGP10, Theorem 2.2]. Using this formula, we can prove the following theorem.

Theorem 2.7.

Let be a payoff function of the log-stock price, and let . Assume that there are such that

| (2.10) |

Then there exist constants independent of , such that if then, for ,

For , we get

Remark 2.8.

We remark that the proof of Theorem 2.7 only needs Theorem 2.2, and no further properties of rough Heston. In particular, let for be random variables, with characteristic functions , such that for all . Then, for any sequence such that Theorem 2.2 is satisfied, Theorem 2.7 holds. Moreover, the interval here and in Theorems 2.2 and 2.7 may be replaced by any subinterval of (where is defined as in (2.8)).

Proof of Theorem 2.7.

By (2.9), we have for all ,

We now bound these two summands separately. Considering the second summand first, we have

where a similar statement is true for . Moreover, note that Theorem 2.2 implies that

Hence, the second summand can be bounded by

Next, we want to bound the first summand using Theorem 2.2. Let be as in Theorem 2.2. and define

for some . Note that we have

In particular, for large enough , i.e. for sufficiently small, say

| (2.11) |

for some independent of , condition (2.5) of Theorem 2.2 is satisfied for all .

Hence, we can apply Theorem 2.2 to bound the first summand, and we have

Now, for ,

Similarly, for ,

Altogether, we get for (and )

with and similarly, for ,

This is almost the statement of the theorem, except that we need to get rid of the parameter . We do this by choosing an appropriate value of , where we restrict ourselves to . We may then sharpen requirement (2.11) to

We remark that for sufficiently small (i.e. for some ). Next, note that for , we have

and in particular (if additionally ),

Now, the requirements and are certainly satisfied for , proving this error bound in this regime.

Next, consider . In this case we still have , and we get

For , we may choose , finishing the proof in this case.

Finally, consider . Clearly, if the decay assumption on holds true for some , it is also true for , implying that for we also have the same bound as for . On the other hand, we may choose , which is admissible for such that . Thus, we get a bound of the form

This proves the corollary. ∎

Essentially, Theorem 2.7 is already what we wanted to show, in that it demonstrates that the weak error in the log-stock price can be bounded by . From here on, we merely want to polish this result. Mainly, we want to formulate the decay condition (2.10) in terms of the payoff function itself (Corollary 2.9), weaken or generalize the decay condition (Corollary 2.10), and to formulate the result in terms of payoffs of the stock price , rather than the log-stock price (Corollary 2.11). Finally, in Corollaries 2.12, 2.13 and 2.14, we give more transparent special cases.

First, we formulate the decay condition (2.10) on the Fourier transform in terms of the payoff function itself.

Corollary 2.9.

Let be a payoff function of the log-stock price, and let be an integer. Assume that is times weakly differentiable, and that there is and such that

Then, there exist constants independent of and , such that if then, for ,

For , we get

Proof.

Observe that we have

In particular, since we have

Moreover, in the same spirit as above, we have

This shows that

The corollary follows by an easy application of Theorem 2.7 once we show that , i.e. and . First, follows immediately from the assumptions. For the second condition, we merely note that ∎

In Corollary 2.9, the payoff needs to satisfy a very specific growth condition of the form for some . Since is a function of the log-stock price , this translates roughly to a polynomial growth condition of the form , where is the corresponding payoff function of the stock price . In general, this is a reasonable requirement, since may not exist for . This non-existence of the moments of the stock price is also referred to as moment-explosion, and has been studied e.g. in [GGP19] for the rough Heston model. However, depending on the parameters of the rough Heston model, the moments may exist for all . In Lemma A.1 in the appendix, we give some sufficient conditions for the existence of moments for some or .

In the following corollary, we want to extend Corollary 2.9 to allow also other growth conditions on the payoff function, depending on the existence of the moments . The statement below with all its parameters may look quite formidable, but all it says is that if the payoff function grows slightly slower than would be permitted for the existence of , and if the derivatives of up to some order grow at most exponentially fast (for ), then we can give a rate of convergence. More precisely, the parameters and should be interpreted as the largest and smallest moments of that exist, and denote how much slower grows than permitted by and , and and determine how fast the derivatives of grow. Furthermore, we apply Corollary 2.9 with the parameter . Since this Corollary is rather difficult to comprehend, we give some much simpler special cases in Corollaries 2.12, 2.13 and 2.14 below.

Corollary 2.10.

Let , let , and let . Let be a payoff function of the log-stock price, and let be an integer. Assume that is times weakly differentiable, and that there is , taking values in such that is locally bounded, and such that for all ,

| (2.12) | ||||

| (2.13) |

Then, there exist constants independent of , such that if then, for ,

| (2.14) |

where

and

The same result holds true for if we multiply the upper bound (2.14) by

Proof.

The proof is rather technical, so we only give the general idea. Fix some parameters . Let be a function that is times weakly differentiable such that for

| (2.15) | ||||

Finally, we formulate Corollary 2.10 in terms of payoff functions of the stock price .

Corollary 2.11.

Let , let , and let . Let be a payoff function of the stock price, and let be an integer. Assume that is times weakly differentiable, and that there is , taking values in such that is locally bounded and , and such that for all ,

Then, there exist constants independent of ( also independent of ), such that if then, for ,

where is as in Corollary 2.10, and

The same results hold true for if we multiply the upper bounds by

Proof.

We do not claim that the rate of convergence in Corollary 2.11 is necessarily best possible in general. However, the assumptions imposed on the payoff function are quite natural. They essentially amount to requiring that grows slightly slower than the largest moment of that exists. If this is the case we can give a specific convergence rate in .

Since Corollary 2.11 can be quite intimidating, we now give a few special cases.

Corollary 2.12.

Let be 8 times weakly differentiable and compactly supported. Then there is such that

Proof.

Choose , , , such that (by Lemma A.1), , , and , so that . We then get constants such that if , then

We can drop the restriction by noting that is uniformly bounded, and hence for ,

Corollary 2.13.

Let be a payoff function of the stock price that is twice weakly differentiable. Let and be such that , and assume that for and for . Assume furthermore that the first two derivatives of grow only polynomially in for and . Then there exist some such that

Proof.

This is really just a non-quantitative reformulation of Corollary 2.11. ∎

The following corollary has convenient assumptions that are usually satisfied in practice. It merely requires (global) Lipschitz continuity of the payoff, and the existence of a moment with . We remark that the convergence rate is of course very bad, and certainly not optimal. However, the purpose of this corollary is to demonstrate that the weak error can be bounded using the -error in the kernel, not just the -error.

Corollary 2.14.

Let be a Lipschitz continuous payoff function of the stock price, and let . Then, there exist constants independent of and , such that if , then

Remark 2.15.

The condition can be removed by a localization argument similar to Corollary 2.12 using Lipschitz continuous approximations with compact support, at the cost of a worse convergence rate.

Proof.

Since is Lipschitz continuous, the limit certainly exists. Furthermore, by replacing with , we may assume without loss of generality that . Denote by the Lipschitz constant of .

Now, assume for a moment that is additionally twice weakly differentiable with bounded derivatives. Let be the supremum norm on and . In Corollary 2.11, set , , , , , , , . Then, there exist constants independent of , such that if then,

Next, we define a sequence of twice weakly differentiable functions approximating . The functions are defined via their second weak derivative , together with the initial conditions . The function is given by

It is easily verified that

where is the Lipschitz-norm of .

Therefore, we get

Setting

we get

3. -approximation of the fractional kernel

The aim of this section is to give kernels of the form (1.6), such that

converges quickly for We give two different approximations in Sections 3.1 and 3.2, respectively. Throughout, we will make heavy use of the representation of in terms of its inverse Laplace transform, i.e.,

| (3.1) |

3.1. Geometric Gaussian approximations

Let us now define the approximations we use, which deviate slightly from the approximations in [BB23]. We denote by the function rounding to the nearest positive integer.

Definition 3.1 (Geometric Gaussian Rules).

Let be the total number of nodes and be parameters of the scheme. Define

| (3.2) |

Let be the nodes and be the weights of a Gaussian quadrature formula of level on the interval with the weight function . Furthermore, let be the nodes and be the weights of a Gaussian quadrature formula of level on to the intervals for with the weight function . Then we define the geometric Gaussian rule of type to be the set of nodes with weights defined by

The approximation of is then given by

In what follows we will often drop the function in (3.2) and assume that and can be real numbers, and that exactly, purely for convenience. This does not affect the convergence rates.

Remark 3.2.

In geometric Gaussian rules, we have four parameters that we can freely choose: . These parameters can be interpreted as follows:

-

•

The parameter determines the cutoff point of the integral in (3.1), i.e. we approximate the integral only on the interval .

-

•

The parameter determines the level of the Gaussian quadrature rule.

-

•

The parameter determines the size of the first interval . This interval is special due to the singularity in the weight function .

-

•

The parameter is used for fine-tuning the results.

In particular, parameter is mainly responsible for controlling the error in our approximation on the interval , parameter is mainly responsible for controlling the error on , and parameter is mainly responsible for controlling the error on .

Throughout this section, we will use the following proposition. It states that Gaussian quadrature is lower-biased for completely monotone functions.

Proposition 3.3.

Let be completely monotone, and let be the nodes and be the weights of Gaussian quadrature with respect to the weight function . Then,

Proof.

This follows immediately from Theorem D.1, using that derivatives of even order of completely monotone functions are non-negative. ∎

We now start with the proof of the convergence rate, by stating a lemma on the error of Gaussian quadrature. This is a sharpened version of [Tre19, Theorem 19.3] for the specific function . The proof is very technical, and delegated to Appendix C.

Lemma 3.4.

Let where , and . Let be the nodes and be the weights of Gaussian quadrature of level on with weight . Define , assume that set and Then,

where

Recall the representation (3.1) of . In the following Lemmas, we split up the error of Gaussian quadrature on the interval into several smaller intervals that we treat separately. More precisely, in Lemma 3.5, we consider intervals with , in Lemma 3.6 the interval , in Lemma 3.7 the interval , and in Lemma 3.8 the interval . Finally, we will combine all these error bounds in Theorem 3.9.

Lemma 3.5.

Let , and . Let be the nodes and be the weights of the Gaussian quadrature of level on the interval with weight function . Then,

where , , and , and are as in Lemma 3.4.

Proof.

Since the function is completely monotone, Proposition 3.3 implies that

This is obviously the error of Gaussian quadrature for the function on the interval . By a simple linear transformation and Lemma 3.4, we get the result. ∎

To simplify, we only prove asymptotic bounds from now on. More precisely, if we write , then we mean , so that leading constants remain valid.

Lemma 3.6.

Let be the nodes and be the weights of a geometric Gaussian rule with parameters , , and , cf. Definition 3.1. Assuming , we have

where

Proof.

Denote , and . Applying the triangle inequality for the intervals with , and using Lemma 3.5, we get

| (3.3) |

where

and , , and and where we assume that

Consider first the sum in (3.3). Since , we have

| (3.4) |

Next, we want to determine the rate at which (3.3) decays. Heuristically, it seems that the rate is mainly determined by the term . Note that

where , for . Let us hence consider the expression Here, depends on and , while depends on , so with this simplification we have removed the dependence of the rate on the parameters and . Recalling Remark 3.2, we want to choose a good value of (i.e. a good degree of the Gaussian quadrature rule) to make the error as small as possible. Therefore, we consider the optimization problem

After some manipulations, we see that minimizing this is equivalent to minimizing

Perhaps surprisingly, this can be optimized in closed form, and the solution is

This implies

Moreover, for all ,

Using this bound, and (3.4), we get

It is now that we start using asymptotic bounds. As , we have . Since , we have , , , and . Plugging in these values, we get the bound in the statement of the theorem. After noting that is satisfied for all , this proves the lemma. ∎

We have now estimated the approximation error on the interval . Next, we consider the interval .

Lemma 3.7.

Let be the nodes and be the weights of Gaussian quadrature of level on the interval with respect to the weight function with . Assume . Then,

Proof.

Since is a completely monotone function, Proposition 3.3 implies that

This is obviously the Gaussian quadrature error of the function

on the interval with respect to the weight function . In particular, because Gaussian quadrature integrates exactly polynomials up to degree , instead of we may consider

If

Hence, for , we have (due to the positivity of the weights)

Finally, the following formula for the approximation error on is trivial.

Lemma 3.8.

We have

Proof.

This follows immediately using Fubini’s theorem with

We are finally able to state the following result on the convergence rate of the Gaussian approximations.

Theorem 3.9.

Let be the nodes and be the weights of the geometric Gaussian rule with , , , and . Then,

| (3.5) |

If instead we choose then,

| (3.6) |

Remark 3.10.

We decided to give two different bounds depending on the choice of the parameter in the theorem above. While the latter bound obviously yields the ever so slightly better convergence rate, the former bound may be more convenient in theoretical applications. This is because in the latter bound, the largest node has an additional polynomial factor of growth that is not present in the former bound. Hence, using the latter bound in theoretical applications may lead to additional annoying logarithmic error terms that can be avoided by using the former bound.

Proof.

We only prove (3.5), the proof of (3.6) being similar. By the triangle inequality, and Lemmas 3.7, 3.6, and 3.8,

where is the constant from Lemma 3.6, and where we assume that , , , and .

Let us now choose such that

in order to ensure that the latter two terms converge at the same speed. It is clear that this is achieved for

Next, we want to ensure that the first summand converges at the same speed as the other two. Using Stirling’s formula, we have

To ensure a similar speed of convergence, we need

Obviously, for this choice of we have . Furthermore, we now have

Assuming that we choose constant (i.e. independent of ), such that , we see that only the last summand in the above bound is relevant, due to the polynomial terms in . Indeed, since for some it is not hard to see that we have both

3.2. Non-geometric Gaussian approximations

We will try to further improve the results of Section 3.1 by choosing non-geometrically spaced intervals .

Definition 3.11 (Non-geometric Gaussian Rules).

Let be the total number of nodes and be parameters of the scheme, where . We define

| (3.7) |

Here, we assume that for all , which is true if we choose large enough. Define to be the nodes and to be the weights of Gaussian quadrature of level on the interval with the weight function . Furthermore, let be the nodes and be the weights of Gaussian quadrature of level on to the intervals for with the weight function . Then we define the non-geometric Gaussian rule of type to be the set of nodes with weights defined by

Remark 3.12.

Non-geometric Gaussian rules have three free parameters: . They can be interpreted as follows.

-

•

The parameter determines the cutoff point of the interval in (3.1), similar to the parameter in geometric Gaussian rules. It is hence mainly used to control the error on .

-

•

The parameter determines the degree of the Gaussian quadrature rule, similar to the parameter in geometric Gaussian rules. It is hence mainly used to control the error on .

-

•

The parameter determines the size of the interval , which is again special due to the singularity in the weight function . Similarly to the parameter in geometric Gaussian rules, it is mainly used to control the error on .

Finally, we remark that the reason for the specific definition of in (3.7) will become apparent in the proof of Lemma 3.13. Furthermore, the parameters will not depend on in our proofs.

The following lemma is the equivalent of Lemma 3.6 for non-geometric Gaussian rules. It bounds the error of the quadrature rule on .

Lemma 3.13.

Let be the nodes and be the weights of a non-geometric Gaussian rule. Then,

where , , , and and where we assume that for .

Proof.

While Lemma 3.13 is the equivalent of Lemma 3.6 for non-geometric Gaussian rules to bound the error on , Lemma 3.7 for the error on and Lemma 3.8 for the error on can be reused exactly. The only difference to the geometric Gaussian rules is that we do not have an explicit formula for , but merely the recursion (3.7). However, the size of is needed to determine the error contribution on in Lemma 3.8. Hence, in the following lemma we determine the approximate size of for non-geometric Gaussian rules.

Lemma 3.14.

Let be the solution of the ODE

| (3.8) |

Note that has a finite explosion time . The following two statements are equivalent.

-

(1)

The explosion time , i.e. .

-

(2)

There exists such that for sufficiently large we have

(3.9)

If one of these conditions is satisfied, then

Remark 3.15.

We need to have to ensure that the non-geometric Gaussian rule is well-defined, cf. (3.7). This lemma hence gives a semi-explicit asymptotic formula for if we satisfy this condition even with an additional of leeway.

Proof.

Define and assume that is large. Recall that

Set Then,

This is almost the Euler discretization of the ODE (3.8), whose solution we denote by .

If we now have the uniform bound , clearly also remains uniformly bounded in . In particular, we may assume that the vector field in (3.8) is bounded (for ), and we have the convergence

The error will of course depend on . Furthermore, this also implies that , and hence .

Conversely, assume that , and for now, assume also . Since the vector field governing is increasing and non-negative, the Euler discretization is lower-biased. This implies in particular that . If , then there exists with Clearly, as . Again since the Euler scheme is lower-biased, we have

where the second inequality holds for sufficiently large. Therefore,

where the last (strict!) inequality holds, since the explosion time is exactly at Thus, since the inequality is strict, and since is independent of , we can find a uniform satisfying (3.9).

Finally, assume that one of these two conditions (and hence both) are satisfied. Then, we prove the asymptotic formula for . Due to the boundedness of the vector field (since ), we have that the solution of the ODE is Lipschitz in the initial condition and in the driving vector field. Now, , , and , implying that we have

where satisfies Therefore,

We can now proceed with the proof of the error bound for non-geometric Gaussian rules.

Theorem 3.16.

Define the constants and Let be a Gaussian approximation coming from a non-geometric Gaussian rule with parameters , , and , where or . Then,

In the first inequality, the higher order terms explode as , and in the second inequality, the leading constant explodes for the same limit. Furthermore, we have

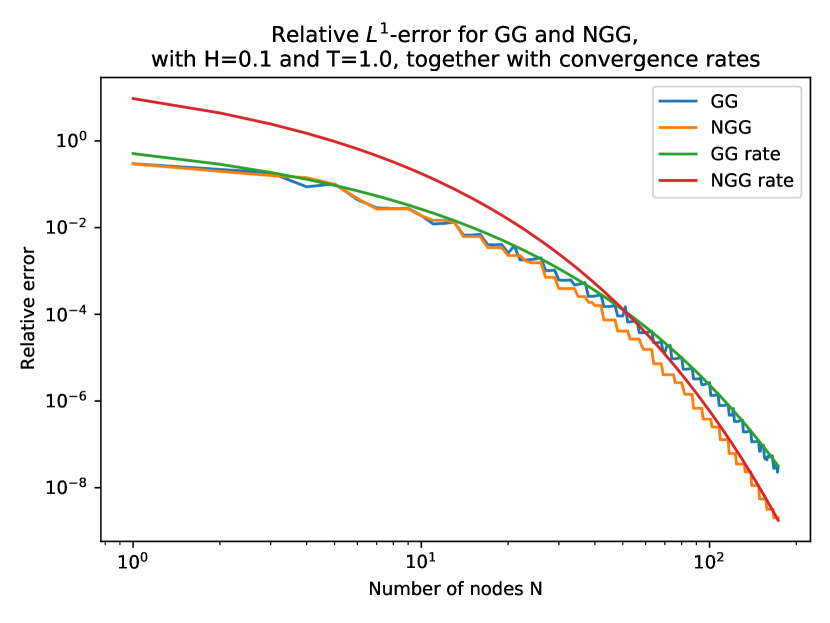

In Figure 1 we compare the convergence rates of our results with the previously achieved strong convergence rate in [BB23, Theorem 2.1].

Proof of Theorem 3.16.

Assume for now that the conditions of Lemma 3.14 are satisfied, i.e. the explosion time of in (3.8) satisfies . Then we can apply the triangle inequality on the intervals , , and , and apply Lemmas 3.7, 3.13, 3.8 and 3.14, to get

| (3.10) |

where , , , , and and where we assume that

The first summand in this bound converges factorially fast (for independent of ), and will hence be of no further concern. On the other hand, we want that the second and the third summand converge at the same speed. Hence, we wish to solve the optimization problem

This is equivalent to

| (3.11) |

The solution can be numerically computed to be

For these values, we have

However, we still need to ensure that . In fact, for the choice , it is not hard to see that this condition will likely be violated. Indeed, recall that the explosion happens exactly when or equivalently, when . But this is precisely the constraint in the optimization problem (3.11) with . Therefore, Lemma 3.14 is in fact not applicable for . This can be remedied by choosing or slightly larger. Indeed, note that the vector field in (3.8) is strictly decreasing in both and , and hence, is strictly increasing. Therefore, if , , and or , then , and our application of Lemma 3.14 was valid.

What does this choice of and mean for the convergence rate of the kernel error? Recall that was the solution to the optimization problem where we wanted to optimize over the convergence rate subject to the constraint that the second and third summand in (3.10) converge at the same speed. If we now increase or , then the second term will converge faster, while the third term will converge more slowly. We can further quantify this by stating that

for some small depending on .

We have now almost shown that the second term in (3.10) converges faster than the third term, and that we can hence (asymptotically) ignore it. However, we still need to treat the constants in front, to ensure that they do not cause additional troubles as . Indeed, one can show that

Altogether, this shows the bound

Finally, we note that only the error on the interval remains in the above bound, the errors on the other intervals having converged with higher order. Therefore, we also have

4. Numerics

Throughout this section, we compare the approximations of given in Section 3 with previously proposed methods. We demonstrate the efficiency of the geometric and non-geometric Gaussian rules for the pricing of various options under the rough Heston model, but we also indicate possible ways how these theoretically derived rules can be further improved numerically. With that in mind, below is a list of the quadrature rules we compare for approximating by .

-

(1)

“GG” (Geometric Gaussian quadrature): This is the quadrature rule from Theorem 3.9 with and .

-

(2)

‘’NGG” (Non-Geometric Gaussian quadrature): This is the quadrature rule from Theorem 3.16 with , , and .

-

(3)

“OL1” (Optimal -error): This is the quadrature rule we get by optimizing the -error between and . We use the intersection algorithm outlined in Appendix E for computing the -errors.

-

(4)

“OL2” (Optimal -error): This is the quadrature rule we get by optimizing the -error between and . We use [BB23, Proposition 2.11] for computing -errors.

-

(5)

“BL2” (Bounded -error): This quadrature rule essentially minimizes the -error between and , but penalizes large nodes . A more precise description of the algorithm underlying this quadrature rule can be found in Appendix F.

-

(6)

“AE” (Abi Jaber, El Euch): This is the quadrature rule suggested in [AJEE19a, Section 4.2].

- (7)

We note that the algorithms OL2, AK, and BL2 focus on minimizing the -error, while the algorithms GG, NGG, OL1, AE focus on the -error. Since the -norm of is infinite for , the -algorithms can only be applied for positive . In contrast, the -algorithms work for all . Perhaps surprisingly, BL2 still works for negative despite minimizing the -norm, since we penalize large mean-reversions, which corresponds to a smoothing of the singularity of the kernel, see also Appendix F.

Throughout this section we compute option prices under rough Heston using Fourier inversion, since the characteristic function of the log-stock price in (1.1) is known in semi-closed form see e.g. [AJLP19]. The same is true for the characteristic function of the Markovian approximation obtained by replacing by , see e.g. [AJEE19]. For the computation of , we need to solve a fractional Riccati equation. This is done using the Adam’s scheme, see e.g. [DFF04]. To obtain , we need to solve an ordinary (-dimensional) Riccati equation. This is done using a predictor-corrector scheme, as explained in [AJEE19a, BB23]. We remark that generally speaking, Fourier inversion of the Markovian approximation tends to be faster, as we only have to solve an ordinary (higher-dimensional) Riccati equation, which has a cost of , where is the number of time steps. In contrast, solving the fractional Riccati equation, which is a Volterra integral equation, has a cost of . This difference is especially pronounced if we need to compute prices with high accuracy, small maturity, or tiny (especially negative) Hurst parameter .

This numerical section is structured as follows. First, we compare the computational cost of computing all these quadrature rules, as well as their largest nodes in Section 4.1. Next, in Section 4.2 we verify that the weak error can indeed be bounded by the -error in the kernel as shown in Section 2, rather than the -error, by conducting some specific comparisons of the algorithms OL1 and OL2. In Section 4.3 we numerically verify the convergence rates of the -errors between and that we proved in Section 3, and compare these rates with the other algorithms. Finally, in Section 4.4, we compute various option prices and verify stylized facts and properties of the rough Heston model and its Markovian approximations. This includes implied volatility smiles in Section 4.4.1, implied volatility surfaces in Section 4.4.2, implied volatility skews in Section 4.4.3, and finally, prices of digital European call options in Section 4.4.4, where we want to illustrate that the Markovian approximations still converge quickly despite the lack of regularity in the payoff function that is required in Section 2.

4.1. Computational Times and Largest Nodes

Before discussing convergence rates below, let us compare two important quantities associated with these quadrature rules: computational time and the largest nodes.

First, the time it took to compute the quadrature rules for the various algorithms was largely independent of the Hurst parameter . For the quadrature rules GG, NGG, OL2, AE and AK, the computation is basically instant, taking at most a few ms. BL2 is still quite fast, with computational times ranging from a few ms (for ) to a few seconds (for ). Finally, OL1 is the most expensive, where computing for already takes about 15 min.

The largest node gives us some insight into how well the singularity of the kernel is captured. If a quadrature rule with small nodes performs very well, this may indicate that the singularity (and hence the roughness of the volatility) is not very important for that particular problem, and vice versa. Also, quadrature rules with small nodes are typically preferable over ones with large nodes (if they perform equally well), as larger nodes might lead to more problems of numerical stability and higher computational times. It will turn out that this is not a particularly severe problem for European options as we consider them, but it is much more relevant if one decides to simulate paths using the Markovian approximation, see also [BB].

The largest nodes are given in Table 1. We see that quadrature rules that aim to minimize the -error (i.e. OL2, AK) reach very large nodes for small . Compared to that, the largest nodes seem to remain bounded for for quadrature rules that aim to minimize the -error (i.e. GG, NGG, OL1, AE). Interestingly, BL2 also has bounded nodes for small , with largest nodes of similar sizes as for OL1.

| N | GG | NGG | OL1 | BL2 | AE | GG | NGG | OL1 | OL2 | BL2 | AE | AK | GG | NGG | OL1 | OL2 | BL2 | AE | AK |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 0.18 | 0.05 | 0.24 | 0.24 | -0.46 | 0.12 | 0.00 | 0.14 | 0.87 | 0.87 | -0.53 | - | 0.06 | -0.07 | 0.02 | 0.34 | 0.34 | -0.62 | - |

| 2 | 1.17 | 0.95 | 1.40 | 1.35 | 0.08 | 1.02 | 0.95 | 1.28 | 6.83 | 1.43 | 0.05 | 3.32 | 0.92 | 0.95 | 1.18 | 2.56 | 0.94 | 0.03 | 1.48 |

| 3 | 1.59 | 1.70 | 2.24 | 2.08 | 0.27 | 1.39 | 1.70 | 2.07 | 12.2 | 1.83 | 0.25 | 3.32 | 1.25 | 1.70 | 1.93 | 4.28 | 1.67 | 0.22 | 1.48 |

| 4 | 1.94 | 2.49 | 2.98 | 2.80 | 0.39 | 1.70 | 2.49 | 2.75 | 17.3 | 2.43 | 0.37 | 7.10 | 1.58 | 2.49 | 2.57 | 5.77 | 2.24 | 0.34 | 3.13 |

| 5 | 2.24 | 3.32 | 3.66 | 3.45 | 0.48 | 2.02 | 3.32 | 3.35 | 36.7 | 3.02 | 0.46 | 7.10 | 1.81 | 1.09 | 3.14 | 7.11 | 2.81 | 0.43 | 3.13 |

| 6 | 2.57 | 4.16 | 4.24 | 4.10 | 0.55 | 2.26 | 1.86 | 3.91 | 44.0 | 3.52 | 0.53 | 11.5 | 2.04 | 1.86 | 3.65 | 8.34 | 3.32 | 0.50 | 4.40 |

| 7 | 2.82 | 2.66 | 4.79 | 4.67 | 0.61 | 2.48 | 2.66 | 4.42 | 31.1 | 4.15 | 0.59 | 11.5 | 2.24 | 2.66 | 4.28 | 9.48 | 3.77 | 0.56 | 4.40 |

| 8 | 3.04 | 2.66 | 5.32 | 5.17 | 0.66 | 2.68 | 2.66 | 4.90 | 35.5 | 4.54 | 0.64 | 15.5 | 2.42 | 2.66 | 4.58 | 10.5 | 4.52 | 0.61 | 5.45 |

| 9 | 3.24 | 2.66 | 6.03 | 5.62 | 0.70 | 2.86 | 2.66 | 5.35 | 39.7 | 4.90 | 0.69 | 15.5 | 2.58 | 2.66 | 5.20 | 11.6 | 4.90 | 0.66 | 5.45 |

| 10 | 3.44 | 3.49 | 6.65 | 6.03 | 0.74 | 3.04 | 3.49 | 6.02 | 43.9 | 5.25 | 0.72 | 20.0 | 2.75 | 3.49 | 5.74 | 12.5 | 5.27 | 0.70 | 6.35 |

4.2. Comparing OL1 with OL2

We have shown in Section 2 that the weak error of the Markovian approximations of the rough Heston model can be bounded by the -error in the kernel. This suggests, in contrast to e.g. the work in [BB23] that if we want to price options using the Markovian approximations, we may want to focus on minimizing the -error in the kernel, instead of the -error, i.e. should use the algorithm OL1 rather than OL2. The difference becomes especially pronounced for very small , as in that case, is barely square-integrable. Furthermore, weak formulations of rough Heston are possible in the regime of , see e.g. [AJ21, AJDC23, JR20].

In the following figures we aim to show that the error of approximating European call option implied volatility smiles indeed decreases rapidly as the number of nodes in the kernel increases, if those nodes are chosen such that the -error in the kernel is minimized. We compare these results with using the kernel resulting from minimization of the -error.

Throughout, we consider European call options with the same parameters as in [AJEE19a, Section 4.2], i.e.

We choose 201 values for the log-moneyness linearly spaced in the interval . The implied volatility smiles of the true (i.e. non-approximated) rough Heston model are computed using Fourier inversion with the Adams scheme, see e.g. [DFF04]. The implied volatility smiles for the Markovian approximations are computed using a similar predictor-corrector scheme, see e.g. [AJEE19a, BB23]. All implied volatility smiles were computed with a maximal relative error of .

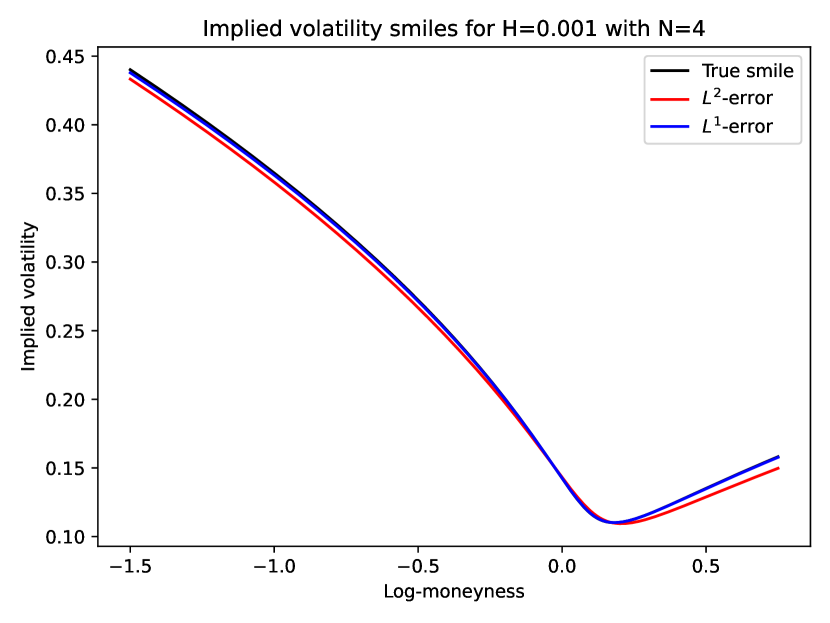

The left plot of Figure 2 compares the implied volatility smiles for the European call option with a tiny , and using nodes. The Markovian approximation using the -optimized kernel (blue) is directly over the true rough Heston smile (black). The approximation using the -optimized kernel (red) is still a bit off. Moreover, it will converge only very slowly to the black line, as is illustrated in the right plot of Figure 2. Here, we see how the errors in the implied volatility smiles decrease very rapidly for the -approximation as increases, even for tiny (or negative) . In contrast, while the -approximation still achieves good results for large enough, we see that the convergence rate is very slow for tiny . The precise values of the errors are given in Table 2.

| minimizing | minimizing | |||||||

| 1 | 16.58 | 12.33 | 9.281 | 6.961 | 4.986 | 7.678 | 0.897 | 0.778 |

| 2 | 6.675 | 4.297 | 2.833 | 1.879 | 1.192 | 6.541 | 0.606 | 0.464 |

| 3 | 3.396 | 1.935 | 1.133 | 0.672 | 0.382 | 5.835 | 0.525 | 0.255 |

| 4 | 1.908 | 0.975 | 0.515 | 0.278 | 0.144 | 5.317 | 0.412 | 0.139 |

| 5 | 1.130 | 0.517 | 0.256 | 0.127 | 0.061 | 4.874 | 0.313 | 0.076 |

| 6 | 0.713 | 0.303 | 0.135 | 0.062 | 0.023 | 4.513 | 0.234 | 0.042 |

| 7 | 0.462 | 0.181 | 0.064 | 0.032 | 0.014 | 4.276 | 0.175 | 0.024 |

| 8 | 0.306 | 0.111 | 0.043 | 0.018 | 0.005 | 4.022 | 0.130 | 0.014 |

| 9 | 0.208 | 0.060 | 0.021 | 0.007 | 0.002 | 3.798 | 0.097 | 0.008 |

| 10 | 0.127 | 0.035 | 0.011 | 0.004 | 0.001 | 3.596 | 0.072 | 0.004 |

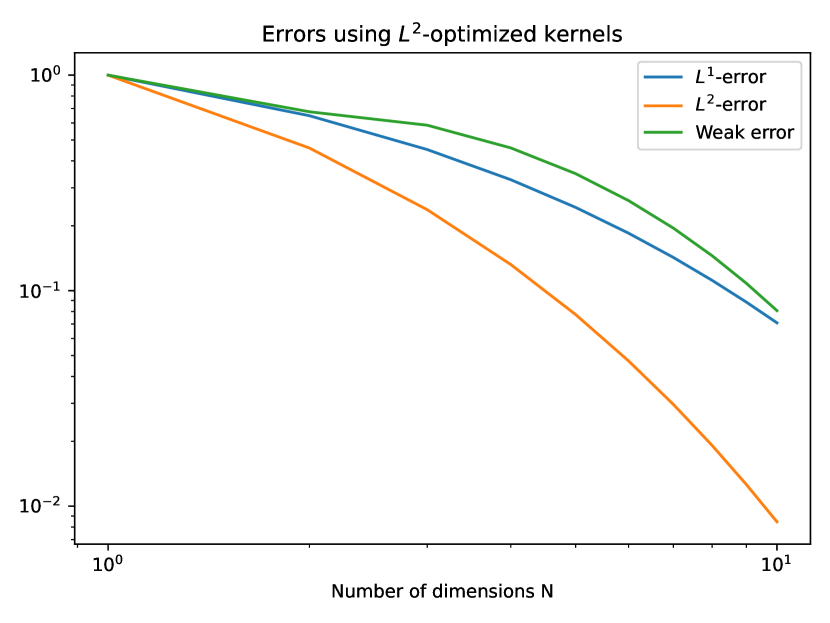

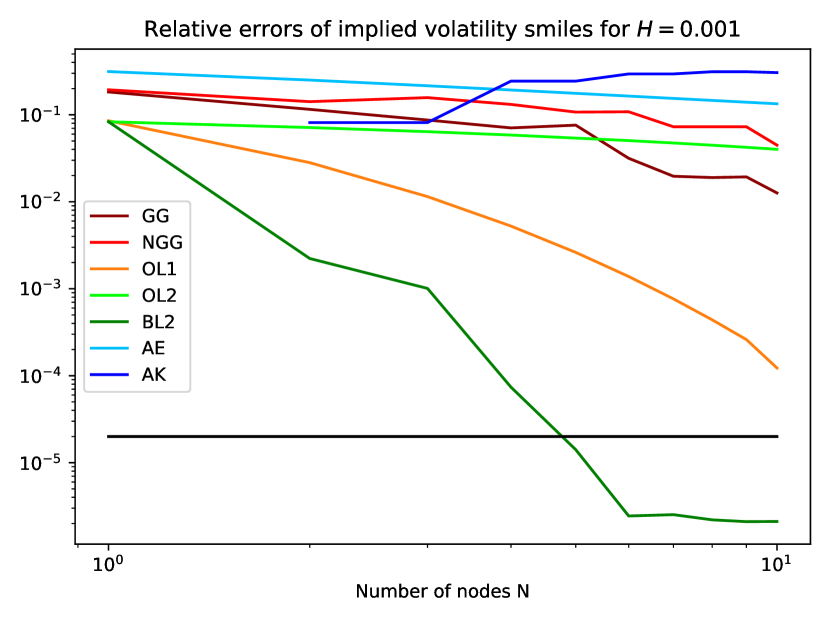

Finally, we want to demonstrate that the error of the implied volatility smiles indeed converges at the same rate as the -error of the kernels. To this end, we fix the Hurst parameter , and compute the -errors and the -errors of the kernels, as well as the maximal errors of the volatility smiles for kernels minimizing the -error or the -error . The results are illustrated in Figure 3. Note that the errors of the implied volatility smiles decrease roughly at the same speed as the -errors of the kernels, consistent with our theoretical results.

4.3. -error in the kernel

In this section, we want to numerically verify our that the -errors of GG and NGG converge super-polynomially, and that their convergence rate does not become arbitrarily bad for small .

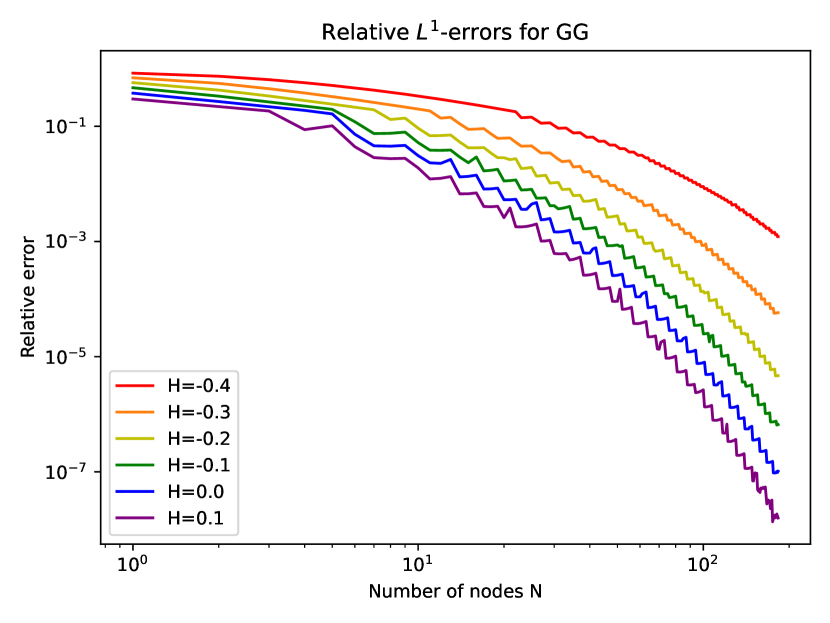

In the left plot of Figure 4 we see the relative -errors for GG and NGG for and . We clearly see that both exhibit super-polynomial convergence. Furthermore, this figure includes lines representing the convergence rates in Theorems 3.9 and 3.16 (with suitably fitted leading constants), showing that the errors converge at the rate that we proved there. The right plot of Figure 4 shows that the convergence rates do not become arbitrarily bad for tiny , and only significantly worsens once we approach . We remark that the error lines are wiggly due to the discrete choice of the level of the Gaussian quadrature rule.

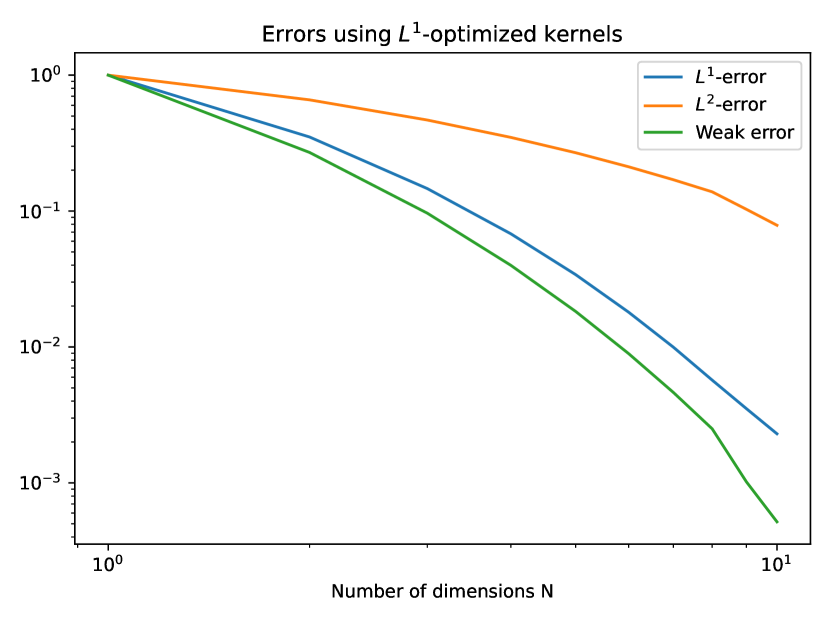

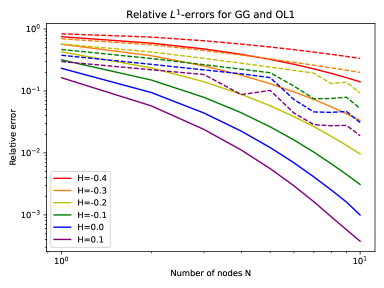

Finally, for small , we compare GG with OL1. In Figure 5 we show that there still is significant room for improvement. The figure only goes up to because of the high computational cost of computing -errors, cf. Section 4.1.

4.4. Weak convergence of the stock price

In this section we numerically investigate the weak convergence of the Markovian approximations of the rough Heston model. Throughout, we use the same parameters as in [AJEE19a, Section 4.2], i.e.

As mentioned before, we carry out all these computations using Fourier inversion. This introduces discretization errors for both the approximation of the Fourier inversion integral, and the numerical solution of the (fractional) Riccati equations needed for the characteristic function. Since we are not interested in the behaviour of these discretization errors, we will always try to keep them very small. Our implementation of the Fourier inversion (both the Adams scheme and the Markovian approximations) takes an error tolerance TOL and returns option prices or implied volatilities that were computed with a combined relative error of the Fourier inversion and the Riccati equations that is less than TOL. The specific choice of TOL will vary depending on the option we consider, and will always be stated explicitly.

4.4.1. Implied volatility smiles for European call options

First, let us consider call options with 301 different values of log-moneyness linearly spaced in the interval , where we set the maturity , and . We compute these smiles using Fourier inversion with a relative accuracy of at least for , and for (due to the higher computational cost associated with smaller ).

Indeed, especially for high-accuracy computations with tiny or , the computational times can become very large. However, the Adams scheme is more affected by this than the Markovian approximations. For example, the computation of the smile for with relative accuracy took 6183 seconds using the Adams scheme, while the Markovian approximations took – seconds, depending on and the quadrature rule used. This is because in both cases, we need to solve a Riccati equation to compute the characteristic function, and this is a fractional Riccati equation for the Adams scheme, while it is an ordinary (-dimensional) Riccati equation for the Markovian approximations. The numerical solution of a fractional Riccati equation has a computational cost of for time steps, compared to for ordinary Riccati equations. This difference becomes especially pronounced for large , which is needed for high accuracy, and when and are small.

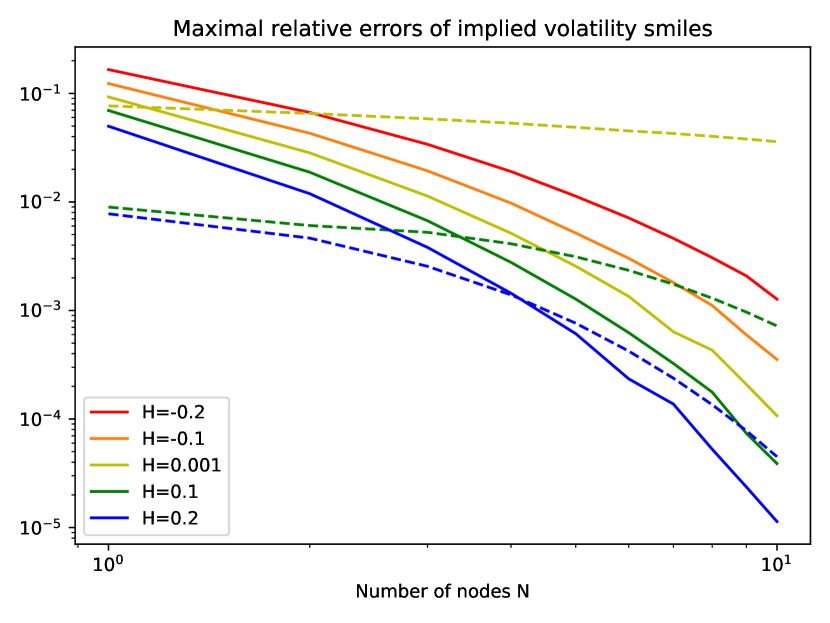

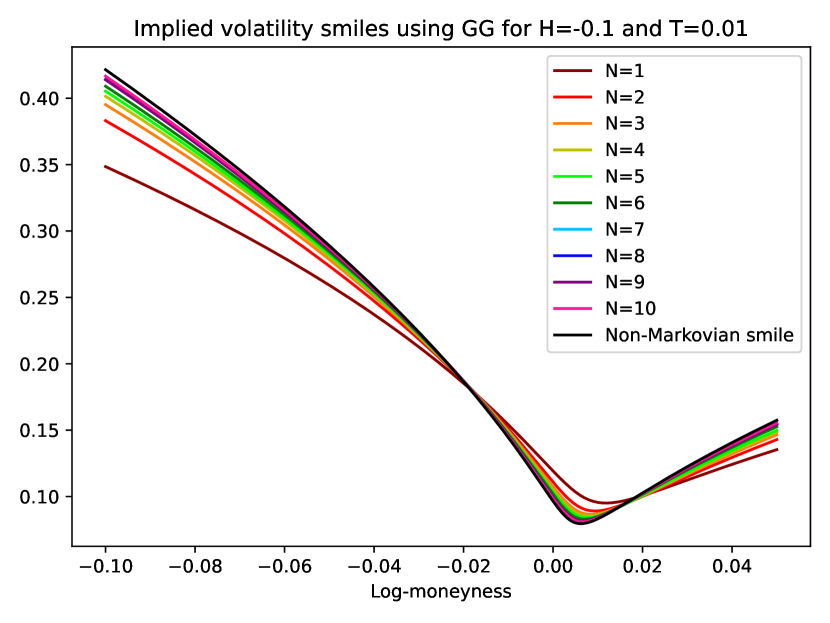

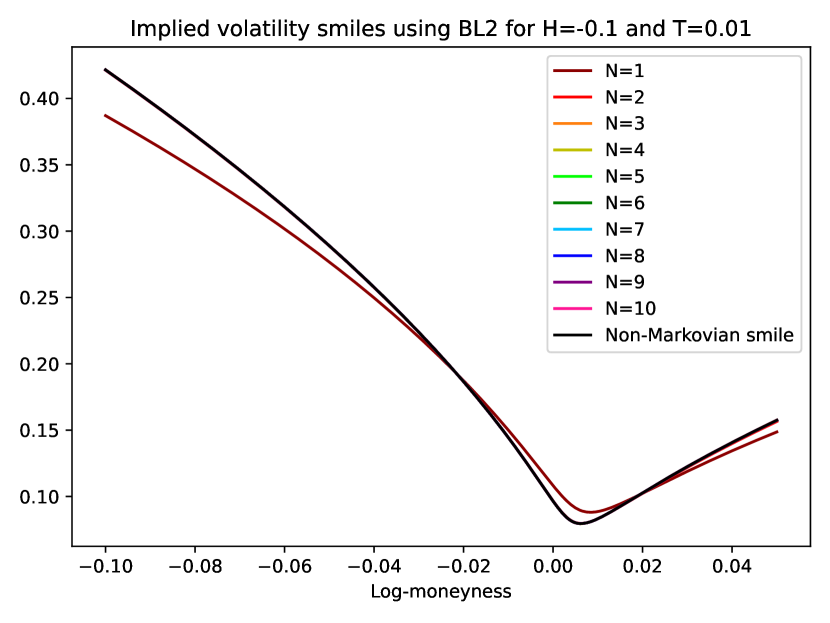

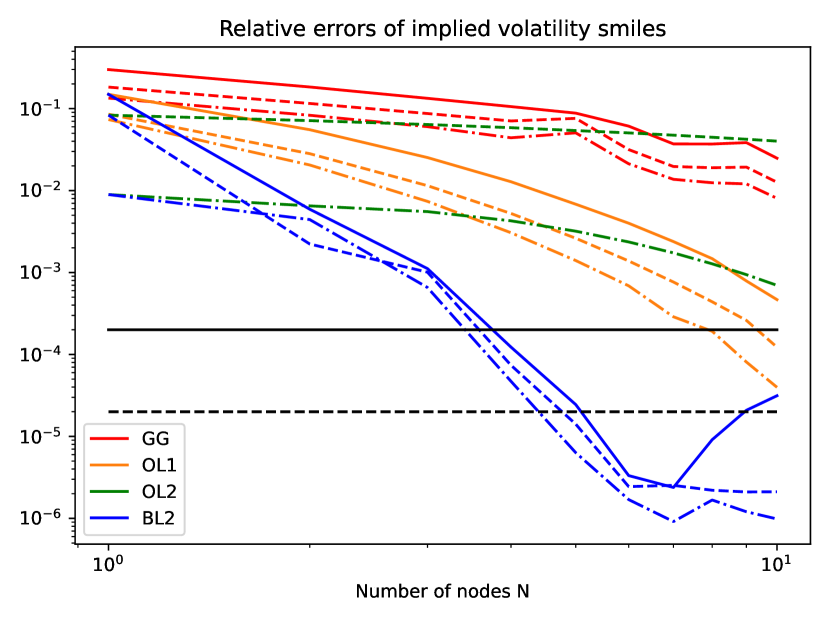

In Figure 6 we see the approximations using GG and BL2 quadrature rules for the implied volatility smile with . We see that already a very small number of nodes is sufficient to achieve a high accuracy. Indeed, for BL2 already is sufficiently accurate that we cannot see the any difference to the exact, non-approximated smile anymore without zooming in.

In Table 3 we see the maximal relative errors of the implied volatility smiles in . As expected, quadrature rules relying on the -error (i.e. OL2, AK) perform very badly for tiny (and are not well-defined for negative ), while quadrature rules relying on the -error (i.e. GG, NGG, OL1, AE) still work well even for . The exception here is BL2, which, despite optimizing the (penalized) -error outperforms every other method by multiple magnitudes, even for tiny or negative . We study this phenomenon a bit further in Appendix F. Aside from that, both GG and NGG seem to clearly outperform AE, with GG yielding better results. We guess that for sufficiently large , NGG will outperform GG, but such large are likely not necessary for usual applications. Also, there is still a lot of room for improvement, as OL1 (and of course BL2) show.

In Figure 7 we compare all the methods. In the left figure, we see that algorithms using the -error show almost no convergence, while BL2 significantly outperforms all other algorithms. In the right figure, we see that the error does not deteriorate too much for GG, OL1, and BL2 as becomes small or negative, while it does for OL2.

| N | GG | NGG | OL1 | BL2 | AE | GG | NGG | OL1 | OL2 | BL2 | AE | AK | GG | NGG | OL1 | OL2 | BL2 | AE | AK |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 29.93 | 31.86 | 14.93 | 14.93 | 49.44 | 18.29 | 19.38 | 8.538 | 8.315 | 8.315 | 31.40 | - | 13.43 | 14.77 | 7.348 | 0.894 | 0.894 | 24.36 | - |

| 2 | 18.35 | 21.82 | 5.526 | 0.591 | 39.77 | 11.55 | 14.16 | 2.818 | 7.133 | 0.223 | 25.07 | 8.138 | 8.288 | 10.67 | 2.050 | 0.650 | 0.442 | 20.07 | 1.112 |

| 3 | 13.35 | 23.46 | 2.527 | 0.112 | 34.46 | 8.704 | 15.75 | 1.147 | 6.394 | 0.101 | 21.56 | 8.138 | 6.017 | 12.31 | 0.738 | 0.553 | 0.066 | 17.60 | 1.112 |

| 4 | 10.58 | 20.14 | 1.281 | 0.012 | 31.01 | 7.066 | 13.16 | 0.525 | 5.848 | 0.007 | 19.28 | 24.38 | 4.405 | 9.812 | 0.306 | 0.427 | 0.005 | 15.92 | 2.004 |

| 5 | 8.802 | 15.84 | 0.681 | 0.002 | 28.56 | 7.599 | 10.74 | 0.262 | 5.395 | 0.001 | 17.65 | 24.38 | 5.058 | 6.501 | 0.140 | 0.319 | 0.001 | 14.67 | 2.004 |

| 6 | 6.109 | 13.38 | 0.399 | 0.000 | 26.72 | 3.161 | 10.83 | 0.138 | 5.051 | 0.000 | 16.41 | 29.50 | 2.121 | 9.107 | 0.069 | 0.236 | 0.000 | 13.68 | 1.659 |

| 7 | 3.707 | 11.78 | 0.238 | 0.000 | 25.27 | 1.965 | 7.282 | 0.077 | 4.740 | 0.000 | 15.43 | 29.50 | 1.371 | 5.525 | 0.029 | 0.174 | 0.000 | 12.88 | 1.659 |

| 8 | 3.697 | 11.78 | 0.147 | 0.001 | 24.07 | 1.898 | 7.282 | 0.044 | 4.469 | 0.000 | 14.63 | 31.27 | 1.245 | 5.525 | 0.019 | 0.128 | 0.000 | 12.21 | 0.999 |

| 9 | 3.844 | 11.78 | 0.079 | 0.002 | 23.07 | 1.932 | 7.282 | 0.026 | 4.228 | 0.000 | 13.95 | 31.27 | 1.206 | 5.525 | 0.008 | 0.094 | 0.000 | 11.64 | 0.999 |

| 10 | 2.482 | 7.052 | 0.047 | 0.003 | 22.22 | 1.263 | 4.476 | 0.012 | 4.010 | 0.000 | 13.38 | 30.54 | 0.804 | 3.414 | 0.004 | 0.070 | 0.000 | 11.15 | 0.503 |

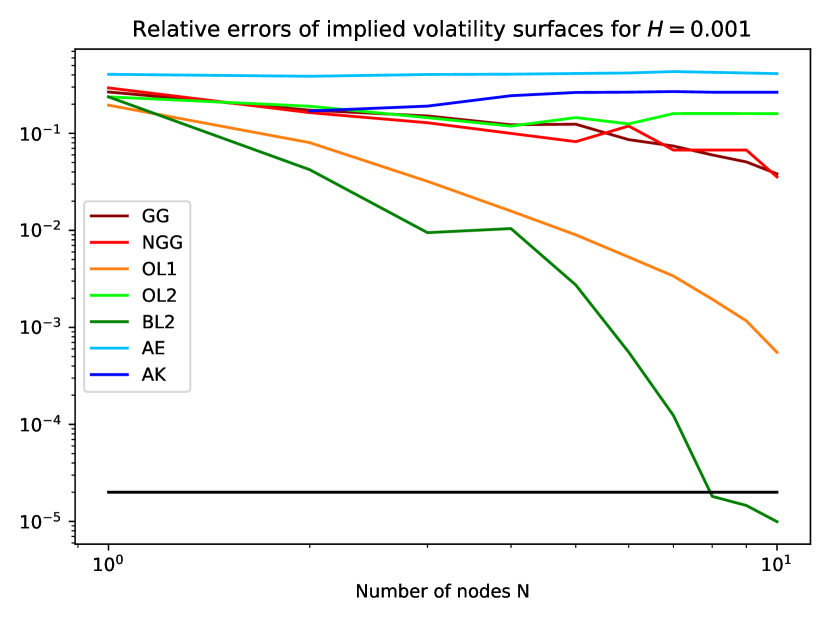

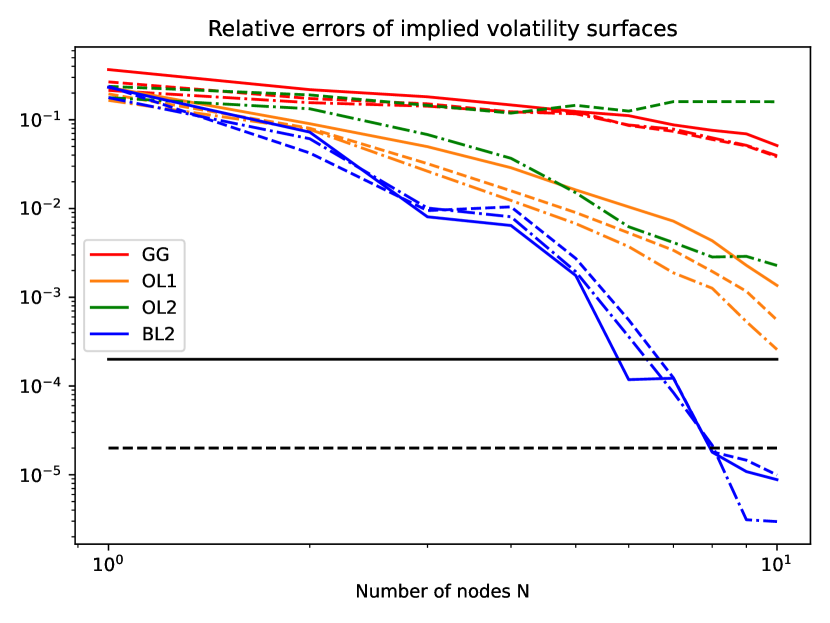

4.4.2. Implied volatility surfaces for European call options

Next, we consider implied volatility surfaces, using 25 maturities linearly spaced in , where we define and . For each maturity we take 301 linearly spaced values of log-moneyness in the interval .

Of course, despite computing implied volatilities for multiple maturities, we use the same quadrature rule for all of them, i.e. we do not adapt the quadrature rule to each individual maturity. But the quadrature rules above all require us to consider on some interval . Thus, the question arises how we choose . A natural choice would be , the maximal maturity. This is also a very reasonable choice for large , since if we chose , we could not expect a good approximation on the interval . However, when is very small, choosing yields very good results for maturities , while giving very bad approximations for maturities . After some numerical experiments, the choice

| (4.1) |

where

seemed to yield good results.

We computed all surfaces with a relative error tolerance of for and for . The computational times for the Adams scheme was 1951 seconds for , 1598 seconds for , and seconds for . In contrast, typical computational times for the Markovian approximations were between 30 and 100 seconds.

The maximal relative errors (maximum over both the strikes and maturities) are reported in Table 4. The results are largely similar to Table 3, although the errors generally tend to be a bit larger since we are now jointly approximating a volatility surface rather than just a single smile. We note that overall, BL2 again performed best, achieving errors around for and errors below the discretization error of were reached for largely independent of .

In Figure 8 we see the maximal relative errors for for all quadrature rules on the left, and a comparison for varying on the right.

| N | GG | NGG | OL1 | BL2 | AE | GG | NGG | OL1 | OL2 | BL2 | AE | AK | GG | NGG | OL1 | OL2 | BL2 | AE | AK |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 36.76 | 40.53 | 23.21 | 23.21 | 52.90 | 26.71 | 29.43 | 19.54 | 23.78 | 23.78 | 40.62 | - | 21.42 | 23.68 | 16.53 | 17.75 | 17.75 | 33.85 | - |

| 2 | 21.84 | 23.04 | 9.025 | 7.255 | 51.21 | 17.34 | 16.35 | 8.027 | 19.04 | 4.223 | 38.77 | 17.02 | 15.58 | 13.63 | 7.787 | 13.30 | 6.111 | 32.23 | 3.945 |

| 3 | 18.14 | 18.14 | 4.975 | 0.806 | 52.76 | 15.12 | 12.87 | 3.203 | 14.52 | 0.948 | 40.45 | 19.10 | 14.22 | 11.09 | 2.632 | 6.808 | 1.012 | 33.71 | 4.089 |

| 4 | 14.68 | 13.81 | 2.881 | 0.644 | 53.02 | 12.26 | 9.995 | 1.583 | 11.88 | 1.044 | 40.74 | 24.45 | 12.27 | 8.611 | 1.233 | 3.679 | 0.807 | 33.07 | 2.426 |

| 5 | 12.38 | 11.15 | 1.620 | 0.176 | 53.61 | 12.43 | 8.213 | 0.900 | 14.55 | 0.274 | 41.42 | 26.41 | 11.67 | 19.72 | 0.676 | 1.505 | 0.194 | 34.57 | 2.153 |

| 6 | 11.12 | 9.455 | 1.043 | 0.012 | 54.04 | 8.618 | 11.90 | 0.531 | 12.52 | 0.056 | 41.94 | 26.59 | 8.732 | 9.581 | 0.372 | 0.623 | 0.036 | 35.03 | 1.218 |

| 7 | 8.756 | 10.84 | 0.720 | 0.012 | 55.16 | 7.406 | 6.733 | 0.338 | 16.00 | 0.012 | 43.36 | 26.98 | 7.845 | 5.410 | 0.188 | 0.414 | 0.008 | 36.31 | 1.473 |

| 8 | 7.604 | 10.84 | 0.434 | 0.002 | 54.58 | 5.997 | 6.733 | 0.196 | 16.02 | 0.002 | 42.60 | 26.56 | 6.253 | 5.410 | 0.126 | 0.284 | 0.002 | 35.62 | 1.197 |

| 9 | 6.933 | 10.84 | 0.229 | 0.001 | 54.02 | 5.077 | 6.733 | 0.117 | 16.00 | 0.001 | 41.92 | 26.56 | 5.148 | 5.410 | 0.053 | 0.289 | 0.000 | 35.01 | 1.197 |

| 10 | 5.121 | 5.967 | 0.136 | 0.001 | 53.50 | 3.829 | 3.557 | 0.056 | 15.96 | 0.001 | 41.29 | 26.56 | 3.940 | 2.831 | 0.026 | 0.228 | 0.000 | 34.45 | 0.994 |

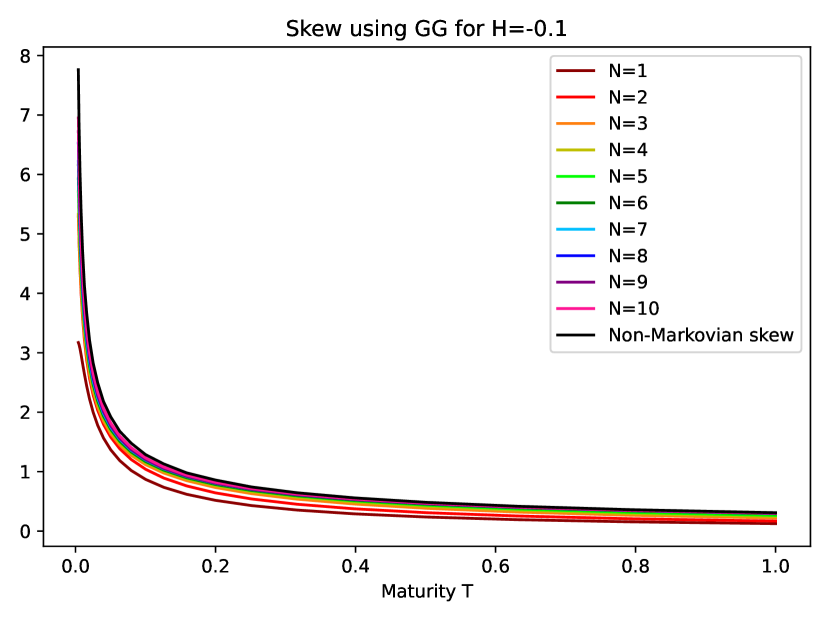

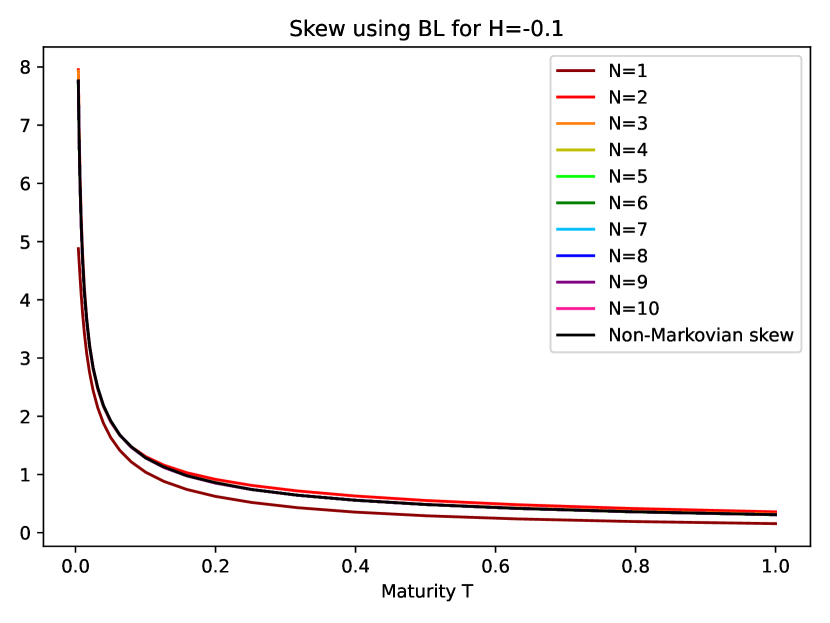

4.4.3. Skew of European call options

Next, we compute the skew of the implied volatility surface for European call options. We recall that in non-rough stochastic volatility models, the skew remains bounded for , while in rough Heston with Hurst parameter , the skew explodes like . Our Markovian approximations are of course just ordinary stochastic differential equations. Hence, the skew will remain bounded as for fixed quadrature rules. However, we hope to be able to show that with the right choice of quadrature rule we can exhibit a similar explosion of the skew on reasonable time scales . To this end, we use 25 geometrically spaced maturities on the interval , i.e. we have maturities between 1 day and 1 year that we want to jointly approximate.

Similarly to the computation of implied volatility surfaces in Section 4.4.2, we are faced with a vector of maturities , and need to choose a suitable representative for approximating by . We use the same choice of as for the implied volatility surfaces given in (4.1).

We computed the skews with relative errors of at most for and , and with relative errors of at most for . The computational times for the skews for the Adams scheme were 6095 seconds for , 4677 seconds for , and seconds for . In contrast, typical computational times for the Markovian approximations were between 60 and 240 seconds.

In Figure 9 we see the skews for GG on the left, and for BL2 on the right. While we can still clearly see that the skews for GG with and the non-Markovian skew do not align perfectly, it is evident that the Markovian skews yield an explosion similar to on the time interval . On the other hand, we cannot make out any difference between the skew for BL2 with and the non-Markovian skew with the naked eye, illustrating that the Markovian approximations using BL2 capture the explosion of the skew well on reasonable time intervals. In particular, BL2 achieved errors below for and errors below the discretization error of for for positive .

4.4.4. Pricing digital European call options

Finally, we consider digital European call options. This illustrates that it is not strictly necessary for the payoff function to be smooth. We consider the option prices themselves and not implied volatilities, as these are not necessarily well-defined for digital options. We take and 301 linearly spaced values of log-moneyness in the interval .

All option prices were computed with a relative accuracy of at least . The computational times for the option prices for the Adams scheme were 950.8 seconds for , 988.9 seconds for , and seconds for . In contrast, typical computational times for the Markovian approximations were between 1 and 5 seconds.

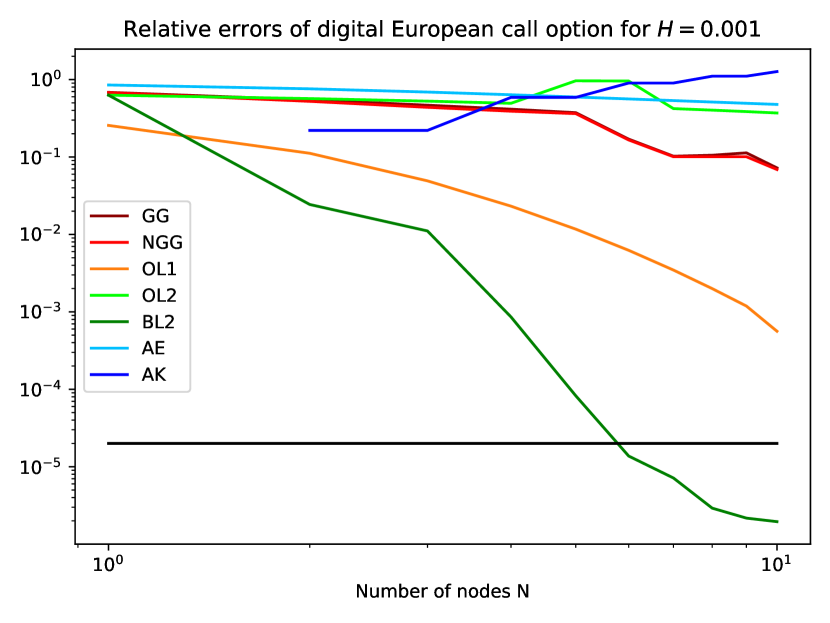

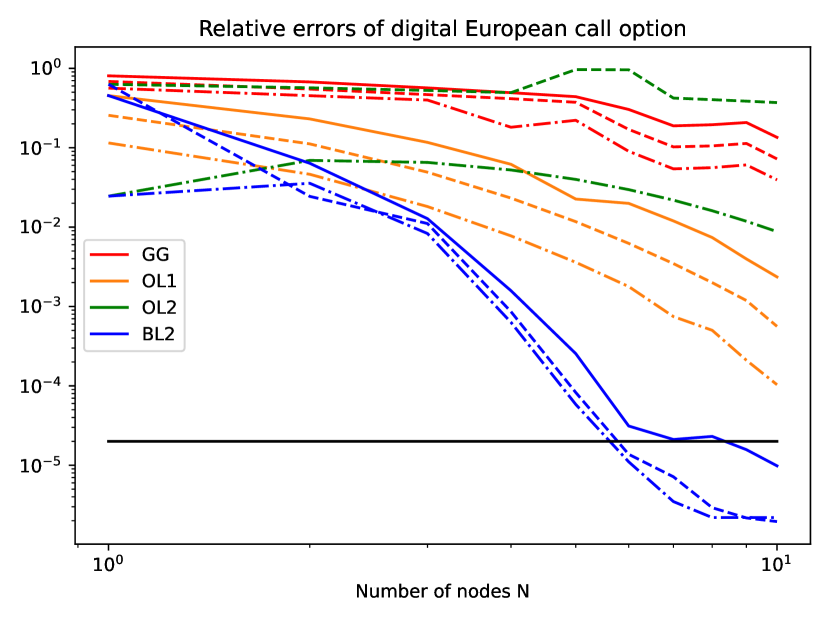

In Figure 10 we see the maximal relative errors for for all quadrature rules on the left, and a comparison for varying on the right. Again, BL2 performed best overall, achieving errors around for and errors below the discretization error of for , largely independent of .

Appendix A Moment explosion of the rough Heston model

In this section, we recall and expand on the results of [GGP19] on the existence of moments of . For all , we denote

Lemma A.1.

Let . Then, for all if and only if for all . This is the case if and only if

In particular, the set of for which for all is an interval , and there is an such that

| (A.1) |

is contained in . In particular, some negative moment of always exists for all .

Proof.

By [GGP19, Theorem 2.4], for all if and only if or

| (A.2) |

The first case () is proved in [GGP19, Proposition 3.7], while the second case is proved in [GGP19, Proposition 3.6]. In both cases, the function in these proofs can be bounded by a constant that depends on the function in these proofs. The function does not depend on the kernel, making the bound independent of . Also, the kernels satisfy all the assumptions of [GGP19, Proposition 3.1], so that the arguments in the proof remain unchanged for . Hence, in both cases. On the other hand, if , then trivially , proving the first claim of the lemma.

Next, we want to prove that the set with is an interval , and that the interval in (A.1) is contained in . Note that conditional on the first condition in (A.2) being true, we have , and the second condition in (A.2) is necessarily true on an interval with . Since the second condition is a quadratic polynomial in (for , with negative leading sign), the second condition is in fact satisfied on an interval of this form.

If , the condition amounts to the interval proving the claim for .

If , the condition amounts to the interval , proving the statement for .

Finally, if , the condition is always satisfied, yielding the interval , proving the statement for . ∎

Appendix B Localizing functions

In this section we prove a simple lemma on approximating smooth functions on by compactly supported smooth functions. While the following results are undoubtedly well-known, we were not able to find precise references.

Lemma B.1.

Let , and let be an times weakly differentiable function. Let . Then there exists a function which is times weakly differentiable such that

where , are absolute constants independent of everything but .

Proof.

Let be non-negative and supported on with

Define the function

We immediately get that is infinitely differentiable and non-increasing, that for , that for , and that

Now, define . Obviously, for and for . Moreover,

Corollary B.2.

Let , and let be an times weakly differentiable function. Let . Then there exists a function which is times weakly differentiable such that

where , are absolute constants independent of everything but .

Proof.

Just apply Lemma B.1 twice. ∎

Appendix C Proof of Lemma 3.4

The aim of this section is to prove Lemma 3.4. First, some technical lemmas are needed. The interesting case in the following lemma is . The purpose of this lemma is that it allows us to remove a quantity in the rate of convergence at the cost of the factor .

Lemma C.1.

Let and Then,

where

is where the infimum is attained.

Proof.

Taking the derivative with respect to and setting it conveniently leads to a quadratic equation with the (unique positive) solution where the infimum is attained. For simplicity, we write instead of .

Define for brevity. Then,

Since by the lower bound on in the statement of the lemma, we can apply the bound

valid for all , to get

yielding in total the bound

We now want to show that the last two summands are non-negative. Indeed, since we have and hence,

where we additionally used Therefore, we have the bound

| (C.1) |

We remark that all the computations were carried out in such a way that the error in this lower bound is of order as , for fixed . Finally,

It merely remains to verify that . We have

Then, if ∎

In the proof of Lemma 3.4, we will represent using its Chebyshev series. Consequently, we need bounds for the coefficients of that series. The following Lemma gives such a bound. We remark that a bound of the form below would be trivial by bounding by its maximum. The improvement to is achieved by noting that the integral only spends amount of time close to the singularity.

Lemma C.2.

Let , where and . Let and be such that , and let . Then,

Proof.

Define so that We have

The integrand only comes close to the singularity for . Hence, we split the integral into a part with , and a part where is far from . First, let us consider the part where . There,

For the remainder of the integral, we note that

Define . Since , we have

This implies for the integral that

Putting these estimates together, we obtain

Transforming back to yields the result. ∎

We can now proceed with the proof of Lemma 3.4.

Proof of Lemma 3.4.

For the proof we follow [Tre19, Theorem 19.3] very closely. In fact, the main difference is that we use a sharper bound on the Chebyshev coefficients below.

Let be the Chebyshev polynomial of degree . By [Tre19, Theorem 3.1], has a representation as a Chebyshev series

Since Gaussian quadrature of level is exact for polynomials up to degree , and, by symmetry, furthermore exact for odd functions, and since the Chebyshev polynomials of odd degree are odd functions, we get the error bound

Since and for , [Tre19, Theorem 19.2] implies that

Appendix D Gaussian Approximations of the fractional kernel

This section is devoted to some simple results on both geometric (Section 3.1) and non-geometric (Section 3.2) Gaussian approximations of the fractional kernel . All results in this section are simple corollaries of the following general error representation formula of Gaussian quadrature.

Theorem D.1.

[BSS02, Theorem 3.6.24] If , and are the nodes and are the weights of Gaussian quadrature with respect to the weight function , then

where is some point with , and is a specific polynomial of degree .

The following corollary will not be explicitly used in the proof of the convergence rates, but it is perhaps an interesting observation.

Corollary D.2.

Let be an approximation of stemming from a geometric or non-geometric Gaussian rule. Then,

Proof.

This follows immediately from Proposition 3.3 once we note that both and are completely monotone. ∎

The next corollary gives us an error representation formula for Gaussian approximations. Note that this formula is not valid for general approximations. Also, we will not use it in the proof of the convergence rates. However, we use this corollary to compute the actual errors of Gaussian approximations in the numerical part.

Corollary D.3.

Let be the nodes and be the weights of a geometric or non-geometric Gaussian rule, and let be the corresponding approximation. Then,

Proof.

By Corollary D.2, we have

Appendix E Computing -errors

Especially for the algorithm OL1 it is necessary to be able to compute the error between and quickly and with high accuracy. We remark that Corollary D.3 is not applicable since we are dealing with arbitrary approximations that do not stem from Gaussian rules. Simple quadrature rules like the trapezoidal rule prove unsuitable due to the singularity of the kernel at , as we will see below. Also, simple changes of variables to remove that singularity do not sufficiently solve this problem. Hence, we describe here an algorithm that allows us to compute the -error within a few milliseconds for moderate values of . More precisely, we give below three different algorithms in increasing sophistication and efficiency.

-

(1)

Trapezoidal: This is just the trapezoidal rule, where we use the midpoint rule on the first interval due to the singularity in .

-

(2)

Trapezoidal exact singularity: We determine the first root of . On we integrate exactly, on we use the trapezoidal rule.

-

(3)

Intersections: We determine all roots when (where and ), and compute the error exactly using that

and the fact that we can integrate and in closed form.

Let us now describe how we find the roots of , where we remark that there are at most such roots. Assume that we are given a relative error tolerance TOL, and that we only have to compute the error up to this relative error tolerance.

To find the roots, we exploit that both and are completely monotone. In particular, this implies the inequalities

for , with similar inequalities for .

We then find the crossings inductively, by moving from to . First, obviously, . Next, we solve

This has an explicit solution , and thanks to complete monotonicity, there was no crossing on .

Suppose now that we are currently at time , and we want to take the next step. Assume without loss of generality that In the other case, we just swap the roles of and . We now differentiate between two cases.

-

(1)

In this case, we are rather far away from the next crossing. We then take the next point as the solution of the equation

This quadratic equation has only one explicit solution , and thanks to complete monotonicity, the kernels did not cross on .

-

(2)

In this case, we might be very close to a crossing. If we proceeded exactly as in Case 1, the steps would become arbitrarily small if a crossing is ahead. To ensure that the algorithm terminates at some point, we always need to take a step that is lower bounded by some constant. We achieve this by choosing such that

This in particular ensures that the relative error on is bounded by , so we again do not overshoot. The above condition can be phrased as two inequalities without the absolute value sign. We then approximate and by their zeroth or first order Taylor polynomial (depending on the direction of the inequality). This yields two linear inequalities, and we choose to be the largest value satisfying both inequalities. Therefore, in the resulting interval , the relative error between the kernels is bounded by .

We have thus given an algorithm on how to travel along the interval . It is not difficult to show that the algorithm reaches the final point in finitely many steps. Next, we describe how we determine where the crossings of are.

Assume again that we are currently at some point , that , and that the next point we step to is . We differentiate between two cases.

-

(1)

If , we say that there were no crossings on the interval .

-

(2)

If , we say that there is a crossing at , an no other crossing in .

In Tables 5 we compare the three methods for computing the -errors. We see that the “Trapezoidal” algorithm is basically useless, while “Intersections” clearly outperforms “Trapezoidal exact singularity”.

| Trapezoidal | Trapezoidal exact singularity | Intersections | |||||||

|---|---|---|---|---|---|---|---|---|---|

| TOL | Rel. error | Time (ms) | Rel. error | Time (ms) | Rel. error | Time (ms) | |||

| 1 | 100 | 0.35 | 100 | 1.30 | 25 | 2.81 | |||

| 800 | 0.87 | 34.3 | 73 | 6.38 | |||||

| 14270 | 220 | 346 | 20.6 | ||||||

| 915 | 1990 | 119 | |||||||

| 1774 | 7120 | 416 | |||||||

| 6992 | 5358 | 321 | |||||||

| 35983 | 5195 | 321 | |||||||

| 122490 | 4264 | 421 | |||||||

| 4124 | 260 | ||||||||

| 3704 | 230 | ||||||||

Appendix F The algorithm BL2

Here, we give a rough description on the algorithm BL2 which usually achieved the best results in Section 4. We remark that the actual implementation additionally contains many minor tweaks to ensure better numerical stability. The implementation can be found in https://github.com/SimonBreneis/approximations_to_fractional_stochastic_volterra_equations in the function european_rule in RoughKernel.py.

Comparing the algorithms OL1 and OL2, we note the following differences: OL1 has better convergence rates and smaller nodes, while OL2 is faster to compute (due to the explicit error formula in [BB23, Proposition 2.11]) and may outperform OL1 for large (e.g. ) and small , see e.g. Table 3. The idea of BL2 is to combine the advantages of OL1 and OL2 into one algorithm.

The reason for the bad asymptotic performance and huge nodes of OL2 is the overemphasis of the singularity of at due to the square (which is less relevant for large and small , explaining the good results of OL2 in this setting). We may eliminate this problem by optimizing the -norm under the conditions that the nodes stay bounded by some constant , i.e. . This is also where the name BL2 (Bounded ) comes from. We denote by opt the algorithm that optimizes the -norm of the kernel with Hurst parameter on the interval , using nodes of size at most . This algorithm opt returns the minimized -approximation error and the corresponding quadrature rule.

It remains to find a good bound . The algorithm BL2 given above does this by choosing some small initial value of (say ), and iteratively comparing the errors when using mean-reversions in , with using mean-reversions. If the improvement is too small (a relative improvement of less than ), we increase by a factor . The first time the improvement is significantly large (a relative improvement bigger than ), we stop and return the current optimal quadrature rule.

It remains to choose the hyperparameters and . After lots of trial and error, the choice and (surprisingly) was numerically found to be optimal, though we remark that especially the choice of may depend on the optimization algorithm used in opt.

References

- [AJ21] Eduardo Abi Jaber “Weak existence and uniqueness for affine stochastic Volterra equations with -kernels” In Bernoulli 27.3 Bernoulli Society for Mathematical StatisticsProbability, 2021, pp. 1583 –1615 DOI: 10.3150/20-BEJ1284

- [AJDC23] Eduardo Abi Jaber and Nathan De Carvalho “Reconciling rough volatility with jumps” In Available at SSRN 4387574, 2023

- [AJEE19] Eduardo Abi Jaber and Omar El Euch “Markovian structure of the Volterra Heston model” In Statistics & Probability Letters 149 Elsevier, 2019, pp. 63–72

- [AJEE19a] Eduardo Abi Jaber and Omar El Euch “Multifactor approximation of rough volatility models” In SIAM Journal on Financial Mathematics 10.2 SIAM, 2019, pp. 309–349

- [AJLP19] Eduardo Abi Jaber, Martin Larsson and Sergio Pulido “Affine Volterra processes” In The Annals of Applied Probability 29.5 Institute of Mathematical Statistics, 2019, pp. 3155–3200

- [AK21] Aurélien Alfonsi and Ahmed Kebaier “Approximation of Stochastic Volterra Equations with kernels of completely monotone type” In arXiv preprint arXiv:2102.13505, 2021

- [Bay+23] “Rough Volatility” to appear SIAM, 2023+

- [BB] Christian Bayer and Simon Breneis “Simulation of rough Heston”

- [BB23] Christian Bayer and Simon Breneis “Markovian approximations of stochastic Volterra equations with the fractional kernel” In Quantitative Finance 23.1 Taylor & Francis, 2023, pp. 53–70

- [BFG16] Christian Bayer, Peter Friz and Jim Gatheral “Pricing under rough volatility” In Quantitative Finance 16.6 Taylor & Francis, 2016, pp. 887–904

- [BSS02] Roland Bulirsch, Josef Stoer and J Stoer “Introduction to numerical analysis” Springer, 2002

- [CC98] Laure Coutin and Philippe Carmona “Fractional Brownian motion and the Markov property” In Electronic Communications in Probability 3, 1998, pp. 12

- [DFF04] Kai Diethelm, Neville J Ford and Alan D Freed “Detailed error analysis for a fractional Adams method” In Numerical algorithms 36 Springer, 2004, pp. 31–52

- [EER19] Omar El Euch and Mathieu Rosenbaum “The characteristic function of rough Heston models” In Mathematical Finance 29.1 Wiley Online Library, 2019, pp. 3–38

- [EGP10] Ernst Eberlein, Kathrin Glau and Antonis Papapantoleon “Analysis of Fourier transform valuation formulas and applications” In Applied Mathematical Finance 17.3 Taylor & Francis, 2010, pp. 211–240

- [GGP19] Stefan Gerhold, Christoph Gerstenecker and Arpad Pinter “Moment explosions in the rough Heston model” In Decisions in Economics and Finance 42 Springer, 2019, pp. 575–608

- [Har19] Philipp Harms “Strong convergence rates for Markovian representations of fractional Brownian motion” In arXiv preprint arXiv:1902.01471 Feb, 2019

- [JR20] Paul Jusselin and Mathieu Rosenbaum “No-arbitrage implies power-law market impact and rough volatility” In Mathematical Finance 30.4 Wiley Online Library, 2020, pp. 1309–1336

- [Tre19] Lloyd N Trefethen “Approximation Theory and Approximation Practice, Extended Edition” SIAM, 2019