From Programming Bugs to Multimillion-Dollar Scams: An Analysis of Trapdoor Tokens on Uniswap

Abstract

We investigate in this work a recently emerging type of scam token called Trapdoor, which has cost the investors hundreds of millions of dollars in the period of 2020-2023. In a nutshell, by embedding logical bugs and/or owner-only features to the smart contract codes, a Trapdoor token allows users to buy but prevent them from selling. We develop the first systematic classification of Trapdoor tokens and a comprehensive list of their programming techniques, accompanied by a detailed analysis on representative scam contracts. We also construct the very first dataset of 1859 manually verified Trapdoor tokens on Uniswap and build effective opcode-based detection tools using popular machine learning classifiers such as Random Forest, XGBoost, and LightGBM, which achieve at least 0.98% accuracies, precisions, recalls, and F1-scores.

1 Introduction

The widespread adoption of the blockchain technology together with the ever-growing demand for trading digital assets has led to the emergence of hundreds of cryptocurrency centralized exchanges (CEXs) such as Binance [3], Coinbase [12], and KuCoin [27], all of which employ the traditional trading mechanism with the vital role of a central authority. By contrast, decentralized exchanges (DEXs) such as Uniswap [39], Pancakeswap [30], and Sushiswap [32], have been developed to facilitate decentralization and enhance user privacy. Governed solely by a set of smart contracts, DEXs allow users to trade their digital assets directly to each other without any intermediary, hence providing them with a full control of their assets, better anonymity, as well as censorship resistance. On the other hand, the lack a central authority on DEXs also means little quality control, regulations, and customer support, making their users susceptible to a plethora of issues, most notably price slippage, smart contracts bugs and vulnerabilities, and low-quality or downright malicious scam tokens [4, 5, 13, 17, 28, 45].

Founded in 2018, Uniswap has become one of the most popular DEXs operating on top of the Ethereum blockchain, with the daily trading volume exceeding US$40 million [15] at the time of writing. This DEX, however, has been reported to be littered with scam tokens. For example, the recent study by Xia et al. [45] indicated that about 95% among more than 10,000 tokens collected by their team from Uniswap are actually scam tokens. Marorra et al. [28] extended this dataset further to include more than 26,000 tokens and also concluded that around 97.7% of them are malicious. In a recent significant cryptocurrency-related court case [22, 41], six investors from North Carolina, Idaho, New York, and Australia, who lost money after investing in various scam tokens on Uniswap, decided to sue Universal Navigation Inc., the company behind the exchange, and its founder/CEO Hayden Z. Adams to the US District Court of New York. Uniswap’s counsel argued that making them liable for scam tokens on their DEX is like holding “a developer of self-driving cars liable for a third party’s use of the car to commit a traffic violation or to rob a bank”, to which the judge agreed. The case was dismissed by the judge in August 2023, but has surely become a legal landmark on cryptocurrency investment scams.

In this manuscript, we set out to investigate Trapdoor scam, a recently emerging type of investment scam on DEXs that has cost the investors hundreds of millions of dollars111How much of this is due to wash trading is the subject of another on-going research., according to our analysis on a collection of nearly 2,000 scam smart contracts collected in the period from 2020 to 2023 on Uniswap (see our labeled dataset [1]). We also found in our initial analysis that around 50,000 investors (unique addresses) had lost their investment to these contracts. The top three losses reached 3,452 ETHs or US$5,702,117, whereas the top three scam contracts WallStreetBets, Hashmasks, and Soulja made in total 6,992 ETHs or US$11,541,904 in this period. In a nutshell, a Trapdoor smart contract employs programming logical bugs such as an “if” condition that is never satisfied, a fee-manipulation mechanism that can only be called by the contract owner, or numerical exceptions such as division by zero, in order to allow the investors to buy newly created tokens (paid with ETH or a valuable token) but prevent them from selling the tokens back to the contract to earn a profit.

Trapdoor scam is very often misclassified as Honeypot, which is a closely related type of cryptocurrency scam [37]. A Honeypot scam, as it name suggests, lures the investors (victims) in by exposing a vulnerability in the contract code that could potential be exploited, which turns out to be a fake one. A trapdoor scam, on the contrary, hides the bugs and pretends to be a legitimate and high-yield token. A more detailed comparison between these two types of scam token is given in Section 3.1. Trapdoor scam is also sometimes treated as a sub-type of Rug-pull scams (see, e.g. [45, 28]), which was the most common cryptocurrency financial scam and responsible for 37% of all cryptocurrency scam revenue in 2021 according to the 2022 Crypto Crime Report from Chainanalysis [7]. In fact, Rug-pull is an umbrella term that refers to scams in which the project developers first lure the investors into buying a new and seemingly profitable token and then disappear with all of the funds, leaving the victims with worthless assets. Trapdoor, on the other hand, refers to a particular set of techniques that ensure that the investors cannot sell back their bought tokens, which is one specific way to allow the liquidity pool to be rug-pulled later.

To the best of our knowledge, there has been no systematic study of Trapdoor scam tokens on Uniswap. We aim to address that gap in this manuscript. Our main contributions are given below.

-

•

We provided the very first comprehensive analysis of Trapdoor tokens, including a classification and a full list of scam techniques and maneuvers. As part of the discussion, we also dissected a number of scam contracts to demonstrate how they actually work. Additionally, full contract analyses are provided for 20 representative scam tokens222https://github.com/bsdp2023/trapdoor_reports.

-

•

We built the very first dataset333https://github.com/bsdp2023/trapdoor_data of 1,859 scam Trapdoor tokens on Uniswap, which were first tested by a buy-sell simulation and then manually verified.

-

•

We also developed machine learning detection tools444https://github.com/bsdp2023/trapdoor_tool that can detect the malicious tokens with very high accuracy. These tools rely on the frequencies of opcodes extracted from the contract’s bytecode, which will work even when the token Solidity codes are not available. We also extracted a list of the most important opcodes and gave an interpretation of why such opcodes play a more important role in distinguishing a Trapdoor token.

The paper is organized as follows. In Section 2 we provide the background knowledge of the Ethereum blockchain, ERC-20, decentralised exchange (DEX), and Uniswap interaction flow. In Section 3, we first define Trapdoor and then describe how our dataset of Trapdoor tokens on Uniswap was created.We present in Section 4 a classification of Trapdoor tokens based on the three key techniques they use to prevent investors from selling. This is followed by the analysis of various tricks the scammers use to place and conceal the traps in the code. In Section 6, we explain in detail our machine learning based detection tools, including feature aggregation, experimental configuration, evaluation metrics, and feature analysis. The paper is concluded in Section 7.

2 Background

2.1 Ethereum smart contract and ERC-20

The concept of a smart contract, an automated executable program, was introduced in 1997 by Nick Szabo [34]. However, this concept only got its first practical implementation in the release of Ethereum in 2015. Smart contracts on Ethereum can be implemented using a Turing-complete programming language called Solidity [21]. A contract’s source code is then compiled into low-level bytecode and deployed onto the Ethereum blockchain through a transaction. Once the contract’s bytecode is stored successfully on the chain, it becomes immutable and publicly available on the chain for everyone to freely access. Besides, a unique address is provided to identify a newly deployed smart contract, which users can use later for interacting with the contract. Any communication with the contract, e.g. function invoking, fund transferring, will be recorded in its transaction history with complete information about the function called, function input, success status, execution time, etc.

Fungible (interchangeable) tokens are the most popular and special smart contracts that can represent virtual assets, such as company shares, lottery tickets, or even fiat currencies. These tokens are implemented by following ERC-20 standard, which defines a list of rules that developers must follow [20]. These rules include standard methods and events (see Table 1) that should come with any tokens.

| Type | Signature | Description |

| Method | name() | Return name of the token (e.g., Dogecoin) |

| symbol() | Return symbol of the token (e.g., DOGE) | |

| decimals() | Returns the number of decimals the token uses | |

| totalSupply() | Return the total amount of the token in circulation | |

| balanceOf() | Return the amount of token owned by given address | |

| transfer() | Transfers amount of tokens to given address from message caller | |

| transferFrom() | Transfers amount of tokens between two given accounts | |

| approve() | Allow a spender spend token on behalf of owner | |

| allowance() | Return amount that the spender will be allowed to spend | |

| Event | Transfer() | Trigger when tokens are transferred, including zero value transfers. |

| Approval() | Trigger on any successful call to approve() |

Among the signatures mentioned in Table 1, transfer and transferFrom are two functions that we primarily focus on in this study because these are fundamental methods used to transfer tokens between two arbitrary accounts. Moreover, the token exchange operations on DEX platforms also relies on these two transfer functions for swapping tokens back and forth. Thus, scammers often aim at these two functions or relevant functions called from them to embed their malicious code.

2.2 Decentralized Exchange

Decentralised exchanges (DEXs) allow users to exchange their digital assets without the involvement of central authorities [44]. Instead, all trades on DEX are stored permanently onto a chain that can be audited publicly. A DEX executes a digital trade without storing user funds (non-custodial exchange) or personal data on a centralised server. Instead, the mechanism of pairing buyers and sellers for a trade is defined clearly in the smart contract.

DEXs are primarily operated based on one of two different trading price determination mechanisms: order-book and automated market maker (AMM). Like the traditional stock exchanges, an order-book-based DEX performs a trade by recording traders’ orders into the order-book and waiting until the DEX finds a suitable order that matches the preset price, allowing traders to buy or sell their digital asset at the expected price. Unlike the order-book model, digital assets’ price in the AMM model is calculated using a mathematical formula. This model is more popularly adopted in blockchain environments due to its computational performance [44]. In general, AMM DEXs work on the concept of liquidity pool that allows traders to exchange their virtual assets without any permission. Particularly, users exchange assets by transferring one asset into the pool and withdrawing another by a corresponding ratio (an asset price). Different DEX uses different formulas to determine an asset price.

2.3 Token Exchange on Uniswap

Uniswap [39] is the largest decentralized exchange that adopts the AMM model successfully. This exchange platform was launched onto the Ethereum network in 2018, and currently, it has three different versions that operate independently. Among these three versions, UniswapV2 entirely outperforms other versions in terms of the number of listed tokens and the number of exchange pools (liquidity pools) [14]. Moreover, UniswapV2 has more than 450 forks [19] across different blockchains due to its public source code and license [40]. For the reasons mentioned above, this research only focuses on UniswapV2 but the approaches in this study are applicable to other versions and folks.

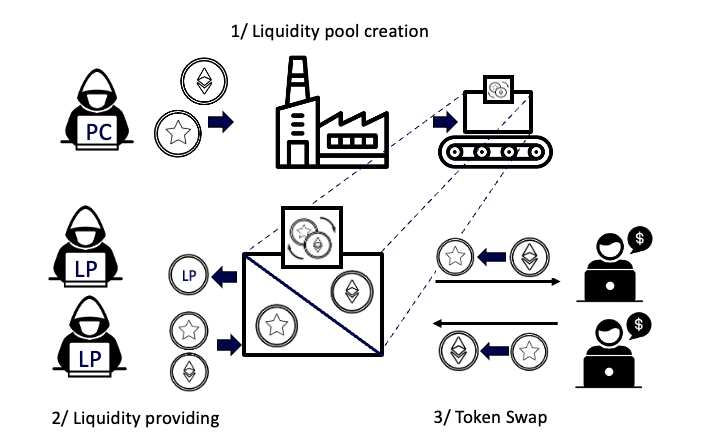

In UniswapV2, each liquidity pool is like an automatic exchange counter for a pair of two different ERC-20 tokens. Imagine the pool consists of two boxes, each storing an exchangeable amount of a single token so that the amount of those two is equivalent in terms of market value. To clarify how an exchange pool works, we look into the interaction flow between users and UniswapV2 as depicted clearly in Figure 1. It is worth noting that UniswapV2 operates mainly through three smart contracts: UniswapV2Factory555https://github.com/Uniswap/v2-core/blob/master/contracts/UniswapV2Factory.sol, UniswapV2Pair666https://github.com/Uniswap/v2-core/blob/master/contracts/UniswapV2Pair.sol, and UniswapV2Router777https://github.com/Uniswap/v2-periphery/blob/master/contracts/UniswapV2Router02.sol.

-

1.

Everything starts from the UniswapV2Factory. On a particular blockchain, there is only one UniswapV2Factory contract which has the primary mission is to generate a UniswapV2Pair contract (liquidity pool) for two given arbitrary ERC-20 tokens. For example, if a user wants to create a new exchange pool and launch it onto Uniswap, he must call the function createPair() in the UniswapV2Factory contract with the inputs are two corresponding token addresses and the user who create a pool is referred as a pool creator (PC).

-

2.

After the liquidity pool is launched successfully, any user (even PC) is able to deposit two paired tokens into the pool as exchange liquidity and who added liquidity into the pool is called liquidity provider (LP). Since a UniswapV2Pair itself is also an ERC-20 token, the pool mints its token (LP-tokens) as the proof of liquidity contribution and sent back to the liquidity contributor every time it receives tokens from LPs. These LP-tokens are then used to withdraw the fund back by burning them. In UniswapV2Pair contract, two corresponding functions mint() and burn() are provided to support the aforementioned features.

-

3.

When a user wants to exchange one of the tokens in the pair for another, he must use the swap() function of a liquidity pool. The exchange rate is calculated based on the ratio of tokens available in the pool, following the constant product formula below.

(1) where and are the current amounts (reserves) of the two tokens in the pool. is the amount of tokens that the user receives while is the amount the user needs to deposit into the pool. For each exchange on the pool, is the fee charged from the trader and proportionally distributed to all LPs in the pool as rewards for their liquidity contribution. Hence, when users exchange one token for another token, the price of the latter will rise. In a swap, a user must first transfer his token to the pool. Then the corresponding amount of the target token will be calculated based on the exchange rate and sent to the buyer. In UniswapV2, UniswapV2Router acts as an intermediary between the user and the UniswapV2Pair, which helps the user estimate the amount of output token before swapping or exchange ETH to WETH or vice versa.

Generally, a newly created token often pairs with a popular and valuable token for easier approaching traders on the market. Hence, we refer to the swap from a popular token to a newly created token as buying a new token, while the reversed swap is referred to as selling a new token.

3 Building a Dataset of Trapdoor Tokens

In this section, we first introduce the concept of Trapdoor tokens and describe the main steps for a scammer to execute the scam on a DEX. We then present in detail the process of creating a reliable dataset of 1,859 Trapdoor tokens on Uniswap, in particular, how we collected tokens on this DEX, what filtering criteria we used to extract tokens that are very likely scams, and how we tested and labeled them.

3.1 Definition of Trapdoor

Note that scam tokens are always paired with high-valued tokens, a general definition of which is given below.

Definition 1 (High-value Token)

A high-value token is a token that is very popular in the cryptocurrency market and trusted by investors worldwide. Moreover, such a token must have a consistently high market cap and has been paired with many other tokens on exchanges.

Definition 2 (Trapdoor Token)

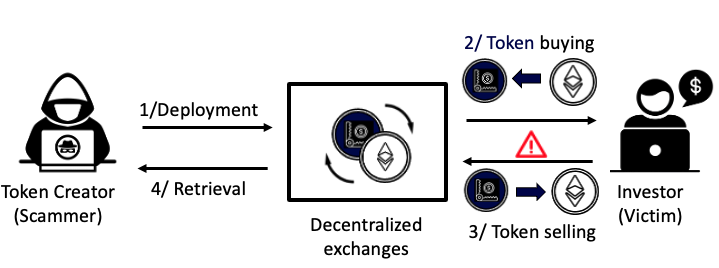

Trapdoor token is a digital token pretending to be a potential cryptocurrency that seemingly brings a high profit to investors (victims) if exchanged. However, the investment fund (in the form of a high-valued token) from investors will be trapped in the liquidity pool due to intentional programming tricks, which can only be withdrawn by the token creator (scammer) or some specific addresses allowed by the creator.

A Trapdoor scam can be carried out on a DEX in four steps (see Fig. 2).

-

1.

The scammer deploys a Trapdoor token onto the chain and creates a liquidity pool on DEX that includes the Trapdoor token and a high-value one.

-

2.

Once the liquidity pool is active, the investors can buy the Trapdoor token by transferring the high-value token to the pool. The scammer often sets the buying fee minimal to encourage the investor to buy more.

-

3.

As more investors buy the Trapdoor token from and add more high-value token to the pool, the value of the scam token rises with respect to the high-value one. However, the investors cannot sell to gain profit as they expected.

-

4.

The scammer now withdraws all high-value tokens from the liquidity pool, including what investors have invested, and disappears.

We note that Trapdoor scams sometimes are referred to as Honeypot scams in several sources. However, these two types are quite different with respect to the targeted victims, how they attract them, and how they embed malicious codes to achieve their goal. More specifically, Honeypot scams often target investigators with some level of experience, who can read the smart contracts, while Trapdoor scams target novice investors who cannot understand the contract very well. Honeypot scams lure the victims by intentionally exposing an easy-to-spot loophole that seemingly could be exploited by investors to gain a big profit from the contract, which turns out to be a fake loophole: the hopeful investor observes the (fake) loophole, invests into the contract, and ends up losing all the investment. A Trapdoor token, on the contrary, aims to hide the malicious/buggy code, making it harder for users to detect. The techniques used in a Honeypot scam, as reported in [38], are also very different from those in a Trapdoor scam.

3.2 Collection of Trapdoor Tokens

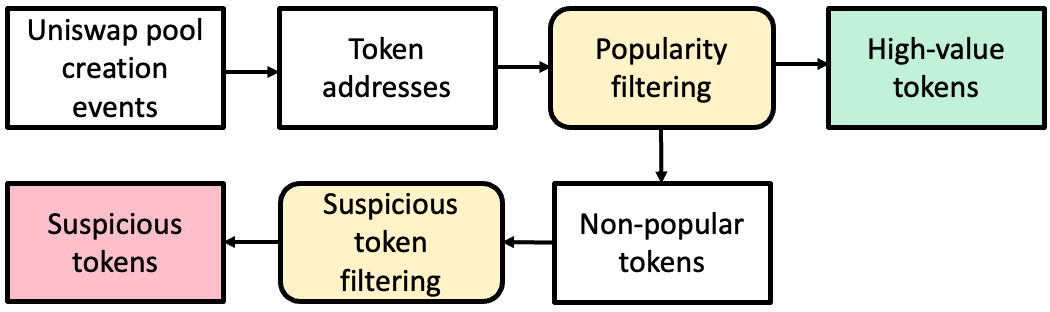

Data collection. Data in this study was collected by using web3 library [43] for querying data on the Infura archive node [24]. As depicted in Fig 3, we first gathered all token addresses listed on UniswapV2 from May 2020, when this platform was launched, to January 2023. We queried from the chain all PairCreated events of UniswapV2Factory888https://etherscan.io/address/0x5c69bee701ef814a2b6a3edd4b1652cb9cc5aa6f contract that store the creation information of generated liquidity pools. Next, we scanned over each event and collected 131,172 unique token addresses listed on this platform. Besides, we also retrieved information on each token, such as the creator address, token name, token symbol, token decimal, and token total supply with the help of Etherscan API [36] for further analyses.

Afterwards, we filtered all non-malicious tokens (high-value tokens) in the list according to their popularity. The popularity of a token is based on its market capitalization and number of liquidity pools it is involved in. Following information on the cryptocurrency ranking website [16], we collected 843 high-value tokens using the below criteria.

Finally, for retrieving Trapdoor suspicious tokens we conducted consequently two steps. In the first step, we gathered tokens that pair with high-value tokens because the main goal of a Trapdoor token is to trap valuable assets from users. In the second step, we filtered and selected tokens that are highly likely to be scam tokens by following the filtering criteria listed below:

-

1.

Number of sellers 1

-

2.

Number of buying transactions 0

-

3.

Number of selling transactions / Number of buying transactions 5%

-

4.

Time period from token deployment to data collection 1 month

According to the nature of the Trapdoor token, nobody can sell a Trapdoor token to get a high-value token back except the token creator (scammer). Therefore, we have criterion (1) to reflect this characteristic. The lower sign happens when the creator withdraws all liquidity in the pool but not selling the Trapdoor tokens for the high-value tokens. Criteria (2) and (3) ensure that this token is successful in attracting investors and eliminates all under-performing tokens. Criterion (4) is used to discard all newly listed tokens because there is a high probability that the user who just bought them will not sell due to insufficient profit, leaving them with similar trading histories like Trapdoor’s. As a result, we gathered 4150 suspicious tokens but only 2723 tokens have source code available on Etherscan [35]. We would like to emphasize that our aim is to build a reliable data set but not detect all Trapdoor tokens on Uniswap. Therefore, we only include tokens that we ensure they are malicious and remove all uncertainties.

Limitation. Those proposed filtering criteria are used for retrieving tokens with a high probability of being malicious. That does not mean a token that does not satisfy the criteria is non-malicious. They can be frauds, but it is very hard to discriminate them from normal tokens if only based on the auto-filtering method. It requires an intensive analysis of the contract source code to prove the token is malicious, which is very time-consuming. Although applying those criteria may skip some Trapdoor variants that adopts a wash-trading technique, it helps reduce the workload significantly, and the number of matching tokens is enough for this scam’s first dataset, which is the foundation for building a machine learning-based detection tool.

Trapdoor ground truth labelling. To construct a ground truth dataset, we must ensure every token in this dataset has Trapdoor malicious nature that allows investors to buy but prevents them from selling. To verify each token in the retrieved list, we follow the process displayed in Figure 4, noting that we only focus on 2723 source code available tokens since we have to analyse the source code and transaction history of each to prove that a considered token is scam token.

First of all, for determining if a suspicious token really acts as a Trapdoor token, we simulate buy and sell transactions by using Brownie [6], a Python-based development and testing framework for smart contracts. The detail of the verification method is represented below.

The test scenario of token buying and selling includes two parts: trading result asserting and trading fee asserting. For trading result asserting, we aim to check if the token transfer success. We expect that token buying is successfully completed while token selling is not because that will prove the characteristic of Trapdoor. The trading fee asserting will be only conducted if the transferring result in success. In this assertion, we will check if the trading fee that the user will be charged directly from the transferring amount while trading is affordable. In our study, we set the acceptable threshold for this fee at 30% of the sending amount. Similarly to the previous assertion, we expect a very small fee to be applied on buying transactions to encourage users to buy this token as many as possible while the selling fee should be extremely high to prevent them from retrieving high-value tokens back. The test result of each token then will be stored and used for the next comprehensive analysis.

In the next step, we only focus on tokens that failed in the sell test regardless of the buy test outcome because, in some situations, a scammer will disable the token trading (triggering the trap) to prevent the sale from investors or apply a considerable trading fee for both buying and selling transactions that make the users lose their funds instantly after exchanging this scam token. Then every selected token has been manually assessed to figure out all tricks used by scammers. The detail of Trapdoor tricks is categorized and explained in Section 4. Ultimately, our ground truth dataset is constructed from 1859 verified Trapdoor tokens.

3.3 General Overview of Trapdoor Tokens and Impacts

In this section, we analyze the collected Trapdoor tokens from different perspectives to obtain more insights into this type of scam.

The lifetime of Trapdoor tokens. One of the characteristic of Blockchain is an immutability that means once a token is deployed onto Ethereum, it will be there forever. Thus, we define the lifetime of a token as follow: The lifetime of a token starts at the block where this token was created and finishes at the block where the last Transfer event of this token was emitted. We found that 1098 tokens (59%) in our dataset only had a lifetime less than 24 hours. Especially, 309 tokens of them had a lifetime even less than 1 hour but they were still exchanged by users. For example, the token EternalMoon999https://etherscan.io/address/0x8da2d78da8266a27bc8ffd170fccf64616e6b90d was purchased by 132 different users although its lifetime only last for 68 blocks. The remaining 41% are long-life Trapdoor tokens that seem to be more hidden and difficult to detect. Surprisingly, 17 tokens among them lived longer than 1 years. The most successful scam token is Mommy Milkers, which stole money from about 1,400 different investors.

Same-name-fake-token strategy. While tokens should have a unique name and symbol, scammers can still name their Trapdoor token similarly to a popular token to make users mistakenly think that they are exchanging with the original one. By comparing token names and symbols, we found 303 tokens (15.7%) that have the same name or symbol with high-value tokens. For instance, 35 different Trapdoor tokens among them have the same symbol with the high-value token Bone ShibaSwap (BONE)101010https://coinmarketcap.com/currencies/bone-shibaswap/ and those tokens have successfully scammed 2,723 investors in total. This strategy was also observed in an earlier work by Xia et al. [45] for the general Rug-pull scams.

| Representative token | Tokens | Creators |

|---|---|---|

| 0xc51a16e0573c796a445bfda2ec33d9ab9151dfbd | 84 | 25 |

| 0x520ad62c62fa93799b68c9095e3402dab4236847 | 52 | 52 |

| 0x15489e5e954f91f530f5521dec51d9e704e931e9 | 48 | 48 |

| 0xa9fba963eb3bc7d6dd9b73c377a46d26a86ee148 | 34 | 34 |

| 0xaf9f277eda18928414934dc93c63e8687aed01b3 | 26 | 7 |

Contract cloning. In our analysis, we also found 1,647 different scammers (unique addresses) behind 1,859 scam tokens, 96% of them only created one token. A scammer might have used different strategies such as using multiple accounts for creating multiple scam tokens or generating a fresh profile for each newly deployed scam token. To dig further, we examined tokens that have exactly the same source codes and grouped them into 52 different groups. The largest group contains 84 different tokens which have the same source code as the token Fei Protocol111111https://etherscan.io/address/0xc51a16e0573c796a445bfda2ec33d9ab9151dfbd. Those tokens were created by 25 different accounts. Furthermore, the second largest token group contains 52 same source-code tokens created by 52 different accounts. Table 2 presents more information about the five largest token groups.

Trapdoor impacts. We provide in Table 3 some economic statistics of 1,859 Trapdoor tokens, with top five profit tokens identified. In total, the scam tokens in our dataset have collected over 133,676 ETHs (or 220 million US dollars) from 53,318 unique investor addresses. Among them, the top three tokens WallStreetBets, Hashmasks, and Soulja have gained a total of 6,992 ETH from nearly 700 investors. Moreover, the top three losses reached 3,452 ETHs (US$5,702,11), in which the investors purchased at least 50 different scam tokens.

| Address | Name | ETH | Victims |

|---|---|---|---|

| 0xbbff2cccd0e774478b2316fbbb22913f1f1475a7 | WallStreetBets | 3024 | 323 |

| 0xf836bcea14bfd5fcc449539ad9bcd58032cd5eaf | Hashmasks | 2234 | 205 |

| 0x34787b6b81173385729242caad95837321cc1bf9 | Soulja | 1664 | 161 |

| 0x34173aa873f754169e269d5ec3526573c1433200 | Doge Set Dollar | 1516 | 218 |

| 0x4c334f280f9e440788b66c4e5260c03e4477267a | Hop.Exchange | 1510 | 169 |

| Total | 1859 tokens | 133677 | 53318 |

4 Trapdoor classification

In this section we classify Trapdoor tokens into three broad groups based on the key techniques that they use to prevent the investors from selling the token back to the pool: conditional assertion, trading fee manipulation, and numerical exception.

4.1 Conditional assertion

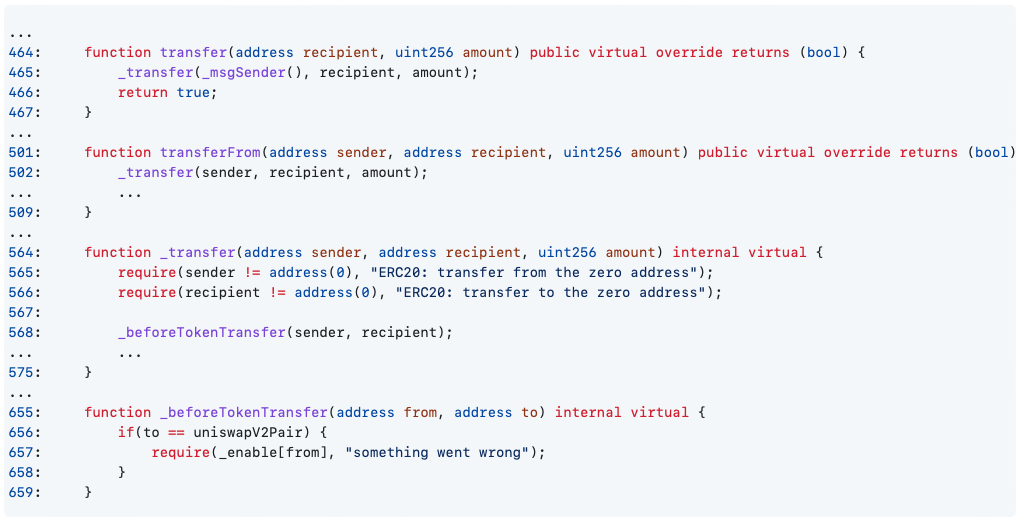

The contracts of tokens in the first group often define a condition that must be satisfied before any selling. To illustrate this technique, let’s consider the contract of a Trapdoor token called AquaDrops (see Fig. 5). At first glance, the contract code looks quite normal. It provides two functions transfer and transferFrom to support token transferring between two arbitrary addresses. Both functions call the common function _beforeTokenTransfer before starting the transfer, which performs a special check when someone sends tokens to the liquidity pool uniswapV2Pair. More specifically, it uses an assert function require for checking if the sender address is in the eligible list _enable (see line 657). If the sender’s address is invalid, an error will be raised and the transaction will be terminated. However, _enable is used nowhere except in the contract’s constructor where the address of the creator itself is added to this list. Thus, only the contract creator (scammer) can transfer a Trapdoor token to the liquidity pool uniswapV2Pair to receive the high-value token from the pool.

Another example is the token LGT (see Fig. 15). Similar to AquaDrops, the function _transfer is used as the core function of both mandatory functions transfer and transferFrom. The first if-else block (line 394-408) seems to be used for preventing any transaction from snipers, i.e. auto-trading bots. Such a check is clearly necessary to prevent instant buying and selling from bots that may drive the price of the token go down dramatically. However, it turns out that this is just smoke and mirrors. By examining the transaction history of this token161616https://etherscan.io/tx/0x647d5425f86809d3c54d96fc34cbe2b0bff82ad036815d3112bffbfc7a607569, we discovered that the token owner had added the address of the corresponding liquidity pool into the list snipers. As snipers now contains the pool address, the first if and else if conditions are satisfied only if both to and from are the pool address (automatedMarketMakerPairs also contains the pool address), which never happens. Therefore, if an investor tries to sell, as snipers[to] = TRUE, the if condition in the last else block will be satisfied, and the function is returned without executing the sell transfer.

4.2 Trading fee manipulation

Unlike conditional assertion, tokens in the trading fee manipulation group will charge senders an extremely high trading fee, e.g. by burning a large amount of Trapdoor token every time the investor buys or sells. As a consequence, after a buy-sell cycle, investors will lose almost all, e.g. 99%, of the investment. The burning percentage/trading fee ratio can be either defined explicitly in the contract or updated later by the token creator. Let’s examine the contract of Seppuku as an example of the former (see Fig. 7). In this contract, both functions transfer and transferFrom call findNinetyPercent to calculate the amount of token to be burned (permanently removed) from the transferring amount. Scammer deceives investors by naming the output of findNinetyPercent as tenPercent but it is actually almost 90%. Thus, only 10% of what was sent will be transferred to the receiver. As the deduction is applied to every buy/sell transaction, investors will be charged 99% when conducting a buy-sell cycle, and the remaining 1% will be insufficient to cover even for the transaction fee.

A less obvious fee manipulation strategy was employed by the token 88 Dollar Millionaire (see Fig. 8, which started with low fee but raised it later to steal all the investment fund. In the contract, the buying fee is the sum of buymktFee (marketing fee) and buyliqFee (liquidity fee) whereas the selling fee is combined from sellmktFee and sellliqFee. At the beginning, the value of buymktFee and buyliqFee were 1% and 6% (at the beginning of the code, not captured in Fig. 8), respectively, which are reasonable. sellmktFee and sellliqFee also had the same initial values. However, sellmktFee was later updated to 99% by the scammer191919https://etherscan.io/tx/0xb61b83676396791d4edc4243fb8ae6d6725efd8578809d41efe25f8354c77b60 using the backdoor function sellFee at line 439, making the fee rate rise up to 105% (99% + 6%). As a consequence, the investor won’t receive any payment back.

4.3 Numerical exceptions

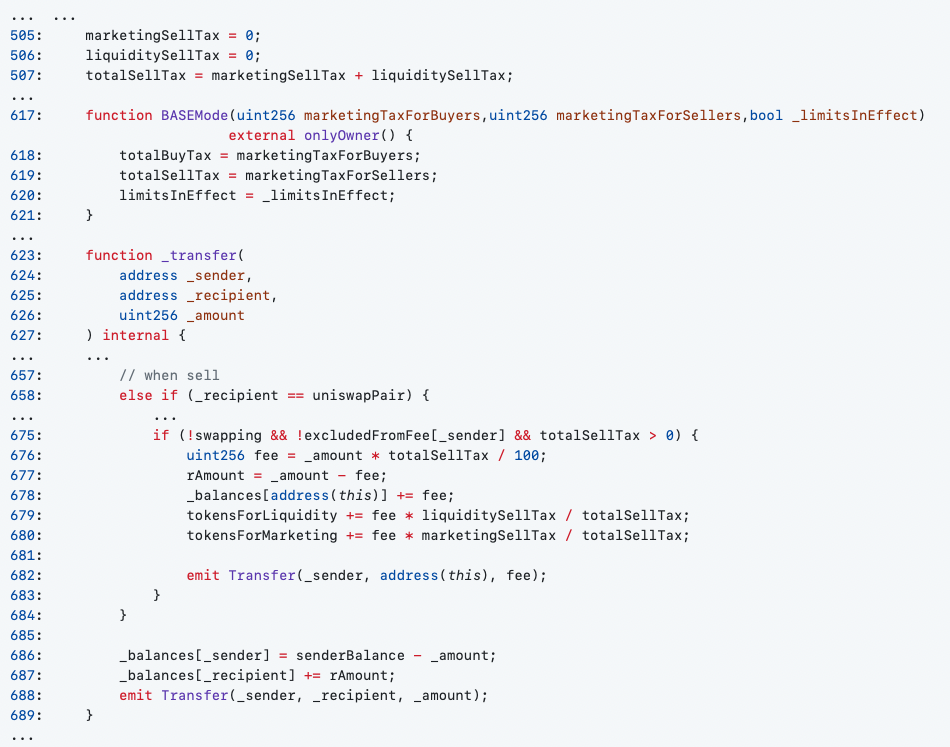

Scam tokens in the third group also tend to cause errors to terminate transactions on pre-set conditions. However, instead of causing an error actively using require, a numerical exception occurs due to the calculation of invalid values intentionally updated by the scammer. That makes those tricks harder to detect. For instance, the contract of CPP4U (Figure 9) uses a variable totalSellTax to record the trading fee percentage, which was originally set to 0 (line 505-507). However, the token creator later secretly increased222222https://etherscan.io/tx/0x034963d54d10c801d9674224ab41c305111214f708983c37c8ce60c2c0837548 this value to 1000%, resulting in the fee ten times higher than the value _amount of the transaction (line 676). The subtraction of fee from _amount, therefore, will be a negative number (line 677), which is then assigned to rAmount, an unsigned integer (line 636). This assignment immediately causes the exception "Integer overflow".

In the case of CPP4U, an investor who came and checked the transaction history of the token after the fee had been increased to 1000% would be immediately alerted. The token Squid-X (Figure 10) has another way to trick even these more careful investors. It intentionally updated the buying fee252525https://etherscan.io/tx/0xc11c3a8183bad5af71bbc2c81dd27ac13ec9ce6e72b02b877b35efccb0491ccb and selling fee to zero262626https://etherscan.io/tx/0xe6ed2a587efbaddc15e50f2856200e40ee27f391562fe2d05f8433e038ea00a0 to attract those investors who actually looked into the transaction. To make the contract look even more legitimate, trading fee value checks are given in setBuyFees and setSellFees, line 613 and 625, respectively, to ensure updated fees do not exceeds 30%. However, by inspecting the function swapBack (line 500-520) more closely, realTotalFee turns out to be zero because buyTotalFee, sellTotalFee, stakingFee, and sellFeeStaking are all zeros, which then cause "division by zero" numeric exception at line 505. Moreover, in transfer and transferFrom, the swapBack function is called based on the shouldSwapBack’s return value. Regardless of swap status and token’s balance checking, the function shouldSwapBack only returns true if the sender is not the liquidity pool (line 476). Therefore, investors can buy Squid-X tokens without any problem but cannot sell them back.

5 Trapdoor Maneuvers Analysis

Although we only list three types of Trapdoor token above, there are several important aspects of these tokens that should also be investigated. We structure our discussion around three essential factors of a Trapdoor token: how the trap is created (trap mechanism), where the trap is located (trap location), and how it is concealed (trap concealment).

Trap mechanisms. There are a number of simple mechanisms that could be used to create a trap in the token contract, which will prevent the investors to sell the token back to the pool and get paid.

| Types | Functions |

|---|---|

| Switch | Turn the trap on/off |

| Exchange-limit | Limit/Deduct the quantity in a sell transaction |

| Blacklist | Prohibit all transfers from addresses in the list |

| Whitelist | Accept only transfers from addresses in the list |

The simplest trap can be constructed by using a boolean variable as a switch, which was originally off so that investors can exchange tokens back and forth. At a particular point, the creator can turn the switch on to activate the trap, effectively preventing the tokens being sold from investors. Some good case studies for this trap include the ILLUSION292929https://etherscan.io/address/0x950247e6697d3e62b80cb49ffd5cb78a1cab7233 token (lines 255-259) and the miniKeiko303030https://etherscan.io/address/0xFD6A7390c424A2c2c3cb06433B7D29926FfAf09F token (lines 293-295). The scammer can put a switch in the assertion method require that will raise an error and terminate all transfers from users if the value of the switch is false (switch off). Another way is to put it in an if-else condition to throw exception whent it’s off.

Instead of using a switch, scammers can also employ an exchange limit (integer number) for restricting the transfer amount in each transaction from investors and open a backdoor function to manipulate this exchange limit. In the early stage, the limit is set to a large number, letting investors buy the scam token without any restriction. Subsequently, the scammer updates this limit to a very small number (e.g, 0 or 1), effectively preventing selling. For example, the creator of the token Cobrashi313131https://etherscan.io/address/0x579aA9419741eb4842A4Bc2439176A34260A259f set the sell limit to 1 and the buy limit to , making it technically a buy-only token. Apart from applying a limit on the sell amount, a scammer can also use a trading fee to drain the expected transfer amount as mentioned in the section on trading fee manipulation.

Using a blacklist or a whitelist is also very typical among the scam tokens. While a blacklist contains all prohibited addresses that is forbidden from exchanging tokens, a whitelist stores addresses that have permission to trade in some circumstances. while these two lists were originally designed to prohibit transactions from auto-trading programs (sniper bots) or to refuse transactions from angel investors in the early stages (prior to DEXs listing), they are often manipulated in scam contracts to restrict selling from investors, while still create a false perception of safety. For example, a scammer can embed malicious codes or call an owner-only function to automatically include investor addresses into a blacklist in their first transaction (buy transaction). This is the case for the token EasyINU323232https://etherscan.io/address/0x93fe5eabd054524fdaaeae7913a90bf73889ebf9 (lines 277-290). Another example is where the scammer marks an exchange pool address as a black address, which makes the contract reject all (selling) transactions sent to the pool address (see Oasis333333https://etherscan.io/address/0xDcbdA615b422eCaCe7242058EB2C321949290ff6). The scammer can also add his address into a whitelist so that only he can sell the Trapdoor token to withdrawn the high-value one from the pool (e.g., see Iron Bank Fixed Forex343434https://etherscan.io/address/0x5a8003ee9cae173c8c2dcb7e8b6e897c3021ba8a).

Trap placement. In trapdoor tokens, malicious codes can be placed anywhere as long as they are used by the transfer functions. More complex Trapdoor tokens may place their traps in a location other than the transfer function, making finding this trap in thousands of lines of code like finding a needle in a haystack. According to our analysis, there are three different locations a trap are often be placed:

-

•

Modifier: modifier is a special type of function whose mission is to perform an additional task before a function is executed (e.g., to validate function inputs). To use a modifier, a developer must attach it to a function by placing its signature next to the function definition where is often neglected by users while scanning a contract. Hence, a scammer often put the trap in a modifier and attaches this modifier to the transfer functions, thereby making the trap more hidden (see, e.g. YearnLending.Finance353535https://etherscan.io/address/0x03ed890912679A0796C759e0224F32E1A3b2F0B7).

-

•

Function: Similar to the idea of using a modifier, a scammer can place the trap anywhere and then call it from the transfer functions indirectly across multiple code layers to hide the association between the trap and the transfer functions, making investors lose track while analyzing the source code. We can take The Reckoning Force363636https://etherscan.io/address/0xa027eb7d1f17a6f888a504c5fb32fe42e0d07d8e as a good example, in which a transfer fee is calculated from multiple sources and from different nested functions that make it very challenging to know where the fee comes from and how it is calculated.

-

•

Contract: In an even more complicated scenario, scammers can place their trap in another contract. This will require more advanced detection techniques than mere source code inspection to discover their trap. For example, Elongate Deluxe373737https://etherscan.io/address/0x348bb716bc4378560cd269f4a039aba957e24d1b calls functions in another contract botProtection to manage their trap. Those functions’ names are encoded already, which makes it hard to tell what those functions actually perform from the calls. Moreover, the source code of the contract botProtection is unavailable, making it rather difficult to explore the malicious logic used by the scammer. In such cases, we can first check the transaction history to find the address of botProtection and then use the tool Panoramix383838https://oko.palkeo.com/0xe20EC16A3B574Fd6399ecC29c6886bf3f5A0Ccc7/code/ to decompile the contract bytecode to obtain a readable source code.

Trap concealing. Embedding malicious code in different locations is not the only trick for hiding a trap. We list below all the tricks that scammers have used to conceal their traps that we have encountered in our analysis of the dataset.

-

•

Blank error message: Using a revert or a require method with a blank message that gives investor no information when they receive an error, making them clueless about the real cause of the (sell) transaction failure. Some tokens using this technique are Takeoff393939https://etherscan.io/address/0x8196464fb1319b4dad2f4d5690895554c78e17b3, and ElonTheDoughboy404040https://etherscan.io/address/0xb6e11ef3ed33577a1ce9948a9e594b882b6e2778.

-

•

Single-character names: Using hard-to-see letters such as i, t or l for a switch’s name that could be overlooked when reading a contract. Furthermore, searching for a single letter in a contract will yield many unrelated results, making it hard to track the updates of the switch’ value. A good example of a scam token using this trick is Teen Mutant Turtle414141https://etherscan.io/address/0x7deb87a7e3f8f42bfdfd9f8f48b6702118154f68.

-

•

Misleading names: Typically, scammers name their malicious variables or functions with misleading names to deceive the investors. For instance, they often name a blacklist as a bot list or an exchange pool address as zero address, which misleads the users. An example of such tokens is The Art424242https://etherscan.io/address/0x457A0677d206970A20212f95f35378Cfc68eaA0C.

-

•

Dummy function: Fraudsters create dummy functions to show users that the value of a particular variable is updated correctly. These functions are often named as initialization functions (e.g. init()). However, this function will never be called and the variable will always have the value the scammer wants, serving the purpose of the scam (e.g. AIRSHIB434343https://etherscan.io/address/0xf69A9B73a45e8CE7Fd75BC0e7773824C585f6F35).

-

•

Incomplete renouncement: Contract ownership renouncement is one way to build trust from users, showing that the contract creator no longer own the token. However, scammers can actually exploit this action to create false trust. For example, before giving up ownership, the scammer can secretly add another of his (unknown to the investors) addresses, which still allows him to manipulate the contract, e.g., modify the transaction fees without the ownership. Therefore, although investors can see that the contract creator has relinquished the ownership, the token is still secretly under his control (see, e.g. DYDZ444444https://etherscan.io/address/0x0dbce1083e55d34a7763558e5eedef04e4d93d85 and POLY ELON454545https://etherscan.io/address/0xed28ef42af3a742c9ccbc897210c61f6d468a439).

-

•

Invalid callback: This maneuver works as follows. Every time investors call the transfer function to sell a token, a special function is used to call back the transfer function with invalid inputs that cause the transaction to fail and rollback. An example of this sophisticated maneuver is ELONAJA464646https://etherscan.io/address/0xeac8976401037b0f1a706d915285d442423b9b3c.

6 Trapdoor Tokens Detection

6.1 Non-malicious data

Unlike Trapdoor tokens, non-malicious tokens cannot be verified based on buying/selling tests. It is because a token that can be bought and sold now can be turned into a Trapdoor token in the future when a scammer activates a trap. Or the token can simply be another type of scam (e.g., Rug-Pull, Ponzi). Thus, we gathered non-malicious data based on the high-value token dataset, including 843 tokens collected in Section 3.2 and non-malicious dataset including 631 tokens from previous studies [28, 29]. We obtained 621 non-malicious tokens by taking the intersection of these datasets. In fact, these tokens have very high popularity ranked on some reputable websites (e.g., www.coinmarketcap.com, www.coingecko.com), and have been purchased by many investors. Moreover, those tokens have been also audited by external companies such as Certik, Quantstamp, and Hacken (see [28, Section 6.1.2]). Finally, we combined them with 1,859 Trapdoor tokens collected in Section 3.2 to create the experimental dataset of 2,480 tokens used for our detection experiments in Section 6.4.

6.2 Code Features

Scam detection tools often use two main data sources: smart contract codes (source codes, bytecodes, or opcodes) and transaction history. Using transaction features for detecting Trapdoor tokens has some advantages: the transaction history is permanently available on the chain and captures several aspects not visible in the contract code, such as trading patterns and contract owner’s actions. However, we need to be cautious in building the dataset when using transaction histories for training machine learning models. In fact, it is quite hard to select the non-malicious group because if we pick the most popular ones, their transaction histories will surely look very different from those of the scam contracts, which often have much fewer activities and exist for much shorter periods. This will cause over-fit. On the other hand, if we also pick less popular contracts, then the problem is that it is not easy to verify if they are definitely not a scam.

To avoid the aforementioned dilemma, in this research, we decide to build our detection tool based on the smart contract opcodes, which has proved to be quite successfully in detecting Ponzi scam on blockchain [9, 11, 10, 25, 42]. The intuition for using opcode features is that they should look quite different between contracts that have different purposes. Moreover, opcode features are not impacted by the token popularity and can be extracted even when the source code (in Solidity) of the smart contracts have been removed. To aggregate opcode features, we first collect all contracts’ bytecode from Etherscan APIs [36]. After that, we disassemble the smart contracts’ bytecode into opcodes and calculate the occurrence frequency of each unique opcode. As a result, 283 different code features are collected from the 2,480 contracts’ opcodes.

6.3 Classification Models

Our goal is to train and test a few well-known machine classification methods using our proposed dataset and compared their performance to find the most suitable classification model for this problem. The models are listed below

-

•

Random Forest (RF) [33] is a computationally efficient classification algorithm that works effectively in several domains [31] including fraud detection [2]. The key idea of this algorithm is to get a better result by aggregating the predictions from all trees in the forest, which is generated by using the Bootstrap resampling technique.

-

•

XGBoost (XGB) [8] is a gradient-boosting-based algorithm that creates gradient-boosted decision trees in sequential form and then groups these trees to form a strong model. Unlike RF, which aggregates the results from all trees to get the final result, and the result of XGB is the prediction of the last model, which addressed data misclassified from previous models.

-

•

-nearest neighbour (KNN) [18] is a non-parametric classifier that uses proximity to estimate the likelihood that a data point will become a member of one group.

-

•

Support vector machine (SVM) [23] is the algorithm that has been widely applied in binary classification or fraud detection problems. SVM performs classification by establishing a hyperplane that enlarges the boundary between two categories in a multi-dimensional feature space.

-

•

LightGBM (LGBM) [26] is also a gradient-boosting-based algorithm that grows a tree vertically (leaf-wise). By adopting leaf-wise algorithms, LGBM often has better accuracy and shorter training time than other gradient-boosting-based algorithms.

6.4 Detection Experiment

Datasets. In our experiment, instances in the dataset are shuffled randomly and split into a training set (80%) and a test set (20%). While a training set is used for training our detection models, a test set is used for validating the model’s performance. Furthermore, we also adopt the 5-fold cross-validation to train and validate the selected model on the training set. Finally, a trained model was used to classify the tokens in the unseen test dataset. To make our result more reliable, we repeated the experiment process ten times, and the final result was obtained by taking the average. We note that the same hyperparameters were used for the same models to make a fair comparison. Our Python code and dataset are available online at https://github.com/bsdp2023/trapdoor_tool.

Evaluation metrics. Every selected classifier’s performance is evaluated by using four different standard metrics that are calculated based on the numbers of true positives (TP), true negatives (TN), false positives (FP), and false negatives (FN). More specifically, Accuracy is the fraction of correct predictions, calculated as , Precision is the fraction of the actual scams out of all the predicted scams by the method, calculated as , Recall is the fraction of detected scams among all actual scams, calculated as , and F1-score is the harmonic mean of Precision and Recall and is calculated as .

Experimental results. A comparison of various scores of different detection models is provided in Table 5. The best scores are shown in a bold font. Overall, all selected classification algorithms have the F1-score over 0.90, indicating that models built based on contract opcode features are able to detect Trapdoor tokens quite well. Among the implemented models, we noticed that classifiers built on decision trees were more efficient in Trapdoor token detection than others. In particular, Random Forest, XGBoost and LightGBM achieved all four metrics greater than or equal to 0.98. LightGBM had the best performance not only in the F1-score but also in Accuracy, Precision and Recall.

| Classifier | Accuracy | Precision | Recall | F1-score |

|---|---|---|---|---|

| KNN | 0.891 | 0.886 | 0.980 | 0.931 |

| SVM | 0.855 | 0.839 | 0.998 | 0.911 |

| Random Forest | 0.980 | 0.993 | 0.981 | 0.987 |

| XGBoost | 0.980 | 0.986 | 0.987 | 0.987 |

| LightGBM | 0.983 | 0.989 | 0.988 | 0.989 |

Feature analysis. To understand the effectiveness of opcode features in detecting Trapdoor tokens and make an effort to interpret the results, we retrieved the importance of each opcode from the best performance model LightGBM in the previous experiment. The importance of a feature is defined by the number of times this feature is used to split the data across all decision trees. Hence, the most important feature is the most efficient opcode used to discriminate non-malicious and Trapdoor tokens. To this end, we extracted the top ten important features and counted their occurrences in each token in our dataset. The statistics are provided in Table 6.

| Opcode | Description | Trapdoor | Normal |

|---|---|---|---|

| CALLDATALOAD | Get input data of environment | 19 | 23 |

| SLOAD | Load from storage | 66 | 42 |

| CALLDATASIZE | Get size of input data in environment | 13 | 10 |

| GT | Greater-than comparison | 20 | 11 |

| PUSH16 | Place 16 byte item on stack | 0 | 1 |

| MUL | Multiplication operation | 28 | 12 |

| OR | Bitwise OR operation | 10 | 4 |

| LOG1 | Append log record with one topic | 0 | 2 |

| LT | Less-than comparison | 24 | 16 |

| NOT | Bitwise NOT operation | 14 | 9 |

From Table 6, we can observe that the opcodes GT, LT, OR, and NOT appear in the Trapdoor contracts more than normal contracts. This is not surprising since Trapdoor tokens often use comparisons as the condition to throw an exception intentionally, such as comparing a transfer amount and a transfer limit or checking whether a receiver’s address is an exchange pool’s address. Besides, the number of MUL opcode, which is often used to calculate and apply the transfer fee, is also higher in Trapdoor tokens than in normal contracts. Finally, SLOAD opcode appears in Trapdoor tokens more frequently than in non-malicious tokens, which could be because the blacklist and whitelist in Trapdoor tokens are always loaded for checking transfer permission.

7 Conclusion

We provide in this work a comprehensive analysis of Trapdoor tokens, a new financial fraud on Uniswap, one of the most popular decentralized exchange. The study reveals a range of simple to advanced techniques successfully employed by the scammers and the devastating economic impact they have had on the victims. The verified dataset of Trapdoor scam tokens, the machine learning detection models, together with the detailed analysis provided in this paper will facilitate future studies in crypto scams, which are currently running rampant across different investment platforms.

References

- [1] Labeled Trapdoor dataset (2023), https://github.com/bsdp2023/trapdoor_data

- [2] Bhattacharyya, S., Jha, S., Tharakunnel, K., Westland, J.C.: Data mining for credit card fraud: A comparative study. Decision support systems 50(3), 602–613 (2011)

- [3] Binance: Binance Exchange (Jul 2017), https://www.binance.com/en

- [4] Blockchainmagazine: Your guide to decentralized cryptocurrency exchange: Features, advantages, disadvantages (2023), https://blockchainmagazine.net/your-guide-to-decentralized-cryptocurrency-exchange-features-advantages-disadvantages/

- [5] Blocktelegraph: The Rise of decentralized exchanges: Pros and cons unveiled (2023), https://blocktelegraph.io/decentralized-exchanges-pros-and-cons/

- [6] Brownie: Python-based development and testing framework for Ethereum smart contracts (2019), https://github.com/eth-brownie/brownie

- [7] Chainanalysis: The 2022 Crypto Crime Report. http://demo.chainalysis.com/2022- crypto-crime-report/ (2022), accessed: 2022-04-24

- [8] Chen, T., Guestrin, C.: Xgboost: A scalable tree boosting system. In: Proceedings of the 22nd acm sigkdd international conference on knowledge discovery and data mining. pp. 785–794 (2016)

- [9] Chen, W., Zheng, Z., Cui, J., Ngai, E., Zheng, P., Zhou, Y.: Detecting ponzi schemes on ethereum: Towards healthier blockchain technology. In: Proceedings of the 2018 world wide web conference. pp. 1409–1418 (2018)

- [10] Chen, W., Zheng, Z., Ngai, E.C.H., Zheng, P., Zhou, Y.: Exploiting blockchain data to detect smart ponzi schemes on ethereum. IEEE Access 7, 37575–37586 (2019)

- [11] Chen, W., Li, X., Sui, Y., He, N., Wang, H., Wu, L., Luo, X.: SADPonzi: Detecting and characterizing Ponzi schemes in Ethereum smart contracts. Proceedings of the ACM on Measurement and Analysis of Computing Systems 5(2), 1–30 (2021)

- [12] Coinbase: Coinbase Exchange (May 2012), https://www.coinbase.com/au

- [13] Coindesk: Centralized exchange (CEX) vs. decentralized exchange (DEX): What’s the difference? (2022)

- [14] Coingecko: Decentralized exchanges (2023), https://www.coingecko.com/en/exchanges/decentralized

- [15] Coingecko: Uniswapv2 Ethereum (2023), https://www.coingecko.com/en/exchanges/uniswap-v2-ethereum

- [16] Coinmarketcap: Total Cryptocurrency Market Cap (2021), https://coinmarketcap.com/charts/

- [17] Cointelegraph: Centralized vs. decentralized crypto exchanges, https://cointelegraph.com/learn/centralized-vs-decentralized-crypto-exchanges

- [18] Cover, T., Hart, P.: Nearest neighbor pattern classification. IEEE transactions on information theory 13(1), 21–27 (1967)

- [19] Defillama: UniswapV2 Folks (2023), https://defillama.com/forks

- [20] Ethereum: ERC-20 Token Standard (2015), https://ethereum.org/en/developers/docs/standards/tokens/erc-20/

- [21] Ethereum: Solidity (2015), https://docs.soliditylang.org/en/v0.8.16/

- [22] Finance, Y.: Don’t blame Uniswap for crypto scams, judge rules—and she’s right (2023), https://finance.yahoo.com/news/don-t-blame-uniswap-crypto-151307251.html

- [23] Hearst, M.A., Dumais, S.T., Osuna, E., Platt, J., Scholkopf, B.: Support vector machines. IEEE Intelligent Systems and their applications 13(4), 18–28 (1998)

- [24] INC, I.: Infura (2016), https://www.infura.io

- [25] Jung, E., Le Tilly, M., Gehani, A., Ge, Y.: Data mining-based ethereum fraud detection. In: 2019 IEEE International Conference on Blockchain (Blockchain). pp. 266–273. IEEE (2019)

- [26] Ke, G., Meng, Q., Finley, T., Wang, T., Chen, W., Ma, W., Ye, Q., Liu, T.Y.: Lightgbm: A highly efficient gradient boosting decision tree. Advances in neural information processing systems 30 (2017)

- [27] KuCoin: Kucoin Exchange (Sep 2017), https://www.kucoin.com

- [28] Mazorra, B., Adan, V., Daza, V.: Do not rug on me: Leveraging machine learning techniques for automated scam detection. Mathematics 10(6), 949 (2022)

- [29] Nguyen, M.H., Huynh, P.D., Dau, S.H., Li, X.: Rug-pull malicious token detection on blockchain using supervised learning with feature engineering. In: Proceedings of the 2023 Australasian Computer Science Week, pp. 72–81 (2023)

- [30] Pancakeswap: Pancakeswap (2023), https://pancakeswap.finance/

- [31] Rokach, L.: Decision forest: Twenty years of research. Information Fusion 27, 111–125 (2016)

- [32] Sushiswap: Sushiswap (2023), https://www.sushi.com/

- [33] Svetnik, V., Liaw, A., Tong, C., Culberson, J.C., Sheridan, R.P., Feuston, B.P.: Random forest: a classification and regression tool for compound classification and qsar modeling. Journal of chemical information and computer sciences 43(6), 1947–1958 (2003)

- [34] Szabo, N.: Smart Contracts: Building Blocks for Digital Markets (1996), https://www.fon.hum.uva.nl/rob/Courses/InformationInSpeech

- [35] Etherscanners team, T.: Etherscan (2015), https://etherscan.io

- [36] Etherscanners team, T.: Etherscan API (2015), https://etherscan.io/apis

- [37] Torres, C.F., Steichen, M., State, R.: The Art of The Scam: Demystifying Honeypots in Ethereum Smart Contracts. In: in Proceedings of the USENIX Security Symposium. pp. 1591–1607 (2019)

- [38] Torres, C.F., Steichen, M., et al.: The art of the scam: Demystifying honeypots in ethereum smart contracts. In: 28th USENIX Security Symposium (USENIX Security 19). pp. 1591–1607 (2019)

- [39] Uniswap: Uniswap (2023), https://uniswap.org/

- [40] Uniswap: UniswapV2 source code (2023), https://github.com/Uniswap/v2-core/

- [41] UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF NEW YORK, KATHERINE POLK FAILLA, D.J.: Risley v. Universal Navigation Inc., Memorandum & Opinion — document #90 (2023), https://www.courtlistener.com/docket/63213270/90/risley-v-universal-navigation-inc/

- [42] Wang, L., Cheng, H., Zheng, Z., Yang, A., Zhu, X.: Ponzi scheme detection via oversampling-based long short-term memory for smart contracts. Knowledge-Based Systems 228, 107312 (2021)

- [43] Web3Python: Python library for interacting with Ethereum (2016), https://github.com/ethereum/web3.py

- [44] Werner, S., Perez, D., Gudgeon, L., Klages-Mundt, A., Harz, D., Knottenbelt, W.: Sok: Decentralized finance (defi). In: Proceedings of the 4th ACM Conference on Advances in Financial Technologies. pp. 30–46 (2022)

- [45] Xia, P., Wang, H., Gao, B., Su, W., Yu, Z., Luo, X., Zhang, C., Xiao, X., Xu, G.: Trade or Trick? Detecting and Characterizing Scam Tokens on Uniswap Decentralized Exchange. In: Proceedings of the ACM on Measurement and Analysis of Computing Systems. vol. 5.3, pp. 1–26 (2021)