Income, education, and other poverty-related variables:

a journey through Bayesian hierarchical models

Abstract

One-shirt-size policy cannot handle poverty issues well since each area has its unique challenges, while having a custom-made policy for each area separately is unrealistic due to limitation of resources as well as having issues of ignoring dependencies of characteristics between different areas. In this work, we propose to use Bayesian hierarchical models which can potentially explain the data regarding income and other poverty-related variables in the multi-resolution governing structural data of Thailand. We discuss the journey of how we design each model from simple to more complex ones, estimate their performance in terms of variable explanation and complexity, discuss models’ drawbacks, as well as propose the solutions to fix issues in the lens of Bayesian hierarchical models in order to get insight from data.

We found that Bayesian hierarchical models performed better than both complete pooling (single policy) and no pooling models (custom-made policy). Additionally, by adding the year-of-education variable, the hierarchical model enriches its performance of variable explanation. We found that having a higher education level increases significantly the households’ income for all the regions in Thailand. The impact of the region in the households’ income is almost vanished when education level or years of education are considered. Therefore, education might have a mediation role between regions and the income. Our work can serve as a guideline for other countries that require the Bayesian hierarchical approach to model their variables and get insight from data.

Highlights

-

•

One-shirt-size policy cannot handle poverty issues well since each region has its unique challenge while having custom-made policy for each region separately is unrealistic in term of resources.

-

•

In this work, hierarchical models are deployed to explain income and poverty-related variables in the multi-resolution governing structural data of Thailand.

-

•

Having a higher education level increases significantly the households’ income for all the regions in Thailand.

-

•

The impact of the region in the households’ income is almost vanished when education level or years of education are considered. Therefore, education might have a mediation role between regions and income.

-

•

For each year-of-education the monthly income of a household is increased in 1880 THB on average at the national level. This amount might vary between 1278 THB for Western Thailand up to 2545 THB for Eastern Thailand.

-

•

Households with a high education level earn on average 8325 THB more per month than households with a mid education level and 14844 THB more than households with a low education level.

1 Introduction

Poverty is one of the most important issues that mankind faces [1]. It is one of the main root causes that harms several aspects of society such as economy development [2], education [3], healthcare systems [4], etc. For each year, there were millions of human deaths causing by poverty [5]. To combat poverty issues, a government needs appropriate policies to solve them [6, 7]. With the proper policies and sufficient resources, poverty can be alleviated effectively. However, finding the right policy is a non-trivial task due to the complexity of issues and unique characteristics of regions. For instance, in a similar problem, one solution in a specific region might not be able to solve it in another region even though they have similar characteristics in many aspects [8, 9].

One-shirt-size policy is a popular way to solve an issue by policy makers since it is simple to implement and typically uses less resources than a custom-made policy that is designed for a specific region. Nevertheless, one-shirt-size policy is unable to handle issues in all regions of a country effectively since each region might have their own unique socioeconomic context or other issues of poverty [10, 11, 12]. On the other hand, making a specific policy for each region to solve their unique problems is impossible due to the limitation of time and resources [13].

To find an optimal solution between the two extremes of one-shirt-size and custom-made policies, in this work, we propose to use Bayesian hierarchical models [14] to find a proper model that effectively explains target variables (e.g. income, debt, savings, etc.) related to poverty. To the best of our knowledge, there is no work in the literature that makes use of Bayesian hierarchical models to analyze variables of poverty in Thailand. For some variables, we found that complete pooling (representing one-shirt-size policy) and no pooling (representing custom-made policy) cannot explain a target variable while hierarchical models can, which represents the middle ground between these two extremes. The analyses and results of our work can be used as a role model for the analysis in other countries.

1.1 Related works

In the past, poverty was about lacking of income. However, the concept of poverty is complex and multidimensional [1, 15], which implies that solving only monetary problems is not enough to alleviate the issues of poverty. Therefore, the Multidimensional Poverty index (MPI) [16, 17] was developed and used by United Nations Development Programme (UNDP) as a standard way to measure poverty in multidimensions such as living standard, health, education, etc. The MPI indices from nations around the world have been reported annually by UNDP. Another index that is typically used for measuring income inequality is the Gini coefficient [18], which represents the distribution of resources among people. Instead of the Gini coefficient, the work in [19] proposed to use the network density of income gaps (edges represent significant gaps) to measure income inequality among different occupations.

Even though these indices provide rich information regarding poverty and income inequality in each area, they never provide the information of resolution of poverty issues; given multiple areas, it is impossible to tell from MPI whether these areas share similar issues and need only a single policy to solve poverty. To address this gap, both minimum description length (MDL) [13] and Gaussian Mixture Models [20, 21, 22] can be used to find optimal multiresolution partitions that can place a single policy for each partition since each one represents an area that have a similar model of issues. However, these works cannot be used to provide insights regarding dependencies of issues between different area resolution levels. Does income variables in the national level affects income variables in provinces or lower levels? The next section provides the reasons of using Bayesian hierarchical models in our work.

1.2 Relevance of Bayesian hierarchical models

One of the approaches to model policies is to use Bayesian’s statistics and modeling, which is widely used to model public policies in government setting [23] as well as public opinions [24]. In this work, we propose to use Bayesian hierarchical models to analyze variables that are related to poverty and inequality from a population dataset of Thai households.

Some datasets are collected with an inherent multilevel structure, for example, households within a region of a country. Then, hierarchical modeling is a direct way to include clusters at all levels of a phenomenon, without being overwhelmed with the problems of overfitting. At a practical level, hierarchical models are flexible tools combining partial pooling of inferences. They have been successfully involved in various practical problems, including biomedicine [25, 26], genetics [27, 28], ecology [29, 30], psychology [31], among others. We refer to [32] for a review on Bayesian modeling and a further list of their applications, including Bayesian hierarchical models.

The traditional alternatives to hierarchical modeling are complete pooling, in which differences between groups are ignored, and no pooling, in which data from different sources are analyzed separately. As we shall discuss, both these approaches have problems. However, the extreme alternatives can be useful as preliminary estimates.

The rest of the article is organized as follows. In Section 2 we explain our methodology to select the variables studied in this work, how simple and complex models interact between them, and the criterion used to compare different models. In Section 3 we introduce the hierarchical model as a trade-off between no pooling and complete pooling models. In Section 4 we present a hierarchical model that incorporates two non-nested clusters. Section 5 is devoted to Bayesian hierarchical regression. Finally, in Section 6 we discuss the principal insights observed throughout this work.

2 Methodology

With the proliferation of Bayesian methods (see [32] for a list of open Bayesian software programs), they have become easier to build and implement than to understand what they are doing. In an attempt to narrow this gap, in this work we present a comprehensive framework for hierarchical models. Thus, we do not only show how to implement these models, but also how to interpret the parameters according to the level where they belong in the hierarchy and their relation with other parameters.

Instead of starting directly with the hierarchical models, we begin with the extreme cases of no pooling and complete pooling. It is only after analyzing their implications and their lack to explain adequately certain aspects of the data, that we introduce the hierarchical models as a way to mitigate these problems. Thus, every time we introduce a new hierarchical model is always as an extension of a previous one.

Noninformative priors (also known as reference priors or objective priors) are notoriously difficult to derive for many hierarchical models. Thus, throughout this work, we present an approach in which simpler models are used for prior specification in more complex models. This contrasts with the most common approach to prior specification in which a prior distribution is selected because it has been previously used in the literature. Based on the assumption that the community of people using that prior are doing it for a good reason. However, as pointed out by [33], most of these priors have been chosen for specific problems and might be inappropriate for others. Furthermore, as commented by [34]:

There’s an illusion sometimes that default procedures are more objective than procedures that require user choice, such as choosing priors. If that’s true, then all “objective” means is that everyone does the same thing. It carries no guarantees of realism or accuracy.

As commented by [35], hierarchical models allow a more “objective” approach to inference by estimating the parameters of prior distributions from data rather than requiring them to be specified using subjective information. Moreover, in hierarchical models where priors depend on hyperparameter values that are data-driven avoids the direct problems linked to double-dipping [32]. Therefore, our approach follows the tendency by part of the Bayesian community to move from noninformative priors [14, 34, 36, 37]. We do not claim that the proposed approach is optimal. Instead, we make the more modest claim that it is useful for practical purposes.

2.1 Data and related information

The dataset used throughout this work has been collected in 2022 by Thai government agencies. The main purpose of this dataset is for supporting government policy makers to calculate MPI to support poverty alleviation policy making in the Thai People Map and Analytics Platform project (www.TPMAP.in.th) [13]. The original dataset has 12,983,145 observations (each one corresponding to a household). However, there were 569 households that declared having no-income, which represents 0.0044% of the observations. We consider this percentage negligible and do not consider them for further analyses. The number of households consulted for each province goes from 44,012 up to 645,433, then, for all practical purposes, we can ignore the uncertainty within each province.

2.2 Comparison of models

Since different models are implemented for the same data and variables, we need to develop a methodology that allows us to compare them. For this purpose, we considered the Widely Applicable Information Criterion (WAIC), renamed in [38] as the Watanabe-Akaike Information Criterion. This information criterion allows a fair comparison between models of different complexity. Compared to other information criteria like the Akaike Information Criterion (AIC) [39], WAIC averages over the posterior distribution rather than conditioning on a point estimate (like the maximum likelihood estimator), making it a more suitable criterion for Bayesian models. Moreover, AIC is defined relative to the maximum likelihood estimate and so is inappropriate for hierarchical models. In Section A.1 we provide further details about the WAIC.

We emphasize that the WAIC is just another statistical summary of our models, and it is not, in any way, a substitute of an appropriate analysis of the models and their results. If we find that the model does not fit for its intended purposes, we are obliged to search for a new model that fits. Then, understanding different aspects of the models and their implications must be the principal guide for their selection and comparison. See [40] for further discussion on Bayesian predictive model assessment, selection, and comparison methods.

2.3 Variables to analyze

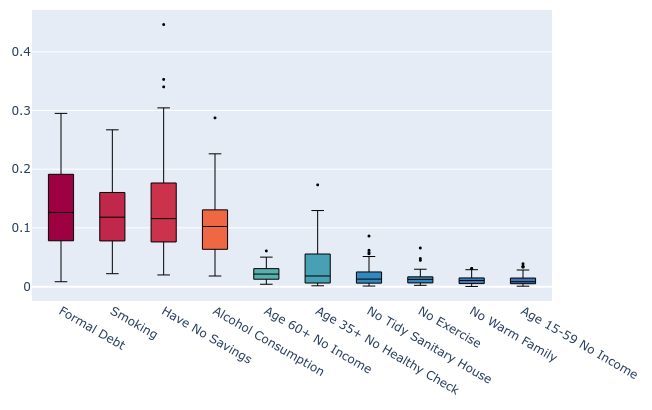

For its direct relation with poverty, we exemplify our methodology throughout this work considering the monthly average income in households. However, this approach is suitable to be applied to a widely variety of variables. To decide the variables where to apply our methodology, we first calculated the percentage of households in each province affected by the variables considered in the dataset. In Figure 1, we present boxplots for the 10 issues with the largest percentage.

Due to the large percentage of households affected by (having) formal debt, smoking, having no savings, and alcohol consumption, as well as their large variance between provinces, we also analyzed these variables with the different models presented in this work. The WAIC for the models implemented on these variables are presented in Table 1.

3 Hierarchical model with one cluster: income per region

3.1 No pooling model and complete pooling model

3.1.1 No pooling model

Let be the average household in the province , which belongs to the region , each region with observations. We consider 6 regions for Thailand: Northern Thailand, Northeast Thailand, East Thailand, Central Thailand, Western Thailand and Southern Thailand.

Before jumping directly into our hierarchical model, we first consider separate independent models for each region. Thus, each region has its own mean and its own variance . We assume that denotes a normal distribution with location and scale ., . This model is represented graphically on the left of Figure 2. For a simple model like this, we can consider vague noninformative priors without any harm, thus we use the well-known noninformative prior denotes the indicator function, defined as for some set where is properly defined.

It is not difficult to prove that the conditional posterior distributions for each and are given byInverse- denotes a scaled inverse distribution with degrees of freedom and scale .

where

Which makes it straightforward to simulate from the joint posterior distribution using Gibbs sampling [41].

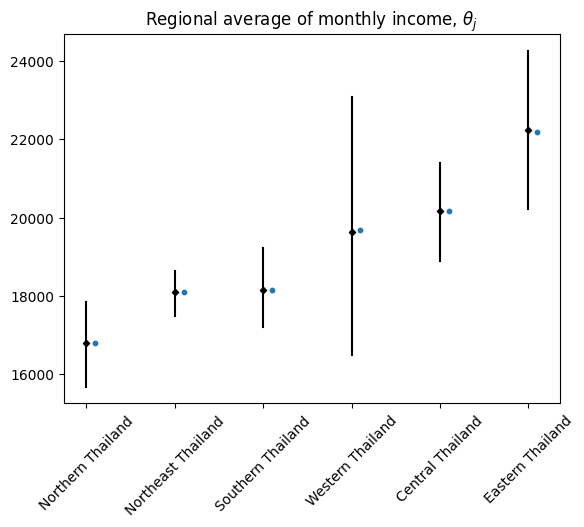

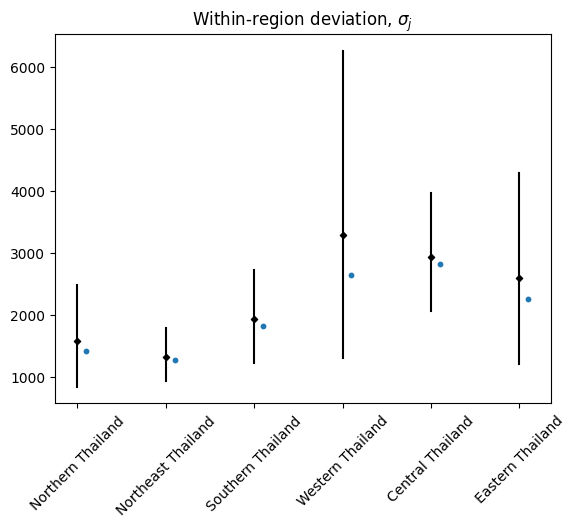

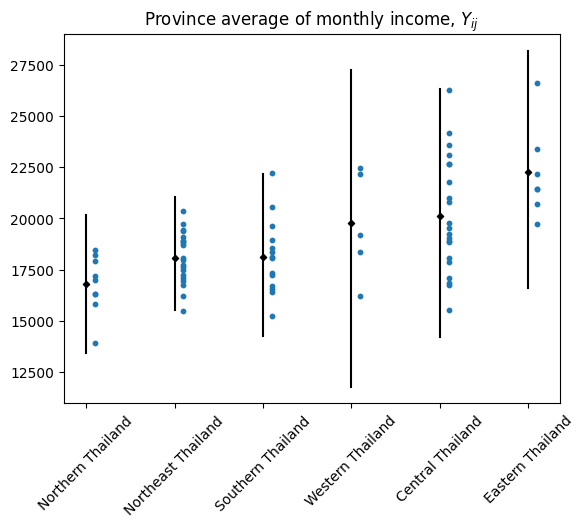

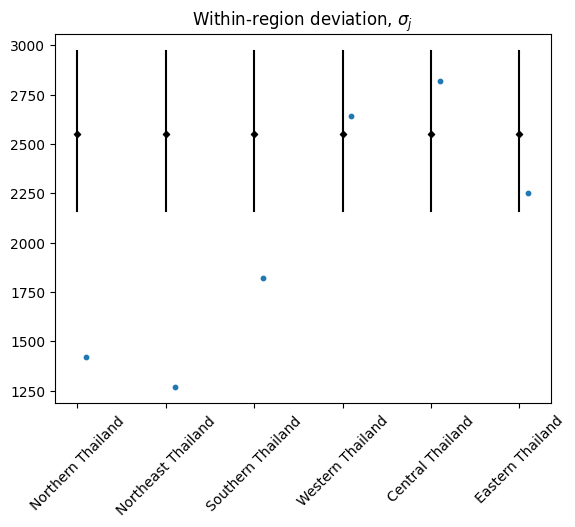

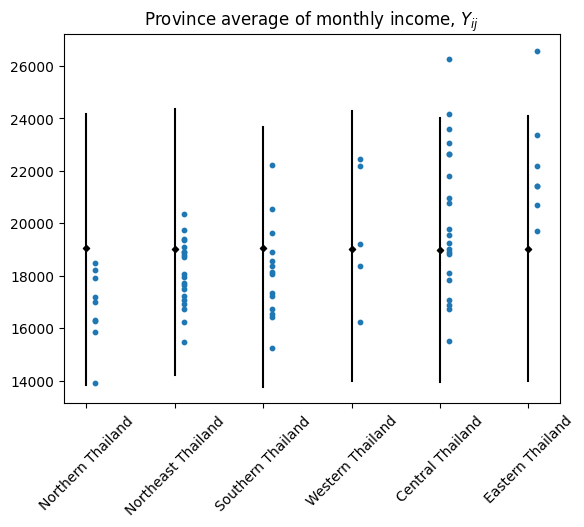

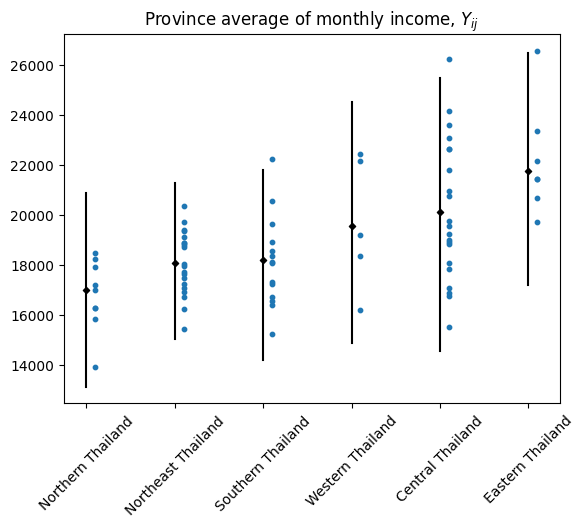

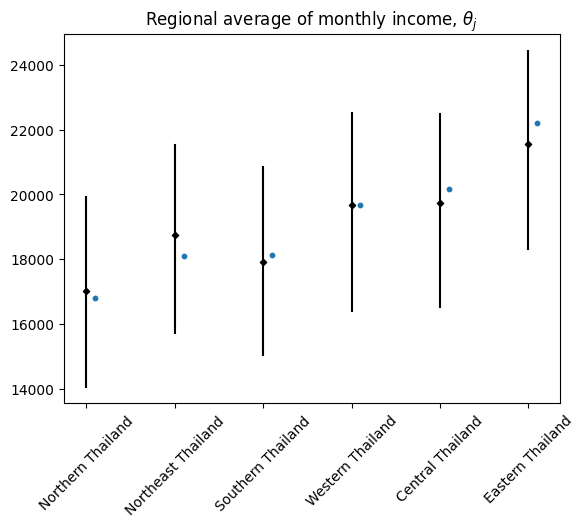

On the top left of Figure 3, we present the estimated mean for each region, , with a credible interval of 0.95 posterior probability. We observe that, since we considered noninformative priors, the estimations are centered on the observed regional averages. Note also that, because the regions share no information between them, credible intervals are large, especially for regions with few provinces. On the top right, we present a similar plot for the standard deviation for each region, . On the bottom, we present credible intervals for the average monthly income in each region. We present these credible intervals with the observed average for the provinces belonging to the region.

3.1.2 Complete pooling model

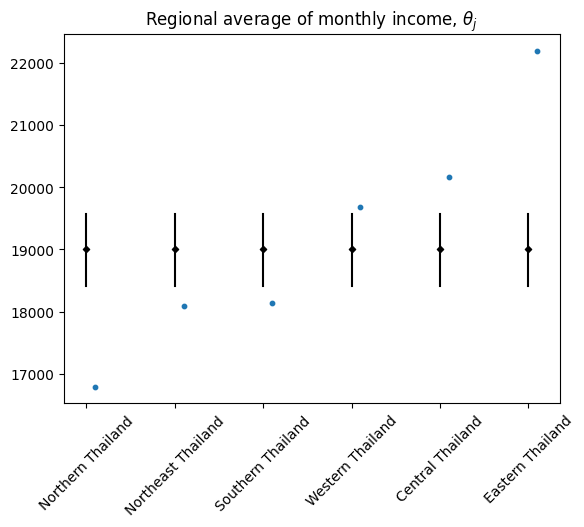

We can observe in Figure 3 that the intervals overlap for most of the regions. This overlapping suggests that all the parameters might be estimating the same quantity. In fact, it is highly unlikely that the regions are independent between them, which makes difficult to justify an independent model for each one. Thus, we can consider the complete pooling model, in which all the regional means, , and their variances, , are equal to some common values and , respectively. That is, for the complete pooling model, we assume that . Similar to the no pooling model, the complete pooling is represented by the graph on the left of Figure 2, with the constraints that and for all .

For this model we still consider the noninformative prior distribution for and ,

It is not difficult to prove that the conditional posterior distribution of is given by , where

while the conditional posterior distribution of is given by , with

Once again, having access to the conditional posterior distributions allows us to simulate from the joint posterior distribution using Gibbs sampling.

We present in Figure 4 the analogous results of Figure 3 for the complete pooling model. Comparing both Figures, we observe much narrower intervals (also calculated at a 0.95 posterior probability), this is because now we are using all the observations to estimate the same common quantities, reducing the uncertainty significantly. However, we observe that the common mean can barely explain the mean of a few regions, being an unreliable estimate for the regions with the largest and smallest means. We can also observe that the estimator of the common within-region deviation is not centered around the average of the observed sample deviations, but upward. This is because now that we have constraint the regional means to be all the same, the only way to explain the variation throughout the observations is by estimating a higher value for the common deviation . Note also, on the bottom row of Figure 4, that all the provinces in Northern Thailand are on the below half of the credible interval, while all the provinces in Eastern Thailand are above. We can conclude from all these observations that a complete pooling model is inappropriate.

3.2 Hierarchical model with common within-cluster variance

Because considering independent models for each region seems difficult to justify and we observe a poor performance for the complete pooling model, we consider as a better approach a model that makes a trade-off between these two extreme cases. A hierarchical model achieves this compromise.

Instead of adding a hierarchical structure to all the parameters, we propose to add it to one parameter first, and consider more complex models only as suggested by the data after analyzing the results of the previous model. For this reason, we maintain a common within-region variance , but consider different regional means, . However, these means are not independent, instead they share a common structure. From a statistical perspective this means to abandon the noninformative prior for and consider a distribution that depends on some hyperparameters, as it is represented by the graph in the center of Figure 2.

For the simplicity of a conjugate model [37], we consider the prior . In this model, represents the national average of the monthly income and represents the between-regions deviation. For the within-regions variance, we still consider the noninformative prior

To complete our model, we must assign prior distributions for and . However, we must be careful since the usual noninformative distributions for location and scale parameters might lead to the non existence of the posterior distributions. For example, using the usual noninformative prior of a variance parameter for , yields an improper posterior distribution. Meanwhile, the vague prior

generates a proper posterior distribution, thus we use this prior for . For , we use the usual noninformative prior

In Section A.2, we present an empirical approach (developed in [37]) to estimate these parameters, and explore in more detail the qualitative implications of the priors and the values taken by the parameters in the hierarchical models.

With this model, the following conditional distributions for the parameters can be deduced [37].

Conditional posterior for

where

| (1) |

Conditional posterior for

where .

Conditional posterior for

where , and

Conditional posterior for

where

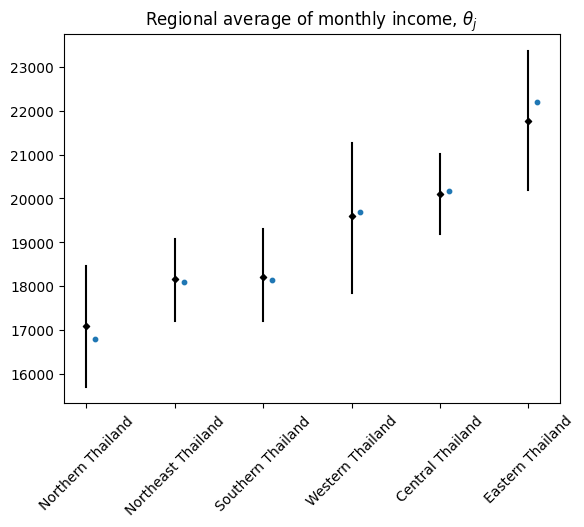

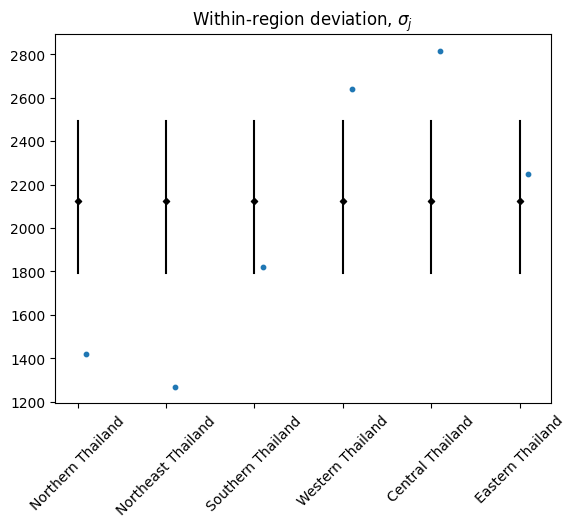

As we did with the previous two models, we present in Figure 5 the estimated mean for each region, , the estimated common within-region deviation , and the average province monthly income, all of them with their respective credible intervals of 0.95 posterior probability. For the regional means, we can observe that the uncertainty is considerable less that when we considered independent analyses (see Figure 3) without having a poor performance as the complete pooling model. Also, since we accept different means for each region, now the common variance is not overestimated. However, we can observe that a common variance is infeasible to explain the observed variability for most of the regions.

3.3 Hierarchical model varying within-cluster variance

Because a common within-region variance seems infeasible, we can impose a hierarchical level to it, similarly as we did with the regional means. Thus, we allow each region to have its own variance , but all of them sharing a common structure. For simplicity of a conjugate model, we consider the following prior distribution

This model is represented graphically on the right of Figure 2. These graphical representations, called Bayesian networks, meet two objectives. First, they visualize easily the hierarchical relations between variables, which helps with the interpretation of the parameters and the understanding of the model. Second, they allow us to use -separation rules [42] to deduce the conditional independence between the parameters. We suggest [43] and [44] for gentle introductions to Bayesian networks and -separation.

Consider, for example, the graph presented on the right of Figure 2, while a priori is independent of , we can see that conditioning on creates a dependence between both parameters, that is , but . However, if we condition on both and , is independent of and . This implies that the full conditional posterior of is exactly the same as in the model of Section 3.2, which assumes the same variance for all the regions (with the minor change of defining instead of ). Using the same reasoning, it is easy to see that the posterior distributions of and are also the same as those presented in Section 3.2.

Therefore, we only need to calculate the posterior distributions of , and . Due to the conjugacy property of the model, it is not difficult to prove (see [37]) that

where

To complete our model, we must assign prior distributions for and . Note that, considering the Bayesian network associated to the model, and -separation, it is easy to see that once we condition on , is independent of all the other variables and parameters of the model, except for . For , we can prove (see Section A.3.1) that the vague prior

yields the conditional posteriorGamma denotes a gamma distribution with shape parameter and rate parameter .

where

Unfortunately, the conditional posterior of is far more complicated, let be , then

This is an intricate expression, which gives little guide for the selection of a prior distribution for yielding a proper known distribution.

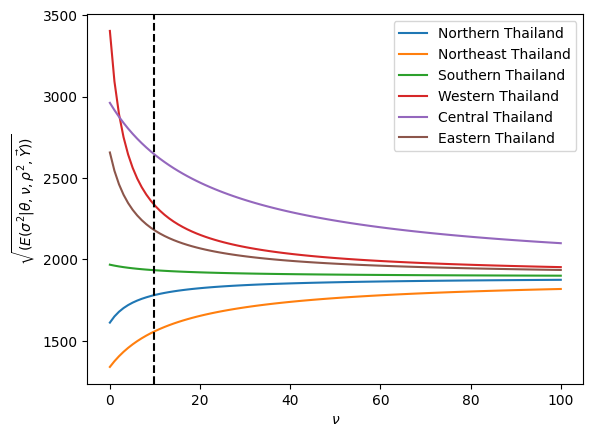

In general, it remains challenging to propose noninformative priors for the degrees of freedom of a distribution. In [45] the authors present different proposals for the degrees of freedom of a -distribution under certain conditions. Notably, in [33], the authors present a process to build objective priors, which they called Penalised Complexity or PC priors. Let as it be, these approaches do not necessarily applied for the degrees of freedom of an Inverse- distribution. Thus, in this work we consider three different approaches to propose a prior distribution for .

3.3.1 Estimating and : the hierarchical model with fixed

Because , we can use the method of moments to estimate and . Let be the average of the observed sample within-group variances, , and their variance, using the method of moments (see Section A.3.2), we get the following estimates

| (2) |

and

| (3) |

Thus, the first option considered in this work is to fix the value of to its empirical estimator.

3.3.2 Using a vague improper prior for

Setting to a fix value like ensures us that the posterior distribution would exist for all the parameters, except which is no longer modeled as a random variable. This means that, setting the value of to a fix value, eliminates the uncertainty that we have on that parameter, and makes our model overconfident because it acts as if would be the real value of . For this reason, the second approach in this work is to consider a vague prior for .

For modeling the degrees of freedom of a multivariate -distribution, [46] proposed the prior , while [47] proposed to use . Thus, we proposed a prior for of the form , fixing the value of . We have seen in simulations that large values of tend to make each within-variance, , to concentrate in the observed sample variance at the cost of increasing the uncertainty in their estimates. Meanwhile, smaller values for have the opposite effect, generating models that are closer to the case where a single common within-variance, , is considered for all the groups. However, even while it seems as a reliable approach in the simulations, we do not have any guarantee that the posterior distribution would exist using these improper priors. For example, the limit case , corresponding with the prior , generates an improper monotonically increasing posterior for , which makes all the within-variances to concentrate in a common-variance quantity. In this work we present results for .

Note that performing Gibbs sampler for this approach is still possible. To sample from the distribution of , we could use a grid of values and sample them with a probability proportional to the (conditional) posterior of those values. However, this requires the extra-effort of finding an appropriate grid.

3.3.3 Using a regularizing prior for

Because setting the value of to a fix value, , eliminates the uncertainty on , and using an improper distribution does not gives guarantee for the existence of the posterior distribution, the third option that we propose is to use a regularizing prior for .

A regularizing prior is a prior distribution whose parameters are learn from the data, which might prevent overfitting [34, 36]. With this approach, we maintain the uncertainty on with the guarantee of the existence of the posterior distribution. In this work, we consider an exponential distribution whose rate parameter is set at , but other distributions might be considered as well.

As commented previously, using Gibbs sampler is still feasible, but requires an extra-effort of finding an appropriate grid of values to sample from. However, we can use other Monte Carlo techniques to simulate from the joint posterior distribution. For this purpose, we used No U-Turn Sampler (NUTS) [48] which is a Hamiltonian Monte Carlo technique [49], implemented in the library PyMC (formerly PyMC3) [50].

3.4 Comparison of models

We implemented the discussed models for the variables selected in Section 2.3 and calculated the WAIC for each one of them. We present in Table 1 these values. We show in bold the lowest value of the WAIC for each variable, which corresponds with the preferred model according with this criterion.

| No | Complete | Hierarchical | Hierarchical | |

|---|---|---|---|---|

| Pooling | Pooling | common | fixed | |

| Monthly Income | 1382.01 | 1410.13 | 1386.44 | 1378.58 |

| Percentage with Formal Debt | -216.66 | -183.14 | -217.39 | -221.02 |

| Formal Debt | 1795.12 | 1816.79 | 1790.54 | 1790.54 |

| Percentage without Savings | -189.07 | -149.70 | -191.04 | -193.89 |

| Yearly Savings | 1515.78 | 1519.94 | 1518.12 | 1512.98 |

| Smoking | -265.82 | -217.48 | -262.48 | -267.08 |

| Alcohol Consumption | -244.94 | -223.07 | -252.58 | -250.27 |

| Hierarchical | Hierarchical | Hierarchical | Hierarchical | |

|---|---|---|---|---|

| Exponential() | ||||

| Monthly Income | 1379.21 | 1380.30 | 1380.15 | 1380.31 |

| Percentage with Formal Debt | -221.04 | -219.30 | -220.08 | -219.97 |

| Formal Debt | 1790.54 | 1792.28 | 1791.51 | 1790.73 |

| Percentage without Savings | -193.98 | -191.80 | -191.86 | -192.60 |

| Yearly Savings | 1513.16 | 1513.94 | 1513.56 | 1514.96 |

| Smoking | -267.70 | -266.74 | -266.99 | -265.20 |

| Alcohol Consumption | -250.43 | -247.72 | -249.07 | -252.85 |

More important that its use for model selection, the WAIC can help us for comparison of models. The objective is not to determine which is the correct model, a statement that is probably false for all the models, especially in the field of social science, but to determine which models can be potentially feasible to explain the data.

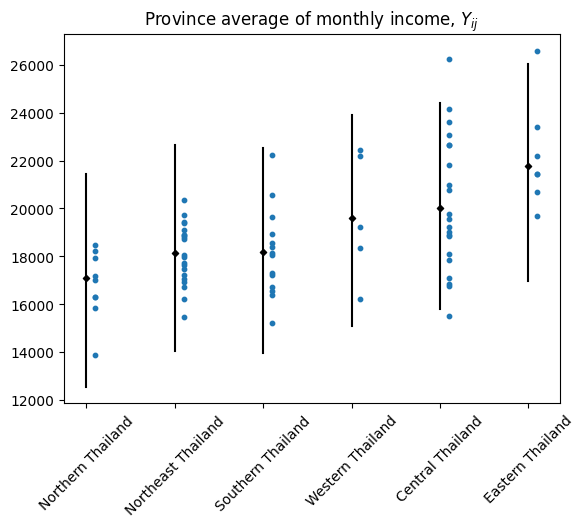

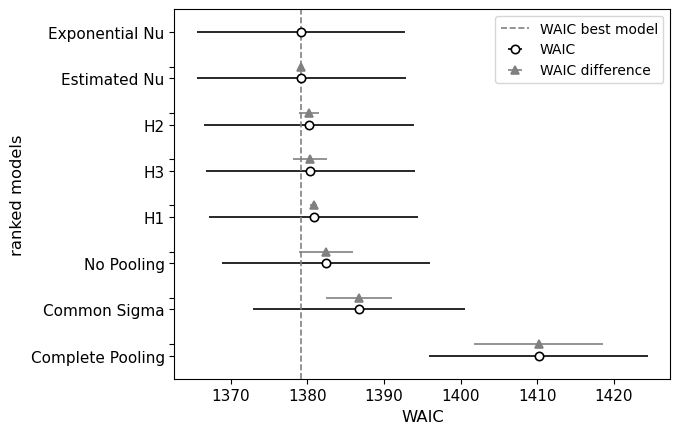

To answer this problem, a punctual value of the WAIC is not enough. Then, in Figure 6, we present the credible intervals for the WAIC (at a 0.95 posterior probability) of the implemented models for the monthly income variable. The model with the lowest WAIC is when we fix to the estimate value . However, all the hierarchical models that introduce a multilevel structure in the regional means and the within-region variances are feasible for explaining our data. Meanwhile, the WAIC of the models that assume a common within-variance or complete pooling are far from the preferred one, so we cannot consider them as reliable models for our data.

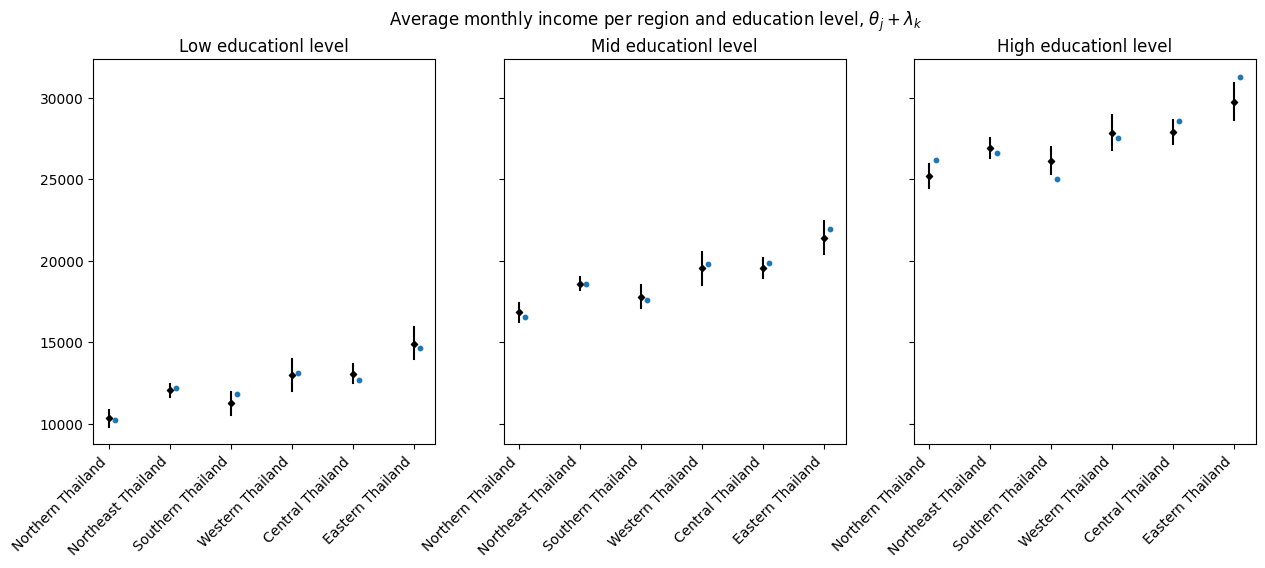

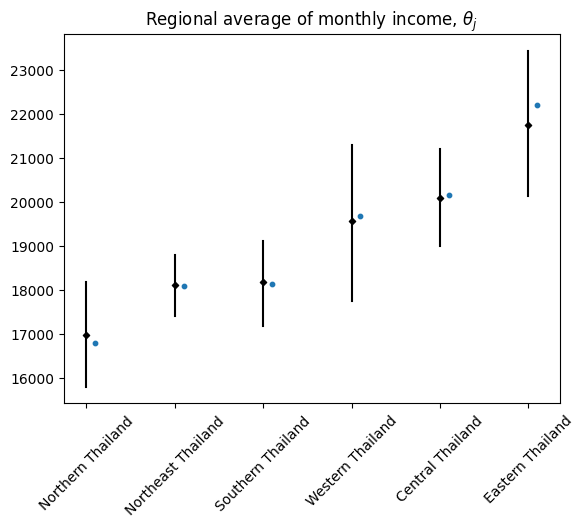

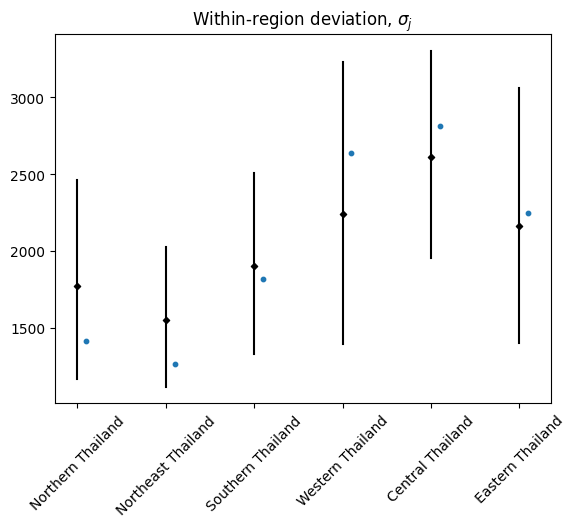

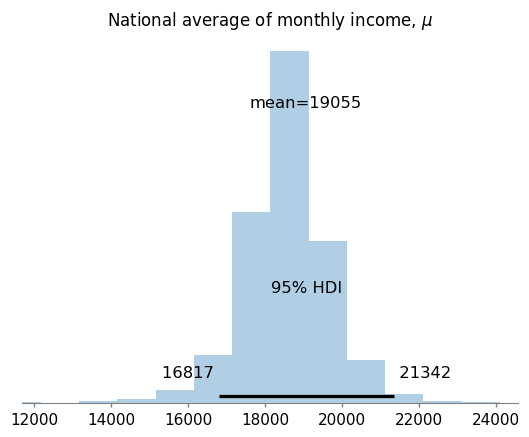

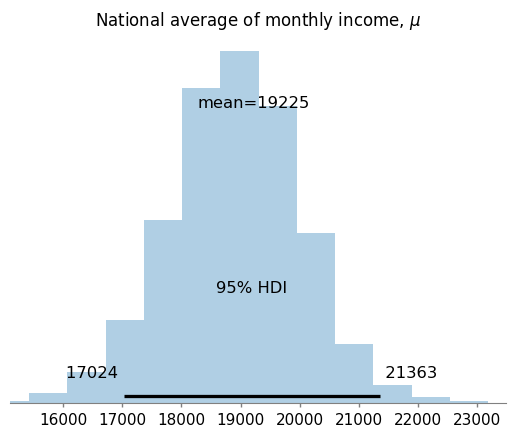

As it is usual now, Figure 7 shows the results of the model with the lowest WAIC for the monthly income variable. On the left of the top row we present the regional mean of the monthly income, while the deviation within each region is presented on its right. We observe that the model can explain not only the observed average in each region, but also its variability. On the left of the bottom row we show the average monthly income per province in each one of the regions. An important difference from the complete pooling or no pooling models, is that the hierarchical model explicitly add parameters that model the national behavior. For example, the parameter models the national average monthly income, whose posterior distribution is presented on the right of the bottom row in Figure 7.

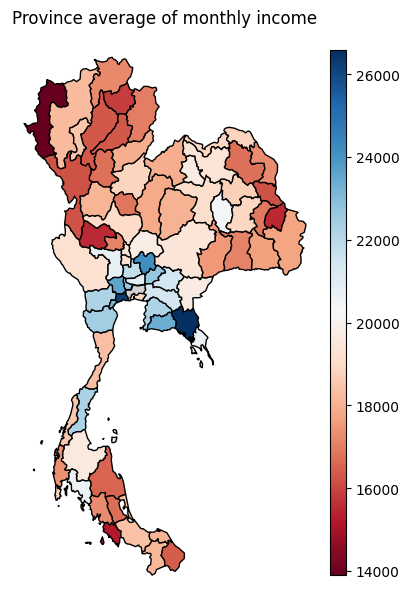

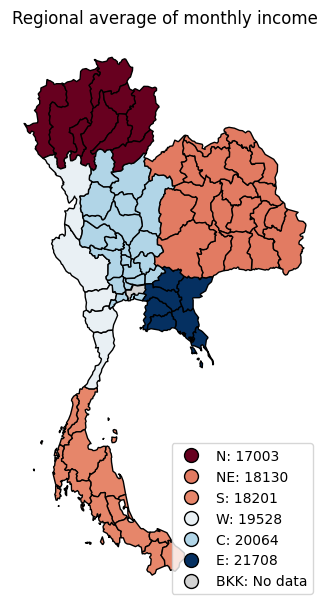

Finally, Figure 8 presents two maps of ThailandSource for the raw map of Thailand: https://github.com/cvibhagool/thailand-map, the observed average income per province is presented on the left, while the regional average income is presented on the right.

4 Hierarchical model with two non-nested clusters: income per region and education level

In this section we extend our hierarchical model to estimate the income not only by region, but also by education level. From a statistical perspective adding the education level to our model means that we add another cluster to the model which do not hold a hierarchical structure with the first one. For this purpose, we have assigned the observations to one of three mutually exclusive groups according to the highest education of the people in the house. We have called this variable education level, whose possible values are low, mid or high, and whose assignation is done accordingly to the rule presented in Table 2

In Table 3, we present the percentage of the population belonging to the different levels of education, we can observe that approximately half of the population belongs to the mid education level, i.e. they completed elementary school but do not hold a bachelor or post-graduate degree, with the other two groups representing a significant percentage of the population each one. The percentage of the population with a low education level rounds 27% while the percentage for those with a high education level is around 22%. Thus, the amount of observations belonging to each group is large enough to achieve reliable results per education level.

| Education | Years of education | Education level |

|---|---|---|

| Uneducated | 0 | Low |

| Kindergarten | 0 | |

| Pre-elementary school | 3 | |

| Elementary school | 6 | |

| Junior high school | 9 | Mid |

| Senior high school | 12 | |

| Vocational degree | 14 | |

| Bachelor degree | 16 | High |

| Post-graduate | 19 |

| UN-EDU | KDG | P-ELEM | ELEM | JHS | SHS | VD | BD | PG |

|---|---|---|---|---|---|---|---|---|

| 0.82% | 0.03% | 2.25% | 23.65% | 17.35% | 23.94% | 9.88% | 20.97% | 1.11% |

| 26.75% | 51.17% | 22.08% |

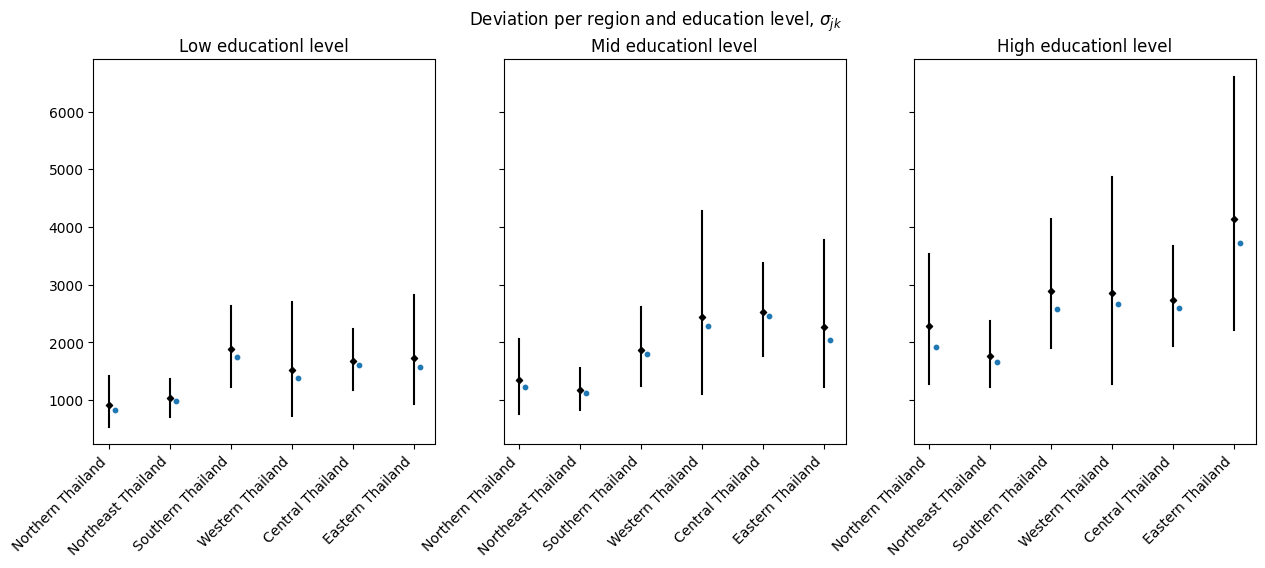

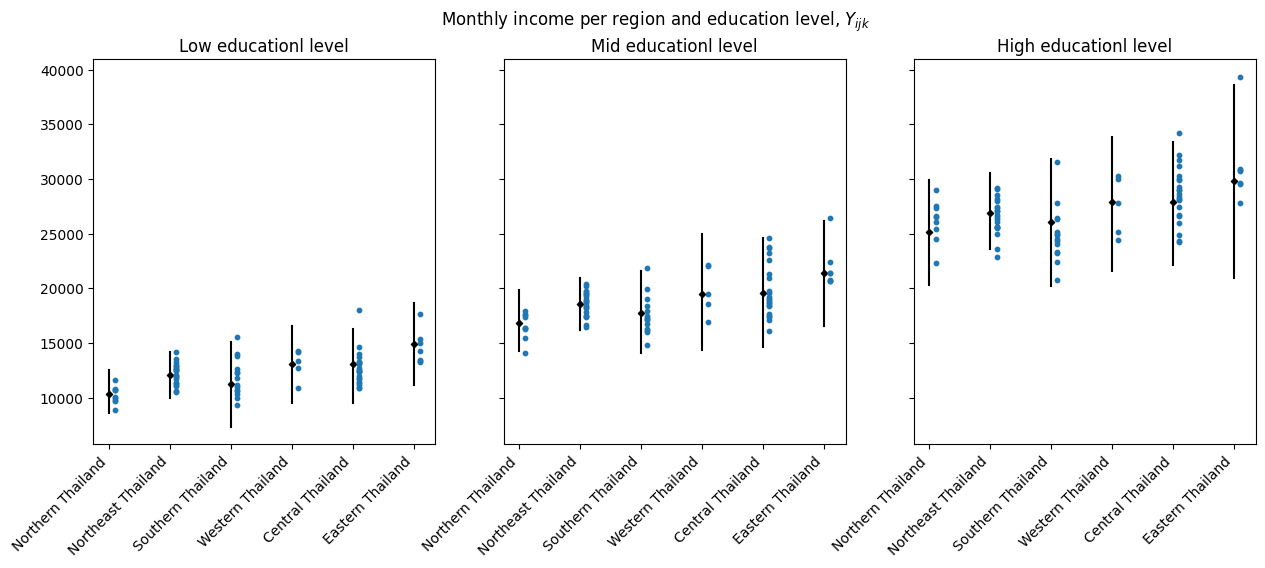

Let be the average income in province the , belonging to region , when the education level is equal to . We maintain the hierarchical structure for both the regional mean and the within-region variance. But in this case, we allow the variance, , to vary not only between regions but also between education levels. We now present our hierarchical model, whose Bayesian network is shown in Figure 9:

We proceed to explain the different parts of this model and how the hyperprior distributions where setting.

Likelihood.

The first line of our model corresponds with the likelihood. We model as a normal variable with variance , and mean . The average monthly income of region is still modeled by , while is interpreted as the additional income due to the education level.

Prior distribution for .

For the regional average monthly income we use a normal distribution as before, with mean representing the average national monthly income, and variance representing the variance of the monthly income between regions.

Prior distribution for .

To establish the prior distribution for we use the hierarchical model proposed in Section 3.3. Then, we use the posterior sample of , being its average and its variance.

Prior distribution for .

Similarly to the prior distribution of . To establish the prior distribution for we use one more time the hierarchical model proposed in Section 3.3. Then, we use the posterior sample of , being its average. Note that, in this way, we use previous simpler models as building blocks to construct the priors of more complex models.

Prior distribution for .

Consider the mean of , , and note that because and follow normal distributions, it can be written as

where and are independent standard normal variables. From this expression, it is easy to observe that we have set the mean of to zero to have an identifiable model. If, on the other hand, we introduce a non-zero mean for , we would not have any way to distinguish between both and this new hyperparameter.

For a fix , we can estimate as follows. We first implement the hierarchical model proposed in Section 3.3 but only for those observations whose education level equals , let be the national monthly income for this model. On the other hand, we implement the same hierarchical model for all the observations (note that this is the model used for the prior specification of both and ). Thus, a punctual estimator for , denoted as , is given by the posterior mean of the variable .

Prior distribution for .

Because represents the variance of , we can estimate it with the variance of , denoted as . Then, for the prior distribution of we use an exponential distribution with rate .

Prior distribution for .

For this model, we assume that the within-region variance can vary not only between regions but also between education levels. For the prior of we use the usual inverse- distribution presented in Section 3.3.

Prior distribution for .

For a fix , we estimate through Equation 2 considering those observations whose education level equals . An exponential distribution with rate parameter equal to is used as proposed in Section 3.3.3.

Prior distribution for .

For , we use the vague prior , which yields a proper posterior distribution.

We show in Table 4 the WAIC with and without considering the education level. We observe that considering the education level leads to a huge reduction of the WAIC, preferring the model that incorporates both clusters. Note that the values of the WAIC are around three times those presented in Table 1 for the monthly income variable. However, these quantities are not comparable. The reason is that when the education level is considered we have the union of three datasets, one for each education level for the 76 provinces. Then, the model which incorporates the education level has three times the number of observations of the models that do not incorporate it, making the WAIC incomparable between both set of models.

| Without | With region and | |

| education level | education level | |

| Monthly Income | 4662.59 | 4096.79 |

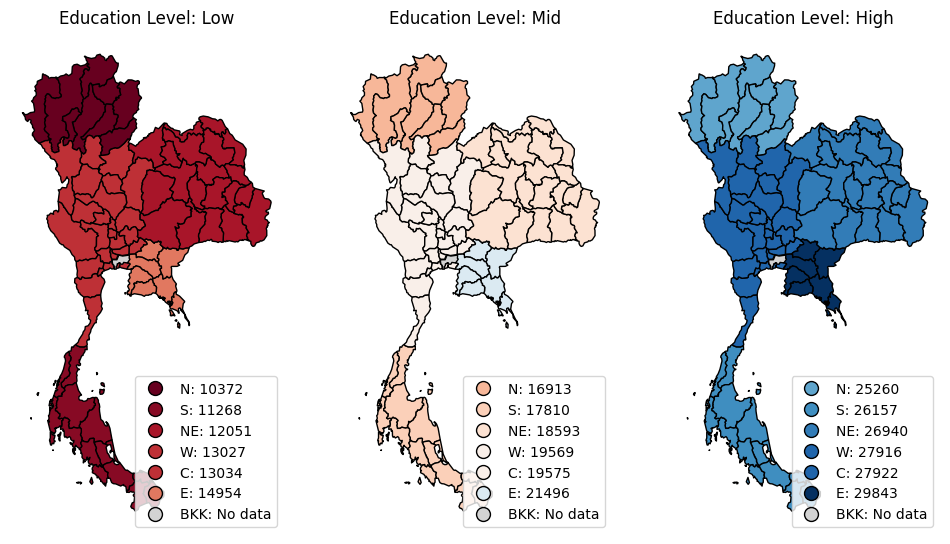

In Figure 10 we present the estimated monthly income at a national (left) and regional level (right). A close inspection reveals a similar distribution for the national average compared with the results presented in Figure 7. However, the regional averages show more overlap, this indicates that, once we consider the education level, the region has less impact in the income. This might be the result of a mediation relation, in which education level acts as a mediator between the region and the income. This same phenomenon can be observed in Figure 11 with more color-homogeneous maps for each education level, but with large differences between them. For those readers interested in causal inference, we recommend [44, 51, 52].

In Appendix B we present supplementary Figures for this model.

5 Bayesian hierarchical regression: income considering years of formal education

5.1 National model and separate models

Instead of considering the education as a categorical variable, we can approximate the years of formal education received, using the rule presented in Table 2, called this new variable . Then, we can implement a regression model that estimates the income taking as input the years of education.

According to our proposed procedure, before presenting the full hierarchical model, we first consider two simple models. The complete pooling model and separate independent models for each region. These models are represented graphically in Figure 12.

5.1.1 National model

Let be the average years of formal education in the province belonging to region . The complete pooling model means the implementation of a single regression function that models the national relation between the income and the years of formal education. With this simple model, we can use vague priors for the parameters without harmful. We introduce now our national model:

The expected income is modeled through the regression function that takes as input the years of education , for simplicity we have considered a linear function for the regression, given by , where is the average years of formal education between all the provinces, that is

where . Note that represents the average national income when the years of education equal the national average, while represents the amount of income added per year-of-education.

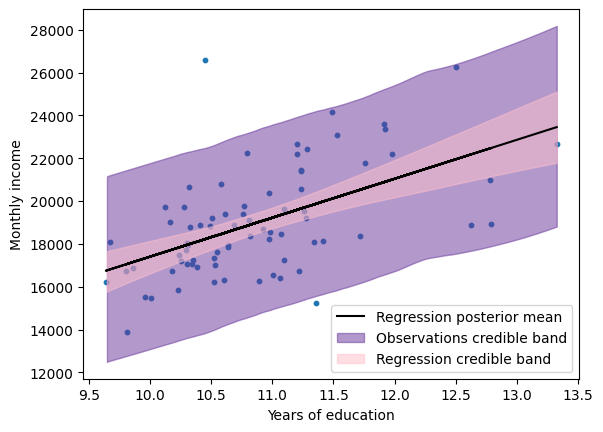

We present in Figure 13 the posterior distributions for and , Figure 14 presents the estimated regression function, we also present credible bands for the regression function and the income, both bands are calculated at a 0.95 posterior probability.

5.1.2 Separate models

Instead of considering just one regression function for all the regions, we can estimate a regression function for each one of the regions, independent from the others. Similarly to the national regression model, for each one of these models we can use vague priors for the parameters without harmful:

We consider a linear function for the regression in each region , given by , where

is the average years of formal education in the region . Note that represents the average income in the region when the years of education equal the regional average, while represents the amount of income added per year-of-education in the region.

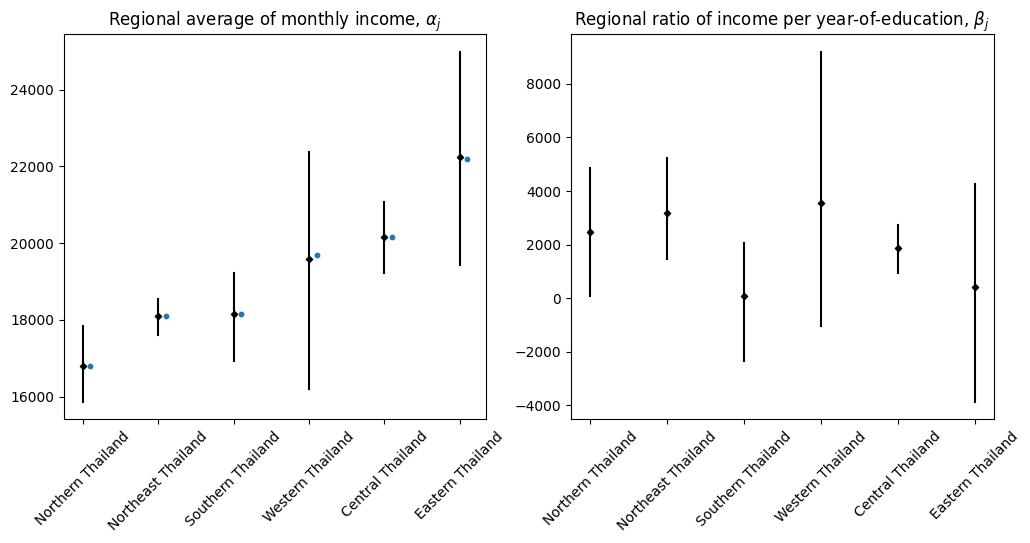

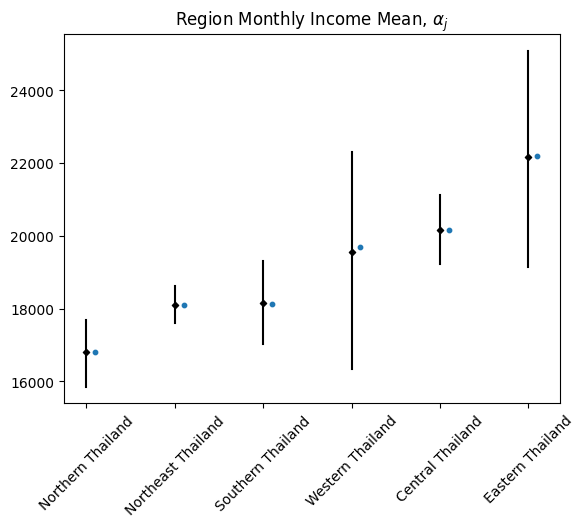

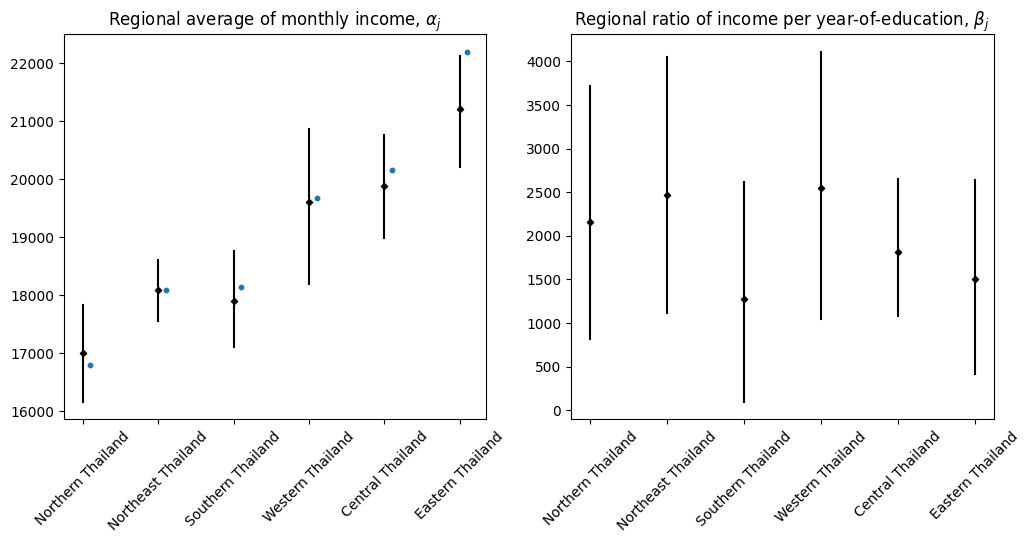

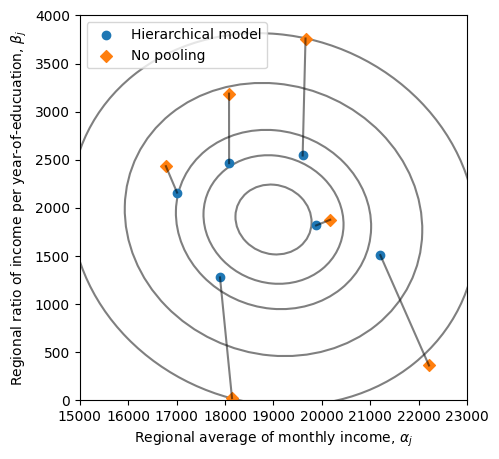

On the left of Figure 15, we present the average monthly income for each region when the years of education are equal to the regional mean, , with their respective credible intervals of 0.95 posterior probability and the observed average income in each region. Analogously, on the right we present the ratio of income per year-of-education, . Because this model assumes that the regions do not share any information, we observe large credible intervals, for some regions like Southern Thailand or Eastern Thailand these intervals even include negative values, which seems implausible. Moreover, as we pointed before, pretending that each region is independent for the others seems unrealistic. Therefore, we introduce the hierarchical regression model as a compromise between a single regression model and an independent regression model for each region.

5.2 Bayesian hierarchical regression varying intercepts

We already observed in Section 3.3 that adding a common structure to the region average income and to the within-regions variance results in a better model, so we can implement a model with those characteristics for the regression task. This model is represented graphically in Figure 16.

We now present our hierarchical model for the regression task:

Many parts of this model have been inherited from our previous hierarchical models. Then, we explain only the prior distributions of the hyperparameters that changed from the previous models.

Prior distribution for .

Note that has a similar interpretation than the intercept parameter in the national regression model. Thus, we set and to the mean and deviation (respectively) of the intercept parameter in the national regression model.

Prior distribution for .

Note that models the variance between . Then, we can estimate this quantity from the no pooling regression model. To do so, we first compute the average for the intercept parameter for each region, and then take the variance between these values.

In Figure 17 we present analogous graphs of those presented in Figures 13 and 15. Note that the distribution of includes negative values, which could indicate that different slopes should be preferred instead of a common national parameter.

5.3 Bayesian hierarchical regression varying intercepts and slopes

Because a common slope for all the regions seems inappropriate for this case, we now present a model that implements a hierarchical model on both parameters, the intercept and the slope. This model is represented graphically in Figure 18.

Instead of just incorporating a normal distribution for the slopes into the previous model, we model the intercepts and slopes through a multivariate normal distribution, allowing them to covary. Then, and will follow a multivariate normal distribution with mean and a matrix of variances and covariances

which can be written as

where

is the correlation matrix.

We are now ready to present our hierarchical model:

Likelihood.

In this model we do not consider anymore a normal likelihood for our data. Instead, we consider a Laplace distribution. The density of a random variable that follows a Laplace distribution with parameters and is given by

This change in the likelihood is analogous to median regression in which the absolute errors are minimized, and thus corresponding to a robust regression model. As mentioned in [53], this can be generalized to other quantiles using the asymmetric Laplace distribution [54, 55].

We can observe in Figure 19 and Table 5 that with this change none of the credible intervals (calculated at a 0.95 posterior probability) for the ratio of income per year-of-education includes negative values, even while a constraint of positive values for these parameters was not incorporated in the model. If instead of a Laplace distribution, we would have considered a normal distribution for the data, some of these intervals would include negative values, which seems unfeasible to explain.

Prior distribution for .

Analogously to the prior distribution for , we set and to the mean and variance of the posterior distribution for the slope parameter in the national regression model.

Prior distribution for .

To set the prior of we follow the same strategy used for the prior of . That is, we calculate the posterior mean of the slopes for the separate independent regression models, and then we set to the variance of these posterior means.

Prior distribution for .

For the prior of we consider the LKJ distribution [56], which is a distribution over all positive definite correlation matrices where the shape is determined by a single parameter, . Setting results in a uniform distribution over all the correlations , however setting is an alternative that has been considered in the literature [34, 57, 58, 59] to define a weakly informative prior over . It implies that is near zero, reflecting the prior belief that there is no correlation between intercepts and slopes.

In Figure 19 we present analogous graphs of those presented in Figure 13. Comparing the credible interval of the slopes, we can observe not only narrower intervals, but also that they contain only positive values, which means that every extra year of education generates a higher income. The credible intervals for the slopes and their posterior mean are also shown in Table 5. The fact that these intervals overlap suggests that this increment in the income is similar for all the regions.

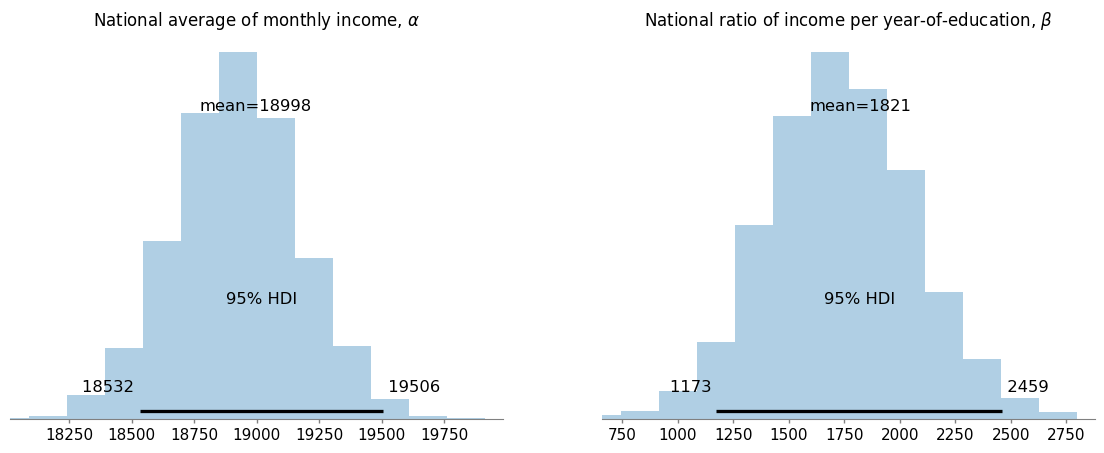

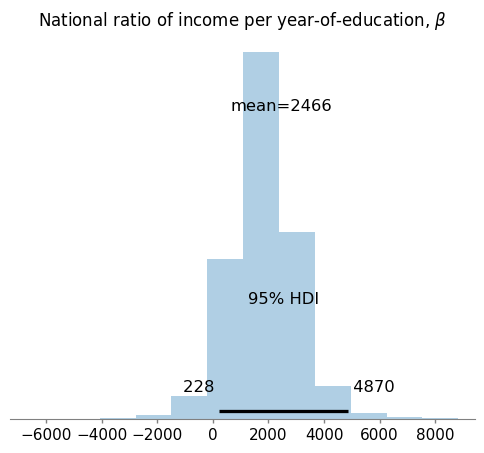

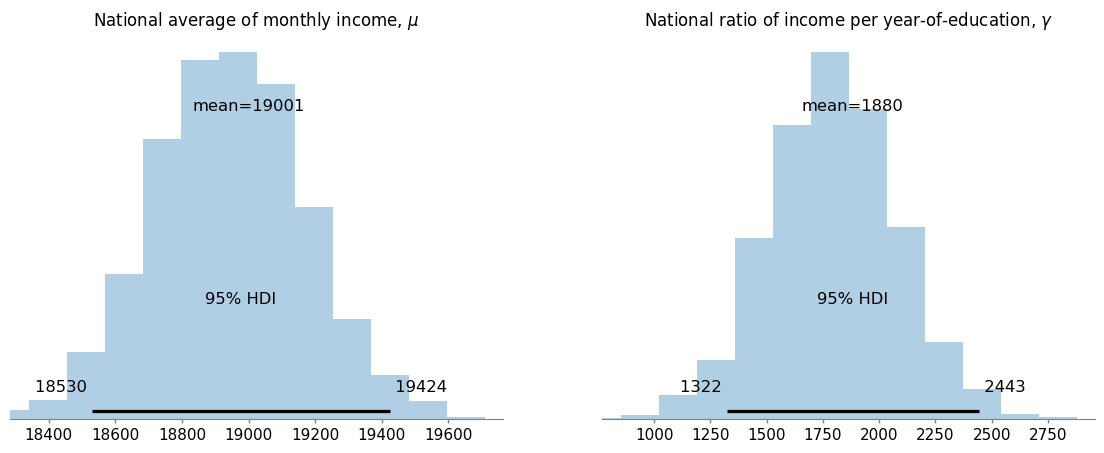

With our hierarchical model, we can estimate the national average income when the years of education equal the national average years, which is modeled by , and whose posterior distribution is shown on the left of Figure 20. On the right side we present the posterior distribution of , which models the national ratio of income-per-year of education.

| Amount of monthly income | |

| added per year-of-education (THB) | |

| National level | 1880; (1322, 2443) |

| Northern Thailand | 2159; (814, 3719) |

| Southern Thailand | 2466; (1111, 4056) |

| Western Thailand | 1278; (94, 2613) |

| Eastern Thailand | 2545; (1051, 4109) |

| Northeast Thailand | 1818; (1076, 2648) |

| Central Thailand | 1509; (413, 2642) |

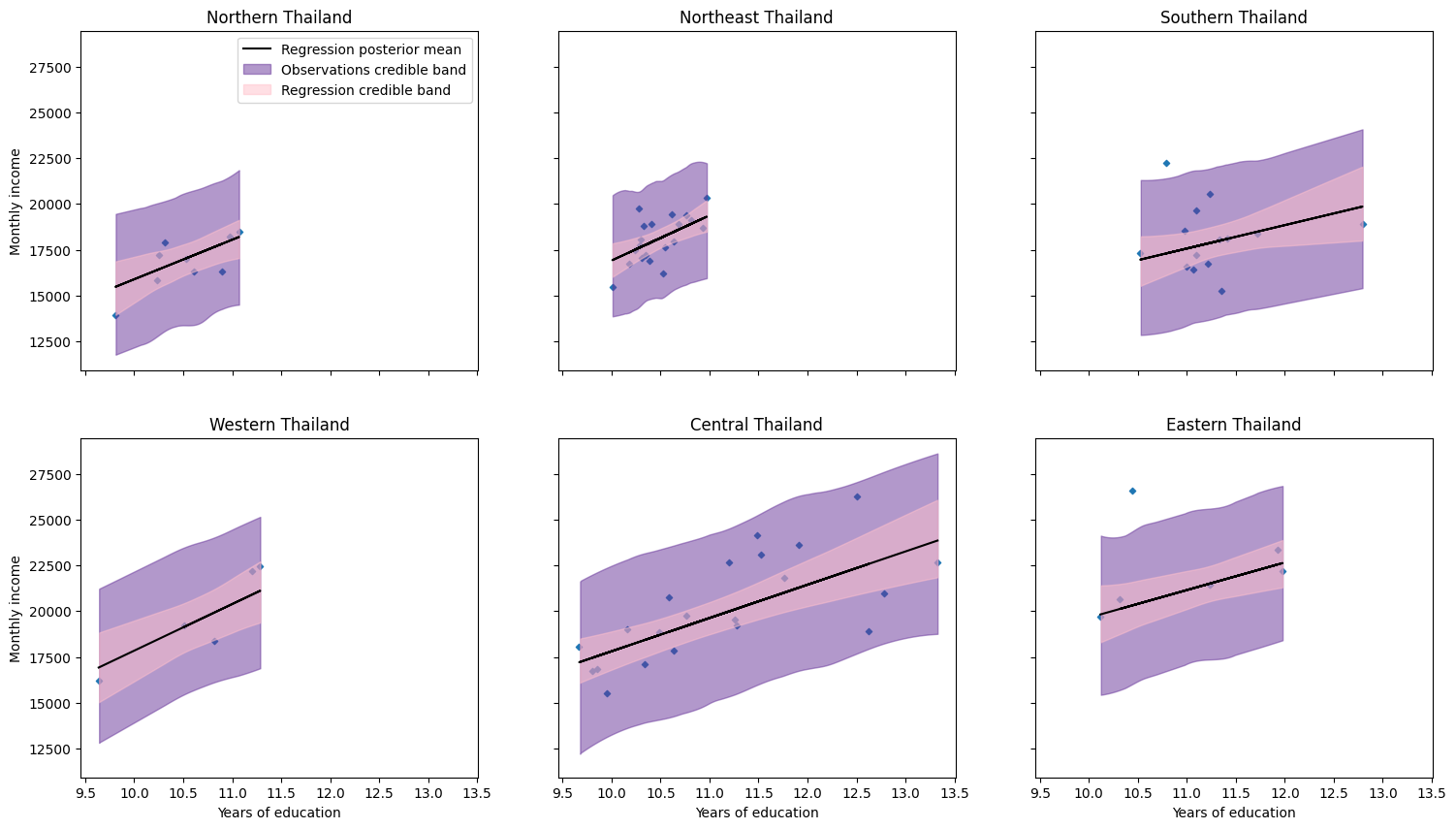

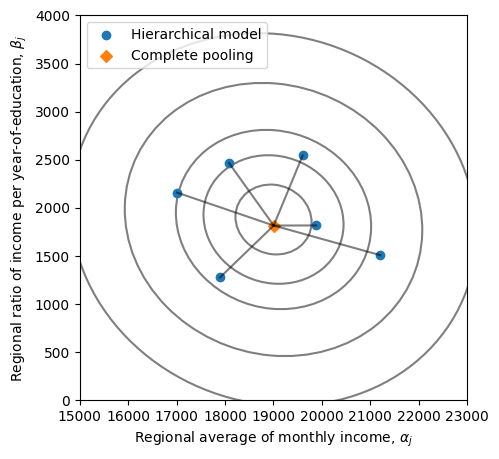

We show in Figure 21 the estimated regression models with credible bands for the regression functions and the province monthly income, both bands are calculated at a 0.95 posterior probability. In Figure 22 we show the joint posterior of the intercepts and slopes. On the left side we show the posterior mean of each pair and compare them to the posterior mean of the pair for the national regression model. Similarly, on the right side we present our estimates for the slopes and intercepts, and compare them with the extreme case of considering separate independent models for each region. We can observe how the estimators are closer to more probable regions when we impose a hierarchical structure.

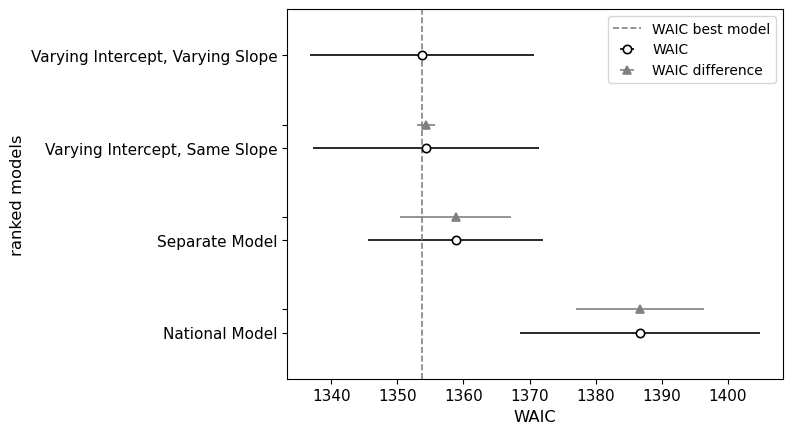

Finally, we show in Table 6 and Figure 23 the WAIC for all the regression models. We also present in Table 6 the WAIC for the preferred model without a covariate variable (see Table 1). Note that the model that allows variation between intercepts with a common slope is as feasible as the model that allows different intercepts and slopes. We observe that, except for the national regression model, all the regression models present a lower WAIC value, making them more reliable models accordingly to this criterion.

| Without | National | Separate | Varying , | Varying , | |

| Covariable | Model | Models | Common | Varying | |

| Monthly Income | 1378.58 | 1387.08 | 1358.77 | 1354.37 | 1353.82 |

6 Discussion of results and conclusions

Throughout this work we presented and discussed several Bayesian hierarchical models. These models were implemented for the variables with the largest percentage of Thai households’ affected. Instead of starting with complex hierarchical models, we first introduced the extreme cases of no pooling and complete pooling models, corresponding to one-shirt-size and custom-made policies, respectively. After analyzing the results of these models and their lack of explanation for certain aspects of the data, the hierarchical models were presented as a better approach, being a trade-off between these two extremes.

In Section 3.3, we extended our previous hierarchical model, incorporating a multilevel structure for the within-cluster variance through an inverse distribution, and proposed three different approaches for the prior specification of the degrees of freedom for this distribution. For the comparison of the models, alongside the analysis and discussion of the results, we used the Widely Applicable Information Criterion (WAIC), which always preferred the hierarchical models for the variables considered. Later, in Section 4, we introduced the education level into our hierarchical model, creating a model with two non-nested clusters. Section 5 was devoted to the discussion of Bayesian hierarchical regression, explaining the households’ monthly income as a function of the years of education. We achieved the best performance when a robust hierarchical regression was implemented.

From these analyses, we could observe the important impact of the education in the income, always showing a positive relation, and which almost vanished the effect of the region in the income. Furthermore, we were able to estimate the average income for each education level and the ratio of income per year-of-education, at a regional and national levels.

Throughout this work we explained how simple models can be used as building blocks for the prior specification of the hyperparameters in more complex hierarchical models.

Note

Codes to reproduce our results are available in https://github.com/IrvingGomez/BayesianHierarchicalIncome

Acknowledgement

The authors would like to give a special thanks to Dr. Anon Plangprasopchok and Ms. Kittiya Ku-kiattikun who managed the data, cleaned it, and provided insight about the data for us.

References

- [1] Chainarong Amornbunchornvej, Navaporn Surasvadi, Anon Plangprasopchok, and Suttipong Thajchayapong. Framework for inferring empirical causal graphs from binary data to support multidimensional poverty analysis. Heliyon, 9(5):e15947, 2023.

- [2] Luciano Nakabashi. Poverty and economic development: Evidence for the Brazilian states. Economia, 19(3):445–458, 2018.

- [3] Marisol Silva-Laya, Natalia D’Angelo, Elda García, Laura Zúñiga, and Teresa Fernández. Urban poverty and education. a systematic literature review. Educational Research Review, 29:100280, 2020.

- [4] Hussein Ibrahim, Xiaoxuan Liu, Nevine Zariffa, Andrew D Morris, and Alastair K Denniston. Health data poverty: an assailable barrier to equitable digital health care. The Lancet Digital Health, 3(4):e260–e265, 2021.

- [5] Thomas Pogge. World poverty and human rights. Ethics & international affairs, 19(1):1–7, 2005.

- [6] Yuanyuan Zhang, Chenyujing Yang, Shaocong Yan, Wukui Wang, and Yongji Xue. Alleviating relative poverty in rural China through a diffusion schema of returning farmer entrepreneurship. Sustainability, 15(2):1380, 2023.

- [7] EF Okpala, Louise Manning, and RN Baines. Socio-economic drivers of poverty and food insecurity: Nigeria a case study. Food Reviews International, 39(6):3444–3454, 2023.

- [8] Glada Lahn and Paul Stevens. The curse of the one-size-fits-all fix: Re-evaluating what we know about extractives and economic development. Technical report, WIDER Working Paper, 2017.

- [9] Felix Rioja and Neven Valev. Does one size fit all?: a reexamination of the finance and growth relationship. Journal of Development Economics, 74(2):429 – 447, 2004.

- [10] Julio Berdegue, Germán Escobar, et al. Rural diversity, agricultural innovation policies and poverty reduction. Agricultural Research and Extension Network, 2002.

- [11] Patrick Commins. Poverty and social exclusion in rural areas: characteristics, processes and research issues. Sociologia Ruralis, 44(1):60–75, 2004.

- [12] DG Pringle, Sally Cook, MA Poole, and Adrian Moore. Cross-border deprivation analysis: a summary guide. Oak Tree Press, 2000.

- [13] Chainarong Amornbunchornvej, Navaporn Surasvadi, Anon Plangprasopchok, and Suttipong Thajchayapong. Identifying linear models in multi-resolution population data using minimum description length principle to predict household income. ACM Trans. Knowl. Discov. Data, 15(2), jan 2021.

- [14] Andrew Gelman and Jennifer Hill. Data analysis using regression and multilevel/hierarchical models. Cambridge university press, 2006.

- [15] Xiaolin Wang. On the relationship between income poverty and multidimensional poverty in China. In Multidimensional Poverty Measurement: Theory and Methodology, pages 85–106. Springer, 2022.

- [16] Sabina Alkire, Usha Kanagaratnam, and Nicolai Suppa. The global multidimensional poverty index (MPI) 2021. OPHI MPI Methodological Note 51, 2021.

- [17] Sabina Alkire, José Manuel Roche, Paola Ballon, James Foster, Maria Emma Santos, and Suman Seth. Multidimensional poverty measurement and analysis. Oxford University Press, USA, 2015.

- [18] Simplice A Asongu and Joel Hinaunye Eita. The conditional influence of poverty, inequality, and severity of poverty on economic growth in Sub-Saharan Africa. Journal of Applied Social Science, page 372–384, 2023.

- [19] Chainarong Amornbunchornvej, Navaporn Surasvadi, Anon Plangprasopchok, and Suttipong Thajchayapong. A nonparametric framework for inferring orders of categorical data from category-real pairs. Heliyon, 6(11), 2020.

- [20] Bettina Grün, Friedrich Leisch, et al. Applications of finite mixtures of regression models. URL: http://cran. r-project. org/web/packages/flexmix/vignettes/regression-examples. pdf, 2007.

- [21] Bettina Grün and Friedrich Leisch. Fitting finite mixtures of linear regression models with varying & fixed effects in R. In Proceedings in Computational Statistics, pages 853–860. Physica Verlag - Springer, 2006.

- [22] Friedrich Leisch. Flexmix: A general framework for finite mixture models and latent class regression in R. Journal of Statistical Software, Articles, 11(8):1–18, 2004.

- [23] Stephen E. Fienberg. Bayesian models and methods in public policy and government settings. Statistical Science, 26(2):212 – 226, 2011.

- [24] Devin Caughey and Christopher Warshaw. Dynamic estimation of latent opinion using a hierarchical group-level IRT model. Political Analysis, 23(2):197–211, 2015.

- [25] Michael Smith, Benno Pütz, Dorothee Auer, and Ludwig Fahrmeir. Assessing brain activity through spatial Bayesian variable selection. NeuroImage, 20(2):802–815, 2003.

- [26] Linlin Zhang, Michele Guindani, Francesco Versace, and Marina Vannucci. A spatio-temporal nonparametric Bayesian variable selection model of fMRI data for clustering correlated time courses. NeuroImage, 95:162–175, 2014.

- [27] Catalina A Vallejos, John C Marioni, and Sylvia Richardson. BASiCS: Bayesian analysis of single-cell sequencing data. PLoS computational biology, 11(6):e1004333, 2015.

- [28] Jingshu Wang, Divyansh Agarwal, Mo Huang, Gang Hu, Zilu Zhou, Chengzhong Ye, and Nancy R Zhang. Data denoising with transfer learning in single-cell transcriptomics. Nature methods, 16(9):875–878, 2019.

- [29] Laura F Boehm Vock, Brian J Reich, Montserrat Fuentes, and Francesca Dominici. Spatial variable selection methods for investigating acute health effects of fine particulate matter components. Biometrics, 71(1):167–177, 2015.

- [30] J Andrew Royle and Robert M Dorazio. Hierarchical modeling and inference in ecology: the analysis of data from populations, metapopulations and communities. Elsevier, 2008.

- [31] Michael D Lee. How cognitive modeling can benefit from hierarchical Bayesian models. Journal of Mathematical Psychology, 55(1):1–7, 2011.

- [32] Rens van de Schoot, Sarah Depaoli, Ruth King, Bianca Kramer, Kaspar Märtens, Mahlet G Tadesse, Marina Vannucci, Andrew Gelman, Duco Veen, Joukje Willemsen, et al. Bayesian statistics and modelling. Nature Reviews Methods Primers, 1(1):1, 2021.

- [33] Daniel Simpson, Håvard Rue, Andrea Riebler, Thiago G. Martins, and Sigrunn H. Sørbye. Penalising model component complexity: A principled, practical approach to constructing priors. Statistical Science, 32(1):1 – 28, 2017.

- [34] Richard McElreath. Statistical rethinking: A Bayesian course with examples in R and Stan. Chapman and Hall/CRC, 2018.

- [35] Andrew Gelman. Prior distributions for variance parameters in hierarchical models (comment on article by Browne and Draper). Bayesian Analysis, 1(3):515 – 534, 2006.

- [36] Nathan P Lemoine. Moving beyond noninformative priors: why and how to choose weakly informative priors in bayesian analyses. Oikos, 128(7):912–928, 2019.

- [37] A. Gelman, J.B. Carlin, H.S. Stern, D.B. Dunson, A. Vehtari, and D.B. Rubin. Bayesian Data Analysis, Third Edition. Chapman & Hall/CRC Texts in Statistical Science. Taylor & Francis, 2013.

- [38] Sumio Watanabe and Manfred Opper. Asymptotic equivalence of Bayes cross validation and widely applicable information criterion in singular learning theory. Journal of machine learning research, 11(12), 2010.

- [39] Hirotugu Akaike. Information theory and an extension of the maximum likelihood principle. In 2nd International Symposium on Information Theory, pages 267–281. Akadémiai Kiadó Location Budapest, Hungary, 1973.

- [40] Aki Vehtari and Janne Ojanen. A survey of Bayesian predictive methods for model assessment, selection and comparison. Statistics Surveys, 6(none):142 – 228, 2012.

- [41] Stuart Geman and Donald Geman. Stochastic relaxation, Gibbs distributions, and the Bayesian restoration of images. IEEE Transactions on pattern analysis and machine intelligence, PAMI-6(6):721–741, 1984.

- [42] Thomas Verma and Judea Pearl. Causal networks: Semantics and expressiveness. In Machine intelligence and pattern recognition, volume 9, pages 69–76. Elsevier, 1990.

- [43] David Barber. Bayesian reasoning and machine learning. Cambridge University Press, 2012.

- [44] Judea Pearl. Models, reasoning and inference. Cambridge, UK: CambridgeUniversityPress, 19(2):3, 2000.

- [45] Cristiano Villa and Francisco J. Rubio. Objective priors for the number of degrees of freedom of a multivariate t distribution and the t-copula. Computational Statistics & Data Analysis, 124:197–219, 2018.

- [46] Francis J Anscombe. Topics in the investigation of linear relations fitted by the method of least squares. Journal of the Royal Statistical Society: Series B (Methodological), 29(1):1–29, 1967.

- [47] Daniel A Relles and William H Rogers. Statisticians are fairly robust estimators of location. Journal of the American Statistical Association, 72(357):107–111, 1977.

- [48] Matthew D Hoffman, Andrew Gelman, et al. The No-U-Turn sampler: adaptively setting path lengths in Hamiltonian Monte Carlo. J. Mach. Learn. Res., 15(1):1593–1623, 2014.

- [49] Simon Duane, A.D. Kennedy, Brian J. Pendleton, and Duncan Roweth. Hybrid Monte Carlo. Physics Letters B, 195(2):216–222, 1987.

- [50] John Salvatier, Thomas V Wiecki, and Christopher Fonnesbeck. Probabilistic programming in Python using PyMC3. PeerJ Computer Science, 2:e55, 2016.

- [51] Judea Pearl, Madelyn Glymour, and Nicholas P Jewell. Causal inference in statistics: A primer. John Wiley & Sons, 2016.

- [52] Jonas Peters, Dominik Janzing, and Bernhard Schölkopf. Elements of causal inference: foundations and learning algorithms. The MIT Press, 2017.

- [53] B. Arnold Jeffrey. Bayesian notes. https://jrnold.github.io/bayesian_notes/.

- [54] Dries F Benoit and Dirk Van den Poel. bayesQR: A Bayesian approach to quantile regression. Journal of Statistical Software, 76:1–32, 2017.

- [55] Keming Yu and Jin Zhang. A three-parameter asymmetric Laplace distribution and its extension. Communications in Statistics—Theory and Methods, 34(9-10):1867–1879, 2005.

- [56] Daniel Lewandowski, Dorota Kurowicka, and Harry Joe. Generating random correlation matrices based on vines and extended onion method. Journal of multivariate analysis, 100(9):1989–2001, 2009.

- [57] Zhenxun Wang, Yunan Wu, and Haitao Chu. On equivalence of the LKJ distribution and the restricted Wishart distribution. arXiv preprint arXiv:1809.04746, 2018.

- [58] Lendie Follett and Brian Vander Naald. Explaining variability in tourist preferences: A Bayesian model well suited to small samples. Tourism Management, 78:104067, 2020.

- [59] Tanner Sorensen and Shravan Vasishth. Bayesian linear mixed models using Stan: A tutorial for psychologists, linguists, and cognitive scientists. arXiv preprint arXiv:1506.06201, 2015.

Appendix A Technical Appendix

A.1 WAIC

We can compare the average log-probability for each model to get an estimate of the relative distance of each model from the real distribution of the data. The Bayesian version of the log-probability score is called the log-pointwise-predictive-density (lppd) defined as

where is the number of simulated samples from the posterior distributions, is the -th set of sampled parameter values and is the density of given the parameters .

However, we should also consider the ‘complexity’ of the model, this complexity is given by the effective number of parameters of the model, labeled and defined as

Because we count with a sample of the posterior distribution of the parameters, this quantity can be well-approximated taking the sample variance of the log-density for each observation , and then summing up these variances.

Therefore, to get a quantitative way to compare the models, we consider the Watanabe-Akaike information criterion (WAIC) defined as

In Watanabe’s original definition, WAIC is the negative of the average lppd, thus is divided by and does not have the factor 2; it is common to scale it to be comparable with AIC and other measures of deviance.

A.2 Qualitative characteristics of the parameters and models

Consider the model presented in Section 3.2, and the prior , it is not difficult to prove [37] that

where

Note that

Note that , and . Meanwhile, , and . This implies that both the complete pooling and no pooling models can be seen as extreme cases of the hierarchical model, achieved when and , respectively. Then, the hierarchical model provides a compromise between these two extreme models.

On the other hand, in [37] it is discussed an empirical approach, based on an analysis of variance (ANOVA), to estimate the parameters and , which we now present and analyze here.

The mean square within groups is given by

and the mean square between groups by

Then, unbiased estimators for and are given by and .

The same authors prove that

Note that everything multiplying approaches a nonzero constant limit as tends to zero. Thus, the behavior of the posterior density near is determined by the prior density. The usual noninformative function is not integrable for any small interval including and yields a nonintegrable posterior density. Meanwhile, the uniform prior distribution yields a proper posterior density.

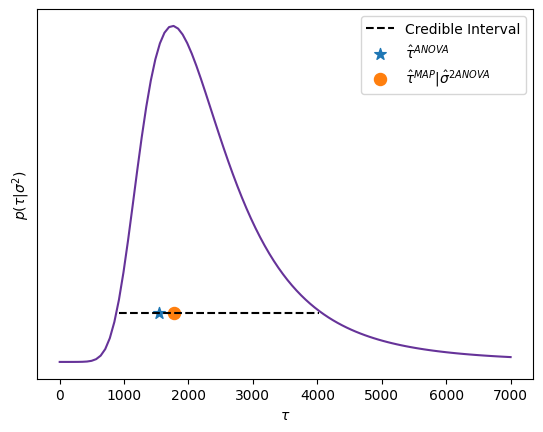

In Figure 24 we present the posterior conditional distribution of conditional on the empirical estimate of , that is . We also present the mode of this distribution, and an approximate interval of 0.95 probability. Under conditions of regularity a probability interval is given by

where denotes the quantile of probability of a distribution with 1 degree of freedom.

In Figure 25 we present , calculated in Equation 4, as a function of and setting the value of to . We plot a vertical dashed line on the value . We can observe how this estimated value lies between the extreme cases of the complete pooling and no pooling models.

Consider now the model presented in Section 3.3, and remember that

where

Then,

and

from this expressions is easy to see that and . On the other hand, if , then , corresponding with the no pooling inference.

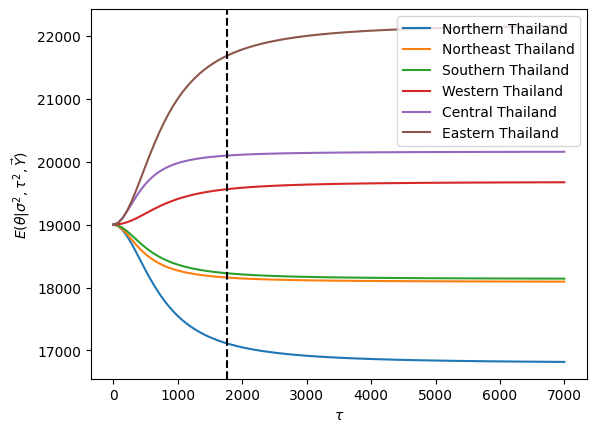

In Figure 26 we present , as a function of and setting the value of to the estimator calculated with Equation 3, and substituting for the observed variance. We plot a vertical dashed line on the value (see Equation 2). Once again, we can observe how this estimated value lies between the extreme cases of complete pooling and no pooling models.

In Figure 27 we present a diagram representing the different models considered in Section 3 and their relation with the parameters. On the bottom left of the diagram we present the complete pooling model, which assumes the same within variance for all the regions and the same mean. While on the other extreme of the diagram we present the no pooling model, where separate independent models are adjusted for each region. The hierarchical models are between these two extreme cases. When we consider , we observed trough simulations that large values of tend to generate within-region variances similar to the no pooling model, while a common within-region variance is obtained when . Somewhere around these models are our other two approaches, set to a fixed estimated value or assign a prior exponential distribution. Next to each model we present its corresponding WAIC value for the monthly income variable, showing in bold the model with the lowest WAIC (see Table 1).

A.3 Proofs

A.3.1 Conditional posterior distribution of

To calculate the conditional posterior distribution of , note that

Setting yields

It is immediate from the previous expression that

where

Note that is the harmonic mean of the within-groups variances. Thus models the “common” within-variance.

A.3.2 Estimating and

Because , then

and

Let be the average of the observed sample within-group variances and their variance. Then, using the method of moments we have

and

thus

Appendix B Supplementary Figures

B.1 Income per region and education level

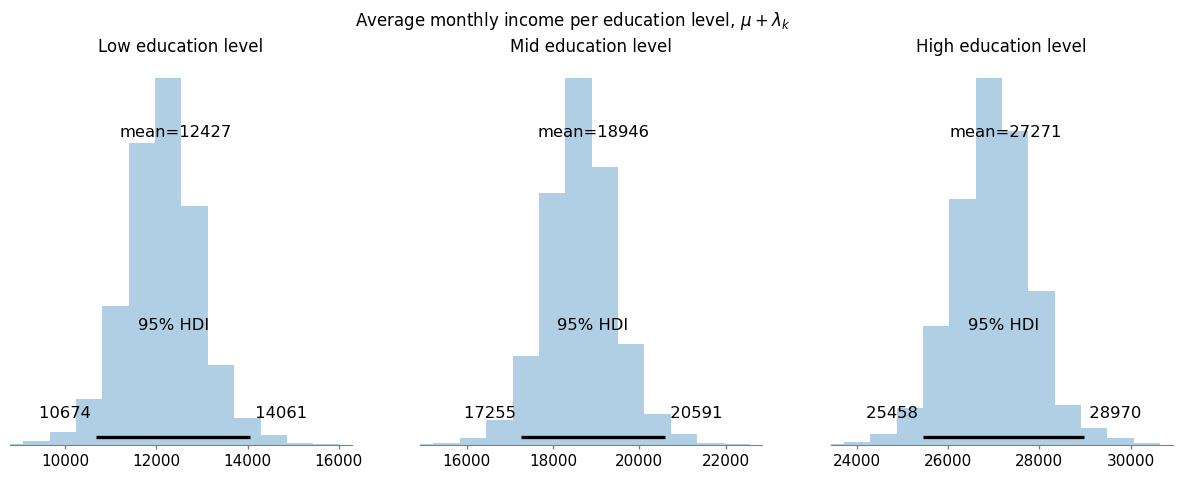

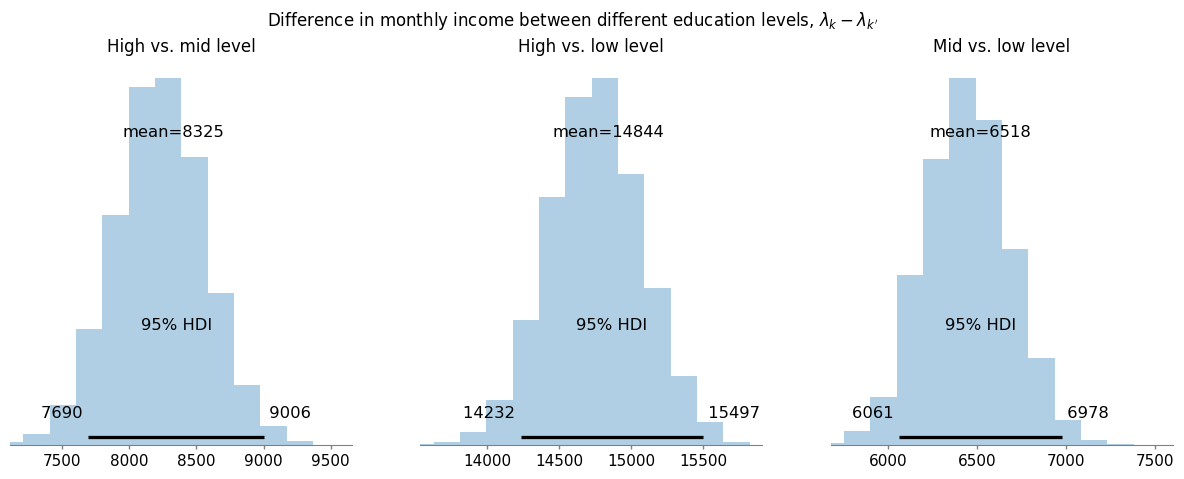

Remember that the expected monthly income for the region and the education level is given by , where . Then, fixing the education level, and taking the average over all the regions, i.e. computing the expected value over , we obtain the expected value of the monthly income for the education level , given by . We present in Figure 28 the expected monthly income for each education level. Similarly, Figure 29 shows the difference of income between the education levels. We can conclude from these Figures that the education level has an important impact on the income of households, when averaging over all the regions, a higher education level is related with a higher income.

We present in Figures 30, 31 and 32 our ubiquitous graphs showing the regional average, the regional deviation and the province average of the monthly income. This time, however, we present these quantities for each education level. We observe that the education level has an important impact on income regardless of the region.