Multivariate Majorization

in Principal–Agents Models

Abstract

We introduce a definition of multivariate majorization that is new to the economics literature. Our majorization technique allows us to generalize Mussa and Rosen’s (1978) “ironing” to a broad class of multivariate principal-agents problems. Specifically, we consider adverse selection problems in which agents’ types are one dimensional but informational externalities create a multidimensional ironing problem. Our majorization technique applies to discrete and continuous type spaces alike and we demonstrate its usefulness for contract theory and mechanism design. We further show that multivariate majorization yields a natural extension of second-order stochastic dominance to multiple dimensions and derive its implications for decision making under multivariate risk.

Keywords: Multivariate majorization, multidimensional ironing, mechanism design, principal-agent problems, access rights

JEL Classification Numbers: D42, D47

1 Introduction

We consider principal-agent(s) models with adverse selection and informational externalities. Examples include the design of mass-produced goods with interdependent values, the production of public or club goods, and multi-agent contracting. In each of these cases, information held by one agent may be pertinent to another. For instance, when a next generation smart phone comes out, one buyer may know about its processing speed while another knows about its screen’s resolution. Both attributes determine the value of the product for each buyer, possibly in different ways as buyers need not agree on what makes a product valuable.

The principal is not privy to agents’ private information and must elicit this information to make an optimal decision. Agents optimally reveal their private information truthfully if the principal’s decision rule satisfies certain “incentive compatibility” constraints, which can typically be reduced to monotonicity constraints on the allocation rule. Moreover, with ex post incentive constraints the principal’s optimal decision is robust in that it does not rely on agents’ beliefs.111Under Bayesian incentive constraints, monotonicity is only required on the interim expected allocation rules. Nevertheless, the system of monotonicity constraints still needs to be solved as a whole and the problem therefore remains multidimensional. Our proposed technique, with some modification, would still be needed. The principal’s problem for a broad class of applications can thus be formulated as

| (1) |

where the multidimensional type set is a finite subset (or compact subset) of , is an exogenously specified continuous function and is a convex function of the principal’s decision variable . The monotonicity condition that be non-decreasing in each coordinate reflects the requirement of incentive compatible (or equilibrium) behavior by the agents.

In the “regular” case, i.e. when is non-decreasing in each coordinate, the solution to (1) simply follows from first-order conditions. However, when informational externalities exist, the regularity assumption is overly restrictive and in many important applications is not a non-decreasing function. This raises the question how to solve the principal’s problem in (1).

For a one-dimensional model of quality choice, Mussa and Rosen (1978) first showed that the solution to the principal’s problem follows by replacing with an “ironed” version that is non-decreasing so that standard first-order conditions apply. Mussa and Rosen’s ironing technique has found ubiquitous application in economics and finance.222Mussa and Rosen’s (1978) paper has almost 4,500 Google Scholar citations. However, their methodology cannot be immediately applied to a setting with informational externalities, which is naturally multidimensional.333Roughgarden and Talgam-Cohen (2016), for example, note that a naive generalization of ironing in a model with interdependent values fails to properly account for incentive-compatibility constraints. Likewise, the ironing technique proposed by Myerson (1981), which entails convexifying the primitive of , does not readily extend to multidimensional settings.

In this paper we develop a constructive approach to multidimensional ironing. We extend Mussa and Rosen’s (1978) ironing approach by manipulating the function in (1) to generate an alternative problem whose unconstrained solution is the same as the solution to the original constrained problem. To accomplish this, we reinterpret multidimensional ironing in terms of multivariate majorization. This generalizes insights developed by Goeree and Kushnir (2023) who first noted the connection between one-dimensional ironing and univariate majorization. While the result is not a closed-form solution to the original problem (1), we do provide a convenient and easily implementable algorithm for calculating the solution as well as some its general characteristics.

Several definitions of multivariate majorization exist in the mathematics literature, e.g. row-majorization, column-majorization, and linear-combinations majorization (see Marshall et al., 2010, Chapter 15), but none of these are relevant for solving the principal’s problem in (1). We exploit a notion of multivariate majorization that generalizes univariate majorization to higher dimensions.444See also Hwang (1979) and Brualdi and Dahl (2013) who apply this notion to arbitrary partially-ordered sets. Recall that if and are non-decreasing functions over some finite ordered type set then majorizes , denoted , iff

| (2) |

for with equality when . The relevance of majorization for solving the principal’s problem in the univariate case stems from two classic results by Hardy et al. (1929). The first is that iff where is a doubly-stochastic operator. The second is that iff

| (3) |

for any convex function where the inequality is strict if is strictly convex and . Goeree and Kushnir (2023) exploit both properties to show that for a given function , not necessarily non-decreasing, there exists a unique that is the minimum with respect to majorization order, i.e. for any other we have .

Our definition of multivariate majorization generalizes the lower sums in (2) to sums over lower subsets of the multidimensional type set in (1). For non-decreasing functions and we show that iff where belongs to a restricted class of (orthogonal) doubly stochastic operators. Unlike the univariate case, for a given multivariate function there does not necessarily exist a unique that is the minimum with respect to the majorization order, i.e. there may exist for which neither nor . We show, however, that the that is relevant for solving (1) is a minimal element with respect to the majorization order, i.e. if there exists such that then . We exploit a generalization of (3) to the multivariate case to select a unique function, , from the set of minimal elements. The principal’s optimal decision when faced with then readily follows from first-order conditions and solves the original problem in (1).

1.1 Related Literature

One of the earliest attempts to deal with multidimensional incentive-compatibility constraints in a general setting is Rochet and Choné (1998). In their environment, a monopolist with strictly convex costs sells to a consumer with multidimensional preferences, each dimension corresponding to an attribute of the good designed by the seller. They introduce the concept of “sweeping.” Roughly, sweeping is an operation that redistributes the density of a measure in a way that preserves the original center-of-mass of the measure. Rochet and Choné (1998) do not use sweeping to construct a solution but instead its use is to verify whether a candidate incentive-compatible solution is optimal. Specifically, their results say that if (the derivative of) the first-order condition of the seller’s unconstrained problem, evaluated at the candidate solution, is non-zero but can be “swept” to zero then the candidate solution is optimal. In a similar environment, Daskalakis et al. (2017) deal with multidimensional incentive-compatibility constraints through an optimal transport problem that is dual to the mechanism design problem. Their analysis shows that accommodating the incentive compatibility constraints requires the application of mean-preserving spreads on measures in the dual problem, echoing Rochet and Choné (1998)’s sweeping results.

Some recent progress has been made on multidimensional ironing in multidimensional monopolist problem environments, in particular by Carroll (2017), Cai et al. (2016) and Haghpanah and Hartline (2021). These papers construct generalized virtual values based on the Lagrangian dual of the monopolist’s problem. Carroll (2017) is interested in the mechanism that maximizes the monopolist’s worst-case expected profits over all possible joint beliefs consistent with known marginal beliefs. Cai et al. (2016) seek simple mechanisms that are approximately optimal. Haghpanah and Hartline (2021) characterize when pure bundling is optimal for the monopolist.

Our paper differs from these approaches in that agents’ types are one dimensional but informational externalities create multidimensional incentive constraints. Another difference is that we develop a constructive, and computationally simple, method for multidimensional ironing.

1.2 Organization

The next section introduces our novel definition of multivariate majorization (Section 2.1) and shows how it can be used to implement ironing in the multidimensional case (Section 2.2). We also show how to extend the results to continuous type spaces (Section 2.3). Section 3 introduces access rights that allow the principal to screen out some types, e.g. to increase revenues. We show how our multivariate majorization approach can be extended to include probabilistic or all-or-nothing access rights. Section 4 discusses applications to decision making under multivariate risk, the optimal design of mass-produced goods, as well as multi-agent contracting. Section 5 concludes. Proofs can be found in Appendix A.

2 Multivariate Majorization and Ironing

Let denote the set of agents. It is instructive to start with the discrete case, i.e., where each is an ordered finite set. For , the type is drawn from according to distribution with probability function (or density if is continuous) . We make no assumptions about or but assume independence across bidders, i.e. is drawn according to . For a profile of types we write with , and . For , we write () if () for all and define .

Let and . For an arbitrary function we define the partial derivatives and where is the type just above (below) with the convention that and . (In the case of continuous types, .) A function is non-decreasing if implies . Let .

2.1 Multivariate Majorization

We start with the multivariate version of a lower set.

Definition 1

A subset is a lower set of if and with implies .

For instance, each of the subsets in the left panel of Figure 1 is an example of a lower set, while neither subset in the right panel is.

Definition 2

For and , majorizes , denoted , if for any lower set we have and .

This definition is not restricted to non-decreasing functions as this would make it irrelevant for developing a multidimensional version of Mussa and Rosen’s (1978) ironing method.555Definition 2 can be motivated by a Kuhn-Tucker approach, see an earlier version of this paper (Bedard et al., 2020). While it is not surprising that non-decreasingness constraints can be captured by a Kuhn-Tucker program, it is surprising that the resulting conditions form a well-defined mathematical structure that generalizes univariate majorization. The multivariate majorization notion of Definition 2 offers a conceptual and computational approach to multidimensional ironing.

It will be useful below to paramterize the majorization relation between two functions. To do so we will adapt a well-known concept in the univariate majorization literature call a -transform: a doubly stochastic operator of the form with the identity, a permutation that interchanges only two elements, and . Under a -transform the sequence maps to , i.e. there is a transfer from type to .666If represents “wealth” and is non-decreasing in type then this amounts to a non-negative transfer from a “wealthier” to a “poorer” type (i.e. it is a “Robin Hood” transfer).

Muirhead (1903) showed that for non-decreasing univariate functions and , a necessary and sufficient condition for is that can be obtained from via a series of -transforms. We obtain a similar result below for functions defined over the multidimensional set if we restrict transfers to be between and for some , , and . We refer to -transforms of this type as orthogonal -transforms.

Theorem 1

Let and be non-decreasing in each coordinate. Then if and only if can be obtained from via a series of orthogonal -transforms.

For the univariate case, Hardy et al. (1929) sharpened Muirhead’s (1903) result to if and only if for some doubly stochastic operator . But in the multivariate case, the orthogonality requirement restricts the possible doubly-stochastic transformations. In particular, orthogonality does not allow the transformation to mix between arbitrary elements of . To illustrate, suppose and so we can represent by a matrix where the rows correspond to agent 1’s types and the columns to agent 2’s types. If, for instance, and is obtained from by averaging along columns then but not if we average along the diagonal, i.e. but .

The multivariate majorization order in Definition 2 is a preorder. Given , we say that a non-decreasing function is a minimal element that majorizes if the existence of a non-decreasing function such that implies . As we show below, the properly ironed will be a minimal element that majorizes . In the univariate case, this minimal element is unique (see Goeree and Kushnir, 2023). In the multivariate case, there may exist multiple minimal elements, as we show in the following example.

Example 1 (Minimal Elements)

Suppose and types are uniformly distributed. Let

where the rows and columns correspond to and respectively. It is straightforward to verify that

is a non-decreasing function that majorizes . It is, however, not minimal. To find all minimal elements we parameterize

with so that (i.e. a transfer from each agent’s lowest type to her highest type). The lower boundary of the set determined by the constraints that ensure is non-decreasing, i.e. and , corresponds to the set of minimal elements, which form the polyline for . Below we determine how to choose the correct minimal element as the ironed version of .

2.2 Multivariate Ironing

In this section, we determine the ironed such that the relaxed problem

| (4) |

is equivalent to (1), i.e. it has the same solution and optimal value. We show that can be obtained via a convex minimization problem that selects a unique member from the set of minimal elements. Uniqueness of then implies the solution, , to (4) is also unique.

Theorem 2 below establishes the existence of a function that is non-decreasing and is a minimal element that majorizes . We also describe how generates a particular partition of . We write if implies .

Definition 3

is ultramodular if and implies . A partition of is ultramodular if all its cells are ultramodular.

Intuitively, is ultramodular if for any line parallel to one of the axes or of positive slope, the intersection with is empty, a point, or a single segment. (Akin to the definition of convex sets for which the intersection with any line is empty, a point, or a single segment.)

Theorem 2

The solution to (1) is given by

| (5) |

where is the unique minimal element that solves

| (6) |

for any strictly convex function with .

The solution is non-decreasing and its level sets form an ultramodular partition of : for , the cell of containing is and , i.e. is constant on any partition cell.

Importantly, the convex minimization program in (6) provides a convenient method to compute the ironed . To deal with the majorization constraint in (6), , we formulate as a function of with a series of transfers from lower types to higher types, within the same agent. Intuitively, this is reflects Theorem 1 and the fact that an orthogonal transform is equivalent to transfers between adjacent types of an agent. We know the transfer must be from a lower type to a higher type by the inequalities that define . For , let be the non-negative transfers for agent from her type to her next highest type with . By convention, for all . Define

| (7) |

We can confirm that does majorize : for any lower set ,

E[g(x)—x∈X_-]&=E[α(x)-∑_i∈NΔ_i λ_i(x)/f(x) — x∈X_-]

=E[α(x)—x∈X_-]-∑_x ∈ ¯∂X_-∑_i ∈ Nλ_i(x)

≤ E[α(x)—x∈X_-]

where denotes the set of extreme upper points of , i.e. if there does not exist with such that .777 For instance, in the left panel of Figure 1, the set of extreme upper points of and coincide with their borders in the interior of whereas the set of extreme points of is the collection of right-hand corners of each step in the border of .

Equation (7) holds with equality if all the vanish on . In particular, since for all and , we have

| (8) |

Together (7) and (8) show that defined in (7) majorizes . Remarkably, the solution to (6) does not depend on the function ; for convenience, we will use . The can be obtained from the simple quadratic optimization program

| (9) |

which produces a unique and, hence, a unique .

Example 1 (continued)

Recall that the minimal elements are given by

with and . Picking in (6) yields and

with ultramodular partition where and .

2.3 Restricted Least Squares

In this section we outline an alternative method for computing the ironed values. For not necessarily non-decreasing consider the restricted least-squares program

| (10) |

where is the squared norm of . The so obtained is identical to that obtained from (6). To see this, write (10) as a saddle-point problem

where the second term implements the non-decreasingness constraint. Changing the order of summation for this term and then taking first-order conditions yields

where solves

| (11) |

The solutions to (11) and (9) are identical. For the one-dimensional case, (10) provides a computationally convenient alternative to Mussa and Rosen’s (1978) and Myerson’s (1981) methods.

2.4 Continuous Types

In this section, we show that continuous types can be dealt with in much the same manner as the discrete-type case studied above. Without loss of generality we assume . Let be a filtered probability space where is the -algebra generated by dyadic cubes of sidelength , is a Borel -algebra, and is an absolutely continuous distribution function.

Definition 4

Let denote the collection of all lower subsets in and let be two integrable functions. We say majorizes , denoted , iff

| (12) |

for all with equality when .

Assume is a bounded integrable function on . The conditional expectation of on is denoted . The form a Doob martingale. Let be the ironed value that follows from Theorem 2.

Theorem 3

The proof can be found in Appendix A where we also prove the stronger result that any sequence converges to almost everywhere if the original is continuous and has bounded variation. For the continuous case, the geometric intuition behind multivariate majorization can be illustrated using the Gauss divergence theorem. Similar to the discrete case we define

where for all and .

Consider any lower set with boundary that is the union of the upper boundary and the lower boundary . The geometry of lower sets is such that the normal to any point on the upper boundary is positive, i.e. , whence . On the lower boundary we must have for some , in which case the normal is minus the th unit vector and since . By the Gauss divergence theorem we have

E[¯α(x) — x ∈X_-]&=E[α(x)-div(λ(x))/f(x) — x ∈X_-]

=E[α(x) — x ∈X_-]-1F(X-)∫_¯∂X_-λ(x)⋅n(x)

≤ E[α(x) — x ∈X_-]

with equality if on . In particular, since for all and , we have .

To summarize, Definition 2 readily extends to functions over continuous type spaces.

Example 2

3 Discriminatory Access Rights

In this section, we introduce access rights that allow the principal to “screen out” certain types. While our concept of majorization is most clearly demonstrated without screening, the ubiquity of such access rights in the real world makes it important that we show how our technique can accommodate them.888Access rights for public goods are also called “exclusions” in the literature. For example, see Cornelli (1996); Ledyard and Palfrey (1999); Hellwig (2003) and Norman (2004). Our formulation below most closely follows Norman (2004). For instance, mass-produced goods such as smart phones may be prohibitively costly for some buyers. Likewise, public goods are often restricted to a limited set of people. Besides all-or-nothing access rights used to screen out certain types we also consider probabilistic access rights that can be used to alleviate incentive constraints. We show that the principal’s problem

| (13) |

can again be solved via multivariate majorization. To this end, we wish to manipulate each to generate such that the following unconstrained problem is equivalent to (13):

| (14) |

We will need a notion of univariate majorization that applies to multidimensional functions.

Definition 5

For , , majorizes in coordinate , denoted , if for all , with equality if .

Now consider

| (15) |

for some strictly convex function . There is a trivial way in which the solution to (15) is not unique, unlike the solution to (6). If for some , then we could replace it with any other negative number. This multiplicity poses no problem since these cases are screened out and the principal’s optimal decision is unique (see Lemma 1 in Appendix A). Another difference with the previous section is that we cannot use level sets of to define the partition .

Example 3

Suppose there are two agents with and types are uniformly distributed. Let

For any strictly convex , e.g. , Theorem 2 yields

| (16) |

which is the result without access rights, i.e. for all , . With access rights, the program in (15) yields

| (17) |

Based on level sets of , the partition would consist of five cells: two singletons, two sets of size two, and a set of size three. However, this partition violates the majorization requirement that has the same expected value as on each cell. The correct ultramodular partition can be obtained from the program in (15), which can be executed by parameterizing , with and for and , and then minimizing over the s. This yields

For agent we fix and find the largest (if any) for which as well as the largest for which to form the sets, , which are highlighted above. We do this for all agents and then “overlay” the individual sets to find the partition. Profiles that do not belong to any of the highlighted sets form singletons on which . For the above example, the correct partition is: where , , , and . Now has the same expected values as on each of the cells.

Theorem 4

The solution to the full problem (13) is

| (18) |

and with is associated a ultramodular partition of . For , let be the cell of containing and let . The optimal access rights is given by

where is such that is constant on and non-decreasing in .999In detail, (i) if there exists such that then , (ii) otherwise for all and for any with and .

Example 3 (continued)

Unlike , the solution that follows from (15) is not necessarily constant on a cell, cf. (16) and (17) above. Incentive compatibility is maintained by choosing appropriate access rights, i.e.

and is the transpose of . This example shows that besides all-or-nothing access rights that can be used to screen out agents, probabilistic access rights can be beneficial in that they allow the ironed to more closely track the original when the latter are non-monotonic.

4 Applications

In this section we detail three applications of our concept of multivariate majorization. First we discuss two examples of principal-agents problems with interdependent agent types. Next we show how applying the theory of multivariate majorization to cumulative distribution functions provides a natural extension of second-order stochastic dominance, providing a useful tool for analyzing multivariate risk.

4.1 Optimal Mechanisms For Mass-Produced Goods

Any seller of a mass-market good faces the challenge of designing a single good to appeal to a large number of diverse consumers. The decision of interest is not how many copies of a good to make but how to best design the template used to generate copies. In particular, the seller chooses a single quality level for the good to be enjoyed commonly by all consumers of the good. In addition, the seller may restrict access to the good and collect transfers. Virtually any product sold as identical goods to more than one person will fit into this framework. For example, producers of popular movies, books, television programming and music rely on wide appeal to generate profits, rather than finding the ideal fit for each customer. Schools must contend with how to design lectures and deliver courses and, as technology relaxes physical constraints to the learning environment, whom to exclude, if anyone. Mass-produced goods such as furniture, electronics, and some food and drinks have the same characteristic. Most restaurants offer consistent menus over time as customers flow through, certainly in the case of national and global chains. Many non-profit outfits such as library, schools, museums, theatres and orchestras, and public parks similarly satisfy large groups with limited offerings. We assume that a buyer’s valuation for the good depends on her own signal as well as the signals of all other buyers, i.e. valuations are interdependent. In particular, buyer ’s valuation for the good given type profile is , where is non-decreasing in for all . Buyer ’s payoff, given choices by the seller and type profile is . The seller’s problem is to choose a mechanism to maximize the expected sum of transfers from buyers net of the expected cost. The cost of providing quantity is , which is assumed to be an increasing convex (and differentiable) function with . Due to the revelation principle, we can focus on (incentive compatible) direct mechanisms: where (i) maps type profiles into quantity choices; (ii) maps type profiles into access rights; and (iii) maps type profiles into transfers. The seller’s problem is therefore to choose a direct mechanism to maximize

subject to (ex post) incentive compatibility and individual rationality. Using standard arguments, we can solve for the transfers

where to rewrite the seller’s profit as

where and, for ,

The seller’s problem is thus to choose the quality, , and access rights, , to maximize such that is non-decreasing in for all , and set transfers, , as above. Let denote the seller’s profits when using the optimal mechanism .

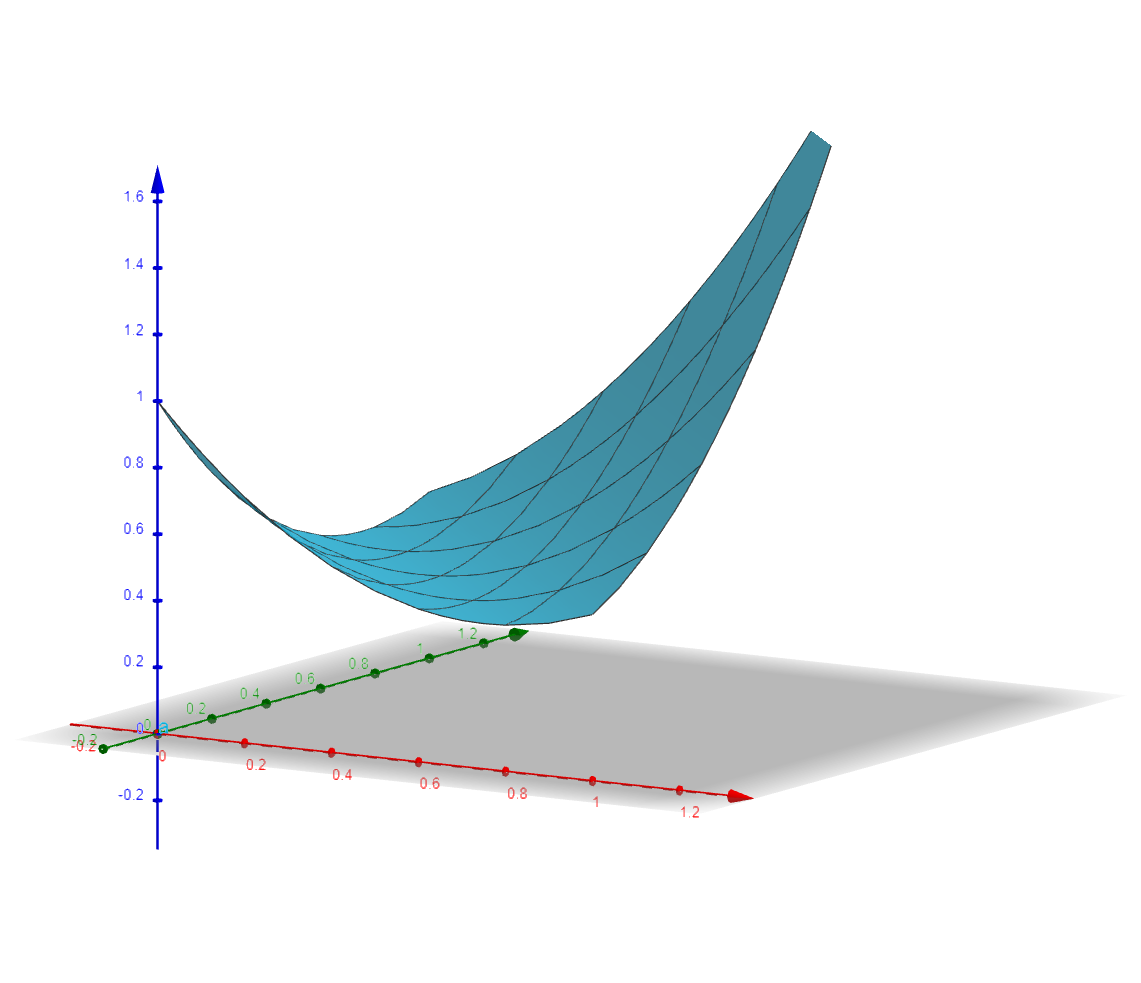

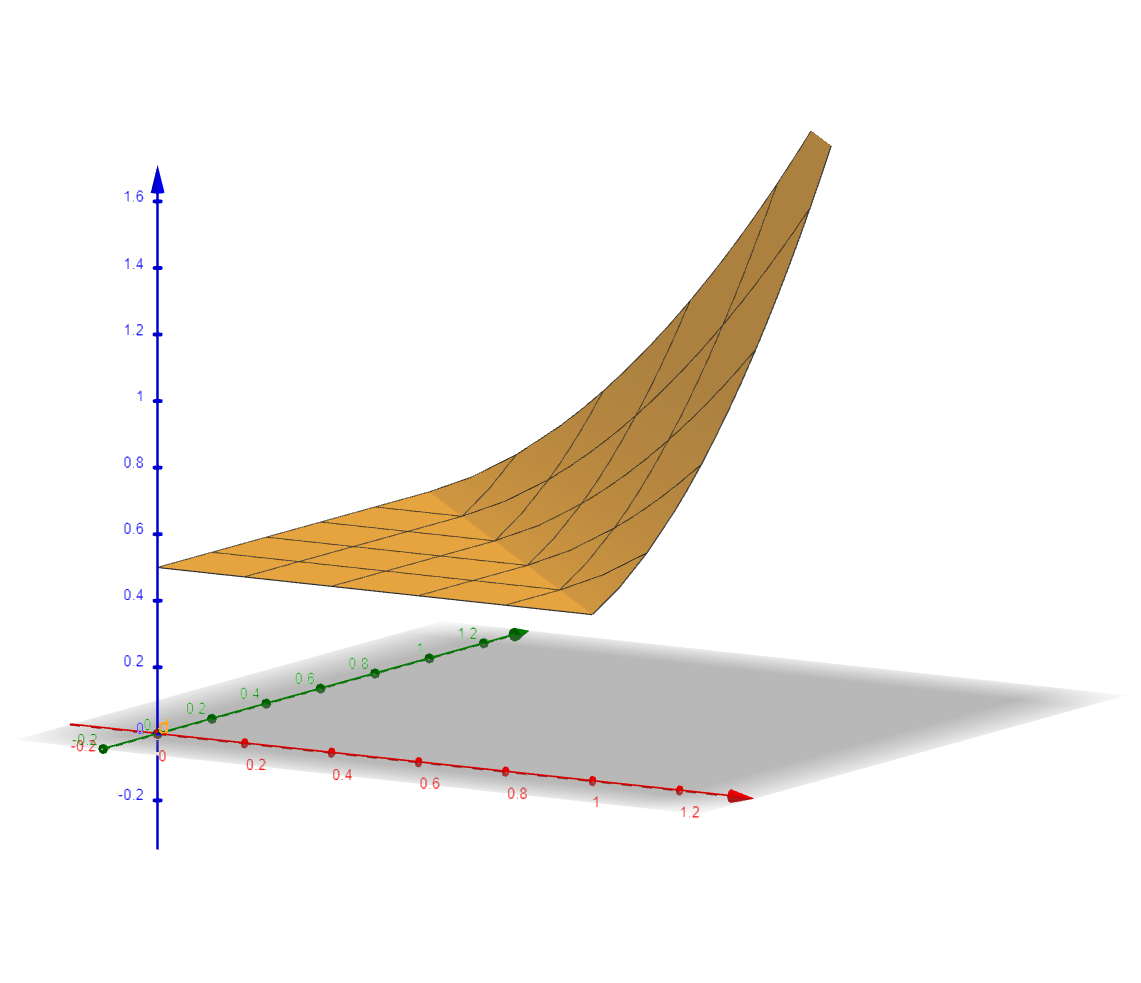

Example 4 (Probabilistic access rights with continuous types)

For , let buyers’ value functions be given by where the types are uniformly distributed on . The sum of marginal revenues

is decreasing for higher types and . As a result, Theorem 2 yields , i.e. without access rights the seller’s optimal choice is to bunch all buyers and offer zero quality independent of their types. With access rights, however, the optimal quality that follows from Theorem 4 is

which bunches buyer pairs according to , i.e. the minimum of their types. When both buyers have above-average types, , the seller offers them zero quality. Otherwise, they get offered a positive quality that is higher the lower is . While the optimal quality is constant in a buyer’s type when the buyer has the higher type it is strictly decreasing in a buyer’s type when the buyer has the lower type. To maintain incentive compatibility the seller optimally uses probabilistic access rights

and . The optimal quality and access rights are shown in the left and right panels of Figure 3.

Besides the interpretation of the seller choosing design quality, one can also view this model as the private provision of a public good with private information, with the seller choosing the quantity of the public good to provide. The analysis of this problem in a mechanism design framework goes back at least as far as Groves and Ledyard (1977). Classically, the decision is binary, i.e. to provide the good or not, and participation is compulsory, i.e. the good is non-excludable. The relevant question is whether the good is provided efficiently (see Güth and Hellwig, 1986). More recently, exclusions and continuous levels of the good have been allowed (see Cornelli, 1996; Ledyard and Palfrey, 1999; Hellwig, 2003; Norman, 2004). Preferences in these papers are purely private valued. More broadly, there is a separate literature exploring the implementation of social choice functions when agents have interdependent preferences (see Bergemann and Morris, 2009; Ollár and Penta, 2017, 2021). These papers are not concerned with optimal mechanisms per se but rather with exploring how a principal can implement particular equilibrium outcomes given various assumptions of the principal’s knowledge of agents’ first- and higher-order beliefs.

4.2 Multi-Agent Contracting

Consider a contracting relationship where the principal chooses a duration, , during which agents must exert effort. Examples include a factory deciding the number of hours in a workday or a coach choosing the length of a football practice. For , agent ’s cost of exerting effort for a total amount of time equals where the marginal cost is decreasing in the agent’s own type and may depend on others’ types. For example, training an hour with professional footballers may be unusually exhausting. The principal’s payoff is where the production function has decreasing marginal returns and is the transfer to agent . For , agent ’s payoff is . As in the previous section, we can solve out the transfers using standard arguments and write the principal’s problem as

| (19) |

with

and . With continuous types the principal’s optimal choice is

where follows from (6). Discrete types can readily be handled as well by replacing with its discrete version

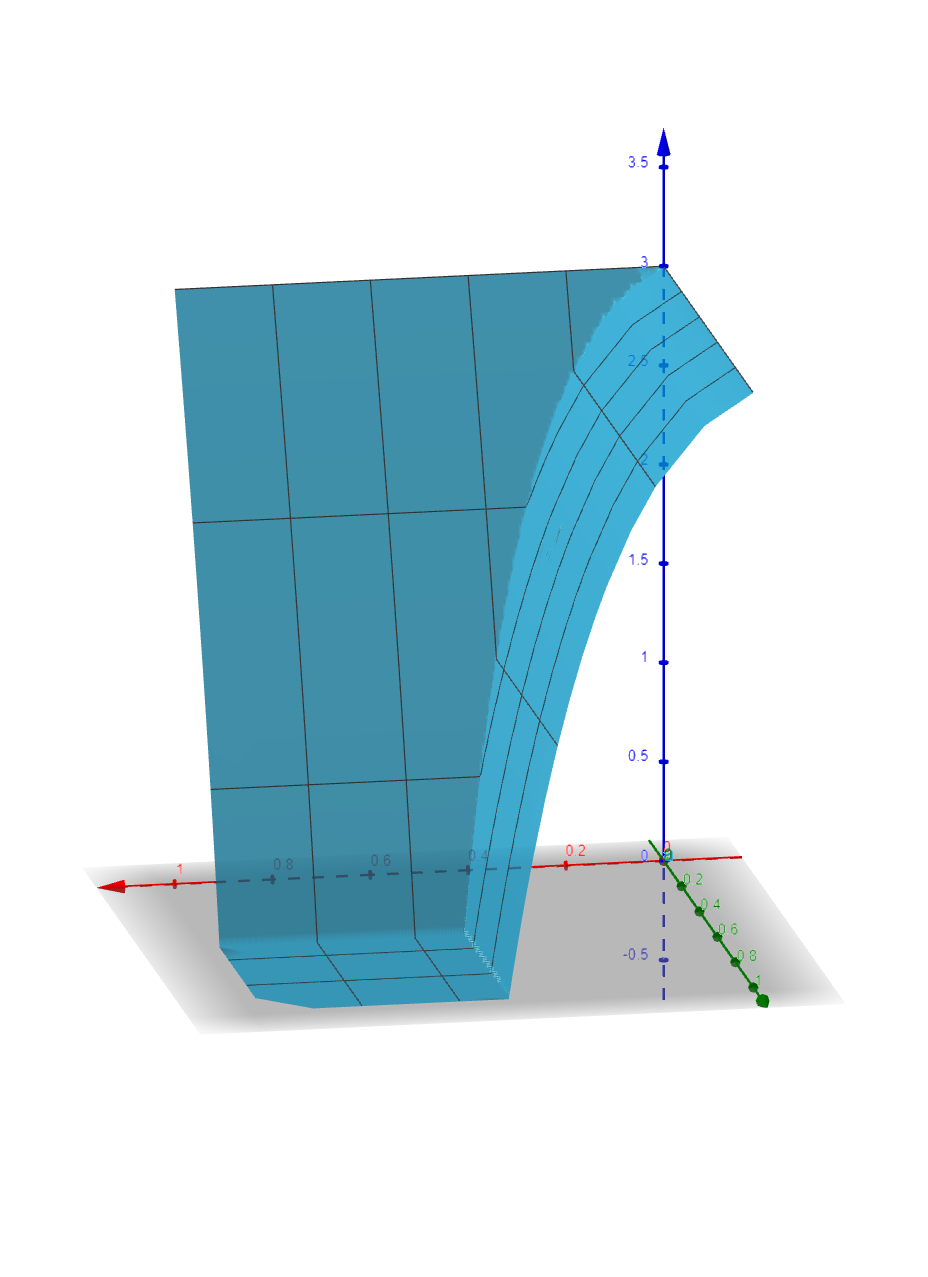

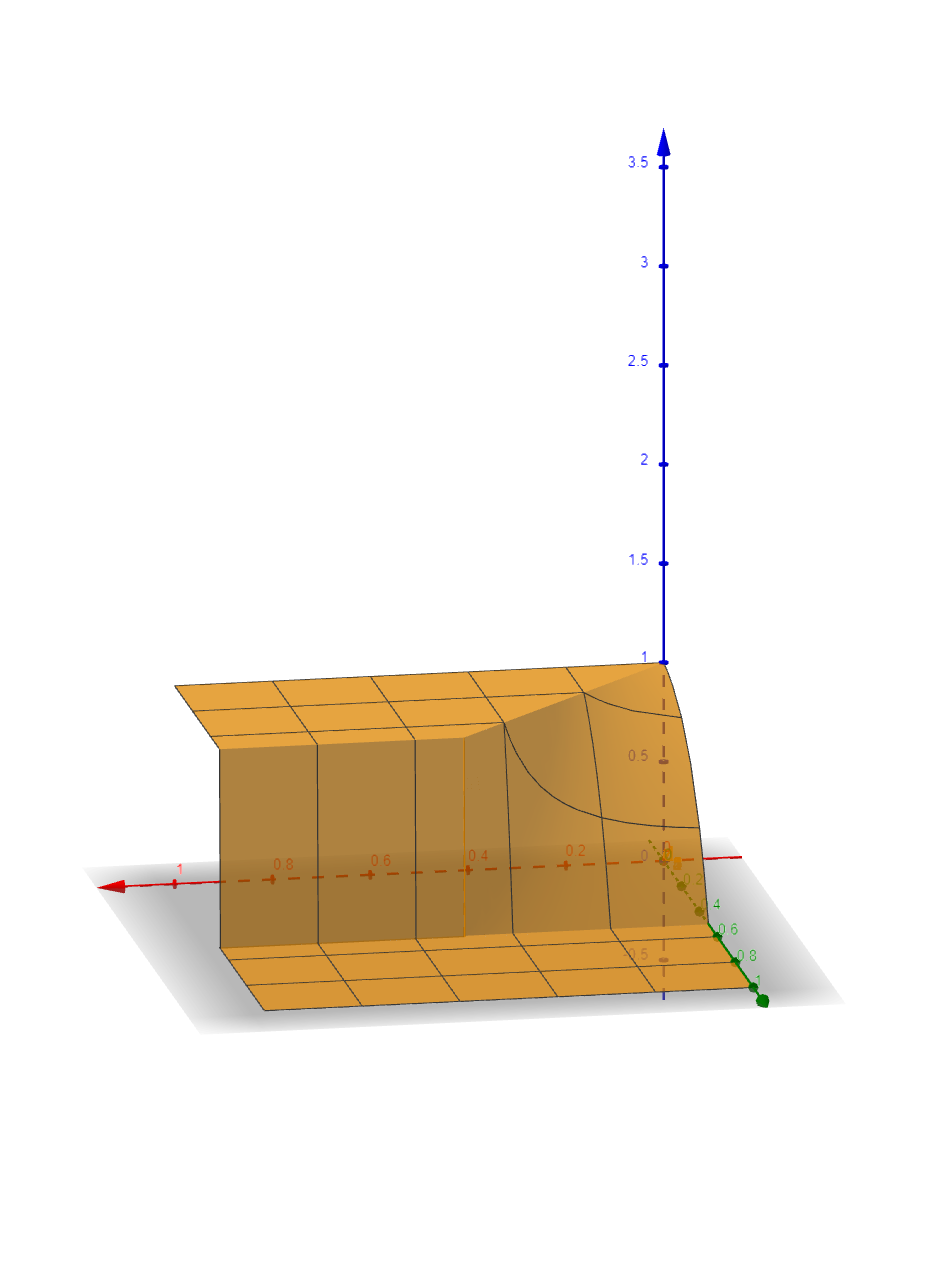

Example 5

Suppose and, for , the cost functions are where the types are uniformly distributed and . The sum of agents’ marginal costs

is not everywhere non-decreasing. The ironed version

yields the optimal duration .

4.3 Decisionmaking Under Multivariate Risk

Second-order stochastic dominance is a powerful tool to rank uncertain prospects for a broad class of preferences. The concept was developed over half a century ago (e.g. Hadar and Russell, 1969; Hanoch and Levy, 1969; Rothschild and Stiglitz, 1970) and has since been applied in economics, finance, decision theory, mathematical programming, stochastic processes, etc. Recall that distribution function second-order stochastically dominates the distribution function if

for all with equality when . (The latter ensures that as can be verified by partial integration.) This is the exact definition of univariate majorization. In other words, second-order stochastic dominance is simply univariate majorization applied to a restricted class of (distribution) functions. Second-order stochastic dominance is well-known to be related to mean-preserving spreads. Random variable is a mean-preserving spread of random variable if with . For the densities and associated with and respectively, a mean-preserving spread implies

where is a sweeping operator, e.g. Rochet and Choné (1998), that satisfies

for , with boundary conditions and since the endpoints cannot be swept in a mean-preserving manner (here denotes the Dirac delta function).

Theorem 5

Let and be the distributions associated with and respectively. Then is a mean-preserving spread of if and only if

with a doubly-stochastic operator, i.e. for .

We thus can state the following variant of a classic result due to Rothschild and Stiglitz.

Theorem 6 (Rothschild and Stiglitz, 1970)

The following statements are equivalent:

-

1.

second-order stochastically dominates .

-

2.

where is a doubly-stochastic operator.

-

3.

for any concave utility function .

Most of the literature has focused on univariate risk where wealth is the only random variable.101010See e.g. the discussion in Chapter 17 of Levy (2016) who notes that papers that consider multivariate risk focus only on first-order stochastic dominance. However, many decisions involve multiple sources of risk, e.g. when individuals care about their health and their wealth. First-order stochastic dominance can readily be generalized to multidimensional settings using the lower sets introduced above. Let and denote the densities associated with and respectively. Then first-order dominates if

for any lower set with equality when . However, there is no definition in the literature for multivariate second-order stochastic dominance. We next provide such a definition. To a multivariate distribution function we associate the complement of the survival function

which is non-decreasing in each argument with and if one or more of the . Note that for the univariate case we have . Our definition for multivariate second-order stochastic dominance is simply that of multivariate majorization.

Definition 6

second-order stochastically dominates if

| (20) |

for any lower set with equality when .

Let denote the set of all non-empty subsets of . An element of is a set of labels where and the for are different elements of . Let equal with the -th argument set to zero if . Likewise, let equal with the -th argument set to zero if . Finally, let .

Definition 7

A utility function is ortho-concave if is non-increasing in each argument for all .

Examples of ortho-concave functions include Cobb-Douglas utility functions with for .111111Note that for and for since the Cobb-Douglas utility vanishes if one or more arguments are zero. Note that is concave only when in addition .

Theorem 7

The following statements are equivalent:

-

1.

second-order stochastically dominates .

-

2.

where is an orthogonal doubly-stochastic operator.

-

3.

for any ortho-concave utility function .

5 Conclusion

We develop a constructive approach to multidimensional ironing via a novel concept of multivariate majorization. Using this new technique, we characterize the optimal mechanism for a class of principal-agents problems when agents’ values are interdependent. We show how the interdependency of agents’ values creates multidimensional incentive-compatibility constraints on the principal’s problem. These constraints cannot be addressed using the univariate “ironing” method developed by Mussa and Rosen (1978) and Myerson (1981). Instead, we use multivariate majorization to jointly iron buyers’ preferences. The resulting preferences are sufficiently well behaved that the incentive constraints no longer strictly bind allowing the principal to effectively ignore them. While we mostly focus on the case where all agents are guaranteed access to the good regardless of their type, we show that our approach extends directly to the case of excludable access. In so doing, we demonstrate that exclusions and random access rights are important ways for the monopolist to raise profits. The former allows the monopolist to exclude buyers with negative marginal revenue and the latter allows the monopolist to fine tune incentives, both without manipulating the overall choice of quality for the market. We demonstrate that the same multivariate majorization technique applies to discrete and continuous type spaces, unlike the univariate ironing methods developed by Mussa and Rosen (1978) and Myerson (1981). We further show that the ironed function can be obtained via a restricted least-squares problem, both in the univariate and multivariate case. Restricting the class of multivariate functions to cumulative distribution functions, our multivariate majorization technique provides a multidimensional extension of second-order stochastic dominance. This allows us to generalize Rothschild and Stiglitz’ (1970) classic analysis of decisionmaking under risk to the multivariate case. Interesting avenues to explore include determining whether our multivariate majorization approach can be adapted to cases where the principal’s objective is non-separable and/or agents’ types are multidimensional. We leave these for future research.

Appendix A Proofs

Proof of Theorem 1. For notational convenience, we prove the proposition for the case of a uniform distribution over types for all players. We say that is lexicographically lower than , written , if there is a such that , then there exists , such that ; is strictly lexicographically lower than , written if and . In words, we first sort type profiles by player, then by type. Suppose . Choose and such that there is and with , , and where is the lexicographically lowest such profile and is the lexicographically highest such type (lexicographically below ). Let

where and define the orthogonal -transform

Then

It is clear that . It is also true that . To see this, suppose instead that there is a lower set such that . Then but . By our choice of , , and , we may assume

But so that

and Since is a lower set, this contradicts our assumption that and we conclude that . Finally, for any two functions and on , let denote the number of type profiles such that . Then . Therefore, repeating this step at most times will result in . Now suppose that where is the product of a sequence of orthogonal -transforms for some finite integer . Suppose mixes between type profiles and , with probability for and . Define

Then

So that . Iterating in this way, we can conclude that . Proof of Theorem 2. The constraint in (6) defines a convex polyhedron so the convex program has a unique minimizer, denoted . In order to deal with the majorization constraint , we parameterize

| (21) |

where, for , the are non-negative for with for all . The solutions to (21) must satisfy, for ,

| (22) | |||||

| (23) |

which imply and for any convex with . Suppose, in contradiction, that is not non-decreasing, i.e. for some , . Then lowering slightly while raising by the same amount lowers the objective in (6), a contradiction. Suppose, in contradiction, that is not minimal, i.e. there exists a non-decreasing such that . By Theorem 1 there exists a doubly stochastic operator such that . But, convexity of the objective in (6) then implies that yields a lower value than , a contradiction. Next, suppose, in contradiction, that the level sets of do not form an ultramodular partition, i.e. for some but for some . If either or then is not non-decreasing. Finally we show that does indeed solve the original problem 1. Note that any non-decreasing can be written as where the sum is over all lower sets of that are strict subsets of , the s are scalars with and , and the are indicator functions with if and otherwise. The intuition behind the majorization conditions in Definition 2 is that they ensure, for any , that and, hence, . And since we wish the latter to hold with equality, the sought after must be a minimal element. Next consider a partition of and denote the cell of that belongs to by , which may be a singleton or contain multiple types. Suppose for we replace with and that is non-decreasing, majorizes , and is minimal. The that maximizes (4) is then constant on any of the partition cells. Hence,

i.e. there is “no gap:” . Moreover, for any non-decreasing we have

where the first inequality follows from , the second inequality from optimality of for , and the final equality from the “no gap” result. Together they show solves problem 1. Proof of Theorem 3. By Theorem 2, is non-decreasing. Let be the vertices of all dyadic cubes. Because is bounded, it follows that is uniformly bounded and there exists a subsequence such that pointwise convergents on to a function , i.e., . Extend to on entire :

By definition, is non-decreasing. Let the set of discontinuous points of be , and note that is countable, see Borwein et al. (2004). When , then . To see this, by density of and continuity of at , for , there exist such that and . Due to pointwise convergence of at , if is sufficiently large, then and . Also by the monotonicity of , . Since are non-decreasing,

Let , then . Let be any lower set of , choose some , it follows that

with equality if . First let in above inequality, by dominated convergence theorem, it follows that . Due to continuity from below of , i.e. , then let , we obtain for any lower set . Thus, . Next we show Problem (1) and (4) are equivalent under . We denote the objective function of Problem (1) and (4) by . As , by bounded convergence theorem, . Note that , by Theorem 2, and , it follows that and let on both sides, we get . We can obtain stronger results with more mild assumptions on .

Corollary 1

If is a continuous function of bounded variation, i.e.,

converge a.e. to .

Proof of Corollary 1. . By Theorem 3, the second term on RHS tend to a.e., we show the first term is a.e. a Cauchy sequence. The value jump of the ironed part of both and tend to and on the intersections of non-flat parts of and if large enough. Also note that the flat parts become stable because is absolute continuous. In addition, the jump points are countable and the result follows. Proof of Theorem 4. Let us write the principal’s problem as a saddle point problem. The constraint that is non-decreasing in for all can be dealt with by adding where the are non-negative for all with for all . This term can rewritten to yield the following saddle-point problem

| (24) |

We construct the partition used in the proposition and prove it is ortho-convex. First note that for any player, or any dimension, , while fixing , ’s type space is partitioned into intervals such that (i) for ; (ii) for ; and (iii) if then for . Denote this partition by . The following algorithm constructs the ironed or flattened subset of containing . Let . By the Kuhn-Tucker conditions associated with problem (24), any feasible mechanisms requires that be constant in for all . Moreover, . Given , define

The set adds to all intervals with positive multipliers in all dimensions that intersect with (but are not already contained in ). The solution to (15) must be such that is constant on . To see this, suppose is constant on and that there is some and such that and – i.e. an interval in dimension that intersects with and is not inside . Then on by assumption. Using the Kuhn-Tucker conditions associated with problem (24) in dimension , this extends to the entire set . Each iterative set is ortho-convex, after possibly adding some knife-edge type profiles where the monotonicity constraint just binds: take and with . Since any incentive compatible mechanism requires that be non-decreasing in dimension , for any . But so for any . If the interval , add it to the set before moving to the next step. The algorithm ends when the set is empty for all players (i.e. when no intervals not inside the iterative set intersect with the iterative set). Call the resulting set . Then is ortho-covex and . To see the latter, suppose was the final step in the algorithm and that is empty for all players but there exists such that . Then, there must be for some by definition of . But, since for any , it must be that . Therefore and , contradicting the assumption that is empty. Repeating this algorithm for all and all results in a partition of the type space; denote this partition by . Define . Next, we show the saddle-point problem for restricted rights has the strong duality property under the choice of and . From above, we have that for any cell , is contained in one cell of , and, for fixed , is constant on . Because on each ironed interval , , we have

We calculate the value gap between the saddle-point problem and the primal problem under :

We thus have

where the first inequality follows because, for every , and is non-decreasing implies , the second inequality follows from optimality of for , and the final equality follows from the zero value gap. Hence, is optimal for . Therefore, strong duality holds for the saddle-point problem with restricted access rights, is a saddle-point for the Lagrangian, and solves the primal problem.

Lemma 1

If there exist two solutions, and , to (15) then the associated optimal mechanisms and are identical.

Proof of Lemma 1. Since both and are assumed to achieve the maximum in problem (15) and since is strictly convex over the positive range of , we can assume that and whenever . Otherwise, for the convex combination ,

and . Moreover, if and whenever , then . Suppose then that there exists such that and without loss of generality suppose it is the largest type with . Then and for any . But this implies that for all (since otherwise Theorem 4 would require that ). Similarly, if then and we are done. Suppose instead that . There exists such that since and must have the same expectation below . Since is the largest type for which the two solutions differ, . Further, since , ; that is, the monotonicity constraints binds between for and . Furthermore, either or . In words, either the is negative for the type just below or the monotonicity constraints bind between for , and . Iterating in this way, we can conclude that for all which implies that is constant over this interval. Since , Proposition 4 requires . Proof of Theorem 5. We have

The first term on the far right side is equal to zero when and it is equal to when . Let and for with . Then

where we defined

We first show that is doubly stochastic. We have

for all , and

for all . Conversely, if then

since . Proof of Theorem 7. Using partial integration, we have

The inequality in the third line follows from two observations. First, since is non-decreasing in each argument it can be written as a linear combination, with non-negative coefficients, of indicator functions of upper sets , which are upper sets in the hypercube’s boundary with the -th coordinate zero if . Second, (20) implies for any lower set . In particular, for lower sets in the hypercube’s boundary where the -th coordinate is zero if . And since we have for any upper set in the hypercube’s boundary with the -th coordinate zero if . Combining these two observations establishes the inequality. Conversely, suppose for all ortho-concave . Take

where is the indicator function for the lower set as before. Then

and, similarly, . Hence, for any lower set .

References

- Bedard et al. (2020) Bedard, N., J. K. Goeree, and N. Sun: 2020, ‘Optimal Mechanisms for Mass-Produced Goods’. AGORA working paper.

- Bergemann and Morris (2009) Bergemann, D. and S. Morris: 2009, ‘Robust Implementation in Direct Mechanism’. Review of Economic Studies 76, 1175–1204.

- Borwein et al. (2004) Borwein, J. M., J. V. Burke, and A. S. Lewis: 2004, ‘Differentiability of Cone-Monotone Functions on Separable Banach Space’. Proceedings of the American Mathematical Society 132(4), 1067–1076.

- Brualdi and Dahl (2013) Brualdi, R. A. and G. Dahl: 2013, ‘Majorization for Partially Ordered Sets’. Discrete Mathematics 313, 2592–2601.

- Cai et al. (2016) Cai, Y., N. R. Devanur, and S. M. Weinberg: 2016, ‘A duality based unified approach to bayesian mechanism design’. SIAM Journal on Computing 50(3), 160–200.

- Carroll (2017) Carroll, G.: 2017, ‘Robustness and separation in multidimensional screening’. Econometrica 85(2), 453–488.

- Cornelli (1996) Cornelli, F.: 1996, ‘Optimal Selling Procedures with Fixed Costs’. Journal of Economic Theory 71(0106), 1–30.

- Daskalakis et al. (2017) Daskalakis, C., A. Deckelbaum, and C. Tzamos: 2017, ‘Strong duality for a mutliple good monopolist’. Econometrica 85(3), 735 – 767.

- Goeree and Kushnir (2023) Goeree, J. K. and A. Kushnir: 2023, ‘A geometric approach to mechanism design’. Journal of Political Economy Microeconomics, 1(2), 321–347.

- Groves and Ledyard (1977) Groves, T. and J. O. Ledyard: 1977, ‘Optimal allocation of public goods: a solution to the “free rider” problem’. Econometrica 45(4), 783–810.

- Güth and Hellwig (1986) Güth, W. and M. Hellwig: 1986, ‘The private suply of a public good’. Journal of Economics pp. 121–159.

- Hadar and Russell (1969) Hadar, J. and W. R. Russell: 1969, ‘Rules for Ordering Uncertain Prospects’. American Economic Review 59, 25–34.

- Haghpanah and Hartline (2021) Haghpanah, N. and J. Hartline: 2021, ‘When is pure bundling optimal?’. Review of Economic Studies 88, 1127–1156.

- Hanoch and Levy (1969) Hanoch, G. and H. Levy: 1969, ‘The Efficiency Analysis of Choices Involving Risk’. Review of Economic Studies 36, 335–346.

- Hardy et al. (1929) Hardy, G. H., J. E. Littlewood, and G. Pólya: 1929, ‘Some simple inequalities satisfied by convex functions’. Messenger of Mathematics 58, 145–152.

- Hellwig (2003) Hellwig, M.: 2003, ‘Public-good provision with many participants’. The Review of Economic Studies 70(3), 589–614.

- Hwang (1979) Hwang, F. K.: 1979, ‘Majorization on a Partially Ordered Set’. Proceedings of the American Mathematical Society 76, 199–203.

- Ledyard and Palfrey (1999) Ledyard, J. O. and T. R. Palfrey: 1999, ‘A characterization of intermin efficiency with public goods’. Econometrica 67(2), 435–448.

- Levy (2016) Levy, H.: 2016, Stochastic Dominance. Springer Science & Business Media.

- Marshall et al. (2010) Marshall, A. W., I. Olkin, and B. Arnold: 2010, Inequalities: Theory of majorization and its applications. Springer Science & Business Media.

- Muirhead (1903) Muirhead, R. F.: 1903, ‘Some methods applicable to identities and inequalities of symmetric algebraic functions of letters’. Proc. Edinburgh Math. Soc. 21, 144–157.

- Mussa and Rosen (1978) Mussa, M. and S. Rosen: 1978, ‘Monopoly and Product Quality’. Journal of Economic Theory 18, 301–317.

- Myerson (1981) Myerson, R. B.: 1981, ‘Optimal Auction Design’. Mathematics of Operations Research 6(1), 58–73.

- Norman (2004) Norman, P.: 2004, ‘Efficient mechanisms for public good with exclusions’. The Review of Economic Studies 71(4), 1163–1188.

- Ollár and Penta (2017) Ollár, M. and A. Penta: 2017, ‘Full implementation and belief restrictions’. American Economic Review 107(8), 2243–2277.

- Ollár and Penta (2021) Ollár, M. and A. Penta: 2021, ‘A network solution to robust implementation: The case of identical but unknown distributions.’.

- Rochet and Choné (1998) Rochet, J.-C. and P. Choné: 1998, ‘Ironing, sweeping, and multidimensional screening’. Econometrica 66(4), 783–826.

- Rothschild and Stiglitz (1970) Rothschild, M. and J. Stiglitz: 1970, ‘Increasing Risk I: A Definition’. Journal of Economic Theory 2, 225–243.

- Roughgarden and Talgam-Cohen (2016) Roughgarden, T. and I. Talgam-Cohen: 2016, ‘Optimal and robust mechanism design with interdependent values’. ACM Transactions on Economics and Computation 4(18), 18:1–18:34.