Procurement in welfare programs: Evidence and implications from WIC infant formula contracts††thanks: This paper supersedes an earlier version “Who Pays for WIC’s Formula? A Structural Analysis of the US Infant Formula Market”. We are grateful to Jorge Balat, Steve Puller, Aviv Nevo, Marc Rysman, Frank Verboven, Mo Xiao, Daniel Xu, Wei Zhao, and seminar participants at Central University of Finance and Economics, Fudan University, North Carolina State University, Vanderbilt University, Wuhan University, the 15th Annual International Industrial Organization Conference (2017), the 87th Annual Meeting of the Southern Economic Association (2017) for helpful comments or discussions. We thank the Economic Research Service of USDA and personnel from the Food and Nutrition Service of USDA for support collecting and organizing manufacturer bid data.

Abstract

This paper examines the impact of government procurement in social welfare programs on consumers, manufacturers, and the government. We analyze the U.S. infant formula market, where over half of the total sales are purchased by the Women, Infants, and Children (WIC) program. The WIC program utilizes first-price auctions to solicit rebates from the three main formula manufacturers, with the winner exclusively serving all WIC consumers in the winning state. The manufacturers compete aggressively in providing rebates which account for around 85% of the wholesale price. To rationalize and disentangle the factors contributing to this phenomenon, we model manufacturers’ retail pricing competition by incorporating two unique features: price inelastic WIC consumers and government regulation on WIC brand prices. Our findings confirm three sizable benefits from winning the auction: a notable spill-over effect on non-WIC demand, a significant marginal cost reduction, and a higher retail price for the WIC brand due to the price inelasticity of WIC consumers. Our counterfactual analysis shows that procurement auctions affect manufacturers asymmetrically, with the smallest manufacturer harmed the most. More importantly, by switching from the current mechanism to a predetermined rebate procurement, the government can still contain the cost successfully, consumers’ surplus is greatly improved, and the smallest manufacturer benefits from the switch, promoting market competition.

Keywords: WIC, government procurement, social program, market competition

JEL: D44, D82, C14, C57, H57, L13, L74, R42

1 Introduction

Means-tested welfare programs, such as Medicaid, the Supplemental Nutrition Assistance Program, and the Temporary Assistance for Needy Families, are prominent in the U.S. On average, over 20 percent of all U.S. families participated in at least one major means-tested program per month, and the spending on federal programs expanded rapidly and reached $1078 billion in 2020.111See Foster and Rojas (2018) and Landers et al. (2021) for summary of federal welfare programs. In many of those programs, the government procures products or services from private sectors using a variety of mechanisms and provides them to program participants. Government procurement naturally separates consumers into two segments, one comprising non-participants and the other comprising less price-sensitive program participants. Market segmentation can distort manufacturers’ behavior and affect non-participating consumers. The distortionary impacts depend on factors such as the procurement mechanism, the program size, the market structure, etc. Despite its importance in program evaluations and policy recommendations, there is very limited literature on government procurement’s effects on markets and non-participating consumers. This paper aims to fill the gap by documenting such distortionary effects in the U.S. infant formula market, disentangling factors and channels driving the impacts, and simulating the effects of alternative procurement mechanisms.

Over half of the sales in the U.S. infant formula market are procured for the WIC participants from the three dominating manufacturers – Abbott, Mead Johnson (MJ), and Nestlé.222Nestlé purchased Gerber baby foods in 2007 and marketed infant formula under the Gerber Good Start brand name. Nestlé’s infant formula production and brands were purchased by Perrio in 2022. In each state, the manufacturers compete to exclusively serve WIC participants through a first-price auction by bidding a rebate for their selected auction brands. The manufacturer with the lowest net price, computed as the wholesale price minus the rebate, wins a multi-year contract to serve exclusively WIC participants in the state. The auction data on rebates are striking: manufacturers submit extremely high rebates relative to their wholesale prices to win WIC contracts. Specifically, submitted rebates exceed 80% and 90% of wholesale prices for more than 75% and 25% bids, respectively, which significantly contain the cost of the program.

Motivated by the success of the auction, we answer five crucial questions in this market and beyond. First, what are the underlying determinants of the high rebates offered by the manufacturers? Second, what role does the WIC program size play in the impact of the auction procurement? Third, how does the connection between the two market segments affect non-WIC consumers’ retail prices? Would it incentivize the manufacturers to charge a higher retail price so that the non-WIC consumers partially bear the rebate provided to the government? Fourth, how does the procurement auction affect the market structure, particularly the competition among the manufacturers? This question is of particular importance because Wyeth-Ayerst (Wyeth), the fourth major infant formula manufacturer, exited the market in 1996, several years after the onset of the auction mechanism. Competitive bidding for the exclusive right to serve WIC participants is one of the main driving forces of the exit.333Moore, A. K. (1996, January 29), Wyeth-Ayerst Leaving U.S. Formula Market. Retrieved from https://www.supermarketnews.com/archive/wyeth-ayerst-leaving-us-formula-market. Lastly, would the other prevalent procurement mechanism - a predetermined rebate chosen by the government - be better for consumers, manufacturers, and the government? The answer to this question is vital for policymakers to design future procurement rules. We answer all the aforementioned questions by presenting reduced-form evidence, proposing and estimating a structural model of the market, and conducting counterfactual analyses.

We first conduct reduced-form analyses to document the significant impact of winning a WIC contract on the non-WIC markets. We find that non-WIC sales rise significantly upon winning a WIC contract.444Huang and Perloff (2014) demonstrate that a spillover effect is likely essential for manufacturers to compete in the market. Compared with losing an auction, winning boosts the winner’s non-WIC sales for auctioned and non-auctioned brands by about 80% and 130%, respectively. Retail prices also rise upon winning. Specifically, the retail price of the winner’s auction brand is 8% higher than that from losing. The prices of its non-auction brands rise with a smaller magnitude but are not statistically significant. These results indicate that the WIC auction procurement might distort the non-WIC market outcome despite the price regulation by the federal government.

To explore and disentangle the determinants and channels of the distortionary effects, we propose a structural model to characterize the behaviors of manufacturers and non-WIC consumers in the infant formula market. We model the demand of non-WIC consumers in the traditional random coefficient discrete choice fashion and allow non-WIC consumers to prefer the products of the winning manufacturer. On the supply side, manufacturers compete sequentially in two stages: they submit rebates to compete for the WIC contract in the first stage and then set retail prices after observing the auction outcome. We mainly focus on the pricing competition in the second stage and rely on a flexible reduced-form analysis to capture the determinants of the rebates in the auction stage.

Several new features distinguish our model of price competition from the existing ones. First, the auction winner faces two demand segments - regular non-WIC consumers and price-insensitive WIC consumers. Second, the winning brand’s retail price is regulated to have an implicit cap, and the two segments cannot be discriminated in price. The existence of price-insensitive consumers and the price regulation in the market impose unprecedented challenges on our analysis of the retail pricing game. On the one hand, economic theory suggests that if consumers are price-insensitive, the price should be as high as possible. On the other hand, price regulation effectively restricts the equilibrium price that can be reached. The two features work in opposite directions, resulting in a slightly higher equilibrium price from our reduced-form analyses. It is unclear in the existing literature how to model price competition incorporating both features. To tackle this challenge, we propose a novel sequential pricing model, where, first, the winning manufacturer determines the price for the WIC brand based on the non-WIC demand, then raises the equilibrium price for the brand for both segments of consumers based on the information of demand and regulations. We allow such a pricing strategy to be manufacturer-specific. Second, given the price of WIC brands, the manufacturers conduct Bertrand price competition to determine the prices of other brands. It is worth noting that we also allow possibly lowered marginal costs for winning manufacturers, capturing cost savings from the economies of scale, less promotion and advertisement spending, etc.

We estimate the model using sales data from NielsenIQ and manufacturers’ rebates data from the U.S. Department of Agriculture (USDA)’s Food and Nutrition Service (FNS). The first step is to estimate the consumers’ preferences using the BLP approach (Berry et al. (1995)), confirming a sizeable spill-over effect of winning a WIC auction on the demand of non-WIC consumers. This indicates a great advantage for winning manufacturers in the non-WIC market. Next, we recover the marginal cost using the estimated demand parameters and the observed retail prices. We find considerable cost savings upon winning, and all three manufacturers raise the prices of their WIC brands after winning. These findings rationalize the significant rebates provided by manufacturers and address the first question raised.

We further show that, on average, winning manufacturers’ after-rebate prices to WIC agencies are significantly lower than their corresponding marginal costs for more than half of the winning markets, resulting in negative profits in the WIC market. Nevertheless, their loss in the WIC market is compensated by extra profit in the non-WIC market, in which the winners enjoy a high price-cost margin (around 50%) due to the substantial spillover effect and considerable cost savings. We also found that the marginal cost is significantly lower than the wholesale price, suggesting that manufacturers enjoy large market power in the non-WIC market.

Using the demand and supply estimation results, we answer the four remaining questions by simulating the market outcomes, including manufacturers’ profits, consumer surplus for both WIC and non-WIC consumers, and government expenditures in different hypothesized market mechanisms. First, to fully evaluate the impact of the WIC auction, we simulate and compare the market outcomes with and without the WIC auction, where in the latter scenario, the government provides a voucher for quantities of food, as in the case of all food products provided by the WIC program. We find that (1) without the WIC auction, consumer surplus would increase 11%, with WIC and non-WIC consumers better off and worse off, respectively. WIC consumers are better off because of the availability of more options555Under the current WIC program, infants can only choose the brand contracted by the state agency, which restricts the WIC participants’ choices and, thus, their welfare is affected negatively. The consequences of such restriction are even more severe during the 2022 infant formula shortage.. Surprisingly, non-WIC consumers would be worse off. This is due to the lower retail prices resulting from the spillover effect and cost savings enjoyed by the winner when the WIC auction is used for procurement. (2) The WIC auction significantly reduces manufacturers’ profits. Nestlé, the smallest manufacturer, faces the most significant negative impact of the auction. Compared with procured without auctions, the profit of Abbott, MJ, and Nestlé drops by 42%, 58%, and 75%. (3) As expected, the government can contain the cost using the auction mechanism. Specifically, the government’s monthly expenditure reduces by 65% due to the WIC auction.

We next investigate how WIC program size affects the market outcomes, mainly the manufacturers’ profits in the current mechanism with the auction. We find that the larger the program size, the higher profits for the two larger manufacturers. In contrast, the profit of the smallest manufacturer Nestlé decreases in the WIC program size. Our finding confirms the statement of Wyeth, which had a similar market share as Nestlé, that “ the increasing growth of the WIC Program contributed to the decision” of exiting the domestic market. An important implication of our finding is that the impacts of WIC auctions on manufacturers are asymmetric and small ones suffer more. This might imply that the WIC auction is an entry barrier in the infant formula market.

Finally, we explore another prominent procurement mechanism: predetermined rebates, employed by the Medicaid drug rebate program (MDRP). Under such a mechanism, manufacturers voluntarily join the program and provide products or services to program participants by accepting the rebates determined by the government ex ante. We simulate the market outcomes if the government switches from competitive bidding procurement to predetermined rebates. We find that in the mechanism of predetermined rebates, the government pays 27% more relative to the competitive bidding. However, both consumer surplus and total surplus would be higher. The surplus of WIC consumers increases substantially (25.5%) while that of non-WIC consumers decreases slightly (5.1%). Manufacturers, again, are affected asymmetrically. Nestlé’s profit would be 47.3% higher while that for Abbott and MJ would be 30.3% and 14.8% lower, respectively.

This paper contributes to the literature by thoroughly analyzing the infant formula market, explaining the unreasonably high rebate, and evaluating the impacts of WIC on nonparticipants. To the best of our knowledge, this is the first work to model and estimate pricing competition with two market segments, where one is price inelastic.666Abito et al. (2022) also study the WIC program. Their focus is on the spill-over effect in the demand size. They assume manufacturers conduct Bertrand pricing competition on the supply side but only maximize non-WIC profits without incorporating the two market segment features. Moreover, they do not model the price regulation by the government, which results in a negative marginal cost estimate. Using an event study, Oliveira et al. (2004) argue that non-WIC consumers are price insensitive. Thus, retailers increase the contracted brand’s price. Similarly, using a Cournot oligopoly model, Prell et al. (2004) also attributes the substantial rebate and relatively high wholesale prices to the demand elasticities of consumers. Our paper is fundamentally different from the existing work in that (1) we model manufacturers’ pricing strategies in non-WIC and WIC markets jointly by a sequential game; (2) we utilize both sales data and manufacturers’ rebates for estimation; and (3) we rigorously investigate the impacts of the WIC program by counterfactual analyses.

Our paper is also related to other studies on infant formula, focusing on different topics. Huang and Perloff (2014) and Oliveira et al. (2010) identify a spillover effect as an essential factor in setting prices for infant formula. Davis (2011) considers the spillover effect and shows that manufacturers’ marginal costs are often lower than the after-rebate prices. Hence, the WIC program has no impact on non-WIC consumers. Black et al. (2004) and Miller et al. (1985) document the effects of WIC formula on the health outcomes of infants. More generally, Meckel (2020); Li et al. (2022) study impacts of Electronic Benefit Transfer on the WIC program. McLaughlin et al. (2019) focus on authorized vendors that derive more than 50% of their food sales through WIC.

Our counterfactual analyses shed light on how government procurement may affect market competition and nonparticipants’ behavior toward other welfare programs. Although the infant formula market is uniquely characterized by the rebate program and high concentration, our analysis and empirical results can provide useful tools and policy implications to other markets where government programs affect related markets. The existing literature on welfare programs is largely silent on the programs’ distortionary effects on the market and nonparticipants. A notable exception is Duggan and Morton (2006), which finds that government procurement methods in the Medicaid program can change the equilibrium price of pharmaceuticals and product proliferation in the private sector. Our paper fills the gap by providing empirical evidence that WIC’s rebate and auction procurement method serves as a barrier for manufacturers with small market shares to enter or grow in the market.

Finally, this paper is also related to the literature on consumer subsidy policies where manufacturers compete for their products’ eligibility for a subsidy. Fan and Zhang (2022) studies a Chinese cellphone subsidy program “Home Appliances Going to the Countryside,” and finds that such competition mitigates price increases and improves consumer and total surpluses while limiting government subsidy payments. Our paper is different in that we explicitly model manufacturers’ competition for eligibility, while Fan and Zhang (2022) assumes the eligibility is given exogenously.

The outline of the paper is as follows. Section 2 provides institutional background on the US infant formula market and describes the data used for analyses. Section 3 presents some reduced-form analyses of the effects of winning a WIC contract on sales and prices. Section 4 proposes a structural model of manufacturers’ two-channel competition. Section 5 describes the identification and estimation strategies. Section 6 presents the estimation results. Section 7 conducts several counterfactual analyses, and Section 8 concludes. Figures and tables are in the appendix.

2 The Institutional Background and Data

2.1 The WIC program

The WIC program, established in 1972, provides various services and supplemental foods for low-income women, infants, and young children under five years of age. The program is administered jointly by the FNS of USDA and authorized state agencies. A family member at nutritional risk is eligible if (1) the family income is less than 185% of the U.S. poverty income guidelines or (2) the family is enrolled in the federal Medicaid, Food Stamp, or Temporary Assistance for Needy Families programs, even if the family income exceeds 185% of the poverty line.777States may use enrollment status in other means-tested programs, such as the National School Lunch Program or the Supplemental Security Income program, to qualify an applicant as automatically eligible for WIC. The program participants receive vouchers to redeem at authorized retail stores. State agencies reimburse retailers for the items sold to WIC participants based on the redeemed vouchers. WIC provides infant formulas for participated infants from 0 to 12 months. During our data period 2006-2015, 47.4% infants participated in the WIC program.

WIC state agencies purchase infant formulas using a competitive bidding process (sealed-bid auction) under the federal law implemented in 1989 to contain the procurement costs. WIC state agencies can solicit bids independently or as part of multistate alliances.888Currently, there are five multistate alliances and territories and Indian tribal organizations. Mountain Plains (Missouri, Nebraska, South Dakota); Southwest, Mountain Plains, and Midwest (Iowa, Minnesota, and Texas); New England and Tribal Organizations (Connecticut, Maine, Massachusetts, New Hampshire, and Rhode Island); Western States Contracting Alliance (Alaska, Arizona, Delaware, District of Columbia, Hawaii, Idaho, Kansas, Maryland, Montana, Nevada, Oregon, Utah, Washington, West Virginia, and Wyoming); Southwest Region (Oklahoma); and Southwest/Southeast (Arkansas, New Mexico, and North Carolina). In 2004, Congress limited the size of new alliances to 100,000 participating infants and limited the ability of current alliances with over 100,000 participating infants to expand. Those states with home delivery (Vermont) or direct distribution (Mississippi) or Indian State agencies with 1,000 or fewer participants are exceptional and excluded from our analysis. The auction proceeds as follows. Infant formula manufacturers submit sealed bids that specify a rebate for the brands they choose to participate in the program, i.e., auctioned brands. Those auctioned brands usually are infant formulas suitable for routine issuance to generally healthy, full-term infants. The contract is awarded to the manufacturer asking for the lowest net price, calculated as wholesale price subtracts rebate. A contract typically lasts three years; occasionally, it can be extended via negotiation between the winning manufacturer and the state agency. WIC infants can only get the contracted brand during the contract period.999Most state agencies also provide alternative therapeutic formulas for those infants with special needs if a medical documentation form or medical prescription is provided. The percentage of therapeutic formulas is negligible.

The cost of infant formula to the WIC program is the difference between the WIC brand retail price and the winning manufacturers’ rebate. The state agency regulates the retail prices of WIC infant formula. The motivation for such regulations is that WIC consumers are price insensitive, so profit optimization manufacturers/retailers might charge a very high retail price, which would work against the cost containment objective. Even though the regulation details vary across states, the main limitations on retail prices are that they must be competitive with, and within the limitations for, similarly situated vendors, e.g., in terms of type and size of the store and geographic location. Such a price restriction is imposed as a requirement for obtaining the eligibility to carry WIC products in the state.101010In addition to price regulations, there are some other selection criteria for authorizing retailers to carry WIC products, e.g., a minimum stock of WIC products, accessibility to participants and WIC staff, business integrity, etc. Only authorized retailers are eligible to obtain reimbursement from the redeemed vouchers. An example of the regulation is that the WIC agency sets price ceilings, called maximum allowable redemption rates or maximum allowable reimbursement level (MARL), by peer group for each food instrument the group redeems. Different states impose different regulations to implement the MARL. Some states set a specific number as MARL, e.g., Pennsylvania. Others set it to be a percentage of prices for the peer group, e.g., Texas.

2.2 The infant formula market and data

2.2.1 The market

Infant formula is vital for formula-feeding babies’ healthy growth and development in their first year. In the U.S., approximately 54% and 74% of infants in 2018 were partially or fully fed with formula after 3 and 6 months, respectively.111111https://www.cdc.gov/breastfeeding/data/nis_data/results.html, retrieved May 27, 2022. The U.S. infant formula market size is $3.65 billion in 2019 and is projected to increase by 5.8% annually. There are three major manufacturers in the market: Abbott, MJ, and Nestlé with their leading infant formula brands being Similac, Enfamil, and Gerber, respectively.121212Wyeth was active in the domestic market until 1996 and discontinued its premium formulas in the US. In 1997, Wyeth reentered the US market as a producer of infant formula for PBM Products, Inc., which produces most of the generic-branded infant formula in the US and holds about a 1% market share. The generic formula is usually sold at much lower prices compared to the products of the three major manufacturers. The three manufacturers dominate the market, with their domestic market shares being 39.9% for Abbott, 39.7% for MJ, and 15.2% for Nestlé in 2005-2016. Each manufacturer produces its infant formula in several production centers. The production centers of Abbott are in Casa Grande, AZ; Columbus, OH; Sturgis, MI; and Alta Vista, VA. MJ’s are in Evansville, IN; Zealand, MI; and Springfield, MO. Nestlé only has one production center in Eau Clair, WI.

The main products in the market are milk- and soy-based infant formula with three physical forms: liquid concentrate, powder, and ready-to-feed. Milk-based powder dominates the market with a 78.3% of market share, while the shares of milk-based liquid concentrate, milk-based ready-to-feed, soy-based powder, liquid concentrate, and ready-to-feed are 4.4%, 7.0%, 8.6%, 1.0%, and 0.7%, respectively. To simplify our analysis, in this paper, we focus on milk-based powder, which involves 20 brands from the three leading manufacturers. We also exclude formula brands that target children between 12-24 months because WIC provides infant formulas for participating infants from 0 to 12 months only.

2.2.2 Data

Our data are from a variety of sources: (1) the price, volume, and sales of infant formula are from the Retail Scanner data from NielsenIQ; (2) nutritional characteristics of infant formula are collected from brands’ websites; (3) the national wholesale prices and bids for WIC auctions are from the Food and Nutrition Service of USDA; (3) demographics and cost shifters of infant formula are from various sources.

The Retail Scanner data provide information from 2006 to 2015 on infant formula’s dollar and volume sales in supermarkets, grocery stores, and drug stores from more than 90 participating retail chains in 48 states (no data on sales in Alaska and Hawaii) and the District of Columbia. In addition, the data consist of detailed information on product characteristics, e.g., brand names, container sizes, package sizes, etc., and location and time of sales.

The dollar sales and volume of infant formula for non-WIC consumers are calculated using the Retail Scanner data, the number of WIC and non-WIC infants, as well as the breastfeeding rates of WIC and non-WIC infants at the state-year level. The main idea is based on the representative nature of the NielsenIQ sales data, which allows us to reasonably approximate the ratio of non-WIC formula sales to the total sales in our data by using the proportion of formula-feed non-WIC infants to all formula-feed infants in the general population. The construction details are in Appendix A.

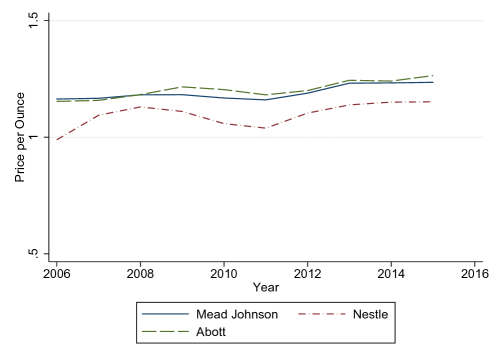

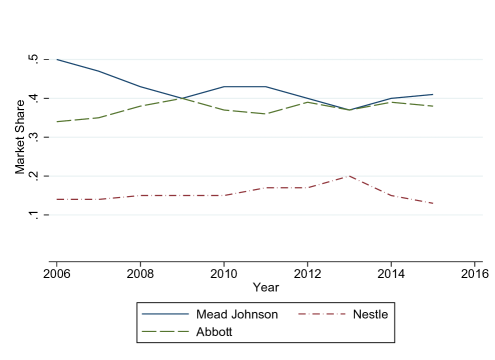

We present summary statistics for milk-based powder across all states and years in Table 1. At the state level, the average monthly non-WIC dollar sales for all the brands is $444,430, the average monthly volume sold is 391,730 ounces, and the average sales-weighted retail price is $1.16 per oz. MJ leads the market with an average monthly sales of $626,580, followed by Abbott and Nestlé. The prices for MJ and Abbott are $1.21 and $1.22 per oz, respectively, which are very close. Nestlé charges a much lower price $0.94 per oz. We display the average prices and market shares for the three manufacturers from 2006-2015 in Figure 1, from which the market structure is very robust for our sample period: Nestlé continues to be the smallest manufacturer and to ask for a significantly lower price among the three dominant manufacturers

The auctioned brands of milk-based powdered formula for the three manufacturers are Similac Advance, Enfamil Infant, and Gerber Good Start. In most cases, only one brand, known as the auctioned brand, is provided to all WIC infants from the manufacturer who emerges as the winner in the WIC auction. For instance, in Pennsylvania in 2016, Similac Advance from Abbott was the exclusive milk-based formula for WIC infants. There are occasional instances in certain states where more than one brand from the winning manufacturers is supplied to WIC infants. For example, in Connecticut, there are occasions when Similac Sensitive is provided alongside Similac Advance, which is the contracted brand. Nonetheless, the sales of these additional brands are generally minimal. To simplify our analysis, when multiple WIC formulas are available in a state, we aggregate all the products into a single auctioned brand. Subsequently, we calculate the sales-weighted nutritional characteristics for the aggregated auctioned brand. In this study, we focused on two specific characteristics of infant formula: anti-spit-up and probiotics. While there are other essential characteristics in infant formula, such as iron or DHA, we were unable to include them because almost all the formula products contain iron and DHA.

The WIC auction data include a panel of the three manufacturers’ annual national wholesale prices and rebates for milk and soy-based infant formula with three physical forms in 48 states and the District of Columbia (DC) from 1988 through 2015.131313 Vermont used a home-delivery system, and Mississippi used a direct distribution system during our study period. Therefore, we exclude them from our analysis. Both states have now transitioned to retail delivery with the adoption of EBT. The details of the WIC contracts, e.g., previous winner, starting and ending time, and alliance status, are also available in the data. Wyeth also participated in the WIC auctions from 1988 to 1996 but exited the market afterward. To avoid modeling Wyeth leaving the market, we use the auction data from 1998, after which only MJ, Abbott, and Nestlé are potential bidders.

The WIC auctions can be categorized into uncoupled and coupled ones. Specifically, in the coupled auctions, milk and soy-based formulas either have the same percentage rates or their rebates are determined by complicated and unknown procedures. In the uncoupled auctions, the state agency hosts separately one auction for milk and one for soy formula. We only keep auctions for milk-based powder, including the uncoupled and those coupled ones with milk and soy-based formula having the same percentage of rebates.141414In the data, the winner of a contract is always consistent with the winner of the milk-based power auctions.

Table 2 presents summary statistics of the three manufacturers’ national wholesale prices and rebates, both in dollar per ounce and their ratio. On average, the national wholesale price is $1.032 per ounce, the rebate is $0.858 per ounce, and the rebate-wholesale price ratio is 82.4%, which is substantial. Nestlé’s rebate-wholesale price ratio is 86.4%, higher than that of Abbott and MJ, whose ratios are 79.7% and 82.5%, respectively. Some of Nestlé’s rebates are even higher than its wholesale prices. For all three manufacturers, the rebate-wholesale price ratio is over 90% for more than 25% rebates submitted. In other words, the manufacturers only charge the WIC program 10% of their national wholesale price for over 25% of WIC contracts.

3 Reduced-form evidence

In this section, we present reduced-form evidence on the distortionary effects of the WIC program on the infant formula market. The analysis is motivated by the high rebates shown in Table 2, demonstrating that manufacturers compete aggressively for the WIC contracts.

Intuitively, the aggressive competition for the WIC markets could be rationalized by the following features. First, the marginal cost for the manufacturers is very low, so it is still profitable to serve the WIC market with a high rebate. For this to be consistent with the significantly high retail price in the non-WIC market, non-WIC consumers need to be highly price insensitive. Second, the marginal cost is not very low so the winner suffers a loss from winning, but there are additional benefits in both demand and supply to winning the WIC contract. Therefore, the additional benefit compensates for the loss, so the overall effect of winning is still desirable. Specifically, winning a WIC contract might boost the demand of non-WIC consumers and decrease the winner’s marginal costs due to economies of scale, saving in advertisements, transportation, etc. Since marginal costs are unobserved in the data, we provide some regression patterns to investigate how the equilibrium prices and sales change when the manufacturers are WIC winners.

3.1 The effects of winning on volume sales

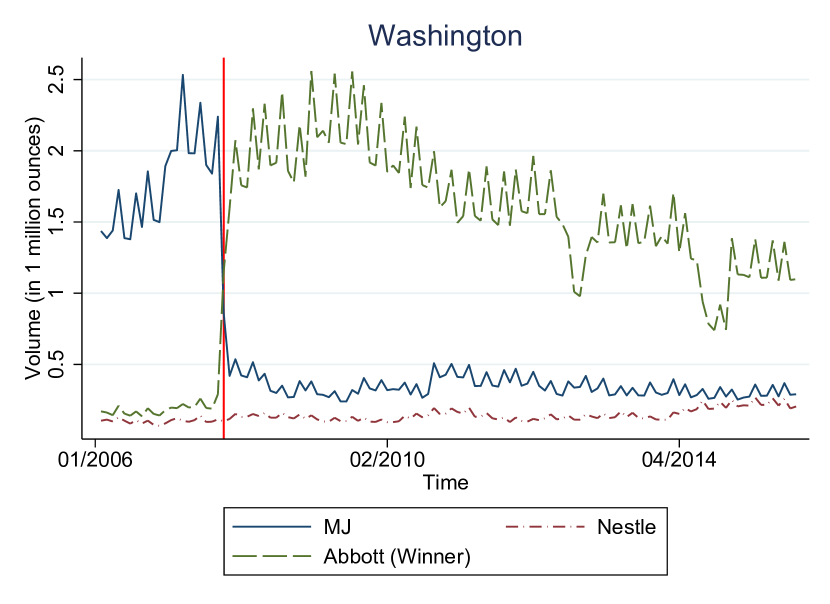

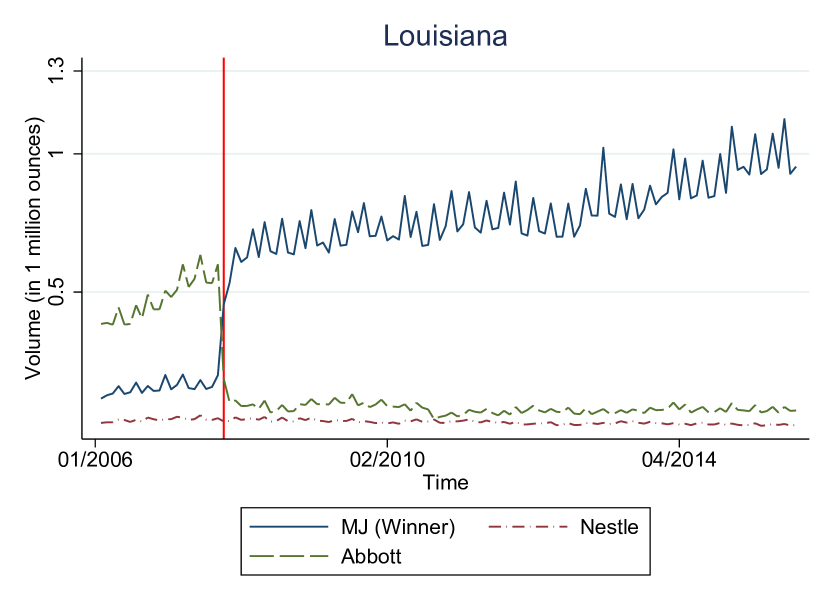

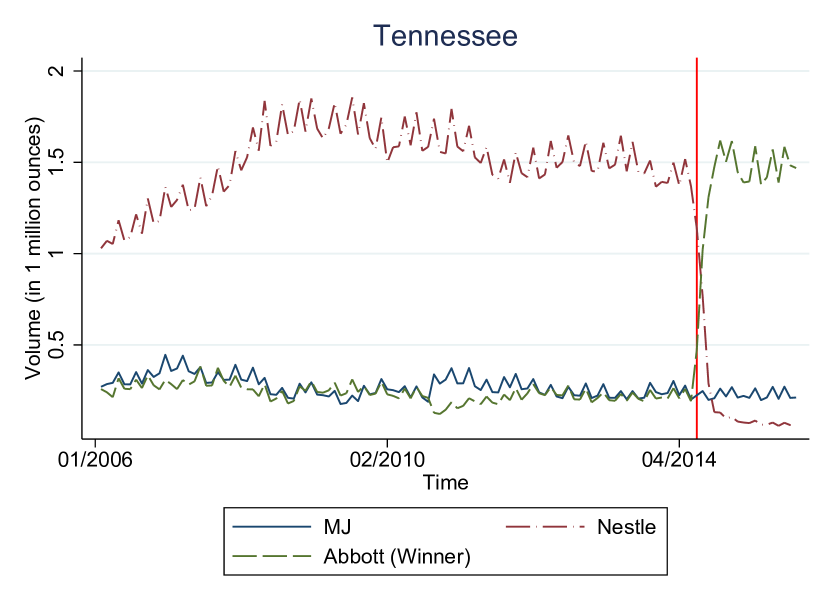

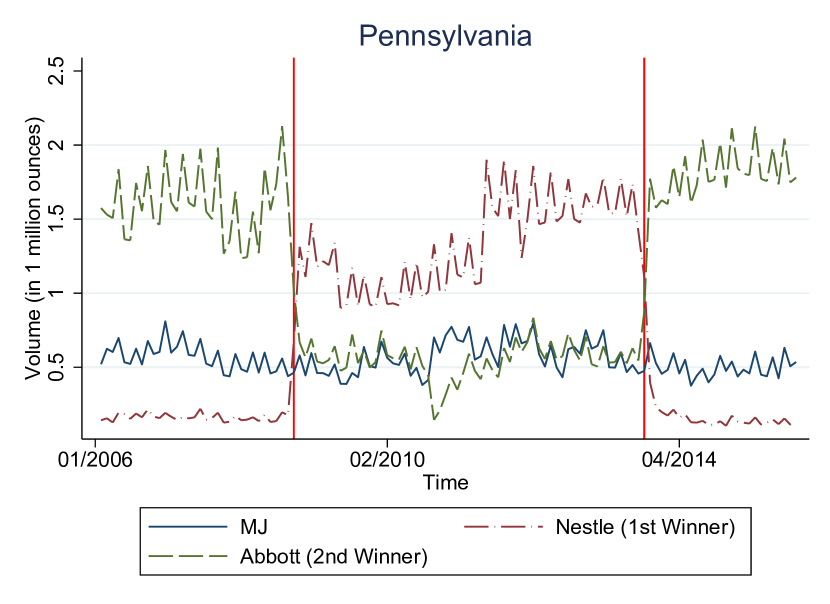

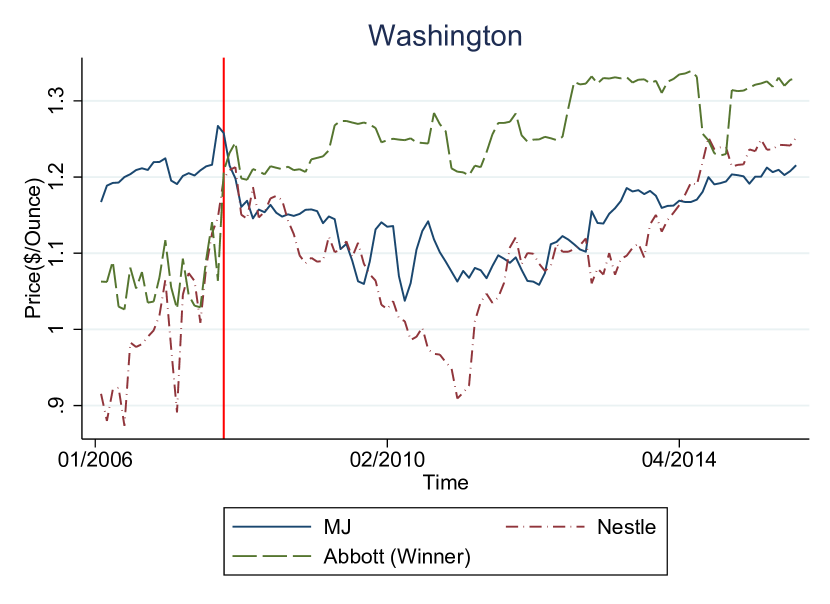

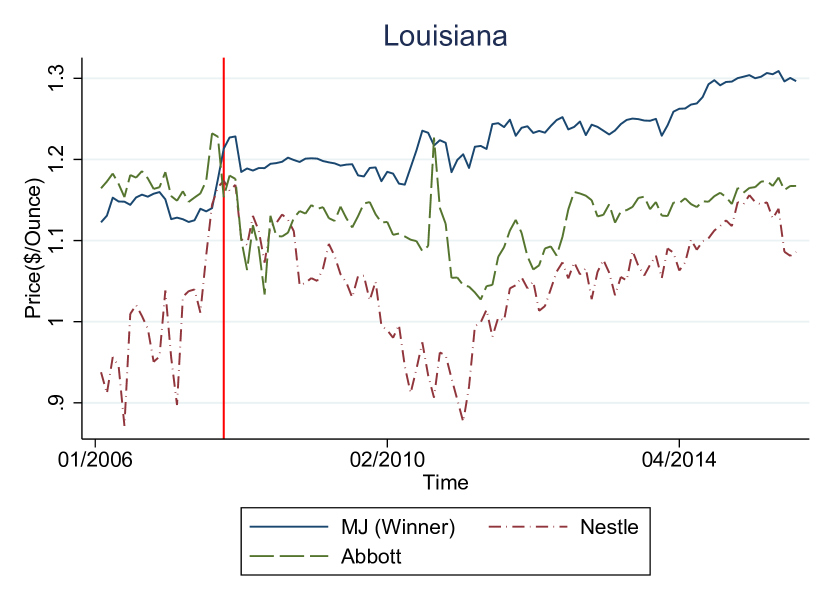

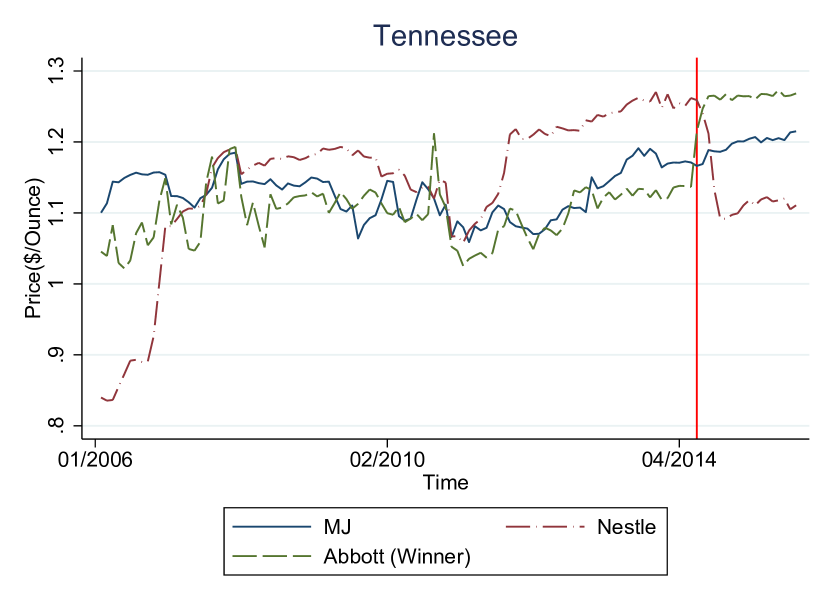

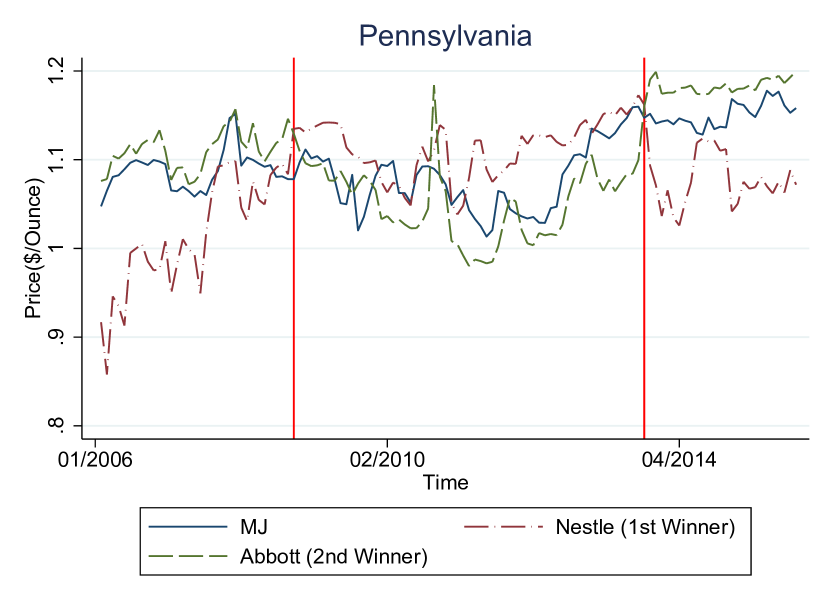

We first provide some visualization of the impact of winning a WIC contract on non-WIC sales. Figure 2 provides a visual illustration of the impact using Louisiana, Pennsylvania, Tennessee, and Washington as examples. The red vertical line indicates when the winner changes during the data period. For the three states except for Pennsylvania, the winner changed from MJ to Abbott, Abbott to MJ, and Nestlé to Abbott, respectively. For Pennsylvania, the winner switched from Abbott to Nestlé and then to Abbott. All four states display a similar pattern; we only describe it for Washington. MJ dominates the non-WIC infant formula market when it has a WIC contract. However, the volume sales of MJ plummeted when Abbott became the winner starting from October 2007, and the volume sales of Abbott in the non-WIC market skyrocketed immediately after the new contract began. The volume sales of Nestlé are relatively stable during the whole period.

To quantify the effect of winning WIC contracts on non-WIC sales, we run a series of simple pooled regressions of the logarithm of volume sales on an indicator of winning and other covariates.

| (1) | |||||

where denotes manufacturer, denotes brand, denotes state, denotes month, denotes the volume sales for manufacturer ’s brand in state at month , and are state and brand fixed effects, respectively, is a manufacturer dummy, is a dummy variable indicating whether manufacturer is the winner in market at year , is a dummy variable indicating whether brand is the auctioned brand of manufacturer , which does not vary across market and month . is the logarithm retail price of brand for manufacturer in market and month , includes a variety of covariates, such as the number of non-WIC infants and other demographic variables that may affect the demand of infant formula. In equation (1), captures the spillover effect, allows the spillover effect to be different for the WIC and non-WIC brands, and and describes the variation of the spillover effects across manufacturers.

In the regression above, prices are potentially endogenous because they are from the equilibrium. We use raw milk price, the average distance between manufacturers’ production centers to the market, and the electricity rate as instrumental variables for prices. These instruments are valid because they affect infant formula production and retail costs and, thus, are correlated with prices in the focal market; however, these factors are uncorrelated with market-specific demand shocks.

We present the regression results in Table 3. The main finding is that the non-WIC sales for the same manufacturers are much larger when winning than losing. The results in column (3) show that winning a WIC contract boosts the sales of non-auctioned and auctioned brands by 75% and 126%, respectively. The impacts of winning on sales are heterogeneous across manufacturers. For non-auctioned brands, the increase in sales for MJ is larger than that for Abbott and Nestlé, but for auctioned brands, the rise in sales for MJ is smaller than that for Abbott and Nestlé. The larger benefit from winning for Nestlé and Abbott relative to MJ could be due to their relatively small market shares.

Several possible channels may lead to the above positive spillover effects. First, since the winning brand serves the WIC market exclusively, retailers adjust by allocating more shelf space and better product placement for this brand. Second, hospitals and physicians often recommend the winning brand considering that around half of the newborns are eligible for WIC. For example, the WIC agency in Wisconsin explicitly requires physicians to recommend the WIC brand.151515Source: https://www.dhs.wisconsin.gov/publications/p4/p40023.pdf, retrieved on March 22, 2023. Third, being the WIC brand may increase credibility for some non-WIC consumers, which might also serve as advertisements for WIC brands. Last but not least, WIC participants may affect non-WIC consumers through social networks or peer effects.

?3 presents the heterogeneity in the spillover effects across manufacturers. Overall, compared to Mead Johnson, Nestlé and Abbott benefits the most from winning the auctions. As a top seller in almost all markets, Med Johnson will not experience a percentage increase in volume sales as high as as the other two manufacturers from winning the auctions.

3.2 The effects of winning on retail prices

Since WIC consumers are price inelastic, a retailer that serves non-WIC and WIC consumers could increase its profit by setting a higher price for the winning brand. Nevertheless, such an incentive may be dampened by the WIC regulation. Therefore, to investigate whether winning a WIC contract increases retail prices, we run a series of regressions of retail prices on a winning indicator and other covariates.

| (2) | |||||

where is a vector of cost shifters, including the raw milk price, electricity rate, and distance between retailers and manufacturers. In the price regression above, the volume sale is endogenous because it is affected by price. We use demand shifters, such as the number of non-WIC infants, the logarithm of median income in a market, and the percentage of women labor participation in a market, as the instrument variables for the logarithm of volume sales.

We present the regression results in Table 4. There are several interesting observations from the results. First, we document a significant distortionary effect of the WIC contract on the price for non-WIC consumers. The results in column (3) demonstrate that the prices of winning manufacturers’ auctioned brands are 8.1% higher. However, winning a WIC contract does not significantly affect the price of the winner’s non-auctioned brands. Note that the price of auction brands does not differ significantly from non-auction brands for losing manufacturers. Second, the effects of winning a WIC contract on prices are heterogeneous across manufacturers. For auctioned brands, the price increases for Abbott and Nestlé are 8.5% and 7.9% higher than MJ, as shown in column (6).

In summary, the regression results in this section document a significant distortionary effect of the WIC contract on the prices and quantities of the winner’s brands. To further explore these sources, we propose a structural model of the market for infant formula in the next section.

4 The Model

This section presents a structural model concerning demand and supply for the US infant formula market. We first describe consumers’ preferences and then propose a supply model where manufacturers compete sequentially for WIC contracts and retail pricing. In the retail pricing part, we further propose a two-step pricing game in that the winner determines the price for the WIC brand, and then all manufacturers do Bertrand pricing for the non-WIC brands.

4.1 Demand

Suppose we observe markets, where a market is defined as a state-month combination.161616In our analysis, we treat a multistate alliance as a state. Its demographics are taken average across the states in the alliance. For ease of notation, Let and denote a generic manufacturer and the WIC auction winning manufacturer, respectively; , , and denote a generic, auctioned, and WIC (winning) brand, respectively; denote the set of all the brands of manufacturer , and denote the number of brands of manufacturer , .

Motivated by the reduced-form evidence that winning a WIC contract has spillover effects on the demand of non-WIC consumers, we model the indirect utility of a non-WIC consumer from product in market as follows.

| (3) |

where is an indicator that is a non-auctioned brand of the winning manufacturer , is an indicator that brand is the auctioned brand of , is a vector of observable product characteristics including manufacturer dummy, is the price of product in market , is the unobserved product characteristics, and is the idiosyncratic preference shock. The outside options for consumers are other formulas such as soy-based powder and other physical forms, store-brand infant formulas, e.g., Perrigo, and breastfeeding.

In the specification above, we allow the spillover effects of winning a WIC contract on the auctioned brand () to be different from a non-auctioned brand (). If winning a WIC contract has no spillover effect, then in the utility specified in (3). Based on the reduced-form evidence, we expect that both spillover effects are positive, i.e., and . The random coefficients and may depend on consumers’ demographic variables. For ease of exposition, we denote , , and , respectively, the vector of prices, the vector of product characteristics, and the vector of unobserved product characteristics for all the brands in market .

We further express the random coefficients as

| (4) |

where is a vector of observed individual demographics, the matrix captures how consumer characteristics affect taste, is a vector of unobserved individual characteristics, the matrix captures how consumer characteristics affect tastes, is a standard multivariate normal distribution, and is a known distribution from other data sources.

Each non-WIC consumer chooses a brand of formula or the outside option to maximize her utility. Note that the consumer’s optimal choice depends on the winning manufacturer’s identity because she prefers the brands of the winning manufacturers. We use to represent the market share of brand in market where the winning manufacturer is . Following the existing literature in discrete choice demand estimation, we assume that the taste shocks are i.i.d. draws from a type-one extreme value distribution so that the propensity of each household purchasing brand has a closed-form logit expression, resulting in the following aggregated market share representation.

where the expectation is taken over the distributions of the random coefficients and . We then use to represent the demand of brand in market with being the size of market and the WIC winner being manufacturer .

4.2 Supply

Based on the institutional background and the reduced-form evidence, we model the competition of the three manufacturers in market using a multi-stage game. Before the first stage, the national wholesale price for each manufacturer’s auctioned brand (each manufacturer has only one) is realized and becomes common knowledge among all manufacturers.171717Manufacturers could endogenously choose their auctioned brands. Nevertheless, auctioned brands are the most popular by sales, and they do not vary much across states or over time. Therefore, we assume auctioned brands are exogenously given.

In the first (auction) stage, there is an independent procurement auction in a market where manufacturers compete for the exclusive right to serve the WIC participants. Specifically, each manufacturer submits a rebate for its auctioned brand to maximize its overall expected payoff considering the auction outcome’s uncertainty. Once the rebates are revealed, the exclusive right is awarded to the manufacturer with the lowest net price, calculated as the national wholesale price subtracting the submitted rebate. In the second (pricing) stage, each manufacturer sets retail prices for their products based on the auction winner’s identity.181818There are no auctions in some markets because a typical contract lasts for three years, and during the contract period, manufacturers only decide retail prices.

We make the following two assumptions regarding the national wholesale prices to be consistent with the institutional background. First, the national wholesale price for the auctioned brand is non-binding in the post-auction competition. Even though the winner is determined jointly by the national wholesale price and the rebate, the government’s expenditure, which is the difference between the retail price and rebate, does not depend on the national wholesale price after winning the auction. Second, the national wholesale price does not change in the post-auction period. Note that if the winning manufacturer does adjust its national wholesale price after winning the auction, the agency requires the winner to adjust the rebates by the same amount to keep the net price invariant. This unique feature by the agency discourages the winning manufacturer from raising the national wholesale price.

We now present the supply model backward and characterize its equilibrium.

4.2.1 The pricing stage

In each market, a manufacturer chooses brand-level retail prices to maximize its overall profit upon observing the auction winner’s identity. For simplicity, we suppress the market index . Note that the auction winners’ and losers’ pricing decisions differ, so we model them separately.

Let denote the demand of brand for manufacturer , where is the vector of prices of all the brands in the market, and the superscript indicates the winning manufacturer’s identity. The overall profit of manufacturer from the non-WIC market is

| (6) |

where is the marginal cost of brand , and is the manufacturer’s fixed cost. We allow the non-WIC demand of brand for manufacturer at a given price vector to depend on the winner’s identify .191919This is motivated by the reduced-form evidence that the impacts of winning on sales depend on the winner’s identity. If , the profit function represents the winner’s non-WIC profit.

The pricing competition in the infant formula market is complicated and unprecedented due to several unique features. First, there are two types of consumers, including regular non-WIC consumers and price-insensitive WIC consumers. If the winning manufacturer optimizes its overall profit, the optimal price would be set as high as possible because of the inelastic WIC consumers. Second, the WIC brand’s price is regulated to prevent the winning manufacturer from discriminating against consumers and any retailer from charging much higher prices than its peer retailers.202020 The state agencies impose various restrictions on the pricing ceiling for the WIC products, based on the price of a retailer’s peer group, including both non-WIC and WIC stores. Violating such a pricing ceiling might result in losing the WIC eligibility, so the pricing ceiling is binding. Third, winning may reduce marginal costs for the winner’s products due to the economy of scale, saving in advertisement and transportation, etc.

Facing these challenges, we model the pricing decision in two steps: the first is determining the WIC brand price, and the second is determining the non-WIC brand prices. In the first step (WIC pricing step), the winner determines the initial price for the WIC brand through a perceived profit maximization process where only non-WIC consumers are considered and assuming all other manufacturers choose prices to maximize their profits. This perceived process is essentially a Bertrand price competition.

| (7) |

which generates a perceived equilibrium price for WIC brand, denoted as .

The winner then adjusts the WIC brand’s price to respond to the demand from price-insensitive WIC consumers and comply with governmental regulations. Note that the WIC demand incentivizes the winner to raise the WIC brand price, but governmental regulations restrict it from rising. Because of the implicit regulation, it is unclear how they affect the WIC brand’s price. We combine all these factors and model the winner’s price adjustment in the following reduced-form fashion:

| (8) |

where is the final price of the WIC brand, is the price adjustment, which we refer to as the WIC pricing strategy and varies across manufacturers, i.e., is indicated by the manufacturer indicator .

In the second step (non-WIC brand pricing step), taking the WIC brand price as given, all manufacturers compete to determine their retail prices for their products simultaneously in the traditional Bertrand fashion except the winner, who only solve the optimal price for its non-auctioned brands. The profit optimization for the winning and losing manufacturers can be summarized as follows.

| (9) |

where collects the vector of prices besides the price for the WIC brand. It is worth noting that there is a subtle difference in the winner’s pricing optimization in this step from the standard Bertrand competition. Even though the winner does not adjust the WIC brand’s price when the winner decides the price for her other brands, the winner still considers the negative effect of these prices on the WIC brand’s non-WIC demand and, thus, the overall profit.

Using the following first-order conditions, we can characterize the profit maximization separately for winning and losing manufacturers. A losing manufacturer ’s first-order-condition is

| (10) |

The first-order-condition of the winning manufacturer for its non-WIC brands is:

| (11) | |||||

The equilibrium conditions above are similar to that in the standard Bertrand pricing game framework, except that it does not consist of the optimization for the WIC brand. We can still represent the equilibrium pricing strategies in the following matrix expression:

| (12) |

where and are vectors of prices and marginal costs, respectively with being the total number of brands in the market, including the WIC brand, and is a matrix defined as follows.

| (13) |

In the definition above, because the winning manufacturer does not set the price as in a Bertrand framework, so is excluded. is a vector of market shares of all the brands except the WIC brand.

4.2.2 The auction stage

The procurement auction in which manufacturers compete to serve WIC infants exclusively is non-standard because of the following features. First, the payoff of a losing manufacturer may depend on the winner’s identity due to the asymmetric competition between the three manufacturers, this is called identity-dependent externality. In contrast, the payoff of a losing bidder is usually zero regardless of who wins the auction in a standard auction. Moreover, the expected payoff of a manufacturer participating in the auction is much more complicated than in a standard auction: the payoff from winning depends not just on their costs but also on the opponents’ costs because the cost affects the opponent’s retail prices in the second stage. As a result, we cannot represent the expected payoff as a product of the benefit from winning and the probability of winning. Lastly, the equilibrium strategy is asymmetric because manufacturers have different payoff functions due to consumers’ heterogeneous preferences for brands.

Facing these challenges in modeling the manufacturers’ bidding behavior in the WIC auction, even in theory, it is infeasible to show the existence and the uniqueness of equilibrium. Therefore, we propose to take an alternative route and rely on a flexible reduced-form analysis to approximate the determinant of the rebates from the data directly. The benefit of such an approach is that we do not need to take a stance on how the manufacturers view this complicated auction environment and save us from the risk of mis-specifications. However, the cost of such an approach limits our scope in conducting counterfactual analysis. We can only simulate the model outcomes limited to the situations where the data have some information about those situations. We will be more specific about the limitations in the counterfactual analysis section.

Intuitively, the rebates are affected by both the cost and demand shifters. Considering all the information available to a manufacturer, we use a predictive model to approximate the rebating rule that the manufacturers adopt for determining the rebate. We assume the bidding function is linear in a manufacturer’s wholesale prices and the distance to the production center, demand shifters, including income and the number of WIC infants and non-WIC infants, and cost shifters, including the raw milk prices and the electricity rate. The manufacturer also considers the competition from rivals, so the rivals’ wholesale prices and transportation distances might affect the rebate, too.

Note that there is a spill-over effect from winning the WIC auction to the non-WIC market, captured by the boosted consumer preferences for the winning manufacturer’s products, i.e., and . The manufacturers’ rebate could vary with such a spill-over effect. However, such a spill-over effect results in a heterogeneous spill-over impact in sales, depending on the market characteristics, including the cost and demand shifters. As a result, it is infeasible to quantify the direct consequence of the spill-over effect on the rebate. This infeasibility limits our capability to simulate the retail prices in the scenario varying the spilled-over effect. That is, the specification of the reduced-form regression of the rebate implicitly reveals the impact of the spill-over effect on the rebate. Our counterfactual analysis, therefore, can only be conducted with the assumption that the spill-over effect is the same as in the data.

5 Identification and Estimation

In this section, we first describe the identification and estimation of both the demand and supply sides and then present how we predict the rebate in the auction stage. We focus on identification and estimation on the supply side because of the challenges discussed in the last section, while the demand side is standard following the seminal work BLP.

5.1 Identification

It is worth emphasizing that we allow the manufacturers’ marginal costs to depend on whether they win the WIC auction. Specifically, we model the marginal costs as a linear function of product characteristics and cost savings:

| (14) |

where collects manufacturer and auction brand level fixed effects, product characteristics such as spitup and prebiotics, and cost shifters such as transportation distance, the raw milk price, and the electricity price. is idiosyncratic shock to marginal cost.

The model parameters from the supply side include marginal costs for all the brands in the market , cost reductions of the winning manufacturer for the WIC brand and the non-WIC brands , and the price adjustment coefficient . Identifying parameters on the supply side is challenging and new because our model in Section 4.2.1 differs from a conventional Bertrand pricing competition, where one can recover the marginal cost from the manufacturers’ first-order conditions.

We take multiple steps to recover the parameters. First, considering that the pricing strategies of losing manufacturers are the same as in a Bertrand pricing model, we use the observed prices and demand functions to identify the marginal costs for the losing manufacturers from the following first-order-conditions.

| (15) |

where only the conditions for the losing manufacturers are used.

Second, we establish that the marginal costs of non-WIC brands can be expressed as a linear function of the WIC brand’s marginal cost. Note that it is infeasible to recover the winning manufacturers’ marginal costs from its first-order-conditions because there are marginal costs but equations, because the winner only optimizes for its non-WIC brands but not the WIC one. For ease of exposition, assume that brand 1,…, are non-WIC brands. For the first-order conditions of the winner described in Equation 11, we can represent the marginal cost for each of the non-WIC brands as a linear function of the marginal cost of the WIC brand.

| (16) |

Rewrite the matrix equation above,

| (17) |

where and are vectors and can be calculated directly from the data. Therefore, the marginal costs for the non-WIC brands can be non-parametrically identified and estimated once the marginal cost of the WIC brand is known.

Third, we identify the marginal cost of the WIC brand using the winning manufacturer’s pricing decision. The identification is achieved for any fixed parameter of price adjustment . That is, we show that the marginal costs of all the brands produced by the winning manufacturer can be identified as a function of the parameter . We will discuss how to calibrate . For a given , the (unobserved) perceived optimal price for the WIC brand is

where is observed in the data, indicating that the perceived optimal price for WIC brand considered only WIC demand is known once is given. Note that the perceived optimal price is determined through the following Bentrand pricing optimization:

| (18) |

where and are defined analogously to and , respectively, but the row for the WIC brand was added back, such that is a matrix, and is a vector. Vector consists of all the marginal costs for all products in the market, with losing manufacturers’ marginal costs being known, and winning manufacturer’s marginal costs of non-WIC brands are a linear function of the marginal cost of the WIC brand as specified in equation (17).

If the perceived optimal prices are observed in the data, the first-order equations above construct a system of equations with the WIC brand’s marginal costs being the only unknown. We can solve the equations to obtain the marginal cost of the WIC brand as a function of the parameter . However, one only observes the perceived optimal price for the WIC brand. Intuitively, A vector of the marginal cost will generate a vector of equilibrium price. Therefore, one can use the observed to pin down the unknown . Consequently, all marginal costs for non-WIC brands of the winning manufacturer can be recovered as functions of the parameter , too.

Once we recover all the marginal costs nonparametrically for any given , we can directly identify the cost savings and , which are components of marginal costs for non-WIC and WIC brands of the winning manufacturer, respectively. Intuitively, after controlling for other factors that affect marginal costs, the difference in marginal costs between a market where the manufacturer loses and a market where the manufacturer wins allows us to obtain cost savings. A potential issue of such an approach is that the cost shocks might have different distributions in the case of winning and losing. The manufacturer might be subject to more negative shocks than losing in those winning markets, leading to lower marginal costs and higher winning probabilities. Nevertheless, this is less likely in our case because the manufacturers bid once every three years (it could be longer oftentimes or shorter occasionally between two auctions in a market). At the same time, the post-auction pricing competition takes place on a monthly level. It is unlikely for the manufacturers to predict the cost shocks three years ahead.

Note that the identification of the marginal costs and cost savings is up to the WIC pricing of the winning manufacturer, . We now provide additional information to identify the WIC pricing strategy parameter. First, Such a pricing strategy is proposed to reduced-formally characterize the two special features in our model: perfectly price inelastic WIC demand and governmental regulation; both work in opposite directions and sort of cancel each other out. Failing explicitly to model their roles in pricing decisions, it is infeasible to point identify the parameter without additional information. As discussed in Section 2, data reveal that the three manufacturers bid aggressively to win the exclusive right to serve the WIC consumers. As a rational agent, the manufacturer would not want to bid or even win if the expected profit from losing is higher than from winning. This feature provides additional restrictions on the WIC pricing strategy. We use this intuition to identify a lower bound of the parameter at which a manufacturer is different between winning and losing, i.e., the expected profit of winning is the same as losing. Specifically, the WIC pricing strategy should satisfy the restriction that the winner’s profit is not smaller than that if the manufacturer loses, which provides a set identification of the WIC pricing strategy.

5.2 Estimation

In this section, we present the estimating strategies for the model parameters. First, the demand parameters are estimated using the generalized method of moments (GMM) as in BLP. We then estimate the supply model following the identification procedure closely.

5.2.1 Demand estimation

The estimation is to exploit population moment conditions constructed by the product of the structural error and the instrumental variables. Specifically, Let collect all preference parameters, i.e., , and let represent the mean utility of brand in market , that is,

In the equation above, the price is likely to be affected by the unobserved characteristic . We use instrumental variables to control for the endogeneity following the existing literature. Instruments used include three sets: (1) cost shifters, including raw milk price, electricity price, and the average transportation distance from a manufacturer’s production plant to a market, (2) BLP instruments, including characteristics of rivals’ products in the same market, and (3) Hausman price IVs, i.e., prices of products in other markets.

We construct moment conditions using those instrumental variables. Let be the -th instrumental variable for brand in market , we have . The sample analog of the moment condition from the instrument can be represented as

where is the overall number of brands across markets and time. Stacking all the moment conditions induced by all the instrumental variables and denoting them as vector , the GMM estimator of the parameters is

| (19) |

where is an estimate of the efficient weighting matrix based on parameter estimates obtained from a first-stage estimation with a 2SLS weighting matrix.

5.2.2 Supply estimation

The estimation on the supply side takes several steps. First, we nonparametrically estimate the marginal costs of all the brands for losing manufacturers in any single market using the first-order conditions of their profit optimization problems.

In the second step, for a given pricing adjustment, we nonparametrically estimate the marginal cost of winning manufacturers by using her optimization condition, which involves the optimal pricing for non-WIC brands and the determination of the WIC brand’s price. Specifically, given the marginal cost of the WIC brand, we recover the marginal cost of the non-WIC brand nonparametrically. We then can estimate the WIC brand’s marginal cost by finding such a market-level marginal cost so that the perceived optimal price for the WIC brand is the same as that observed in the data with the pricing adjustment. Once the marginal costs are non-parametrically estimated, we exploit variation of estimated marginal costs across states to estimate the cost parameters, including the cost-saving parameter and .

Lastly, we pin down the manufacturer-specific WIC price adjustment . Note that the WIC pricing parameters are only partially identified, and estimating the identified set via moment inequality is challenging. Fortunately, the profit from winning is monotone with the WIC pricing strategy, given other factors. Therefore, we can estimate the lower bound of manufacturer-specific such that a manufacturer’s profit from winning is the same as that from losing. Instead of searching for all possible values, to ease the computation burden, we allow the WIC pricing strategy for each manufacturer to be chosen from any point in the predetermined set and choose the combination of the set such that the average profit from winning is not lower than that from losing for all three manufacturers.

In particular, for each given set of for all three manufacturers, we first directly compute the WIC winner’s profit in each market using the recovered marginal costs, prices in the data, market shares, and the number of WIC and non-WIC infants. Second, we calculate the expected profit of the winner from losing by assuming an equal probability that each opponent wins, where we solve for the new equilibrium price and market shares for the hypothetical new winner. Note that only the winner benefits from a cost saving and the demand spill-over effect, so we adjust the marginal cost for the losing and winning manufacturers accordingly before we solve for the new equilibrium. We compute the profit under such a hypothetical situation. We have to conduct these exercises for every market.

5.3 Reduced-form Bidding strategies

To estimate the reduced-form bidding (rebate) function, we assume rebates to be a linear function of three categories of variables. The first category is cost shifters, including manufacturer fixed effects, the distance between a manufacturer’s production plant to a market, which captures the transportation cost, raw milk price, and electricity price. The second category is demand shifters such as the length of the contract, the number of WIC and non-WIC infants, and the median state-level income in a market. The third category of variables includes wholesale price and distance of rivals that account for a manufacturer’s strategic response to its rivals in the bidding process. Since each manufacturer has two rivals, we take an average of the variables for two rivals to represent the overall competition in the market.

In the data, we only observe two participating manufacturers in some auctions. MJ and Abbott participate in almost all WIC auctions while Nestlé does so less frequently. Nevertheless, since all three manufacturers have competed in the market for a long time, it is reasonable to assume that all the manufacturers believe that the other two manufacturers will participate in the auction and submit a rebate.

6 Estimation Results

6.1 Demand

We present the estimation results for the main demand specification in Table 5. The estimated means of the distribution of marginal utilities are summarized in the first column. All coefficients except the constant are statistically significant and of the expected sign. The positively significant estimate of the winning dummy variable implies that consumers prefer products of the winning manufacturer, i.e., there are significant spillover effects of winning a WIC contract on all the products of the winner. Moreover, there are additional significant spillover effects on the WIC brand of the winner on top of other brands of the same manufacturer. The estimated coefficients on the manufacturer-level fixed effects demonstrate that consumers prefer products of MJ the most, then of Abbott and Nestlé the least. This is consistent with the observed market shares in the markets.

The next two columns present estimates of preference heterogeneity of the means in the first column. The standard deviation estimates for price and constant are insignificant, implying that marginal utility heterogeneity is not substantial for infant formula consumers. However, the estimates of the interaction between price and demeaned income is significantly positive, suggesting that high-income consumers are less sensitive to price.

We estimate the implied own- and cross-price elasticities of demand among the three manufacturers and between WIC and non-WIC brands for all the markets and present the median elasticities in Table 9. Each entry ,, where indexes row and column, gives the elasticity of brand with respect to a change in the price of brand . The own-price elasticities are negative for all products. The median elasticity across markets and brands is roughly -2.5, smaller than other food products studied in the literature, such as breakfast cereal estimated in Nevo (2000). This relatively low price sensitivity is consistent with the fact that parents are usually reluctant to switch infant formula products even if the price rises. In general, consumers are less elastic for auctioned brands than for non-auctioned brands for all three manufacturers. Consumers’ demand is the least elastic for Abbott’s auctioned brand and most elastic for MJ’s non-auctioned brand.

Moreover, our estimated substitution patterns exhibit significant variation across auction and non-auction brands. Abbott’s auction brand appears to be the most popular substitute for all other products, MJ’s auction brand is the next, and Nestlé’s auction brand is the least popular. The auction brand of MJ is a closer substitute of Abbott’s than Nestlé’s, suggesting that consumers view MJ and Abbott’s products similarly but view Nestlé’s products differently from the other two manufacturers. This finding is consistent with the fact that Nestlé’s price is relatively lower than the other two manufacturers.

6.2 Supply

Using the demand estimates, we estimate the marginal costs of all the products nonparametrically from the first-order conditions of losing and winning manufacturers’ optimization problem for a given WIC pricing strategy and estimate the cost saving and cost functions using those marginal costs. We present the estimation results in Table 7.212121Supply parameters are robust to variation of the WIC price adjustments from 0.01 to 0.2.

The results display a few interesting patterns. First, there is considerable heterogeneity in price adjustment across the three manufacturers. Nestlé increases the WIC brand’s price by 11% by the perceived optimal price without considering WIC demand. In contrast, the increases for Abbott and MJ are 7% and 1%, respectively. This can be due to the fact that Nestlé charges a relatively lower price for its products without a WIC contract. All cost savings are statistically significant at 1%.

Second, there is also massive heterogeneity in the cost savings from winning. MJ’s cost saving for its WIC brand is only slightly larger than its non-WIC brands. Compared with MJ, Nestlé has a lower cost saving for its non-WIC brands, but a higher cost saving on the WIC brand; Abbott has similar cost saving to MJ.

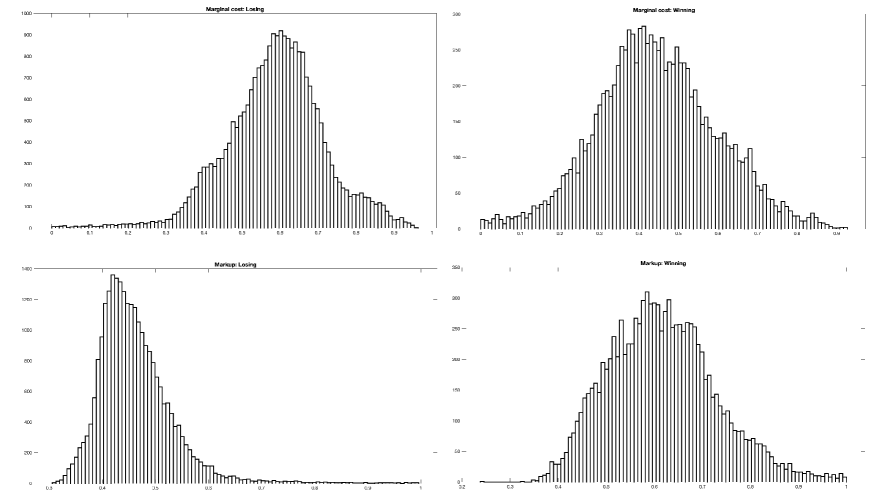

We present the histograms of the estimated marginal costs and markups in Figure 4 and their summary statistics in Table 8 separately when winning and losing WIC auctions. When manufacturers do not have a WIC contract, the mean and median marginal costs of all products across all markets are estimated to be $0.587/ounce and $0.594/ounce, respectively. The markup has a median of 45% and a mean of 46%, with a small standard deviation of 8.5% across all products and all markets. The relatively high markups of informant formula products are due to the considerable market power of the three manufacturers who dominate the market. Because of cost savings due to winning a WIC contract, the marginal cost is lower and the markup is higher upon winning for all three manufacturers.

The histogram in Figure 4 and the estimated results in Table 8 illustrate significant heterogeneity of marginal costs and markups across three manufacturers. The heterogeneity of marginal costs across manufacturers is relatively substantial: MJ’s marginal cost is the highest ($0.636/ounce) on average, and Nestlé is the lowest ($0.569/ounce) with a 10.5% difference. However, the markups of the three manufacturers are more uniform; the highest markup (Abbott) is only 4.4% higher than the lowest markup (Nestlé). The increase in markup due to winning a WIC contract also differs. Abbott’s mean markup rises from 47.8% to 67.0%, a 40.2% increase, while the change is 30.4% for MJ and 31.5% for Nestlé.

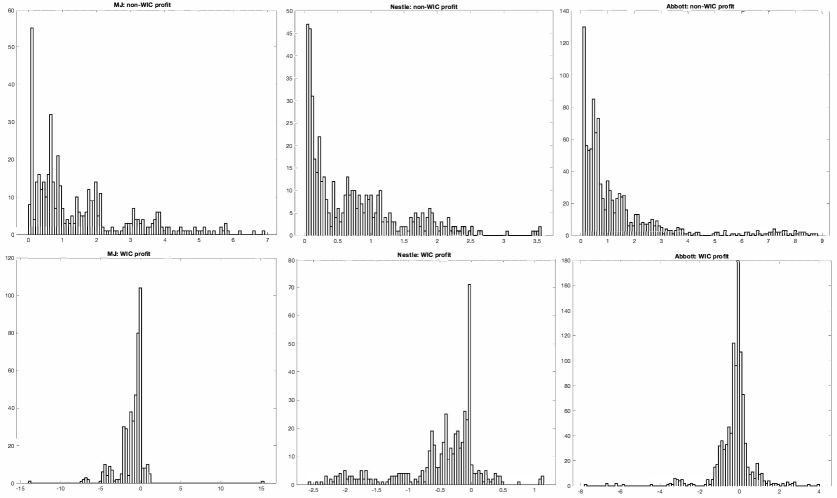

Figure 5 illustrates the distributions of manufacturers’ profits in both the WIC and non-WIC markets. The average profits in a WIC market are -1.044, -0.482, and -0.265 million dollars for MJ, Nestlé, and Abbott, respectively. All three manufacturers have negative profits from more than half of the WIC markets.

Our findings have an interesting implication for the structure of the infant formula market: if a manufacturer decides to participate in a WIC auction in a market, then a sufficient large non-WIC market share is necessary for the manufacturer to survive. Suppose the manufacturer wins in a market, then its profit in the WIC market is negative on average due to the high rebate. The manufacturer has to get a sufficiently large profit from the non-WIC market. On the other hand, if the manufacturer loses the auction, it will also lose a substantial portion of its demand to the winner due to the spillover effects. This indicates that the presence of the exclusive right by auction might affect the manufacturers asymmetrically in the market.

6.3 Reduced-form Bidding functions

We estimate the approximated bidding functions under several specifications and present the estimation results in Table 10. A few interesting patterns arise. First, a manufacturer’s rebate responds positively and statistically significantly to its wholesale price: every percent increase in the wholesale price leads to a 2.1% increase in rebate. This suggests that the higher the wholesale price, the higher the rebate to maintain the profit margin. Moreover, a manufacturer submits a 1.1% lower rebate if its rival’s wholesale price is 1% higher. This negative association is statistically significant for the three more complete specifications (columns (3)-(6)). This effect is the outcome of the manufacturer weighing its winning probability and payoff. The rival would submit a higher rebate if its wholesale price is higher. Therefore, the probability of winning is smaller for a manufacturer. The manufacturer could bid higher to increase the winning probability. However, given a winning probability, the manufacturer would bid lower to make more profit.

The estimates also show that a manufacturer bids a lower rebate in a market with a larger number of WIC infants. This can be rationalized by the fact that the winning manufacturer loses money in the WIC market. Thus the returns from winning are lower. By contrast, the rebate increases in the non-WIC market size. This is mainly due to the substantial spillover effects of winning the WIC contract.

Finally, we also observe that everything else equal, Nestlé’s rebate is 9% higher than MJ, and the difference is statistically significant. Meanwhile, the difference in rebates between Abbott and MJ is not statistically significant. This demonstrates that Nestlé bids more aggressively than its opponents to maintain or increase its market power.

7 Counterfactual Analyses

In this section, we aim to evaluate the effectiveness of government procurement fully. First, what are the impacts of the WIC procurement auction on the government, consumers, and manufacturers? Second, how WIC program size affects the market outcomes, i.e., government expenditure, consumer surplus, and manufacturer profits? Lastly, what would the market outcome be if the government adopts a pre-predetermined rebate approach employed by MDRP? For these purposes, we simulate the outcomes under three common procurement methods: (1) competitive bidding as implemented in the current infant formula market, (2) the government directly reimburses the program participants’ purchases, as in the case of other food products in WIC, and (3) the government sets a predetermined rebate and those manufacturers who choose to participate have to provide the rebate.

7.1 Basic setup

The first issue we need to address in our simulation is that some key market features, including consumers’ spill-over effects for WIC and non-WIC consumers, cost savings from winning the auctions, and the WIC pricing strategy, are estimated using data with the WIC auction. Those features may differ in the alternative mechanisms, so we must make assumptions about those features in our simulations.

When the government reimburses the program participants directly without competitive bidding, we assume that the government still has some requirements on the products provided by WIC and only the current auction brands, which are the most popular products, are available for WIC consumers. Since there is no sole WIC provider anymore, we assume that the WIC manufacturers share the spill-over effect equally. For instance, if all three manufacturers provide WIC products, the spill-over effect becomes 1/3 of the original estimated effect in the competitive bidding mechanism. Under this assumption, non-WIC consumers prefer WIC products to non-WIC ones, but the magnitude becomes 1/3 of that under the competitive bidding mechanism. We make similar assumptions for cost savings. Lastly, because WIC manufacturers are still facing two market segments, one being price inelastic, we assume that manufacturers adopt the same pricing strategy as that with auctions. That is, all WIC manufacturers solve for the optimal prices for their WIC products considering only the non-WIC profits. The manufacturers then determine their WIC products’ prices using their WIC pricing strategies. Given the WIC product prices, they then optimize their prices for non-WIC products. Analogously, we also make the same assumptions above in the pre-determined rebates mechanism.

Another challenge to our simulation study is the lack of information about WIC consumers’ preferences. To address this issue, we assume that WIC consumers have the same preference as non-WIC consumers over infant formulas. Under such an assumption, WIC consumers would choose the brand that maximizes their indirect utility, but the coefficient of the price in their indirect utility is set to zero.

To simulate the market outcome, we use the information of all the markets in 2015 from the data (there are 502 markets in total). A market’s exogenous features include demand and supply shifters, for instance, the number of WIC and non-WIC infants, demographics in the state, the manufacturers’ cost shifters, wholesale prices, etc.

7.2 Procurement mechanisms

In this subsection, we provide details on the three procurement methods and how we solve for equilibrium for each method.

7.2.1 Competitive bidding