Rectangularity and duality of distributionally robust Markov Decision Processes

The main goal of this paper is to discuss several approaches to formulation of distributionally robust counterparts of Markov Decision Processes, where the transition kernels are not specified exactly but rather are assumed to be elements of the corresponding ambiguity sets. The intent is to clarify some connections between the game and static formulations of distributionally robust MDPs, and delineate the role of rectangularity associated with ambiguity sets in determining these connections.

Keywords: Markov Decision Process, distributional robustness, game formulation, strong duality, risk measures

1 Introduction

Consider (finite horizon) Markov Decision Process (MDP)

| (1.1) |

Here be the state space, is the action set and is the cost function, at stage . For the sake of simplicity, in order to concentrate on the main issues discussed in this paper, we assume that the sets and are finite. Unless stated otherwise the optimization in (1.1) is performed over randomized Markovian policies , , where is the cardinality of the set and denotes the -dimensional simplex. We also allow the action set to depend on , . We assume that the set is nonempty for every and that is a fixed state. It is also possible to consider random following a given distribution without changing the essence of our ensuing discussions. We denote the set of randomized Markovian policies as . For a policy the expectation is taken with respect to the probability law defined by the transition kernels . Since both the state and action spaces are finite, we can view a kernel as a finite dimensional vector with components , , , . In particular, specifies the probability distribution of conditioned on the current state-action pair .

The main goal of this paper is to discuss several approaches to the formulation of distributionally robust counterparts of the MDP (1.1), where the transition kernels are not specified exactly but rather are assumed to be elements of the corresponding ambiguity sets. Existing literature largely focuses on the so-called static formulation111What is called in this article the static formulation, in some publications is referred to as robust MDPs, e.g., [7, 9, 18]., where the objective in (1.1) is replaced by the worst-case scenario when the transition kernel defining the expectation is subject to variations. The tractability of the static formulation in turn hinges upon the existence of certain robust version of dynamic equations. To certify such dynamic equations, structural conditions on the ambiguity sets, termed rectangularity, have been identified in prior studies [6, 5, 7, 9, 15, 17]. Note that establishing dynamic equations with different classes of ambiguity sets oftentimes follows a case-by-case analysis.

In some prior work (e.g., [7, 9]), a game formulation is identified for a certain class of rectangular ambiguity set, where a term-based zero-sum game with perfect information is formulated and shown to be equivalent to the static formulation. Nevertheless, game formulation of distributionally robust MDP has received limited attention in existing studies. In addition, the aforementioned term-based zero-sum game is asymmetric as the information of different players is different. Formulating such a game is also limited to certain rectangular ambiguity sets. In a nutshell, considering such a game formulation seems to offer no clear advantage over the static formulation as they both require case-by-case treatment.

In this manuscript we consider a natural game formulation of distributionally robust MDP. We show that this game formulation is simpler, more powerful, and serves as a unifying venue to study different ambiguity sets for both game and static formulations.

This paper is organized as follow. In Section 2, we introduce the game formulation and its dual, and establish their dynamic equations through an elementary argument. From dynamic equations we naturally investigate the strong duality of the game formulation. We propose two structural assumptions on the ambiguity sets that serve as sufficient conditions of the strong duality, and discuss their implications in determining the existence of non-randomized optimal policies. Through simple verification, we show that these structural assumptions encompass all mainstream rectangularity conditions of ambiguity sets. We also discuss history-dependent policies in Subsection 2.2.

In Section 3, we show that the dynamic equations of the game formulation provide a useful instrument to establish equivalence between the game and static formulations. In particular, the aforementioned structural assumptions are sufficient to certify such an equivalence. As immediate consequences of this equivalence: (i) the dynamic equations naturally carry to the static formulations without any additional analytical overhead; (ii) the strong duality of the static formulation is also established. Notably, this allows one to consider static formulations with different ambiguity sets with a unifying treatment.

In Section 4, we show that all the aforementioned results hold similarly for cost-robust MDP, where cost functions, instead of the transition kernels, are subject to ambiguity. Importantly, the discussion follows exactly the same argument as for the distributionally robust MDP. As a byproduct, a cost-robust MDP can be reduced to a regular (i.e., non-robust) MDP with a convex policy-dependent cost function.

In Section 5, we consider risk-averse setting, where we discuss a natural construction of ambiguity sets based on law invariant coherent risk measures. Finally, in Section 6, we point out to an essential difference between distributionally robust formulations in the MDP and Optimal Control frameworks.

Note that since the set is finite, a probability distribution supported on can be identified with probability vector . By we denote Dirac measure of mass one at point . Let us recall the following properties of the min-max problem:

| (1.2) |

where and are nonempty sets and is a real valued function. A point is a saddle point of problem (1.2) if and If the saddle point exists, then problem (1.2) has the same optimal value as its dual

| (1.3) |

and is an optimal solution of problem (1.2) and is an optimal solution of problem (1.3). Conversely, if the optimal values of problems (1.2) and (1.3) are the same, and is an optimal solution of problem (1.2) and is an optimal solution of problem (1.3), then is a saddle point. If and are convex subsets of finite dimensional vector spaces, is continuous, convex in and concave in , and at least one of the sets or is compact, then the optimal values of problems (1.2) and (1.3) are equal to each other. This is a particular case of Sion’s minimax theorem [14].

2 Distributionally robust MDP

Assume that for , there is a set of transition kernels . At this point we do not specify a particular construction of the ambiguity sets . Unless stated otherwise we make the following assumption: the sets , are closed. Since the probabilities , the sets , , are bounded and hence are compact.

2.1 Game formulation of distributionally robust MDP

The game formulation of distributionally robust MDP considers a dynamic game between the decision maker (the controller) and the adversary (the nature). The nature can choose a kernel for each , , and this defines a policy of the nature (cf., [8, 13]). Consider the decision process determined by the decision history , where , , . The controller chooses a randomized policy of the form , , where . Subsequently the nature chooses its policy , . It is said that a policy is non-randomized if for every , , the corresponding probability distribution is supported on a single point of (i.e., is the delta function).

Policies and , of the controller and nature, define the respective probability distribution on the set of the histories of the decision process (Ionescu Tulcea theorem). The corresponding expectation is denoted . It is said that a policy of the controller is Markovian if , , does not depend on the history . Similarly a policy of the nature is Markovian if is a function of alone. Unless stated otherwise we deal with Markovian policies of the controller and the nature222History-dependent policies are discussed in Section 2.2., and denote by the set of (randomized) Markovian policies of the controller and by the set of Markovian policies of the nature. The corresponding problem of the game formulation is

| (2.1) |

We refer to (2.1) as the primal problem of the game formulation.

It is well known that in the case of the MDP problem (1.1), the optimal policies are Markovian. We will discuss in Section 2.2 the issue of non-Markovian optimal policies in the distributionally robust setting.

Given a policy of the controller, the nature chooses a policy so as to maximize the total expected cost, i.e.,

| (2.2) |

-

By writing we mean that the transition kernel is viewed as an element of the ambiguity set . Throughout the rest of our discussion, a particular choice of (for instance, the optimal solution of (2.3) below) can depend on the state , i.e., can be different for different values of . We will say explicitly that is independent of when the considered element of the ambiguity set is the same for all . Of course the transition probability depends on .

Proposition 2.1.

Given a policy of the controller, problem (2.2) admits the following dynamic programming equations: and for and ,

| (2.3) |

where equals the optimal value of problem

| (2.4) |

Proof.

Solving (2.2) is equivalent to solving a regular MDP of the nature defined as follows. At stage , the state space is given by ; the possible actions at are given by ; the cost function of the nature is given by ; and the transition probability is given by

| (2.5) |

Note that the action space of nature’s MDP is compact. Applying standard dynamic equations (cf., Theorem 4.3.2, [11]) of regular MDPs yields (2.3). ∎

We also have that for a policy , the corresponding optimal policy of the nature is determined by dynamic equations

| (2.6) |

The maximum of (2.2) is then minimized over and we can write the following dynamic programming equations for the primal problem (2.1).

Proposition 2.2.

The dynamic programming equations for the primal problem (2.1) are: and for and ,

| (2.7) |

where equals the optimal value of

| (2.8) |

Proof.

Let us consider the (Markovian) policies

| (2.9) |

, determined by the dynamic programming equations (2.7). Since is compact, the minimization problem in the right hand side of (2.9) always has an optimal solution . In view of Proposition 2.2, the corresponding policy is an optimal solution (optimal policy of the controller) of the primal problem (2.1). The non-randomized policies of the controller are determined by the counterpart of (2.9) with being the Dirac measure, that is

| (2.10) |

The dual of the min-max problem in the right hand side of (2.7) is obtained by the interchange of the min and max operations. That is, given a policy of the nature, the corresponding dynamic programming equations for the controller are: and for ,

| (2.11) |

Consequently the dynamic programming equations for the dual problem are: and for ,

| (2.12) |

The dynamic equation (2.12) define the dual of the primal problem (2.1). That is, starting with and going backward in time, eventually gives the optimal value of the dual problem. The optimal solutions , , in the right hand side of (2.12) determine an optimal (Markovian) policy of the nature in the dual problem. Since the sets are assumed to be closed and hence compact, the maximum in (2.12) is attained.

We write the dual problem as

| (2.13) |

In the dual setting the nature first chooses its policy . Then the controller finds the corresponding optimal (Markovian) policy to minimize the total expected cost, i.e.,

| (2.14) |

In the dual framework the decision process is determined by the history , .

By the standard theory of min-max problems we have that the optimal value of the dual problem (2.13) is less than or equal to the optimal value of the primal problem (2.1), that is

| (2.15) |

We address now the question when actually the equality in (2.15) holds, i.e., there is no duality gap between the primal and dual problems. In particular, the following remark illustrates our essential strategy.

Remark 2.1.

For we have that . Going backward in time suppose that and consider the dynamic programming equations (2.7) and (2.12) for the stage . For the function in the right hand side of (2.7) can be considered as a function of two variables and . Then we can talk about the concept of saddle point for the min-max problem (2.7) and its max-min dual problem (2.12). Again, from weak duality we have

| (2.16) |

If the saddle point exists for (2.7), then based on (2.12) and our induction hypothesis that , we have the equality in (2.16). Therefore if we can ensure existence of the saddle point for all and , then going backward in time eventually , and hence the optimal values of the primal problem (2.1) and its dual (2.13) are equal to each other, i.e. the strong duality holds.

Going forward we introduce conditions (Assumptions 2.1 and 2.2) that certify the existence of saddle point for the min-max problem (2.7). These conditions define a specific structure of the ambiguity sets.

Assumption 2.1.

-

(a)

For every there is a kernel , potentially depending on , with

(2.17) for any .

-

(b)

There is a kernel such that condition (2.17) holds for all and any .

Since the set is assumed to be closed and hence compact, the maximizer in the right hand side of (2.17) always exists. In condition (a) of the above assumption, the kernel can be different for different values of the state , while in condition (b) it is assumed to be the same (independent of ). Clearly, condition (b) in the above assumption is stronger. It can also be noted that condition (b) is equivalent to the following: there is a kernel such that

| (2.18) |

Similar remark can be made for condition (a).

Suppose that Assumption 2.1(a) holds and consider

| (2.19) |

It follows directly from (2.17) and (2.19) that is a saddle point of the min-max problem (2.7). Consequently we have the following result.

Theorem 2.1.

A sufficient condition ensuring Assumption 2.1(b) is the so-called -rectangularity of the ambiguous sets of kernels.

Definition 2.1 (-rectangularity, [7, 9]).

Define

| (2.20) |

The ambiguity set is said to be -rectangular if for every ,

| (2.21) |

If is independent of , then the -rectangularity means that can be represented as the direct product of , , .

Proposition 2.3.

Proof.

For and consider the optimization problem

| (2.22) |

Since and hence is compact, it follows that for any and problem (2.22) has an optimal solution . Let . By the -rectangularity of we have that , and moreover condition (2.18) holds for any , and hence Assumption 2.1(b) follows. This completes the proof. ∎

Remark 2.2.

Under the assumption of -rectangularity, dynamic equations of a form similar to (2.7) have been established in [7, 9]. Nevertheless, it is important to note that the dynamic equations established there are for the static formulation, which we will discuss in detail in Section 3. In comparison, Proposition 2.3 is established for the game formulation.

The -rectangularity is not a necessary condition for Assumption 2.1(b). Indeed, the following simple two-stage problem () gives an example where the ambiguity set is not -rectangular while Assumption 2.1(b) still holds.

Example 2.1.

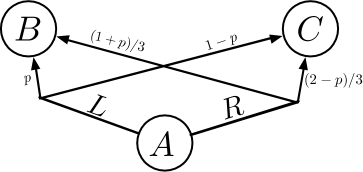

Consider a two-stage problem with three states . Suppose , and there are two actions and at state , i.e. . In addition, the cost functions are given by , and and for some constants . In the considered setting, for the corresponding transition kernel we only need to specify the probability of moving to the state conditional on action , and the probability conditional on action , since and . Let us consider the ambiguity set at stage defined as

| (2.23) |

(see Figure 1). The corresponding set , defined in (2.20), is determined by a kernel from the ambiguity set . It follows then by (2.21) that the ambiguity set is not -rectangular.

On the other hand, since and is bigger than , we have that kernel from the set for , i.e., defined as

satisfies the condition of Assumption 2.1(b).

The above example falls into a broader class of ambiguity set defined below.

Definition 2.2 (-rectangularity, [6, 5]).

The ambiguity set is said to be -rectangular if there exist sets , and for every and , one can choose nonnegative numbers such that every can be represented as probability vector of the form

| (2.24) |

for some , .

Remark 2.3.

The above definition of -rectangularity is slightly weaker than the one considered in [5, 6]. Indeed, -rectangularity in [6, 5] requires additionally that and that . This additional condition is sufficient for to be a probability vector, although is not necessary. Indeed, the ambiguity set of Example 2.1 (defined in equation (2.23)) satisfies -rectangularity by taking and , , , , , , , , , with , and .

It can be seen that by taking , with proper specification of the coefficients and sets , every -rectangular set can be represented as an -rectangular set. We proceed to verify Assumption 2.1(b) if the costs do not depend on the next state .

Proposition 2.4.

Proof.

For -rectangular sets the maximization problem in (2.17) is equivalent to

where we denote by the -dimensional vector with components , , and is the scalar product of vectors .

We now proceed to introduce the second condition that requires the convexity of state-wise marginalization of the ambiguity set . As will be shown shortly, such a condition can be used to certify strong duality in the absence of Assumption 2.1.

Assumption 2.2.

The state-wise marginalization of , defined as

| (2.26) |

is convex.

It can be noted that the above assumption holds if the set is convex.

Theorem 2.2.

Suppose Assumption 2.2 is fulfilled. Then the following holds.

- (i)

- (ii)

Proof.

Clearly, (2.7) is equivalent to the following optimization problem

| (2.27) |

The objective function of problem (2.27) is linear with respect to and linear with respect to , and both sets and are convex and the set is compact. Therefore the strong duality follows by Sion’s theorem. Moreover the primal and dual problems posses optimal solutions and hence there exists the corresponding saddle point. This completes the proof of (i).

Now let us observe that the minimum in the max-min problem (2.12) is always attained at Dirac measure, and hence we can write

| (2.28) |

Suppose that (2.10) has a saddle point . Then is a saddle point of (2.28), and hence is a non-randomized optimal policy of the controller. Conversely suppose that the primal problem has a non-randomized policy. By (i) we have that there is no duality gap between the primal and dual problems. Therefore there is saddle point with being Dirac measure. This completes the proof of (ii). ∎

We next introduce an example demonstrating the essential role of convexity in Assumption 2.2.

Example 2.2.

Consider the same MDP as defined in Example 2.1, except that we have

Direct computation shows

| (2.29) |

and hence .

As Example 2.2 shows, without the convexity in Assumption 2.2 , the weak duality (2.15) can be strict. On the other hand, with Assumption 2.2, Theorem 2.2 allows us to certify strong duality when Assumption 2.1 does not hold. It should be noted that in this case the optimal policies of the controller can be all randomized. This should be contrasted with conclusion (iii) of Theorem 2.1, which always certifies the existence of non-randomized optimal policies. The next example illustrates this aforementioned observation.

Example 2.3.

Consider the same MDP as defined in Example 2.2, except that in the definition of we let . Direct computation shows that when , the unique solution of (2.17) is given by and . In comparison, when , the unique solution of (2.17) is given by and . Consequently Assumption 2.1(a) does not hold. Nevertheless, is convex and closed, and hence Theorem 2.2 applies and strong duality holds. Finally, it can be readily verified that the optimal policy of (2.1) is unique and is given by

Note that the policy is randomized.

Remark 2.4 (Nature’s Randomized Policies).

It is also possible to consider randomized policies of the nature when the kernel is chosen at random according to a probability distribution supported on the ambiguity set . Then the counterpart of dynamic equations (2.7) can be written as

| (2.30) |

where is the set of probability distributions on equipped with its Borel sigma algebra. By Sion’s theorem the min-max problem (2.30) has a saddle point (note that here the existence of saddle point does not require the convexity of ). By arguments similar to the proof of part (ii) of Theorem 2.2, we have here that the nature possesses a non-randomized policy iff the min-max problem (2.7) has a saddle point for all and .

2.2 History-dependent policies

In this section we discuss history-dependent policies of the controller and/or the nature. We denote by and the sets of history-dependent policies of the controller and the nature, respectively, and consider the counterparts of the primal problem (2.1) and its dual (2.13) when and are replaced by their history-dependent counterparts and .

Proposition 2.5.

The following holds. (i) Suppose the controller is Markovian and the nature is history-dependent, i.e., consider the problem

| (2.31) |

(ii) Suppose both the controller and the nature are history-dependent, i.e., consider the problem

| (2.32) |

Then for any , we have , and for ,

| (2.33) |

where is equal to the optimal value of problem

| (2.34) |

Moreover, defined in (2.7), is equal to the optimal value of

| (2.35) |

Proof.

For claim (i), note that the argument of Proposition 2.1 holds even if the nature uses history-dependent policies, since optimizing over Markovian policies is the same as optimizing over history-dependent policies for regular MDPs. Consequently Proposition 2.2 also holds.

We proceed to establish claim (ii). Let us first consider (2.34). Fixing any , it is immediate that ,

| (2.36) |

defines such that

Here in (2.36) is specified by nature’s policy , i.e., . We now show by induction that for . The claim is obvious at . In addition,

from which we complete the induction step. Here follows from the induction hypothesis, and follows from (2.36).

Now let be the history-dependent policy of the nature that attains the maximum in (2.33), then from (2.36) it holds that . Consequently, we obtain and (2.34).

With (2.33) in place, one can follow essentially the same lines as in the proof of Proposition 2.2 and readily obtain that dynamic equations ,

| (2.37) |

define , which equals the optimal value of (2.35). To conclude our proof for claim (ii), it suffices to show that only depends on and does not depend on . We now show this by induction. Clearly, this holds trivially at . Suppose the claim holds at stage , then from (2.37) we obtain

from which it is clear that only depends on but not . From this we complete the induction step and the proof for claim (ii) is completed. ∎

In [16, section 5] are presented examples when the controller is allowed history-dependent policies while the nature is Markovian, which are not amendable to writing dynamic programming equations similar to (2.7). We show now that the respective dynamic equations still hold provided there is no duality gap between the primal problem (2.1) and its dual (2.13).

Proposition 2.6.

Proof.

Let us denote . Then the following is immediate:

where follows from the fact that is a regular MDP of the controller as the nature is Markovian, subsequently for the controller minimizing over Markovian policies is equivalent to minimizing over history-dependent policies. If holds, then clearly all the above inequalities indeed hold with equality, from which we conclude the proof. ∎

3 Static formulation of distributionally robust MDP

Let us consider the following static formulation of distributionally robust MDP,

| (3.1) |

As it was also mentioned in Remark 2.2, in some publications the static formulation is referred to as robust MDPs. The essential difference between (3.1) and the game formulation (2.1) is that in (3.1) the nature chooses the kernels prior to the realization of the Markov process. The dual of (3.1) is

| (3.2) |

Formulations (3.1) and (3.2) can be viewed as the static counterparts of the respective problems (2.1) and (2.13).

Below we first discuss when the static formulation (for both primal and dual problems) is equivalent to the game formulation discussed in Section 2.1.

Theorem 3.1.

The following holds. (i) If for any policy , there exists a solution of (2.3) that is independent of , for every and , then the primal problem (2.1) of the game and its static counterpart (3.1) are equivalent, i.e.,

| (3.3) |

and the dynamic equations (2.7) hold for the static problem (3.1) as well.

(ii) If for problem (2.12) (not necessarily having a saddle point), there exits a solution such that is independent of , for every and , then the dual problem (2.13) of the game and its static counterpart (3.2) are equivalent, i.e.,

| (3.4) |

and the dynamic equations (2.12) hold for the static problem (3.2) as well.

Proof.

For the claim (i), given the specified condition, it can be readily seen that for any ,

| (3.5) |

On the other hand, it holds trivially that the first term in (3.5) is at least that of the last term in the above relation, which implies that the above inequality holds with equality. Since this holds for any , the claim (i) follows.

For the claim (ii), from the specified condition we have that for the dual problem (2.13), the optimal policy is given by , and consequently

Combining the above relation with yields the claim (ii). ∎

Clearly, the conditions in Theorem 3.1 hold for - and -rectangular sets discussed in Section 2.1. Below we introduce another class of commonly used ambiguity sets for the static formulation that trivially satisfies these conditions (the verification uses a similar argument as in Proposition 2.3).

Theorem 3.1 allows one to immediately obtain the dynamic equations of the static formulation for the ambiguity sets commonly used for the static formulation.

Corollary 3.1.

Remark 3.1.

At this point it might be worth mentioning that prior studies of the static formulation for each of the ambiguity sets adopt a case-by-case analysis in establishing the corresponding dynamic equations (cf., [17, 6, 7, 9]). The formulation equivalence we consider and establish here has not been discussed in the prior literature. In particular, this formulation equivalence allows one to provide a unified treatment for different ambiguity sets with rather simple arguments.

As the last result in this section, we are ready to discuss the duality of the static formulation.

Theorem 3.2.

Suppose for every and , a saddle point exists for (2.7), and does not depend on , then

| (3.6) |

That is, the static formulation (for both primal and dual problems) is equivalent to the game formulation, and the strong duality holds for the static formulation.

Proof.

Corollary 3.2.

Proof.

In view of Theorem 3.2 it suffices to verify that a saddle point exists for (2.7) and does not depend on . This trivially holds for ambiguity sets satisfying Assumption 2.1(b), and in particular, for - and -rectangular sets. On the other hand, for -rectangular sets satisfying Assumption 2.2, the existence of saddle point for (2.7) follows from Theorem 2.2. The fact that can be chosen independent of follows trivially using the similar argument in Proposition 2.3 and the definition of -rectangularity. ∎

Remark 3.2.

Similar to Remark 3.1, the strong duality of the static formulation involving - and -rectangular sets has been discussed in [9] and [6] respectively, following a case-by-case analysis. Here our argument differs by first discussing the strong duality of the game formulation and then using the equivalence of the game and static formulations. Both steps are conceptually simple and provides a unifying treatment of different ambiguity sets. In particular, the strong duality discussion of s-rectangular sets for the static formulation seems to be new.

It is worth noting here that for -rectangular sets, the strong duality of the static formulation hinges upon the convexity of . Indeed, it can be readily verified that Example 2.2 considers an -rectangular ambiguity set with non-convex . Consequently we have

where the equalities follows from Corollary 3.1, and the strict inequality follows from Example 2.2. The essential role of convexity in the strong duality of static formulations involving -rectangular sets has not been discussed in [17].

4 Cost-robust MDP

Our discussion so far has focused on ambiguity of the transition kernels. In this section, we show that by following the same lines of argument, one can naturally consider ambiguity on the cost functions. Specifically, we assume in this section that the transition kernels are given (fixed), and there exists a set , , of cost functions. For simplicity we assume that there is no cost ambiguity at . It is worth noting that since each is of the same dimension as the , we can define -, - and -rectangularity for in exactly the same manner as in Sections 2 and 3.

4.1 Game formulation of cost-robust MDP

We define the game formulation of cost-robust MDP similarly as in Section 2. In this case, a (Markovian) policy of the nature maps from into . As before we denote by and the sets of Markovian policies of the controller and the nature, respectively. The corresponding primal problem of the game formulation is

| (4.1) |

Given a policy of the controller, the nature chooses a policy so as to maximize the total expected cost, i.e.,

| (4.2) |

Proposition 4.1.

Given a policy of the controller, problem (4.2) admits the following dynamic programming equations: and for ,

| (4.3) |

where corresponds to the optimal value of problem

Furthermore, it holds that

| (4.4) |

where

| (4.5) |

It can be noted that function , defined in (4.5), is given by the maximum of linear in functions, and hence is convex and positively homogeneous for any .

Proposition 4.2.

The dynamic programming equations for the primal problem (4.1) are: and for ,

| (4.6) |

where corresponds to the optimal value of

Furthermore, it holds that

| (4.7) |

It follows from (4.7) in Proposition 4.2 that the game formulation of cost-robust MDP can be reduced to a regular (i.e., non-robust) MDP with convex policy-dependent cost functions, provided the function is real valued for every .

Theorem 4.1.

The game formulation (4.1) of cost-robust MDP is equivalent to a regular (i.e., non-robust) MDP with the same state and action spaces and transition kernels. For a given policy , the cost of the regular MDP at state is given by .

The dual of problem (4.1) is defined as

| (4.8) |

The dynamic programming equations for the dual problem are: and for ,

| (4.9) |

Similar to Section 2, we now introduce sufficient conditions that certify the strong duality of the game formulation for cost-robust MDP.

Assumption 4.1.

-

(a)

For every there is a cost function , potentially depending on , with

(4.10) for any .

-

(b)

There is a cost function such that condition (4.10) holds for all and any .

Suppose that Assumption 4.1(a) holds and consider

| (4.11) |

It follows directly from (4.10) and (4.11) that is a saddle point of the min-max problem (4.6). Consequently we have the following result.

Theorem 4.2.

An immediate application of Theorem 4.2 yields the following propositions.

Proposition 4.3.

Proposition 4.4.

The following condition can be viewed as the counterpart of Assumption 2.2 for the cost functions.

Assumption 4.2.

The state-wise marginalization of , defined as

| (4.12) |

is convex.

Clearly, Assumption 4.2 holds if the set is convex. The next result then follows from the same argument as in Theorem 2.2.

4.2 Static formulation of cost-robust MDP

Let us consider the following static formulation of cost-robust MDP,

| (4.13) |

The corresponding dual problem is given by

| (4.14) |

Formulations (4.13) and (4.14) can be viewed as the static counterparts of the respective problems (4.1) and (4.8).

With the same argument as in Theorem 3.1, one can establish the following equivalence of game and static formulations for cost-robust MDP.

Theorem 4.4.

The following holds. (i) If for any policy , there exists a solution of (4.3) that is independent of , for every and , then the primal problem (4.1) of the game and its static counterpart (4.13) are equivalent, i.e.,

| (4.15) |

and the dynamic equations (4.6) hold for the static problem (4.13) as well.

(ii) If for problem (4.9) (not necessarily having a saddle point), there exits a solution such that is independent of , for every and , then the dual problem (4.8) of the game and its static counterpart (4.14) are equivalent, i.e.,

| (4.16) |

and the dynamic equations (4.9) hold for the static problem (4.14) as well.

Corollary 4.1.

For the -, - and -rectangular sets, the game formulation is equivalent to the static formulation for cost-robust MDP. In particular, (4.6) provides the dynamic equations of the primal problem (4.13) of the static formulation, and (4.9) provides the dynamic equations of the dual problem (4.14) of the static formulation.

We now conclude this section by discussing the duality of the static formulation. As before, the following result follows from the same lines as that of Section 2 (i.e., Theorem 3.2).

Theorem 4.5.

Suppose for every and , a saddle point exists for (4.6), and does not depend on , then

| (4.17) |

That is, the static formulation (for both primal and dual problems) is equivalent to the game formulation, and the strong duality holds for the static formulation.

5 Risk averse setting

In this section we discuss a risk averse formulation of MDPs and its relation to the distributionally robust approach. Consider a finite set equipped with sigma algebra of all subsets of . Let be the space of functions . Note that can be identified with -dimensional vector with components , , and hence can be identified with . Let be a convex functional. Suppose that is monotone, i.e. if , then ; positively homogeneous, i.e. for any and ; and such that for any and . The functional can be viewed as a coherent risk measure defined on the space of (measurable) functions (cf., [1]). We can refer to [4, 12] for a thorough discussion of coherent risk measures defined on general probability spaces.

It is said that is law invariant with respect to a probability measure , defined on , if can be considered as a function of the cumulative distribution function (e.g., [12, Section 6.3.3]). Law invariant coherent risk measure has the following dual representation, in the distributionally robust form,

| (5.1) |

where is a set of probability measures (probability vectors), depending on , such that every is absolutely continuous with respect to . Note that in the considered setting of finite , measure is absolutely continuous with respect to iff implies that . Of course if all probabilities are positive, any probability measure is absolutely continuous with respect to .

Let be a specified (reference) transition kernel. Considering as a probability measure on , we can consider the corresponding law invariant coherent risk measure depending on and . This suggests the following counterpart of dynamic equations (2.7):

| (5.2) |

From the dual representation of , the dynamic equation (5.2) can be written in the form of (2.7):

| (5.3) |

where

| (5.4) |

It follows directly from Definition 2.1 that the ambiguity sets are -rectangular. Consequently by Theorem 3.1 we have that the corresponding problem of the form (2.1) is equivalent to its static counterpart (3.1) with the respective ambiguity sets of the form (5.4) and dynamic equations (5.2). Also we have by Theorem 2.1(iii) that it suffices here to consider non-randomized policies , .

Let , , be a non-randomized policy, and consider the scenario tree formed by scenarios (sample paths) of moving from state to state , . The corresponding probability distribution on this scenario tree is determined by the conditional probabilities . In turn this defines the nested functional associated with the coherent risk measure and the (non-randomized) policy . That is, at time period the conditional risk functional is determined by the considered risk measure and the reference distribution . Then is defined as the composition of these conditional functionals (cf., [12, Section 6.5.1, equations (6.225) and (6.227)]). Consequently the risk averse (distributionally robust) problem can be written as

| (5.5) |

where consists of non-randomized Markovian policies. Of course if (the corresponding set is the singleton), then (5.5) becomes the risk neutral problem (1.1). As it was pointed above, in the considered setting the nested formulation (5.5) is equivalent to the static formulation (3.1) with the ambiguity sets of the form (5.4).

Remark 5.1.

Note that the probability structure on the scenario tree determined by the conditional distributions is Markovian, i.e., the probability does not depend on the history . Therefore if in the nested formulation (5.5) the policies are allowed to be history-dependent, problem (5.5) still possesses a Markovian optimal policy (compare with Proposition 2.5(ii)).

An important example of law invariant coherent risk measure is the Average Value-at-Risk (also called Conditional Value-at-Risk, Expected Shortfall, Expected Tail Loss):

The has dual representation (5.1) with

and hence

| (5.6) |

This leads to the respective dynamic programming equations of the form (5.3) (cf., [3]).

6 Optimal control model

The MDP setting can be compared with the Stochastic Optimal Control (SOC) (discrete time, finite horizon) model (e.g., [2]):

| (6.1) |

Here , is a sequence of independently distributed random vectors, the state spaces and control (action) spaces are finite, the support of distribution of is finite, and is a set of randomized policies determined by the state equations

| (6.2) |

We assume that the distribution of does not depend on our actions, . Also for the sake of simplicity assume that for all the action spaces do not depend on , and that the following feasibility condition holds

The SOC setting can be formulated in the MDP framework by defining the distribution of transition kernel as

| (6.3) |

where is the probability measure of , .

The distributionally robust counterpart of (6.1) is obtained by considering a set of probability measures (distributions) of , supported on , . That is, the ambiguity set of probability distributions of consists of , with , . This defines the corresponding ambiguity sets of the respective MDP formulation by considering sets of transition kernels determined by equation (6.3) for . The corresponding dynamic programming equations take the form: , and for

| (6.4) |

Without loss of generality we can make the following assumption.

Assumption 6.1.

The sets , , are convex and closed.

The dual of the min-max problem (6.4) is

| (6.5) |

By Sion’s theorem problems (6.4) and (6.5) have the same optimal value and possess saddle point . Note that the minimum in (6.5) is attained at a single point of , i.e., problem (6.5) can be written as

| (6.6) |

Therefore we have the following condition for existence of non-randomized policies of the distributionally robust SOC problem associated with the dynamic equations (6.4).

Proposition 6.1.

The distributionally robust SOC problem possesses a non-randomized optimal policy iff for every , and the min-max problem (6.6) has a saddle point .

For the non-randomized policies the dynamic equations (6.4) become , and for

| (6.7) |

Because of the assumption that the distribution of the process , does not depend on the decisions, the set of policies can be viewed as functions of the data process, , with initial value . Then for a given (non-randomized) policy , the expectation in (6.1) is taken with respect to the probability distribution of . The dynamic equations (6.7) correspond to the problem

| (6.8) |

where is the set of the respective non-randomized policies. Here , where is the space of functions , and is the nested functional given by the composition of the conditional counterparts of the functionals

(cf., [10]).

Note the essential difference between the SOC and MDP approaches to distributionally robust optimization. In the MDP framework, in the formulation (5.5) the nested functional is defined on the scenario tree determined by scenarios of realizations of the state variables, and depends on the (non-randomized) policy . On the other hand in the SOC framework the nested functional corresponds to the sample paths (scenarios) of the data process , and does not depend on a particular policy .

Remark 6.1.

The ambiguity set can be written here as

| (6.9) |

and the sets and , defined in (2.20) and (2.26), respectively, can be written as

where is defined in (6.3). We have that the -rectangularity holds iff for all and all ; and the -rectangularity holds iff for all and all . In particular, suppose that the points are all different from each other for different . Then the -rectangularity (and hence -rectangularity) can hold only if the ambiguity set is the singleton.

7 Conclusions

For robust MDP with static formulation of the form (3.1), the arguably most important factor is its tractability.

Indeed it is shown in [17] that for general ambiguity sets the static formulation (3.1) is NP-hard.

Consequently many efforts have been devoted to constructing structured ambiguity sets that allow efficient computation. Most of the time this hinges upon certain dynamic equations or fixed-point characterization of the value function in the stationary case.

The -, -, and -rectangularity are some notable discoveries among this line of research.

Nevertheless each of them requires a case-by-case analysis in establishing such dynamic equations or the strong duality of the static formulation.

Through our discussions we argue that these properties of static formulation arise precisely as its equivalence to the game formulation and the strong duality of the game formulation.

Such a connection also creates possibilities for new construction of ambiguity sets for static formulation with tractability (see Remark 2.3).

In Section 6 we show that from the point of view of the distributionally robust setting, the Stochastic Optimal Control model differs from its MDP counterpart in that in seemingly natural formulations the basic condition of -rectangularity and -rectangularity can hold only if all ambiguity sets are the singletons.

Acknowledgement

The authors are indebted to Eugene Feinberg for insightful discussions which helped to improve the presentation.

References

- [1] P. Artzner, F. Delbaen, J.-M. Eber, and D. Heath. Coherent measures of risk. Mathematical Finance, 9:203–228, 1999.

- [2] D.P. Bertsekas and S.E. Shreve. Stochastic Optimal Control, The Discrete Time Case. Academic Press, New York, 1978.

- [3] R. Ding and E.A. Feinberg. Sequential optimization of CVaR. https://arxiv.org/pdf/2211.07288.pdf, 2023.

- [4] H. Föllmer and A. Schied. Stochastic Finance: An Introduction in Discrete Time. Walter de Gruyter, Berlin, 2nd edition, 2004.

- [5] Joel Goh, Mohsen Bayati, Stefanos A Zenios, Sundeep Singh, and David Moore. Data uncertainty in markov chains: Application to cost-effectiveness analyses of medical innovations. Operations Research, 66(3):697–715, 2018.

- [6] Vineet Goyal and Julien Grand-Clement. Robust markov decision processes: Beyond rectangularity. Mathematics of Operations Research, 48(1):203–226, 2023.

- [7] G.N. Iyengar. Robust Dynamic Programming. Mathematics of Operations Research, 30:257–280, 2005.

- [8] A. Jaśkiewicz and A. S. Nowak. Zero-sum stochastic games. In T. Basar and G. Zaccour, editors, Handbook of dynamic game theory. Springer, 2016.

- [9] A. Nilim and L. El Ghaoui. Robust control of Markov decision processes with uncertain transition probabilities. Operations Research, 53:780–798, 2005.

- [10] A. Pichler and A. Shapiro. Mathematical foundations of distributionally robust multistage optimization. SIAM Journal of Optimization, 70:3044 – 3067, 2021.

- [11] M. L. Puterman. Markov decision processes: discrete stochastic dynamic programming. John Wiley & Sons, 2014.

- [12] A. Shapiro, D. Dentcheva, and A. Ruszczyński. Lectures on Stochastic Programming: Modeling and Theory. SIAM, Philadelphia, third edition, 2021.

- [13] L. S. Shapley. Stochastic games. Proceedings of the National Academy of Sciences, 39:1095–1100, 1953.

- [14] M. Sion. On general minimax theorems. Pacific Journal of Mathematics, 8:171–176, 1958.

- [15] Y. Le Tallec. Robust, Risk-Sensitive, and Data-Driven Control of Markov Decision Processes. Ph.D. thesis, Massachusetts Institute of Technology. Cambridge, MA, 2007.

- [16] S. Wang, N. Si, J. Blanchet, and Z. Zhou. On the foundation of distributionally robust reinforcement learning. https://arxiv.org/abs/2311.09018, 2023.

- [17] W. Wiesemann, D. Kuhn, and B. Rustem. Robust Markov decision processes. Mathematics of Operations Research, 38(1):153 – 183, 2013.

- [18] H. Xu and S. Mannor. Distributionally Robust Markov Decision processes. Mathematics of Operations Research, 37(2):288 – 300, 2012.