On Block Cholesky Decomposition for Sparse Inverse Covariance Estimation

Xiaoning Kang, Jiayi Lian and Xinwei Deng∗

∗Department of Statistics, Virginia Tech

Abstract

The modified Cholesky decomposition is popular for inverse covariance estimation, but often needs pre-specification on the full information of variable ordering. In this work, we propose a block Cholesky decomposition (BCD) for estimating inverse covariance matrix under the partial information of variable ordering, in the sense that the variables can be divided into several groups with available ordering among groups, but variables within each group have no orderings. The proposed BCD model provides a unified framework for several existing methods including the modified Cholesky decomposition and the Graphical lasso. By utilizing the partial information on variable ordering, the proposed BCD model guarantees the positive definiteness of the estimated matrix with statistically meaningful interpretation. Theoretical results are established under regularity conditions. Simulation and case studies are conducted to evaluate the proposed BCD model.

Keywords: Graphical model, modified Cholesky decomposition, regularization, sparsity, variable ordering.

1 Introduction

The estimation of covariance and inverse covariance matrices is of fundamental importance in the multivariate statistics with a broad spectrum of applications, such as linear discriminant analysis (Clemmensen et al., 2011), portfolio optimization (Deng and Tsui, 2013), and assimilation (Nino-Ruiz et al., 2019). In high-dimensional data, sparse estimation of an inverse covariance matrix has specially attracted great attention, since it is closely related to a graphical model for inferring the conditional independence between variables of multivariate normal data. However, estimation of a large inverse covariance matrix often encounters two challenges. First, the estimated matrix needs to be positive definite for the valid statistical inferences. Second, the number of parameters in the model increases quickly in a quadratic order in terms of the matrix dimensionality.

Existing studies on the inverse covariance estimation in the literature generally fall into two categories. Denote the random variables of interest by with mean for simplicity and covariance matrix . The first category needs the pre-specification on the full ordering information of variables . That is, the variables have a natural ordering, which typically occurs in longitudinal data, time series, spatial data, spectroscopy and so forth. In this situation, banded or tapering estimation for the high-dimensional matrices has been developed (Bickel and Levina, 2008), requiring an assumption that the variables are becoming weakly correlated as their positions in the ordering are far away. Although these methods are straightforward and easy in computation, the resultant estimates may not be positive definite. A better technique for estimating the inverse covariance matrix in this category is the modified Cholesky decomposition (MCD) introduced by Pourahmadi (1999). It not only guarantees the positive definiteness of the estimated matrix, but also utilizes the information of variable ordering, leading to an accurate estimate. Moreover, this decomposition has a meaningful regression interpretation, allowing the use of the regularization for sparse estimation (Huang et al., 2006; Kang and Wang, 2021). That is, the sparse pattern in the Cholesky-based matrix estimates can be induced by the sparsity in the Cholesky factors through linear regressions in the decomposition.

The second category considers that the information of variable ordering is not available. In this case, one strategy is to identify a proper variable ordering based on a certain data driven mechanism, transforming it into the estimation problem of the first category. For example, Wagaman and Levina (2009) determined the variable ordering by the Isomap algorithm and proposed an Isoband matrix estimate. Dellaportas and Pourahmadi (2012) suggested using BIC criterion to seek for the variable ordering before applying the MCD technique. Rajaratnam and Salzman (2013) recovered the variable ordering via the best permutation algorithm, which is very efficient for autoregressive model. However, a potential drawback is obvious that the accuracy of such estimates relies on the accuracy of the estimated orderings of variables. Furthermore, some real data, for example gene data and medical data, practically may not have a natural variable ordering, which means that it is not adequate to find a variable ordering for such data. Alternatively, another strategy in this category is to consider a permutation invariant estimation for inverse covariance matrix. One popular method is the Graphical lasso (Glasso) proposed by Meinshausen and Bühlmann (2006) and Yuan and Lin (2007), of which the algorithms and properties have been widely studied (Friedman et al., 2008; Lam and Fan, 2009; Yuan, 2010). Other works on the permutation invariant estimation for inverse covariance matrix can be found in Xue et al. (2012); Wang et al. (2015); Cai et al. (2016); Van Wieringen (2019); Wang et al. (2020), among many others.

By comparing two categories of estimation methods, it is seen that the MCD is an appropriate method for estimating the inverse covariance matrix when the information of variable ordering is fully available, while the Glasso is suitable when the information of variable ordering is not available. However, in many applications, there is only partial information of variable ordering available. Here the partial information means that the variables can be divided into several groups (including one group) with the group ordering known but the variable ordering within each group unknown. For example, in the multi-stage manufacturing process (Shi, 2006), each stage contains a set of variables and the stages have a natural ordering among themselves because of the nature of manufacturing process. Thus, the full information of variable ordering is not available since the variables within the same stage may not have an ordering. In this case the partial information of variable ordering is present since there is an ordering among stages. To estimate the inverse covariance matrix of variables in such a multi-stage manufacturing process, neither the MCD method nor the Glasso method is adequate. Another concrete example is the Covid-19 data in Case Studies Section. The data were weekly collected from 37 continuous weeks at the beginning of the pandemic. In each week, four variables which have no ordering among themselves are recorded. Such four variables in a certain week are correlated with variables in the former weeks (see details in Case Studies). Therefore the variables can be naturally divided into 37 groups by calendar week, which forms a partial information of the variable ordination.

In this work, we fill in the gap to develop a block Cholesky decomposition (BCD) method for estimating the inverse covariance matrix given the partial information of variable ordering. The proposed BCD method takes advantage of such partial information on the variable ordination to estimate the inverse covariance matrix via the joint estimation of a set of penalized multivariate regressions. It guarantees the positive definiteness of the estimated sparse inverse covariance matrix with statistically meaningful interpretation. Moreover, the proposed method provides a unified framework of estimating the inverse covariance matrix, where the MCD, the Glasso method, the Witten et al. (2011)’s estimator and Rothman et al. (2010a)’s estimator can be all considered as special cases of the proposed method. The theoretical results suggest that the proposed model can have faster consistent rate than that of Glasso method when the partial information on the variable ordination is present. The R codes of implementing the proposed model are available at https://github.com/xiaoningmike/BCD.

The remainder of this work is organized as follows. Section 2 develops the proposed method along with its parameter estimation. The asymptotically theoretical property is established in Section 3 under regularity conditions. Sections 4 and 5 demonstrate the merits of the proposed model via simulations and two real data examples. We conclude our work with some discussion in Section 6. All technical proofs are reported in the Appendix.

2 The Proposed Method

In this section, we describe the proposed methodology of the BCD method. Different from the MCD technique, the proposed BCD method only requires partial information of the variable ordination.

2.1 Block Cholesky Decomposition for Inverse Covariance Matrix

Suppose that the variables in can be partitioned into groups, with the th group of variables denoted as , where is the number of variables in the th group, and . Assume that these groups of variables have a natural ordering of , while there is not any ordering structure among variables within each group . We call such ordering information of these groups as the partial information of the variable ordination. Note that when , it reduces to the case that there is no ordering information for the variables , and corresponds to the case that the variables have a full ordering information. In this work, we assume both of and can be diverged as the sample size goes to infinity.

Without loss of generality, we write with its inverse covariance matrix . The key idea of the BCD model is to decompose by a block lower triangular matrix constructed from the multivariate regression coefficients when the variable group is regressed on its preceding variable groups for . Specifically, the BCD method considers a series of multivariate regressions

| (2.1) |

where and with being the coefficient matrix. Here is the -dimensional vector of error term for the th multivariate regression with and . Hence, we can construct a block lower triangular matrix written as

with its th diagonal element being a zero matrix, and its lower left part composed of all the regression coefficient matrices in Equation (2.1). Besides, define

Denote by the block diagonal covariance matrix of vector . Thus the multivariate regressions in (2.1) can be written as

| (2.2) |

where represents the identity matrix, and is a unit block lower triangular matrix having ones on its diagonal. The matrices and are called the block Cholesky factors. By taking in Equation (2.2), we have , which consequently leads to

| (2.3) |

where . As a result, the BCD method reduces the challenge of modeling an inverse covariance matrix based on the partial information of the variable ordination into the problem of estimating multivariate linear regressions. Because of the decomposition (2.3), the general sparsity in would induce some sparsity in (although it may not induce certain structured sparsity), which is easily implemented by the regularization on the linear regressions in (2.1). The decomposition (2.3) also indicates that the BCD method can guarantee the positive definiteness of the resulting estimate of provided that are all positive definite. Note that there is no constraint required for parameters in matrix . We would like to remark that although the proposed model needs information on the group ordering, it is invariant to the permutation of variables within each group because the coefficient estimation of multivariate regressions in (2.1) is not affected by the ordering of variables in and . This point is verified in the simulation study. Moreover, it is seen that the MCD is a special case of the proposed BCD with (i.e., for ), which represents the case where the variables have a full ordering information.

2.2 Parameter Estimation

Denote by the independently and identically distributed observations from the multivariate normal distribution . Let be the data matrix. Based on the partial information of the variable ordination, we partition by columns and write , where represents the sub-data matrix corresponding to the th variable group . Based on the methodology of BCD, we need to model a set of multivariate regressions in (2.1) to obtain the estimates of block Cholesky factors matrices and . The negative joint log-likelihood function is expressed as

| (2.4) |

up to some constant. The symbol , where stands for the data matrix of the first groups of variables. By encouraging the sparsity in the estimates and , we can obtain a sparse estimate . Thus, the penalized log-likelihood function in the following is considered for parameter estimation as

| (2.5) |

where with being zero matrix. Here and are tuning parameters, the matrix norm , and with being the elements of matrix .

Note that different components contain different parameters and . Hence minimizing is equivalent to minimizing each separately, which facilitates a parallel computing procedure for estimating simultaneously to save computational time. For each minimization of , although the objective function is not convex with respect to , it is a biconvex optimization (Gorski et al., 2007). That is, is convex over when fixing , and is also convex over when fixing . This property enables us to apply a coordinate descent algorithm to iteratively estimate by minimizing for a given , and estimate by minimizing for a given (Rothman et al., 2010b; Sofer et al., 2014). Specifically, for a given , we solve

| (2.6) |

where , and . Here vec denotes the vectorization operator and the Kronecker product, and their property is applied. The optimization problem (2.2) is thus a linear regression with Lasso penalty (Tibshirani, 1996). The initial value for is set to be the identity matrix. On the other hand, for a given , we solve

| (2.7) |

where . It has the same form as Glasso estimation. Accordingly, the estimates and are iteratively solved from optimization problems (2.2) and (2.2) until convergence. After obtaining the estimates and , we construct the block Choleksy factor estimate with as the th block row and the identity matrix being the block diagonal. The estimate is constructed with as its th block diagonal. Then is a sparse estimate of inverse covariance matrix under the partial information of variable ordination. We briefly summarize the above estimation procedure in Algorithm 1.

Algorithm 1

Input: Data , tuning parameters and .

Output: Estimate corresponding to and .

For to do

Step 0: Set an initial value of .

Step 1: Given , solve in (2.2) by the Lasso technique.

Step 2: Given , solve in (2.2) by the Glasso technique.

Step 3: Repeat Steps 1 and 2 till both and converge.

End

Step 4: and , then .

Here and represent the estimates of and in the th iteration. The convergence criteria are and , where and are two pre-selected small quantities, and stands for the Frobenius norm. Since the objective (2.2) is not joint convex, there is no guarantee of finding the global minimum. However, Algorithm 1 uses a coordinate descent to compute a local solution of (2.2). Steps 1 and 2 both ensure a decrease in the value of objective, leading to the convergence of and . In Step 3, we also set a maximum number of iterations as 100 in case that the parameter estimation is not empirically converged. However, in the simulation we have tried, almost all the parameter estimates satisfy the convergence criteria quickly with several tens of iterations.

Note that there are two tuning parameters and in the objective function (2.2). To choose their optimal values, studies in the literature often suggest cross-validation, information criteria, independent validation set mechanism and so forth. In this work the BIC (Bayesian information criterion) proposed by Yuan and Lin (2007) is adopted to determine the optimal values of tuning parameters as follows

where is the sample covariance matrix, and represents the number of non-zeros in the lower triangular part of estimate . The optimal values of tuning parameters are selected to minimize BIC.

At the end of this section, we would like to point out that the literatures studying the MCD often assume a certain type of sparse structure, e.g. banded structure, for the underlying inverse covariance matrix. Then some sparse patterns in will lead to certain desired sparse structures of estimate . However when the underlying matrix have a general unstructured sparsity, the relationship of sparsity between matrices and is not very explicit. Nonetheless, the sparsity in is also able to be induced by a sparse estimate empirically (Huang et al., 2006; Kang and Deng, 2020). Moreover, we justify this point in the simulation by FSL criterion which evaluates the capability of catching the sparsity of underlying matrix.

2.3 Comparison and Connection with Several Existing Methods

The proposed BCD method obtains a sparse inverse covariance matrix estimate under the partial information of variable ordination. Both of the Cholesky factors’ estimates and contain the sparsity resulting from a set of penalized multivariate regressions. It makes close connection with several existing methods.

Firstly, we demonstrate that the MCD, Glasso, Rothman et al. (2010a) and Witten et al. (2011) are all special cases of the proposed method. The MCD method for estimating is a special case when , indicating that there is a full ordering information. When data have partial ordering information, the MCD is not suitable. The MCD needs a pre-specified full ordering before analyzing data, but the variables have no ordering within each group. Therefore, one needs to identify an ordering before applying the MCD. However, different orderings would lead to different estimates (Chang and Tsay, 2010), and an incorrectly identified ordering would result in an inaccurate estimate. Additionally, the Glasso is a special case of the proposed BCD with , implying that there is no ordering information. Besides, Rothman et al. (2010a) studied a banded estimate of via MCD. Their approach can also be viewed as a special case of the proposed BCD model by and regressing only on its several nearest previous group variables instead of all the previous group variables in Equation (2.1). Furthermore, the proposed BCD method can be easily extended to estimate the inverse covariance matrix with a banded block structure.

In addition, Witten et al. (2011) introduced a block diagonal inverse covariance estimation with each block obtained by the Glasso on the corresponding group variables. Their method assumed that variables in different groups are independent. Thus their estimator is also a special case of the proposed BCD, in the sense that the block Cholesky factor becomes the identity matrix under the independence assumption between group variables, and each is then estimated from Glasso on . The estimate is the same as that in Witten et al. (2011).

Secondly, we compare several methods from perspective of ordering information. When there is no ordering among variables, apart from Glasso which penalizes likelihood function, some papers investigated matrix estimation through penalized pseudo-likelihood. They solve their optimization problems often in a column-by-column fashion, such as Yuan (2010); Cai et al. (2011); Liu and Luo (2015); Liu and Wang (2017) and so forth. Liu and Luo (2015) extended the idea of Cai et al. (2011) and proposed SCIO estimator as

where is the th column of the identity matrix, is a tuning parameter, and is the estimate of the th column of . However the estimates obtained from a column by column fashion are not guaranteed to be positive definite, and a symmetrization step is also needed to make their estimates symmetric. In the contrast, the proposed BCD estimate is itself symmetric and positive definite.

On the other hand, when variables have a full information on the ordering, two recent works Yu and Bien (2017) and Khare et al. (2019) proposed to estimate via the classical Cholesky decomposition , where the Cholesky factor is a lower triangular matrix. Both of such decomposition and the MCD induce the sparse estimates by the sparsity in the Cholesky factors. The advantage of classical Cholesky decomposition is to directly result in a convex objective with respect to parameter , hence guaranteeing a global convergence with an appropriate penalty. But it lacks statistical meanings and interpretation as explicit as the MCD technique. Yu and Bien (2017) assumed “local dependence” in the ordered data in the sense that the th variable is correlated with its nearest variables, where can be different. That is, they assumed structured sparse pattern in the underlying , while the proposed BCD is suitable for a general or unstructured sparsity. Khare et al. (2019) introduced CSCS estimator, which accommodates the unstructured sparsity by imposing a Lasso-type penalty on the likelihood function in terms of , and developed a cyclic coordinate algorithm which leads to a closed form of solution for the estimates of each row of . To the best of our knowledge, few works have contributed to the inverse covariance estimation when variables have partial ordering information.

3 Theoretical Properties

In this section, we establish the asymptotically theoretical properties for the proposed BCD estimator. To facilitate the presentation and proofs, we introduce some notation and make assumptions on the true model. Let be the underlying inverse covariance matrix with its block MCD according to the group variables . Let , and be the counterpart of in the block Cholesky factor . That is, is the th block row in the lower triangular part of matrix . Define as the collection of nonzero elements in the matrix . Similarly, denote the counterpart of in the block Cholesky factor by the matrix , which is the th block diagonal of matrix . Let be the collection of nonzero off-diagonal elements in the matrix . Denote by and the cardinality of and , respectively. Let and . In order to achieve the asymptotic consistent property of the proposed estimator, a mild condition is needed that there exists a constant such that the singular values of are bounded as

| (3.1) |

where represent the singular values of matrix in a decreasing order. This assumption is made to guarantee the positive definiteness of . In addition, assume that there exist constants and such that

| (3.2) |

Assumption (3.2) characterizes the relation between each and for high-dimensional data. If diverges to infinity, corresponds to the case where is fixed and controlled by , while implies that also diverges, but not faster than , where is some positive arbitrarily small number. Denote , the set of indices that the corresponding groups have a diverging number of variables. Now, we present the main results in Theorems 1 and 2.

Theorem 1.

Suppose that are independently and identically distributed observations from . Let and be any estimates of and obtained from the path of Algorithm 1. Under (3.1) and (3.2), assume that the tuning parameters and satisfy , , then

(a) there exists a local minimum of such that .

(b) there exists a local minimum of such that .

Theorem 2.

Let be the estimate of obtained by Algorithm 1. Assume all the assumptions in Theorem 1 hold, then we have

Under the condition , .

Theorem 1 provides asymptotic consistent rates of the estimators and that are obtained by minimizing in (2.2) and minimizing in (2.2). Theorem 2 establishes the property for the inverse covariance estimate obtained from the proposed Algorithm 1, which demonstrates the consistent rate of our estimate in practice. Moreover, we would like to have the following remarks.

First, from Theorem 1 we have . Such rate is sharper than the theoretical Glasso consistent rate ( is a measure of sparsity), which has been obtained in the literature (Lam and Fan, 2009), because of resulting from , where . The equality holds only in the situation that all the variables are in one group, where it is exactly a Glasso problem. This implies that, as long as there are at least two groups of variables, the proposed BCD model with partial information of variable ordination is useful in reducing the consistent rate.

Second, the estimation of is decomposed into separate Glasso estimations in the proposed method. According to the log sum inequality, we have . The equality holds when for all , indicating that the lowest bound of the proposed estimator’s consistent rate would be achieved when each group has the equal number of variables. In view of this, we would like to point out that: (i) a larger number of variable groups leads to a smaller value of the lowest bound of the consistent rate; (ii) the more evenly that variables are assigned into groups, the more closely that the consistent rate tends to the lowest bound.

Third, the requirement in Theorem 2 is a relatively weaker condition compared with the assumption for the Glasso model. Note that , then we may require a stronger condition . Moreover, if we further loose the upper bound of , the proposed BCD model needs an even stronger condition , which however is the similar condition as that for the Glasso estimator.

4 Numerical Study

In this section, we conduct simulation studies to evaluate the performance of the proposed BCD model (Prop) in comparison with several existing methods, including the MCD method, Glasso, SCIO (Liu and Luo, 2015) and CSCS (Khare et al., 2019). The MCD, where , reduces Equation (2.1) to univariate linear regressions with their coefficients estimated by Lasso. The Glasso and SCIO are two popular methods, but do not consider ordering information. The CSCS is suitable for data with full ordering information and implemented via classical Cholesky decomposition. The tuning parameters in the Glasso, SCIO and CSCS methods are selected based on BIC. Besides, to examine whether the proposed model is permutation invariant within each group, we also implement the Prop∗ method, which estimates by Algorithm 1 from data which randomly permutate variables within each group.

The data are independently generated from with sample size and number of variables . We consider two different cases of variable groups: (1) five groups with each containing 40 variables; (2) four groups with each subsequently containing 30, 60, 40 and 70 variables. Let represent a squared matrix with autoregressive structure with th entry as , . Let indicate a squared banded matrix with the main diagonal elements 1, and the subsequent sub-diagonal elements are 0.5, 0.4 and 0.3 respectively. Denote an non-squared matrix if , and otherwise, where represents the matrix with all elements 0. Similarly, Denote an non-squared matrix if , and otherwise. To systematically investigate the performance of the proposed method, we consider the following different structures of inverse covariance matrix .

-

•

Scenario 1. .

-

•

Scenario 2. .

-

•

Scenario 3.

+ . The value of is gradually increased to ensure that is positive definite.

-

•

Scenario 4. , where is generated by randomly permuting rows and corresponding columns of each block of

. The value of is gradually increased to ensure that is positive definite. -

•

Scenario 5. , where is a block diagonal matrix with its each diagonal block as AR(0.5), and with and otherwise.

-

•

Scenario 6. , where is a block diagonal matrix with its each diagonal block being MA(0.5,0.4,0.3), and with and otherwise.

-

•

Scenario 7. . Here the diagonal elements of are 0, and each off-diagonal element is generated independently as , where is a Bernoulli random variable with probability 0.15 equal 1. The value of increases gradually to make sure is positive definite.

Scenario 1 is the AR structure with the variables’ correlations decaying when they are far apart from each other. Scenarios 2 is a block diagonal matrix with multiple groups of variables, where the variables in different groups are independent. Scenarios 3 and 4 are block matrices with multiple groups of variables with variables in different groups possibly correlated. Scenarios 5 and 6 are similarly used in Huang et al. (2006). Scenario 7 is a general sparse matrix with random structure.

To evaluate the accuracy of each estimate for the underlying inverse covariance matrix , we consider the loss measures , the matrix spectral norm , the Frobenius norm F of as follows

where is the maximum value of eigenvalues. We also use the Kullback-Leibler loss (KL) as well as the quadratic loss (QL)

In addition, to gauge the ability of the proposed model to capture the underlying sparse structure, we report the false selection loss FSL = (FP + FN) / in percentage, where FP is the false positive and FN is the false negative. The simulation results of loss measures for each method are summarized in Tables 1 and 2, reporting their averages and corresponding standard errors (in parenthesis) over 50 replicates.

| Scenario | Fnorm | KL | QL | FSL (%) | |||

|---|---|---|---|---|---|---|---|

| 1 | MCD | 50.25 (6.628) | 16.66 (2.187) | 196.5 (24.94) | 4.000 (0.670) | 4.738 (1.027) | 34.75 (0.302) |

| Glasso | 8.852 (0.001) | 8.717 (0.001) | 28.61 (0.004) | 0.518 (0.001) | 0.601 (0.004) | 27.67 (0.001) | |

| SCIO | 8.843 (0.002) | 8.685 (0.001) | 28.43 (0.004) | 0.451 (0.003) | 0.655 (0.005) | 27.35 (0.006) | |

| CSCS | 8.750 (0.004) | 8.577 (0.002) | 28.06 (0.009) | 0.415 (0.002) | 0.505 (0.005) | 27.30 (0.019) | |

| Prop | 8.768 (0.004) | 8.581 (0.001) | 27.87 (0.006) | 0.363 (0.001) | 0.397 (0.004) | 25.89 (0.022) | |

| 2 | MCD | 41.23 (15.07) | 32.46 (4.881) | 34.83 (5.265) | 0.366 (0.054) | 2.921 (0.699) | 29.53 (0.580) |

| Glasso | 2.613 (0.004) | 2.379 (0.003) | 12.57 (0.009) | 0.242 (0.001) | 0.410 (0.003) | 7.875 (0.001) | |

| SCIO | 2.618 (0.005) | 2.363 (0.003) | 12.48 (0.010) | 0.240 (0.003) | 0.419 (0.003) | 7.769 (0.003) | |

| CSCS | 2.586 (0.006) | 2.324 (0.005) | 12.20 (0.031) | 0.222 (0.002) | 0.390 (0.003) | 7.711 (0.010) | |

| Prop | 2.539 (0.007) | 2.259 (0.002) | 11.78 (0.008) | 0.195 (0.001) | 0.340 (0.003) | 7.343 (0.006) | |

| 3 | MCD | 61.20 (5.725) | 205.6 (20.88) | 245.2 (25.91) | 4.671 (0.303) | 28.53 (6.462) | 49.24 (0.163) |

| Glasso | 9.592 (0.001) | 9.414 (0.001) | 25.87 (0.004) | 0.778 (0.001) | 2.952 (0.023) | 36.35 (0.001) | |

| SCIO | 9.579 (0.002) | 9.348 (0.001) | 25.62 (0.004) | 0.703 (0.003) | 3.506 (0.029) | 35.99 (0.007) | |

| CSCS | 9.543 (0.007) | 9.153 (0.005) | 25.14 (0.016) | 0.591 (0.003) | 1.604 (0.024) | 34.72 (0.032) | |

| Prop | 9.530 (0.005) | 9.140 (0.001) | 25.09 (0.003) | 0.424 (0.001) | 0.681 (0.009) | 36.99 (0.018) | |

| 4 | MCD | 50.70 (6.839) | 16.30 (2.144) | 19.04 (2.179) | 3.108 (0.210) | 54.44 (11.78) | 47.52 (0.204) |

| Glasso | 4.221 (0.031) | 3.474 (0.012) | 11.33 (0.111) | 0.568 (0.041) | 10.79 (2.661) | 21.14 (0.079) | |

| SCIO | 3.936 (0.001) | 3.546 (0.001) | 11.91 (0.012) | 0.597 (0.083) | 9.475 (1.973) | 19.70 (0.001) | |

| CSCS | 6.880 (0.140) | 3.300 (0.006) | 10.12 (0.032) | 0.566 (0.019) | 2.601 (0.067) | 22.23 (0.109) | |

| Prop | 4.341 (0.010) | 3.373 (0.002) | 10.50 (0.008) | 0.466 (0.001) | 2.075 (0.043) | 21.12 (0.014) | |

| 5 | MCD | 136.7 (13.75) | 50.75 (5.017) | 67.67 (5.552) | 1.282 (0.086) | 47.12 (6.803) | 31.27 (0.281) |

| Glasso | 9.354 (0.005) | 8.612 (0.005) | 30.83 (0.029) | 0.626 (0.006) | 8.278 (0.366) | 23.54 (0.013) | |

| SCIO | 9.543 (0.002) | 8.841 (0.002) | 32.11 (0.010) | 0.637 (0.008) | 3.559 (0.034) | 23.85 (0.001) | |

| CSCS | 9.532 (0.014) | 8.540 (0.015) | 29.38 (0.075) | 0.966 (0.014) | 1.786 (0.013) | 22.77 (0.043) | |

| Prop | 9.311 (0.007) | 8.390 (0.005) | 29.77 (0.026) | 0.614 (0.003) | 0.665 (0.085) | 23.09 (0.055) | |

| 6 | MCD | 34.50 (2.309) | 13.79 (0.952) | 27.24 (0.814) | 1.493 (0.016) | 20.98 (0.858) | 25.59 (0.234) |

| Glasso | 8.291 (0.004) | 5.340 (0.005) | 25.74 (0.028) | 1.052 (0.009) | 1.717 (0.121) | 12.45 (0.027) | |

| SCIO | 10.52 (0.713) | 7.234 (0.382) | 26.68 (0.478) | 1.243 (0.083) | 1.494 (0.062) | 10.70 (0.001) | |

| CSCS | 7.987 (0.017) | 4.921 (0.008) | 21.62 (0.044) | 1.278 (0.039) | 1.275 (0.018) | 11.33 (0.111) | |

| Prop | 7.724 (0.024) | 5.003 (0.015) | 22.92 (0.103) | 1.062 (0.008) | 0.803 (0.258) | 10.31 (0.064) | |

| 7 | MCD | 78.65 (9.265) | 25.19 (2.910) | 28.24 (2.983) | 4.042 (0.291) | 11.57 (2.259) | 48.25 (0.290) |

| Glasso | 5.112 (0.054) | 1.638 (0.005) | 10.88 (0.041) | 0.537 (0.010) | 3.615 (0.313) | 16.97 (0.027) | |

| SCIO | 4.502 (0.008) | 1.663 (0.001) | 10.74 (0.017) | 0.547 (0.008) | 3.227 (0.412) | 14.86 (0.010) | |

| CSCS | 5.776 (0.099) | 1.580 (0.005) | 9.346 (0.034) | 0.524 (0.007) | 2.444 (0.081) | 17.16 (0.092) | |

| Prop | 4.618 (0.020) | 1.540 (0.003) | 9.701 (0.027) | 0.468 (0.002) | 2.129 (0.054) | 16.88 (0.028) |

| Scenario | Fnorm | KL | QL | FSL (%) | |||

|---|---|---|---|---|---|---|---|

| 1 | MCD | 48.46 (6.760) | 16.19 (2.258) | 178.1 (23.47) | 4.400 (0.556) | 3.809 (0.841) | 33.46 (0.316) |

| Glasso | 8.850 (0.001) | 8.718 (0.001) | 28.62 (0.003) | 0.518 (0.001) | 0.597 (0.003) | 27.68 (0.001) | |

| SCIO | 8.845 (0.002) | 8.683 (0.001) | 28.43 (0.004) | 0.489 (0.002) | 0.648 (0.004) | 27.35 (0.005) | |

| CSCS | 8.771 (0.003) | 8.603 (0.002) | 28.05 (0.010) | 0.451 (0.003) | 0.497 (0.004) | 27.29 (0.022) | |

| Prop | 8.785 (0.003) | 8.610 (0.003) | 28.04 (0.016) | 0.387 (0.002) | 0.421 (0.003) | 26.43 (0.030) | |

| 2 | MCD | 23.83 (19.01) | 36.34 (6.053) | 38.72 (6.322) | 0.397 (0.060) | 3.993 (0.879) | 28.31 (0.577) |

| Glasso | 2.612 (0.004) | 2.384 (0.002) | 12.60 (0.008) | 0.243 (0.001) | 0.418 (0.003) | 8.099 (0.001) | |

| SCIO | 2.635 (0.019) | 2.367 (0.002) | 12.51 (0.008) | 0.242 (0.003) | 0.430 (0.004) | 7.998 (0.003) | |

| CSCS | 2.605 (0.008) | 2.331 (0.005) | 12.26 (0.036) | 0.227 (0.002) | 0.400 (0.004) | 7.976 (0.015) | |

| Prop | 2.573 (0.008) | 2.271 (0.004) | 11.88 (0.026) | 0.201 (0.002) | 0.354 (0.004) | 7.687 (0.013) | |

| 3 | MCD | 16.27 (1.882) | 60.19 (7.668) | 81.22 (7.474) | 2.385 (0.119) | 16.14 (2.668) | 41.68 (0.223) |

| Glasso | 7.953 (0.003) | 7.766 (0.007) | 22.23 (0.034) | 1.147 (0.033) | 7.825 (0.492) | 21.93 (0.030) | |

| SCIO | 7.971 (0.055) | 7.668 (0.041) | 21.14 (0.042) | 1.337 (0.054) | 9.113 (0.230) | 21.38 (0.010) | |

| CSCS | 7.845 (0.011) | 7.451 (0.009) | 20.01 (0.032) | 0.953 (0.048) | 1.564 (0.036) | 22.53 (0.115) | |

| Prop | 7.817 (0.006) | 7.405 (0.002) | 20.78 (0.007) | 0.486 (0.002) | 0.789 (0.016) | 23.73 (0.021) | |

| 4 | MCD | 26.29 (4.073) | 8.836 (1.365) | 11.09 (1.435) | 1.883 (0.142) | 18.57 (4.659) | 39.62 (0.273) |

| Glasso | 4.284 (0.051) | 2.809 (0.008) | 9.456 (0.055) | 0.347 (0.015) | 2.629 (1.172) | 15.57 (0.037) | |

| SCIO | 3.576 (0.001) | 2.939 (0.001) | 10.22 (0.012) | 0.405 (0.026) | 2.506 (1.088) | 14.13 (0.001) | |

| CSCS | 5.846 (0.119) | 2.684 (0.005) | 8.746 (0.024) | 0.369 (0.010) | 1.782 (0.043) | 15.88 (0.046) | |

| Prop | 4.491 (0.025) | 2.788 (0.003) | 9.024 (0.008) | 0.358 (0.001) | 1.487 (0.033) | 15.82 (0.017) | |

| 5 | MCD | 69.74 (5.203) | 25.87 (1.396) | 56.76 (1.174) | 1.714 (0.097) | 68.35 (9.419) | 36.22 (0.221) |

| Glasso | 25.84 (0.003) | 20.54 (0.002) | 53.62 (0.008) | 0.824 (0.005) | 11.44 (0.379) | 35.91 (0.014) | |

| SCIO | 25.96 (0.002) | 20.65 (0.001) | 54.02 (0.002) | 0.797 (0.008) | 4.084 (0.035) | 37.30 (0.001) | |

| CSCS | 25.62 (0.007) | 20.35 (0.003) | 52.98 (0.010) | 1.057 (0.035) | 3.884 (0.011) | 34.60 (0.035) | |

| Prop | 25.76 (0.004) | 20.42 (0.003) | 53.07 (0.013) | 0.734 (0.002) | 3.003 (0.200) | 33.54 (0.049) | |

| 6 | MCD | 38.13 (3.725) | 15.74 (1.756) | 29.40 (1.459) | 1.032 (0.022) | 22.71 (1.110) | 25.72 (0.266) |

| Glasso | 8.295 (0.005) | 5.364 (0.005) | 25.81 (0.031) | 1.072 (0.010) | 1.355 (0.114) | 12.55 (0.031) | |

| SCIO | 9.359 (0.798) | 6.426 (0.358) | 27.73 (0.641) | 1.106 (0.094) | 1.379 (0.056) | 10.99 (0.019) | |

| CSCS | 7.985 (0.022) | 4.827 (0.009) | 21.68 (0.047) | 1.091 (0.018) | 1.308 (0.021) | 11.65 (0.128) | |

| Prop | 7.659 (0.017) | 5.005 (0.009) | 22.86 (0.070) | 0.902 (0.005) | 0.726 (0.159) | 11.08 (0.033) | |

| 7 | MCD | 40.16 (5.131) | 13.34 (1.641) | 16.00 (1.795) | 2.658 (0.200) | 37.25 (8.799) | 47.28 (0.289) |

| Glasso | 5.944 (0.099) | 1.588 (0.006) | 10.53 (0.060) | 0.480 (0.015) | 4.094 (0.968) | 16.34 (0.038) | |

| SCIO | 4.682 (0.001) | 1.619 (0.001) | 10.34 (0.014) | 0.483 (0.009) | 3.901 (0.876) | 15.13 (0.001) | |

| CSCS | 8.205 (0.198) | 1.604 (0.038) | 9.022 (0.032) | 0.451 (0.006) | 1.756 (0.068) | 17.52 (0.070) | |

| Prop | 4.992 (0.029) | 1.503 (0.001) | 9.063 (0.010) | 0.374 (0.001) | 1.312 (0.029) | 17.15 (0.016) |

Overall, the Prop method gives relatively superior performance compared with other methods for the considered loss measures. Especially it performs substantially well with respect to KL and QL for all the scenarios. Note that the results of Prop∗ are omitted in the tables since they are exactly the same as the results of the Prop method. It further confirms that the proposed BCD model is permutation invariant for the variables within each group. In scenario 1, the CSCS and Prop are the best models. The CSCS method is slight better than Prop regarding and Fnorm since it is designed for inverse covariance estimation of data with full information on variable ordering. For other scenarios 2-7, we observe that (1) the Prop is at least comparable with or slightly better than CSCS method; (2) the Prop outperforms SCIO, Glasso and MCD methods for most loss measures. In addition, the compared methods also show their advantages in some loss functions. For example, the SCIO produces the lowest values in terms of and FSL for both of scenarios 4 and 7. The CSCS gives the best performance in terms of Fnorm for scenarios 5, 6 and 7. It is also superior over other methods regarding for scenarios 4 and 6.

Besides, one can see that the MCD approach does not perform well compared with other methods, possibly due to that most simulated data do not have a valid full information of natural variable ordering. It can make the MCD, the performance of which heavily depends on the variable ordering, being inferior to other methods. Moreover, for Scenario 7 without any variable ordering, we observe that the Glasso can be better in certain criteria such as and . Especially, the Glasso is superior in FSL as expected since it is good at inducing sparsity. Comparing with CSCS, the Glasso gives similar performance on , although not as good in terms of Fnorm and QL.

5 Case Studies

5.1 Covid-19 Data

We further evaluate the performance of the proposed model through a real data example of Covid-19 pandemic, which is available on the official website of Virginia health department. The data were weekly collected during May 29th, 2020 to February 6th, 2021 (37 weeks) from 34 districts in Virginia State such as Arlington, Fairfax, Richmond, Roanoke, Virginia Beach, etc. For each week the data contain four variables: the accumulative number of cases, the accumulative number of people hospitalized, the accumulative number of deaths and the accumulative number of people taking the PCR (polymerase chain reaction) tests, resulting in variables.

Denote the collected data by , and transform to make the data distribution close to normal (Brown et al., 2005). We then apply the proposed model as well as the MCD, SCIO, CSCS and Glasso methods to estimate the inverse covariance matrix. To conduct data analysis, the 148 variables are partitioned into 37 groups with each group naturally corresponding to a calendar week. Hence it is seen that the data have a partial information of the variable ordination in a weekly scale. To examine the performance of methods in comparison, we predict the accumulative number of cases, the accumulative number of people hospitalized, the accumulative number of deaths and the accumulative number of people taking PCR in the last 2 weeks using the inverse covariance estimates obtained from the data in the first 35 weeks. Specifically, let , where and represent the data in the first 35 weeks and last 2 weeks for the th district, . Hence contains variables and contains variables. Accordingly, the mean vector and the inverse covariance matrix are divided as

Assuming multivariate normality, we have

| (5.1) |

The 34 observations are split into a training set and a testing set using the leaving-one-out mechanism. That is, each observation is considered as a testing point with the rest 33 observations as training set. The training set is used to estimate the mean vector and the inverse covariance matrix . The values of in the testing data are used to predict based on Equation (5.1). For each variable in , define the average absolute prediction error (APE) by

where is the predicted value.

| 36th week | 37th week | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Cases | Hospitalizations | Deaths | PCR | Cases | Hospitalizations | Deaths | PCR | ||

| MCD | 2.90 (0.26) | 0.79 (0.11) | 0.79 (0.11) | 1.41 (0.16) | 1.65 (0.22) | 0.87 (0.12) | 0.75 (0.09) | 2.20 (0.40) | |

| Glasso | 3.57 (0.43) | 1.03 (0.13) | 1.02 (0.13) | 5.50 (0.68) | 2.41 (0.32) | 1.00 (0.10) | 0.93 (0.11) | 5.16 (0.75) | |

| SCIO | 2.48 (0.32) | 0.95 (0.13) | 1.04 (0.12) | 2.65 (0.34) | 2.22 (0.31) | 0.99 (0.10) | 0.93 (0.11) | 3.02 (0.51) | |

| CSCS | 2.54 (0.24) | 1.06 (0.13) | 0.79 (0.12) | 1.50 (0.19) | 1.64 (0.19) | 0.85 (0.10) | 0.84 (0.08) | 1.68 (0.40) | |

| Prop | 2.39 (0.33) | 0.80 (0.11) | 0.75 (0.12) | 1.33 (0.17) | 1.61 (0.24) | 0.80 (0.09) | 0.73 (0.08) | 2.55 (0.39) | |

Table 3 reports the values of APEj for , corresponding to the prediction measurements for weeks 36 and 37. The columns “Hospitalizations” and “PCR” represent the variables that the number of people hospitalized, and the number of people attending the PCR tests, respectively. We observe that the Prop outperforms the SCIO and Glasso, and is slightly better than the CSCS and MCD approaches. Specifically, the Prop provides more accurate prediction in the number of cases, which is of practically importance for pandemic study on the risk assessment. It also predicts well in the number of deaths, and performs comparably with the CSCS and MCD in predicting the number of people who will take the PCR tests and the number of patients in hospital due to Covid-19. Additionally, it is seen that the CSCS and MCD methods perform better than the Glasso and SCIO on this data set. One possible reason is that the data, although not very strictly, have a natural time ordering by weeks among the variables. The CSCS and MCD methods utilize this information and show the advantages over the Glasso and SCIO.

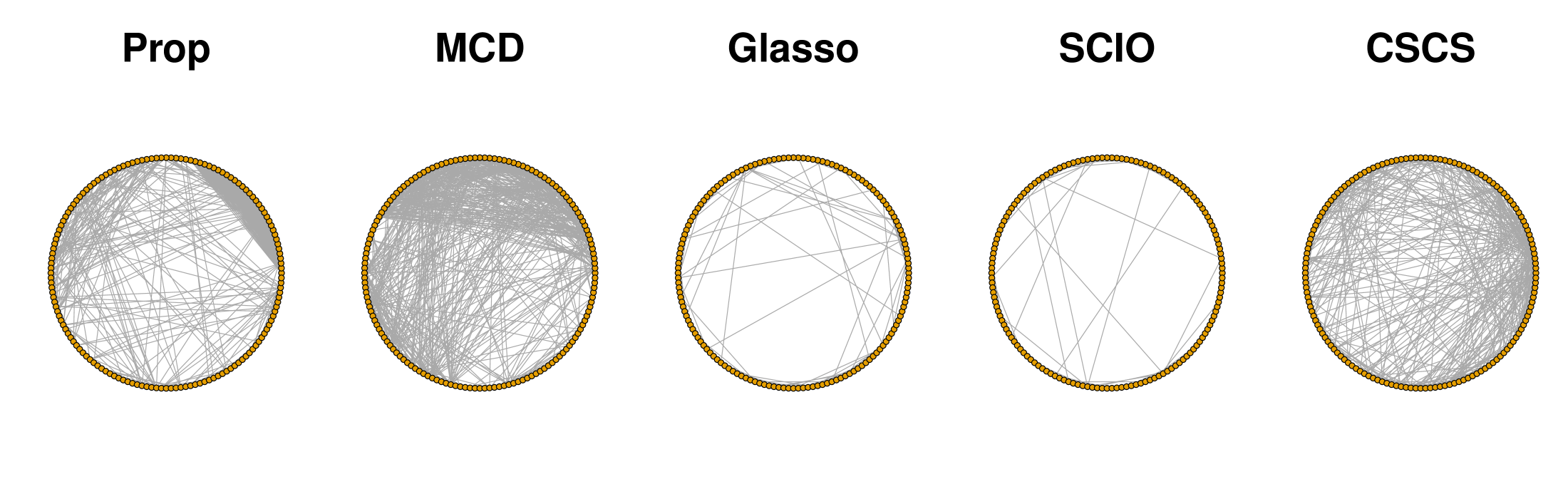

In addition, Figure 1 displays the estimated conditional dependency relationship between variables through network plots, which provide a further insight into the analysis results from the compared methods. It is seen that the CSCS and MCD methods yield an excessive amount of connections, which complicates the estimated model with difficult interpretation. While the graphs constructed from the Glasso and SCIO appear to give few connections, not providing sufficient information to infer the conditional dependency among variables. In contrast, the proposed model identifies a proper number of variable connections with certain sparsity. For a clear presentation, Figure 2 shows the estimated networks for the 60 consecutive variables, corresponding to the 5th week to 20th week. One would expect a meaningful network with nearby variables having some connections while the far-away variables having few connections. From Figure 2, it appears that the proposed model outperforms other methods, since the MCD method presents relatively too many connections of far-away variables, and the Glasso and SCIO provide too little information of dependency relationship between nearby variables. The CSCS displays a proper number of connections as the Prop method, while the Prop method seems to infer more connections of nearby variables, which is indicated by dense connections on the both upper right and bottom right of network plot constructed by the Prop method.

5.2 Call Center Data

In this section, we apply the proposed model to analyze the call center data from Huang et al. (2006). The data set was collected from one of call centers in a major U.S. northeastern financial organization. It recorded the time that every call arrives at the service queue from 7:00am until midnight in each day of 2002, except for 6 days when the data collecting equipment was out of order. The 17-hour period is divided into 102 10-minute intervals, and the number of calls during each time interval is counted. Since the arrival patterns of calls are different between weekdays and weekends, the analysis focuses on weekdays here. In addition, screening out some outliers that include holidays and days when the recording equipment was faulty, we are left with 239 observations.

Denote such data by , where is the number of calls received by the call center for the th 10-minute interval on day . Do the transformation to make the data distribution close to normal (Brown et al., 2005). We apply the compared methods to estimate the inverse covariance matrix. The 102 variables are partitioned into three groups with each group subsequently containing 30, 30 and 42 variables, corresponding to three time intervals of 7:00am - 12:00am, 12:00am - 5:00pm and 5:00pm - midnight. To compare the performance of different methods, we predict the number of arriving calls later in a day based on the arrival patterns at earlier times of that day. As in Section 5.1, we use notation , where and measure the arrival patterns in the early and later times of day . To examine the performance of the proposed model, the 239 observations are split into a training set which contains the first 205 data corresponding to dates from January to October, and a testing set with the rest 34 data corresponding to dates from November and December. The values of in the testing data are used to predict based on Equation (5.1). Two different settings of are considered as (A): and (B): . Setting A is used in Huang et al. (2006) and represents using the data from the early half of a day to predict the call numbers in the later half of the day. Setting B means using the data from the daytime to predict the call numbers in the evenings. For each time interval in , the APE is computed as

where is the predicted value, for setting A and for setting B.

| Setting | MCD | Glasso | SCIO | CSCS | Prop |

|---|---|---|---|---|---|

| A | 1.240 (0.052) | 1.258 (0.053) | 1.194 (0.063) | 1.152 (0.045) | 0.991 (0.031) |

| B | 1.159 (0.045) | 1.163 (0.044) | 1.083 (0.030) | 1.098 (0.039) | 1.023 (0.030) |

Table 4 shows the averages and corresponding standard errors of APE over from each compared method for Settings A and B. The proposed model generally gives superior performance over other methods with lowest values of APE. The SCIO appears to be comparable with the CSCS method, and they perform better than MCD and Glasso. The application results demonstrate the merits of the proposed model when data have partial information of the variable ordination.

6 Discussion

In this work, we propose a block Cholesky decomposition (BCD) method for inverse covariance estimation when the partial information of variable ordination is available. The proposed model adopts the MCD to induce the sparsity by imposing the regularization on the multivariate regressions. The proposed method provides a unified framework for several existing methods. including the MCD, the Glasso, and the estimators of Rothman et al. (2010a) and Witten et al. (2011). The theoretical results indicate that the proposed model enjoys a faster consistent rate than the Glasso if the data have the partial ordination among the variables.

There are several directions for future research. First, the objective function (2.2) is not jointly convex, hence the theoretical global minimizer is not guaranteed. A potential way to address this issue is to employ the classical Cholesky decomposition for the inverse covariance estimation (Yu and Bien, 2017; Khare et al., 2019), which leads to a convex optimization. However, the statistical interpretation of the classical Cholesky decomposition may not be as explicit as the MCD, where the Cholesky factor matrix can be constructed from regressions. It will be interesting to further investigate how to incorporate the partial information of variable ordering into the classical Cholesky decomposition. Second, the proposed method can be extended to investigate the multivariate response regression, where the multivariate response variables have certain ordering information, such as data with outcomes collected in a time sequence order. Third, the error bounds in Theorem 1 and Theorem 2 could be further improved. Note that and in Theorem 1 are generated on the path of Algorithm 1. When they are close to the underlying true parameters, several terms of in the proof could be close to 0, making a smaller constant term in the error bound.

References

- (1)

- Bai and Silverstein (2010) Bai, Z., and Silverstein, J. (2010), Spectral analysis of large dimensional random matrices Springer Series in Statistics. Springer, New York.

- Bickel and Levina (2008) Bickel, P. J., and Levina, E. (2008), “Regularized estimation of large covariance matrices,” The Annals of Statistics, 36(1), 199–227.

- Brown et al. (2005) Brown, L., Gans, N., Mandelbaum, A., Sakov, A., Shen, H., Zeltyn, S., and Zhao, L. (2005), “Statistical analysis of a telephone call center: A queueing-science perspective,” Journal of the American statistical association, 100(469), 36–50.

- Cai et al. (2011) Cai, T., Liu, W., and Luo, X. (2011), “A constrained minimization approach to sparse precision matrix estimation,” Journal of the American Statistical Association, 106(494), 594–607.

- Cai et al. (2016) Cai, T. T., Li, H., Liu, W., and Xie, J. (2016), “Joint estimation of multiple high-dimensional precision matrices,” Statistica Sinica, 26(2), 445.

- Chang and Tsay (2010) Chang, C., and Tsay, R. (2010), “Estimation of covariance matrix via the sparse Cholesky factor with Lasso,” Journal of Statistical Planning and Inference, 140, 3858–3873.

- Clemmensen et al. (2011) Clemmensen, L., Hastie, T., Witten, D., and Ersbøll, B. (2011), “Sparse discriminant analysis,” Technometrics, 53(4), 406–413.

- Dellaportas and Pourahmadi (2012) Dellaportas, P., and Pourahmadi, M. (2012), “Cholesky-GARCH models with applications to finance,” Statistics and Computing, 22(4), 849–855.

- Deng and Tsui (2013) Deng, X., and Tsui, K.-W. (2013), “Penalized covariance matrix estimation using a matrix-logarithm transformation,” Journal of Computational and Graphical Statistics, 22(2), 494–512.

- Friedman et al. (2008) Friedman, J., Hastie, T., and Tibshirani, R. (2008), “Sparse inverse covariance estimation with the graphical lasso,” Biostatistics, 9(3), 432–441.

- Gorski et al. (2007) Gorski, J., Pfeuffer, F., and Klamroth, K. (2007), “Biconvex sets and optimization with biconvex functions: a survey and extensions,” Mathematical methods of operations research, 66(3), 373–407.

- Huang et al. (2006) Huang, J. Z., Liu, N., Pourahmadi, M., and Liu, L. (2006), “Covariance matrix selection and estimation via penalised normal likelihood,” Biometrika, 93(1), 85–98.

- Jiang (2012) Jiang, X. (2012), “Joint estimation of covariance matrix via Cholesky Decomposition,” Ph.D Dissertation, Department of Statistics and Applied Probability, National University of Singapore.

- Kang and Deng (2020) Kang, X., and Deng, X. (2020), “An improved modified cholesky decomposition approach for precision matrix estimation,” Journal of Statistical Computation and Simulation, 90(3), 443–464.

- Kang and Deng (2021) Kang, X., and Deng, X. (2021), “On variable ordination of Cholesky-based estimation for a sparse covariance matrix,” Canadian Journal of Statistics, 49(2), 283–310.

- Kang and Wang (2021) Kang, X., and Wang, M. (2021), “Ensemble sparse estimation of covariance structure for exploring genetic disease data,” Computational Statistics and Data Analysis, 159, 107220.

- Khare et al. (2019) Khare, K., Oh, S.-Y., Rahman, S., and Rajaratnam, B. (2019), “A scalable sparse Cholesky based approach for learning high-dimensional covariance matrices in ordered data,” Machine Learning, 108(12), 2061–2086.

- Lam and Fan (2009) Lam, C., and Fan, J. (2009), “Sparsistency and rates of convergence in large covariance matrix estimation,” Annals of Statistics, 37(6B), 4254–4278.

- Liu and Wang (2017) Liu, H., and Wang, L. (2017), “Tiger: A tuning-insensitive approach for optimally estimating gaussian graphical models,” Electronic Journal of Statistics, 11(1), 241–294.

- Liu and Luo (2015) Liu, W., and Luo, X. (2015), “Fast and adaptive sparse precision matrix estimation in high dimensions,” Journal of multivariate analysis, 135, 153–162.

- Meinshausen and Bühlmann (2006) Meinshausen, N., and Bühlmann, P. (2006), “High-dimensional graphs and variable selection with the lasso,” Annals of statistics, 34(3), 1436–1462.

- Nino-Ruiz et al. (2019) Nino-Ruiz, E. D., Sandu, A., and Deng, X. (2019), “A parallel implementation of the ensemble Kalman filter based on modified Cholesky decomposition,” Journal of Computational Science, 36, 100654.

- Pourahmadi (1999) Pourahmadi, M. (1999), “Joint mean-covariance models with applications to longitudinal data: unconstrained parameterisation,” Biometrika, 86(3), 677–690.

- Rajaratnam and Salzman (2013) Rajaratnam, B., and Salzman, J. (2013), “Best permutation analysis,” Journal of Multivariate Analysis, 121(10), 193–223.

- Rothman et al. (2010a) Rothman, A. J., Levina, E., and Zhu, J. (2010a), “A new approach to Cholesky-based covariance regularization in high dimensions,” Biometrika, 97(3), 539–550.

- Rothman et al. (2010b) Rothman, A. J., Levina, E., and Zhu, J. (2010b), “Sparse multivariate regression with covariance estimation,” Journal of Computational and Graphical Statistics, 19(4), 947–962.

- Shi (2006) Shi, J. (2006), Stream of variation modeling and analysis for multistage manufacturing processes CRC press.

- Sofer et al. (2014) Sofer, T., Dicker, L., and Lin, X. (2014), “Variable selection for high dimensional multivariate outcomes,” Statistica Sinica, 24(4), 1633–1654.

- Tibshirani (1996) Tibshirani, R. (1996), “Regression shrinkage and selection via the lasso,” Journal of the Royal Statistical Society. Series B (Methodological), 58(1), 267–288.

- Van Wieringen (2019) Van Wieringen, W. N. (2019), “The generalized ridge estimator of the inverse covariance matrix,” Journal of Computational and Graphical Statistics, 28(4), 932–942.

- Wagaman and Levina (2009) Wagaman, A. S., and Levina, E. (2009), “Discovering sparse covariance structures with the Isomap,” Journal of Computational and Graphical Statistics, 18(3), 551–572.

- Wang et al. (2015) Wang, C., Pan, G., Tong, T., and Zhu, L. (2015), “Shrinkage estimation of large dimensional precision matrix using random matrix theory,” Statistica Sinica, 25, 993–1008.

- Wang et al. (2020) Wang, L., Chen, Z., Wang, C. D., and Li, R. (2020), “Ultrahigh dimensional precision matrix estimation via refitted cross validation,” Journal of Econometrics, 215(1), 118–130.

- Witten et al. (2011) Witten, D. M., Friedman, J. H., and Simon, N. (2011), “New insights and faster computations for the graphical Lasso,” Journal of Computational and Graphical Statistics, 20(4), 892–900.

- Xue et al. (2012) Xue, L., Zou, H. et al. (2012), “Regularized rank-based estimation of high-dimensional nonparanormal graphical models,” The Annals of Statistics, 40(5), 2541–2571.

- Yu and Bien (2017) Yu, G., and Bien, J. (2017), “Learning local dependence in ordered data,” The Journal of Machine Learning Research, 18(1), 1354–1413.

- Yuan (2010) Yuan, M. (2010), “High dimensional inverse covariance matrix estimation via linear programming,” The Journal of Machine Learning Research, 11, 2261–2286.

- Yuan and Lin (2007) Yuan, M., and Lin, Y. (2007), “Model selection and estimation in the Gaussian graphical model,” Biometrika, 94(1), 19–35.

Appendix

In this section, we provide all the technical proofs for the main results of the paper. Before proving theorems, we present several lemmas.

Lemma 1.

Denote a squared block diagonal matrix by . Suppose have eigenvalues , then the eigenvalues of matrix are .

Proof.

Let be the eigenvalue decomposition, where , and is composed of the corresponding eigenvectors. Define and . Then we have

which indicates , and establishes the lemma. ∎

Lemma 1 describes a property of eigenvalues for the block diagonal matrix. The following Lemma 2 is from Theorem A.10 in Bai and Silverstein (2010). It demonstrates the property of matrix singular values. Its result is stated here for completeness.

Lemma 2.

Let and be two matrices of order and . For any , we have

Based on the results of Lemmas 1 and 2, we present the following Lemma 3, which provides a relationship between matrix and its block Cholesky factor matrices () in terms of their singular values.

Lemma 3.

Let be the block MCD of the inverse covariance matrix. If the condition (3.1) is satisfied, that is, there exists a constant such that , then there exist constants and such that

and

Proof.

By the decomposition (2.1), we partition into blocks according to the variable groups such that its diagonal blocks are of order , and . Write , where

with . Note that is a symmetric matrix due to the symmetry of . In addition, it is obvious to have , implying that is semi-positive definite. Consequently we have

| (6.1) |

Taking determinant on both sides of yields

By for each via (6.1), together with Lemma 1, it is easy to see . We hence have

which gives . As a result,

To bound singular values of matrix , on one hand, we use Lemma 2 to obtain , indicating

On the other hand, applying Lemma 2 again for yields , implying

As a result,

Taking and establishes the lemma. ∎

It is seen from Lemma 3 that the singular values of the matrices and are bounded if the singular values of the inverse covariance matrix are bounded. Now we give the proofs of Theorems.

Proof.

Proof of Theorem 1.

From the negative log-likelihood (2.4), we have

By the notation , it is easy to see

where . Consequently, can be written as

where and are the th elements of matrices and , respectively.

For part (a), we define . Let for , where are positive constants. We will show that for , probability is tending to 1 as for sufficiently large , where are the boundaries of . Additionally, since when , the minimum point of is achieved when . That is .

Assume . Write , then we decompose as

where

The above decomposition of into to is very similar to that in the proof of Lemma 3 of Kang and Deng (2021); hence it is omitted here. Now we bound each component respectively. Note that . Therefore, based on the proof of Theorem 3.1 in Jiang (2012), for any , there exists a constant such that with probability greater than , we have

where is a positive constant satisfying . Next, for the penalty term corresponding to ,

where , and

Combine all the terms above together, with probability greater than , we have

Here is only related to the sample size and . Assume where , and choose , then . Therefore, we prove .

The proof of part (b) follows the same principle as that for part (a). Similarly, define . Let for , where are positive constants. We only need to show that for , probability is tending to 1 as for sufficiently large , where are the boundaries of .

Assume . Write , then we decompose as

where

The above decomposition of into to is similar to that in the proof of Lemma 3 of Kang and Deng (2021). Next we bound each component respectively. Note that . Therefore, based on the proof of Theorem 3.1 in Jiang (2012) together with Lemma 3, we can have the following two results (I) and (II).

(I) Let be a positive constant satisfying , and note that , then

(II) For any , there exists a constant such that with probability greater than , we have

where is the th element of matrix , and the second inequality applies Lemma 3 of Lam and Fan (2009).

Next, we decompose , where , and

Combine all the terms above together, with probability greater than , we have

Here is only related to the sample size and . Assume where , and choose , then . Therefore, we prove . ∎

Proof.

Proof of Theorem 2.

Let and be the estimates obtained from Step 3 in Algorithm 1. We first prove the consistent rates under Frobenius norm of and are and , respectively.

At the first iteration of Step 1 in Algorithm 1, the estimate found by minimizing is consistent according to part (a) of Theorem 1. In Step 2, the estimate found by minimizing is consistent according to part (b) of Theorem 1. Next, an estimate obtained by minimizing is consistent, and which minimizes is consistent. Following this, we hence have that (or equivalently ) and are and consistent. This implies

and

Next, we derive of consistent rate of the estimate . Let and , then we decompose as

Now we bound four terms separately. Use the symbol to represent the spectral norm of matrix . Since and by Lemma 3, it is obvious that . In addition, the single values of are bounded since the single values of are bounded, which together with Lemma 3 leads to , hence similarly . As a result, it is easy to obtain

and the second term . For the third term,

For the fourth term,

Consequently, by the convergence rates of and from Theorem 1, we reach the conclusion

∎