Information Geometry and Asymptotics for Kronecker Covariances

Abstract

We explore the information geometry and asymptotic behaviour of estimators for Kronecker-structured covariances, in both growing- and growing- scenarios, with a focus towards examining the quadratic form or partial trace estimator proposed by Linton and Tang [26]. It is shown that the partial trace estimator is asymptotically inefficient An explanation for this inefficiency is that the partial trace estimator does not scale sub-blocks of the sample covariance matrix optimally. To correct for this, an asymptotically efficient, rescaled partial trace estimator is proposed. Motivated by this rescaling, we introduce an orthogonal parameterization for the set of Kronecker covariances. High-dimensional consistency results using the partial trace estimator are obtained that demonstrate a blessing of dimensionality. In settings where an array has at least order three, it is shown that as the array dimensions jointly increase, it is possible to consistently estimate the Kronecker covariance matrix, even when the sample size is one.

Keywords: exponential family; Fisher information metric; high-dimensional; Kronecker product; orthogonal parameterization; partial trace; tensor.

1 Introduction

An order- tensor, or synonymously, an array with a -tuple of indices, , is a collection of numbers where the index ranges from to for each [22]. Vectors and matrices give familiar examples of order one and order two arrays respectively. Each index set is referred to as a mode of the tensor, where the dimension of mode is defined as . In data analysis settings the th mode can be interpreted as a factor with different levels. An observation of a random tensor is tantamount to obtaining real-valued measurements at every -way combination of factors. For instance, the international trade data examined in Section 8, consists of an order-3 tensor , representing the trade from country to country at time [19]. Some other examples of tensor-valued data include microarray data [1], financial time-series [6], fMRI data [33], and MIMO communication signals [8].

In this work we study a covariance matrix estimation problem for tensor data. As the number of entries of a tensor is , the covariance matrix of any vectorization of is -dimensional. When the order of the tensor or the dimension of the modes are large, a substantial number of parameters have to be estimated, leading to unstable estimates of the covariance matrix. Alternatively, restrictions can be placed on the hypothesized covariance structure for which more stable estimators are available, assuming that the restricted covariance submodel is approximately valid. The Kronecker covariance structure is one such restriction that leverages the tensor structure of , and describes the influence of each of the index-factors on the covariance of in an interpretable manner [9].

A random tensor is defined to have the Kronecker covariance matrix when

| (1) |

and each is in the set is a of non-singular, dimensional, positive-definite matrices. The notation

| (2) |

denotes the set of Kronecker-structured covariance matrices. The number of parameters needed to define a Kronecker covariance is on the order of , a number that is typically much smaller than the order parameters needed to defined a covariance matrix with no constraints.

An interpretation of the Kronecker factors is that the covariance along mode is proportional to . Fixing all modes but mode , equation (1) implies the proportionality equation

| (3) |

When and is a random matrix, the content of equation (3) is that the covariance of every row of is proportional to and the covariance of every column is proportional to . Kronecker covariance structures arise naturally through matrix, and more generally multilinear, multiplication. If is a matrix with i.i.d. standard normal entries then has the Kronecker covariance matrix . It should be noted that alternative notation is commonly used, where the covariance of is denoted by instead of . This distinction amounts to vectorizing a matrix row-wise for or column-wise for . To remain consistent with the definition (1), where represents the covariance of mode , we use the notation .

Formalizing the scenario we consider throughout this work, let be independent observations of tensors that each have the Kronecker covariance , defined by (1). Equivalently, can also be reduced to the sample covariance matrix sufficient statistic, . We consider to be indexed as a -dimensional array where

and thus

| (4) |

Asymptotic properties of various estimators for are analyzed in this article. A wide variety of asymptotic regimes are relevant for tensor data, as the numbers , and can all be adjusted. Previous work on the efficiency of estimators for Kronecker covariances can be found in [37]. In [14] it is shown that the effective sample size of partial trace estimates of correlation matrices in a setting is small when there is strong between-row or between-column correlation. Our approach emphasizes geometric aspects of efficiency that lend additional insights into the behaviour of the partial trace estimator. Specifically, we show how the dispersion of the eigenvalues of the Kronecker factors impacts the asymptotic performance of the partial trace estimator. Prior work on high-dimensional sampling properties of the MLE and the partial estimator that we build upon are provided in [36, 26].

In the first portion of this work we explore large and fixed asymptotics. To aid comprehension, these results are formulated primarily for order-two arrays. Order- generalizations follow in a straightforward manner. Section 2 begins by describing the information geometry of the Kronecker submodel, contained in the full, Wishart exponential family. Two important estimators for Kronecker covariances, the maximum likelihood estimator and the partial trace estimator, are characterized in Section 3. An analysis of the level sets of these estimators given in Section 4 shows that the partial trace estimator is asymptotically inefficient, except at the identity matrix. A rescaled version of the partial trace estimator is proposed and shown to be asymptotically efficient. Motivated by the rescaled partial trace estimator, an orthogonal parameterization for Kronecker covariances is introduced in Section 6, where we describe the implications of this parameterization to testing problems. In Section 7 a fixed and growing asymptotic regime is analyzed. We establish mild conditions on and the eigenvalues of for which the partial trace estimator is consistent in relative Frobenius norm. A simulation study and a high-dimensional data example that support our theoretical results appear in the last section.

2 Wishart Fisher Information Geometry

In this section we introduce the relevant Fisher information geometry of the Wishart model that will be used to contrast the asymptotic performance of estimators for Kronecker covariance matrices. Given a regular, parametric model , the Fisher information matrix at the distribution is the positive definite matrix with entries

| (5) |

where is the log-likelihood function of , and is the partial derivative with respect to the th component of . The matrix (5) has direct statistical implications in that is the asymptotic variance matrix of an optimal, asymptotically efficient estimator of .

Rather than deal with directly, it can be more convenient to work with the quadratic form associated with this matrix. An inner product over can be defined according to the rule

| (6) |

which is referred to as the Fisher information metric (FIM) at [2]. The Fisher information metric gives the parameter space the geometric structure of a Riemannian manifold where the FIM is a Riemannian metric [25]. More generally, a Riemannian metric over a manifold is a collection of smoothly varying inner products, where is an inner product over the tangent space at the point . The tangent space can be viewed as the affine plane that intersects the surface tangentially at . Tangent spaces are especially simple when is an open set in , as the approximating tangent plane is all of . This is the case for the FIM on a regular parametric model, where is assumed to be open in . Further information on tangent spaces and differential geometry can be found in [24, 25].

The unconstrained Wishart model is a regular exponential family [4] that can be parameterized by the mean parameter . The set can be viewed as an open set in the -dimensional vector space of dimensional symmetric matrices. The vector space has the standard inner product

| (7) |

Applying the above Fisher information construction to in mean parameterization, the FIM can be succinctly represented [34] as

| (8) |

As is an open set contained in , the tangent space at the point can be identified with itself. The Riemannian metric (8), also referred to as the affine-invariant Riemannian metric (AIRM), gives the structure of a complete Riemannian manifold [23, Ch 12].

Affine-invariance refers to the invariance of the AIM with respect to the congruence group action of the general linear group of invertible matrices on . This transitive action preserves the metric, as it is easily checked that

| (9) |

From a statistical perspective, this invariance is a result of the Wishart model being a group transformation family under . Specifically, if then . The existence of this transitive group action simplifies many arguments, as a statement typically only has to be shown at a single, conveniently chosen, .

The relationship between the FIM and the asymptotic variance matrix for asymptotically efficient estimators takes an especially simple form for sufficient statistics and mean parameters in regular exponential families. Projecting the sufficient statistic onto the one-dimensional subspaces determined by , the covariance of these projections is given by

| (10) |

Formula (10) is a restatement of the fact that the variance of the sufficient statistic in an exponential family is equal to the Fisher information matrix with respect to the corresponding canonical parameter [2]. See Lemma 0.1 in the Appendix for a proof.

2.1 Kronecker Fisher Information Geometry

We define the Kronecker submodel of . Formally, is a curved exponential family that can be parameterized by the submanifold contained in [21, Sec 2.3]. That has a manifold structure follows from the map , where , are matrices with trace and . This map gives a global parameterization of in terms of a product of relatively open [31, Sec 6] sets in Euclidean space. As the dimension of the set of matrices in with trace is , the dimension of as a manifold is .

The tangent plane at in is more complicated than , since the former tangent plane to the surface depends on . The subspace can be found by computing all possible derivatives of smooth curves passing through at . By the product rule

| (11) |

where and are symmetric matrices. As a subspace of , the tangent space is the vector space

| (12) |

The submodel of inherits the same Fisher information metric (8) as , restricted to the tangent space (12).

The collection of Kronecker covariances also has a natural group action on it that results from restricting the congruence action defined previously. Let denote the subgroup of Kronecker products of non-singular matrices, . The group acts transitively on according to the map:

Each such congruence transformation preserves the FIM by (9). A related subgroup of consisting of tensor products of orthogonal matrices is . The significance of is that any Kronecker covariance can be diagonalized by orthogonal matrices in this group.

3 Estimators for Kronecker Covariances

3.1 The Partial Trace Estimator

Moving to the problem of estimating , given an observation , Linton and Tang introduce an estimator for in [26], that they call the quadratic form estimator. The estimator can be motivated by the observation that (4) implies

| (13) |

Consequently, by summing over certain blocks of the sample covariance matrix it is possible to construct an estimator with expectation that is proportional to . Assuming that is the sample covariance of the i.i.d. Gaussian matrices , the summation in (13) can be viewed as summing the sample covariance matrix of each row of the matrices. In [14] Efron examined drawbacks of using estimates for the correlation matrices of the Kronecker factors that are effectively based on partial traces.

Generalizing this block-summation, the partial trace operators and are defined by

| (14) |

The notation we have chosen for the partial trace estimator emphasizes that the image of is in . Alternative notation lets the index in denote the mode(s) over which the summation is performed.

Partial trace operators can be defined similarly in the tensor case by where and by

| (15) |

Mathematically, if each mode corresponds to the -dimensional vector space , the matrix can be viewed as a linear operator , where is the dual space of . The partial trace operator is equal to contracting, or equivalently taking the trace, of every pair except for the th pair. See the Appendix for additional details.

The quadratic form estimator of , which we refer to as the partial trace (PT) estimator, is defined in terms of these partial traces as

| (16) |

Each Kronecker factor in can be viewed as estimating up to scale, while the multiplicative factor rescales to have the same trace as . The partial trace estimator not only preserves the trace of , but it has the stronger property of being the unique function into that preserves the partial traces of . Thus, . By the linearity of the partial trace operator, is partial trace unbiased, in the sense that .

The PT estimator has intuitive appeal as it can be understood as aggregating the sample covariance matrix for every mode of an array and then taking the Kronecker product of the resulting sample covariance aggregates. It is also trivial to compute and it exists with probability one for any sample size . However, it will be shown in subsequent sections that the PT estimator is asymptotically inefficient and performs poorly near the boundary of the cone .

3.2 The Kronecker MLE

The Kronecker maximum likelihood estimator (MLE) is the solution to the following likelihood equations

| (17) | ||||

| (18) |

These equations state the average partial traces of the decorrelated sample covariance matrix equal the identity matrix. Using the equivariance and cyclic permutation properties of the partial trace operator provided in Lemmas 0.2 and 0.3 in the Appendix, equivalent likelihood equations are

| (19) | ||||

| (20) |

While there is no general closed form expression for , a block-coordinate descent algorithm that initializes at an arbitrary matrix, such as , and iterates between the equations (19) and (20) can be used to find the MLE [12]. Conditions on the sample size for which the MLE exists, is non-singular, and is unique with probability one are explored in [11, 10], with a simple sufficient condition being [10]. By taking the Kronecker structure into account, this sample size requirement is much less stringent than the requirement needed for the sample covariance matrix to be non-singular with probability one.

4 Inefficiency of the Partial Trace Estimator

While the partial trace estimator is simple to compute and analyze, it is shown in this section that it is inefficient, having a larger asymptotic variance than the MLE. The key result that simplifies this analysis is that asymptotic efficiency, or lack thereof, can be appraised by an orthogonality property between subspaces with respect to the Fisher information metric. We begin by providing explicit expressions for these subspaces for both the MLE and PT estimators in Lemma 1. In Theorem 1 the asymptotic variance of the partial trace estimator is related to a principle angle between subspaces, where this angle is shown to be related to the eigenstructure of in Lemma 3.

The first relevant tangent subspace, the tangent space to the auxiliary space, is one that is associated with a given estimator, and it determines whether or not an estimator is efficient. Any estimator of a Kronecker covariance maps a sample covariance matrix to the Kronecker covariance . Conversely, for each the set of sample covariance matrices that get mapped to is defined as the the auxiliary space of at [2, Ch 4]. That is, this auxiliary space is the level set

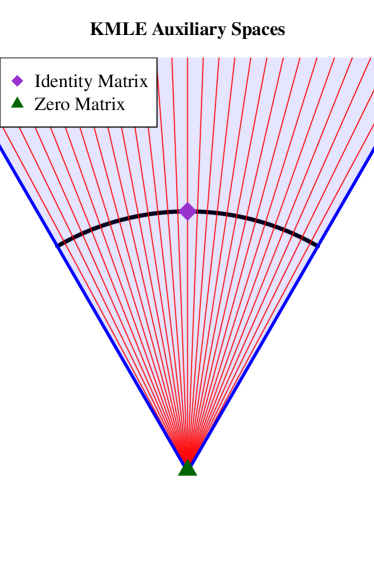

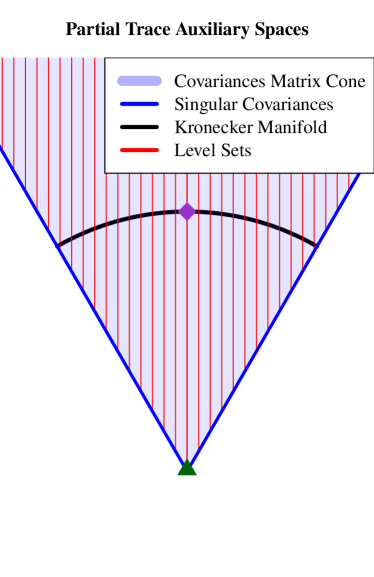

The auxiliary space at is a possibly curved surface that passes through . If is sufficiently smooth, the tangent space to at the point is a subspace contained in the tangent space . The tangent space to the Kronecker submanifold is also a subspace of . The orthogonality result states that an estimator is asymptotically efficient if and only if is orthogonal to with respect to the FIM [2, Thm 4.3]. A more precise formulation is given in Theorem 1 below. First, we summarize the simple, affine structure of the auxiliary spaces of and . See Figure 1 for an illustration of these auxiliary spaces. We remark that this low-dimensional representation of does not capture its cone structure, where for any and .‘

Lemma 1.

Both and are the intersection of affine subspaces in with the mean parameter space of the exponential family . These auxiliary spaces are defined by the equations

with associated tangent subspaces

At any positive multiple of the identity . The orthogonality condition necessary for asymptotic efficiency holds at all for the MLE, but only holds at the matrices that are proportional to the identity matrix for the partial trace estimator.

The auxiliary tangent spaces of and are both defined in terms of partial traces, with the distinction between these spaces being the decorrelation operation that appears in the the MLE auxiliary tangent space. As the subspaces are identical as varies, the auxiliary spaces are all parallel in .

Lemma 1 shows that is asymptotically inefficient, but it does not provide any indication of where performs poorly. Intuitively, the degree to which orthogonality between the auxiliary and Kronecker tangent spaces is violated corresponds to the degradation of the asymptotic performance of . Figure 1 suggests that since the parallel, PT auxiliary spaces do not account for the bending of the Kronecker submanifold, the asymptotic performance of is the poorest near the boundary of . The following theorem generalizes Theorem 2.6.8 in [21] and relates the relative, worst-case asymptotic variance of the partial trace estimator to the degree that orthogonality is violated, as summarized by a principle angle:

Theorem 1.

Let be the smallest principle angle between and with respect to the mean space inner product (8). Then

| (21) |

where , and is the asymptotic variance of the associated limiting normal distribution.

This theorem expresses the asymptotic variance ratio of the PT and the MLE estimators, projected onto the one-dimensional line determined by , in terms of a principle angle. As is asymptotically efficient, regardless of , the projected asymptotic variance ratio will always be bounded below by one. Further insight into the variance ratio (21) can be obtained by bounding the principle angle above. Equivariance considerations show that this principle angle only depends on the eigenvalues of :

Lemma 2.

The functions, and are and equivariant respectively, implying that the auxiliary spaces are equivariant while the spaces are equivariant:

In particular, if has the eigendecomposition , all of the principle angles between and with respect to are identical to the principle angles between and with respect to .

Maximizing the inner product between vectors in the auxiliary and Kronecker tangent spaces gives the following bound on the asymptotic variance ratio:

Lemma 3.

Denote the eigenvalues of and by and respectively. The maximal asymptotic variance ratio of the partial trace estimator is bounded below, as follow

| (22) |

If and are the angles between and then the lower bound (22) can be written as

| (23) |

The bound (23) confirms the geometric intuition garnered from Figure 1 that the PT estimator performs poorly near the boundary of . Specifically, the angles and are large when the eigenvalues of and are widely dispersed, and are small when these eigenvalues are all nearly identical. When is proportional to , the lower bound in (22) is as is efficient in this case. This qualitative behaviour is consistent with Theorem 2 of [14], where it is shown that the effective sample size of estimators of Kronecker correlation matrix factors is reduced when there is significant across-row or across-column correlation.

The largest possible limiting angle between a vector of positive eigenvalues and the vector occurs when the vector of eigenvalues approaches any standard basis vector. Consequently, the lower bound (22) is maximized in the limit when , , and . The limiting value of the lower bound, as converges to zero, is

| (24) |

The implication of (24) is that in high-dimensional settings the PT estimator can perform much worse than the MLE, possibly having an asymptotic variance along a particular direction that is times larger. In the next section we provide an interpretation for why this is the case and how the PT estimator can be modified to obtain an asymptotically efficient estimator.

5 An Efficient Rescaled Partial Trace Estimator

Consider the setting where and is large. The partial trace operator is a sum of matrix-blocks that are roughly equal to

For small values of , the value of the partial trace is dominated by the first term in the sum with

Due to the discrepancy of the magnitudes of the terms in the partial trace sum, the PT trace estimator effectively discards the terms that have a negligible impact on the sum. This explains why the worst-case performance of the PT estimator compared to the MLE deteriorates as grows, as shown by equation (24). As evidenced by the efficiency of at scalar multiples of the identity, this scaling issue disappears when . To correct for this scaling imbalance, we introduce a rescaled version of the partial trace operator.

Definition 1.

The determinant-rescaled partial trace operators are defined as

| (25) |

The rescaled partial trace estimator is defined in terms of the determinant-rescaled partial trace operators by

| (26) |

Each operator is a sum of matrices with unit determinant. The reason for rescaling by determinants rather than a different scale-equivariant function, such as the trace, is that the determinant is a homomorphism from to the multiplicative group of real numbers. This equivariance ensures that the rescaled partial trace estimator is equivariant.

Theorem 2.

The function is equivariant. If , the estimator is asymptotically efficient.

Similar to the PT estimator matching partial traces, the multiplicative factor appearing in (26) is chosen so that has the same determinant as . Compared to the MLE, the RPT estimator has the benefit of having a closed form expression.

It is helpful to rewrite equation (26) as

| (27) |

This formulation makes clear that is composed of the scaling factor , and the Kronecker factors that each have determinant one. The RPT estimator is non-singular with probability one only when and thus . While this is a restrictive sample size requirement, the determinant-one Kronecker factors, which are of primary interest, exist as long as .

6 Asymptotic Distribution Using an Orthogonal Parameterization

In this section we explore an orthogonal parameterization of , motivated by the factors in (27). The orthogonality of this parameterization implies the asymptotic independence of certain estimates of the Kronecker factors, modulo scaling. Moreover, the asymptotic distribution of efficient estimates of the Kronecker factors is shown to behave like a Wishart distribution. As an application, we demonstrate how these properties simplify hypothesis tests for structured Kronecker factors.

The individual factors in and in the Kronecker product are only identifiable up to scale as for . It is possible to decompose into an overall scale factor, along with the scale-invariant remnants of the Kronecker factors. Using the determinant as a measure of scale, we obtain a decomposition

| (28) |

that was previously used in [16, 15]. Letting denote the collection of positive definite matrices with determinant one, which can be viewed as a projective space over the cone , the decomposition (28) induces a bijective map .

Alternative decompositions, such as dividing each by are possible; however, (28) has the useful property of providing an orthogonal parameterization [7] of . Moreover, this parameterization inherits an equivariance property, detailed in Lemma 0.6 in the Appendix, with respect to the product group of real numbers under addition and the special linear group under matrix multiplication.

Theorem 3.

The map , with defined as is a bijection that is an orthogonal parameterization. The Riemannian metric on the Cartesian product induced from the FIM on is a product metric, where has the standard Euclidean metric scaled by a factor of and each is equipped with the restriction of the FIM (8) on scaled by a factor of , .

Restricting our attention to the first two components in the orthogonal parameterization, the Kronecker FIM is seen to be the same as the FIM from a related Wishart model:

Corollary 1.

The map , with defined as is an orthogonal parameterization of the Wishart model . The FIM induced on by and equals the FIM induced on by the Kronecker model . Equivalently, the block of the Fisher information matrix corresponding to is the same in both and . An analogous statement holds for the component of .

An implication of this result is that the asymptotic variance of an efficient estimator of in the Kronecker model where is parameterized to have determinant one, is the same as that in a Wishart model with more observations. The dimension of the second mode in the Kronecker model acts as a sample size multiplier when estimating . This sample size amplification is explicit in the expression for the partial trace estimator, as sums over matrix blocks. In the next section we explore this phenomena further in the context of large- asymptotics.

In terms of the Fisher information matrix, parameter orthogonality amounts to the matrix being block diagonal. Although we do not investigate this here, orthogonality can be useful for Newton-Raphson or Fisher-scoring algorithms where the information matrix only has to be inverted block-wise [30, 7]. As the inverse of the Fisher information matrix is the asymptotic variance matrix for an asymptotically efficient estimator, orthogonality also implies an asymptotic independence property:

Corollary 2.

As , the components of , namely

are asymptotically independent. Similarly, the components of are asymptotically independent.

An application of this asymptotic independence is to hypothesis testing problems concerning the Kronecker factors. In many instances it is hypothesized that the Kronecker factors and are structured covariance matrices, such an autoregressive covariance, a graphical model, an exchangeable covariance, or an isotropic covariance [17, 32, 35, 36]. Specifically, let and define the hypotheses , . Further, assume that the subset is cone, implying that if then so is for . The majority of relevant hypotheses, including all of those listed above and hypotheses that can be specified using only correlation matrices, satisfy this scale-invariance assumption. The asymptotic independence of efficient estimates can be used to test the intersection hypothesis , and asymptotically control the Type I error rate:

Lemma 4.

Assume that is a smooth, scale-invariant test statistic for the hypothesis in the model , , , with and independent. Further assume that converges weakly to a non-degenerate distribution that does not depend on under . Let be the intersection hypothesis with respect to the model . The asymptotic distribution of the test statistics

| (29) |

equal the asymptotic distribution of

| (30) |

In particular, if is an asymptotic level- quantile of , the test that rejects when for either or has asymptotic level . Similar statements apply, by replacing all occurrences of above with the Kronecker MLE factors .

To illustrate Lemma 4, we test the hypotheses that is spherical and that follows a compound symmetry model given an observation . We use the test statistics where the are the respective Kronecker factors of the MLE, is a pivotal test statistic based on the affine-invariant distance, and is the likelihood ratio test statistic. Additional details regarding these tests are provided in Appendix B. The contingency Table 1 records the observed joint proportion of rejections of and , computed from Monte Carlo samples. Also provided in Table 1 are the fitted expected proportions of rejection if and were independent. As dictated by Lemma 4, it is seen that for large sample sizes the hypotheses and are approximately rejected independently. Even when is only independence approximately holds.

| Null | Alternative | |||||

| No Reject | Reject | No Reject | Reject | |||

| No Reject | 0.818 (0.814) | 0.106 (0.109) | 0.789 (0.786) | 0.132 (0.135) | ||

| Reject | 0.064 (0.067) | 0.012 (0.009) | 0.064 (0.068) | 0.015 (0.012) | ||

| No Reject | 0.887 (0.888) | 0.059 (0.058) | 0.657 (0.652) | 0.209 (0.215) | ||

| Reject | 0.051 (0.051) | 0.003 (0.003) | 0.095 (0.100) | 0.039 (0.033) | ||

| No Reject | 0.896 (0.896) | 0.049 (0.050) | 0.119 (0.116) | 0.399 (0.402) | ||

| Reject | 0.051 (0.051) | 0.003 (0.003) | 0.105 (0.108) | 0.377 (0.374) | ||

Operationally, Lemma 4 can be used to simplify testing procedures for the hypothesis . A likelihood ratio test of requires that the MLE under be computed. This can be computationally expensive as it involves iterating a block-coordinate descent algorithm, where at each step a constrained estimate of under is found. Lemma 4 shows that when is sufficiently large, it is enough to compute , or any other asymptotically efficient estimator of , and apply tests developed for the Wishart distribution to each estimated Kronecker factor.

7 Large- Asymptotics: A Blessing of Dimensionality

The columns of the random matrix each follow the normal distribution . As increases, it is conceivable that up to scaling, the variability of estimates of decreases. In the special case that this intuition exactly holds since , . While may be easier to estimate as grows, there is a tradeoff in the Kronecker model as concomitantly the dimension of increases. In this section we provide convergence rates of the partial trace estimator as the dimensions grow. For matrix data, the effects of simultaneously increasing and cancel out with each other, and the Kronecker estimation problem in high-dimensions is no more difficult than in low-dimensions. Even more surprising is that for tensor-valued data, it becomes easier to estimate a Kronecker covariance in high-dimensional settings, with the estimator converging in relative Frobenius norm to the underlying Kronecker covariance as the s jointly increase.

In this section it is assumed that , is -dimensional, and is the dimension of . The partial trace estimator is extended to the tensor setting by defining

| (31) |

with the partial trace operators given by (15). The scale factor ensures that .

Our central asymptotic result is the following:

Theorem 4.

Let with and . Denote by , take to be the length vector of eigenvalues of , and let to be the length vector of eigenvalues of . If

| (32) |

then

| (33) |

Related convergence results in the matrix case for block-coordinate descent iterates of the MLE can be found in Theorem 2 of [36]. As compared to the theorem in [36] Theorem 4, although applied to a more tractable estimator, has advantages in that it gives a faster convergence rate by a factor of , does not require any constraints on the sample size, and does not require a uniform bound on the spectrum of . We note that the proof of Theorem 4 can be extended beyond the normal-Wishart family, to sample covariance matrices obtained from elliptically symmetric distributions with finite fourth-order moments.

The angle between and the vector of all ones appears in (33), where related angles were encountered previously in Lemma 3. This angle effectively replaces uniform spectral bounds. It is worth examining what kind of eigenvalue behaviour results in being bounded asymptotically. The following lemma shows that is finite under the mild condition that the eigenvalues grow at a polynomial rate.

Lemma 5.

Let be a non-zero polynomial with non-negative coefficients . If , then as . If , grows exponentially then as . Lastly, if has a spiked eigenvalue structure with entries that equal , entries that equal , and , then

where . This expression is if or .

Under the assumption that , and for all , Theorem 4 shows that in the matrix case converges to in relative Frobenius norm at a rate of

Consequently, a sufficient condition for relative Frobenius norm consistency in the matrix setting under these conditions is . For higher-order tensors, we obtain the following consistency result that holds even when the sample size is only one:

Corollary 3.

A consequence of this corollary is that, even though the dimension of the parameter space is growing, it actually becomes easier to estimate in high-dimensions. In the setting, there are “pseudo”-sample vectors that can be used to estimate . The intuition is that as long as is large enough, can be estimated consistently in relative Frobenius norm. This consistency result is possible because the Kronecker covariance assumption is a strong assumption, especially in high-dimensions where the dimension of the parameter space is reduced from to .

8 Simulation Study and Data Example

In this last section we provide an empirical assessment of the performance of the PT estimator, and compare it to the performance of the MLE in different settings. We also apply the PT estimator to a high-dimensional data set that only contains a single observation (). Despite this sample size limitation, the PT estimator is seen to produce plausible estimates for an underlying Kronecker covariance structure.

8.1 International Trade Data

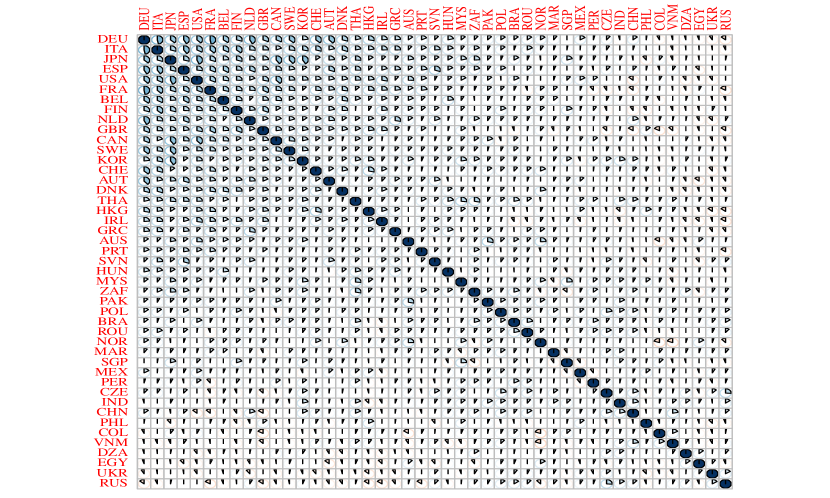

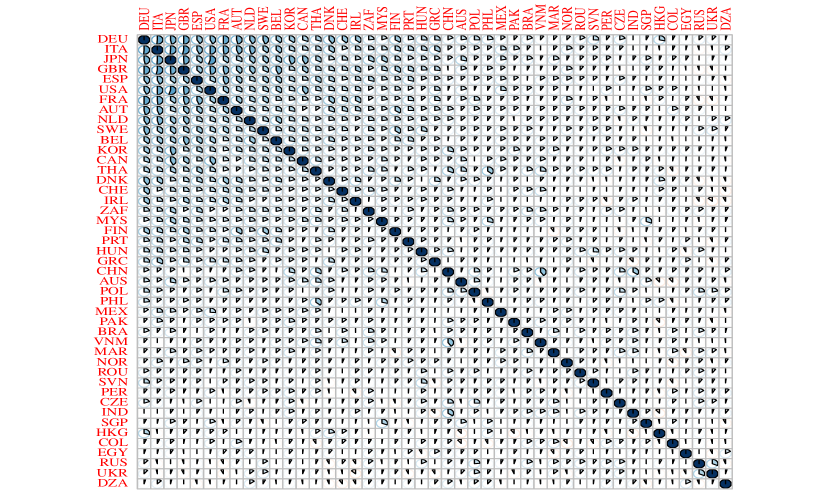

The UN Comtrade database contains information about the amount, in US dollars, of pairwise imports and exports between 229 countries across 9 different commodity types [19]. We demonstrate in this section how the partial trace estimator can be applied to a subset of the high-dimensional UN Comtrade data. These data are high-dimensional in the sense that the sample size is significantly smaller than the dimension of the observed tensor. Let be the order-3 tensor with entries that equal the sum of the total quantity of trade, aggregated over all commodity types, exported from country to country in year . Both countries and report the quantity of exports and imports respectively. These possibly differing reports are averaged when constructing . As some country pairings report no trade, a subset of 45 of the largest countries by trade, that all have non-zero pairwise imports and exports, is selected. The tensor is dimensional, with missing values along the country country diagonal . Although a measure, such as the GDP for country in year , could be imputed for , the other entries of are sufficiently distinct quantities that we opt to analyze the array without this imputation.

Letting , it is postulated that the tensor is distributed according to the following autoregressive model on the log-scale:

| (34) | ||||

According to this model, the log-trade between countries and at time is equal to the trade in the previous year plus a noise term and a constant , that captures the state of the global economy in year . The noise is assumed to have a Kronecker covariance structure that reflects the correlation between the import and export behaviour across countries. For example, the import and export behaviour of countries that are signatories on a multilateral trade agreement may be similar. The baseline trade values at , the magnitude of which differs greatly across country pairings, will not be analyzed here.

We fit the model (34) by first defining . The averages are used as estimates for the ’s. Estimates of the Kronecker covariance of the error term are found using . There are benefits to using partial trace estimator in this problem as it is simple to compute, even though the entries are not defined. The MLE is more challenging to compute as the iterates of the block-descent algorithm (19) and (20) are no longer well-defined. We use the approximate partial trace estimates

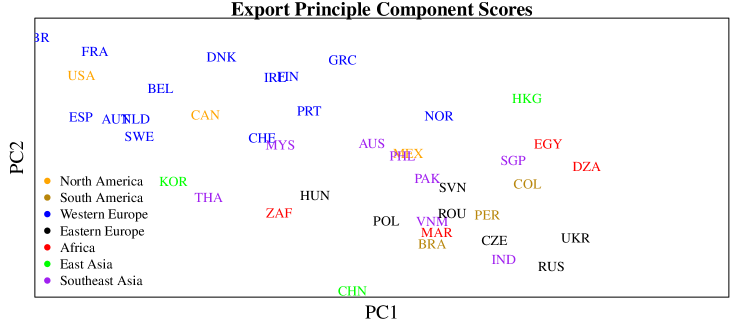

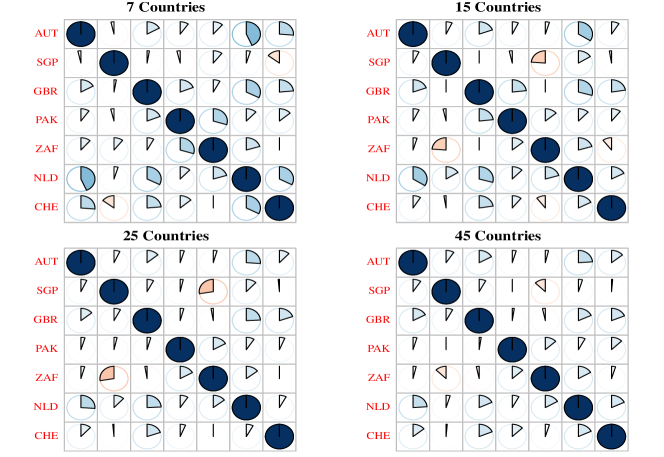

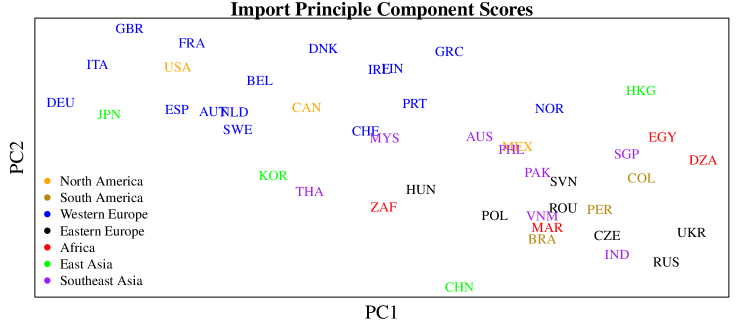

and examine the correlation matrices associated with these estimates. The estimated correlation matrices along with a collection of other plots are provided in Appendix B. It is seen that the estimated time correlation matrix is close to the identity matrix, showing that the model (34) has largely accounted for time-effects through the autoregressive structure and . The estimated import and export correlation matrices primarily have positive entries, with the import matrix generally having larger correlations. As might be expected, the import and export behaviour of high-income countries is positively correlated. To visualize the relationships between the import behaviour of countries, the first two principle component scores obtained from for each country are plotted in Figure 2. It is clear that there is some relationship between these principle components and country income.

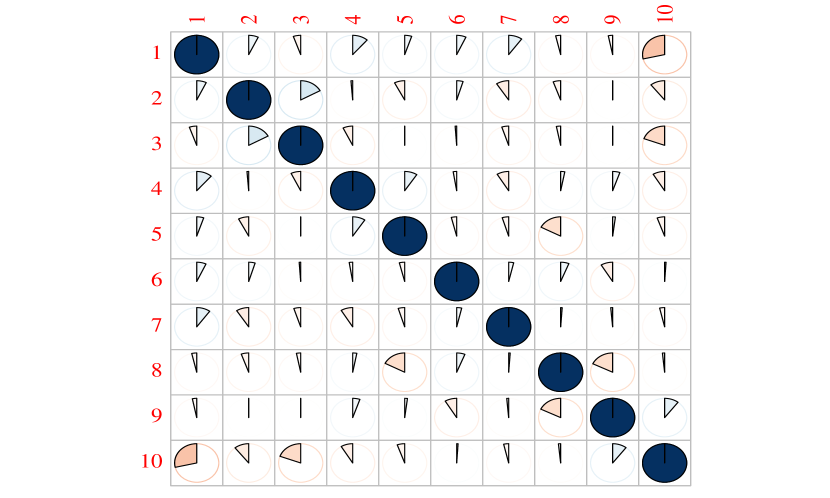

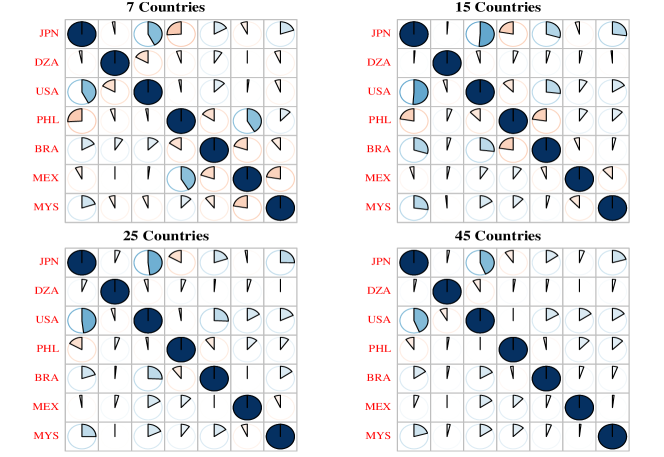

It was argued in Section 7 that the performance of partial trace estimator can improve as the dimension of the underlying tensor increases. To illustrate this, Figure 3 displays the estimated correlation matrix associated with that is estimated after holding out data. Specifically, each correlation matrix is computed from a sub-tensor of , where and range over a subset of the countries. As more countries are included, the correlation estimates appear to stabilize. In the next section we provide further empirical evidence of this phenomena in simulations.

8.2 Simulation Study

We present three different simulation regimes in this section. The first regime (Table 2) has fixed values of and a large value of , illustrating the asymptotic efficiency properties of the PT, RPT and MLE estimators. The second regime (Table 3) compares the PT and MLE estimators for sample sizes the are of a similar order to the array dimensions. In the last setting (Table 4) we illustrate the performance of the PT estimator for high-dimensional tensor-valued data with a sample size of one. The squared, relative Frobenius norm, loss function is used to gauge the performance of the aforementioned estimators. As this loss function is orthogonally invariant and all of the estimators are orthogonally equivariant, the various risk functions will only depend on the eigenvalues of the Kronecker model from which observations are drawn. It is thus sufficient to examine the risk function for Kronecker models that have diagonal covariance matrices.

| 3 | 7 | 3 | 7 | 3 | 7 | ||

| PT | 50 | 2.46 | 2.26 | 10.04 | 9.30 | 128.69 | 130.61 |

| 200 | 0.61 | 0.56 | 2.52 | 2.30 | 31.92 | 31.88 | |

| 2500 | 0.05 | 0.04 | 0.20 | 0.18 | 2.52 | 2.54 | |

| MLE | 50 | 2.52 | 2.31 | 8.93 | 7.63 | 92.46 | 43.43 |

| 200 | 0.62 | 0.56 | 2.19 | 1.86 | 22.22 | 10.63 | |

| 2500 | 0.05 | 0.05 | 0.17 | 0.15 | 1.74 | 0.87 | |

| RPT | 50 | 2.43 | 18.79 | 8.84 | 74.93 | 92.88 | 928.63 |

| 200 | 0.61 | 1.19 | 2.17 | 4.43 | 22.31 | 45.94 | |

| 2500 | 0.05 | 0.05 | 0.17 | 0.16 | 1.74 | 1.08 | |

| 3 | 7 | 20 | 3 | 7 | 20 | 3 | 7 | 20 | ||

| PT | 5 | 2.69 | 2.50 | 2.31 | 8.33 | 7.77 | 7.02 | 15.92 | 17.07 | 16.58 |

| 15 | 0.85 | 0.78 | 0.72 | 2.61 | 2.38 | 2.19 | 5.14 | 5.15 | 5.37 | |

| 30 | 0.41 | 0.38 | 0.36 | 1.28 | 1.17 | 1.08 | 2.56 | 2.65 | 2.56 | |

| MLE | 5 | 4.72 | 4.12 | 3.67 | 12.21 | 9.85 | 8.27 | 18.39 | 8.40 | 9.03 |

| 15 | 0.92 | 0.85 | 0.79 | 2.49 | 2.09 | 1.83 | 3.91 | 1.91 | 1.37 | |

| 30 | 0.43 | 0.40 | 0.37 | 1.16 | 0.98 | 0.86 | 1.84 | 0.90 | 0.49 | |

| PT | 5 | 0.91 | 1.02 | 1.30 | ||

| 50 | 0.25 | 0.29 | 1.27 | |||

| 200 | 0.12 | 0.14 | 1.29 | |||

| 4 | 1.12 | 1.20 | 1.27 | |||

| 8 | 0.37 | 0.50 | 0.63 | |||

| 16 | 0.03 | 0.07 | 0.12 |

Summarizing the results in the tables, first note that the RPT estimator has a noticeably large risk function in the large simulations. A large sample size of is needed for risk of the RPT estimator to be comparable to the MLE. Consequently, we do not recommend using the RPT estimator in practice, as the determinant rescaling introduces too much additional variability in the estimator. From both the large and moderate simulations we see that the PT estimator has performance that is comparable to the MLE in the cases where the eigenvalues are identical or linearly increasing. Interestingly, the first column of Table 3 shows that the PT estimator has better small sample performance than the MLE when . As predicted by our efficiency results for the PT estimator, the MLE appreciably outperforms the PT estimator when the eigenvalues have the form . These simulations suggest that if the eigenvalues of the true covariance matrix are not expected to be extremely dispersed then the PT estimator is a reasonable alternative to the MLE, especially in small sample settings or high-dimensional settings where it is computationally expensive to find the MLE.

Table 4 corroborates the consistency results in Section 7. When the relative Frobenius norm risk of the PT estimator decreases as increases for eigenvalue structures that increase at a polynomial rate. However, when the eigenvalues increase at an exponential rate the risk of the PT estimator remains approximately constant as increases. Moreover, when the number of modes increases but is held fixed at , the risk decreases at an exponential rate. The implication of these results is that the Kronecker covariance assumption, assuming that it is approximately true, is especially useful for modelling the covariance matrices of high-dimensional data, since the partial trace estimator is consistent with respect to under mild eigenvalues assumptions.

9 Conclusion

We have examined the performance of the partial trace estimator in various asymptotic settings in this article. A useful orthogonal parameterization of the Kronecker submodel was introduced in the course of our examinations. To conclude, we remark on two extensions that are relevant to the present work.

All of our results are predicated on the covariance structure of the data under consideration having a Kronecker covariance matrix. Shrinkage estimators were that allow for the Kronecker covariance assumption to be violated are described in [3, 20]. An alternative is to consider the larger class of models where the covariance matrix is assumed to be a sum of separable covariance matrices, meaning that it has the form [28, 27, 5, 18]. We postulate that it is possible to obtain fixed and increasing consistency results for the Kronecker sum model with a fixed rank and . For this model, . Letting vary, it ostensibly is possible to recover each of up to scaling, and likewise for the Kronecker factors corresponding to the other modes of the array.

A second extension of the results presented here is to other curved exponential families that have a tensor product structure on the mean parameter space. An example of this is the following log-linear Poisson model for contingency table data :

| (35) |

where this notation is equivalent to independently. Each mode of the tensor can be viewed as representing a factor or variable, with the th factor having levels. The analogue of the th partial trace operator is the sum over every mode but the th mode. Reminiscent of (13), the expectation of the analogue of the first partial operator is

It is expected that fixed- consistency results with a growing number of factors or levels within each factor are possible for this separable Poisson model. Additionally, the orthogonal parameterization introduced Section 6 has an analogue for the model (35). If ,

is an orthogonal parameterization. In future work it would be interesting to characterize classes of exponential families for which the results in this article can be generalized.

References

- [1] G. I. Allen and R. Tibshirani. Inference with transposable data: modelling the effects of row and column correlations. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 74(4):721–743, 2012.

- [2] S.-i. Amari and H. Nagaoka. Methods of information geometry, volume 191 of Translations of Mathematical Monographs. American Mathematical Society, Providence, RI; Oxford University Press, Oxford, 2000. Translated from the 1993 Japanese original by Daishi Harada.

- [3] E. Bersson and P. D. Hoff. Bayesian covariance estimation for multi-group matrix-variate data. arXiv preprint arXiv:2302.09211, 2023.

- [4] L. D. Brown. Fundamentals of statistical exponential families with applications in statistical decision theory, volume 9 of Institute of Mathematical Statistics Lecture Notes—Monograph Series. Institute of Mathematical Statistics, Hayward, CA, 1986.

- [5] A. Charkaborty and V. M. Panaretos. Testing for the rank of a covariance operator. Ann. Statist., 50(6):3510–3537, 2022.

- [6] D. Cheng, Y. Liu, Z. Niu, and L. Zhang. Modeling similarities among multi-dimensional financial time series. IEEE Access, 6:43404–43413, 2018.

- [7] D. R. Cox and N. Reid. Parameter orthogonality and approximate conditional inference. J. Roy. Statist. Soc. Ser. B, 49(1):1–39, 1987.

- [8] M. N. da Costa, G. Favier, and J. M. T. Romano. Tensor modelling of MIMO communication systems with performance analysis and kronecker receivers. Signal Processing, 145:304–316, 2018.

- [9] A. P. Dawid. Some matrix-variate distribution theory: notational considerations and a Bayesian application. Biometrika, 68(1):265–274, 1981.

- [10] H. Derksen and V. Makam. Maximum likelihood estimation for matrix normal models via quiver representations. SIAM J. Appl. Algebra Geom., 5(2):338–365, 2021.

- [11] M. Drton, S. Kuriki, and P. Hoff. Existence and uniqueness of the Kronecker covariance MLE. Ann. Statist., 49(5):2721–2754, 2021.

- [12] P. Dutilleul. The MLE algorithm for the matrix normal distribution. Journal of statistical computation and simulation, 64(2):105–123, 1999.

- [13] M. L. Eaton. Multivariate statistics, volume 53 of Institute of Mathematical Statistics Lecture Notes—Monograph Series. Institute of Mathematical Statistics, Beachwood, OH, 2007.

- [14] B. Efron. Are a set of microarrays independent of each other? Ann. Appl. Stat., 3(3):922–942, 2009.

- [15] D. Gerard and P. Hoff. Equivariant minimax dominators of the MLE in the array normal model. J. Multivariate Anal., 137:32–49, 2015.

- [16] D. Gerard and P. Hoff. A higher-order LQ decomposition for separable covariance models. Linear Algebra Appl., 505:57–84, 2016.

- [17] K. Greenewald and A. O. Hero, III. Robust Kronecker product PCA for spatio-temporal covariance estimation. IEEE Trans. Signal Process., 63(23):6368–6378, 2015.

- [18] K. Greenewald, T. Tsiligkaridis, and A. O. Hero. Kronecker sum decompositions of space-time data. In 2013 5th IEEE International Workshop on Computational Advances in Multi-Sensor Adaptive Processing (CAMSAP), pages 65–68. IEEE, 2013.

- [19] P. Hoff, B. Fosdick, A. Volfovsky, and Y. He. Amen: Additive and multiplicative effects models for networks and relational data. R package version, 1(9), 2017.

- [20] P. Hoff, A. McCormack, and A. R. Zhang. Core shrinkage covariance estimation for matrix-variate data. arXiv preprint arXiv:2207.12484, 2022.

- [21] R. E. Kass and P. W. Vos. Geometrical foundations of asymptotic inference. Wiley Series in Probability and Statistics: Probability and Statistics. John Wiley & Sons, Inc., New York, 1997. A Wiley-Interscience Publication.

- [22] T. G. Kolda and B. W. Bader. Tensor decompositions and applications. SIAM Rev., 51(3):455–500, 2009.

- [23] S. Lang. Fundamentals of differential geometry, volume 191 of Graduate Texts in Mathematics. Springer-Verlag, New York, 1999.

- [24] J. M. Lee. Introduction to smooth manifolds. Springer, 2013.

- [25] J. M. Lee. Introduction to Riemannian manifolds. Springer, 2018.

- [26] O. B. Linton and H. Tang. Estimation of the Kronecker covariance model by quadratic form. Econometric Theory, 38(5):1014–1067, 2022.

- [27] T. Masak, T. Rubin, and V. M. Panaretos. Inference and computation for sparsely sampled random surfaces. J. Comput. Graph. Statist., 31(4):1361–1374, 2022.

- [28] T. Masak, S. Sarkar, and V. M. Panaretos. Separable expansions for covariance estimation via the partial inner product. Biometrika, 110(1):225–247, 2023.

- [29] P. McCullagh. Tensor methods in statistics. Monographs on Statistics and Applied Probability. Chapman & Hall, London, 1987.

- [30] M. Pourahmadi. Cholesky decompositions and estimation of a covariance matrix: orthogonality of variance-correlation parameters. Biometrika, 94(4):1006–1013, 2007.

- [31] R. T. Rockafellar. Convex analysis, volume 11. Princeton university press, 1997.

- [32] A. Roy and R. Khattree. On implementation of a test for Kronecker product covariance structure for multivariate repeated measures data. Stat. Methodol., 2(4):297–306, 2005.

- [33] M. Shvartsman, N. Sundaram, M. Aoi, A. Charles, T. Willke, and J. Cohen. Matrix-normal models for fMRI analysis. In International conference on artificial intelligence and statistics, pages 1914–1923. PMLR, 2018.

- [34] L. T. Skovgaard. A Riemannian geometry of the multivariate normal model. Scand. J. Statist., 11(4):211–223, 1984.

- [35] M. S. Srivastava, T. von Rosen, and D. von Rosen. Models with a Kronecker product covariance structure: estimation and testing. Math. Methods Statist., 17(4):357–370, 2008.

- [36] T. Tsiligkaridis, A. O. Hero, III, and S. Zhou. On convergence of Kronecker graphical lasso algorithms. IEEE Trans. Signal Process., 61(7):1743–1755, 2013.

- [37] K. Werner, M. Jansson, and P. Stoica. On estimation of covariance matrices with Kronecker product structure. IEEE Trans. Signal Process., 56(2):478–491, 2008.

Appendix A Proofs

Lemma 0.1.

Let be a regular exponential family with densities that have the form . If and is the mean parameter of the exponential family then

where .

Proof.

In a regular exponential family is the cumulant generating function of with . Moreover, the information matrix in the mean parameterization is . We compute

Equation (10) follows by using the sufficient statistic and the corresponding canonical parameter in the Wishart exponential family. ∎

As noted in Section 3.1 the partial trace operator is formally defined as performing contractions on upper and lower indices of a tensor in . Let have coordinates . Using the Einstein summation notation, where there is an implicit summation between repeated upper and lower indices, the th partial trace operator is defined as

| (36) |

where is the Kronecker-delta tensor with coordinates if , if [29]. To be precise we have explicitly represented the tensor as having covariant (lower) and contravariant (upper) indices here. Throughout this article it is assumed that each vector space is endowed with an inner product so that there is a canonical identification , and there is no distinction between upper and lower indices. Thus, the tensor is equal to with lowered indices. This tensor notation simplifies the verification of properties of the partial trace operator. For example, we have

and

The above equation generalizes (13).

Lemma 0.2.

If and then the partial trace operator satisfies the cyclic permutation property

| (37) |

Proof.

Lemma 0.3.

If , , and then the partial trace operator satisfies the equivariance property

| (38) |

Proof.

Lemma 1.

Both and are the intersection of affine subspaces in with the mean parameter space of the exponential family . These auxiliary spaces are defined by the equations

with associated tangent subspaces

At any positive multiple of the identity . The orthogonality condition necessary for asymptotic efficiency holds at all for the MLE, but only holds at the matrices that are proportional to the identity matrix for the partial trace estimator.

Proof.

The form of follows immediately as the condition is equivalent to solving the likelihood equations (17) and (18) with respect to an observation .

If then , , and . By the definition of , , so . Conversely, if then

with a symmetric equation holding for . Thus, , proving the desired equality . As and are affine, and equal the translations of and to the origin.

Theorem 1.

Let be the smallest principle angle between and with respect to the mean space inner product (8). Then

| (39) |

where , and is the asymptotic variance of the associated limiting normal distribution.

Proof.

Let be the differential of at the point . This differential can be viewed as a linear map from to . The subspace is contained in the kernel of since for any curve with image contained in that passes through at . Any tangent vector in is not in the kernel of as for any curve that passes through at . This shows that the differential is idempotent. By counting dimensions it follows that has kernel and range . The orthogonality established in Lemma 1 implies that is the orthogonal projection onto with respect to the FIM.

An identical argument shows that the differential of at the point is idempotent, has kernel and range . However, is in general only a projection, not an orthogonal projection.

Using the delta method, equation (10), and the fact that is self-adjoint we compute

Similarly,

where the second equality is a result of being the orthogonal projection onto and having range . Defining , the maximum asymptotic variance ratio is

For any , decompose with and so that , giving

We now argue that if and are fixed, up to a choice of scaling, then the maximum of is equal to where is the angle under the FIM between the lines and . The scaling of does not change the value of so without loss of generality we fix and minimize over . Any point necessarily lies on the line . The minimizing value of is the FIM orthogonal projection of onto the affine subspace . The points form a parallelogram with equalling the angle between and at , which is equal to the angle at between and . The triangle is a right triangle with right angle at as is the orthogonal projection onto . The side opposite to this right angle has length , while the side opposite the angle has length , from which it follows that . This gives the desired result as

is maximized when is the smallest angle between lines and of and , namely the principle angle between these two subspaces. ∎

Reasoning similar to that above provides the following useful characterization of the asymptotic variance of efficient estimators in curved exponential families.

Lemma 0.4.

Let be an open set in the vector space and take to be a smooth submanifold of . Additionally, let be a curved exponential family contained in the regular exponential family with Fisher information metric . If is the sufficient statistic based on independent observations from , and is an smooth, efficient estimator of in the submodel , the variance of the asymptotic normal distribution of is , where is the orthogonal projection onto .

Proof.

We equip with an arbitrary inner product , where the self-adjoint Fisher information matrix associated with the Fisher information metric satisfies

As was argued in the proof of Theorem 1, if is efficient and for all , the differential of at is equal to . The distribution of converges weakly to , where if then is the matrix that satisfies [13, Ch1]

| (40) |

By the delta method and the fact that is self-adjoint with respect to the FIM, the asymptotic distribution of equals the asymptotic distribution of

Applying (40), the variance of the asymptotic distribution of the above quantity is

∎

Lemma 0.5.

Define as in Lemma 0.4. Let be a smooth reparameterization of , with the associated estimator sequence . If the manifold is equipped with the push-forward Riemannian metric defined by

then the asymptotic variance of is .

Proof.

The delta method shows that the asymptotic variance of equals that of

where the last equality follows from Lemma 0.4. We note that as is a map with domain , the differential is only defined on vectors that lie in the tangent space . We extend so that it takes the value on . This ensures that the quantity is well-defined. ∎

Lemma 2.

The functions, and are and equivariant respectively, implying that the auxiliary spaces are equivariant while the spaces are equivariant:

In particular, if has the eigendecomposition , all of the principle angles between and with respect to are identical to the principle angles between and with respect to .

Proof.

The equivariance of follows from the likelihood equations (19) and (20). If satisfies

The equivariance claim also follows from (37) and (38) since for

A similar equation holds for , yielding

The corresponding equivariance of and holds by the definition of an auxiliary space.

To prove the last statement regarding principle angles, consider the map on that sends to . By the equivariance of the linear space , the image of this subpace under this map equals . Likewise, the image of is . This map is an inner product space isometry between the inner product spaces and by (9). Principle angles, being defined in terms of a sequential maximization of inner products, are preserved by vector space isometries, completing the proof. ∎

Lemma 3.

Denote the eigenvalues of and by and respectively. The maximal asymptotic variance ratio of the partial trace estimator is bounded below, as follows

| (41) |

If and are the angles between and then the lower bound (22) can be written as

| (42) |

Proof.

Lemma 2 shows that without loss of generality can be taken to be the diagonal matrix . That is, the maximum asymptotic variance ratio only depends on the eigenvalues of . To ease notation, let . We also let represent the Hadamard product and define the element-wise division of vectors for .

Take , with . We define

where by construction and so that . The norm of can be represented as

where the norm on the right hand side is the usual Euclidean norm of vectors.

We want to find a vector that has a large inner product with . Assume that has the form . Then

If then . We compute

The optimal choice of maximizing the above inner product, subject to the scale constraint, is the matrix

With this choice of , and

so that

| (43) |

Now we optimize this expression with respect to . As this expression is scale invariant we assume that . Make a change of variables , or equivalently . The partial trace constraint can be rewritten as . The optimization problem becomes

Using Lagrange multipliers the optimal equals where ensures that this expression has unit norm. The optimal is therefore . Plugging this optimal back into (43) yields

If we take to be the angle between and and to be the principle angle between and then

Note that is equal to .

Symmetric equations hold with respect to , where in this case has the form and the subsequent maximization is performed over . ∎

Theorem 2.

The function is equivariant. If , the estimator is asymptotically efficient.

Proof.

In showing the equivariance of , note that

The equivariance of follows from the computation

Symmetrically, . In particular,

This proves that is -equivariant:

The map is a smooth, surjective map and by equivariance it has constant rank [24, Thm 4.14 a)].

To prove that is asymptotically efficient, by equivariance it is enough to show that the auxiliary space of at the identity is orthogonal to the tangent space , meaning that . As is a submersion, the dimension of equals the dimension of . Consequently, if it is shown that then this containment will imply the desired orthogonality property.

Let be a curve in with and . For an arbitrary , we want to show that , which implies the containment . As

assume that and .

To ease notation, form the matrices

so that

By the product rule we have

The derivatives of the diagonal entries of are

where the second equality follows from Jacobi’s formula and the last equality follows from . We conclude that and the derivative of is at . Similarly, . It remains to find the derivative of the multiplicative constant

From what we have just shown with respect to and , the derivative of the right-most factor above will be . Thus, by the product rule

Recalling that for Kronecker products, , one last application of the product rule shows that

completing the proof. ∎

Theorem 3.

The map , with defined as is a bijection that is an orthogonal parameterization. The Riemannian metric on the Cartesian product induced from the FIM on is a product metric, where has the standard Euclidean metric scaled by a factor of and each is equipped with the restriction of the FIM on scaled by a factor of , .

Proof.

Let be a tangent vector of at the point . We define . The determinant one constraint on the spaces implies that each has trace . The tangent vector in is

The induced Riemannian metric on is

where the third equality uses to show that the three terms are orthogonal to each other. By polarization, the above formula shows that the induced inner product on is exactly the inner product on the stated product Riemannian manifold . ∎

Lemma 0.6.

Define a -action on by

The parameterization map , or equivalently , is -equivariant with respect to the above action and the conjugation action on . The map defined by

is a group isomorphism that extends the parameterization map .

Proof.

The equivariance of follows from

Any can be uniquely decomposed as

with and , showing that is bijective.

That is a homomorphism is seen from

∎

Corollary 1.

The map , with defined as is an orthogonal parameterization of the Wishart model . The FIM induced on by and equals the FIM induced on by the Kronecker model . Equivalently, the block of the Fisher information matrix corresponding to is the same in both and . An analogous statement holds for the component of .

Proof.

The Wishart model has the Riemannian metric on

The model has the Fisher information metric

| (44) |

on , where have the property that

The first term in the expression (44) involving is the same as the FIM in the model , proving that the restricted FIM on the first two components of is identical to the FIM on . The orthogonality of the parameterization of follows from a similar computation to that in the proof of Theorem 3. ∎

Corollary 2.

As , the components of , namely

are asymptotically independent. Similarly, the components of are asymptotically independent.

Proof.

The delta method shows that is asymptotically normal with mean zero. It remains compute the asymptotic covariance of this random vector. Define to be the induced Riemannian metric on . By the reparameterization Lemma 0.5

for . As is asymptotically efficient this variance equals by Lemma 0.4. By polarization, the asymptotic variance matrix determines the asymptotic covariance matrix, where we conclude that

The orthogonality of the -parameterization shown in Theorem 3 implies for instance that if and then . This implies that the components of , namely , and , are asymptotically pairwise-uncorrelated. As these components are jointly asymptotically normal, the desired independence statement follows. ∎

Lemma 4.

Assume that is a smooth, scale-invariant test statistic for the hypothesis in the model , , , with and independent. Further assume that converges weakly to a non-degenerate distribution that does not depend on under . Let be the intersection hypothesis with respect to the model . The asymptotic distribution of the test statistics

| (45) |

equal the asymptotic distribution of

| (46) |

In particular, if is an asymptotic level- quantile of , the test that rejects when for either or has asymptotic level . Similar statements apply, by replacing all occurrences of above with the Kronecker MLE factors .

Proof.

Implicitly we are assuming that the asymptotic distribution of (29) is obtained by performing a Taylor expansion on the s and applying the delta method. Consequently, using the scale invariance of the test statistics, it is enough to show that

| (47) |

has the same asymptotic normal distribution as

| (48) |

Both of the components in (47) and (48) are asymptotically independent, the former by construction, and the latter by Corollary 2. It remains to establish that has the same asymptotic variance as . The proof of Corollary 2 shows that

where is the FIM (8) and is in .

The same reasoning as in Theorem 3 can be applied to show that the map gives an orthogonal parameterization of the family onto the space , where the factor has FIM (8) restricted to . As is an efficient estimator of , the reparameterization Lemma 0.5 implies that

from which we obtain the desired equality

The statement regarding the asymptotic level of the joint test of is a consequence of the asymptotic independence of the components of (48). As the maximum likelihood estimator is asymptotically efficient, the asymptotic normal distribution of (48) will be the same as the same statistic that has the occurrences of replaced by . ∎

Lemma 0.7.

Let with and . Denote the length vector of eigenvalues of by . Then

| (49) |

and

Proof.

Without loss of generality we take and by the orthogonal equivariance of the partial trace operators we assume that is diagonal for .

We can write with . Using the equivariance and cyclic permutation properties of the partial trace,

| (50) |

To ease notation define

and let . The right hand side of (50) becomes

| (51) |

We denote the unit-trace diagonal matrix by and decompose as

| (52) |

where are the diagonal entries of and are the dimensional blocks of . All of the scaled blocks are independent and follow the distribution . The expectation of equals

The Frobenius norm of can be computed as

Plugging this back into (51) gives

The remaining result follows from

where

∎

Theorem 4.

Let with and . Denote by and take to be the length vector of eigenvalues of . If

| (53) |

then

| (54) |

Proof.

First we compute the variance of . Without loss of generality can be taken to be diagonal, and after rescaling by , it can be assumed that , with being equal to the diagonal entries of divided by their sum. Taking , has the same distribution as . Then

| (55) |

where we have used the fact that the diagonal entries of have independent scaled chi-squared distributions with variance . By Chebychev’s inequality,

Note so that

Define . We can decompose the norm of interest as

which is bounded above by

where by the first assumption (32) this term is .

Decomposing , we get

Using the fact that

Inductively decomposing in a similar manner, we obtain

Next we bound by

The second assumption in (32) is used to get that in the denominator above. By the binomial theorem

gives the correct convergence rate for .

∎

Lemma 5.

Let be a non-zero polynomial with non-negative coefficients . If , then as . If , grows exponentially then as . Lastly, if has a spiked eigenvalue structure with entries that equal , entries that equal , and , then

where . This expression is if or .

Proof.

In the case , we compute

By Faulhaber’s formula and thus

The case for a general polynomial follows similarly since

assuming that .

In the exponential growth case, and

It follows that , as needed.

Dropping the subscripts on , for readability, the formula for the remaining case follows from expression

If , for all then

If for all then

∎

Appendix B Simulation Study Details

B.1 Hypothesis Testing

The rejection probabilities presented in the simulation study in Section 6 are obtained from first drawing observations . Under the null hypothesis of sphericity and compound symmetry and are taken to be and respectively. Under the simulations for the alternative hypothesis equals , and equals , where .

The test statistic used to test is where equals the diagonal matrix that has the same diagonal entries as . The affine-invariant distance is equal to the Riemannian distance on the set of positive definite matrices induced by the Fisher information metric. It is defined by , where is the matrix logarithm. The sphericity test statistic is pivotal under the null hypothesis due to the affine invariance of :

In particular, this test statistic is scale-invariant. The quantile of is approximated by computing over independent draws of . Invariance of the test statistic under the group of diagonal matrices, or equivalently the fact that the test statistic is pivotal, ensures that the quantile does not depend on which diagonal matrix is chosen for . Lemma 4 implies that the Wishart distribution with degrees of freedom gives the correct quantile asymptotically.

The test of compound symmetry that is used in this simulation study is the likelihood ratio test. The likelihood ratio test statistic is compared to the quantile of a chi-squared distribution with four degrees of freedom. The likelihood ratio statistic is scale-invariant, as needed for Lemma 4 to apply.

B.2 Comtrade Data Plots