Stochastic smoothing accelerated gradient method for nonsmooth convex

composite optimization††thanks: Submitted to the editors DATE.

\fundingThis work was funded by National Natural Science Foundation of China (No. 12171027).

Ruyu Wang

School of Mathematics and Statistics, Beijing Jiaotong University

(, ).

wangruyu@bjtu.edu.cnzc.njtu@163.comChao Zhang222https://datahub.io/machine-learning/mnist_784/

Abstract

We propose a novel stochastic smoothing accelerated gradient (SSAG) method for general constrained nonsmooth

convex composite optimization, and analyze the convergence rates. The SSAG method allows various smoothing techniques, and can deal with the nonsmooth term that is not easy to compute its proximal term, or that does not own the linear max structure. To the best of our knowledge, it is the first stochastic approximation type method with solid convergence result to solve the convex composite optimization problem whose nonsmooth term is the maximization of numerous nonlinear convex functions. We prove that the SSAG method achieves the best-known complexity bounds in terms of the stochastic first-order oracle (), using either diminishing smoothing parameters or a fixed smoothing parameter. We give two applications of our results to distributionally robust optimization problems. Numerical results on the two applications demonstrate the effectiveness and efficiency of the proposed SSAG method.

In this paper, we develop and analyze a novel stochastic smoothing accelerated gradient (SSAG) method for the following class of nonsmooth convex composite optimization problems. Let be a closed convex set in the Euclidean space , be a convex and -smooth function, and be a general continuous nonsmooth convex function.

We consider the following nonsmooth optimization problems of the form

(1)

Here we always assume that is well defined and finite valued in , and (1) has at least one global minimizer and as its optimal value. The nonsmooth term includes a broad range of functions. It can be the expectation of nonsmooth closed proper convex functions as

(2)

where is a random vector whose probability distribution supported on , and is the expectation with respect to . The nonsmooth term can also be the maximum of numerous convex nonlinear functions as

(3)

where can be a large integer greater than thousands, is convex and -smooth over , and

(4)

Problem (1) is challenging mainly for two reasons. First, the nonsmooth term may be rather complex. For instance, in (2) is complex that it has no explicit proximal operator, and in (3) is highly nonlinear for some .

Second, the objective value and/or the subgradient are hard or expensive to obtain. Applications can be found in various problems arising in machine learning and distributionally robust optimization [9, 32, 21, 12].

To address the first difficulty mentioned above, smoothing techniques for the objective function and smoothing methods are promising [25, 11, 10, 42, 41, 39, 40]. The smoothing techniques for deterministic nonsmooth convex programming problems are well known, including the integral convolution [11], the Nesterov’s smoothing technique [25], as well as the inf-conv smoothing approximation [6]. For stochastic programming problems, the randomized smoothing (RS) technique was proposed in [14] and the Nesterov’s smoothing technique was also shown to be applicable [35].

To tackle the second difficulty, the stochastic approximation (SA) algorithms are appropriate. Ever since the pioneering work [30], SA algorithms have been attracted much attention and well developed [27, 28, 24, 19]. Several SA algorithms such as RSPG [17] and AM-SGD [43] have been proposed to solve nonsmooth stochastic convex composite problems (1)-(2), but they require that the nonsmooth

term is relatively simple, e.g., , so that the proximal operator can be obtained easily. Complexity results have been given in terms of the number of to get an -approximate solution. Recall that we say is an -approximate solution of (1), if

(5)

where the expectation is taken to , the history of randomness up to the -th iterate.

For nonsmooth stochastic convex optimization, the order of the complexity required to find an -approximate solution for a predetermined accuracy , cannot be smaller than for a first-order method,

as pointed out in [24]. Recently, variance reduction techniques have been enrolled in SA algorithms.

The popular stochastic variance reduction methods for nonsmooth problems such as SAGA [13], SVRG [29], SARAH [26], IPSG [36], and Katyusha [1] also require the proximal operator to be easily computed.

Duchi et al. in [14] proposed a novel randomized smoothing (RS) method, which is the pioneering work for combining SA and smoothing technique that can solve (1)-(2). The RS method combines the RS technique with Tseng’s accelerated gradient method [34] for deterministic smooth optimization problems. A convolution-based smoothing technique and a random sampling technique are used to construct smoothing functions, and the best-known complexity results are obtained. In the RS method, the smoothing parameter is flexible, and can either be diminishing or fixed. When the smoothing parameter is diminishing, the RS method can adopt any batch size, and no prior knowledge of the iteration limit is required to implement the method. The two properties make the RS method possible to find an appropriate batch size and render it suitable for online and streaming applications. For the smoothing parameter to be fixed, the iteration limit needs to be known ahead, but no specific analysis in given on how to choose the iteration limit in order to get an -approximate solution. Furthermore, the smoothing techniques used by the RS method are dimension-dependent, and the complexity bounds in (Theorems 2.1,2.2, and Corollaries 2.3-2.5 of [14]) are dimension-dependent, which may cause the RS method time-consuming for high-dimensional problems.

Recently, Wang et al. in [35] proposed a stochastic Nesterov’s smoothing accelerated (SNSA) method for solving (1) -(2) that can achieve the best-known complexity of first-order SA algorithms to find an -approximate solution.

The Nesterov’s smoothing technique in [25] is employed, which requires that for each fixed , has the linear max structure

(6)

where is a bounded closed convex set, is a linear operator, and is a continuous convex function. In contrast to the RS method, the Nesterov’s smoothing technique and the complexity results of the SNSA method are dimension-independent, which is attractive for high-dimensional problems. A predetermined smoothing parameter is adopted in the SASA method. For the three special choices of batch sizes, explicit formulas for computing the iteration limit and the smoothing parameter to obtain an -approximate solution are given in [35]. When is a singleton, the SNSA method coincides with the Nesterov’s smoothing accelerated method in [25] for deterministic nonsmooth optimization problems.

There are urges to further develop stochastic smoothing first-order methods for solving (1) from real applications. In numerical experiments, we consider two applications in distributionally robust optimization: a family of Wasserstein distributionally robust vector machine (DRSVM) with being in the form of (2) [21], and a discretization scheme of distributionally robust portfolio optimization (DRPO) with being in the form of (3) [38]. For (1)-(2) arising in Wasserstein DRSVM, the newly developed efficient algorithm is the incremental proximal point algorithm (IPPA) in [21] that is deterministic. Stochastic approximation type methods are promising to enhance the efficiency for problems involving large dataset than the deterministic algorithms. Even though the RS and the SNSA methods can solve the Wasserstein DRSVM, the dimension-dependent complexity results in the RS method, the fixed smoothing parameter, and the only three choices of batch sizes in the SNSA method may lead computational inefficiency. As far as our knowledge, there is no stochastic smoothing first-order method for solving

(1) with defined in (3) where is very large. For (1) with defined in (3) arising from DRPO, the existing algorithm

is a cutting plane (CP) method that is deterministic [38].

In this paper, we propose an SSAG method for solving

optimization problems (1) with a nonsmooth convex component in the form of (2) or (3). We do not assume that has the linear max structure in (6), or its proximal operator is easily obtained.

We can adopt any smoothing technique as long as the smoothing approximation for satisfies Definition2.1 in Section2.

We use the decreasing setting of the smoothing parameter similar as that in [14], and can choose the appropriate batch size to fasten the computational speed.

We show that the SSAG method achieves the best-known complexity of first-order SA algorithms to find an -approximate solution. The complexity results can be dimension-independent with proper smoothing techniques. Numerical experiments on the two applications from distributionally robust optimization demonstrate the effectiveness and efficiency of our method, compared to the state-of-the-art methods.

The remaining of this paper is organized as follows. In Section2, we outline some important smoothing techniques and show that the corresponding smoothing approximations satisfy Definition2.1 and 2.1 required in this paper. In Section3, we develop the SSAG method. We show that various smoothing techniques can be enrolled in the method, and the order of the complexity of the proposed SSAG method is the same as the state-of-the-art first-order SA algorithms for stochastic nonsmooth convex optimization. In particular, the complexity results can be dimension-independent if the smoothing technique does not relate to the dimension. Numerical experiments on two distributionally robust optimization problems using real datasets are given in Section4 to demonstrate the effectiveness and efficiency of our SSAG method.

Notation. We denote

by the Euclidean norm, by the norm, and by

the inner product. For any real number , we denote by and the nearest integer to from above and below, respectively.

We denote by the closed ball of radius centered at .

The set refers to the -dimensional simplex. Given a square matrix , let denote the largest eigenvalue of . The set of all positive semidefinite matrices is denoted by . A function is -Lipschitz over if

We say is -smooth over if

(7)

For a function , its convex conjugate is defined by

(8)

2 Smoothing properties

There exist several existing smoothing techniques to construct smoothing approximations of the original nonsmooth function. Throughout the paper, a smoothing approximation is called a smoothing function if it satisfies the following definition.

Definition 2.1.

We call a smoothing function of the convex function , if for any , is continuously differentiable in and satisfies the following conditions:

;

(convexity) is convex on ;

(Lipschitz continuity with respect to ) there exists a constant such that

(9)

(Lipschitz smoothness with respect to ) there exist constants and irrelevant to such that is -smooth on with Lipschitz constant .

Definition2.1 is closely related to Definition 3.1 of [7] and Definition 2.1 of [6]. Besides, Definition 3.1 of [7] requires the gradient consistency property that

for any .

The -approximate solution of this paper will be measured by (5), using only objective values.

Consequently, a smoothing function in this paper does not require the gradient consistency property. Moreover, Definition2.1 (iv) is the same as Definition 2.1 (ii) of [6], while the parameter in Definition 3.1 (iv) of [7].

Below we outline several smoothing techniques to construct smoothing approximations for the nonsmooth terms in (2) and

in (3), respectively.

–Nesterov’s smoothing for (2)

The Nesterov’s smoothing technique for a deterministic nonsmooth function was introduced in [25]. Now we extend it to a stochastic nonsmooth function.

Assume that has the max linear structure in (6) for almost everywhere (a.e.). Then the Nesterov’s smoothing technique [25] can be used to construct a smoothing approximation

of in (2) as follows.

By inserting a non-negative, continuous and -strongly convex function in (6), we obtain

(10)

According to Theorem 1 of [25], the gradient of has the formula

(11)

where is the unique optimal solution of the maximization problem in (10).

The linear max structure of in (6) and easily obtainable for a.e. are essential for the applicabilty of Nesterov’s smoothing technique.

–Inf-conv smoothing for both (2) and (3)

The inf-conv smoothing technique for a deterministic nonsmooth function has been intensively studied in section 4 of [6].

For in (2) involving expectation, we define

its inf-conv smoothing approximation as , in which is constructed according to Definition 4.2 of [6] by

(12)

where is convex and -smooth. When the inf-conv smoothing technique is used, we always assume that for any , a.e., and any , is finite.

When the quadratic function is chosen, the inf-conv smoothing technique reduces to the well-known Moreau approximation [6]. By Theorem 4.1 of [6], has a “dual” formulation

(13)

where and are the convex conjugates of and , respectively.

Moreover, is differentiable with gradient

of the form

(14)

where is the unique minimizer of the right-hand side of the inf problem in (12).

For in (3) that involves the maximization of finite convex functions, we can obtain the inf-conv approximation of by Examples 4.4 and 4.9 of [6]. To be specific, let and be of the form

(15)

Then the gradient of is

(16)

and the convex conjugate of is

(17)

The inf-conv smoothing approximation can be expressed as

(18)

(19)

Let ,

the inf-conv smoothing approximation of the function over is given by

(20)

Interestingly, in (20) is the same as the so-called Neural Networks smoothing function for in (3) constructed by convolution and mathematical induction in [11].

By direct computation, the gradient

is

(21)

Let be a smoothing function of satisfying Definition2.1. The smooth counterpart of (1) is

(22)

For (1)-(2), a stochastic gradient for the smoothing function at is

(23)

where is the random vector following a certain probability density over the support set , and is a smoothing function of in (2).

For (1) with defined in (3), a stochastic gradient for the smoothing function is

(24)

where is a random index whose probability is in (21) over the support set that is caused by the inf-conv smoothing technique.

Throughout the paper, we make the following assumptions for the smoothing stochastic gradients of smoothing functions.

Assumption 2.1.

For every and every ,

where is a constant, and the expectation is taken with respect to the random vector with given probability density.

For a fixed , (a) and (b) in Assumption 2.1 are common assumptions for stochastic algorithms dealing with smooth objective functions; see

e.g., Assumption 1 of [17], and (5.1)–(5.2) of [20]. In contrast, Assumption 2.1 needs (a) and (b) to be held for every .

For every , and , Assumption 2.1 a) is easy to fulfil. When considering (1)-(2),

where the position of the gradient operator and the expectation operator can be changed according to Proposition 4 of [31] and the facts that is well defined and finite, and is convex and differentiable at every .

When considering (1) with defined in (3), we view as a probability of over the support set and by (21),

Assumption 2.1 b) holds for every and every , when considering (1)-(2), because

(25)

We show in the following lemmas that the smoothing approximations constructed by

the Nesterov’s smoothing and the inf-conv smoothing techniques

satisfy Definition2.1 as well as 2.1 under mild conditions.

Lemma 2.2.

For in (2), assume that

has a linear max structure in (6) for a.e., and there exists a constant such that for a.e. Let with constructed by the Nesterov’s smoothing technique in (10). Then the following statements hold.

(i)

The function is a smoothing function of satisfying Definition2.1, with , , and .

By taking the expectation of the above inequalities with respect to , we find

Hence Definition2.1 (i) holds.

By using Theorem 1 of [25] on and taking the expectation, we know that the convex function is -smooth with . Thus, satisfies Definition2.1 (ii) and (iv) with and .

For any , without loss of generality, we assume and consequently

We have

where the first inequality holds because for any continuous functions ,

We consider the approximations constructed by the inf-conv smoothing technique.

Lemma 2.4.

For in (2), let

with

constructed by the inf-conv smoothing technique in (12).

The following statements hold.

(i)

Assume that

for all .

Then

is a smoothing function of

satisfying Definition2.1, with , , and .

(ii)

Assume that . Then Assumption 2.1 holds with the constant

Proof 2.5.

By Lemma 4.2 of [6],

(13), and the assumption that

for all , we know that

for every , is convex continuous for and

By taking expectation on the above inequalities with respect to , we know that satisfies Definition 2.1 (i). Moreover, by using Theorem 4.1 of [6] for and taking expectation on , we know that is convex continuous, finite-valued, differentiable, and -smooth with constant . Thus, satisfies Definition2.1 (ii) and (iv) with and .

For any , without loss of generality, we assume that . Consequently , according to (13) and the assumption that for all . By using the definition of and the similar arguments as for the Nesterov’s smoothing approximation in Lemma 2.2, we have

Hence satisfies Definition2.1 (iii) with . Statement (i) holds as desired.

For defined in (15), its convex conjugate in (17) satisfies the assumption in Lemma2.4 (i) that for all , and its gradient in (16) satisfies the assumption in Lemma2.4 (ii) that .

Hence by the definition of in (15). Till now we have shown that the statement (i)

holds.

Using the similar arguments as (2) and , we have statement (ii) holds because

3 SSAG method

In this section, we develop the SSAG method for (1). We will show the SSAG method achieves the best-known complexity bounds in terms of the among the SA methods using the first-order information.

At the -th iterate, we randomly choose a mini-batch samples

of the random vector following the given probability density, where is the batch size. We use to denote all randomness occurred before the -th iterate, i.e., .

For any , we denote the mini-batch stochastic gradients by

The following lemma addresses the relations of to , which can be shown without difficulty using the arguments similar as those for Lemma 2 in [17].

Given the iteration limit , initial points , the batch sizes with , the smoothing parameters with , and with , and positive sequences and .

fordo

Step 1. Set

Step 2. Call the times to obtain , , and compute .

Step 3. Find

Step 4. Find

endfor

return

We now specify the algorithmic parameters of the SSAG method. For given and ,

(26)

(27)

(28)

The sequences and are defined in (26), the same as those in Duchi’s work [14].

According to Lemma 4.3 of [14],

(29)

Similar as (2.9) of [16], the sequence is set in (27). It is a nondecreasing sequence that satisfies

The sequence is set in

(28), which is designed for the later theoretical analysis.

By Definition2.1, we can easily obtain that for any and any ,

(30)

(31)

Lemma3.2 below is a special case of Lemma 2 in [15].

Lemma 3.2.

Let the convex function , the point , and the scalar be given. If

then for any , we have

Recall that refers to an arbitrary optimal solution of (1). For ease of notation, we define some symbols in Table1.

In view of the definitions of and in Table1, it follows that

(36)

By the convexity of , we have for any ,

(37)

Since is an -smooth function over , by setting and respectively in (37), we have

Subtracting from both sides of the above inequality, using the definitions of , , and in Table1,

we get

(38)

where the last inequality is based on in Step 1 of Algorithm1. It is clear that , and for any nonnegative , and . Then by setting , , and that is positive according to (27), we have

(39)

In view of (38) and (39), it follows that (34) holds.

Since , and are deterministic if is given, we have by the definition of in Table1, Lemma3.1 (a), and by the similar arguments in the proof of Lemma 3 of [35],

(40)

Taking the expectation on both sides of (34) with respect to , and using the observation (40), 2.1 and Lemma3.1 (b), and the definition of in Table1, we get (35) as desired.

Theorem 3.7.

Let , , , and be defined in (26)–(28) for

Algorithm1. Under 2.1, we have for any ,

(41)

where the expectation is taken with respect to .

Proof 3.8.

By the definition of in Table1

and Lemma3.5,

we have for any

(42)

Multiplying both sides of this inequality by , we obtain

Based on the definition of in Table1, , and , we have

(46)

By the definition of in Table1, and for from (27), we have

(47)

With the above observations (44), (46), (47), and by (29), and multiplying (43) by , we obtain

(48)

In view of (30), (48), by (26), and by (29), we have

The proof is completed.

Remark 3.9.

From (41), in order to get an -approximate solution, we need

Then, we can choose

(50)

Thus the order of the complexity for finding an -approximate solution is the same as

that obtained by the state-of-the-art SA algorithms [24, 19, 15, 16]. It is worth mentioning that our SSAG method does not require the nonsmooth components to have easily obtainable proximal operators, as that required in [24, 19, 15, 16].

Unlike the complexity result of the RSPG method given by Ghadimi et al. in [17] and the complexity results of the SNSA method given by Wang et al. in [35], our SSAG method does not require the exact calculation of the batch size . For a predetermined accuracy and the batch size , the iteration limit is calculated by (50). That is, for any batch size , the corresponding iteration limit can be obtained. Hence, the appropriate choice of need not be balanced with the iteration limit as in [17, 35].

In addition, unlike the bounds in the complexity results of the RS method (Corollaries 2.3-2.6 of [14]) that are dimension-dependent, the bound of our complexity result in Theorem 3.7 can be dimension-independent if proper smoothing techniques are employed, which is beneficial for high-dimensional problems.

At the end of this section,

we conclude with a theorem using a fixed setting of the smoothing parameter . It is clear that by setting , the complexities achieved by Theorem3.7 above and Theorem3.10 below are identical up to constant factors.

Theorem 3.10.

Suppose that for all .

With the remaining conditions as in Theorem3.7, we have for any ,

(51)

where the expectation is taken with respect to .

Proof 3.11.

If we fix for all , then the bound (42) holds with the second term , i.e., the upper bound of (48) is changed into

(52)

where for all .

The remainder of the proof follows unchanged, with for all . Then, we have

We consider a Wasserstein DRSVM problem [21] in Section4.1, and a discretization scheme of DRPO with matrix moments in [38] in Section4.2. Both applications use real datasets. The batch size of our SSAG method is determined in the following way.

For different batch sizes, , we make 5 runs of our SSAG method under a CPU time limit of 50 seconds (50s) for each run, and select the optimal batch size so that the average objective value decreases the fastest with this .

Then the iteration limit for SSAG is computed by using (50). The CPU time is measured with MATLAB command “cputime”. Multiplying by the batch size chosen for the SSAG method gives us , the limit of calls, i,e., the budget of total number of calls to .

For the Wasserstein DRSVM problem

in Section4.1,

we compare our SSAG method with the following methods.

-

SNSA [35]: The smoothing parameter, the batch size, and the stepsize choices in the SNSA method follow from Theorem 2 and Corollary 2 of [35].

-

S-Subgrad [24]: The Armijo’s step size rule is used instead of in [24] because the computational performance is better than that using stepsize in [24].

-

RS [14]:

The RS method combines the convolution technique and the random sampling technique to get a smooth approximation. It requires to enrolling an auxiliary random vector , with a given probability density function . In numerical experiment, we choose that is uniform on . The initial smoothing parameter, the formula for the diminishing sequence of smoothing parameters, the stepsize choices, and the parameters in the RS method follow from Corollary 2.3 of [14].

-

IPPA [21]: It is a deterministic method.

We use the code of IPPA that is available at https://github.com/ gerrili1996/Incremental_DRSVM. Each iteration of IPPA requires solving single-sample proximal point subproblems, where is the number of the training samples.

For the DRPO problem in Section4.2, we compare our SSAG method with the following two deterministic methods, since we do not find SA-type algorithms with convergence guarantee for nonsmooth term being the maximization of numerous convex functions.

-

Subgrad: It is the S-Subgrad method mentioned above with batch size in each iteration.

For each problem, obtained by our SSAG method is set to be the limit of calls for all methods. The iteration limit and batch size for S-Subgrad are the same as those of SSAG. For RS, the batch size is determined as follows. We make 5 runs using different batch sizes, , and , respectively. The CPU time limit for each run is 50s. The optimal batch size is finally selected because it leads to the fastest decrease in the objective value. Here larger batch sizes are tried than those for our SSAG method, because RS employs the additional random vector . Then the iteration limit of RS can be calculated as . Since IPPA and CP are deterministic methods, their batch size equals the number of training samples in the problem. Additionally, their iteration limits are computed in the same way as RS. Denote by the sample size, and by the number of training samples.

We follow the way of estimating the parameter as in [17]. To be specific, using the training samples, we compute the stochastic gradients of the objective function times at 100 randomly selected points and then take the average of the variances of the stochastic gradients for each point as an estimation of .

For the Wasserstein DRSVM problem, We estimate an approximate solution

by running S-Subgrad 10000 iterations as in [2]. For the DRPO problem, we estimate an approximate solution

by running Subgrad 10000 iterations.

We follow the way of giving a CPU time budget as in [3, 2]. For each problem, we make 20 runs of each method under the CPU time budget 200s for each run in order to have statistical relevance of the results. Let be the th iterate point of a certain method. We also use

(53)

to stop the method. If one of the three conditions (CPU time budget, (53), the total number of calls to ) is met, then we stop the method.

All experiments are performed in Windows 10 on a PC with an Intel Core 10 CPU at 3.70 GHZ and 64 GB of RAM, using MATLAB R2021a.

4.1 Wasserstein DRSVM problem

Support vector machine (SVM) is one of the most frequently used classification methods and has enjoyed notable empirical successes in machine learning and data analysis [37, 33, 8]. However, there are a few literature addressing the development of fast algorithms for its Wasserstein distributionally robust optimization formulation, which takes the form

(54)

Here, is the regularization term with , denotes a feature vector and is the associated label, is the hinge loss with respect to the random vector and the vector .

Let be the empirical

measure associated with the training samples in the feature-label space . The ambiguity set

is defined on the space of probability measures centered at the empirical measure and has radius with respect to Wasserstein distance

where is the random vector with the empirical measure, represents the relative emphasis between feature mismatch and label uncertainty, and is the set of couplings of and . We set and that are the same as [21] in our numerical experiments.

Let . In [21], it is pointed out that (54) can be reformulated as

(55)

where . Using the inf-conv smoothing technique, we obtain the smooth counterpart of (55) as

(56)

where , . By Theorem 5.12 of [5], we can choose the parameters

For the SNSA method in [35], we need to estimate an upper bound of the strongly convex function at an optimal solution . Let us denote by the ice cream cone. By (55), we get for any , and consequently

where

is the approximate solution obtained by running S-Subgrad 10000 iterations. In implementing Algorithm 1, we need to compute the projection of a vector on the ice cream cone , which has a closed form formula given in Theorem 3.3.6 of [4].

First, in order to compare the performance

of each method in training dataset, we fix in (55) and use a real dataset - a8a that is also used in [21]. The a8a dataset111https://www.csie.ntu.edu.tw/ cjlin/libsvmtools/datasets/binary/a8a/ has samples of features taken from Adult dataset for binary classification. Let

Let the predetermined accuracy , 0.001, and 0.0001, respectively. We list the mean (Mean) and the variance (Var) of objective value (Obj) at the computed solutions

(20 runs for all methods) in Table2, corresponding to each . For smoothing parameter , “” and “-” respectively represent that the smoothing parameters are diminishing and do not exist. Since IPPA is a deterministic method, the objective value and the accuracy of 20 times are the same, and consequently “Obj Var” and “Acc Var” for IPPA are 0. Among the comparisons of various methods, the values in bold denote the winners’ performances. It is clear that SSAG provides the computed solutions with the smallest “Obj Mean”, and the highest “Acc Mean” among all the methods, and obtain the smallest “Obj Var” and “Acc Var” among all the SA-type methods for .

Moreover, when only our SSAG method stops using (53) before reaching the CPU time budget 200s. We can see from Table2 that the CPU times of SSAG are around

6 times faster to 41 times faster than that of the other methods.

Table 2: Obj, Acc, and CPU time on a8a with parameters , when .

ALG.

Obj

Obj

Acc

Acc

CPU

Mean

Var

Mean

Var

0.01

9.73e+06

SSAG

2000

0.7391

9.35e-06

0.8332

2.84e-07

4.81

S-Subgrad

-

2000

0.7491

7.35e-04

0.8248

1.59e-04

40.09

SNSA

4.90e-03

2373

0.7489

5.58e-05

0.8257

4.26e-05

32.45

RS

10000

0.7857

5.43e-02

0.7574

2.98e-04

200.00

IPPA

-

22696

0.9681

0

0.7767

0

97.98

0.001

5.41e+08

SSAG

2000

0.7301

6.73e-09

0.8338

1.80e-07

9.91

S-Subgrad

-

2000

0.7487

2.01e-06

0.8262

2.03e-05

200.00

SNSA

6.52e-04

17686

0.7321

4.73e-08

0.8290

1.10e-05

108.57

RS

10000

0.7855

7.66e-04

0.7581

3.02e-05

200.00

IPPA

-

22696

0.7545

0

0.7817

0

200.00

0.0001

4.97e+10

SSAG

2000

0.7292

7.82e-06

0.8339

3.06e-06

19.41

S-Subgrad

-

2000

0.7481

8.91e-03

0.8270

4.70e-04

200.00

SNSA

6.80e-05

69642

0.7315

2.46e-04

0.8285

6.17e-05

200.00

RS

10000

0.7835

1.05e-02

0.7612

4.06e-04

200.00

IPPA

-

22696

0.7545

0

0.7817

0

200.00

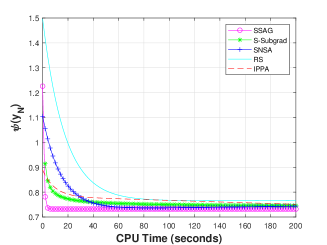

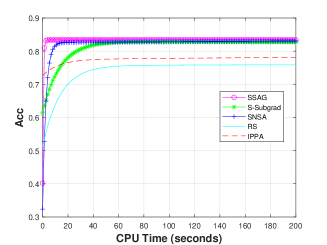

We draw the curves of average Obj and Acc versus (v.s.) CPU time for these methods when in Fig.1. We can see that the objectives of the sequence generated by our SSAG method decrease quickly at the beginning and also reach stability quickly.

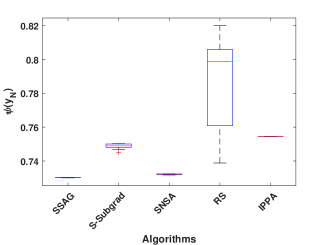

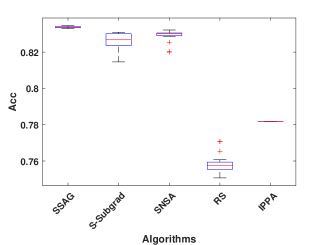

Fig.2 draws the boxplots of Obj and Acc of the training data for all methods in 20 runs, when . Due to the similarity of the results, we omit the figures of and . It is clear that our SSAG method performs much better than the others. From Table2, Fig.1 and Fig.2, our SSAG method significantly outperforms the IPPA method because IPPA solves subproblems at every iteration. The proposed SSAG method decreases Obj and increases Acc faster than the SNSA method. This might be benefited by the diminishing smoothing parameters in Algorithm1.

When , the IPPA method stops since it meets , the total number of calls. The corresponding number of iterations of the IPPA method is .

Figure 1: Average Obj and Acc v.s. CPU time of 20 runs on a8a, when and .

Figure 2: The boxplots of Obj and Acc of 20 runs on a8a, when and .

Next, to compare the classification accuracy of these methods, cross-validation (CV) is used to select the best for each method.

Apart from a8a dataset, we also test on 2-class versions of MnistData-10, and TDT2 datasets, denoted as MnistData-10(B), and TDT2(B), respectively. We adopt a similar approach to [23] by analyzing datasets in 2-class versions. MnistData-10 dataset is composed of handwritten digits, available from the website222https://datahub.io/machine-learning/mnist_784/. MnistData-10(B) discriminates between the first 5 classes and the remaining ones.

TDT2 dataset can be downloaded from the website333http://www.cad.zju.edu.cn/home/dengcai/Data/TextData.html. TDT2(B) discriminates between the first 15 classes and the remaining ones. The total number of samples and the dimension of each sample are listed in Table3.

We choose the optimal value of parameter via the 3-fold CV using 20 random runs, which are determined by varying it on the grid and the values with the best average Acc are chosen for each of the SSAG, S-Subgrad, SNSA, RS, and IPPA methods. We use the predetermined accuracy . We record in Table3 the parameter we find by the 3-fold CV, together with the corresponding average Acc of the computed solution and the average CPU time to find the computed solution in seconds. We can see that our SSAG method has the best average accuracy for all datasets. The CPU times of the SSAG method are faster than those of the other methods.

Table 3: Acc and CPU time determined by 3-fold CV on three datasets with parameters

Dataset

()

ALG.

Acc

CPU

a8a(22696,123)

4.39e+08

SSAG

0.000

2000

0.8362

23.60

S-Subgrad

0.020

-

2000

0.8003

200.00

SNSA

0.000

6.16e-04

15058

0.8139

136.37

RS

0.000

10000

0.7623

200.00

IPPA

0.015

-

15130

0.8005

200.00

MnistData-10(B)(6996,784)

1.13e+09

SSAG

0.060

1000

0.8586

42.22

S-Subgrad

0.045

-

1000

0.8158

200.00

SNSA

0.050

1.88e-04

16795

0.8426

200.00

RS

0.050

1000

0.7978

200.00

IPPA

0.060

-

4664

0.8387

200.00

TDT2(B)(9394,36771)

1.18e+12

SSAG

0.060

3000

0.9906

47.08

S-Subgrad

0.040

-

3000

0.9425

200.00

SNSA

0.065

1.56e-04

29518

0.9626

198.74

RS

0.060

30000

0.8781

200.00

IPPA

0.060

-

6262

0.9573

200.00

4.2 DRPO

Risk management in portfolio optimization determines an optimal weight for each asset, by solving specific optimization problems reflecting the risk attitudes of the manager on known data samples [18, 22].

We consider the following distributionally robust portfolio optimization problem (Example 5.1 of [38]):

(58)

where is the random return rate of asset , and is the proportion of asset among all assets, .

The ambiguity set is described by moment constraints that rely on estimates of the mean and covariance matrix of the random vector; see Example 2.3 of [38] for detail. To be specific,

(59)

where denotes the set of all probability distributions over the support set ,

, , and . The mean and covariance matrix and are calculated through samples obtained from historical data.

Let . As in [38], through Lagrange dual and discretization, (58) can be approximately solved by

(60)

s.t.

where are independent and identically distributed samples in .

We employ the smoothing function (20) and obtain the smoothing problem of (60) as

(61)

s.t.

We use a historical daily return rate of stocks between January 2005 and July 2023 from National Association of Securities Deal Automated Quotations (NASDAQ) index222https://cn.investing.com, which contains samples. We denote the daily return rates of assets on the -th day as , where represents the ratio of the closing price to the opening price of the -th asset on the -th day for .

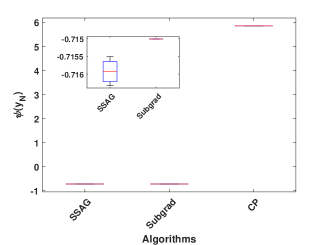

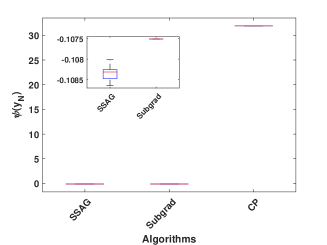

Three methods are employed to solve (60), and each method runs 20 times. We list the mean of objective value (Obj) in the training set, and the CPU time in Table4. Since Subgrad and CP are deterministic methods, the objective values of 20 times are the same, which leads “Obj Var” to be 0. It is clear that SSAG provides the computed solutions with the smallest “Obj Mean” for among all the methods.

The “Obj Var” is also very small.

Moreover, we can see from the last column of Table4 that the proposed SSAG method can obtain the desired objective value within 20 seconds, and the CPU time does not grow dramatically as the dimension increases, and the decreases. In contrast, the CPU time of the Subgrad method grows quickly as decreases. The CP method, however, can not obtain the desired value within the time budget 200s for all the cases.

Table 4: Obj and CPU time with parameters

ALG.

Obj

Obj

CPU

Mean

Var

0.01

2.04e+06

SSAG

100

-0.7045

1.17e-07

8.22

Subgrad

-

4675

-0.6944

0

33.82

CP

-

4675

5.8572

0

200.00

0.001

2.20e+07

SSAG

100

-0.7159

8.49e-08

10.71

Subgrad

-

4675

-0.7150

0

104.53

CP

-

4675

5.8572

0

200.00

0.0001

3.87e+08

SSAG

100

-0.7235

1.06e-07

11.88

Subgrad

-

4675

-0.7228

0

200.00

CP

-

4675

5.8572

0

200.00

0.01

2.03e+06

SSAG

100

-0.1347

3.68e-08

6.78

Subgrad

-

4675

-0.1334

0

39.68

CP

-

4675

31.9135

0

200.00

0.001

2.12e+07

SSAG

100

-0.1083

2.79e-08

11.96

Subgrad

-

4675

-0.1075

0

128.21

CP

-

4675

31.9135

0

200.00

0.0001

2.92e+08

SSAG

100

-0.1106

4.10e-08

17.92

Subgrad

-

4675

-0.1098

0

200.00

CP

-

4675

31.9135

0

200.00

Fig.3 draws the boxplots of Obj in the training data for all methods in 20 runs, when . Due to the similarity, we omit the figures of and . It is clear that our SSAG method performs much better than the others.

(a)

(b)

Figure 3: The boxplots of Obj in 20 runs, when .

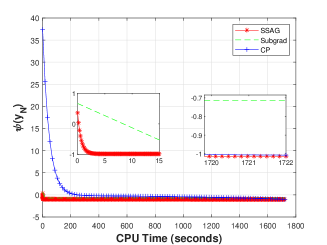

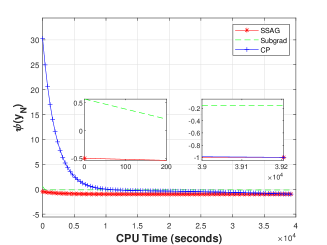

We also employ the same stopping criteria used in [38] for the CP method, and then run the SSAG method and the Subgrad method using the same CPU time as that for the CP method to stop.

We plot in Fig.4 the average Obj v.s. CPU time when the stopping criteria in [38] is employed. The two small inner figures are the enlarged beginning period and ending period of the large figure, respectively. We can observe that the SSAG method has the fastest descending speed. The Subgrad method fails to further reduce the objective value in the ending period. Eventually, the CP method obtains the optimal value, but it uses a much longer CPU time than our SSAG method.

(a)

(b)

Figure 4: Average Obj v.s. CPU time of 20 runs

5 Conclusions

In this paper, we propose a stochastic smoothing accelerated gradient method for solving nonsmooth convex

composite minimization problems. Various smoothing techniques can be employed to construct smoothing functions (Definition2.1) that also satisfy Assumption 2.1. We do not need the requirement that the nonsmooth component is of linear max structure as in [25, 35]. The requirement that the proximal operator of the nonsmooth component does not also need, compared to [7]. As far as we know, it is the first time to propose a stochastic smoothing accelerated first-order method to solve the constrained convex composite optimization problem whose nonsmooth term is the maximization of numerous nonlinear convex functions. The adaptive strategy for decreasing the smoothing parameter is also beneficial to faster computational speed. The complexity results match the best complexity results of the state-of-the-art SA methods using the first-order information. Moreover, the complexity results can be dimension-independent, unlike the complexity results of the RS method that are dimension-dependent. The effectiveness and efficiency of our SSAG method have been demonstrated by numerical results of distributionally robust optimization problems.

Acknowledgement.

We are grateful to Prof. Yongchao Liu of Dalian University of Technology, for providing us the Matlab code of the CP method used in [38].

References

[1]Z. Allen-Zhu, Katyusha: The first direct acceleration of

stochastic gradient methods, J. Mach. Learn. Res., 18 (2017),

pp. 8194–8244.

[2]J. Bai, W. W. Hager, and H. Zhang, An inexact accelerated stochastic

ADMM for separable convex optimization, Comput. Optim. Appl., 81 (2022),

pp. 479–518.

[3]J. Bai, D. Han, H. Sun, and H. Zhang, Convergence on a symmetric

accelerated stochastic ADMM with larger stepsizes, CSIAM Trans. Appl.

Math., 3 (2022), pp. 448–479.

[4]H. H. Bauschke, Projection algorithms and monotone operators, PhD

thesis, Simon Fraser University, 1996.

[5]A. Beck, First-order Methods in Optimization, SIAM,

Philadelphia, 2017.

[6]A. Beck and M. Teboulle, Smoothing and first order methods: A

unified framework, SIAM J. Optim., 22 (2012), pp. 557–580.

[7]W. Bian and X. Chen, A smoothing proximal gradient algorithm for

nonsmooth convex regression with cardinality penalty, SIAM J. Numer. Anal.,

58 (2020), pp. 858–883.

[8]J. Cervantes, F. Garcia-Lamont, L. Rodríguez-Mazahua, and A. Lopez,

A comprehensive survey on support vector machine classification:

Applications, challenges and trends, Neurocomputing., 408 (2020),

pp. 189–215.

[9]O. Chapelle, V. Sindhwani, and S. S. Keerthi, Optimization

techniques for semi-supervised support vector machines., J. Mach. Learn.

Res., 9 (2008), pp. 203–233.

[10]C. Chen and O. L. Mangasarian, A class of smoothing functions for

nonlinear and mixed complementarity problems, Comput. Optim. Appl., 5

(1996), pp. 97–138.

[11]X. Chen, Smoothing methods for nonsmooth, nonconvex minimization,

Math. Program., 134 (2012), pp. 71–99.

[12]K. Crammer and Y. Singer, On the algorithmic implementation of

multiclass kernel-based vector machines, J. Mach. Learn. Res., 2 (2001),

pp. 265–292.

[13]A. Defazio, F. Bach, and S. Lacoste-Julien, SAGA: A fast

incremental gradient method with support for non-strongly convex composite

objectives, NIPS, 27 (2014), pp. 1646–1654.

[14]J. C. Duchi, P. L. Bartlett, and M. J. Wainwright, Randomized

smoothing for stochastic optimization, SIAM J. Optim., 22 (2012),

pp. 674–701.

[15]S. Ghadimi and G. Lan, Optimal stochastic approximation algorithms

for strongly convex stochastic composite optimization I: A generic

algorithmic framework, SIAM J. Optim., 22 (2012), pp. 1469–1492.

[16]S. Ghadimi and G. Lan, Accelerated gradient methods for nonconvex

nonlinear and stochastic programming, Math. Program., 156 (2016),

pp. 59–99.

[17]S. Ghadimi, G. Lan, and H. Zhang, Mini-batch stochastic

approximation methods for nonconvex stochastic composite optimization, Math.

Program., 155 (2016), pp. 267–305.

[18]P. J. Kremer, S. Lee, M. Bogdan, and S. Paterlini, Sparse portfolio

selection via the sorted -norm, J. Bank. Financ., 110 (2020),

pp. 105687.1–205687.15.

[19]G. Lan, An optimal method for stochastic composite optimization,

Math. Program., 133 (2012), pp. 365–397.

[20]G. Lan, S. Lee, and Y. Zhou, Communication-efficient algorithms for

decentralized and stochastic optimization, Math. Program., 180 (2020),

pp. 237–284.

[21]J. Li, C. Chen, and A. M.-C. So, Fast epigraphical projection-based

incremental algorithms for Wasserstein distributionally robust support

vector machine, NIPS, 33 (2020), pp. 4029–4039.

[22]L. Martínez-Nieto, F. Fernández-Navarro, M. Carbonero-Ruz, and

T. Montero-Romero, An experimental study on diversification in

portfolio optimization, Expert. Syst. Appl., 181 (2021),

pp. 115203.1–115203.14.

[23]S. Melacci and M. Belkin, Laplacian support vector machines trained

in the primal, Journal of Machine Learning Research, 12 (2011),

pp. 1149–1184.

[24]A. Nemirovski, A. Juditsky, G. Lan, and A. Shapiro, Robust

stochastic approximation approach to stochastic programming, SIAM J. Optim.,

19 (2009), pp. 1574–1609.

[25]Y. Nesterov, Smooth minimization of non-smooth functions, Math.

Program., 103 (2005), pp. 127–152.

[26]L. M. Nguyen, J. Liu, K. Scheinberg, and M. Takáč, SARAH: A novel method for machine learning problems using stochastic

recursive gradient, ICML, (2017), pp. 2613–2621.

[27]B. T. Polyak, New stochastic approximation type procedures,

Automat. i Telemekh., 7 (1990), pp. 98–107.

[28]B. T. Polyak and A. B. Juditsky, Acceleration of stochastic

approximation by averaging, SIAM J. Control Optim., 30 (1992), pp. 838–855.

[29]S. J. Reddi, A. Hefny, S. Sra, B. Póczos, and A. Smola, Stochastic variance reduction for nonconvex optimization, ICML, (2016),

pp. 314–323.

[30]H. Robbins and S. Monro, A stochastic approximation method, Ann.

Math. Statist., (1951), pp. 400–407.

[31]A. Ruszczyński and A. Shapiro, Stochastic Programming

Models, Elsevier, Amsterdam, 2003.

[32]P. K. Shivaswamy and T. Jebara, Relative margin machines., NIPS, 19

(2008), pp. 1481–1488.

[33]M. Singla, D. Ghosh, and K. Shukla, A survey of robust optimization

based machine learning with special reference to support vector machines,

Int. J. Mach. Learn. Cyb., 11 (2020), pp. 1359–1385.

[35]R. Wang, C. Zhang, L. Wang, and Y. Shao, A stochastic Nesterov’s

smoothing accelerated method for general nonsmooth constrained stochastic

composite convex optimization, J. Sci. Comput., 93 (2022), pp. 1–35.

[36]X. Wang, S. Wang, and H. Zhang, Inexact proximal stochastic gradient

method for convex composite optimization, Comput. Optim. Appl., 68 (2017),

pp. 579–618.

[37]Z. Wang, Y.-H. Shao, L. Bai, C.-N. Li, L.-M. Liu, and N.-Y. Deng, Insensitive stochastic gradient twin support vector machines for large scale

problems, Inf. Sci., 462 (2018), pp. 114–131.

[38]H. Xu, Y. Liu, and H. Sun, Distributionally robust optimization with

matrix moment constraints: Lagrange duality and cutting plane methods,

Math. Program., 169 (2018), pp. 489–529.

[39]M. Xu and J. J. Ye, A smoothing augmented Lagrangian method for

solving simple bilevel programs, Comput. Optim. Appl., 59 (2014),

pp. 353–377.

[40]M. Xu, J. J. Ye, and L. Zhang, Smoothing SQP methods for solving

degenerate nonsmooth constrained optimization problems with applications to

bilevel programs, SIAM J. Optim., 25 (2015), pp. 1388–1410.

[41]C. Zhang and X. Chen, Smoothing projected gradient method and its

application to stochastic linear complementarity problems, SIAM J. Optim.,

20 (2009), pp. 627–649.

[42]C. Zhang and X. Chen, A smoothing active set method for linearly

constrained non-Lipschitz nonconvex optimization, SIAM J. Optim., 30

(2020), pp. 1–30.

[43]K. Zhou, Y. Jin, Q. Ding, and J. Cheng, Amortized Nesterov’s

momentum: A robust momentum and its application to deep learning, UAI,

(2020), pp. 211–220.