Second-Order Approximation of Limit Order Books

in a Single-Scale Regime

Abstract

We establish a first and second-order approximation for an infinite dimensional limit order book model (LOB) in a single (“critical”) scaling regime where market and limit orders arrive at a common time scale. With our choice of scaling we obtain non-degenerate first-order and second-order approximations for the price and volume dynamics. While the first-order approximation is given by a standard coupled ODE-PDE system, the second-order approximation is non-standard and described in terms of an infinite-dimensional stochastic evolution equation driven by a cylindrical Brownian motion. The driving noise processes exhibit a non-trivial correlation in terms of the model parameters. We prove that the evolution equation has a unique solution and that the sequence of standardized LOB models converges weakly to the solution of the evolution equation. The proof uses a non-standard martingale problem. We calibrate a simplified version of our model to market data and show that the model accurately captures correlations between price and volume fluctuations.

Key words. Second-order approximation, high frequency limit, limit order book, stochastic evolution equation.

2010 Mathematics Subject Classification. 60F17, 91G80.

1 Introduction

In modern financial markets the overwhelming majority of transactions is settled through electronic limit order books. A limit order book (LOB) is a record, maintained by a specialist or an exchange that contains unexecuted limit orders offering to buy or sell an asset at pre-specified prices that are multiples of a certain tick size. Incoming buy/sell limit orders can be placed at any price level above/below the best ask/bid price, and incoming market orders are usually matched against standing volume according to a set of precedence rules. In view of its inherent complexity, the detailed working of a LOB is difficult to describe.

Scaling limits allow for a tractable description of key macroscopic LOB quantities like prices and aggregate volumes in terms of the underlying (microscopic) dynamics of individual order arrivals and cancellations in a “high frequency” regime, when the number of order arrivals and cancellations tends to infinity. For a Markovian queuing model that describes an order book with finitely many price levels, diffusive high frequency limits for prices and/or volumes were for example obtained in [JA13, CdL13, CST10, HR17]. In [LRS17] the authors study a one-sided measure-valued order book model, for which the scaling limit is given by a diffusive price process together with a block-shaped order book for standing volumes. A more macroscopic perspective has been adopted in [KM16] and [Zhe12] where the order book dynamics is described in terms of a coupled system of SPDEs separated by a random interface that can be interpreted as the price (stochastic Stefan problem). An approximation by a reflected SPDE has been obtained in [HKN20]; cf. also [HK19, HK20] for a similar approach via a reflected moving boundary problem.

To provide microscopic foundations for PDE or SPDE order book models one needs to consider order books with an infinite number of price levels together with a tick size that converges to zero in the high frequency limit. Depending on the scaling assumptions fluid limits [GD18, HK17, HX19] and diffusion limits [BHQ17, HK18, HK19a, HX19, KM23] have been derived in the literature. In all of the aforementioned works, prices and/or volumes either follow a non-diffusive dynamics or the limiting dynamics is described by a SDE system driven by independent noise processes originating from the stochasticity of price movements and limit order placements, respectively. The independence of the driving processes contradicts many empirical findings that document a non-trivial correlation of price and volume increments, especially increments at the top of the book.

In this paper, we establish a first- and second-order approximation for LOBs where the second-order approximation can be described in terms of an infinite-dimensional stochastic evolution equation driven by correlated noise processes. The correlation operator can be identified by analyzing a novel infinite-dimensional martingale problem and explicitly represented in terms of the model parameters.

Following [HK18] we allow the LOB dynamics to depend on volume indicators such as the volume at the top of the book or volume imbalances between the bid and ask side. In that paper, starting from the first-order approximation derived in [HK17], the authors derive a second-order approximation for LOBs in which limit orders arrive at a much higher rate than market orders. If the first-order approximation of the price process is constant, they were able to rescale by a fast rate, in which case the limiting volume fluctuations could be described by an infinite dimensional SDE. With the first-order approximation of the price being constant, this choice of scaling describes the dynamics when the LOB is observed on a very fast time scale and over very short time periods during which volumes change but prices do not. Allowing for a non-degenerate first-order approximation of the price process required a slower scaling rate. In the slower scaling regime, the second-order approximation of the price process converges to a process with a mean-reverting component, while the volume dynamics converge to a PDE with random coefficients. This choice of scaling describes the LOB dynamics when the book is observed on a much slower timescale and longer time periods, where volume fluctuations average out but price fluctuations persist. In both scaling regimes the proportion of market orders and spread placements among all events (order arrivals and cancellations) is decreasing in the scaling rate and converges to zero in the scaling limit.

Accounting for the well documented fact that the proportion of market orders among all events does not vanish (unless one considers LOB dynamics over very short time intervals between two price changes), we consider a one-sided (for simplicity) LOB model in a single (“critical”) scaling regime in which prices and volumes change on a common time scale; in particular we allow for a fixed ratio of market to limit orders in the scaling limit. Our choice of scaling describes the LOB dynamics on intermediate time scales where neither price nor volume fluctuations average out. Our first-order approximation of the price-volume process is standard: the process converges to the solution of a coupled system of an ODE that describes the limiting price process, and a first-order PDE that describes the limiting dynamics of the standing volume. Our convergence concept is convergence in probability in a space of distributions, and is hence weaker than the one in [HP17] or [HK17], which accounts for change in scaling assumptions. The second-order approximation is non-standard. In our setting the rescaled price-volume process converges weakly to the unique solution of an infinite-dimensional linear stochastic evolution equation driven by additive noise with time-dependent covariance structure. We identify both the drift and the covariance operator that both depend on the first-order approximation, and prove that the limiting equation has a unique mild solution induced by a time-dependent evolution family. Identifying the drift and covariance operator is not straightforward as there are no canonical candidate for the said operators. Instead, we identify the operators by analyzing the limit of a sequence of martingale problems associated with the approximating LOB models.

To gain additional insights into the price-volume correlations we consider a simplified model where the second-order price approximation is a martingale and where the total standing volume acts as volume indicator. In this case the second-order approximation conveniently reduces to a two dimensional Ornstein-Uhlenbeck process whose covariance structure can be explicitly computed. In particular, price-volume fluctuations would be independent if the driving Brownian motions were independent. This highlights the importance or correlated noises. The explicit computation suggests that volumes at the top of the book are a key determinant of price-volume fluctuations. This confirms many empirical findings that show that volume imbalances at the top of the book (in a two-sided model) are an important determinant of price movements; see [CH15] and references therein for details. We calibrate the simplified model to market data using one-day order book data of the Deutsche Telekom AG stock and show that our model adequately captures the correlation in price-volume fluctuations.

To arrive at the second-order approximation, we face several mathematical challenges, many of which originating from the fact that volume functions shift in space when prices change. This prevents an immediate invocation of standard Grönwall-type arguments to establish moment estimates and hence tightness for our price-volume dynamics. To bypass this problem, by analogy to the linear transport equation, we rewrite the dynamics of the volume function along the stochastic characteristic corresponding to the stochastic dynamics of the best bid price process. We first establish pathwise growth estimates for the volume fluctuations in terms of submartingale increments starting from time zero by linearizing the dynamics of the residual terms and only then invoke Grönwall arguments. Subsequently, we establish suitable moment estimates for the submartingale increments that allow us to deduce tightness bounds. Finally, an application of Mitoma’s theorem guarantees the weak convergence of the second-order approximation to a distribution-valued process in the Skorokhod space.

To identify the limiting dynamics we express the discrete LOB dynamics in terms of discrete martingales, linearize their coefficients and employ the obtained moment estimates to control the difference between the discrete martingales and their continuous counterparts. These bounds together with tightness provide us with the desired limiting dynamics of the fluctuations in terms of a martingale problem. Notably, our choice of scaling results in a state-independent covariance operator, while the drift operator is linear in the state variable. Altogether, the second-order approximation is given in terms of a linear stochastic evolution system with additive noise, which we show to have a unique mild solution in the framework of stochastic evolution equations induced by a time-dependent evolution family.

Martingale problems are a powerful tool to characterize scaling limits of stochastic processes. In the context of market microstructure, martingale problems have been formulated to derive scaling limit of a finite-dimensional multiscale queueing model in [BC13] and to characterize the Hilbert space-valued limit of microstructure models driven by Hawkes random measure in [HX19]. A measure-valued deterministic LOB limit has been obtained in [GD18], where the martingale problem formulation of the microscopic dynamics has been considered, but the martingale part vanishes under their scaling. To the best of our knowledge, the martingale problem approach has not been applied for Hilbert space-valued approximations of market microstructure models with infinite-dimensional driver. However, this approach has been used extensively for SPDE approximations of interface growth models and interacting particle systems, cf. for example [LV94, BG97, EL15].

The remainder of this paper is structured as follows: in the next section we introduce the modelling framework and establish the first-order approximation. We introduce the stochastic evolution equation corresponding to the second-order approximation, prove its well-posedness and state our main convergence theorem. Thereafter, we calibrate our model to market data, derive testable implications from our theoretical analysis, and verify them within the calibrated model. In Section 3 we prove some auxiliary results about the discrete LOB dynamics. In Section 4 we first derive pathwise growth estimates, which allow us to deduce the aforementioned moment estimates. In Section 5 we prove tightness of the sequence of discrete order book models and establish martingale relations under the limiting measure, which establishes convergence to the unique mild solution of the system describing the second-order approximation.

Notation. For real numbers and we write whenever there exists a positive constant such that . If the constant depends on some other parameter , then we write .

For a Banach space we denote by and the space of continuous and càdlàg -valued processes, respectively.

For we denote by the classical Sobolev space . For the Sobolev spaces of negative order are dual spaces of endowed with the norm

where is a complete orthonormal system of . We also consider Sobolev spaces of fractional order defined on the torus with the norm

Also note that

For a scaling parameter and a given time interval we put and . For we write . Furthermore, we introduce the translation operators which act on a function according to

| (1.1) |

and introduce the left and right finite differences . Note that for any ,

| (1.2) |

2 Model and main results

Our goal is to derive a second-order approximation for the sequence of limit order book models introduced in [HK17] in a single-scaling regime where the inverse trading frequency, the tick size, and the average size of a limit order placement/cancellation are all scaled by the same scaling parameter . We prove that the second-order approximation can be described by a stochastic evolution equation with linear drift and time-dependent diffusion operator and calibrate a simplified version of our model to market data.

2.1 The microstructure model

Following [HK17] and [HK18], we assume that the dynamics of the buy side of the limit order book in the -th model is described by a càdlàg, -valued stochastic process

supported on a filtered probability space . The -valued component of the process corresponds to the best bid price dynamics, while the -valued component corresponds to the dynamics of the relative buy side volume density function which indicates the liquidity available at different price levels, relative to the best bid price.

At the initial time the state of the limit order book is deterministic and denoted by

The state of the book changes, due to incoming market and limit orders and cancellations. In the -th model there are such events taking place at times

where . The state of the book after events is denoted by the piecewise constant, continuous-time interpolation is given by

Orders can be submitted at the relative price levels for . The -valued volume density function is a càglàd step function on the price grid . The standing volume available at time at the relative price level , that is, at the price level ticks below the best bid is given by

| (2.1) |

Remark 2.1.

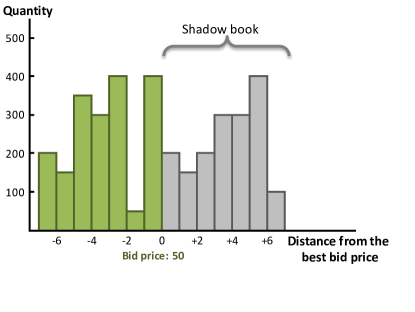

We emphasize that the volume density functions are defined on the whole real line to model the arrival of spread placements; see Figure 1. The restriction of the function to the interval corresponds to the actual buy side of the order book at time ; the restriction to the positive half line corresponds to the shadow book, which specifies volumes placed into the spread should such events occur next; we refer to [HP17, HK17] and references therein for further details on the working of the shadow book.

At each time , one of the three following events occurs, changing the buy side of the limit order book:

-

(A)

placement of a sell limit order of the size into the spread one tick above the best bid price. In this case the best bid price increases by one tick, and the relative volume density function shifts one tick to the left.

-

(B)

arrival of a market buy order of size , which removes the entire volume at the top of the book. In this case the best bid price decreases by one tick and the relative volume density function shifts one tick to the right.

-

(C)

placement/cancellation of a buy limit order of size at the relative price level (cancellation corresponds to ).

Following [HP17, HK18] we call an order an active order if it changes the price (events (A) and (B)) and a passive order if it does not (event (C)).

The assumption that incoming market orders match precisely against the liquidity at the top of the book has also been made in [BHQ17, HK18, HK19a, HK17, HX19, KM23]; it is made primarily for mathematical convenience. There is some empirical evidence, though, that this assumption is not too restrictive. In an empirical study the authors of [Far+04] found that in their data sample around 85% of the sell market orders that lead to price changes match exactly the size of the volume standing at the best bid price.

The randomness in the -th model is coming from a field of random variables

The random variable corresponds to the type of the event taking place at time . The random variable determines the relative price level of the placement/cancellation of the limit order of size in case . It is more convenient to work with a real-valued random variable such that , so that the discrete dynamics can be equivalently described in terms of

For we introduce the shorthand notation . The volume density increments can thus be described in terms of the placement operator

In terms of the translation operators defined in (1.1) the discrete dynamics can thus be summarized by the following stochastic difference equations:

| (2.2) | ||||

In what follows, we allow the order flow dynamics to depend on a volume indicator of the form

where is supported on . For example, the volume indicator can extract the volume standing at the top of the book. In this way one can account for the empirically well-documented fact that volumes at the top of the book (and volume imbalances in a two-sided model) are important determinants of price movements.

2.2 Assumptions and first-order approximation

Our key assumption is that the main model parameters – the tick size, the time between order arrivals, and the average limit order size – scale by the same parameter . In particular, we do not require a vanishing proportion of active orders in the scaling limit as in [HP17, HK17, HK18].

Remark 2.2.

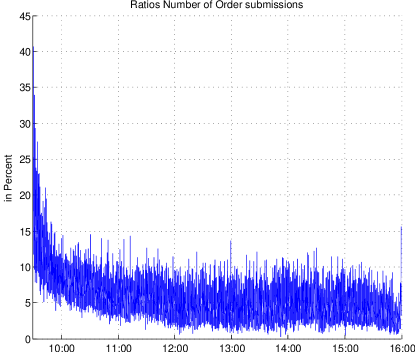

The assumption of a vanishing proportion of active orders is difficult to justify empirically as shown by Figure 2. This figure displays the intraday evolution of the proportion of spread placements among all orders for all NASDAQ traded stocks for the month of March 2016. We see that the proportion of spread placements is quite high when markets open and then varies around 5% for the rest of the day.

We also require a series of (mild) assumptions on the conditional order arrival dynamics. To state our standing assumptions we define, for every and the -fields and denote the corresponding filtration .111We note that is not the market filtration as it also contains information about the shadow book and thus about future spread placements. However, Assumptions H3, H4, H5, and H6 below guarantee that this extra information does not enter the LOB dynamics. Moreover, for a given function we set

We fix a number large enough so that the assumptions below are consistent with the properties of the LOB we are modelling. We start with the following standard assumption on the initial states of the book.

Assumption H1.

For all the initial volume density functions are non-negative step functions with step size , which satisfy the following conditions:

-

(H1.1)

are supported on for all ;

-

(H1.2)

are uniformly bounded in the uniform norm:

-

(H1.3)

There exist and a function such that

We assume that placements and cancellations take place at a finite distance from the best bid price and that placed volumes are almost surely bounded.

Assumption H2.

For all and it holds that:

-

(H2.1)

The order placement price is bounded a.s.: ;

-

(H2.2)

The order volume is bounded a.s.: .

The next assumption states that conditional distributions of the random variables which determine the price level of a limit order placement/cancellation depend on the history of the LOB only through the current best bid price and volume indicator.

Assumption H3.

There exist functions such that

-

(H3.1)

The next assumption states that conditional distributions of the next event depend on the history of the LOB only through the current best bid price and volume indicator and that there exists a function with bounded derivatives corresponding to the mean price imbalance of the limiting system.

Assumption H4.

For there exist functions such that

-

(H4.1)

;

-

(H4.2)

For any it holds that

-

(H4.3)

The function is twice continuously differentiable in both arguments, and

We introduce the notation

If there is no confusion, we drop the superscript denote the (conditional) mean price imbalances by

We specify an analogous assumption for the first conditional moment of the order flow.

Assumption H5.

There exist functions such that

-

(H5.1)

;

-

(H5.2)

The functions are uniformly bounded in the uniform norm

-

(H5.3)

The function is twice continuously differentiable and

-

(H5.4)

For any it holds that

Finally, we specify an analogous assumption for the second conditional moment of the order flow.

Assumption H6.

There exist functions such that

-

(H6.1)

;

-

(H6.2)

The functions and are uniformly bounded in the uniform norm

-

(H6.3)

It holds that

-

(H6.4)

The function belongs to for some .

Remark 2.3.

We emphasize that the speed of propagation of our system is bounded by 1 since . Since the initial volume density function is supported on , due to Assumptions H1.1 and H1.3 the first-order approximation introduced in Section 2.2 is supported on the trapezoid

Moreover, the discrete volume functions defined in (2.2) is also supported on , since again the initial volume density functions are supported on for all , due to Assumption H1.1, the order placement price is also supported on due to Assumption H2.1 and the volume density function shifts at most by one tick over the time increment . The same applies also to the volume fluctuations defined in Section 2.3 below. Therefore, by taking , in the following we reduce the problem to the compact set

consider test functions supported on , and assume that functions in for satisfy zero boundary conditions. Moreover, by Assumption H2.1 the functions and are supported on for all .

The above assumptions readily allow us to establish the following first-order approximation of our LOB model.

Proposition 2.4.

For any and any test function , it holds that

| (2.3) |

where the deterministic process satisfying

| (2.4) |

is the unique classical solution to the coupled Integro-ODE-PDE system

| (2.5) |

with initial condition , where is the volume indicator function.

Proof.

Our choice of scaling corresponds to the case in [HK17]. The proof is identical to the proof therein, except for the calculation at the bottom of p. 14, which needs to be adapted: for any function by Kondrachov’s embedding theorem it holds that

| (2.6) |

Thus, using Jensen and Hölder inequalities, Assumption H3.1, and (2.6) we observe that

| (2.7) | ||||

Using that and (2.7)

Hence, the volume fluctuations vanish as and so one can proceed further as in [HK17] by applying a weak law of large numbers for triangular martingale difference arrays. ∎

2.3 Second-order approximation

In this section, we describe the second-order approximation for our LOB model. To this end, we introduce the rescaled discrete fluctuation processes

| (2.8) |

along with the fluctuations of the volume indicator

| (2.9) |

The corresponding continuous time interpolations on are denoted by

and the initial value is denoted by

2.3.1 Limiting dynamics

In what follows we set . Our goal is to establish the weak convergence of sequence

in the Skorokhod space to the unique weak solution of the infinite-dimensional linear stochastic differential equation of the form

| (2.10) |

where and is an -valued cylindrical Brownian motion.

Since there are no canonical candidates for the drift and volatility operators, identifying the respective operators is challenging and will be achieved by an approximation argument in later sections. To specify the operators we use the following shorthand notation: given the first-order approximation of the price and volume indicator process process, we put

It turns out that the drift operators in (2.10) are defined as follows: for all ,

is an unbounded operator with time-invariant domain , and

is a linear operator given by

Remark 2.5.

Notably, the operators and are the same as in [HK18, Theorem 6.9], i.e. when rescaling the model on the slow time scale. Contrary to that result, though, our approximation preserves volume fluctuations in the limit.

We prove in Proposition 5.5 that the volatility operator belongs to . To explicitly define the operator we introduce the volatility function

It turns out that the diffusion operator is the square-root of the trace-class operator

whose components are defined in terms of the functions

and the family of linear operators ()

The key operator in our model is , which captures the correlations between the noise processes that drive price and volume fluctuations, respectively. We see that the correlations are mainly driven by differences in standing volumes, relative to the best bid price. Standing volumes relative to the best bid price change, due to price movements and placements/cancellations. The first effect is captured by the derivative , the second by the placement function .

2.3.2 Well-posedness of the stochastic evoluation equation and main result

In what follows, we show that the limiting equation (2.10) is well-posed and has a unique weak solution. To this end, we first formalize the notion of a solution to equation (2.10).

Definition 2.6.

An -valued continuous predictable process supported on the filtered probability space is called a weak solution to (2.10) if its trajectories are -a.s. Bochner integrable and for all and we have -a.s. that

| (2.11) |

Note that if we had , the operator would generate a -semigroup, which would amount to a translation at constant speed . The equation (2.11) would then be solvable, for example, in the classical framework of [DZ14, Section 7.1]. However, the differential operator in our equation varies over time, leading to a non-autonomous stochastic Cauchy problem.

Instead, our operator with the domain generates a unique strongly continuous evolution family in the sense of [VZ08]. We are hence required to work in the framework of evolution families instead of semigroups. In the absence of the drift , the existence, uniqueness and continuity of the unique mild solution as well as the equivalence between weak and mild solutions was established in [VZ08, Section 3]. Making use of those results, we can effortlessly accommodate the drift by a fixed-point argument.

We introduce the translation evolution family on given by (for ):

This is a strongly continuous evolution family generated by in the sense of [VZ08, Section 2.1]. Moreover, it holds . In the following proof we make use of Proposition 5.5 below, which establishes properties of the volatility operator, resulting from the martingale relations proved later.

Proposition 2.7.

There exists a unique weak solution to equation (2.11).

Proof.

It is well known that the bounded operator from into a Hilbert space is -Radonifying if and only if it is Hilbert–Schmidt. Since the covariance operator is Hilbert–Schmidt by virtue of Proposition 5.5, it satisfies the hypothesis of [VZ08, Theorem 3.3]. Therefore, it follows that the stochastic integral

is integrable and has a modification with continuous paths in . We now fix and define a map by

Note that since and is uniformly Lipschitz in with some constant , we have

so for small enough the map is a contraction on the space . In this case, taking

the unique fixed point yields the global mild solution with continuous paths:

Since the Lipschitz constant does not depend on the initial condition, we can iterate to obtain a mild solution on for arbitrary .

Hence, it suffices to prove that every weak solution is a mild solution. We proceed along the lines of [DZ14, Theorem 5.4]. Note that we have , i.e. for all the domain of the adjoint is given by , and the adjoint semigroup is given by . Consider first for some and . We get by Itô’s formula

Since the functions are dense in , the equality above holds for any . We fix and consider , so that . We get by stochastic Fubini theorem

Since is dense in , it follows that is also mild solution; hence each weak solution is unique. ∎

Armed with the preceding existence and uniqueness of solutions result, we are now ready to state the following second-order approximation that is the main result of this paper. It states that the fluctuations of the price-volume process converge in law to the weak solution of the said stochastic evolution equation. Note that convergence takes place in a negative Sobolev norm due to our tightness estimates.

Theorem 2.8.

The proof of the above theorem is split into several steps and is carried out in Sections 3–5. Before turning to the proof, we will briefly discuss the empirical implementation of our LOB model in the next subsection.

2.4 A simplified model with martingale price dynamics

To gain further insights into the dynamics of the price-volume fluctuations, we now analyze a simplified model where the infinite dimensional evolution equation (2.10) reduces to a two dimensional SDE. We explicitly compute the correlation structure and calibrate the model to market data.

2.4.1 Model

In what follows we consider a benchmark model, where the-first-order price approximation is constant and hence the second-order approximation is a martingale, that is, we suppose that

We consider the total standing volume as our volume indicator, i.e. we set In order to reduce the infinite dimensional dynamics to a finite dimensional system, we take

Moreover, we assume that the aggregated volume placement and cancellation function is independent of the price. Considering the total volume throughout the whole book, this assumption does not seem to be too restrictive.

Dropping the dependence of the volume dynamics on the constant first-order price approximation in what follows, the dynamics of the aggregate volume is given by

| (2.12) |

where

denotes the aggregated conditional first moment of order placements. Similarly, we denote the aggregated conditional second moment of order placements by

To determine the covariance operator, we also need the dynamics of the top-of-the-book volume, which is given by

If the first-order price approximation is constant, the covariance operator of the second-order approximation of conveniently reduces to a matrix

where

The second-order approximation reduces to a two-dimensional Ornstein-Uhlenbeck process

| (2.13) |

where and is a two-dimensional standard Brownian motion. In particular, the covariance structure is explicitly given by

| (2.14) | ||||

Some observations about the simplified model dynamics are in order: first, in out current setting price and volume fluctuations are correlated because the driving Brownian motions are. If the driving noises were independent as in [BHQ17, HK18, HK19a], the fluctuations were independent as well. Second, while we considered a one-sided book for simplicity, our analysis easily extends to two-sided books. In a two-sided book the variance of the price process would depend on the standing volumes on both sides, for instance on their difference. Third, price and volume fluctuations are correlated through the proportion of market orders and spread placements among all orders as well as through the volume at the top of the book. Since is bounded by one, the top of the book volume turns out to be the key determinant of price-volume correlations. The last two observations confirm many empirical findings showing that volume imbalances, especially imbalances at the top of the book are an important determinant of price movements.

2.4.2 Empirical implementation and correlation

Our simplified model easily lends itself to empirical calibrations. Our data set comprises time-stamped snapshots of the limit order book of Deutsche Telekom AG stock from Oct 18, 2022 from 11:30 to 17:00, traded at the Frankfurt stock exchange (FRA:DTE), resampled to the frequency of 1 second, thus amounting to samples. We collect limit order book data for 10 levels closest to the best bid/ask price, respectively. We consider the model dynamics over 3 minute intervals, which amounts to observations. Since the stock is traded with a tick size of €, we choose and hence in what follows. Moreover, we estimate the functions , , , and , using a simple linear model, i.e.

| (2.15) | ||||

Estimated coefficients for each side of the book reported in Tables 1 and 2, respectively.

| – | – | – | ||

| – | – | – | ||

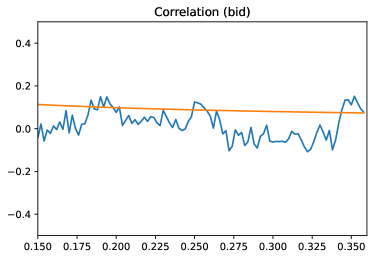

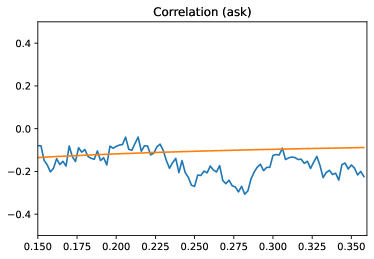

Slicing the time series into 3-minute windows, we calculate the sample correlation for each timestep of the window and contrast it to the mean (over all windows) of the correlation function , resulting from the covariance structure (2.14) with . The theoretically predicted correlations will clearly deviate from the sample correlations on short time intervals, due to the dependence on the initial data. As the model evolves the first- and second-order approximations approach equilibrium and it makes sense to compare predicted and the sample correlations away from the initial time. Figure 3 displays the predicted and the sample correlations on the time interval . Our (superficial) empirical analysis suggests that the sample correlations estimated from the data do indeed fluctuate around the mean correlation predicted by the model. Note, however, that the sample correlation is still quite noisy due to the small number of samples.

3 Properties of the discrete dynamics

In this section we establish a series of auxiliary results on the discrete models that will be used repeatedly in our subsequent analysis. We write and for any generic random variable such that in probability and for some , respectively, and for any generic constant which may vary from line to line.

For notational convenience, we introduce for any function , the short hands

Since

| (3.1) |

the dynamics of the volume fluctuations can be rewritten as

| (3.2) | ||||

The next proposition uses the above representation to rewrite the dynamics of the volume fluctuations along the stochastic characteristic given by the best bid price process.

Proposition 3.1.

For any with , the discrete scheme for the volume fluctuations can be rewritten as

| (3.3) |

where

| (3.4) | ||||

The term in the above decomposition corresponds to the initial value of the volume fluctuation profile shifted along the stochastic characteristic . The term corresponds to the difference between the transport term of the microscopic dynamics and the one of the deterministic first-order approximation. The term corresponds to the difference in the source contributions of the microscopic dynamics and the deterministic first-order approximation. To apply standard tightness criteria, we will have to derive moment estimates for all three terms. While this unproblematic for and , the challenge is to control the term as it apparently requires a priori bounds on itself. We will deal with this issue in Section 4.

Proof of Proposition 3.1.

We proceed by induction. For it follows from (3.2) that

Using the induction hypothesis, the desired result can be obtained as follows:

∎

The following lemma will be used repeatedly throughout the paper. It allows to pass from discrete coefficient functions to their continuous counterparts.

Lemma 3.2.

There exist real-valued random variables and , which converge to zero in probability uniformly in , such that for it holds that

Likewise, there exist -valued random variables and , which converge to zero in probability uniformly in , such that for it holds that

Proof.

We show the proof for the price drift only, the volume drift is handled analogously. Let

Applying a Taylor expansion yields that

where

It follows from Assumption H4.2 that . Moreover, due to Assumption H4.3 and the regularity of and , it follows that

| (3.5) |

Using the definition of we get that

| (3.6) |

Lastly, similarly to the proof of [HK18, Lemma 5.9], there exist random variables and converging to zero in probability uniformly in such that

∎

4 Growth estimates

In this section we derive moment estimates for the fluctuation processes. More precisely, our goal is to show that for any ,

| (4.1) |

This estimate for arbitrary will be used in the tightness proof in Section 5.1. Moreover, for , the estimate yields a growth estimate for the moments of the fluctuations, which will be used to establish martingale relations in Section 5.2.

To derive the estimate (4.1) for any , one would like to derive estimates on the increments of , which allow for an application of Grönwall inequality. However, the presence of the initial value contribution in the decomposition of the volume dynamics (cf. Proposition 3.1), which arises from the transport dynamics of the system, precludes us from directly applying Grönwall inequality to derive the above moment estimate for , since the growth of the volume fluctuation profile for cannot be controlled a priori.

To address this problem, we first provide pathwise estimates of and (cf. Lemmas 4.2 and 4.3). Subsequently we derive a pathwise growth estimate for in Proposition 4.5, relying on the assumption that the initial volume fluctuation profile is vanishing. This will allow us to control the initial value contribution and, ultimately, to obtain the moment estimate (4.1) in Proposition 4.8.

We first introduce shorthand notations for some martingales that will arise later in the decomposition of the fluctuation dynamics. For a fixed function and we define the processes

by

| (4.2) | ||||

Each of the processes above is a martingale starting at zero. For the sum of the -th powers of the said martingales we write

This process is a submartingale starting at zero.

4.1 Pathwise estimates

We first establish a pathwise estimate of the price fluctuations in terms of a discrete integral, a submartingale, and a residual term with the desired scaling.

Lemma 4.1.

Let and . Then

Next, we establish a pathwise estimate for the transport contribution in the decomposition of the volume fluctuations, cf. Proposition 3.1, in terms of a discrete integral, a submartingale, and a residual term with the desired scaling.

Lemma 4.2.

Let and . Then

Proof.

We consider the decomposition

|

|

By definition of , we have that

| (4.3) |

Using Hölder inequality and (1.2), we can write

Using Hölder inequality and (1.2), we obtain

Using Hölder inequality, Lemma 3.2, and (1.2), we have

|

|

Using Hölder inequality, (1.2), and (3.5), we obtain

Putting all estimates together yields the statement. ∎

It remains to establish a pathwise estimate for the quantity in the decomposition of the volume fluctuations, again in terms of a discrete integral, a submartingale, and a residual term with the desired scaling. The proof is similar to that of Lemma 4.2 above.

Lemma 4.3.

Let and . Then

Proof.

We consider the decomposition

By the definition of , we have

Using Cauchy–Schwarz and Hölder inequalities, the fact that whenever , and Assumption H2.2, we observe that

Using Lemma 3.2 and Hölder inequality, we obtain

|

|

Using Hölder inequality, due to (3.5) there exist random variables such that

Putting all estimates together yields the statement. ∎

Combining the three lemmata proven above, we obtain the following pathwise growth estimate for the fluctuations of both, price and volume.

Proposition 4.4.

Let and . Then

| (4.4) | ||||

We emphasize that the estimate in Proposition 4.4 contains the term on the RHS, which depends on the volume fluctuation . This precludes us from applying Grönwall inequality directly. To bypass this problem, we first consider the pathwise estimate for and . Then, we can apply the Grönwall inequality, since we know that the initial volume fluctuations are vanishing due to Assumption H1.3.

Proposition 4.5.

Let and . Then,

| (4.5) | ||||

| (4.6) |

4.2 Moment estimates

We close this section with a series moment estimates for the submartingale part appearing in Proposition 4.4.

Lemma 4.6.

For and , it holds that

| (4.11) |

Proof.

Using the definition (4.2), we obtain

Using the definition (4.2) and Hölder inequality, we obtain

Using the definition (4.2), Assumption H2.2, Cauchy–Schwarz and Jensen inequalities and (2.7), we observe that

|

|

Using Burkholder–Davis–Gundy inequality, Hölder inequality, and the above estimates, we obtain

∎

Finally, we are able to give an estimate on the term , which still appears on the RHS in Proposition 4.4.

Lemma 4.7.

It holds

| (4.12) |

Proof.

The final moment estimates now follows from a combination of the previous results.

Proposition 4.8.

For and , it holds that

| (4.15) | ||||

| (4.16) |

5 Martingale problem and weak solution

Using the moment estimates established in the previous section, we establish in this section the tightness of the price volume fluctuations and prove that any weak limit is continuous. Subsequently, we prove a series of martingale relation, both in the pre-limit and the limit. This allows us to show that the limiting dynamics can be obtained as a weak solution of our evolution equation by a martingale representation argument.

5.1 Tightness

We start by deriving from Proposition 4.8 an estimate for the moments of the dual Sobolev norm, which we will use to infer continuity of the limiting process.

Lemma 5.1.

Let . Then

| (5.1) |

Proof.

We now proceed to prove tightness of the fluctuation dynamics and continuity of the limit using the moment estimates from the previous section. To this end, we consider probability measures on the pathspace with canonical process denoted by , such that for all ,

Proposition 5.2.

The sequence is tight in and each limiting measure is supported on .

Proof.

Let us put , and consider an arbitrary sequence of bounded -stopping times and a vanishing sequence . By the Markov inequality and Proposition 4.8, we obtain for ,

| (5.4) | ||||

Thus Aldous’ criterion [Wal86, Theorem 6.8] implies tightness of the laws of in . Since is arbitrary, tightness in follows by Mitoma’s theorem [Wal86, Theorem 6.13]. Moreover, from Proposition 4.8, we obtain

| (5.5) |

Thus tightness in follows from (5.5) and Corollary 6.16 in [Wal86].

Let us denote by a weak limit of . By Skorokhod’s representation theorem there exists a filtered probability space

which supports random variables and such that

and

Therefore, there exist continuous bijections on such that and converges to uniformly. Using Lemma 5.1, we obtain

from which C-tightness follows by Kolmogorov’s continuity criterion. Moreover, since both processes are C-tight, the joint tightness in follows from Corollary C.4 in [BHQ17].

∎

5.2 Martingale relations

In this section, we will prove that for all the following processes are continuous square-integrable -martingales:

| (5.6) | ||||

To this end, we define discrete martingale relations, which are satisfied in the microscopic models, obtain moment estimates for the discrete martingales, and then deduce martingale relations under the limiting measure.

Let and be as in Section 5.1 and, as before, denote by the canonical process on the space .

5.2.1 Martingale relations in the pre-limit

In the discrete setting it is more convenient to work with the following discrete scalar product:

| (5.7) |

For any ,

Moreover, we can rewrite the discrete scalar product in terms of the step function approximation

Since by construction –a.s., we conclude from Proposition 4.8 that for any ,

| (5.8) | ||||

Thus, the moment estimates from the previous section apply mutatis mutandis to the discrete scalar product.

Our next goal is to define discrete drift and covariance operators for the discrete 2nd-order approximation. To this end, we first introduce the discrete version

of variance function introduced in Section 2 and proceed by computing the building blocks of the desired drift and covriance operator. Using Assumption H6.1 we obtain

| (5.9) | ||||

Moreover, using that active and passive events are disjoint, we have

| (5.10) | ||||

Also note that

| (5.11) |

Recalling that by definition, -almost surely, we define the discrete drift operators

and discrete covariance operators

Altogether, the definition of the discrete dynamics (2.2), the first-order approximation (2.5), the definition of the fluctuations (2.8) and (2.9), and equations (3.2), (5.9), (5.10), and (5.11) imply that the following are -martingales:

| (5.12) | ||||

where the remainder terms are , uniformly in .

The next proposition proves the integrability of the martingales defined in (5.12) and their convergence towards the continuous counterparts defined in (5.6).

Proposition 5.3.

Let .

-

(i)

The following uniform bounds hold:

(5.13) (5.14) (5.15) (5.16) (5.17) -

(ii)

The following convergence results hold:

(5.18)

Proof.

We proceed in various steps, analyzing the , , , , and part separately.

The part. We write

Using Jensen inequality and Lemma 3.2, we conclude by Proposition 4.8 that

| (5.19) |

Using Jensen inequality, Lemma 3.2, Proposition 4.8 and Assumptions H4.2 and H4.3, we have for all , , and some ,

| (5.20) |

This establishes the first bound in (5.13). The second bound in (5.13) follows from (5.19) and (5.20).

The part. We write

with

Using Cauchy–Schwarz inequality and noting that the first factor below vanishes due to (5.19) and the second factor is uniformly bounded due to (5.13), we obtain

Using Jensen inequality and Lemma 3.2, we conclude by Proposition 4.8 that

Overall, we have

| (5.21) |

Using Lemma 3.2, Proposition 4.8, Assumptions H4.2 and H4.3 and (5.20), we have for all , , and some ,

| (5.22) |

This establishes the first bound in (5.15). The second bound in (5.15) follows from (5.21) and (5.22).

The part. We write

with

It follows from (5.8) that

Using Jensen inequality, Lemma 3.2, Young inequality and Proposition 4.8, we obtain

By Hölder inequality, (1.2), Proposition A.1, and Proposition 2.4, we have

Using Jensen inequality, Hölder inequality, and Proposition A.1,

Note that we can write

The terms in the first two lines can be controlled using the regularity and integrability of the first-order approximation, cf. Proposition 2.4. The terms in the last two lines can be controlled with Lemma 3.2 and (1.2). Overall, we get from Proposition 4.8 that

vanishes analogously to . Altogether, we obtain

| (5.23) |

The part. We can write

with

Using Cauchy–Schwarz inequality, noting that the difference term vanishes due to (5.23) and that the sum term is uniformly bounded due to (5.14), we obtain

Other residuals vanish via calculations similar to the proof of the part. Overall, we obtain

The part. We can write

with

Again, using Cauchy–Schwarz inequality and , noting that the difference term vanishes due to (5.19) and (5.23) and that the sum term is uniformly bounded due to (5.13) and (5.14), we obtain

Again, other residuals vanish with calculations similar to the proof of the part. Overall, we obtain

∎

5.2.2 Martingale relations in the limit

In order to show that the martingale relations are satisfied under the limiting measure, we employ [JS03, Proposition IX.1.12], cf. Theorem B.1 in the appendix.

Proposition 5.4.

For any , all processes defined in (5.6) are continuous square-integrable –martingales.

Proof.

We only show the proof for for a fixed . The proof for other processes is analogous. To this end, we want to apply Theorem B.1. Denote by the canonical process on and . Then, it holds that and condition (ii) of Theorem B.1 is trivially satisfied. The uniform integrability of the family follows from Proposition 5.3(i) and the de-la-Vallée-Poussin criterion. Thus, condition (i) is also satisfied. Note that by Proposition 5.2, the law is supported on , which allows to deduce the validity of condition (iii) from the definition of . Moreover, this also implies the continuity of the limiting process . Finally, condition (iv) is satisfied by the virtue of Proposition 5.3(ii). Square-integrability follows by Proposition 5.3 and Fatou’s lemma. ∎

5.3 Proof of the main theorem

In this subsection we show that the limiting dynamics can be obtained as a weak solution of the evolution equation (2.10) by a martingale representation argument. To this end, we construct a cylindrical Brownian motion on the probability space satisfying the martingale relations (5.6) using an appropriate representation theorem. We first need to ensure that the variance operator is positive and trace class as required for the quadratic variation of a Hilbert space-valued martingale. This can be directly deduced from the obtained moment estimates of Section 4.

Proposition 5.5.

For all , the operator is non-negative and is a trace-class operator. In particular, the square root of exists, i.e. , and is a Hilbert-Schmidt operator for each with .

Proof.

Note that for , we have

Thus, the operator is non-negative for all . Recall from Remark 2.3 that we may restrict the space variable to and, hence, let us consider the orthonormal basis of . We have for ,

| (5.24) |

Using non-negativity of , Assumptions H4.3, H5.3, H6.4, (5.24), and Young inequality, we obtain

| (5.25) | ||||

Therefore, considering an orthonormal basis of , we have

uniformly in , i.e. and thus also are trace class operators. Moreover,

Thus, is a Hilbert-Schmidt operator, and since the bound is uniform in it follows that

∎

We are now ready to prove the main result of the paper.

Proof of Theorem 2.8.

We want to apply Theorem B.2 with . Consider as a linear map

Using non-negativity of , Hölder inequality, Assumptions H4.3, H5.3, H6.2, and Proposition 2.4, it follows that

| (5.26) |

Using Doob’s inequality, Itô’s isometry, and (5.26), we have for all ,

| (5.27) |

Since is a linear operator and , the space of all continuous, -valued, square-integrable martingales, is complete, by density we can extend to such that (5.27) holds for all , i.e. for all . For an orthonormal basis of , we define a process and its approximations for all . Obviously, , i.e. each is a continuous, -valued, square-integrable martingale. Using Parseval’s identity, monotone convergence, Doob’s inequality, and (5.25), we obtain

Since is a Banach space, we have . By Proposition 5.5, for all the operator is trace class. Thus we can define an -valued martingale with quadratic variation given by

By Proposition 5.5, for all the operator is Hilbert-Schmidt. Thus by Theorem B.2, there exists an extended filtered probability space which supports an -valued cylindrical Brownian motion such that -a.s.

| (5.28) |

Moreover, since the martingales defined in (5.6) are linear in , it holds -a.s. for any and that

| (5.29) |

Since is a cylindrical Brownian motion over , by pathwise uniqueness of , cf. Proposition 2.7, the relation (5.29) holds for all , which concludes the proof.

∎

Appendix A Growth estimates on the discrete LOB dynamics

In the proof of the moment estimates in Section 4, we need the following uniform growth estimates on the discrete state dynamics.

Proposition A.1.

For any , it holds that

| (A.1) |

Proof.

We only show the proof for the volume dynamics. The estimate for the price dynamics is obtained similarly, but the proof for the volume dynamics is more involved. Since only events of type contribute to the change in the volume profile (other events merely shift it), it is more convenient in this context to work with absolute volume density functions

so that the events of type and can be omitted, while .

Preliminaries. Note that with

it holds that

| (A.2) |

Denote . Then,

| (A.3) |

We list some estimates that we will use below. First, note that

| (A.4) | ||||

Also note that for , using the tower rule and the fact that is supported on a compactum, we can write

| (A.5) | ||||

Finally, note that

| (A.6) |

Induction proof. We want to show by induction that

| (A.7) |

For , using (A.4), (A.5) and , we have

Now we proceed to the induction step. Using (A.3), we can write

where is a partition of which depends on , such that

For and , using the tower rule, (A.4), and (A.5), we get that

Furthermore, using the tower rule, (A.6), and (A.4), we obtain for

Moreover, using (A.4) we obtain for

Thus, it follows that

| (A.8) |

Using that , , , , the constraint , and Assumption H5.2, we obtain

| (A.9) |

By the induction hypothesis, (A.8) and (A.9), it follows that

Conclusion. Since we consider finite, due to (A.2) it follows that

Since the asymptotic estimate does not depend on and , the bound holds uniformly in and . ∎

Appendix B Auxiliary results

Theorem B.1 ([JS03], Proposition IX.1.12).

For each , consider a stochastic basis , on which there are defined an -valued, càdlàg process and a martingale . Furthermore, let be a càdlàg adapted process on the space , endowed with the usual augmentation of the filtration generated by the canonical process . Let be a dense subset of . Assume that:

-

(i)

the family is uniformly integrable;

-

(ii)

, where ;

-

(iii)

for all , the map is -a.s. continuous on ;

-

(iv)

in -probability for all .

Then the process is a martingale with respect to the canonical filtration generated by .

Theorem B.2 ([DZ14], Theorem 8.2).

Let and be separable Hilbert spaces. Assume that is an -valued, continuous, square-integrable martingale on a filtered probability space , starting from , with

for a predictable -valued process . Then, there exists a filtered probability space and a cylindrical Brownian motion with values in , defined on , adapted to , such that

where

References

- [BC13] Jose Blanchet and Xinyun Chen “Continuous-Time Modeling of Bid-Ask Spread and Price Dynamics in Limit Order Books”, arXiv:1310.1103 e-print, 2013

- [BG97] Lorenzo Bertini and Giambattista Giacomin “Stochastic Burgers and KPZ Equations from Particle Systems” In Communications in Mathematical Physics 183.3, 1997, pp. 571–607 DOI: 10.1007/s002200050044

- [BHQ17] Christian Bayer, Ulrich Horst and Jinniao Qiu “A Functional Limit Theorem for Limit Order Books with State Dependent Price Dynamics” In The Annals of Applied Probability 27.5, 2017, pp. 2753–2806

- [CdL13] Rama Cont and Adrien Larrard “Price Dynamics in a Markovian Limit Order Market” In SIAM Journal on Financial Mathematics 4.1, 2013, pp. 1–25 DOI: 10.1137/110856605

- [CH15] Gökhan Cebiroğlu and Ulrich Horst “Optimal Order Display in Limit Order Markets with Liquidity Competition” In J. Econom. Dynam. Control 58 Elsevier, 2015, pp. 81–100

- [CST10] Rama Cont, Sasha Stoikov and Rishi Talreja “A Stochastic Model for Order Book Dynamics” In Oper. Res. 58.3, 2010, pp. 549–563

- [Don64] W. Donoghue “On a Theorem of K. Maurin” In Studia Mathematica 24.1, 1964, pp. 1–5 DOI: 10.4064/sm-24-1-1-5

- [DZ14] Giuseppe Da Prato and Jerzy Zabczyk “Stochastic Equations in Infinite Dimensions” Cambridge: Cambridge University Press, 2014 DOI: 10.1017/CBO9781107295513

- [EL15] Alison M. Etheridge and Cyril Labbé “Scaling Limits of Weakly Asymmetric Interfaces” In Communications in Mathematical Physics 336.1, 2015, pp. 287–336 DOI: 10.1007/s00220-014-2243-2

- [Far+04] J. Farmer et al. “What Really Causes Large Price Changes?” In Quantitative Finance 4(4), 2004, pp. 383–397

- [GD18] Xuefeng Gao and S.J. Deng “Hydrodynamic Limit of Order-book Dynamics” In Probability in the Engineering and Informational Sciences 32.1, 2018, pp. 96–125

- [HK17] Ulrich Horst and Dörte Kreher “A Weak Law of Large Numbers for a Limit Order Book Model with Fully State Dependent Order Dynamics” In SIAM Journal on Financial Mathematics 8.1, 2017, pp. 314–343 DOI: 10.1137/15M1024226

- [HK18] Ulrich Horst and Dörte Kreher “Second Order Approximations for Limit Order Books” In Finance and Stochastics 22.4, 2018, pp. 827–877 DOI: 10.1007/s00780-018-0373-7

- [HK19] Ben Hambly and Jasdeep Kalsi “A Reflected Moving Boundary Problem Driven by Space–time White Noise” In Stochastics and Partial Differential Equations: Analysis and Computations 7 Springer, 2019, pp. 746–807

- [HK19a] Ulrich Horst and Dörte Kreher “A Diffusion Approximation for Limit Order Book Models” In Stochastic Processes and their Applications 129.11, 2019, pp. 4431–4479

- [HK20] Ben Hambly and Jasdeep Kalsi “Stefan Problems for Reflected SPDEs Driven by Space–time White Noise” In Stochastic Processes and their Applications 130.2 Elsevier, 2020, pp. 924–961

- [HKN20] Ben Hambly, Jasdeep Kalsi and James Newbury “Limit Order Books, Diffusion Approximations and Reflected SPDEs: from Microscopic to Macroscopic Models” In Applied Mathematical Finance 27.1-2 Taylor & Francis, 2020, pp. 132–170

- [HP17] Ulrich Horst and Michael Paulsen “A Law of Large Numbers for Limit Order Books” In Mathematics of Operations Research 42.4, 2017, pp. 1280–1312

- [HR17] Weibing Huang and Mathieu Rosenbaum “Ergodicity and Diffusivity of Markovian Order Book Models: A General Framework” In SIAM Journal on Financial Mathematics 8.1, 2017, pp. 874–900

- [HX19] Ulrich Horst and Wei Xu “A Scaling Limit for Limit Order Books Driven by Hawkes Processes” In SIAM Journal on Financial Mathematics 10.2, 2019, pp. 350–393 DOI: 10.1137/17M1148682

- [JA13] Aymen Jedidi and Frédéric Abergel “On the Stability and Price Scaling Limit of a Hawkes Process-Based Order Book Model” In Capital Markets: Market Microstructure eJournal, 2013

- [JS03] Jean Jacod and Albert N. Shiryaev “Limit Theorems for Stochastic Processes” Berlin, Heidelberg: Springer Berlin Heidelberg, 2003 DOI: 10.1007/978-3-662-05265-5

- [KM16] Martin Keller-Ressel and Marvin S. Müller “A Stefan-type Stochastic Moving Boundary Problem” In Stochastics and Partial Differential Equations: Analysis and Computations 4.4, 2016, pp. 746–790 DOI: 10.1007/s40072-016-0076-z

- [KM23] Dörte Kreher and Cassandra Milbradt “Jump Diffusion Approximation for the Price Dynamics of a Fully State Dependent Limit Order Book Model” In SIAM Journal on Financial Mathematics 14.1, 2023, pp. 1–51

- [LRS17] P. Lakner, J. Reed and F. Simatos “Scaling Limit of a Limit Order Book Model via the Regenerative Characterization of Lévy Trees.” In Stochastic Systems 7.2, 2017, pp. 342–373

- [LV94] C. Landim and M.E. Vares “Equilibrium Fluctuations for Exclusion Processes with Speed Change” In Stochastic Processes and their Applications 52.1, 1994, pp. 107–118 DOI: 10.1016/0304-4149(94)90103-1

- [VZ08] MC Veraar and Jan Zimmerschied “Non-autonomous Stochastic Cauchy Problems in Banach Spaces” In Studia Mathematica 185.1 Polish Academy of Sciences, Institute of Mathematics, 2008, pp. 1–34

- [Wal86] John B. Walsh “An Introduction to Stochastic Partial Differential Equations” In École d’Été de Probabilités de Saint Flour XIV - 1984 1180 Springer Berlin Heidelberg, 1986, pp. 265–439

- [Zhe12] Z. Zheng “Stochastic Stefan Problems: Existence, Uniqueness and Modeling of Market Limit Orders”, PhD thesis, Graduate College of the University of Illinois at Urbana-Champaign, 2012