Commitment and the

Dynamics of Household Labor Supply††thanks: This paper develops and supersedes our previous work in Chiappori et al. (2020). We thank the editor, Francesco Lippi, three anonymous referees, and seminar and conference participants in the Structural Econometrics Group at Tilburg, Essex, KU Leuven, the ISR/PSID, Porto, Wuppertal, Barcelona Summer Forum (Income Dynamics and the Family & Structural Microeconometrics workshops), SOLE, SED, the Labor & Marriage Markets workshop at Aarhus, the Gender & Family Webinar by CY Cergy, and the Econometric Society North American Summer Meeting at UCLA for helpful comments. We benefited from many discussions with Jaap Abbring, Richard Blundell, Jeff Campbell, Sam Cosaert, George-Levi Gayle, Krishna Pendakur, Luigi Pistaferri, and Michèle Tertilt.

Abstract

The extent to which individuals commit to their partner for life has important implications. This paper develops a lifecycle collective model of the household, through which it characterizes behavior in three prominent alternative types of commitment: full, limited, and no commitment. We propose a test that distinguishes between all three types based on how contemporaneous and historical news affect household behavior. Our test permits heterogeneity in the degree of commitment across households. Using recent data from the Panel Study of Income Dynamics, we reject full and no commitment, while we find strong evidence for limited commitment.

Keywords: Household behavior; Intertemporal choice; Commitment; Collective model; Family labor supply; Dynamics; Wages; PSID.

JEL classification: D12; D13; D15; J22; J31.

1 Introduction

Large amounts of commitment are necessary for investing in common assets, for producing goods at home efficiently, and for pooling risk across family members. By contrast, limits to commitment typically induce investments in private assets, prevent the partners from economically abusing each other, and offer a way out from a bad marriage. In this paper, we develop a lifecycle collective model of the household, through which we characterize behavior in three alternative regimes: full, limited, and no commitment. We show that current and past news affect behavior differently in each case and we propose a test that distinguishes between all three. Using recent PSID data, we reject full and no commitment, while we find strong evidence for limited commitment with large heterogeneity across households.

Consider two or more parties who interact repeatedly sharing risk, such as spouses who offer each other intra-household insurance (Mazzocco, 2007; Lise and Yamada, 2019), village households who transfer goods or income among them (Townsend, 1994; Ligon et al., 2002), workers who supply labor and firms that offer employment (Thomas and Worrall, 1988; Beaudry and DiNardo, 1991), or agents who trade assets (Kehoe and Levine, 1993; Alvarez and Jermann, 2000). The extent to which the parties commit to some future behavior is clearly crucial as it shapes the degree of risk sharing between them.

This paper investigates this issue from a household perspective. We follow the by now dominant approach to household behavior, the collective model (Chiappori, 1988, 1992), which relies on cooperative game theory. While in its static version this approach assumes that individuals reach Pareto-efficient agreements, its dynamic aspects are more complex. Although ex post efficiency is generally maintained, ex ante efficiency strongly depends on assumptions about the spouses’ ability to commit. Following Mazzocco (2007), the literature has considered three alternative modes of commitment. At one extreme, full commitment is assumed: the spouses commit to a plan that disciplines the sharing of resources regardless of shocks that may affect them differently (e.g. Chiappori et al., 2018). Full commitment has nice normative properties but its realism is disputable; in particular, there exists few (if any) legal ways to enforce this type of agreement. At the other extreme, no form of commitment is possible, and the relationship amounts to a sequence of short-term bargaining games (see Lundberg and Pollak, 2003, for a theoretical analysis, or Goussé et al., 2017, for an empirical application). Clearly, such models result in a high level of dynamic inefficiency; in particular, they imply very strong restrictions on the ability to share risk within the group.

In the middle are limited commitment models, in which the spouses commit to a plan up to the point that some shock reduces one’s individual welfare below their outside option (Mazzocco, 2007). They then renegotiate the plan or unilaterally switch to their outside option as in the case of unilateral divorce (e.g. Voena, 2015). Such models have mostly been developed in a non-cooperative context (Thomas and Worrall, 1988; Kocherlakota, 1996); as such, they typically require an infinite horizon for the existence of non-trivial subgame perfect equilibria. Yet, they admit a straightforward, cooperative interpretation; namely, they are ex ante efficient in a second best sense, i.e. taking into account the limitations that exist from the spouse’s ability to commit. Nevertheless, limited commitment models still assume quite a lot of commitment. For instance, if an agent’s outside option increases (although not enough to become binding), she will not try to renegotiate a better outcome, even though the static bargaining solution will have evolved in her favor.111In the non-cooperative setting of Thomas and Worrall (1988) or Kocherlakota (1996), partial commitment is enforced via the infinite horizon and the possibility of future retaliations in any period. In our finite horizon setting, only trivial subgame perfect equilibria exist, and partial commitment has to be assumed, in line with the mostly axiomatic approach of cooperative game theory. This point becomes clearer below.

Most studies of the dynamics of household behavior make specific assumptions about commitment; their predictions are thus dependent on such assumptions. Yet, a few papers develop comparisons between models (Mazzocco, 2007; Lise and Yamada, 2019). Relying on a parametric framework, these works try to identify the Pareto weight in each period and contrast its dynamics between full and non-full commitment. The goal of our paper is to propose a more direct, reduced form approach by focusing on which variables affect behavior in each (full, limited, no) commitment mode. Specifically, we do three things.

First, we characterize household behavior in each commitment mode. We establish that shocks to the economic environment of the family affect behavior differently in each case. The differences manifest via the Pareto weight on each person’s preferences that disciplines the sharing of marital surplus. In full commitment, shocks, whether current or past, do not affect the Pareto weight, which remains constant over time or across states of the world. In limited commitment, current shocks may shift the Pareto weight if they trigger a renegotiation; this depends on the history of the couple, therefore also on past shocks, because individual welfare from marriage is a function of the past sharing of resources in the couple. In no commitment, by contrast, current shocks shift the Pareto weight continuously regardless of past shocks or circumstances. These restrictions on the Pareto weight translate into analogous restrictions on family labor supply, as we establish subsequently.

Second, we show that the set of variables that enter the full commitment Pareto weight (for which neither current nor historical information matters) is nested within the set that enters the no commitment weight (for which current information matters but historical information does not), which in turn is nested within the set that enters the limited commitment weight (for which all information matters). Thus the direction of nesting is not what one would expect by the names of the commitment regimes alone. Nesting, a common recursive form across modes (which we derive), and natural exclusion restrictions from current and past news allows us to devise a test that, for the first time, separates the three regimes.

Our test is about the presence of effects from current and past shocks, as well as the sign of such effects. In limited commitment, current shocks to distribution factors (variables that enter the Pareto weight) affect behavior in a way that is tightly determined by the assignability of the shock. Consider a cash transfer to women (e.g. Armand et al., 2020). If the transfer triggers a renegotiation, the female Pareto weight should increase, raising her leisure and reducing her labor supply. By contrast, the male weight would decrease, reducing his leisure and increasing his labor supply. These asymmetric effects reflect a power shift in the couple, where favorable news empower its recipient and simultaneously weaken their partner. The renegotiation, however, depends on the individual welfare from marriage today, which depends positively on the Pareto weight until today, which is itself determined by previous renegotiations. Therefore, the Pareto weight has memory and past shocks to distribution factors matter for current behavior in the same asymmetric way between spouses as current shocks do. By contrast, history does not matter in no commitment and past shocks are bygones. Neither current nor past shocks matter in full commitment.

Third, we confirm that wages enter the Pareto weight naturally even though they are not conventional distribution factors (they also affect the budget set). We show that their bargaining effects (effects through the Pareto weight) are distinguishable from conventional income and substitution effects and can thus be used to test for commitment. This is appealing because wages are more easily available in household data than conventional distribution factors, they are assignable, and they typically vary considerably over time.

We implement our test empirically in a sample of married couples from the Panel Study of Income Dynamics in the US over the last two decades. Our main outcome of interest is individual labor supply in the household while our main source of shocks is male and female wage shocks. Our primary empirical exercise can thus be seen as one that investigates the dynamic effects of (current and past) wages on family labor supply.

We consistently reject full and no commitment. By contrast, we find strong evidence for limited commitment. Favorable shocks reduce one’s own labor supply and increase the partner’s; this is simultaneously true for current and historical shocks from multiple periods, precisely as limited commitment postulates. These effects, which cannot be explained on the basis of substitution, income, wealth, or tax adjustments, are consistent with power shifts in which favorable shocks improve the bargaining power of the recipient spouse. History matters under limited commitment, so shocks that shifted past bargaining power have lasting effects on behavior in a very specific way. This is exactly what we find in the data.

The simplest form of our test can be implemented fairly easily in reduced form, without parameterizing or estimating individual preferences. This is appealing because, on one hand, the test does not rely on a specific functional form for utility and, on the other hand, it can help quickly inform about commitment without simulating a rather involved dynamic model. However, estimation of parts of the underlying structure permits and reveals large heterogeneity in the degree of commitment across households. The overall evidence for limited commitment masks in fact that many couples exhibit full commitment (null bargaining effects), while others strongly exhibit limited commitment.

This paper contributes to the literature on household behavior and, in particular, to its intertemporal aspects. Bargaining and in particular collective models have recently become the norm in this literature. Voena (2015) develops a limited commitment labor supply model to study the impact of unilateral divorce. Fernández and Wong (2017) have a similar goal, though their choice of model is one of no commitment. Chiappori et al. (2018) develop a full commitment labor supply model to study the labor and marriage market implications of education choice. Lise and Yamada (2019) use a time use model with no commitment to study resource sharing. Foerster (2020) builds a household model with limited commitment to study how alimony affects parents’ welfare.222Bronson (2014) and Mazzocco et al. (2014) use limited commitment (LC) lifecycle models to study education choices and household specialization; Goussé et al. (2017) study home production under no commitment; Low et al. (2018) study welfare reforms with LC; Blasutto and Kozlov (2021) and Reynoso (2022) study how unilateral divorce affects cohabitation and the marriage market under LC; De Rock et al. (2023) study demand for housing in a LC setting. Chiappori and Mazzocco (2017) review the literature. While these excellent works select a priori the commitment technology available to agents (so their conclusions are conditional on that choice), we take a step back and test for the extent of commitment in married couples. As such, the closest paper to ours is the seminal work of Mazzocco (2007), who tests for full vs. non-full commitment based on whether current news affects consumption sharing. Lise and Yamada (2019) do similarly in a model with home production. They all find evidence for this and reject full commitment. While this is often seen as evidence for limited commitment, in reality these tests cannot separate no from limited commitment. By contrast, the test we propose distinguishes between all three alternatives based on the additional role of historical information. Moreover, our test is not only about the presence of effects from current and past news but also about the sign of such effects that is strictly disciplined by theory.333Other tests include Townsend (1994) in the context of risk sharing in village economies, Blau and Goodstein (2016) in a household context, and Walther (2018) in a setting with production inefficiencies. Lafortune and Low (2020) show empirically that home ownership affects the degree of commitment.

The test is motivated by our characterization of behavior across commitment modes. The paper thus also relates to the macro and development literatures that study transfers without commitment (e.g. Coate and Ravallion, 1993; Kocherlakota, 1996; Ligon et al., 2002; Dubois et al., 2008).444Our paper is also related to an expanding family literature in macroeconomics; see Doepke and Tertilt (2016) and Greenwood et al. (2017) for excellent reviews. Mazzocco (2007) and Adams et al. (2014) do similarly in a full information, collective household context without, however, considering all three regimes we analyze here.555Chiappori and Ekeland (2006) and Cherchye et al. (2007) characterize static collective behavior. However, there are alternative modes of behavior, e.g. cooperative models with asymmetric information (Ashraf et al., 2022), moral hazard (Kinnan, 2022), or general infinite horizon non-cooperative models, to which our test is not directly applicable.

The paper is finally related to the literature in labor economics that concerns the labor supply response to wages, particularly to the partner’s wages, as in Lundberg (1985) and Hyslop (2001); Bellou and Kaymak (2012), Blundell et al. (2016) and Wu and Krueger (2021) are recent contributions. Our distinctive feature is the focus not only on responses to current wages but also on dynamic responses to spousal wages multiple periods in the past.

The paper develops as follows. Section 2 illustrates the main ideas in a simple setting. Section 3 presents the full lifecycle model and the complete characterization of behavior. Section 4 presents the formal test for commitment, section 5 discusses its implementation, and section 6 shows the results. Section 7 discusses extensions and section 8 concludes.

2 Illustration of main ideas

This section illustrates the main ideas in a simple parametric framework with two periods , no discounting, and no savings. The next section relaxes these restrictions.

A household consists of two individuals, a male and a female, respectively subscripted by . Each partner has logarithmic indirect utility , where may be any assignable expenditure on goods or leisure; we will be more specific about this in section 3. Individual expenditure must satisfy the budget constraint in each period, where denotes the realization of ’s income at . Each spouse has in each period an outside option , which may depend on his/her current income realization. We will now derive individual consumption in each commitment case.

Under full commitment, the couple decides its full (contingent) allocation plan ex ante. Specifically, it solves a program of the form , subject to the budget constraint in each period and an ex ante participation constraint for individual , given by . Here is defined ex ante and may reflect the situation on the marriage market (as in Chiappori et al., 2018) or stem from some initial, cooperative bargaining game, e.g., over the partners’ expectations of future income.

If denotes the Lagrange multiplier on the last constraint, the household program can be written as , subject to the budget constraint in each period. is the multiplier on spouse 1’s utility. Equivalently, the household solves, in each period , the program subject to the budget constraint at , with solutions given by

| (1) |

The crucial point is that the Pareto weights, and , remain constant; in particular, they do not depend on the realization of individual income in any period.666Individual expenditure thus depends only on total income, not its individual realizations. This property, called the mutuality principle, characterizes efficient risk sharing, enabled by the full commitment assumption. Under log utility, this implies a constant share of total income accruing to each individual.

Limited commitment requires deriving the ex ante, second best optimal contract. Different cases must be distinguished, depending on whether some participation constraint in marriage is violated (and, if so, in which period) by the full commitment solution. For instance, if the latter satisfies all participation constraints, then it coincides with the limited commitment solution. Alternatively, if income realizations result in a second period constraint being violated by the first best solution (1), then the second period Pareto weight will be modified such that the constraint becomes exactly binding; as a result, the second period allocation will be affected by the second period income shocks.

A complete resolution is left to section 3; here, we simply focus on a particularly interesting case when a first period participation constraint is violated. For brevity, we let the outside options at be very low (so that second period constraints can be omitted). The ex ante, second best program can be written as , subject to the budget constraint in each period and the first period participation constraints , for . Suppose, now, that the full commitment solution (1) violates one participation constraint – say, of , namely , while the constraint of is satisfied. At the second best solution, spouse 1’s constraint must be binding; its Lagrange multiplier will be positive (while that on spouse 2’s constraint is nil) and depend on the income realization . The household program then becomes subject to the budget constraint in each period (details in appendix A). Its solutions are

and the expenditure shares at depend on the realization of period 1 income through . Technically, spouse ’s weight increases from to in period 1 following the binding constraint, and this change persists in the absence of new violations. Note that the model assumes quite a lot of commitment; the period 2 outside option may have increased, but not enough to bind, so the spouses do not try to further renegotiate. It is precisely this level of commitment that generates the memory property we describe.

Under no commitment, in the definition of ‘bargaining in marriage’ of Lundberg and Pollak (2003) and Pollak (2019), the spouses bargain in each period. Cooperative bargaining theory requires that, in each period, the allocation be Pareto efficient in the ex post sense; therefore the household in period maximizes a weighted sum of utilities , giving the solution

In order to determine the Pareto weights and the allocation of resources in each period, the model is solved backwards. In period 2, the allocation, as summarized by the weights , depends only on the period 2 bargaining framework, i.e. total income and the second period reservation utilities and .777The exact form of depends on the specific bargaining concept at play (Nash, Kalai–Smorodinsky, etc.), on which no assumptions are made beyond cooperation. In period 1, and the allocation depend on and , as well as on the expectations of individual future incomes , given , , but, obviously, not on the realizations of and .

Two remarks are due here. First, from a non-cooperative viewpoint, in any finite horizon model of this type, the only subgame perfect equilibrium leads to the above no commitment outcome. Second, the period 2 allocation does not vary with period 1 incomes. In period 2 the spouses play a static, cooperative bargaining game, the outcome of which depends only on current total income and outside options, as summarized by . None of the past period’s incomes matter anymore – bygones are bygones.

In summary, under full commitment, idiosyncratic income realizations cannot affect expenditure shares in any period. Under limited commitment, expenditure shares may reflect current realizations (if a current participation constraint is violated) and past ones (if those have modified the past Pareto weight but current realizations have left it intact). Under no commitment, idiosyncratic realizations in each period influence the expenditure shares for that period, but past ones influence neither current nor future expenditure shares.

3 Household lifecycle behavior

We now switch to our full setting, namely the lifecycle collective model in which forward-looking spouses make consumption/hours choices subject to idiosyncratic wage risk.

A household consists of a male () and a female () spouse, who get married at time and live for periods. In each period , each person enjoys utility from joint consumption and disutility from labor hours , as per individual preferences . We assume that has continuous first/second partial derivatives with , (disutility of work), and , (concavity); utility is not quasi-linear, a class of preferences for which we find no empirical support anyway.

The couple’s budget constraint, common across commitment alternatives, is given by

| (2) |

where is common financial assets at the start of the period and is the deterministic interest rate.888The extension to risky assets is straightforward and does not affect the subsequent discussion. Assets in marriage are jointly held reflecting the community property regime in the US (Mazzocco, 2007). maps gross household earnings into disposable income , accounting for joint taxation and benefits (e.g. EITC). is the (individual, stochastic) price of an hour of market labor and is the set of wages in the couple. We assume the spouses hold identical beliefs about future stochastic elements.

Both and individual utility depend on demographics, such as fertility. We suppress those here for brevity (we thus fix a household type), but we do account for them in the empirical application. Appendix A shows the role of demographics in the model explicitly.

3.1 Commitment modes

The next three subsections present the collective model in the three alternative commitment regimes. For now, we disregard divorce and thus model behavior conditional on continued marriage. Divorce is discussed in appendix A.

3.1.1 Full commitment

Upon marriage, the individuals commit fully to all future but state-contingent allocations of resources between them. In other words, they commit at to a plan that disciplines their actions in the future. Choices made under full commitment are therefore ex ante efficient and can be represented by the solution to the following problem at :

| (3) | ||||

| subject to the budget constraint (2) , |

where is the set of household choice variables in period . For brevity, we do not show their dependence on contingent states – we relegate this to appendix A.999We maintain a common discount factor between spouses; see Adams et al. (2014) for a generalization.

The Pareto weights and are the utility weights the household places on each person’s preferences at marriage. They determine ex ante the relative allocation of resources between spouses. is the set of variables that affect the Pareto weights; because the weights are determined at marriage, it follows that must only include information known or predicted at the time the household is formed, that is, at time .101010The discussion that follows only requires that some variables known at affect the Pareto weights at marriage; it does not require to specify why exactly this happens. One may think that the weights arise from a bargaining game played at marriage or from equilibrium conditions in the marriage market (e.g. Chiappori et al., 2018). In either case, information at (e.g. variables summarizing the marriage market) affects the Pareto weights; we thus allow and to depend on to reflect, in reduced form, such a link.

The expectations, common between spouses as we assume throughout, are taken over the stochastic elements of future states in , , such as future wages. Generally, the state space differs across commitment alternatives. We have purposefully not defined what explicitly goes into but we will return to this point in the following sections.

3.1.2 Limited commitment

When an individual can unilaterally walk away from their partner (e.g. unilaterally divorce), not all future allocations are feasible in all states of the world. Certain plans may make one person better off outside the household. Assuming there is always a positive marital surplus to be shared, the household must make sure to not implement those plans.

Upon marriage, the spouses commit to future and state-contingent allocations of resources up to the point that one’s marital participation constraint is violated. Choices under limited commitment are ex ante second-best efficient (ex ante efficient subject to participation constraints) and can be represented by the solution to the following problem at :

| (4) | ||||

| subject to the budget constraint (2) , and the participation constraints: |

where is the set of household choice variables in period and is the reservation utility of person at , defined over – more on this below.

The participation constraints, one per individual and time period, ensure that each person enjoys at least as much value inside their joint household as they can possibly get from their outside option, i.e. by walking away from the relationship. In other words, the participation constraints ensure individual rationality in the relationship. The constraints consist of two parts, the inside (left hand side) and outside (right hand side) values, defined on the basis of the forward-looking continuation value of each option.

The inside value of person reflects the share of marital surplus that accrues to him/her given the choices made by the household in the period. Naturally, this value varies with the applicable Pareto weight in the period: a larger Pareto weight on person implies household choices more tailored to ’s tastes, thus accruing a larger share of marital surplus to him/her, and vice versa. This link between the Pareto weight and the individual inside value from marriage disciplines the dynamics of the Pareto weight in limited commitment, a point to which we return in the next sections.

The outside value of person reflects how he/she may fare in life outside the current relationship; its precise form depends on specific assumptions about that situation. For instance, we may, as in Voena (2015), assume that the outside option is divorce, and that the corresponding value is the present value of future expected utility of a single/divorced person – in which case we have:

Here, we let preferences depend on marital status (i.e. may differ from ) to capture marital preference shifts. may include stochastic elements that reflect, in reduced form, the utility flow from possible future remarriage or grieving following the breakup.

Other interpretations are however possible and the precise form of does not matter for the subsequent discussion. The key aspect is that is defined over the (single’s) state space . Three distinct sets of variables enter , whose role we describe below: the individual wage rate (wages matter for ’s budget as single and for his/her labor market and possibly remarriage prospects), distribution factors , and marital assets . The expectations are taken over the stochastic elements of future states in , .

Distribution factors are exogenous stochastic variables that affect the singles’ lifecycle prospects but not preferences or the couple’s budget set conditional on household income (Bourguignon et al., 2009).111111Examples include relative non-labor incomes (e.g. Thomas, 1990; Attanasio and Lechene, 2014), the sex ratio in the marriage market (Chiappori et al., 2002), or divorce and property division laws (Voena, 2015). These variables thus affect the outside but not the inside options in the household. The difference between and is that the former variables vary during the course of the relationship while the latter do not. As the variables in vary stochastically over time, the single’s outside value varies in response, which may make a participation constraint occasionally bind. To satisfy the constraint, the inside value of the constrained spouse must adjust, thus creating a link from the time-varying distribution factors to the choices made in the couple as we illustrate subsequently.

Upon household break-up, financial wealth accumulated during marriage is split between partners according to some fixed rule. Marital assets thus determine the wealth that a newly single possesses upon break-up, so wealth enters ’s outside value at . This renders the outside options endogenous to choices made during marriage. A couple in our setting makes savings choices accounting for the implications of those choices for the outside options, in addition to the standard lifecycle/precautionary motives present also in full commitment.121212The dependence of the outside options on wealth may move the household away from second-best efficiency; for example, the couple may overinvest in financial assets to improve their outside options. Chiappori and Mazzocco (2017) have a lengthy discussion of this as well as of an interesting opposite case.

3.1.3 No commitment

While full and limited commitment feature some form of commitment at marriage to a future plan (the plan contingent on the Pareto weights at marriage and, in the case of limited commitment, the participation constraints), no commitment features no such marital ‘contract’. Upon marriage, the spouses do not commit to a future plan, that is, they do not guarantee each other a certain or minimum allocation of resources.

Without commitment, new information that arises over time changes the division of marital surplus between spouses according to the bargaining game they play. Choices under no commitment can be represented by the solution to the following problem at :

| (5) | ||||

| subject to the budget constraint (2) , |

where is the set of household choice variables in period .

The underlying premise of no commitment is that the spouses engage in some form of repeated bargaining over the marital surplus in a way that reflects the prevailing economic environment, captured by wages , distribution factors , and wealth . As new information arises over time, a person’s bargaining position shifts given the bargaining game played by the spouses. The variables in are fixed after marriage but they enter the Pareto weights because they may influence the type of game the couple plays.

Choices under no commitment are ex ante inefficient. This is because ex ante efficiency, at least in the first-best sense, implies that there exist no time-contingent transfers that improve both spouses’ expected utilities (Browning et al., 2014). This requires the Pareto weights be the same over time, which is clearly not the case here. Choices are dynamically inefficient also because the bargaining weights depend on wealth. The spouse whose future weight increases more with wealth has an incentive to overinvest in assets, thus creating inefficiencies over time. Whether such inefficiency appeals to couples is ultimately an empirical question that our test for commitment helps address. Nevertheless, choices in a given period are ex post efficient in the sense that they maximize a weighted sum of individual period utilities.

Our representation of no commitment (in particular how new information impacts the Pareto weights) is arguably abstract and lacks the precise microfoundations of full or limited commitment. Nevertheless, this abstractness enables it to be consistent with several popular underlying structures, such as resource allocations with Nash bargaining over the marriage market (Goussé et al., 2017), household sharing when labor market shocks shift the balance of power (Lise and Yamada, 2019), equilibrium allocations with bargaining over a default arrangement (Kato and Ríos Rull, 2023), and other. We return to this point below.

3.2 Common recursive formulation

The household problem in each commitment mode is a dynamic planning problem over the allocation of resources between spouses and across periods of time. Following Marcet and Marimon (2019), we can recast each problem in the common recursive form:

| (6) | ||||

| subject to the budget constraint (2), and | ||||

| restrictions on the Pareto weights , , defined subsequently, |

with details reported in appendix A. In each period, the household maximizes a weighted sum of period utilities, an appropriate continuation value, and an additional term described below. Expectations are over the stochastic elements in , given the realization of .

The additional term, , aggregates the singles’ endogenous outside options in limited commitment. It is given by in limited commitment, where is the Lagrange multiplier on spouse ’s participation constraint at , and by otherwise. highlights that a couple makes savings choices in limited commitment taking into account the effect of those choices on the partners’ outside options. Chiappori and Mazzocco (2017) provide a further discussion of this motive.

The solution to (6) is a set of time-consistent131313The policy functions depend on time because the horizon is finite. optimal policy functions , , , and , which depend on the state space in each commitment alternative. Our test for commitment relies on estimating equations derived directly from (6) and its corresponding policy functions, given restrictions that the Pareto weight imposes on the state space in each case. The crucial point in (6) is that there is a pair of applicable Pareto weights and in each period, the dynamics of which we will now characterize.

3.3 Characterization of the Pareto weight and the state space

Bargaining power is relative inside the household since the sum can be normalized to a constant. Therefore, we subsequently refer to the Pareto weight in singular. Moreover, any variable that affects one person’s Pareto weight must simultaneously and mechanically enter and affect the partner’s weight in the opposite direction.141414One can show this formally by explicitly including the restriction in program (6).

Full commitment. The Pareto weight is determined at marriage as a function of the initial bargaining variables . The weight remains constant over time, namely

as we show in appendix A. The variables in vary in the cross-section reflecting the couple’s characteristics at marriage, local marriage market conditions, or other heterogeneity that the individuals base their initial bargaining on. So also varies in the cross-section of households. includes at least one variable that improves ’s initial bargaining power () and, consequently, worsens that of the partner (). These bargaining variables remain fixed for after marriage, so also remains fixed within a given family over time. The initial weight at marriage thus serves as the spouses’ intra-household bargaining power over their entire lifecycle.

The time and state invariance of the Pareto weight (conditional on ) is a well-known implication of first-best efficiency (Browning et al., 2014). Intuitively, once the initial bargaining weight is set at marriage, future shocks (for example, shocks to wages) do not change the allocation of marital surplus between spouses, who fully share any idiosyncratic risk between them. Of course efficiency requires that the spouses exploit the economic opportunities that arise from variation in wages or other shocks; but with full commitment, those effects remain compatible with ex ante efficiency and the Pareto weight does not change in response. This implies that policies that seek to empower, say, women, e.g. cash transfers targeted to women, cannot affect the division of marital surplus if they are implemented after marriage. The only policies that matter under full commitment are those that affect .

Limited commitment. The Pareto weight is given by:

where is the Lagrange multiplier on spouse ’s participation constraint at . We derive this in appendix A. The Pareto weight shifts when the continuation of the previous allocation of resources, summarized by the past weight , violates one’s participation constraint. In such case, the constrained spouse’s weight jumps by , i.e. the multiplier on the binding constraint. If no participation constraint binds, then , and the Pareto weight remains unchanged. Whether a participation constraint binds depends on the variables underlying the constraint, so we may write as we explain below.

Consider the distribution factors. As shift the outside options, a person’s participation constraint may bind for some realization of . To relax the constraint, the constrained person’s bargaining power increases by , which shifts household decisions towards her preferences and improves her inside value. The increase in power is the smallest possible that makes indifferent between staying in the relationship and leaving. This follows from second-best efficiency as analyzed in Ligon et al. (2002).151515The present analysis is conditional on the spouses remaining married (marital surplus remains positive), so at most one participation constraint can bind in a given period (Kocherlakota, 1996). Therefore, following the increase in ’s power, there exists a feasible allocation at which her partner’s constraint is also satisfied.

Wages also impact the participation constraints, though their workings are more nuanced. While typically includes at least one variable that improves ’s outside option, increases her bargaining power () and symmetrically worsens the partner’s (), wages simultaneously affect ’s outside and inside values. An increase in , however, should improve ’s outside value more, because any value from wages inside the relationship must be shared with her partner. As her participation constraint may thus bind, we expect and, in turn, . The wage also affects the partner’s inside value through sharing; a wage rise loosens the partner’s constraint while a wage cut tightens it (both income effects), so like above.

Wealth also enters the participation constraints; but it does not clearly favor one party unless policies or explicit agreements dictate this (e.g. prenuptial contracts).

The extent to which a participation constraint binds in response to or depends on the person’s inside value, which, as we established earlier, varies with the applicable Pareto weight. Suppose is the Pareto weight at the start of period , after shocks manifest but before decisions are made in the period. A relatively larger implies a relatively larger share of marital surplus for , thus making her outside option less desirable for a given realization of or ; and vice versa. So whether ’s constraint binds at the start of period depends on . Consequently, and the updating of the Pareto weight upon decision making later on in the period also depend on it.

Where does come from? The nature of decision making is such that the participation constraints are always satisfied at the updated at the end of the period. No further updating takes place before decision making in the following period, therefore at the end of is also the applicable weight at the start of . By deduction, is therefore the weight that materialized at the end of . By the time of decision making in period , summarizes the history of the household through binding past constraints and renegotiations, which is an artifact of the recursive nature of the participation constraints. Intuitively, a given shock that improves ’s outside option will not trigger a renegotiation if has been ‘happy’ inside her relationship, that is, if she has historically earned a ‘good’ share of the marital pie. So certain shocks trigger renegotiation in certain histories but not in other. History is summarized by a single variable, , and conditional on it, older information does not matter for decision making today (Kocherlakota, 1996).

This step-like movement of the Pareto weight in response to binding participation constraints is a well-known feature of limited commitment (Mazzocco, 2007). The couple commits to the resource allocation enacted at marriage for as long as the participation constraints remain slack. Therefore, a given allocation and Pareto weight can be quite persistent. The spouses thus fully share risk up to the point when a renegotiation takes place to satisfy a constrained spouse. After the renegotiation, the new weight may itself persist until another constraint binds. The Pareto weight thus varies cross-sectionally but also longitudinally, within a given family. Policies that seek to empower women, e.g. targeted cash transfers, can thus be implemented during the relationship and may have lasting effects on the balance of power if they successfully improve women’s outside options. Persistence and history are features of limited commitment that we subsequently exploit for testing.

No commitment. The Pareto weight is determined in each period given the prevailing information in the period; by construction, it is given by

The Pareto weight varies with the initial bargaining variables , which influence the type of game the spouses play. It also varies with new information that reveals over time, i.e. shocks to wages and distribution factors (the bargaining effects of which are typically assignable), and assets. For example, an increase in should empower spouse () and simultaneously weaken her partner (). How precisely this is done depends on the exact bargaining game on which no assumption is made beyond cooperation.

The continuous response of the Pareto weight to contemporaneous information is a well-known feature of no commitment and cooperative bargaining (e.g. Lise and Yamada, 2019). The main implication is that the spouses cannot share risk efficiently as they cannot commit to transfer resources from one period to another. This lack of history, at least conditional on assets, makes the Pareto weight transitory in nature. It implies that policies that seek to empower women may be implemented during the relationship (e.g. by improving elements in or that are assignable to women) but their effect is temporary. As soon as the policy disappears, any gains in the Pareto weight also disappear. Lack of history stems from cooperative bargaining and the finite horizon of our setting, as we illustrated in section 2. This absence of history is a feature of no commitment that we exploit for testing.

State space. The policy functions derived from (6) vary with wages and assets , which affect the budget set in all commitment modes and, through it, the trade-off between consumption, savings, and work. The policy functions also vary with the applicable Pareto weight . In all alternatives, a relatively larger implies period choices that favor spouse , and vice versa. Consequently, the state space is given by , common across modes.161616In practice, only one person’s weight enters the state space because of the restriction . However, each commitment alternative imposes different restrictions on . For example, in full commitment is exclusively determined by the initial bargaining variables . We may thus replace in the state space with , so in this case. By a similar argument, the limited commitment state space is given by while the no commitment state space by . We show subsequently that these sets are nested, which enables us to test for the type of commitment.

3.4 Nesting and restrictions on household behavior

To understand how the different commitment modes are related, it is useful to pool together the corresponding Pareto weights, namely

where in limited commitment.

The limited commitment Pareto weight depends on its past value, which summarizes the history of the household from marriage until today. If observed and accounted for, is a sufficient statistic for the past (Kocherlakota, 1996). In practice, however, is unobserved. From its law of motion, we can substitute the past weight recursively until (marriage) to obtain . Unconditional on its past value, thus depends on the entire information set since marriage, which includes all historical wages , distribution factors , and assets , , that affected past participation constraints and, through them, the historical dynamics of bargaining power in the household. In other words, any variable that affects the unaccounted must also affect the Pareto weight today. Consolidating the variables that enter the limited commitment weight and reordering the modes, we obtain

which reflects the nesting of the sets of variables that matter for bargaining in each case.171717Let . To be precise, we should write in limited commitment, where is the reduced form of . To avoid unnecessary notation (namely the tilde), we reinstate as the reduced form of its structural counterpart.

Contemporaneous information (e.g. information in or ) does not matter for the Pareto weight in full commitment but it does matter in no and limited commitment. Full commitment is thus nested (in terms of the variables that matter for bargaining) within both non-full commitment alternatives, which is a well-known result since Mazzocco (2007). This implies that if contemporary variables affect the Pareto weight, this effect serves as evidence against full commitment. In other words, current information is a natural exclusion restriction that can help separate full from non-full commitment.

Historical information (e.g. information in or , ) does not matter for the Pareto weight in no (or full) commitment but it does matter in limited commitment. No commitment is thus nested within limited commitment, which is a new result in the literature. This implies that if historical variables affect the contemporaneous Pareto weight, this effect serves as evidence against no commitment. In other words, history is a natural exclusion restriction that can help separate no from limited commitment.

The problem with this approach is that the Pareto weight is unobserved. From the theory of dynamic programming, however, the optimal labor supply policies that solve (6) are functions of the state space . Therefore, the previous exclusion restrictions on the Pareto weight immediately become exclusion restrictions on the (typically observed) individual labor supplies and in the household, given by

for . This holds for all choices in the household; however, the assignability of labor supply allows us to exploit the properties of the so-called sharing rule.

The sharing rule summarizes the share of total income each spouse can devote to own expenditure in a given period. If leisure is a normal good and utility not quasi-linear (as we assume throughout), an increase in increases ’s leisure and decreases her supply of labor. Moreover, there is an one-to-one increasing relationship between ’s Pareto weight and share , therefore . This also implies as bargaining power is relative. In words, an improvement in ’s bargaining position increases her leisure and reduces her labor supply; in parallel, her partner’s bargaining position deteriorates, which reduces his leisure and increases his labor supply. This allows us to characterize how the various variables that enter the Pareto weight affect household labor supply.

Suppose we observe at least one initial bargaining variable and at least one time-varying distribution factor ; suppose that theory or intuition suggest that both and empower . Under limited commitment, we must jointly observe

because, as and empower , they must decrease her labor supply and increase her partner’s. This must be true also for past distribution factors in (III) because, as changes in bargaining power are persistent in limited commitment, any variable that affected bargaining power in the past will have a lasting effect on behavior in the future. Moreover, the recursive nature of the weight (and the fact that more recent shifts in distribution factors may undo previous shifts) implies that the effects of historical variables should diminish in magnitude the further back in time we go. We return to this point subsequently.

Full commitment implies that effects (II) and (III) are absent, while no commitment implies that (III) is absent. This is a consequence of the type of information that matters for the Pareto weight in each case. Effect (I) can only be observed cross-sectionally while effects (II) and (III), if present, can be observed cross-sectionally and longitudinally. Finally, effect (II) of current information is present in both no and limited commitment. Therefore, testing for current information alone, as in Mazzocco (2007) and Lise and Yamada (2019), does not inform whether limited or lack of commitment is the right framework through which household behavior should be analyzed.

Two final remarks are in order. First, additional distribution factors increase the number of restrictions on household labor supply. Second, wages are additional time-varying variables that enter the Pareto weight outside of full commitment. As is evident in the non-bargaining state variables in , of which is part, wages are not conventional distribution factors because they also affect the budget set. However, past wages do not enter the state space outside of bargaining in limited commitment, so they satisfy the exclusion restriction of history. As they are also assignable, we should observe effect (III) in limited commitment also through past wages. Moreover, we will show that, conditional on household income, the partner’s current wage does not enter the state space outside of bargaining in no/limited commitment, so it satisfies the exclusion restriction of contemporaneous information. The partner’s current wage thus serves as an additional distribution factor, inducing analogous effects to (II) in no and limited commitment. This role of wages is appealing because wages are readily available in household data while conventional distribution factors are harder to find. With these points in mind, we now turn to our test for commitment.

4 Test for commitment

Limited commitment describes an environment in which current and historical distribution factors affect behavior. No commitment is a special case as history does not matter whereas current distribution factors do, while full commitment is a special case of no commitment in that current distribution factors do not matter. One may thus test for commitment by testing whether current and historical values of variables that enter the Pareto weight affect household behavior – in this case labor supply – and with what sign.

There are two main ways to estimate the optimal policy functions , which are the objects over which we implement our test. The first approach involves the full or partial specification of preferences, expectations, and bargaining. The alternative approach leaves preferences and expectations unspecified while it only specifies the reduced form dependence of the Pareto weight on its arguments. This is inspired by Blundell et al. (2016) who study how wage shocks transmit into labor supply and consumption in a unitary context.181818Theloudis (2017) extends this approach to a collective setting.

While the first approach enables the recovery of the specification and the assessment of counterfactuals, its main drawback is that it requires the estimation of preferences together with bargaining. Therefore, any test for commitment is ultimately a joint test of commitment and the specification used for preferences. The second approach avoids this as it does not require the specification of preferences – consequently, it is unable to recover deep parameters or evaluate counterfactuals. As our goal here is to test for commitment rather than recover preferences or bargaining primitives, it is natural to follow the second path. This entails the derivation of estimable labor supply equations from the model’s first order conditions and the reduced form specification of the Pareto weight, both of which we describe below.

4.1 Dynamics of household labor supply

We use the general form of the household problem in (6) to derive the static optimality conditions for male and female hours. These conditions depend on the tax/benefits function through the budget constraint. It is hard to make progress without restricting , so we follow Heathcote et al. (2014) and Blundell et al. (2016) and approximate as . Tax/benefits parameters and reflect the proportionality and progressivity of the tax and benefits system. A progressive system has a strictly positive progressivity parameter while a proportional tax system has . In that case, the spouses are taxed separately at the proportionality rate .

Except a few special cases of utility, the optimality conditions are implicit functions of hours and cannot be directly estimated in the data. We follow Blundell et al. (2016) and carry out a standard log-linearization of , the marginal utility of hours, around the most recent values of consumption and hours.191919Unlike Blundell et al. (2016), we do not log-linearize the intertemporal budget constraint. We show in appendix B that this operation yields a closed-form expression for the growth rate of male and female hours in terms of changes in the Pareto weight and other variables, given by

| (7) | ||||

where , indicates ’s partner, and is the first difference between and .202020We assume the progressivity tax parameter does not change between proximate periods, so . This assumption is innocuous (we show this in appendix B) and makes the notation more compact. The first two terms reflect the disincentives from shifts in, respectively, the proportionality of taxes and the partner’s earnings due to progressive joint taxation. The third term reflects the wealth and income effects from shifts in the marginal utility of wealth (the Lagrange multiplier on the sequential budget constraint). The fourth term captures consumption-hours complementarities. The fifth term reflects the substitution effects on labor supply from shifts in own wage , accounting for progressive taxation. Finally, the sixth term reflects the bargaining effects on labor supply from shifts in the Pareto weight .

Parameter is given by one over , where is approximately equal to ’s Frisch elasticity of labor supply scaled by his/her hours of work, and is ’s share of family earnings. It follows that , which helps sign most of the terms above. For example, an increase in the proportionality of taxes reduces labor supply due to tax disincentives (term 1) while an improvement in ’s Pareto weight reduces his/her hours reflecting the bargaining effects we described earlier (term 6). Finally, reflects the nature of the consumption-hours complementarity and can thus be of any sign.212121We show in appendix B that and .

Terms 1 through 5 appear also in the dynamic unitary model of Blundell et al. (2016) while term 6 is unique to the dynamic collective model. Expression (7) is common across commitment modes in the latter case, with differences in behavior across modes arising mostly through the last term, i.e. through the way the Pareto weight changes in each mode.222222Couples in limited commitment make savings choices taking into account the effects of those choices on the outside options. Therefore, the marginal utility of wealth behaves differently in limited commitment compared to the other modes but this is a feature we do not exploit for testing. Then specifying an expression for the (reduced form) dependence of on its arguments, which we do in the next section, allows us to use (7) to test for commitment.

The partner’s current wage does not explicitly appear in (7) even though was previously part of the non-bargaining state space of the problem. This is because, aside of bargaining, only induces tax disincentives and income effects that are fully accounted for by the partner’s earnings and the marginal utility of wealth. Therefore, conditional on and , does not affect spouse ’s hours outside of bargaining. This is in contrast to which is the price of time and thus affects hours irrespective of bargaining.

Two final remarks are due here. First, the nature of the log-linearization is such that the outcome equation is in terms of hours growth rather than of hours levels. While (7) is fully consistent with the policy function , it is nonetheless not the policy function itself which generally disciplines the levels of hours. Second, the Euler equation in our model is very complicated because wealth enters the Pareto weight outside of full commitment.232323Mazzocco (2007) uses a simpler Euler equation by assuming wealth does not affect the outside options. Our use of the static optimality condition avoids this complication at the cost of introducing a term for the marginal utility of wealth, , to which we return in section 5.3.

4.2 Dynamics of the Pareto weight

Our goal is to specify the reduced form dependence of the Pareto weight on its arguments, which will enable us to take (7) to the data. Consider the structural version of the most general Pareto weight, i.e. of limited commitment, given by with , . To simplify the discussion, let be a function of one stochastic distribution factor and the past Pareto weight only, i.e. , and let be a function of one initial factor . Assume without loss of generality that both factors empower spouse , i.e. and . We generalize the discussion to multiple distribution factors (as well as wages and assets) in appendix C.

Suppose momentarily that is the smooth approximation of . If the steps in are sufficiently small, will be a reasonable approximation of the true dynamics of the Pareto weight. Appendix C shows that a log-linearization of yields , where is the elasticity of w.r.t. and is its elasticity w.r.t. the past weight (the subscript denotes the lag). Economic theory disciplines the signs of these elasticities; in this case due to the assignability of while reflecting persistence in the Pareto weight in limited commitment. The elasticities depend on the past levels of the distribution factor due to the nature of the log-linearization and they thus vary in the cross-section. This expression is useful because it relates the contemporaneous shifts in the Pareto weight to the contemporaneous shifts in the distribution factor and the most recent historical dynamics of the weight.

Exploring the recursive nature of , we can substitute the past weight backwards until we reach , i.e. marriage, and on the right hand side. describes the formation of the initial Pareto weight at marriage, i.e. the difference between the initial weight and a generic one available to all individuals when they first meet and start dating at .242424Let newly met individuals start dating with the same bargaining power (an innocuous normalization); the weight of pairs that marry at differs from the generic value at , with the difference determined by the distribution factor realized at . The difference is driven by the initial distribution factor and, as different couples differ in , varies in the cross-section as a function of it. We adapt the simple log-linear formulation , where reflects the loading factor of onto the initial weight. We expect from the assignability of .

Combining these steps (exact derivation in online appendix C) yields

| (8) |

where reflects the number of periods since marriage. (8) shows that the limited commitment Pareto weight at is the accumulation of gradual shifts in the weight over time as a result of shifts in current () and historical () distribution factors , as well as that reflects the formation of bargaining power at marriage. The effect of the distribution factor on the current weight is given by . In appendix C, we show that , so historical distribution factors have a gradually smaller effect as the length of time increases, with the rate of decay determined by .

Expression (8) encapsulates the alternative commitment modes and our nesting argument. Limited commitment has , , , with the latter two signed by the assignability of and . No commitment has , , ; as such no commitment is nested within limited commitment in terms of the variables that enter the Pareto weight. Full commitment has , , ; as such full commitment is nested within no commitment. Finally, the unitary model has , , ; as such the unitary model is nested within the full commitment collective model. Conditional on identifying , , , these points suggest the type of hypotheses one can formulate and assess in the data.

Informed by (8), our choice of specification for the reduced form dependence of the Pareto weight on its arguments is

| (9) |

The ’s and are reduced form elasticities for the response of ’s Pareto weight to distribution factors: captures the effect of the factor periods in the past; captures the effect of the initial factor periods after marriage. With additional distribution factors (and wages and assets) affecting bargaining, the number of parameters increases considerably as we show in appendix C. Moreover, in our richest specification subsequently, we let the ’s depend on the past levels of the distribution factors, that is , to mimic the dependence of the elasticities and on the past levels of the factors. A given shift in a distribution factor may thus shift the Pareto weight or not (that is, in spite of the smooth formulation in (9)), depending on the factors’ historical values.

4.3 Formulation of test

Our final equation for hours combines the dynamics of household labor supply in (7) with the Pareto weight in (9). After introducing additional distribution factors and , reinstating wages and assets as arguments in , and pooling common terms, the combined hours equation for spouse is given by

| (10) | ||||

where indicates ’s spouse. To simplify the discussion, we introduce the parameters as the reduced form coefficients on wages and distribution factors that enter ’s hours. We show in square brackets indexing which variable each coefficient corresponds to; e.g., is the coefficient on , the partner’s wage periods in the past.

Except one’s own current wage, all other current and past wages and distribution factors enter the equation exclusively through the Pareto weight. We may thus formulate testable hypotheses on their coefficients in accordance with the alternative models. The own current wage enters (10) irrespective of bargaining ( is the price of one’s own hours), so cannot be part of these hypotheses.

Distribution factors do not affect behavior in the unitary model, which thus has

In words, the coefficients on the partner’s current wage, all past wages, all current and past distribution factors, and the initial factors at marriage, are zero in the unitary model.

In the full commitment collective model, initial distribution factors affect behavior through the time Pareto weight but later realizations of distribution factors do not. While this seems to suggest that , the coefficients on the initial factors be non-zero, this is not true in our formulation. Contrasting the reduced form specification of the Pareto weight in (9) with its structural counterpart in (8), it is clear that . Even if and the initial factor structurally affects the initial weight, the past does not matter for behavior in full commitment, which has and therefore . In other words, any effect of the initial distribution factor on the Pareto weight today is through the recursive structure and the persistence of the weight that are features of limited commitment alone. Consequently, full commitment has

which is the same as . This is because our dynamic differences framework revolves around the growth of the Pareto weight, , which is observationally equivalent between full commitment and the unitary model. The main implication is that if we fail to reject the common null, this failure cannot inform us about the true underlying structure.

Under no commitment, past distribution factors do not matter for behavior (this includes the initial factors at marriage for similar reasons as above) while current distribution factors do. No commitment thus has

Moreover, the remaining ’s must clearly be of the correct sign: (the partner’s wage worsens ’s bargaining power and increases ’s hours) while is signed according to the assignability of .252525The partner’s wage worsens ’s bargaining power so , the reduced form coefficient on in equation (9), must be negative. Then because by construction.

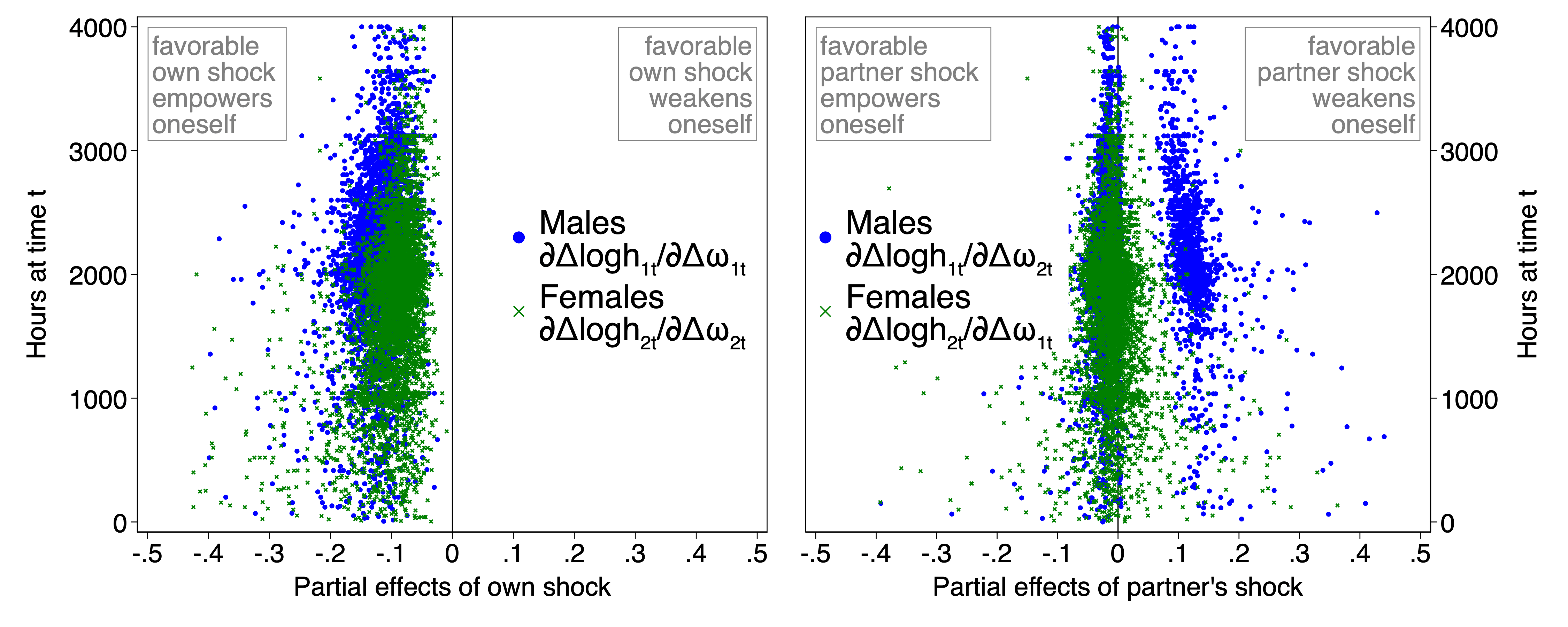

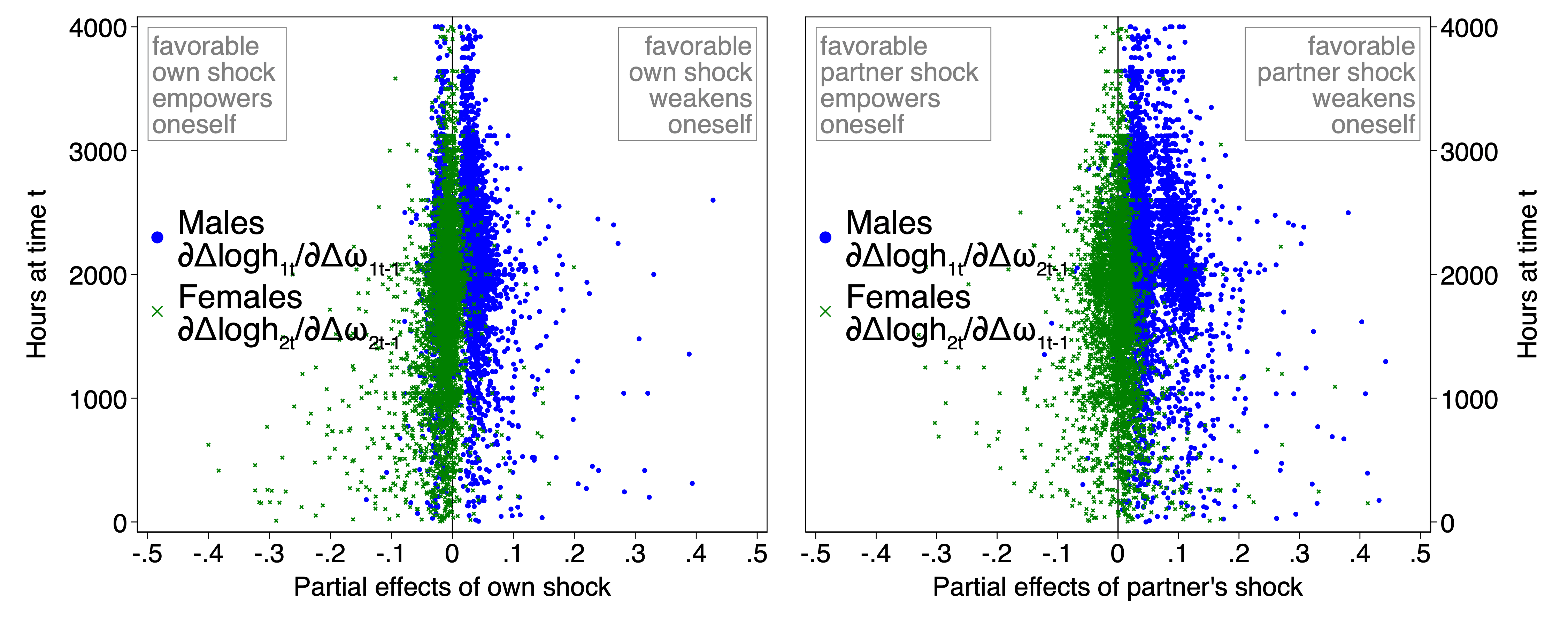

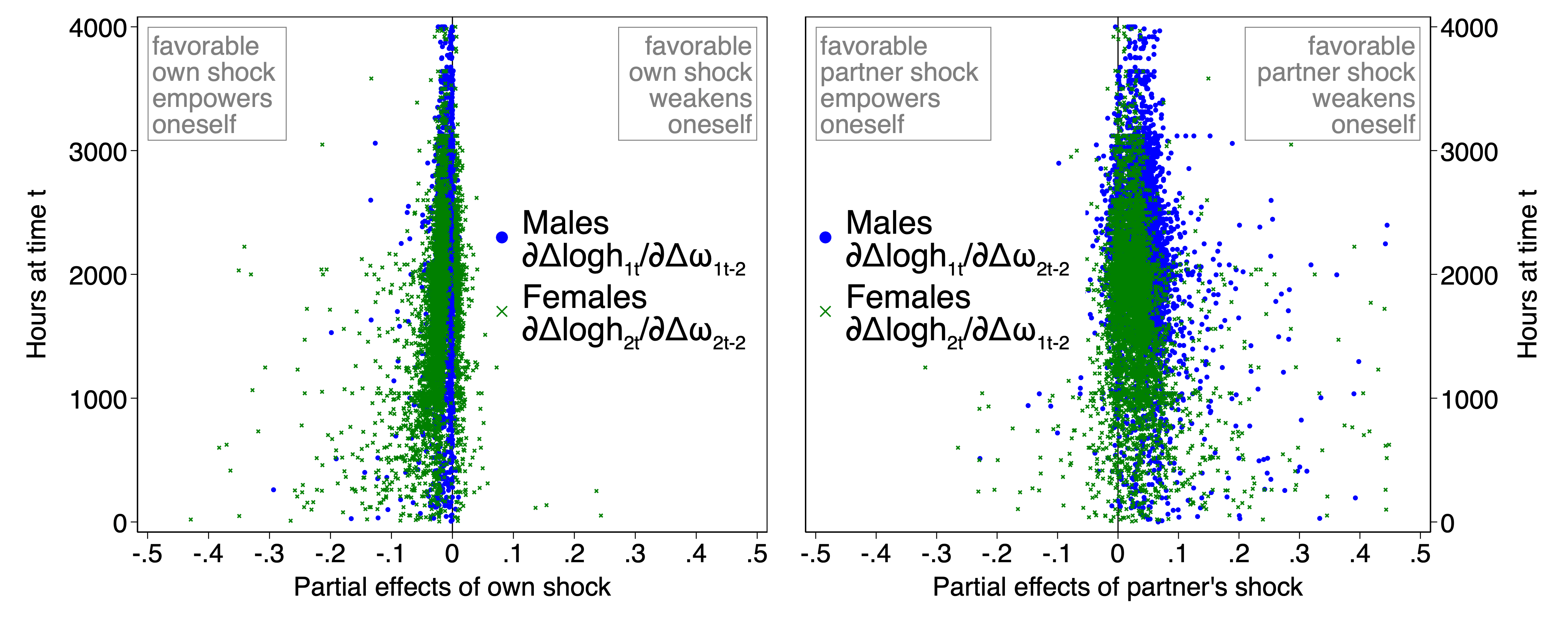

Under limited commitment, finally, all current and past distribution factors matter for behavior, so all ’s are different from zero. Limited commitment is the most general setting so it is without an alternative hypothesis or a conventional statistical test for it. Nevertheless, limited commitment remains testable in a conceptual sense. Clearly, all bargaining-related ’s must be of the correct sign, disciplined by the assignability of the corresponding distribution factors. For example, (as in no commitment), for (own past wages improve past bargaining power and, through persistence in the Pareto weight, decrease own hours today), (for opposite reasons), and similarly for the many ’s and ’s according to the assignability of and . Our test is therefore about the presence of effects from current and past wages and distribution factors, as well as, conceptually, about the sign of such effects.

The test offers many over-identifying restrictions. The obvious ones concern the partner’s hours equation. For instance, to reject no commitment, we must reject as illustrated above and reject the analogous hypothesis for the ’s. Another set of restrictions stems from the presence of multiple distribution factors that give rise to proportionality restrictions as in Bourguignon et al. (2009). From the structural form of the Pareto weight in (8), it is easy to see that the ratio of partial effects of any two concurrent distribution factors is independent of when the factors are timed, e.g. independent of . This translates into proportionality restrictions on the bargaining effects on hours, that is is the same for all .262626The proportionality restrictions extend beyond this illustration. For example, the ratio of partial effects of a given distribution factor periods apart is independent of when the effects are exactly timed.

Two final remarks are due here. First, the hypotheses do not involve assets even if assets enter the Pareto weight outside of full commitment. Unlike wages or and , wealth is non-assignable so it is not clear whom it empowers. Second, although is not useful for testing because the own current wage affects hours irrespective of bargaining, it turns out that we can identify , the Pareto weight coefficient on . This parameter must be positive in no and limited commitment, which offers an additional testable restriction.

5 Empirical implementation

5.1 Data requirements

Our test requires panel data over at least three periods. Two periods are needed to form the concurrent growth of hours and distribution factors, thus test whether contemporaneous factors affect behavior; this essentially tests for full commitment as in Mazzocco (2007). A third period is needed to form the immediately past growth of distribution factors, thus test whether history affects behavior; this in turn separates no and limited commitment. Additional periods strengthen the test with over-identifying restrictions on the role of history.

The test requires at least one time-varying and one initial distribution factor assignable in the couple in order to assess all parts of and . Assignability enables us to assess the sign of the coefficients. The partner’s wage is the obvious assignable time-varying factor (conditional on wealth and the partner’s earnings, does not affect choices outside of bargaining), so additional are not strictly needed.

Given the requirement to have data on the household over a minimum of three periods, it follows that the couple must stay intact, i.e. not divorce, over this course of time. A couple may divorce later (see appendix A) but information from those periods is not part of our test since (10) describes behavior for as long as the couple remains married.

5.2 Sample selection

We use public data from the Panel Study of Income Dynamics in the US. The PSID started in 1968 as an income and employment survey of a representative sample of households and their split-offs. It was later redesigned to enable the collection also of expenditure and wealth information. As our estimating equation includes consumption and wealth controls, we focus on the period between 1999-2019 when this information is available.272727The PSID is biennial over 1999-2019; we let denote the first difference in between ‘current’ and ‘previous’ periods, even though the ‘previous’ period refers to two calendar years in the past.

We focus on the core Survey Research Center (initially representative) sample and we select married households in which the spouses are between 21 and 65 years old. Consistent with our data requirements, we keep couples observed for at least three consecutive periods. We require complete data on earnings, hours, consumption, wealth, and demographics. Given our outcome variable, we restrict the sample to couples in which both partners participate in the labor market.282828Among couples who meet all other selection criteria, 91.6% of men and 80.1% of women work for pay. We return to this last selection in section 7.

Appendix table E.1 summarizes our baseline sample of 13,955 observations that meet these criteria. The sample conforms to expectations about income, hours, and demographics among married couples in the PSID (e.g. Blundell et al., 2016). For example, women work on average for 1,758 hours/year and earn $47,843, which is about 79% of men’s average hours (2,231 hours/year) but only 59% of men’s earnings ($81,742) respectively.

5.3 Estimation details and econometric issues

Modeling choices. We must address three final issues before we run the test. The first concerns the marginal utility of wealth. reflects the change from to in the couple’s marginal utility over total income and wealth. The couple adjusts wealth endogenously in expectation of future states of the world; this reflects precautionary savings and, in limited commitment, investment in the outside options. As is unobserved, we replace it with a function of the growth in household income and wealth , namely . Since may depend on the initial values of income and wealth, we also include terms for those.

The second issue concerns the hourly wage. Wages have a lifecycle component that agents typically anticipate and which is unlikely to induce bargaining between spouses. We specify the growth rate of wages as the sum of a deterministic component, anticipated at , and a stochastic component (see Meghir and Pistaferri, 2011, for a review of income processes). We write , where is a vector of demographics (e.g. age) that enter the deterministic part and is the wage shock such that . We assume that the shock is the only part that induces bargaining between the spouses, that is, the only component of wages that shifts the Pareto weight under no/limited commitment.292929Nevertheless, the deterministic profile of own wages affects the gradient of hours through the own wage term 5 in equation (7). We show this point in detail in appendix D.

The third issue concerns our choice of distribution factors in and . For , we seek assignable factors set at that remain constant thereafter; but we rarely observe the time of marriage in the PSID, which limits our options. We use two age-gap-at-marriage variables, namely . The first dummy indicates the husband is younger than the wife while the second indicates he is much older.303030We consider the husband older if he is at least 4 years older than the wife. The underlying premise is that youth empowers oneself as the youngest person’s marriage market is typically more active, perhaps due to fertility concerns (Low, 2024). For , we seek assignable factors that vary over time. We follow Chiappori et al. (2012) and Dupuy and Galichon (2014) and use anthropometric measures, specifically the spouses’ body mass index . Both choices are subject to limitations, which we discuss subsequently. Recall, however, that are not strictly needed for our test (wages are time-varying distribution factors) so we present results without in the text and relegate the results with to appendix E.

Specifications and heterogeneity. After implementing these modeling choices within (10), the final equation for hours of spouse , abstracting from , is given in compact form by

| (11) | ||||

Appendix D constructs this equation step by step.

We estimate three gradually richer specifications. The first is the reduced form linear regression of on the right hand side variables in (5.3), treating the coefficients as constant in the cross-section/over time. Estimation via OLS delivers estimates of the reduced form bargaining effects of wages and distribution factors, enabling quick testing of the commitment hypotheses. This simplest form of our test thus affirms that the test is easy to implement in reduced form without imposing or estimating preferences.

The pure reduced form neglects the dependence of the coefficients on hours and earnings through . Our second specification estimates (5.3) respecting the underlying structure of the coefficients. We fix the tax progressivity parameter (Blundell et al., 2016) and identify through ; see appendix D for details. This enables us to estimate (a scaled Frisch labor supply elasticity) and all bargaining parameters , including that describes how the Pareto weight shifts with own current wage .

The elasticities of the Pareto weight depend on the immediate past levels of the distribution factors (section 4.2). We reflect this in our third specification by letting the ’s depend on such past levels. There is no reason to believe that all couples feature the same degree of commitment: in reality, some couples may commit fully while others may not. In principle, we could test for commitment on a household-by-household basis, allowing each household their own degree of commitment, i.e. a household-specific . Albeit theoretically appealing, this requires long time series that we clearly lack. To get around this, we pool households together and estimate a form of aggregate bargaining effect across households, one that depends, however, on the past values of wages and distribution factors. A distribution factor may thus induce heterogeneous bargaining effects for given hours and earnings, depending on the distribution factors’ historical values.

We estimate all three specifications initially in the baseline sample of households that we observe for at least three consecutive periods. Subsequently, we estimate them again over a smaller sample of households observed for at least four consecutive periods. This strengthens our test with additional restrictions on the role of history. We do not go beyond four periods because we run into small samples.

Empirical strategy. Unlike the first specification, estimation in the second and third cases requires GMM because of the non-linear structure of . GMM estimation of the full structure of (5.3) is slow due to the dimensionality of the wage covariates and the household observables that we empirically account for (appendix A shows the role of demographics in the model explicitly). To avoid this, we run a first stage regression to net of the demographics. We then estimate the remaining terms in a second stage using residual hours on the left hand side. This two-step estimation is similar to Blundell et al. (2016); a single step delivers similar point estimates, albeit much more slowly.

Our empirical strategy proceeds as follows. First, we regress wage growth on observables to obtain the wage shock . Second, we regress hours growth on inverse past hours and taste/wage observables (times inverse past hours) to obtain residual hours consistent with the first line in (5.3).313131The first stage observables for wages and hours include dummies for year, year of birth, education, race, region, number of family members (and its change over time), number of children (and its change over time), the presence of income recipients other than the main couple (present and past), and the presence of outside dependents (present and past). We also include education-year, race-year, and region-year interactions. Third, we regress residual hours on all other variables in (5.3), which allows us to estimate the various bargaining effects. Whenever there are over-identifying restrictions, we use multiple moments and a diagonal weighting matrix. We estimate heteroskedasticity-consistent standard errors, with the household serving as a cluster. We discuss measurement error in wages and hours below.

6 Results