Approximately optimal trade execution strategies under fast mean-reversion

Abstract

In a fixed time horizon, appropriately executing a large amount of a particular asset — meaning a considerable portion of the volume traded within this frame — is challenging. Especially for illiquid or even highly liquid but also highly volatile ones, the role of “market quality” is quite relevant in properly designing execution strategies. Here, we model it by considering uncertain volatility and liquidity; hence, moments of high or low price impact and risk vary randomly throughout the trading period. We work under the central assumption: although there are these uncertain variations, we assume they occur in a fast mean-reverting fashion. We thus employ singular perturbation arguments to study approximations to the optimal strategies in this framework. By using high-frequency data, we provide estimation methods for our model in face of microstructure noise, as well as numerically assess all of our results.

keywords:

Optimal execution; Fast mean-reversion; Stochastic liquidity; Stochastic volatility.MSC:

[2020] 41A60; 49N90; 91G80; 93E20.

1 Introduction

1.1 The optimal execution problem

Whenever we want to execute (meaning to liquidate or to acquire) a large volume of a particular asset, several difficulties arise. Basically, the bulk of execution algorithms is to deal, in the most excellent way possible, with the trade-off between two financial complexities: trading costs and the uncertainty in price movements. On the one hand, we manage the latter aspect by fixing a trading horizon and then fractionating the larger trade into smaller ones, i.e., by setting up a trading schedule. On the other hand, some direct trading costs, such as fees from brokerage firms, are easy to handle. However, the same is not valid for some indirect costs — it is sometimes hard for us to even describe the latter qualitatively, let alone quantify them. Here, we will concentrate on the type of indirect cost known as price impact. This issue is relatively deep, being the subject of many papers in both the empirical and theoretical literature. Early efforts in modeling price impact are [44, 55] — see also the efforts [9, 54] of linking those two. Relevant empirical advances comprise [4, 26]; see also [20, 24, 56] for more in-depth discussions on market microstructure and price impact.

A ubiquitous type of impact in the optimal execution literature is the temporary one. This market friction represents the excess amount a trader has to pay per share, relative to the marked-to-market price, to consume additional layers of the Limit Order Book (LOB) to have an order she sent filled. Under the assumption that the temporary price impact is linear on the agent’s turnover rate, Almgren and Chriss (AC) proposed in the seminal work [2] their celebrated model. They also considered a permanent price impact, in a way to capture the influence of the trades on the dynamics of the asset’s price. Further important advances regarding price impacts in optimal execution include the model of Bertsimas and Lo [19] (which is, in a sense, a precursor of the AC model) and the model of Obizhaeva and Wang [62], modeling the LOB using supply/demand functions.

It is fair to say that the AC approach to the execution problem led to a flourishing of the field, especially in what regards generalizations of their model. The work [42] concerns the use of a geometric Brownian motion instead of an arithmetic one. The papers [22, 48] address the use of limit orders simultaneously to market orders. Regarding price impacts, a transient type of this cost figures in [43] as an alternative to its permanent counterpart. Also, [5] contain contributions relaxing the linearity assumption on the temporary and permanent impacts per share. In [23], authors regard the presence of a background noise affecting price dynamics. Another important assumption of the AC model is its measure of execution quality: they benchmark their performance with the pre-trade price, leading to Implementation Shortfall orders. We refer to [24, 47] for investigations of the execution problem under other benchmarks. Moreover, it is worthwhile to remark that the AC framework was quite suitable for studying problems other than optimal execution, such as hedging [3, 10, 49]. Recently, works such as [27, 29, 30, 35, 37, 38, 36, 39, 40] used this frictional market model to investigate the problem of price formation; see also [34, 59, 61] for further related game-theoretic models.

1.2 Stochastic volatility and liquidity

For large-capitalization stocks in highly liquid markets, it is commonly reasonable to assume that the temporary impact is either constant or has a deterministic profile — see, e.g., the third panel in [23, Figure 2]. However, a typical issue is that less liquid or highly volatile assets are more difficult to trade. Indeed, as Almgren describes in [1], for assets in the former class, there are some moments in the day when trading is cheap and others when negotiating is expensive; at some times, delaying trades is near to cost less, and at others, doing so results in a lot of volatility risk. For some highly volatile assets such as cryptocurrencies, the assumptions of constant volatility and liquidity are also quite far from true. A subtlety that renders the problem even harder is that these circumstances vary randomly throughout the day. Thus, in these scenarios, adaptive trading strategies can be expected to perform better.

The way [1] models stochastic volatility and liquidity is by assuming that the temporary price impact coefficient and the volatility of the asset price (which in turn follows an arithmetic Brownian motion) are both stochastic. On top of that, here we argue in favor of using some asymptotic techniques that are closely related to the ones that Fouque et al. applied in [32] to several financial problems, especially option pricing. For singular approximations to even more general multiscale optimal control problems, M. Bardi et al. made several advances in the last decades, see [6, 7, 8, 13, 11, 12, 14, 15]. The basic modeling assumption is that the underlying stochastic processes have as their drivers fast mean-reverting ones; see [32, Subsection 3.2] for detailed discussions in this matter. In the sequel, we will make the case about how we can see stochastic volatility and liquidity as fast mean-reverting. We will do so by arguing empirically.

1.3 The data

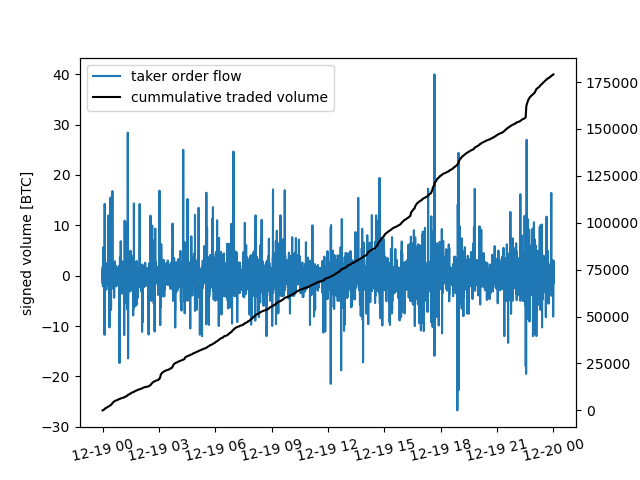

Throughout this paper, we will use a data set of level two order book updates of the asset BTCUSDT traded on the Binance spot cryptocurrencies exchange.111For estimating price impact parameters, using proprietary execution data is more adequate, see [4]. However, using public data also leads to reasonable models, cf. [24] for such an approach, which presents results in line with [4].222We remark that crytocurrency markets provide an appropriate setting for the use of models such as we develop. In effect, since the tick size is usually very small, and we can typically trade really small amounts (such as BTC in the current setting), the assumptions of continuous inventory and continuous prices are good approximations to reality. Those markets have been calling the attention of the trade execution research community; we refer to [52] and the references therein for more discussions on the matter. It contains all the order book states333Thus, each is such that as they are formed by the timestamp (making if ), as well as order book layers, each of which is a 4-tuple comprised of a bid price, bid amount, ask size, and ask amount. (up to twenty-five layers for the ask and for the bid) at each time when Binance sends an update.444When subscribing to Binance’s spot market stream channel, Binance sends at most one order book update each 100ms. When there are more than one update within such a time frame, they aggregate all of them in a single message. Unless we state otherwise, all plots will be relative to December 19, 2022. We provide a few descriptive statistics of this data set in Table 1, and the full mid-price path in Figure 1, alongside some trade data to bring further insight into this market’s behaviour.

| Symbol | BTCUSDT |

|---|---|

| Tick size [$] | 0.01 |

| Bid-ask spread [$] | 0.44 |

| (0.27) | |

| Mid-quote [$] | 16676.24 |

| (95.99) | |

| Number of seconds within | 0.135 |

| a day per number of LOB | |

| updates [seconds] | |

| Total ask liquidity [BTC] | 2.0595 |

| (2.3846) | |

| Total bid liquidity [BTC] | 2.3766 |

| (2.9920) | |

| Daily traded volume [BTC] | 179090.7037 |

1.4 Estimation of the temporary price impact coefficient

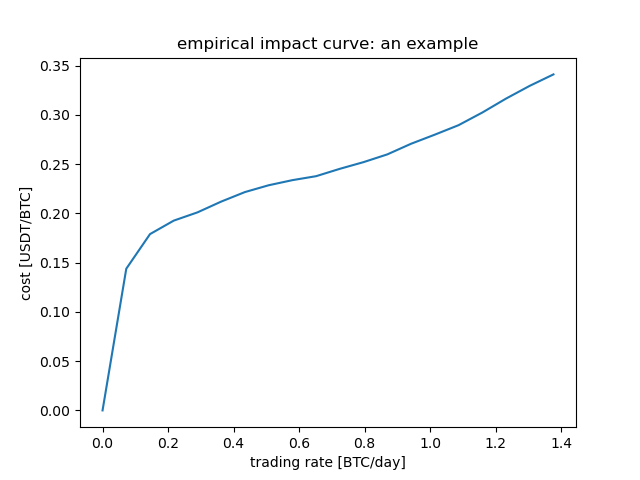

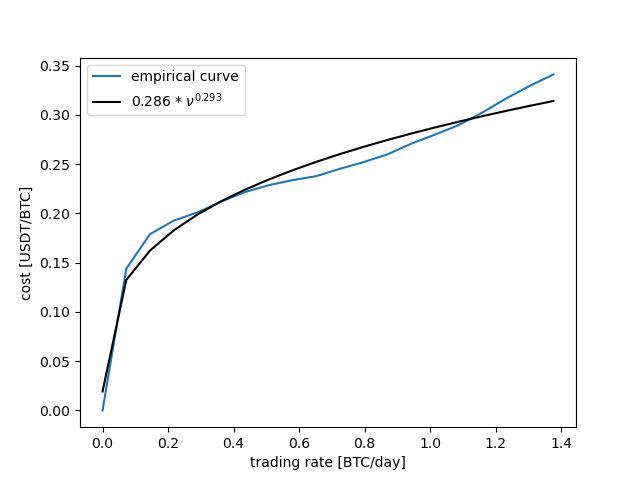

Let us begin by discussing the power-law we stipulate for the temporary price impact. From here on, we will focus on liquidation programs, interacting with the LOB by sending sell market orders; hence, we will concentrating on the bid side of the order book snapshots. At each timestamp we take a state of Then, for each hypothetical sell volume we walk as many layers of as necessary for our trade to be executed, resulting in a realized price per share Using Physics jargon, is the realized time price per share corresponding to a virtual trade of volume More rigorously, the unit of is not that of volume, but it represents our theoretically continuous rate of trading (whence it is measured in terms of volume per unit of time), so is the result of its instantaneous interaction with the market at time In this way, we compute the impact per share undergone by this trade as the difference between the current bid price and the realized price per share i.e., see Figure 2 for an illustration. We emphasize that we compute for each directly via the data in The power-law assumption (see, e.g., [20, Eq. (8)] and the references therein) postulates that

| (1.1) |

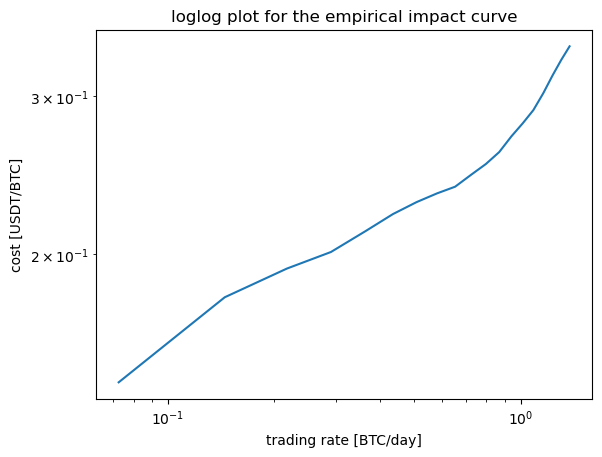

We illustrate (1.1) in Figure 3. We remark that there is strong evidence for concavity of the temporary price impact in the empirical literature, i.e., see [57, 58]. We will corroborate this stylized fact in our particular experiments.

In this work, we will assume that the exponent in relation (1.1) is constant, but we will model stochastic liquidity in a similar way as in [1]: by assuming that is stochastic. We carry out the estimation of them via a two step procedure, which we now describe.

-

1.

We first estimate using a bagging methodology, cf. [21]. Namely, we fix positive integers and and we create subsets of each of which comprising order book states sampled randomly but with replacement from (bootstrapping). Then, for each we solve555We use a BFGS algorithm to solve this minimization problem.

where we regard while we denoted by the sum of all of the bid amounts from the first layer to the last one.666In particular, since there are layers, . Then, we get our estimate of by aggregating:

-

2.

Next, we fix a lookback period . For each timestamp we estimate as the slope of the following linear regression777Here, we use Ordinary Least Squares.:

(1.2) Above, for each timestamp we consider and as in the previous step, and we have written .

The bagging methodology we conduct in step one above seems adequate because it fits exponents for various batch of books, whence we expect the exponent we estimated to work decently in a uniform manner. From Table 2, we also see that the variance in our estimate is quite small, indicating an adequate fit. Bagging methods are commonly appropriate to reduce predictors’ variance and reduce overfitting; we again refer to [21] and the references therein for a more detailed account.888It is also worth mentioning that it points out how bagging works well for unstable procedures. It seems to be the case for financial high-frequency settings, where we have the presence of microstructural noise.

| 1% | 25% | median | 75% | 99% | |

|---|---|---|---|---|---|

| 0.2833 | 0.2631 | 0.2763 | 0.2847 | 0.2911 | 0.3046 |

| (0.0116) |

Regarding step two, taking leads to performance of the regressions in (1.2) in an update-by-update manner. Using a time window is in line with what we did in the previous step. It will aggregate a few order books for each update time and provide an estimate working for all of them throughout a certain (small) time frame. Not only using helps filter out microstructural noise, but it is also consistent with the fact that the trader is subject to latency, so whenever she wants to interact with the LOB, say at time she will do so with an uncertain state with for some (the latency999We remark that latency is stochastic itself. Here, we can think of a constant as its average value, for instance. of her infrastructure).

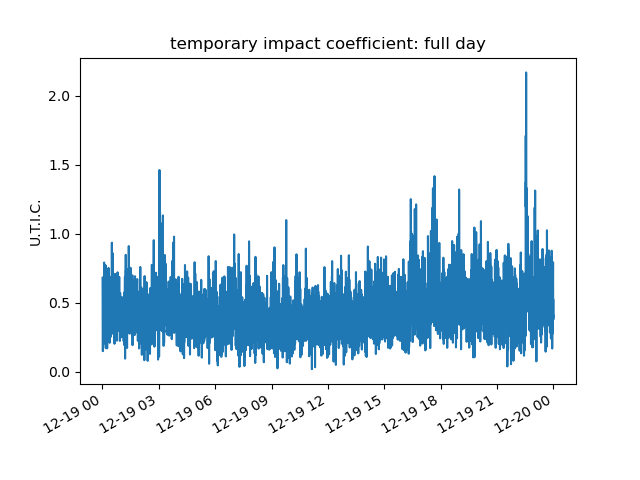

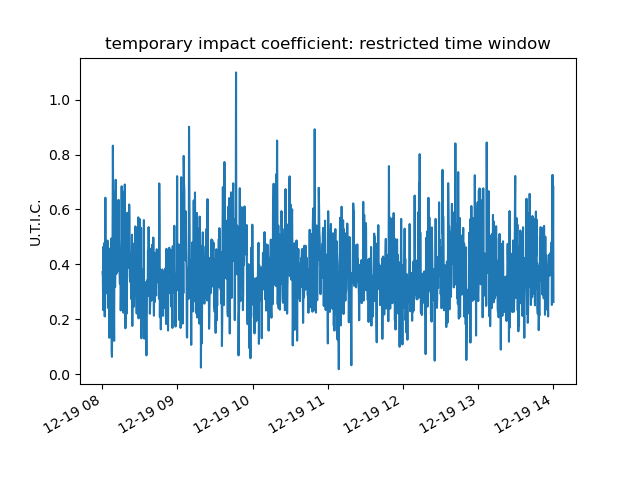

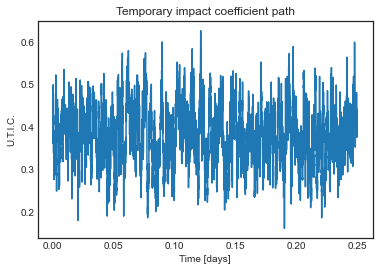

In Figure 4, we present an example of the estimated path for for our reference data set. In all examples of this work, we fix 101010We also ran the estimations with more trials (greater ) but it did not yield an estimate too far from the current one. and in step one of our bagging estimation algorithm, as well as a lookback window of second.

1.5 Estimation of intraday volatility

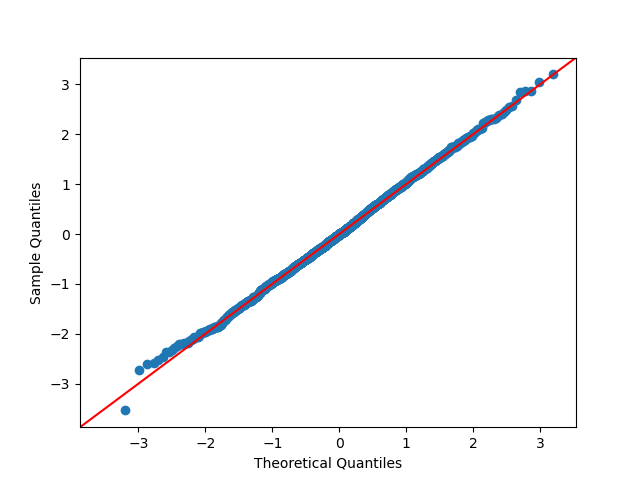

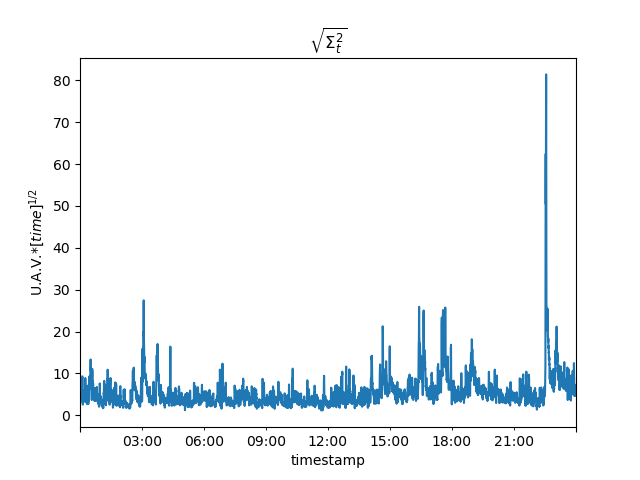

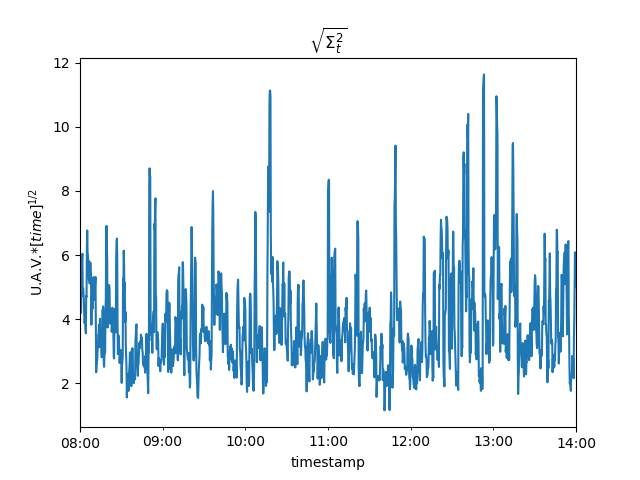

We estimate the intraday volatility by applying the Two-Scale Realized Variance (TSRV) method of Zhang, Mykland, and Aït-Sahalia [66]. We remark it is also a bagging-like estimator, which is based on averaging the estimated variance on subsamples, and then correcting the biases. The work [41] studies several such volatility estimators — among which TSRV. From their results, we expect this procedure to yield a decent estimation in the face of microstructure noise. Since we focus on liquidation programs, we estimate the asset’s bid price volatility. We fix a lookback time and for each update time we gather all bid prices over whenever they change111111We do not sample repeated prices since in this way we typically obtain better estimates. and use them to get the TSRV estimate In the TSRV estimator, we employ a maximum subsampling bandwidth of size five. In order to assess the reasonableness of our estimate, we form the price differences

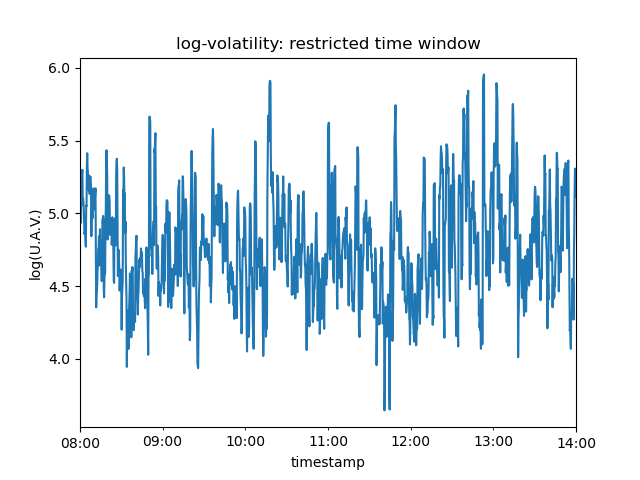

where is the bid price time series. Henceforth, we fix minute. We present statistics of the random variables consisting of samples of the process in Table 3, and some corresponding illustrative plots in Figures 5, 6 and 7, both for the whole day and a restricted six hour time window from AM to PM. During this time window, the mean of volatility tends to be more stable,121212We can make the overall mean more stable, e.g., by de-seasonalizing the volatility. The work [31] discusses extracting a seasonal profile, which can be replicated here. For the AM to PM time frame, assuming that the mean of the volatility is stable is quite reasonable for Binance’s BTCUSDT market, at least as of the period consisting of December 2022 days. We could also model the mean of the volatility itself as being stochastic; the techniques we develop here also serve to treat this case. We choose not to do pursue such endeavors for the sake of simplicity. so from here on we will focus on it. From those tables and figures, we see that the estimate constrained to the restricted time window is also rather decent. In view of Table 3, the empirical variances of are reasonably close to one, and one can check that this is consistent at least throughout the days of December 2022.

| Time window | Sample mean | Sample variance |

|---|---|---|

| Full day | 0.0142 | 0.8865 |

| Restricted | 0.0139 | 0.7888 |

Our natural estimate for the intraday volatility at time is thus

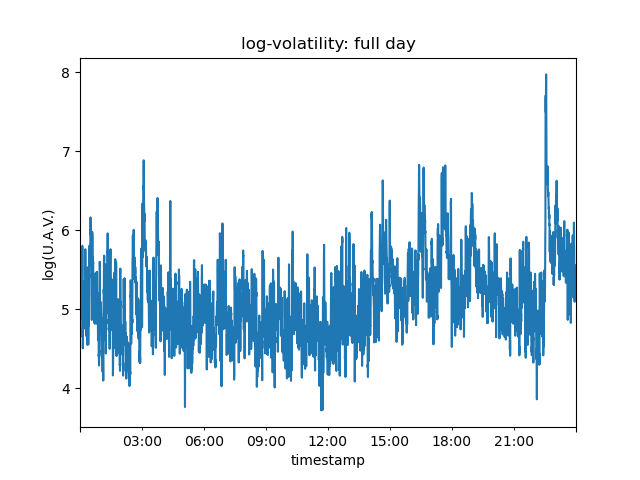

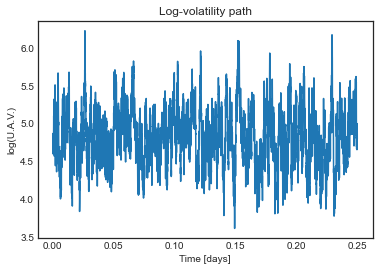

where is the empirical variance of over the restricted time window from AM to PM.131313We make the in-sample correction the TSRV by so as to make the subsequent paremeter estimations better. In practice, we do not need to make it, as is usually sufficiently close to one (as it is now), whence the original estimate uses to be quite decent. We present in Figure 8 plots of our estimation of the log-volatility process for the full trading day and for the restricted time frame.

Relating this estimate of to that of in the previous subsection, we present empirical correlation between those process is

| (1.3) |

In particular, we notice that it is positive, which makes sense: higher (resp., lower) volatility and lower (resp., higher) liquidity141414Lower (resp., higher) liquidity corresponds to higher (resp., lower) trading costs, meaning higher (resp., lower) values of . are commonly associated in cryptocurrencies (in general, in highly volatile markets).

1.6 Fast mean-reversion

We now argue that it is reasonable to expect to model both the temporary price impact coefficient and the uncertain intraday volatility as fast mean-reverting. We do so by fitting Ornstein-Uhlenbeck (OU) processes to the corresponding estimated data, wherefrom we will see that their speeds of mean reversion are sufficiently high. In general, given a OU process with speed of mean reversion long-run mean and diffusion coefficient151515We avoid to call “volatility” here so as not to confuse it with the price volatility we were discussing before, which is central to the current work. i.e.,

for a given Brownian motion , we estimate these parameters as in [50, Eq. (49)]. Namely, we run the ARMA(1,1) regression

| (1.4) |

for a time sampling with ( being independent of ), and some i.i.d. random variables We then set

| (1.5) |

We apply this technique to and see Figure 9. In carrying out the estimates, we restrict the processes to the window starting at AM and ending at PM, where we can see from Figures 4 and 8 that their long-term means are more stable.161616We could also seek modelling the processes using double OU processes, where means are themselves mean-reverting (possibly slowly). We can approach the problem under this assumption with the same techniques we use here, cf. [32]. Moreover, we sample the processes once each seconds — which leads to more stable estimates — filtering out some microstructure noise. Hence, under those constraints, we model as an OU process, whereas regarding as an expOU one. More precisely, we run the regression (1.4) using as either the process itself, or the natural logarithm of , in both cases with a proper downsampling, and then we showcase in Table 4 the parameters we estimate for them according to (1.5). Our results corroborate the claim that we can safely regard them both as fast mean-reverting.

1.7 Related literature

The paper [1] deals with a model comprising stochastic temporary price impact, but assuming linearity, i.e., that in (1.1). They also allow volatility to be stochastic and devise a numerical method for computing the optimal strategy under suitable assumptions. In a discrete-time setting, the work [25] models stochastic volatility and liquidity as independent processes in a Markov chain. See also [65] for a discrete-time discrete-space solution for the problem under discussion. In a game-theoretic framework, [28] considers a market model with stochastic volatility and liquidity. We also refer to [64] for theoretical and numerical results about the optimal strategy of the model we will investigate in the current work, but not necessarily in an ergodic setting.

Some other works consider stochastic price impact only, regarding volatility as being constant. The use of jump processes for modeling the stochastic price impact is the approach of [60, 16] — see also other frameworks for studying stochastic price impacts in [17, 33]. The work in [53] addresses optimal slicing of VWAP orders under stochastic volatility without considering price impact. The papers [46, 51] allow for the uncertainty of both the price impact and the risk aversion — the latter including stochastic volatility (if we assume that the urgency parameter of the trader is proportional to the variance of the asset price, say). A few other efforts model uncertain resilience, such as [63], extending the OW model, under regime-switching stochastic resilience, and also [45]. As for applying fast mean-reversion asymptotic techniques to problems in finance, we mention the standard monograph [32] and the references therein. The work [31] applies such techniques to optimal trading, but assuming that volatility is constant and a linear impact () in (1.1).

1.8 Our contributions

We consider a model with stochastic liquidity, modeling it as an uncertain temporary price impact subject to the power-law (1.1), determining the randomly varying coefficient. Together with the latter parameters, we also allow volatility to be stochastic, and we assume a multi-dimensional Markov diffusion drives their dynamics. We concentrate on the class of assets for which it is realistic to regard the speeds of mean-reversion towards a long-run level as being sufficiently large, in a way to be made precise. The reference framework under which we carry out our numerical experiments is when this Markov diffusion is a two-dimensional OU process.

The way we identify the optimal trading strategy is the same as in [64]. Fortunately, the rate we obtain in the regularized problem is uniformly bounded with respect to the small parameter with respect to which we wish to develop our asymptotic analysis. We begin our investigation by conducting a formal asymptotic analysis, from where we will derive a leading-order approximation for the optimal trading strategy. We proceed to provide some numerical illustrations — using the parameters we obtained from our estimations — to illustrate the behavior of the trading rate we derived. Then, we continue our formal analysis to derive the first-order correction to our approximately optimal strategy. We then carry out numerical assessments, analogous to the ones we previously discussed, but we construct now for the first-order approximation.

Finally, we provide some accuracy results establishing that the two approximations we obtained do have the order of approximation we expect of them. The idea of both proofs is to linearize the equations in a way to make feasible the application of the usual Feynman-Kac Theorem. We obtain “reflexive” representations for the error terms, i.e., representations of these as fixed-point relations. Under the suppositions we make, we are apt to carry out suitable estimates and employ Gronwall’s Lemma to deduce the asymptotics we desire. For the leading-order approximation, we prove a pointwise result in a somewhat direct manner. For the first-order correction, we provide a result on the size of the error term computed over the paths of the multi-dimensional driver. In order for the latter to hold uniformly with respect to time, we need the aid of an appropriate weight. From this, a pointwise result uniformly away from the terminal time follows. We are also apt to show that the desired accuracy for the first-order correction holds on the homogeneous average in time as well.

1.9 Structure of the paper

We organize the remainder of the paper as follows. We finish this introductory Section by fixing some notations and terminologies. Then, we present the details of our model and describe some results established elsewhere, with appropriate references, in Section 2. In Section 3, we carry out the formal analysis for the derivation of the leading-order approximation, as well as corresponding numerical experiments. We do a similar procedure regarding the first-order correction in Section 4. In Section 5, we give accuracy results for the approximations we derived. We provide our conclusions in Section 6.

1.10 Some notations and terminologies

-

1.

Henceforth, we fix the terminal time horizon as well as a complete filtered probability space with We suppose that this space supports a one-dimensional Brownian motion and also a dimensional one where We consider as the statistical (or historical measure) — we will work under it throughout the present work, writing all the expectations (including the conditional ones) under Moreover, for a multi-dimensional Markovian process we put

-

2.

For a probability measure on the Euclidean space let us write if, and only if, is measurable and In this case, we write

-

3.

The letter denotes a generic positive constant, which may change from line to line within estimates. Unless we state otherwise, possibly depends on all model parameters.

-

4.

We write for three functions and to mean that pointwise. Whenever is a model parameter (thus a constant function), we allow to depend on the point which we calculate Generally, in case we want to emphasize the dependence of on a variable we write

-

5.

We will consider, for each the admissible control set comprising the progressively measurable processes such that

2 The model

2.1 Dynamics of the state variables

Beginning at a time we consider an agent who is negotiating a financial instrument with price process171717As long as the resulting strategy does not lead to price manipulation, as in [64, Corollary 3.10], we can consider as the bid (respectively, ask) price for a liquidation (respectively, acquisition) execution program, as we did in Section 1. satisfying

for a volatility process We denote the trader’s turnover rate at time by whence her inventory holdings evolve according to

where we assume that her initial inventory is given. The agent incurs a temporary price impact whose value per share is proportional to for some in such a way that her execution price per share at time is

We emphasize that we allow to be a stochastic process above. The resulting agent’s cash process is thus

From now on we assume (with slight abuse of notations) that and are such that

for suitable deterministic continuous functions and a dimensional Markov diffusion

| (2.1) |

where is an dimensional Brownian motion, whereas and are two deterministic functions. In case we want to emphasize the dependence on in (2.1), we write Let us observe that

However, in any circumstance where we refer to the process with no superscript, we mean where shall be clear from the context.

The trader’s wealth at time consists of her current cash holdings plus the book value of her current inventory i.e., Thus, it is straightforward to derive that

Henceforth, we rely on the following assumptions:

-

(H1)

The functions and are Lipschitz continuous.

-

(H2)

Both and are continuous functions and there are such that and Moreover, the exponent of the power-law assumption belongs to and the parameter is positive.

2.2 Performance criteria and the value function

The performance criteria of the trader consist of the difference between her terminal and initial wealth, along with some penalizations for holding inventory. More precisely,

The corresponding value function

| (2.2) |

is a viscosity solution of the HJB

with terminal condition see [64], where the operator is the infinitesimal generator of when i.e.,

and We define the domain of as181818We write to denote the space of functions which are continuous.

We envisage proceeding in a suitable ergodic framework — specifically, the one we find described in [32, Subsection 3.2]. Thus, we fix the further hypotheses:

-

(H3)

The operator has a discrete spectrum with a positive gap, i.e., zero is an isolated eigenvalue. We also suppose that the remaining eigenvalues of satisfy and that they are all simple.

-

(H4)

The process with infinitesimal generator has a unique invariant distribution Moreover, we assume that has moments of all orders, bounded uniformly in time.

-

(H5)

For each continuous at most polynomially growing that is centered, i.e., the Poisson equation admits at most polynomially growing solutions

Remark 2.1.

The normalized eigenfunctions of are those that satisfy and They form a basis of and for our operator we have Moreover, we can express every as

where see [32, Eq. (3.10)].

Remark 2.2.

Regarding (H3), we notice as in [32, Eq. (3.11)] that, whenever with

| (2.3) |

uniformly in and ,191919Uniformly here meaning that the constant the big-O implies is independent of the time variable and parameter within this range. We understand the estimate on the boundaries in the pointwise limit sense. where is the spectral gap of

Remark 2.3.

The unique invariant distribution of whose existence we have postulated in (H4), is characterized as the solution to the PDE

where

see [32, Eq. (3.7)].

Example 2.4.

The multi-dimensional Ornstein-Uhlenbeck (OU) process

where is diagonal, with positive entries, and the matrix is invertible, is such that all hypotheses (H3)-(H5) are valid. In this case,

where solves

2.3 Some previous results

Theorem 2.5.

(a) There exists a unique continuous and bounded viscosity solution of (2.5).

(b) The function satisfies

where the positive constant is independent of

(c) The value function satisfies for each

As a consequence of Theorem 2.5 (c) and (2.4), we obtain the following characterization of the optimal strategy in terms of

Corollary 2.6.

The optimal control in feedback form is given by

| (2.6) |

2.4 Expanding in a power series in the fast mean-reversion parameter

We formally expand

| (2.7) |

Our aim is to find the zeroth and first-order terms in this expansion. In this direction, let us write

It follows that

| (2.8) |

| (2.9) |

| (2.10) |

and the terminal conditions ought to be and In (2.10), we have written

3 Leading-order approximation

3.1 Derivation of the leading-order approximation

From (2.8), we derive Then, we obtain from (2.9), together with the corresponding terminal condition, that

| (3.1) |

whence we have the representation

| (3.2) |

where is defined as

Definition 3.1.

In the case we have the closed-form expression

| (3.3) |

for the parameters

| (3.4) |

and

| (3.5) |

3.2 A first set of numerical experiments

In view of (2.6), our leading-order approximation of (cf. (3.1) or (3.2)), corresponding to a risk aversion parameter suggests us to use the rate of trading given in feedback form by

| (3.6) |

From here on, we will denote the inventory and cash processes corresponding to the strategy by and respectively. In particular, in the risk-neutral setting, we put

For any given benchmark strategy we refer to the quantity (in basis points)

as the performance of relative to (or simply the relative performance, when there is no ambiguity about the benchmark), where is the terminal cash we obtain from following strategy

Regarding the model dynamics, we take a two-dimensional OU process

for a two-dimensional Brownian motion Moreover, we assume that each factor models each one of the processes and

Above, we take202020We write and

for the parameters and we present in Table 5.

We introduce the matrices

implying

As a particular case of our Example 2.4, let us recall that we have the closed-form expression

| (3.7) |

with being the solution to the matrix equation which here is given explicitly by

| (3.8) |

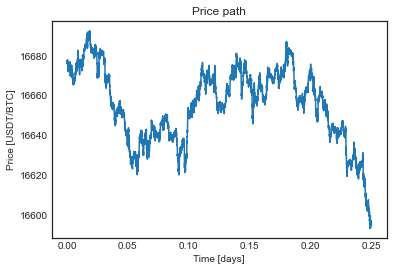

In Section 1.2, we obtained our estimates and of the parameters (for and respectively, for BTCUSDT at December 19, 2022. We expose the simulation’s parameters resulting from those developments in Tables 6 and 7. We provide an example of sample paths for the temporary price impact coefficient, the log-volatility, and the corresponding price process in Figure 10.

| 0.2833 | 0.2096 | 0.0008 |

We will take see Table 7. We assess the performance of the strategies we described above by running Monte Carlo simulations for each set of parameters, using the same price, volatility, and liquidity innovations across experiments for distinct strategies (the approximations and its benchmarks), with day, and we provide our results in what follows. We consider a liquidation program with initial data given in Table 8. During the restricted time window from AM to PM for BTCUSDT on Binance at the day we analyzed it, the traded volume amounted to 33217.79 BTC. Thus, we are simulating an execution of roughly one third of that window’s traded volume.

| [BTC] | [/BTC] | [U.T.I.C] | [log(U.A.V.)] | |

|---|---|---|---|---|

| 16676 |

We benchmark the performance of our leading-order approximation using the standard Almgren-Chriss in which we assume and Thus, in feedback form, where solves (3.1) with and in place of and respectively. Thus, as our benchmark, we consider the strategy a trader assuming constant liquidity and volatility (equal to their long-run mean values) should use if she were to optimize with our objective functional.

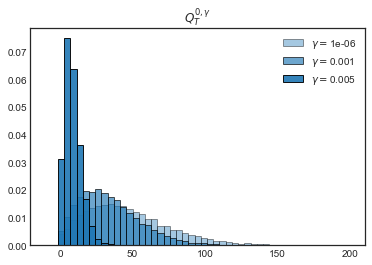

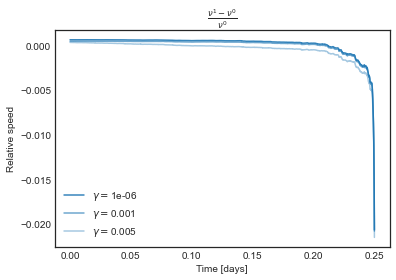

Firstly, we analyze the risk neutral setting, i.e., with We present in Figure 11 a sample path of the state and control variables for both the approximation and the benchmark corresponding to the innovations of the paths we showed in Fig 10. Even in the risk neutral setting, the leading-order approximation has the advantage of being adaptative with respect to the stochastic liquidity, see (3.2). In Table 9, we present some quantitative aspects to support that the approximation not only consistently outperforms the benchmark, but it also commonly ends up holding less inventory. Thus, we can conclude that it provides a considerable edge from the viewpoint of a trader willing to liquidate her sizeable portfolio. In Figure 12, we further illustrate the approximation’s performance.

| Relative performance [bps] | Improvement rate | ||||

|---|---|---|---|---|---|

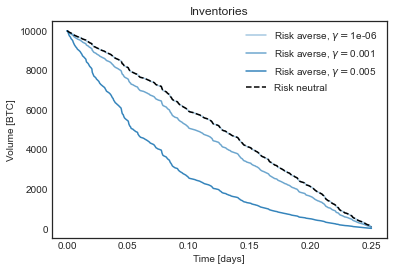

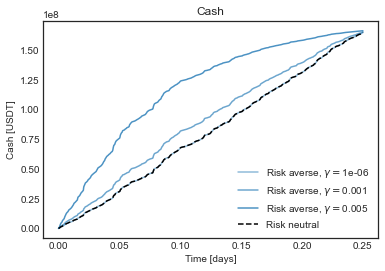

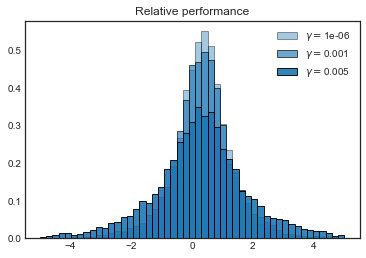

Next, we move the risk averse case, i.e., Our benchmark is still with the same as we regard in the approximation. Regarding its behavior, we showcase in Figure 13 its inventory and cash. As we would expect, it is more front loaded than the risk neutral one. Moreover, relative to the benchmark, by using higher values of risk aversion the trader still maintains a consistent average edge over the benchmark with the same risk aversion level, see Table 10. However, as we can see in Figure 14, the performance relative to the benchmark becomes a bit more uncertain, as its variance is a bit larger. We point out that the risk averse agent is not directly adaptative with respect to the price volatility. The trader is only sensitive this process through a suitable effective mean, see (3.1) and (3.6). We have illustrated how using the effective mean adds up some value relative to using

| Relative performance [bps] | |

|---|---|

Finally, relative to the risk neutral setting, adding some risk aversion seems to be useful in any case, see Table 11. In effect, the penalization of the running inventory does not always overcome the terminal wealth. Thus, adding at a small degree of urgency to her program (i.e., being weakly risk averse), leads to ending up with a larger terminal wealth on average than the risk neutral counterpart, but with inventory and price risk mitigated. Furthermore, larger values of risk aversion mitigate the variance of the terminal inventory, and makes its mean value be closer to zero, see Figure 15.

| Relative performance [bps] | |||

|---|---|---|---|

4 First-order Correction

4.1 Derivation of the first-order correction

4.2 Some complementary numerical experiments

We will consider the same particular model as in Section 3.2. Our first-order correction (corresponding to a risk aversion parameter ) leads us to consider the strategy given in feedback form by

We write whenever there is no danger of confusion, and we denote the cash and inventory processes resulting from following this trading rate by and respectively. However, we observe that we must address some numerical subtleties concerning the computation of and in (4.2) and (4.3), respectively. We present a rigorous analysis of this issue in A. In the present section, we resort to discuss the results we obtain by implementing this first-order correction term to the leading-order approximation. We run Monte Carlo simulations, with the same price, volatility, and impact innovations as in Section 3.2.

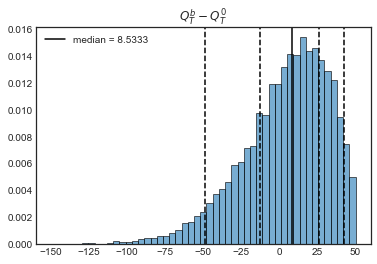

We present in Table 12 the relative performance of with respect to We see that does perform consistently better than but also that that the edge is quite marginal. It is noteworthy that the relative performance of with respect to for moderately risk averse traders is of the order of see Table 7. We note that is adaptative with respect to the factor whence for high risk aversion levels it ends up not improving the terminal wealth of , but rather concentrating in managing inventory risk throughout the execution program. Moreover, typically liquidates more inventory and terminates with more cash than which further shows its enhanced effectiveness from a risk management viewpoint.

| Relative performance [bps] | |

|---|---|

For the innovations leading to the paths we showed in Figure 10, we present the difference of and in terms of itself for different risk aversion levels in Figure 16. As the first-order correction is more front-loaded than the leading-order one, it decelerates relative to towards the end, cf. Table 13. Since we are working in a very fast mean reverting market, see Table 4, the correction we make in the first-order approximation is not too sizeable. Since the bulk of the edge added over the other benchmarks we considered were already present in the leading-order approximation, the fact that the latter is much easier to compute advocates in favor of prioritizing its use in practice.212121Of course, we can only conclude this after computing the first-order correction and comparing to the leading-order one.

5 Accuracy results

5.1 Leading-order approximations

Theorem 5.1.

We have222222Here and henceforth, the big-Os may depend on the point

for each

Proof.

Throughout this proof, all the generic constants figuring in the estimates are independent of Let us write

| (5.1) |

From Eqs. (2.5), (3.1) and (4.1), we deduce

| (5.2) |

with terminal condition

where we have written

Particularly, we have

| (5.3) |

For each let us set

Firstly, we have

| (5.4) | ||||

since and are bounded (independently of cf. Theorem 2.5 (b) and (3.2)). Secondly, it follows analogously that

| (5.5) |

From the boundedness properties of and (cf. (3.2) and (4.5)), it follows that

| (5.6) |

From (3.2) and (4.5), alongside the ODEs (3.1) and (4.4), we also see that

| (5.7) |

Furthermore, we also see from (3.2) that from where we deduce the estimate

whence, together with (5.5), we derive the following

| (5.8) |

for a sufficiently large integer since and are at most polynomially growing.

5.2 First-order correction

Lemma 5.2.

We can take satisfying (2.10), and at most polynomially growing in the spatial variable.

Proof.

A function such as must comply with the subsequent equations:

| (5.10) | ||||

Firstly, we notice that

| (5.11) |

Secondly, we write

| (5.12) |

In this way, by introducing the auxiliary function

| (5.13) |

as well as the at most polynomially growing solutions and to the Poisson equations

it follows from (4.2), (5.10), (5.11), and (5.12) that must satisfy

Hence, upon taking

| (5.14) |

it is straightforward to conclude that has the properties we stated in the present Lemma. ∎

Remark 5.3.

Any function complying with the properties we stated Lemma 5.2 must differ from the one we exposed in (5.14) by another one which only depends on time. In this connection, the way we chose the boundary layer term in the definition of was key in the last proof. If we were to seek further higher-order approximation results, we would need to take this time-dependent difference in an appropriate way (thus identifying additional boundary layer terms). For our current purpose, which is to investigate the accuracy of the first-order correction, taking according to (5.14) will suffice.

Theorem 5.4.

Let us assume in (2.3) that with at most polynomial growth and implies232323Cf. the developments within Section 3.2 from [32, Eq. (3.10)] onwards.

| (5.15) |

where is the spectral gap of the constant and the positive integer are sufficiently large, but independent of and for some small enough Then, for and we have the asymptotics

| (5.16) |

and

| (5.17) |

Proof.

Let us fix according to the construction (5.14) we made in the proof of Lemma 5.2. We deduce from Eqs. (2.5), (3.1), (4.1) and (2.10) that must solve

| (5.18) |

Since we observe that

| (5.19) | ||||

where we define

| (5.20) |

Putting (5.18) and (5.19) together, we obtain

where we define and as

and

We now proceed to show that and are at most polynomially growing in the spatial variable, uniformly in time and also for sufficiently small values of We emphasize that in subsequent estimates, we assume the generic constant and the integers to be sufficiently large, and they may change from line to line throughout estimates. However, both and are independent of a particular point or of a particular positive

CLAIM 1: We have for some large enough integer where we can take uniformly with respect to

Indeed, by using (H2) and (5.3), we can argue as in (5.4) to obtain

for some sufficiently large positive integer as and is at most polynomially growing in uniformly in time, see (5.6) and (5.8).

CLAIM 2: We have for some large enough integer where we can take uniformly with respect to

To prove the bound on let us first notice that by (5.20), we have

Let us recall from (H2) that Thus, by invoking once again (5.3), we deduce

| (5.21) | ||||

where we used that as well as the same bounds on and which we used in the proof of Theorem 5.1. By the boundedness of it is straightforward to conclude that figuring in (5.13) is bounded uniformly in Furthermore, since , and recalling (5.7), we deduce this same boundedness property for Hence, using the fact that and are at most polynomially growing in we infer from (5.14) the following relation:

| (5.22) |

Putting this estimate together with (5.21), gives the result we stated as CLAIM 2.

Next, we remark that the terminal condition for is

Since is not identically vanishing but only cancels on a suitable average, we will interpret (5.18) in the form

for wherefrom the Feynman-Kac Theorem gives the representation

| (5.23) | ||||

Above, we have written omitting the superscript and will continue to do so until the end of the proof.

By the centering of i.e., alongside the fact that it belongs to and that it has at most polynomial growth, we can apply our assumption (5.15) to obtain

| (5.24) |

For and we write

In the subsequent estimates, the generic constant may depend on and (through time-uniform bounds on the moments of the path cf. (H4)).

Now, from (5.23), we use the the Claims 1 and 2 we proved above, Eqs. (5.22) and (5.24), the Tower Property of conditional expectations, the Hölder Inequality (writing ), and Fubini’s Theorem — whenever it is convenient — as well as (H4), to derive for :

From these estimates, we employ Gronwall’s Lemma and take th powers — using their monotonicity and subadditivity — to deduce

| (5.25) |

By multiplying (5.25) by and using that

we obtain (5.16). Alternatively, by integrating (5.25) with respect to time, we get (5.17). This finishes the proof of the Theorem. ∎

Consequently, we get from Theorem 5.4 (specifically, from (5.16)) the following pointwise result away from the boundary.

Corollary 5.5.

Given and we have

6 Conclusions

We investigated the optimal execution problem under a framework where both liquidity and volatility are stochastic. We modeled the uncertainty in the aspects by stipulating that a multi-dimensional Markovian factor drives them. Building upon previous results on this setting, we further proposed to assume that this stochastic driver is a fast mean-reverting process. We used the resulting ergodicity of the system to obtain approximations to the optimal strategy, which yielded insightful strategies that are suited to the types of markets we studied — particularly, for highly volatile financial products.

Firstly, we derived the leading-order approximation. We then assessed the strategy we obtained by carrying out Monte Carlo simulations. We observed the desired effect in the strategy’s behavior relative to the risk aversion parameter. It indicated that some positive risk aversion level might be beneficial to the trader, even from the pure viewpoint of wealth maximization. Subsequently, we derived the first-order correction to the leading-order approximation. It included a boundary layer term due to the problem’s singularity at the terminal time (mitigated by assuming a finite terminal inventory penalization, which regularizes the problem). We computed the first-order correction via an iterative numerical scheme, and we have seen that it is indeed a consistent — although marginal — improvement of the leading-order approximation.

Finally, we concluded the work by establishing some accuracy results concerning our approximations. We used appropriate representations of the solutions of the HJB via the Feynman-Kac Theorem in such a way that we were able to derive conclusions regarding the asymptotics of our approximations. For the leading-order one, we provided pointwise results rather directly. For the first-order correction, the analysis was more subtle. In this instance, we were able to identify suitable topologies for which the desired accuracy results hold, from where we obtained a similar pointwise consequence.

Acknowlegements

YT was financed in part by Coordenação de Aperfeiçoamento de Pessoal de Nível Superior - Brasil (CAPES) - Finance code 001.

References

- Almgren, [2012] Almgren, R. (2012). Optimal trading with stochastic liquidity and volatility. SIAM Journal on Financial Mathematics, 3(1):163–181.

- Almgren and Chriss, [2001] Almgren, R. and Chriss, N. (2001). Optimal execution of portfolio transactions. Journal of Risk, 3:5–40.

- Almgren and Li, [2016] Almgren, R. and Li, T. M. (2016). Option hedging with smooth market impact. Market microstructure and liquidity, 2(01):1650002.

- Almgren et al., [2005] Almgren, R., Thum, C., Hauptmann, E., and Li, H. (2005). Direct estimation of equity market impact. Risk, 18(7):58–62.

- Almgren, [2003] Almgren, R. F. (2003). Optimal execution with nonlinear impact functions and trading-enhanced risk. Applied mathematical finance, 10(1):1–18.

- Alvarez and Bardi, [2002] Alvarez, O. and Bardi, M. (2002). Viscosity solutions methods for singular perturbations in deterministic and stochastic control. SIAM journal on control and optimization, 40(4):1159–1188.

- Alvarez and Bardi, [2003] Alvarez, O. and Bardi, M. (2003). Singular perturbations of nonlinear degenerate parabolic pdes: a general convergence result. Archive for rational mechanics and analysis, 170:17–61.

- Alvarez and Bardi, [2010] Alvarez, O. and Bardi, M. (2010). Ergodicity, stabilization, and singular perturbations for Bellman-Isaacs equations. American Mathematical Soc.

- Back and Baruch, [2004] Back, K. and Baruch, S. (2004). Information in securities markets: Kyle meets glosten and milgrom. Econometrica, 72(2):433–465.

- Bank et al., [2017] Bank, P., Soner, H. M., and Voß, M. (2017). Hedging with temporary price impact. Mathematics and financial economics, 11(2):215–239.

- Bardi and Cesaroni, [2011] Bardi, M. and Cesaroni, A. (2011). Optimal control with random parameters: a multiscale approach. European journal of control, 17(1):30–45.

- Bardi et al., [2014] Bardi, M., Cesaroni, A., and Ghilli, D. (2014). Large deviations for some fast stochastic volatility models by viscosity methods. arXiv preprint arXiv:1405.3206.

- Bardi et al., [2010] Bardi, M., Cesaroni, A., and Manca, L. (2010). Convergence by viscosity methods in multiscale financial models with stochastic volatility. SIAM Journal on Financial Mathematics, 1(1):230–265.

- Bardi and Kouhkouh, [2022] Bardi, M. and Kouhkouh, H. (2022). Deep relaxation of controlled stochastic gradient descent via singular perturbations. arXiv preprint arXiv:2209.05564.

- Bardi and Kouhkouh, [2023] Bardi, M. and Kouhkouh, H. (2023). Singular perturbations in stochastic optimal control with unbounded data. ESAIM: Control, Optimisation and Calculus of Variations, 29:52.

- Bayraktar and Ludkovski, [2011] Bayraktar, E. and Ludkovski, M. (2011). Optimal trade execution in illiquid markets. Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics, 21(4):681–701.

- Becherer et al., [2018] Becherer, D., Bilarev, T., and Frentrup, P. (2018). Optimal liquidation under stochastic liquidity. Finance and Stochastics, 22(1):39–68.

- Beckner, [1989] Beckner, W. (1989). A generalized poincaré inequality for gaussian measures. Proceedings of the American Mathematical Society, pages 397–400.

- Bertsimas and Lo, [1998] Bertsimas, D. and Lo, A. W. (1998). Optimal control of execution costs. Journal of Financial Markets, 1(1):1–50.

- Bouchaud, [2010] Bouchaud, J.-P. (2010). Price impact. Encyclopedia of quantitative finance.

- Breiman, [1996] Breiman, L. (1996). Bagging predictors. Machine learning, 24:123–140.

- Cartea and Jaimungal, [2015] Cartea, A. and Jaimungal, S. (2015). Optimal execution with limit and market orders. Quantitative Finance, 15(8):1279–1291.

- Cartea and Jaimungal, [2016] Cartea, A. and Jaimungal, S. (2016). Incorporating order-flow into optimal execution. Mathematics and Financial Economics, 10(3):339–364.

- Cartea et al., [2015] Cartea, Á., Jaimungal, S., and Penalva, J. (2015). Algorithmic and high-frequency trading. Cambridge University Press.

- Cheridito and Sepin, [2014] Cheridito, P. and Sepin, T. (2014). Optimal trade execution under stochastic volatility and liquidity. Applied Mathematical Finance, 21(4):342–362.

- Cont et al., [2014] Cont, R., Kukanov, A., and Stoikov, S. (2014). The price impact of order book events. Journal of financial econometrics, 12(1):47–88.

- Evangelista et al., [2022] Evangelista, D., Saporito, Y., and Thamsten, Y. (2022). Price formation in financial markets: a game-theoretic perspective. arXiv preprint arXiv:2202.11416.

- Evangelista and Thamsten, [2020] Evangelista, D. and Thamsten, Y. (2020). On finite population games of optimal trading. arXiv preprint arXiv:2004.00790.

- Féron et al., [2020] Féron, O., Tankov, P., and Tinsi, L. (2020). Price formation and optimal trading in intraday electricity markets with a major player. Risks, 8(4):133.

- Féron et al., [2021] Féron, O., Tankov, P., and Tinsi, L. (2021). Price formation and optimal trading in intraday electricity markets. In Network Games, Control and Optimization: 10th International Conference, NetGCooP 2020, France, September 22–24, 2021, Proceedings 10, pages 294–305. Springer.

- Fouque et al., [2021] Fouque, J.-P., Jaimungal, S., and Saporito, Y. F. (2021). Optimal trading with signals and stochastic price impact. arXiv preprint arXiv:2101.10053.

- Fouque et al., [2011] Fouque, J.-P., Papanicolaou, G., Sircar, R., and Sølna, K. (2011). Multiscale stochastic volatility for equity, interest rate, and credit derivatives. Cambridge University Press.

- Fruth et al., [2019] Fruth, A., Schöneborn, T., and Urusov, M. (2019). Optimal trade execution in order books with stochastic liquidity. Mathematical Finance, 29(2):507–541.

- Fu et al., [2022] Fu, G., Horst, U., and Xia, X. (2022). Portfolio liquidation games with self-exciting order flow. Mathematical Finance, 32(4):1020–1065.

- Fujii, [2019] Fujii, M. (2019). Probabilistic approach to mean field games and mean field type control problems with multiple populations. arXiv preprint arXiv:1911.11501.

- Fujii, [2022] Fujii, M. (2022). Equilibrium pricing of securities in the co-presence of cooperative and non-cooperative populations. arXiv preprint arXiv:2209.12639.

- Fujii and Sekine, [2023] Fujii, M. and Sekine, M. (2023). Mean-field equilibrium price formation with exponential utility. arXiv preprint arXiv:2304.07108.

- Fujii and Takahashi, [2021] Fujii, M. and Takahashi, A. (2021). Equilibrium price formation with a major player and its mean field limit. arXiv preprint arXiv:2102.10756.

- [39] Fujii, M. and Takahashi, A. (2022a). A mean field game approach to equilibrium pricing with market clearing condition. SIAM Journal on Control and Optimization, 60(1):259–279.

- [40] Fujii, M. and Takahashi, A. (2022b). Strong convergence to the mean field limit of a finite agent equilibrium. SIAM Journal on Financial Mathematics, 13(2):459–490.

- Gatheral and Oomen, [2010] Gatheral, J. and Oomen, R. C. (2010). Zero-intelligence realized variance estimation. Finance and Stochastics, 14(2):249–283.

- Gatheral and Schied, [2011] Gatheral, J. and Schied, A. (2011). Optimal trade execution under geometric brownian motion in the almgren and chriss framework. International Journal of Theoretical and Applied Finance, 14(03):353–368.

- Gatheral et al., [2012] Gatheral, J., Schied, A., and Slynko, A. (2012). Transient linear price impact and fredholm integral equations. Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics, 22(3):445–474.

- Glosten and Milgrom, [1985] Glosten, L. R. and Milgrom, P. R. (1985). Bid, ask and transaction prices in a specialist market with heterogeneously informed traders. Journal of financial economics, 14(1):71–100.

- Graewe and Horst, [2017] Graewe, P. and Horst, U. (2017). Optimal trade execution with instantaneous price impact and stochastic resilience. SIAM Journal on Control and Optimization, 55(6):3707–3725.

- Graewe et al., [2018] Graewe, P., Horst, U., and Séré, E. (2018). Smooth solutions to portfolio liquidation problems under price-sensitive market impact. Stochastic Processes and their Applications, 128(3):979–1006.

- Guéant, [2016] Guéant, O. (2016). The Financial Mathematics of Market Liquidity: From optimal execution to market making, volume 33. CRC Press.

- Guéant et al., [2012] Guéant, O., Lehalle, C.-A., and Fernandez-Tapia, J. (2012). Optimal portfolio liquidation with limit orders. SIAM Journal on Financial Mathematics, 3(1):740–764.

- Guéant and Pu, [2017] Guéant, O. and Pu, J. (2017). Option pricing and hedging with execution costs and market impact. Mathematical Finance, 27(3):803–831.

- Holỳ and Tomanová, [2018] Holỳ, V. and Tomanová, P. (2018). Estimation of ornstein-uhlenbeck process using ultra-high-frequency data with application to intraday pairs trading strategy. arXiv preprint arXiv:1811.09312.

- Horst and Xia, [2020] Horst, U. and Xia, X. (2020). Continuous viscosity solutions to linear-quadratic stochastic control problems with singular terminal state constraint. Applied Mathematics & Optimization, pages 1–26.

- Jaimungal et al., [2023] Jaimungal, S., Saporito, Y. F., Souza, M. O., and Thamsten, Y. (2023). Optimal trading in automatic market makers with deep learning. arXiv preprint arXiv:2304.02180.

- Konishi, [2002] Konishi, H. (2002). Optimal slice of a vwap trade. Journal of Financial Markets, 5(2):197–221.

- Krishnan, [1992] Krishnan, M. (1992). An equivalence between the kyle (1985) and the glosten—milgrom (1985) models. Economics Letters, 40(3):333–338.

- Kyle, [1985] Kyle, A. S. (1985). Continuous auctions and insider trading. Econometrica: Journal of the Econometric Society, pages 1315–1335.

- Laruelle and Lehalle, [2018] Laruelle, S. and Lehalle, C.-a. (2018). Market microstructure in practice. World Scientific.

- Lillo et al., [2003] Lillo, F., Farmer, J. D., and Mantegna, R. N. (2003). Master curve for price-impact function. Nature, 421(6919):129–130.

- Loeb, [1983] Loeb, T. F. (1983). Trading cost: the critical link between investment information and results. Financial Analysts Journal, 39(3):39–44.

- Micheli et al., [2021] Micheli, A., Muhle-Karbe, J., and Neuman, E. (2021). Closed-loop nash competition for liquidity. arXiv preprint arXiv:2112.02961.

- Moazeni et al., [2013] Moazeni, S., Coleman, T. F., and Li, Y. (2013). Optimal execution under jump models for uncertain price impact. Journal of Computational Finance, 16(4):1–44.

- Neuman and Voß, [2023] Neuman, E. and Voß, M. (2023). Trading with the crowd. Mathematical Finance.

- Obizhaeva and Wang, [2013] Obizhaeva, A. A. and Wang, J. (2013). Optimal trading strategy and supply/demand dynamics. Journal of Financial Markets, 16(1):1–32.

- Siu et al., [2019] Siu, C. C., Guo, I., Zhu, S.-P., and Elliott, R. J. (2019). Optimal execution with regime-switching market resilience. Journal of Economic Dynamics and Control, 101:17–40.

- Souza, [2022] Souza, M. O. (2022). On regularized optimal execution problems and their singular limits. Applied Mathematical Finance, 29(2):79–109.

- Walia, [2006] Walia, N. (2006). Optimal trading: Dynamic stock liquidation strategies. Senior thesis, Princeton University.

- Zhang et al., [2005] Zhang, L., Mykland, P. A., and Aït-Sahalia, Y. (2005). A tale of two time scales: Determining integrated volatility with noisy high-frequency data. Journal of the American Statistical Association, 100(472):1394–1411.

A On the numerical computation of the first-order correction

We circumvent the issue that zero is an eigenvalue of by taking in such a way that does not belong to the spectrum of From now on, we suppose that for each sufficiently small such the operator is not only injective but that its image contains all continuous functions with at most polynomial growth. We propose the following algorithm to compute the242424The fact that there is at most one follows from (H3) and the zero average condition. solution to the PDE

| (A.1) |

where is centered and at most polynomially growing:

Lemma A.1.

Proof.

In effect, since the matrix we defined in Eq. (3.8) is symmetric and positive definite, we can find a symmetric invertible such that From Beckner’s inequality for Gaussian measures, cf. [18, Theorem 1, inequality (2)], we know that

| (A.2) |

for every and Given as in the statement of the current Lemma, let us set We notice that meets the conditions for us to apply inequality (A.2); the change of variables yields

as we wanted to show. ∎

Proposition A.2.

Let us suppose that the assumptions of Lemma (A.1) are in force, and that, for every sufficiently small and at most polynomially growing, the equation

admits a unique at most polynomially growing solution whose derivatives up to order two also share this growth property. Let us denote by the sequence resulting from Algorithm 1. Then, the following claims are true:

-

(a)

The sequence is well-defined;

-

(b)

If is centered, then we have for every positive integer

-

(c)

If we fix sufficiently small, then there exists such that in and almost everywhere, as

Proof.

Proving by induction is straightforward. To prove it suffices to notice that

since Recalling that the above relations inductively imply what we stated in Now, let us show We write for positive It follows that

| (A.3) |

We claim that

| (A.4) |

In effect, carrying out some integration by parts, we have that

We emphasize that the boundary terms all vanish due to the fact that and its derivatives are at most polynomially growing, whereas is in the Schwartz class. Moreover, from Lemma A.1, we have the Poincaré inequality for our Gaussian weight:

| (A.5) |

Corollary A.3.

Proof.

Let us notice that

On the one hand, proceeding in a similar way as we did in the proof of Proposition A.2, derive

| (A.8) |

On the other hand,

| (A.9) |

Putting (A.8) and (A.9) together, and having in mind that

we infer that

Thus, up to a subsequential refinement, converges weakly in the Hilbert space hence, its limit must be equal to distributionally. Indeed, let us fix On the one hand, the weak convergence in implies, for the relation

| (A.10) |

since On the other hand, we have

| (A.11) |

From (A.10) and (A.11), we deduce that holds distributionally. In this manner, we have proved our first assertion.

Next, let us observe that the strong convergence in alongside the relations (valid for every positive integer ), allows us to infer that Finally, with the convergence properties of the sequence we have at hand, checking that solves (A.1) in the sense of distributions is straightforward — we omit the details here.

∎