Contextual Dynamic Pricing with Strategic Buyers

Abstract

Personalized pricing, which involves tailoring prices based on individual characteristics, is commonly used by firms to implement a consumer-specific pricing policy. In this process, buyers can also strategically manipulate their feature data to obtain a lower price, incurring certain manipulation costs. Such strategic behavior can hinder firms from maximizing their profits. In this paper, we study the contextual dynamic pricing problem with strategic buyers. The seller does not observe the buyer’s true feature, but a manipulated feature according to buyers’ strategic behavior. In addition, the seller does not observe the buyers’ valuation of the product, but only a binary response indicating whether a sale happens or not. Recognizing these challenges, we propose a strategic dynamic pricing policy that incorporates the buyers’ strategic behavior into the online learning to maximize the seller’s cumulative revenue. We first prove that existing non-strategic pricing policies that neglect the buyers’ strategic behavior result in a linear regret with the total time horizon, indicating that these policies are not better than a random pricing policy. We then establish that our proposed policy achieves a sublinear regret upper bound of . Importantly, our policy is not a mere amalgamation of existing dynamic pricing policies and strategic behavior handling algorithms. Our policy can also accommodate the scenario when the marginal cost of manipulation is unknown in advance. To account for it, we simultaneously estimate the valuation parameter and the cost parameter in the online pricing policy, which is shown to also achieve an regret bound. Extensive experiments support our theoretical developments and demonstrate the superior performance of our policy compared to other pricing policies that are unaware of the strategic behaviors.

Key Words: Bandit algorithm; Contextual dynamic pricing; Online learning; Strategic buyers; Reinforcement learning.

1 Introduction

Price discrimination based on customer features, such as web browser, purchasing history, job status, is a common practice among firms (Mikians et al., 2013; Hannak et al., 2014). Personalized pricing uses information on each individual’s observed characteristics to implement consumer-specific price discrimination. However, consumers can also manipulate their data to obtain a lower price, thereby contaminating the data that firms use for targeted pricing. These facts result in firms not always benefiting from acquiring more data to infer consumer preferences. These manipulating behaviors do not alter the true valuation of the costumers, but affect the offered price. Also, the manipulating behavior incurs some costs, which are determined by factors such as laws, technology, educational programs (Li and Li, 2023).

Strategic behaviors often arise when buyers become aware of personalized pricing strategies. One specific example is that Home Depot discriminates against Android users (Hannak et al., 2014). The buyers can use browser plugins such as the User-Agent Switcher to manipulate their device information. The feature manipulation does not change the buyer’s valuation of the product, but it incurs some costs. One cost is to find the fact that Android users get a higher price on Home Depot. The other cost is to learn how to manipulate device information. Another example is loan fraud. To acquire a loan, the borrower may manipulate the income, job status, the value of the car or house (Błaszczyński et al., 2021). The borrower’s valuation of the loan does not change due to the manipulation, but the manipulation causes some costs, such as, preparing documents to prove the income and job status, paying a price to the assets appraisal agency to obtain a high assessed value of the asset.

In this paper, we study contextual dynamic pricing problem with strategic buyers. The buyer strategically manipulates features for pursuing a lower price. We consider the manipulating behavior which aims at gaming the pricing policy without altering the true valuation. Figure 1 shows the schematic representation of the online dynamic pricing process with strategic buyers. At each time step , a buyer arrives with a true feature vector . In order to obtain a lower price, the buyer incurs certain costs to manipulate the true feature and subsequently reveals the manipulated feature to the seller. Upon receiving the manipulated feature vector , the seller makes a pricing decision by selecting a price . The buyer, after comparing the price with the valuation , which is determined based on the true feature vector , decides whether to make a purchase () or not (). Finally, the seller collects the revenue at time . These steps are repeated for buyers that arrives sequentially, forming the online dynamic pricing process. Our goal is to develop an online pricing policy to decide the price at each each time to maximize the overall revenue.

1.1 Our Contribution

The aforementioned strategic behavior has not been taken into account in previous dynamic pricing literature (Javanmard and Nazerzadeh, 2019; Xu and Wang, 2021; Fan et al., 2022; Xu and Wang, 2022; Luo et al., 2022; Wang et al., 2022; Luo et al., 2023), which we refer to as the non-strategic dynamic pricing policies. Studying the strategic behavior of myopic buyers is a necessary and practical topic. To fill the gap, we develop a strategic dynamic pricing policy that takes into consideration buyers’ strategic behaviors. As the best of our knowledge, we are the first to consider the strategic behavior of manipulating features in the field of dynamic pricing.

Our policy comprises two phases: the exploration phase and the exploitation phase. In the exploration phase, the seller uses a uniform pricing policy, offering prices from a uniform distribution, to collect features without manipulation and obtain an estimation of buyers’ preference parameters based on the collected true features. The rationale behind revealing true features lies in the fact that the offered uniform price is independent of the features, and the optimal action for buyers is to reveal their true features during the exploration phase. In the exploitation phase, the seller employs an optimal pricing policy to collect more revenues. The exploration phase incurs a higher regret but improves the accuracy of parameter estimation. The estimated parameters obtained from the exploration phase aid in learning the true features and implementing the optimal pricing policy during the exploitation phase, resulting in a smaller cumulative regret over a long run. Therefore, the seller faces the exploration-exploitation trade-off to decide between learning about the model parameters (exploration) and utilizing the knowledge gained so far to collect revenues (exploitation).

The performance of the pricing policy is evaluated via a (cumulative) regret, which is the cumulative expected revenue loss against a clairvoyant policy that possesses complete knowledge of both the valuation model parameters and the true features of buyers in advance, and always offers the revenue-maximizing price. Theoretically, we prove that our strategic dynamic pricing policy achieves a regret upper bound of , where is the time horizon. In a strategic environment, the seller faces the challenge of not having direct access to the true buyer features. This lack of direct observation makes it difficult for the seller to accurately learn the true value associated with each buyer, as the true value is inherently determined by these unobservable features. Importantly, our policy is not a mere amalgamation of existing dynamic pricing policies and strategic behavior handling algorithms. Our policy can also accommodate the scenario when the marginal cost of manipulation is unknown in advance. To account for it, we simultaneously estimate the valuation parameter and the cost parameter in the online pricing policy, where the cost of manipulation is inferred via a small portion of repeated buyers in the exploration and exploitation stages. In theory, our strategic dynamic pricing policy with unknown manipulation cost is also shown to achieve an regret bound. In contrast, we prove that any non-strategic pricing policy has an regret lower bound, indicating the necessity of considering strategic dynamic pricing in our problem.

1.2 Related Literature

Our work is related to recent literature on contextual dynamic pricing with online learning, strategic classification, and timing and untruthful bidding in pricing and auction design.

1.2.1 Contextual Dynamic Pricing with Online Learning

There has been a growing interest in studying contextual dynamic pricing with online learning. Several aspects of contextual dynamic pricing have been studied, including dynamic pricing in high-dimensions (Javanmard and Nazerzadeh, 2019), dynamic pricing with unknown noise distribution (Fan et al., 2022; Luo et al., 2022; Xu and Wang, 2022; Luo et al., 2023), always-valid high-dimensional dynamic pricing policy (Wang et al., 2022), dynamic pricing with adversarial settings (Xu and Wang, 2021). Notably, in these studies, the sellers have access to the true customer characteristics, and the buyers are not strategic in their behaviors. To enhance this existing body of work, our study introduces a novel dimension by considering strategic buyers who can manipulate features to game the pricing system. This extension allows us to explore the interplay between strategic behaviors and dynamic pricing, thereby contributing to the understanding of more realistic and complex market dynamics.

1.2.2 Strategic Classification

Strategic classification studies the interaction between a classification rule and the strategic agents it governs. Rational agents respond to the classification rule by manipulating their features (Hardt et al., 2016; Dong et al., 2018; Chen et al., 2020; Ghalme et al., 2021; Bechavod et al., 2021; Shao et al., 2023). Two kinds of strategic behaviors in classification are commonly explored: gaming and improvement. Gaming corresponds to the case where the agent response causes a change in the prediction but not the underlying target variable, while improvement corresponds to the case where the agent response to the predictor causes a positive change in the target variable (Miller et al., 2020). The strategic classification problem differs significantly from our setting. Strategic classification is a supervised learning problem, where the objective is to minimize misclassification errors. The focus is on developing algorithms that can effectively classify instances based on their features, considering the strategic behavior of the entities involved. In contrast, the dynamic pricing problem we address is an online bandit learning problem, where the seller needs to make pricing decisions in a sequential and adaptive manner, and our objective is to minimize regret.

1.2.3 Timing and Untruthful Bidding in Pricing and Auction Design

Existing strategic work mainly focused on timing and untruthful bidding in pricing and auction design. Timing refers to the time of purchases. In this setting, the buyers are forward looking and time-sensitive, and the strategy for these buyers is choosing the time of purchasing. The private valuations of buyers decay over time and buyers incur monitoring costs. The buyers strategize about the time of purchases to maximize the utility (Chen and Farias, 2018). In addition, untruthful bidding appears in repeated auctions. In auctions, the strategy used by the buyers is lie, which happens if the buyer accepts the price while the price offered is above his valuation, or when he rejects the price while his valuation is above the offered price (Amin et al., 2014; Mohri and Munoz, 2015; Chen et al., 2022). In the contextual auction literature, both the seller and buyers are able to observe the true features (Golrezaei et al., 2023). While the strategic behaviors of timing and untruthful bidding have received considerable attention, the manipulation of features in pricing setting, particularly in the online dynamic pricing setting, has remained relatively unexplored. By including this strategic behavior, our work enriches the understanding of strategic behaviors in dynamic pricing problems, providing a comprehensive framework for considering buyer manipulation in pricing decisions.

1.3 Notation

Throughout this paper, we denote for any positive integer . For any vector and any positive integer , the -norm is . For any matrix , we use to denote the spectral norm of . For any event , represents an indicator function which equals to 1 if is true and 0 otherwise. For two positive sequences , we say if for some positive constant , and if for some positive constant . We let represent the same meaning of except for ignoring log factors.

1.4 Paper Organization

The rest of the paper is organized as follows. In Section 2, we define the dynamic pricing problem with strategic buyers, and provide the necessary elements for our policy. In Section 3, We present the policy for dynamic pricing with the known marginal cost. In Section 4, we relax the known marginal cost assumption, and develop a policy for dynamic pricing with unknown marginal cost. In Section 5, we analyze the regret of our proposed strategic policies. In Section 6, we conduct experiments to demonstrate the performance of our algorithm. We conclude our work with some future directions in Section 7. The proofs are included in the supplemental materials.

2 Problem Setting

We study the pricing problem where a seller has a single product for sale at each time period , where denotes the length of the horizon and may be unknown to the seller. At time , a seller with a vector of true covariates arrives.

Remark 1.

In dynamic pricing literature, covariates typically include product features, e.g., insurance product features, and customer characteristics, e.g., customer financial status, and both are observable by the seller. Since product features cannot be modified by buyers, to simply the presentation we only consider customer characteristics in the covariates to study the buyers’ strategic behavior of manipulating customer characteristics. Our analysis can be straightforwardly extended to the scenario where includes both product features and customer characteristics.

Following the dynamic pricing literature (Javanmard and Nazerzadeh, 2019; Xu and Wang, 2021, 2022; Luo et al., 2022; Wang et al., 2022; Luo et al., 2023), we assume the buyer’s valuation of the product is a linear function of the feature covariates , which is unobservable by the seller. In particular, we define , where are independently and identically distributed () samples from an unknown distribution supported on a bounded subset . The buyer’s valuation function is defined as

where represents the buyer’s true preference parameter, which is unknown to the seller, and are noises from a distribution with mean zero and a cumulative density function . At each period , the seller posts a price . If , a sale occurs, and the seller obtains the revenue . Otherwise, no sale occurs. We denote as the response variable that indicates whether a sale occurs at the period , ,

| (1) |

The response variable can be represented by the following probabilistic model,

2.1 Clairvoyant Policy and Performance Metric

A clairvoyant seller who knows the true parameter and the true feature is able to conduct an oracle pricing policy, which can serve as a benchmark for evaluating a pricing policy. The goal of a rational seller is to obtain more revenue. Hence, a clairvoyant seller would post the price by maximizing the expected revenue, that is,

| (2) |

The first-order condition of (2) yields

We define as the virtual valuation function and as the pricing function. By simple calculations, we obtain the oracle pricing policy as follows,

| (3) |

Now, we discuss the performance measure of a pricing policy. Let be the seller’s policy that sets price at time . To evaluate the performance of any policy , we compare its revenue to that of an oracle pricing policy run by a clairvoyant seller who knows both and and offers according to (3) for any given . The worst-case regret is defined as follows,

| (4) |

where the expectation is with respect to the randomness in the noise and the feature . Here represents the set of probability distributions supported on a bounded set . Our objective is to find a pricing policy such that the above total regret is minimized.

2.2 Feature Manipulation

As shown in (3), the seller’s price is determined by the features. Therefore, the buyer has an incentive to manipulate the features to lower the price of the product. Following Bechavod et al. (2022), we consider a quadratic cost function. That is, the buyers’ cost for modifying feature to is

where is a fixed marginal cost of manipulating features. The marginal cost is assumed to be a symmetric positive definite matrix with the minimum eigenvalue and the maximum eigenvalue . This functional form is a simple way to model important practical situations in which features can be modified in a correlated manner, and investing in one feature may lead to changes in other features. In Section 3, we assume the marginal cost of manipulation is known by the seller, same as Bechavod et al. (2022), and in Section 4, we relax this assumption by considering a more challenging unknown manipulation cost.

Let be the manipulated feature, which is observable by the seller. We define . From buyers’ perspective, the seller assesses the expected valuation by . The total cost of buyers is the price and the manipulation cost , where the price is determined by the seller’s pricing policy. We consider two pricing policies, the uniform pricing policy in the exploration stage and the optimal pricing policy in the exploitation stage. In the exploration stage, the seller focuses on collecting more informative data for parameter estimation and hence implements a uniform pricing policy such that is randomly chosen form a uniform distribution . After this initial period, the exploitation stage implements an optimal pricing policy such that price is set by the pricing function . Let be the seller’s estimation of . In our pricing process, we assume that the seller’s pricing policy is transparent to the buyers (Chen and Farias, 2018), meaning that the buyers are aware that the seller is implementing either a uniform pricing policy or an optimal pricing policy . It is important to note that the specific assessment rule used by the seller is not revealed to the buyers, which is a similar assumption made in Bechavod et al. (2022).

By revealing the manipulated features to the seller, buyers believe that the price for the product is when the optimal pricing policy is conducted. Given the true covariate and the pricing policy , the buyer chooses the manipulated features by minimizing the following total cost,

| (5) |

where

When the uniform pricing policy is conducted in the exploration stage, the price is not related to the features, hence buyers have no incentive to manipulate features, and . When the optimal pricing policy is conducted, the first-order condition of (5) yields

| (6) |

Figure 2 displays the schematic representation of the strategic dynamic pricing policy.

Remark 2.

Equation (6) is the first-order necessary condition of minimizing (5) when the optimal pricing policy is conducted. For simplicity, we consider the case where is convex in and hence (6) is a unique minimizer of (5). When minimizing (5) is not a convex problem, from (6) is not necessarily the global minimum, and multiple ’s may satisfy (6). In practice, the buyers can try different ’s which satisfy (6) and determine an such that is the smallest.

2.3 Linear Regret for Non-strategic Pricing Policy

While various dynamic pricing policies have been proposed (Javanmard and Nazerzadeh, 2019; Fan et al., 2022; Luo et al., 2022; Wang et al., 2022), none of them considers the impact of strategic behaviors in the pricing problem. Since the true feature is unobservable by the seller, the pricing policy used in previous literature is not applicable. In this case, the non-strategic pricing policy would set the price as , which uses the manipulated feature for pricing.

In this section, we prove that the non-strategic pricing policy incurs a linear regret lower bound of in the considered pricing problem. We first present some standard assumptions in the dynamic pricing literature. Under these assumptions, the non-strategic pricing policy incurs a linear regret. In later sections, we will show that our proposed strategic pricing policy achieve a sub-linear regret under the same assumptions.

Assumption 1.

for some constants .

Assumption 1 is standard in dynamic pricing literature (Javanmard and Nazerzadeh, 2019; Fan et al., 2022; Zhao et al., 2023). By Assumption 1, we know .

Assumption 2.

The buyers’ valuation for a known constant .

Assumption 2 assumes a known upper bound for the buyers’ valuations (Fan et al., 2022; Luo et al., 2022), which is a mild condition in practical applications. With this assumption, the seller can set a price

Assumption 3.

The function is strictly increasing, and are log-concave in . For , where , we assume and , for some constants .

The assumption of log-concavity is commonly used in dynamic pricing literature (Javanmard and Nazerzadeh, 2019). By Assumptions 1 and 2, we have . Assumption 3 states that and are bounded on a finite interval , and is satisfied by some common probability distributions including normal, uniform, Laplace, exponential, and logistic distributions.

Assumption 4.

The population covariance matrix is positive definite. We denote the minimum eigenvalue and maximum eigenvalue of as and , respectively.

Assumption 4 is a standard condition on the feature distribution, and holds for many common probability distributions, such as uniform, truncated normal, and in general truncated version of many more distributions (Javanmard and Nazerzadeh, 2019).

Theorem 1.

Theorem 1 reveals that under a uniform distribution , the non-strategic pricing policy with strategic buyers has a linear regret lower bound of , indicating that it is not better than a random pricing policy. This result underscores the necessity of a new strategic pricing policy in the presence of strategic buyers. Motivated from this, in Sections 3 and 4, we develop new strategic dynamic pricing policies to account for the strategic behaviors.

3 Strategic Pricing with Known Marginal Cost

In this section, we introduce a novel dynamic pricing policy when the marginal cost is known in advance. In Section 4, we will relax this assumption and consider the case of unknown . Our policy operates in an episodic manner, allowing for the consideration of an unknown total time horizon . Episodes are indexed by and time periods are indexed by . The length of episode is denoted by . Each episode is divided into distinct phases, the exploration phase of length and the exploitation phase of length . The detail of the strategic pricing policy with known marginal cost is shown in Algorithm 1.

| (7) |

Algorithm 1 requires three input parameters. The first input is the upper bound of market value , which is assumed to be known in Assumption 2. This is consistent with the approach used in previous works such as Fan et al. (2022) and Luo et al. (2022). The second input is the minimum episode length , which is also aligned with the approach used in Fan et al. (2022) and Luo et al. (2022). The third input is denoted as and is used to determine the length of the exploration phase. In our algorithm, the length of the exploration phase is set to , which differs from previous works such as Fan et al. (2022) and Luo et al. (2022). In Fan et al. (2022), the exploration length is with , while in Luo et al. (2022), it is for some constants and or . Our approach results in a shorter exploration phase length compared to Fan et al. (2022) and Luo et al. (2022), particularly when the time period is sufficiently large. This shorter exploration phase leads to a reduced regret, making our algorithm more efficient in the strategic setting.

Algorithm 1 can been seen as a variant of the explore-then-commit algorithm. During the exploration phase, the seller implements the uniform pricing policy, and the buyers do not manipulate features and reveal . Note that by design, prices posted in the exploration phase are independent from the noise . The seller collects the true features to obtain an accurate estimate of by the maximum likelihood estimation (MLE). During the exploitation phase, the estimated model parameters are fixed, and the seller commits to the optimal pricing policy by using the parameters obtained in the exploration phase. It is worth mentioning that the seller only discloses the function but keeps the assessment rule undisclosed (Bechavod et al., 2022).

The two-phase exploration-exploitation mechanism in Algorithm 1 is commonly employed in the dynamic pricing literature. In Golrezaei et al. (2019), reserve prices are randomly set during the exploration periods to incentivize the buyers to be truthful. In Broder and Rusmevichientong (2012) and Bó et al. (2023), a fixed price sequences are offered in the exploration phase to avoid the uninformative price. Moreover, in Fan et al. (2022) and Luo et al. (2022), prices are also set from the uniform distribution during the exploration phase to facilitate parameter estimation. Our exploration stage aligns with this last line of work, although it features a considerably shorter exploration phase. An important distinction is the consideration of strategic behavior during the exploitation phase, which leads to a significantly improved regret bound.

4 Strategic Pricing with Unknown Marginal Cost

In Algorithm 1, the seller has knowledge of the marginal cost . In this section, we extend Algorithm 1 to the scenario where the marginal cost is unknown. We first introduce how to match the true features and the manipulated features for the repeated buyers. Then we present the strategy to handle the unknown marginal cost. Finally, we develop the strategic pricing policy with unknown marginal cost.

4.1 Matching of True Features and Manipulated Features

We assume that some buyers return to make repeated purchases, which is common in real-world scenarios such as the mentioned Home Depot and loan application examples. The seller keeps track of an unique identification number (ID, denoted by ) assigned to each buyer, such as the account email in the Home Depot example or the social security number in the loan example. By recording the ID of each buyer, the seller can distinguish between different buyers and keep track of their reported features. To develop a strategic dynamic pricing algorithm in the absence of the known marginal cost, we introduce a concept of the repeat buyer rate , which is also used in previous literature (Funk, 2009; Behera and Bala, 2023).

Definition 1.

The repeat buyer rate is the proportion of buyers who have made purchases during both the exploration and the exploitation phases.

The presence of a repeat buyer rate allows the seller to acquire both the original features and the manipulated features of the same buyer. During the exploration phase, the seller collects the original feature along with the corresponding unique ID for each buyer. These pairs are recorded by the seller. In the exploitation phase, the seller obtains the manipulated feature and the corresponding ID , and again records the pairs . By matching the unique ID obtained from both phases, the seller can establish the feature pair for the same buyer. This matching process allows the seller to link the original and manipulated features for individual buyers.

4.2 Strategy for Unknown Marginal Cost

In this section, we introduce the strategy to handle the unknown marginal cost . Let be an estimate of . For the matched pair , using Equation (6), we can obtain

| (8) |

To simplify Equation (8), we introduce the following new variables,

| (9) | ||||||

By introducing these new variables, Equation (8) can be rewritten as the following -dimensional equation,

| (10) |

In Equation (10), is known by the seller, and can be obtained using the matched pairs recorded by the seller. Let and be the -th () component of and , respectively. The -th component equation of (10) can be written as Assume that we obtain repeated samples , and define By the least square method, we obtain the estimation of as

| (11) |

This can be used in our pricing policy to handle the case of unknown marginal cost . Note that if we directly estimate the unknown , we would need to estimate a total of elements ( is a symmetric matrix). However, with our strategy, we can reduce the number of elements to be estimated to by using Equation (11). This significantly reduces the complexity of the estimation process and makes it more computationally feasible.

4.3 Pricing Policy with Unknown Marginal Cost

By leveraging the results of Section 4.1 and Section 4.2, we are ready to introduce the details of the strategic dynamic pricing policy with unknown marginal cost in Algorithm 2.

Algorithm 2 takes six input parameters. The first three inputs, and , are the same as those used in Algorithm 1. The set is used to store the IDs and true features of buyers collected during the exploration phase. The set stores the IDs and manipulated features of buyers collected during the exploitation phase. The set stores the matched pairs by linking the unique ID from sets and . These sets play a crucial role to link the true and manipulated features in the exploration and exploitation phases to enable the cost parameter estimation shown in Section 4.2. The core principle of Algorithm 2 remains similar to that of Algorithm 1, as they both employ a two-phase mechanism consisting of an exploration phase and an exploitation phase.

The distinguishing feature of Algorithm 2 lies in its handling of the unknown marginal cost . To address this challenge, the algorithm uses the matched and to learn the pricing parameter . It is important to highlight that the number of matched pairs is controlled by the repeat buyer rate . The higher the , the more different buyers make repeated purchases, resulting in a larger pool of matched pairs . This increase in matched pairs leads to a more precise estimate of , which in turn enhances the effectiveness of the pricing strategy. By leveraging the matched pairs and adjusting the repeat buyer rate, Algorithm 2 can effectively learn the pricing parameter and implement the pricing policy in the absence of knowledge about the marginal cost .

The detail of the calculation of the price during the exploitation phase is shown in Algorithm 3. If the original feature is recorded in the seller’s system, the price can be directly determined as . On the other hand, if the original feature is not recorded, the seller utilizes the estimated to determine the price. In the absence of an estimation of , the price is set as . Once the estimation of becomes available, the price is determined as .

5 Regret Analysis

In this section, we analyze the regret of the proposed pricing policy when the marginal cost is known (Section 5.1) and unknown (Section 5.2).

5.1 Regret Analysis under Known Marginal Cost

We consider the strategic dynamic pricing policy in Algorithm 1 with strategic buyers. We first introduce two important measures to characterize the properties related to the function . We define the "steepness" of the function as

| (12) |

and the "flatness" of the function log as

| (13) |

We then present a lemma that establishes an upper bound on the estimation error of at the end of the exploration phase within each episode.

Lemma 1.

Lemma 1 shows that the expected squared estimation error of decreases as the exploration length increases. As increases, the number of the samples used to estimate becomes larger, leading to a better estimation accuracy for parameters. However, when is too large, the pricing policy will over-explore and incur a large regret. By using the optimal choice of in our Algorithm 1, we establish a tight upper bound on the regret for the proposed strategic dynamic pricing policy with known .

Theorem 2.

The constants and in the regret bound only depend on some absolute constants derived from the assumptions. To read the regret bound, we break it into three elements. First, the regret bound is influenced by the minimum eigenvalue of the marginal cost , serving as an indicator of the manipulation capability. As expressed in (6), the extent of deviation between the manipulated feature and the original feature is associated with the marginal cost . When the minimum eigenvalue decreases, the deviation between and increases, making the pricing problem more challenging and resulting in a higher regret. Second, the regret bound depends on the dimension of the features at the rate . A larger feature dimension makes the estimation of the parameters more difficult, leading to a larger regret. Third, the regret bound depends on the time length at the rate of . In comparison, Theorem 1 demonstrates that the non-strategic pricing policy has a regret bound of at least . Consequently, our proposed strategic dynamic pricing policy, which accounts for the strategic behavior of buyers, outperforms the non-strategic pricing policy in terms of minimizing regret.

5.2 Regret Analysis under Unknown Marginal Cost

In this section, we analyze the regret of the strategic dynamic pricing policy with the unknown marginal cost. We first provide an upper bound on the estimation error of .

Lemma 2.

Suppose that Assumptions 1, 2, 3 and 4 hold, and the latest sample used in (11) is obtained in the -th episode. Let be the total length of the -th episode, be the repeat buyer rate defined in Definition 1. We denote as the estimate of , where is estimated from (11). There exists constant such that for

Lemma 2 reveals the estimate error of scales inversely with the repeat buyer rate. This implies that a higher repeat buyer rate leads to a lower estimation error, as more samples can be obtained to estimate when is higher. Now we establish an upper bound on the total expected regret for the strategic pricing policy in the case of an unknown marginal cost.

Theorem 3.

The regret bound is influenced by several interesting factors, including , , , and . The relationship between the regret bound and the first three factors , , and is similar to that established in Theorem 2. Here, we focus on analyzing the impact of the repeat buyer rate on the regret bound. As the repeat buyer rate increases, the seller obtains more samples that can be used to estimate the parameters . This increase in the sample size leads to a more accurate estimation of , as indicated by Lemma 2. Consequently, the seller obtains a more precise estimate of the true feature , which translates to a lower regret. Theorem 3 establishes that our proposed strategic pricing policy, even in the absence of prior knowledge regarding the marginal cost, attains the same regret upper bound of as demonstrated in Theorem 2.

6 Experiments

In this section, we empirically evaluate the performance of our proposed strategic dynamic pricing policies and compare them with the benchmark method. We first conduct simulation studies to validate the theoretical results and investigate the impacts of key factors on our policies, then perform sensitivity tests on the hyperparameters, and finally evaluate the performance of our policies using real-world data.

6.1 Justification of Theoretical Results

We consider the dimension of the features , with the true parameter . The covariates and are both independently and identically distributed from Unif(0, 4). The noise distribution is assume as the normal distribution .

To implement our algorithm, we divide the time horizon into consecutive episodes, with the length of the -th episode set to , where . We further partition each episode into an exploration phase with length , and an exploration phase with length . In the exploration phase, we sample from Unif(0, 6) among all the policies, and we obtain the estimate . In the exploitation phase, we implement different policies to compare the performance.

- •

-

•

For the strategic pricing policy with the known marginal cost, the price is determined by according to Algorithm 1.

-

•

For the strategic pricing policy with the unknown marginal cost, the price is determined according to Algorithm 2.

Among the experiments, we denote the base marginal cost , and consider different repeat buyer rates and .

6.1.1 Comparison of Strategic and Non-strategic Pricing Policies

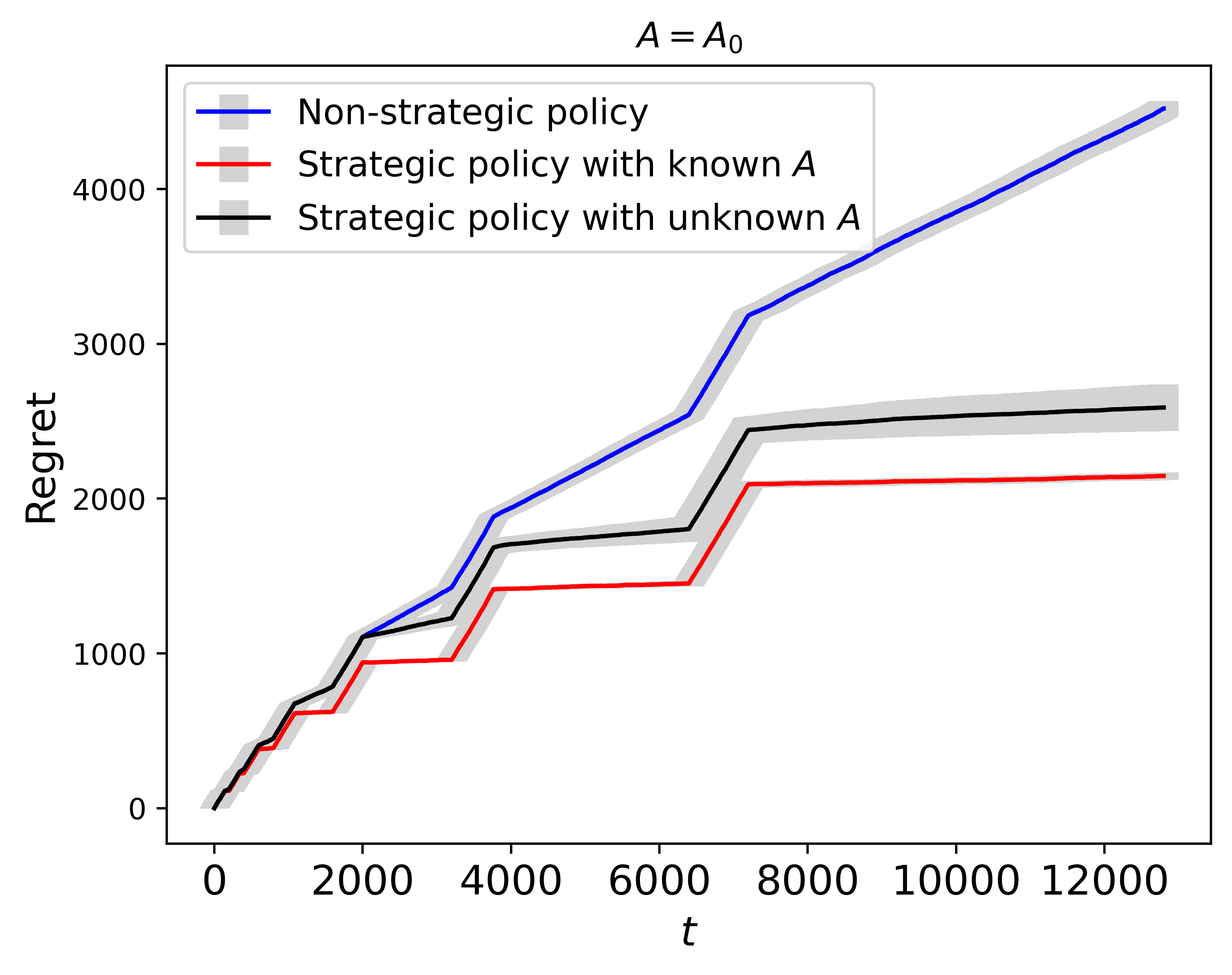

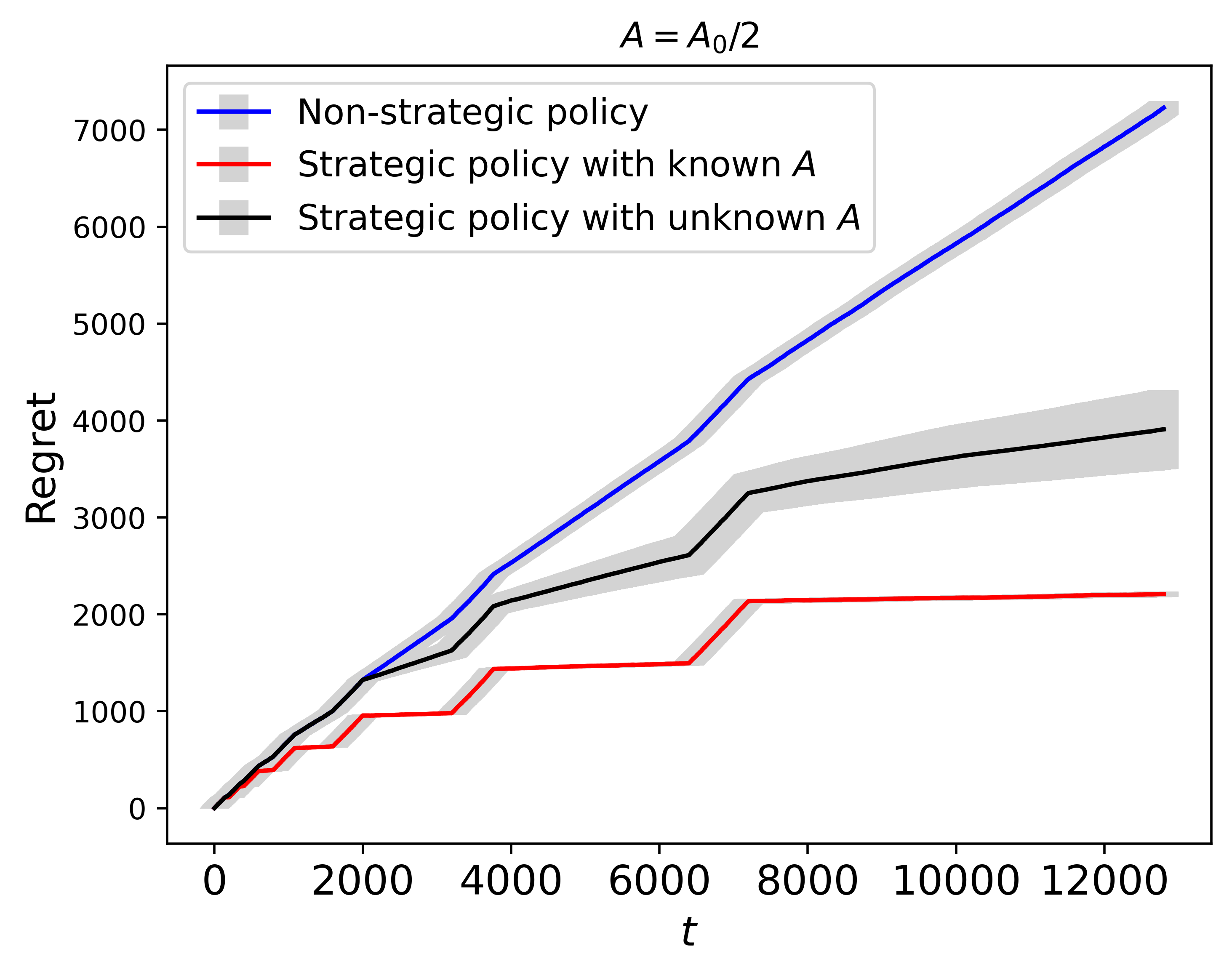

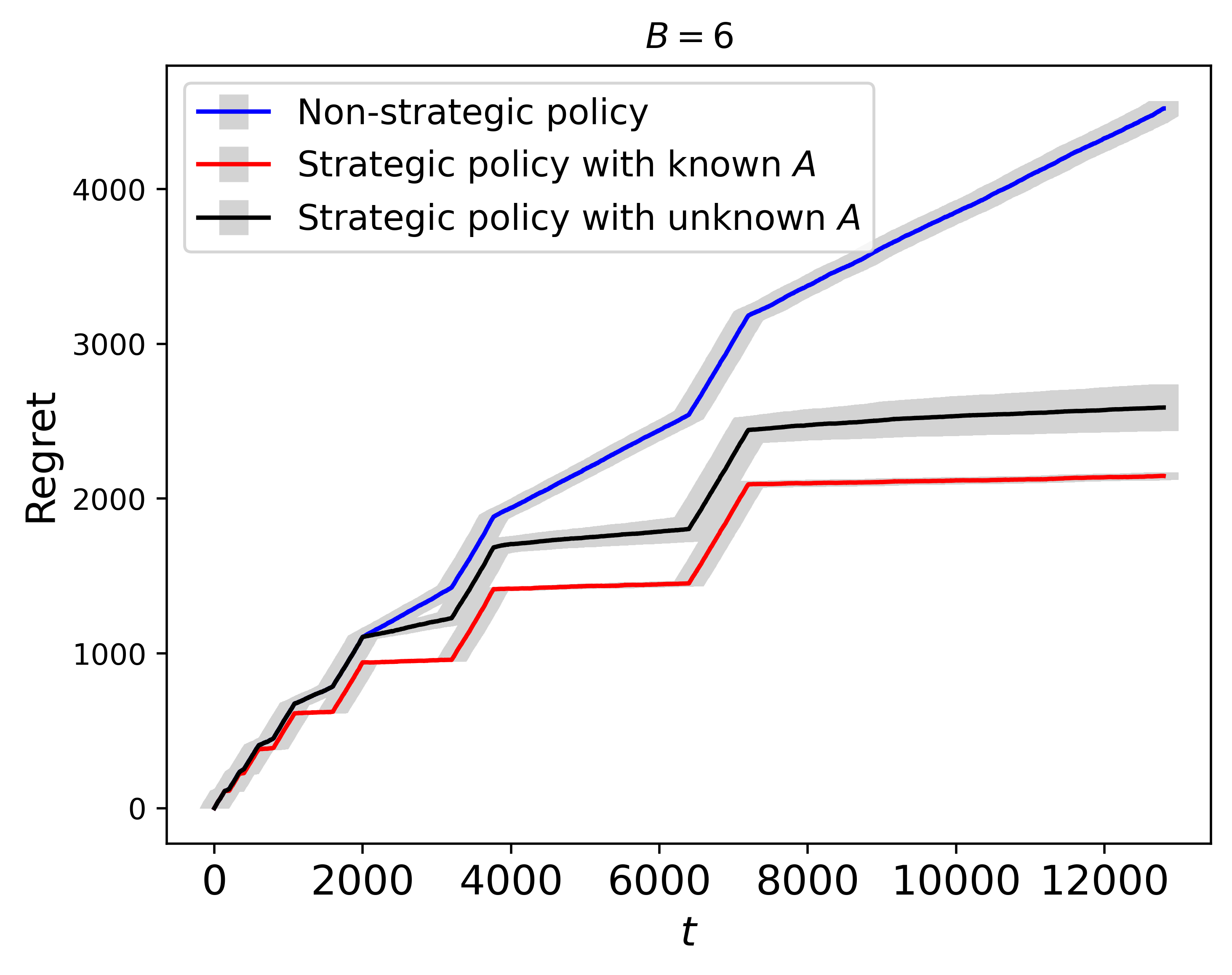

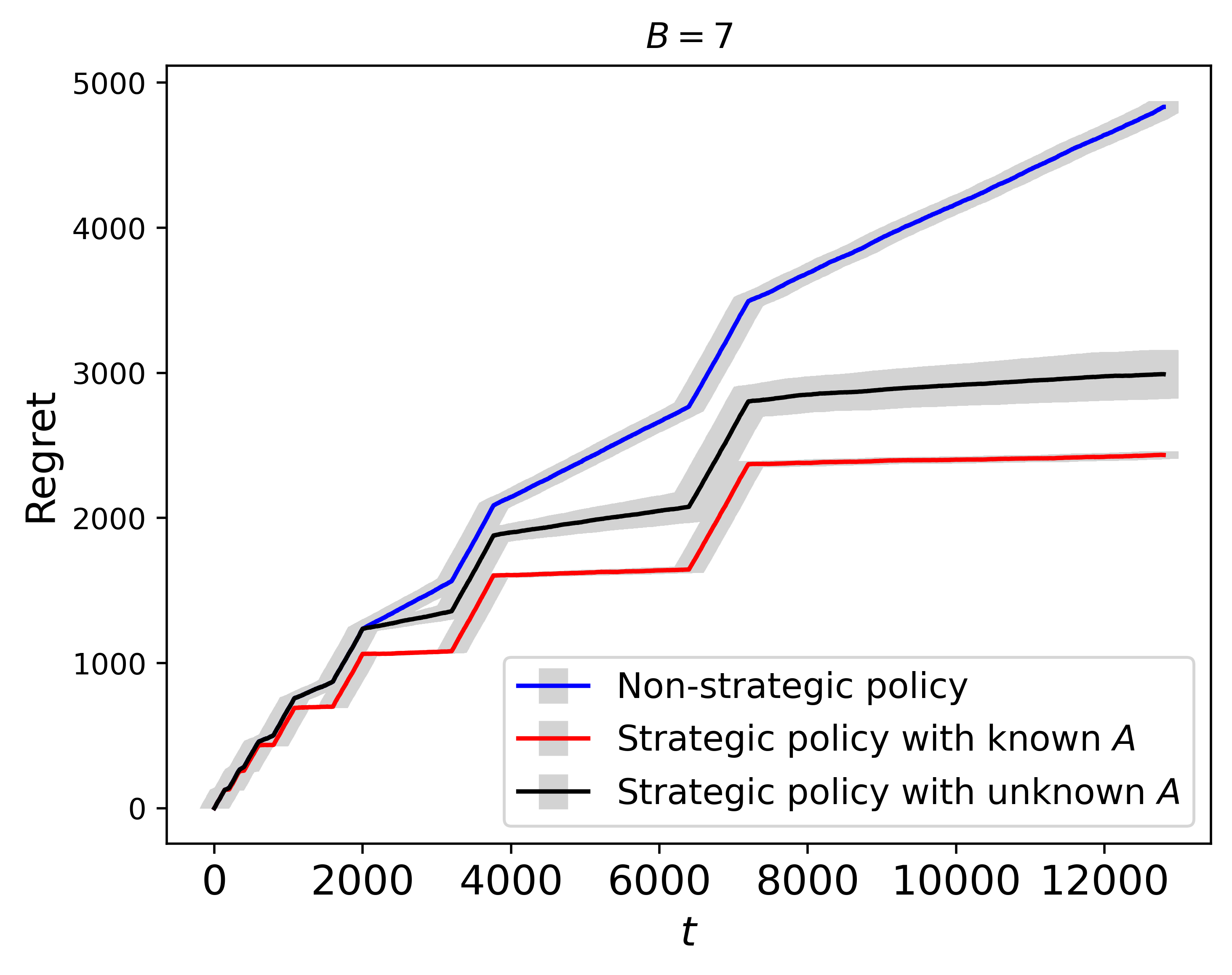

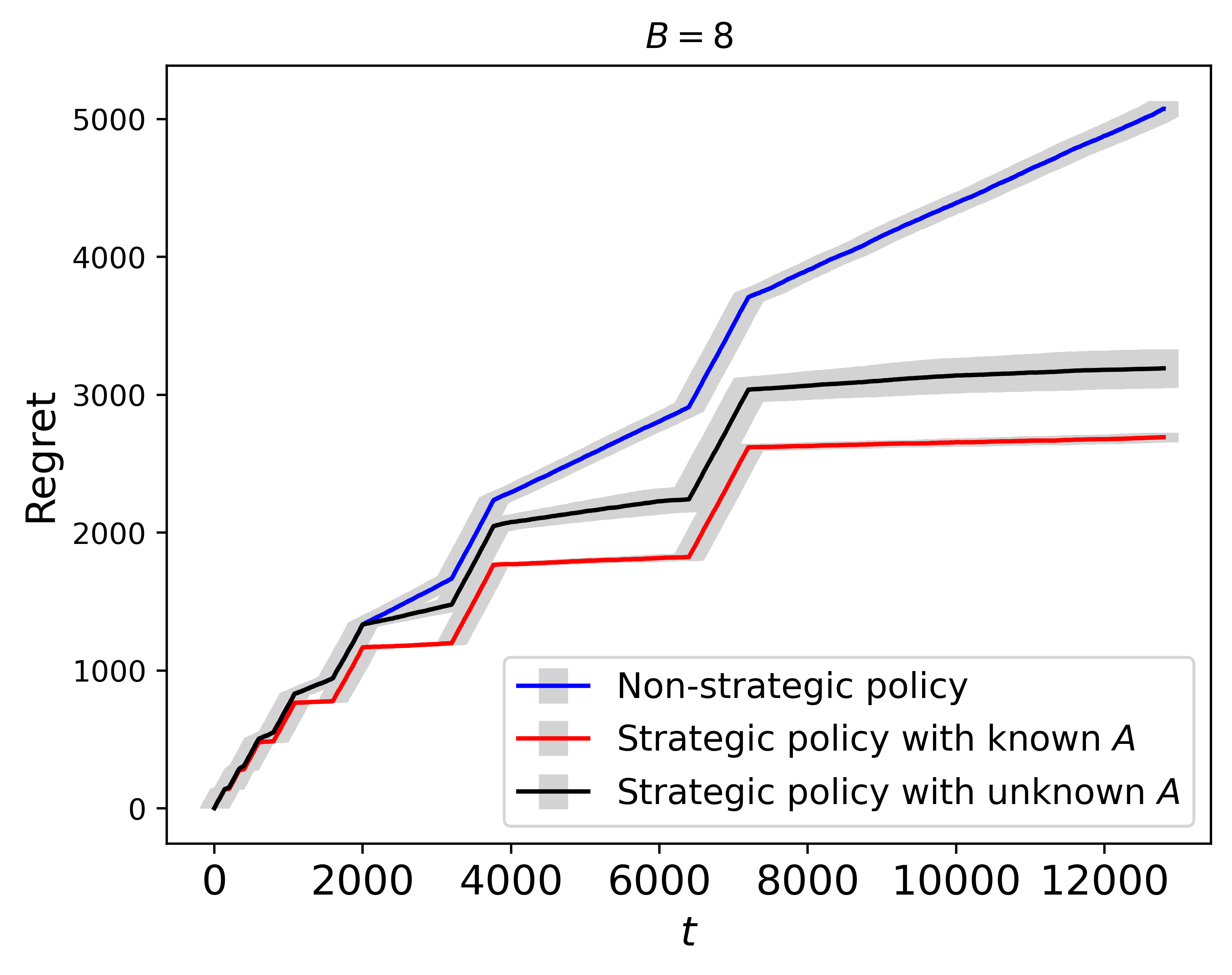

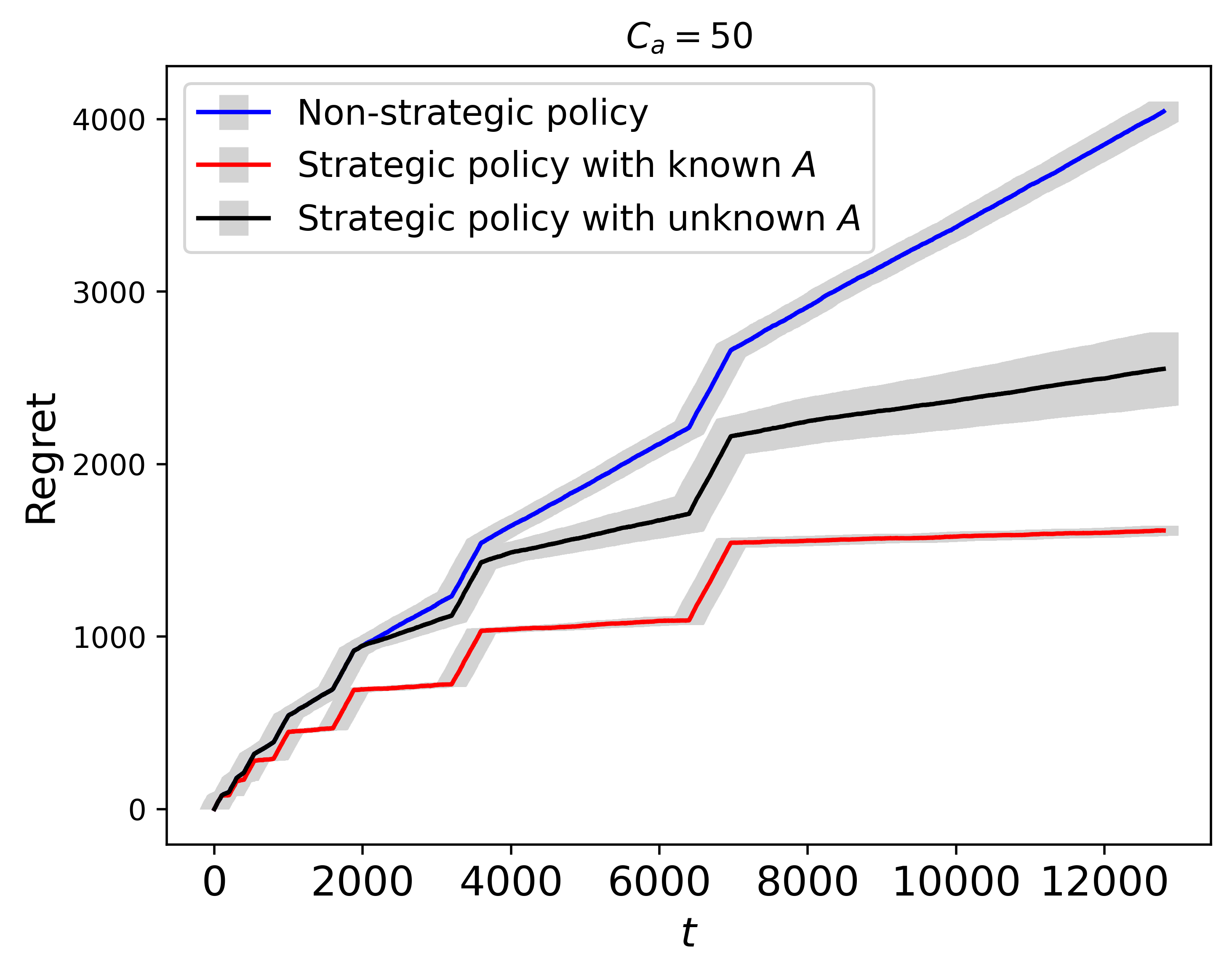

In this section, we compare the performance of the strategic and non-strategic pricing policies. Figure 3 shows the regrets of the non-strategic pricing policy, the strategic pricing policies with known and unknown marginal cost . We set .

|

|

Based on the results presented in Figure 3, it can be concluded that the non-strategic policy generates larger rates of empirical regrets increment compared to the strategic policies under both settings and . The performance comparison between the strategic policy with known and unknown depends on the repeat buyer rate of the buyer. For smaller , the regret of the strategic policy with unknown is higher. As increases, the gap of regrets between these two policies decreases. This phenomenon can be attributed to two reasons. Firstly, with a larger , the estimate of becomes more accurate, leading to a lower regret. Secondly, a larger indicates the presence of more returning buyers. In the strategic policy with unknown marginal cost , the seller is assumed to record the information of the buyer. If the buyer’s information is stored in the seller’s system, the seller can set the price based on , which also results in a smaller regret. It indicates that collecting and storing buyer information thus helps the seller increase the profit, which has a great practical significance.

6.1.2 Impact of Marginal Cost on Strategic Pricing Policy

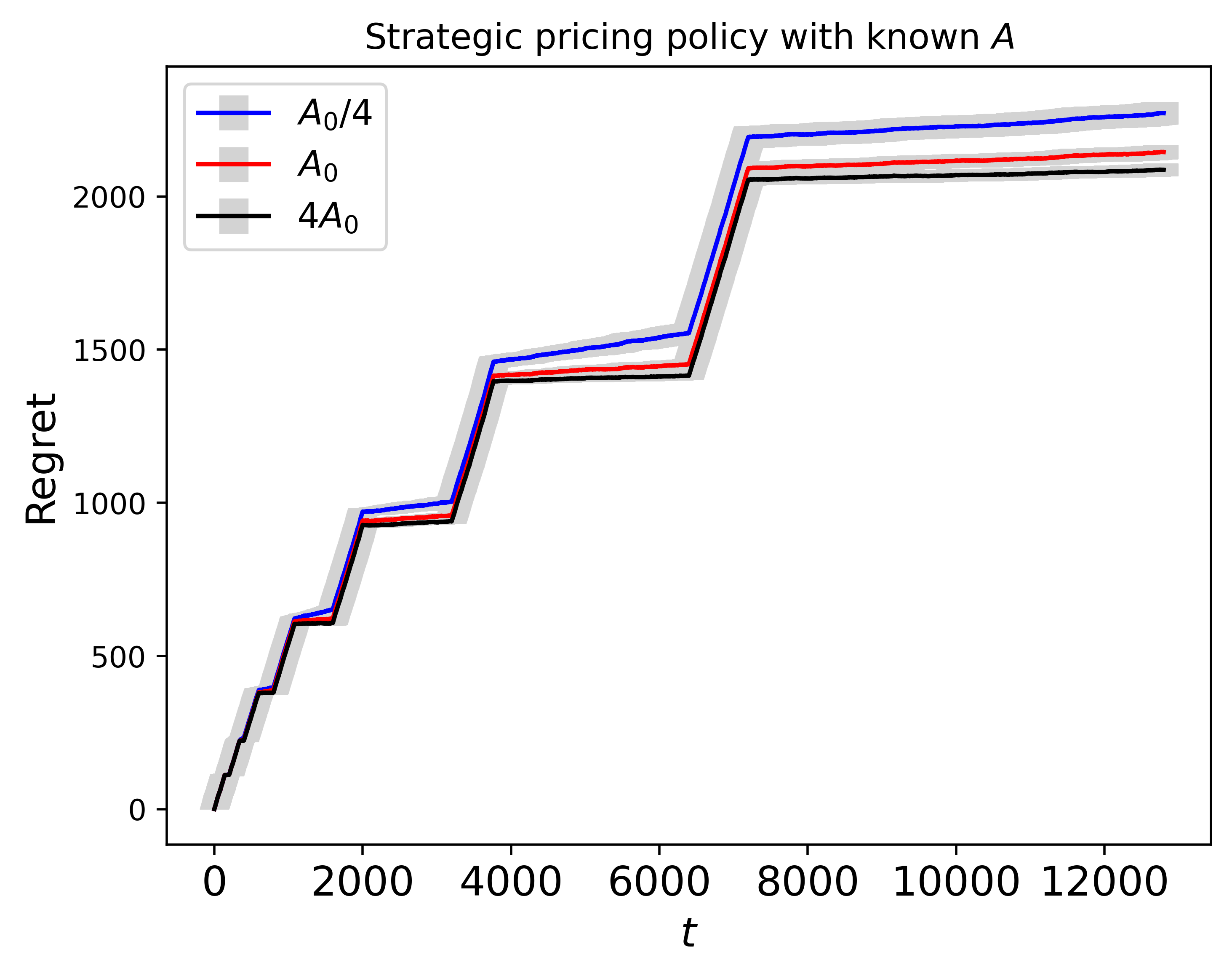

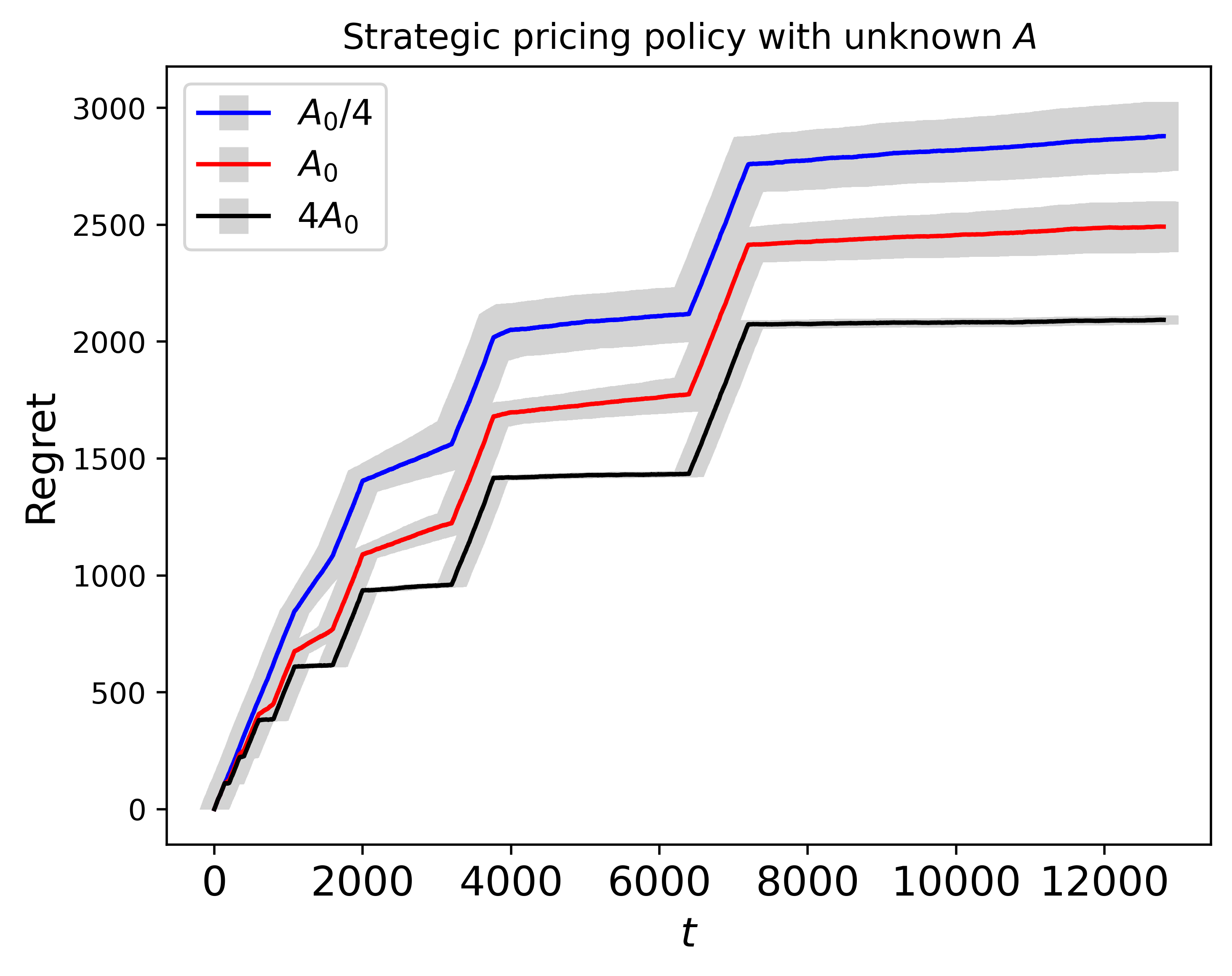

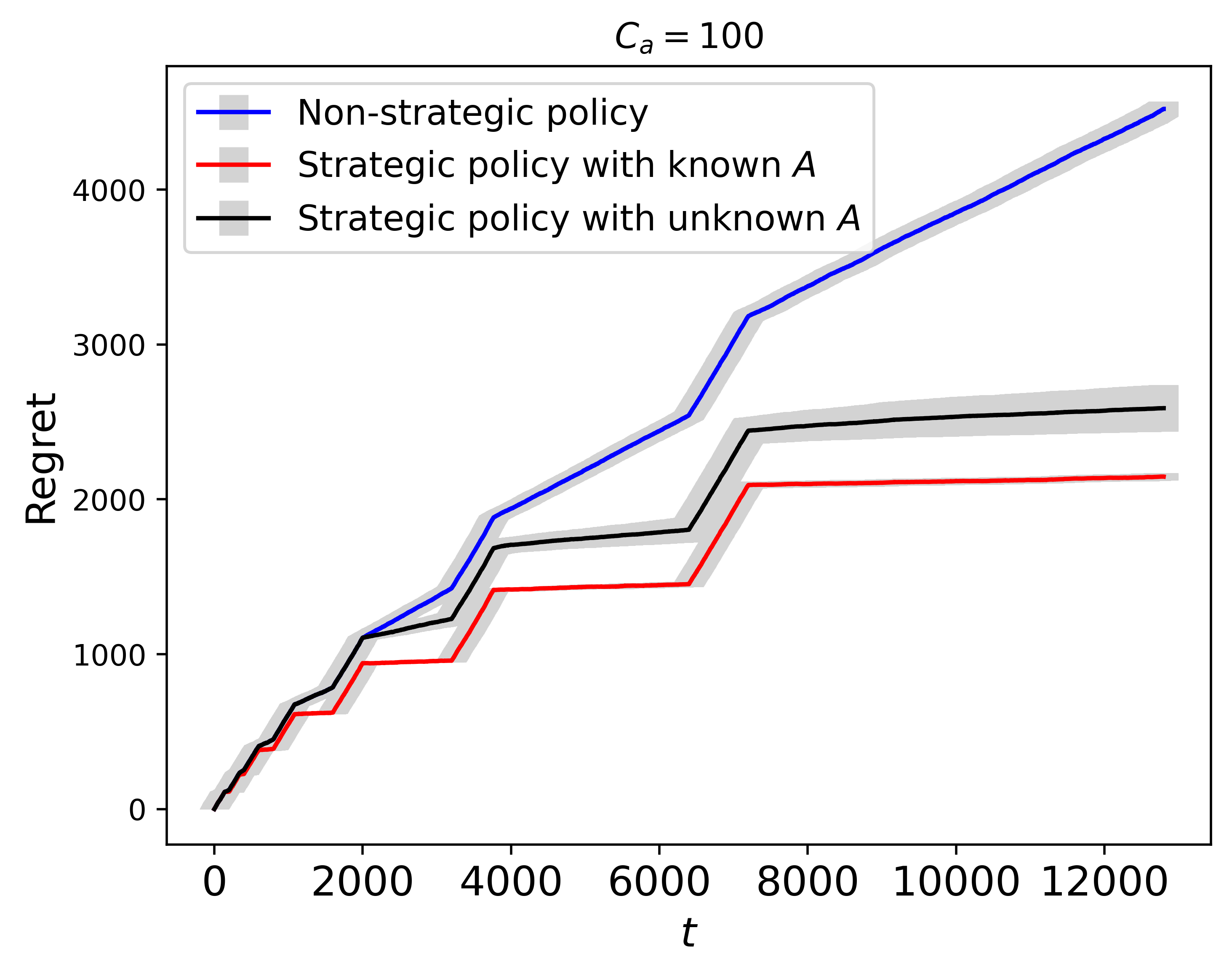

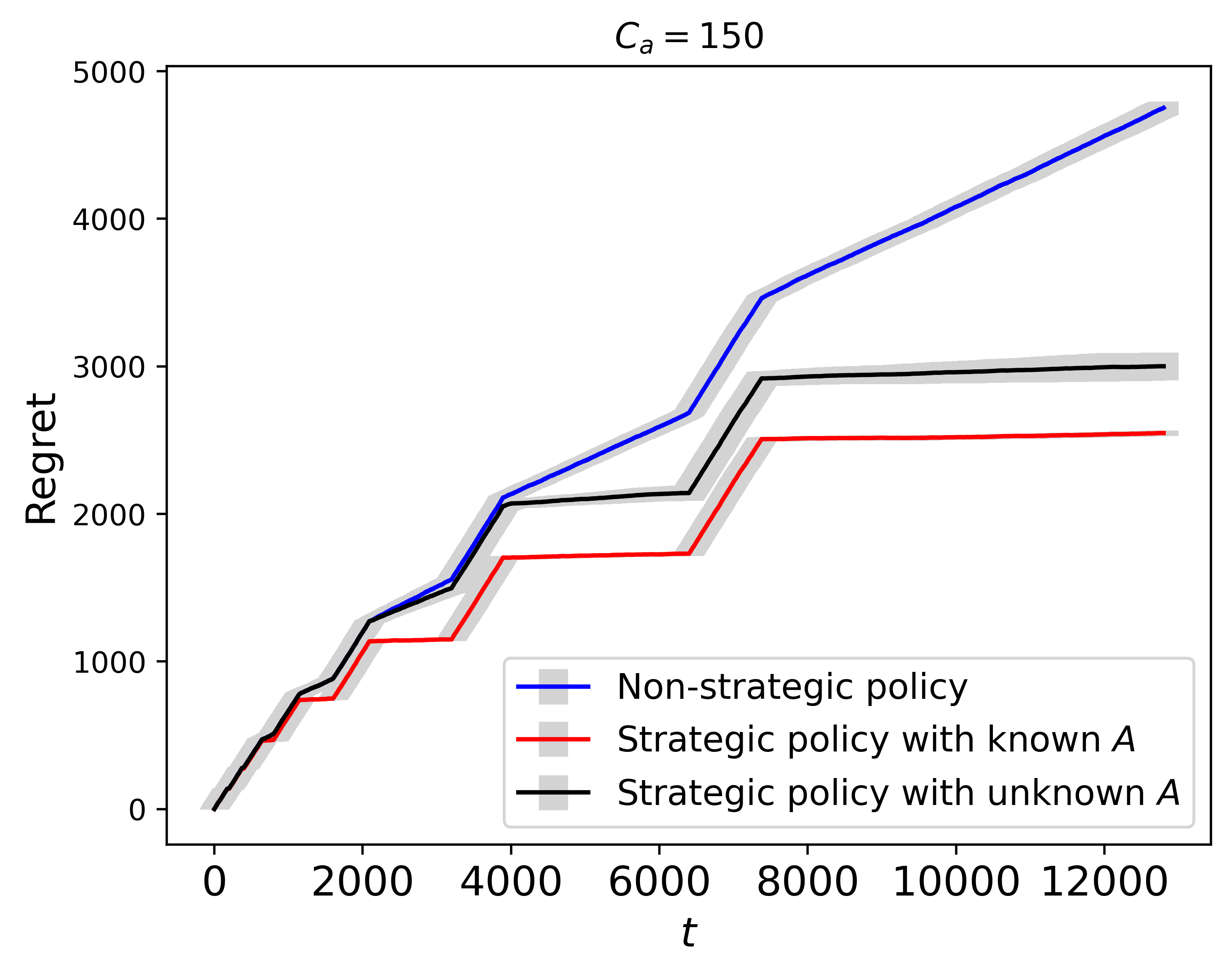

In this section, we study the impact of the marginal cost on the strategic pricing policy. We set .

|

|

The marginal costs, denoted as , , and , are intentionally designed to have varying minimum eigenvalues. Specifically, has the smallest minimum eigenvalue, while has the largest minimum eigenvalue. In Figure 4, we observe the impact of different marginal costs on the regret. It is evident that the pricing policy based on the marginal cost yields the lowest regret, whereas the policy based on results in the highest regret, regardless of whether the marginal cost is known or unknown. This observation aligns with the findings of Theorems 2 and 3.

6.1.3 Impact of Repeat Buyer Rate on Strategic Pricing Policy

In this section, we investigate the influence of the repeat buyer rate on the strategic pricing policy with an unknown marginal cost. Figure 5 shows that the regret of the strategic pricing policy, in the presence of an unknown marginal cost , with varying repeat buyer rate ’s. Comparing the results at the same marginal cost, we observe that the regret is higher when compared to when . This observation is consistent with the conclusions drawn from Theorem 3. The repeat buyer rate plays a crucial role in determining the effectiveness of the strategic pricing policy under the unknown marginal cost.

|

|

6.2 Sensitivity Tests

In this section, we investigate the sensitivity of our policies to the hyperparameters , , and . Here, represents an upper bound on the price, denotes the minimum episode length, and is a constant used in determining the length of the exploration phase. To assess the sensitivity of our policies, we conduct simulations with different values of these hyperparameters while keeping and fixed.

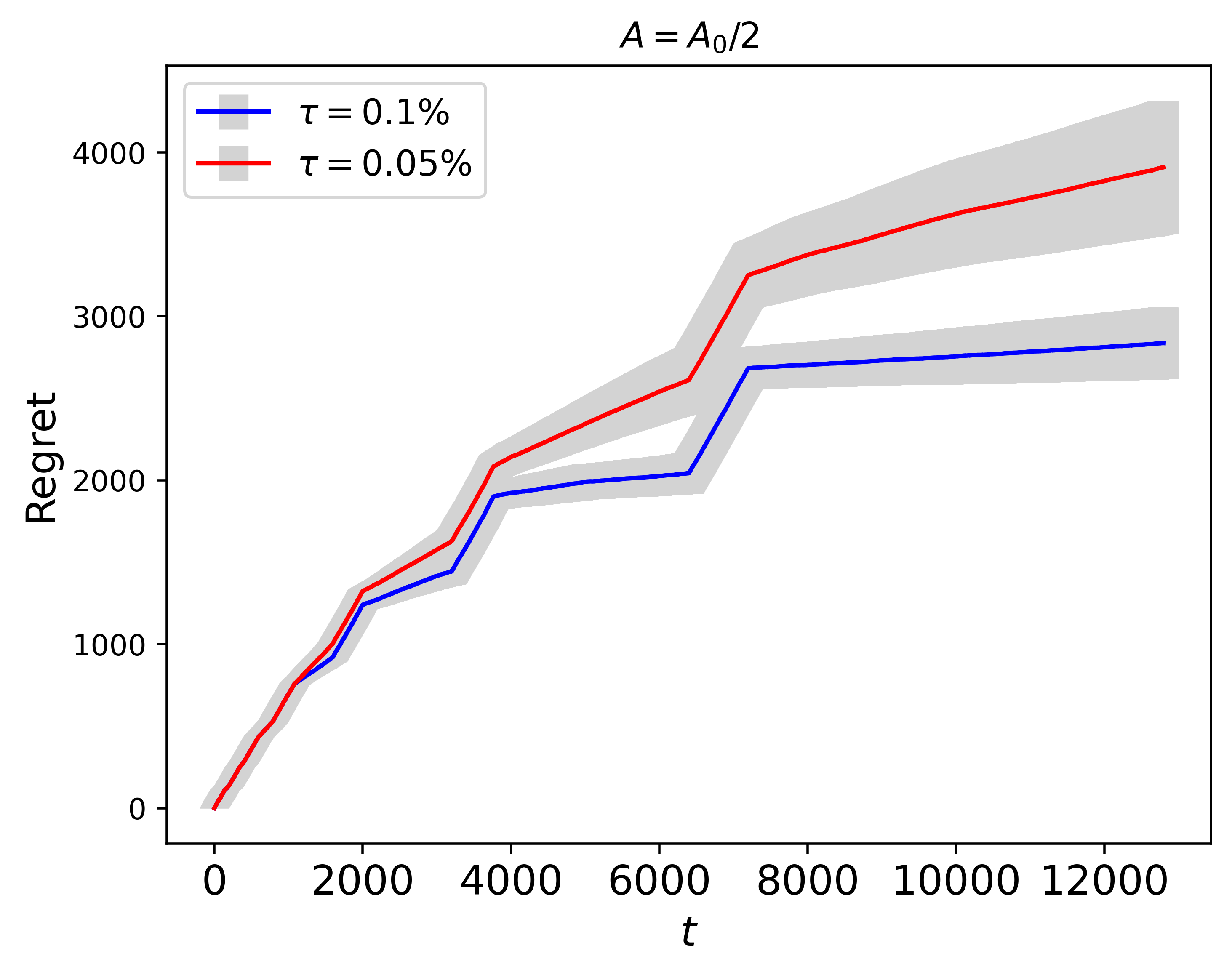

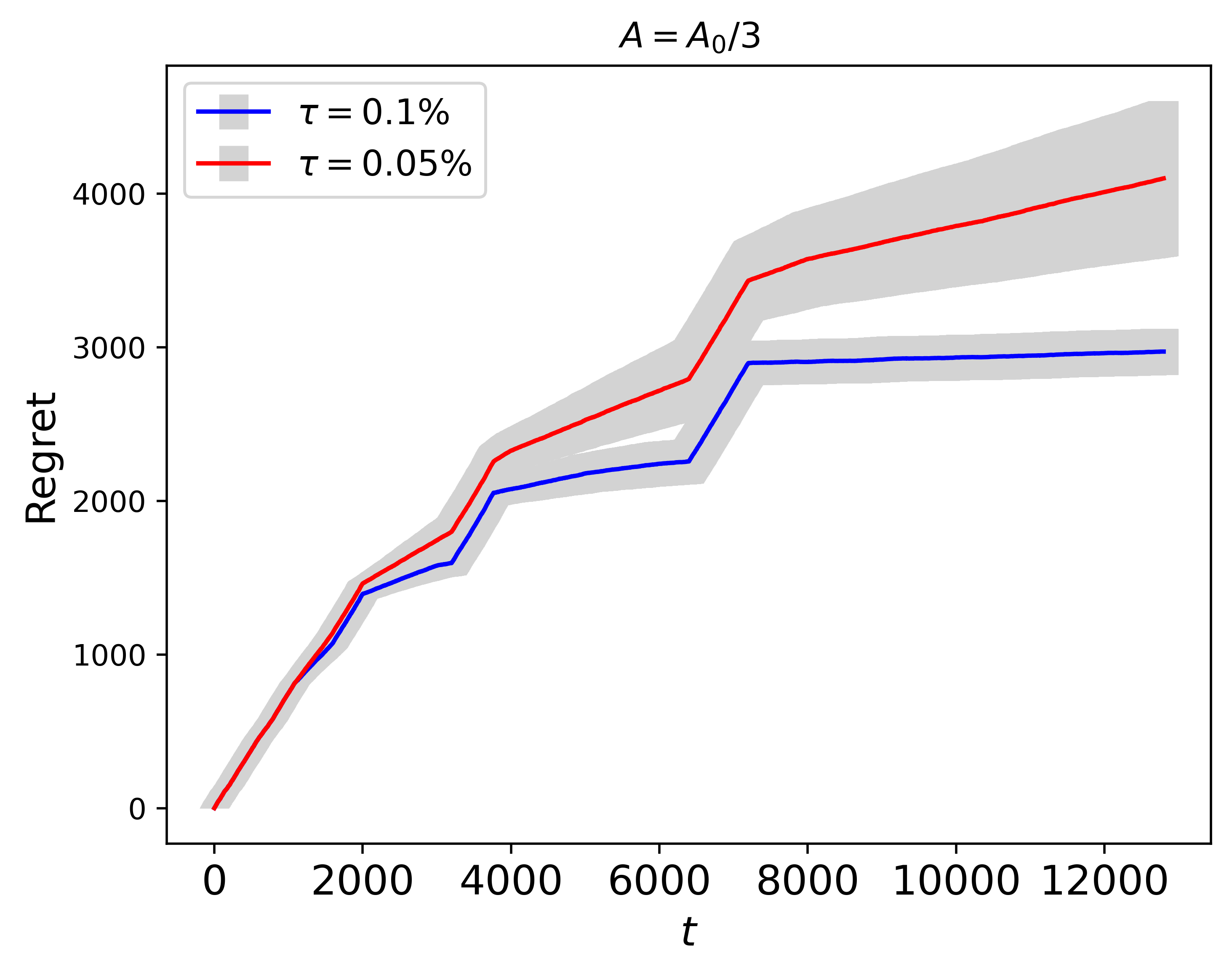

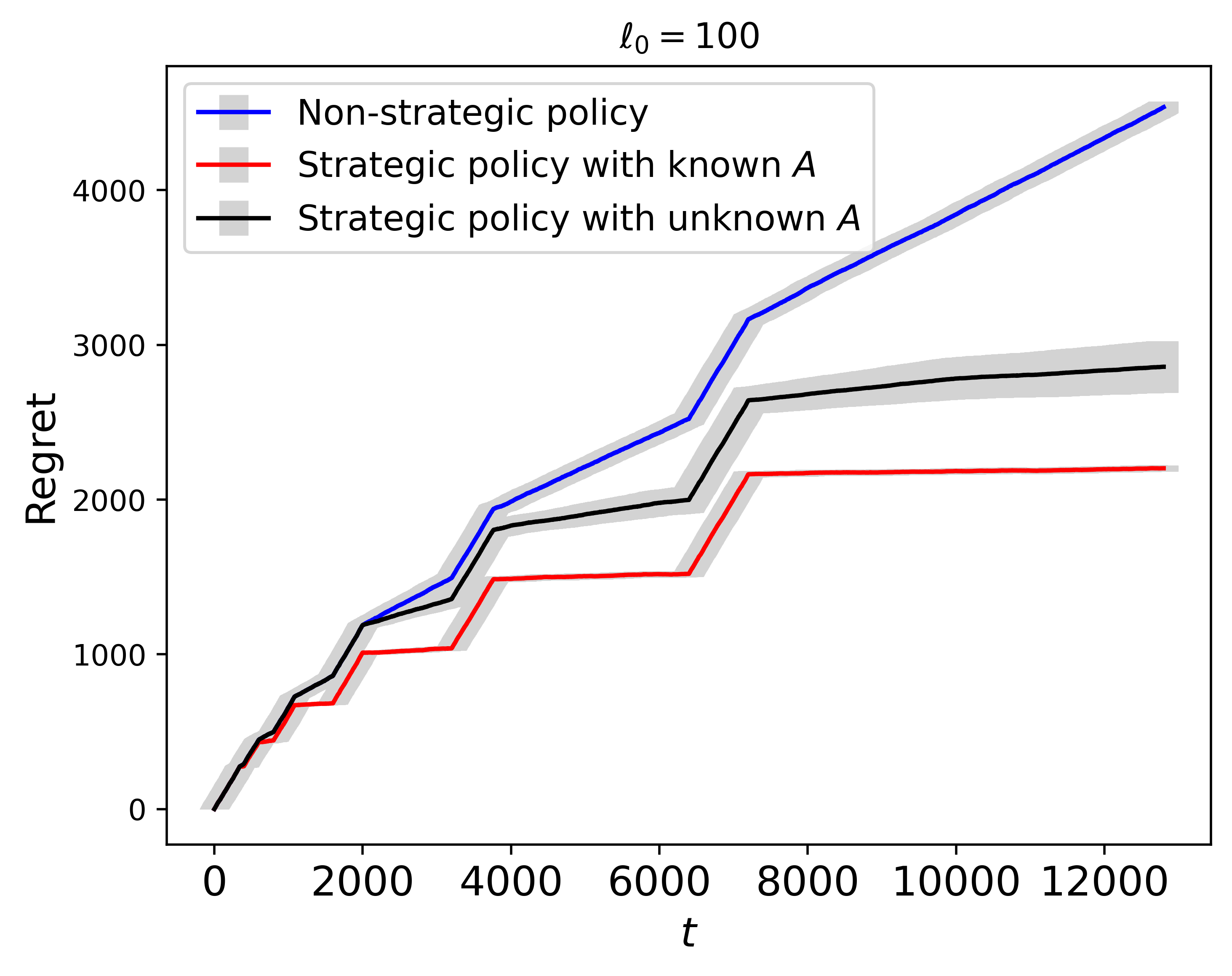

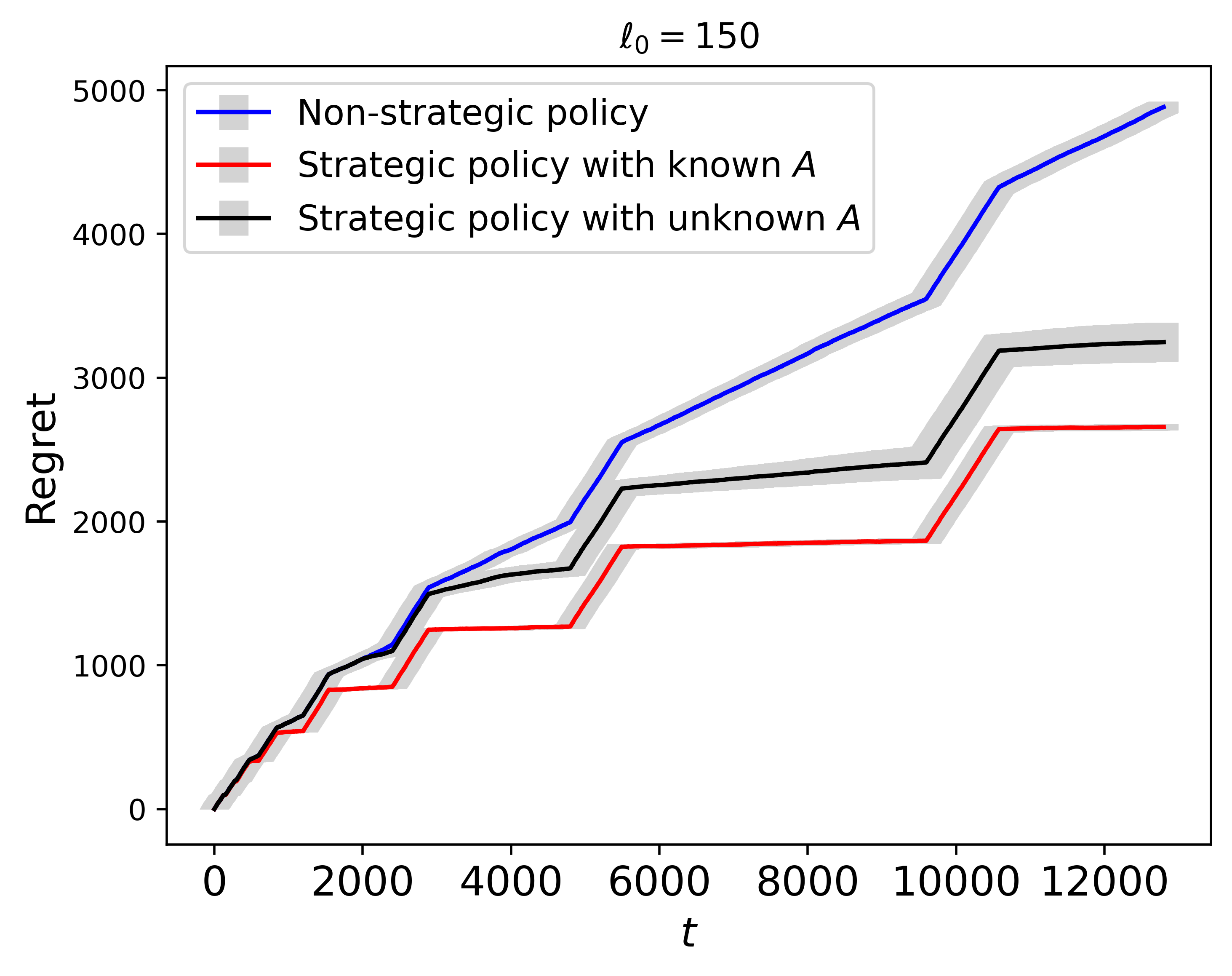

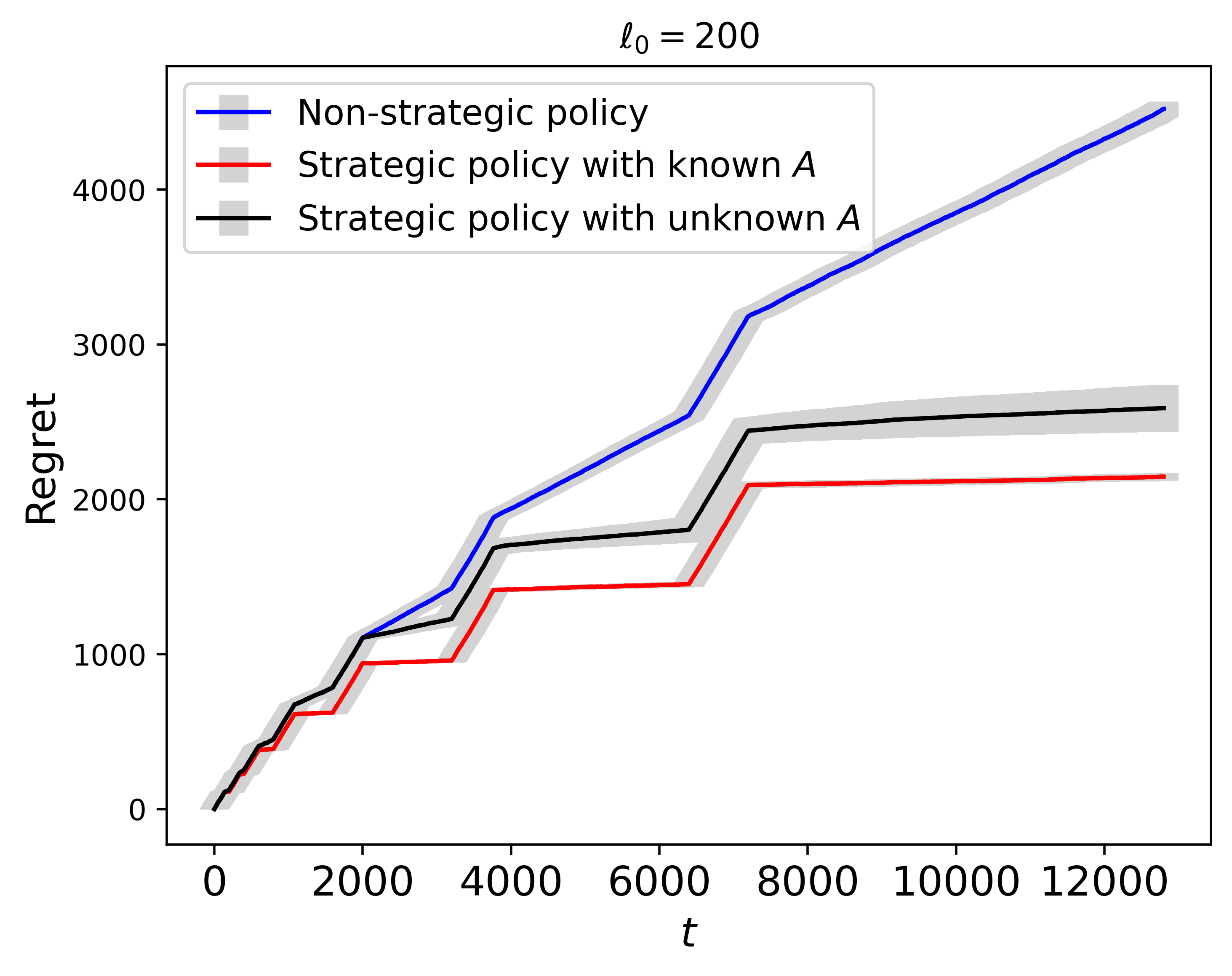

First, we examine the sensitivity of . For these simulations, we set and . Figure 6 illustrates the regrets of the three policies under three scenarios: , , and . The figure demonstrates that the comparison results remain robust across different choices of .

|

|

|

Next, we evaluate the sensitivity of . In these simulations, we set and . Figure 7 displays the regrets of the three policies for three different scenarios: , , and . The figure shows that the comparison results remain consistent across different choices of .

|

|

|

Finally, we assess the sensitivity of . In these simulations, we set and . Figure 8 presents the regrets of the three policies for three different scenarios: , , and . The figure demonstrates that the comparison results are robust across different choices of .

|

|

|

Overall, our sensitivity analysis indicates that the performance of our policies remains consistent and robust under variations in the hyperparameters , , and .

6.3 Real Application

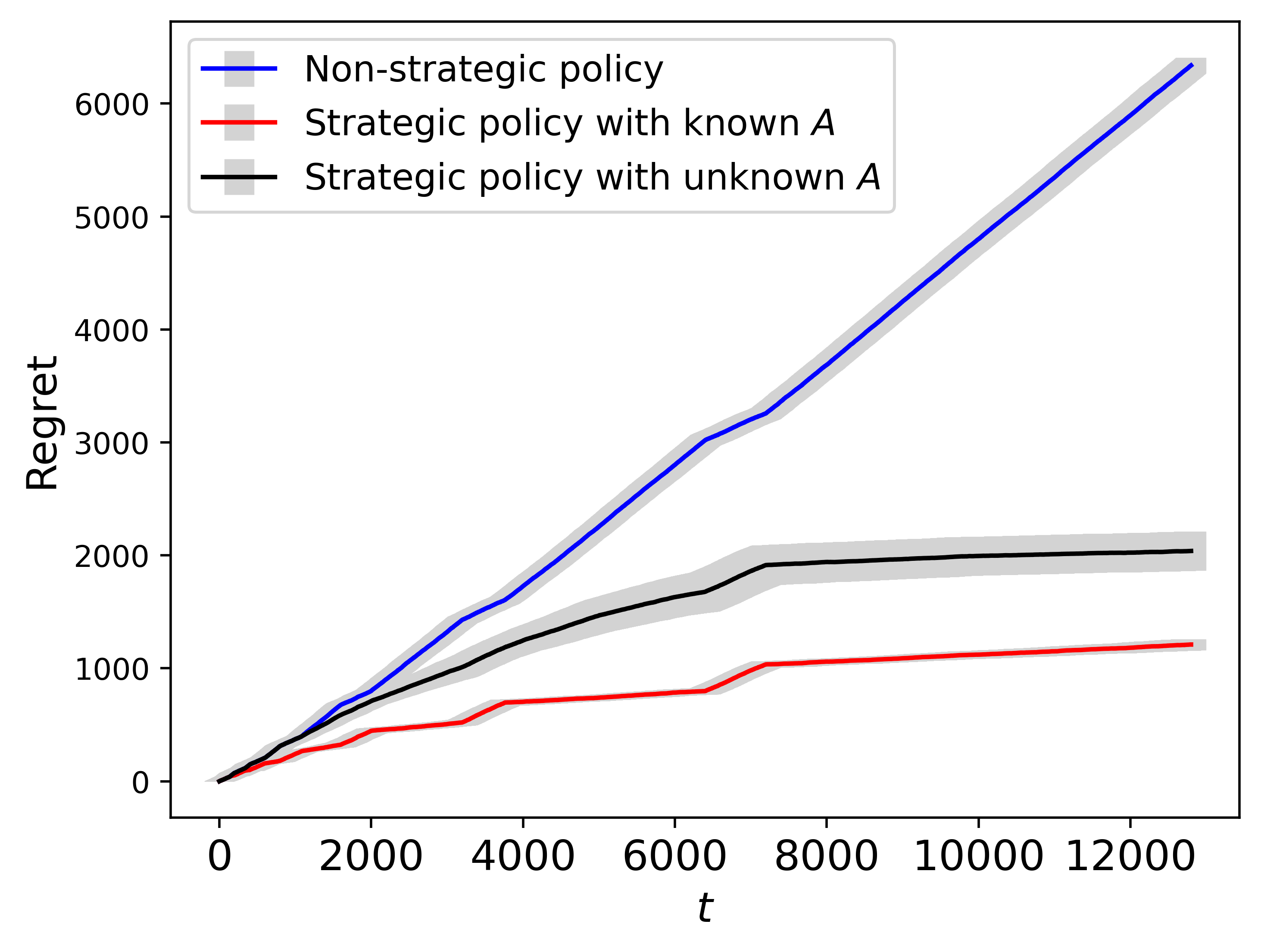

We explore the efficiency of our proposed policy on a real-world auto loan dataset provided by the Center for Pricing and Revenue Management at Columbia University. This dataset has been used by several dynamic pricing works (Phillips et al., 2015; Ban and Keskin, 2021; Bastani et al., 2022; Wang et al., 2022; Fan et al., 2022; Luo et al., 2023). It contains 208,805 auto loan applications received between July 2002 and November 2004. For each application, we observe some loan-specific features such as the amount of loan, the borrower’s information. The dataset also records purchasing decision of the borrowers. We adopt the features used in Ban and Keskin (2021); Fan et al. (2022); Luo et al. (2023) and consider the following four features: the loan amount approved, FICO score, prime rate, and the competitor’s rate. The price of a loan is computed by Monthly Payment Loan Amount, and the rate is set at (Fan et al., 2022; Luo et al., 2022).

We acknowledge that online responses to any dynamic pricing strategy are not available unless a real online experiment is conducted. To address this issue, we adopt the calibration approach used in Ban and Keskin (2021); Wang et al. (2022); Fan et al. (2022); Luo et al. (2023) to first estimate the binary choice model using the entire dataset and leverage it as the ground truth for our online evaluation. We randomly sample 12,800 applications from the original dataset for 20 times and apply the policies to each of the 20 replications and then record the average cumulative regrets. In the experiment, we assume , and , and set and .

|

Figure 9 depicts the cumulative regret of the non-strategic pricing policy compared to our proposed strategic pricing policies. It is evident from the plot that the cumulative regret of the non-strategic policy increases at a much faster rate compared to our strategic policies. This observation aligns with our previous findings in the simulated data. The strategic policies, which take into account the potential manipulation behavior of buyers, outperform the non-strategic policy in terms of the cumulative regret.

7 Conclusion

In this paper, we propose new strategic dynamic pricing policies for the contextual pricing problem with strategic buyers. We establish a sublinear regret bound for the proposed policy, improving the regret lower bound of existing non-strategic pricing policies.

There are several promising avenues for future exploration. Firstly, we can examine the strategic dynamic pricing problem under an unknown noise distribution . One possible solution is to incorporate the method of estimating proposed in Fan et al. (2022) into our policy. Secondly, we can study the pricing problem of strategic buyers by incorporating fairness-oriented policy (Chen et al., 2021; Fang et al., 2022). Thirdly, we can explore the strategic pricing problem with censored demand (Qi et al., 2022), unobserved confounding (Qi et al., 2023), high-dimensional features (Hao et al., 2020; Shi et al., 2021; Zhao et al., 2023), or adversarial setting (Cohen et al., 2020; Xu and Wang, 2021, 2022). Finally, when the feature distribution is non-stationary, we can explore the dynamic pricing problem with more general reinforcement learning settings (Zhu et al., 2015; Li et al., 2022; Shi et al., 2022; Hambly et al., 2023).

References

- Amin et al. (2014) Amin, K., Rostamizadeh, A., and Syed, U. (2014), “Repeated Contextual Auctions with Strategic Buyers,” in Advances in Neural Information Processing Systems, eds. Ghahramani, Z., Welling, M., Cortes, C., Lawrence, N., and Weinberger, K., Curran Associates, Inc., vol. 27.

- Ban and Keskin (2021) Ban, G.-Y. and Keskin, N. B. (2021), “Personalized Dynamic Pricing with Machine Learning: High-Dimensional Features and Heterogeneous Elasticity,” Management Science, 67, 5549–5568.

- Bastani et al. (2022) Bastani, H., Simchi-Levi, D., and Zhu, R. (2022), “Meta Dynamic Pricing: Transfer Learning Across Experiments,” Management Science, 68, 1865–1881.

- Bechavod et al. (2021) Bechavod, Y., Ligett, K., Wu, S., and Ziani, J. (2021), “Gaming Helps! Learning from Strategic Interactions in Natural Dynamics,” in Proceedings of The 24th International Conference on Artificial Intelligence and Statistics, eds. Banerjee, A. and Fukumizu, K., PMLR, vol. 130 of Proceedings of Machine Learning Research, pp. 1234–1242.

- Bechavod et al. (2022) Bechavod, Y., Podimata, C., Wu, S., and Ziani, J. (2022), “Information Discrepancy in Strategic Learning,” in Proceedings of the 39th International Conference on Machine Learning, eds. Chaudhuri, K., Jegelka, S., Song, L., Szepesvari, C., Niu, G., and Sabato, S., PMLR, vol. 162 of Proceedings of Machine Learning Research, pp. 1691–1715.

- Behera and Bala (2023) Behera, R. K. and Bala, P. K. (2023), “Unethical use of information access and analytics in B2B service organisations: The dark side of behavioural loyalty,” Industrial Marketing Management, 109, 14–31.

- Broder and Rusmevichientong (2012) Broder, J. and Rusmevichientong, P. (2012), “Dynamic Pricing Under a General Parametric Choice Model,” Operations Research, 60, 965–980.

- Bó et al. (2023) Bó, I., Chen, L., and Hakimov, R. (2023), “Strategic Responses to Personalized Pricing and Demand for Privacy: An Experiment,” arXiv preprint arXiv:2304.11415.

- Błaszczyński et al. (2021) Błaszczyński, J., de Almeida Filho, A. T., Matuszyk, A., Szeląg, M., and Słowiński, R. (2021), “Auto loan fraud detection using dominance-based rough set approach versus machine learning methods,” Expert Systems with Applications, 163, 113740.

- Chen et al. (2022) Chen, X., Gao, J., Ge, D., and Wang, Z. (2022), “Bayesian dynamic learning and pricing with strategic customers,” Production and Operations Management, 31, 3125–3142.

- Chen et al. (2021) Chen, X., Zhang, X., and Zhou, Y. (2021), “Fairness-aware Online Price Discrimination with Nonparametric Demand Models,” arXiv preprint arXiv:2111.08221.

- Chen and Farias (2018) Chen, Y. and Farias, V. F. (2018), “Robust Dynamic Pricing with Strategic Customers,” Mathematics of Operations Research, 43, 1119–1142.

- Chen et al. (2020) Chen, Y., Liu, Y., and Podimata, C. (2020), “Learning Strategy-Aware Linear Classifiers,” in Advances in Neural Information Processing Systems, eds. Larochelle, H., Ranzato, M., Hadsell, R., Balcan, M., and Lin, H., Curran Associates, Inc., vol. 33, pp. 15265–15276.

- Cohen et al. (2020) Cohen, M. C., Lobel, I., and Paes Leme, R. (2020), “Feature-Based Dynamic Pricing,” Management Science, 66, 4921–4943.

- Dong et al. (2018) Dong, J., Roth, A., Schutzman, Z., Waggoner, B., and Wu, Z. S. (2018), “Strategic Classification from Revealed Preferences,” in Proceedings of the 2018 ACM Conference on Economics and Computation, New York, NY, USA: Association for Computing Machinery, p. 55–70.

- Fan et al. (2022) Fan, J., Guo, Y., and Yu, M. (2022), “Policy Optimization Using Semiparametric Models for Dynamic Pricing,” Journal of the American Statistical Association, in press.

- Fang et al. (2022) Fang, E. X., Wang, Z., and Wang, L. (2022), “Fairness-Oriented Learning for Optimal Individualized Treatment Rules,” Journal of the American Statistical Association, in press.

- Funk (2009) Funk, B. (2009), “Optimizing Price Levels in E-Commerce Applications with Respect to Customer Lifetime Values,” in Proceedings of the 11th International Conference on Electronic Commerce, Association for Computing Machinery, ICEC ’09, p. 169–175.

- Ghalme et al. (2021) Ghalme, G., Nair, V., Eilat, I., Talgam-Cohen, I., and Rosenfeld, N. (2021), “Strategic Classification in the Dark,” in Proceedings of the 38th International Conference on Machine Learning, eds. Meila, M. and Zhang, T., PMLR, vol. 139 of Proceedings of Machine Learning Research, pp. 3672–3681.

- Golrezaei et al. (2023) Golrezaei, N., Jaillet, P., and Cheuk Nam Liang, J. (2023), “Incentive-aware Contextual Pricing with Non-parametric Market Noise,” in Proceedings of The 26th International Conference on Artificial Intelligence and Statistics, eds. Ruiz, F., Dy, J., and van de Meent, J.-W., PMLR, vol. 206 of Proceedings of Machine Learning Research, pp. 9331–9361.

- Golrezaei et al. (2019) Golrezaei, N., Javanmard, A., and Mirrokni, V. (2019), “Dynamic Incentive-Aware Learning: Robust Pricing in Contextual Auctions,” in Advances in Neural Information Processing Systems, vol. 32.

- Hambly et al. (2023) Hambly, B., Xu, R., and Yang, H. (2023), “Recent advances in reinforcement learning in finance,” Mathematical Finance, 33, 437–503.

- Hannak et al. (2014) Hannak, A., Soeller, G., Lazer, D., Mislove, A., and Wilson, C. (2014), “Measuring Price Discrimination and Steering on E-Commerce Web Sites,” in Proceedings of the 2014 Conference on Internet Measurement Conference, Association for Computing Machinery, p. 305–318.

- Hao et al. (2020) Hao, B., Lattimore, T., and Wang, M. (2020), “High-Dimensional Sparse Linear Bandits,” in Advances in Neural Information Processing Systems, eds. Larochelle, H., Ranzato, M., Hadsell, R., Balcan, M., and Lin, H., Curran Associates, Inc., vol. 33, pp. 10753–10763.

- Hardt et al. (2016) Hardt, M., Megiddo, N., Papadimitriou, C., and Wootters, M. (2016), “Strategic Classification,” in Proceedings of the 2016 ACM Conference on Innovations in Theoretical Computer Science, p. 111–122.

- Javanmard and Nazerzadeh (2019) Javanmard, A. and Nazerzadeh, H. (2019), “Dynamic Pricing in High-dimensions,” Journal of Machine Learning Research, 20, 1–49.

- Koren and Levy (2015) Koren, T. and Levy, K. (2015), “Fast Rates for Exp-concave Empirical Risk Minimization,” in Advances in Neural Information Processing Systems, eds. Cortes, C., Lawrence, N., Lee, D., Sugiyama, M., and Garnett, R., Curran Associates, Inc., vol. 28.

- Li et al. (2022) Li, G., Chi, Y., Wei, Y., and Chen, Y. (2022), “Minimax-Optimal Multi-Agent RL in Markov Games With a Generative Model,” in Advances in Neural Information Processing Systems, eds. Koyejo, S., Mohamed, S., Agarwal, A., Belgrave, D., Cho, K., and Oh, A., Curran Associates, Inc., vol. 35, pp. 15353–15367.

- Li and Li (2023) Li, X. and Li, K. J. (2023), “Beating the Algorithm: Consumer Manipulation, Personalized Pricing, and Big Data Management,” Manufacturing Service Operations Management, 25, 36–49.

- Luo et al. (2022) Luo, Y., Sun, W. W., and Liu, Y. (2022), “Contextual Dynamic Pricing with Unknown Noise: Explore-then-UCB Strategy and Improved Regrets,” in Advances in Neural Information Processing Systems, eds. Oh, A. H., Agarwal, A., Belgrave, D., and Cho, K.

- Luo et al. (2023) Luo, Y., Sun, W. W., and Liu, Y. (2023), “Distribution-Free Contextual Dynamic Pricing,” Mathematics of Operations Research, in press.

- Mikians et al. (2013) Mikians, J., Gyarmati, L., Erramilli, V., and Laoutaris, N. (2013), “Crowd-Assisted Search for Price Discrimination in e-Commerce: First Results,” in Proceedings of the Ninth ACM Conference on Emerging Networking Experiments and Technologies, Association for Computing Machinery, p. 1–6.

- Miller et al. (2020) Miller, J., Milli, S., and Hardt, M. (2020), “Strategic Classification is Causal Modeling in Disguise,” in Proceedings of the 37th International Conference on Machine Learning, eds. III, H. D. and Singh, A., vol. 119 of Proceedings of Machine Learning Research, pp. 6917–6926.

- Mohri and Munoz (2015) Mohri, M. and Munoz, A. (2015), “Revenue Optimization against Strategic Buyers,” in Advances in Neural Information Processing Systems, eds. Cortes, C., Lawrence, N., Lee, D., Sugiyama, M., and Garnett, R., Curran Associates, Inc., vol. 28.

- Phillips et al. (2015) Phillips, R., Şimşek, A. S., and van Ryzin, G. (2015), “The Effectiveness of Field Price Discretion: Empirical Evidence from Auto Lending,” Management Science, 61, 1741–1759.

- Qi et al. (2023) Qi, Z., Miao, R., and Zhang, X. (2023), “Proximal learning for individualized treatment regimes under unmeasured confounding,” Journal of the American Statistical Association, 1–14.

- Qi et al. (2022) Qi, Z., Tang, J., Fang, E., and Shi, C. (2022), “Offline Feature-Based Pricing under Censored Demand: A Causal Inference Approach,” Available at SSRN 4040305.

- Shao et al. (2023) Shao, H., Blum, A., and Montasser, O. (2023), “Strategic Classification under Unknown Personalized Manipulation,” arXiv preprint arXiv:2305.16501.

- Shi et al. (2021) Shi, C., Song, R., Lu, W., and Li, R. (2021), “Statistical Inference for High-Dimensional Models via Recursive Online-Score Estimation,” Journal of the American Statistical Association, 116, 1307–1318.

- Shi et al. (2022) Shi, C., Zhu, J., Ye, S., Luo, S., Zhu, H., and Song, R. (2022), “Off-Policy Confidence Interval Estimation with Confounded Markov Decision Process,” Journal of the American Statistical Association, in press.

- Wang et al. (2022) Wang, C.-H., Wang, Z., Sun, W. W., and Cheng, G. (2022), “Online Regularization towards Always-Valid High-Dimensional Dynamic Pricing,” arXiv preprint arXiv:2007.02470.

- Xu and Wang (2021) Xu, J. and Wang, Y.-X. (2021), “Logarithmic Regret in Feature-based Dynamic Pricing,” in Advances in Neural Information Processing Systems, vol. 34, pp. 13898–13910.

- Xu and Wang (2022) Xu, J. and Wang, Y.-X. (2022), “Towards Agnostic Feature-based Dynamic Pricing: Linear Policies vs Linear Valuation with Unknown Noise,” in Proceedings of The 25th International Conference on Artificial Intelligence and Statistics, eds. Camps-Valls, G., Ruiz, F. J. R., and Valera, I., PMLR, vol. 151 of Proceedings of Machine Learning Research, pp. 9643–9662.

- Zhao et al. (2023) Zhao, Z., Jiang, F., Yu, Y., and Chen, X. (2023), “High-Dimensional Dynamic Pricing under Non-Stationarity: Learning and Earning with Change-Point Detection,” arXiv preprint arXiv:2303.07570.

- Zhu et al. (2015) Zhu, R., Zeng, D., and Kosorok, M. R. (2015), “Reinforcement learning trees,” Journal of the American Statistical Association, 110, 1770–1784.

Supplementary Materials

“Contextual Dynamic Pricing with Strategic Buyers"

Pangpang Liu, Zhuoran Yang, Zhaoran Wang, Will Wei Sun

In this supplement, we provide the detailed proofs of the theorems and the lemmas. Section S.1 gives the proof under the non-strategic pricing policy, , Theorem 1. Section S.2 provides the proofs under the strategic pricing policy with the known marginal cost , including Lemma 1 and Theorem 2. Section S.3 offers the proofs under the strategic pricing policy with the unknown marginal cost , including Lemma 2 and Theorem 3. Section S.4 includes the supporting technical lemmas.

S.1 Proof under non-strategic pricing policy

S.1.1 Proof of Theorem 1

The regret (4) is defined as the maximum gap between a policy and the oracle policy over different and . In order to obtain a lower bound on the regret, it suffices to consider a specific distribution in . We consider the distribution as the uniform distribution on (-1/2, 1/2). The marginal cost matrix is , and .

In order to bound the total regret, we try to bound the regret at each time . The expected revenue at time during the exploitation phase is

By the first-order derivative , the oracle price is

Therefore, the expected revenue at time by the oracle pricing policy is

| (S1) |

We first analyze the regret during the exploration phase. Since the non-strategic price is randomly chosen from the distribution Unif(0, 7/16), The expected revenue at time using non-strategic pricing policy is

| (S2) |

By (S1) and (S2), the expected regret at time during the exploration phase is

| (S3) |

Now, we analyze the regret during the exploitation phase. By (6), the manipulated feature is

| (S4) |

Assume that is in the -th epoch, and is the MLE of . The non-strategic pricing policy is . The difference of the expected revenues between the oracle policy and the non-strategic pricing policy is

| (S5) | ||||

We need to find a lower bound of . We fist analyze . For , we have

| (S6) |

Now, we analyze . By (S4), we have . Therefore,

| (S7) | ||||

Let be a fixed number. When

we have . Therefore, he expected regret at time during the exploitation phase of the episode is

| (S8) |

By (S3) and (S8), the expected regrets at time during both the exploration and exploitation phases are larger than . Therefore, when , we have

S.2 Proof under strategic pricing policy with known

In this section, we first prove Lemma 1, which provides an upper bound on the estimation error of the maximum likelihood estimator. This lemma serves as a crucial building block for the proof of Theorem 2. Once we establish Lemma 1, we proceed to prove Theorem 2.

S.2.1 Proof of Lemma 1

The proof of Lemma 1 is inspired by the proofs in Koren and Levy (2015) and Xu and Wang (2021). We first define the log-likelihood function at time period as

| (S9) |

Next, we define the expected log-likelihood function Before proving Lemma 1, we will first establish two lemmas: Lemma S3, which provides a bound on the error of the expected log-likelihood function, and Lemma S4, which deals with the likelihood error of the maximum likelihood estimator. These lemmas will serve as building blocks for the proof of Lemma 1.

Now, we proceed with the presentation and proof of Lemma S3, where we present a lower bound for .

Lemma S3.

Proof.

By taking the derivative of defined in (S9) with respect to , we have

By Assumptions 1 and 2, we have , where . Next, we take the derivative of , and get

| (S11) | ||||

By Assumption 3, exists. By taking Taylor expansion of at , we have

| (S12) |

where is between and . Since the true parameter always maximizes the expected likelihood function, we have . Taking the expectation of Equation (S12), we have

The first inequality is due to (S11), and the second inequality is due to Assumption 4. ∎

Now, we present an upper bound on the likelihood error of the maximum likelihood estimator.

Lemma S4.

Proof.

We define the "leave-one-out" log-likelihood function as

and let Denote . By (S11), and noting are , and are in the exploration phase, we have

By the singular value decomposition, we have , where . We define . There exist , such that . We define the following new functions,

By taking the second derivative of , we have

Therefore,

Thus, . Therefore, is locally -strongly convex with respect to at . Similarly, we can prove is convex. Let and . Then . We define and . According to Lemma S7, we have

| (S13) |

By the convexity of , we have

| (S14) |

Therefore,

| (S15) |

The first inequality is from (S14) and the Hölder’s inequality, and the second inequality follows (S13). Since

we have

| (S16) |

The second inequality is from Since is the MLE of samples, have exactly the same distribution. Thus,

Noting , the proof is completed. ∎

S.2.2 Proof of Theorem 2

In order to bound the total regret, we first try to bound the regret at each episode . The regret in the exploration phase during the -th episode is bounded by . Now we analyze the upper bound on the regret during the exploitation phase.

We let be the expected revenue. We define the filtration generated by all transaction records up to time as . We also define as the filtration obtained after augmenting by the new feature . We define the regret at time as . Then the conditional expectation of the regret at time given previous information and is

| (S18) |

Note that and hence we have . Using Taylor expansion, we have

| (S19) |

where is some value between and . By Assumptions 2 and 3, we have

| (S20) |

Now we can obtain an upper bound on the conditional expectation of the regret at time given . By (S.2.2), (S19) and (S20), we have

| (S21) |

Now we give an upper bound of . During the episode , for time in the exploitation phase, we have

| (S22) | ||||

The first inequality is due to Lemma S5. The second equality is from Equation (6).

We first analyze . By Lemma 1, we have

| (S23) | ||||

Next, we analyze . By Lemma S6, we assume on the bounded interval for some constant . Therefore,

| (S24) | ||||

The last second inequality is due to Lemma S6. The last inequality is from . Now, we derive a upper bound of . By Equation (6), we have

| (S25) | ||||

The first inequality is because of Assumption 1. Then, by (S24) and (S25), we have

| (S26) | ||||

The first inequality is from Assumption 1, and the third inequality is form Lemma 1. By Equations (S21), (S22), (S23) and (S26), the expected regret at time during the exploitation phase of the episode is

Therefore, The total expected regret during the -th episode including the exploration phase and the exploitation phase is

Denote . We have

Noting that minimizes the upper bound of . Now, since the length of episodes grows exponentially, the number of episodes by period is logarithmic in . Specifically, belongs to episode . Therefore,

Thus, the total expected regret up to time period can be bounded by

Finally, we define two new constants,

The proof is completed.

S.3 Proof under strategic pricing policy with unknown

In this section, our first step is to prove Lemma 2, which establishes an upper bound on the estimation error of . This lemma plays a pivotal role as a fundamental component in the proof of Theorem 2. Once we have successfully demonstrated Lemma 2, we will proceed with the subsequent step of proving Theorem 3.

S.3.1 Proof of Lemma 2

Assume that we obtain samples , and the latest sample is obtained in the -th episode. We define By Equation (11), the estimation error of the -th component of is

| (S27) |

To establish an upper bound on , we need to bound the terms and separately.

Firstly, we derive a lower bound on . Since by Lemma S5 and is continuous, there exists such that over the bounded interval . Let be the estimate of calculated from (7). By the definition of in (9), we have

| (S28) |

Secondly, we derive an upper bound on . By Lemma S6, is locally Lipschitz continuous on . Then there exists constant such that on the bounded interval . Therefore,

| (S29) | ||||

The last inequality is due to (S25). Next, we have

| (S30) | ||||

The second inequality is from Lemma 1. The last inequality is from , and the fact . Noting that , by (S30), we have

| (S31) |

S.3.2 Proof of Theorem 3

The main idea of the proof of Theorem 3 is similar to the proof of Theorem 2. The regret in the exploration phase during the -th episode is bounded by . Thus, our focus now shifts to analyzing the upper bound of the regret during the exploitation phase. By referring to equation (S21), we observe that the conditional expectation of regret at time in the exploitation phase can be bounded by . Consequently, our proof begins by deriving a bound for .

During the episode , for in the exploitation phase, we have

| (S34) | ||||

The first inequality is because of Lemma S5. The second equality follows Equation (6). Noting that in (S34) is exactly the same with that in (S22). Therefore, we only need to find a upper bound on .

Now, we analyze . By Lemma S6, we assume on the bounded interval for some constant . From (S34), we have

| (S35) | ||||

The last second inequality is due to Lemma S6. Now, we derive a upper bound of . Assume that is estimated from samples. We have

| (S36) |

The last inequality is due to by Lemma S5, and hence By (11), we have

| (S37) |

The last inequality is due to (S28) and (S36). Therefore,

| (S38) |

The last inequality is due to . Then, by (S35) and (S38), we have for

| (S39) | ||||

The second inequality is due to (S25) and (S38). The third inequality follows Lemma 1 and 2. By equations (S21), (S23), (S34) and (S39), for , the expected regret at time is

To simplify the above formula, we define

Therefore,

| (S40) |

Therefore, The total expected regret during the -th episode including the exploration phase and the exploitation phase is

We choose , which minimizes the upper bound of . Therefore,

Since the length of episodes grows exponentially, the number of episodes by period is logarithmic in . Specifically, belongs to episode . The total expected regret can be bounded by

Finally, we define two new constants,

The proof is completed.

S.4 Technical Lemmas

Lemma S5.

If is log-concave, the pricing function is 1-Lipschitz continuous.

Proof.

We write the virtual valuation function as where is the hazard function. Since is log-concave, the hazard function is increasing, , . Then,

| (S41) |

Since , we have By equation (S41), we obtain . Therefore, is 1-Lipschitz continuous. ∎

Lemma S6.

If is log-concave, the first derivative is locally Lipschitz continuous on .

Proof.

We next present a lemma from Koren and Levy (2015) as our supporting Lemma.

Lemma S7.

(Lemma 5, Koren and Levy (2015)) Let be two convex functions defined over a closed and convex domain , and let and . Assume that is locally -strongly-convex at with respect to a norm . Then, for , we have

where is a dual norm.