Perkins Embedding for General Starting Laws

Abstract.

The Skorokhod embedding problem (SEP) is to represent a given probability measure as a Brownian motion at a particular stopping time. In recent years particular attention has gone to solutions which exhibit additional optimality properties due to applications to martingale inequalities and robust pricing in mathematical finance.

Among these solutions, the Perkins embedding sticks out through its distinct geometric properties. Moreover is the only optimal solution to the SEP which so far has been limited to the case of Brownian motion started in a dirac distribution.

In this paper we provide for the first time an optimal solution to the Skorokhod embedding problem for the general SEP which leads to the Perkins solution when applied to Brownian motion with start in a dirac. This solution to the SEP also suggests a new geometric interpretation of the Perkins solution which better clarifies the relation to other optimal solutions of the SEP.

1. Introduction

Let be a probability measure on the real line with finite second moment and write for a Brownian motion started according to a probability measure , i.e. . The Skorokhod embedding problem ([33, 34]) is to find a stopping time such that the measure can be represented in the sense that

| (SEPλ,μ) |

Skorokhod [33, 34] gave a solution in the case where Brownian motion is started in an atom. A necessary and sufficient condition for the SEPλ,μ to admit a solution is for to be prior to in convex order, i.e. for any convex function . This follows by combining Skorokhod’s results with Strassen’s theorem [35] on the existence of martingales with given marginals. We will tacitly assume this condition throughout the paper. The condition is imposed to exclude trivial solutions.

Skorokhod’s work initiated an active field of research. Obłój’s survey [27] provides a comprehensive overview of the developments up to 2004 and describes more than 20 different solutions to the Skorokhod problem given by different authors.

During the 2000’s a particular stimulous for the field has come from the connection with robust finance which was discovered in Hobson’s seminal paper [21], see also [22]. In view of these applications, it is of particular importance to construct stopping times which optimize certain functionals subject to satisfying the embedding constraint. This question is known as the optimal Skorokhod embedding problem and has been considered extensively, see [9, 12, 11, 13, 14, 19, 28, 4, 5, 17, 10, 2, 16, 3, 15, 6] among others.

Perkins Embedding

In this article we focus on a particular solution to (SEPλ,μ) established by Perkins [29] for the deterministic start case where , i.e. . The Perkins embedding solves an optimal Skorokhod embedding problem: It has the characteristic optimality property of minimizing the law of the running maximum of the underlying Brownian motion while simultaneously maximizing the law of the running minimum among all solution to (SEPλ,μ). Here (and below) maximization / minimization of laws is understood with respect to first order stochastic dominance.

The Perkins embedding is of importance for robust pricing of barrier and lookback options, see [7, 21, 22]. While other solutions to the optimal Skorokhod embedding problem have been given in the case of a general starting distribution or admit direct extensions to this case, there is no known solution in the general starting case which extends the Perkins embedding.

In [23] Hobson and Pedersen propose a solution to (SEPλ,μ) allowing for a general starting law which minimizes the law of the running maximum. Remarkably, the Hobson-Pederson embedding bears some resemblance to the Azéma-Yor [1] embedding. As pointed out in [23], the Hobson-Pederson embedding does not maximize the running minimum in the case and specifically differs from the Perkins embedding also in this case. A further difference between the Hobson-Pederson embedding and the Perkins embedding, is that the latter does not require external randomization (unless , see Section 3.2).

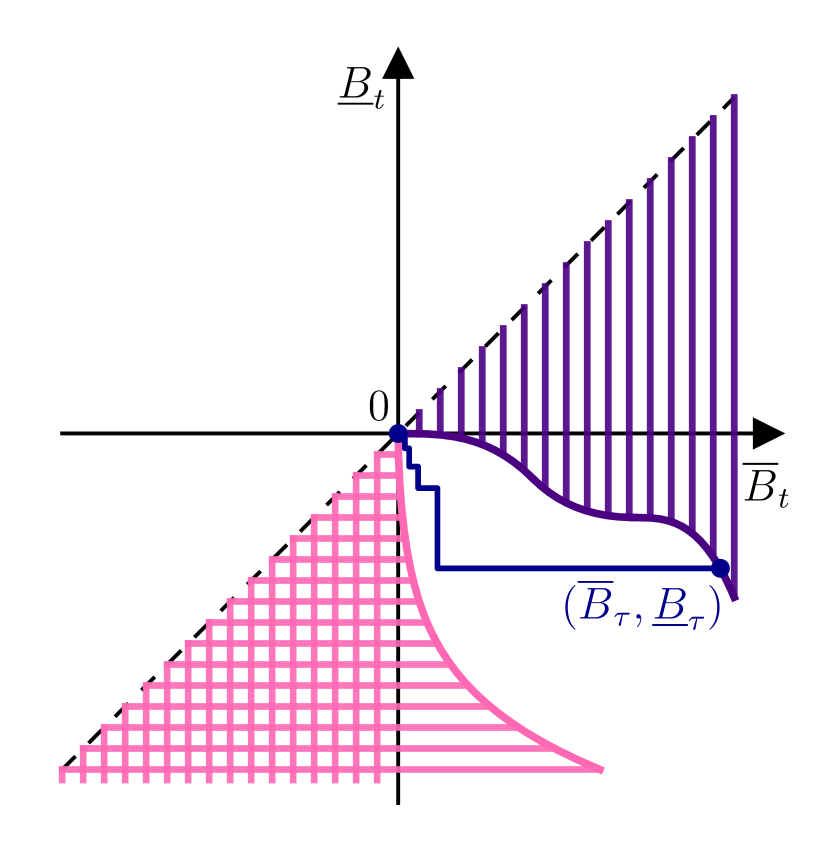

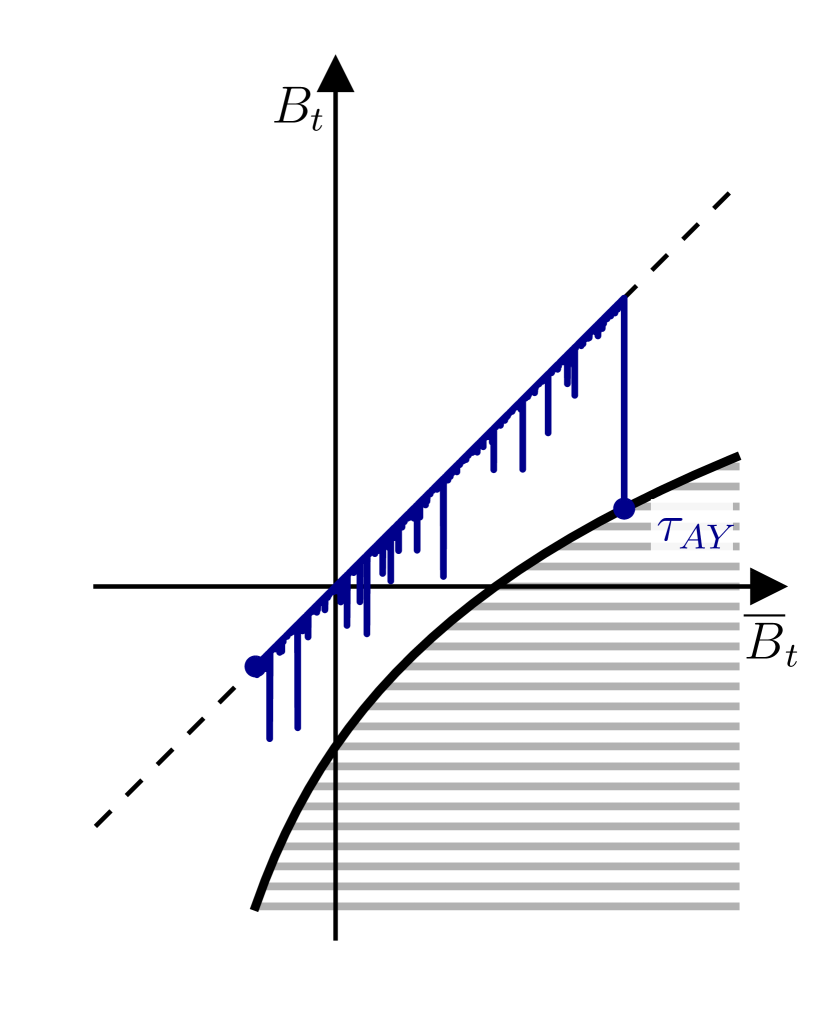

Of specific interest is the geometric structure of Perkins solution. In the case it can be identified as a hitting time of the process of a specifically structured target set , see Figure 1 (A). The set is a union of ‘lines’ of two types:

-

(v)

vertical lines which start below the diagonal and terminate in the diagonal. These lines will be depicted in ‘violett’.

-

(h)

lines which start on the right of the diagonal. They move horizontally until being reflected by the diagonal and continue to move vertically towards . These lines will be depicted in ‘hot pink’.

We will say that has vh-barrier structure. Note that traditionally the Perkins picture is drawn without the horizontal lines being reflected downwards. These downward lines are irrelevant in the deterministic starting case however become crucial when allowing for general starting as we will see below.

Our main contribution is to extend the Perkins solution to the case of general starting law. Specifically, setting we have:

Theorem 1.

There exists a vh-barrier such that the stopping time defined by for Borel and on by

| (1.1) |

is a solution to (SEPλ,μ). Moreover minimizes the law of the running maximum and further maximizes the law of the running minimum among all these solutions.

If and are mutually singular measures we have almost surely and is adapted to the filtration generated by the underlying Brownian motion.

The solution will be unique in the sense that if is another stopping time of the form (1.1) then we have almost surely.

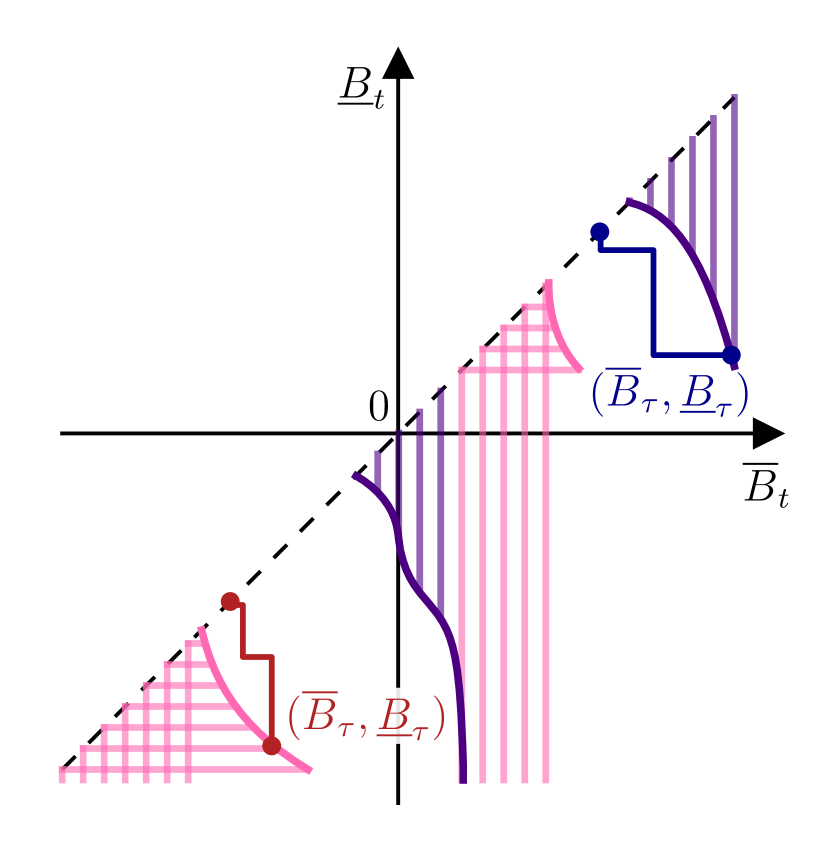

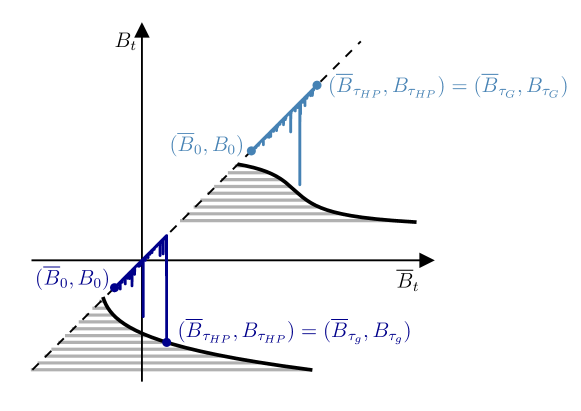

A possible realization of a general starting Perkins solution can be seen in Figure 1 (B). We point out two important properties of this solution. Firstly external randomization is only needed at time 0 and only if the two measure and share mass. This answers a question raised in [23, Remark 2.3] concerning the existence of adapted solutions in this setting. Secondly this solutions features the same representation as the hitting time of the process as the original Perkins solution and recovers it in the case as illustrated in Figure 1.

We will focus on discussing the Perkins solution from a barrier type solution viewpoint.

Barrier Type Solutions

A barrier type solution to (SEPλ,μ) is traditionally of the form

| (1.2) |

for a sufficiently regular processes and a Borel set featuring some additional barrier structure.

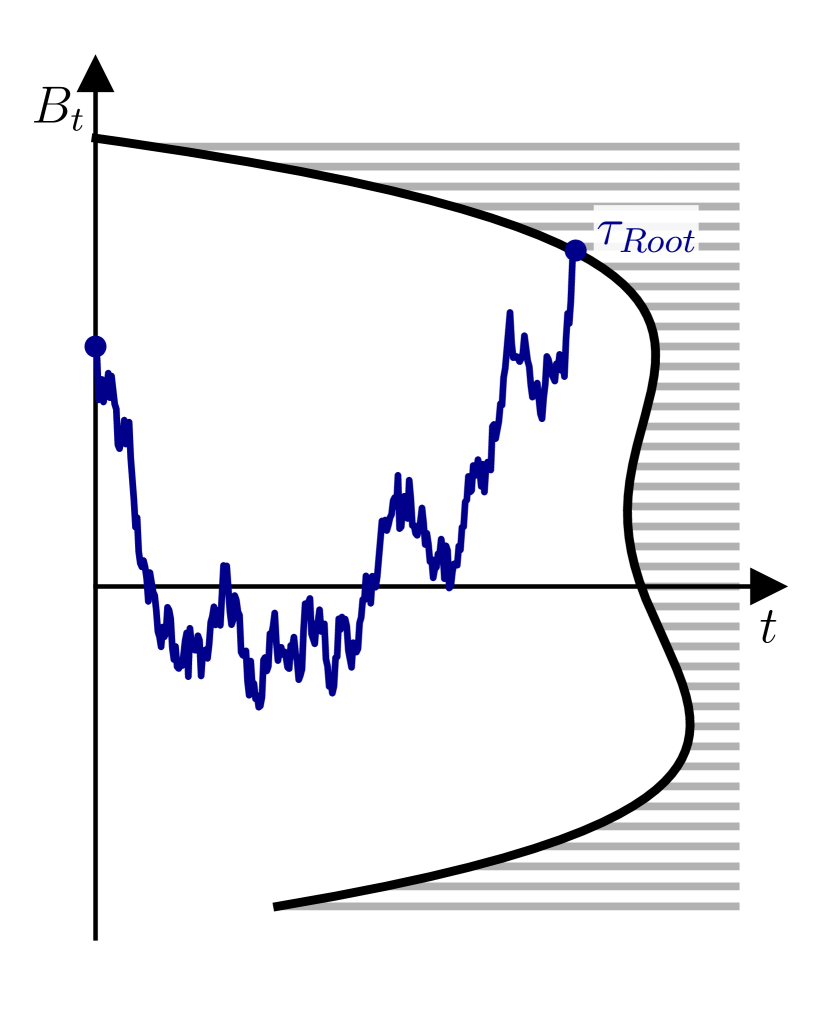

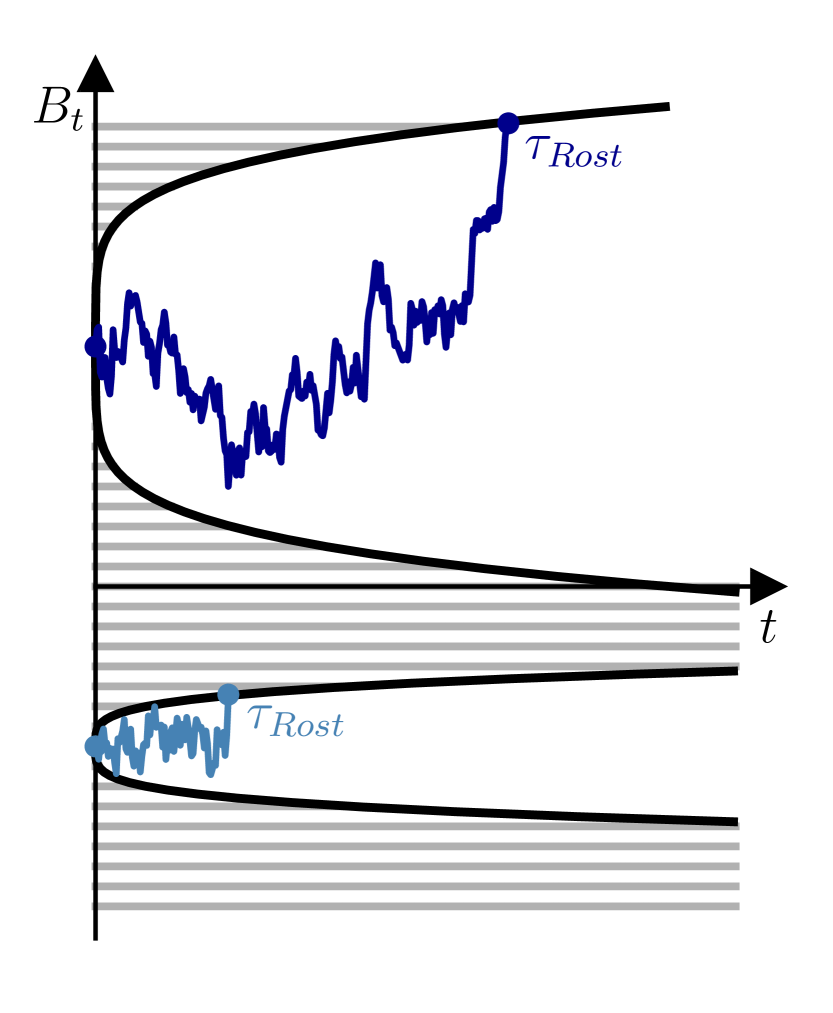

Barrier type solutions not only come with natural geometric interpretations, we also see that all these solution are adapted to the filtration of the underlying Brownian motion (apart from potential additional randomization at time if and share mass). Furthermore, barrier type solutions feature the following intrinsic uniqueness property highlighted by Loynes [26]: if is another barrier such that solves (SEPλ,μ) then we have almost surely. Prototypical barrier type solutions and also the solutions to originally coin the notion of a barrier resp. inverse barrier are the solutions by Root [30] and Rost [31, 32]. A (Root) barrier is a set such that implies for all while for an inverse barrier we require that implies for all . The Root resp. Rost solution is then given as the hitting time

and is known for minimizing resp. maximizing among all solutions to (SEPλ,μ) (see [25] and [32]). To be precise, in the Rost case, if the initial and the terminal law share mass, this shared mass might need to be stopped immediately, i.e.

Another barrier type solution to (SEPλ,μ) worth mentioning here is the Azéma-Yor solution [1] which is known for maximizing the law of the running maximum of the underlying Brownian motion. This solution is also given as the hitting time of a barrier in the Root sense, however of the joint process , thus

A general starting law version was found by Hobson in [20] and - as in the Root case - the barrier type representation of the solution did not change. See Figure 2 for examples of Root, Rost and Azéma-Yor barrier type solution.

As both the Perkins solution and the Hobson-Pedersen solution minimize the law of the running maximum of the underlying Brownian motion, they can be seen as a pendant to the Azéma-Yor embedding in a similar way as the Rost embedding can be seen as a pendant to the Root embedding.

Further barrier type solutions to (SEPλ,μ) are e.g. the Vallois embedding [36], the Jacka embedding [24] or the cave embedding [4]. We also refer to [4] for a unifying framework for barrier type solutions.

Notably it is not possible to find a process such that the Perkins solution can be represented as a barrier type solution in the classical sense (1.2), that is as a hitting time of the joint process . However, it is possible to identify it as a hitting time of the process of a vh-barrier as described above.

In [4] the authors use ideas and concepts of optimal mass transport to give existence results for solutions to (SEPλ,μ) featuring additional extremal properties and moreover provide techniques on how connections between these additional properties of the solutions and their geometric characterizations as barrier type solutions can be made. Minor variations of these techniques will allow us prove Theorem 1 and moreover to identify the right kind of phase space to interpret the Perkins embedding as the hitting time of a Rost inverse barrier, completing the Azéma-YorPerkins - RootRost analogy described earlier. Furthermore this representation will enable us to prove a Loynes-type uniqueness result for this solution.

Outline of the Article

In Section 2 we recall notation and results of [4] and extend them to a multifold optimization problem over solutions to (SEPλ,μ). These results will be applied in Section 3 to obtain existence of a Perkins embedding with general starting law as a solution to (SEPλ,μ) with the desired additional extremal properties. In Section 4 we discuss uniqueness of barrier type solutions and propose a setting in which these results can be applied to the Perkins embedding. This will conclude the proof of Theorem 1.

2. Multifold Optimal Skorokhod Embedding

For this article we will adopt the underlying assumptions of [4], that is, we will work on a stochastic basis which is rich enough to support a Brownian motion and a uniformly distributed -random variable independent of .

2.1. Optimal Skorokhod Embedding

The theory of finding solutions to the Skorokhod embedding problem featuring some optimality properties is presented from a systematic viewpoint in [4], see also [18]. Historically it was also common to find a new solution to (SEPλ,μ) and to only later establish its additional optimality property. In [4] this was turned around by imposing an optimization problem to the Skorokhod embedding problem and then to derive structural properties of the embedding problem from a ‘first order condition’.

For this we consider the set of stopped paths.

Definition 2.1 (stopped paths).

We define the set of stopped paths

The optimal Skorokhod embedding is formulated in the following way:

Definition 2.2 (optimal Skorokhod embedding problem).

For a function

the optimal Skorokhod embedding problem is to find a stopping time on solving the following optimization problem

We will always assume (OptSEPλ,μ) to be well posed in the sense that for all stopping times solving (SEPλ,μ), we have that exists, that and that there is at least one stopping time such that .

The solutions presented in the introduction can be recovered as solutions to the optimal Skorokhod embedding problem in the following way. The Root solution can be obtained by choosing , the Rost solution by and the Azéma-Yor solution by . Many more classic solutions to the Skorokhod embedding problem can be represented this way, see [4].

As pointed out in the introduction, the Perkins solution stands out due to its two fold optimality property. The optimal Skorokhod embedding problem as described above will not suffice to describe this special embedding. Also, in the construction of optimal solutions it is often useful to impose additional auxiliary optimality conditions in order to guarantee uniqueness of solutions. Thus we consider the following multifold optimal Skorokhod embedding problem.

Definition 2.3 (multifold optimal Skorokhod embedding problem).

Let and consider a function

Let be the set of all -stopping times on solving the following optimization problem

For define as the set of all stopping times that solve the optimization problem

We call the multifold optimal Skorokhod embedding problem.

The optimization problem is well posed if for all stopping times solving (SEPλ,μ), we have that exists, that and that there is at least one stopping time so that . We call well posed, if is well posed and for all the problem is well posed in the above sense (considering stopping times in ).

2.2. Randomized Stopping Times

The requirement of solutions to (SEPλ,μ) to be stopping times with respect to the filtration generated by Brownian motion is often too restrictive (as seen for the Hobson-Pedersen solution in the next section).

The key idea of linking the Skorokhod embedding problem to optimal transport is to think of a stopping time as a transport plan, mapping the mass of a trajectory in the space (where denotes the law of a Brownian motion started according to the distribution ) to the endpoint in . Even tough optimal transport theory cannot be applied directly, the appropriate analogues for this setup are developed in [4].

The necessary relaxation of this problem is to consider so called randomized stopping times which can be seen as stopping times in the usual sense but on a probability space that is possibly enlarged.

The idea of randomized stopping times is made precise by defining them as a subset of subprobability measures on , for details we refer to [4, Chapter 3.2].

Definition 2.4 (randomized stopping times).

A subprobability measure on is called a randomized stopping time (of Brownian motion with initial distribution ) if

-

(i)

.

-

(ii)

Given the disintegration of w.r.t. the first coordinate , is -measurable for all (Here denotes the natural augmented filtration on ).

For the probability measure on we define the subset which consists of those such that

-

(i)

,

-

(ii)

For all we have .

2.3. Existence of an Optimizer

One important result of [4] is to establish existence of optimizers under fairly general conditions. Even though the main proofs were carried out for (Theorem 4.1) and generalizations are provided for (Theorem 6.1), we can generalize in precisely the same way to arbitrary . Let us formulate the optimal Skorokhod embedding problem for randomized stopping times and then give the existence results for this generalized problem.

Definition 2.5 ((OptSEP)).

Let and consider a function

Let be the set of all randomized stopping times solving the following optimization problem

For define as the set of all stopping times wich solve the optimization problem

We define ):= .

Theorem 2 (Existence of a minimizer, cf. [4], Theorem 4.1).

Let be lsc and bounded from below in the following sense:

For all there exist constants such that

| (2.0) |

holds on .

Then admits a minmizer .

The following lemma provides equivalence between optimization over stopping times on our enlarged probability space and optimization over randomized stopping times.

Lemma 2.6 (cf. [4], Lemma 3.11).

Let be a -stopping time and consider the map

Then and for any measurable map we have

| () |

for the function

For any randomized stopping time we can find a -stopping time such that and holds.

2.4. Monotonicity Principle

In optimal transport theory it was an important development to be able to identify optimal transport plans by the geometry of its support - see c-cyclical monotonicity. A monotonicity principle (‘first order condition’) similar to -cyclical monotonicity for optimal Skorokhod embeddings is given in [4]. We define the support of a stopping time as a subset such that

Specific properties of this set will be crucial to our geometric approach to the Skorokhod embedding problem.

We will consider possible continuations of a given path and therefore define an operation of concatenation.

Definition 2.7 (concatenation of paths).

For two paths we define an operation of concatenation by

Definition 2.8 (going paths).

For any set of stopped paths we define the set of initial segments of this paths as

and call it the set of going paths.

In the multifold optimal Skorokhod embedding problem we consecutively optimize over functions of stopped paths. We will soon learn that it is interesting and useful to derive structural arguments about the sets of stopped paths satisfying these optimality conditions. In order to do this, we would like to have a strategy for dealing with different paths stopping at the same value. Among those paths we would like to identify those paths that should be stopped and those paths that should be allowed to continue - keeping in mind our optimization problem. This leads us to the notion of stop-go pairs, which by considering possible continuations of the paths gives a rule on how to decide on which one to stop and which one to allow to continue.

Definition 2.9 (Stop-Go Pair).

A pair of paths is called a stop-go pair with respect to (short: SG-pair) if

-

(i)

-

(ii)

in the lexicographic ordering of for every -stopping time such that , both sides are well defined and the left-hand side is finite in every component.

For the set of all SG-pairs we will write

and for we will call

the -th stop-go condition (SGCj).

We now want to identify sets of stopped paths, such that it is not advantageous to stop any of these paths earlier in comparison to the other paths in this set. In other words, the stopping rule cannot be improved within this set.

Definition 2.10 (-Monotonicity).

A set of stopped paths is called -monotone if

Theorem 3 (Monotonicity Principle).

Let be Borel measurable and let be a minimizer of . Then there exists a -monotone Borel set such that

Similar to the existence result also the monotonicity principle can be formulated for randomized stopping times. As these technicalities are not important for the rest of this paper we will refer the reader to [4] for further details.

We will see that the monotonicity principle is the key to the geometric approach to optimal Skorokhod embedding problems.

3. The Perkins Embedding

3.1. Perkins Embedding with Deterministic Starting

We will first give a precise formulation of the original Perkins solution in a barrier type formulation.

Finding a geometric interpretation of this solution in the case of is feasible with the methods established in [4], see Theorem 6.8 therein.

We will give the following slight reformulation of this theorem in order to stress our interest in the specific structure of the target set.

In addition to the barriers defined in the introduction we will furthermore consider an upwards barrier,

that is a set such that implies for all .

Theorem 4 (The Perkins embedding, cf. [29]).

Let and assume . Let be a bounded continuous function which is strictly increasing in both arguments. Then there exists a stopping time which minimizes

over all solution to (SEPλ,μ) and which is of the form

Here will be a vh-barrier which can be represented as with being an upwards barrier induced by (v)-lines and being an inverse barrier induced by (h)-lines. Moreover the boundaries of and are both given by decreasing functions (see Figure 1 A).

The solution will in fact coincide almost surely for each choice of the auxiliary function thus giving first order stochastic dominance.

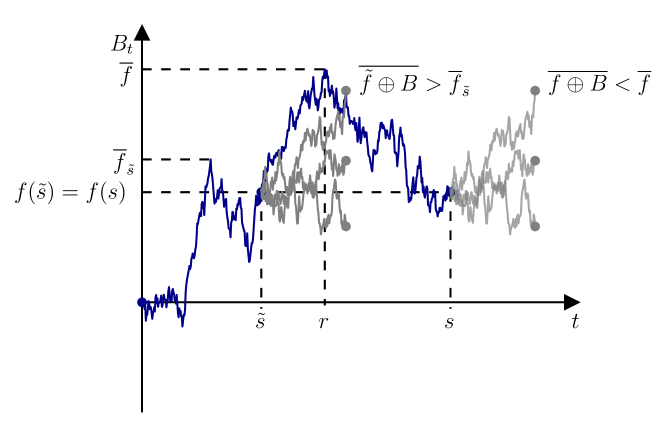

Unfortunately, some of the arguments in the proof of this theorem do not extend to the random starting case. Foremost it is no longer possible to optimize over the running minimum and the running maximum simultaneously. The stopping rule of Perkins’ problem will only stop paths when they reach a new running extremum. This justifies the representation of as a hitting time of the process . Note that since we do not allow to hold any mass in , we have and by properties of Brownian motion then a.s. These two facts imply that whenever we consider two paths stopped by this stopping rule at the same terminal value, either their running minima or their running maxima coincide. However, now it becomes very easy to decide on which one of those two paths to stop if we look at the other running extremum.

If we now allow for random starting we can also encounter (among other problems) the following situation: Two paths stop at the same value, that is , however - lets say - does so by reaching a new running minimum and by reaching a new running maximum. Then and . It is therefore no longer obvious, which of those two paths should be stopped and we can see that the solution can no longer be identified as the hitting time of a set serving both optimization problems simultaneously.

3.2. Perkins Embedding with Random Starting

The Hobson-Pedersen Solution

A first take on Perkins’ embedding with random starting is due to Hobson and Pedersen in [23]. We will give a brief sketch of their solution.

The authors define a function and a random variable which is independent of the randomly started Brownian motion . Both are explicitly determined by the measures and . They further define the two stopping times

where one should note the resemblance to the Azéma-Yor solution of the second stopping time. The solution to the Perkins problem with random starting is then given by

see Figure 3 for an illustration.

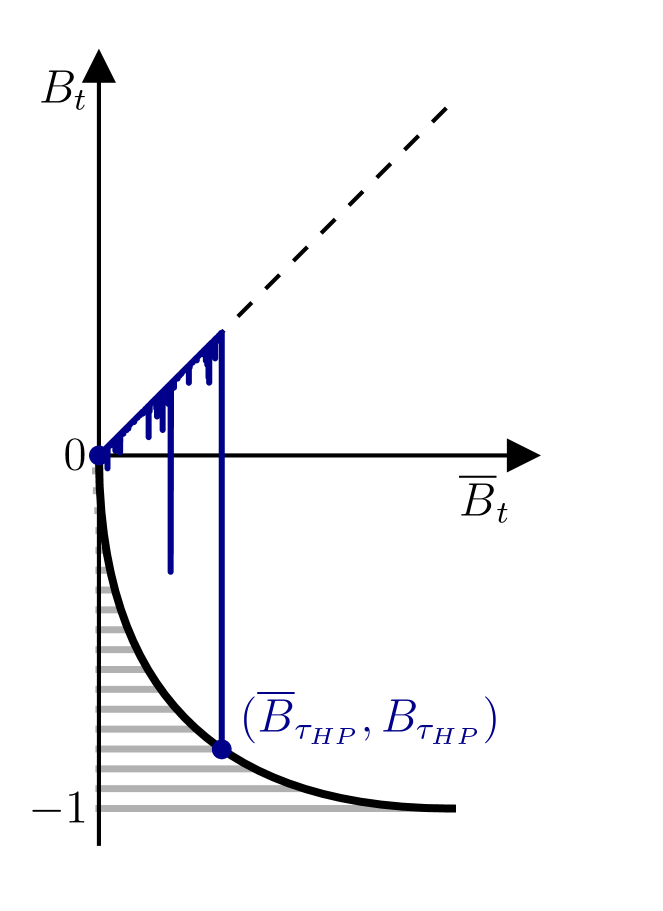

Due to this external randomization given via the random variable this solution is not adapted to the filtration of the underlying Brownian motion. Moreover this external randomization generally remains to be needed in the deterministic case of as seen in Figure 4. In particular, the original solution by Perkins is not a special case of the Hobson-Pedersen solution. The authors also discover that simultaneous optimization is no longer possible for general initial distributions and choose to prioritize minimizing the law of the running maximum.

Existence of a Perkins Embedding Allowing for a General Starting Law

By interpreting Perkins’ problem with general starting law as an (OptSEPλ,μ) for a well chosen as introduced in Section 2 we can use the methods and results therein to prove existence of a solution that is given as the hitting time of the process of a specifically structured target set.

It was explained above why we can no longer optimize simultaneously over the running minimum and the running maximum. We will therefore decide - as in the Hobson-Pederson solution presented above - that from now on the running maximum is more important to us. However, it should be obvious that all following results and calculations work analogously if our choice fell on the running minimum instead.

The following theorem provides a generalization of Perkins’ theorem in the slightly weaker formulation of optimization in expectation over an auxiliary function . While this is needed in order to apply the results of the previous section, the proof of Theorem 1 can be concluded in the next chapter by showing that all such solutions must coincide almost surely independently of the choice of . Thus our solution will optimize over all such which will conclude optimization in first order stochastic dominance.

We no longer exclude the possibility of and sharing mass. This leads to the situation of some randomization needed at time .

Theorem 5.

Let be a continuous bounded strictly increasing function. Then there exists a stopping time which minimizes over all solutions of and maximizes over all stopping times satisfying the former. For we have

and there exists a set such that on we have

Proof.

We will consider the function given by

Then all are bounded from below in the sense of (2.0) (due to the boundedness of ).

Thus Theorem 2 guarantees the existence of a minimizer which by Theorem 3 is supported by a -monotone Borel set .

The stop-go conditions amount to the following:

Let such that , then

| (SGC1) | ||||

| (SGC2) |

| (SGC3) | ||||

| (SGC4) |

Let us first consider . By standard properties of Brownian motion we then may assume that for we have .

To legitimate that on the stopping time is given as the hitting time of the process we will start by showing that will only stop Brownian motion when it is reaching a new running minimum or running maximum.

Consider a path which stops somewhere between its current running extrema, that is a path such that . Let be the time where hits its last new extremum. As does not reach a new extremum at time we can consider the initial segment of this path up to a time point such that and either or , where

Let , then we claim that .

1. Case: and as depicted in Figure 5, that is the last new extremum hit was a new maximum.

Assume , then and (SGC1) reads

and we see that in both cases a strict inequality holds due to our assumptions.

On the other hand, if , then as well as and this leads to an equality in (SGC1).

Since we also have an equality in (SGC2) and therefore jump to our third condition (SGC3):

Again, due to our assumptions , and as is strictly increasing, a strict inequality holds and thus .

2. Case: and , that is the last new extremum hit was a new minimum. Now (SGC1) as well as (SGC3) will always exhibit an equality and conditions (SGC2) and (SGC3) can be treated analogously to the previous case.

As now due to -monotonicity it follows that , that is, when stopped we will almost surely have reached a new running minimum or a new running maximum.

Summing up, we now know that stops paths of Brownian motion only when they reach a new running minimum or a new running maximum.

We will denote the set of stopped paths satisfying this condition by

This justifies to consider the phase space . All possible paths will lie below the diagonal, i.e. in the set .

We propose that there are two sets of points , such that , where

Let us legitimate this target set structure:

Assume we know that there is a path such that and , that is we stop at a new running maximum. We claim that it is impossible for a trajectory of the process to traverse the line-segment and then be stopped as seen in Figure 6 (A).

Consider a path such that , and . Then there has to exist a timepoint such that and note that still has to hold. However, this situation equals the 1. case of the above discussion, hence again . By -monotonicity it now follows that , therefore and our claim is proven.

It becomes clear that by choosing the definition of as above is reasonable.

Now assume we know that there is a path such that and , that is we stop at a new running minimum. We claim that it is impossible for a trajectory of the process to traverse either the or the line-segment and then be stopped as seen in Figure 6 (B).

Consider a path such that and . Let us first assume . Then again there has to exist a time point such that while . Again as in the 1. case above.

Now assume . It is then possible to find a timepoint such that and still . We remember that (SGC1) exhibits an equality if , which in our setting is equivalent to . If on the other hand , we will have a strict inequality. However as trivial stopping times are excluded, the later will always happen with positive probability and thus taking the expectation (SGC1) will always lead to a strict inequality, implying that .

This concludes the proof of .

Again, in analogy to the above let us take to justify the definition of .

Now define the following two target sets

and consider

Note that since is Borel, the sets and are analytic sets since they are continuous images of Borel sets. This implies that and are analytic sets and we see that and are stopping times.

We would like to show that a.s. as our claim then follows.

As it is obvious that a.s. by definition of .

To show that a.s. let us assume that this is not the case.

Choose

such that

and assume

.

Then there has to exist an such that for we have .

As it follows, that , that is is a going path.

By definition of we can find find a point such that or a point such that .

However, we then find ourselves in the same situation of traversing line-segments as above.

More precisely, by considering the path corresponding to this respectively point we again find a SG-pair contradicting the -monotonicity of .

Hence a.s.

By standard properties of Brownian motion now a.s. which concludes the proof in the case.

Let us now consider stopping in time .

Note that .

We want to show that a strict inequality stands in conflict with the -monotonicity.

If then there has to exists some such that there are paths in starting in but not immediately stopping and also paths which stop in at a strictly positive time.

By above discussion we see that this would constitute SG-pairs and we can conclude

∎

4. Uniqueness

In the previous section we have seen that the Perkins solution with random starting is given as a hitting time of the process of a specifically structured target set. As mentioned in the introduction it was proved by Loynes [26] that Root’s barrier type solution is essentially unique. In this chapter we will briefly discuss the extension of this argument to barrier type solutions of the form

for sufficiently regular processes .

We will then propose a setting in which the Perkins solution with random starting can also be seen as a barrier type solutions and show how the Loynes argument extends to this setting. This will enable us to conclude the proof of Theorem 1.

4.1. The Loynes Uniqueness Result

Root initially defined barriers as topologically closed subsets of . Loynes uniqueness argument relies on this fact by using that we are actually inside the barrier when we stop. A suitable generalization for our purposes would be to ask our process to be sufficiently regular such that is jointly Markov satisfying the Blumenthal-Getoor 0-1-law. Instead of topological closures we then consider fine closures with respect to the process .

The fine closure of a set with respect to a jointly Markov process will be denoted by and is defined as

By this definition follows a.s. and by Blumenthal-Getoor.

Moreover we also have and .

For details on fine closures refer to [8], see also the arguments in [4].

We see that taking fine closures does not alter the stopping properties and we will therefore assume without loss of generality that our barriers are always finely closed with respect to .

Proposition 4.1.

Let and be two barriers such that

are stopping times both generating the same law . Then also generates and the corresponding stopping time is given by

Proof.

Consider the set

and define

Note that as well as .

Now assume that .

By definition of and by the above discussion we have .

This means, and it is now impossible to have (otherwise would have stopped in ).

This implies that we cannot have and therefore .

As we have:

and altogether

It is now clear that the sets

and

are essentially disjoint and their union has full probability.

Therefore a.s.

That generates the same law is now obvious (due to decomposition into and ).

∎

Corollary 4.2.

If is a barrier type solution to the (SEPλ,μ), then is a.s. unique.

Proof.

For any solution to (SEPλ,μ) we have and thus . Now if is another solution to (SEPλ,μ) and , then , hence a.s. and we call such a solution minimal. Let be the barrier inducing the solution and let be a different solution induced by the barrier . By Proposition 4.1 we have that is also a solution to the (SEPλ,μ). Since trivially we have that due to the minimality observation before. Now analogously , hence a.s. concluding the proof of uniqueness. ∎

We see that this uniqueness result cannot immediately be applied to the solutions found in Theorem 5. However, an analogous uniqueness result holds in this setting. The target set constructed in the proof of Theorem 5 can be seen as an inverse barrier in the sense of Rost and the Loynes type uniqueness result can be extended to this setting.

4.2. Uniqueness of the Perkins Solution

To give a Loynes type uniqueness result for the Perkins embedding we need to identify the right space and setting to be able to consider vh-barriers as barriers in the classic sense. We aim to represent vh-barriers as inverse barriers in the Rost sense.

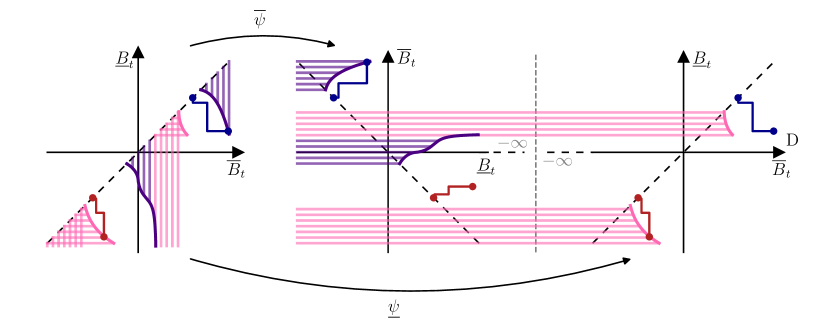

Let be a disjoint copy of the real numbers where the order is flipped, i.e. for we have if and only if in the usual order of the real numbers. We keep distinguishable from . Consider and define an order on in the following way.

This order enables us to depict the set as linearly ordered from left to right. Moreover we can consider as the left half of while considering as the right half of . To emphasize this we consider the map

which embeds into . Then

thus we may consider as reflected in the origin.

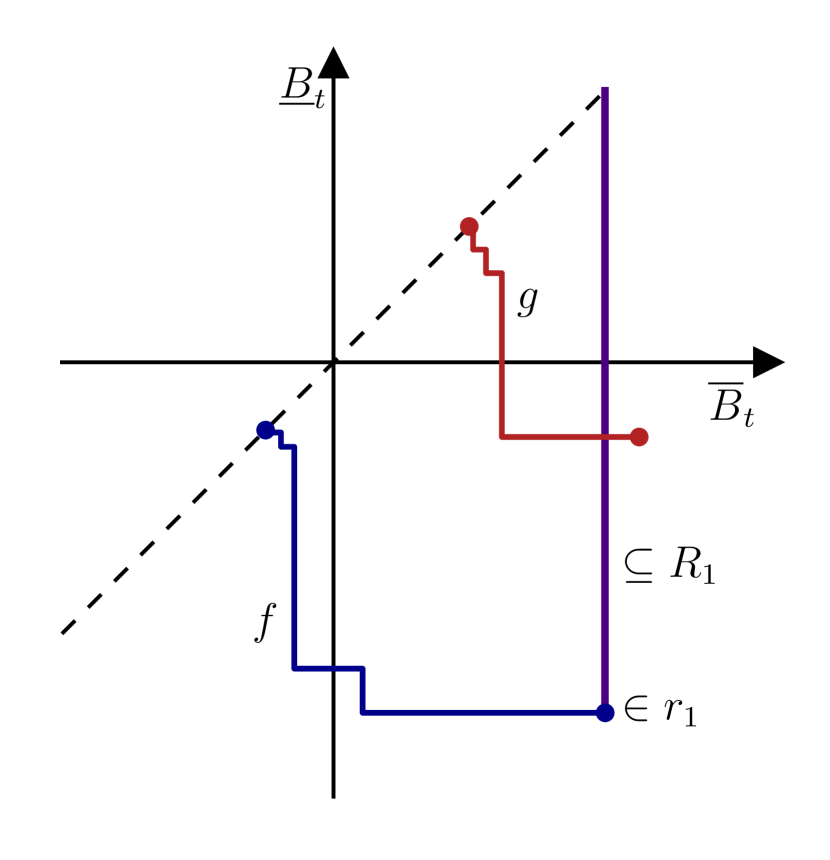

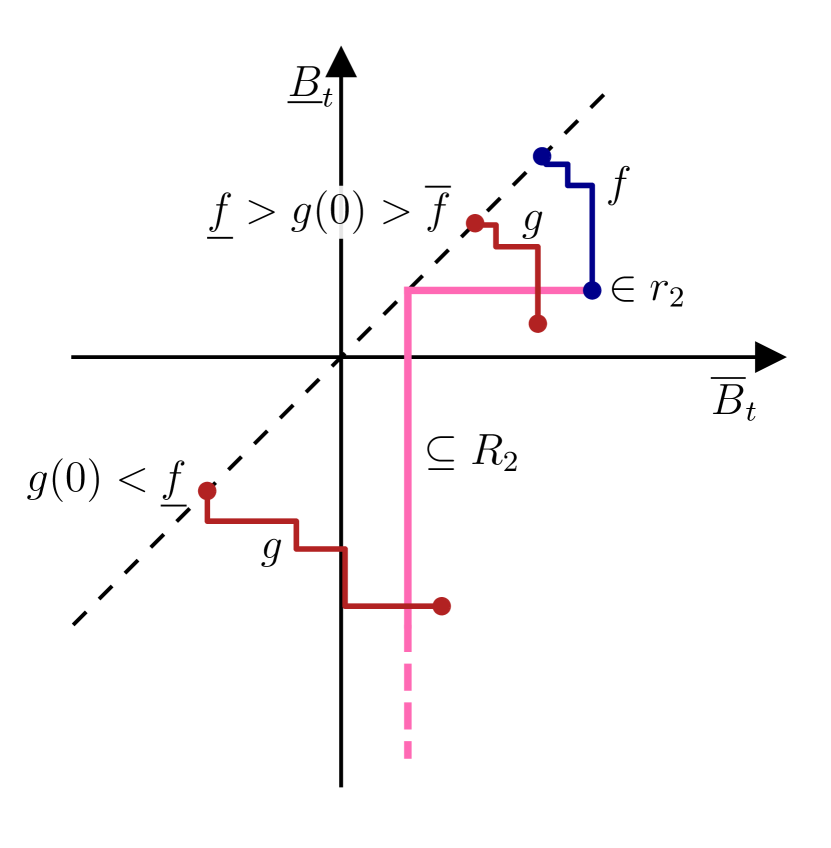

We will now construct barriers in . Note that in the proof of Theorem 5 the vh-barrier was established as where was induced by , the endpoints of paths being stopped at a new running maximum while was induced by , the endpoints of paths being stopped at a new running minimum. While is a barrier in we can also use and to define a corresponding barrier in the following way. For every we have and also for all such that . Note that as of course we have for all . Analogously for we have and also for all such that . Note that this especially implies for all .

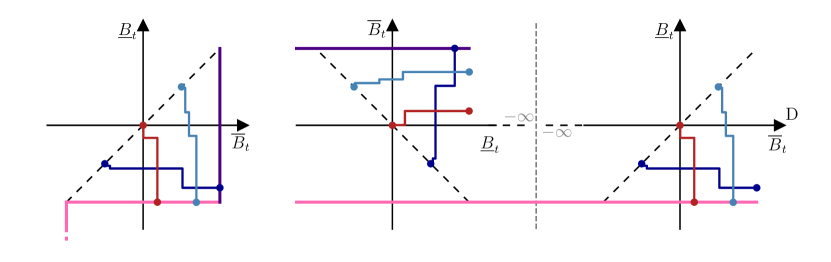

Thus every path stopped at a new running maximum creates a line in the left half of while every path stopped at new running minimum creates a line in the right half of which continues on into the left half creating a structure of Rost barrier type. Figure 7 gives an illustration of how the vh-barrier picture in Figure 1 (B) translates into a barrier in which will be of inverse barrier structure.

We want to consider the path in , more precisely we want to consider the path on the lhs as well as on the rhs of separately but simultaneously. So we define the following two maps embedding into the respective space.

While will plainly embed the path into the right half , the map will reflect the path along the main diagonal before embedding it into the left half . As we have ‘flipped’ the order on we will perceive the action of as a counter clockwise rotation by . Due to the order defined on these two paths will now both travel from left to right. In the left half the path will move vertically upwards whenever a new running maximum is reached and will move only horizontally when a new running minimum is reached. Furthermore this implies that the barrier can only be hit when a new running maximum is reached and no stopping will happen in the left hand side due to a new running minimum. In the right half the path will move vertically downwards whenever a new running minimum is reached but will travel perfectly horizontal at the level of the current running minimum when a new running maximum is reached. In other words, all stopping due to new running maxima will happen on the left hand side while all stopping due to new running minima will happen on the right hand side . We consider the respective stopping times of the embedded processes

Now if and are both induced by the same sets and found in Theorem 5, then

thus both representations of the hitting time of the barrier will be equivalent. We will assume to be finely closed with respect to as well as and give a Loynes type uniqueness argument for the stopping time .

Theorem 6.

Let be two vh-barriers and let resp. denote their hitting times by the process . If and both embed the same law , then a.s.

Proof.

Note that by the above discussion we must have inverse barriers corresponding to the vh-barriers resp. such that and . Analogously to Proposition 4.1 and Corollary 4.2 the almost sure equality will follow by defining a set of those levels where barrier is ‘longer’ than barrier and showing that

| (4.1) |

Considering the order on as well as the fact that respectively are both inverse barriers we define

Thus now we can consider the subset

and define and analogously. Then we have and .

Consider , then it is crucial to observe that our stopping times will only stop Brownian motion at a new running minimum or running maximum, hence by definition of the respective stopping times we will either have or , thus either

Assume . Then and by the definition of , hence and it is impossible to have as otherwise would have stopped in as well. We have the analogous result when , hence (4.1) is clear. We can conclude the proof analogously to the proof of Proposition 4.1 and Corollary 4.2. ∎

We can now complete the proof of Theorem 1.

Proof.

For an arbitrary choice of consider as found in Theorem 5. Let be another stopping time constructed as in Theorem 5 but for a different choice of .

First note that the behaviour in is independent of , hence for we have

Now note that on both stopping times are given as hitting times of vh-barriers and embed the same law , hence by Theorem 6 we have a.s. Since the choices for were arbitrary we must have optimality for any such , thus we can conclude that minimizes resp. maximizes resp. in law. ∎

4.3. An Example

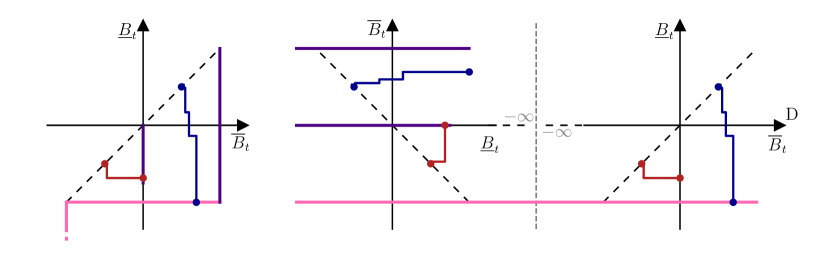

We will illustrate the occurrences of the different type of lines of the Perkins barrier solution in the following simple atomic example. Consider the initial measure

and for the terminal measure

Depending on the size of the atom in we have the following different cases.

-

:

The measure and share mass in , thus and all mass needed in will get stopped immediately while all other mass will be left to run to as illustrated in Figure 8.

-

:

Since we have . Hence all mass available in will be stopped immediately but then still a little more mass is needed. An additional v-line in where some of the paths starting in will stop upon reaching a new running maximum in will provide this missing mass as illustrated in Figure 9. Note that by adding this additional v-line we can at maximum acquire an additional of mass in , hence resulting in a maximal atom size of to be embedded this way.

-

:

As seen in the previous case we have and all mass available in will be stopped immediately. However as discussed above merely adding a v-line will no longer suffice to acquire the atom in . Hence we also need to stop (some) paths starting in upon reaching a new running minimum in via an h-line in as illustrated in Figure 10. Note that by adding this horizontal line we can at most acquire an additional of mass in from the paths started in , adding up to a total atom size of that could be embedded this way.

-

:

The measures fails to be prior to in the convex order when . While technically we could provide vh-barriers such that the corresponding hitting time would embed the measure , the resulting stopping time would no longer be integrable hence not be a solution to (SEPλ,μ).

References

- [1] J. Azéma and M. Yor. Une solution simple au problème de Skorokhod. In Séminaire de Probabilités, XIII (Univ. Strasbourg, Strasbourg, 1977/78), volume 721 of Lecture Notes in Math., pages 90–115. Springer, Berlin, 1979.

- [2] E. Bayraktar and T. Bernhardt. On the continuity of the root barrier. Proceedings of the American Mathematical Society, 150, 07 2022.

- [3] E. Bayraktar and X. Zhang. Embedding of walsh brownian motion. Stochastic Processes and their Applications, 134:1–28, 2021.

- [4] M. Beiglböck, A. Cox, and M. Huesmann. Optimal transport and Skorokhod embedding. Invent. Math., 208(2):327–400, 2017.

- [5] M. Beiglböck, A. M. G. Cox, and M. Huesmann. The geometry of multi-marginal Skorokhod Embedding. Probab. Theory Related Fields, 176(3-4):1045–1096, 2020.

- [6] M. Beiglböck, M. Nutz, and F. Stebegg. Fine properties of the optimal Skorokhod embedding problem. J. Eur. Math. Soc. (JEMS), 24(4):1389–1429, 2022.

- [7] H. Brown, D. Hobson, and L. C. G. Rogers. Robust hedging of barrier options. Math. Finance, 11(3):285–314, 2001.

- [8] K. L. Chung and J. B. Walsh. Markov Processes, Brownian Motion, and Time Symmetry. 249. Springer-Verlag New York, 2 edition, 2005.

- [9] A. M. G. Cox and D. Hobson. A unifying class of skorokhod embeddings: Connecting the azéma: Yor and vallois embeddings. Bernoulli, 13(1):114–130, 2007.

- [10] A. M. G. Cox, J. Obł ój, and N. Touzi. The Root solution to the multi-marginal embedding problem: an optimal stopping and time-reversal approach. Probab. Theory Related Fields, 173(1-2):211–259, 2019.

- [11] A. M. G. Cox and J. Wang. Optimal robust bounds for variance options. ArXiv e-prints, August 2013.

- [12] A. M. G. Cox and J. Wang. Root’s Barrier: Construction, Optimality and Applications to Variance Options. Ann. Appl. Probab., 23(3):859–894, 2013.

- [13] P. Gassiat, A. Mijatović, and H. Oberhauser. An integral equation for Root’s barrier and the generation of Brownian increments. Ann. Appl. Probab., 25(4):2039–2065, 2015.

- [14] P. Gassiat, H. Oberhauser, and G. dos Reis. Root’s barrier, viscosity solutions of obstacle problems and reflected FBSDEs. Stochastic Processes and their Applications, 125(12):4601–4631, 2015.

- [15] P. Gassiat, H. Oberhauser, and C. Z. Zou. A free boundary characterization of the root barrier for markov processes. Probability Theory and Related Fields, 180:33–69, 2021.

- [16] N. Ghoussoub, Y. Kim, and T. Lim. Optimal brownian stopping when the source and target are radially symmetric distributions. SIAM Journal on Control and Optimization, 58(5):2765–2789, 2020.

- [17] N. Ghoussoub, Y. Kim, and A. Z. Palmer. PDE methods for optimal Skorokhod embeddings. Calc. Var. Partial Differential Equations, 58(3):Paper No. 113, 31, 2019.

- [18] G. Guo, X. Tan, and N. Touzi. On the monotonicity principle of optimal skorokhod embedding problem. SIAM Journal on Control and Optimization, 54(5):2478–2489, 2016.

- [19] P. Henry-Labordère, J. Obłój, P. Spoida, and N. Touzi. The maximum maximum of a martingale with given marginals. Ann. Appl. Probab., 26(1):1–44, 2016.

- [20] D. Hobson. The maximum maximum of a martingale. In Séminaire de Probabilités, XXXII, volume 1686 of Lecture Notes in Math., pages 250–263. Springer, Berlin, 1998.

- [21] D. Hobson. Robust hedging of the lookback option. Finance and Stochastics, 2:329–347, 1998.

- [22] D. Hobson. The Skorokhod embedding problem and model-independent bounds for option prices. In Paris-Princeton Lectures on Mathematical Finance 2010, volume 2003 of Lecture Notes in Math., pages 267–318. Springer, Berlin, 2011.

- [23] D. Hobson and J.L. Pedersen. The minimum maximum of a continuous martingale with given initial and terminal laws. Ann. Probab., 30(2):978–999, 2002.

- [24] S. Jacka. Doob’s inequalities revisited: A maximal -embedding. Stochastic processes and their applications, 29(2):281–290, 1988.

- [25] J. Kiefer. Skorohod embedding of multivariate RV’s, and the sample DF. Z. Wahrscheinlichkeitstheorie und Verw. Gebiete, 24(1):1–35, 1972.

- [26] R. M. Loynes. Stopping times on Brownian motion: Some properties of Root’s construction. Z. Wahrscheinlichkeitstheorie und Verw. Gebiete, 16:211–218, 1970.

- [27] J. Obłój. The Skorokhod embedding problem and its offspring. Probab. Surv., 1:321–390, 2004.

- [28] J. Obłój and P. Spoida. An Iterated Azéma-Yor Type Embedding for Finitely Many Marginals. Ann. Probab., to appear, 2016.

- [29] E. Perkins. The Cereteli-Davis solution to the -embedding problem and an optimal embedding in Brownian motion. In Seminar on stochastic processes, 1985, pages 172–223. Springer, 1986.

- [30] D. H. Root. The existence of certain stopping times on Brownian motion. Ann. Math. Statist., 40:715–718, 1969.

- [31] H. Rost. The stopping distributions of a Markov Process. Invent. Math., 14:1–16, 1971.

- [32] H. Rost. Skorokhod stopping times of minimal variance. In Séminaire de Probabilités, X (Première partie, Univ. Strasbourg, Strasbourg, année universitaire 1974/1975), pages 194–208. Lecture Notes in Math., Vol. 511. Springer, Berlin, 1976.

- [33] A. V. Skorohod. Issledovaniya po teorii sluchainykh protsessov (Stokhasticheskie differentsialnye uravneniya i predelnye teoremy dlya protsessov Markova). Izdat. Kiev. Univ., Kiev, 1961.

- [34] A. V. Skorokhod. Studies in the theory of random processes. Translated from the Russian by Scripta Technica, Inc. Addison-Wesley Publishing Co., Inc., Reading, Mass., 1965.

- [35] V. Strassen. The existence of probability measures with given marginals. Ann. Math. Statist., 36:423–439, 1965.

- [36] P. Vallois. Le probleme de Skorokhod sur : une approche avec le temps local. In Séminaire de Probabilités XVII 1981/82, pages 227–239. Springer, 1983.