Conditional independence testing under

misspecified inductive biases

Abstract

Conditional independence (CI) testing is a fundamental and challenging task in modern statistics and machine learning. Many modern methods for CI testing rely on powerful supervised learning methods to learn regression functions or Bayes predictors as an intermediate step; we refer to this class of tests as regression-based tests. Although these methods are guaranteed to control Type-I error when the supervised learning methods accurately estimate the regression functions or Bayes predictors of interest, their behavior is less understood when they fail due to misspecified inductive biases; in other words, when the employed models are not flexible enough or when the training algorithm does not induce the desired predictors. Then, we study the performance of regression-based CI tests under misspecified inductive biases. Namely, we propose new approximations or upper bounds for the testing errors of three regression-based tests that depend on misspecification errors. Moreover, we introduce the Rao-Blackwellized Predictor Test (RBPT), a regression-based CI test robust against misspecified inductive biases. Finally, we conduct experiments with artificial and real data, showcasing the usefulness of our theory and methods.

1 Introduction

Conditional independence (CI) testing is fundamental in modern statistics and machine learning (ML). Its use has become widespread in several different areas, from (i) causal discovery [12, 24, 34, 11] and (ii) algorithmic fairness [28], to (iii) feature selection/importance [5, 37] and (iv) transfer learning [25]. Due to its growing relevance across different sub-fields of statistics and ML, new testing methods with different natures, from regression to simulation-based tests, are often introduced.

Regression-based CI tests, i.e., tests based on supervised learning methods, have become especially attractive in the past years due to (i) significant advances in supervised learning techniques, (ii) their suitability for high-dimensional problems, and (iii) their simplicity and easy application. However, regression-based tests usually depend on the assumption that we can accurately approximate the regression functions or Bayes predictors of interest, which is hardly true if (i) either the model classes are misspecified or if (ii) the training algorithms do not induce the desired predictors, i.e., if we have misspecified inductive biases. Misspecified inductive biases typically lead to inflated Type-I error rates but also can cause tests to be powerless. Even though these problems can frequently arise in practical situations, more attention should be given to theoretically understanding the effects of misspecification on CI hypothesis testing. Moreover, current regression-based methods are usually not designed to be robust against misspecification errors, making CI testing less reliable. In this work, we study the performance of three major regression-based conditional independence tests under misspecified inductive biases and propose the Rao-Blackwellized Predictor Test (RBPT), which is more robust against misspecification.

With more details, our main contributions are:

-

•

We present new robustness results for three relevant regression-based conditional independence tests: (i) Significance Test of Feature Relevance (STFR) [7], (ii) Generalized Covariance Measure (GCM) test [31], and (iii) REgression with Subsequent Independence Test (RESIT) [42, 24, 12]. Namely, we derive approximations or upper bounds for the testing errors that explicitly depend on the level of misspecification.

-

•

We introduce the Rao-Blackwellized Predictor Test (RBPT), a modification of the Significance Test of Feature Relevance (STFR) [7] test that is robust against misspecified inductive biases. In contrast with STFR and previous regression/simulation-based111Simulation-based tests usually rely on estimating conditional distributions. methods, the RBPT does not require models to be correctly specified to guarantee Type-I error control. We develop theoretical results about the RBPT, and experiments show that RBPT is robust when controlling Type-I error while maintaining non-trivial power.

2 Preliminaries

Conditional independence testing. Let be a random vector taking values in and be a fixed family of distributions on the measurable space , where is the Borel -algebra. Let and assume . If is the set of distributions in such that , the problem of conditional independence testing can be expressed in the following way:

In this work, we also write and . We assume throughout that we have access to a dataset independent and identically distributed (i.i.d.) as , where splits into a test set and a training set . For convenience, we use the training set to fit models and the test set to conduct hypothesis tests, even though other approaches are possible.

Misspecified inductive biases in modern statistics and machine learning. Traditionally, misspecified inductive biases in statistics have been linked to the concept of model misspecification and then strictly related to the chosen model classes. For instance, if the best (Bayes) predictor for given , , is a non-linear function of , but we use a linear function to predict , then we say our model is misspecified because is not in the class of linear functions. In modern machine learning and statistics, however, it is known that the training algorithm also plays a crucial role in determining the trained model. For example, it is known that training overparameterized neural networks using stochastic gradient descent bias the models towards functions with good generalization [14, 33]. In addition, D’Amour et al. [9] showed that varying hyperparameter values during training could result in significant differences in the patterns learned by the neural network. The researchers found, for instance, that models with different random initializations exhibit varying levels of out-of-distribution accuracy in predicting skin health conditions for different skin types, indicating that each model learned distinct features from the images. The sensitivity of the trained model concerning different training settings suggests that even models capable of universal approximation may not accurately estimate the target predictor if the training biases do not induce the functions we want to learn.

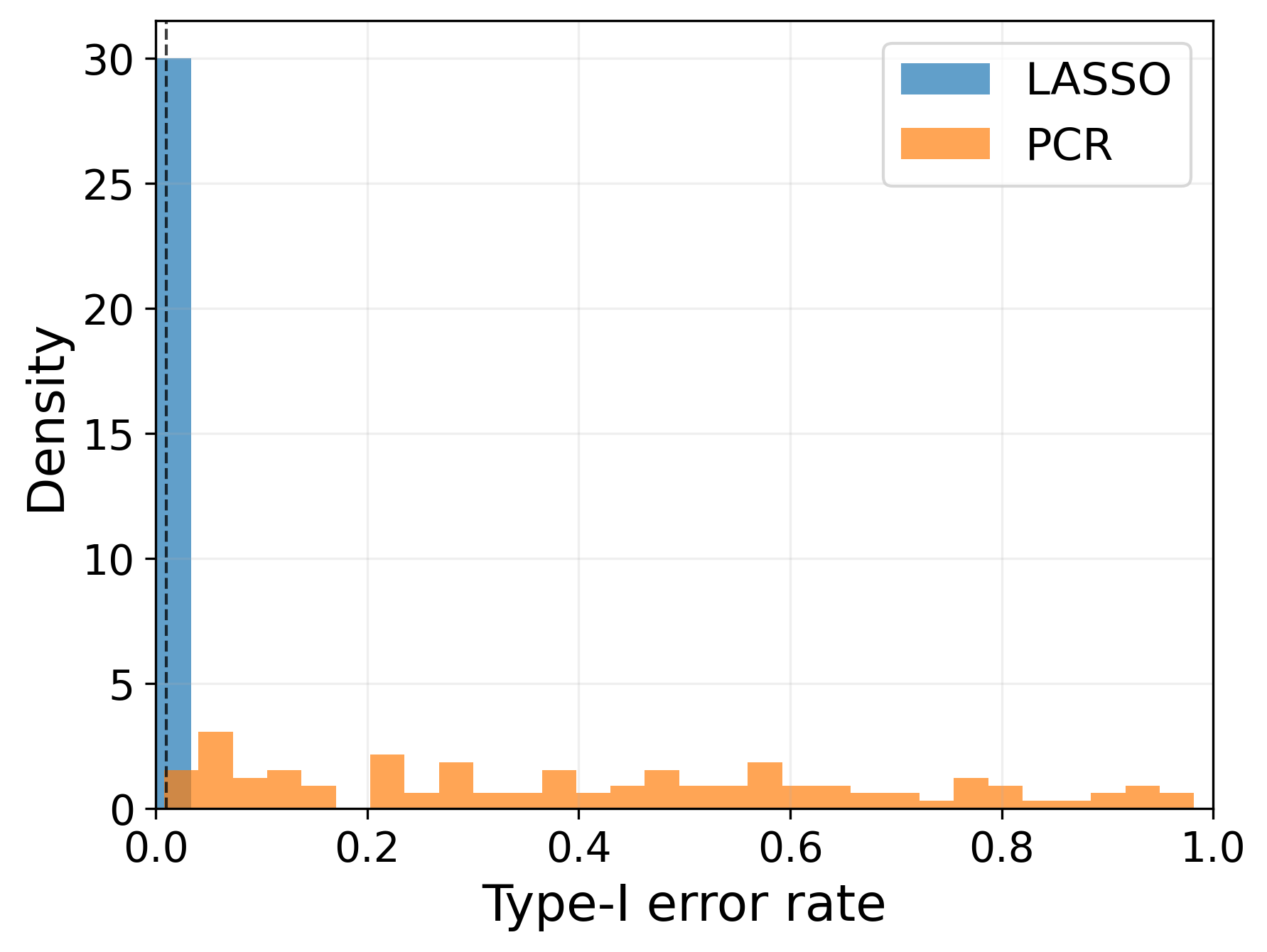

We present a toy experiment to empirically demonstrate how the training algorithm can prevent us from accurately estimating the target predictor even when the model class is correctly specified, leading to invalid significance tests. We work in the context of a high-dimensional (overparameterized) regression with a training set of observations and covariates. We use the Generalized Covariance Model (GCM) test222See Appendix A.3 for more details [31] to conduct the CI test. The data are generated as

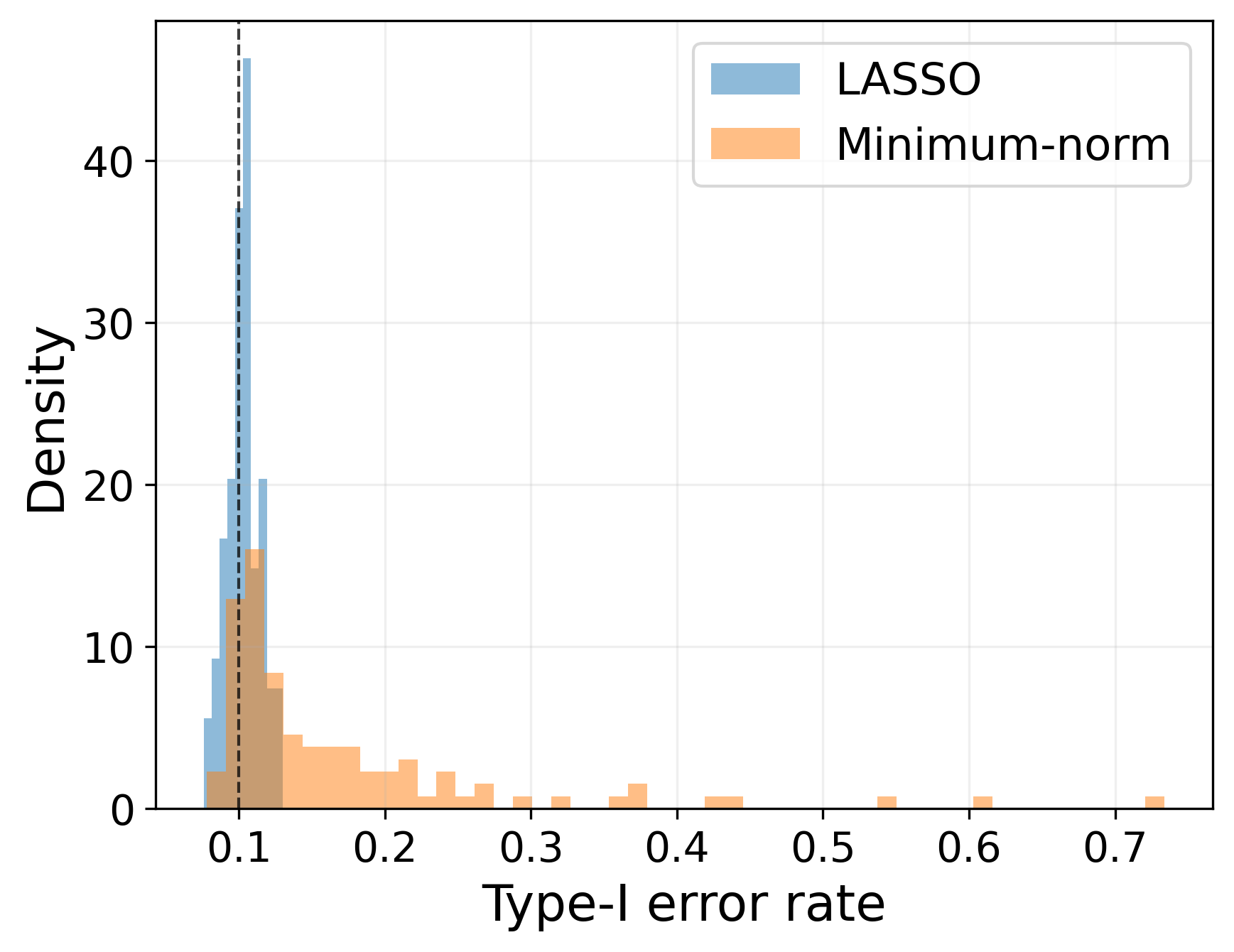

where the first five entries of are set to , and the remaining entries are zero, while the last five entries of are set to , and the remaining entries are zero. This results in and being conditionally independent given and depending on only through a small number of entries. Additionally, and , indicating that the linear model class is correctly specified. To perform the GCM test, we use LASSO ( penalization term added to empirical squared error) and the minimum-norm least-squares solution to fit linear models that predict and given . In this problem, the LASSO fitting approach provides the correct inductive bias since and are sparse.

We set the significance level to and estimate the Type-I error rate for different training sets. Figure 1 provides the Type-I error rate empirical distribution and illustrates that, despite using the same model class for both fitting methods, the training algorithm induces an undesired predictor in the minimum-norm case, implying an invalid test most of the time. On the other hand, the LASSO approach has better Type-I error control. In Appendix A, we give a similar example but using the Significance Test of Feature Relevance (STFR) [7].

In this work, we formalize the idea of misspecified inductive biases in the following way. Assume that a training algorithm is used to choose a model from the class . We further assume that the sequence converges to a limiting model in a relevant context-dependent sense. We use different notions of convergence depending on the specific problem under consideration, which will be clear in the following sections. We say that "carries misspecified inductive biases" if it does not equal the target Bayes predictor or regression function . There are two possible reasons for carrying misspecified biases: either the limiting model class is small and does not include , or the training algorithm cannot find the best possible predictor, even asymptotically.

Notation. We write and for the expectation and variance of statistics computed using i.i.d. copies of . Consequently, , where is the indicator of an event . If and are conditioned on some other statistics, we assume those statistics are also computed using i.i.d. samples from . As usual, is the distribution function. If and are sequences of scalars, then is equivalent to as and means . If is a sequence of random variables, where as constructed using i.i.d. samples of for each , then (i) means that for every we have as , (ii) means that for every there exists a such that , (iii) means , (iv) means , and (v) means . Finally, let be a family of random variables that distributions explicitly depend on and . We give an example to clarify what we mean by "explicitly" depending on a specific distribution. Let , where . Here, explicitly depends on because of the quantity . In this example, ’s outside the expectation can have an arbitrary distribution (unless stated), i.e., could be determined by or any other distribution. With this context, (i) means that for every we have as , (ii) means that for every there exists a such that , (iii) means , and (iv) means .

Related work. There is a growing literature on the problem of conditional independence testing regarding both theoretical and methodological aspects333See, for example, Marx and Vreeken [21], Shah and Peters [31], Li and Fan [19], Neykov et al. [23], Watson and Wright [37], Kim et al. [15], Shi et al. [32], Scetbon et al. [30], Tansey et al. [35], Zhang et al. [39], Ai et al. [1]. From the methodological point of view, there is a great variety of tests with different natures. Perhaps, the most important groups of tests are (i) simulation-based tests [5, 3, 4, 32, 35, 20], (ii) regression-based tests [40, 24, 42, 38, 31, 7], (iii) kernel-based tests [10, 8, 34, 30], and (iv) information-theoretic based tests [29, 16, 39]. Due to the advance of supervised and generative models in recent years, regression and simulation-based tests have become particularly appealing, especially when is not low-dimensional or discrete. A related but different line of research is constructing a lower confidence bound for conditional dependence of and given [41]. In that work, the authors propose a method that relies on computing the conditional expectation of a possibly misspecified regression model, which can be related to our method presented in Section 4. Despite the relationship between methods, their motivations, assumptions, and contexts are different.

Simulation-based tests depend on the fact that we can, implicitly or explicitly, approximate the conditional distributions or . Two relevant simulation-based methods are the conditional randomization and conditional permutation tests (CRT/CPT) [5, 3, 4, 35]. For these tests, Berrett et al. [4] presents robustness results showing that we can approximately control Type I error even if our estimates for the conditional distributions are not perfect and we are under a finite-sample regime. However, it is also clear from their results that CRT and CPT might not control Type I error asymptotically when models for conditional distributions are misspecified. On the other hand, regression-based tests work under the assumption that we can accurately approximate the conditional expectations and or other Bayes predictors, which is hardly true if the modeling and training inductive biases are misspecified. To the best of our knowledge, there are no published robustness results for regression-based CI tests like those presented by Berrett et al. [4]. We explore this literature gap.

3 Regression-based conditional independence tests under misspecified inductive biases

This section provides results for the Significance Test of Feature Relevance (STFR) [7]. Due to limited space, the results for the Generalized Covariance Measure (GCM) test [31] and the REgression with Subsequent Independence Test (RESIT) [42, 24, 12] are presented in Appendix A. From the results in Appendix A, one can easily derive a double robustness property for both GCM and RESIT, implying that not all models need to be correctly specified or trained with the correct inductive biases for Type-I error control.

3.1 Significance Test of Feature Relevance (STFR)

The STFR method studied by Dai et al. [7] offers a scalable approach for conducting conditional independence testing by comparing the performance of two predictors. To apply this method, we first train two predictors and on the training set to predict given and , respectively. We assume that candidates for are models in the same class as but replacing with null entries. Using samples from the test set , we conduct the test rejecting if the statistic exceeds , depending on the significance level . We define and as

| (3.1) |

with . Here, is a loss function, typically used during the training phase, and are small artificial random noises that do not let vanish with a growing training set, thus allowing the asymptotic distribution of to be standard normal under . If the -value is defined as , the test is equivalently given by

| (3.2) |

The rationale behind STFR is that if holds, then and should have similar performance in the test set. On the other hand, if does not hold, we expect to have significantly better performance, and then we would reject the null hypothesis. Said that, to control STFR’s Type-I error, it is necessary that the risk gap between and , , under vanishes as the training set size increases. Moreover, we need the risk gap to be positive for the test to have non-trivial power. These conditions can be met if the risk gap of and , the limiting models of and , is the same as the risk gap of the Bayes’ predictors

where the minimization is done over the set of all measurable functions444We assume and to be well-defined and unique.. However, the risk gap between and will typically not vanish if and are not the Bayes’ predictors even under . In general, we should expect to perform better than because the second predictor does not depend on . Furthermore, their risk gap can be non-positive even if performs better than . In Appendix A.2, we present two examples in which model misspecification plays an important role when conducting STFR. The examples show that Type-I error control and/or power can be compromised due to model misspecification.

To derive theoretical results, we adapt the assumptions from Dai et al. [7]:

Assumption 3.1.

There are functions , , and a constant such that

Assumption 3.2.

There exists a constant such that

Assumption 3.3.

For every , there exists a constant such that

Finally, we present the results for this section. We start with an extension of Theorem 2 presented by Dai et al. [7] in the case of misspecified inductive biases.

Theorem 3.4.

Theorem 3.4 demonstrates that the performance of STFR depends on the limiting models and . Specifically, if , then even if holds. In practice, we should expect because of how we set the class for . In contrast, we could have , and then , even if the gap between Bayes’ predictors is positive. See examples in Appendix A.2 for both scenarios. Next, we provide Corollary 3.6 to clarify the relationship between testing and misspecification errors. This corollary formalizes the intuition that controlling Type-I error is directly related to misspecification of , while minimizing Type-II error is directly related to misspecification of .

Definition 3.5.

For a distribution and a loss function , define the misspecification gaps:

The misspecification gaps defined in Definition 3.5 quantify the difference between the limiting predictors and and the Bayes predictors and , i.e., give a misspecification measure for and . Corollary 3.6 implies that the STFR controls Type-I error asymptotically if , and guarantees non-trivial power if the degree of misspecification of is not large compared to the performance difference of the Bayes predictors , that is, when .

Corollary 3.6 (Bounding testing errors).

Suppose we are under the conditions of Theorem 3.4.

(Type-I error) If holds, then

where denotes uniform convergence over all as .

(Type-II error) In general, we have

where denotes uniform convergence over all as and

4 A robust regression-based conditional independence test

This section introduces the Rao-Blackwellized Predictor Test (RBPT), a misspecification robust conditional independence test based on ideas from both regression and simulation-based CI tests. The RBPT assumes that we can implicitly or explicitly approximate the conditional distribution of and does not require inductive biases to be correctly specified. Because RBPT involves comparing the performance of two predictors and requires an approximation of the distribution of , we can directly compare it with the STFR [7] and the conditional randomization/permutation tests (CRT/CPT) [5, 4]. The RBPT can control Type-I error under relatively weaker assumptions compared to other tests, allowing some misspecified inductive biases.

The RBPT can be summarized as follows: (i) we train that predicts given using ; (ii) we obtain the Rao-Blackwellized predictor by smoothing , i.e.,

then (iii) compare its performance with ’s using the test set and a convex loss555The loss function needs to be convex with respect to its first entry () for all . Both the test set and training set sizes, and the loss function can be chosen using the heuristics introduced by Dai et al. [7]. function (not necessarily used to train ), and (iv) if the performance of is statistically better than ’s,

we reject . The procedure described here bears a resemblance to the Rao-Blackwellization of estimators. In classical statistics, the Rao-Blackwell theorem [17] states that by taking the conditional expectation of an estimator with respect to a sufficient statistic, we can obtain a better estimator if the loss function is convex. In our case, the variable can be seen as a "sufficient statistic" for under the assumption of conditional independence . If holds and the loss is convex in its first argument, we can show using Jensen’s inequality that the resulting model has a lower risk relative to the initial model , i.e., . Then, the risk gap in RBPT is non-positive under in contrast with STFR’s risk gap, which we should expect to be always non-negative given the definition of in that case. That fact negatively biases the RBPT test statistic, enabling better Type-I error control.

In practice, we cannot compute exactly because is usually unknown. Then, we use an approximation , which can be given explicitly, e.g., using probabilistic classifiers or conditional density estimators [13], or implicitly, e.g., using generative adversarial networks (GANs) [22, 3]. We assume that is obtained using the training set. The approximated is

where the integral can be solved numerically in case has a known probability mass function or Lebesgue density (e.g., via trapezoidal rule) or via Monte Carlo integration in case we can only sample from . Finally, for a fixed significance level , the test is given by Equation 3.2 where the -value is obtained via Algorithm 1.

Before presenting RBPT results, we introduce some assumptions. Let represent the limiting model for . The conditional distribution depends on the underlying distribution , but we omit additional subscripts for ease of notation. Assumption 4.1 defines the limiting models and fixes a convergence rate.

Assumption 4.1.

There is a function , a conditional distribution , and a constant s.t.

where denotes the total variation (TV) distance. Additionally, assume that both and are dominated by a common -finite measure which does not depend on or .

The common dominating measure in Assumption 4.1 could be, for example, the Lebesgue measure in . Next, Assumption 4.2 imposes additional constraints on the limiting model . Under that assumption, the limiting misspecification level must be uniformly bounded over all .

Assumption 4.2.

For all , the chi-square divergence

is a well-defined integrable random variable and .

Now, assume is chosen from a model class . Assumption 4.3 imposes constraints on the model classes and loss function .

Assumption 4.3.

Assume (i) , for some real and positive , uniformly for all , and (ii) that is a Lipschitz loss function (with respect to its first argument) for a certain , i.e., for any , we have that .

Assumption 4.3 is valid by construction since we choose and the loss function . That assumption is satisfied when, for example, (a) models in are uniformly bounded, (b) with , and (c) is a bounded subset of , i.e., in classification problems and most of the practical regression problems. The loss , with , is also convex with respect to its first entry and then a suitable loss for RBPT. It is important to emphasize that does not need to be the same loss function used during the training phase. For example, we could use in classification problems, where is a one-hot encoded class label and is a vector of predicted probabilities given by a model trained using the cross-entropy loss.

Theorem 4.4.

When holds and is a strictly convex loss function (w.r.t. its first entry), we have that , allowing666In practice, we do not need to be strictly convex for the Jensen’s gap to be positive. Assuming that depends on under is necessary, though. That condition is usually true when is not the Bayes predictor. some room for the "incorrectness" of . That is, from Theorem 4.4, as long as , i.e., if ’s incorrectness (measured by ) is not as big as Jensen’s gap , RBPT has asymptotic Type-I error control. Uniform asymptotic Type-I error control is possible if . This is a great improvement of previous work (e.g., STFR, GCM, RESIT, CRT, CPT) since there is no need for any model to converge to the ground truth if , which is a weaker condition. See however that a small reduces the room for incorrectness. In the extreme case, when is the Bayes predictor, and therefore does not depend on under , we need777In this case, Assumption 3.3 is not true. We need to include artificial noises in the definition of as it was done in STFR by Dai et al. [7] in case we have high confidence that models converge to the ground truth. almost surely. On the other hand, if is close to the Bayes predictor, RBPT has better power. That imposes an expected trade-off between Type-I error control and power. To make a comparison with Berrett et al. [4] ’s results in the case of CRT and CPT, we can express our remark in terms of the TV distance between and . It can be shown that if , then Type-I error control is guaranteed (see Appendix A.5). This contrasts with Berrett et al. [4] ’s results because is not needed.

We conclude this section with some relevant observations related to the RBPT.

On RBPT’s power. Like STFR, non-trivial power is guaranteed if the predictor is good enough. Indeed, the second part of Corollary 3.6 can be applied for an upper bound on RBPT’s Type-II error.

Semi-supervised learning. Let denote a label variable. Situations in which unlabeled samples are abundant while labeled samples are scarce happen in real applications of conditional independence testing [5, 4]. RBPT is well suited for those cases because the practitioner can use the abundant data to estimate flexibly. The semi-supervised learning scenario also applies to RBPT2, which we describe next.

Running RBPT when it is hard to estimate : the RBPT2. There might be situations in which it is hard to estimate the full conditional distribution . An alternative approach would be estimating the Rao-Blackwellized predictor directly using a second regressor. After training , we could use the training set, organizing it in pairs , to train a second predictor to predict given . That predictor could be trained to minimize the mean-squared error. The model should be more complex than , in the sense that we should hope that the first model performs better than the second under in predicting . Consequently, this approach is effective when unlabeled samples are abundant, and we can train using both unlabeled data and the given training set. After obtaining , the test is conducted normally. We name this version of RBPT as "RBPT2". We include a note on how to adapt Theorem 4.4 for RBPT2 in Appendix A.6.

5 Experiments

We empirically888Code in https://github.com/felipemaiapolo/cit. analyze RBPT/RBPT2 in the following experiments and compare them with relevant benchmarks, especially when the used models are misspecified. We assume and . The benchmarks encompass STFR [7], GCM [31], and RESIT [42], which represent regression-based CI tests. Furthermore, we examine the conditional randomization/permutation tests (CRT/CPT) [5, 4] that necessitate the estimation of .

|

|

Artificial data experiments. Our setup takes inspiration from Berrett et al. [4], and the data is generated as

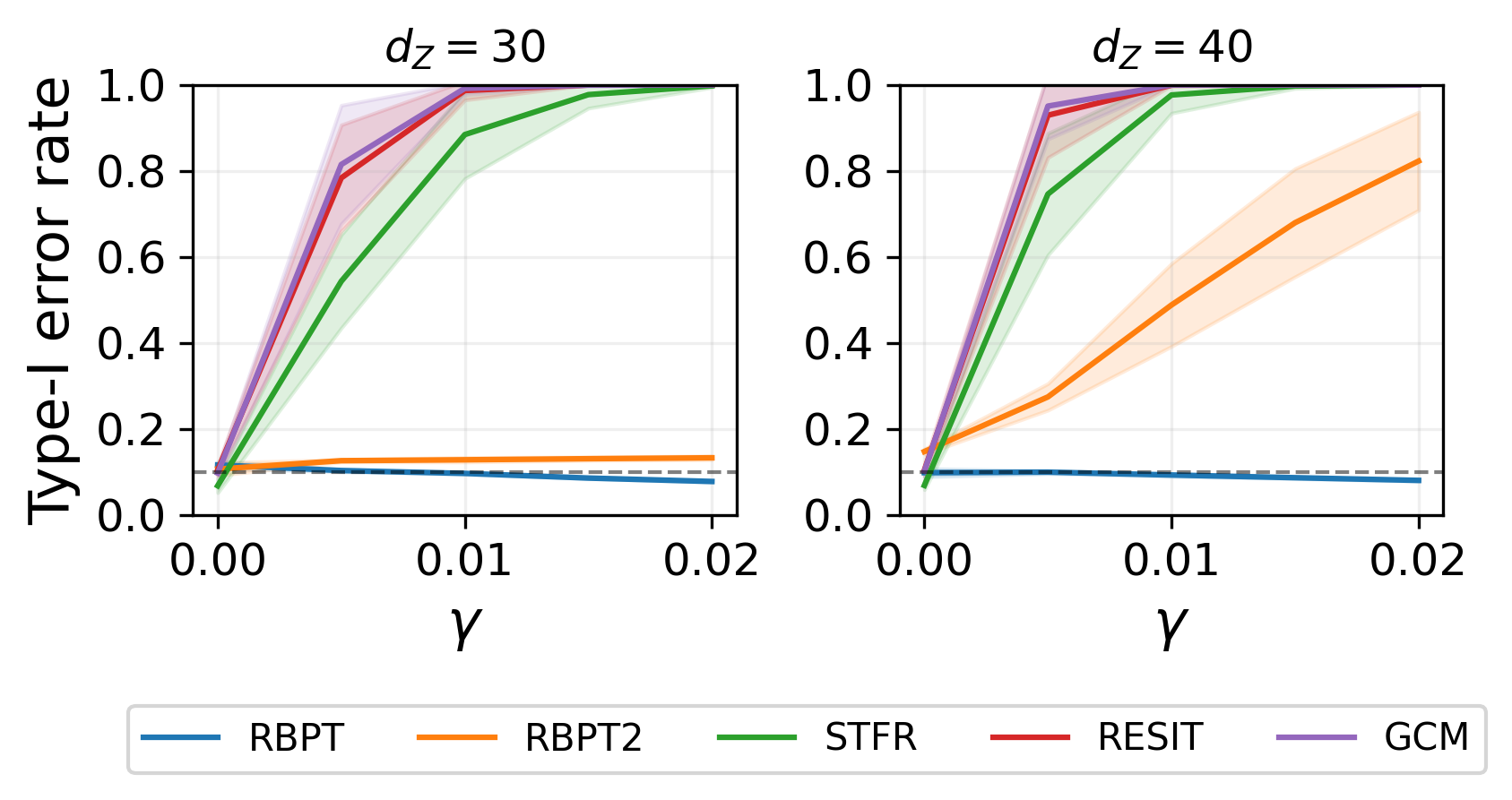

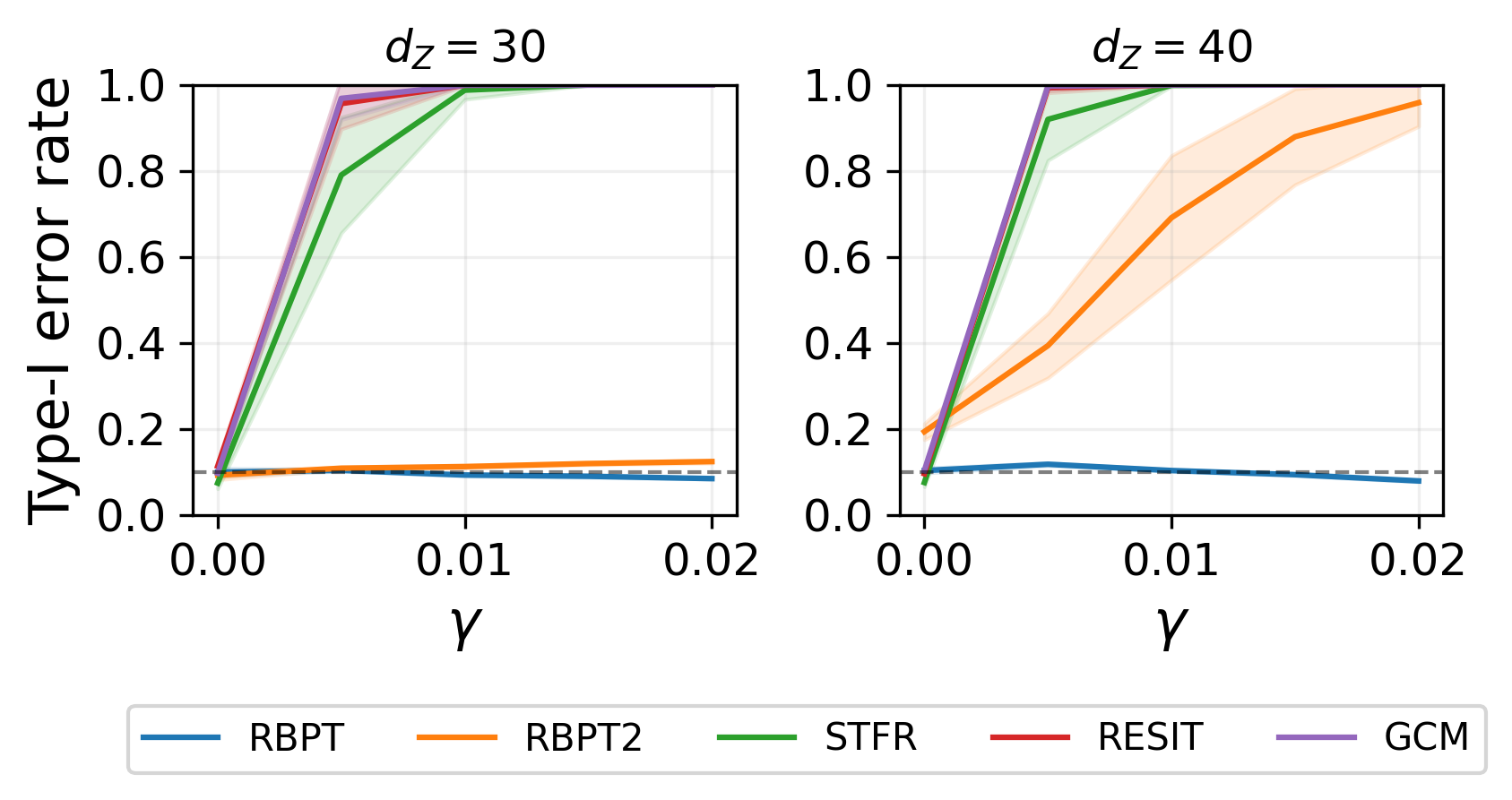

Here, denotes the dimensionality of , and are sampled from , the constant determines the conditional dependence of and on , and the parameter dictates the hardness of conditional independence testing: a non-zero implies potential challenges in Type-I error control as there might be a pronounced marginal dependence between and under . Moreover, the training (resp. test) dataset consists of 800 (resp. 200) entries, and every predictor we employ operates on linear regression. RESIT employs Spearman’s correlation between residuals as a test statistic while CRT and CPT999For CPT execution, the Python script at http://www.stat.uchicago.edu/~rina/cpt.html was used, operating a single MCMC chain and preserving all other parameters as defined by the original authors. deploy STFR’s test statistic, all of them with -values determined by conditional sampling/permutations executed 100 times (), considering . The value of gives the error level in approximating . To get in the two variations of RBPT, we either use (RBPT) or kernel ridge regression (KRR) equipped with a polynomial kernel to predict from (RBPT2). We sample generative parameters five times using different random seeds, and for each iteration, we conduct 480 Monte Carlo simulations to estimate Type-I error and power. The presented results are the average ( standard deviation) estimated Type-I error/power across iterations.

In Figure 2 (resp. 4) we compare our methods’ Type-I error rates (with ) (resp. power) against benchmarks. Regarding Figure 2, we focus on regression-based tests (STFR, GCM, and RESIT) in the first two plots and on simulation-based tests (CRT and CPT) in the last two plots. Regarding the first two plots, it is not straightforward to compare the level of misspecification between our methods and the benchmarks, so we use this as an opportunity to illustrate Theorem 4.4 and results from Section 3 and Appendix A. Fixing for RBPT, the Rao-Blackwellized predictor is perfectly obtained, permitting Type-I error control regardless of the chosen . Using KRR for RBPT2 makes close to when is not big and permits Type-I error control. When is big, more data is needed to fit , which can be accomplished using unlabeled data, as demonstrated in Figure 3 and commented in Section 4. On the other hand, Type-I error control is always violated for STFR, GCM, and RESIT when grows. Regarding the final two plots, we can more readily assess the robustness of the methods when discrepancies arise between and as influenced by varying . Figure 2 illustrates that CRT is the least robust test in this context, succeeded by RBPT and CPT.

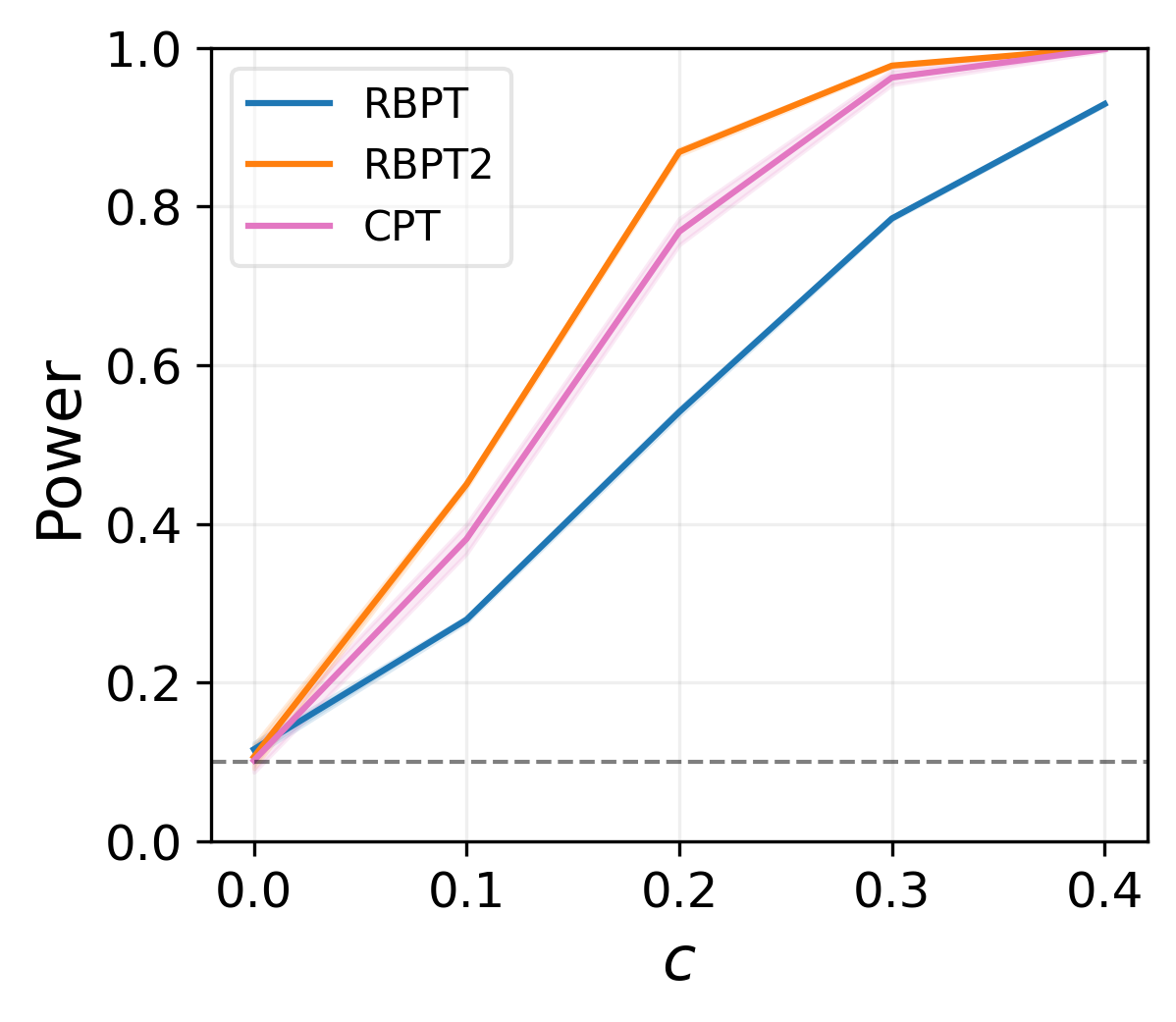

In Figure 4, we investigate how powerful RBPT and RBPT2 can be in practice when . We compare our methods with CPT (when ), which seems to have practical robustness against misspecified inductive biases. Figure 4 shows that RBPT2 and CPT have similar power while RBPT is slightly more conservative.

Some concluding remarks are needed. First, RBPT and RBPT2 have shown to be practical and robust alternatives to conditional independence testing, exhibiting reasonable Type-I error control, mainly when employed in conjunction with a large unlabeled dataset, and power. Second, while CPT demonstrates notable robustness and relatively good power, its practicality falls short compared to RBPT (or RBPT2). This is because CPT needs a known density functional form for (plus the execution of MCMC chains) whereas RBPT (resp. RBPT2) can rely on conventional Monte Carlo integration using samples from (resp. supervised learning).

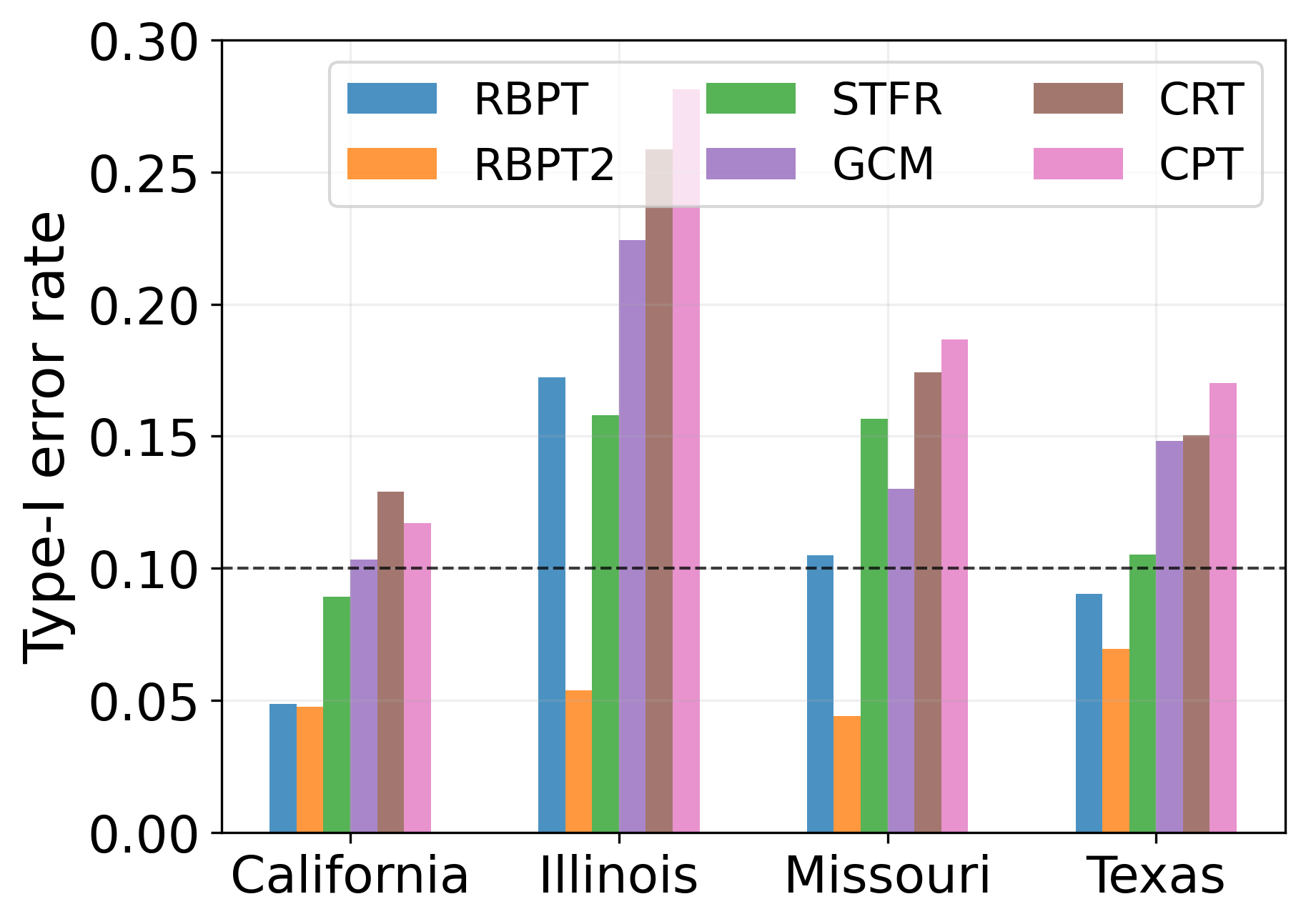

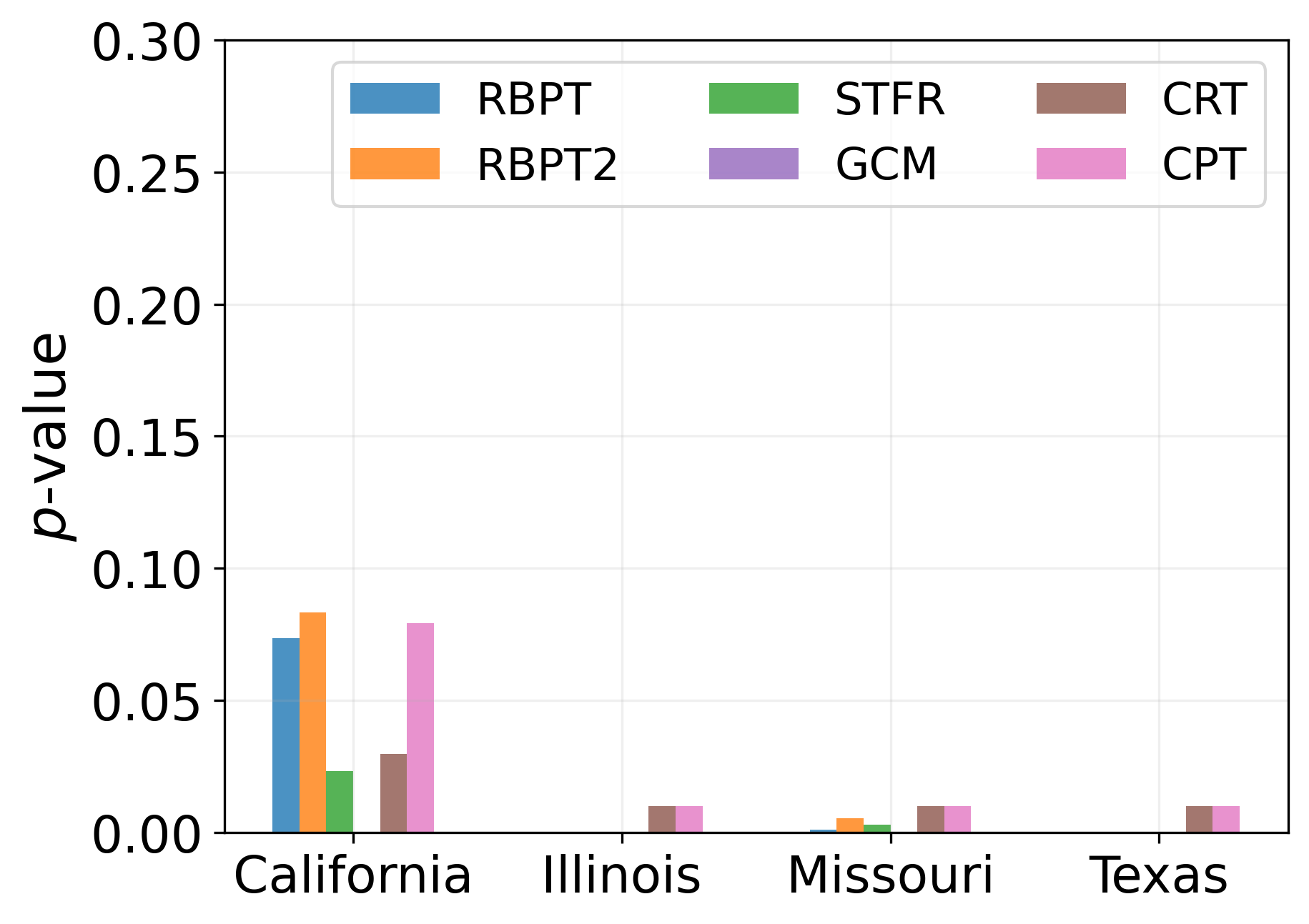

Real data experiments. For our subsequent experiments, we employ the car insurance dataset examined by Angwin et al. [2]. This dataset encompasses four US states (California, Illinois, Missouri, and Texas) and includes information from numerous insurance providers compiled at the ZIP code granularity. The data offers a risk metric and the insurance price levied on a hypothetical customer with consistent attributes from every ZIP code. ZIP codes are categorized as either minority or non-minority, contingent on the percentage of non-white residents. The variables in consideration are , denoting the driving risk; , an indicator for minority ZIP codes; and , signifying the insurance price. A pertinent question revolves around the validity of the null hypothesis , essentially questioning if demographic biases influence pricing.

We split our experiments into two parts. In the initial part, our primary goal is to compare the Type-I error rate across various tests. To ensure that is valid, we discretize into twenty distinct values and shuffle the values corresponding to each discrete value. If a test maintains Type-I error control, we expect it to reject for at most of the companies in each state. In the second part, we focus on assessing the power of our methods. Given our lack of ground truth, we qualitatively compare RBPT and RBPT2 findings with those obtained by baseline methods and delineated by Angwin et al. [2], utilizing a detailed and multifaceted approach. In this last experiment, we aggregate the analysis for each state without conditioning on the firm. We resort to logistic regression for estimating the distribution of used by RBPT, GCM, CRT, and CPT. For RBPT2, we use a CatBoost regressor [26] to yield the Rao-Blackwellized predictor. We omit RESIT in this experiment as the additive model assumption is inappropriate. Both CRT and CPT methods utilize the same test metrics as STFR. The first plot101010We run the experiment for 48 different random seeds and report the average Type-I error rate. of Figure 5 shows that RBPT and RBPT2 methods have better control over Type-I errors compared to all other methods, including CPT. The second plot reveals that all methods give the same qualitative result that discrimination against minorities in ZIP codes is most evident in Illinois, followed by Texas, Missouri, and California. These findings corroborate with those of Angwin et al. [2], indicating that our methodology has satisfactory power while maintaining a robust Type-I error control.

|

|

6 Conclusion

In this work, we theoretically and empirically showed that widely used regression-based conditional independence tests are sensitive to the specification of inductive biases. Furthermore, we introduced the Rao-Blackwellized Predictor Test (RBPT), a misspecification-robust conditional independence test. RBPT is theoretically grounded and has been shown to perform well in practical situations compared to benchmarks.

Limitations and future work. Two limitations of RBPT are that (i) the robustness of RBPT can lead to a more conservative test, as we have seen in the simulations; moreover, (ii) it requires the estimation of the conditional distribution , which can be challenging. To overcome the second problem, we introduced a variation of RBPT, named RBPT2, in which the Rao-Blackwellized predictor is obtained in a supervised fashion by fitting a second model that predicts the outputs of the first model . However, this solution only works if is better than in predicting under , which ultimately depends on the model class for and how that model is trained. Future research directions may include (i) theoretically studying the power of RBPT in more detail and (ii) better understanding RBPT2 from a theoretical or methodological point of view, e.g., answering questions on how to choose and train the second model.

7 Acknowledgements

This paper is based upon work supported by the National Science Foundation (NSF) under grants no. 1916271, 2027737, 2113373, and 2113364.

References

- Ai et al. [2022] Chunrong Ai, Li-Hsien Sun, Zheng Zhang, and Liping Zhu. Testing unconditional and conditional independence via mutual information. Journal of Econometrics, 2022.

- Angwin et al. [2017] Julia Angwin, Jeff Larson, Lauren Kirchner, and Surya Mattu. Minority neighborhoods pay higher car insurance premiums than white areas with the same risk, April 2017. URL https://www.propublica.org/article/minority-neighborhoods-higher-car-insurance-premiums-white-areas-same-risk. [Online; last accessed in 09-September-2022].

- Bellot and van der Schaar [2019] Alexis Bellot and Mihaela van der Schaar. Conditional independence testing using generative adversarial networks. Advances in Neural Information Processing Systems, 32, 2019.

- Berrett et al. [2020] Thomas B Berrett, Yi Wang, Rina Foygel Barber, and Richard J Samworth. The conditional permutation test for independence while controlling for confounders. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 82(1):175–197, 2020.

- Candes et al. [2018] Emmanuel Candes, Yingying Fan, Lucas Janson, and Jinchi Lv. Panning for gold:‘model-x’knockoffs for high dimensional controlled variable selection. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 80(3):551–577, 2018.

- Cappé et al. [2009] Olivier Cappé, Eric Moulines, and Tobias Rydén. Inference in hidden markov models. In Proceedings of EUSFLAT conference, pages 14–16, 2009.

- Dai et al. [2022] Ben Dai, Xiaotong Shen, and Wei Pan. Significance tests of feature relevance for a black-box learner. IEEE Transactions on Neural Networks and Learning Systems, 2022.

- Doran et al. [2014] Gary Doran, Krikamol Muandet, Kun Zhang, and Bernhard Schölkopf. A permutation-based kernel conditional independence test. In UAI, pages 132–141, 2014.

- D’Amour et al. [2020] Alexander D’Amour, Katherine Heller, Dan Moldovan, Ben Adlam, Babak Alipanahi, Alex Beutel, Christina Chen, Jonathan Deaton, Jacob Eisenstein, Matthew D Hoffman, et al. Underspecification presents challenges for credibility in modern machine learning. Journal of Machine Learning Research, 2020.

- Fukumizu et al. [2007] Kenji Fukumizu, Arthur Gretton, Xiaohai Sun, and Bernhard Schölkopf. Kernel measures of conditional dependence. Advances in neural information processing systems, 20, 2007.

- Glymour et al. [2019] Clark Glymour, Kun Zhang, and Peter Spirtes. Review of causal discovery methods based on graphical models. Frontiers in genetics, 10:524, 2019.

- Hoyer et al. [2008] Patrik Hoyer, Dominik Janzing, Joris M Mooij, Jonas Peters, and Bernhard Schölkopf. Nonlinear causal discovery with additive noise models. Advances in neural information processing systems, 21, 2008.

- Izbicki and B. Lee [2017] Rafael Izbicki and Ann B. Lee. Converting high-dimensional regression to high-dimensional conditional density estimation. 2017.

- Kalimeris et al. [2019] Dimitris Kalimeris, Gal Kaplun, Preetum Nakkiran, Benjamin Edelman, Tristan Yang, Boaz Barak, and Haofeng Zhang. Sgd on neural networks learns functions of increasing complexity. Advances in neural information processing systems, 32, 2019.

- Kim et al. [2021] Ilmun Kim, Matey Neykov, Sivaraman Balakrishnan, and Larry Wasserman. Local permutation tests for conditional independence. arXiv preprint arXiv:2112.11666, 2021.

- Kubkowski et al. [2021] Mariusz Kubkowski, Jan Mielniczuk, and Pawel Teisseyre. How to gain on power: Novel conditional independence tests based on short expansion of conditional mutual information. J. Mach. Learn. Res., 22:62–1, 2021.

- Lehmann and Casella [2006] Erich L Lehmann and George Casella. Theory of point estimation. Springer Science & Business Media, 2006.

- Lehmann et al. [2005] Erich Leo Lehmann, Joseph P Romano, and George Casella. Testing statistical hypotheses, volume 3. Springer, 2005.

- Li and Fan [2020] Chun Li and Xiaodan Fan. On nonparametric conditional independence tests for continuous variables. Wiley Interdisciplinary Reviews: Computational Statistics, 12(3):e1489, 2020.

- Liu et al. [2022] Molei Liu, Eugene Katsevich, Lucas Janson, and Aaditya Ramdas. Fast and powerful conditional randomization testing via distillation. Biometrika, 109(2):277–293, 2022.

- Marx and Vreeken [2019] Alexander Marx and Jilles Vreeken. Testing conditional independence on discrete data using stochastic complexity. In The 22nd International Conference on Artificial Intelligence and Statistics, pages 496–505. PMLR, 2019.

- Mirza and Osindero [2014] Mehdi Mirza and Simon Osindero. Conditional generative adversarial nets. arXiv preprint arXiv:1411.1784, 2014.

- Neykov et al. [2021] Matey Neykov, Sivaraman Balakrishnan, and Larry Wasserman. Minimax optimal conditional independence testing. The Annals of Statistics, 49(4):2151–2177, 2021.

- Peters et al. [2014] Jonas Peters, Joris M Mooij, Dominik Janzing, and Bernhard Schölkopf. Causal discovery with continuous additive noise models. Journal of Machine Learning Research, 15:2009–2053, 2014.

- Polo et al. [2023] Felipe Maia Polo, Rafael Izbicki, Evanildo Gomes Lacerda Jr, Juan Pablo Ibieta-Jimenez, and Renato Vicente. A unified framework for dataset shift diagnostics. Information Sciences, 649:119612, 2023.

- Prokhorenkova et al. [2018] Liudmila Prokhorenkova, Gleb Gusev, Aleksandr Vorobev, Anna Veronika Dorogush, and Andrey Gulin. Catboost: unbiased boosting with categorical features. Advances in neural information processing systems, 31, 2018.

- Resnick [2019] Sidney Resnick. A probability path. Springer, 2019.

- Ritov et al. [2017] Ya’acov Ritov, Yuekai Sun, and Ruofei Zhao. On conditional parity as a notion of non-discrimination in machine learning. arXiv preprint arXiv:1706.08519, 2017.

- Runge [2018] Jakob Runge. Conditional independence testing based on a nearest-neighbor estimator of conditional mutual information. In International Conference on Artificial Intelligence and Statistics, pages 938–947. PMLR, 2018.

- Scetbon et al. [2021] Meyer Scetbon, Laurent Meunier, and Yaniv Romano. An asymptotic test for conditional independence using analytic kernel embeddings. arXiv preprint arXiv:2110.14868, 2021.

- Shah and Peters [2020] Rajen D Shah and Jonas Peters. The hardness of conditional independence testing and the generalised covariance measure. The Annals of Statistics, 48(3):1514–1538, 2020.

- Shi et al. [2021] Chengchun Shi, Tianlin Xu, Wicher Bergsma, and Lexin Li. Double generative adversarial networks for conditional independence testing. J. Mach. Learn. Res., 22:285–1, 2021.

- Smith et al. [2020] Samuel Smith, Erich Elsen, and Soham De. On the generalization benefit of noise in stochastic gradient descent. In International Conference on Machine Learning, pages 9058–9067. PMLR, 2020.

- Strobl et al. [2019] Eric V Strobl, Kun Zhang, and Shyam Visweswaran. Approximate kernel-based conditional independence tests for fast non-parametric causal discovery. Journal of Causal Inference, 7(1), 2019.

- Tansey et al. [2022] Wesley Tansey, Victor Veitch, Haoran Zhang, Raul Rabadan, and David M Blei. The holdout randomization test for feature selection in black box models. Journal of Computational and Graphical Statistics, 31(1):151–162, 2022.

- Tsybakov [2004] Alexandre B Tsybakov. Introduction to nonparametric estimation, 2009. URL https://doi.org/10.1007/b13794. Revised and extended from the, 9(10), 2004.

- Watson and Wright [2021] David S Watson and Marvin N Wright. Testing conditional independence in supervised learning algorithms. Machine Learning, 110(8):2107–2129, 2021.

- Zhang et al. [2019] Hao Zhang, Shuigeng Zhou, Jihong Guan, and Jun Huan. Measuring conditional independence by independent residuals for causal discovery. ACM Transactions on Intelligent Systems and Technology (TIST), 10(5):1–19, 2019.

- Zhang et al. [2022] Hao Zhang, Shuigeng Zhou, Kun Zhang, and Jihong Guan. Residual similarity based conditional independence test and its application in causal discovery. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 36, pages 5942–5949, 2022.

- Zhang et al. [2012] Kun Zhang, Jonas Peters, Dominik Janzing, and Bernhard Schölkopf. Kernel-based conditional independence test and application in causal discovery. arXiv preprint arXiv:1202.3775, 2012.

- Zhang and Janson [2020] Lu Zhang and Lucas Janson. Floodgate: inference for model-free variable importance. arXiv preprint arXiv:2007.01283, 2020.

- Zhang et al. [2017] Qinyi Zhang, Sarah Filippi, Seth Flaxman, and Dino Sejdinovic. Feature-to-feature regression for a two-step conditional independence test. In 33rd Conference on Uncertainty in Artificial Intelligence, UAI 2017. Association for Uncertainty in Artificial Intelligence (AUAI), 2017.

Appendix A Extra content

A.1 Misspecified inductive biases in modern statistics and machine learning

We present a toy experiment to empirically demonstrate how the training algorithm can prevent us from accurately estimating the Bayes predictor even when the model class is correctly specified, leading to invalid significance tests. We work in the context of a high-dimensional (overparameterized) regression with a training set of observations and covariates. We use the Significance Test of Feature Relevance test111111See Section 3.1 for more details (STFR) [7] to conduct the CI test. The data are generated as

where the first thirty entries of are set to 1, and the remaining entries are zero. See that and that is linearly related to and , and then the class of linear predictors is correctly specified when predicting from or . To perform the STFR test, we use LASSO ( penalization term added to empirical squared error) and principal components regression (PCR) to train the linear predictors. Since is sparse, the LASSO fit provides the correct inductive bias while PCR leads to misspecification. We set the significance level to and estimate the Type-I error rate for different training sets. Figure 6 provides the Type-I error rate empirical distribution and illustrates that, despite using the same model class for both fitting methods, the training algorithm induces the wrong model in the PCR case, implying an invalid test most of the time.

A.2 Examples on when STFR fails

Examples A.1 and A.2 show simple situations in which Type-I error control is compromised or the conditional independence test has no power due to model misspecification. As we see in the next examples, Type-I error control is directly related to misspecification, while Type-II error minimization directly relates to misspecification.

Example A.1 (No Type-I error control).

Suppose and , where are independent noise variables and has finite variance. Consequently, . Let and be the classes of linear regressors with no intercept, i.e.,

If denotes the mean squared error, we have that because the model class is misspecified, that is, it does not contain the Bayes predictor given by the conditional expectation .

Example A.2 (Powerless test).

Suppose , where . Consequently, . Define and as in Example A.1. If denotes the mean squared error, we have that121212Because . even though the different Bayes’ predictors have a difference in performance. This happens because the model is not close enough to the Bayes predictor .

A.3 Generalized Covariance Measure (GCM) test

In the GCM test proposed by Shah and Peters [31], the expected value of the conditional covariance between and given is estimated and then tested to determine if it equals zero. To simplify the exposition, we consider and univariate and work in a setup similar to the STFR’s. If , the GCM test relies on the observation that we can always write

where and while the error terms have zero mean when conditioned on . Consequently, we can write . To estimate , we can first fit two models and , that approximate and , using the training set , and then compute an empirical version of using , , and .

In the GCM test, we reject if the statistic exceeds , depending on the test significance level . Here, and are defined as in 3.1 with . If the -value is defined as , the test is analogously given by Equation 3.2. Like the STFR, the GCM test depends on the models’ classes and implicitly on the training algorithm. If the limiting models and are not and , then Type-I error control is not guaranteed.

We introduce definitions and assumptions. Assumption A.3 gives a rate of convergence for the models in the mean squared error sense. Definition A.4 gives a definition for the misspecification gaps.

Assumption A.3.

There are functions , , and a constant such that

Definition A.4.

For each , define the misspecification gap as .

In the next result, we approximate GCM test Type-I error rate and power using the gaps in Definition A.4 and Assumptions A.3, 3.2, and 3.3 applied to this context.

Theorem A.5.

From Theorem A.5, it is possible to verify that if is zero for at least one , i.e., if at least one model converges to the conditional expectation, the GCM test asymptotically controls Type-I error. This can be seen as a double-robustness property of the GCM, which is not present131313This property is clear in our result because we consider data splitting. in Shah and Peters [31]. If , then as even when . Under the alternative, if , Type-II error approaches asymptotically.

A.4 REgression with Subsequent Independence Test (RESIT)

As revisited by Zhang et al. [42], the idea behind RESIT is to first residualize and given and then test dependence between the residuals. It is similar to GCM, but requires the error terms and to be independent. When that assumption is reasonable, one advantage of RESIT over GCM is that it has power against a broader set of alternatives. In this section, we use a permutation test [18, Example 15.2.3] to assess the independence of residuals. We analyse RESIT’s Type-I error control.

If and can be modeled as an additive noise model (ANM), that is, we can write

| (A.1) |

where , , and the error terms are independent of , it is possible to show that To facilitate our analysis141414In practice, data splitting is not necessary. However, this procedure helps when theoretically analyzing the method., we consider first fitting two models and that approximate and using the training set and then test the independence of the residuals151515We omit the residuals superscript to ease notation. and using the test set . Define (i) (test set residuals vertically stacked in matrix form) and (ii) as one of the permutations, i.e., consider that we fix and permute row-wise. Let be a test statistic and and its evaluation on the original residuals and the -the permuted set. If the permutation -value is given by

| (A.2) |

a test aiming level is given by Equation 3.2.

Similarly to STFR and GCM, we consider and to be the limiting models for and . Different from GCM, both models and are multi-output since and are not necessarily univariate.

Now, we introduce some assumptions before we present our result for RESIT. Assumption A.6 gives a rate of convergence for the models in the mean squared error sense.

Assumption A.6.

There are models , , and a constant such that

Assumption A.7 puts more structure on the distributions of the error terms and is a mild assumption.

Assumption A.7.

Assume that for all , the distribution of , , is absolutely continuous with respect to the Lebesgue measure in with -Lipschitz density for a certain . That is, for any and , we have

We assume that does not depend on .

Assumption A.8 states that some of the variables we work with are uniformly almost surely bounded over all . This assumption is realistic in most practical cases.

Assumption A.8.

There is bounded Borel set such that

and

Here, is taken over the model classes we consider (if the model classes vary with , consider the union of model classes). In the following, we present the result for RESIT. For that result, let: (i) and , where the misspecification gaps are given as in Definition A.4; (ii) represent the total variation (TV) distance between two probability distributions [36]; and (iii) the superscript , e.g., in , represent a product measure.

Theorem A.9.

From Theorem A.9, we can see that if at least one of the misspecification gaps or is null, then under . This can be seen as a double-robustness property of the RESIT. If none of the misspecification gaps are null, we do not have any guarantees on RESIT’s Type-I error control. It can be shown that the proposed upper bound converges to .

A.5 RBPT extra derivation

Let be a dominating measure of and that does not depend on . Let (resp. ) be (resp. ) density with respect to .

If

then

A.6 How to obtain a result for RBPT2?

where with

and

If we wanted to adapt that result for RBPT2, we would have to redefine . The analogue of for RBPT2 would be

where denotes the limiting regression model to predict given . If we assume the existence of a big unlabeled dataset, deriving a result might be easier as we can avoid the asymptotic details on the convergence of the second regression model by assuming that the limiting Rao-Blackwellization model, for a fixed initial predictor, is known. The only challenge is proving the convergence of to .

Appendix B Technical proofs

B.1 STFR

Lemma B.1.

Assume we are under the conditions of Theorem 3.4. Then:

Proof.

First, see that for an arbitrary , there must be161616Because of the definition of . a sequence of probability measures in , , such that

Pick one of such sequences. Then, to prove that , it suffices to show that

Now, expanding we get

Then,

Using a law of large numbers for triangular arrays [6, Corollary 9.5.6] (we comment on needed conditions to use this result below) and the continuous mapping theorem, we have that

-

•

-

•

-

•

and then

, i.e.,

Conditions to use the law of large numbers. Let be an arbitrary sequence of probability measures in . Define our triangular arrays as and , where and . Now, we comment on the conditions for the law of large numbers [6, Corollary 9.5.6]:

-

1.

This condition naturally applies by definition and because of Assumption 3.2.

- 2.

- 3.

∎

Theorem 3.4. Suppose that Assumptions 3.1, 3.2, and 3.3 hold. If is a function of such that and as , then

where denotes uniform convergence over all as and

Proof.

First, note that there must be171717Because of the definition of . a sequence of probability measures in , , such that

Then, it suffices to show that the RHS vanishes when we consider such a sequence .

Now, let us first decompose the test statistic in the following way:

Given that is a function of , we omit it when writing the ’s. Define and see that

| (B.1) |

Implying that

Justifying step B.1. First, from a central limit theorem for triangular arrays [6, Corollary 9.5.11], we have that

we comment on the conditions to use this theorem below.

Second, we have that

To see why the random quantity above converges to zero in probability, see that because of Assumption 3.3, Lemma B.1, and continuous mapping theorem, we have that

Additionally, because of Assumptions 3.1, 3.3 and condition , we have that

Finally,

by Slutsky’s theorem. Because is a continuous distribution, we have uniform convergence of the distribution function [27][Chapter 8, Exercise 5] and we do not have to worry about the fact that depends on .

(Type-I error) If holds, then

where denotes uniform convergence over all as .

(Type-II error) In general, we have

where denotes uniform convergence over all as and .

B.2 GCM

Theorem A.5. Suppose that Assumptions A.3, 3.2, and 3.3 hold. If is a function of such that and as , then

where denotes uniform convergence over all as and

Proof.

First, note that there must be181818Because of the definition of . a sequence of probability measures in , , such that

Then, it suffices to show that the RHS vanishes when we consider such a sequence .

Now, let us first decompose the test statistic in the following way:

The terms involving one of the and were all zero and were omitted. Given that is a function of , we omit it when writing the ’s. Define and see that

| (B.2) |

Implying that

Justifying step B.2. First, from a central limit theorem for triangular arrays [6, Corollary 9.5.11], we have that

The conditions for the central limit theorem [6, Corollary 9.5.11] can be proven to hold like in Theorem 3.4’s proof.

Second, we have that

and

To see why the random quantities above converge to zero in probability, see that because of Assumption 3.3, Lemma191919We can apply this STFR’s lemma because it still holds when we consider GCM’s test statistic. B.1, and continuous mapping theorem, we have that

Additionally, because of Assumptions A.3, 3.3, Cauchy-Schwarz inequality, and condition , we have that

Finally,

and

by Slutsky’s theorem. Because is a continuous distribution, we have uniform convergence of the distribution function [27][Chapter 8, Exercise 5] and we do not have to worry about the fact that or depends on .

∎

B.3 RESIT

Lemma B.2.

Let and be two distributions on , , with . Assume and are dominated by a common -finite measure and that is dominated by a -finite measure , for all . Then,

where denotes the total variation distance between two probability measures.

Proof.

Let and denote the densities of and w.r.t. , and let denote the density of w.r.t. . From Scheffe’s theorem [36][Lemma 2.1], we have that:

∎

Lemma B.3.

For all , consider

where and .

Under Assumption A.7 and , we have that

where denotes the total variation distance between two probability measures.

Proof.

Let us represent the stacked residuals (in matrix form) as . See that

Then, because the random quantities above are conditionally discrete, their distribution is dominated by a counting measure depending on . Because the distribution of is absolutely continuous with respect to the Lebesgue measure, and are also absolutely continuous202020Given any training set configuration, the vectors , , are given by the sum of two independent random vectors where at least one of them is continuous because of Assumption A.7 and therefore the sum must be continuous, e.g., . See Lemma B.4 for a proof. for every training set configuration, and then we can apply Lemma B.2 to get that

In the last step, we abuse TV distance notation: by the TV distance of two random variables, we mean the TV distance of their distributions.

Now, define the event

By the definition of the TV distance, we have that (under ):

where the last equality holds from the fact that, given the training set, rows of and are i.i.d.. See that because holds and therefore (making the permuted samples exchangeable).

Using symmetry, we have that

∎

Lemma B.4.

For any , consider that

where , , , and . Then, under and Assumptions A.6 and A.7, all six distributions are absolutely continuous with respect to the Lebesgue measure and their densities are given by

Additionally, we have that

Proof.

Assume we are under . In order to show that is absolutely continuous w.r.t. Lebesgue measure (for each training set configuration) and that its density is given by

it suffices to show that

for any measurable set .

Using Fubini’s theorem, we get

The proof is analogous to the other distributions.

Now, we proceed with the second part of the lemma. Using Assumptions A.6 and A.7, we get

where the last inequality is obtained via Jensen’s inequality. Because the upper bound obtained through Lipschitzness does not depend on , we get

The results for the other converging quantities are obtained in the same manner. ∎

Theorem A.9. Under Assumptions A.6, A.7, and A.8, if holds and is a function of such that and as , then

where denotes uniform convergence over all as .

Proof.

We are trying to prove that

It suffices to show that as . Next step is to show that

and

as . Given the symmetry, we focus on the first problem.

By the triangle inequality, we obtain

and consequently

We treat these terms separately.

(I) Consider a sequence of probability distributions in such that

Here, the distributions and determine not only the distribution associated with but also the distribution of . Because we have that

where is the volume of a ball containing the support of the RVs (existence of that ball is due to Assumption A.8), we also have that , when samples come from the sequence . By the Dominated Convergence Theorem (DCT) [27, Corollary 6.3.2], we have

To see why we can use the DCT here, realize that when samples come from , can be seen as a measurable function going from an original probability space to some other space. Different distributions are due to different random variables while the original probability measure is fixed. Because of that,

for the bounded random variable , where the last expectation is taken in the original probability space. We apply the DCT in .

(II) Following the same steps as in part (I), we obtain

Going back to step B.3, consider another sequence of probability distributions in such that

where

Because of continuity of and

and

we have that

B.4 RBPT

Theorem 4.4. Suppose that Assumptions 4.1, 4.2, 4.3, 3.2, and 3.3 hold. If is a function of such that and as , then

where denotes uniform convergence over all as and

with

and

Proof.

First, note that there must be212121Because of the definition of . a sequence of probability measures in , , such that

Then, it suffices to show that the RHS vanishes when we consider such a sequence .

Now, let us first decompose the test statistic in the following way:

Given that is a function of , we omit it when writing the ’s. Define and see that

| (B.4) | |||

| (B.5) |

Implying that

Justifying step B.5. First, from a central limit theorem for triangular arrays [6, Corollary 9.5.11], we have that

The conditions for the central limit theorem [6, Corollary 9.5.11] can be proven to hold like in Theorem 3.4’s proof.

Second, we have that

To see why the random quantity above converges to zero in probability, see that because of Assumption 3.3, Lemma222222We can apply this STFR’s lemma because it still holds when we consider GCM’s test statistic. B.1, and continuous mapping theorem, we have that

Additionally, because of Assumptions 4.1, 4.2, and 4.3 and condition , we have that

where is an upper bound for the sequence (Assumption 4.3) and is an upper bound for the sequence (Assumption 4.2).

Finally,

by Slutsky’s theorem. Because is a continuous distribution, we have uniform convergence of the distribution function [27][Chapter 8, Exercise 5], and we do not have to worry about the fact that depends on .

∎

Appendix C Experiments

C.1 Running times

Artificial-data experiments.

Regarding running times (average per iteration), RBPT took to run, RBPT2 took , STFR took , RESIT took , GCM took , CRT took , and CPT took , all in a MacBook Air 2020 M1.

Real-data experiments.

Regarding running times (average per iteration), RBPT took to run, RBPT2 took , STFR took , GCM took , CRT took , and CPT took , all in a MacBook Air 2020 M1.

C.2 Extra results

We include extra experiments in which has skewed normal distributions with location , scale , and shape (shape lead to the normal distribution). From the following plots, we can learn that the skewness often impacts negatively in Type-I error control.

|

|

|

|