A Comprehensive Framework for Evaluating Time to Event Predictions using the Restricted Mean Survival Time

Abstract. The restricted mean survival time (RMST) is a widely used quantity in survival analysis due to its straightforward interpretation. For instance, predicting the time to event based on patient attributes is of great interest when analyzing medical data. In this paper, we propose a novel framework for evaluating RMST estimations. Our criterion estimates the mean squared error of an RMST estimator using Inverse Probability Censoring Weighting (IPCW). A model-agnostic conformal algorithm adapted to right-censored data is also introduced to compute prediction intervals and to evaluate variable importance. Our framework is valid for any RMST estimator that is asymptotically convergent and works under model misspecification.

Keywords. RMST, prediction, IPCW, Brier score, conformal, prediction intervals, variable importance.

1 Introduction

In survival analysis, in the context of right-censored data, it is common to model the effect of covariates on the hazard rate, using the ubiquitous Cox model [8, see]. This model is interpreted in terms of hazard ratios and is widely used to analyze incomplete data in medical applications. However, it relies on the strong assumption of proportional hazard (PH). As a result, approaches that focus on other estimands, such as the restricted mean survival time (RMST), have been proposed. This quantity represents the expected duration of the minimum between the occurrence of an event of interest and a predefined time horizon. It is clinically meaningful (as an expected time) and has gained considerable attention in recent years due to its simple interpretability. While initial works on this topic still relied on the PH assumption [16, 31, see], new approaches have been developed to directly model the RMST without making any assumptions [2, 26, 29, see].

Also, in time to event analysis, it might be of interest to predict the future occurrence of the event of interest using an estimation of the RMST. This is the case for instance, when clinicians aim at predicting the time to relapse, cancer occurrence or death of a patient. In recent years, new methods have been developed in this context [30, see] and there is thus a need for evaluating the performance of those learning models. This is usually a challenge in the presence of right-censored data because the censored times are not observed and it is therefore difficult to assess the performance of the learning model for those times. To address this challenge, the C-index [14, see] has emerged as a widely used metric, particularly as it has been adapted to censored data [12, see]. However, it has been shown not to be a proper scoring function [3, see]. In contrast, the time-dependent area under the ROC curve is a proper score, but it is also based on the evaluation of the rank preservation of the predictions. When it comes to quantitative measures, the mean squared error (MSE) is a proper one, but it is not readily available due to censoring. [13] proposed a measure designed to approximate the MSE of a survival function estimator, but, prior to our work, this had not been extended to the context of RMST.

Another important topic in this context concerns the construction of prediction intervals, which evaluate the degree of confidence in the prediction by taking into account the individual variability. The conformal approach originally proposed by [28] and later expanded and popularized by [21], offers a way to build prediction intervals with guaranteed coverage. Although this approach has been adapted to right-censored data, it is still subject to significant constraints. [4], [7], [25] proposed model-specific conformal inference algorithms for random survival forests, DeepHit, and Cox-MLP, respectively. [6] proposed a model-agnostic algorithm to build a prediction lower bound for right-censored data, but with no upper bound and only for censoring of type I.

Finally, being able to interpret the output from a learning model is crucial, especially when using black-box models. To that end, one possibility is to determine the variables importance by using permutations as developed in [5] in the context of random forests. This technique is widely used and has been extended to right-censored data, for instance in [15] and [30]. Recently, model-agnostic importance measures such as LIME and SHAP have been adapted to the estimation of the survival function [18, 19, see] but no extensions for the RMST have been developed yet. Although the leave-one-covariate-out (LOCO) conformal approach introduced by [21] provides an alternative method for exploring variable importance, it has not yet been extended to right-censored data.

In this work, our goal is to propose a new measure designed to approximate the MSE of an RMST estimator, relying on Inverse Probability Censoring Weighting (IPCW) to take into account right-censoring. This measure is similar to the Brier score introduced in [13]. In addition, a new conformal algorithm based on IPCW for the construction of prediction intervals for restricted times to event is developed,which is inspired from the split algorithm in [21]. It is further extended to study local and global variable importance within a learning model. In particular, a statistical test for global variable importance is proposed. Those methods are based on the LOCO procedure from [21] and take into account right-censored data using IPCW. All our methods are proved to be asymptotically valid. They are illustrated on simulations and on a real data analysis on breast cancer.

In Section 2 we give the main notations used in the following sections. In Sections 3, 4, 5 we present the new methods described previously, respectively the mean squared error measure, the prediction intervals algorithms and the variable importance measures. The results on simulations are presented in Section 6 and on real data in Section 7.

2 Notations and assumptions

In the context of right-censored data, we denote by the variable of interest, the censoring time, the observed variable and the censoring indicator. An observation is then represented by the vector where is a covariate vector. We introduce the following notations for the cumulative distribution and survival functions: , , and are the cumulative distribution functions of , , and , respectively. is the survival function of . For all these functions, the same notations are used for the joint and conditional cumulative distribution functions with respect to , for instance . Finally, we note .

Let . The RMST is defined for a fixed time horizon as

| (1) |

We suppose that the i.i.d. observations are divided into a training set of size and a test set of size . We will call a learning model/algorithm , a function that maps a training set to an RMST estimator , also referred to as a predictor. is the space of possible outcomes of . We impose that these functions verify for a positive constant . In the following, when the split conformal intervals will be introduced (see Section 4), the training set will be further split in two parts, that is, will be divided into two subsets and of sizes and respectively, such that . In that case, , , will be the corresponding subsets of . Estimators of the functions , , and computed on the training set are written , , , and respectively. If they are computed on one of the subsets , , they are denoted , , and , respectively.

Unless mentioned otherwise, we will assume conditional independence in the following sense:

| (2) |

We will also assume the RMST estimator to be convergent in the following sense: for all , there exists such that

| (3) |

Moreover we say that the model is correctly specified if and . It should be noted that this assumption allows for model misspecification since we do not impose to be equal to the true RMST (and in practice this will usually not be the case). Finally, we will assume the censoring estimator to be consistent using two different definitions. A censoring estimator is said to be strongly consistent if for all ,

| (4) |

and weakly consistent if

| (5) |

We emphasize that, in those two definitions, we impose the censoring estimator to converge towards the true . This is a strong assumption since it imposes that the censoring model is correctly specified.

3 Performance criterion for the estimation of the RMST

When the data are fully observed, a classical quantity to measure the prediction performance of an estimator is the Residual Sum of Squares (RSS)

| (6) |

where is computed on the training set and the RSS is evaluated on the test set. When the RMST estimator is convergent (see Equation (3)) then, as and go to infinity, the RSS will converge to the Mean Squared Error (MSE)

However, in the context of right-censored data, the event times are not all observed and the score (6) cannot be computed. This issue has been addressed in [13] when the goal is to estimate the survival function. In our work, we use a similar approach to estimate the MSE of an RMST estimator, based on Inverse Probability Censoring Weighting (IPCW). We define:

| (7) |

where

| (8) |

and is a consistent estimator of the censoring cumulative distribution function. We have the following result.

Theorem 1.

Note that the validity of the result relies on Equation (5). If the latter is verified with the estimator of the censoring distribution function computed on the training set only, then it also holds on the pooled data including both the training and the test set. In applications we recommend to use all the data to estimate . Also, a straightforward result from Theorem 1 is that our WRSS estimator is asymptotically equivalent to the RSS estimator defined in Equation (6) since both estimators converge towards .

Finally, we recall that the mean squared error can be decomposed in the following way:

| (9) |

where on the right-hand side of the equation, the first quantity represents an imprecision term and the second one, an inseparability term [13, see]. If the model is correctly specified, i.e. , then the imprecision term will vanish. In that case, the WRSS estimator will converge to the inseparability term, as and go to infinity.

4 Prediction intervals

In this section, we explain how a prediction interval can be built from the RMST estimator. Our method is based on the conformal intervals method, developed initially by [28] and extended, among others, by [21]. In the latter article, the authors provide algorithms to construct prediction intervals that have finite-sample validity without making any assumptions on the distribution of the observations. More specifically, for a given confidence level and a new individual with covariate , the aim is to construct a prediction interval such that

Our method adapts the conformal prediction approach from [21] using the IPCW technique to deal with right-censored data.

4.1 IPCW Split Conformal algorithm

Since the original conformal prediction algorithm is computationally intensive, we rely on the so-called split conformal prediction developed by [21] as an alternative approach. Its computational cost is a small fraction of the full conformal method and finite-sample guarantees are very similar. It operates as follows. First divide into two subsets and of size and respectively, such that . Let , , be the corresponding subsets of . Train the learning algorithm on . The resulting estimator provides predictions for the data in , namely , .

For the ease of presentation, consider first a situation where the data are uncensored. In this setting, the residuals

can be directly computed from the data. As a result, the cumulative distribution function of the residuals, defined for all by , can be approximated by the empirical estimator

Finally, the prediction interval for a new individual with covariate is defined as

with the quantile of the empirical distribution , where denotes the order statistics of . By exchangeability between the residual at and those at , we have

However, when the data are censored, the residuals can no longer be computed. Clearly, computing the residuals from the observed times

will induce a bias. To correct for this bias, we therefore propose to adjust the estimator of the cumulative distribution function of the residuals by IPCW, using the same weights as in Equation (8). The distribution estimator now becomes

We present below the algorithm that summarizes the procedure. Then, Theorem 2 ensures that the prediction intervals produced by Algorithm 1 have asymptotically valid coverage.

Theorem 2.

Suppose that is strongly consistent in the sense defined by Equation (4). If the observations , , are i.i.d., then for a new i.i.d. individual with event time and covariate , under conditional independence (see Equation (2)),

for the split conformal prediction interval constructed by Algorithm 1. In addition, if the residuals have a continuous distribution, then

Remark 1.

The validity of the results only relies on the accuracy of the estimate of the cumulative distribution function of the residuals, which depends on . However, a higher value of yields a better predictor , resulting in smaller residuals and shorter prediction intervals, which is desired in applications.

Remark 2.

In most cases the residuals will have a continuous distribution. However, it may happen that the residuals distribution put a positive mass on discrete values when some predictions are identical and the corresponding observations are also equal. This can occur if some individuals have the exact same covariate values or if they only differ for some covariates that are not used by the learning model. It is also common to use a reference model that does not take into account the covariates at all, in which case all predictions will be identical. When the residuals have a positive mass on some discrete values it may not be possible to exactly reach the desired confidence level and, in that case, the quantile of the residuals will be chosen such that the coverage exceeds . Another approach consists in randomly breaking the ties in the residuals, as in [20].

4.2 IPCW In-Sample Split Conformal algorithm

The split algorithm introduced in the previous section aims at producing a prediction interval with the correct coverage for a new individual independent from the training set. However it might also be of interest to construct prediction intervals for the individuals in the training set itself. A simple, yet computationally inefficient, way to compute the prediction interval for each , is to apply Algorithm 2 using all observations but as training set. A more interesting approach is the Rank-One-Out (ROO) Split Conformal algorithm introduced by [21] to construct valid prediction intervals for all training data without requiring much more calculation. Similarly to Section 4.1, we adapt the ROO algorithm to the right-censoring framework using IPCW. Our weighted leave-one-out method is presented in Algorithm 2. Asymptotic guarantees as in Theorem 2 can be similarly derived for Algorithm 2 but have been omitted for the sake of conciseness.

5 Variable importance

Conformal inference can also be used to assess the importance of each variable in the learning model. In particular, the Leave-One-Covariate-Out (LOCO) inference method described by [21] can be adapted to the estimation of the RMST with censored data based on the new algorithms described in Section 4. To evaluate the importance of the th variable, , the approach involves comparing the accuracy of the predictor trained with or without the th variable. The magnitude of the performance difference indicates the variable significance in the model. Specifically, if we denote the predictor trained on data without the th variable, we are interested in the random variable

| (10) |

that measures the increase in prediction accuracy resulting from the inclusion of the th variable in the model. The higher its value above zero, the greater the variable importance. This analysis can be conducted globally to assess the variable overall importance in the model or locally to identify specific variable values that have a more significant impact on the outcome.

5.1 Local measure of variable importance

The aim is to construct a prediction interval for . Let be a prediction interval constructed with the split procedure for given with coverage . For all , define

Then from the asymptotic coverage of the prediction interval , we have

| (11) |

It should be stressed that the result is not given conditionally on , however varying the value of the covariate will nevertheless have an impact on the intervals. Therefore, it will be of interest to evaluate the effect of the th variable by plotting the intervals for .

5.2 Global measure of variable importance

In this section, we consider that the data set is fixed. As opposed to the previous sections, we make the additional assumption that the censoring is independent from the time to event and from the covariates . We use the IPCW technique to construct the statistical test below, specifying that the weights use the Kaplan-Meier estimator for the censoring distribution based on the sample . Formally, with denoting the Kaplan-Meier estimator of the censoring survival function, the weights , , become

| (12) |

The global measure of the importance of the th variable is constructed from the distribution of marginally over . We consider the cumulative distribution function of conditional on being lower than the threshold , with . For simplicity, we suppose this distribution to be continuous and we are interested in inferring its median:

Specifically, we want to perform the following test

which is equivalent to the test

with . Let . In particular, note that

We introduce the new test statistic

| (13) |

where denotes the Kaplan-Meier estimator of the survival function, the censoring weights , are defined as in Equation (12), and

with . This is a modification of the standard sign test statistic suited for right-censored data. In Theorem 3, we show that this test statistic follows asymptotically a Gaussian distribution with variance equal to under . This allows us to construct the statistical test with predefined level. The construction of an asymptotic confidence interval for is also proposed in Theorem 3.

Theorem 3.

Let be a fixed data set. Let , denote the Kaplan-Meier estimators of the functions , respectively, computed on a data set independent from . Let the censoring be independent from the time to event and from the covariates. We consider the weights as defined in Equation (12). Then, under , the test statistic defined in Equation (13) follows asymptotically a Gaussian distribution with variance equal to . Let denote the quantile of this distribution, then

We also have

| (14) |

Remark 3.

To simplify the proof, Theorem 3 is presented with the censoring estimator being calculated on . We were not able to prove that the results would still hold if the censoring estimator was calculated from all the data but our simulations suggest that this would be the case.

Remark 4.

In some cases, the inclusion or exclusion of the th variable in the learning model may not affect the predictions. This may occur for models that are independent of covariates such as the Kaplan-Meier model, or in learning models that include variable selection steps like the LASSO. When this happens, equals and is equal to , although would better indicate that the covariate has no predictive power. One way to address this issue is to introduce a different definition of based on a jittered version of :

| (15) |

where and . This jittering approach randomly allocates a sign to when it is equal to , which avoids putting mass on and guarantees that for the th variable if it is not used by the predictor.

6 Simulations

This section illustrates all the methods and results described in Sections 3, 4 and 5 through simulated experiments. In Section 7 an application to the German Breast Cancer Study Group (GBCSG) is also presented. In both sections, the following learning algorithms are implemented and then evaluated using our methods.

- Integrated Kaplan-Meier:

-

A Kaplan-Meier estimator is fitted to to estimate the survival function. By integrating this curve on the interval , we obtain an estimation of the RMST that is identical for all individuals in the test sample . This represents a naive algorithm since it does not take into account the covariates.

- Integrated Cox:

-

A Cox model [8, see] is fitted to . Unless mentioned otherwise, no interaction between covariates is included in the model. The fitted model provides an estimation of the survival curve for each observation in , adjusted with respect to the covariate . The estimation of the RMST is obtained by integrating this curve with respect to time on the interval .

- Integrated Random Survival Forest (RSF):

-

The procedure is identical to the one described above with the difference that an RSF [15, see] is fitted to instead of a Cox model.

- Pseudo-observations and linear model:

-

We transform the censored data in into pseudo-observations [2, see]. We use the linear model as the link function to obtain a linear model for the RMST. Unless mentioned otherwise, no interaction term is included in the linear model.

We stress that, in the simulations, the RMST estimations obtained with those algorithms will never be truncated even if they exceed . This avoids creating ties in the residuals as mentioned in Remark 2. We consider three different simulations schemes.

- Scheme A:

-

Following the setting from [29], the event times are simulated according to the following linear model:

where , the covariates are denoted with and is a random noise. From this model we obtain the following closed form for the RMST:

(16) where is computed from million Monte-Carlo samples. The value of is fixed to which yields . Next, two different types of censoring are considered. In scheme A1, the censoring is simulated independently from the covariates according to an exponential law with parameter , leading to of censored data. In scheme A2, the censoring is simulated from a Cox model with Weibull baseline hazard defined as

We set , , and , , leading to of censored data.

- Scheme B:

-

The event times are simulated according to a Cox model with Weibull baseline hazard and three covariates , where for , with Cox regression parameters . Note that the survival function can be expressed as

and the RMST can be obtained from Equation (1). Parameters are set to , , , . The censoring is simulated independently according to an exponential law with parameter , leading to censored data. The time horizon is chosen as the th percentile of the observed times which gives .

- Scheme C:

-

Similarly to scheme B, the event times are simulated according to a Cox model with Weibull baseline hazard , , with

and , . Let , we simulate the covariates such that for and . As a result, only the first covariates are associated with the event times, but the other covariates (that are non-informative) will still be included in our regression models. The survival function is expressed as:

and the RMST can be obtained from Equation (1). The censoring distribution is the same as in scheme B, leading to censored data. The time horizon is chosen as the th percentile of the observed times which gives .

6.1 Illustration of the WRSS estimator

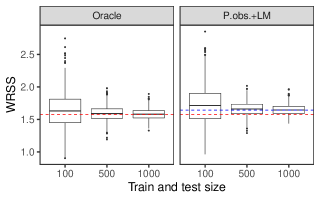

In this section, we want to illustrate Theorem 1. It states that, if the censoring estimator is consistent, then our prediction performance criterion, called WRSS (see Equation (7)), converges towards the MSE as the sample size goes to infinity. We recall that and that is the limit of the predictor, as defined in Equation (3). We also recall that can be decomposed into an inseparability and imprecision terms, as shown in Equation (9). We will consider the simulation schemes A1, A2 and two learning models. The first one is a linear model that is directly fitted on the minimum between the true event times and the time horizon , using the correct link function (see Equation (16)). It is considered as the oracle model. The second one is based on pseudo-observations with linear link function. The latter is implemented without interaction terms, i.e. only the covariates , are included.

In the scenario A1, the censoring is independent of the covariates and we use the Kaplan-Meier estimator to estimate its cumulative distribution function which is a consistent estimator (in the weak sense). Thus, the WRSS should converge to the MSE (see Theorem 1). In addition, for the oracle model, the imprecision term should vanish as the model is correctly specified and the WRSS should therefore converge to the inseparability term. On the other hand, for the model based on pseudo-observations, the imprecision term will not vanish and the WRSS should then be larger than with the oracle model. Since the RMST has an explicit form, the inseparability term can be easily computed using Monte Carlo simulations. For the imprecision term of the model based on pseudo-observations, was approximated by a predictor trained on a sample of size and the expectation was calculated using a million Monte-Carlo simulations. In Figure 6.1, we represent the WRSS based on train and test samples of equal size , and for those two learning algorithms. The boxplots are obtained from repetitions. We clearly see that the oracle estimator converges towards the inseparability term, displayed in red in the figure. On the contrary, we see that, with the estimator based on pseudo-observations, the WRSS converges towards a value greater than the inseparability term, as expected. With the pseudo-observations model, we observe that the imprecision term is relatively small compared to the inseparability term which suggests that, while the regression model is incorrect, it still provides predictions that are close to the ones obtained using the oracle model.

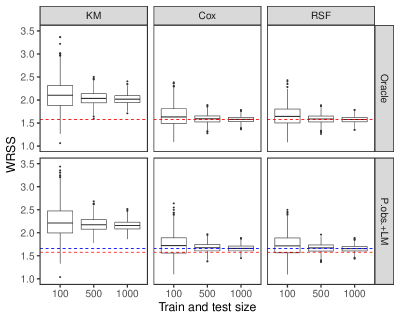

In the scenario A2, the censoring depends on the covariates through a Cox model. In this setting we also compare the performance of the two learning algorithms using different censoring models: a Kaplan-Meier method, a Cox model and an RSF model are implemented. We stress that the Kaplan-Meier method is no longer consistent while the Cox model is a consistent estimator for the censoring distribution. The results are illustrated in Figure 6.2 where the boxplots are also obtained from repetitions. We clearly observe that the Kaplan-Meier method for the censoring distribution provides biased estimates of the MSE. On the other hand, the Cox and RSF models provide accurate estimations of the MSE. As in the scenario A1, the imprecision term is seen to vanish with the oracle model and has a relatively small value compared to the inseparability term, when using the pseudo-observations model. Those results also suggest that the RSF model for the censoring distribution is a consistent estimator (in the weak sense) since the results are almost identical with the results from the Cox model.

6.2 Illustration of the IPCW Split Conformal algorithm

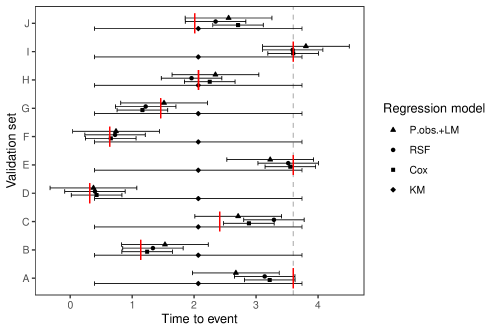

In this section, we illustrate the construction of prediction intervals using the IPCW split conformal algorithm introduced in Section 4.1 (see also Algorithm 1). We simulate data using the simulation scheme B and we train all four learning models introduced at the beginning of Section 6. We first start by displaying in Figure 6.3 the prediction intervals at level on a sample of 10 individuals while the algorithms were trained on a single independent sample of size .

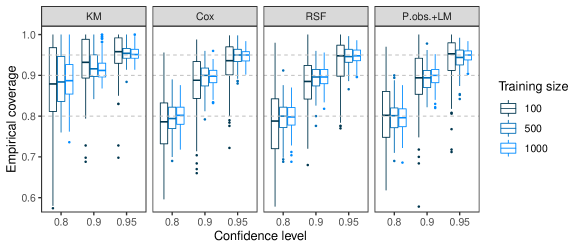

Then, the coverage of the intervals, as claimed by Theorem 2, is assessed in Figure 6.4, with equal to , or . This time, the learning algorithms were trained on samples of size , and and the testing set is of size . The simulations were repeated times. We observe that for all learning models and confidence levels, the empirical coverage converges to , except for the integrated Kaplan-Meier algorithm which converges to a level greater than . Since this algorithm gives an RMST estimation that is identical for all individuals (as it does not take into account the covariates), the observations that are greater than will all have the same residual value. These ties make the distribution of the residuals discrete and therefore the empirical quantile of order is such that the coverage exceeds (see Remark 2).

6.3 Illustration of the LOCO variable importance measures

In this section, we provide illustrations of the use and performance of the LOCO variable importance measures introduced in Section 5. We consider the simulation scheme B and, for all four learning algorithms, we want to test versus , for . We use the definition (15) for so as to get , , for the Kaplan-Meier model as explained in Remark 4. In this scenario, has no effect on the outcome since in the Cox model used to generate the data. When using the Kaplan-Meier estimator, is equal to for all since adding or removing a variable will have no impact on the prediction result. However, the value of is unknown when using other algorithms and in particular, we do not know in advance if ( is true) or if ( is true). Their values are thus approximated via Monte-Carlo simulations. We first simulate a training set of size which remains unchanged throughout the whole simulations (note that Theorem 3 holds for a fixed ). Next, we train the learning algorithms on this data set, simulate pairs and compute from the distribution of the corresponding . Table 1 shows the resulting values.

| Learning model | |||

|---|---|---|---|

| Kaplan-Meier | 0.50 | 0.50 | 0.50 |

| Cox | 0.87 | 0.79 | 0.49 |

| Random Survival Forests | 0.82 | 0.71 | 0.44 |

| Pseudo-observations and linear model | 0.84 | 0.70 | 0.46 |

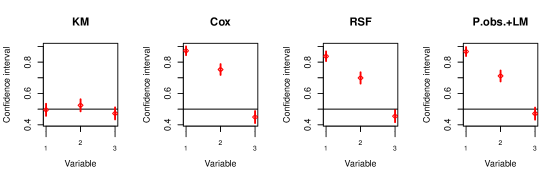

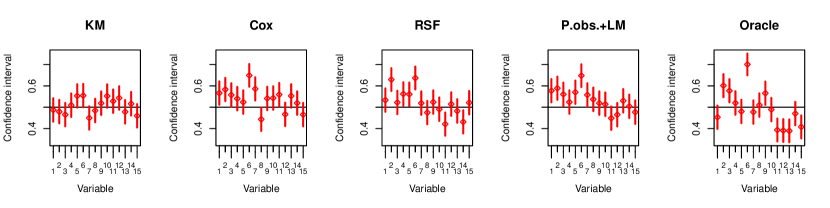

In practice, global variable importance can be determined using Theorem (3). In Figure (6.5), using Equation (14), the confidence intervals at the level for for the four learning algorithms are displayed based on and a data set of size simulated independently according to scenario B. We observe that the Cox model, the RSF model and the linear model based on pseudo-observations seem to all agree that only the first two covariates are important. For the Kaplan-Meier estimator, the three confidence intervals cross .

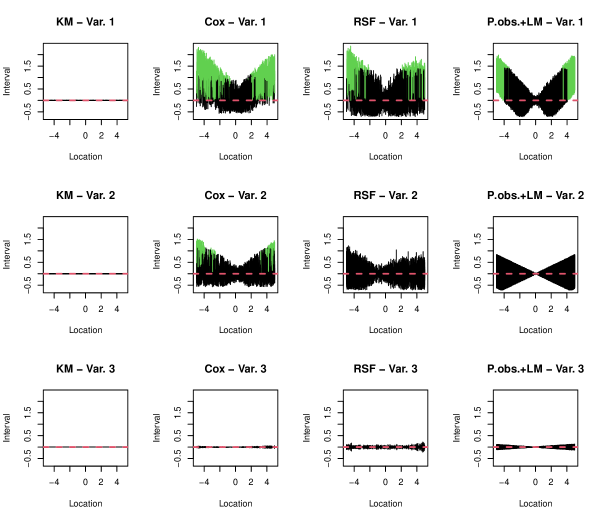

Using the same data sets and , the local variable importance is illustrated for all four models and all three covariates in Figure 6.6. The Kaplan-Meier model is set as a reference as none of the three covariates play a role in it. The other learning algorithms all consider the first covariate to have importance in its high and low values and the third covariate to have no importance in the predictions, but they do not reach the same conclusions about the second covariate. The Cox model detects its importance for high and low values of the variable while the other two do not detect any importance of the variable. When the size of the data set increases, our simulations show that the RSF also comes to detect importance in high and low values (data not shown). The Cox and RSF models provide then very similar conclusions for all three covariates in terms of local variable importance.

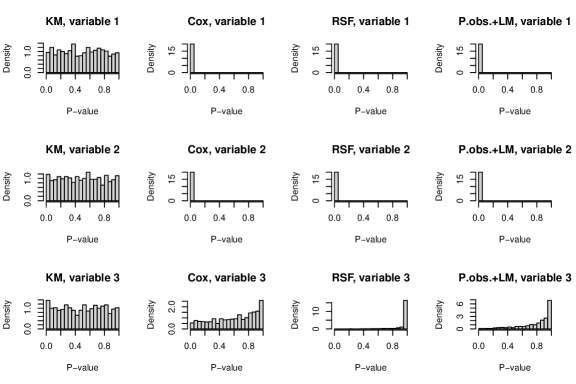

Still using the same fixed data set , we empirically assess the calibration and power of our test for global importance by simulating samples of size and by computing for each one the p-value for the statistical test. The histograms of those p-values for each value of and all four algorithms are displayed in Figure 6.7. We first observe that the p-values for the Kaplan-Meier estimator are uniformly distributed, since in this case, for all ( is true). For the other algorithms, when , we observe a skewed distribution of the p-values towards . This was also expected since the hypothesis is composite and, according to Table 1, is true for for all models. Finally, when ( is true) we observe that all three algorithms have a very strong power (all p-values are less than 0.01).

6.4 Multi-splitting

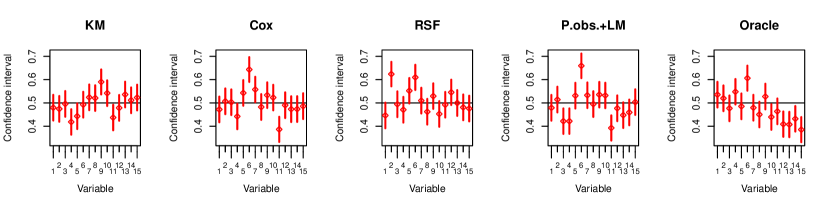

We want to emphasise that variable importance results depend not only on the learning algorithm but also on the split of the data. In particular when it comes to assessing global variable importance, results may vary drastically depending on the split, for instance when the link between covariates and outcome is complex such as in the simulation scheme C. As an illustration, the LOCO global variable importance test is performed for all four learning models, on a data set of size simulated with the simulation scheme C. The oracle Cox model taking interactions into account is added for comparison. Figure 6.8 presents the outputs of the procedure repeated twice, the only difference being the data split. Some variables seem to improve the accuracy of the model on one split, and on the contrary to degrade it on the other.

To reduce the effect of the split, methods like multi splitting described in [9] can be considered. Specifically the authors of this paper propose to choose splits of the data, and then compute a p-value for each split. Twice the resulting median or average p-value provides a valid p-value for the overall test. The overall Type 1 error can be controlled and bounded under , however this comes with a loss of power compared to a single split. We selected splits of our data set simulated according to simulation scheme C. For each split, each learning algorithm and each variable, we computed a p-value. Twice the median p-value is computed for each setting and reported in Table 2. No variables have a notable impact in the Kaplan-Meier model. For the other models, binary variables such as , and seem to play a significant role on the predictions. There is a consensus on variables to , which are uninformative and indeed seem to have no impact. The effect of other variables is elusive, and can vary depending on the model.

| Variable | P-value KM | P-value Cox | P-value RSF | P-value P.obs.+LM | P-value Oracle | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 1 | 0.62 | 1 | 0.588 | 1 | |||||

| 2 | 0.982 | 0.007 | ** | 0 | *** | 0.012 | * | 0.001 | ** | |

| 3 | 0.963 | 0.545 | 1 | 0.489 | 0.467 | |||||

| 4 | 0.891 | 1 | 0.863 | 1 | 0.145 | |||||

| 5 | 1 | 0.105 | 0.466 | 0.054 | . | 0.102 | ||||

| 6 | 1 | 0 | *** | 0.001 | ** | 0 | *** | 0 | *** | |

| 7 | 1 | 0.453 | 0.54 | 0.804 | 0.225 | |||||

| 8 | 1 | 0.958 | 1 | 0.677 | 0.576 | |||||

| 9 | 1 | 0.087 | . | 0.05 | . | 0.067 | . | 0.046 | * | |

| 10 | 0.893 | 0.992 | 1 | 1 | 0.46 | |||||

| 11 | 1 | 1 | 1 | 1 | 1 | |||||

| 12 | 1 | 1 | 1 | 1 | 1 | |||||

| 13 | 1 | 1 | 1 | 1 | 1 | |||||

| 14 | 1 | 1 | 1 | 1 | 1 | |||||

| 15 | 0.98 | 1 | 1 | 0.893 | 1 | |||||

Significance codes: 0 ’***’ 0.001 ’**’ 0.01 ’*’ 0.05 ’.’ 0.1 ’ ’ 1

7 Application on real data

We illustrate our comprehensive framework for evaluating RMST estimators on the classic German Breast Cancer Study Group (GBCSG) data set, which was first introduced in [24] and is now available in the survival R package. The GBCSG gathered patients with node-positive breast cancer. The study was conducted from 1984 to 1989 and aimed to investigate the impact of hormone treatment on recurrence-free survival time. The event of interest is then the recurrence of a cancer, which was observed for 299 of the 686 patients. 246 patients were treated with additional hormonal therapy. Finally, prognostic factors were collected on all patients: age, menopausal status, tumour size, tumour grade, number of positive nodes, progesterone receptor and estrogen receptor. We estimated the censoring survival function using the Kaplan-Meier model. We set the time horizon at the 90th percentile of the observed times distribution (2014 days) and were interested in the recurrence time prediction up to that time limit. We tried all four of the learning algorithms described in Section 6. For each one, the WRSS is computed based on -fold cross-validation in Figure 7.1. The Kaplan-Meier model is less performing than the covariate-dependent models, indicating that the chosen prognostic factors indeed play a role on the recurrence-free survival time. The RSF seems to have a slightly better performance than the Cox model and the linear model based on pseud-observations, though the variability of the results makes it difficult to identify clearly which algorithm is best suited to the data. Results of the global variable importance test using multi-splitting on splits are displayed in Table 3. Interestingly, no variables turn out to be important in the RSF predicting the recurrence time, despite its observed overall good predictive performance. Hormonal therapy, progesterone receptors, and tumor grade are important in the prediction with both the Cox model and the linear model based on pseudo-observations.

| Variable | P-value KM | P-value Cox | P-value RSF | P-value P.obs.+LM | ||||

|---|---|---|---|---|---|---|---|---|

| hormon | 1 | 0.001 | ** | 0.166 | 0.001 | ** | ||

| age (years) | 1 | 1 | 1 | 1 | ||||

| menopausal status | 1 | 0.203 | 1 | 0.093 | . | |||

| tumour size (mm) | 1 | 0.989 | 0.498 | 1 | ||||

| number of positive nodes | 1 | 1 | 0.329 | 1 | ||||

| progesterone receptor (fmol) | 1 | 0 | *** | 0.359 | 0 | *** | ||

| estrogen receptor (fmol) | 1 | 1 | 1 | 1 | ||||

| tumour grade | 1 | 0 | *** | 0.516 | 0 | *** | ||

Significance codes: 0 ’***’ 0.001 ’**’ 0.01 ’*’ 0.05 ’.’ 0.1 ’ ’ 1

8 Conclusion

One way of assessing the fit of a model and its prediction ability is to evaluate its MSE based on a test sample. This is a general measure that allows to compare a wide range of models without making any specific model assumption. In the presence of right-censoring, due to tail estimation issues, it is natural to focus on the prediction of the restricted time based on a clinically relevant fixed time horizon [10, see]. Over the recent years, there has been a wide variety of new models that can handle censored data from the random survival forest method to neural networks based methods [15, 30, see]. Those methods make few assumptions as compared to the ubiquitous Cox model that relies on the proportional hazard assumption and it is interesting to evaluate and compare their prediction abilities. Based on the MSE it is well known that the best prediction model is the conditional expectation of the restricted time and therefore predicting the restricted time amounts to estimating the RMST.

Methods for evaluating RMST estimation models remain limited. Prior to our work, concordance measures were used to compare predictive performances of RMST estimators but no quantitative metric was suggested. In addition, no model-agnostic methods were available to construct prediction intervals. In this context, we propose a complete framework for evaluating a time to event predictor using the RMST. Specifically, we propose methods to assess its prediction ability and variability, and to estimate variable importance, globally and locally. The steps of the implementation can be summarized as follows.

-

1.

Evaluate the predictive performance of the predictor quantitatively with the WRSS (7), an estimator of the MSE based on IPCW. To reduce the variability induced by the splitting procedure, -fold cross-validation is recommended.

- 2.

-

3.

For each variable of interest, evaluate its global importance in the regression model with the statistical test (13) and construct the corresponding confidence interval given by (14). Note that this measure is inherent in the model and in the data split and can differ from the true significance of the variable.

-

4.

Compute the local variable importance when it is relevant, that is for variables with a sufficient amount of possible values. This measure is also inherent in the model and in the data split.

In a context of high-dimensional data, one can form groups of variables that are relevant according to domain-specific knowledge. To this aim, in the definition (10), the which represents the th variable can equivalently represent the th group of variables. Otherwise, we recommend to focus only on a subset of relevant covariates by first applying a pre-selection step on the data, typically with selection variables methods such as the Lasso or based on an AIC criterion [17, see for instance]. These methods allow to reduce the computational cost of our procedure.

Under consistency assumptions defined in Section 2, we proved that all the methods described above are asymptotically valid. We want to stress that the whole analysis procedure is model-agnostic, thus robust against model misspecification, but not against censoring model misspecification. This is a classical limitation when using IPCW methods: in particular, the same assumption on the censoring model is required for the standard Brier score [13, see]. Another limitation concerns the independence assumption between censoring and covariate for the global variable importance test, in Theorem 3. Unfortunately, we were not able to extend this result to a more general dependence relation. The distribution of the test statistic relies on properties of Kaplan-Meier integrals and new theoretical results would need to be derived for a test statistic that would be based on a general estimator of the censoring cumulative distribution. This is left to future research.

9 Technical proofs

9.1 Proofs for Section 3

9.2 Proofs for Section 4

Let be the inverse probability censoring weights computed with the unknown function , i.e. for all

Lemma 1.

Let be an observation independent of . Let

such that is almost surely finite. Then

Proof.

We have:

where in the third equality we used the independence assumption between and conditional on . ∎

Lemma 2.

For independent of , let be a function verifying a.s. for all . If is strongly consistent in the sense defined by (4) then

Proof.

As the , , are conditionally independent given with the same conditional distribution, then by the strong conditional law of large numbers [23, see Theorem 4.2 in] and by Lemma 1,

On the other hand, as that there exists such that for high enough and ,

where the convergence to zero follows from the strong consistency of the censoring estimator defined by (4) and the law of large numbers for . ∎

Proof of Theorem 2.

Then for all ,

For all , let and be the quantiles of the cumulative distribution functions and respectively. Then from Lemma 21.2 in [27] we have that for all

Finally, applying the continuous mapping theorem to the function gives

i.e.

In particular, if the residuals have a continuous distribution given , then .

∎

9.3 Proofs for Section 5

We provide here a slightly more general result than the one given by Theorem 3, where the function can be any bounded function with support on . For clarity, we state the theorem in its general form below.

Proposition 1.

Let and be a uniformly bounded function with support . Let

Suppose that . Let , and denote the Kaplan-Meier estimators of the functions and computed on . The censoring weights , are defined as in Equation (12). Let

be an estimator of . Then

where

with . Moreover, the estimator

where , is consistent for the variance .

Proof.

For all , we introduce the martingale residuals

First note that the weights , defined in Equation (12) simplify into because has support . Then

From [22], is a Kaplan-Meier integral and we have

where for all ,

Moreover, using the martingale decomposition of the Kaplan-Meier estimator [1, see for instance], we can rewrite as

Finally, the term tends to in probability as tends to infinity since (see Proposition 2.3.1 in [22]) and from the consistency of the Kaplan-Meier estimator. Finally, we obtain the following centered and i.i.d representation of :

The convergence in law follows from the central limit theorem.

Next, we compute the asymptotic variance, denoted , in the following way:

First,

by Proposition 2.3.1 in [22]. Second, using Theorem 2.4.4 in [11],

Third,

We then study the term. From the definition of and the Fubini theorem, we have

In addition, using the fact that and cannot jump at the same time, we have

We now take the conditional expectation with respect to for the first term, with respect to for the second term and we use the relations , in order to obtain the following result

This proves that . To conclude, we have shown that

Finally,

The consistency of the variance estimator follows from the consistency of the Kaplan-Meier integrals [22, see], the consistency of and the consistency of . ∎

References

- [1] Per Kragh Andersen, Ørnulf Borgan, Richard D. Gill and Niels Keiding “Statistical Models Based on Counting Processes”, Springer Series in Statistics New York, NY: Springer US, 1993 DOI: 10.1007/978-1-4612-4348-9

- [2] Per Kragh Andersen, Mette Gerster Hansen and John P. Klein “Regression Analysis of Restricted Mean Survival Time Based on Pseudo-Observations” In Lifetime Data Analysis 10.4, 2004, pp. 335–350 DOI: 10.1007/s10985-004-4771-0

- [3] Paul Blanche, Michael W. Kattan and Thomas A. Gerds “The c-index is not proper for the evaluation of $t$-year predicted risks” In Biostatistics 20.2, 2019, pp. 347–357 DOI: 10.1093/biostatistics/kxy006

- [4] Henrik Boström, Ulf Johansson and Anders Vesterberg “Predicting with Confidence from Survival Data” In Proceedings of the Eighth Symposium on Conformal and Probabilistic Prediction and Applications PMLR, 2019, pp. 123–141

- [5] Leo Breiman “Random Forests” In Machine Learning 45.1, 2001, pp. 5–32 DOI: 10.1023/A:1010933404324

- [6] Emmanuel Candès, Lihua Lei and Zhimei Ren “Conformalized survival analysis” In Journal of the Royal Statistical Society Series B: Statistical Methodology 85.1, 2023, pp. 24–45 DOI: 10.1093/jrsssb/qkac004

- [7] George H. Chen “Deep Kernel Survival Analysis and Subject-Specific Survival Time Prediction Intervals” In Proceedings of the 5th Machine Learning for Healthcare Conference PMLR, 2020, pp. 537–565 URL: https://proceedings.mlr.press/v126/chen20a.html

- [8] David R. Cox “Partial Likelihood” In Biometrika 62.2, 1975, pp. 269–276 DOI: 10.2307/2335362

- [9] Cyrus J. DiCiccio, Thomas J. DiCiccio and Joseph P. Romano “Exact tests via multiple data splitting” In Statistics & Probability Letters 166, 2020, pp. 108865 DOI: 10.1016/j.spl.2020.108865

- [10] Anne Eaton, Terry Therneau and Jennifer Le-Rademacher “Designing clinical trials with (restricted) mean survival time endpoint: Practical considerations” In Clinical Trials 17.3, 2020, pp. 285–294 DOI: 10.1177/1740774520905563

- [11] Thomas R. Fleming and David P. Harrington “Counting Processes and Survival Analysis”, Wiley Series in Probability and Statistics Hoboken, NJ, USA: John Wiley & Sons, Inc., 2005 DOI: 10.1002/9781118150672

- [12] Thomas A. Gerds, Michael W. Kattan, Martin Schumacher and Changhong Yu “Estimating a time-dependent concordance index for survival prediction models with covariate dependent censoring” In Statistics in Medicine 32.13, 2013, pp. 2173–2184 DOI: 10.1002/sim.5681

- [13] Thomas A. Gerds and Martin Schumacher “Consistent Estimation of the Expected Brier Score in General Survival Models with Right-Censored Event Times” In Biometrical Journal 48.6, 2006, pp. 1029–1040 DOI: 10.1002/bimj.200610301

- [14] Patrick J. Heagerty and Yingye Zheng “Survival Model Predictive Accuracy and ROC Curves” In Biometrics 61.1, 2005, pp. 92–105 DOI: 10.1111/j.0006-341X.2005.030814.x

- [15] Hemant Ishwaran, Udaya B. Kogalur, Eugene H. Blackstone and Michael S. Lauer “Random survival forests” In The Annals of Applied Statistics 2.3, 2008 DOI: 10.1214/08-AOAS169

- [16] Theodore Karrison “Restricted Mean Life With Adjustment for Covariates” In Journal of the American Statistical Association 82.400, 1987, pp. 1169–1176 DOI: 10.2307/2289396

- [17] Masahiro Kojima “Variable Selection using Inverse Survival Probability Weighting” arXiv, 2022 URL: http://arxiv.org/abs/2212.02109

- [18] Maxim S. Kovalev, Lev V. Utkin and Ernest M. Kasimov “SurvLIME: A method for explaining machine learning survival models” In Knowledge-Based Systems 203, 2020, pp. 106164 DOI: 10.1016/j.knosys.2020.106164

- [19] Mateusz Krzyziński, Mikołaj Spytek, Hubert Baniecki and Przemysław Biecek “SurvSHAP(t): Time-dependent explanations of machine learning survival models” In Knowledge-Based Systems 262, 2023, pp. 110234 DOI: 10.1016/j.knosys.2022.110234

- [20] Arun Kumar Kuchibhotla “Exchangeability, Conformal Prediction, and Rank Tests” arXiv, 2021 DOI: 10.48550/arXiv.2005.06095

- [21] Jing Lei, Max G’Sell, Alessandro Rinaldo, Ryan J. Tibshirani and Larry Wasserman “Distribution-Free Predictive Inference for Regression” In Journal of the American Statistical Association 113.523, 2018, pp. 1094–1111 DOI: 10.1080/01621459.2017.1307116

- [22] Olivier Lopez “Réduction de dimension en présence de données censurées”, 2007 URL: https://pastel.archives-ouvertes.fr/tel-00195261

- [23] Dariusz Majerek, Wioletta Nowak and Wies Ziba “Conditional strong law of large number” In International Journal of Pure and Applied Mathematics 20, 2005

- [24] M. Schumacher, G. Bastert, H. Bojar, K. Hübner, M. Olschewski, W. Sauerbrei, C. Schmoor, C. Beyerle, R. L. Neumann and H. F. Rauschecker “Randomized 2 x 2 trial evaluating hormonal treatment and the duration of chemotherapy in node-positive breast cancer patients. German Breast Cancer Study Group.” In Journal of Clinical Oncology 12.10, 1994, pp. 2086–2093 DOI: 10.1200/JCO.1994.12.10.2086

- [25] Jiaye Teng, Zeren Tan and Yang Yuan “T-SCI: A Two-Stage Conformal Inference Algorithm with Guaranteed Coverage for Cox-MLP” In Proceedings of the 38th International Conference on Machine Learning PMLR, 2021, pp. 10203–10213 URL: https://proceedings.mlr.press/v139/teng21a.html

- [26] Lu Tian, Lihui Zhao and L. J. Wei “Predicting the restricted mean event time with the subject’s baseline covariates in survival analysis” In Biostatistics 15.2, 2014, pp. 222–233 DOI: 10.1093/biostatistics/kxt050

- [27] Aad W. Van Der Vaart “Asymptotic statistics”, Cambridge series in statistical and probabilistic mathematics Cambridge, UK: Cambridge University Press, 1998

- [28] Vladimir Vovk, A. Gammerman and Glenn Shafer “Algorithmic learning in a random world” New York: Springer, 2005

- [29] Xin Wang and Douglas E. Schaubel “Modeling restricted mean survival time under general censoring mechanisms” In Lifetime Data Analysis 24.1, 2018, pp. 176–199 URL: http://link.springer.com/10.1007/s10985-017-9391-6

- [30] Lili Zhao “Deep neural networks for predicting restricted mean survival times” In Bioinformatics 36.24, 2021, pp. 5672–5677 DOI: 10.1093/bioinformatics/btaa1082

- [31] David M. Zucker “Restricted Mean Life with Covariates: Modification and Extension of a Useful Survival Analysis Method” In Journal of the American Statistical Association 93.442, 1998, pp. 702–709 DOI: 10.2307/2670120