Distributed Semi-Supervised Sparse Statistical Inference

Abstract

The debiased estimator is a crucial tool in statistical inference for high-dimensional model parameters. However, constructing such an estimator involves estimating the high-dimensional inverse Hessian matrix, incurring significant computational costs. This challenge becomes particularly acute in distributed setups, where traditional methods necessitate computing a debiased estimator on every machine. This becomes unwieldy, especially with a large number of machines. In this paper, we delve into semi-supervised sparse statistical inference in a distributed setup. An efficient multi-round distributed debiased estimator, which integrates both labeled and unlabelled data, is developed. We will show that the additional unlabeled data helps to improve the statistical rate of each round of iteration. Our approach offers tailored debiasing methods for -estimation and generalized linear models according to the specific form of the loss function. Our method also applies to a non-smooth loss like absolute deviation loss. Furthermore, our algorithm is computationally efficient since it requires only one estimation of a high-dimensional inverse covariance matrix. We demonstrate the effectiveness of our method by presenting simulation studies and real data applications that highlight the benefits of incorporating unlabeled data.

Keywords: Distributed learning; semi-supervised learning; debiased lasso; -estimation; generalized linear model

1 Introduction

High-dimensional models are prevalent in various scientific fields such as genomic analysis, image processing, signal processing, finance, and so on. However, traditional methods, such as maximum likelihood, least square regression, and principle component analysis break down due to the high dimensionality. To address this issue, new statistical methods and theories have been developed in high-dimensional statistics, which have played a critical role in advancing these fields. A common approach is to impose a sparsity structure on the data and model parameters. Many pioneering methods, such as regularization (Tibshirani, 1996), non-convex regularization (Fan and Li, 2001; Zhang, 2010b, a), iterative hard thresholding (Blumensath and Davies, 2009; Jain et al., 2014; Yuan et al., 2018) and debiasing techniques (Javanmard and Montanari, 2014; van de Geer et al., 2014; Zhang and Zhang, 2014; Cai et al., 2021) have been proposed to overcome these problems.

Upon entering the era of big data, modern datasets exhibit more complex structures and larger scales, which pose additional challenges for data analysis. For example, in internet companies and hospitals, data are often stored across multiple agents independently. However, direct data sharing may be prohibited due to privacy concerns, and communication between agents can be costly. As a result, distributed learning has emerged as a natural solution and has garnered significant attention in recent years. On the other hand, in some datasets, such as electronic health records and genetics data, the covariates are much more easily attainable than the labels. The need to utilize unlabeled data to improve the overall performance of statistical models naturally calls for research on semi-supervised learning.

In this paper, we aim to estimate the parameter defined by the following population risk minimization problem

| (1) |

in a distributed semi-supervised setup. This type of loss function encompasses a wide range of applications, such as Huber regression, logistic regression, quantile regression, and others. Specifically, we assume that the target parameter is sparse, meaning that the number of nonzero elements of , , is much less than the dimension . While there has been extensive research on problem (1) in both low dimensional and high dimensional scenarios (see, e.g., Javanmard and Montanari (2014); van de Geer et al. (2014); Zhang and Zhang (2014); Huang and Huo (2019); Battey et al. (2018); Jordan et al. (2019); Fan et al. (2023)), the statistical analysis in a distributed semi-supervised setup poses unique challenges and is scarce in the existing literature.

In the field of distributed learning, there is a vast literature investigating the trade-off between communication efficiency and statistical accuracy. Among these methods, the divide-and-conquer (DC) approach stands out for its simplicity and practicality. This method involves executing the algorithm in parallel and combining the local estimators through averaging. The DC approach has been widely applied to various problems such as quantile regression (Volgushev et al., 2019; Chen et al., 2019), kernel ridge regression (Zhang et al., 2015; Lin et al., 2017) and kernel density estimation (Li et al., 2013). Although these one-shot methods offer high communication efficiency, it faces stringent restriction on the number of machines to obtain a minimax convergence rate. To alleviate these constraints, many iterative algorithms, such as distributed approximate Newton method (Shamir et al., 2014; Zhang and Lin, 2015; Jordan et al., 2019; Fan et al., 2023), distributed primal-dual framework (Smith et al., 2017), local stochastic gradient descent (Stich, 2019), have been proposed. There are also some works studying the lower bound of communication complexity (Zhang et al., 2013; Arjevani and Shamir, 2015).

For high-dimensional distributed learning, naively averaging the penalized estimators would incur a large bias and would not improve over the local estimators. To address this issue, many works apply the divide-and-conquer method coupled with a well-known debiasing technique (Javanmard and Montanari, 2014; van de Geer et al., 2014; Zhang and Zhang, 2014; Lee et al., 2017; Zhao et al., 2020; Lian and Fan, 2018) to achieve better performance. The debiasing technique is particularly useful when conducting hypothesis testing and constructing a confidence interval for high-dimensional parameters (Lee et al., 2017; Battey et al., 2018; Liu et al., 2021). In the classical distributed debiased estimator, each machine constructs a local estimator , and computes the local debiased estimator

| (2) |

where is an estimator of the inverse Hessian matrix , and denotes the index set of the data on the -th machine (where ). Then it takes the average of these estimators as the final result. However, existing distributed debiased estimators are mostly one-shot, and unlike the single machine setup, a one-step debiasing approach may not be sufficient to eliminate the bias in a distributed setting, especially when the size of the local labeled sample is small, and the number of machines is large. Nevertheless, it is not straightforward to extend existing distributed debiased estimators to multi-round methods. Indeed, each debiasing step requires computing an estimator of the high-dimensional inverse Hessian matrix , which is computationally prohibitive. Naively extending the algorithm to a multi-round procedure would incur a significant computational burden, rendering it impractical in practice.

To address the aforementioned issues, we improve the classical distributed debiased estimators from two aspects: reducing the overall computational cost of the debiasing step and accelerating the per-round statistical rate. In traditional debiasing methods, the Hessian matrix varies with respect to the model parameter . In each round of iteration, we have to update the entire inverse Hessian matrix, which is computationally expensive. To reduce the overall computation burden of the multi-round debiasing approach, we propose debiasing methods for -estimations and generalized linear models, respectively. Specifically, for the -estimation problem, we propose to estimate the inverse Hessian matrix separately in two parts. For the generalized linear model, we weigh the gradients to eliminate the dependence of the Hessian matrix on the parameter . In both approaches, we only need to estimate one inverse covariance matrix in the first round, which greatly facilitates computation. Our approach can also handle non-smooth loss functions like absolute deviation loss. Additionally, instead of constructing the debiased estimator on every local machine as in (2), our method aggregates gradients and constructs one debiased estimator on the first machine, which further saves computational resources.

On the other hand, to improve the convergence rate in each round and reduce the number of communication rounds, we propose a semi-supervised debiased estimator. Specifically, we leverage the unlabeled data to estimate the inverse Hessian matrix, which can significantly reduce bias when the unlabeled sample size is much larger than the locally labeled sample size. Semi-supervised learning has recently gained much interest in the statistical community, and several articles have provided semi-supervised inference frameworks that focus on estimating the mean of the response variable in both low dimensional (Zhang et al., 2019) and high dimensional (Zhang and Bradic, 2021) scenarios. Additionally, in Chakrabortty and Cai (2018); Azriel et al. (2022); Deng et al. (2020), the authors considered semi-supervised inference for the miss-specified linear model in both low-dimensions and high-dimensions, while some works have studies inferring explained variance in high-dimensional linear regression (Cai and Guo, 2020) and evaluating the various prediction performance measures for the binary classifier (Gronsbell and Cai, 2018). For distributed SSL, Chang et al. (2017) studied kernel ridge regression and showed that the semi-supervised DC method benefits significantly from unlabeled data and allows more machines than the ordinary DC. Following this line of research, a bunch of works such as Lin and Zhou (2018); Guo et al. (2017, 2019); Hu and Zhou (2021) have been proposed. However, these works all focused on one-shot non-parametric learning. To the best of our knowledge, there is no work considering distributed semi-supervised learning in high dimensions.

In summary, our contribution is threefold:

-

•

Firstly, we propose a DIstributed Semi-Supervised Debiased (DISSD) estimator that utilizes more unlabeled data to estimate the inverse Hessian matrix. We show that the additional unlabeled data helps to reduce the local bias and enhance the accuracy. In this paper, we mainly consider one machine having unlabeled data, which differs from the work of Chang et al. (2017). Our result can be easily extended to cases where more than one machine has unlabeled data (see Remark 2).

-

•

Secondly, for the -estimation and generalized linear model, we propose two different debiasing techniques tailored to the specific form of the loss functions. Both approaches facilitate the use of unlabeled covariates information and help to reduce the computational cost in the multi-round debiasing step. Our method is much more computationally efficient than existing distributed debiased estimators like Lee et al. (2017); Battey et al. (2018); Zhao et al. (2020).

-

•

Lastly, simulation studies are carried out to demonstrate the necessity of multi-round debiasing in distributed learning, as well as the superiority of our semi-supervised method over the fully-supervised counterpart. We have numerically explored the impact of various hyperparameters on our model’s performance. Moreover, we have conducted a comparative analysis with existing methods, showcasing the advantages of our method both in terms of statistical accuracy and computational time.

To better illustrate the advantage of our proposed method, we have incorporated a table to succinctly summarize the detailed comparisons between our work and existing methodologies. The results can be found in Table 1 below.

| Method | Statistical accuracy | Communication complexity | Computational complexity | Statistical inference |

| DC (Battey et al., 2018) | Yes | |||

| Multi-round DC naive extending Battey et al. (2018) | Yes | |||

| CSL (Jordan et al., 2019) | No | |||

| CEASE (Fan et al., 2023) | No | |||

| DISSD (this work) | Yes | |||

Upon examination of the table, it becomes evident that our multi-round debiased estimator offers a notable reduction in computational burden when compared to the existing naive DC debiased estimator in Battey et al. (2018) (saves a factor of and respectively). It’s important to note that both Jordan et al. (2019) and Fan et al. (2023) primarily address -penalized loss functions, limiting their utility for statistical inference. To conduct statistical inference using the resultant estimators from these methods, one would need to perform one-step debiasing, incurring an additional computational overhead of . In contrast, the computational complexity of our approach has remainder term , which is comparatively smaller than these two methods, offering a savings factor of . Moreover, our method introduces a novel element by leveraging additional unlabeled data to expedite the distributed training process, which is a distinctive contribution to the literature. In summary, our methodology stands out by requiring the smallest total computational complexity while simultaneously delivering a statistically optimal estimator that facilitates statistical inference.

1.1 Paper Organization and Notations

The remainder of this paper is organized as follows. In Section 2, we introduce the basic idea of our distributed debiased estimator starting from linear regression. In Section 3 and Section 4, we propose debiasing methods for -estimation and generalized linear model respectively. Theoretical results are presented in each section to demonstrate the acceleration effect of the semi-supervised methods. The simulation studies are given in Section 5 to show how each factor affects the performance. Finally, we provide concluding remarks in Section 6. All proofs of the theory are relegated to the Appendix.

For a vector , denote , and . Moreover, we use as the support of the vector . For a matrix , define as various matrix norms, and as the largest and smallest eigenvalues of respectively. For two sequences , we say if and only if and hold at the same time. Lastly, the generic constants are assumed to be independent of , and .

Throughout the paper we assume that the labeled pairs are evenly stored in machines . We denote as the index set of labeled data on the -th machine. Moreover, on the first machine , there are additional unlabeled covariates , whose indices are collected in the set . Therefore there are , , and . We call the first machine as the master machine.

2 Distributed Semi-Supervised Debiased Estimator for Sparse Linear Regression

In this section, we consider the distributed sparse linear regression with square loss as a toy example. We assume that the covariate and the label are generated from the following linear model

| (3) |

Throughout this section, we take the loss function as . Then the empirical loss function on the -th machine becomes

| (4) |

To conduct distributed learning, the classical way is to take the average of the debiased lasso estimator, which has been studied in Lee et al. (2017); Battey et al. (2018). More precisely, let be the local Lasso estimator using the data on the -th machine, and be the local estimator of the precision matrix , then the one-shot debiased estimator is constructed as

| (5) |

where . While this method has been proven to enjoy a better convergence rate, there is still much room for improvement in our setting. On the one hand, it requires each machine to estimate the inverse covariance matrix , which may waste much computational effort. On the other hand, we hope to incorporate the unlabeled data into the estimator.

To address these difficulties, we propose an alternative estimator as follows. We first construct an initial estimator and send it to each machine, then each machine computes the local gradient and sends to the master machine. Next, we construct the following estimator

| (6) |

where denotes the consistent estimator of the precision matrix using all the covariates ’s on the master machine . Compared with (5), our method only requires estimating one inverse covariance matrix, therefore saving much computational cost. Moreover, it makes use of all covariates information on . As will be shown in Theorem 1, the semi-supervised estimator constructed in (6) has a better convergence rate than its fully supervised counterpart.

For the estimation of in high dimension, there are many works such as Meinshausen and Bühlmann (2006); Cai et al. (2011); Yuan (2010); Liu and Luo (2015). In this paper, we utilize the method proposed in Liu and Luo (2015), which suggests to forming the estimator row by row. More specifically, the -th row is given by minimizing the objective function

| (7) |

where denotes the unit vector on the -th coordinate, and is the corresponding regularization parameter. The problem (7) can be solved by many efficient algorithms like FISTA (Beck and Teboulle, 2009) and ADMM (Boyd et al., 2011), which makes our method more effective.

Remark 1.

Newton’s method has been widely employed in the domain of distributed learning, spanning applications in low dimensional learning (Shamir et al., 2014; Huang and Huo, 2019; Jordan et al., 2019; Fan et al., 2018), sparse learning (Wang et al., 2017), and kernel learning (Zhou, 2020). Our proposed method resembles the distributed approximate Newton method and is tailored for the high-dimensional debiased estimator, which is unexplored in the literature. Consequently, our work makes a valuable contribution to distributed high-dimension statistical inference. Further, the existing body of work in this area has predominantly centered on the fully-supervised setup, with limited exploration of semi-supervised scenarios. In this paper, we advance this research by introducing a substantial quantity of unlabeled data to enhance the estimation of Hessian information. Our findings provide theoretical evidence that the incorporation of unlabeled data effectively accelerates the distributed training process. It is conceivable that the methodologies elucidated in the aforementioned works can be readily extended to the semi-supervised framework, thereby yielding similar acceleration benefits.

Remark 2.

By leveraging the idea of Lee et al. (2017), our method can be easily extended to cases where more than one machine contains unlabeled data. Denote as the index of machines containing unlabeled data. Then we can let the -th machine (where ) to estimate rows of . The master machine sends the averaged gradient to each , where . Suppose the -th machine estimates the -th row, then the -th coordinate can be estimated as

where is given by (7) using the covariates on . This helps to further reduce the computational burden as the estimation of ’s is processed in parallel.

In this section, we have presented the fundamental concept of our approach, which distinguishes itself from the existing distributed debiased estimators in two aspects. Firstly, we aggregate the gradients from all local machines, instead of the local estimators, and only estimate one high-dimensional inverse Hessian matrix; Secondly, we employ more unlabeled covariates to estimate the Hessian matrix to improve per-round accuracy. It should be noted that the Hessian matrix of the square loss is uncomplicated since it is independent of both the parameter and the label . However, in the subsequent sections, we discuss -estimation and generalized linear model, which have more complex forms. To eliminate the dependence of the Hessian matrix on other parameters, we present two customized techniques for the specific forms of the loss functions, which will be elaborated on in the following sections.

3 Distributed Semi-Supervised Debiased Estimator for Sparse -Estimation

In this section, we consider the distributed semi-supervised learning for a broader class of sparse -estimation problems. In this model, the data are assumed to be generated from the linear model (3). Based on different assumptions on the noise , we should choose different loss functions . In general, the empirical loss function on the -th machine is

| (8) |

The situation becomes different from linear regression. To conduct the debiasing approach, a key step is to estimate the inverse of the population Hessian matrix, which is . Notice that contains the label information , therefore we cannot directly use the unlabeled covariates in the debiasing step.

3.1 Separated Estimation of Inverse Hessian

To address this issue, we observe that when is close to the true parameter , the corresponding Hessian matrix satisfies

| (9) |

which is the multiplication of a scalar value and a matrix only involving the covariate . Therefore we can estimate the terms and separately. More specifically, given a consistent estimator of , we can construct the following distributed semi-supervised debiased estimator

| (10) |

The construction of will be presented in the next part. Since the debiased estimator is dense, it does not have -norm and -norm consistency. To further encourage sparsity, we propose the thresholded estimator where each coordinate is defined by

If we repeatedly take back to the above procedure, we can obtain an iterative algorithm, which is presented in Algorithm 1. It is worth noting that, by (10) we know the estimator is unchanged throughout iterations. Therefore, we only need to estimate one time at the beginning of the procedure and keep it in the memory. At each iteration, it is enough to update the scalar and the vector , which makes our algorithm much efficient.

Input: Labeled data on worker machine for , and unlabeled data on , the regularization parameter , the thresholding level , the number of iterations .

Output: The final estimator .

For the choice of the initial parameter , when the local sample size is sufficiently large, we can adopt the approach of minimizing the -penalized fully supervised loss as formulated below:

| (11) |

This optimization is carried out on the master machine . If the local labeled sample size is too small such that the estimator in (11) does not fulfill the conditions on the initial rate in Theorem 1 and 2, one can apply the early-stopped distributed proximal gradient descent to obtain a better initial estimator.

Construction of

In (9), we assume the loss function is twice differentiable for the ease of presentation. Indeed, we allow to be nonsmooth so that our theory embraces the case of median regression (see Example 2). To achieve this goal, we first define the function . Then we know

Therefore, to estimate , we apply the same method as in Section 2.3 of Tu et al. (2023). More precisely, assume has finitely many distinct discontinuous points , and it is differentiable outside of these points. We denote

as the function gap at , then can be explicitly written as

| (12) |

where denotes the second-order derivative of , which can be defined almost everywhere on . Here denotes the density function of the noise . Given a kernel function , a bandwidth and a consistent estimator , on each local machine , can be locally estimated by

| (13) |

Then the worker machine sends the local estimator to the master machine , and we take average over these local estimators . In the -th iteration, we can estimate in the same fashion.

Example 1.

(Huber regression) Huber loss function is defined as

where is some pre-specified robustification parameter. In this case, the first-order derivative is continuous, and we can compute that . Therefore , and from (13) we know each local estimator can be constructed by

Example 2.

(Median regression) In the median regression problem, the loss function is defined as Therefore its derivative is discontinuous at point . We can easily obtain that (for the discontinuous point , we can directly define ), and . Therefore from (12) we have . By equation (13), we can estimate by

on each local machine .

Remark 3.

Debiased estimators for linear models have been extensively studied in the literature (Javanmard and Montanari, 2014; Zhang and Zhang, 2014; Cai et al., 2021). However, for general loss functions, existing works typically recommend directly estimating the inverse Hessian matrix (van de Geer et al., 2014; Battey et al., 2018; Zhao et al., 2020), which varies with the parameter . This approach hurdles the development of multi-round debiasing estimators, which are necessary in a distributed setup. Separated Hessian estimation has been introduced in the context of quantile regression (Zhao et al., 2014; Chen et al., 2020), and extended to general loss functions in Tu et al. (2023). However, these previous works have focused primarily on transforming the loss function to a square loss to overcome the computational bottlenecks arising from the non-smoothness of the loss function, which differs from our motivation.

3.2 Theoretical Results of for -Estimation

In this section, we provide the theoretical results for the proposed methods. We first present several technical assumptions as follows. For ease of presentation, we denote where is a random variable and is some fixed number.

Condition A1.

There exists some constants such that

| (14) |

where and .

Condition A2.

The loss function satisfies . Furthermore, there exist constants such that, for every pair of , there is

Condition A3.

There exists a constant such that the noise has probability density function which satisfies

Moreover, there exists a constant such that .

Condition A4.

The kernel function satisfies and for . Moreover, is Lipschitz continuous satisfying holds for arbitrary .

Condition AS.

(Smooth loss) There exists a constant such that, for any two points , there is

Condition ANS.

(Non-smooth loss) There exist constants such that, for every pair of , there is

Condition A1 is some regularity conditions on the covariate . In particular, we assume the inverse covariance matrix is -sparse (where ), a condition frequently utilized as an alternative to the strict sparse condition (see, e.g., Bickel and Levina (2008); Cai et al. (2011); Raskutti et al. (2011)). Condition A2 assumes the continuity of the second-order derivative in a weak sense. This condition also appears in Tu et al. (2023). Condition A3 and A4 assumes the probability density function and to be regular. Clearly, they are used only when the loss function is not second-order differentiable. We impose different conditions for smooth loss (Condition AS) and non-smooth loss (Condition ANS). As will be seen in Appendix 7.4, the Huber regression model in Example 1 and the median regression model in Example 2 satisfy these conditions given the covariate admits sub-gaussian property.

Given the above conditions, we can prove the following convergence rate for both smooth and non-smooth losses.

Theorem 1.

Theorem 2.

As we can see, the convergence rate of for smooth loss and non-smooth loss only differs in the second term in (15) and (16) respectively. When , the second term is always dominated by the first term, therefore could be eliminated. From the third term of (15) and (16), we can see that the convergence rate is refined by a factor , which is better than in the fully supervised case. The thresholding parameter is suggested to have the same order as , which depends on the unknown initial rate . In practice, we can use by letting if is obtained from (11). The constant should be tuned carefully. As a corollary, we can show the convergence rate of the multi-round estimator .

Corollary 1.

In order to attain a near-optimal convergence rate , we require the last two terms in (17) to be dominated by the first term. Given that the third term converges at a super-exponential rate, our primary concern centers on the second term. More specifically, we seek conditions under which holds. By taking logarithm to both sides and rearranging the terms, we have that

| (18) |

In the fully-supervised case where , the required number of iterations should satisfy (18) with replaced by . Consequently, when significantly exceeds , our supervised algorithm demands notably fewer iterations to achieve the near-optimal rate. This observation is also validated through our experimental results (see Section 5).

Next, we prove the asymptotic normality result for our estimator.

Theorem 3.

Under assumptions in Corollary 1, and the iteration number is large enough such that . Further assume the rate constraints , then we have that

where

As we can see, to guarantee asymptotic normality, the sparsity level should satisfy

, which is looser than the fully supervised case (where

).

4 Distributed Semi-Supervised Debiased Estimator for Sparse GLM

In this section, we consider distributed semi-supervised learning for generalized linear models (GLM). In a GLM, given a function , the observations are generated according to the following conditional probability function

| (19) |

where and are some scale constants, and is the true model parameter. The corresponding empirical loss function on the -th machine is

| (20) |

We note that the population Hessian matrix at ,

| (21) |

does not contain the label . Therefore, to construct a DSS debiased estimator, a direct way is to use all covariate information to estimate the inverse Hessian matrix (21). However, the Hessian matrix is dependent on the model parameter . When performing a multi-round debiasing approach, we need to update the parameter and estimate the inverse Hessian matrix recursively, which is computationally expensive.

4.1 Accelerated Debiasing by Weighted Gradients

To alleviate the computational burden and accelerate the multi-round debiasing algorithm, we propose a gradient-weighting approach as follows. To motivate our construction, we first consider the generic form of the one-step debiased estimator. More precisely, for each coordinate , there is

where is an initial estimator, ’s are data-dependent gradient weight, and ’s are the projection directions. Applying Taylor expansion for at , we can decompose the error of as follows

| (22) |

where , for some lying between and , and is the canonical basis of . From this decomposition, to conduct statistical inference for the debiased estimator, we require the second term dominated by the first term in (22). Therefore, the projection direction should approximate the -th column of the inverse of the matrix . However, to construct for every coordinate, we should solve high-dimensional optimization problems successively, which incurs heavy computational overhead. To reduce the computational burden, we can take so that the matrix is independent of the parameter .

In summary, given an initial parameter , we compute the following weighted gradient

| (23) |

and construct the distributed semi-supervised debiased estimator

| (24) |

Compared with directly estimate the inverse of in (21), this approach only estimate the inverse covariance matrix , which is independent of the parameter . Therefore we only need to estimate for one time, which saves much computational power when performing multi-round algorithm.

To obtain a sparse estimator, we threshold each coordinate and get where

The iterative algorithm is presented in Algorithm 2.

Input: Labeled data on worker machine for , and unlabeled data on , the regularization parameter , the thresholding level , the number of iterations .

Output: The final estimator .

Similarly to the approach detailed in Algorithm 1, the choice of the initial parameter can be made by minimizing the local -penalized loss as in (11), or through the implementation of early-stopped proximal gradient descent. The decision between these methods is contingent upon the specific local labeled sample size.

Example 3.

(Logistic regression) In the logistic regression model, we generate the labels from the following distribution

| (25) |

Then the function is defined as

We can readily compute that and .

Remark 4.

In this section, we have demonstrated the significance of the gradient-weighting technique in reducing the computational cost of implementing the multi-round debiasing approach. The gradient-weighting technique has been applied in contemporary works for various purposes, such as simultaneous testing (Ma et al., 2021), case probability inference (Guo et al., 2021), genetic relatedness inference (Ma et al., 2022), and confidence interval construction (T. Tony Cai and Ma, 2023) for logistic regression models. Different weights were proposed for different applications. However, these studies primarily focus on a single-machine setup, and the rationale for weighting the gradient differs from ours. Furthermore, while all aforementioned works only consider logistic models, our method extends to a broader class of generalized linear models.

4.2 Theoretical Results of for GLM

In this section, we provide the theories of for GLM. We first list some technical conditions as follows.

Condition B1.

There exists some constants such that

| (26) |

where and .

Condition B2.

There exists some constants such that

Condition B3.

The function is three-time differentiable, and there exists a uniform constant such that

Condition B4.

With probability not less than , there holds for () and some small constant .

Condition B1 is the same as Condition A1 in Section 3.2. Condition B2 assumes subgaussianity of the gradient . In Condition B3, we assume the function to be smooth with bounded derivatives. Condition B4 requires to be bounded for all with high probability, which is a common assumption in the literature. As will be seen in Appendix 7.4, the logistic regression model in Example 3 satisfies these conditions given the covariate is uniformly bounded.

With the above conditions, we can prove the following convergence rate.

Theorem 4.

We can observe that the convergence rate of for GLM is similar to that of M-estimator in Theorem 1, except for the last term. More specifically, the last term of GLM has an additional factor , which is caused by the weighting procedure. Compared with Theorem 1 and 2, the theory for GLM requires more stringent conditions on the initial rate , which can be regarded as the price of weighting the gradients. Next, we present the convergence rate of the multi-round estimator .

Corollary 2.

Similarly as in Corollary 1, achieving a near-optimal statistical rate entails the dominance of the first term over the second term in (28). Consequently, the number of iterations required, denoted as , should align with the conditions established in (18). Next, we prove the asymptotic normality result for our estimator for GLM.

Theorem 5.

Under assumptions in Corollary 2, and the iteration number is large enough such that . Further assume the rate constraints , , then we have that

where

Compared with Theorem 3, we have a more strict constraint on the sparsity level, namely, . This is also caused by the gradient-weighting technique.

5 Simulation Study

In the empirical analysis, we conduct two classes of experiments to demonstrate the effectiveness of our method. The first part examines our proposed method on synthetic data. The latter is an application to the corresponding sparse linear regression task.

5.1 Experiments on the Synthetic Data

In this section, we show the performance of the distributed semi-supervised debiased estimator on the synthetic dataset.

Parameter Settings.

Throughout the experiments, we fix dimension and the true coefficient

We fix the sparsity level to be , unless specified otherwise. The covariate is sampled from , where is a block diagonal matrix whose block size is and each block has off-diagonal entries equal to and diagonal . We repeat 100 independent simulations and report the averaged estimation error and the corresponding standard error.

To illustrate the performance of our method, we mainly compare six methods

-

•

Local Lasso: Solve the Lasso problem using only the data on ;

-

•

Pooled Lasso: Collect all data together and solve the Lasso problem;

- •

-

•

CSL: Communication-efficient surrogate likelihood framework proposed in Jordan et al. (2019), which solves

(29) in each iteration.

Several other distributed algorithms have been proposed for high-dimensional learning, including CEASE from Fan et al. (2023) and Debias-DC from Battey et al. (2018). However, due to the extensive processing time these methods require and the lack of substantial improvement in statistical error, we have opted not to include a comparison with them in our synthetic data experiments. Instead, we conduct a thorough comparative analysis using a real dataset.

5.1.1 Huber Regression

In the Huber regression problem, we generate the noise from the mixture of normal distributions . More precisely, with probability , the value of is distributed according to and is otherwise drawn from a distribution. For the choice of robustification parameter , we follow the classical literature (Huber, 2004) and take . In Table 2, we maintain a fixed local labeled sample size of and a dimension of , while varying the number of machines in and adjusting the size of the unlabeled sample size within . The reported results include the -error and -score for both 1-Step DISSD and 5-Step DISSD. The table clearly demonstrates the consistent superiority of the semi-supervised estimator over its fully supervised counterpart. Additionally, the error diminishes with increasing unlabeled sample size, highlighting the positive impact of the larger unlabeled dataset. Furthermore, the multi-round method consistently diminishes estimation error.

| 1-Step DISSD | 5-Step DISSD | ||||

| -error | -score | -error | -score | ||

| 100 | 1.227(0.061) | 0.705(0.008) | 0.363(0.093) | 0.788(0.040) | |

| 20 | 250 | 1.025(0.053) | 0.697(0.006) | 0.287(0.047) | 0.773(0.033) |

| 550 | 0.919(0.049) | 0.689(0.003) | 0.315(0.047) | 0.750(0.020) | |

| 100 | 1.155(0.061) | 0.836(0.043) | 0.204(0.056) | 0.987(0.023) | |

| 50 | 250 | 0.888(0.056) | 0.801(0.031) | 0.077(0.023) | 0.993(0.018) |

| 550 | 0.678(0.049) | 0.757(0.019) | 0.064(0.020) | 0.985(0.025) | |

| 100 | 1.149(0.063) | 0.949(0.045) | 0.196(0.060) | 0.994(0.017) | |

| 100 | 250 | 0.870(0.057) | 0.961(0.037) | 0.060(0.018) | 1.000(0.000) |

| 550 | 0.633(0.047) | 0.927(0.040) | 0.039(0.010) | 1.000(0.000) | |

In Table 3, we maintain a fixed labeled sample size of , set the unlabeled sample size to be , and keep the number of machines constant at . We then vary the dimension across and adjust the sparsity level within . The results clearly demonstrate that both larger values of and correspond to increased statistical errors and a decline in the -score. This aligns with our theoretical expectations outlined in Corollary 1.

| 1-Step DISSD | 5-Step DISSD | ||||

| -error | -score | -error | -score | ||

| 5 | 0.427(0.049) | 1.000(0.000) | 0.027(0.009) | 1.000(0.000) | |

| 200 | 10 | 0.580(0.053) | 0.965(0.031) | 0.037(0.011) | 1.000(0.000) |

| 20 | 0.847(0.058) | 0.740(0.009) | 0.078(0.015) | 0.935(0.031) | |

| 5 | 0.459(0.046) | 1.000(0.000) | 0.025(0.009) | 1.000(0.000) | |

| 400 | 10 | 0.636(0.051) | 0.954(0.036) | 0.039(0.012) | 1.000(0.000) |

| 20 | 0.932(0.055) | 0.708(0.004) | 0.098(0.017) | 0.889(0.033) | |

| 5 | 0.456(0.051) | 1.000(0.000) | 0.028(0.012) | 1.000(0.000) | |

| 600 | 10 | 0.623(0.052) | 0.922(0.045) | 0.039(0.010) | 1.000(0.000) |

| 20 | 0.966(0.049) | 0.695(0.002) | 0.113(0.017) | 0.858(0.029) | |

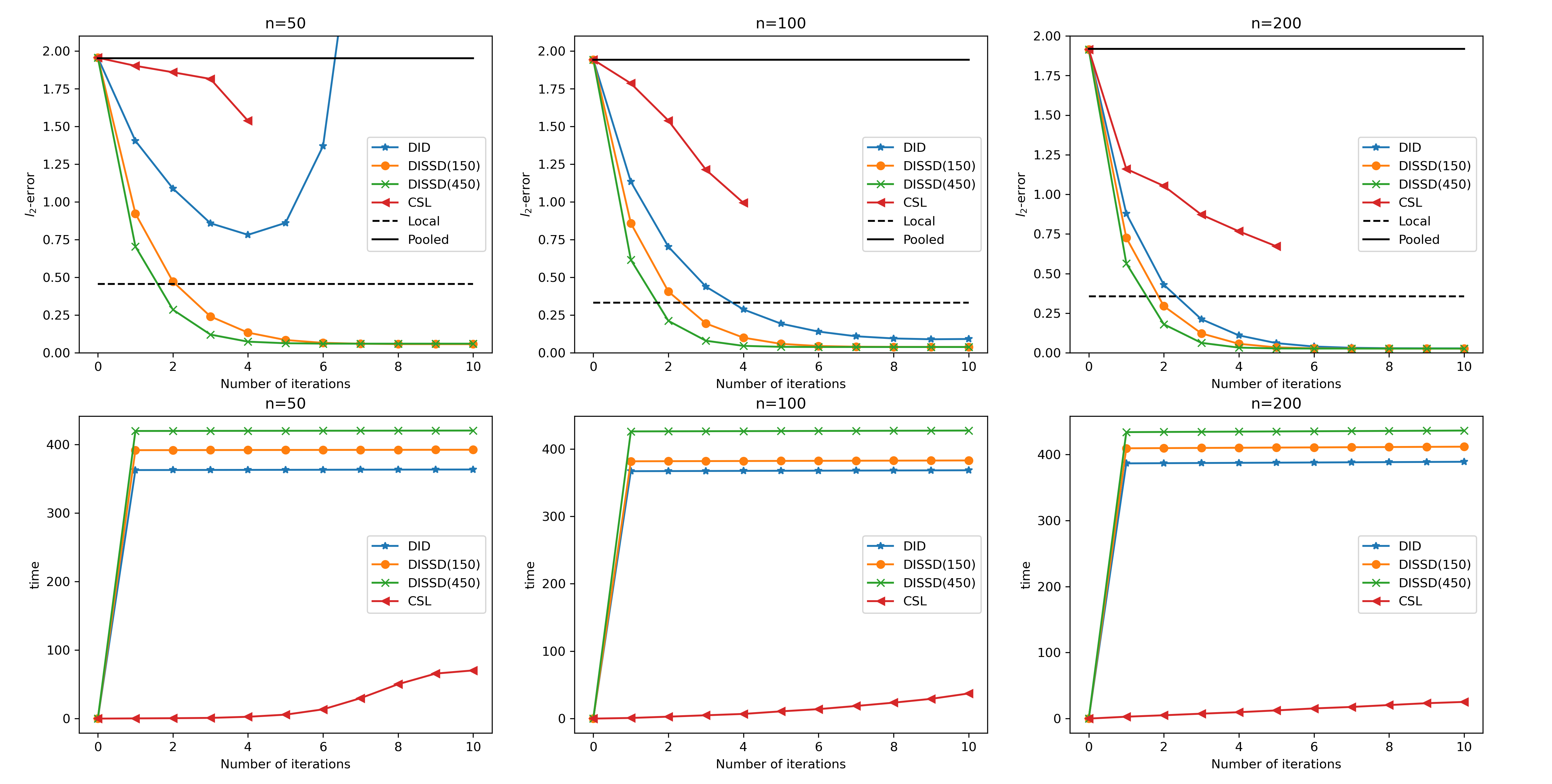

In Figure 1, the dimension is set at , and we vary the local labeled sample size among , while adjusting the unlabeled sample size in . The figure presents the -error and processing time for these methods. It is evident from the figure that the inclusion of unlabeled data significantly contributes to error reduction. Particularly noteworthy is the observation that when the local labeled sample size is too small, the fully supervised distributed debiased estimator may diverge. It is clear that our DISSD method outperforms the CSL method in terms of statistical accuracy. Specifically, each step of CSL requires approximately ten times the processing time of DISSD (after computing the inverse Hessian matrix). Additionally, CSL necessitates the tuning of the parameter in (29) at each step, further augmenting its runtime.

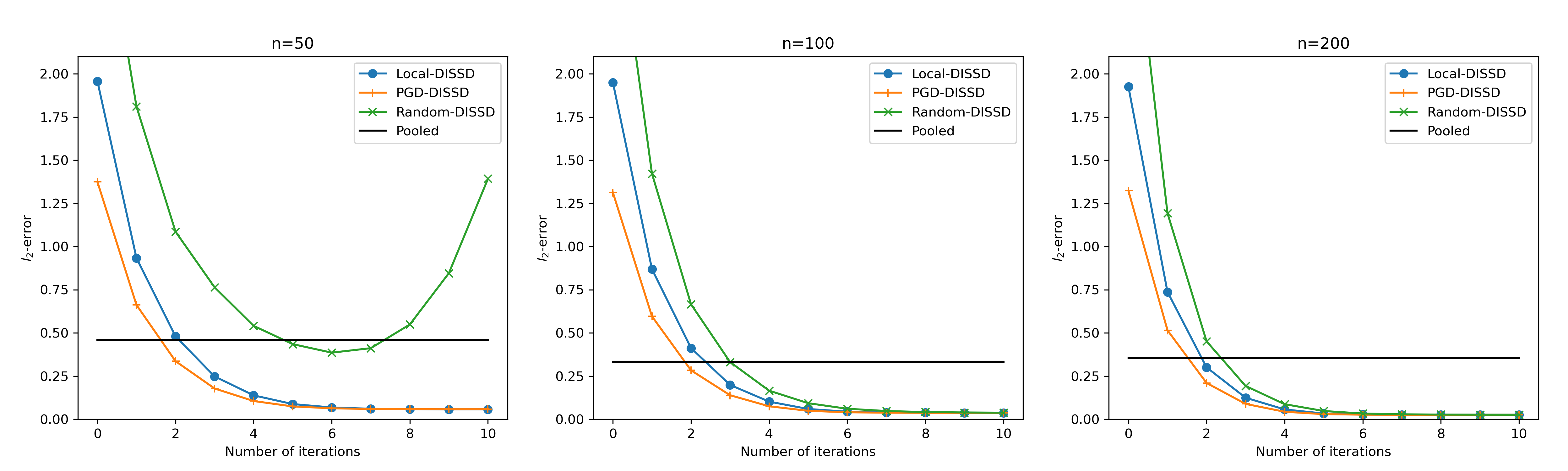

In Figure 2, we investigate the efficacy of our method under three distinct initializations: local estimator, random initialization, and 10-round distributed proximal gradient descent (PGD). The dimension is set at , and we vary the local labeled sample size among , while taking the unlabeled sample size . The figure presents the -error for these methods. The results reveal a clear trend: when the local labeled sample size is relatively large, all three initializations in the DISSD method yield consistent estimators. However, in scenarios where the local labeled sample size is limited, DISSD with random initialization exhibits divergence as the iteration number increases. Notably, the early-stopped distributed proximal gradient descent outperforms other methods, thereby expediting the training process. It is essential to note that while PGD provides superior performance, it necessitates additional communication compared to the local estimator. Consequently, the choice of initialization should consider both statistical accuracy and communication constraints. In cases where communication costs are a concern, employing the local estimator for initialization is a prudent choice.

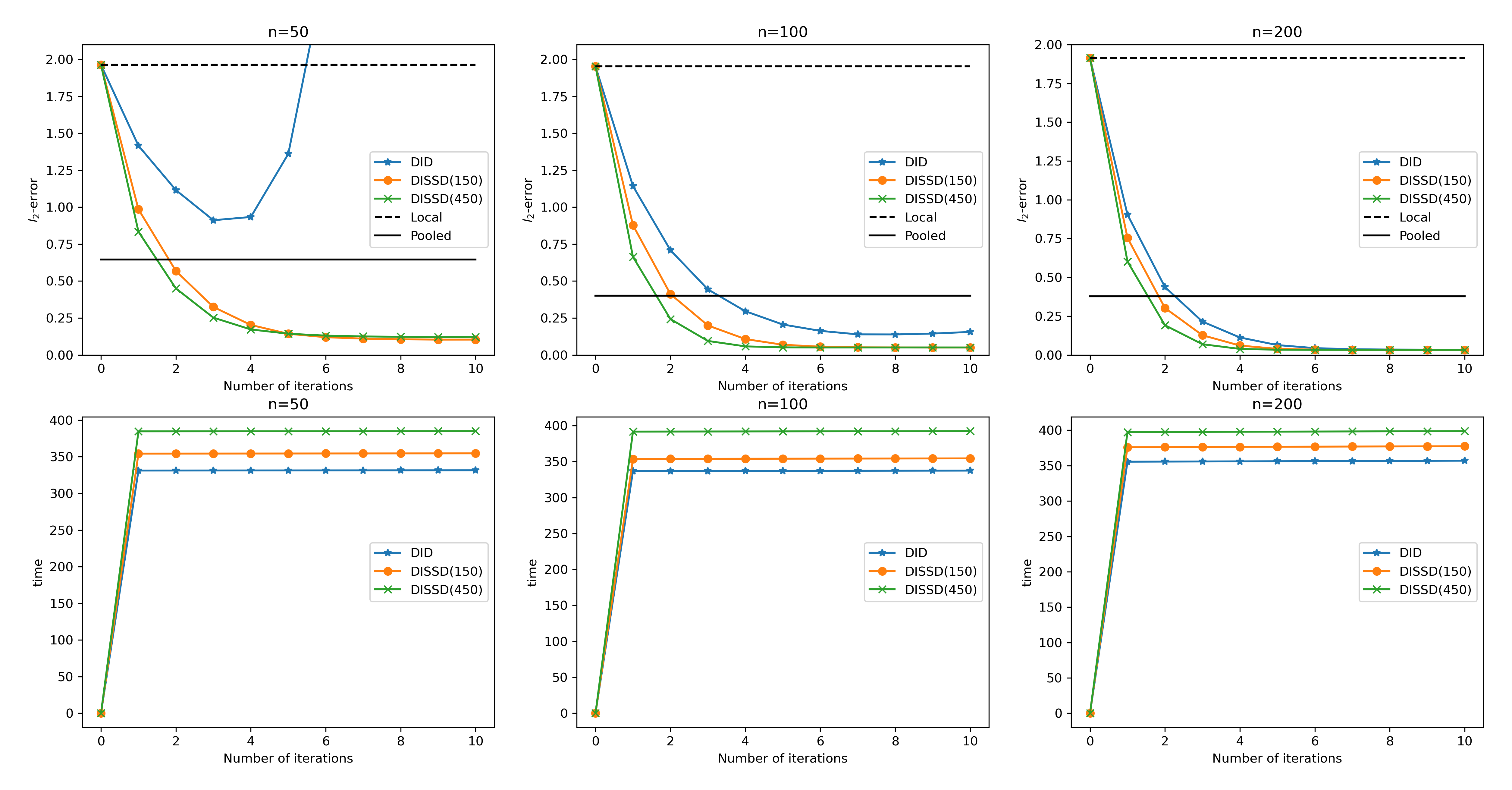

5.1.2 Median Regression

In the problem of median regression, we generate the noises from standard Cauchy distribution . We chose the kernel function as biweight kernel function, which can be formulated as

As for the bandwidth , we uniformly take . The results are shown in Table 4, Table 5 and Figure 3. In Figure 3, we exclude CSL from the comparison due to its original theory, which does not extend to non-smooth loss functions such as absolute deviation loss. Similar phenomena to the Huber regression models can be observed from the simulation results. In Table 4, we observe that the 1-Step DISSD method exhibits a decreasing -error with the increase in the unlabeled sample size , aligning with our theoretical findings in Corollary 1. However, an interesting trend emerges with the 5-step DISSD method when the number of machines is relatively small. In this scenario, the -error when is slightly larger than that when . We suspect that this phenomenon arises due to a larger unlabeled sample size introducing a greater bias in the smaller order terms.

| 1-Step DISSD | 5-Step DISSD | ||||

| -error | -score | -error | -score | ||

| 100 | 1.357(0.077) | 0.687(0.009) | 3.598(15.238) | 0.685(0.013) | |

| 20 | 250 | 1.241(0.078) | 0.684(0.007) | 1.203(0.816) | 0.684(0.009) |

| 550 | 1.215(0.115) | 0.681(0.005) | 1.505(0.931) | 0.679(0.005) | |

| 100 | 1.183(0.090) | 0.738(0.033) | 0.272(0.109) | 0.888(0.070) | |

| 50 | 250 | 0.966(0.085) | 0.721(0.025) | 0.148(0.061) | 0.895(0.055) |

| 550 | 0.825(0.071) | 0.705(0.017) | 0.153(0.047) | 0.867(0.055) | |

| 100 | 1.144(0.085) | 0.859(0.053) | 0.201(0.072) | 0.994(0.020) | |

| 100 | 250 | 0.885(0.091) | 0.836(0.055) | 0.070(0.023) | 0.997(0.012) |

| 550 | 0.671(0.091) | 0.786(0.045) | 0.052(0.015) | 0.996(0.013) | |

| 1-Step DISSD | 5-Step DISSD | ||||

| -error | -score | -error | -score | ||

| 5 | 0.449(0.094) | 0.998(0.016) | 0.033(0.012) | 1.000(0.000) | |

| 200 | 10 | 0.629(0.110) | 0.860(0.057) | 0.049(0.014) | 0.998(0.009) |

| 20 | 0.875(0.150) | 0.721(0.007) | 0.142(0.021) | 0.834(0.028) | |

| 5 | 0.459(0.093) | 0.998(0.016) | 0.033(0.012) | 1.000(0.000) | |

| 400 | 10 | 0.651(0.104) | 0.799(0.051) | 0.052(0.016) | 0.998(0.010) |

| 20 | 0.992(0.136) | 0.695(0.004) | 0.193(0.024) | 0.774(0.018) | |

| 5 | 0.471(0.090) | 0.996(0.020) | 0.035(0.012) | 1.000(0.000) | |

| 600 | 10 | 0.673(0.095) | 0.771(0.042) | 0.052(0.019) | 0.995(0.016) |

| 20 | 1.069(0.095) | 0.687(0.002) | 0.248(0.022) | 0.740(0.011) | |

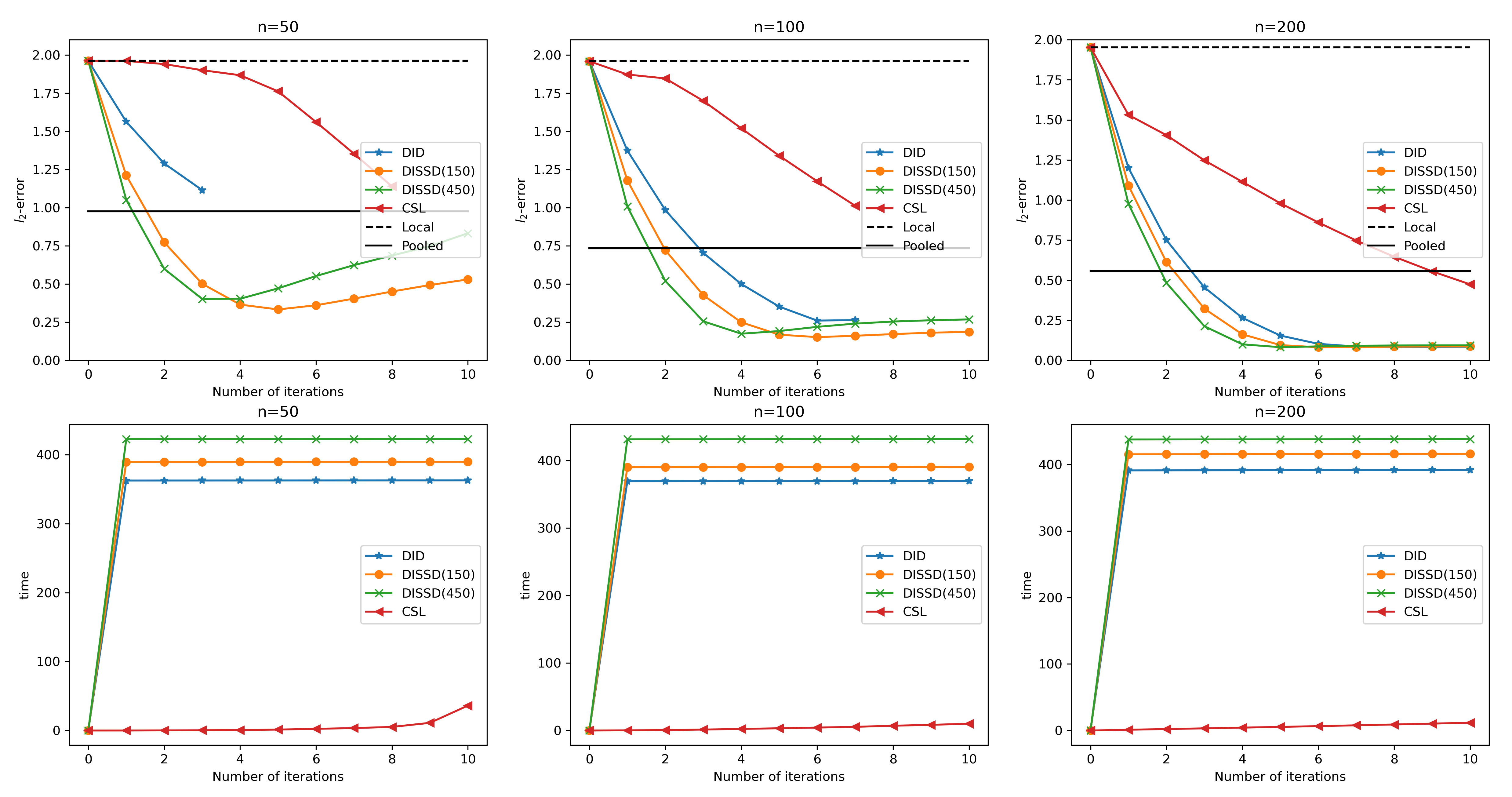

5.1.3 Logistic Regression

In the logistic regression model, we generate the labels according to the distribution in (25). The detailed comparison of these approaches is given in Table 6, Table 7, and Figure 4.

| 1-Step DISSD | 5-Step DISSD | ||||

| -error | -score | -error | -score | ||

| 100 | 1.416(0.054) | 0.713(0.011) | 0.896(0.300) | 0.694(0.007) | |

| 20 | 250 | 1.249(0.046) | 0.704(0.007) | 1.187(0.140) | 0.683(0.003) |

| 550 | 1.146(0.041) | 0.694(0.004) | 2.196(1.234) | 0.676(0.003) | |

| 100 | 1.380(0.054) | 0.843(0.049) | 0.401(0.071) | 0.831(0.042) | |

| 50 | 250 | 1.180(0.044) | 0.842(0.041) | 0.349(0.046) | 0.753(0.020) |

| 550 | 1.025(0.040) | 0.792(0.028) | 0.515(0.056) | 0.710(0.008) | |

| 100 | 1.375(0.054) | 0.907(0.049) | 0.354(0.075) | 0.958(0.033) | |

| 100 | 250 | 1.170(0.041) | 0.961(0.035) | 0.162(0.039) | 0.932(0.042) |

| 550 | 1.005(0.037) | 0.958(0.035) | 0.189(0.035) | 0.835(0.037) | |

| 1-Step DISSD | 5-Step DISSD | ||||

| -error | -score | -error | -score | ||

| 5 | 0.652(0.042) | 0.986(0.037) | 0.057(0.024) | 1.000(0.000) | |

| 200 | 10 | 0.991(0.038) | 0.965(0.031) | 0.149(0.032) | 0.897(0.043) |

| 20 | 1.559(0.032) | 0.796(0.018) | 0.386(0.034) | 0.731(0.008) | |

| 5 | 0.678(0.040) | 0.988(0.034) | 0.054(0.021) | 1.000(0.000) | |

| 400 | 10 | 1.010(0.036) | 0.961(0.033) | 0.171(0.031) | 0.856(0.036) |

| 20 | 1.600(0.030) | 0.753(0.011) | 0.500(0.036) | 0.704(0.003) | |

| 5 | 0.680(0.040) | 0.984(0.039) | 0.052(0.021) | 1.000(0.000) | |

| 600 | 10 | 1.021(0.037) | 0.951(0.037) | 0.201(0.034) | 0.822(0.038) |

| 20 | 1.604(0.031) | 0.727(0.009) | 0.617(0.038) | 0.693(0.002) | |

We can observe similar trends as in the former simulation results, that the semi-supervised estimator always outperforms the fully supervised counterpart. In Table 6 and Figure 4, we find that a larger unlabeled sample size plays a positive role in accelerating the convergence in the early-stage iterations, corroborating the findings in Corollary 2. However, an intriguing observation surfaces when either the local sample size or the number of machines is small: a larger unlabeled sample size adversely affects the statistical error in the post-stage iterations. This phenomenon challenges our current theoretical understanding and may necessitate the development of additional theoretical techniques for a comprehensive explanation.

5.2 Application to Real-World Benchmarks

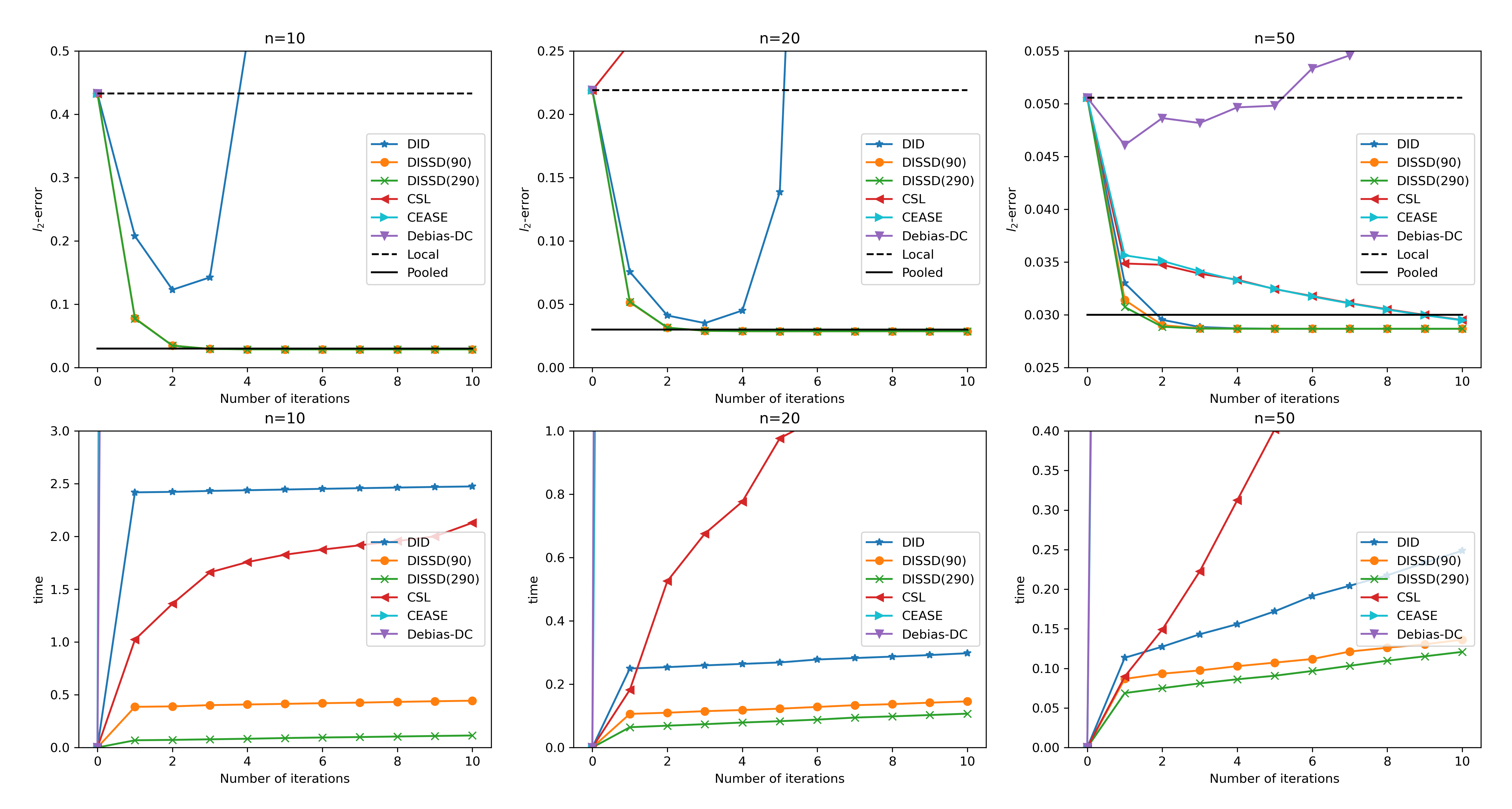

In the study, we analyze the Ames Housing data set111http://jse.amstat.org/v19n3/decock.pdf, which was compiled by Dean De Cock for use in data science education. This data set contains all sales that occurred within Ames from 2006 to 2010. The response variable is the house sale price; the covariates include various house features. We aim to learn a sparse least square regression model to predict the house price by applying our proposed methods and to compare the performance in terms of prediction error. After weeding out the outliers and applying principal component analysis, we obtained 2902 observations and 51 features. We can compute that the -sparsity of the empirical inverse covariance matrix of the covariate is , which suffices Condition A1. We randomly partition the data set into 2000 training data and 612 testing data. Among them, we remove the label of 290 data and treat it as the unlabeled covariates. We perform 100 random partitions of the dataset and report the averaged prediction error and processing time on the testing set. We consider three cases where and respectively. In our experimental analysis, we conducted a comparative evaluation of our DISSD method against the CSL method from Jordan et al. (2019), the CEASE method from Fan et al. (2023), and the Debias-DC method detailed in Battey et al. (2018). The results are summarized in Figure 5. Notably, the semi-supervised methods consistently outperform their fully-supervised counterparts. Particularly for small sample sizes (specifically and ), CSL, CEASE, and Debias-DC all exhibit instability, leading to divergence. Even at a sample size of , these methods are surpassed by our DISSD method in terms of performance. From the computational perspective, both CEASE and Debias-DC demonstrate considerably longer processing times compared to other methods.

6 Concluding Remarks and Future Study

In this paper, we investigate the problem of semi-supervised sparse learning in a distributed setup and demonstrate that incorporating unlabeled data can enhance the statistical accuracy in distributed learning. Throughout this paper, we construct the inverse covariance matrix using SCIO Liu and Luo (2015), which requires to be sparse in each column. However, there exist other debiasing approaches, such as Javanmard and Montanari (2014); van de Geer et al. (2014); Zhang and Zhang (2014); Cai et al. (2021), that can eliminate the sparsity constraint on . It would be interesting to explore the application of these approaches to our DISSD method in future work to see if similar results can be achieved. Furthermore, in addition to debiased estimators, other methods for sparse learning exist, such as adding penalty (Tibshirani, 1996) or non-convex penalties (Fan and Li, 2001; Zhang, 2010b, a), or using the iterative hard thresholding method (Blumensath and Davies, 2009; Jain et al., 2014; Yuan et al., 2018). Investigating the use of distributed semi-supervised methods for these techniques is of significant importance.

References

- Arjevani and Shamir (2015) Arjevani, Y. and Shamir, O. (2015), “Communication Complexity of Distributed Convex Learning and Optimization,” in Advances in Neural Information Processing Systems, Curran Associates, Inc., vol. 28, pp. 1756–1764.

- Azriel et al. (2022) Azriel, D., Brown, L. D., Sklar, M., Berk, R., Buja, A., and Zhao, L. (2022), “Semi-Supervised Linear Regression,” J. Amer. Statist. Assoc., 117, 2238–2251.

- Battey et al. (2018) Battey, H., Fan, J., Liu, H., Lu, J., and Zhu, Z. (2018), “Distributed testing and estimation under sparse high dimensional models,” Ann. Statist., 46, 1352–1382.

- Beck and Teboulle (2009) Beck, A. and Teboulle, M. (2009), “A fast iterative shrinkage-thresholding algorithm for linear inverse problems,” SIAM J. Imaging Sci., 2, 183–202.

- Bickel and Levina (2008) Bickel, P. J. and Levina, E. (2008), “Covariance regularization by thresholding,” Ann. Statist., 36, 2577 – 2604.

- Blumensath and Davies (2009) Blumensath, T. and Davies, M. E. (2009), “Iterative hard thresholding for compressed sensing,” Appl. Comput. Harmon. Anal., 27, 265–274.

- Boyd et al. (2011) Boyd, S., Parikh, N., Chu, E., Peleato, B., and Eckstein, J. (2011), “Distributed optimization and statistical learning via the alternating direction method of multipliers,” Found.Trends Mach. Learn., 3, 1–122.

- Cai et al. (2021) Cai, T., Cai, T. T., and Guo, Z. (2021), “Optimal statistical inference for individualized treatment effects in high-dimensional models,” J. R. Stat. Soc. Ser. B. Stat. Methodol., 83, 669–719.

- Cai and Liu (2011) Cai, T. and Liu, W. (2011), “Adaptive thresholding for sparse covariance matrix estimation,” J. Amer. Statist. Assoc., 106, 672–684.

- Cai et al. (2011) Cai, T., Liu, W., and Luo, X. (2011), “A constrained minimization approach to sparse precision matrix Estimation,” J. Amer. Statist. Assoc., 106, 594–607.

- Cai and Guo (2020) Cai, T. T. and Guo, Z. (2020), “Semisupervised inference for explained variance in high dimensional linear regression and its applications,” J. R. Stat. Soc. Ser. B. Stat. Methodol., 82, 391–419.

- Chakrabortty and Cai (2018) Chakrabortty, A. and Cai, T. (2018), “Efficient and adaptive linear regression in semi-supervised settings,” Ann. Statist., 46, 1541–1572.

- Chang et al. (2017) Chang, X., Lin, S.-B., and Zhou, D.-X. (2017), “Distributed semi-supervised learning with kernel ridge regression,” J. Mach. Learn. Res., 18, 1493–1514.

- Chen et al. (2020) Chen, X., Liu, W., Mao, X., and Yang, Z. (2020), “Distributed High-Dimensional Regression under a Quantile Loss Function,” J. Mach. Learn. Res., 21.

- Chen et al. (2019) Chen, X., Liu, W., and Zhang, Y. (2019), “Quantile regression under memory constraint,” Ann. Statist., 47, 3244 – 3273.

- Chow and Teicher (2012) Chow, Y. and Teicher, H. (2012), Probability Theory: Independence, Interchangeability, Martingales, Springer Texts in Statistics, Springer New York.

- Deng et al. (2020) Deng, S., Ning, Y., Zhao, J., and Zhang, H. (2020), “Optimal semi-supervised estimation and inference for high-dimensional linear regression,” arXiv e-prints, arXiv:2011.14185.

- Fan et al. (2023) Fan, J., Guo, Y., and Wang, K. (2023), “Communication-Efficient Accurate Statistical Estimation,” J. Amer. Statist. Assoc., 118, 1000–1010.

- Fan and Li (2001) Fan, J. and Li, R. (2001), “Variable selection via nonconcave penalized likelihood and its oracle properties,” J. Amer. Statist. Assoc., 96, 1348–1360.

- Fan et al. (2018) Fan, J., Liu, H., Sun, Q., and Zhang, T. (2018), “I-LAMM for sparse learning: Simultaneous control of algorithmic complexity and statistical error,” Ann. Statist., 46, 814–841.

- Gronsbell and Cai (2018) Gronsbell, J. L. and Cai, T. (2018), “Semi-supervised approaches to efficient evaluation of model prediction performance,” J. R. Stat. Soc. Ser. B. Stat. Methodol., 80, 579–594.

- Guo et al. (2021) Guo, Z., Rakshit, P., Herman, D. S., and Chen, J. (2021), “Inference for the Case Probability in High-dimensional Logistic Regression,” J. Mach. Learn. Res., 22, 1–54.

- Guo et al. (2019) Guo, Z.-C., Lin, S.-B., and Shi, L. (2019), “Distributed learning with multi-penalty regularization,” Appl. Comput. Harmon. Anal., 46, 478–499.

- Guo et al. (2017) Guo, Z.-C., Shi, L., and Wu, Q. (2017), “Learning theory of distributed regression with bias corrected regularization Kernel Network,” J. Mach. Learn. Res., 18, 1–25.

- Hu and Zhou (2021) Hu, T. and Zhou, D.-X. (2021), “Distributed regularized least squares with flexible Gaussian kernels,” Appl. Comput. Harmon. Anal., 53, 349–377.

- Huang and Huo (2019) Huang, C. and Huo, X. (2019), “A distributed one-step estimator,” Mathematical Programming, 174, 41–76.

- Huber (2004) Huber, P. J. (2004), Robust Statistics, vol. 523, John Wiley & Sons.

- Jain et al. (2014) Jain, P., Tewari, A., and Kar, P. (2014), “On iterative hard thresholding methods for high-dimensional M-estimation,” in Advances in Neural Information Processing Systems, Curran Associates, Inc., vol. 27, pp. 685–693.

- Javanmard and Montanari (2014) Javanmard, A. and Montanari, A. (2014), “Confidence Intervals and Hypothesis Testing for High-Dimensional Regression,” J. Mach. Learn. Res., 15, 2869–2909.

- Jordan et al. (2019) Jordan, M. I., Lee, J. D., and Yang, Y. (2019), “Communication-efficient distributed statistical inference,” J. Amer. Statist. Assoc., 114, 668–681.

- Kuchibhotla and Chakrabortty (2022) Kuchibhotla, A. K. and Chakrabortty, A. (2022), “Moving beyond sub-Gaussianity in high-dimensional statistics: applications in covariance estimation and linear regression,” Inf. Inference, 11, 1389–1456.

- Lee et al. (2017) Lee, J. D., Liu, Q., Sun, Y., and Taylor, J. E. (2017), “Communication-efficient sparse regression,” J. Mach. Learn. Res., 18, 115–144.

- Li et al. (2013) Li, R., Lin, D. K., and Li, B. (2013), “Statistical inference in massive data sets,” Appl. Stoch. Models Bus. Ind., 29, 399–409.

- Lian and Fan (2018) Lian, H. and Fan, Z. (2018), “Divide-and-conquer for debiased -norm support vector machine in ultra-high dimensions,” J. Mach. Learn. Res., 18, 1–26.

- Lin et al. (2017) Lin, S.-B., Guo, X., and Zhou, D.-X. (2017), “Distributed learning with regularized least squares,” J. Mach. Learn. Res., 18, 1–31.

- Lin and Zhou (2018) Lin, S.-B. and Zhou, D.-X. (2018), “Distributed kernel-based gradient descent algorithms,” Constr. Approx., 47, 249–276.

- Liu et al. (2021) Liu, M., Xia, Y., Cho, K., and Cai, T. (2021), “Integrative high dimensional multiple testing with heterogeneity under data sharing constraints,” J. Mach. Learn. Res., 22, 1–26.

- Liu and Luo (2015) Liu, W. and Luo, X. (2015), “Fast and adaptive sparse precision matrix estimation in high dimensions,” J. Multivariate Anal., 135, 153–162.

- Ma et al. (2021) Ma, R., Cai, T. T., and Li, H. (2021), “Global and Simultaneous Hypothesis Testing for High-Dimensional Logistic Regression Models,” J. Amer. Statist. Assoc., 116, 984–998.

- Ma et al. (2022) Ma, R., Guo, Z., Cai, T. T., and Li, H. (2022), “Statistical Inference for Genetic Relatedness Based on High-Dimensional Logistic Regression,” arXiv e-prints, arXiv:2202.10007.

- Meinshausen and Bühlmann (2006) Meinshausen, N. and Bühlmann, P. (2006), “High-dimensional graphs and variable selection with the Lasso,” Ann. Statist., 34, 1436 – 1462.

- Raskutti et al. (2010) Raskutti, G., Wainwright, M. J., and Yu, B. (2010), “Restricted Eigenvalue Properties for Correlated Gaussian Designs,” J. Mach. Learn. Res., 11, 2241–2259.

- Raskutti et al. (2011) — (2011), “Minimax Rates of Estimation for High-Dimensional Linear Regression Over -Balls,” IEEE Trans. Inform. Theory, 57, 6976–6994.

- Shamir et al. (2014) Shamir, O., Srebro, N., and Zhang, T. (2014), “Communication-efficient distributed optimization using an approximate Newton-type method,” in Proceedings of the 31st International Conference on Machine Learning, vol. 32, pp. 1000–1008.

- Smith et al. (2017) Smith, V., Forte, S., Ma, C., Takáč, M., Jordan, M. I., and Jaggi, M. (2017), “CoCoA: A general framework for communication-efficient distributed optimization,” J. Mach. Learn. Res., 18, 8590–8638.

- Stich (2019) Stich, S. U. (2019), “Local SGD converges fast and communicates little,” in 7th International Conference on Learning Representations, ICLR 2019, May 6-9, 2019.

- T. Tony Cai and Ma (2023) T. Tony Cai, Z. G. and Ma, R. (2023), “Statistical Inference for High-Dimensional Generalized Linear Models With Binary Outcomes,” J. Amer. Statist. Assoc., 118, 1319–1332.

- Tibshirani (1996) Tibshirani, R. (1996), “Regression shrinkage and selection via the lasso,” J. R. Stat. Soc. Ser. B. Stat. Methodol., 58, 267–288.

- Tu et al. (2023) Tu, J., Liu, W., and Mao, X. (2023), “Byzantine-robust distributed sparse learning for M-estimation,” Mach. Learn., 112, 3773–3804.

- van de Geer et al. (2014) van de Geer, S., Bühlmann, P., Ritov, Y., and Dezeure, R. (2014), “On asymptotically optimal confidence regions and tests for high-dimensional models,” Ann. Statist., 42, 1166 – 1202.

- Vershynin (2010) Vershynin, R. (2010), “Introduction to the non-asymptotic analysis of random matrices,” arXiv e-prints, arXiv:1011.3027.

- Volgushev et al. (2019) Volgushev, S., Chao, S.-K., and Cheng, G. (2019), “Distributed inference for quantile regression processes,” Ann. Statist., 47, 1634 – 1662.

- Wang et al. (2017) Wang, J., Kolar, M., Srebro, N., and Zhang, T. (2017), “Efficient Distributed Learning with Sparsity,” in Proceedings of the 34th International Conference on Machine Learning, vol. 70, pp. 3636–3645.

- Wu et al. (2023) Wu, Z., Wang, C., and Liu, W. (2023), “A unified precision matrix estimation framework via sparse column-wise inverse operator under weak sparsity,” Ann. Inst. Statist. Math., 75, 619–648.

- Yuan (2010) Yuan, M. (2010), “High dimensional inverse covariance matrix estimation via linear programming,” J. Mach. Learn. Res., 11, 2261–2286.

- Yuan et al. (2018) Yuan, X.-T., Li, P., and Zhang, T. (2018), “Gradient hard thresholding pursuit,” J. Mach. Learn. Res., 18, 1–43.

- Zhang et al. (2019) Zhang, A., Brown, L. D., and Cai, T. T. (2019), “Semi-supervised inference: General theory and estimation of means,” Ann. Statist., 47, 2538 – 2566.

- Zhang (2010a) Zhang, C.-H. (2010a), “Nearly unbiased variable selection under minimax concave penalty,” Ann. Statist., 38, 894–942.

- Zhang and Zhang (2014) Zhang, C.-H. and Zhang, S. S. (2014), “Confidence intervals for low dimensional parameters in high dimensional linear models,” J. R. Stat. Soc. Ser. B. Stat. Methodol., 76, 217–242.

- Zhang (2010b) Zhang, T. (2010b), “Analysis of multi-stage convex relaxation for sparse regularization,” J. Mach. Learn. Res., 11, 1081–1107.

- Zhang and Bradic (2021) Zhang, Y. and Bradic, J. (2021), “High-dimensional semi-supervised learning: in search of optimal inference of the mean,” Biometrika.

- Zhang et al. (2013) Zhang, Y., Duchi, J., Jordan, M. I., and Wainwright, M. J. (2013), “Information-theoretic lower bounds for distributed statistical estimation with communication constraints,” in Advances in Neural Information Processing Systems, Curran Associates, Inc., vol. 26, pp. 2328–2336.

- Zhang et al. (2015) Zhang, Y., Duchi, J., and Wainwright, M. (2015), “Divide and conquer kernel ridge regression: A distributed algorithm with minimax optimal rates,” J. Mach. Learn. Res., 16, 3299–3340.

- Zhang and Lin (2015) Zhang, Y. and Lin, X. (2015), “DiSCO: Distributed optimization for self-concordant empirical loss,” in Proceedings of the 32nd International Conference on Machine Learning, PMLR, vol. 37 of Proceedings of Machine Learning Research, pp. 362–370.

- Zhao et al. (2014) Zhao, T., Kolar, M., and Liu, H. (2014), “A General Framework for Robust Testing and Confidence Regions in High-Dimensional Quantile Regression,” arXiv e-prints, arXiv:1412.8724.

- Zhao et al. (2020) Zhao, W., Zhang, F., and Lian, H. (2020), “Debiasing and distributed estimation for high-dimensional quantile regression,” IEEE Trans. Neural Netw. Learn. Syst., 31, 2569–2577.

- Zhou (2020) Zhou, D.-X. (2020), “Distributed Kernel Ridge Regression with Communications,” J. Mach. Learn. Res., 21.

7 Appendix

The appendix consists of three parts. Appendix 7.1 includes some technical lemmas for the proof. The proof of theorems in Section 3.2 in the main paper are given in Appendix 7.2. The proof of theories in Section 4.2 is presented in Appendix 7.3.

7.1 Technical Lemmas

Lemma 1.

(Exponential Inequality, Lemma 1 in Cai and Liu (2011)) Let be independent random variables all with means zero. Suppose that there exist some constants and such that , where . Then uniformly for and , there is

7.2 Proof of Theories in Section 3.2

Proof.

For simplicity, we assume that only has one discontinuous point , i.e. , . Define as the collection of index sets having elements. Then we know that . For each , we denote the parameter sets , and construct the following random variable

We construct , an -net of the set . By definition we know that is a ball in with radius . By Lemma 5.2 of Vershynin (2010), we have . From Lipschitz continuity of in Assumption A4, we have

From Assumption A1, we can show that

by letting large enough. Moreover, from Assumption A2, we can apply Lemma 1 to the i.i.d. random variables

and prove that, for any , there exists a constant such that

Therefore we have

| (31) |

Moreover, by Lipschitz continuity of and in Assumption A2 and A3, for every , we can compute that

From Assumption A1, we have

| (32) |

On the other hand, we define

Compute that

Therefore we have .

It is worthwhile noting that, when the loss function is smooth, there is no term in . Follow the same procedure we can prove that

| (34) |

Lemma 4.

Proof.

Firstly we consider the case that Condition ANS holds true. Define as the collection of index sets having elements. Then we know that . For each , we denote the parameter sets . For each , we construct , an -net of the set . By definition we know that is a ball in with radius . By Lemma 5.2 of Vershynin (2010), we have . Then we have

For simplicity we denote

From Condition ANS, we have

Therefore by using Lemma 1, we can show that, for every , there exists large enough such that

By letting , we have

| (35) |

From Condition ANS, we can show that

Then again by Lemma 1 we have that, for every , there exists large enough such that

Therefore we have

| (36) |

Combining (35) and (36), the second part of the lemma is proved. Follow the same idea we can prove the first part. Indeed from Condition AS we can show that

and then the first part can be proved. ∎

Proof of Theorem 1, 2 and Corollary 1.

From (10), we have the following decomposition.

| (37) | ||||

where the third line follows from Condition A2 and

Taking norms on both sides we have that

Under Condition AS, we applying Lemma 2, 3 and 4, and know that

When the threshold level is larger than , we know that for , therefore . For , there is

Therefore,

Similarly, we can prove that

which proves Theorem 1. Under the non-smooth condition ANS, the rate becomes

Following the same argument as above, we can show that

which proves Theorem 2. Then Corollary 1 can be easily obtained by applying the above formula iteratively. ∎

Proof of Theorem 3.

By (37) and Lemma 2, 3 and 4, we have that

| (38) |

where the remainders are bounded in norm. Notice that the major term is the sum of i.i.d. variables, for each coordinate (where ), we know the variance is

Therefore, by central limit theorem (see, e.g., Theorem 9.1.1 of Chow and Teicher (2012)), we have that

| (39) |

When satisfies the constraints

we can substitute (39) into (38) and obtain that

which proves the theorem. ∎

7.3 Proof of Theories in Section 4.2

Throughout this section, we denote

| (40) |

for convenience.

Proof.

Proof.

We note that

| (42) | ||||

We denote

Define as the collection of index sets having elements. Then we know that . For each , we denote the parameter sets . For each , we construct , an -net of the set . By definition we know that is a ball in with radius . By Lemma 5.2 of Vershynin (2010), we have . Then we turn to bound

For each for some , and each coordinate , we have that

Therefore, we have that each element of follows -sub-Weibull distribution. By Theorem 3.1 of Kuchibhotla and Chakrabortty (2022), we have that

for some large constants . Therefore we can obtain that

Substitute it into (42) we have

which proves the lemma. ∎

Lemma 7.

Let be random variables and be a sequence of event. Further assume to be a measurable function of the tuple taking values in , and be a measurable set in . Then we have that

Proof.

Proof of Theorem 4 and Corollary 2.

From (24), we have the following decomposition

| (43) | ||||

By Lemma 5 and 6, we have that (43) equals to

Apply Lemma 8 and Lemma 2 we have that

When the threshold level is larger than , we know that for , therefore . For , there is

Therefore,

Similarly, we can prove that

which proves Theorem 4. Then Corollary 2 can be obtained by applying the above rate iteratively. ∎

Proof of Theorem 5.

From (43), when , we have that

The major term is the average of i.i.d. terms of . We know the covariance matrix is . Then for each coordinate (where ), we denote the variance

by the central limit theorem, we have that

| (44) |

When there are constraints

we can substitute (44) to (43) and obtain that

which proves the theorem. ∎

7.4 Examples Verification

Proposition 1.

Proof.

The proof can be found in Proposition 1 of the supplementary materials in Tu et al. (2023). ∎

Proposition 2.

Proof.

The proof can be found in Proposition 2 of the supplementary materials in Tu et al. (2023). ∎