Fast, Distribution-free Predictive Inference for Neural Networks with Coverage Guarantees

Abstract

This paper introduces a novel, computationally-efficient algorithm for predictive inference (PI) that requires no distributional assumptions on the data and can be computed faster than existing bootstrap-type methods for neural networks. Specifically, if there are training samples, bootstrap methods require training a model on each of the subsamples of size ; for large models like neural networks, this process can be computationally prohibitive. In contrast, our proposed method trains one neural network on the full dataset with -differential privacy (DP) and then approximates each leave-one-out model efficiently using a linear approximation around the differentially-private neural network estimate. With exchangeable data, we prove that our approach has a rigorous coverage guarantee that depends on the preset privacy parameters and the stability of the neural network, regardless of the data distribution. Simulations and experiments on real data demonstrate that our method satisfies the coverage guarantees with substantially reduced computation compared to bootstrap methods.

1 Introduction

To assess the accuracy of parameter estimates or predictions without specific distributional knowledge of the data, the idea of re-sampling or sub-sampling on the available data has been long-established to construct prediction intervals, and there is a rich history in the statistics literature on the jackknife and bootstrap methods, see Stine (1985), Efron (1979), Quenouille (1949), Efron and Gong (1983). Among these re-sampling methods, leave-one-out methods (generally referred to as “cross-validation” or “jackknife”) are widely used to assess or calibrate predictive accuracy, and can be found in a large line of literature (Stone, 1974, Geisser, 1975).

While it has been demonstrated in a large body of past work with extensive evidence that jackknife-type methods have reliable empirical performance, the theoretical properties of these types of methods are studied relatively little until recently, see Steinberger and Leeb (2018), Bousquet and Elisseeff (2002). One of the most important results among these theoretically guaranteed works is Foygel Barber et al. (2019), which introduces a crucial modification compared to the traditional jackknife method that permits rigorous coverage guarantees of at least regardless of the distribution of the data points, for any algorithm that treats the training points symmetrically. We will revisit this work and give more relative details in Section 2.1.

Although theoretically jackknife+ has been proven to have coverage guarantees without distributional assumptions, in practice, this method is computationally costly, since we need to train (which is the training sample size) leave-one-out models from scratch to find the predictive interval. Especially for large and complicated models like neural networks, this computational cost is prohibitive. The goal of this paper is to provide a fast algorithm that provides similar theoretical coverage guarantees to those in jackknife+.

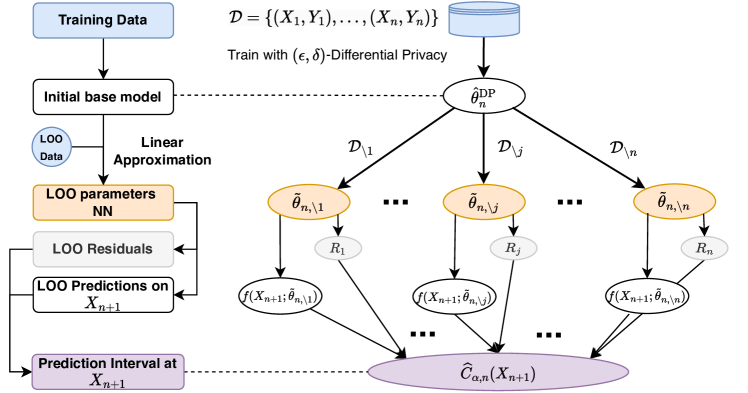

To achieve this goal, we develop a new procedure, called Differentially Private Lazy Predictive Inference (DP-Lazy PI), which combines two ideas: lazy training of neural networks and differentially private stochcastic gradient descent (DP-SGD). To accelerate the procedure, we introduce a lazy training scheme inspired by Chizat et al. (2020), Gao et al. (2022) to train the leave-one-out models. The intuition is that with data exchangeability, the leave-one-out models should be quite close or similar to each other and there is no need to train each one from scratch ( i.e., random initialization). Instead, we first train a model on the full data and use this model as a good initialization. By using DP-SGD as the initializer for our full model, we are able to provide coverage guarantees since the privacy mechanism prevents information leakage across leave-one-out estimators. In particular, we prove that our DP-Lazy PI procedure has a coverage of at least where represents an out-of-sample stability parameter and are the differential privacy parameters. Empirically, we show through simulations and real-data experiments that our method has significant advantage over the existing jackknife+ method in run-time while still maintaining good coverage.

2 Preliminaries

We first define key notation. For any values indexed by , define

| (1) |

i.e., the quantile of the empirical distribution of these values; Similarly,

| (2) |

is the quantile of the empirical distribution.

2.1 Distribution-free Prediction Intervals

Suppose we have training data for , and a new test point , drawn independently from the same distribution. We fit a regression model to the training data, i.e., a function where predicts given a new feature vector , and then provide a prediction interval centered around for the test point. Specifically, given some target coverage level , we aim to construct a prediction interval , such that We call the probability as the coverage, and as the interval width of , which is the distance between the left and right endpoints.

Naïve Prediction Interval

A naïve way to construct a predictive interval at the new test point is to center the interval at and estimate the margin ( i.e., half of the interval width) from the training residuals . Therefore, a naïve prediction interval can be constructed as:

where is defined as (1). Due to the problem of overfitting when the training errors are typically smaller than the test errors, this naïve interval may undercover— i.e., the probability that falls outside the interval can be larger than , as discussed in Foygel Barber et al. (2019).

Jackknife Prediction Interval

To avoid undercoverage due to model overfitting, the jackknife method estimates the margin of errors is estimated by leave-one-out residuals instead of training residuals (Steinberger and Leeb, 2016, 2018). The idea is straightforward: for each , we fit a regression function using all the training data except the -th training sample. Based on these leave-one-out models , we can therefore compute the leave-one-out residuals: .

With the leave-one-out residuals as well as the regression function fitted on the full training data, the jackknife prediction interval is constructed as:

Jackknife+ Prediction Interval

The jackknife+ is a modification of jackknife, and both of these methods use the leave-one-out residuals when constructing the prediction intervals. The difference is that the jackknife interval is centered at the predicted value (where is fitted on the full training data), whereas jackknife+ uses the leave-one-out predictions instead to the build the prediction interval:

Foygel Barber et al. (2019) provides the non-asymptotic coverage guarantee for jackknife+ without assumptions beyond the training and test data being exchangeable. Theoretically, a distribution-free coverage guarantee of at least is provided, and it’s observed that the method can achieve coverage in empirical studies.

Summary of coverage guarantees and computational costs

The coverage guarantees and the computational cost of the above methods are summarized in Table 1. Concretely computational cost refers to the computation at two stages, model training and evaluation and we measure cost in terms of number of models trained during the training phase and number of calls to the trained function in the evaluation stage.

Coverage Guarantee Computation Distribution-free Theory Empirical # models trained # calls to trained function Naïve No guarantee jackknife No guarantee jackknife+

Clearly the cost of model training is the largest cost, especially when training a complicated model such as a neural network. Our method attempts to only train a single model (like the naïve model) while still providing a coverage guarantee (like jackknife+).

3 Method and Algorithm

Our method involves using the lazy estimation framework (Chizat et al., 2020) with an initialization using differential privacy stochastic gradient descent (DP-SGD, Abadi et al. (2016)).

3.1 Lazy Estimation

To calculate the predictive interval fast and reduce the computational cost, we consider using a lazy estimation scheme when estimating the leave-one-out (LOO) models for calculating the predictive interval. The key idea of our approach is given an initialization parameterized by , for each , we approximate by linearizing around initial base model and training the linearized model using all but the training sample. Thus instead of training neural networks explicitly, we train a single neural network followed by linear models, leading to a substantial computational saving.

For any dataset and a large model , where denotes the model parameters, we define a lazy estimation operator with the ridge regression parameter and initialization , we estimate the LOO models by taking a linearization around and minimize the penalized training loss on data ,

| (3) |

3.2 Differential Privacy (DP) initialization

One of the important questions with lazy estimation is how to choose the initialization . For this we use the concept of differential privacy, which allows us to achieve coverage guarantees with a large reduction in computational costs.

Definition 1 (Differential Privacy (Dwork and Lei, 2009)).

A randomized mechanism with domain and range satisfies -differential privacy if for any two adjacent datasets and for any subset of outputs it holds that

| (4) |

In essence, this differential privacy (DP) condition ensures that the output distribution does not change much when the input data has some small change, which makes it hard to distinguish between the input databases on the basis of the output. Abadi et al. (2016) proposes Algorithm 1, which performs stochastic gradient descent with noisy gradients and showed that it achieves -differential privacy, where noise is added to the gradients in the scale of . Algorithms to ensure DP are always designed based on the sensitivity of the original algorithm. More precisely, given an algorithm and a norm function over the range of , the sensitivity of is defined as

| (5) |

The Laplacian mechanism to construct a differentially private algorithm is as follows (see (Koufogiannis et al., 2015, Holohan et al., 2018)): for an algorithm (or function) , the random function satisfies -differential privacy, where the elements follows a Laplacian distribution : . We can set and as small constants ( e.g., and ), and adjust the noise levels in different DP mechanisms.

3.3 Our method: Lazy Estimation with Differential Privacy

First, we use a noisy SGD method (Abadi et al., 2016) with differential privacy to get a full model parameter estimation , which for convenience will be denoted as . Fig. 3.1 provides an overview of our procedure.

Based on this , we estimate the LOO model parameters by using lazy training to take a linearization around and minimize the penalized training loss on data ,

| (6) |

Here is defined in (3). Based on the LOO model parameters, we can calculate the LOO residuals by

For a test data , its predictive interval using our method is:

| (7) |

where is a relaxation term that is close to 0. Our full method is presented in Algorithm 2.

4 Coverage Guarantee

Recall that is the NN parameter estimate from -DP algorithm using the full training data . For any , define as NN parameter estimate from an -DP algorithm trained with the -th sample deleted, i.e., using data . Based on , we define another lazy estimate:

| (8) |

Theorem 1.

For any and , such that

| (9) |

the coverage of the DP-Lazy prediction interval defined in Equation 7 is larger than , where are the DP parameters, i.e.,

| (10) |

Remark 1.

In Theorem 1, essentially (9) requires an out-of-sample stability in the DP algorithm, which appears elsewhere in the literature Foygel Barber et al. (2019) and is referred to as “hypothesis stability” in Bousquet and Elisseeff (2002). We want to emphasize that this out-of-sample stability only requires that, for a test data point that is independent of the training data, the predicted value does not change much if we remove one point in the training data set, which can hold even for algorithms that suffer from strong overfitting in contrast to the in-sample stability. As an illustrative example, the K-nearest-neighbor algorithm is shown to satisfy the out-of-sample stability with and (see Example 5.5 in Foygel Barber et al. (2019)).

For neural networks, notions of stability are also assumed in the literature (Verma and Zhang, 2019, Forti et al., 1994). In the Supplementary Material, we also give an example showing that if is multivariate Gaussian, for a two-layer neural network (one hidden layer) with activation functions like ReLU, sigmoid or tanh and (defined in Equation 5), (9) holds true with up to some log terms and for some constant .

4.1 Proof Overview of Theorem 1

In this section, we’ll provide the key ideas and the skeleton of the proof for the coverage guarantee, while the completed proof is postponed in the Appendix. Recall and define

First, for any we show that a jackknife+ type interval defined as

| (11) |

is contained within our rapidly calculated prediction interval with high probability that depends on the relaxation term and the DP parameters :

| (12) | ||||

| (13) | ||||

| (14) | ||||

| (15) | ||||

| (16) | ||||

| (17) |

The probabilities are taken with respect to all the training data as well as the test data . (13) holds by the definitions of the prediction intervals of interest, which is equivalent to (14); by data exchangeability and Markov inequality, (15) holds true; by the property of differential privacy in the Appendix, the in-sample stability term in (15) is relaxed to an out-of-sample stability condition in (16), which is bounded by the condition in Equation 9.

By the jackknife+ coverage guarantee in Foygel Barber et al. (2019) that

| (18) |

we can bound the miscoverage rate for the prediction interval :

| (19) | ||||

| (20) | ||||

| (21) |

for all . Take , we therefore have the coverage of :

5 Experiments

We compare the following methods for estimating prediction intervals: (1) jackknife+: defined in Section 2.1, with the base algorithm being neural networks with random initialization; (2) DP-Lazy PI (labeled lazy_dp in plots): our proposed method with the same NN architecture used in jackknife+, with the relaxation term set to zero, and differential parameters set as ; (3) Lazy PI without DP (labeled lazy_finetune in plots): removes the privacy mechanism compared to DP-Lazy PI, i.e., use instead of as in the lazy estimation step (3).

For evaluation, we consider the following three performance aspects on the test data set with size for a prediction interval : (1) Coverage: (2) Compute time; (3) Average interval width: . As we set the level as , our target of the coverage is , we want to emphasize that a higher coverage of the prediction intervals is not always desirable, since it may suggest that the prediction intervals are overly wide and conservative.

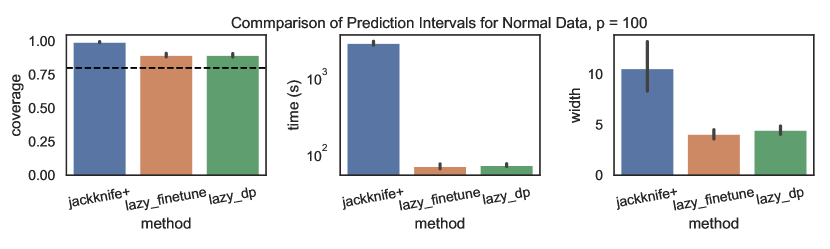

5.1 Simulation

To generate the data, are randomly selected from a Gaussian distribution , where . The responses are generated by:

| (22) |

We consider a neural network with two hidden layers, each contains 64 nodes. The data are randomly split into the training data with the training size , and evaluation set with the size .

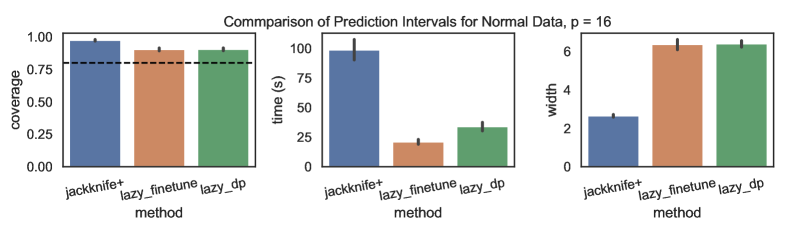

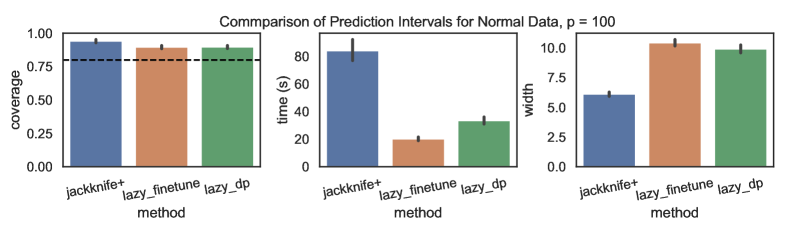

We construct prediction intervals using jackknife+, lazy finetune and DP-Lazy PI respectively on the training data with . When training the neural networks, the training batch size is and the max number of epochs is . The penalty parameter is taken as in the lazy type of methods.

As shown in Figure 5.1, the coverage of our method is closer to the target coverage and in terms of the compute time, lazy methods reduce the average compute time significantly compared to jackknife+. As the feature dimension increases, the coverage is still guaranteed; we can also see in Figure 5.1 (b) that compared to lazy finetune without noise added in the full model training, lazy DP becomes better in the interval width, which might come from the interpolation (near zero training error) in the high-dimensional case that makes the LOO estimates in lazy finetune stays at the initial base model in the lazy procedure.

|

| (a) Simulated data with dimension |

|

| (b) Simulated data with dimension |

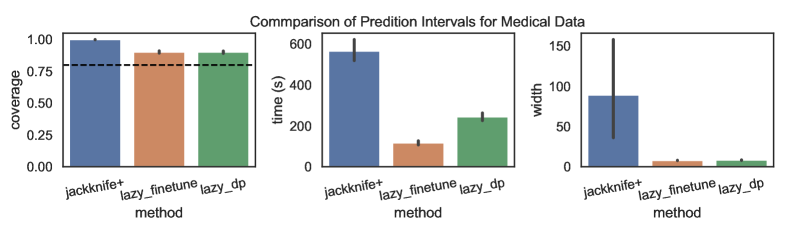

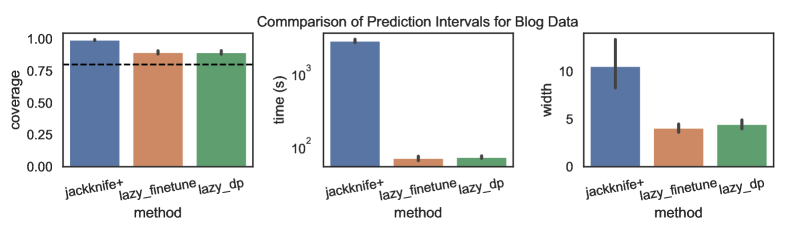

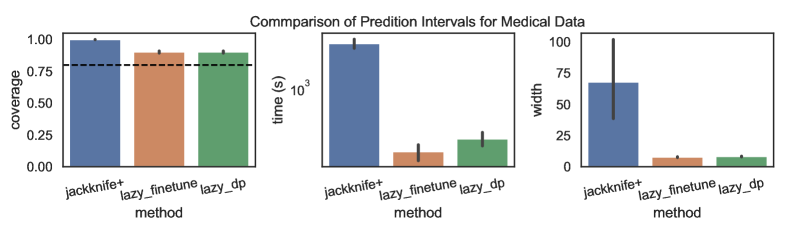

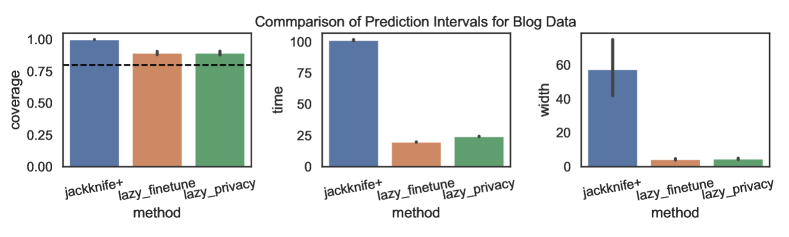

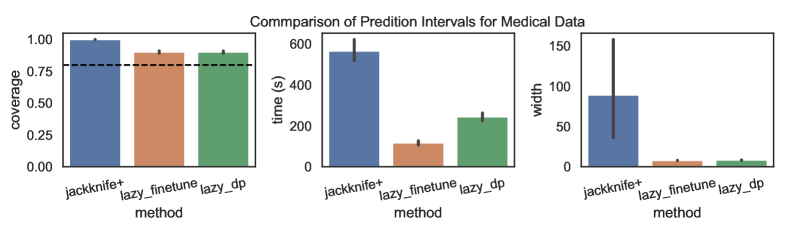

5.2 Real Data

Data sets

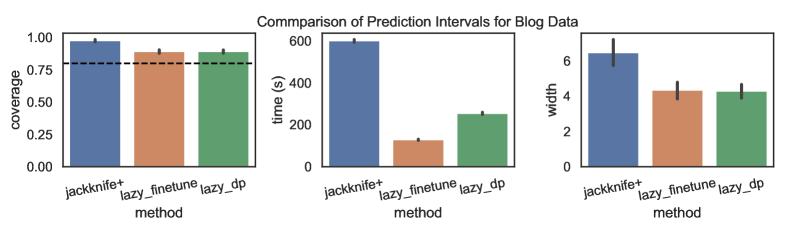

(1) The BlogFeedback111https://archive.ics.uci.edu/ml/datasets/BlogFeedback data set (Spiliopoulou et al., 2014, Foygel Barber et al., 2019), contains information on 52397 blog posts with covariates. The response is the number of comments left on the blog post in the following 24 hours, which we transformed as . (2) The Medical Expenditure Panel Survey 2016 data set222https://meps.ahrq.gov/mepsweb/data_stats/download_data_files_detail.jsp?cboPufNumber=HC-192 contains records on individuals’ utilization of medical services such as visits to the doctor, hospital stays etc with feature dimension with relevant features such as age, race/ethnicity, family income, occupation type, etc. Our goal is the predict the health care system utilization of each individual, which is a composite score reflecting the number of visits to a doctor’s office, hospital visits, days in nursing home care, etc.

Experiment Settings

The training size to construct the prediction interval is set . We consider the 3-layer neural network with hidden layers as the base NN architecture. To train the model parameters in jackknife+, we initialize the NN randomly for each LOO models. The penalty level is set as , and the DP parameters are . The batch size is and the maximum number of epochs is 10. We repeat the trials times with different random seeds for the train-test split and the random initialization of NN parameters in jackknife+. The figures show the average coverage, computing time and the interval width across these random trails.

|

| (a) BlogFeedback data set |

|

| (b) Medical Expenditure Panel Survey 2016 data set |

Results

As shown in Figure 5.2 (a) and (b), when we look into the real data sets, DP-Lazy PI decreases the computing time while enjoys a narrower interval width, while achieving the coverage guarantee at . Compared to the data generated in the simulation, for real data with much complicated data structure, the model mis-specification makes the width of the jackknife+ estimator greater and the implicit regularization of the lazy approach reduces this width. The implementation codes can be found in https://github.com/VioyueG/DP_LAZY_PI.

6 Discussion and Limitations

In this paper, we describe a new method, Differential Privacy Lazy Predictive Inference or DP-Lazy PI, which provides a fast method for distribution-free inference for neural networks. Our method involves using differentially private stochastic gradient descent (DP-SGD) as an initial estimate and then computing leave-one-out approximations using lazy training and then re-combining the leave-one-out estimators to form the predictive interval. Importantly, we are able to provide coverage guarantees that closely match the coverage guarantees provided for the jackknife+ procedure with a fraction of the computational cost since only a single neural network model needs to be trained.

The two real data examples also suggest that when we have significant model misspecification, the implicit regularization that lazy training provides means that our DP Lazy-PI method has narrower width prediction intervals than jackknife+.

An alternative method we evaluated in our experiments was lazy finetune, which removes the privacy mechanism prior to lazy training. The simulation results show very similar and at times slightly improved performance compared to our DP Lazy-PI approach; however, a limitation is that we lack theoretical guarantees for this approach. It remains an open question whether we can provide theoretical guarantees for lazy finetune, noting that in the zero training error regime where we can perfectly interpolate, lazy training does not apply since we are at a zero gradient initialization, making linearized models useless. However, in higher dimensions, the implicit regularization through early stopping of neural network training may be the reason lazy training works well. A further limitation of this work is that our method requires the base algorithm ( e.g., the neural network estimation) to be stable and satisfy the condition (9).

Acknowledgements

R. Willett gratefully acknowledges the support of AFOSR grant FA9550-18-1-0166 and NSF grants DMS-2023109 and DMS-1925101. G. Raskutti acknowledges the support of NIH grant R01 GM131381-03.

References

- Abadi et al. (2016) Martin Abadi, Andy Chu, Ian Goodfellow, H. Brendan McMahan, Ilya Mironov, Kunal Talwar, and Li Zhang. Deep learning with differential privacy. In Proceedings of the 2016 ACM SIGSAC Conference on Computer and Communications Security. ACM, oct 2016. doi:10.1145/2976749.2978318. URL https://doi.org/10.1145%2F2976749.2978318.

- Bousquet and Elisseeff (2002) Olivier Bousquet and Andre Elisseeff. Stability and Generalization. The Journal of Machine Learning Research, 2:499–526, 2002.

- Chernozhukov et al. (2021) Victor Chernozhukov, Kaspar Wüthrich, and Yinchu Zhu. Distributional conformal prediction. Proceedings of the National Academy of Sciences, 118(48):e2107794118, 2021.

- Chizat et al. (2020) Lenaic Chizat, Edouard Oyallon, and Francis Bach. On lazy training in differentiable programming, 2020.

- Dwork and Lei (2009) Cynthia Dwork and Jing Lei. Differential privacy and robust statistics. In Proceedings of the Forty-First Annual ACM Symposium on Theory of Computing, STOC ’09, page 371–380, New York, NY, USA, 2009. Association for Computing Machinery. ISBN 9781605585062. doi:10.1145/1536414.1536466. URL https://doi.org/10.1145/1536414.1536466.

- Efron (1979) B. Efron. Bootstrap Methods: Another Look at the Jackknife. The Annals of Statistics, 7(1):1–26, January 1979. ISSN 0090-5364, 2168-8966. doi:10.1214/aos/1176344552. URL https://projecteuclid.org/journals/annals-of-statistics/volume-7/issue-1/Bootstrap-Methods-Another-Look-at-the-Jackknife/10.1214/aos/1176344552.full. Publisher: Institute of Mathematical Statistics.

- Efron and Gong (1983) Bradley Efron and Gail Gong. A Leisurely Look at the Bootstrap, the Jackknife, and Cross-Validation. The American Statistician, 37(1):36–48, 1983. ISSN 0003-1305. doi:10.2307/2685844. URL https://www.jstor.org/stable/2685844. Publisher: [American Statistical Association, Taylor & Francis, Ltd.].

- Forti et al. (1994) Mauro Forti, Stefano Manetti, and Mauro Marini. Necessary and sufficient condition for absolute stability of neural networks. IEEE Transactions on Circuits and Systems I: Fundamental Theory and Applications, 41(7):491–494, 1994.

- Foygel Barber et al. (2019) Rina Foygel Barber, Emmanuel J Candes, Aaditya Ramdas, and Ryan J Tibshirani. Predictive inference with the jackknife+. arXiv e-prints, pages arXiv–1905, 2019.

- Gao et al. (2022) Yue Gao, Abby Stevens, Garvesh Raskutti, and Rebecca Willett. Lazy estimation of variable importance for large neural networks. In Kamalika Chaudhuri, Stefanie Jegelka, Le Song, Csaba Szepesvari, Gang Niu, and Sivan Sabato, editors, Proceedings of the 39th International Conference on Machine Learning, volume 162 of Proceedings of Machine Learning Research, pages 7122–7143. PMLR, 17–23 Jul 2022. URL https://proceedings.mlr.press/v162/gao22h.html.

- Geisser (1975) Seymour Geisser. The predictive sample reuse method with applications. Journal of the American Statistical Association, 70(350):320–328, 1975. ISSN 0162-1459. doi:10.2307/2285815. URL https://www.jstor.org/stable/2285815.

- Holohan et al. (2018) Naoise Holohan, Spiros Antonatos, Stefano Braghin, and Pól Mac Aonghusa. The bounded laplace mechanism in differential privacy, 2018.

- Kasiviswanathan and Smith (2014) Shiva P. Kasiviswanathan and Adam Smith. On the 'semantics' of differential privacy: A bayesian formulation. Journal of Privacy and Confidentiality, 6(1), jun 2014. doi:10.29012/jpc.v6i1.634. URL https://doi.org/10.29012%2Fjpc.v6i1.634.

- Koufogiannis et al. (2015) Fragkiskos Koufogiannis, Shuo Han, and George J. Pappas. Optimality of the laplace mechanism in differential privacy, 2015.

- Lei and Wasserman (2014) Jing Lei and Larry Wasserman. Distribution-free prediction bands for non-parametric regression. Journal of the Royal Statistical Society: Series B: Statistical Methodology, pages 71–96, 2014.

- Li and Yuan (2017) Yuanzhi Li and Yang Yuan. Convergence analysis of two-layer neural networks with ReLU activation, 2017.

- Quenouille (1949) M. H. Quenouille. Approximate Tests of Correlation in Time-Series. Journal of the Royal Statistical Society. Series B (Methodological), 11(1):68–84, 1949. ISSN 0035-9246. URL https://www.jstor.org/stable/2983696. Publisher: [Royal Statistical Society, Wiley].

- Rogers et al. (2016) Ryan Rogers, Aaron Roth, Adam Smith, and Om Thakkar. Max-information, differential privacy, and post-selection hypothesis testing, 2016.

- Spiliopoulou et al. (2014) Myra Spiliopoulou, Lars Schmidt-Thieme, and Ruth Janning. Data analysis, machine learning and knowledge discovery. Springer, 2014.

- Steinberger and Leeb (2016) Lukas Steinberger and Hannes Leeb. Leave-one-out prediction intervals in linear regression models with many variables. arXiv preprint arXiv:1602.05801, 2016.

- Steinberger and Leeb (2018) Lukas Steinberger and Hannes Leeb. Conditional predictive inference for high-dimensional stable algorithms. arXiv preprint arXiv:1809.01412, 2018.

- Stine (1985) Robert A. Stine. Bootstrap Prediction Intervals for Regression. Journal of the American Statistical Association, 80(392):1026–1031, 1985. ISSN 0162-1459. doi:10.2307/2288570. URL https://www.jstor.org/stable/2288570. Publisher: [American Statistical Association, Taylor & Francis, Ltd.].

- Stone (1974) M. Stone. Cross-Validatory Choice and Assessment of Statistical Predictions. Journal of the Royal Statistical Society: Series B (Methodological), 36(2):111–133, January 1974. ISSN 00359246. doi:10.1111/j.2517-6161.1974.tb00994.x. URL https://onlinelibrary.wiley.com/doi/10.1111/j.2517-6161.1974.tb00994.x.

- Verma and Zhang (2019) Saurabh Verma and Zhi-Li Zhang. Stability and generalization of graph convolutional neural networks. In Proceedings of the 25th ACM SIGKDD International Conference on Knowledge Discovery & Data Mining, pages 1539–1548, 2019.

- Vovk et al. (2005) Vladimir Vovk, Alex Gammerman, and Glenn Shafer. Algorithmic Learning in a Random World. Springer-Verlag, Berlin, Heidelberg, 2005. ISBN 0387001522.

- Zhong et al. (2017) Kai Zhong, Zhao Song, Prateek Jain, Peter L Bartlett, and Inderjit S Dhillon. Recovery guarantees for one-hidden-layer neural networks. In International conference on machine learning, pages 4140–4149. PMLR, 2017.

Appendix A Appendix

A.1 Complete Proof of Theorem 1

Recall the leave-one-out residuals we used in DP-Lazy PI

and define a set of jackknife+ type residuals

We construct a jackknife+ type of predictive interval as a reference interval for theoretical purposes:

| (23) |

Lemma 1.

(Foygel Barber et al., 2019) For any test data , the coverage of the is:

| (24) |

Lemma 1 gives the coverage of the jackknife+ interval . This predictive interval is only constructed for theoretical purposes as a reference interval, while in practice, we avoid it due to its prohibitive computational cost. We show that the probability that our rapidly calculated predictive interval does not contain a reference interval can be bounded by a small term that related to and the DP parameters . The proof of Lemma 1 is based on the results in Foygel Barber et al. (2019).

Complete Proof of Theorem 1

Proof.

In the following equations, we intend to bound the event that the right endpoint of the interval is larger than the right endpoint of the interval for any :

| (25) | |||

| (26) | |||

| (27) |

The first inclusion from (25) to (26) holds true because the -th largest value among the set is larger than the -th largest value among the set by the definition of quantiles in (25). By the fact that , we know that . Therefore, for any , we always have

| (28) |

i.e., there exist at least number of -s, such that (28) holds true.

The symmetric event of (25) is that the left endpoint of the interval is smaller than the left endpoint of the interval for any . We can bound this event with the same technique:

| (29) | |||

| (30) |

The event that happens when either (25) or (29) happens, while from the above inclusions, these two events are both included in the event in (27).

Hence for any ,

| (31) | ||||

| (32) | ||||

| (33) | ||||

| (34) | ||||

| (35) | ||||

| (36) | ||||

| (37) | ||||

| (38) |

The above set of equations/inequalities aim to bound the event that a -relaxed lazy-DP interval doesn’t contain a jackknife+ interval based on the data exchangeability and the differential privacy in the algorithm. The probabilities are taken with respect to all the training data as well as the test data . Specifically, (33) comes from the inclusions in (27),(30); (A.1) comes from the Markov equality that for any random variable and non-negative constant ; as we calculate the sum of expectations, the exchangeability of the training data makes (35) hold true; by the fact that

we could split (35) into the form (36). we have a factor in the denominator of (35) thus the factor can be dropped by . (37) is derived by the differential privacy property in Lemma 4; the final bound in (38) holds true due to the out-of-sample stability.

If we take , by the fact that

| (39) |

we can bound the miscoverage rate for the predictive interval :

| (40) | ||||

| (41) | ||||

| (42) | ||||

| (43) |

Hence the coverage of is

∎

A.2 Proofs of Supporting Lemmas

For any two random variables , and has the joint distribution ; then the marginal distribution of is , and similarly ; has the the product distribution of and , i.e.,

Therefore, the distribution of is equivalent to the joint distribution of , where is an independent copy of , i.e., has the same marginal distribution as , but is independent with and .

To describe the “similarity” of two random vectors, we introduce the following notion of indistinguishability that is also used in Kasiviswanathan and Smith (2014), Rogers et al. (2016).

Definition 2.

(Indistinguishability (Kasiviswanathan and Smith, 2014)) Two random vectors in a space are -indistinguishable, denoted , if for all , we have

The following lemma is utilized in the course of proof for Lemma 3.2 in Rogers et al. (2016). The proof is provided as well for the completeness of the paper.

Lemma 2.

Let be a -DP algorithm,and is the pretrained estimator with the full training data . Denote as the leave-one-out data set with the -th data deleted. Then for all , we have

| (44) |

i.e., for an independent copy of , we have

| (45) |

for any .

Proof.

Fix any set . We then define for any realization of . We now have

| (46) |

for any realization for . Here the last line in (46) comes from the fact that is differentially private. By multiplying to the RHS and LHS in (46), we have

| (47) | |||

| (48) | |||

| (49) | |||

| (50) | |||

| (51) | |||

| (52) | |||

| (53) |

With a similar argument, we can prove its symmetric counterpart:

| (54) |

Since , we finish the proof that is ()-indistinguishable with given the other data points , i.e.,

∎

Lemma 3.

The dependency of the leave-one-out estimator on the -th data point can be controlled by

| (55) |

i.e., for an independent copy of for ,

| (56) |

Proof.

Recall the definition of :

Lemma 4.

(Closeness of in-sample and out-of-sample stability) For any , we have

| (59) | |||

| (60) |

Remark 1.

As we can see, illustrates the change of out-of-sample prediction when a training data is removed in the model training, while depicts the change of in-sample prediction when a training data is removed. Normally the in-sample and out-of-sample stability are different and have to be considered separately as in Foygel Barber et al. (2019), but due to the differential privacy in the training algorithm, we can show through the following lemma that these two types of stabilities can be bridged by differential privacy, therefore we only need out-of-sample stability in the algorithm.

Proof.

First, we know by the definition of and and the fact that , we know that ; therefore, for any and , we have

| (61) | |||

| (62) | |||

| (63) | |||

| (64) | |||

| (65) |

Here (62) and (65) holds true due to the conditional independence; (63) is from Lemma 3. By the same argument, we have

| (66) | |||

| (67) |

Hence for any ,

| (68a) | |||

| (68b) | |||

| (68c) | |||

| (68d) | |||

| (68e) | |||

for any . ∎

Appendix B Appendix. Discussion of the Stability Condition

B.1 The Laplacian Mechanism

Given an algorithm and a norm function over the range of , the sensitivity of is defined as

| (69) |

(Usually the norm function is either or norm.)

Based on the definition of sensitivity defined as Equation 69, the Laplacian mechanism to construct differential private algorithm is as follows (Koufogiannis et al., 2015, Holohan et al., 2018): for an algorithm (or function) , the random function satisfies -differential privacy, where follows a Laplacian distribution :

Specifically, let be the algorithm to find the empirical risk minimization(ERM) on a certain data set :

Let be it sensitivity defined in Equation 69.

Let and be the ERM estimations respectively on the full training data and leave-one-out data ;

Consider the -DP algorithm , and we have the -DP estimators

Assumption 1.

The parametrization of neural network is differentiable with a locally Lipschitz differential .

Assumption 2.

(Local strong convexity of neural networks) For all , is locally Lipschitz continuous w.r.t with Lipschitz constant , and is Lipschitz continuous with a Lipschitz constant , i.e., for any with :

where is defined as the empirical norm.

According to Lemma 1, for one-hidden-layer neural networks with activation function being ReLU, sigmoid or tanh, can be satisfied. We’ll revisit this assumption in Section B.2.

Theorem 1.

Consider the Laplacian mechanism with -DP parameters. Suppose Assumptions 1 and 2 and , with probability at least for some constant , we have

| (70) |

Proof.

Step 1. Show that and are both in the neighborhood of with high probability.

Recall the fact that , by triangle inequality and the fact that , we have

Therefore, by the property of that , we have

On the other hand, is obtained by adding perturbations around the , therefore we have

Hence with probability at least , we have and .

Step 2. Show that and are close.

Recall that and , denote , and the linearized function of around as

then is the ERM of the linearized function on the LOO data set:

| (71) |

Define the gradient flow of in the parameter space as , which satisfies and solves the ODE:

| (72) |

On the other hand, as , we define the gradient flow on the neural network initialized at ( i.e., ) and solves the ODE:

| (73) |

By Theorem 2.3 in Chizat et al. (2020), we can show that

| (74) |

By the strong convexity and continuity of , we can show that converge to its minimizer (take ) fast:

| (75) |

where is strong convex and Lipschitz continuous, and is the smallest eigenvalue of .

By Lemma B.1 in Chizat et al. (2020), if is strong convex with -Lipschitz continuous gradient and the smallest eigenvalue of lower bounded by for , then can converge fast to the minimizer :

| (76) |

Hence,

| (77) | ||||

| (78) | ||||

| (79) |

here we take .

By the result from the first step that and w.h.p, as well as the fact that and , we have

| (80) |

Step 3. Complete the statement

With probability at least , we have

Hence, suppose , we have with probability at least for some ,

∎

B.2 Local Strong Convexity of Neural Network

Researchers have found that for the parameter recovery setting of neural networks, recovery guarantees can be provided if the neural network is initialized around the ground truth, due to the local strong convexity in the neighborhood of the ground truth parameters, see Zhong et al. (2017). Also, Li and Yuan (2017) shows that in general, the convergence of NN parameters can be split into two phases. Once the parameters fall into a -one point strong convex regime near the ground truth, the convergence changes to phase II, leading to fast parameter convergence to the ground truth.

Lemma 1.

(Positive Definiteness of Hessian near the ground truth in one-hidden-layer neural network (Zhong et al., 2017)) If are sampled i.i.d. from the distribution: with being the activation functions as ReLU, sigmoid or tanh, and being the number of nodes in the hidden layer, we can show that as long as , if , where we have with probability at least ,

| (81) |

where is the -th singular value of , , , and (defined in Zhong et al. (2017)) is related to the activation function.

Appendix C Appendix. Additional Experiment Results

In this section, we include experiment results in different settings.

C.1 Effect of stopping time when training the neural networks

To look into the effects of stopping time of the full-data model, we increase the maximum number of epochs when training neural network models in all three mentioned methods (including all leave-one-out models in the jackknife+ method).

We generate the data in the same way as described in Section 5.1 with dimension , i.e., , where , and

| (82) |

We construct the prediction intervals using jackknife+, lazy finetune and DP-Lazy PI using the training and calibration with and . When training the neural network with hidden layers, we increase the maximum number of epochs from (as in Section 5.1) to to avoid the early stopping of the NN training, while we keep the other parameters unchanged: and batch size .

The results in Figure C.1 demonstrate that lazy methods reliably maintain a coverage above , exhibit significantly faster computation times compared to jackknife+, and yield more accurate prediction intervals. Moreover, an examination of Figure 2(b) reveals that increasing the maximum number of epochs negatively impacts jackknife+’s performance while enhancing the accuracy of lazy methods. Since lazy methods require training the full model only once, increasing the stopping time has minimal impact on computation time. In contrast, Jackknife+ experiences a dramatic increase in computing time due to the multiplication of training time by the training sample size. This disparity makes the computation more prohibitive for jackknife+. In terms of the interval width, the results depicted in the right panel Figure C.1 highlight the superior interval width accuracy achieved by lazy methods.

This result also reconciles the performance of simulated data and real data experiments that for high-dimension data, jackknife+ tends to give a much wider and more unstable prediction interval than DP-Lazy PI.

We also investigate the effect of increasing the maximum number of epochs on real data sets, specifically the BlogFeedback data set and Medical Expenditure Panel Survey 2016 data set. The results demonstrate a similar phenomenon as depicted in Figure C.2, highlighting extended training epochs on the performance of the models make the jackknife+ prediction intervals worse(wider).

|

| (a) BlogFeedback data set, max #epochs=20 |

|

| (b) Medical Expenditure Panel Survey 2016 data set, max #epochs=20 |

C.2 Effect of batch size when training the neural networks

All the experiments in the main paper have the batch size given the training size when training the neural networks. In this section, we give the real data experiment results when the batch size is set to be and compare the results from different methods.

As the batch size set to be 1 when training the neural network, Figure C.3 shows that jackknife+ gets worse (wider) prediction intervals compared to Figure 3, due to the more severe overfitting problem.

|

| (a) BlogFeedback data set, batch size=1 |

|

| (b) Medical Expenditure Panel Survey 2016 data set, batch size=1 |