Heterogeneous Autoregressions in Short Panel Data Models††thanks: We are grateful to Alexander Chudik and Ron Smith for helpful comments and suggestions.

Abstract

This paper considers a first-order autoregressive panel data model with individual-specific effects and a heterogeneous autoregressive coefficient. It proposes estimators for the moments of the cross-sectional distribution of the autoregressive coefficients, with a focus on the first two moments, assuming a random coefficient model for the autoregressive coefficients without imposing any restrictions on the fixed effects. It is shown that the standard generalized method of moments estimators obtained under homogeneous slopes are biased. The paper also investigates conditions under which the probability distribution of the autoregressive coefficients is identified assuming a categorical distribution with a finite number of categories. Small sample properties of the proposed estimators are investigated by Monte Carlo experiments and compared with alternatives both under homogenous and heterogeneous slopes. The utility of the heterogeneous approach is illustrated in the case of earning dynamics, where a clear upward pattern is obtained in the mean persistence of earnings by the level of educational attainments.

Keywords: Dynamic panels, categorical distribution, random and group heterogeneity, short panels, earnings dynamics

JEL Classification: C22, C23, C46

1 Introduction

The importance of cross-sectional heterogeneity in panel regressions is becoming increasingly recognized in the literature. When the time dimension of the panel, , is short, significant advances have been made in the case of random coefficient models with strictly exogenous regressors, for example, Chamberlain (1992), Wooldridge (2005), Arellano and Bonhomme (2012), Bonhomme (2012) and Graham and Powell (2012). A trimmed version of the mean group estimator proposed by Pesaran and Smith (1995) can also be applied to ultra short panels when the regressors are strictly exogenous. See Pesaran and Yang (2023). In contrast, there are only a few papers that consider the estimation of heterogeneous dynamic panels when the time dimension is short.

There are some limitations to applying existing estimation methods to such heterogeneous short dynamic panels. The generalized method of moments (GMM) estimators applied after first-differencing by Anderson and Hsiao (1981, 1982), Arellano and Bond (1991), Blundell and Bond (1998), and Chudik and Pesaran (2021), allow for intercept heterogeneity but not if the autoregressive (AR) coefficients are heterogeneous and, as shown in this paper, will lead to biased estimates and distorted inference. Gu and Koenker (2017) and Liu (2023) consider estimation of panel AR(1) models with exogenous regressors using Bayesian techniques. While they assume random coefficients on strictly exogenous regressors, they still impose homogeneity on the AR coefficients. The mean group and hierarchical Bayesian estimators proposed by Hsiao et al. (1999) allow for heterogeneity but require that is reasonably large relative to . Baltagi et al. (2008) provide a review of the estimators for heterogeneous linear panel data models with a moderate size .

When is reasonably large, Okui and Yanagi (2019) and Okui and Yanagi (2020) propose non-parametric estimators for the distribution of sample mean, autocovariances and autocorrelations, and their density functions. Also for moderate values of , analytical, Bootstrap, and Jackknife bias correction approaches have been also proposed to deal with the small sample bias of the mean group and other related estimators. See Pesaran and Zhao (1999) on the mean group estimator, as well as Okui and Yanagi (2019) and Okui and Yanagi (2020). Even with bias corrections, cannot be too large compared with , since a valid inference based on the asymptotic distribution often requires for some constant . In short, none of the above approaches are appropriate and can lead to seriously biased estimates and distorted inference when is small and fixed with

Nonetheless, heterogeneity in dynamics can play an important role in many empirical studies using panel data models with moderately short , for example, earnings dynamics studied by Meghir and Pistaferri (2004), unemployment dynamics by Browning and Carro (2014), and firm’s growth by Liu (2023). Parametric approaches are widely used to take account of dynamic heterogeneity, particularly in the analyses of earnings dynamics using the Panel Study of Income Dynamics (PSID) data. Meghir and Pistaferri (2004) categorized individuals into three educational groups and assumed that autoregressive coefficients are heterogeneous across groups but homogeneous within groups.111However, the within-group homogeneity assumption is not supported by the data. See Section 28.11.8 of Pesaran (2015). Browning et al. (2010) focused on white males with a high-school degree and showed that allowing for heterogeneity makes a substantial difference to the estimates. Alan et al. (2018) developed a structural model allowing for heterogeneous parameters in both consumption and income dynamic processes, and used mean group estimation to deal with heterogeneity. Browning and Carro (2014) studied the unemployment dynamics of Danish workers and found evidence of heterogeneity. These studies should be commended for their explicit treatment of heterogeneity, yet many empirical studies abstract from heterogeneity in dynamics not because they are not present, but because they are difficult to accommodate in dynamic panels when is short.

The paper first shows that some existing GMM estimators of panel AR(1) models are asymptotically biased under heterogeneity of the AR(1) coefficients, , and derives analytical expressions for their bias in simple cases. It then proposes estimators for the moments of , using cross-sectional averages of the autocorrelation coefficients of first differences, rather than the cross-sectional average of the estimates of under the mean group estimation. In terms of the estimation approach, the most relevant paper to ours is by Robinson (1978), who considered a random coefficient AR(1) model without fixed effects. He proposed identifying the moments of the as functions of the autocovariance of different orders, which he then used to estimate the unknown parameters of an assumed parametric distribution for .

In our analysis, we allow for both individual fixed effects and heterogeneous AR coefficients. We eliminate the fixed effects by first differencing, then derive two estimators for the moments of for , a relatively simple estimator based on autocorrelations of first differences denoted by FDAC, and a generalized method of moments estimator based on autocovariances of first differences denoted by HetroGMM. We do not make any assumptions about the fixed effects, , and allow them to have arbitrary correlations with , but require the underlying AR(1) processes to be stationary and assume and the error variances are independently distributed. We also provide estimators for the distribution of assuming its underlying distribution is categorical. It is possible to extend our analysis to higher-order panel AR processes and possibly dynamic panels with exogenous regressors. However, these important extensions are outside the scope of the present paper.

We compare our proposed estimator to the kernel-weighting likelihood estimator proposed by Mavroeidis et al. (2015), which we refer to as the MSW estimator. Based on the deconvolution technique, Mavroeidis et al. (2015) propose a likelihood estimator for the cross-sectional distribution of conditional on the initial observations, . Assuming independently distributed Gaussian errors with cross-sectional heteroskedasticity, Mavroeidis et al. (2015) show that the unknown distribution of heterogeneous coefficients can be identified provided the linear operator that maps the unknown distribution to the joint distribution of data is complete (or “invertible”). They provide an estimation algorithm for the parametric version of their estimator assuming the heterogeneous coefficients and ) follow a multivariate normal distribution. The estimation algorithm becomes computationally very demanding if the parametric assumption about the distribution of is relaxed.

There are also Bayesian approaches in the literature that we do not pursue in this paper. Liu et al. (2017) provide a recent example that builds on Hsiao et al. (1999), and develop a hierarchical Bayesian approach for panel AR(1) models with correlated random coefficients.222Liu et al. (2017) also consider non-stationary initial values but require them to be normally distributed. See p. 1545 in Liu et al. (2017).

We investigate the small sample properties of the proposed FDAC estimators of and using Monte Carlo experiments. The simulations show that the relatively simple FDAC estimator performs better than the HetroGMM estimator uniformly across different sample sizes, and is robust to non-Gaussian errors and conditional error heteroskedasticity. The latter is particularly relevant as heteroskedastic error variances play an important role in empirical studies of earnings dynamics. See, for example, MaCurdy (1982), Abowd and Card (1989), and Gu and Koenker (2017). We then compare the small sample properties of the FDAC estimator of with a number of GMM estimators derived under homogeneity (denoted by HomoGMM), including the popular Arellano and Bond (1991), AB, and Blundell and Bond (1998), BB, estimators. The simulation results confirm the neglected heterogeneity bias of the HomoGMM estimators, and show that the FDAC estimator of performs well for all values of and and , so long as the underlying processes are stationary. This is true for bias, root mean square errors, and the size of the tests of the hypotheses involving the first and the second order moments of . It is, however, worth highlighting that the FDAC estimator can result in biased estimates and size distortions if there are major departures from the stationary distribution.

Using Monte Carlo experiments we also provide a limited comparison of the MSW and FDAC estimators, and find that the small sample properties of the MSW estimator are sensitive to the degree of heterogeneity and underlying distribution of . The MSW estimator can be severely biased when the degree of heterogeneity is relatively high. The small sample properties of the MSW estimator also depend on the assumed distribution of .

The plugged-in estimator for the parameters of the categorical distribution is also shown to be large consistent with the root mean squared errors shrinking steadily in . But precise estimation of these parameters requires very large values of , since they are functions of the inverse of estimated variances, which could be close to zero in finite samples. The fact that very large values of are required for reliable estimation of the categorical distribution has also been observed by Gao and Pesaran (2023) in the context of pure cross section regressions with heterogeneous coefficients.

We also provide an empirical application using five and ten yearly samples from the PSID dataset over the 1976-1995 period to estimate the persistence of real earnings. To this end, we extend the basic panel AR(1) model to allow for linear trends. Following the empirical literature we report estimates for three educational categories (high school dropouts, high school graduates, and college graduates) and all three categories combined. We find comparable estimates for the linear trend coefficients across sub-periods and educational categories, around 2 per cent per annum. The FDAC estimates of mean persistence for the sub-periods 1991–1995 and 1986–1995 fall in the range of 0.570–0.734, and tend to rise with the level of educational attainment, with college graduates showing the highest degree of persistence. No such patterns are observed for other estimates, which are around 0.3, 0.9 and 0.41 for the AB, BB and MSW estimators, respectively. The FDAC estimates of for all three categories combined are statistically significant and are given by 0.100 (0.042) and 0.129 (0.023) for the sub-periods 1991–1995 and 1986–1995, respectively, providing further evidence of heterogeneity in real earnings persistence.

The rest of the paper is set out as follows. Section 2 sets out the model and assumptions. Section 3 shows that the HomoGMM estimators are biased in the heterogeneous panel AR(1) models. Section 4 derives identification conditions for the moments of . Section 5 considers group heterogeneity and how their parameters can be estimated. Section 6 proposes the FDAC and HetroGMM estimators for the moments of . The respective asymptotic distributions are also derived. Section 7 evaluates the performance of the FDAC, HomoGMM, and MSW estimators by Monte Carlo simulations. Section 8 presents the empirical application results for the earnings dynamic process. Section 9 concludes. Additional Monte Carlo evidence and empirical results can be found in the online supplement.

2 Model and assumptions

Consider the following first-order autoregressive panel data model

| (2.1) |

where is observed across cross section units over the periods with a total of observations . We introduce the following assumptions.

Assumption 1

(errors) (a) The idiosyncratic errors, , are cross-sectionally and serially independent over and , and for all .

Assumption 2

(autoregressive coefficients) (a) The autoregressive coefficients, , for are independent draws from the probability density function , defined over the bounded support, , with mean and variance and , for all and (b) are distributed independently of the error variances, . (b) and are distributed independently.

Assumption 3

(initialization) The dynamic processes in (2.1) have started from a long time prior to date .

Assumption 4

(individual effects) The individual specific effects, , are bounded, , but could be correlated with and/or .

Assumption 1 is standard in short dynamic panels, but it rules out the possibility of unconditional time series heteroskedasticity, namely it does not allow to differ across . However, this assumption does not rule out conditional heteroskedasticity, such as GARCH effects. Assumptions 2 and 3 are required for the identification of the moments of , which are the parameters of interest. Assumption 4 imposes minimal restrictions on the fixed effects. Admittedly, the assumption that all processes are initialized from a distant past, is restrictive. We investigate the effects of departures from this assumption via Monte Carlo experiments. But its relaxation is beyond the scope of the present paper.

Before introducing our identification and estimation strategies, we illustrate the asymptotic bias of the HomoGMM estimators of that neglect heterogeneity of over and proceed assuming that heterogeneity of is a reasonably satisfactory working assumption.

3 Neglected heterogeneity bias

Under homogeneity where for all , can be consistently estimated by the method of moments after eliminating by first-differencing. We begin our analysis by showing the HomoGMM estimators are biased when are heterogeneous. The extent of the bias depends on the degree of heterogeneity. To simplify the exposition, without loss of generality, we consider the case where , the minimum required to identify . For the Anderson-Hsiao (AH) estimator, , given (2.1) we have

| (3.1) |

Also under Assumptions 2 and 3, for a given we have which can be written equivalently in terms of as

| (3.2) |

It is now easily seen that, for , we have

and hence

| (3.3) |

Also . Using these results in (3.1) for and , now yields (as )

In the homogeneous case (), we have , as expected. Under heterogeneity, is clearly not a consistent estimator of . The extent of the bias depends on the joint distribution of and . When and are independently distributed we obtain the following expression for the asymptotic bias of

Since , then , and , and since is a convex function of then by Jensen inequality , and it follows that , namely we expect the AH estimator to be downward biased. The equality holds only and only if for all . The magnitude of the asymptotic bias depends on the distribution of . For example, suppose are random draws from a uniform distribution centered at , then we have where for . To ensure that we also require that . The homogeneous case arises when . The degree of heterogeneity of measured by its standard deviation is . For this distribution we obtain

where . It is easily seen that with . The magnitude of the asymptotic bias of the AH estimator for and will be around and respectively. The asymptotic bias of AB and BB estimators under heterogeneous slopes are derived in Section S.2 of the online supplement.

Asymptotic bias, even if small, can lead to substantial size distortions when is sufficiently large. See Section 7.3 for Monte Carlo evidence on the bias and size distortions of AH and other HomoGMM estimators.

4 Identification of moments of the AR coefficients

Based on the representation (3.2), moments of can be identified by constructing moment equations, where moments of are functions of covariances of first differences. First, the conditional second moment of the first-differenced process can be calculated as . Since by Assumption 2, and are distributed independently, then

| (4.1) |

Similarly, using (3.3)

| (4.2) |

It is also instructive to write the above expression more explicitly as

| (4.3) | ||||

| (4.4) |

As can be seen, and are general functions of , the parameters of the cross-sectional distribution of .

4.1 Identification conditions

In this section, we formally establish identification conditions of on the minimum number of periods used in estimation, . Since under Assumption 2, we have bounded moments of polynomial functions of , i.e., , then it follows . Since the distribution of has a bounded support with for all and , it also follows that . Combining the above results with , it follows from (4.1) that . Denote the -order autocorrelation coefficients of first differences as given by

| (4.5) |

for , with . Using (4.1) and (3.3), for , can be written as

| (4.6) |

Suppose that can be consistently estimated using the moment estimators of and . Then the identification condition of can be derived by the system of equations in (4.6). For , , which can be equivalently written as

| (4.7) |

For , , and using (4.7) yields

| (4.8) |

Similarly, for we have , which yields

| (4.9) |

The variance of is now given by

| (4.10) |

For ,

and upon using the results of the lower-order moments we obtain

| (4.11) |

Higher-order moments of can be obtained similarly. To identify the order moment of requires consistent estimation of for .

Suppose now that observations on the unit are available over the period . Then we have data on over the period , and a consistent estimator of is given by

| (4.12) |

Therefore, we must have , as to identify from available observations.

Remark 1

5 Panel autoregressions with group heterogeneity

In many empirical applications, it is of further interest to go beyond estimation of moments and learn about the nature of heterogeneity. One particular feature is heterogeneity across groups. When group characteristics are known, the dynamic panel can be estimated over sub-groups, or the panel could be augmented with group-specific interactive effects. But when individual characteristics are not observed, it is still possible to estimate group-specific probabilities centered on a suitable partition of the parameter space. In the case of heterogeneous we could postulate the following categorical distribution assuming that possible outcomes of can be grouped into categories:

with , , and for . Under this specification, the object of the exercise is to estimate unknowns with . To identify , note that

Hence we must have to identify the unknown parameters. Also to identify the first moments, we need . Combining these two inequalities, we have . These are order conditions, and we still require rank conditions that ensure a unique solution for . But it is clear that the number of groups that can be entertained is closely related to the size of , which rises linearly in . In the simplest possible case with , let , , and , and we need the following moment conditions

where the moments , for can be consistently estimated using the pooled estimator of given by in (4.12) with . Since by assumption , then we obtain three solutions for that must coincide:

| (5.1) |

Let . Eliminating the common factor from the denominators of the above yields

The above equations have the unique solution

| (5.2) |

where

| (5.3) |

Therefore, given the moments , and , and can be obtained as the solutions to the following quadratic equation333See Gao and Pesaran (2023) for a similar solution in the case of heterogeneous cross-sectional regressions.

| (5.4) |

Namely

| and | (5.5) |

Clearly, or are identified from the moments if condition (5.3) holds. For real solutions to exist, it is required that . Once and are obtained, can then be identified using (5.1). A consistent estimator of can now be obtained by replacing , for by their estimators suggested in Sections 6.1 and 6.2.

Remark 2

Other parametric distributions for can also be considered. Prominent choices are uniform and beta distributions. In the case of a uniform distribution it is important that is defined on a bounded region that does not include , otherwise, the condition with could be violated. For example, suppose that is distributed uniformly over , then

It is clear that when , the condition is not met.

Remark 3

Further complications arise when have started from a finite past, or if we wish to allow for exogenous regressors, even if the regressors are strictly exogenous.

Example 1

As an example, suppose that is distributed uniformly over with , but the categorical model with is used as an approximation. In this setting Using this result in (5.2) we have

and the two solutions are given by and . Also, .

6 Estimation of moments of the AR coefficients

6.1 Method of moments estimator based on autocorrelations

When the moments of are just identified or is very short, estimation of moments can be carried out straightforwardly by the method of moments using the sample analogues of given by (4.12). We denote this estimator by FDAC. Let , then the FDAC estimator of is given by

| (6.1) |

| (6.2) |

and

| (6.3) |

where for are given by (4.12).

6.2 Generalized method of moments estimator based on autocovariances

The FDAC estimator combines equally-weighted time averages of available data points to estimate different for , then plug them into equations (6.1) and (6.2). An alternative and arguably more efficient approach would have the estimation based on the sample moments of rather than , which allows us to consider the optimum weighting of the moment conditions at different periods.

6.2.1 Generalized method of moments estimator of

Given (4.5), the moment condition (4.8) can be written equivalently as

| (6.4) |

which yields a total moment conditions for , requiring that .

The FDAC estimator can now be used to obtain initial estimates for the generalized method of moments (HetroGMM) estimator. When is small, note that may use more information from data than , as estimating of different uses respective data points rather than the subset of data points. The moment conditions in (6.4) can be written as

where is the true value of and for a given value of ,

To optimally combine these moment conditions, let

and

Then

where . Using (6.4), it readily follows that . The HetroGMM estimator of is given by

where is a positive definite stochastic weight matrix, and for any , it tends to a non-stochastic positive definite matrix as . The most efficient HetroGMM estimator is given by

| (6.5) |

where is the optimal weight matrix with

Given (6.4), , and are cross-sectionally independent, then

It is difficult to derive an analytical expression for , but for a given value of , can be consistently estimated by its sample mean as

| (6.6) |

A standard two-step GMM estimator of can now be obtained using to estimate the optimal weight matrix in the first step. When , substituting into (6.6) yields the following two-step HetroGMM estimator

| (6.7) |

where

| (6.8) |

It is also possible to obtain an iterated version of the above, where is used to obtain a new estimate of , namely , and so on. But there seems little gain in doing so since is asymptotically efficient. The asymptotic distribution of is given by

| (6.9) |

where can be consistently estimated by

| (6.10) |

where

Remark 4

The above estimators should work fine asymptotically under , so long as the time variations of is stationary, in a sense that . One important example is when has a stationary GARCH specification, for example, if

where , , and the processes of have started in a distant past. Note that for the above GARCH processes, .

6.2.2 Generalized method of moments estimator of

Similarly, the HetroGMM estimator of can also be obtained based on the equation below for ,

| (6.11) | ||||

Let and

Denote , and , where and are vectors (with ). Then, the two-step HetroGMM estimator of the second moment can be derived as

| (6.12) |

where the initial estimator can be the FDAC estimator of given by equation (6.2), and . Finally, the asymptotic distribution of can be derived as the following

| (6.13) |

where is the true value of , and can be consistently estimated by

| (6.14) |

6.3 Plug-in estimator of

Consider now the estimation of . By definition, it can be written as . By plugging estimators into the above formula, we derive a consistent estimator of the variance given by

| (6.15) |

Note that is a valid estimator if , which requires to be sufficiently large. Suppose the asymptotic distribution of is the following . Then the asymptotic distribution of plug-in estimator is given by

| (6.16) |

where derived by the Delta method. can be consistently estimated by , where is a consistent estimator of .

7 Monte Carlo experiments

7.1 Data generating process

The dependent variable is generated as

where measure the mean of stationary , and .

We consider both Gaussian errors, , and non-Gaussian errors, , where , and is a chi-squared variate with two degrees of freedom. captures both cross-sectional and conditional heteroskedasticity generated as GARCH(1,1), given by , with , , , and .444The coefficients in the GARCH(1,1) model can be heterogeneous across . In this case, the FDAC and HetroGMM estimators are still applicable. The case where errors are conditionally homoskedasticity is obtained as a special case setting . The and processes are generated with the initial values , , and . For all , the first 51 time series observations are discarded, and the estimation of the moments of are based on .

We experiment with two distributions for : uniform with a medium and a high degree of heterogeneity, and a categorical distribution with two groups as follows.

-

(a)

Uniform distributions: , , with and , which gives and .

-

(b)

Categorical distribution: with probability , and with probability . We set , , and , thus yielding , and .

Individual fixed effects are generated as with , which allows for non-zero correlations between and .

We carry out replications for the experiments that compare the small sample performances of FDAC, HetroGMM, and a number of estimators proposed in the literature for the homogeneous slope case (denoted by HomoGMM), specifically the estimators proposed by Anderson and Hsiao (1981, 1982) (AH), Arellano and Bond (1991) (AB), Blundell and Bond (1998) (BB), and the augmented Anderson-Hsiao (AAH) estimator proposed by Chudik and Pesaran (2021), as well as the FDLS estimator due to Han and Phillips (2010).555We have downloaded the codes of the AH, AB, BB, and AAH estimators from the supplementary materials of Chudik and Pesaran (2021) using the link: https://www.econ.cam.ac.uk/people-files/emeritus/mhp1/fp21/CP_AAH_paper_July_2021_codes_and_data.zip. We are grateful to Alexander Chudik for making the codes publicly available. For experiments that compare our proposed estimator with the MSW estimator proposed by Mavroeidis et al. (2015), we use replications as it takes a substantial amount of time to compute the MSW estimator.666We have downloaded the codes of the MSW estimator used in empirical applications from the supplementary materials of Mavroeidis et al. (2015) using the link: https://drive.google.com/file/d/1hdRFpcWo3r88YV_5Kc40ur-siCYGSBDN/view?usp=sharing. We are grateful to Yuya Sasaki for also sharing the codes of the MSW estimator used in their Monte Carlo experiments by private correspondence.

7.2 Comparison of FDAC and HetroGMM estimators

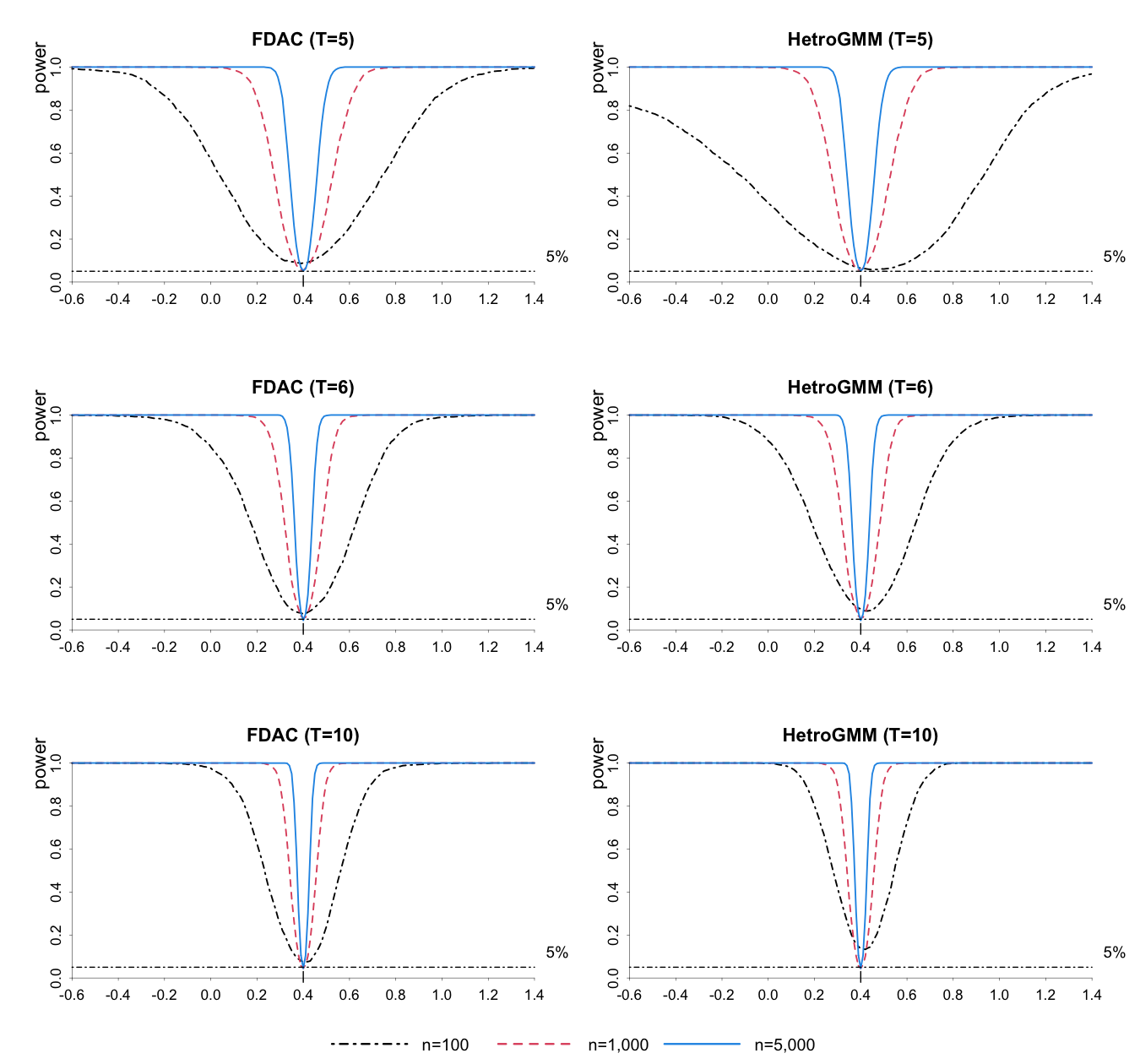

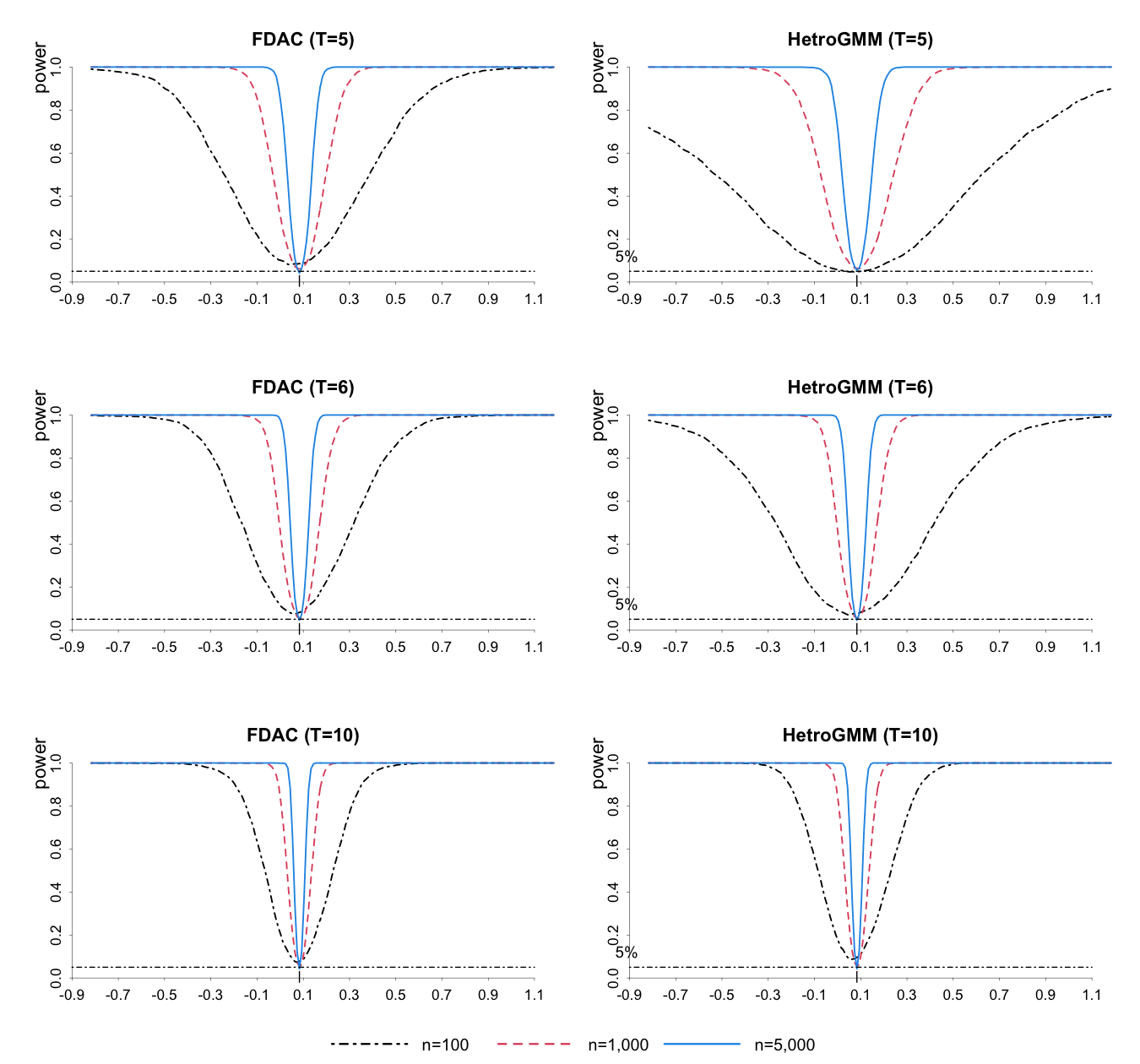

Detailed results of the Monte Carlo experiments are summarized in the online supplement. Tables S.1 to S.2 of the online supplement give bias, root mean square errors (RMSE), and size of the FDAC and HetroGMM estimators for and with and , in the case of Gaussian errors with GARCH effects. The results cover both cases where are generated as uniform with and (see (a) above), and categorical as specified under (b). The associated empirical power functions are displayed in Figures S.1 to S.4 of the online supplement. As can be seen, the FDAC estimator has uniformly smaller bias across all sample sizes, and lower RMSE and greater power when . This could be because the FDAC estimator uses averages of the individual sample moments both over time and across units, and is not subject to the many moments problems. Most importantly, tests based on the FDAC estimator are not adversely affected as is increased with relatively small, and its size is mostly around the nominal size of five per cent. But tests based on the HetroGMM estimator, tend to over-reject as is increased when is relatively small (). These results are in line with the results obtained in the literature when GMM is applied to homogeneous dynamic panels.

The simulation results reported in Tables S.17–S.24 in the online supplement also show that the performance of the FDAC estimator is reasonably robust to non-Gaussian errors and/or GARCH effects. The RMSE and size distortions of the FDAC estimator increase only slightly as we move from Gaussian to non-Gaussian errors and allow for GARCH effects.

Overall, the FDAC estimator outperforms the HetroGMM estimator and seems to be reasonably robust to non-Gaussian errors and GARCH effects. It is also simple to compute. In what follows we focus on comparing the FDAC estimator with the HomoGMM estimators as well as the MSW estimator that allows for slope heterogeneity.

7.3 Comparison of FDAC and HomoGMM estimators

Since it is not known if the heterogeneity bias is serious, it is natural to ask if the FDAC estimator continues to perform equally well under homogeneity (, and if its performance under homogeneity is comparable to the HomoGMM estimators of . Tables 1, 2, and 3 report the bias, RMSE, and size of the FDAC, FDLS, AH, AAH, AB, and BB estimators under slope homogeneity (, and under two uniformly distributed heterogeneous slope cases with and . All experiments allow for unrestricted heterogeneous intercepts (fixed effects). The results in these tables are based on Gaussian errors and allow for GARCH effects for the sample sizes , and . Results for non-Gaussian errors with GARCH effects are provided in Tables S.3–S.5 in the online supplement.

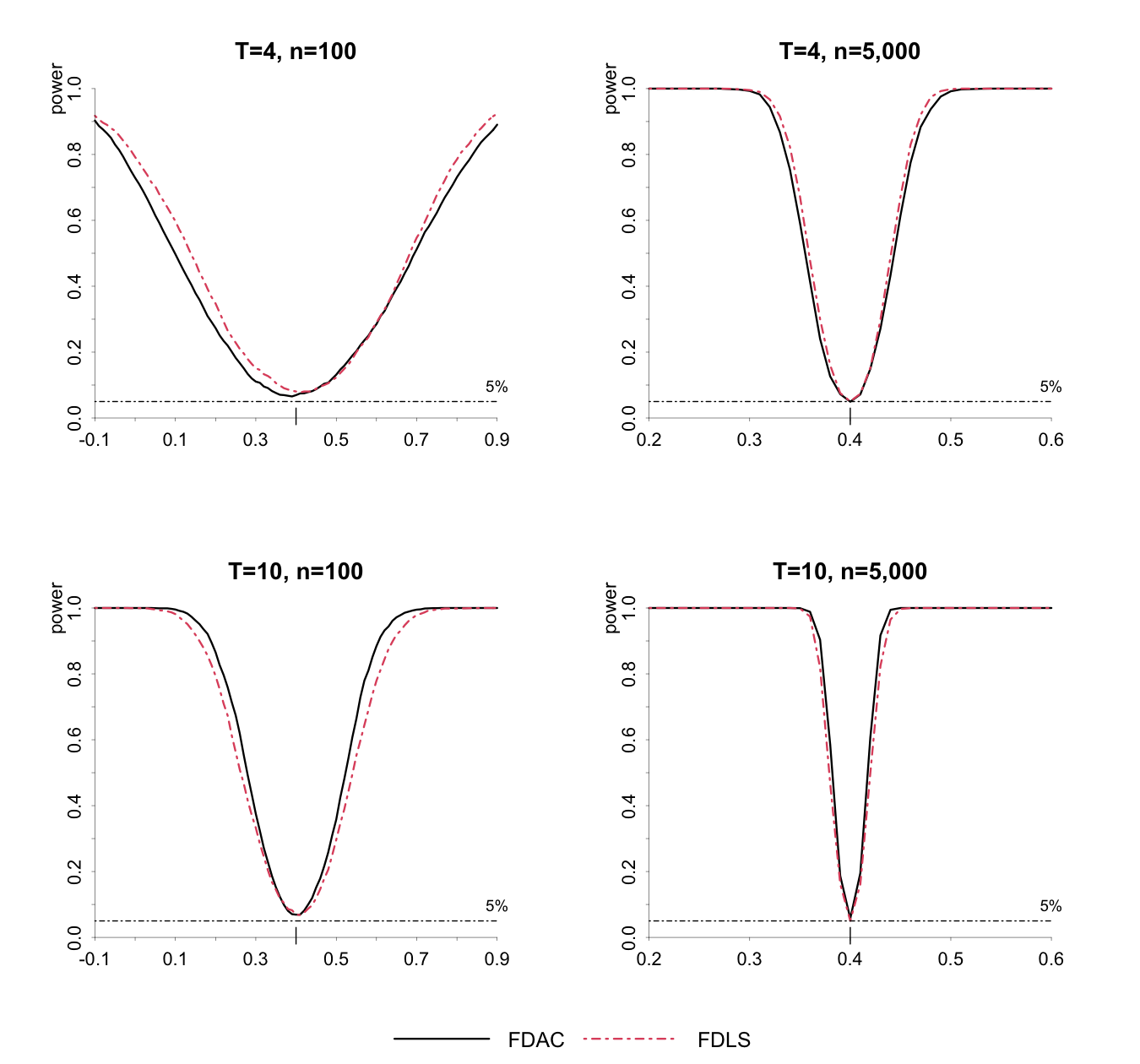

As can be seen from the results in Table 1, the FDAC estimator continues to perform well even under slope homogeneity. Its bias is close to zero and only shows a small degree of size distortions when . It is closest to the FDLS estimator since both estimators assume the initial values, , are drawn from the steady state distribution of and combine the moments by averaging them over both and . Figure S.5 in the online supplement compares the empirical power functions of the FDAC and FDLS estimators. Compared to the FDLS estimator, the FDAC estimator makes use of higher order autocorrelation of first differences that are not needed for identification of under homogeneity. As a result, the FDLS estimator is marginally more powerful than the FDAC for small , but suffers from size distortion when both and are small.

However, when comparing the FDAC and the other HomoGMM estimators (such as AAH, BB, or AB) one needs to be cautious, since these estimators do allow for the distribution of to depart from the steady state distribution of . With this in mind, we note that the FDAC estimator performs well when compared to AH and AB estimators, although it is marginally less efficient when compared to the AAH and BB estimators. Also, the FDAC estimator has less size distortion and better power performance compared to all HomoGMM estimators as is increased.

These results demonstrate the FDAC estimator is reliable and has desirable small-sample performance even in homogeneous panels with stationary outcome processes. Note that the AH and AAH estimators can be applied to homogeneous dynamic panel data models with less restrictive assumptions, including the unit root case and time series heteroskedasticity.

For the heterogeneous case, Table 2 gives the summary of the results when heterogeneity is moderate (namely ), and Table 3 provides the results when . The performance of the HomoGMM estimators deteriorates quite rapidly as the degree of heterogeneity is increased, but the FDAC estimator continues to have satisfactory properties irrespective of the degree of heterogeneity. With a moderate degree of heterogeneity (), the FDAC estimator continues to have close to zero bias and the correct size for all sample sizes under consideration. But for the HomoGMM estimators, the magnitudes of the bias are much larger and the size distortions are much more serious. In the case of high heterogeneity (, the FDAC estimator has the smallest RMSE and has the correct size, whilst the HomoGMM estimators all suffer from large size distortions. The simulation results also confirm that there is a downward bias in the AH estimator in heterogeneous panel AR(1) models. Note that with and , the simulated bias of the AH estimator is very close to the analytical value derived in Section 3. Also, the bias of the HomoGMM estimators does not diminish with increases in and/or , and as a result, the size distortions of the HomoGMM estimators become even more pronounced as and/or are increased.

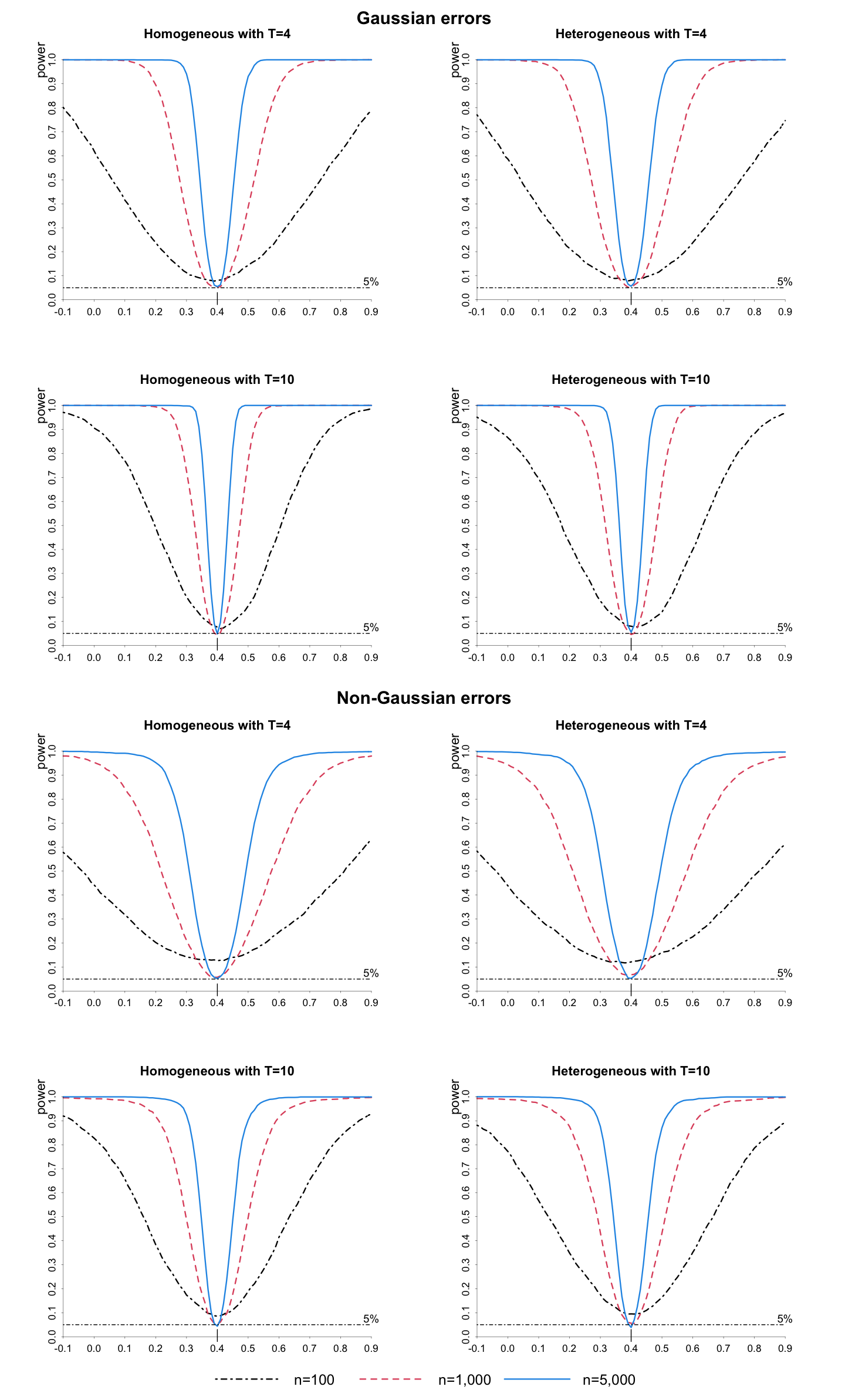

Figure 1 in the online supplement displays empirical power functions for the FDAC estimator in the case of homogeneous and heterogeneous panel AR(1) models with both Gaussian and non-Gaussian errors, and GARCH effects. The power functions become steeper as and increase. In general, the power of the FDAC estimator is similar under heterogeneous and homogeneous . But with non-Gaussian errors, the power functions become noticeably flatter, and the size distortions become more pronounced for .

| Bias | RMSE | Size () | ||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| FDAC | FDLS | AH | AAH | AB | BB | FDAC | FDLS | AH | AAH | AB | BB | FDAC | FDLS | AH | AAH | AB | BB | |||||

| 4 | 100 | -0.002 | 0.006 | 0.453 | 0.096 | -0.037 | 0.014 | 0.189 | 0.183 | 14.925 | 0.326 | 0.290 | 0.171 | 8.1 | 9.8 | 8.0 | 14.1 | 12.6 | 18.4 | |||

| 4 | 1,000 | -0.001 | 0.001 | 0.024 | 0.072 | -0.004 | 0.002 | 0.062 | 0.058 | 0.213 | 0.222 | 0.088 | 0.056 | 5.4 | 5.6 | 4.7 | 15.9 | 6.6 | 6.8 | |||

| 4 | 5,000 | -0.001 | -0.001 | 0.003 | 0.020 | -0.002 | 0.000 | 0.029 | 0.026 | 0.088 | 0.121 | 0.039 | 0.025 | 5.5 | 5.3 | 4.3 | 7.1 | 5.0 | 4.4 | |||

| 6 | 100 | -0.001 | 0.004 | -0.059 | 0.028 | -0.052 | 0.014 | 0.117 | 0.130 | 0.215 | 0.163 | 0.158 | 0.107 | 7.6 | 8.1 | 18.8 | 27.4 | 21.6 | 28.8 | |||

| 6 | 1,000 | -0.002 | 0.000 | -0.007 | 0.000 | -0.006 | 0.002 | 0.038 | 0.041 | 0.067 | 0.035 | 0.047 | 0.032 | 4.2 | 5.6 | 6.5 | 7.4 | 7.0 | 8.2 | |||

| 6 | 5,000 | -0.001 | 0.000 | -0.001 | 0.001 | -0.001 | 0.001 | 0.018 | 0.019 | 0.031 | 0.016 | 0.021 | 0.014 | 4.8 | 4.3 | 5.3 | 5.3 | 4.2 | 5.0 | |||

| 10 | 100 | 0.001 | 0.003 | -0.041 | 0.008 | -0.038 | 0.004 | 0.081 | 0.093 | 0.099 | 0.083 | 0.090 | 0.068 | 8.3 | 8.2 | 39.8 | 53.3 | 45.5 | 54.5 | |||

| 10 | 1,000 | -0.001 | 0.000 | -0.005 | 0.001 | -0.005 | 0.001 | 0.026 | 0.030 | 0.030 | 0.020 | 0.026 | 0.019 | 4.8 | 6.0 | 9.5 | 12.3 | 10.7 | 12.4 | |||

| 10 | 5,000 | 0.000 | 0.000 | -0.001 | 0.000 | -0.001 | 0.000 | 0.012 | 0.014 | 0.014 | 0.009 | 0.012 | 0.009 | 5.5 | 5.5 | 6.0 | 5.9 | 5.5 | 5.8 | |||

Notes: The DGP is given by for , and with , where errors, , are generated to be Gaussian distributed and cross-sectionally heteroskedastic with GARCH effects: , and with , , , and . The initial values are given by , , and . The AR(1) coefficients are generated to be homogeneous: for with . For each experiment, are generated differently across replications. The FDAC estimator is calculated by (6.1), and its asymptotic variance is estimated by the Delta method. “FDLS” denotes the first-difference least square estimator proposed by Han and Phillips (2010). “AH”, “AAH”, “AB”, and “BB” denote the 2-step GMM estimators proposed by Anderson and Hsiao (1981, 1982), Chudik and Pesaran (2021), Arellano and Bond (1991), and Blundell and Bond (1998). The estimation is based on for . The nominal size of the tests is set to 5 per cent. The number of replications is .

| Bias | RMSE | Size () | ||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| FDAC | FDLS | AH | AAH | AB | BB | FDAC | FDLS | AH | AAH | AB | BB | FDAC | FDLS | AH | AAH | AB | BB | |||||

| 4 | 100 | -0.001 | -0.012 | -0.035 | 0.064 | -0.074 | 0.007 | 0.192 | 0.188 | 9.664 | 0.304 | 0.339 | 0.180 | 8.6 | 10.2 | 9.8 | 14.8 | 14.0 | 19.8 | |||

| 4 | 1,000 | -0.001 | -0.021 | -0.051 | 0.021 | -0.030 | -0.013 | 0.064 | 0.064 | 0.203 | 0.182 | 0.102 | 0.061 | 5.3 | 6.6 | 9.8 | 16.0 | 9.0 | 7.4 | |||

| 4 | 5,000 | 0.000 | -0.022 | -0.068 | -0.024 | -0.025 | -0.017 | 0.029 | 0.035 | 0.108 | 0.062 | 0.049 | 0.032 | 5.2 | 12.2 | 17.8 | 14.5 | 10.5 | 10.5 | |||

| 6 | 100 | 0.000 | -0.016 | -0.101 | 0.011 | -0.084 | 0.006 | 0.123 | 0.135 | 0.235 | 0.153 | 0.184 | 0.115 | 7.5 | 8.8 | 22.7 | 23.9 | 26.0 | 30.1 | |||

| 6 | 1,000 | -0.002 | -0.022 | -0.054 | -0.010 | -0.030 | -0.007 | 0.040 | 0.048 | 0.087 | 0.038 | 0.061 | 0.036 | 4.3 | 8.3 | 17.0 | 8.0 | 12.3 | 9.6 | |||

| 6 | 5,000 | 0.000 | -0.021 | -0.048 | -0.010 | -0.022 | -0.006 | 0.019 | 0.029 | 0.057 | 0.018 | 0.032 | 0.017 | 5.3 | 19.4 | 36.4 | 8.9 | 17.2 | 7.8 | |||

| 10 | 100 | 0.002 | -0.018 | -0.063 | -0.002 | -0.056 | 0.001 | 0.086 | 0.099 | 0.117 | 0.088 | 0.107 | 0.078 | 8.3 | 7.8 | 45.0 | 52.1 | 49.0 | 58.4 | |||

| 10 | 1,000 | -0.001 | -0.022 | -0.028 | 0.001 | -0.019 | 0.003 | 0.028 | 0.038 | 0.044 | 0.023 | 0.035 | 0.022 | 5.6 | 11.7 | 23.0 | 8.7 | 17.0 | 12.3 | |||

| 10 | 5,000 | 0.000 | -0.022 | -0.024 | 0.003 | -0.013 | 0.006 | 0.013 | 0.026 | 0.029 | 0.010 | 0.019 | 0.011 | 5.3 | 34.8 | 40.1 | 4.3 | 19.1 | 10.7 | |||

Notes: The DGP is given by for , and with featuring Gaussian distributed errors with GARCH effects. The heterogeneous AR(1) coefficients are generated as case (a): with , , and . The FDAC estimator is calculated based on (6.1), and its asymptotic variance is estimated by the Delta method. “FDLS” denotes the first-difference least square estimator proposed by Han and Phillips (2010). “AH”, “AAH”, “AB”, and “BB” denote the 2-step GMM estimators proposed by Anderson and Hsiao (1981, 1982), Chudik and Pesaran (2021), Arellano and Bond (1991), and Blundell and Bond (1998). The estimation is based on for . The nominal size of the tests is set to 5 per cent. The number of replications is . See also the notes to Table 1.

| Bias | RMSE | Size () | ||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| FDAC | FDLS | AH | AAH | AB | BB | FDAC | FDLS | AH | AAH | AB | BB | FDAC | FDLS | AH | AAH | AB | BB | |||||

| 4 | 100 | 0.000 | -0.048 | -0.092 | 0.013 | -0.162 | 0.012 | 0.201 | 0.200 | 3.690 | 0.287 | 0.423 | 0.219 | 8.2 | 10.3 | 14.5 | 18.4 | 19.5 | 26.7 | |||

| 4 | 1,000 | -0.001 | -0.061 | -0.172 | -0.053 | -0.112 | -0.047 | 0.067 | 0.088 | 0.245 | 0.135 | 0.170 | 0.083 | 5.2 | 17.0 | 28.4 | 23.0 | 23.2 | 15.8 | |||

| 4 | 5,000 | 0.000 | -0.062 | -0.185 | -0.072 | -0.104 | -0.056 | 0.031 | 0.068 | 0.200 | 0.078 | 0.118 | 0.064 | 5.7 | 59.4 | 70.2 | 62.9 | 51.2 | 47.5 | |||

| 6 | 100 | 0.001 | -0.053 | -0.185 | -0.017 | -0.167 | 0.011 | 0.133 | 0.151 | 0.286 | 0.146 | 0.253 | 0.144 | 8.0 | 10.9 | 34.7 | 23.4 | 39.0 | 39.8 | |||

| 6 | 1,000 | -0.002 | -0.062 | -0.143 | -0.031 | -0.112 | -0.029 | 0.043 | 0.077 | 0.160 | 0.048 | 0.130 | 0.049 | 4.6 | 29.1 | 58.9 | 14.8 | 50.6 | 19.4 | |||

| 6 | 5,000 | -0.001 | -0.061 | -0.138 | -0.031 | -0.102 | -0.027 | 0.020 | 0.065 | 0.142 | 0.035 | 0.107 | 0.032 | 5.5 | 86.3 | 98.9 | 39.2 | 94.0 | 36.8 | |||

| 10 | 100 | 0.002 | -0.056 | -0.121 | -0.028 | -0.110 | 0.010 | 0.095 | 0.119 | 0.166 | 0.101 | 0.155 | 0.104 | 8.5 | 12.2 | 60.9 | 52.3 | 63.3 | 66.1 | |||

| 10 | 1,000 | -0.001 | -0.062 | -0.091 | -0.021 | -0.079 | -0.010 | 0.031 | 0.070 | 0.099 | 0.036 | 0.088 | 0.030 | 5.3 | 45.6 | 75.7 | 16.3 | 71.1 | 17.8 | |||

| 10 | 5,000 | 0.000 | -0.062 | -0.087 | -0.019 | -0.072 | -0.003 | 0.014 | 0.064 | 0.089 | 0.023 | 0.074 | 0.014 | 5.4 | 98.4 | 99.8 | 29.4 | 99.0 | 11.6 | |||

Notes: The DGP is given by for , and with featuring Gaussian distributed errors with GARCH effects. The heterogeneous AR(1) coefficients are generated as case (a): and with and . For each experiment, are generated differently across replications. The FDAC estimator is calculated by (6.1), and its asymptotic variance is estimated by the Delta method. “FDLS” denotes the first-difference least square estimator proposed by Han and Phillips (2010). “AH”, “AAH”, “AB”, and “BB” denote the 2-step GMM estimators proposed by Anderson and Hsiao (1981, 1982), Chudik and Pesaran (2021), Arellano and Bond (1991), and Blundell and Bond (1998). The estimation is based on for . The nominal size of the tests is set to 5 per cent. The number of replications is . See also the notes to Table 1.

7.4 Comparison of FDAC and MSW estimators

This section compares the small-sample performance of the FDAC estimator with the MSW estimator by Mavroeidis et al. (2015). Table 4 reports bias, RMSE, and size of the FDAC and MSW estimators for for , and , under heterogeneous with , and Gaussian errors with GARCH effects. The left panel of the table reports the results for , and the right panel for . The performance of the FDAC estimator is in line with the ones already discussed and as noted earlier is not affected by the degree of heterogeneity for stationary outcome processes. In contrast, the performance of the MSW estimator seems to depend critically on the degree of heterogeneity. When , and or , the MSW estimator performs better than the FDAC estimator in terms of bias and RMSE, but exhibits mild size distortions when and or . However, the MSW estimator breaks down if we consider the results for . For example, the RMSE of the MSW estimator for and rises from when to when . The size of the MSW estimator also rises from per cent to per cent as is increased from to , for the same sample sizes.777The performance of the MSW estimator under homogeneity is investigated in the online supplement, with the results summarized in Table S.6. Compared with the FDAC estimator, the MSW estimator has much greater bias, higher RMSE, and noticeable size distortions for most of the sample sizes, and for the values of we consider.

| Medium degree of heterogeneity | High degree of heterogeneity | |||||||||||||||||

| Bias | RMSE | Size () | Bias | RMSE | Size () | |||||||||||||

| FDAC | MSW | FDAC | MSW | FDAC | MSW | FDAC | MSW | FDAC | MSW | FDAC | MSW | |||||||

| 4 | 100 | -0.005 | 0.003 | 0.165 | 0.084 | 6.8 | 6.8 | -0.005 | 0.248 | 0.168 | 0.300 | 7.3 | 34.4 | |||||

| 4 | 1,000 | 0.001 | 0.007 | 0.050 | 0.030 | 3.8 | 10.7 | 0.001 | 0.240 | 0.052 | 0.246 | 4.4 | 99.7 | |||||

| 6 | 100 | 0.002 | 0.012 | 0.099 | 0.084 | 6.0 | 4.4 | 0.004 | 0.260 | 0.106 | 0.310 | 5.8 | 36.2 | |||||

| 6 | 1,000 | 0.000 | 0.023 | 0.031 | 0.036 | 5.1 | 15.5 | 0.000 | 0.261 | 0.034 | 0.266 | 4.9 | 100.0 | |||||

| 10 | 100 | 0.000 | 0.020 | 0.070 | 0.089 | 6.4 | 4.7 | 0.001 | 0.265 | 0.078 | 0.315 | 6.5 | 37.4 | |||||

| 10 | 1,000 | 0.001 | 0.024 | 0.022 | 0.038 | 4.3 | 15.2 | 0.001 | 0.263 | 0.024 | 0.269 | 4.5 | 100.0 | |||||

Notes: The DGP is given by for , and with featuring Gaussian errors with GARCH effects. The heterogeneous AR(1) coefficients are generated as case (a): and with and . The FDAC estimator is calculated by (6.1), and its asymptotic variance is estimated by the Delta method. “MSW” denotes the kernel-weighting likelihood estimator proposed by Mavroeidis et al. (2015) and calculated assuming that with initial values given by , , , and . The nominal size of the tests is set to 5 per cent. Due to the extensive computations required for the implementation of the MSW estimator, the number of replications is .

7.5 Non-stationary initialization

One of the key assumptions behind the FDAC estimator is the stationarity of . This assumption requires that the initial values are drawn from the steady state distribution of the underlying processes, which is given by

| (7.1) |

where . As shown in Section S.3 of the online supplement, the moment conditions (4.1) and (4.2) can also be derived under the above initial distribution, but need not hold if the distribution of departs from the steady state distribution. The same is also true for some of the HomoGMM estimators. It is, therefore, of interest to investigate the sensitivity of the FDAC and HomoGMM estimators to departures from the steady state distribution in (7.1). Here we model this departure by assuming that starts from periods before the first observation, , used in the estimation process. Assuming that all AR(1) processes are generated from we have888One can also allow for heterogeneity in the way different processes are initialized, for example, by starting from periods in the past, with drawn randomly for each from the set of integers ( to ).

| (7.2) |

It is clear that as , the distribution of converges to the steady state distribution given by (7.1). This suggests that departures from the steady state distribution can be conveniently represented by using relatively small values of . To investigate the effects of departures from the steady state distribution, we generate the initial values as , which converges to the stationary distribution as . We consider both homogeneous and heterogeneous cases and set , where , with . In the case of non-stationary initial values, the distribution of the FDAC estimator, as well as a number of GMM estimators, depends on the the ratio , which in the case of our MC design reduces to . It is clear that is dominated by and to highlight the dependence of and other estimators on and we consider the following combinations and . The MC results for these combinations are summarized in the online supplement. The results for the homogeneous case ( are given in Tables S.8 to S.10, and for the heterogeneous cases are summarized in Tables S.11 to S.13 for and in Tables S.14–S.16 for .

In the homogeneous case (), when , the FDAC, FDLS, and BB estimators all show sizeable bias and size distortions that do not vanish as increases. The magnitudes of bias, RMSE, and size distortions are larger for higher . This is particularly noticeable for the BB estimator, a result already highlighted by Chudik and Pesaran (2021). Also, as to be expected, under homogeneity, the AH, AAH, and AB estimators are robust to non-stationary initialization and have similar performance across different values of and .

In the case of heterogeneous panels, the FDAC estimator is adversely affected when or , and displays bias and size distortions, particularly when there is a high degree of heterogeneity (namely ), and the magnitude of the bias and size distortion rises with . But, as to be expected, the bias and size distortion of FDAC disappear as is increased. Note that the results for with are comparable to the results in Tables 2 and 3 where are generated starting with . For the HomoGMM estimators, the magnitude of neglected heterogeneity bias is much larger, and the size distortions are much more serious and in general, increase with when or , as compared to (which approximately corresponds to the stationary case).999Table S.7 in the online supplement reports the simulation results comparing the FDAC and MSW estimators for with , and confirms a similar pattern with the performance of the MSW estimator deteriorating as we move from stationary to non-stationary processes.

In brief, when is sufficiently large, the performance of the FDAC is not affected by the relative size of the individual fixed effects, , under both slope homogeneity and heterogeneity. Nonetheless, it is clearly a challenge to simultaneously deal with heterogeneity of and the non-stationarity that arises when are not drawn from the steady state distribution of .

7.6 Simulation results for the categorical distribution parameters

Section 5 has already shown that assuming follow a categorical distribution with a finite number of categories, the parameters of the underlying categorical distribution can be identified from the moments of under stationarity. Here we investigate the finite sample performance of estimating the parameters in the simple case of two categories, namely and . Since the procedure for estimating these parameters is based on the first three moments, then we need . See equation (6.3). Precise estimation of and also require quite large samples. Accordingly, we consider the following sample sizes: and .

Table 5 reports the bias and RMSE of the plug-in estimators given by (5.1) and (5.5), using the FDAC estimators of the moments of . Compared with the simulation results for and ), the FDAC estimators of and have much larger RMSEs. Also, the magnitude of bias and RMSE of and are much larger than those of , particularly when . Since the moment conditions of categorical distribution are linear in but nonlinear in and , the nonlinearity plays a crucial role here. Given equation (5.5), the solutions of and are ratios of functions of moments. The denominator is given by the variance of , which could be close to zero in finite samples, and thus, minor estimation errors in the denominator could have large adverse effects on the precision with which and can be estimated.101010See also Remark 15 on p. 26 in Gao and Pesaran (2023).

RMSEs of the FDAC estimators of and decline rapidly with for a given . For example, RMSE of declines from for and to for and . Similar results are obtained by Gao and Pesaran (2023) in the case of pure cross-sectional regressions where it is also shown that relatively large values of are required for precise estimation of the parameters of the categorical distribution.

| , | , | Categorical distributed | ||||||||||||||||||||||||||

| Bias | RMSE | Bias | RMSE | Bias | RMSE | Bias | RMSE | Bias | RMSE | Bias | RMSE | Bias | RMSE | Bias | RMSE | Bias | RMSE | |||||||||||

| 6 | 2,000 | -0.108 | 0.663 | 0.225 | 2.782 | 0.019 | 0.309 | 0.434 | 15.414 | 0.710 | 17.534 | 0.021 | 0.442 | -0.373 | 5.974 | 0.321 | 2.476 | 0.103 | 0.336 | |||||||||

| 6 | 5,000 | -0.036 | 0.193 | 0.073 | 0.264 | 0.016 | 0.239 | 0.034 | 9.148 | 1.786 | 58.043 | 0.020 | 0.405 | -0.042 | 0.271 | 0.084 | 0.678 | 0.068 | 0.256 | |||||||||

| 6 | 10,000 | -0.017 | 0.129 | 0.035 | 0.145 | 0.012 | 0.188 | -0.216 | 1.438 | 0.405 | 2.856 | 0.015 | 0.375 | -0.018 | 0.183 | 0.031 | 0.119 | 0.043 | 0.191 | |||||||||

| 6 | 50,000 | -0.006 | 0.058 | 0.006 | 0.054 | 0.001 | 0.094 | -0.047 | 0.163 | 0.061 | 0.211 | 0.003 | 0.277 | -0.004 | 0.084 | 0.005 | 0.035 | 0.010 | 0.084 | |||||||||

| 8 | 2,000 | -0.041 | 0.216 | 0.089 | 0.784 | 0.020 | 0.252 | -0.460 | 7.728 | 3.726 | 166.514 | 0.023 | 0.412 | -0.067 | 0.678 | 0.130 | 1.028 | 0.079 | 0.272 | |||||||||

| 8 | 5,000 | -0.012 | 0.120 | 0.033 | 0.134 | 0.015 | 0.179 | -0.099 | 1.337 | 0.296 | 4.758 | 0.023 | 0.367 | -0.010 | 0.172 | 0.029 | 0.104 | 0.045 | 0.185 | |||||||||

| 8 | 10,000 | -0.005 | 0.085 | 0.017 | 0.084 | 0.011 | 0.134 | -0.077 | 0.267 | 0.188 | 0.864 | 0.027 | 0.329 | -0.007 | 0.121 | 0.012 | 0.061 | 0.022 | 0.130 | |||||||||

| 8 | 50,000 | -0.002 | 0.039 | 0.003 | 0.035 | 0.002 | 0.063 | -0.018 | 0.100 | 0.030 | 0.115 | 0.011 | 0.215 | 0.000 | 0.055 | 0.002 | 0.021 | 0.006 | 0.054 | |||||||||

| 10 | 2,000 | -0.023 | 0.208 | 0.054 | 0.235 | 0.016 | 0.214 | -0.280 | 5.066 | 0.211 | 9.146 | 0.021 | 0.396 | -0.021 | 0.225 | 0.053 | 0.218 | 0.065 | 0.233 | |||||||||

| 10 | 5,000 | -0.010 | 0.098 | 0.019 | 0.098 | 0.009 | 0.150 | -0.104 | 0.318 | 0.374 | 5.242 | 0.017 | 0.344 | -0.006 | 0.138 | 0.017 | 0.068 | 0.031 | 0.147 | |||||||||

| 10 | 10,000 | -0.004 | 0.068 | 0.010 | 0.064 | 0.006 | 0.110 | -0.052 | 0.193 | 0.100 | 0.314 | 0.019 | 0.299 | -0.005 | 0.099 | 0.008 | 0.044 | 0.015 | 0.103 | |||||||||

| 10 | 50,000 | -0.001 | 0.031 | 0.002 | 0.027 | 0.002 | 0.050 | -0.011 | 0.077 | 0.020 | 0.082 | 0.012 | 0.182 | -0.001 | 0.045 | 0.002 | 0.017 | 0.003 | 0.044 | |||||||||

Notes: The DGP is given by for , and with featuring Gaussian errors with GARCH effects. The heterogeneous AR(1) coefficients are generated by case (a): uniform distribution and with and , and case (b): categorical distribution and with , , and such that . The FDAC estimator is calculated by (5.1) and (5.5). The number of replications is 2,000.

8 Empirical application: heterogeneity in earnings dynamics

8.1 Literature review of estimation of earnings dynamics

Estimating earnings equations is crucial for answering some of the most important economic questions.111111See p. 58 in Guvenen (2009) for a brief summary of several economic inquiries hinging on the estimation of earnings functions. Variance of earnings has been modeled and decomposed to measure income uncertainties in Lillard and Weiss (1979), MaCurdy (1982), Carroll and Samwick (1997), Meghir and Pistaferri (2004), Altonji et al. (2013) and to quantify earnings mobility in Lillard and Willis (1978) and Geweke and Keane (2000). The covariance structures between earnings and other households’ characteristics, for example, work hours, consumptions, and savings have been studied by Abowd and Card (1989) Hubbard et al. (1995), Guvenen (2007), and Alan et al. (2018).

Among these studies, a homogeneous AR or ARMA process is often used as a component when modeling innovations in earnings processes. Based on the Restricted Income Profiles model that assumes homogenous linear trends proposed in MaCurdy (1982), MaCurdy (1982) and Hubbard et al. (1995), obtained close to unit root estimates for the AR(1) coefficient, ranging from 0.946 to 0.998.121212See Table 5 on p. 111 in MaCurdy (1982) using an ARMA(1,1) process. See Table 2 on p. 380 in Hubbard et al. (1995) based on an AR(1) process. Following this literature, a unit root assumption was imposed in Carroll and Samwick (1997) and Meghir and Pistaferri (2004). On the other hand, using the Heterogeneous Income Profiles, by assuming unit-specific linear trends, Lillard and Weiss (1979) obtained estimates of the AR(1) coefficient (assumed to be homogeneous) ranging from 0.153 to 0.860 for a sample with PhD degrees. Guvenen (2009) using PSID data obtained estimates ranging from 0.809 to 0.899.131313See Tables 2, 4, 6 and 7 in Lillard and Weiss (1979), Table 1 on p. 64 in Guvenen (2009), and the abstract of Gu and Koenker (2017).

There are also a number of studies that allow for heterogeneity in the AR(1) coefficients. Prominent examples are Browning et al. (2010), Alan et al. (2018), Browning et al. (2010), and Gu and Koenker (2017). These studies are typically based on panels with a moderate time dimension and make parametric assumptions regarding the distribution of the AR(1) coefficients; often using a Bayesian framework.141414See pp. 227–232 in Browning and Ejrnæs (2013) for a comprehensive survey of heterogeneity in parameters of earnings functions. The application of the FDAC estimator to earnings equation allows for heterogeneity in the AR(1) coefficients without making any strong parametric assumptions, even when is as small as . Also because of first-differencing prior to estimation, the FDAC estimator is robust to unobserved individual-specific characteristics and is not subject to misspecification bias that could arise when log real wages are filtered for individual-specific characteristics before investigating the dynamics of the earnings process.

8.2 A heterogeneous panel AR(1) model of earnings dynamics with linear trends

We consider estimating the earnings equation with fixed effects, heterogeneous autoregressive coefficients, without imposing any restrictions on the joint distributions of , , and . However, to accommodate growth in real earnings we extend our baseline model in (2.1) to allow for linear trends:

| (8.1) |

where is the reported earnings of individual in year , is a general price, and denotes the growth rate of real earnings for individual . The above equation can be written equivalently as

where , and . The steady state distribution of can now be derived using

| (8.2) |

When is sufficiently large individual-specific growth rates, , can be estimated -consistently by running individual least squares regressions of on an intercept and a linear trend, and then using the residuals from these regressions to estimate the moments of . This approach requires and to be both large. In the case of the present empirical application where is short ( or , we provide estimates of the moments of assuming that for individuals within a given group, but allow to differ across groups, classified by the educational attainment levels. -consistent estimators of can be obtained either from the pooled regression of on fixed effects and a common linear trend, namely

| (8.3) |

with and , or after first-differencing of (8.2) (with by

| (8.4) |

For small there is little to choose between these two estimators, and they are identical when . Given either of the above estimators, generically denoted by , can now be used to estimate the moments of using the FDAC or MSW procedures.151515Consistent estimation of in the presence of heterogeneity in both and requires moderate to large values of . The approach used in the empirical literature whereby are first de-meaned and de-trended for each prior to the estimation of is subject to Nickell (1981) bias in the case of short panels, even if .

In addition to the FDAC estimates, we also present estimates based on four estimation methods assuming homogeneous slope coefficients, namely AAH, AB, and BB estimators proposed by Chudik and Pesaran (2021), Arellano and Bond (1991), and Blundell and Bond (1998), and the MSW estimator of Mavroeidis et al. (2015). Following Meghir and Pistaferri (2004), individuals in each time series sample are divided into three education categories, where “HSD” refers to high school dropouts with less than 12 years of education, “HSG” refers to high school graduates with at least 12 but less than 16 years of education, and “CLG” refers to college graduates with at least 16 years of education.161616The sample for all individuals in both and yearly samples covered individuals with consecutive observations of nine years or more, and 36,325 individual-year observations. To allow for possible time variations in the estimates of mean earnings persistence we provide estimates for and yearly non-overlapping sub-periods. The five yearly samples are 1976–1980, 1981–1985, 1986–1990, and 1991–1995. The ten yearly samples are 1976–1985, 1981–1990 and 1991–1995. For each sub-period, we provide estimates for all categories combined, as well as separate estimates for the three educational sub-categories.171717From 1997 PSID data are updated every two years. We confine our analysis to the years 1976 to 1995 to construct panels with and consecutive years. To save space, the results for the last five and ten yearly samples are given in the paper. The estimates for the earlier sub-periods are provided in the online supplement.

Table 6 gives the estimates of mean earnings persistence, and the common linear trend coefficient, , for the sub-periods 1991–1995 () and 1986–1995 (). The estimates of is on average around per cent per annum with some modest variations across the sub-samples and educational categories. The HomoGMM estimates (AAH, AB and BB) differ a great deal, both over sub-periods and across educational categories. The AAH estimates are all around 0.50 and show little variations across the two sub-period and the educational categories. The AB estimates tend to be quite low and are not statistically significant for two of the educational categories in the shorter sub-period . In contrast, the BB estimates are much larger and in many instances are close to unity. For example, for the sub-period 1986-1995 , the BB estimates of earnings persistence for the three educational categories HSD, HSG and CLG are 0.923 (0.003), 0.914 (0.003) and 0.992 (0.004), respectively, with standard errors in brackets.

We also find sizeable differences in the estimates of mean earnings persistence when we consider the FDAC and MSW estimators. The MSW estimates are all around 0.45 and do not vary with the level of educational attainment. In contrast, the FDAC estimates are somewhat larger (lie in the range of 0.570-0.734) and rise with the level of educational attainment. This pattern can be seen in both sub-periods. For example, for the longer sub-period (1986-1995), the mean persistence for HSD, HSG and CLG categories are estimated to be 0.580 (0.071), 0.611 (0.028) and 0.735 (0.040), respectively. Similar results are obtained for the other sub-periods. See Tables S.29 and S.30 of the online supplement. It is interesting that the higher earnings persistence of the college graduate category is a prominent feature of the FDAC estimates for all sub-periods. This result is also in line with a number of theoretical arguments advanced in the literature in terms of the higher mobility of college graduates and their relative job stability. For example, see Carroll and Samwick (1997) and Carneiro et al. (2023).

Although we have not developed a formal statistical test of the heterogeneity , the estimates of provide a good indication of the degree of within-group heterogeneity. Estimates of based on MSW and FDAC procedures for the various sub-periods are given in Tables S.31–S.33 of the online supplement. The FDAC estimates are much larger than the MSW estimates. For example, for the sub-period 1991–1995 the MSW estimates of are all around 0.011 with standard errors in the range of 0.004–009, whilst the FDAC estimates of for the same sub-period are 0.241(0.100), 0.081(0.054) and 0.091(0.09) for the three educational categories of HSD, HSG and CLG, respectively. The degree of within-group heterogeneity also seems to vary over time. For example, for the longer sub-period (1986-1995), the FDAC estimates of are generally larger with lower standard errors for all educational categories.

| 1991–1995, | 1986–1995, | ||||||||||

| All | Category by education | All | Category by education | ||||||||

| categories | HSD | HSG | CLG | categories | HSD | HSG | CLG | ||||

| Homogeneous slopes | |||||||||||

| AAH | 0.526 | 0.490 | 0.547 | 0.447 | 0.546 | 0.569 | 0.535 | 0.522 | |||

| (0.046) | (0.072) | (0.061) | (0.072) | (0.028) | (0.024) | (0.033) | (0.038) | ||||

| AB | 0.278 | 0.105 | 0.320 | -0.013 | 0.311 | 0.310 | 0.335 | 0.232 | |||

| (0.081) | (0.147) | (0.097) | (0.133) | (0.039) | (0.045) | (0.044) | (0.070) | ||||

| BB | 0.488 | 0.872 | 0.602 | 0.964 | 0.880 | 0.923 | 0.914 | 0.992 | |||

| (0.059) | (0.031) | (0.042) | (0.074) | (0.004) | (0.003) | (0.003) | (0.004) | ||||

| Heterogeneous slopes | |||||||||||

| FDAC | 0.586 | 0.582 | 0.567 | 0.635 | 0.636 | 0.580 | 0.611 | 0.734 | |||

| (0.042) | (0.132) | (0.056) | (0.065) | (0.023) | (0.071) | (0.028) | (0.040) | ||||

| MSW | 0.437 | 0.431 | 0.436 | 0.452 | 0.458 | 0.459 | 0.452 | 0.460 | |||

| (0.040) | (0.044) | (0.043) | (0.045) | (0.054) | (0.038) | (0.046) | (0.063) | ||||

| Common linear trend | 0.023 | 0.008 | 0.027 | 0.020 | 0.019 | 0.024 | 0.020 | 0.013 | |||

| 1,366 | 127 | 832 | 407 | 1,139 | 109 | 689 | 341 | ||||

Notes: The estimates are based on , where using the PSID data over the sub-periods 1991–1995 and 1986–1995. “HSD” refers to high school dropouts with less than 12 years of education, “HSG” refers to high school graduates with at least 12 but less than 16 years of education, and “CLG” refers to college graduates with at least 16 years of education. is computed by (8.4). The estimation for is based on for . “AAH”, “AB”, and “BB” denote the 2-step GMM estimators proposed by Chudik and Pesaran (2021), Arellano and Bond (1991), and Blundell and Bond (1998). The FDAC estimator is calculated by (6.1), and its asymptotic variance is estimated by the Delta method. “MSW” denotes the kernel-weighted estimator in Mavroeidis et al. (2015).

9 Conclusion

This paper considers the estimation of heterogeneous panel AR(1) data models with short (and fixed) , as . It allows for fixed effects and proposes estimating the moments of the AR(1) coefficients, , for , using the autocorelation function of first differences. We also show how estimates of , can be used to identify the underlying distribution of , assuming they follow categorical distributions. It is also shown that the standard GMM estimators proposed in the literature for short panels are inconsistent in the presence of slope heterogeneity. Analytical expressions for this bias are derived and shown to be very close to estimates obtained from stochastic simulations.

The small sample properties of the proposed estimators are investigated using Monte Carlo experiments. Under stationarity of the outcome processes, it is shown that the FDAC estimator which is based on the autocorrelations of first-differences (set out in sub-section 6.1) performs much better than the HetroGMM estimator based on autocovariances of the first differences (set out in sub-section 6.2). Focussing on the FDAC estimator, we find that the FDAC estimator performs well even under homogeneous AR(1) coefficients. The magnitudes of bias and RMSE of the FDAC estimators are comparable to the HomoGMM estimators, and the size of the tests based on the FDAC estimator is mostly around the 5 per cent nominal level. The simulation results also confirm the presence of neglected heterogeneity bias of the HomoGMM estimators under slope heterogeneity, which can result in substantial size distortions. The FDAC estimator is shown to be reliable for stationary heterogeneous panel AR(1) models. The simulation results also show that the FDAC estimator is robust to different distributions of autoregressive coefficients and error processes. However, when the initialization of the outcome process deviates from the steady state distribution, the FDAC estimator could suffer from bias and size distortions. We also find that for the estimation of the parameters of the categorical distribution large sample sizes are required.

The utility of the FDAC estimator is illustrated by applying it to the 1976–1995 PSID data using heterogeneous AR(1) panels in log real earnings with a common linear trend. We provide estimates of and over a number of and yearly sub-periods, with 3 educational groupings. The estimates of differ systematically across the education groups, with the mean persistence of real earnings rising with the level of educational attainments (high school dropouts, high school graduates, and college graduates). The estimates of differ across periods and levels of educational attainment, but do not display any particular patterns.

It is, however, important to acknowledge that the scope of the present paper is limited, with a number of remaining challenges: (a) allowing for individual-specific time-varying covariates, such as heterogeneous time trends, and (b) simultaneously dealing with heterogeneity and non-stationary initialization. It is not clear that such extensions will be possible without relaxing the assumption that is short and fixed, as . But these are clearly important topics for future research.

References

- Abowd and Card (1989) Abowd, J. M. and D. Card (1989). On the covariance structure of earnings and hours changes. Econometrica 57, 411–445.

- Alan et al. (2018) Alan, S., M. Browning, and M. Ejrnæs (2018). Income and consumption: a micro semistructural analysis with pervasive heterogeneity. Journal of Political Economy 126, 1827–1864.

- Altonji et al. (2013) Altonji, J. G., A. A. Smith Jr, and I. Vidangos (2013). Modeling earnings dynamics. Econometrica 81, 1395–1454.

- Anderson and Hsiao (1981) Anderson, T. W. and C. Hsiao (1981). Estimation of dynamic models with error components. Journal of the American Statistical Association 76, 598–606.

- Anderson and Hsiao (1982) Anderson, T. W. and C. Hsiao (1982). Formulation and estimation of dynamic models using panel data. Journal of Econometrics 18, 47–82.

- Arellano and Bond (1991) Arellano, M. and S. Bond (1991). Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. The Review of Economic Studies 58, 277–297.

- Arellano and Bonhomme (2012) Arellano, M. and S. Bonhomme (2012). Identifying distributional characteristics in random coefficients panel data models. The Review of Economic Studies 79, 987–1020.

- Baltagi et al. (2008) Baltagi, B. H., G. Bresson, and A. Pirotte (2008). To pool or not to pool? In The Econometrics of Panel Data: Fundamentals and Recent Developments in Theory and Practice, Chapter 16, pp. 517–546. Springer.

- Blundell and Bond (1998) Blundell, R. and S. Bond (1998). Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics 87, 115–143.

- Bonhomme (2012) Bonhomme, S. (2012). Functional differencing. Econometrica 80, 1337–1385.

- Browning and Carro (2014) Browning, M. and J. M. Carro (2014). Dynamic binary outcome models with maximal heterogeneity. Journal of Econometrics 178, 805–823.

- Browning and Ejrnæs (2013) Browning, M. and M. Ejrnæs (2013). Heterogeneity in the dynamics of labor earnings. Annual Review of Econonomics 5, 219–245.

- Browning et al. (2010) Browning, M., M. Ejrnæs, and J. Alvarez (2010). Modelling income processes with lots of heterogeneity. The Review of Economic Studies 77, 1353–1381.

- Carneiro et al. (2023) Carneiro, A., P. Portugal, P. Raposo, and P. M. Rodrigues (2023). The persistence of wages. Journal of Econometrics 233, 596–611.

- Carroll and Samwick (1997) Carroll, C. D. and A. A. Samwick (1997). The nature of precautionary wealth. Journal of Monetary Economics 40, 41–71.

- Chamberlain (1992) Chamberlain, G. (1992). Efficiency bounds for semiparametric regression. Econometrica: Journal of the Econometric Society 60, 567–596.

- Chudik and Pesaran (2021) Chudik, A. and M. H. Pesaran (2021). An augmented Anderson–Hsiao estimator for dynamic short-T panels. Econometric Reviews 41, 1–32.

- Gao and Pesaran (2023) Gao, Z. and M. H. Pesaran (2023). Identification and estimation of categorical random coefficient models. Empirical Economics, a Special Issue in Honor of Peter Schmidt, 1–46.

- Geweke and Keane (2000) Geweke, J. and M. Keane (2000). An empirical analysis of earnings dynamics among men in the PSID: 1968–1989. Journal of Econometrics 96, 293–356.

- Graham and Powell (2012) Graham, B. S. and J. L. Powell (2012). Identification and estimation of average partial effects in “irregular” correlated random coefficient panel data models. Econometrica 80, 2105–2152.

- Gu and Koenker (2017) Gu, J. and R. Koenker (2017). Unobserved heterogeneity in income dynamics: an empirical Bayes perspective. Journal of Business & Economic Statistics 35, 1–16.

- Guvenen (2007) Guvenen, F. (2007). Learning your earning: Are labor income shocks really very persistent? American Economic Review 97, 687–712.

- Guvenen (2009) Guvenen, F. (2009). An empirical investigation of labor income processes. Review of Economic Dynamics 12, 58–79.

- Han and Phillips (2010) Han, C. and P. C. Phillips (2010). GMM estimation for dynamic panels with fixed effects and strong instruments at unity. Econometric Theory 26, 119–151.

- Hsiao et al. (1999) Hsiao, C., M. H. Pesaran, and A. Tahmiscioglu (1999). Bayes estimation of short-run coefficients in dynamic panel data models. In Analysis of Panel Data and Limited Dependent Variable Models. Cambridge University Press.

- Hubbard et al. (1995) Hubbard, R. G., J. Skinner, and S. P. Zeldes (1995). Precautionary saving and social insurance. Journal of Political Economy 103, 360–399.

- Lillard and Weiss (1979) Lillard, L. A. and Y. Weiss (1979). Components of variation in panel earnings data: American scientists 1960-70. Econometrica: Journal of the Econometric Society 47, 437–454.

- Lillard and Willis (1978) Lillard, L. A. and R. J. Willis (1978). Dynamic aspects of earning mobility. Econometrica 46, 985–1012.

- Liu et al. (2017) Liu, F., P. Zhang, I. Erkan, and D. S. Small (2017). Bayesian inference for random coefficient dynamic panel data models. Journal of Applied Statistics 41, 1543–1559.

- Liu (2023) Liu, L. (2023). Density forecasts in panel data models: a semiparametric Bayesian perspective. Journal of Business & Economic Statistics 41, 1–15.

- MaCurdy (1982) MaCurdy, T. E. (1982). The use of time series processes to model the error structure of earnings in a longitudinal data analysis. Journal of Econometrics 18, 83–114.

- Mavroeidis et al. (2015) Mavroeidis, S., Y. Sasaki, and I. Welch (2015). Estimation of heterogeneous autoregressive parameters with short panel data. Journal of Econometrics 188, 219–235.

- Meghir and Pistaferri (2004) Meghir, C. and L. Pistaferri (2004). Income variance dynamics and heterogeneity. Econometrica 72, 1–32.

- Nickell (1981) Nickell, S. (1981). Biases in dynamic models with fixed effects. Econometrica: Journal of the Econometric Society 49, 1417–1426.

- Okui and Yanagi (2019) Okui, R. and T. Yanagi (2019). Panel data analysis with heterogeneous dynamics. Journal of Econometrics 212, 451–475.

- Okui and Yanagi (2020) Okui, R. and T. Yanagi (2020). Kernel estimation for panel data with heterogeneous dynamics. The Econometrics Journal 23, 156–175.

- Pesaran (2015) Pesaran, M. H. (2015). Time Series and Panel Data Econometrics. Oxford University Press.

- Pesaran and Smith (1995) Pesaran, M. H. and R. Smith (1995). Estimating long-run relationships from dynamic heterogeneous panels. Journal of Econometrics 68, 79–113.

- Pesaran and Yang (2023) Pesaran, M. H. and L. Yang (2023). Trimmed mean group estimation of average treatment effects in ultra short-T panels with correlated heterogeneous coefficients. (work in progress).

- Pesaran and Zhao (1999) Pesaran, M. H. and Z. Zhao (1999). Bias reduction in estimating long-run relationships from dynamic heterogeneous panels. In Analysis of Panel Data and Limited Dependent Variable Models. Cambridge University Press.

- Robinson (1978) Robinson, P. M. (1978). Statistical inference for a random coefficient autoregressive model. Scandinavian Journal of Statistics 5, 163–168.

- Wooldridge (2005) Wooldridge, J. M. (2005). Fixed-effects and related estimators for correlated random-coefficient and treatment-effect panel data models. Review of Economics and Statistics 87, 385–390.

Online Supplement to

“Heterogeneous Autoregressions in Short Panel

Data Models ”

M. Hashem Pesaran

University of Southern California, and Trinity College, Cambridge

Liying Yang

Ph.D. student, University of Southern California

S.1 Introduction

This online supplement is organized as follows: Section S.2 derives expressions for the analytical bias of the AB and BB estimators under heterogeneity of when . Section S.3 derives the autocovariances of first differences assuming the initial values are random draws from the steady state distribution of . Section S.4 provides additional Monte Carlo evidence. Section S.5 describes the sample (1976–1995) of the Panel Study of Income Dynamics (PSID) data used in the empirical application, and provides estimation results for a number of sub-periods in addition to the ones reported in the main paper.

S.2 Neglected heterogeneity bias in AB and BB estimators

The AB estimator proposed by Arellano and Bond (1991) is based on the following moment conditions:S1S1S1See equation (8) on p. 5 in Chudik and Pesaran (2021).

| (S.1) |

which can also be written as with moment conditions in total. When , the AB moment conditions, neglecting the heterogeneity, are given by , , and . With a fixed weight matrix , the AB estimator can be written as

| (S.2) |

where and

| (S.3) |

and assuming that is distributed independently of (as assumed under AB) then using (3.2) and (S.3) we have

Hence

| (S.4) |

Given (S.4), we have

Thus, when distributed independently of with for ,

| (S.5) |

where and with and .

In addition to (S.1), consider the following moment condition also used in the system GMM estimator proposed by Blundell and Bond (1998) given byS2S2S2See equation (9) on p. 5 in Chudik and Pesaran (2021).

| (S.6) |

which can also be written as For , with a fixed weight matrix , the BB estimator combining moment conditions in (S.1) and (S.6) is given by

| (S.7) |

where

Using (3.2) and (S.3), similarly, we can derive the following equations

| (S.8) |

and it follows that