Ethereum’s Proposer-Builder Separation:

Promises and Realities

Abstract.

With Ethereum’s transition from Proof-of-Work to Proof-of-Stake in September 2022 came another paradigm shift, the Proposer-Builder Separation (PBS) scheme. PBS was introduced to decouple the roles of selecting and ordering transactions in a block (i.e., the builder), from those validating its contents and proposing the block to the network as the new head of the blockchain (i.e., the proposer). In this landscape, proposers are the validators in the Proof-of-Stake consensus protocol, while now relying on specialized block builders for creating blocks with the highest value for the proposer. Additionally, relays act as mediators between builders and proposers. We study PBS adoption and show that the current landscape exhibits significant centralization amongst the builders and relays. Further, we explore whether PBS effectively achieves its intended objectives of enabling hobbyist validators to maximize block profitability and preventing censorship. Our findings reveal that although PBS grants validators the opportunity to access optimized and competitive blocks, it tends to stimulate censorship rather than reduce it. Additionally, we demonstrate that relays do not consistently uphold their commitments and may prove unreliable. Specifically, proposers do not always receive the complete promised value, and the censorship or filtering capabilities pledged by relays exhibit significant gaps.

1. Introduction

Ethereum’s (Wood, 2014) original design assigns block proposers (miners or validators) the task of building and proposing blocks to the network. Thus, block proposers must gather transactions from the gossip network and combine them into a block before broadcasting the block to their peers. Optimal profit block building is essentially the bin packing problem which has long been known to be NP-hard (Karp, 1972), as there is limited block space and the fees received from transactions can vary widely. In practice, however, proposers have simply ordered transactions according to their gas price, i.e., the fees paid per unit of gas, which reflects the amount of computation required by the transaction. This has changed with the rise of decentralized finance (DeFi) on the Ethereum blockchain.

DeFi refers to a collection of smart contracts, which are executable codes stored on the blockchain (Buterin, 2014), that offer financial services similar to those in traditional finance, such as exchanges and lending. These smart contracts are typically transaction order dependent, meaning that the outcome of a set of transactions is determined by their order. As a result, the concept of miner/maximal extractable value (MEV) has emerged on the Ethereum blockchain. MEV quantifies the potential revenue that can be extracted by including, excluding, or reordering transactions (Daian et al., 2020).

The widespread adoption of DeFi and the related rise of MEV has led to increased complexity in block building, leading to block proposers running their own complicated strategies to maximize the profit they make. In response to this trend, and in anticipation of the transition of the Ethereum blockchain from Proof-of-Work (PoW) to Proof-of-Stake (PoS), the concept of Proposer-Builder Separation (PBS) was introduced (Buterin, 2021a). PBS separates block building from block proposal: instead of having the block’s proposer (a PoS validator that is known in advance) perform both tasks, specialized builders are responsible for creating blocks. Builders and validators both connect to new entities called relays, which receive new blocks from builders and forward them to the validators. When it is their turn to propose a block, the validator simply picks the most profitable block and proposes it to the Ethereum network.

With “the merge”, which marked the end of PoW and the beginning of PoS on Ethereum, PBS was launched and its adoption has been on the rise. In this study, we analyze the current state of the PBS scheme during its opt-in phase and evaluate how well it aligns with its intended objectives.

Contributions. We summarize our main contributions in the following.

-

•

We examine whether PBS successfully achieves its goal of decentralizing block validation by ensuring that large entities do not have an advantage in block building. We find that professionalized builders have a distinct advantage in building profitable blocks. However, PBS effectively provides all validators, regardless of size, access to competitive blocks, thus preventing hobbyists from being outcompeted by institutional players who can optimize block profitability better.

-

•

We further investigate the extent to which PBS prevents censorship, a critical design goal of the scheme. Unfortunately, our analysis reveals that PBS falls short of its goal in practice. In fact, we consistently observe that transactions from sanctioned addresses are twice as likely to be included in non-PBS blocks compared to PBS blocks. This suggests that the current implementation of PBS does not effectively prevent censorship.

Our study highlights the current challenges and open problems associated with PBS, such as builder and relay centralization, the role of PBS in aiding censorship, and the reliability and trustworthiness of relays. By examining these issues, we strive to help the understanding of PBS and provide insights that can direct future improvements in the design and implementation of this new scheme.

2. Background

2.1. The Ethereum Ecosystem

Ethereum Proof-of-Stake. Since the merge on 15 September 2022 (Ethereum Foundation, 2023), Ethereum has been running two layers: the execution layer and the consensus layer. The execution layer is largely similar to the former PoW protocol and is responsible for verifying and executing transactions. The consensus layer, built on top of the Beacon chain, is responsible for reaching consensus amongst validators, i.e., the PoS equivalent of miners. We note that to become a validator one must stake, or lock-in, 32 ETH to incentivize honest behavior.

On the Beacon chain, time is split into 12 second slots, with a group of 32 slots making up an epoch (cf. Figure 1). For each slot, a random validator is selected as the block proposer along with a committee (a group of validators in charge of verifying the newly proposed block). We note that block proposers and committees are announced at least an epoch ahead of time, i.e., 6.4 minutes. There is a chance for a single block to be added to the Ethereum chain in every Beacon slot. When a proposer successfully proposes a block, i.e., the block is added to the canonical chain, they receive a block reward in the Beacon chain (0.034 ETH). The committee members partaking in the validation of the block also receive a smaller reward (0.0000125 ETH).

Importantly, a proposer not only receives the Beacon chain reward for proposing a block but also receives part of the block’s transaction fees, as well as potentially direct payments from users as a bribe for including their transaction (totaling on average 0.1126 ETH per block). We discuss these further in the reward data of Section 3.1.

The Ethereum Network. Ethereum’s execution and consensus layers run over two separate P2P overlays, one primarily responsible for propagating transactions and the other for consensus messages (new blocks and validator votes), respectively. Transactions sent through the P2P network are aggregated in a node’s mempool of pending transactions until they are included in a block. Validators connect directly to these networks, choosing which transactions to include in the next block from the mempool. Additionally, large validators often offer private pathways for users to send transactions to be included in a block bypassing the public mempool. Private pathways also existed pre-merge by large mining pools (Ethermine: Private RPC Endpoint Configuration, 2023), through hidden transaction auction platforms like Flashbots (Flashbots, 2023), and via private services like those offered by bloXroute (Klarman et al., 2018).

2.2. Proposer-Builder Separation

PBS was designed for Ethereum PoS and has gained increased popularity after the merge (cf. Figure 2). With the PBS scheme, the former role of the proposer is separated into two new roles — block building and block proposing. Succinctly, with PBS, block builders are responsible for creating blocks and offering them to the block proposer in each slot. The block proposer then chooses the most profitable block and proposes the block to the network. The PBS design goals are two-fold: (1) prevent censorship, and (2) decentralize transaction validation by not giving large entities an advantage in block building (Ethereum, 2023b; Flashbots, 2023c).

We illustrate the PBS ecosystem in Figure 2 and detail the scheme in the following, by discussing the roles of the involved players. The execution/consensus layers are represented as the Ethereum network and mempool in Figure 2.

Searchers are Ethereum users who prioritize privacy and prefer to use a private transaction pool instead of the public mempool. Common examples of searchers include MEV bots, such as arbitrageurs, sandwich attackers, or liquidation bots, as well as Ethereum users seeking front-running protection, such as DEX traders. With PBS, searchers send bundles containing their own transactions and possibly other transactions from the Ethereum mempool to one or multiple block builders (as shown in Figure 2). Searchers bid for block inclusion using either the gas price or direct ETH transfers to the address of the block builder.

Block builders receive bundles from searchers in the PBS system. Using these bundles along with their private transactions and transactions from the public mempool, block builders attempt to create the most profitable block possible. Once a block is constructed, it is sent to one or more relays in its entirety.

Relays are responsible for holding blocks from builders in escrow for validators. Their role includes accepting blocks from builders, sending the header of the most profitable block to validators, and then sending the full block to validators only after receiving a signed header. Importantly, relays keep the contents of the block private until the validator commits to proposing it for inclusion by signing the block’s header.

Validators are still responsible for proposing blocks to the Ethereum network. They have the option to connect to several relays and then select the most profitable block — the block with the highest profit for the validator — for inclusion in the blockchain. To receive bids from the relays, a validator must install the MEV-Boost client (Flashbots, 2023)111Notably, MEV-Boost is maintained by Flashbots and began as part of Flashbots’ MEV transaction auction platform pre-merge. and add the relays from which they wish to receive bids to the config file.

For blocks built through PBS, the builder’s address is listed in the block’s transaction fee recipient field. Additionally, any direct payments from searchers are sent to the address listed as the block’s fee recipient, i.e., the builder’s address. In the block’s last transaction, the builder address transfers ETH to the proposer’s fee recipient address. The value of this transfer should correspond to the value agreed upon.

3. Data Collection

To measure the PBS ecosystem, we collect data from three data sources detailed below: Ethereum blockchain (cf. Section 3.1), Ethereum network (cf. Section 3.2), and individual data directly gathered from relays (cf. Section 3.3). For all three, our data ranges from block 15,537,394 to block 16,950,602, i.e., from the first block after the merge on 15 September 2022 to the last block on 31 March 2023. Table 1 provides an overview of the different datasets we collected during our data collection process. It includes the number of entries and a description of the data source. We further note that we provide our aggregate data set on GitHub (Aggregate Data Set, 2023).

Dataset Entries Type Source Ethereum blockchain 1,413,209 210,695,337 465,863,321 1,033,519,365 blocks transactions logs traces Erigon node MEV labels 1,389,814 2,155,838 1,196,662 tx labels eigenphi.io, etherscan.io zeromev.org modified version of (Weintraub et al., 2022) mempool data 910,577,701 tx arrival times mempool.guru relay data 427,443,787 proposed blocks etherscan.io, Table 2 OFAC 134 addresses treasury.gov

3.1. Ethereum Blockchain

We extract three types of data from the Ethereum blockchain as described below: reward data, maximal extractable value (MEV), and sanctioned address usage. To collect Ethereum blockchain data, we run an Erigon (Erigon, 2023) execution client along with a Lighthouse (Lighthouse, 2023) consensus client to gather all mainnet blocks and transactions. We collect additional MEV data from third parties as described below.

Reward Data. In this work we are interested in understanding the profit generated from building a block, and where this profit is going (i.e., how much is split between the builder and proposer). Though block proposers/validators also receive rewards for their work in the Beacon network, we omit these from our analysis as they are set values and orthogonal to the PBS scheme. We focus, instead, on the user-generated rewards. Note that throughout we focus on on-chain payments and do not consider possible off-chain payments.

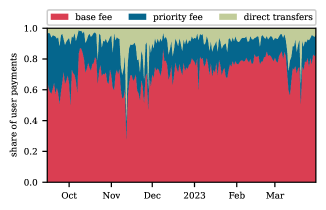

Since the adoption of EIP-1559 (Buterin et al., 2019), a user pays a fee of for their transaction consisting of a base fee and a priority fee . The base fee is paid per unit of gas (a measure of the computation required for a transaction) and is set by the network, adjusting dynamically according to network demand, i.e., higher demand, higher base fee. This base fee is burned by the system and thus is not part of the block rewards. The priority fee, on the other hand, is set by the user and works as a tip for the block creator to include the transaction. In each block, the transaction fee recipient field is set by the creator of the block (i.e., the builder in PBS) and is the address that receives the priority fees.

Recall that users can also “tip” the block creator via direct transfers to the fee recipient address. To capture these, we trace each transaction and record any internal transfer to the fee recipient address that takes place within the execution of a transaction. We record the sum of all priority fees and direct transfers as the total profit of each block. Figure 3 shows the breakdown of the user payments for each block. We observe that the majority of user fees are part of the base fee (on average, 72.3% of user fees are burned each day). The priority fee tends to be the second largest component of user payments (a daily average of 18.4%), while direct transfers make up the smallest part of user payments. Together the priority fee and the direct transfers make up the block’s value for the proposers and builders. Thus, they (are expected to) try to maximize this.

As a standard in the PBS scheme, the block builder pays out the proposer some amount of the profit (generally the majority) in a direct transfer as the last transaction in the block. We record this value as the proposer profit for each block, and the difference between this value and the block profit as the builder profit. For non-PBS blocks, the proposer profit is equal to the total value of the block.

Maximal Extractable Value. MEV refers to any value that can be extracted from block production beyond the standard block reward and gas fees. MEV extraction is performed by either including, censoring, or changing the order of transactions within a block. While searchers, builders, and validators have the capability to extract MEV, there is a clear hierarchy of power where searchers depend on builders to include and not ignore or steal their MEV bundles. Similarly, builders depend on validators to include these MEV bundles in their blocks and not include the validator’s own bundles. The three most common types of MEV are sandwich attacks, arbitrage, and liquidations (Ethereum, 2023a). In short, the attacker makes a financial gain with a sandwich attack by front- and back-running the victim’s trade on a DEX. Arbitrage takes advantage of price differences across DEXes for profit. Finally, liquidations close positions on lending protocols that are close to becoming undercollateralized. Whether MEV benefits or harms the Ethereum ecosystem is actively debated. Regardless, it currently accounts for a significant proportion of block rewards.

We leverage MEV data to understand what impact MEV has after the merge as a source of income for all the parties involved in PBS, and also to understand if relays that claim to be against MEV, truly do not include MEV extraction within their forwarded blocks. Weintraub et al. (Weintraub et al., 2022) publicly released their scripts that detect MEV in the form of sandwiches, arbitrage, and liquidations. There also exist numerous platforms that continuously monitor newly produced blocks to identify and classify MEV. These platforms and scripts have been developed independently from each other and with different focuses. We combine MEV data (i.e., take the union) from three different sources: EigenPhi (EigenPhi, 2023), ZeroMev (Zeromev, 2023), and our own data using a modified version of the scripts of Weintraub et al. (Weintraub et al., 2022) to craft a large MEV dataset. It is difficult to detect MEV, the challenge is in identifying MEV patterns but once a new pattern is identified it is unlikely that flagged transactions are false positives. Thus, to have maximum coverage, we combine MEV data from three different sources (peer-reviewed work and specialized companies).

We wrote a crawler to scrape the MEV data from EigenPhi’s website and leveraged Etherscan’s “EigenPhi” label (Etherscan, 2023) to identify which blocks to scrape from EigenPhi’s website. For ZeroMev, we were able to obtain MEV data via their public API. We slightly modified the scripts of Weintraub et al. (Weintraub et al., 2022) to be compatible with our post-merge Ethereum client. The scripts detect MEV by analyzing the logs that are triggered by events defined within the smart contracts of the individual platforms (i.e., Uniswap, Aave, Maker, etc.). We collected the logs for transactions in our measurement period from our Ethereum client.

Sanctioned Transactions. To identify transactions that involve sanctioned addresses, we first obtain a list of sanctioned addresses from OFAC (of Foreign Assets Control, 2022). We then scan the transaction traces of all transactions in our data collection period to identify any transactions where any nonzero amount of ETH was transferred from or to a sanctioned address. We further scan the logs to identify any transfers of the top five ERC-20 tokens (WETH, USDC, DAI, USDT, and WBTC) from or to any sanctioned address. Additionally, we also monitor all token transfers for TRON as it was sanctioned as of November 2022 (OFAC, 2023a). Thus, we are able to obtain lower bounds for transactions that are not OFAC-compliant. Note that we only consider an address sanctioned from the day after it was sanctioned by OFAC, as the OFAC list updates do not have an exact timestamp but are immediately effective (Sanctions Compliance Guidance for the Virtual Currency Industry, 2021).

3.2. Ethereum Network

We obtain Ethereum network data from the Mempool Guru project (Mempool.guru, 2023), which collects all transactions observed in the Ethereum network via their own nodes. In particular, for each transaction included on the Ethereum blockchain, we receive the timestamps at which each of the seven full nodes run by the project first observed the transaction. For the data collection specification, we refer the reader to (Yang et al., 2022). This data allows us to distinguish between transactions that were publicly propagated in the network, from those sent through private channels to the creator of the block.

3.3. Relay

Relays act as a bridge between builders and proposers (i.e., validators). Builders submit blocks to relays which are tasked with checking and subsequently forwarding them to proposers. Relays maintain a list of proposers that are currently connected to them. Relays also keep track of which block builders proposed to them and which block the relay chose to be forwarded to the subscribed proposers. Relays expose a public API that builders can leverage to submit blocks and which proposers can use to subscribe to the relay (Flashbots, 2023b). This API was proposed by Flashbots (Flashbots, 2023). Table 2, provides an overview of the eleven relays that we crawled during our study. These are all of the known relays during the time window of our analysis. We connected to each individual relay and requested for every block number: (1) the final block that was sent to the proposer, (2) a list of blocks that have been submitted by the builders to the relay, and (3) information about proposers that are currently connected to the relay. Most relays are a fork of MEV Boost – an implementation of PBS built by Flashbots. While Flashbots runs its own relay, anyone can fork Flashbots’ implementation and run their own relay. Blocknative is the only relay that uses its own implementation called Dreamboat. MEV Boost and Dreamboat follow the same API, namely Flashbots’ relay API specification (Flashbots, 2023b).

Relay Name Endpoint Fork Aestus https://aestus.live MEV Boost Blocknative https://builder-relay-mainnet.blocknative.com Dreamboat bloXroute (Ethical) https://bloxroute.ethical.blxrbdn.com MEV Boost bloXroute (MaxProfit) https://bloxroute.max-profit.blxrbdn.com MEV Boost bloXroute (Regulated) https://bloxroute.regulated.blxrbdn.com MEV Boost Eden https://relay.edennetwork.io MEV Boost Flashbots https://boost-relay.flashbots.net MEV Boost GnosisDAO https://agnostic-relay.net MEV Boost Manifold https://mainnet-relay.securerpc.com MEV Boost Relayooor https://relayooor.wtf MEV Boost UltraSound https://relay.ultrasound.money MEV Boost

4. Proposer-Builder Separation Landscape

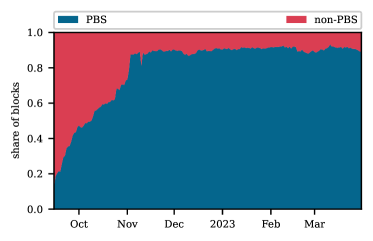

We commence the analysis by providing an overview of the adoption of PBS since the merge. Figure 4 visualizes the proportion of blocks built with PBS over time. We note here that we consider a block to be built through PBS, if it is reported by one of the eleven relays we crawl or if we detect a payment from the builder to the proposer in accordance with the PBS convention. Of all PBS blocks we identify, 99.6% are claimed by at least one of the relays we crawl, while 92% exhibit the payment from the builder to the proposer as specified by PBS. Note here that 99.6% of PBS blocks that do not include the payment from the builder to the proposer have the same builder and proposer address in the PBS data.

The daily share of PBS blocks rises from around 20% on 15 September 2022, the day of the merge, to over 85% on 3 November 2022 (cf. Figure 4). From then on out, the daily share of PBS blocks remains relatively stable and ranges between 85% and 94% with one exception on 10 November 2022, i.e., the sharp dip in Figure 4. This drop in the share of PBS blocks can be traced back to blocks from a builder with incorrect timestamp values being submitted to proposers. Their nodes subsequently rejected the proposed blocks, and the proposers had to fall back to local block production (metachris, 2022).

4.1. Relays

We continue by analyzing the relay landscape. First, we provide an overview of the characteristics of the eleven relays we crawled in Table 3. For one, relays differentiate themselves by how they connect to builders. Two relays, namely Blocknative and Eden, do not connect to any external builders, i.e., the relays only forward blocks from their own builders. There are three relays from bloXroute (bloXroute (E), bloXroute (M), and bloXroute (R)) that run their own builders but also connect to external builders. The process of becoming a builder for these relays is not permissionless though. Finally, for the remaining relays, builders can join in a permissionless manner. Further, of these relays, the Flashbots relay is the only one that also runs its own builder. Regarding censorship, several relays announced that they would comply with OFAC sanctions (Blocknative, bloXroute (R), Eden, and Flashbots). Finally, the bloXroute (E) claims to filter out generalized front-running and sandwich attacks. Depending on these announcements by relays as well as possibly additional consideration, validators choose to connect to any number of relays. Recall that as PBS is an opt-in protocol, they do not need to connect to any relay.

Relay Name Builders Censorship MEV Filter Aestus permissionless x x Blocknative internal OFAC-compliant x bloXroute (E) internal & external x front-running bloXroute (M) internal & external x x bloXroute (R) internal & external OFAC-compliant x Eden internal OFAC-compliant x Flashbots internal & permissionless OFAC-compliant x GnosisDAO permissionless x x Manifold permissionless x x Relayooor permissionless x x UltraSound permissionless x x

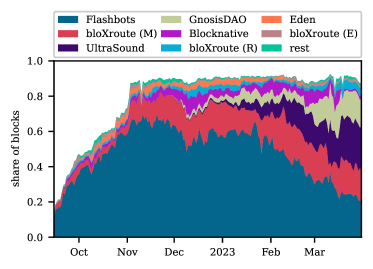

Figure 5 plots the daily share of blocks by each relay during our data collection period. We show the daily block share per relay for the top eight relays (in terms of the number of blocks proposed) and aggregate the daily share of blocks for the remaining relays. We further note that if the same block was proposed by multiple relays, we attribute the block equally to each relay. Around 5% of all PBS blocks were proposed by more than one relay. Unsurprisingly, the Flashbots relay, i.e., the relay that spearheaded PBS, is the largest. They consistently account for more than half of all blocks proposed through PBS from November 2022 onwards and even account for more than half of all (including non-PBS) blocks between November 2022 and January 2023. Since then, the market share of the Flashbots relay has been decreasing, dropping to 23% by the end of March. BloXroute (M) is the second largest relay in terms of total number of blocks built and accounts for 20% of all blocks. All remaining relays are comparatively small initially, but two relays (Ultrasound and GnosisDAO) have experienced a significant increase in their market share since the start of 2023. To summarize, we observe that by the end of March 2023, there are multiple relays with a significant market share while there was only one dominant relay in September 2022.

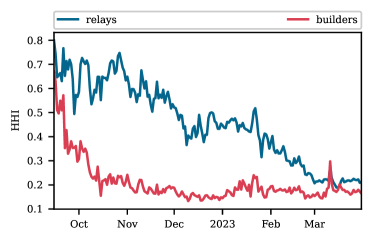

To further investigate the decentralization of the relay landscape, we plot the Herfindahl-Hirschman Index (HHI) for the relays in Figure 6. In economics, the HHI is a statistical measure of the concentration of an industry (Rhoades, 1993) and computed as follows

where is the number of players in a market and is the market share of player . The higher the HHI, the higher the concentration of the industry. We note that as opposed to the Gini coefficient, the HHI also takes the number of players into account. In Figure 6, the blue line shows the concentration amongst the eleven relays. We observe a general downward trend of the HHI with a significant oscillation. The maximum value of the relay HHI is 0.80, and the minimum is 0.19. Generally, an industry with an HHI above 0.15 is said to have a moderate to high concentration. Thus, we summarise that even though the concentration of the relay industry decreases with time, it remains concentrated, i.e., centralized.

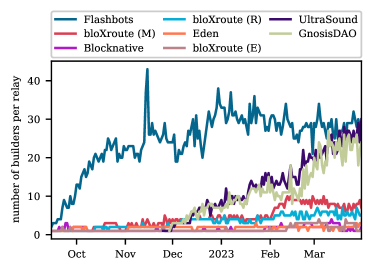

We conclude the general analysis of the relay landscape by analyzing the number of builders per relay. We plot the daily number of different builders sending blocks to each relay over time in Figure 7. For the Flashbots relay, the number of builders experienced an initial increase and remained relatively stable from December 2023 onwards at around 30 builders. The number of builders for the second largest relay (bloXroute (M)) was initially very low but experienced a sharp and consistent increase. Finally, we remark that the number of builders for both the UltraSound and GnosisDAO relays is very similar and rising over time (almost overtaking Flashbots’ numbers by the end of our study period), and the number of builders for the remaining relays has stayed comparatively low. We further observe that the number of builders is increasing, especially for relays that are permissionless (cf. Table 3). Additionally, we notice that permissionless relays with a higher number of builders have a more significant market share (cf. Figure 5).

4.2. Builders

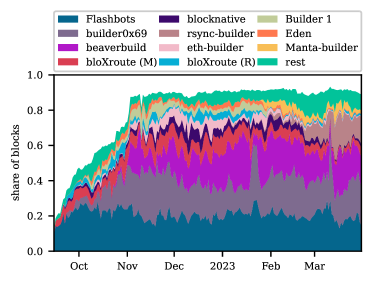

Previously, we analyzed the number of builders per relay but builders themselves can also be connected to multiple relays at a time. Thus, in this section, we take a look at the builder landscape in detail. Note that throughout we will identify individual builders by their builder public key. We further cluster together builders that use the same fee recipient address. We provide a map from the builder name to the builder fee recipient address(es) and the builder public key(s) in Appendix 11 in Table 5. Figure 8 visualizes the daily share of blocks by each of the biggest eleven builders, in terms of the total number of blocks. We notice that the top three builders, i.e., Flashbots, builder0x69, and beaverbuild, consistently account for more than half of all blocks together from November 2022 onwards. The remaining builders all individually account for less than 15% of blocks on each day. Thus, the builder landscape, just as the relay landscape, appears to be dominated by a small number of large players.

This picture cements itself when we calculate the daily builder HHI (cf. red line in Figure 6). In total, there were 133 unique builders, and the builder HHI oscillates between 0.13 and 0.67 with a mean of 0.21. We further observe a very significant downward trend in the concentration initially. From November onwards, the concentration of the builder landscape remains relativity stable at around 0.17. We note that HHI between 0.15 and 0.25 indicates moderate concentration, while only HHI values below 0.15 indicate an unconcentrated industry. Thus, we conclude that the builder landscape is also quite concentrated but generally less so than the relay industry.

5. PBS Impact on Block Composition

In the following, we investigate the block composition of PBS blocks by individual builders and in comparison to non-PBS blocks. We place a particular focus on the block value to analyze whether PBS “decentralizes transaction validation by not giving large entities an advantage in block building” as indented by its design goals (Ethereum, 2023b). The idea is that if validators had to build blocks themselves, large entities would be at an advantage. As a result of the high complexity of block building, large entities would be expected to build comparatively more profitable blocks and would grow even bigger — increasing transaction validation centralization.

5.1. Block Value

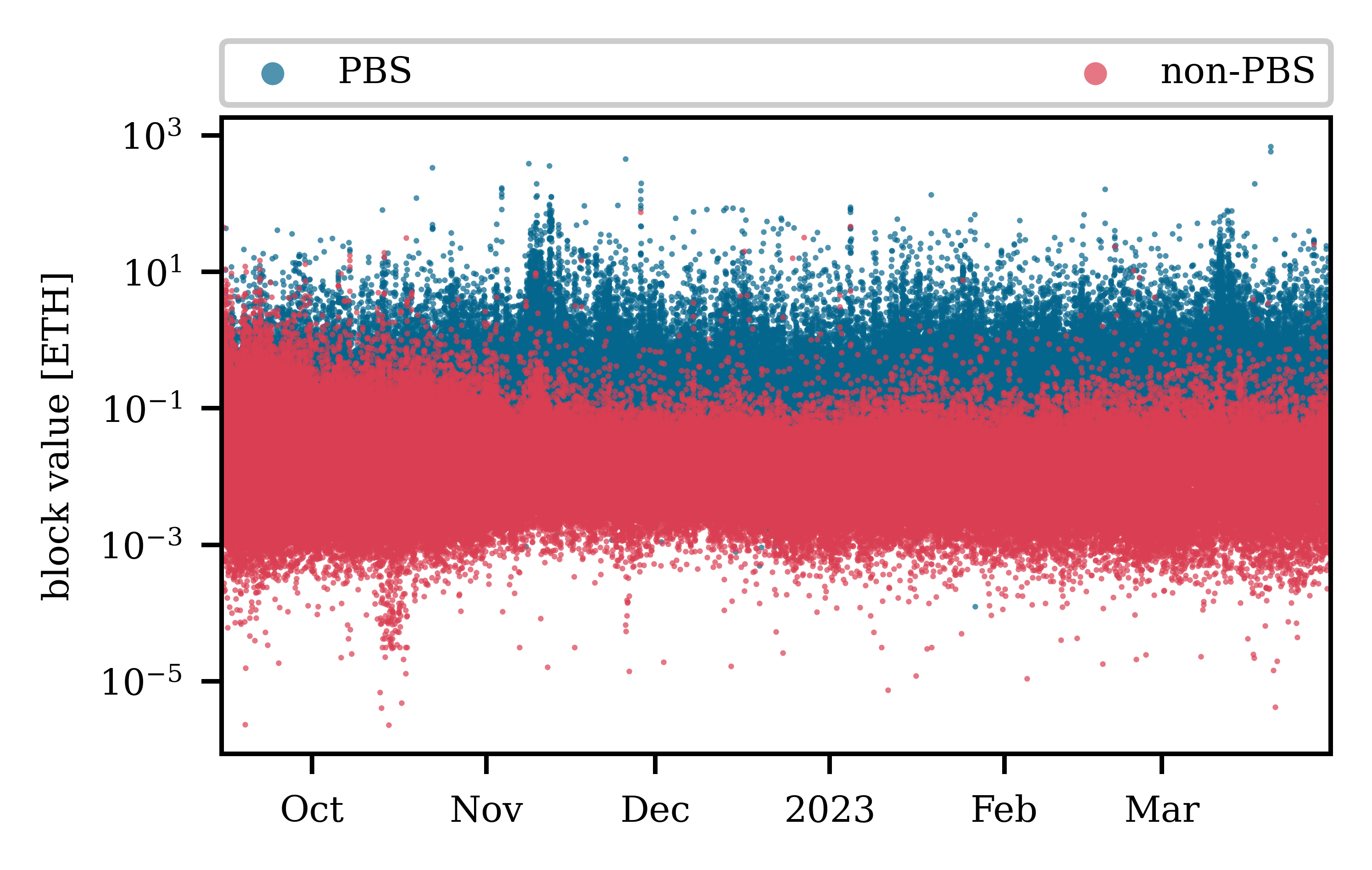

Recall that we define block value as the amount of user-generated reward available in a block (i.e., priority fees and direct transfers) and shared by the builder and proposer. We compare the block value of PBS and non-PBS blocks in Figure 9. Notice that the block value for PBS blocks is consistently significantly higher than for non-PBS blocks. The gap appears to grow with time which might be due to a higher level of PBS adoption or increasing sophistication of PBS block builders. Regardless, it appears that professionalized builders are at an advantage concerning value extraction compared to proposers who are building their blocks outside of PBS.

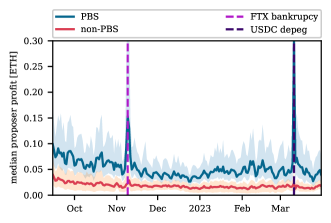

Additionally, we compare the daily median proposer profits (amount the builder pays out to the proposer) for proposers that use PBS and those that do not use PBS (total block value) in Figure 10. We find that PBS proposers have significantly higher median profits (blue line) than non-PBS proposers (red line). This difference is largest on high MEV days, i.e., FTX bankruptcy (violet dashed line) and USDC depeg (purple dashed line). Even more startlingly, the 25th percentile of PBS proposer profits (bottom of blue area) is generally above the 75th percentile of non-PBS proposers (top of red area). Thus, it appears that proposers will generally make greater profits if they use PBS as opposed to building their own blocks — an indication that PBS achieves its goal of not giving institutional validators an advantage over hobbyist validators in value extraction.

5.2. Distribution of Value

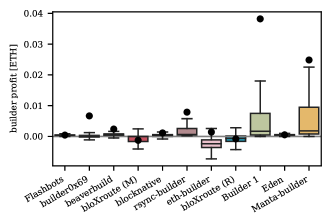

In the following, we analyze the distribution of a block’s value between block builders and proposers. Figure 11 visualizes the builder profit (i.e., priority fees and direct transfers subtracted by the builder payment to the proposer) as a box plot for each of the top eleven builders. One immediately notices that the builder profit varies significantly between builders. The Flashbots, Eden, and blocknative builders appear to follow a similar strategy. The variance of their profit per block is very small, and the mean profit, indicated by the black dot, is between 0.0004 and 0.001 ETH for each of them. We also observe a similar pattern for Builder 1, rsync-builder, and Manta-builder. These three builders are the most profitable builders, with more than 0.0075 ETH average profit per block each. Further, they, along with the previously mentioned builders, do not tend to subsidize (i.e., make a negative profit) on blocks.

For the remaining five builders, the profit per block is regularly negative, i.e., they are subsidizing the blocks. However, while the builder0x69, beaverbuild, and eth-builder frequently subsidize blocks, their mean profit is positive. Thus, while subsidizing some blocks, potentially to encourage transaction flow from searchers and build trust with them, they make up for it on high-value blocks. The mean profit of two bloXroute builders, on the other hand, is not positive. We conclude that they either subsidize blocks or are making a profit in ways that we cannot detect. The bloXroute founder has commented on this phenomenon and noted that “the bloXroute builder can sustainably subsidize their blocks using earnings from other business revenue streams” (Kim, 2023). He, however, did not further hint at the origin of these revenue streams.

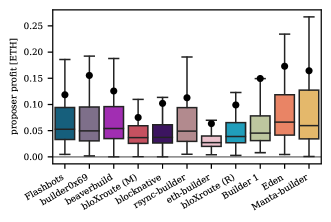

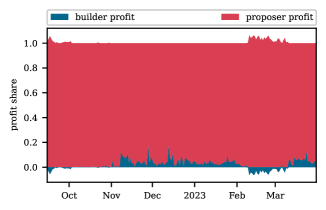

When turning to the proposer profits (cf. Figure 12), the picture looks more uniform. In general, each builder is offering the proposers similar profits for their blocks. We note that we observe differences of more than a factor of two in mean proposer profits for different builders. However, we believe that, in part, these differences likely stem from the builders being active at different times. We also note the proposer profits are highly skewed, i.e., the mean is significantly higher than the median, which is due to the existence of large MEV opportunities that come about rarely and drive up the mean. Combining our builder profit and proposer profit analysis, we conclude that the proposers’ profits are more than a factor of ten higher on average than the builder profits. We provide an additional analysis of this in Appendix 12.

Finally, we analyze what proportion of the value promised by relays to the proposers is actually delivered. Recall that proposers initially only receive a blinded block along with the value of the block, i.e., the profit that is promised to them from the relays. Thus, when choosing to sign a block, they pick the one with the highest value and trust the relay that this value will be delivered. The left side of Table 4 shows, for the blocks that were proposed, the total value delivered to the proposers along with the total value that was promised. We compare the two values and calculate the share of the promised value that was delivered in the third column of Table 4. Astonishingly, each relay, with the notable exception being Aestus, has not delivered the full promised value and thus broke the trust they enjoyed from the proposers.

Despite this, we note that all but two relays delivered more than 99.8% of the value. The two exceptions are the Eden relay, which only delivered 93.8% of the promised value, and the Manifold relay, which only delivered 19.9% of the promised value. For the Eden relay, the vast majority of the missing value stems from a single block. The relay announced the value of block 15,703,347 to be 278.29 ETH but only delivered 0.16 to the proposer. We note that the Eden relay did not deliver the full value in 0.05% of blocks (cf. fourth column of Table 4). Similarly, for Manifold, a large chunk of the missing value stems from the same day — 15 October 2022. On this day, a builder noticed that the Manifold relay was not checking the block rewards of the blocks that it was receiving (manifoldx, 2022). The builder, thus, submitted blocks with wrongly declared rewards, and 184 of these blocks made it onto the blockchain. Then, the profit from these blocks went to the builder, and the proposers were left with nothing. Across all relays, 98.7% of the promised value arrived at the proposers and 0.86% of blocks did not deliver their promised value.

delivered value [ETH] promised value [ETH] share of value [%] share over-promised of blocks [%] sanctioned blocks share of sanctioned blocks [%] Aestus 404.582057 404.582057 100.000000 0.030921 35 1.082251 Blocknative 6086.147269 6087.225188 99.982292 3.553043 1001 1.807610 bloXroute (E) 1027.721708 1028.849142 99.890418 4.449079 780 5.420431 bloXroute (M) 19248.859647 19250.965641 99.989060 2.723592 10038 5.375475 bloXroute (R) 3689.983494 3690.389671 99.988994 0.113681 254 0.824756 Eden 4204.908110 4483.541341 93.785421 0.047946 81 0.323586 Flashbots 90812.869179 90818.879444 99.993382 0.032546 1451 0.210801 GnosisDAO 12461.847484 12462.572553 99.994182 0.894293 2225 2.956300 Manifold 416.283800 2095.806623 19.862701 6.880409 1012 14.356646 Relayooor 319.504570 319.608181 99.967582 2.095704 162 5.658400 UltraSound 13970.478128 13971.955037 99.989429 0.953061 3289 3.309419 PBS 152643.185446 154614.374878 98.725093 0.855103 20328 1.710460

5.3. Block Contents

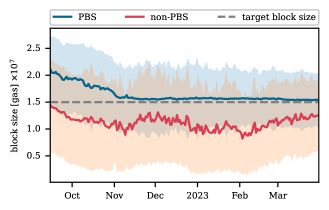

We further analyze how blocks are composed by looking at how builders are including transactions in blocks. In Figure 13 we look at the daily average block size, i.e., the gas usage, of PBS blocks vs. non-PBS blocks. We see that PBS blocks start off higher than Ethereum’s target block size with gas right after the merge and then drop with time until mid-November (blue line in Figure 13). From then on the mean daily block size of PBS block is stable and hovers slightly above Ethereum’s target block size of gas. However, even though the daily average is stable, the standard deviation (the blue-shaded area) is significant. For non-PBS blocks the mean block size, the red line in Figure 13, is continuously below the target size and exhibits greater fluctuations than that of PBS blocks. Similarly, the standard deviation of non-PBS blocks is slightly larger than that of PBS blocks. Thus, PBS blocks tend to, at least on average, be fuller and have a more consistent size than non-PBS blocks.

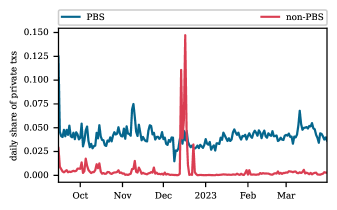

We also explore the fraction of transactions in blocks that are coming from the P2P network (i.e., observed in the public mempools), versus sent via private avenues. In Figure 14 we observe that private transactions are largely being included by PBS block builders. These are likely from the searchers of builders themselves, from searchers sending transactions directly to builders and privacy services to prevent attacks (e.g., Flashbots (Flashbots, 2023) and Bloxroute(Klarman et al., 2018)).

Note that the peak in private transaction share of non-PBS blocks in December is almost entirely made up of a single sender () and receiver () pair, where

-

•

: 0x4d9ff50ef4da947364bb9650892b2554e7be5e2b

-

•

: 0x0b95993a39a363d99280ac950f5e4536ab5c5566.

Both addresses are from Binance and the transactions are simple ETH transfers. In total, these private transactions from Binance make up for more than 88% of all private transactions in non-PBS blocks in December 2022. Of these, more than 90% are 75 blocks proposed by AnkrPool proposers. Thus, it appears that AnkrPool proposers were receiving private transactions from Binance for around two weeks in December 2022.

5.4. MEV value

To conclude our exploration of the impact of PBS on block composition, we take an in-depth look at the number of and the profit from the MEV transactions in PBS and non-PBS blocks. Note that throughout, we will focus on the three most well-known and frequent types of MEV: sandwich attacks, cyclic arbitrage, and liquidations.

We start by commenting on the reliability of the MEV filtering policy by the bloXroute (E) relay. Recall from Table 3 that the bloXroute (E) claims to filter out front-running transactions — including both generalized front-running and sandwich attacks. While it is non-trivial and not always possible to detect generalized front-running as the front-run transactions will likely not be included on the blockchain, we can use our MEV data to identify how many sandwich attacks were in blocks from the bloXroute (E) relay. We find that since the merge, the bloXroute (E) has included 2,002 sandwich attacks and therefore conclude that the filtering performed by the relay exhibits significant gaps.

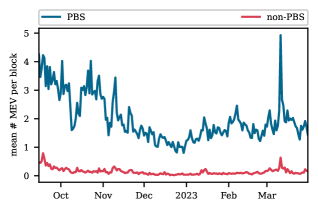

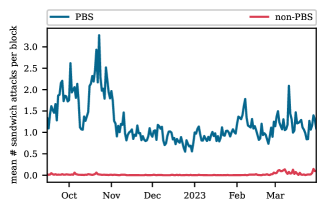

We continue with a more general analysis of MEV in PBS and non-PBS blocks. Figure 15 shows the mean number of MEV transactions per block for PBS blocks (blue line) and non-PBS blocks (red line). One notices that the number of MEV transactions is significantly higher in PBS blocks than in non-PBS blocks. Thus, it appears that builders have better connections to searchers and their in-flow of MEV transactions than proposers building their own blocks. In Appendix 13, we further break up the MEV transactions into sandwich attacks, cyclic arbitrage, and liquidations to compare the prevalence of each type of MEV in PBS and non-PBS blocks.

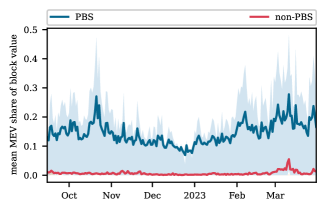

Generally, MEV transaction flow is regarded as crucial for both builders and proposers as it accounts for a significant proportion of block value. We plot the daily mean share of block value that comes from MEV transactions for PBS and non-PBS blocks in Figure 16. Note that the shaded area indicates the 25th and 75th percentile. Similarly to our previous analysis, we find that while MEV makes up a significant share of the block value for PBS blocks, 14.4% on average, very little of the block value can be attributed to MEV for non-PBS blocks.

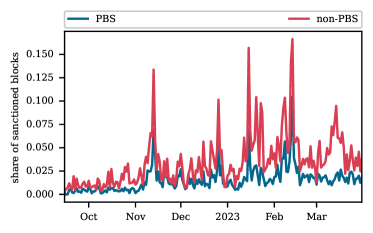

6. Censorship Resistance

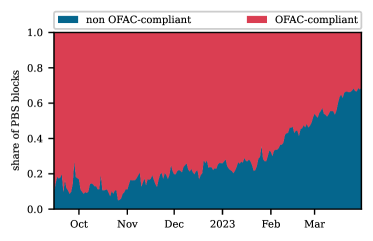

We conclude the analysis by investigating whether PBS achieves its second design goal: preventing censorship. The idea is that since the block proposer only receives the block header and is not aware of the block contents when signing the block, it is not possible for powerful organizations to pressure proposers into complying with their sanctions (Ethereum, 2023b). Throughout this section, we focus on OFAC sanctions when discussing censorship, given that it is the most prominent case study of censorship in the Ethereum ecosystem. As we already pointed out (cf. Table 3), a number of relays announce that they are OFAC-compliant, i.e., they censor transactions in accordance with OFAC sanctions. Thus, we start by analyzing the daily share of blocks produced by relays that self-report themselves as censoring in Figure 17 to obtain an overview of the proportion of blocks that stem from censoring relays. Notice that initially, the share of PBS blocks built by OFAC-compliant relays is more than 80%. From November on, this share starts to decrease and reaches just north of 45% by the end of March. However, even though the proportion of PBS blocks built by non-censoring relays increases, a significant proportion of PBS blocks are built by censoring relays.

To further investigate whether PBS helps prevent censorship, we analyze the share of blocks that include transactions that are not OFAC-compliant in Figure 18. In particular, we compare PBS (shown in blue) and non-PBS (shown in red) blocks and observe that in general, a more significant proportion of non-PBS blocks include transactions that are not OFAC-compliant in comparison to PBS blocks. Thus, it does not appear that PBS is preventing censorship as it was envisioned but instead is linked to more censored blocks. Additionally, PBS gives an avenue for proposers who wish to comply with OFAC sanctions to only connect to relays that promise to comply with OFAC sanctions. Thus, we believe that there are incentives for at least some relays to comply with OFAC sanctions.

Finally, we point out that even though some relays advertise themselves to be OFAC-compliant, they do not always uphold their promises. On the right side of Table 4, we show the number of blocks along with the share of total blocks that each of the biggest eight relays included, which contain transactions that are not OFAC-compliant. We observe that every single relay, regardless of whether they promised to adhere to OFAC sanctions or not, has included transactions that are not OFAC-compliant. The relays that self-report being OFAC-compliant are highlighted in italics in Table 4. Further, we find the most significant gaps in their filtering to follow updates of the OFAC sanctions list. For instance, new Ethereum addresses were added to the OFAC sanctions list on 8 November 2022 (OFAC, 2023a), but the OFAC blacklist of the Flashbots relay was only updated on 10 November 2022 (Flashbots, 2023a). Further, updates to the OFAC list on 1 February 2023 (OFAC, 2023b) were still not reflected in the OFAC blacklist of the Flashbots relay on 1 May 2023.

Though we find that all relays that promise to be OFAC-compliant let through non-OFAC-compliant transactions, the share of blocks that are not OFAC-compliant from these relays is significantly smaller than from the other relays. For instance, while more than 14% of blocks from Manifold do not comply with OFAC sanctions, the same only holds for 0.21% of blocks from the Flashbots relay. Thus these relays are largely reliable in their filtering, modulo days when there are updates to the OFAC sanctions list.

7. Related Work

Mining Pool Distribution. The value proposition of cryptocurrencies is to facilitate payments in a decentralized manner. Gencer et al. (Gencer et al., 2018) were the first to study the level of decentralization of Bitcoin and Ethereum miners. Their work shows that the mining process of both blockchains is fairly centralized. Subsequent studies of the mining power distribution on Ethereum by Kiffer et al. (Kiffer et al., 2021) and Lin et al. (Lin et al., 2021) support these findings. Our work studies Ethereum post-merge and finds that block building via PBS continues to exhibit significant levels of centralization.

Transaction Inclusion. With limited block space, users traditionally bid for inclusion in blocks via the transaction fee mechanism. Previous works by Messias et al. (Messias et al., 2021) and Messias et al. (Messias et al., 2023), explore the lack of transparency in fee auctions for Bitcoin and Ethereum. Both works show that often transactions don’t follow a fee-based ordering and that the lack of transparency leads to higher user costs and miner profits. Earlier work by Pappalardo et al. also explored the inefficiencies of transaction inclusion times in the Bitcoin network (Pappalardo et al., 2018).

Maximal Extractable Value. The increasing complexity of block building is in large part a result of MEV. Eskandari et al. (Eskandari et al., 2020) and Daian et al. (Daian et al., 2020) offer an early description of MEV. A succeeding stream of literature quantifies the amount of MEV on the Ethereum blockchain (Torres et al., 2021; Qin et al., 2022; Wang et al., 2022) and, thereby, demonstrates the immense scale and impact of MEV.

In their pre-merge exploration of MEV, Piet et al. (Piet et al., 2022) place a particular focus on the value distribution between searchers and miners. They find that the majority of MEV profits go directly to the miners. In our exploration of PBS, we analyze the profit share between builders and proposers post-merge and find that most of the profit goes to the proposers.

Given the losses faced by users as a result of MEV, multiple approaches emerged to prevent or lessen the impact of MEV. We refer the reader to (Heimbach and Wattenhofer, 2022) for an overview of these approaches. The approach with the most significant level of adoption pre-merge was MEV auction platforms. These platforms aimed to protect the privacy of the user transactions pre-execution, i.e., provide front-running protection, and move the priority gas auction off-chain. Flashbots (Flashbots, 2023), was the biggest MEV auction platform. Weintraub et al. (Weintraub et al., 2022) provide an empirical analysis of the Flashbots platform. Their work shows that powerful miners doubled their profits with Flashbots, while the profits for searchers decreased. In contrast to their work, we study PBS and the progression of Flashbots, post-merge. Our analysis also indicates that proposers, the new miners, profit by joining PBS.

Proposer-Builder Separation. An early exploration of PBS is provided by Yang et al. (Yang et al., 2022). Their work places a particular focus on the censorship of sanctioned transactions in the PBS ecosystem. They find that in the first couple months of PBS, sanctioned transactions experienced waiting times that were, on average, 68% longer than those of regular transactions. Further, we became aware of two simultaneous works (Wahrstätter et al., 2023b, a) that analyze the PBS landscape and its impact on censorship. Our work provides a more comprehensive analysis of the decentralization of the PBS ecosystem as well as the impact of PBS on block content and censorship.

8. Concluding Discussion

The full integration of PBS into Ethereum clients is currently on the Ethereum road map (Ethereum, 2023b). Thus, it is essential to analyze the current state of PBS during its opt-in phase to investigate how its realities measure up to its promises.

Decentralization of Transaction Validation. Our work investigates whether PBS achieves its design goal of decentralizing block validation by not giving large entities an advantage in block building. Through our in-depth analysis of the impact of PBS on the block (value) composition, we come to the conclusion that professionalized builders have a clear advantage in building profitable blocks. Thus, PBS gives validators access to competitive blocks and can prevent “hobbyists from being out-competed by institutional players that can better optimize the profitability of their block building” (Ethereum, 2023b).

At the same time, we observe a significant centralization for both the relays and builders. Though the main PBS article on the Ethereum Foundation’s website suggests that there is no harm in centralizing block building, as long as the validators are decentralized (Ethereum, 2023b), there are still concerns regarding the potential harm of builder centralization. For one, Vitalik Buterin (Buterin, 2022) commented on the need to prevent new types of censorship vulnerability stemming from builder centralization. Our work suggests this is still an open problem.

Censorship Resistance. With our work, we also shed light on the extent to which PBS achieves its second design goal: preventing censorship. We find no signs of PBS preventing censorship in practice. In fact, we consistently observe that PBS blocks are less likely to include transactions from sanctioned addresses than non-PBS blocks. Thus, our analysis concludes that PBS currently falls short of its second design goal.

Trust in Relays. To conclude, we comment on the trust in relays that is required by the current PBS implementation. Presently, relays are trusted by both builders, to keep their blocks blinded until they are signed, and by proposers, to deliver the promised value and adhere to any additional promises made concerning censorship and MEV filtering, for instance. Our data provides us with the opportunity to analyze whether relays have broken the trust placed on them by proposers. Astonishingly, we find instances of all but one relay falling short of their promises. We observe relays not delivering the full promised value, as well as significant gaps in their censorship and MEV filtering policies.

The current plan for a native implementation of PBS into the Ethereum protocol reduces the aforementioned trust assumptions by eliminating the need for relays (Buterin, 2021b). However, there are still security concerns regarding the present proposal (Monnot, 2022). The proposal is also restricted to ensuring that the value is delivered but does not address the other aspects. Thus, we believe that we are still far from eliminating the need for relays. Meanwhile, the lack of incentives for relays not to misbehave is an open problem: currently, the revenue of these key players is not part of the PBS design.

9. Acknowledgements

We thank Balakrishnan Chandrasekaran and the anonymous IMC 2023 reviewers for their useful suggestions. L. Kiffer contributed to this project while under an armasuisse Science and Technology CYD Distinguished Postdoctoral Fellowship. This work was supported by the Zurich Information Security & Privacy Center (ZISC).

References

- (1)

- Aggregate Data Set (2023) Aggregate Data Set 2023. https://github.com/liobaheimbach/Ethereum-s-Proposer-Builder-Separation-Promises-and-Realities.

- Buterin (2014) Vitalik Buterin. 2014. A next-generation smart contract and decentralized application platform. (2014).

- Buterin (2021a) Vitalik Buterin. 2021a. Proposer/block builder separation-friendly fee market designs. https://ethresear.ch/t/proposer-block-builder-separation-friendly-fee-market-designs/9725.

- Buterin (2021b) Vitalik Buterin. 2021b. Two-slot proposer/builder separation. https://ethresear.ch/t/two-slot-proposer-builder-separation/10980.

- Buterin (2022) Vitalik Buterin. 2022. State of research: increasing censorship resistance of transactions under proposer/builder separation (PBS). https://notes.ethereum.org/@vbuterin/pbs_censorship_resistance.

- Buterin et al. (2019) Vitalik Buterin, Eric Conner, Rick Dudley, Matthew Slipper, Ian Norden, and Abdelhamid Bakhta. 2019. Fee market change for ETH 1.0 chain. https://github.com/ethereum/EIPs/blob/master/EIPS/eip-1559.md.

- Daian et al. (2020) Philip Daian, Steven Goldfeder, Tyler Kell, Yunqi Li, Xueyuan Zhao, Iddo Bentov, Lorenz Breidenbach, and Ari Juels. 2020. Flash boys 2.0: Frontrunning in decentralized exchanges, miner extractable value, and consensus instability. In 2020 IEEE Symposium on Security and Privacy (SP). IEEE, 910–927.

- EigenPhi (2023) EigenPhi 2023. EigenPhi. https://eigenphi.io/. Accessed on February 29, 2024.

- Erigon (2023) Erigon 2023. Erigon. https://github.com/ledgerwatch/erigon.

- Eskandari et al. (2020) Shayan Eskandari, Seyedehmahsa Moosavi, and Jeremy Clark. 2020. Sok: Transparent dishonesty: front-running attacks on blockchain. In Financial Cryptography and Data Security: FC 2019 International Workshops, VOTING and WTSC, St. Kitts, St. Kitts and Nevis, February 18–22, 2019, Revised Selected Papers 23. Springer, 170–189.

- Ethereum (2023a) Ethereum 2023a. Maximal Extractable Value (MEV). https://ethereum.org/en/developers/docs/mev/. Accessed on February 29, 2024.

- Ethereum (2023b) Ethereum 2023b. Proposer-builder separation. https://ethereum.org/nl/roadmap/pbs/. Accessed on February 29, 2024.

- Ethereum Foundation (2023) Ethereum Foundation. 2023. The Merge. https://ethereum.org/en/roadmap/merge/. Accessed on February 29, 2024.

- Ethermine: Private RPC Endpoint Configuration (2023) Ethermine: Private RPC Endpoint Configuration 2023. Ethermine: Private RPC Endpoint Configuration. https://ethermine.org/private-rpc. Accessed on February 29, 2024.

- Etherscan (2023) Etherscan 2023. Etherscan’s Label Word Cloud. https://etherscan.io/labelcloud/eigenphi. Accessed on February 29, 2024.

- Flashbots (2023) Flashbots 2023. Flashbots. https://www.flashbots.net/. Accessed on February 29, 2024.

- Flashbots (2023) Flashbots 2023. Flashbots/mev-boost: Flashbots MEV-Boost Library. https://github.com/flashbots/mev-boost. Accessed on February 29, 2024.

- Flashbots (2023a) Flashbots 2023a. flashbots/rpc-endpoint. https://github.com/flashbots/rpc-endpoint/blob/main/server/ofacblacklist.go. Accessed on February 29, 2024.

- Flashbots (2023b) Flashbots 2023b. Relay API. https://flashbots.github.io/relay-specs/. Accessed on February 29, 2024.

- Flashbots (2023c) Flashbots 2023c. What is MEV-Boost? https://docs.flashbots.net/flashbots-mev-boost/introduction. Accessed on February 29, 2024.

- Gencer et al. (2018) Adem Efe Gencer, Soumya Basu, Ittay Eyal, Robbert Van Renesse, and Emin Gün Sirer. 2018. Decentralization in bitcoin and ethereum networks. In Financial Cryptography and Data Security: 22nd International Conference, FC 2018, Nieuwpoort, Curaçao, February 26–March 2, 2018, Revised Selected Papers 22. Springer, 439–457.

- Heimbach and Wattenhofer (2022) Lioba Heimbach and Roger Wattenhofer. 2022. SoK: Preventing Transaction Reordering Manipulations in Decentralized Finance. In 4th ACM Conference on Advances in Financial Technologies (AFT), Cambridge, Massachusetts, USA.

- Karp (1972) Richard M. Karp. 1972. Computers and Intractability: A Guide to the Theory of NP-Completeness. W.H. Freeman.

- Kiffer et al. (2021) Lucianna Kiffer, Asad Salman, Dave Levin, Alan Mislove, and Cristina Nita-Rotaru. 2021. Under the Hood of the Ethereum Gossip Protocol. In International Conference on Financial Cryptography and Data Security. Springer, 437–456.

- Kim (2023) Christine Kim. 2023. MEV: Maximal Extractable Value Part 2: The Rise of the Builders. https://www.galaxy.com/research/whitepapers/mev-the-rise-of-the-builders/. Accessed on February 29, 2024.

- Klarman et al. (2018) Uri Klarman, Soumya Basu, Aleksandar Kuzmanovic, and Emin Gün Sirer. 2018. bloxroute: A scalable trustless blockchain distribution network whitepaper. IEEE Internet of Things Journal (2018).

- Lighthouse (2023) Lighthouse 2023. Lighthouse: Ethereum consensus client. https://github.com/sigp/lighthouse. Accessed on February 29, 2024.

- Lin et al. (2021) Qinwei Lin, Chao Li, Xifeng Zhao, and Xianhai Chen. 2021. Measuring decentralization in bitcoin and ethereum using multiple metrics and granularities. In 2021 IEEE 37th International Conference on Data Engineering Workshops (ICDEW). IEEE, 80–87.

- manifoldx (2022) manifoldx. 2022. Postmortem of incident on 2022-10-15. https://hackmd.io/@manifoldx/2022-10-15. Accessed on February 29, 2024.

- Mempool.guru (2023) Mempool.guru 2023. Mempool.guru. https://mempool.guru/. Accessed on February 29, 2024.

- Messias et al. (2021) Johnnatan Messias, Mohamed Alzayat, Balakrishnan Chandrasekaran, Krishna P Gummadi, Patrick Loiseau, and Alan Mislove. 2021. Selfish & opaque transaction ordering in the Bitcoin blockchain: the case for chain neutrality. In Proceedings of the 21st ACM Internet Measurement Conference. 320–335.

- Messias et al. (2023) Johnnatan Messias, Vabuk Pahari, Balakrishnan Chandrasekaran, Krishna P Gummadi, and Patrick Loiseau. 2023. Dissecting Bitcoin and Ethereum Transactions: On the Lack of Transaction Contention and Prioritization Transparency in Blockchains. In Financial Cryptography and Data Security: 27th International Conference, FC 2023. Springer.

- metachris (2022) metachris. 2022. Post-mortem for a relay vulnerability leading to proposers falling back to local block production (Nov. 10, 2022). https://collective.flashbots.net/t/post-mortem-for-a-relay-vulnerability-leading-to-proposers-falling-back-to-local-block-production-nov-10-2022/727.

- Monnot (2022) Barnabé Monnot. 2022. Unbundling PBS: Towards protocol-enforced proposer commitments (PEPC). https://ethresear.ch/t/unbundling-pbs-towards-protocol-enforced-proposer-commitments-pepc/13879.

- of Foreign Assets Control (2022) Office of Foreign Assets Control. 2022. Sanctions List. https://www.treasury.gov/ofac/downloads/sanctions/1.0/sdn_advanced.xml. Accessed on February 29, 2024.

- OFAC (2023a) OFAC 2023a. Burma-related Designations; North Korea Designations; Cyber-related Designation; Cyber-related Designation Removal; Publication of Cyber-related Frequently Asked Questions. https://ofac.treasury.gov/recent-actions/20221108. Accessed on February 29, 2024.

- OFAC (2023b) OFAC 2023b. Russia-related Designations; Counter Narcotics Designation Update. https://ofac.treasury.gov/recent-actions/20230201. Accessed on February 29, 2024.

- Pappalardo et al. (2018) Giuseppe Pappalardo, Tiziana Di Matteo, Guido Caldarelli, and Tomaso Aste. 2018. Blockchain inefficiency in the bitcoin peers network. EPJ Data Science 7, 1 (2018), 1–13.

- Piet et al. (2022) Julien Piet, Jaiden Fairoze, and Nicholas Weaver. 2022. Extracting godl [sic] from the salt mines: Ethereum miners extracting value. arXiv preprint arXiv:2203.15930 (2022).

- Qin et al. (2022) Kaihua Qin, Liyi Zhou, and Arthur Gervais. 2022. Quantifying blockchain extractable value: How dark is the forest?. In 2022 IEEE Symposium on Security and Privacy (SP). IEEE, 198–214.

- Rhoades (1993) Stephen A Rhoades. 1993. The herfindahl-hirschman index. Fed. Res. Bull. 79 (1993), 188.

- Sanctions Compliance Guidance for the Virtual Currency Industry (2021) Sanctions Compliance Guidance for the Virtual Currency Industry 2021. Sanctions Compliance Guidance for the Virtual Currency Industry. https://ofac.treasury.gov/media/913571/download?inline Accessed on February 29, 2024.

- Torres et al. (2021) Christof Ferreira Torres, Ramiro Camino, et al. 2021. Frontrunner jones and the raiders of the dark forest: An empirical study of frontrunning on the ethereum blockchain. In 30th USENIX Security Symposium (USENIX Security 21). 1343–1359.

- Wahrstätter et al. (2023a) Anton Wahrstätter, Jens Ernstberger, Aviv Yaish, Liyi Zhou, Kaihua Qin, Taro Tsuchiya, Sebastian Steinhorst, Davor Svetinovic, Nicolas Christin, Mikolaj Barczentewicz, et al. 2023a. Blockchain Censorship. arXiv preprint arXiv:2305.18545 (2023).

- Wahrstätter et al. (2023b) Anton Wahrstätter, Liyi Zhou, Kaihua Qin, Davor Svetinovic, and Arthur Gervais. 2023b. Time to Bribe: Measuring Block Construction Market. arXiv preprint arXiv:2305.16468 (2023).

- Wang et al. (2022) Ye Wang, Yan Chen, Haotian Wu, Liyi Zhou, Shuiguang Deng, and Roger Wattenhofer. 2022. Cyclic arbitrage in decentralized exchanges. In Companion Proceedings of the Web Conference 2022. 12–19.

- Weintraub et al. (2022) Ben Weintraub, Christof Ferreira Torres, Cristina Nita-Rotaru, and Radu State. 2022. A flash (bot) in the pan: measuring maximal extractable value in private pools. In Proceedings of the 22nd ACM Internet Measurement Conference. 458–471.

- Wood (2014) Gavin Wood. 2014. Ethereum: A secure decentralised generalised transaction ledger. (2014).

- Yang et al. (2022) Sen Yang, Fan Zhang, Ken Huang, Xi Chen, Youwei Yang, and Feng Zhu. 2022. SoK: MEV Countermeasures: Theory and Practice. arXiv preprint arXiv:2212.05111 (2022).

- Zeromev (2023) Zeromev 2023. Zeromev API. https://info.zeromev.org/api. Accessed on February 29, 2024.

10. Ethics

Our datasets deal exclusively with publicly available data (i.e., Ethereum blockchain data), MEV and relay data that can be queried by any entity, and mempool data that is logged from the public P2P network (which we use only to mark transactions as private or public). Additionally, all Ethereum addresses presented in this paper are from large entities that purposefully make their addresses publicly known. As such, this paper does not raise any ethical concerns.

11. Builder Address and Public Key

Name Address Public Key beaverbuild 0x95222290dd7278aa3ddd389cc1e1d165cc4bafe5 0x96a59d355b1f65e270b29981dd113625732539e955a1beeecbc471dd0196c4804574ff871d47ed34ff6d921061e9fc27 0xb5d883565500910f3f10f0a2e3a031139d972117a3b67da191ff93ba00ba26502d9b65385b5bca5e7c587273e40f2319 0x8dde59a0d40b9a77b901fc40bee1116acf643b2b60656ace951a5073fe317f57a086acf1eac7502ea32edcca1a900521 0xaec4ec48c2ec03c418c599622980184e926f0de3c9ceab15fc059d617fa0eafe7a0c62126a4657faf596a1b211eec347 bloXroute (M) 0xf2f5c73fa04406b1995e397b55c24ab1f3ea726c 0x94aa4ee318f39b56547a253700917982f4b737a49fc3f99ce08fa715e488e673d88a60f7d2cf9145a05127f17dcb7c67 0x976e63c505050e25b70b39238990c78ddf0948685eb8c5687d17ba5089541f37dd3c45999f2db449eac298b1d4856013 0x8b8edce58fafe098763e4fabdeb318d347f9238845f22c507e813186ea7d44adecd3028f9288048f9ad3bc7c7c735fba 0xaa1488eae4b06a1fff840a2b6db167afc520758dc2c8af0dfb57037954df3431b747e2f900fe8805f05d635e9a29717b bloXroute (R) 0x199d5ed7f45f4ee35960cf22eade2076e95b253f 0x80c7311597316f871363f8395b6a8d056071d90d8eb27defd14759e8522786061b13728623452740ba05055f5ba9d3d5 0xb9b50821ec5f01bb19ec75e0f22264fa9369436544b65c7cf653109dd26ef1f65c4fcaf1b1bcd2a7278afc34455d3da6 0x965a05a1ba338f4bbbb97407d70659f4cea2146d83ac5da6c2f3de824713c927dcba706f35322d65764912e7756103e2 bloXroute (E) 0xf573d99385c05c23b24ed33de616ad16a43a0919 0xb086acdd8da6a11c973b4b26d8c955addbae4506c78defbeb5d4e00c1266b802ff86ec7457c4c3c7c573fa1e64f7e9e0 0x95701d3f0c49d7501b7494a7a4a08ce66aa9cc1f139dbd3eec409b9893ea213e01681e6b76f031122c6663b7d72a331b 0x82801ab0556f7df1fb9bb3a61ca84beea8285a8dc3c455a7ea16a8b2993fe06058e0e7d275b28ea5d9f2ae995aa72605 blocknative 0xbaf6dc2e647aeb6f510f9e318856a1bcd66c5e19 0x8000008a03ebae7d8ab2f66659bd719a698b2e74097d1e423df85e0d58571140527c15052a36c19878018aaebe8a6fea 0x9000009807ed12c1f08bf4e81c6da3ba8e3fc3d953898ce0102433094e5f22f21102ec057841fcb81978ed1ea0fa8246 0xa66f3abc04df65c16eb32151f2a92cb7921efdba4c25ab61b969a2af24b61508783ceb48175ef252ec9f82c6cdf8d8fd 0xa00000a975dffbd1ef61953ac6c90b52b70eb0188eb9d030774346c9248f81e875f7e8bc56c4bbbda297a9543cfa051d builder0x69 0x690b9a9e9aa1c9db991c7721a92d351db4fac990 0x8bc8d110f8b5207e7edc407e8fa033937ddfe8d2c6f18c12a6171400eb6e04d49238ba2b0a95e633d15558e6a706fbe4 0xb194b2b8ec91a71c18f8483825234679299d146495a08db3bf3fb955e1d85a5fca77e88de93a74f4e32320fc922d3027 0xa971c4ee4ac5d47e0fb9e16be05981bfe51458f14c06b7a020304099c23d2d9952d4254cc50f291c385d15e7cae0cf9d 0xa4fb63c2ceeee73d1f1711fadf1c5357ac98cecb999d053be613f469a48f7416999a4da35dd60a7824478661399e6772 0xb8fceec09779ff758918a849bfe8ab43cea79f6a98320af0af5b030f6a7850fcc5883cb965d02efb10eed1ffa987e899 Builder 1 0x473780deaf4a2ac070bbba936b0cdefe7f267dfc 0xa1daf0ab37a9a204bc5925717f78a795fa2812f8fba8bda10b1b27c554bd7dedd46775106facd72be748eea336f514e9 0x89783236c449f037b4ad7bae18cea35014187ec06e2daa016128e736739debeafc5fe8662a0613bc4ca528af5be83b3c Builder 2 0xbd3afb0bb76683ecb4225f9dbc91f998713c3b01 0x82ba7cadcdfc1b156ba2c48c1c627428ba917858e62c3a97d8f919510da23d0f11cf5db53cb92a5faf5de7d31bf38632 Builder 3 0xafc9274fe595e8cff421ab9e73b031f0dff707ea1852e2233ff070ef18e3876e25c44a9831c4b5f802653d4678ccc31f Builder 4 0x3b7faec3181114a99c243608bc822c5436441fff 0xa1f10d66aa4b73c5d9a6cc38a098b2c6ce031a6750ea2da01918ba3ac57c2ce1e39a0da622bd8ccd7c9930861f949fa2 Builder 5 0xb646d87963da1fb9d192ddba775f24f33e857128 0x8bcd1148e83d0a844d2d42f90df0837dbe407055367b3bfcf04227e47ea65a0164fc13a66584aae286f8f7322dc69501 Builder 6 0xa25f5d5bd4f1956971bbd6e5a19e59c9b1422ca253587bbbb644645bd2067cc08fb854a231061f8c91f110254664e943 Eden 0xaab27b150451726ec7738aa1d0a94505c8729bd1 0x8e39849ceabc8710de49b2ca7053813de18b1c12d9ee22149dac4b90b634dd7e6d1e7d3c2b4df806ce32c6228eb70a8b 0xa5eec32c40cc3737d643c24982c7f097354150aac1612d4089e2e8af44dbeefaec08a11c76bd57e7d58697ad8b2bbef5 0x91970c2db7c12510acb2e9c45844f7de602f83a7f31064f7ca04a807b607d7aebfc0abda73c036a92e5c3e56ebca04b7 0xa412007971217a42ca2ced9a90e7ca0ddfc922a1482ee6adf812c4a307e5fb7d6e668a7c86e53663ddd53c689aa3d350 eth-builder 0xfeebabe6b0418ec13b30aadf129f5dcdd4f70cea 0x8eb772d96a747ba63af7acdf92dc775a859f76a77e4c6ed124dca6360e74e4e798a75a925eb8fd0dde866317fff18ad0 0x8ea1393f49d894ae22ec86e38d9aeb64b8336dac947e69cb8468acf510d010ce0b51b21ac3e1244bdb91c52e020ea525 Flashbots 0xb64a30399f7F6b0C154c2E7Af0a3ec7B0A5b131a 0xdafea492d9c6733ae3d56b7ed1adb60692c98bc5 0x81babeec8c9f2bb9c329fd8a3b176032fe0ab5f3b92a3f44d4575a231c7bd9c31d10b6328ef68ed1e8c02a3dbc8e80f9 0x81beef03aafd3dd33ffd7deb337407142c80fea2690e5b3190cfc01bde5753f28982a7857c96172a75a234cb7bcb994f 0xa1dead01e65f0a0eee7b5170223f20c8f0cbf122eac3324d61afbdb33a8885ff8cab2ef514ac2c7698ae0d6289ef27fc Manta-builer 0x5f927395213ee6b95de97bddcb1b2b1c0f16844f 0xa0d0dbdf7b5eda08c921dee5da7c78c34c9685db3e39e81eb91da94af29eaa50f1468813c86503bf41b4b51bf772800e 0xb1b734b8dd42b4744dc98ea330c3d9da64b7afc050afed96875593c73937d530a773e35ddc4b480f9d2e1d5ba452a469 0xb5a688d26d7858b38c44f44568d68fb94f112fc834cd225d32dc52f0277c2007babc861f6f157a6fc6c1dc25bf409046 rsync-builder 0x1f9090aae28b8a3dceadf281b0f12828e676c326 0x978a35c39c41aadbe35ea29712bccffb117cc6ebcad4d86ea463d712af1dc80131d0c650dc29ba29ef27c881f43bd587 0x83d3495a2951065cf19c4d282afca0a635a39f6504bd76282ed0138fe28680ec60fa3fd149e6d27a94a7d90e7b1fb640 0x945fc51bf63613257792926c9155d7ae32db73155dc13bdfe61cd476f1fd2297b66601e8721b723cef11e4e6682e9d87

In Table 5, we provide a map from the builder name to their Ethereum fee recipient address and public key for the biggest 17 builders in terms of the number of blocks built. Notably, we do not have a fee recipient address for Builder 3 and Builder 6 as these builders always note down the proposer address as the fee recipient. Thus, we find no trace of these builders on the Ethereum blockchain.

12. Proposer-Builder Profit Shares

In Figure 19, we explore the daily profit share between builders and proposers. We see that often the builders who subsidize blocks, i.e., have negative block profit, skew the daily average to negative. This behavior was initially prominent, then largely went away until mid-February when we saw an abnormal spike in negative builder profit. In investigating this further, we find that this negative average is almost entirely due to a single builder (beaverbuild), who took a 1.7K ETH loss this month. Though we cannot be certain of beaverbuild’s behavior, we hypothesize that they developed another strategy to extract profit outside of the rewards we measure, and paid the proposers the competitive market price to build the blocks (the negative amount we see).

13. MEV Transaction Types

In the following, we provide a more in-depth analysis concerning the number of various types of MEV transactions in PBS and non-PBS blocks. The most common type of MEV transaction we observe is sandwich attacks. In total, we observed 1,329,368 sandwich attacks during our data collection period. Note that each sandwich attack consists out of two transactions — the front-running and the back-running transaction. We plot the daily average number of sandwich attacks in PBS and non-PBS blocks. There are almost no sandwich attacks in non-PBS blocks, while there is on average more than one sandwich attack in PBS blocks.

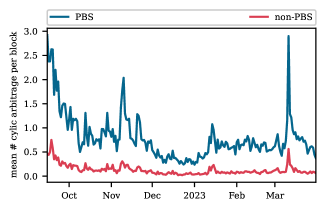

We identify 871,560 cyclic arbitrage transactions. As we show in Figure 21, the vast majority of these are in PBS blocks. However, in comparison to sandwich attacks, the difference is less startling. While there are 0.72 cyclic arbitrage transactions in PBS blocks on average, there are 0.20 in non-PBS blocks. The difference appears biggest on days with total high numbers of cyclic arbitrage transactions.

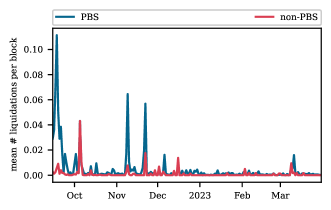

The by far rarest type of MEV transaction we track is liquidations. In total, we identified 4,173 liquidations. Thus, the average number of liquidations per block is low in both PBS and non-PBS blocks. Further, the difference between PBS and non-PBS blocks is the smallest. While there are 0.003 liquidations per non-PBS block on average, there are 0.02 liquidations per PBS block on average. We believe that the smaller difference might be related to the time-sensitive nature of liquidations. A position of a lending protocol becomes available for liquidation once the price oracle updates. These updates can take place in PBS and non-PBS blocks.