Proof.

On the Instability of Fractional Reserve Banking111This paper is a revised version of Chapter 2 of my PhD dissertation at the University of Missouri. I am deeply indebted to my advisor, Chao Gu, for her guidance at all stages of this research project. I am grateful to my committee members, Joseph Haslag, Aaron Hedlund, and Xuemin (Sterling) Yan for helpful comments. I also thank Costas Azariadis, Guido Menzio, Christian Wipf and seminar participants at the 2020 MVEA Conference, 2021 EGSC, and 2021 MEA Annual Meeting for useful feedback and discussion. All remaining errors are mine.

Abstract

This paper develops a dynamic monetary model to study the (in)stability of the fractional reserve banking system. The model shows that the fractional reserve banking system can endanger stability in that equilibrium is more prone to exhibit endogenous cyclic, chaotic, and stochastic dynamics under lower reserve requirements, although it can increase consumption in the steady-state. Introducing endogenous unsecured credit to the baseline model does not change the main results. This paper also provides empirical evidence that is consistent with the prediction of the model. The calibrated exercise suggests that this channel could be another source of economic fluctuations.

JEL Classification Codes: E42, E51, G21

Keywords: Money, Banking, Instability, Volatility

Motivated partly by a desire to avoid such [excessive] price-level fluctuations and possible Wicksellian price-level indeterminacy, quantity theorists have advocated legal restrictions on private intermediation. … Thus, for example, Friedman (1959, p. 21) … has advocated 100 percent reserves against bank liabilities called demand deposit. Sargent and Wallace (1982)

1 Introduction

There have been claims that fractional reserve banking is an important cause of boom-bust cycles, based on the notion that banks create excess credit under fractional reserve banking. (e.g., Fisher, 1935; Von Mises, 1953; Minsky, 1957; Minsky, 1970). For instance, Fisher (1935) views fractional reserve banking as one of several important factors in explaining economic fluctuations. Others believe that this is a primary cause of boom-bust cycles. According to Von Mises (1953), the overexpansion of bank credit as a result of fractional reserve banking is the root cause of business cycles. Minsky (1970) claims that economic booms and structural characteristics of the financial system, such as fractional reserve banking, can result in an economic collapse even when fundamentals remain unchanged.

This idea leads to policy debates on fractional reserve banking. Earlier examples include Peel’s Banking Act of 1844 and the Chicago plan of banking reform with a 100% reserve requirement proposed by Irving Fisher, Paul Douglas, and others in 1939. Later, Friedman (1959) supported this banking reform, whereas Becker (1956) took the opposite position of supporting free banking with 0% reserve requirement.333Sargent (2011) provides a novel review of the historical debates between narrow banking and free banking as tensions between stability versus efficiency. Recently in 2018, Switzerland had a referendum of 100% reserve banking, which was rejected by 75.72% of the voters. The referendum aimed at making money safe from crisis by constructing full-reserve banking.444The official title of the referendum was the Swiss federal popular initiative “for crisis-safe money: money creation by the National Bank only! (Sovereign Money Initiative)” and also titled as “debt-free money.” Whereas the debate on whether a fractional reserve banking system is inherently unstable has been an important policy discussion since a long time ago, the debate has never stopped.

This paper examines the instability of fractional banking by answering the following questions: (i) Can fractional reserve banking be inherently volatile even if we shut down the stochastic component of the economy? (ii) If so, under what condition can fractional reserve banking generate endogenous cycles without the presence of exogenous shocks and changes in fundamentals? To assess the claim that fractional reserve banking causes business cycles, this paper constructs a model of money and banking that captures the role of fractional reserve banking.

In the model, each agent faces an idiosyncratic liquidity shock. Banks accept deposits and extend loans to provide risk-sharing among the depositors whereas the bank’s lending is constrained by the reserve requirement. The real balance of money is determined by two factors: storage value and liquidity premium. The storage value is increasing in the future value of money. However, the liquidity premium, the marginal value of its liquidity function, is decreasing if the money becomes more abundant. When the liquidity premium dominates the storage value, the economy can exhibit endogenous fluctuations. Fractional reserve banking amplifies the liquidity premium because it allows the bank to create inside money through lending. Due to this amplified liquidity premium, the fractional reserve banking system is more prone to endogenous cycles.

In the baseline model, lowering the reserve requirement increases welfare in the steady state. However, lowering the reserve requirements can induce two-period cycles as well as three-period cycles, which implies the existence of periodic cycles of all order and chaotic dynamics. This also implies it can induce sunspot cycles. This result holds in the extended model with unsecured credit. The model also can deliver a self-fulfilling bubble burst. It is worth noting that the full reserve requirement does not necessarily exclude the possibility of endogenous cycles. However, the economy will be more susceptible to cycles with lower reserve requirement.555Gu et al. (2019a) show that introducing banks to the economy could induce instability in various settings which is in line with this result.

This paper departs from previous works in two ways. First, in contrast to the previous works on banking instability, which mostly focus on bank runs following the seminal model by Diamond and Dybvig (1983), this paper focuses on the volatility of real balances of money. It is another important focal point of banking instability because recurring boom-bust cycles associated with banking are probably be more prevalent than bank runs. Second, the approach here differs from a traditional approach to economic fluctuations with financial frictions. To understand economic fluctuations, there are two major points of view. The first one is that economic fluctuations are driven by exogenous shocks disturbing the dynamic system, and the effects of exogenous shocks shrink over time as the system goes back to its balanced path or steady-state. The second one is that they instead reflect an endogenous mechanism that produces boom-bust cycles. While there has been a lot of work on the role of financial friction in the business cycles including Kiyotaki and Moore (1997), Bernanke et al. (1999), and Gertler and Karadi (2011), most of them focused on the first approach, in which all economic fluctuations are caused by exogenous shocks and the financial sectors only serve as an amplifier. This paper, however, takes the second approach and focuses on whether the endogenous cycles arise in the absence of the stochastic components of the economy.

To evaluate the main prediction from the theory that fractional reserve banking induces excess volatility, I test the relationship between the required reserves ratio and the volatilty in real balance using cointegrating regression. A significant negative relationship between the two variables are found, and the results are robust to different measures of inflation and different frequency of time series. Both theoretical and empirical evidence indicate a link between the reserve requirement and the (in)stability.

Related Literature This paper builds on Berentsen et al. (2007), who introduce financial intermediaries with enforcement technology to Lagos and Wright (2005) framework. The approach to introduce unsecured credit to the monetary economy is related to Lotz and Zhang (2016) and Gu et al. (2016) which are based on the earlier work by Kehoe and Levine (1993).

This paper is related to the large literature on fractional reserve banking. Freeman and Huffman (1991) and Freeman and Kydland (2000) develop general equilibrium models that explicitly capture the role of fractional reserve banking. Using those models, they explain the observed relationships between key macroeconomic variables over business cycles. Chari and Phelan (2014) study an economy where private agents have incentives to establish fractional reserve banking as an alternative payment system. This alternative system is inherently fragile because it is susceptible to socially costly bank runs. They study the conditions under which the social benefits of fractional reserve banking can exceed its social costs which crucially depend on communication technologies. For recent work, Wipf (2020) studies the welfare implications of fractional reserve banking in a New Monetarist economy with imperfect competition and identifies the conditions under which fractional reserve banking can be welfare-improving compared to narrow banking. Andolfatto et al. (2020) integrate Diamond (1997) into Lagos and Wright (2005) to provide a model in which fractional reserve banking emerges endogenously and a central bank can prevent bank panic as a lender of last resort. Whereas many previous work on instability focuses on bank runs or societal value at the steady state, this paper studies a different type of instability in the sense that fractional reserve banking induces endogenous monetary cycles.

This paper is also related to the large literature on endogenous fluctuations, chaotic dynamics, and indeterminacy that have been surveyed by Brock (1988), Baumol and Benhabib (1989), Boldrin and Woodford (1990), Scheinkman and Woodford (1994) and Benhabib and Farmer (1999). For a model of bilateral trade, Gu et al. (2013) show that credit markets can be susceptible to endogenous fluctuations due to limited commitment. Using a continuous-time New Monetarist economy, Rocheteau and Wang (2023) show that asset liquidity can be a source of price volatility when assets have a non-positive intrinsic value. Altermatt et al. (2023) study economies with multiple liquid assets and show that liquidity considerations could imply endogenous fluctuations as self-fulfilling prophecies. Gu et al. (2019a) show that introducing financial intermediaries to an economy can engender instability in four distinct setups that capture various functions of banking. The model in this paper is closely related to Gu et al. (2019a), whereas the model here is extended to incorporate fractional reserve banking.

The rest of the paper is organized as follows. Section 2 constructs the baseline search-theoretic monetary model. Section 3 provides main results. Section 4 introduces unsecured credit. Section 5 discusses the empirical evaluation of the model. Section 6 calibrates the model to quantify the theory. Section 7 concludes.

2 Model

The model is based on Lagos and Wright (2005) with a financial intermediary as in Berentsen et al. (2007). Time is discrete and infinite. In each period, three markets convene sequentially. First, a centralized financial market (FM), followed by a decentralized goods market (DM), and finally a centralized goods market (CM). The FM and CM are frictionless. The DM is subject to search frictions, anonymity, and limited commitment. Therefore, a medium of exchange is needed to execute trades.

There is a continuum of agents who produce and consume perishable goods. At the beginning of the FM, a preference shock is realized: With probability , an agent will be a buyer in the following DM and with probability , she will be a seller. The buyers and the sellers randomly meet and trade bilaterally in the DM. Agents discount their utility each period by . Within-period utility is represented by

where is the CM consumption, is the CM disutility from production, and is the DM consumption. As standard , , , , , , and . The CM consumption good is produced one-for-one with , implying the real wage is 1. The efficient consumption in CM and DM is and that solve and , respectively.

There is a representative bank who accepts deposits and lends loans in the FM. In the FM, the agent can borrow money from the bank for a promise to repay money in the subsequent CM at nominal lending rate . The agent can also deposit money to the bank and receive money in the subsequent CM at nominal deposit rate . The banking market is perfectly competitive. The bank can enforce the repayment of loans at no cost. Last, there is a central bank that controls the money supply . Let be the growth rate of the money stock. Changes in money supply are accomplished by lump-sum transfer if and by lump-sum tax if .

2.1 Agent’s Problem

Let , , and denote the agent’s value function in the CM, FM, and DM, respectively, in period . There are two payment instruments for the DM transaction: fiat money (outside money) and loans from the bank (inside money). I will allow the agents to use unsecured credit as a means of payment in the next section. An agent entering the CM with nominal balance , deposit , and loan , solves the following problem:

| (1) |

where is the lump-sum transfer (or tax if it is negative), is the deposit interest rate, is the loan interest rate, is the price of money in terms of the CM goods, and is the money balance carried to the FM where banks take deposits and makes loans. The first-order conditions (FOCs) result in and

| (2) |

where is the marginal value of an additional unit of money taken into the FM of period . The envelope conditions are

implying is linear in , , and .

The value function of an agent at the beginning of FM is

| (3) |

where is the value function of type agent in the FM. Agents choose their deposit balance and loan based on the realization of their types in the following DM. The value function can be written as

| (4) |

where is the value function of type agent in the DM. The FOCs are

| (5) | ||||

| (6) |

where is the Lagrange multiplier for .

The terms of trade in the DM are determined by an abstract mechanism that is studied in Gu and Wright (2016). The buyer must pay to the seller to get where is some payment function satisfying and . As shown in Gu and Wright (2016), if the trading protocol satisfies four common axioms, then the terms of trade can be written in the following form.

| (7) |

where is the payment required to get efficient consumption , and is the total liquidity, , held by the buyer. Many standard mechanisms, such as Kalai and generalized Nash bargaining, are consistent with this specification.

With probability , a buyer meets a seller in the DM while a seller meets a buyer with probability . Since the CM value function is linear, the DM value function for the buyer can be written as

| (8) |

where . Assuming interior solution, differentiating yields

where if and if . Combining the buyer’s FOCs in the FM and the derivatives of yields

| (9) | ||||

| (10) |

A seller’s DM value function is

| (11) |

Differentiating yields

Similar to the buyer’s case, combining the seller’s FOCs in the FM and the first-order derivatives of yields

| (12) | ||||

| (13) |

One can show that buyers do not deposit and sellers always deposit whereas buyers always borrow loans but sellers do not. This is because the buyer needs liquidity to trade for in the DM but the seller does not. Formally, for , we have and because

| (14) | ||||

| (15) |

implying , , , , and as long as .

2.2 Bank’s Problem

A representative bank accepts deposits and makes loans . The depositors are paid at the nominal interest rate by the bank, and the borrowers need to repay their borrowing with a nominal interest rate . The central bank sets reserve requirement . The representative bank solves the following profit maximization problem.

| (22) |

The FOCs for the bank’s problem are

| (23) | ||||

| (24) |

where is the Lagrange multiplier with respect to the bank’s lending constraint. For , we have

| (25) |

while implies . Given the bank’s problem and the agent’s problem, we can define an equilibrium as follows:

Definition 1.

Given , an equilibrium consists of sequences of prices , real balances , and allocations satisfying the following:

- •

- •

-

•

A representative bank solves its profit maximization problem: (22)

-

•

Markets clear in every period:

-

1.

Deposit Market:

-

2.

Loan Market:

-

3.

Money Market:

-

1.

-

•

Transversality condition:

The next step is to characterize the equilibrium. With binding bank’s lending constraint, the equilibrium lending satisfies and . Combine equations (10), (21) and (25), and use equilibrium condition to get

| (26) |

where . Then multiplying both sides of (26) by allows us to reduce the equilibrium condition to one difference equation of real balances :

| (27) |

where and is the liquidity premium.666In the stationary equilibrium, is the nominal interest rate. When , because the buyer has sufficient liquidity to buy . In this case, the liquidity is abundant. When , because the buyer does not have enough liquidity to buy . In this case, the liquidity is scarce.

3 Results

This section establishes key results. Before starting a discussion on dynamics, consider stationary equilibria which are defined as fixed points that satisfy . There always exists a non-monetary equilibrium with . A unique solution of monetary stationary equilibrium exists and solves

| (28) |

when where . Nash and Kalai bargaining provide simple examples for . Under the Inada condition , with Kalai, ; whereas with Nash bargaining, .

Since and (see Gu and Wright, 2016), the following result holds:

Proposition 1.

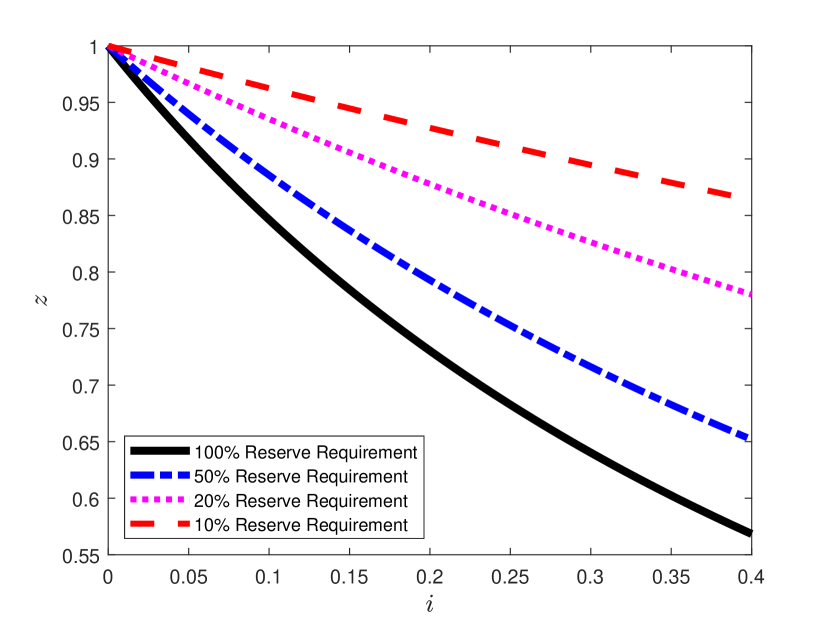

In the stationary equilibrium, lowering or lowering increases .

Proof.

See Appendix A. ∎

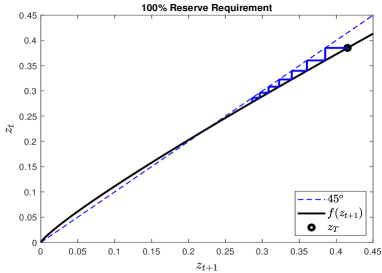

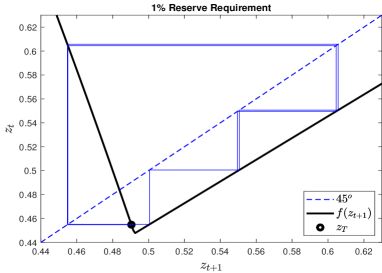

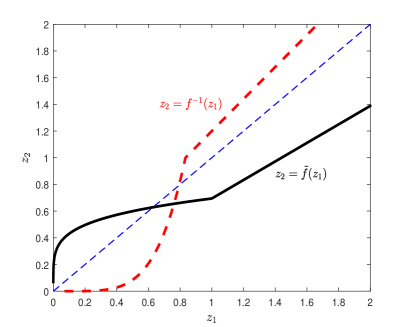

Figure 1(a) plots against . It shows downward-sloping money demand in the stationary equilibrium given the reserve requirement. Lowering the reserve requirement increases because it allows a bank to create more liquidity in the economy which increases as well.

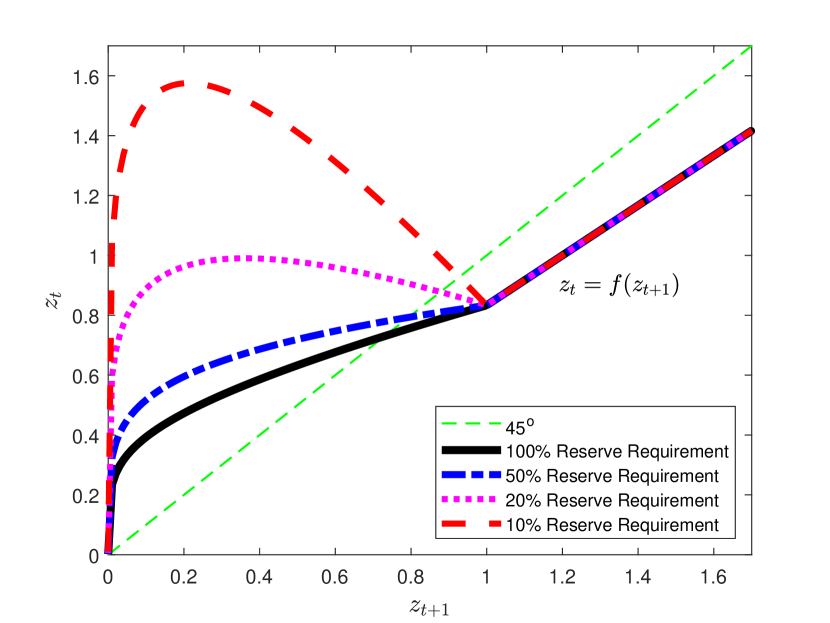

The dynamics of monetary equilibrium are characterized by from equation (27). The first term, on the right-hand side, reflects the store of value, which is monotonically increasing in . The second term , reflecting the liquidity premium, is decreasing in . Because depends on both terms, is nonmonotone in general. Figure 1(b) provides an example. In this example, as the reserve requirement decreases, the equation (27) is more likely to have the backward bending feature. Lowering the reserve requirement amplifies the liquidity premium, as it enables banks to generate more liquidity through lending. This amplification of liquidity enhances the backward-bending feature, potentially leading to endogenous cycles.

The standard treatment for showing the existence of an endogenous cycle is (see Azariadis, 1993). In this case, the economy can exhibit a two-period cycle with which can be either or . However, without further assumptions, we cannot determine the conditions under which this can occur. For illustration, let’s take the derivative of (21) with respect to and evaluate it at . We obtain the following expression:

| (29) |

As is not explicitly defined here, we are unable to establish the conditions under which the standard condition of cycles, , would hold under the general bilateral trading mechanism.

We can show the existence of an endogenous cycle without relying on the standard treatment of . To establish a sufficient condition for an endogenous cycle, consider a two-period cycle with . Since , this cycle satisfies , where solves

It is straightforward to show that because , and solves (28). By checking the condition , we can derive the condition under which the economy exhibits a two-period cycle that satisfies .

Proposition 2 (Two-period Monetary Cycle).

There exists a two-period cycle with if , where

When this type of two-period cycle exists, lowering increases the difference between peak and trough, .

Proof.

See Appendix A. ∎

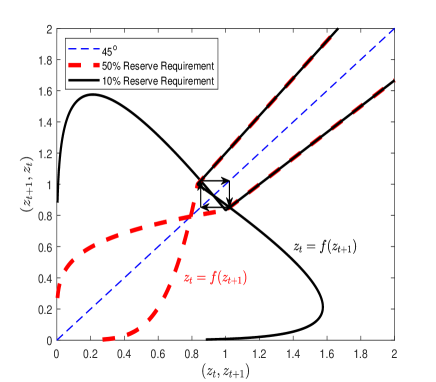

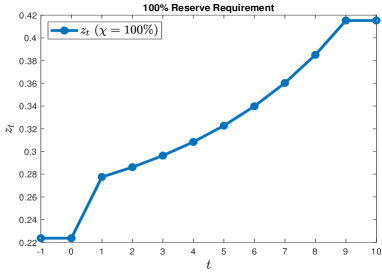

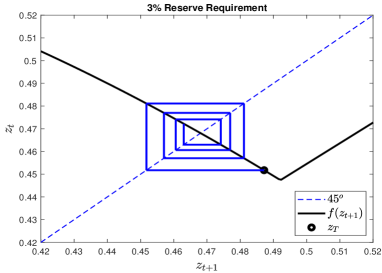

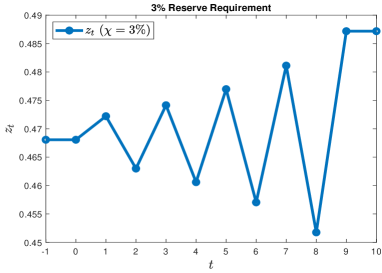

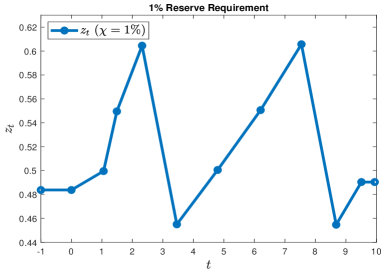

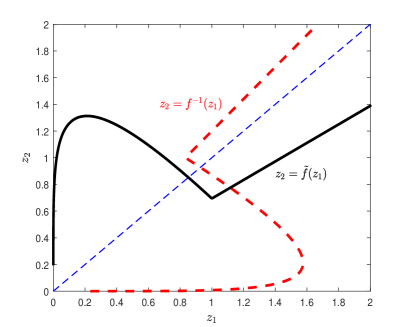

Proposition 2 shows that, under the general trading mechanism, lowering the reserve requirement can induce a two-period cycle and increase the volatility of the real balances. Figure 2 shows an example of this case. By lowering , the liquidity premium dominates the storage value. Consequently, is more likely to exhibit the backward bending feature, which can lead to an endogenous cycle.

Now, let’s introduce some additional assumptions to determine the condition for such that . Consider a special case where , , and the buyer makes a take-it-or-leave-it (TIOLI) offer. In this case, as and , we can rewrite (29) as follows:

| (30) |

where . Solving (30) for yields the following proposition.

Proposition 3.

Assume , , and the buyer makes take-it-or-leave-it offer to the seller. If , where

| (31) |

then .

Proof.

See Appendix A. ∎

Since implies , following the standard textbook method (see Azariadis, 1993), we can show that if , there exists a two-period cycle with . Whereas (31) is written in terms of , this condition can be written in terms of , as follows:

| (32) |

The role of on cycles depends on . By (32), if , lowering either or can induce a cycle. If , is negative when and positive when . In this case, setting higher than eliminates cyclic equilibria. If , is negative for all , implying the cycle does not exist. When , is constant, implying that the has no effect on the cycle in this case.

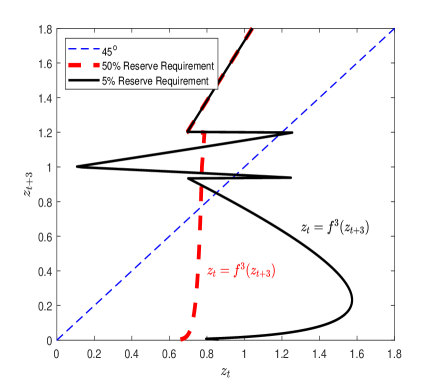

In addition to the conditions for a two-period cycle, the next result provides the condition for a three-period cycle under the general trading mechanism. The existence of three period-cycles implies cycles of all orders as well as chaotic dynamics (see Sharkovskii, 1964 and Li and Yorke, 1975).

Proposition 4 (Three-period Monetary Cycle and Chaos).

A three-period cycle with does not exist. There exists a three-period cycle with if , where

When this type of three-period cycle exists, lowering increases the difference between peak and trough, .

Proof.

See Appendix A. ∎

The following corollary is a direct result from Proposition 4.

Corollary 1 (Binding Liquidity Constraint).

In any n-period cycle, the liquidity constraint binds, , at least one periodic point over the cycle.

Proof.

See Appendix A. ∎

The model can also generate sunspot cycles. Consider a Markov sunspot variable . This sunspot variable is not related to fundamentals but may affect equilibrium. Let and . The sunspot is realized in the FM. Let be the CM value function in state in period , then

The FOC can be written as

| (33) |

Solving the FM problem results in

| (34) |

We substitute (34) into (33) and use the money market clearing condition = to get the Euler equation.

where . Then multiply both sides of the Euler equation by to reduce the equilibrium condition into one difference equation of real balances :

| (35) |

We define a sunspot equilibrium as follows:

Definition 2 (Proper Sunspot Equilibrium).

A proper sunspot equilibrium consists of the sequences of real balances and probabilities , solving (3) for all .

Consider stationary sunspot equilibria with that only depend on the state, not the time. The liquidity constraint is binding in state . By the standard approach (see again Azariadis, 1993 for the textbook treatment), the condition for two-period cycles is also sufficient and necessary for two-state sunspot equilibrium. If or , there exists , , such that the economy has a proper sunspot equilibrium in the neighborhood of .

Proposition 5 (Stationary Sunspot Equilibria).

The stationary sunspot equilibrium exists if either or .

Proof.

See Appendix A. ∎

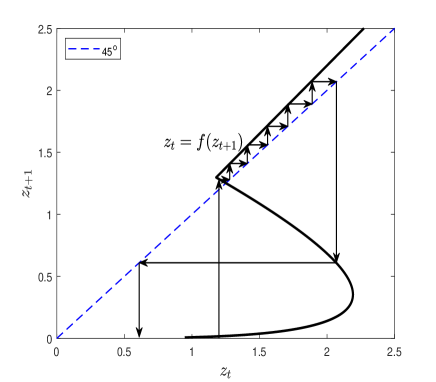

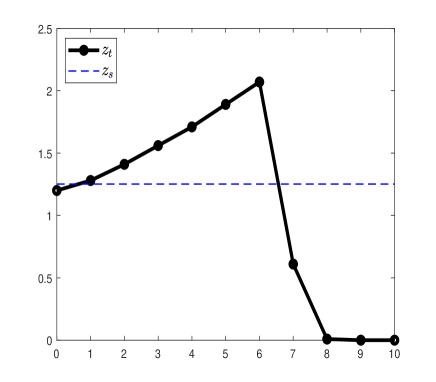

In addition to the deterministic and stochastic cycles, the model also features the equilibria where real balance increases above the steady-state until certain time, , and crashes to zero. Consider a sequence of real balances with (bubble) that crashes to 0 (burst) as , where and . We refer to this equilibrium as a self-fulfilling bubble and burst equilibrium:

Definition 3 (Self-Fulfilling Bubble and Burst Equilibrium).

For initial real balance , a self-fulfilling bubble and burst equilibrium is a sequence of satisfying (27) and , where with .

Figure 4 illustrates an example. In Figure 4, is not monotone, so is a correspondence. When is not monotone, there are multiple equilibrium paths for over some range for . This example starts at , which is lower than , and then increases, surpassing , repeatedly rising until it reaches . Afterward, it crashes and eventually converges to . During the bubble, the return on money is equal to , and liquidity is abundant. However, the real balances cannot continue to increase indefinitely otherwise it would violate the transversality condition. The real balance increases until it reaches a certain point, after which the economy crashes and moves toward a non-monetary equilibrium. The timing of these crashes is indeterminate.

The next step is to examine the conditions under which this type of equilibrium can occur. When , where satisfies , multiple equilibria exist. This implies that solving given yields multiple solutions for . If , the self-fulfilling bubble and burst equilibrium exists. Assuming , , and a buyer makes a TIOLI offer to the seller, Proposition 6 shows that lowering the reserve requirement can induce this type of equilibrium.

Proposition 6 (Existence of Self-Fulfilling Bubble and Burst Equilibria).

Assume , , and the buyer makes take-it-or-leave-it offer to the seller. There exist a self-fulfilling bubble and burst equilibrium, if

Proof.

See Appendix A. ∎

4 Money and Unsecured Credit

Consider an alternative payment instrument in the DM - unsecured credit. The buyer can pay for DM goods using unsecured credit that will be redeemed to the seller in the following CM and she can borrow up to her debt limit, . For simplicity, I assume that the buyer makes a TIOLI offer to the seller in the DM, which means the buyer maximizes her surplus subject to the seller’s participation constraint. The DM cost function is . Suppose the buyer has issued units of unsecured debt in the previous DM (or, if , the seller has extended unsecured loans to the buyer from the previous DM). The CM value function is

| (36) |

which is the same as before except that the agent needs to pay or collect the debt. The agent’s FM problem is identical to the previous section. Then, fraction of agents will deposit , and fraction of agents will borrow loan from the bank. The DM value function is

where . Given , solving equilibrium yields

| (37) |

where .

Next, I am going to endogenize the debt limit. The buyer cannot commit to pay back the debt. If the buyer reneges she is captured with probability . The punishment for a defaulter is permanent exclusion from the DM trade but she can still produce for herself in the CM. The value of autarky is . The incentive condition for voluntary repayment is

One can write the debt limit as . Recall the CM value function. Using the solution of FM, we can rewrite the buyer’s CM value function as

where . Substituting and yields

where and solve (37). Rearranging terms yields

| (38) |

where is the buyer’s trade surplus. The equilibrium can be collapsed into a dynamic system satisfying (37)-(38).

In the stationary equilibrium, (37) becomes

| (39) |

and (38) becomes

| (40) |

where . The stationary equilibrium solves the above two equations, and it falls into one of the three cases: the pure money equilibrium, the pure credit equilibrium, and the money-credit equilibrium. First, if no one can capture the buyer after she reneges, , the unsecured credit is not feasible, . In this case, the equilibrium will be the pure money equilibrium. Second, when solving (40) satisfies then money is not valued, . We have the pure credit equilibrium in this case. Third, if solutions of (39)-(40), are strictly positive then we have the money-credit equilibrium.

The debt limit at the stationary equilibrium, , is a fixed point satisfying where

| (41) |

where solves and . The DM consumption is determined by . Money and credit coexist if and only if , which holds when , where

The DM consumption is decreasing in in the stationary monetary equilibrium.

Consider the dynamics of equilibria where money and credit coexist. I claim the main results from Section 3 - lowering the reserve requirement can induce endogenous cycles - still hold even after unsecured credit is introduced. It is clear that the standard treatment from Azariadis (1993) cannot be used here because now the equilibrium consists of a system of equations. Instead, I apply the approach used in Proposition 2 and 4. For compact notation, let and . The following proposition establishes the conditions for a two-period cycle, a three-period cycle, and chaotic dynamics.

Proposition 7 (Monetary Cycles with Unsecured Credit).

There exists a two-period cycle of money and credit with if , where

There exists a three-period cycle of money and credit with , if , where

Proof.

See Appendix A. ∎

5 Empirical Evaluation: Real Balance Volatility

In the previous sections, the theoretical results show that lowering the required reserve ratio can induce instability. To evaluate the model prediction, I examine whether the required reserve ratio is associated with the cyclical volatility of the real balance of the aggregate money.

Following Jaimovich and Siu (2009) and Carvalho and Gabaix (2013), I measure the cyclical volatility in quarter as the standard deviation of a filtered log real M1 money stock during a 41-quarter (10-year) window centered around quarter . The M1 money stock series are from the H.6 Money Stock Measures published by the Federal Reserve Board and converted to real value using the Consumer Price Index (CPI). Seasonally adjusted series are used to smooth the seasonal fluctuation. I adopt the Hodrick-Prescott (HP) filter with a 1600 smoothing parameter as standard. To construct an annual series, quarterly observations are averaged for each year. The sample period is from 1960:I to 2018:IV so that there are annual series from 1965 to 2013. To check whether the results are sensitive to different measures of the price level, I also use the core CPI, the Personal Consumption Expenditures (PCE), and the core PCE to transform the M1 stock into real value.

To compute the required reserve ratios, I divide the required reserves by the deposit component of M1 instead of using the official legal reserve requirement. The reason for this approach is the following. The legal reserve requirement for demand deposits was 10% from April 2, 1992, to March 25, 2020. However, the Federal Reserve imposed different reserve requirements depending on the size of a bank’s liabilities. For example, from December 29, 2011, to December 26, 2012, the Fed had a reserve requirement exemption for liabilities up to $11.5 million. For liabilities between $11.5 million and $71.0 million, the Fed imposed a 3% reserve requirement. These criteria have changed over time. On December 27, 2012, the Fed increased the exemption threshold to $12.4 million and raised the low reserve tranche from $71.0 million to $79.5 million. During 1992:Q1-2019:Q4, there were 27 changes in these thresholds. Dividing the required reserves by the deposit component of M1 allows us to track these changes as well.

| Price level | CPI | Core CPI | PCE | Core PCE | ||||

|---|---|---|---|---|---|---|---|---|

| Dependent | OLS | CCR | OLS | CCR | OLS | CCR | OLS | CCR |

| variable: | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) |

| ffr | ||||||||

| Constant | ||||||||

| Obs. | 49 | 49 | 49 | 49 | 49 | 49 | 49 | 49 |

| 0.455 | 0.391 | 0.471 | 0.310 | 0.564 | 0.356 | 0.608 | 0.349 | |

| 11.872 | 10.175 | 9.804 | 8.321 | |||||

| 5% CV | ||||||||

| 13.121 | 11.477 | 10.886 | 9.325 | |||||

| 5% CV | ||||||||

Note: For (1), (3), (5) and (7), OLS estimates are reported, and Newey-West standard errors with lag 1 are reported in parentheses. For (2), (4), (6), and (8), first-stage long-run variance estimations for CCR are based on the quadratic spectral kernel and lag 1. The bandwidth selection is based on Newey-West fixed lag, ; denotes the required reserve ratio, ffr denotes federal funds rates and denotes the cyclical volatility of real money balances. ***, **, and * denotes significance at the 1, 5, and 10 percent levels, respectively.

To examine whether there is an association, I regress the required reserve ratio on the cyclical volatility of the money real balances. Column (1) of Table 1 reports its regression estimates with Newey-West standard errors. The estimates show a negative relationship between the cyclical volatility of the real money balance and the required reserve ratio with statistically significant regression coefficients. However, this result can be driven by a spurious regression. Table 2 provides unit root test results for the federal funds rate, the required reserve ratio, and the cyclical volatility of real money balances. Both augmented Dickey-Fuller tests and Phillips-Perron tests fail to reject the null hypotheses of unit roots for these series, whereas they reject the null hypotheses of unit roots at their first differences. In addition to that, the Johansen cointegration test in Column (1), suggests that there is no cointegration relationship between two variables. So it is hard to rule out that Column (1)’s results are driven by a spurious regression.

| Phillips-Perron test | ADF test | |||

|---|---|---|---|---|

| w/ lag 1 | ||||

| ffr | ||||

| (CPI) | ||||

| (Core CPI) | ||||

| (PCE) | ||||

| (Core PCE) | ||||

| (CPI) | ||||

| (Core CPI) | ||||

| (PCE) | ||||

| (Core PCE) | ||||

Note: ffr denotes federal funds rates, denotes required reserve ratio, and denotes cyclical volatility of real money balances. ***, **, and * denotes significance at the 1, 5, and 10 percent levels, respectively.

To overcome this issue, I adopt the cointegrating regression with an additional variable, the federal funds rate. Column (2) of Table 1 provides Johansen cointegration test results for the federal funds rate, the required reserves, and the cyclical volatility of real money balances. The trace test suggests a cointegration relationship among these three variables, which is consistent with the theoretical result: The instability depends on the reserve requirement and the interest rate. With the cointegration relationship, we may not have to worry about a spurious relationship. Column (2) of Table 1 reports the estimates for the cointegrating relationship. Because of the potential bias from long-run variance, I estimate a canonical cointegrating regression (CCR). The estimates suggest a negative association between the required reserves, and the cyclical volatility of money, and the coefficients are statistically significant with a sizeable level.

To check the sensitivity of the results, I redo all the analyses using the core CPI, the Personal Consumption Expenditures (PCE), and the core PCE to transform the M1 money stock into real value. Columns (3), (5), and (7) of Table 1 regress required reserve ratio on the money volatility and report its Newey-West standard errors. They also report the trace test statistics of Johansen cointegration test between these two variables. The results are consistent with the benchmark case in Column (1). Columns (4), (6), and (8) of Table 1 report CCR estimates regressing the required reserve ratio and federal funds rate on the money volatility and the trace test statistics of Johansen cointegration test between these three variables. All the results are consistent with the benchmark case in Column (2).

Appendix B includes more sensitivity analyses: (1) Using quarterly series instead of annual series; (2) Using time series before 2008; (3) Using alternative data of M1 proposed by Lucas and Nicolini (2015) (M1J hereafter); (4) Using another alternative data of M1: M1 adjusted for retail sweeps. All the results are not sensitive with respect to different frequencies, time periods, and alternative data.

6 Calibrated Examples

6.1 Parameters and Targets

In this section, I calibrate the model using U.S. data. I calibrate both the model without unsecured credit and the model with unsecured credit. First, assuming there is no unsecured credit, I calibrate the model without unsecured credit, which will be referred to as Model 1 throughout this section. In addition to Model 1, I also calibrate the model with unsecured credit, referred to as Model 2. For monetary aggregates, I use M1 adjusted for retail sweep accounts as in Aruoba et al. (2011) and Venkateswaran and Wright (2014). Following to Krueger and Perri (2006), revolving consumer credit series are used as unsecured credit.

I set the discount rate to match the real annual interest rate of . Using the average required reserve to deposit ratio for 1980Q1-2008Q4, the benchmark required reserve ratio is set to .777To compute the required reserve ratio, I divide the required reserve ratio, I divide the required reserves by the deposit component of sweep-adjusted M1. The average of this ratio for 1980Q1-2008Q4 is 0.0777 The benchmark value for is set to as the average annualized nominal interest rate is . The matching function in the DM is , where and denotes the measure of buyers and sellers, respectively. This implies and . The fraction of buyer is set to for a normalization. The utility functions for the parameterization are

implying and the DM cost function is given as . Assume the buyer makes a take-it-or-leave-it offer to the seller in the DM trade, implying .

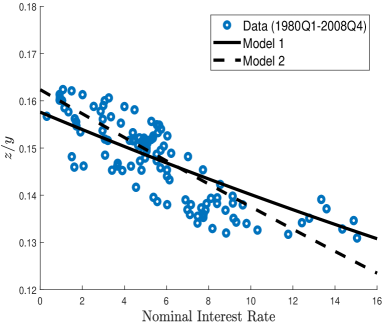

This section focuses on the equilibrium where which requires . To guarantee , we need to have since . Otherwise, the CM consumption is zero, . For normalization, I set . The parameters are set to match the money demand relationship. In the model, the money demand relationship is given by real balances of money as a fraction of output

where is the real output of the economy and elasticity of with respect to

| Data | Model 1 | Model 2 | |

|---|---|---|---|

| No Credit, | With Credit, | ||

| Parameters | |||

| DM utility level, | 0.8488 | 1.0658 | |

| DM utility curvature, | 0.2312 | 0.5436 | |

| Monitoring probability, | - | 0.0547 | |

| Targets | |||

| avg. | 0.1473 | 0.1475 | 0.1482 |

| elasticity of wrt | -0.0661 | -0.0661 | -0.0661 |

| avg. | 0.0466 | - | 0.0464 |

Specifically, the parameter is set to match the average money stock to GDP ratio, which is , and the parameter is set to match the elasticity of with respect to . The target elasticity is estimated using the following regression:

The estimated elasticity is . In Model 2, agents can use unsecured credit in DM trade, and the monitoring probability is set to match the amount of unsecured credit in the economy as a fraction of output, which is . Its model counterpart is . The closed-form solutions of targets from the models can be found in Appendix C. Figure 5 shows the fitted money demand and Table 3 shows the calibrated parameters and the target moments.

6.2 Model Implied Thresholds

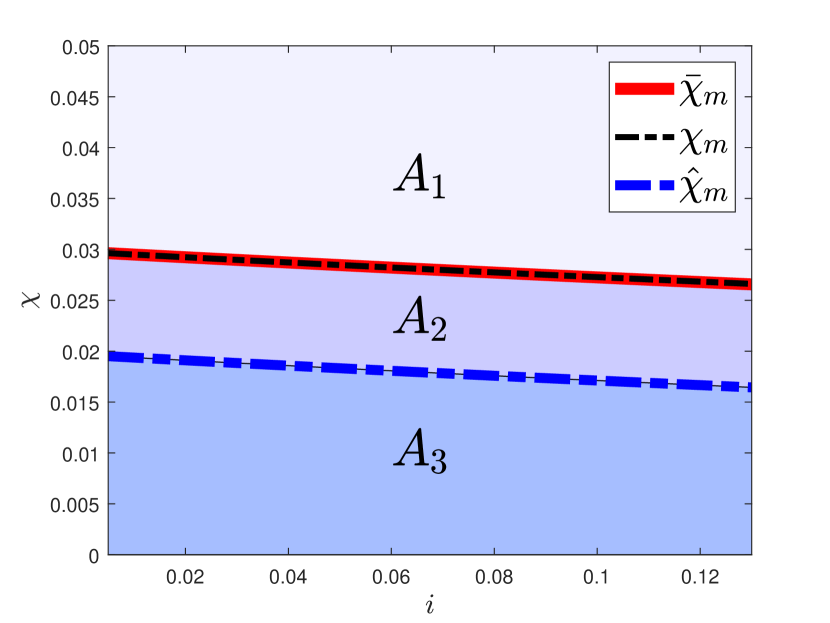

Given the parameterization from the previous section, this section examines whether the conditions for endogenous cycles hold or not. Figure 6(a) displays the thresholds for a two-period cycle, and , and the threshold for a three-period cycle and chaotic dynamics, , under different values of in Model 1. The thresholds decrease as increases. The thresholds for two-period cycles, and , are almost the same and range from 0.0259 to 0.0297. The threshold for a three-period cycle, , varies from 0.0158 to 0.0196. Area denotes the region where , indicating the absence of cycles. Area represents the region where . In area , there are two-period cycles, but higher-order cycles may not exist. Area indicates the region where , implying the presence of higher-order cycles and chaotic dynamics.

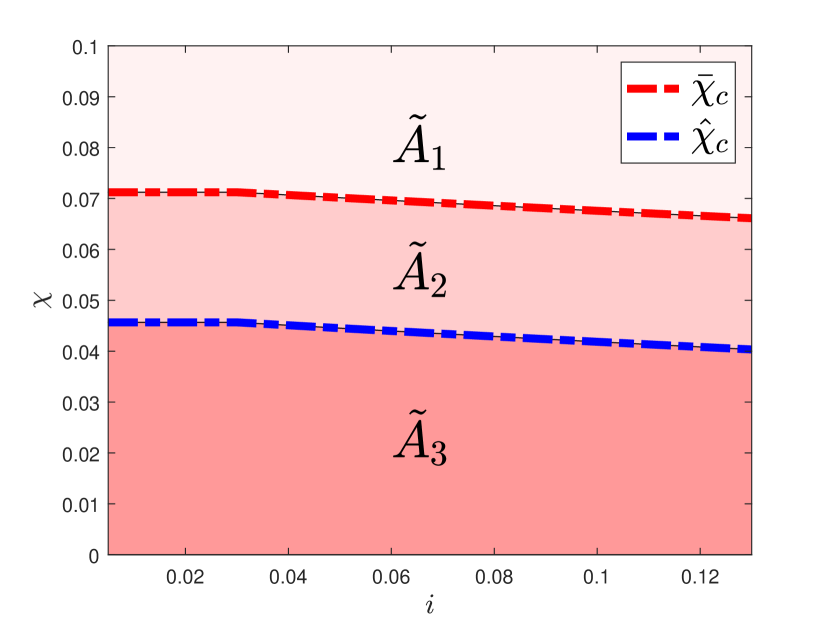

Figure 6(b) presents the thresholds for the two-period cycles, and three-period cycles and chaotic dynamics, in Model 2. The threshold varies from 0.0647 to 0.0712, and the threshold ranges from 0.0389 to 0.0457. The thresholds for cycles in Model 2 are higher than those in Model 1 and decrease as increases. Area , , and denotes the regions where , , and , respectively.

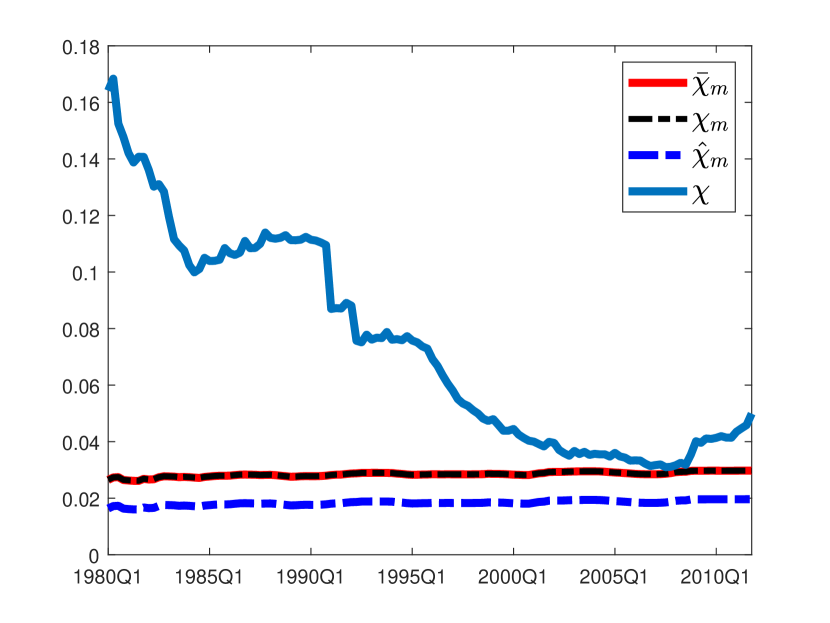

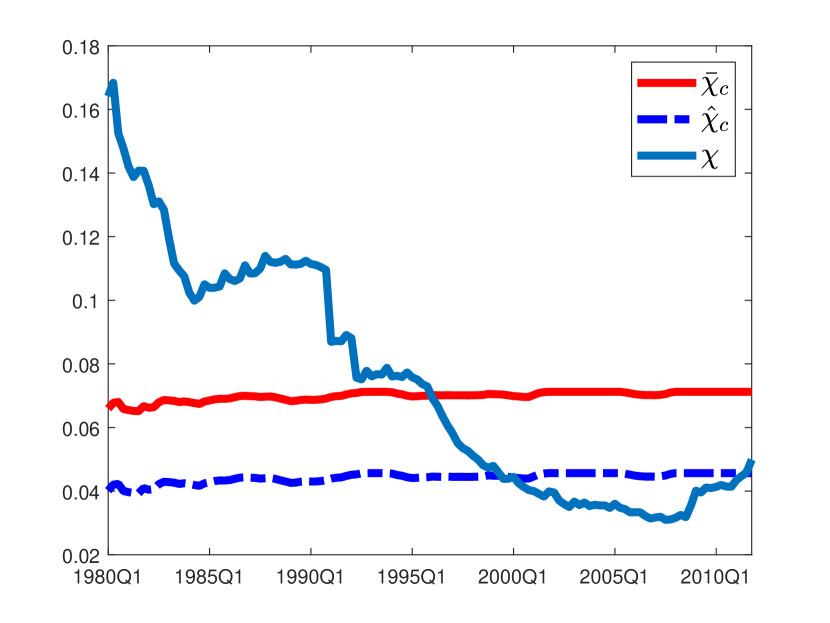

We can compare the thresholds with the actual data.888To compute , I divide the required reserves by deposit component of sweep adjusted M1. Figure 7(a) plots the model-implied thresholds from Model 1 over time. While both of and are higher than , they are very close to after 2000. Figure 7(b) plots the model-implied thresholds from Model 2 over time. Figure 7(b) shows that both of and are lower than after 2000. This says the economy could exhibit endogenous fluctuations and chaotic dynamics. It implies that the economy may have endogenous cycles as well as sunspot cycles due to fractional reserve banking, which is independent of the presence of exogenous shocks and changes in fundamentals.

In both models, the endogenous cycle thresholds are not low enough to be ignored, indicating that this channel of volatility needs to be considered in addition to economic fluctuations induced by exogenous shocks that disrupt the dynamic system.

6.3 News Shocks

This section explores the role of reserve requirements in the dynamics resulting from news about future changes in monetary policy. To analyze the impact of such news, I follow Gu et al. (2019b) who study the effect of news in the economy where liquidity plays a role. Gu et al. (2019b) show that the response to the announcement can be complicated, and it highly depends on parameters. Using calibrated parameters, this section examines how reducing the reserve requirement can complicate the effects of the monetary policy announcement.

Let the central bank change permanently, from to .999The permanent change in implies a permanent change in the rate of monetary expansion, , from to . Suppose news on changes in the monetary policy at is announced at time 0. As in Gu et al. (2019b), I focused on unique transition consistent with stationarity after information shock. Initially, the economy is in its unique stationary equilibrium for a given . At it is announced that will change to at and stay at permanently. Therefore the stationary equilibrium for a given is a fixed terminal condition that pins down the transition by backward induction.

First, consider the dynamics without unsecured credit, i.e., . The permanent change in from to implies a shift of equation (27) from to . Let be a steady state for a given monetary policy, . Then, the transition starts in steady state with and ends with . This can be solved by backward induction, as follows.

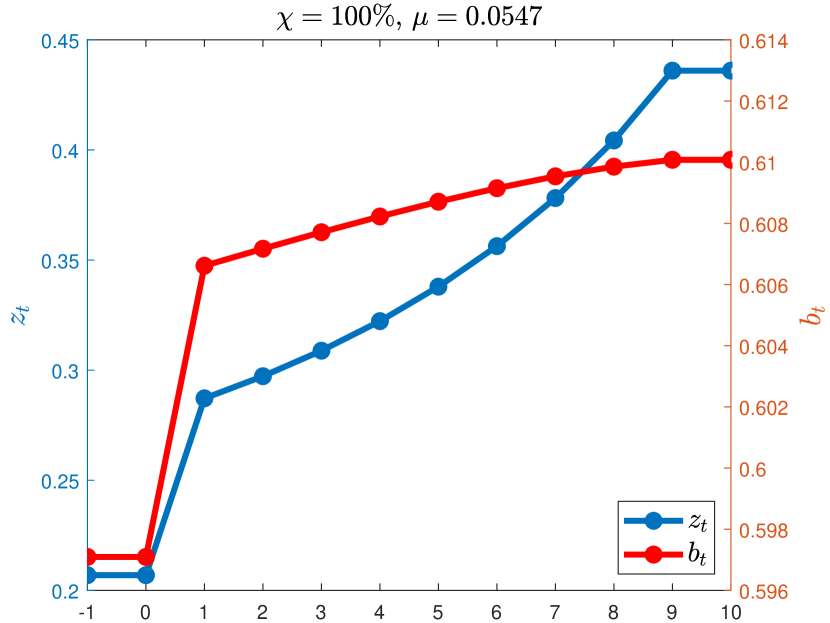

Consider a case with . In Figure 8, we start with a stationary equilibrium with . At time 0, it is announced that there will be a permanent change in to at time . The stationary equilibrium with is a terminal condition. The top-right panel of Figure 8 shows the transition path when . It jumps right after the announcement and steadily converges to a new steady state. The top-left panel of Figures 8 displays its phase diagram. It does not have a backward bending feature, and increases monotonically until it reaches .

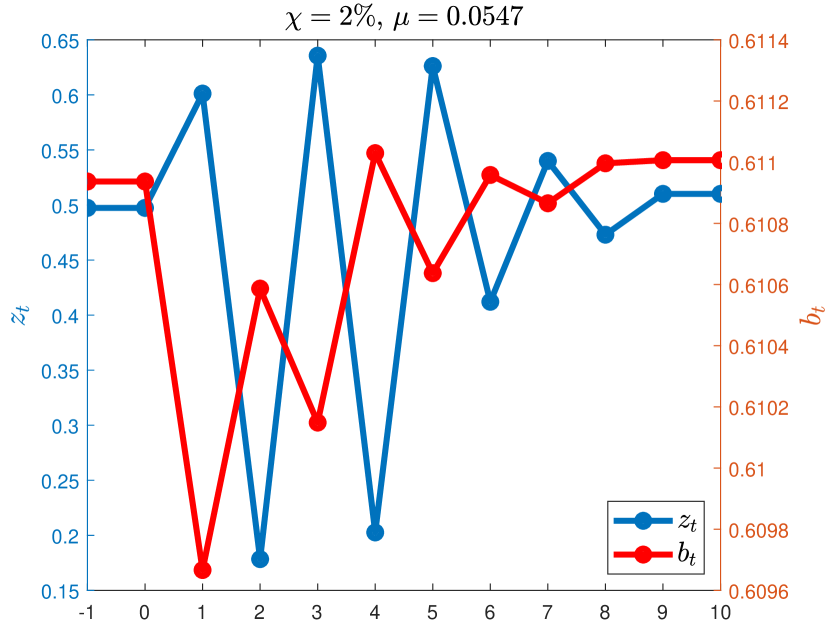

The middle-right panel of Figure 8 shows the transition path when . Despite eventually reaching , its transition dynamics are oscillatory. The middle-left panel of Figure 8 presents the phase diagram. As discussed in Section 3, when the reserve requirement is low, the function exhibits a backward-bending feature that induces oscillations on the path towards convergence to . It is important to note that exceeds both and , implying that there is no endogenous two-period cycle in this case. However, even in the absence of an endogenous cycle, lower reserve requirements can still increase volatility in economic fluctuations when there is a news shock.

The bottom-right panel of Figure 8 shows the transition path when . This also exhibits an oscillatory transition. Even though it eventually goes up from to , it goes even higher than in the transition path. The top-left panel of Figures 8 shows that its phase diagram. In this case, has a more backward bending feature than the case with , and this feature induces large fluctuations during the path to converge to .

Now we introduce unsecured credit. Similar to the previous experiment, the permanent change from to implies a shift of equations (37) and (38), from and to and , respectively. Then, starting in steady state with and ending in steady state with , the transitional dynamics of the equilibrium with unsecured credit also can be solved by backward induction.

Again, let’s consider a case with . In Figure 9, we begin with a stationary equilibrium with . At time 0, an announcement is made that there will be a permanent change in to at time . The stationary equilibrium with is a terminal condition for this dynamics system. Real money balances and credit converge monotonically to the new equilibrium when but they fluctuate considerably when reserve requirements are very low. Similar to Model 1, news about monetary policy induces complicated dynamics in and when reserve requirements are low. The right panel of Figure 9 also shows that there is an asymmetry when the reserve requirement is low. When , news leading to an increase in tends to lower because higher raises equilibrium payoff, which in turn relaxes the endogenous credit limit.

As shown in Figure 8 and 9, transitions display various patterns depending on , with lower reserve requirements more likely to induce cyclic and boom-bust responses. There is perfect foresight about the event and the transition is uniquely determined. However, it can display a wide range of patterns depending on reserve requirements. When reserve requirements are high, increases monotonically towards . However, with low reserve requirements, the economy is more likely to experience cyclic and boom-bust responses following a monetary announcement.

7 Conclusion

The goal of this paper is to examine the (in)stability of fractional reserve banking. To that end, this paper builds a simple monetary model of fractional reserve banking that can capture the conditions for (in)stability under different specifications. Lowering the reserve requirement increases the welfare at the steady state. However, it can induce instability. The baseline model and its extension establish the conditions for endogenous cycles and chaotic dynamics. The model also features stochastic cycles and self-fulfilling boom and burst under explicit conditions. The model shows that fractional reserve banking can endanger stability in the sense that equilibrium is more prone to exhibit cyclic, chaotic, and stochastic dynamics under lower reserve requirements. This is due to the amplified liquidity premium. This result holds in the extended model with unsecured credit.

This paper also provides some empirical evidence that is consistent with the prediction of the model. I test the association between the required reserves ratio and the real money volatility using cointegrating regression. I find a significant negative relationship between the two variables. The calibrated exercise also suggests that this channel could be another source of economic fluctuations. Both theoretical and empirical evidence find a link between the reserve requirement policy and (in)stability.

References

- (1)

- Altermatt et al. (2023) Altermatt, Lukas, Kohei Iwasaki, and Randall Wright, “General equilibrium with multiple liquid assets,” Review of Economic Dynamics, 2023.

- Andolfatto et al. (2020) Andolfatto, David, Aleksander Berentsen, and Fernando M Martin, “Money, Banking, and Financial Markets,” The Review of Economic Studies, 2020, 87 (5), 2049–2086.

- Aruoba et al. (2011) Aruoba, S Borağan, Christopher J Waller, and Randall Wright, “Money and capital,” Journal of Monetary Economics, 2011, 58 (2), 98–116.

- Azariadis (1993) Azariadis, Costas, Intertemporal Macroeconomics, Blackwell Publishing, Cambridge, MA, 1993.

- Baumol and Benhabib (1989) Baumol, William J and Jess Benhabib, “Chaos: Significance, Mechanism, and Economic Applications,” Journal of Economic Perspectives, 1989, 3 (1), 77–105.

- Becker (1956) Becker, Gary, “Free Banking,” Unpublished note, 1956.

- Benhabib and Farmer (1999) Benhabib, Jess and Roger E.A. Farmer, “Indeterminacy and sunspots in macroeconomics,” in J. B. Taylor and M. Woodford, eds., Handbook of Macroeconomics, Vol. 1 of Handbook of Macroeconomics, Elsevier, 1999, chapter 6, pp. 387–448.

- Berentsen et al. (2007) Berentsen, Aleksander, Gabriele Camera, and Christopher Waller, “Money, Credit and Banking,” Journal of Economic Theory, 2007, 135 (1), 171–195.

- Bernanke et al. (1999) Bernanke, Ben S, Mark Gertler, and Simon Gilchrist, “The Financial Accelerator in a Quantitative Business Cycle Framework,” Handbook of Macroeconomics, 1999, 1, 1341–1393.

- Boldrin and Woodford (1990) Boldrin, Michele and Michael Woodford, “Equilibrium Models Displaying Endogenous Fluctuations and Chaos: A Survey,” Journal of Monetary Economics, 1990, 25 (2), 189–222.

- Brock (1988) Brock, William A, “Nonlinearity and Complex Dynamics in Economics and Finance,” in Philip W. Anderson, Kenneth J. Arrow, and David Pines, eds., The Economy as an Evolving Complex System, Vol. 5, CRC Press, Boca Raton, 1988, pp. 77–97.

- Carvalho and Gabaix (2013) Carvalho, Vasco and Xavier Gabaix, “The Great Diversification and Its Undoing,” American Economic Review, 2013, 103 (5), 1697–1727.

- Chari and Phelan (2014) Chari, VV and Christopher Phelan, “On the Social Usefulness of Fractional Reserve Banking,” Journal of Monetary Economics, 2014, 65, 1–13.

- Diamond (1997) Diamond, Douglas W, “Liquidity, Banks, and Markets,” Journal of Political Economy, 1997, 105 (5), 928–956.

- Diamond and Dybvig (1983) and Philip H Dybvig, “Bank Runs, Deposit Insurance, and Liquidity,” Journal of Political Economy, 1983, 91 (3), 401–419.

- Fisher (1935) Fisher, Irving, 100% money, Adelphi Company, New York, 1935.

- Freeman and Kydland (2000) Freeman, Scott and Finn E Kydland, “Monetary Aggregates and Output,” American Economic Review, 2000, 90 (5), 1125–1135.

- Freeman and Huffman (1991) and Gregory W Huffman, “Inside Money, Output, and Causality,” International Economic Review, 1991, pp. 645–667.

- Friedman (1959) Friedman, Milton, A Program for Monetary Stability, Fordham University Press, New York, 1959.

- Gertler and Karadi (2011) Gertler, Mark and Peter Karadi, “A Model of Unconventional Monetary Policy,” Journal of monetary Economics, 2011, 58 (1), 17–34.

- Gu and Wright (2016) Gu, Chao and Randall Wright, “Monetary Mechanisms,” Journal of Economic Theory, 2016, 163, 644–657.

- Gu et al. (2019a) , Cyril Monnet, Ed Nosal, and Randall Wright, “On the Instability of Banking and Financial Intermediation,” Working Papers 1901, Department of Economics, University of Missouri April 2019.

- Gu et al. (2016) , Fabrizio Mattesini, and Randall Wright, “Money and Credit Redux,” Econometrica, 2016, 84 (1), 1–32.

- Gu et al. (2013) , , Cyril Monnet, and Randall Wright, “Endogenous Credit Cycles,” Journal of Political Economy, 2013, 121 (5), 940–965.

- Gu et al. (2019b) , Han Han, and Randall Wright, “The Effects of Monetary Policy Announcements,” in “Oxford Research Encyclopedia of Economics and Finance” 2019.

- Jaimovich and Siu (2009) Jaimovich, Nir and Henry E Siu, “The Young, the Old, and the Restless: Demographics and Business Cycle Volatility,” American Economic Review, 2009, 99 (3), 804–826.

- Kehoe and Levine (1993) Kehoe, Timothy J and David K Levine, “Debt-Constrained Asset Markets,” The Review of Economic Studies, 1993, 60 (4), 865–888.

- Kiyotaki and Moore (1997) Kiyotaki, Nobuhiro and John Moore, “Credit cycles,” Journal of political economy, 1997, 105 (2), 211–248.

- Krueger and Perri (2006) Krueger, Dirk and Fabrizio Perri, “Does Income Inequality Lead to Consumption Inequality? Evidence and Theory,” The Review of Economic Studies, 2006, 73 (1), 163–193.

- Lagos and Wright (2005) Lagos, Ricardo and Randall Wright, “A Unified Framework for Monetary Theory and Policy Analysis,” Journal of Political Economy, 2005, 113 (3), 463–484.

- Li and Yorke (1975) Li, Tien-Yien and James A Yorke, “Period Three Implies Chaos,” The American Mathematical Monthly, 1975, 82 (10), 985–992.

- Lotz and Zhang (2016) Lotz, Sebastien and Cathy Zhang, “Money and Credit as Means of Payment: A New Monetarist Approach,” Journal of Economic Theory, 2016, 164, 68–100.

- Lucas and Nicolini (2015) Lucas, Robert E and Juan Pablo Nicolini, “On the Stability of Money Demand,” Journal of Monetary Economics, 2015, 73, 48–65.

- Minsky (1957) Minsky, Hyman P, “Monetary Systems and Accelerator Models,” American Economic Review, 1957, 47 (6), 860–883.

- Minsky (1970) , “Financial Instability Revisited: The Economics of Disaster,” 1970. Available from https://fraser.stlouisfed.org/files/docs/historical/federa%20reserve%20history/discountmech/fininst_minsky.pdf.

- Von Mises (1953) Mises, Ludwig Von, The Theory of Money and Credit, Yale University Press, 1953.

- Rocheteau and Wang (2023) Rocheteau, Guillaume and Lu Wang, “Endogenous liquidity and volatility,” Journal of Economic Theory, 2023, 210, 105652.

- Sargent (2011) Sargent, Thomas J, “Where to Draw Lines: Stability Versus Efficiency,” Economica, 2011, 78 (310), 197–214.

- Sargent and Wallace (1982) and Neil Wallace, “The Real-Bills Doctrine versus the Quantity Theory: A Reconsideration,” Journal of Political Economy, 1982, 90 (6), 1212–1236.

- Scheinkman and Woodford (1994) Scheinkman, Jose A and Michael Woodford, “Self-Organized Criticality and Economic Fluctuations,” American Economic Review, 1994, 84 (2), 417–421.

- Sharkovskii (1964) Sharkovskii, AN, “Cycles Coexistence of Continuous Transformation of Line in Itself,” Ukr. Math. Journal, 1964, 26 (1), 61–71.

- Venkateswaran and Wright (2014) Venkateswaran, Venky and Randall Wright, “Pledgability and liquidity: A new monetarist model of financial and macroeconomic activity,” NBER Macroeconomics Annual, 2014, 28 (1), 227–270.

- Wipf (2020) Wipf, Christian, “Should Banks Create Money?,” Technical Report, Discussion Papers 2020.

Appendix

Appendix A Proofs

Proof of Proposition 1.

Recall (28)

Since , we have the following:

Since and , it is straightforward to show that lowering or lowering increases . ∎

Proof of Proposition 2.

Let there exists a two-period cycle satisfying . Since , we have . Using (27) with gives

| (42) |

This two-period cycle should satisfy and . The first one can be easily shown using

since we have . Because , the latter one, , is held when

This equilibrium solves

We can check if lowering the reserve requirement also increases the volatility. Consider the difference between peak and trough . Since

reducing the reserve requirement increases the difference between peak and trough. ∎

Proof of the Existence of a Two-period Monetary Cycle where .

Let . With given the unique steady state, for and for . Because is linear increasing function for , there exist a s.t . Since and , satisfies . We can write slope of as follows.

which implies when . And it is easy to show . With given and , there exist a , satisfying which are fix points for . ∎

Proof of Proposition 3.

When DM trade is based on take-it-or-leave-it offer from buyer to seller with and , can be written as

Using gives

where . Substituting yields

Then rearranging terms gives

∎

Proof of Proposition 4.

I divide three period cycles into two cases.

Case 1: Let there exists a three-period cycle satisfying . Since , we have , . Using (27) with gives

| (43) |

This three-period cycle should satisfy and . First one can be easily shown using

since we have . Because , the latter one, , is held when

Case 2: Let there exists a three-period cycle satisfying . Since , we have and solves (44)-(45).

| (44) | ||||

| (45) |

These functions satisfies for , for , for and for where solves . One can easily show . Therefore any intersection between and satisfies which contradicts to our initial conjecture . This implies there is no three-period cycle satisfying . Therefore we can conclude that a three-period cycle exists when

This equilibrium solves

We can check if lowering the reserve requirement also increases the volatility. Consider the difference between peak and trough . Since

reducing the reserve requirement increases the difference between peak and trough.

Proof of Corollary 1:.

Proposition 4 shows that at least one periodic point satisfies in 3- period cycles. Two period cycles satisfies also implies at least one periodic point satisfies in 2-period cycles since . This result holds for any -periodic cycles. Let be the periodic points of a -cycle. Suppose for all . By the definition of a -period cycle, since for .

which shows the contradiction implying at least one periodic point satisfies . ∎

Proof of Proposition 5.

By definition, if there exists satisfying

| (46) | ||||

| (47) |

with , then there exists a proper sunspot equilibrium. Because and are weighted averages of and , where and , by the uniqueness of the positive steady state, necessary and sufficient conditions for (46) and (47) are

Since , above conditions are reduce to

| (48) |

When , there exists that satisfies (48). Rewrite (46) and (47) as

| (49) |

since and . Therefore, when , a stationary sunspot equilibrium exists.

Now consider the case with . Since , there is an interval , which satisfy and for and .

Since , the above condition can be reduce to . There exist multiple solutions, , satisfying given and . These solutions satisfy (49). Therefore, if , there exists a stationary sunspot cycle. ∎

Proof of Proposition 6.

Consider . If where solves . In this case, there exist multiple equilibria. If , then there exist equilibria with (bubble) which crashes to 0 (burst) as , where and . Then there exist equilibria with bubble-burst as a self-fulfilling crisis. Conditions for this case are shown as below. Similar to Corollary 3, consider take-it-leave-it offer with and . Then we have following difference equation:

| (50) |

Step 1: [Multiplicity i.e., where solves ] Consider the following condition.

Since , we have

This can be reduced as

Step 2: [Show ] It is straightforward to show that holds when

Therefore, when

there exist satisfying and , where and . ∎

Proof of Proposition 7.

A two period cycle result is presented and three-period case will follow. Let there exists a two-period cycle satisfying where . Since , we have and where , , and solve

and . This two-period cycle should satisfy and . For given and , first one can be easily shown using

since we have . Now we also can check the latter using the below conditions

The sufficient conditions to have is for and for . Since we have , there exist a three period cycle when

where . Now, let there exists a three-period cycle satisfying where . Since , , we have , , and where , , and solve

and . This three-period cycle should satisfy and . For given and , first one can be easily shown using

since we have . Now we also can check the latter using below conditions

The sufficient conditions to have is for and for . Since we have , there exist a three period cycle when

where . Again, the existence of a three-cycle implies the existence of cycles of all orders and chaotic dynamics by the Sarkovskii theorem and the Li-Yorke theorem. ∎

Appendix B Empirical Appendix

This section provides robustness checks for empirical results. To check the sensitivity of the results, Table 4 and 5 repeat all the empirical analysis, reported in Table 1 and 2, using quarterly series instead of annual data. The results are similar to the benchmark analysis shown in Table 1 and 2.

| Price level | CPI | Core CPI | PCE | Core PCE | ||||

|---|---|---|---|---|---|---|---|---|

| Dependent | OLS | CCR | OLS | CCR | OLS | CCR | OLS | CCR |

| variable: | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) |

| ffr | ||||||||

| Constant | ||||||||

| Obs. | 196 | 196 | 196 | 196 | 196 | 196 | 196 | 196 |

| 0.457 | 0.265 | 0.473 | 0.202 | 0.564 | 0.239 | 0.607 | 0.224 | |

| 9.631 | 10.231 | 10.347 | 10.694 | |||||

| 5% CV | ||||||||

| 11.774 | 12.209 | 12.309 | 12.003 | |||||

| 5% CV | ||||||||

Note: For (1), (3), (5) and (7), OLS estimates are reported, and Newey-West standard errors with lag 4 are reported in parentheses. For (2), (4), (6), and (8), first-stage long-run variance estimations for CCR are based on the quadratic spectral kernel and lag 4. The bandwidth selection is based on Newey-West fixed lag, ; denotes the required reserve ratio, ffr denotes federal funds rates and denotes the cyclical volatility of real money balances. ***, **, and * denotes significance at the 1, 5, and 10 percent levels, respectively.

| Phillips-Perron test | ADF test | |||

|---|---|---|---|---|

| w/ lag 4 | ||||

| ffr | ||||

| (CPI) | ||||

| (Core CPI) | ||||

| (PCE) | ||||

| (Core PCE) | ||||

| (CPI) | ||||

| (Core CPI) | ||||

| (PCE) | ||||

| (Core PCE) | ||||

Note: ffr denotes federal funds rates, denotes required reserve ratio, and denotes cyclical volatility of real money balances. ***, **, and * denotes significance at the 1, 5, and 10 percent levels, respectively.

This section also provides robustness checks using time-series before 2008. Table 6 and 7 repeat the analysis using time-series before 2008. Again, the results are similar to the benchmark analysis shown in Table 1 and 2.

| Price level | CPI | Core CPI | PCE | Core PCE | ||||

|---|---|---|---|---|---|---|---|---|

| Dependent | OLS | CCR | OLS | CCR | OLS | CCR | OLS | CCR |

| variable: | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) |

| ffr | ||||||||

| Constant | ||||||||

| Obs. | 43 | 43 | 43 | 43 | 43 | 43 | 43 | 43 |

| 0.495 | 0.185 | 0.503 | 0.125 | 0.587 | 0.121 | 0.621 | 0.068 | |

| 10.150 | 8.453 | 8.421 | 6.925 | |||||

| 5% CV | ||||||||

| 11.506 | 9.544 | 9.504 | 7.804 | |||||

| 5% CV | ||||||||

Note: For (1), (3), (5) and (7), OLS estimates are reported, and Newey-West standard errors with lag 1 are reported in parentheses. For (2), (4), (6), and (8), first-stage long-run variance estimations for CCR are based on the quadratic spectral kernel and lag 1. The bandwidth selection is based on Newey-West fixed lag, ; denotes the required reserve ratio, ffr denotes federal funds rates and denotes the cyclical volatility of real money balances. ***, **, and * denotes significance at the 1, 5, and 10 percent levels, respectively.

| Phillips-Perron test | ADF test | |||

|---|---|---|---|---|

| w/ lag 1 | ||||

| ffr | ||||

| (CPI) | ||||

| (Core CPI) | ||||

| (PCE) | ||||

| (Core PCE) | ||||

| (CPI) | ||||

| (Core CPI) | ||||

| (PCE) | ||||

| (Core PCE) | ||||

Note: ffr denotes federal funds rates, denotes required reserve ratio, and denotes cyclical volatility of real money balances. ***, **, and * denotes significance at the 1, 5, and 10 percent levels, respectively.

Now the following tables provide robustness checks using the alternative data set, M1J from Lucas and Nicolini (2015). Table 8 and 9 repeat the analysis using the alternative data, M1J from Lucas and Nicolini (2015). The required reserve ratio is calculated by dividing required reserves by the deposit component of M1J. Again, the results are similar to the benchmark analysis shown in Table 1 and 2.

| Price level | CPI | Core CPI | PCE | Core PCE | ||||

|---|---|---|---|---|---|---|---|---|

| Dependent | OLS | CCR | OLS | CCR | OLS | CCR | OLS | CCR |

| variable: | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) |

| ffr | ||||||||

| Constant | ||||||||

| Obs. | 43 | 43 | 43 | 43 | 43 | 43 | 43 | 43 |

| -0.007 | 0.063 | -0.015 | 0.056 | 0.004 | 0.064 | 0.002 | 0.060 | |

| 12.430 | 12.229 | 12.420 | 12.259 | |||||

| 5% CV | ||||||||

| 11.677 | 11.447 | 11.524 | 11.303 | |||||

| 5% CV | ||||||||

Note: For (1), (3), (5) and (7), OLS estimates are reported, and Newey-West standard errors with lag 1 are reported in parentheses. For (2), (4), (6), and (8), first-stage long-run variance estimations for CCR are based on the quadratic spectral kernel and lag 1. The bandwidth selection is based on Newey-West fixed lag, ; denotes the required reserve ratio, ffr denotes federal funds rates and denotes the cyclical volatility of real money balances. ***, **, and * denotes significance at the 1, 5, and 10 percent levels, respectively.

| Phillips-Perron test | ADF test | |||

|---|---|---|---|---|

| w/ lag 1 | ||||

| ffr | ||||

| (CPI) | ||||

| (Core CPI) | ||||

| (PCE) | ||||

| (Core PCE) | ||||

| (CPI) | ||||

| (Core CPI) | ||||

| (PCE) | ||||

| (Core PCE) | ||||

Note: ffr denotes federal funds rates, denotes required reserve ratio, and denotes cyclical volatility of real money balances. ***, **, and * denotes significance at the 1, 5, and 10 percent levels, respectively.

Lastly, the following tables provide robustness checks using another alternative data set, M1 adjusted for retail sweeps. Table 10 and 11 repeat the analysis using the alternative data, M1 adjusted for retail sweeps. The required reserve ratio is calculated by dividing required reserves by the deposit component. Again, the results are similar to the benchmark analysis shown in Table 1 and 2.

| Price level | CPI | Core CPI | PCE | Core PCE | ||||

|---|---|---|---|---|---|---|---|---|

| Dependent | OLS | CCR | OLS | CCR | OLS | CCR | OLS | CCR |

| variable: | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) |

| ffr | ||||||||

| Constant | ||||||||

| Obs. | 44 | 44 | 44 | 44 | 44 | 44 | 44 | 44 |

| 0.036 | 0.038 | 0.000 | 0.014 | 0.105 | 0.013 | 0.107 | -0.007 | |

| 7.548 | 6.364 | 6.460 | 5.291 | |||||

| 5% CV | ||||||||

| 8.882 | 7.824 | 7.639 | 6.362 | |||||

| 5% CV | ||||||||

Note: For (1), (3), (5) and (7), OLS estimates are reported, and Newey-West standard errors with lag 1 are reported in parentheses. For (2), (4), (6), and (8), first-stage long-run variance estimations for CCR are based on the quadratic spectral kernel and lag 1. The bandwidth selection is based on Newey-West fixed lag, ; denotes the required reserve ratio, ffr denotes federal funds rates and denotes the cyclical volatility of real money balances. ***, **, and * denotes significance at the 1, 5, and 10 percent levels, respectively.

| Phillips-Perron test | ADF test | |||

|---|---|---|---|---|

| w/ lag 1 | ||||

| ffr | ||||

| (CPI) | ||||

| (Core CPI) | ||||

| (PCE) | ||||

| (Core PCE) | ||||

| (CPI) | ||||

| (Core CPI) | ||||

| (PCE) | ||||

| (Core PCE) | ||||

Note: ffr denotes federal funds rates, denotes required reserve ratio, and denotes cyclical volatility of real money balances. ***, **, and * denotes significance at the 1, 5, and 10 percent levels, respectively.

Appendix C Closed Form Solution for Calibration

This section provides closed-form solutions that are used for the calibration. The utility functions and the DM cost function for the parameterization are

First, consider Model 1. The stationary equilibrium satisfies

and the DM consumption is

The real balance of aggregate money is equal to the DM consumption i.e., and the real balance to output ratio is given by

A derivative of with respect to is

Then we have

The elasticity of aggregate money with respect to is given by

Consider Model 2. When , unsecured credit limit is determined by

When , the real balance of aggregate money is

where

The derivative of unsecured credit with respect to is

and the derivative of aggregate money real balances with respect to is

The aggregate money real balances to output ratio is

then the derivative of with respect to is

and the elasticity of aggregate money with respect to is