Abstract

This paper generalizes the local variance gamma model of Carr and Nadtochiy, to a piecewise quadratic local variance function. The formulation encompasses the piecewise linear Bachelier and piecewise linear Black local variance gamma models. The quadratic local variance function results in an arbitrage-free interpolation of class . The increased smoothness over the piecewise-constant and piecewise-linear representation allows to reduce the number of knots when interpolating raw market quotes, thus providing an interesting alternative to regularization while reducing the computational cost.

keywords:

volatility surface; interpolation; risk-neutral density; arbitrage; quantitative finance; European optionsxx \issuenum1 \articlenumber1 \history \TitleThe Quadratic Local Variance Gamma Model: an arbitrage-free interpolation of class for option prices \AuthorFabien Le Floc’h \AuthorNamesFabien Le Floc’h

1 Introduction

The financial markets provide option prices for a discrete set of strike prices and maturity dates. In order to price over-the-counter vanilla options with different strikes, or to hedge complex derivatives with vanilla options, it is useful to have a continuous arbitrage-free representation of the option prices, or equivalently of their implied volatilities. For example, the variance swap replication of Carr and Madan consists in integrating a specific function over a continuum of vanilla put and call option prices (Carr and Madan, 2001; Carr and Lee, 2008). More generally, Breeden and Litzenberger (1978) have shown that any path-independent claim can be valued by integrating over the probability density implied by market option prices. An arbitrage-free representation is also particularly important for the Dupire local volatility model (Dupire, 1994), where arbitrage will translate to a negative local variance. A option price representation of class is also key to guarantee the second-order convergence of numerical schemes applied to the Dupire partial differential equation, commonly used to price exotic financial derivative contracts.

A rudimentary, but popular representation is to interpolate market implied volatilities with a cubic spline across option strikes. Unfortunately this may not be arbitrage-free as it does not preserve the convexity of option prices in general. A typical convex interpolation of the call option prices by quadratic splines or rational splines is also not satisfactory in general since it may generate unrealistic oscillations in the corresponding implied volatilities, as evidenced in (Jäckel, 2014). Kahalé (2004) designs an arbitrage-free interpolation of the call option prices, which however requires convex input quotes, employs two embedded non-linear minimizations, and it is not proven that the algorithm for the interpolation function of class converges.

More recently, Andreasen and Huge (2011) have proposed to calibrate the discrete piecewise constant local volatility corresponding to a single-step finite difference discretization of the forward Dupire equation. In their representation of the local volatility, the authors use as many constants as the number of market option strikes for an optimal fit. It is thus sometimes considered to be "non-parametric". Their technique works well in general but requires some care around the choice of discretization grid: it must be sufficiently dense so that two market strikes do not fall in between the same consecutive grid nodes, and sufficiently wide to properly model the boundary behaviour. Those two requirements complicate, and slow down the non-linear optimization involved in the technique. Furthermore the output is a discrete set of option prices, which, while relatively dense, must still be interpolated carefully to obtain the price of options whose strike falls in between grid nodes.

Le Floc’h and Oosterlee (2019b) derived a specific B-spline collocation to fit the market option prices, while ensuring the arbitrage-free property at the same time. While the fit is quite good in general, it may not be applicable to interpolate the original quotes with high accuracy. For example, input quotes may already be smoothed out if they stem from a prior model, or from a market data broker, or from another system in the bank. In those cases, it is desirable to use a nearly exact interpolation.

Le Floc’h (2021) extends the local variance gamma model of Carr and Nadtochiy (2017), which relies on a piecewise-constant representation of the local variance function, to a piecewise-linear Bachelier representation. This paper generalizes the model to a piecewise-quadratic function. It encompasses the piecewise-linear Bachelier and piecewise-linear Black representations. The full piecewise-quadratic model results in an arbitrage-free interpolation of class for the option prices. The smoother implied probability density allows for the use of a sparser set of interpolation knots, thus providing an alternative to regularization in order to avoid overfitting. In addition, a sparser set of knots reduces the computational cost of the technique.

2 Dupire’s PDDE in the local variance gamma model

We recall Dupire’s partial difference differential equation (PDDE) for a call option price of strike and maturity (Carr and Nadtochiy, 2017):

| (1) |

for a Martingale asset price process of expectation .

Let be a increasing set of the strike prices, such that , with the interval being the spatial interval where the asset lives. Furthermore, we require the following to hold

The may correspond to the strike prices of the options of maturity we want to calibrate against, along with the forward price as in (Carr and Nadtochiy, 2017; Le Floc’h, 2021). This choice allows for a nearly exact fit. It may also be some specific discretization of size with lower or equal to the number of market strike prices.

We consider to be a piecewise-quadratic function of class on .

Let be the function defined by . is effectively the price of an out-of-the-money option (the price of a call option for and of a put option for ). The Dupire PDDE leads to

| (2) |

on the interval , where is the Dirac delta function. Instead of solving Equation 2 directly, we look for a solution on the two intervals and separately. On each interval, we have

| (3) |

Then, the continuity of at implies

| (4) |

In order to define a unique , we also impose the absorbing boundary conditions

| (5) |

The continuity of the second derivative of at follows from the continuity of at . We may further impose a continuity relation at :

| (6) |

3 Explicit solution

Let on with . Being a quadratic, may also be expressed as with

In particular, and may be complex numbers. When and , we may define and we have with .

The solutions of Equation 3 on read

| (7) |

with111See Appendix A on how to avoid the use of complex numbers.

where . The normalization makes .

The derivative of reads

| (8) |

with

The conditions to impose continuity of and its derivative at results in the following linear system

| (9) | ||||

| (10) |

for , with

The boundary condition at translates to . At , the boundary condition translates to . The jump condition at reads

with

From the above equations, we deduce that the coefficients are solutions of the following tridiagonal system

| (11) |

with for , ,

for , and .

Using the continuity of , the jump condition of at and the continuity of , the condition (Equation 6) reads

| (12) |

Equation 12 implies that is not continuous at , unless . The condition can not be imposed as an additional constraint on since its value is already fully determined by the tridiagonal system. It may however be imposed by choosing the correct model parameter to adjust the value of at along with its left and right derivative values.

4 Parameterizations

4.1 Linear Bachelier

The linear Bachelier local variance consists in and may be rewritten using values at the knots as

| (13) |

where the parameters .

It corresponds to the parameterization studied in (Le Floc’h, 2021), where it is shown that the local variance function must not be at but must follow condition (Equation 12) in order to avoid a spurious spike at . Under the linear Bachelier local variance, the condition reads

or equivalently

| (14) |

This is not a linear problem, as depends on through in a non-linear way (Equations 9 and 10). Starting with the algorithm described in Section 3 to compute , using Equation 14 with as initial guess for , we may however apply the following iteration

-

•

Update through Equation 14.

-

•

Recalculate and for by solving the updated tridiagonal system.

Three iterations are enough in practice.

4.2 Linear Black

4.3 Positive quadratic B-spline

A B-spline parameterization with positive coefficients implies positive. Furthermore, Equation 12 imposes a double knot at (because the derivative of is not continuous there). We thus consider

| (16) |

where and is the quadratic basis spline with knots . In particular, we have . Using the B-spline derivative identity (De Boor, 1978) and the fact that the order of the B-spline is 3, we obtain

and the condition reads

Using the definitions of and we obtain

or equivalently

| (17) |

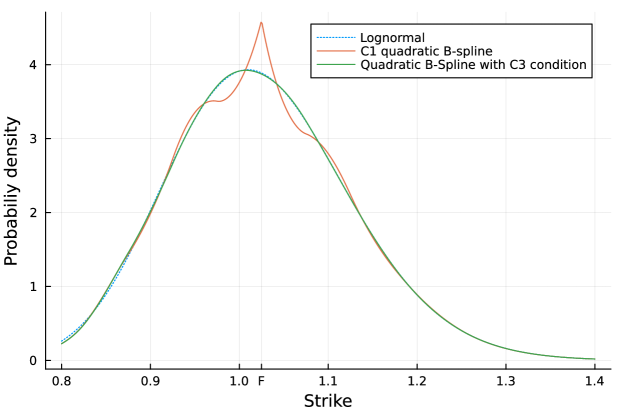

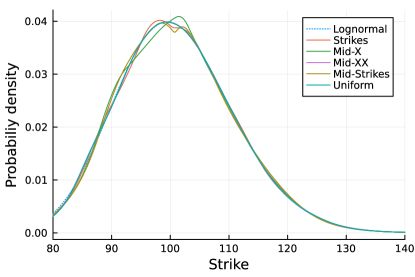

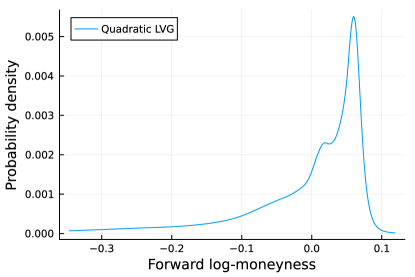

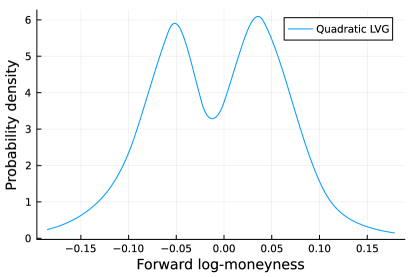

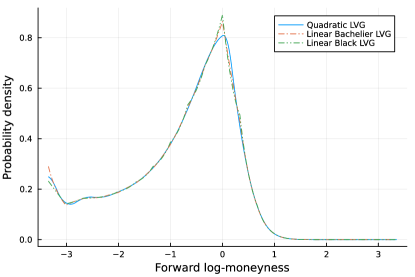

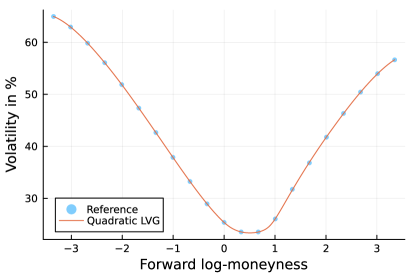

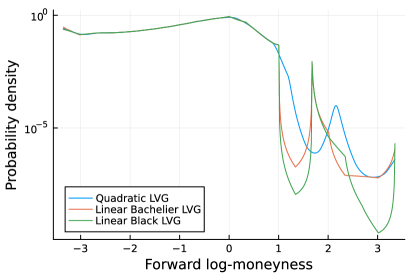

As an illustration, we consider the same example as in (Le Floc’h, 2021): we fit the quadratic LVG model to 10 option prices of strikes (0.85, 0.90, 0.95, 1, 1.05, 1.1, 1.15, 1.2, 1.3, 1.4), obtained by the Black-Scholes model with constant volatility , time to maturity and forward price . We know that the theoretical distribution is a lognormal distribution. A straightforward quadratic B-spline leads to a large spike in the probability density implied from the calibrated LVG model (Figure 1). Adding the condition through an additional B-spline knot recovers a smooth implied probability density.

5 Calibration

5.1 Error measure

The calibration of a single maturity consists in finding the parameters (the for the linear models, or for the quadratic B-spline) such that the function , solution of the Dupire PDDE fits the market option prices of respective strikes according to an appropriate measure. A common practice is to perform a least-squares minimization of the error measure defined by

| (18) |

with for and where is the implied volatility corresponding to the option prices obtained with the piecewise-linear local gamma variance model and is the market implied volatility at strike , are weights associated to the accuracy of the fit at each point.

In order to solve this non-linear least-squares problem, we will use the Levenberg-Marquardt algorithm as implemented by Klare and Miller (2013). The box constraints can be added in a relatively straightforward manner to any Levenberg-Marquardt algorithm, through the projection technique described in (Kanzow et al., 2004), or through a variable transform from to a subset of (for example through the function with some small positive ).

The implied volatility for a given option price may be found efficiently and accurately through the algorithm of Jäckel (2015). In general, we prefer to solve an almost equivalent formulation in terms of option prices, using the error measure defined by

| (19) |

with being the local variance gamma option price with parameter and strike , and the capped inverse Vega weights given by

| (20) |

where is the Black-Scholes Vega corresponding the market option price , and is a cap applied to avoid numerical issues related to the limited machine accuracy (see Le Floc’h and Oosterlee (2019b); Le Floc’h (2021) for the justification).

5.2 Exact interpolation

Sometimes, it is desirable to interpolate a given set of reference prices nearly exactly. This is typically the case when the reference prices come from some prior model. We apply the same least-square minimization but choose the number of free parameters to be equal to the number of reference prices.

5.2.1 Linear models

For the linear models, this means to use and set and to model a flat extrapolation. In general, the market strikes will not include . In this case, must be added to the knots used in the local variance gamma representation. This adds one more parameter to the representation, where is the index corresponding to in the set of knots. The value of is not free, it is given by the condition (Equation 6) and enforced through the iterative procedure described in the previous sections.

5.2.2 B-spline knots locations

For the linear Bachelier and Black parameterization, choosing the knots at the market strikes works well. The situation is more complex for the quadratic B-spline parameterization.

Let be the market options strikes. Let the index be such that . We may:

-

•

place the knots at the market strikes (labeled "Strikes" in the figures)

The dimension of is then if and if . The change in the number of dimensions suggests that the interpolation may change significantly when the forward price moves across a market strike.

-

•

place the knots in the middle of market strikes. According to (De Boor, 1978, p. 61), the quadratic spline is then solution to a diagonally dominant tridiagonal system, which increases the stability and reduce oscillations of the interpolation. There are however several ways to do it:

-

–

choose the direct mid-points (labeled "Mid-Strikes")

The dimension of is then if and if .

-

–

choose the mid-points, excluding the point closest to the forward price (labeled "Mid-X")

The dimension of is then .

-

–

choose the mid-points, excluding the point closest to the forward price and placing the first and last strike in the middle of two knots (labeled "Mid-XX")

The dimension of is then .

-

–

-

•

use a uniform discretization of composed of points, and shift it such that the forward is exactly part of the knots and we have .

In each of those case, we make sure to add the forward price as a double knot, as well as the boundaries . The dimension of implied by the knots is larger than the number of market strikes. We choose the extra parameters as such:

-

•

if , we set , and is obtained from and .

-

•

if , we set , and is obtained from and .

-

•

if , we set , and is obtained from and .

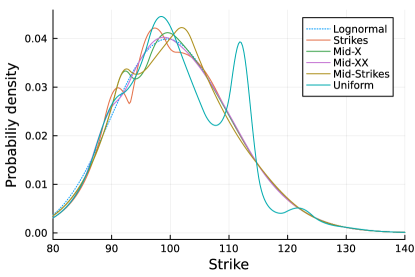

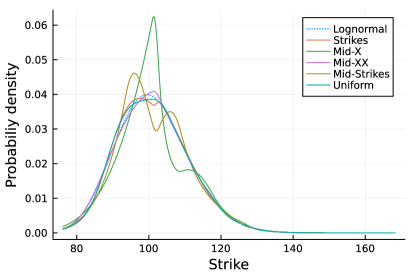

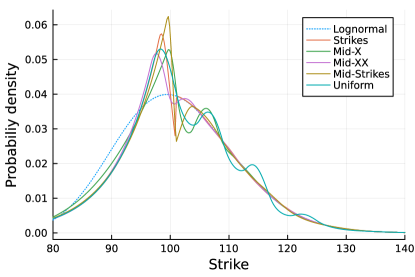

In order to assess the various knots candidates, we consider the same example as in the previous section, but using a few different random sets of 10 strikes in the interval [85,140] and a forward price (Table 1).

| Set | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| A | 88.77 | 92.85 | 93.38 | 99.37 | 107.99 | 120.29 | 122.03 | 123.9 | 134.71 | 135.43 |

| B | 85.02 | 101.92 | 103.55 | 114.45 | 121.85 | 123.69 | 125.07 | 125.58 | 131.63 | 133.86 |

| C | 98.07 | 100.93 | 101.06 | 106.88 | 109.12 | 110.93 | 119.76 | 119.83 | 132.19 | 138.27 |

| D | 85.00 | 90.00 | 95.00 | 100.00 | 101.00 | 105.00 | 110.00 | 115.00 | 120.00 | 130.00 |

| Set | Strikes | Mid-Strikes | Mid-X | Mid-XX | Uniform |

|---|---|---|---|---|---|

| A | 9.4e-8 | 6.0e-3 | 5.2e-3 | 4.1e-8 | 4.8e-9 |

| B | 9.9e-9 | 2.8e-3 | 5.8e-1 | 2.9e-6 | 9.9e-3 |

| C | 1.0e-6 | 1.9e-3 | 1.0e-2 | 1.1e-8 | 1.4e-3 |

| D | 4.1e-4 | 8.1e-2 | 4.1e-2 | 2.6e-5 | 5.0e-7 |

The uniform discretization may222In practice, market strikes are not randomly distributed, but according to multiples of a minimum strike width, with more strikes near the money. The uniform discretization may still be relevant if some regularization is added to the objective of the minimizer. result in strong oscillations due to overfitting in places where no market strike is quoted as in the set A (Figure 2(a)).

The "Mid-Strikes" choice leads to a strong oscillation around the forward in set B (Figure 2(b)). The "Mid-X" produces a somewhat awkward shape on the set B. When the forward is very close to some of the knots as in set C, the "Strikes", "Mid-Strikes" choices lead to a density with a sharp gradient near the forward, a feature not desirable (Figure 2(c)). When the forward is part of the market strikes, a small wiggle is visible at the forward for "Strikes" and "Mid-Strikes" (Figure 2(d)).

Finally it is also interesting to look at the overall root mean square error in implied volatilities for the different choices (Table 2). The "Strikes" and "Mid-XX" choices consistently result in a near-perfect333The error in volatility is always below one basis point. fit.

Overall, the "Mid-XX" knots lead to the most stable probability density along with an excellent fit.

5.2.3 Many quotes, few parameters

In (Le Floc’h, 2021), regularization is employed to ensure a smooth implied probability density when fitting to many, eventually noisy, market option quotes. An interesting simpler alternative is to use few knots/few parameters instead of as many parameters as market quotes: by limiting the number of free-parameters, we may avoid overfitting issues, and at the same time we reduce the number of dimensions of the problem, thus increasing stability and performance. Where to place the knots then? Based on the previous observations, we may choose knots such that the market strikes are equidistributed. Concretely, we use

where with and use the "Mid-XX" knots on top of . It may happen that many market strikes are quoted in a narrow range, in which case the set could be adjusted with a minimum strike width, although we did not need this tweak on the market examples presented below.

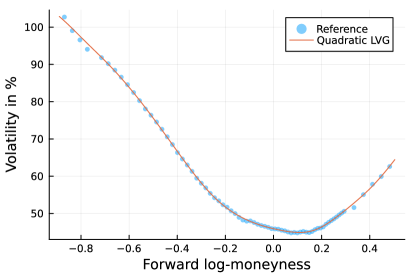

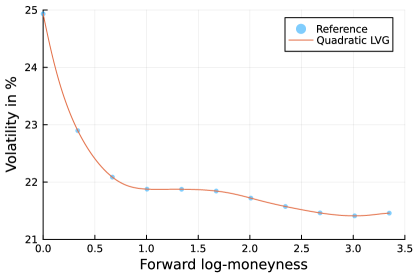

We consider several different underlying assets: SPX500 expiring on March 24, 2017 as March 16, 2017 (one week - 1w) and on March 7, 2018 as of February 5, 2018 (one month - 1m), TSLA of maturity July 20, 2018 as of June 15, 2018 (1m), AAPL with expiry in 4 days as of October 28, 2013 (4d) from Alexiou et al. (2021), as as well as the AUD/NZD currency pair of maturity July 9, 2014 as of July 2, 2014 (1w) from Wystup (2018). There is an apparent focus on short maturities as those are more difficult to capture, with a variety of smile shapes, with some exhibiting multi-modality. The latter are particularly challenging for parametric models such as SVI (Gatheral, 2006), SABR (Hagan et al., 2002), or even polynomial stochastic collocation (Le Floc’h and Oosterlee, 2019a, b). As the implied volatility smile flattens for long maturities, those are much easier to fit to.

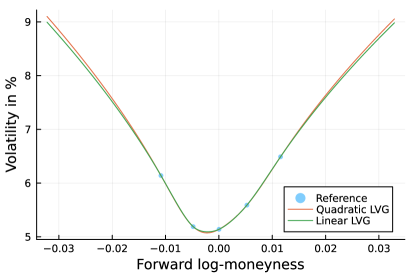

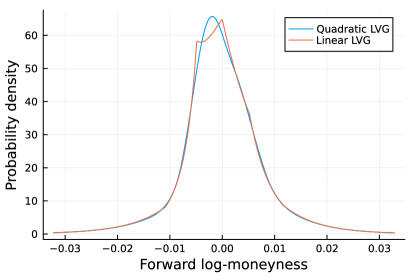

The AUD/NZD foreign exchange smile from Wystup (2018) is useful to see how the local variance gamma model behaves on a minimalistic example: indeed, as is usual on the foreign exchange options market, it involves only five options quotes. In this case we use as many parameters as market quotes. Figure 7(b) shows that the density implied by the quadratic LVG model is smooth, but the one implied by the linear Bachelier LVG model exhibits some sharp unnatural gradients near the money.

Indeed, the linear LVG model leads only to a probability density. Such gradients are then inevitable when the number of quotes is small. On this example, the (unconstrained) SVI model is known to lead to some negative probability density.

In all the examples considered so far, the fit in terms of implied volatilities is excellent, and the implied probability density is smooth, without spurious peaks, although the number of points considered () is somewhat arbitrary.

5.2.4 Challenging examples of exact interpolation

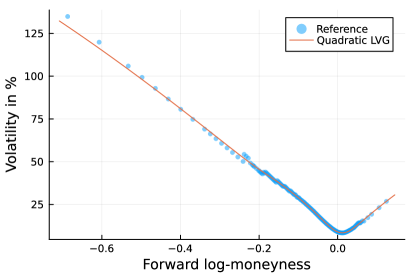

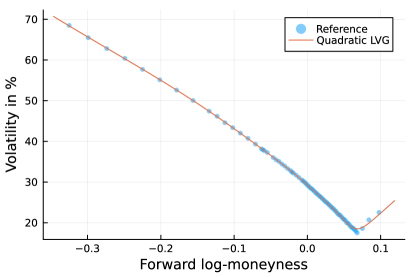

We consider the manufactured examples of Jäckel (2014) presented in Table 8. In the first example, a cubic spline interpolation of option prices is known to produce oscillations in the implied volatility, while a cubic spline on the volatilities introduces spurious arbitrages. In the second example, some of the quotes are at the limit of arbitrage.

On those examples, some care need to be taken in the choice of the boundaries and : they must be far away enough. We pick and where is the smallest quoted strike and the largest.

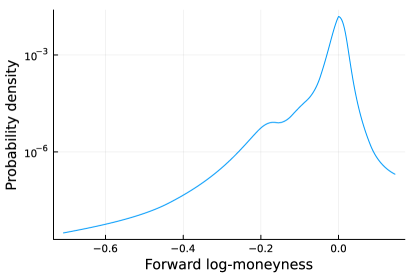

On the example case I, the fit is nearly exact for the linear Bachelier, Black and quadratic LVG models and there is no oscillation or wiggles in the implied volatility interpolation (Figure 8(a)). The corresponding implied probability density is of course smoothest with the quadratic LVG model (Figure 8(b)).

On the example case II, the quadratic LVG model does not allow for an exact fit. The root mean square error is around 4 basis points (Table 3), the fit is qualitatively good (Figure 9(a)). The near-arbitrages impose the probability density to go to almost zero, which conflicts with the continuity constraints of parameterized B-spline density. The density stays however smooth, and looks more natural than the clear overfit of the linear LVG models (Figure 9(b)).

Our choice of range for the parameter does not allow the linear Bachelier model to fit as well as the linear Black model. Increasing the range would make the two implied probability densities even more similar.

| Model | Case I | Case II |

|---|---|---|

| Linear Bachelier | 5.00e-13 | 4.54e-6 |

| Linear Black | 3.64e-12 | 8.04e-8 |

| Quadratic | 2.25e-12 | 4.02e-4 |

6 Conclusion

The quadratic local variance gamma model with a small number of knots lead to smooth implied probability densities on a variety of market option quotes, while providing an excellent fit in terms of implied volatilities, even on challenging examples of non convex implied volatilities or multi-modal probability densities.

It thus constitutes an interesting alternative to the non-parametric approaches of the linear or quadratic local variance gamma models or of the Andreasen-Huge one-step local volatility model, which all require a non-trivial choice of regularization constant to produce a smooth implied probability density.

In similar fashion as Falck and Deryabin (2017), it may be used as specific generic parameterization with a fixed, small number of parameters using only 3 or 5 points. In contrast to Falck and Deryabin (2017), where the linear parameterization leads to edges in the implied probability density and where the problem of the discontinuity at the forward is not dealt with, the probability density of the quadratic LVG model with a reduced number of points will be smooth.

Further research may explore the use of Fourier transforms to recover efficient pricing formulae for European options under the local variance gamma model with a more general local variance function.

yes

References

- Alexiou et al. (2021) Alexiou, Lykourgos, Amit Goyal, Alexandros Kostakis, and Leonidas Rompolis. 2021. Pricing event risk: Evidence from concave implied volatility curves. Swiss Finance Institute Research Paper (21-48).

- Andreasen and Huge (2011) Andreasen, Jesper and Brian Huge. 2011. Volatility interpolation. Risk 24(3), 76.

- Breeden and Litzenberger (1978) Breeden, Douglas T and Robert H Litzenberger. 1978. Prices of state-contingent claims implicit in option prices. Journal of business, 621–651.

- Carr and Lee (2008) Carr, Peter and Roger Lee. 2008. Robust replication of volatility derivatives. In Prmia award for best paper in derivatives, mfa 2008 annual meeting.

- Carr and Madan (2001) Carr, Peter and Dilip Madan. 2001. Towards a theory of volatility trading. Option Pricing, Interest Rates and Risk Management, Handbooks in Mathematical Finance, 458–476.

- Carr and Nadtochiy (2017) Carr, Peter and Sergey Nadtochiy. 2017. Local variance gamma and explicit calibration to option prices. Mathematical Finance 27(1), 151–193.

- De Boor (1978) De Boor, Carl. 1978. A practical guide to splines, Volume 27. Springer-Verlag New York.

- Dupire (1994) Dupire, Bruno. 1994. Pricing with a smile. Risk 7(1), 18–20.

- Falck and Deryabin (2017) Falck, Markus and Mikhail Vladimirovich Deryabin. 2017. Local variance gamma revisited. Available at SSRN 2659728.

- Gatheral (2006) Gatheral, Jim. 2006. The volatility surface: a practitioner’s guide, Volume 357. Wiley. com.

- Hagan et al. (2002) Hagan, Patrick S, Deep Kumar, Andrew S Lesniewski, and Diana E Woodward. 2002. Managing smile risk. Wilmott magazine.

- Healy (2019) Healy, Jherek. 2019. Applied Quantitative Finance for Equity Derivatives. Lulu.com.

- Jäckel (2014) Jäckel, Peter. 2014. Clamping down on arbitrage. Wilmott 2014(71), 54–69.

- Jäckel (2015) Jäckel, Peter. 2015. Let’s be rational.

- Kahalé (2004) Kahalé, Nabil. 2004. An arbitrage-free interpolation of volatilities. Risk 17(5), 102–106.

- Kanzow et al. (2004) Kanzow, Christian, Nobuo Yamashita, and Masao Fukushima. 2004. Levenberg-marquardt methods for constrained nonlinear equations with strong local convergence properties. J. Computational and Applied Mathematics 172, 375–397.

- Klare and Miller (2013) Klare, Kenneth and Guthrie Miller. 2013. Gn–a simple and effective nonlinear least-squares algorithm for the open source literature.

- Le Floc’h (2021) Le Floc’h, Fabien. 2021. An arbitrage-free interpolation of class for option prices. The Journal of Derivatives 28(4), 64–86.

- Le Floc’h and Oosterlee (2019a) Le Floc’h, Fabien and Cornelis W Oosterlee. 2019a. Model-free stochastic collocation for an arbitrage-free implied volatility: Part i. Decisions in Economics and Finance 42(2), 679–714.

- Le Floc’h and Oosterlee (2019b) Le Floc’h, Fabien and Cornelis W Oosterlee. 2019b. Model-free stochastic collocation for an arbitrage-free implied volatility, part ii. Risks 7(1), 30.

- Wystup (2018) Wystup, Uwe. 2018. Arbitrage in the perfect volatility surface. Wilmott 2018(97), 16–17.

no

Appendix A Avoiding the use of complex numbers

We have and we know that since all the B-spline coefficients are positive, thus is either real or imaginary if the sign of is positive (respectively strictly negative). Since involves the ratio , we may equivalently calculate via .

From its definition, we know that is real if and imaginary otherwise.

For we need to consider the two cases where the roots are both real or both complex.

If they are real, we have . We know that since the B-spline coefficients are all positive. If then is real, otherwise .

If the roots are complex with non null imaginary parts, are conjugates of each other. We may write and with . We have then and thus is imaginary.

The term is thus always real. When is imaginary, the term is imaginary.

To evaluate the expression , there are four cases two consider:

-

•

and . All the variables are real.

-

•

and . Take the absolute value in , . Then use instead of . will then be real instead of complex.

-

•

and . The logarithm in may be calculated using . The imaginary part may be directly calculated (without complex numbers). Then use , instead of and terms. will then be real instead of complex.

-

•

and . The logarithm in may be calculated using . The imaginary part may be directly calculated (without complex numbers). Then use , .

Appendix B Market data

| Strike | Volume | Vol | Call Bid | Call Ask | Put Bid | Put Ask | |

| 1800 | -0.2815 | 0 | 0.58 | 0.00 | 1.24 | 0.00 | 0.61 |

| 1850 | -0.2541 | 3300 | 0.53 | 0.00 | 1.14 | 0.00 | 0.56 |

| 1875 | -0.2406 | 3402 | 0.50 | 0.00 | 1.09 | 0.00 | 0.53 |

| 1880 | -0.2380 | 1551 | 0.54 | 0.00 | 1.08 | 0.52 | 0.56 |

| 1890 | -0.2327 | 200 | 0.53 | 0.00 | 1.06 | 0.51 | 0.55 |

| 1900 | -0.2274 | 200 | 0.52 | 0.00 | 1.04 | 0.50 | 0.53 |

| 1910 | -0.2221 | 0 | 0.49 | 0.00 | 1.02 | 0.00 | 0.52 |

| 1980 | -0.1861 | 3 | 0.43 | 0.00 | 0.89 | 0.42 | 0.45 |

| 1990 | -0.1811 | 2 | 0.43 | 0.00 | 0.87 | 0.41 | 0.45 |

| 2000 | -0.1761 | 12 | 0.42 | 0.00 | 0.86 | 0.40 | 0.44 |

| 2010 | -0.1711 | 1 | 0.41 | 0.00 | 0.84 | 0.39 | 0.43 |

| 2030 | -0.1612 | 11 | 0.39 | 0.00 | 0.80 | 0.37 | 0.41 |

| 2035 | -0.1587 | 1 | 0.38 | 0.00 | 0.79 | 0.36 | 0.40 |

| 2050 | -0.1514 | 10 | 0.38 | 0.00 | 0.76 | 0.37 | 0.40 |

| 2055 | -0.1490 | 10 | 0.38 | 0.00 | 0.75 | 0.36 | 0.39 |

| 2085 | -0.1345 | 11 | 0.36 | 0.00 | 0.69 | 0.34 | 0.36 |

| 2090 | -0.1321 | 1 | 0.35 | 0.00 | 0.69 | 0.34 | 0.36 |

| 2100 | -0.1273 | 105 | 0.34 | 0.00 | 0.67 | 0.33 | 0.35 |

| 2105 | -0.1249 | 1 | 0.33 | 0.00 | 0.66 | 0.32 | 0.34 |

| 2120 | -0.1178 | 6 | 0.32 | 0.00 | 0.63 | 0.32 | 0.33 |

| 2125 | -0.1155 | 111 | 0.32 | 0.00 | 0.62 | 0.31 | 0.33 |

| 2130 | -0.1131 | 1 | 0.31 | 0.00 | 0.61 | 0.30 | 0.32 |

| 2135 | -0.1108 | 11 | 0.31 | 0.00 | 0.61 | 0.30 | 0.31 |

| 2140 | -0.1084 | 10 | 0.31 | 0.00 | 0.60 | 0.30 | 0.31 |

| 2150 | -0.1038 | 6610 | 0.29 | 0.00 | 0.53 | 0.29 | 0.30 |

| 2155 | -0.1015 | 1 | 0.29 | 0.00 | 0.52 | 0.28 | 0.30 |

| 2160 | -0.0991 | 8 | 0.29 | 0.00 | 0.51 | 0.28 | 0.30 |

| 2165 | -0.0968 | 2 | 0.28 | 0.00 | 0.50 | 0.28 | 0.29 |

| 2175 | -0.0922 | 3 | 0.27 | 0.00 | 0.48 | 0.27 | 0.28 |

| 2180 | -0.0899 | 66 | 0.27 | 0.00 | 0.47 | 0.27 | 0.28 |

| 2185 | -0.0876 | 15 | 0.27 | 0.00 | 0.46 | 0.26 | 0.27 |

| 2190 | -0.0853 | 26 | 0.26 | 0.00 | 0.45 | 0.26 | 0.27 |

| 2195 | -0.0831 | 13 | 0.26 | 0.00 | 0.44 | 0.25 | 0.26 |

| 2200 | -0.0808 | 113 | 0.25 | 0.00 | 0.43 | 0.25 | 0.25 |

| 2205 | -0.0785 | 13 | 0.25 | 0.00 | 0.42 | 0.25 | 0.25 |

| 2210 | -0.0762 | 14 | 0.24 | 0.00 | 0.41 | 0.24 | 0.25 |

| 2215 | -0.0740 | 102 | 0.24 | 0.00 | 0.41 | 0.23 | 0.24 |

| 2220 | -0.0717 | 2 | 0.23 | 0.00 | 0.40 | 0.23 | 0.24 |

| 2225 | -0.0695 | 43 | 0.23 | 0.00 | 0.39 | 0.22 | 0.23 |

| 2230 | -0.0672 | 93 | 0.22 | 0.00 | 0.38 | 0.22 | 0.23 |

| 2235 | -0.0650 | 2 | 0.22 | 0.00 | 0.37 | 0.21 | 0.22 |

| 2240 | -0.0628 | 134 | 0.21 | 0.00 | 0.36 | 0.21 | 0.22 |

| 2245 | -0.0605 | 11 | 0.21 | 0.00 | 0.35 | 0.21 | 0.21 |

| 2250 | -0.0583 | 104 | 0.20 | 0.00 | 0.34 | 0.20 | 0.21 |

| 2255 | -0.0561 | 205 | 0.20 | 0.00 | 0.34 | 0.20 | 0.20 |

| 2260 | -0.0539 | 184 | 0.19 | 0.00 | 0.33 | 0.19 | 0.20 |

| 2265 | -0.0517 | 89 | 0.19 | 0.00 | 0.32 | 0.19 | 0.19 |

| 2270 | -0.0495 | 74 | 0.18 | 0.00 | 0.28 | 0.18 | 0.19 |

| 2275 | -0.0473 | 377 | 0.18 | 0.00 | 0.27 | 0.18 | 0.18 |

| 2280 | -0.0451 | 207 | 0.17 | 0.00 | 0.26 | 0.17 | 0.17 |

| 2285 | -0.0429 | 478 | 0.17 | 0.00 | 0.25 | 0.17 | 0.17 |

| 2290 | -0.0407 | 295 | 0.16 | 0.00 | 0.24 | 0.16 | 0.17 |

| 2295 | -0.0385 | 280 | 0.16 | 0.00 | 0.18 | 0.16 | 0.16 |

| 2300 | -0.0363 | 1106 | 0.15 | 0.00 | 0.18 | 0.15 | 0.16 |

| 2305 | -0.0342 | 377 | 0.15 | 0.00 | 0.17 | 0.15 | 0.15 |

| 2310 | -0.0320 | 793 | 0.14 | 0.00 | 0.17 | 0.14 | 0.15 |

| 2315 | -0.0298 | 567 | 0.14 | 0.09 | 0.16 | 0.14 | 0.14 |

| 2320 | -0.0277 | 864 | 0.14 | 0.09 | 0.15 | 0.13 | 0.14 |

| 2325 | -0.0255 | 569 | 0.13 | 0.10 | 0.15 | 0.13 | 0.13 |

| 2330 | -0.0234 | 567 | 0.13 | 0.10 | 0.14 | 0.13 | 0.13 |

| 2335 | -0.0212 | 260 | 0.12 | 0.10 | 0.14 | 0.12 | 0.12 |

| 2340 | -0.0191 | 407 | 0.12 | 0.10 | 0.13 | 0.12 | 0.12 |

| 2345 | -0.0170 | 506 | 0.12 | 0.10 | 0.13 | 0.11 | 0.12 |

| 2350 | -0.0148 | 1850 | 0.11 | 0.10 | 0.12 | 0.11 | 0.11 |

| 2355 | -0.0127 | 528 | 0.11 | 0.10 | 0.11 | 0.11 | 0.11 |

| 2360 | -0.0106 | 1134 | 0.10 | 0.10 | 0.11 | 0.10 | 0.11 |

| 2365 | -0.0085 | 436 | 0.10 | 0.10 | 0.10 | 0.10 | 0.10 |

| 2370 | -0.0064 | 1063 | 0.10 | 0.09 | 0.10 | 0.10 | 0.10 |

| 2375 | -0.0042 | 1420 | 0.09 | 0.09 | 0.10 | 0.09 | 0.10 |

| 2380 | -0.0021 | 1248 | 0.09 | 0.09 | 0.09 | 0.09 | 0.09 |

| 2385 | 0.0000 | 229 | 0.09 | 0.09 | 0.09 | 0.09 | 0.09 |

| 2390 | 0.0021 | 2252 | 0.09 | 0.09 | 0.09 | 0.09 | 0.09 |

| 2395 | 0.0041 | 912 | 0.09 | 0.09 | 0.09 | 0.08 | 0.09 |

| 2400 | 0.0062 | 2650 | 0.09 | 0.08 | 0.09 | 0.08 | 0.09 |

| 2405 | 0.0083 | 2523 | 0.08 | 0.08 | 0.09 | 0.08 | 0.09 |

| 2410 | 0.0104 | 789 | 0.08 | 0.08 | 0.09 | 0.08 | 0.10 |

| 2415 | 0.0125 | 863 | 0.08 | 0.08 | 0.08 | 0.07 | 0.10 |

| 2420 | 0.0145 | 905 | 0.08 | 0.08 | 0.09 | 0.00 | 0.13 |

| 2425 | 0.0166 | 1178 | 0.09 | 0.08 | 0.09 | 0.00 | 0.13 |

| 2430 | 0.0187 | 815 | 0.09 | 0.08 | 0.09 | 0.00 | 0.14 |

| 2435 | 0.0207 | 267 | 0.09 | 0.09 | 0.09 | 0.00 | 0.15 |

| 2440 | 0.0228 | 402 | 0.09 | 0.09 | 0.09 | 0.00 | 0.16 |

| 2445 | 0.0248 | 50 | 0.09 | 0.09 | 0.09 | 0.00 | 0.17 |

| 2450 | 0.0268 | 2027 | 0.09 | 0.09 | 0.10 | 0.00 | 0.17 |

| 2455 | 0.0289 | 59 | 0.10 | 0.10 | 0.10 | 0.00 | 0.18 |

| 2460 | 0.0309 | 159 | 0.10 | 0.10 | 0.10 | 0.00 | 0.19 |

| 2465 | 0.0330 | 26 | 0.10 | 0.10 | 0.11 | 0.00 | 0.20 |

| 2470 | 0.0350 | 53 | 0.10 | 0.10 | 0.11 | 0.00 | 0.21 |

| 2475 | 0.0370 | 229 | 0.11 | 0.10 | 0.11 | 0.00 | 0.22 |

| 2495 | 0.0450 | 1 | 0.12 | 0.11 | 0.13 | 0.00 | 0.25 |

| 2550 | 0.0669 | 800 | 0.15 | 0.00 | 0.16 | 0.00 | 0.37 |

| Strike | Logmoneyness | Implied vol. | Strike | Logmoneyness | Implied vol. | |

|---|---|---|---|---|---|---|

| 1900 | -0.325055 | 0.684883 | 2650 | 0.007651 | 0.280853 | |

| 1950 | -0.299079 | 0.6548 | 2655 | 0.009536 | 0.277035 | |

| 2000 | -0.273762 | 0.627972 | 2660 | 0.011417 | 0.273715 | |

| 2050 | -0.249069 | 0.604067 | 2665 | 0.013295 | 0.270891 | |

| 2100 | -0.224971 | 0.576923 | 2670 | 0.01517 | 0.267889 | |

| 2150 | -0.201441 | 0.551253 | 2675 | 0.017041 | 0.264533 | |

| 2200 | -0.178451 | 0.526025 | 2680 | 0.018908 | 0.262344 | |

| 2250 | -0.155979 | 0.500435 | 2685 | 0.020772 | 0.258598 | |

| 2300 | -0.134 | 0.474137 | 2690 | 0.022632 | 0.2555 | |

| 2325 | -0.123189 | 0.461716 | 2695 | 0.024489 | 0.25219 | |

| 2350 | -0.112493 | 0.445709 | 2700 | 0.026343 | 0.249534 | |

| 2375 | -0.101911 | 0.433661 | 2705 | 0.028193 | 0.246659 | |

| 2400 | -0.09144 | 0.42016 | 2710 | 0.03004 | 0.243553 | |

| 2425 | -0.081077 | 0.407463 | 2715 | 0.031883 | 0.240202 | |

| 2450 | -0.070821 | 0.393168 | 2720 | 0.033723 | 0.236588 | |

| 2470 | -0.062691 | 0.381405 | 2725 | 0.03556 | 0.234574 | |

| 2475 | -0.060668 | 0.3793 | 2730 | 0.037393 | 0.230407 | |

| 2480 | -0.05865 | 0.377109 | 2735 | 0.039223 | 0.227866 | |

| 2490 | -0.054626 | 0.372471 | 2740 | 0.041049 | 0.223049 | |

| 2510 | -0.046626 | 0.360294 | 2745 | 0.042872 | 0.219888 | |

| 2520 | -0.04265 | 0.354671 | 2750 | 0.044692 | 0.218498 | |

| 2530 | -0.03869 | 0.350533 | 2755 | 0.046509 | 0.214702 | |

| 2540 | -0.034745 | 0.34419 | 2760 | 0.048322 | 0.210506 | |

| 2550 | -0.030815 | 0.339273 | 2765 | 0.050132 | 0.208175 | |

| 2560 | -0.026902 | 0.333069 | 2770 | 0.051939 | 0.205508 | |

| 2570 | -0.023003 | 0.328206 | 2775 | 0.053742 | 0.199967 | |

| 2575 | -0.021059 | 0.324314 | 2780 | 0.055542 | 0.199007 | |

| 2580 | -0.019119 | 0.322041 | 2785 | 0.057339 | 0.195062 | |

| 2590 | -0.015251 | 0.3168 | 2790 | 0.059133 | 0.190547 | |

| 2600 | -0.011397 | 0.310914 | 2795 | 0.060923 | 0.188427 | |

| 2610 | -0.007559 | 0.305042 | 2800 | 0.062711 | 0.185893 | |

| 2615 | -0.005645 | 0.302416 | 2805 | 0.064495 | 0.182878 | |

| 2620 | -0.003734 | 0.299488 | 2810 | 0.066276 | 0.179292 | |

| 2625 | -0.001828 | 0.29609 | 2815 | 0.068053 | 0.175001 | |

| 2630 | 7.5E-05 | 0.292378 | 2835 | 0.075133 | 0.185751 | |

| 2635 | 0.001974 | 0.289516 | 2860 | 0.083913 | 0.207173 | |

| 2640 | 0.00387 | 0.28584 | 2900 | 0.097802 | 0.225248 | |

| 2645 | 0.005762 | 0.283342 |

| Strike | Mid Vol in % | Weight | Strike | Mid Vol in % | Weight |

| 150.0 | 102.7152094560499 | 1.7320508075688772 | 335.0 | 47.11478482467228 | 7.365459931328131 |

| 155.0 | 99.05195749900227 | 1.0 | 340.0 | 46.78835216769108 | 7.0992957397195395 |

| 160.0 | 96.57262376591365 | 1.224744871391589 | 345.0 | 46.56217516966071 | 7.628892449104261 |

| 165.0 | 94.05597986379826 | 1.0 | 350.0 | 46.299652559206564 | 7.461009761866454 |

| 175.0 | 91.81603362313814 | 2.738612787525831 | 355.0 | 45.939930288424485 | 8.706319543871567 |

| 180.0 | 90.19382314978117 | 1.558387444947959 | 360.0 | 45.856510564386596 | 8.78635305459552 |

| 185.0 | 88.46745842549402 | 1.9999999999999998 | 365.0 | 45.79048747963794 | 7.000000000000021 |

| 190.0 | 86.5754243981787 | 1.2602520756252087 | 370.0 | 45.52139844132191 | 7.745966692414834 |

| 195.0 | 84.561554924342 | 1.3301243435223526 | 375.0 | 45.3447302139774 | 8.093207028119338 |

| 200.0 | 82.45634579529838 | 2.273030282830976 | 380.0 | 45.04013827012644 | 6.16441400296897 |

| 205.0 | 80.28174604214972 | 1.3944333775567928 | 385.0 | 44.800472164335794 | 4.974937185533098 |

| 210.0 | 78.053958851195 | 1.2089410496539776 | 390.0 | 44.91995553643971 | 4.650268809434567 |

| 215.0 | 76.36802684802436 | 1.9999999999999998 | 395.0 | 44.78840707248649 | 4.315669125408015 |

| 220.0 | 74.54192306685303 | 2.0976176963403033 | 400.0 | 45.00659311379786 | 4.636809247747854 |

| 225.0 | 72.60651215584285 | 3.500000000000001 | 405.0 | 45.17530880150887 | 4.732863826479693 |

| 230.0 | 70.58414693439228 | 3.286335345030995 | 410.0 | 44.99007489879635 | 3.1144823004794873 |

| 235.0 | 68.49143304434797 | 2.6692695630078282 | 415.0 | 44.8814967685824 | 2.8809720581775857 |

| 240.0 | 66.3409356115238 | 2.7838821814150116 | 420.0 | 45.16047756853698 | 2.8284271247461894 |

| 245.0 | 64.6230979973991 | 3.1622776601683804 | 425.0 | 45.63938928347205 | 2.7718093060793882 |

| 250.0 | 63.0129173926189 | 3.605551275463988 | 430.0 | 46.002220642176724 | 4.092676385936223 |

| 255.0 | 61.30540004186168 | 3.3541019662496834 | 435.0 | 46.102443173801966 | 2.7041634565979926 |

| 260.0 | 59.469230763484425 | 3.0 | 440.0 | 46.40646817026155 | 2.652259934210953 |

| 265.0 | 58.11921286363728 | 2.9742484506432634 | 445.0 | 47.09795491400157 | 3.710691413905333 |

| 270.0 | 56.87314890047378 | 3.6469165057620923 | 450.0 | 47.625950451280104 | 3.777926319123662 |

| 275.0 | 55.39815904720001 | 3.8729833462074152 | 455.0 | 48.10009989573377 | 3.929942040850535 |

| 280.0 | 54.226712926697765 | 4.183300132670376 | 460.0 | 48.559069655772966 | 3.921096785339529 |

| 285.0 | 53.38887990387771 | 3.7505555144093887 | 465.0 | 49.06446878461756 | 3.70809924354783 |

| 290.0 | 52.34154661207794 | 4.1918287860346295 | 470.0 | 49.60612773473766 | 3.517811819867573 |

| 295.0 | 51.68510552270313 | 3.7670248460125917 | 475.0 | 50.11170526132832 | 3.3354160160315844 |

| 300.0 | 50.72806473672073 | 4.795831523312714 | 480.0 | 50.59204240563133 | 3.1622776601683777 |

| 305.0 | 49.979731599616564 | 4.527692569068711 | 500.0 | 51.591022062492634 | 1.3483997249264843 |

| 310.0 | 48.96563997378466 | 3.482097069296032 | 520.0 | 55.056251469410256 | 1.8929694486000912 |

| 315.0 | 48.23975850368014 | 3.2333489534143167 | 540.0 | 57.838819666460616 | 1.914854215512676 |

| 320.0 | 47.93681836406913 | 3.687817782917155 | 560.0 | 59.92609035805611 | 1.699673171197595 |

| 325.0 | 48.00058538405501 | 6.3245553203367555 | 580.0 | 62.59792014943735 | 1.8708286933869707 |

| 330.0 | 47.57525564073338 | 6.837397165588683 |

| Maturity | 10-Put | 25-Put | ATM | 25-Call | 10-Call |

|---|---|---|---|---|---|

| 1w | 6.14% | 5.19% | 5.14% | 5.59% | 6.49% |

| Moneyness | Volatility (Case I) | Volatility (Case II) |

|---|---|---|

| 0.035123777453185 | 0.642412798191439 | 0.649712512502887 |

| 0.049095433048156 | 0.621682849924325 | 0.629372247414191 |

| 0.068624781300891 | 0.590577891369241 | 0.598339248024188 |

| 0.095922580089594 | 0.553137221952525 | 0.560748840467284 |

| 0.134078990076508 | 0.511398042127817 | 0.518685454812697 |

| 0.18741338653678 | 0.466699250819768 | 0.473512707134552 |

| 0.261963320525776 | 0.420225808661573 | 0.426434688827871 |

| 0.366167980681693 | 0.373296313420122 | 0.378806875802102 |

| 0.511823524787378 | 0.327557513727855 | 0.332366264644264 |

| 0.715418426368358 | 0.285106482185545 | 0.289407658380454 |

| 1 | 0.249328882881654 | 0.253751752243855 |

| 1.39778339939642 | 0.228967051575314 | 0.235378088110653 |

| 1.95379843162821 | 0.220857187809035 | 0.235343538571543 |

| 2.73098701349666 | 0.218762825294675 | 0.260395028879884 |

| 3.81732831143284 | 0.218742183617652 | 0.31735041252779 |

| 5.33579814376678 | 0.218432406892364 | 0.368205175099723 |

| 7.45829006788743 | 0.217198426268117 | 0.417582432865276 |

| 10.4250740447762 | 0.21573928902421 | 0.46323707706565 |

| 14.5719954372667 | 0.214619929462215 | 0.504386489988866 |

| 20.3684933182917 | 0.2141074555437 | 0.539752566560924 |

| 28.4707418310251 | 0.21457985392644 | 0.566370957381163 |