AAffil[arabic] \DeclareNewFootnoteANote[fnsymbol]

Online Resource Allocation in Episodic Markov Decision Processes

Abstract

This paper studies a long-term resource allocation problem over multiple periods where each period requires a multi-stage decision-making process. We formulate the problem as an online allocation problem in an episodic finite-horizon constrained Markov decision process with an unknown non-stationary transition function and stochastic non-stationary reward and resource consumption functions. We propose the observe-then-decide regime and improve the existing decide-then-observe regime, while the two settings differ in how the observations and feedback about the reward and resource consumption functions are given to the decision-maker. We develop an online dual mirror descent algorithm that achieves near-optimal regret bounds for both settings. For the observe-then-decide regime, we prove that the expected regret against the dynamic clairvoyant optimal policy is bounded by where is the budget parameter, is the length of the horizon, and are the numbers of states and actions, and is the number of episodes. For the decide-then-observe regime, we show that the regret against the static optimal policy that has access to the mean reward and mean resource consumption functions is bounded by with high probability. We test the numerical efficiency of our method for a variant of the resource-constrained inventory management problem.

1 INTRODUCTION

We consider a long-term online resource allocation problem where requests for service arrive sequentially over episodes and the decision-maker chooses an action that generates a reward and consumes a certain amount of resources for each request. Such resource allocation problems arise in revenue management (Chen et al.,, 2021; Gong and Simchi-Levi,, 2021) and online advertising (Balseiro et al.,, 2023). Hotels and airlines receive requests for a room or a flight, and they decide how to process them in real-time based on their availability of remaining rooms and flight seats (Talluri and van Ryzin,, 2004). For search engines, when a user arrives with a keyword, they collect bids from relevant advertisers and decide which ad to show to the user (Mehta et al.,, 2007). The decision-maker is informed of or receives stochastic feedback about the reward and resource consumption functions of arriving requests, while the decision-maker makes actions in an online fashion with no knowledge of future requests.

The online resource allocation problem has been studied in the context of or under the name of the AdWords problem (Devanur and Hayes,, 2009; Buchbinder et al.,, 2007), bandits with knapsacks (Badanidiyuru et al.,, 2013; Agrawal and Devanur,, 2014; Immorlica et al.,, 2019), repeated auctions with budgets (Balseiro and Gur,, 2019), online stochastic matching (Karp et al.,, 1990; Feldman et al.,, 2009), online linear programming (Glover et al.,, 1982; Agrawal et al.,, 2014; Gupta and Molinaro,, 2016), assortment optimization with limited inventories (Golrezaei et al.,, 2014), online convex programming (Agrawal and Devanur,, 2015), online binary programming (Li et al.,, 2020), online stochastic optimization (Jiang et al.,, 2022), online resource allocation with concave rewards (Balseiro et al.,, 2020) and nonlinear rewards (Balseiro et al.,, 2023).

Although the above literature assumes that the decision-maker makes a single action for a request, many of the modern service systems allow multi-stage decision-making processes and interactions with customers based on user feedback. For example, medical processes (Sonnenberg and Beck,, 1993) involve sequential decision-making while the prices and costs of medical operations are often predetermined. Multi-stage second-price repeated auctions (Gummadi et al.,, 2012) consider a bidder who is willing to participate in auctions multiple times until winning an item. Modern recommender systems feature continued interactions with customers (Wang et al.,, 2019; Garcin et al.,, 2013). For these applications, actions taken in multiple stages are not necessarily independent, and therefore, it is natural to group a multi-stage decision-making process as an episode. Then this brings about online resource allocation problems where an episode itself involves a sequential decision-making process. Therefore, to model these scenarios, we need a framework to capture multi-stage actions for requests and interactions between service systems and customers.

Motivated by this, we extend the existing framework to consider online resource allocation over an episodic Markov decision process (MDP), generalizing a single action for an episode to multi-stage actions. More generally, we formulate the problem as an episodic finite-horizon constrained MDP (CMDP) (Altman,, 1999; Efroni et al.,, 2020) whose goal is to maximize the cumulative reward by allocating a long-term resource budget over episodes. Basically, the decision-maker prepares a policy for an episode, after running which the decision-maker observes the cumulative reward and resource consumption over the episode. There is a long-term budget for the total resource consumption for all episodes, so the decision-maker can keep track of the remaining budget but cannot observe the reward and resource consumption functions of future episodes. Therefore, the problem is to prepare policies based on past observations and feedback about the reward and resource consumption functions, the remaining resource budget, and the estimation of the unknown transition kernel. The main challenge here is to deal with uncertainties in not only the reward and resource consumption functions of future episodes but also the unknown transition function of the underlying MDP.

We consider two settings, the observe-then-decide regime and the decide-then-observe regime, which differ in how the observations and feedback about the random reward and resource consumption functions are given to the decision-maker. The first setting is related to the contextual MDP literature (Hallak et al.,, 2015; Modi and Tewari,, 2020; Levy and Mansour,, 2023; Levy et al.,, 2023) and assumes that the sampled reward and resource consumption functions of each episode are revealed at the beginning of the episode. Here, we define and study the regret against the dynamic clairvoyant optimal policy. The second setting considers essentially the stochastic finite-horizon episodic constrained MDP (Efroni et al.,, 2020; Qiu et al.,, 2020; Liu et al.,, 2021; Bura et al.,, 2022; Chen et al.,, 2022; Wei et al.,, 2022, 2023) and assumes that the random reward and resource consumption functions for an episode can be observed only after the episode.

Our Contributions

This paper develops and studies a formulation for the long-term sequential allocation problem for multi-step decision processes by providing an integrated view of the online resource allocation problem and the constrained Markov decision process.

We propose what we call the observe-then-decide regime for finite-horizon episodic CMDPs, and we define and study the regret against the dynamic optimal policy that has access to the reward and resource consumption functions of all episodes and the transition kernel. We prove if the reward and resource consumption functions are i.i.d. over episodes, then our online dual mirror descent algorithm guarantees that the expected dynamic regret is bounded above by where is the budget parameter, is the length of the horizon for each episode, is the number of states, is the number of actions, and is the number of episodes. Our algorithm is designed to stop before violating the long-term resource budget constraint.

For the decide-then-observe regime under both the full information and the bandit feedback settings, we show that the online dual mirror descent algorithm achieves regret with probability at least against the static optimal policy that has access to the mean reward and mean resource consumption functions and the transition kernel. This result does not require Slater’s condition or the existence of a strictly safe policy in contrast to and improves upon Efroni et al., (2020); Liu et al., (2021); Wei et al., (2022) whose regret bounds have a suboptimal dependence on for the case of long-term budget constraints.

Our regret bounds for the observe-then-decide and decide-then-observe regimes are nearly tight as there is a lower bound of due to Domingues et al., (2021) based on an instance with a deterministic reward function and no resource budget constraint.

Lastly, we test the numerical performance of our online dual mirror descent method for a variant of the online resource-constrained inventory management problem.

2 PROBLEM SETTING

Finite-horizon Episodic CMDP

We model the online resource allocation problem with a finite-horizon episodic MDP. A finite-horizon MDP is defined by a tuple where is the finite state space with , is the finite action space with , is the finite horizon, is the transition kernel at step , and is the initial distribution of the states. Here, is the probability of transitioning to state from state when the chosen action is at step . Equivalently, we may define a single non-stationary transition kernel with and for . We assume that and thus are unknown.

Before an episode begins, the decision-maker prepares a stochastic policy where is the probability of selecting action in state at step . Here, can be viewed as a non-stationary policy as it may change over the horizon, and this is due to the non-stationarity of the transition kernel over steps . Given a policy for episode , the MDP proceeds with trajectory generated by .

The reward and resource consumption functions of episode is given by , i.e., choosing action at state at step generates a reward and consumes resources of amount . Here, functions and are non-stationary over . Throughout the paper, we assume that for each episode is an i.i.d. sample from an unknown distribution with mean where .

The budget for the total resource consumption over episodes is given by for some . Hence, the goal is to find policies for the episodes to maximize the total cumulative reward, given by

while satisfying the resource budget constraint

Here, we use short-hand notations where and . The decision-maker selects policies in an online fashion because the decision-maker is oblivious to the reward and resource consumption functions of future episodes as well as the true transition kernel .

Observe-then-decide Regime

The first setting we consider assumes that the decision-maker may observe before each episode begins and may adapt to as well as the history . The performance of the decision-maker can be compared to the best possible performance achievable when and are all available in advance, which is given by

This setting is related to the contextual MDP framework (Hallak et al.,, 2015; Modi and Tewari,, 2020; Levy and Mansour,, 2023; Levy et al.,, 2023) in that itself serves as the context for episode . The distinction from these works is that the distribution of reward and resource consumption functions may include infinitely many functions with arbitrary structures.

To measure the performance of a learning algorithm that produces policies , we consider

where is the cumulative reward under the optimal policies . The observe-then-decide regime covers applications in online advertising (Devanur and Hayes,, 2009; Buchbinder et al.,, 2007; Wang et al.,, 2019) and recommender systems with interactions (Garcin et al.,, 2013) and extends the online resource allocation framework without Markovian transitions (Balseiro et al.,, 2023).

Decide-then-observe Regime

The second setting is that the decision-maker prepares a policy based on the history and then observes the associated reward and resource consumption functions. For the full-information setting, we observe and for every . For the bandit feedback setting, we observe and for only the chosen action at state at each step . Here, the performance is evaluated against a single optimal policy applied to all episodes. Let be a policy defined as

Then we define the regret as

where is the cumulative reward under applied to all episodes. The full information setting can model inventory management with observable demands (Chen et al.,, 2021; Gong and Simchi-Levi,, 2021), and the bandit case is what is standard in the stochastic episodic finite-horizon CMDP literature (Efroni et al.,, 2020; Liu et al.,, 2021; Bura et al.,, 2022; Bai et al.,, 2022, 2023; Ding et al.,, 2022; Wei et al.,, 2022, 2023).

Zero Long-term Constraint Violation

We do not allow violating the resource consumption constraint. Hence, an algorithm needs to stop if the remaining budget is not enough to continue the process. To better present our analysis, we assume that even after stopping the process, we take action with for as if we are still running our algorithm.

3 FORMULATION

3.1 Occupancy Measures

Our framework for the long-term online resource allocation problem over an episodic finite-horizon CMDP is based on reformulations via occupancy measures (Altman,, 1999; Zimin and Neu,, 2013; Rosenberg and Mansour,, 2019; Cohen et al.,, 2021). Given a policy and a transition kernel , let be defined as

| (1) |

for . Note that any defined as in (1) has the following properties.

| (C1) | ||||

| (C2) |

The occupancy measure associated with policy and transition kernel is defined as

| (C3) |

Then it follows that

Hence, if a policy is chosen, then the occupancy measure for a loop-free MDP with transition kernel is determined. Conversely, any with satisfying (C1), (C2), (C3) induces a transition kernel and a policy given as follows:

| (2) |

Lemma 3.1.

Therefore, there is a one-to-one correspondence between the set of policies and the set of occupancy measures that give rise to transition kernel . Moreover, the cumulative reward for episode under reward function , policy , and transition kernel can be written in terms of occupancy measure associated with and .

We may express occupancy measure as an -dimensional vector whose entries are given by for . Similarly, we define as the vector whose entries are for . Moreover, we define vector whose entry corresponding to is given by . Then the right-hand side of the above equation is equal to , the inner product of and . Likewise, we define vector to represent the resource consumption function . Consequently,

Then the policy optimization problem can be reformulated as

| (3) |

where is the set of all valid occupancy measures inducing transition kernel . More precisely, is defined as

where is defined as in (2). Hence, is a polytope, and therefore, (3) corresponds to an online linear programming instance.

For the decide-then-observe regime, the optimal policy satisfies

3.2 Confidence Sets

In contrast to the standard online optimization problems, the feasible set is unknown as we do not have access to the true transition kernel . To remedy this issue, we obtain empirical transition kernels to estimate the true transition kernel , based on which we construct relaxations of the feasible set by building confidence sets for . Another issue with applying the existing online dual algorithms, e.g., the dual mirror descent by Balseiro et al., (2023), is that the relaxations are not i.i.d., but instead we will show that they contain with high probability, which turns out to be sufficient for our analysis.

To construct confidence sets for estimating the non-stationary transition kernel , we extend the framework of Jin et al., (2020) developed for the loop-free setting and that of Chen and Luo, (2021) for the stochastic shortest path setting to our finite-horizon non-stationary setting. As Chen and Luo, (2021), we update the confidence set for each episode , in contrast to Jin et al., (2020) where the confidence set is updated over epochs and an epoch may consist of multiple episodes. The distinction is that the transition function is estimated for each distinct step , and this leads to the dependence on in our regret upper bounds, instead of .

We maintain counters to keep track of the number of visits to each tuple and tuple . For each , we define and as the number of visits to tuple and the number of visits to tuple up to the first episodes, respectively, for . Given and , we define the empirical transition kernel for episode as

| (4) |

Next, for some confidence parameter , we define the confidence radius for and as

| (5) |

Based on the empirical transition kernel and the radius, we define the confidence set for episode as

| (6) |

Then, by the empirical Bernstein inequality due to Maurer and Pontil, (2009), we show the following.

Lemma 3.2.

With probability at least , the true transition kernel is contained in the confidence set for every episode .

Lemma 3.3.

With probability at least , for every episode .

3.3 Optimistic Estimators for Reward and Resource Consumption Functions

Our framework applies the optimism in the face of uncertainty principle to estimate the unknown mean reward and resource consumption functions and . Throughout the paper, we denote by and the estimators of and , respectively.

For the observe-then-decide setting, we set

For the decide-then-observe regime, let be the indicator variable for the event that and are observed for state-action pair at step of episode . Then for any and under the full-information setting while only if is visited at step of episode . With this, we define the empirical estimates and of and as follows.

where . Then

where

In contrast to Chen and Luo, (2021), we estimate the reward and resource consumption functions for each distinct step .

Lemma 3.4.

With probability at least , for any and ,

4 ONLINE DUAL METHOD

We present our online dual method (Algorithm 1) for online resource allocation in episodic finite-horizon MDPs.

As explained in Section 3.1, the online resource allocation problem can be reformulated as an online linear optimization problem where each decision is encoded by an occupancy measure that corresponds to a policy for an episode. Then we adapt the online dual mirror descent algorithm by Balseiro et al., (2023) originally developed for nonlinear reward and resource consumption functions under the observe-then-decide regime.

Algorithm 1 proceeds with four parts in each episode. At the beginning of each episode , it first obtains , which is a relaxation of the feasible set with high probability by Lemma 3.3, by constructing the confidence set . Second, the algorithm prepares a policy based on the current dual solution , optimistic reward function estimator , optimistic resource consumption function estimator , and the set . Third, the algorithm runs the episode with policy . Lastly, the algorithm prepares dual solution for the next episode based on the outcomes of episode .

To be more specific, the policy update part works as follows. Given the dual solution prepared before episode starts, we take

Note that is the reward function penalized by the resource consumption function , and is an optimistic estimator of . Then based on (2), we deduce policy associated with the occupancy measure whose vector representation is as in (2). For ease of notation, we denote .

Computing the occupancy measure can be done by solving a linear program as is linear and is a polytope with respect to the vector representation of occupancy measure . In fact, the associated policy as well as can also be computed by an efficient backward dynamic programming algorithm (Jin et al.,, 2020; Efroni et al.,, 2020).

Next, the algorithm executes policy for episode . The algorithm stops if the remaining budget becomes less than 1. Remember that for any . Hence, we would not violate the resource consumption constraint if we run the process only when the remaining resource budget is greater than or equal to 1.

At the end of each episode, the algorithm updates the dual variable for the resource consumption constraint. The dual update rule

follows the standard dual-based algorithm. Note that we have a single resource consumption constraint, in which case is a scalar. In fact, our framework easily extends to multiple resource constraints, for which we use a vector of dual variables where is the number of resource constraints.

We have the following guarantees on the performance of our online dual method.

Theorem 1.

Under the observe-then-decide regime, Algorithm 1 with step size guarantees

where the expectation is taken with respect to the randomness of the reward and resource consumption functions and the randomness in the trajectories of episodes.

Theorem 2.

Under the decide-then-observe regime, Algorithm 1 with step size guarantees

with probability at least .

Note that the bound for the observe-then-decide regime is on the expected regret while we provide a high probability bound for the decide-then-observe regime. This is because we take a dynamic policy as a benchmark for the first setting while we take a static optimal policy with respect to mean reward and resource functions for the second setting. Another remark is that all settings incur regrets of the same asymptotic growth. This is because the largest regret factor in each setting comes from learning the unknown transition function.

Our regret upper bounds are nearly optimal as demonstrated by the following regret lower bound. There is a gap of a factor as well as a polylog factor.

Theorem 3.

(Domingues et al.,, 2021) There is an instance of a finite-horizon episodic MDP with determistic reward and resource consumption functions and unknown transition function for which any algorithm incurs a regret of .

In fact, the instance of Domingues et al., (2021) has no resource budget constraint, which is equivalent to setting for in our setting.

5 REGRET ANALYSIS

Let be the episode in or right after which Algorithm 1 terminates. For , we set for any where action incurs no reward and resource consumption. Moreover, if Algorithm 1 terminates after step in episode , then we take action for step .

For the observe-then-decide regime, we have

where denotes the occupancy measure for and is the benchmark optimal policy for the observe-then-decide setting. Terms (I) and (IV) are due to the randomness in the trajectories, and each of them is the sum of some martingale difference sequence. Term (II) is the regret associated with our online dual method, and term (III) is incurred from learning the unknown transition kernel.

For the decide-then-observe regime, we have

where denotes the occupancy measure and is the benchmark optimal policy for the decide-then-observe setting. Terms (I) and (V) are due to the randomness in the trajectories and the reward function, and as before, each of them is the sum of some martingale difference sequence. Term (II) is associated with our online dual method, term (III) comes from learning the unknown transition kernel, and term (IV) is incurred while learning the mean reward function.

5.1 Regret under the Observe-then-decide Regime

Let be defined as the indicator variable for the event that state-action pair is visited at step of an episode under transition function and an arbitrary policy . Moreover, for an arbitrary function , we have

where is the vector representation of .

For , let denotes an arbitrary policy for episode , and let be any transition kernel from . Then the following lemmas hold.

Lemma 5.1.

Let be an arbitrary reward function for episode . Then with probability at least ,

Note that (I) can be written as where and (IV) equals where , so they can be bounded by Lemma 5.1. Term (III) can be bounded based on the next lemma.

Lemma 5.2.

Let be an arbitrary function for . Then with probability at least ,

5.2 Regret under the Decide-then-observe Regime

Term (I) equals

where . Here, the first sum can be bounded based on Lemma 5.1 while the second one can be bounded using a concentration inequality. Lemma 5.2 applies to bound term (III). To bound term (IV), we show the following lemma.

Lemma 5.3.

Suppose that the statements of Lemma 3.4 hold. Then

Next, to bound term (V), we show the following.

Lemma 5.4.

Suppose that the statements of Lemma 3.4 hold. Then the following statement holds.

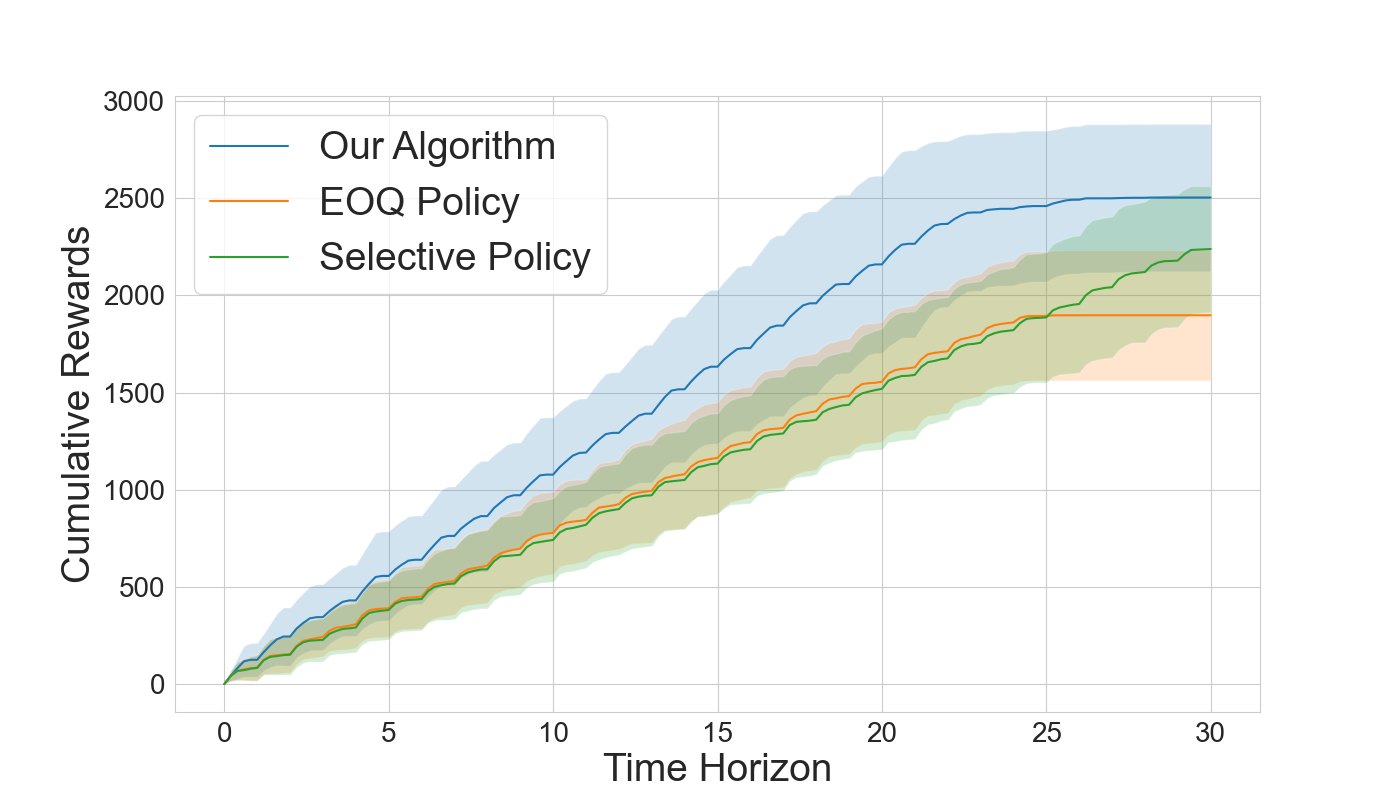

6 NUMERICAL EXPERIMENT

To present a potential use case for our setting we examine a representative inventory management problem, often characterized by cyclical finite horizon episodes (Gong and Simchi-Levi,, 2021). Specifically, we consider a finite-horizon episodic MDP over episodes. In each episode , a customer of type presents a demand for item , with the sequence of future arrivals undisclosed to the decision-maker.

Each episode is a single-item inventory scenario, defined by MDP . States represent inventory levels, and actions denote order quantities, with being the maximum inventory. There’s a fixed order cost , holding cost , and demand , starting each cycle with zero inventory.

For inventory state , the reward function is , with for . The cost per step comprises the quantity ordered, the fixed order cost if ordering occurs, and the holding charge, expressed as .

Our framework can accommodate non-stationary and indeterminate transition kernels within . Transitions from state are governed by , where is a state-dependent shock, assumed to follow . The term reflects uncertainties in receiving the order amount.

In Figure 1 we contrast the efficacy of Algorithm 1 with the traditional Economic Order Quantity (EOQ) policy, setting parameters as episodes, horizon length, maximum inventory, and customer types with returns . We implement these policies and our algorithm and generate the results on an Apple M1 MacBook Pro. Results are averaged across 30 runs, where randomness is over the customer arrival types (uniformly distributed) as well as the and shocks in the state transitions. The EOQ policy, defined by at , disregards customer type and its respective . Consequently, our algorithm’s superiority over the EOQ approach is to be expected. We also benchmark against a "selective" strategy, excluding customer type (return ). As per Figure 1, our algorithm still obtains higher mean cumulative reward, implying nuanced advantages beyond simply customer prioritization.

Acknowledgements

This research is supported, in part, by the KAIST Starting Fund (KAIST-G04220016), the FOUR Brain Korea 21 Program (NRF-5199990113928), the National Research Foundation of Korea (NRF-2022M3J6A1063021).

References

- Agrawal and Devanur, (2014) Agrawal, S. and Devanur, N. R. (2014). Bandits with concave rewards and convex knapsacks. In Proceedings of the Fifteenth ACM Conference on Economics and Computation, EC ’14, page 989–1006, New York, NY, USA. Association for Computing Machinery.

- Agrawal and Devanur, (2015) Agrawal, S. and Devanur, N. R. (2015). Fast algorithms for online stochastic convex programming. In Proceedings of the 2015 Annual ACM-SIAM Symposium on Discrete Algorithms (SODA), pages 1405–1424.

- Agrawal et al., (2014) Agrawal, S., Wang, Z., and Ye, Y. (2014). A dynamic near-optimal algorithm for online linear programming. Operations Research, 62(4):876–890.

- Altman, (1999) Altman, E. (1999). Constrained Markov Decision Processes, volume 7. CRC Press.

- Badanidiyuru et al., (2013) Badanidiyuru, A., Kleinberg, R., and Slivkins, A. (2013). Bandits with knapsacks. In 2013 IEEE 54th Annual Symposium on Foundations of Computer Science (FOCS), pages 207–216, Los Alamitos, CA, USA. IEEE Computer Society.

- Bai et al., (2022) Bai, Q., Bedi, A. S., Agarwal, M., Koppel, A., and Aggarwal, V. (2022). Achieving zero constraint violation for constrained reinforcement learning via primal-dual approach. Proceedings of the AAAI Conference on Artificial Intelligence, 36(4):3682–3689.

- Bai et al., (2023) Bai, Q., Singh Bedi, A., and Aggarwal, V. (2023). Achieving zero constraint violation for constrained reinforcement learning via conservative natural policy gradient primal-dual algorithm. Proceedings of the AAAI Conference on Artificial Intelligence, 37(6):6737–6744.

- Balseiro et al., (2020) Balseiro, S., Lu, H., and Mirrokni, V. (2020). Dual mirror descent for online allocation problems. In III, H. D. and Singh, A., editors, Proceedings of the 37th International Conference on Machine Learning, volume 119 of Proceedings of Machine Learning Research, pages 613–628. PMLR.

- Balseiro and Gur, (2019) Balseiro, S. R. and Gur, Y. (2019). Learning in repeated auctions with budgets: Regret minimization and equilibrium. Management Science, 65(9):3952–3968.

- Balseiro et al., (2023) Balseiro, S. R., Lu, H., and Mirrokni, V. (2023). The best of many worlds: Dual mirror descent for online allocation problems. Operations Research, 71(1):101–119.

- Beygelzimer et al., (2011) Beygelzimer, A., Langford, J., Li, L., Reyzin, L., and Schapire, R. (2011). Contextual bandit algorithms with supervised learning guarantees. In Gordon, G., Dunson, D., and Dudík, M., editors, Proceedings of the Fourteenth International Conference on Artificial Intelligence and Statistics, volume 15 of Proceedings of Machine Learning Research, pages 19–26, Fort Lauderdale, FL, USA. PMLR.

- Buchbinder et al., (2007) Buchbinder, N., Jain, K., and Naor, J. S. (2007). Online primal-dual algorithms for maximizing ad-auctions revenue. In Proceedings of the 15th Annual European Conference on Algorithms, ESA’07, page 253–264, Berlin, Heidelberg. Springer-Verlag.

- Bura et al., (2022) Bura, A., Hasanzadezonuzy, A., Kalathil, D., Shakkottai, S., and Chamberland, J.-F. (2022). DOPE: Doubly optimistic and pessimistic exploration for safe reinforcement learning. In Oh, A. H., Agarwal, A., Belgrave, D., and Cho, K., editors, Advances in Neural Information Processing Systems.

- Chen et al., (2022) Chen, L., Jain, R., and Luo, H. (2022). Learning infinite-horizon average-reward Markov decision process with constraints. In Chaudhuri, K., Jegelka, S., Song, L., Szepesvari, C., Niu, G., and Sabato, S., editors, Proceedings of the 39th International Conference on Machine Learning, volume 162 of Proceedings of Machine Learning Research, pages 3246–3270. PMLR.

- Chen and Luo, (2021) Chen, L. and Luo, H. (2021). Finding the stochastic shortest path with low regret: the adversarial cost and unknown transition case. In Meila, M. and Zhang, T., editors, Proceedings of the 38th International Conference on Machine Learning, volume 139 of Proceedings of Machine Learning Research, pages 1651–1660. PMLR.

- Chen et al., (2021) Chen, Y., Dong, J., and Wang, Z. (2021). A primal-dual approach to constrained markov decision processes.

- Cohen et al., (2021) Cohen, A., Kaplan, H., Koren, T., and Mansour, Y. (2021). Online markov decision processes with aggregate bandit feedback. In Belkin, M. and Kpotufe, S., editors, Proceedings of Thirty Fourth Conference on Learning Theory, volume 134 of Proceedings of Machine Learning Research, pages 1301–1329. PMLR.

- Cohen et al., (2020) Cohen, A., Kaplan, H., Mansour, Y., and Rosenberg, A. (2020). Near-optimal regret bounds for stochastic shortest path. In III, H. D. and Singh, A., editors, Proceedings of the 37th International Conference on Machine Learning, volume 119 of Proceedings of Machine Learning Research, pages 8210–8219. PMLR.

- Devanur and Hayes, (2009) Devanur, N. R. and Hayes, T. P. (2009). The adwords problem: Online keyword matching with budgeted bidders under random permutations. In Proceedings of the 10th ACM Conference on Electronic Commerce, EC ’09, page 71–78, New York, NY, USA. Association for Computing Machinery.

- Ding et al., (2022) Ding, D., Zhang, K., Başar, T., and Jovanović, M. R. (2022). Convergence and optimality of policy gradient primal-dual method for constrained markov decision processes. In 2022 American Control Conference (ACC), pages 2851–2856.

- Domingues et al., (2021) Domingues, O. D., Ménard, P., Kaufmann, E., and Valko, M. (2021). Episodic reinforcement learning in finite mdps: Minimax lower bounds revisited. In Feldman, V., Ligett, K., and Sabato, S., editors, Proceedings of the 32nd International Conference on Algorithmic Learning Theory, volume 132 of Proceedings of Machine Learning Research, pages 578–598. PMLR.

- Efroni et al., (2020) Efroni, Y., Mannor, S., and Pirotta, M. (2020). Exploration-exploitation in constrained mdps.

- Feldman et al., (2009) Feldman, J., Mehta, A., Mirrokni, V., and Muthukrishnan, S. (2009). Online stochastic matching: Beating 1-1/e. In Proceedings of the 2009 50th Annual IEEE Symposium on Foundations of Computer Science, FOCS ’09, page 117–126, USA. IEEE Computer Society.

- Garcin et al., (2013) Garcin, F., Dimitrakakis, C., and Faltings, B. (2013). Personalized news recommendation with context trees. In Proceedings of the 7th ACM Conference on Recommender Systems, RecSys ’13, page 105–112, New York, NY, USA. Association for Computing Machinery.

- Glover et al., (1982) Glover, F., Glover, R., Lorenzo, J., and McMillan, C. (1982). The passenger-mix problem in the scheduled airlines. Interfaces, 12(3):73–80.

- Golrezaei et al., (2014) Golrezaei, N., Nazerzadeh, H., and Rusmevichientong, P. (2014). Real-time optimization of personalized assortments. Management Science, 60(6):1532–1551.

- Gong and Simchi-Levi, (2021) Gong, X.-Y. and Simchi-Levi, D. (2021). Bandits atop reinforcement learning: Tackling online inventory models with cyclic demands.

- Gummadi et al., (2012) Gummadi, R., Key, P., and Proutiere, A. (2012). A repeated auctions under budget constraints. In Proceedings of the Eighth Ad Auction Workshop, volume 4. Citeseer.

- Gupta and Molinaro, (2016) Gupta, A. and Molinaro, M. (2016). How the experts algorithm can help solve lps online. Mathematics of Operations Research, 41(4):1404–1431.

- Hallak et al., (2015) Hallak, A., Castro, D. D., and Mannor, S. (2015). Contextual markov decision processes.

- Hazan, (2016) Hazan, E. (2016). Introduction to online convex optimization. Foundations and Trends® in Optimization, 2(3-4):157–325.

- Immorlica et al., (2019) Immorlica, N., Sankararaman, K. A., Schapire, R., and Slivkins, A. (2019). Adversarial bandits with knapsacks. In 2019 IEEE 60th Annual Symposium on Foundations of Computer Science (FOCS), pages 202–219.

- Jiang et al., (2022) Jiang, J., Li, X., and Zhang, J. (2022). Online stochastic optimization with wasserstein based non-stationarity.

- Jin et al., (2020) Jin, C., Jin, T., Luo, H., Sra, S., and Yu, T. (2020). Learning adversarial Markov decision processes with bandit feedback and unknown transition. In III, H. D. and Singh, A., editors, Proceedings of the 37th International Conference on Machine Learning, volume 119 of Proceedings of Machine Learning Research, pages 4860–4869. PMLR.

- Karp et al., (1990) Karp, R. M., Vazirani, U. V., and Vazirani, V. V. (1990). An optimal algorithm for on-line bipartite matching. In Proceedings of the Twenty-Second Annual ACM Symposium on Theory of Computing, STOC ’90, page 352–358, New York, NY, USA. Association for Computing Machinery.

- Levy et al., (2023) Levy, O., Cohen, A., Cassel, A., and Mansour, Y. (2023). Efficient rate optimal regret for adversarial contextual MDPs using online function approximation. In Krause, A., Brunskill, E., Cho, K., Engelhardt, B., Sabato, S., and Scarlett, J., editors, Proceedings of the 40th International Conference on Machine Learning, volume 202 of Proceedings of Machine Learning Research, pages 19287–19314. PMLR.

- Levy and Mansour, (2023) Levy, O. and Mansour, Y. (2023). Optimism in face of a context:regret guarantees for stochastic contextual mdp. Proceedings of the AAAI Conference on Artificial Intelligence, 37(7):8510–8517.

- Li et al., (2020) Li, X., Sun, C., and Ye, Y. (2020). Simple and fast algorithm for binary integer and online linear programming. In Larochelle, H., Ranzato, M., Hadsell, R., Balcan, M., and Lin, H., editors, Advances in Neural Information Processing Systems, volume 33, pages 9412–9421. Curran Associates, Inc.

- Liu et al., (2021) Liu, T., Zhou, R., Kalathil, D., Kumar, P., and Tian, C. (2021). Learning policies with zero or bounded constraint violation for constrained MDPs. In Beygelzimer, A., Dauphin, Y., Liang, P., and Vaughan, J. W., editors, Advances in Neural Information Processing Systems.

- Maurer and Pontil, (2009) Maurer, A. and Pontil, M. (2009). Empirical Bernstein bounds and sample variance penalization. In Proceedings of the 22nd Annual Conference on Learning Theory.

- Mehta et al., (2007) Mehta, A., Saberi, A., Vazirani, U., and Vazirani, V. (2007). Adwords and generalized online matching. J. ACM, 54(5):22–es.

- Modi and Tewari, (2020) Modi, A. and Tewari, A. (2020). No-regret exploration in contextual reinforcement learning. In Peters, J. and Sontag, D., editors, Proceedings of the 36th Conference on Uncertainty in Artificial Intelligence (UAI), volume 124 of Proceedings of Machine Learning Research, pages 829–838. PMLR.

- Qiu et al., (2020) Qiu, S., Wei, X., Yang, Z., Ye, J., and Wang, Z. (2020). Upper confidence primal-dual reinforcement learning for cmdp with adversarial loss. In Larochelle, H., Ranzato, M., Hadsell, R., Balcan, M., and Lin, H., editors, Advances in Neural Information Processing Systems, volume 33, pages 15277–15287. Curran Associates, Inc.

- Rosenberg and Mansour, (2019) Rosenberg, A. and Mansour, Y. (2019). Online convex optimization in adversarial Markov decision processes. In Chaudhuri, K. and Salakhutdinov, R., editors, Proceedings of the 36th International Conference on Machine Learning, volume 97 of Proceedings of Machine Learning Research, pages 5478–5486. PMLR.

- Sonnenberg and Beck, (1993) Sonnenberg, F. A. and Beck, J. R. (1993). Markov models in medical decision making: A practical guide. Medical Decision Making, 13(4):322–338. PMID: 8246705.

- Talluri and van Ryzin, (2004) Talluri, K. T. and van Ryzin, G. J. (2004). The Theory and Practice of Revenue Management, volume 68 of International Series in Operations Research & Management Science. Springer.

- Wang et al., (2019) Wang, W., Jin, J., Hao, J., Chen, C., Yu, C., Zhang, W., Wang, J., Hao, X., Wang, Y., Li, H., Xu, J., and Gai, K. (2019). Learning adaptive display exposure for real-time advertising. In Proceedings of the 28th ACM International Conference on Information and Knowledge Management, CIKM ’19, page 2595–2603, New York, NY, USA. Association for Computing Machinery.

- Wei et al., (2023) Wei, H., Ghosh, A., Shroff, N., Ying, L., and Zhou, X. (2023). Provably efficient model-free algorithms for non-stationary cmdps. In Ruiz, F., Dy, J., and van de Meent, J.-W., editors, Proceedings of The 26th International Conference on Artificial Intelligence and Statistics, volume 206 of Proceedings of Machine Learning Research, pages 6527–6570. PMLR.

- Wei et al., (2022) Wei, H., Liu, X., and Ying, L. (2022). Triple-q: A model-free algorithm for constrained reinforcement learning with sublinear regret and zero constraint violation. In Camps-Valls, G., Ruiz, F. J. R., and Valera, I., editors, Proceedings of The 25th International Conference on Artificial Intelligence and Statistics, volume 151 of Proceedings of Machine Learning Research, pages 3274–3307. PMLR.

- Zimin and Neu, (2013) Zimin, A. and Neu, G. (2013). Online learning in episodic markovian decision processes by relative entropy policy search. In Burges, C., Bottou, L., Welling, M., Ghahramani, Z., and Weinberger, K., editors, Advances in Neural Information Processing Systems, volume 26. Curran Associates, Inc.

Appendix A AUXILIARY MEASURES AND NOTATIONS

In this section, we define some auxiliary measures and functions that are useful for the analysis of the online dual algorithm (Algorithm 1).

Given a policy , we define the reward-to-go function for a state at step with reward function and transition kernel as follows.

| (8) |

Similarly, we define the state-action value function for at step with reward function and transition kernel as follows.

| (9) |

Furthermore, given a policy and a transition kernel , we define as

| (10) |

for and .

Given two vectors , let be defined as the vector obtained from coordinate-wise products of and , i.e. for . Let be an -dimensional vector all of whose coordinates are .

We define as and for , we define as

where denotes the policy for episode and

is the trajectory generated under policy and transition kernel . Then for , let be defined as the -algebra generated by the random variables in . Then it follows that give rise to a filtration.

We define as and for , we define as

Then for , let be defined as the -algebra generated by the random variables in . Then it follows that give rise to a filtration.

Appendix B MISSING PROOFS FOR SECTION 3

In this section, we first prove Lemma 3.1 which characterizes valid occupancy measures for a finite-horizon MDP. Then we prove the lemmas in Section 3.2 which describe important properties of the confidence sets estimating the true transition kernel. Lastly, we prove the lemmas in Section 3.3 which delineate the accuracy of our optimistic estimators of the mean reward function and the mean resource consumption function .

B.1 Valid Occupancy Measures

First, we provide the proof of Lemma 3.1 which is based on the reduction to the loop-free MDP setting.

Proof of Lemma 3.1.

Given the finite-horizon MDP associated with transition kernel , we may define a loop-free MDP as follows. We define its state space as , which can be viewed as layers for . Its transition kernel is given by for . Next, given , we may define an occupancy measure for the loop-free MDP as for . Then it follows from (Rosenberg and Mansour,, 2019, Lemma 3.1) that is a valid occupancy measure for the loop-free MDP with transition kernel if and only if satisfies

| (C1’) | |||

| (C2’) |

and where is given by

Here, the conditions are equivalent to (C1), (C2), and . Moreover, is a valid occupancy measure with if and only if is a valid occupancy measure with , as required. ∎

B.2 Confidence Sets for the True Transition Kernel

Lemma 3.2 is a modification of (Jin et al.,, 2020, Lemma 2) to our finite-horizon MDP setting. We prove Lemma 3.2 using the empirical Bernstein inequality provided in Lemma F.1.

Proof of Lemma 3.2.

We will show that with probability at least ,

| (11) |

where

holds for every and every episode .

Assume that . Then we define as follows.

Then are i.i.d. with mean , and we have

Moreover, the sample variance of is given by

| (12) |

Then it follows from Lemma F.1 that with probability at least ,

| (13) |

Here, as we assumed that , we have . In addition, we know that and that . Then (13) implies that with probability at least ,

| (14) |

Next, we apply Lemma F.1 to variables that are i.i.d. and have mean . Moreover, the sample variance of is also equal to defined as in (12). Therefore, based on the same argument, we deduce that with probability at least ,

| (15) |

By applying union bound to (14) and (15), with probability at least , (11) holds for . Furthermore, by applying union bound over all , it follows that with probability at least , (11) holds for every , as required. ∎

Lemma 3.2 bounds the difference between the true transition kernel and the empirical transition kernels . Based on Lemma 3.2, the next lemma bounds the difference between the true transition kernel and any contained in the confidence sets . Lemma B.1 is a modification of (Jin et al.,, 2020, Lemma 8) to our finite-horizon MDP setting.

Lemma B.1.

Let . Assume that the true transition kernel satisfies . Then we have

| (16) |

where

for every and every .

Proof.

We follow the proof of (Cohen et al.,, 2020, Lemma B.13). Note that

holds for any value of . As we assumed that , we have that

We may view this as a quadratic inequality in terms of . Note that for any implies that . Therefore, we deduce that

Using this bound on , we obtain the following.

| (17) |

Since we assumed that ,

Moreover, for any , we have

By the triangle inequality, it follows that

as required. ∎

B.3 Optimistic Function Estimators

Lemma 3.4 is a modification of (Chen and Luo,, 2021, Lemma 19) to our finite-horizon MDP setting. We prove Lemma 3.4 using the concentration inequality provided in Lemma F.4. Although we follow the same proof outline of (Chen and Luo,, 2021, Lemma 19), we provide the proof here to make our paper self-contained.

Proof of Lemma 3.4.

If , then while , in which case we have and . Hence, if , the statements of the lemma are trivially satisfied. Thus we may assume that in which case . Moreover, we have .

Applying Lemma F.4 on the first realizations of the random reward for , we deduce that

| (18) |

holds for every with probability at least . Then by taking the union bound for all , with probability at least , (18) holds for all and all . Recall that

This means thst

Since , it follows that

holds if (18) holds. Furthermore, if holds for some , then we have . Applying this to (18) with , it follows that

Based on this inequality, we deduce that

Therefore, it follows that

holds for all with probability at least . as required. Likewise,

holds for all with probability at least . By taking the union bound, both simultaneously hold with probability at least . ∎

Appendix C TECHNICAL LEMMAS

In this section, we prove technical lemmas that are crucial in proving the desired upper bounds on the regret. In particular, our regret analysis heavily depend on Lemmas C.1 and C.8.

Given two vectors , let be defined as the vector obtained from coordinate-wise products of and , i.e. for . Moreover, we define as an -dimensional vector whose coordinate for is . The following lemma is from (Chen and Luo,, 2021), and it is useful to bound the variance of .

Lemma C.1.

(Chen and Luo,, 2021, Lemma 2) Let be any policy for episode , and let denote the occupancy measure . Let be an arbitrary reward function. Then

where are the vector representations of

Proof.

For ease of notation, let denotes , and let and denote and , respectively for . Note that

where the first inequality holds because . Moreover,

Therefore, it follows that

Next, observe that

where the first inequality holds because for any , the first equality holds because

the fifth equality follows from

Therefore, we get that , as required. ∎

The following lemma is from the first statement of (Chen and Luo,, 2021, Lemma 7) with a few modifications to adapt the proof to our setting.

Lemma C.2.

(Chen and Luo,, 2021, Lemma 7) Let be a policy, and let be two different transition kernels. We denote by the occupancy measure associated with and , and we denote by the occupancy measure associated with and . Then

Proof.

We prove the first statement by induction on . When , note that

Hence, both the left-hand side and right-hand side are equal to 0. Next assume that the equality holds with . Then we consider . By the definition of occupancy measures,

To provide an upper bound on Term 1, we use the induction hypothesis for :

where

In addition, observe that

Therefore, it follows that Term 1 is equal to

Next, we upper bound Term 2. Note that

Then it follows that

implying in turn that Term 2 equals

Adding the equivalent expression of Term 1 and that of Term 2 that we have obtained, we get the right-hand side of the statement. ∎

Based on Lemma B.1 and Lemma C.2, we show the following lemma, which is a modification of (Chen and Luo,, 2021, Lemma 7, the second statement).

Lemma C.3.

Let be a policy, and let be two different transition kernels. We denote by the occupancy measure associated with and , and we denote by the occupancy measure associated with and . If , then we have

where are the vector representations of

Proof.

Lemma C.4.

Let be a policy, and let be two different transition kernels. We denote by the occupancy measure associated with and , and we denote by the occupancy measure associated with and . Let , and consider . If , then we have

where are the vector representations of

The following lemma is from (Chen and Luo,, 2021, Lemma 4) after some changes to adapt to our setting.

Lemma C.5.

(Chen and Luo,, 2021, Lemma 4) Let be the policy for episode , and let denote the occupancy measure . Let be an arbitrary reward function, and define . Then

where are the vector representations of

Proof.

For ease of notation, let and denote and , respectively for . Moreover, let denote for . Note that

For ease of notation, let and denote and , respectively. Then

Moreover,

where the inequality is by and . Therefore,

Note that

| (19) |

Then

where the last equality follows from (19). Here, the second term from the right-most side can be bounded from below as follows.

where third equality holds because

and the last inequality holds because

Then it follows that

Repeating the same argument, we deduce that

as required. ∎

Next, using Lemma F.2 that states the Bernstein-type concentration inequality for a martingale difference sequence, we prove the following lemma that is useful for our analysis. Lemma C.6 is a modification of (Jin et al.,, 2020, Lemma 10) and (Chen and Luo,, 2021, Lemma 8) to our finite-horizon MDP setting.

Lemma C.6.

With probability at least , we have

| (20) | ||||

| (21) |

Proof.

Note that

| (22) |

where

As holds for every , we know that is a martingale difference sequence. We know that for each . Let denote . Since is -measurable, we have . Then we deduce

where the second equality holds because it follows from for that

the second inequality holds because if , and the last equality holds true because for any . Then we may apply Lemma F.2 with , and we deduce that with probability at least ,

Plugging this inequality to (22), it follows that

Here, the first term on the right-hand side can be bounded as follows. We have

where the first inequality is due to and the last inequality holds because

Therefore, it follows that

As a result, for any fixed ,

holds with probability at least . By union bound, (20) holds with probability at least .

Next, we will show that (21) holds.

| (23) |

where

As holds for every , we know that is a martingale difference sequence. We know that for each . Then we deduce

where the first inequality is derived by the same argument when bounding , the first equality holds because if , and the last equality holds true because for any . Then we may apply Lemma F.2 with , and we deduce that with probability at least ,

Then with probability at least , (20) holds and

| (24) |

holds. Moreover, we have

where the last equality holds because . Then

where the second equality is due to the Cauchy-Schwarz inequality. Then it follows from (23) and (24) that (21) holds. ∎

Lemma C.7.

Assume that for every episode . Then

for any where and .

Proof.

Let be the vector representations of , respectively. Note that

where the first inequality is from Lemma B.1, the first equality holds because and , the second inequality is due to Lemma C.4. Then plugging in the definition of , it follows that

where the third equality follows from the Cauchy-Schwarz inequality and the last equality is due to Lemma C.6. Therefore, we deduce that

as required. ∎

Next, we provide Lemma C.8, which is a modification of (Chen and Luo,, 2021, Lemma 9) to our finite-horizon MDP setting.

Lemma C.8.

Let be any policy for episode , and let be any transition kernel from . Let denote the occupancy measures , respectively. Let be an arbitrary reward function for episode . Then with probability at least ,

Proof.

We define as and for , we define as

where and denote the policies for episode and episode , respectively, and

is the trajectory generated under policy and transition kernel . Then for , let be defined as the -algebra generated by the random variables in . Then it follows that give rise to a filtration.

Let us define

Note that

where the first equality is due to Lemma C.2 and the first inequality is by Lemma C.7. Moreover,

where , the first equality holds because and is independent of , the first inequality is due to Lemma B.1, and the second inequality is from Lemma B.1 and . Recall that , which implies that

where

Here, we have

Then it follows from Lemma F.5 that with probability at least ,

Note that

where the first inequality holds because , the second inequality holds because and the Cauchy-Schwarz inequality implies that

and the third inequality follows from

Next, the Cauchy-Schwarz inequality implies the following.

Here, the second term can be bounded as follows.

, we define

Then

Furthermore,

where is the vector representation of and the inequality follows from Lemma C.5, ,

and Lemma F.3. Therefore, we finally have proved that

Moreover, we know from Lemma C.1 that

and therefore, it follows that

as required. ∎

Appendix D REGRET ANALYSIS FOR THE OBSERVE-THEN-DECIDE REGIME

D.1 Proofs of Lemmas 5.1 and 5.2

Based on Lemmas C.1 and C.8, we can prove Lemma 5.1 that bounds the difference between the expected reward and the realized reward and Lemma 5.2 that bounds the regret due to the estimation error.

Proof of Lemma 5.1.

We closely follow the proof of (Chen and Luo,, 2021, Theorem 6). For ease of notation, let us use notation for an arbitrary policy for episode , denotes the occupancy measure , and denotes . Then Lemma C.1 implies that

where are the vector representations of We define as and for , we define as

where and denote the policies for episode and episode , respectively, and

is the trajectory generated under policy and transition kernel . Then for , let be defined as the -algebra generated by the random variables in . Then it follows that give rise to a filtration. Then it follows that

Note that the first term on the right-hand side can be bounded as follows.

To upper bound the first term, we consider

Applying Lemma C.8 with function , we deduce that with probability at least ,

where the second equality holds because and the fourth equality holds because . Then it follows that

Therefore, we obtain

Next, we apply Lemma F.2 with is set to

Then we get that with probability at least ,

Similarly, we get that with probability at least ,

as required. ∎

Proof of Lemma 5.2.

We closely follow the proof of (Chen and Luo,, 2021, Theorem 6). For ease of notation, let us use notation for an arbitrary policy for episode , denotes the occupancy measure , and denotes the occupancy measure .

Applying Lemma C.8 with function , we deduce that with probability at least ,

where the second equality holds because and the third equality holds because . ∎

D.2 Bound on the Regret Term (II)

In this section, we prove Lemma D.2 that bounds the regret term (II). We follow the analysis of the online dual mirror descent algorithm due to (Balseiro et al.,, 2023, Theorem 1). In our analysis, we need Lemmas 5.1 and 5.2.

We consider

Lemma D.1.

(Balseiro et al.,, 2023, Proposition 1) For any , we have

Lemma D.2.

The following holds for the regret term (II).

where the expectation is taken with respect to the randomness of the reward and resource consumption functions and the randomness in the trajectories of episodes.

Proof.

For , let denote the amount of resource consumed in episode . We define the stopping time of Algorithm 1 as

By definition, we have . Since for any , it follows that Algorithm 1 does not terminate until the end of episode . Then we have

By Lemma 3.3, with probability at least , we have

| (25) |

where

Recall that the pair of reward and resource consumption functions follows distribution . Then we define as

Since for are i.i.d. with distribution , it follows that

Recall that is the -algebra generated by the information up to episode . Consider

for . Then is -measurable and . Therefore, is a martingale. Since the stopping time is with respect to and is bounded, the Optional Stopping Theorem implies that

Likewise, we can argue by the Optional Stopping Theorem that

Taking the conditional expectation with respect to of both sides of (25), it follows that

where the first equality is due to the tower rule and the last equality holds because is -measurable. Therefore,

where the second equality comes from the Optional Stopping Theorem. Furthermore, note that is the maximum of linear functions in terms of , so is convex for any . Then is also convex with respect to , and therefore,

This implies that

Next, consider the second term on the right-hand side of this inequality:

Let be defined as

Then the dual update rule

corresponds to the online mirror descent algorithm applied to the linear functions for . Since , the standard analysis of online mirror descent (see (Hazan,, 2016)) gives us that

Next, note that for any ,

where the second inequality is implied by and Lemma D.1. In particular, we set , and obtain

Then it follows that

where the last inequality is from the online mirror descent analysis.

If , then we set , in which case

If , then we have

In this case, we set . Then

By Lemma 5.2 and Lemma 5.1, with probability at least , we have

In this case, we deduce that

where the second inequality holds because . Setting

we deduce that

Now we may set

Note that with probability at most ,

Moreover, with probability at least ,

Then it follows that

as required. ∎

D.3 Proof of Theorem 1

Appendix E REGRET ANALYSIS FOR THE DECIDE-THEN-OBSERVE REGIME

Suppose that the statements of Lemma 3.4 hold, which is the case with probability at least .

Recall that

E.1 Bound on the regret term (I)

Lemma E.1.

With probability at least ,

Proof.

Note that term (I) equals

Note that are i.i.d. and that

Then it follows from Lemma F.4 that

holds wity probability at least . With probability at least ,

as required. ∎

E.2 Proofs of Lemmas 5.3 and 5.4

Proof of Lemma 5.3.

Suppose that the statements of Lemma 3.4 hold, which is the case with probability at least . Then it follows that

We first bound Term 2 under both the full information setting and the bandit feedback setting. Let be the probability that and are observed for state-action paper at step of episode . Note that

and that

where is the -algebra generated by the information up to episode . Note that by Lemma F.5, we deduce that

holds with probability at least . Under both the full information setting and the bandit feedback setting, we have

Therefore, Term 2 can be bounded as

For Term 1, note that

where the first inequality is due to the Cauchy-Schwarz inequality and the second inequality holds because and . Under the full information setting, we have . Since , it follows that

Under the bandit feedback setting,

Therefore,

as required. ∎

Proof of Lemma 5.4.

Recall that is the -algebra generated by the information up to episode . By Lemma C.1, we have , which implies that

because is -measurable. Therefore, it follows that

Since for any by Lemma 3.4

| Term 1 |

For Term 2, applying Lemma C.8 to functions , we obtain

| Term 2 | |||

For Term 3, note that

Based on the upper bounds on Terms 1, 2, and 3, we obtain

Moreover,

and for give rise to a martingale difference sequence as . By Lemma F.2 with

we obtain

Next, again by Lemma C.1, we have , which implies that

because is -measurable. Therefore, it follows that

Note that by Lemma 5.4,

| Term 4 | |||

Terms 5 and 6 can be bounded similarly as terms 2 and 3, respectively. Therefore, we deduce

| Term 5 | |||

| Term 6 |

Then it follows that

Moreover, for give rise to a martingale difference sequence as . By Lemma F.2 with

we obtain

as required. ∎

E.3 Bound on the Regret Term (II)

Lemma E.2.

Suppose that the statements of Lemma 3.4 hold. Then the following holds for the regret term (II).

with probability at least .

Proof.

For , let denote the amount of resource consumed in episode . We define the stopping time of Algorithm 1 as

By definition, we have . Since for any , it follows that , and therefore, Algorithm 1 does not terminate until the end of episode . Then we have

Note that

Then it follows that

Then the dual update rule

corresponds to the online mirror descent algorithm applied to the linear functions for . Since , the standard analysis of online mirror descent (see (Hazan,, 2016)) gives us that

Then we deduce that

If , then we set , in which case

If , then we have

In this case, we set . Then

Note that

By Lemma 5.4,

By Lemma 5.3,

By Lemma 5.2, with probability at least ,

Therefore, it follows that

as required. ∎

E.4 Proof of Theorem 2

Recall that

With probability at least , the statements of Lemma 3.4 hold. Then it follows from Lemmas 5.4 and 5.5

| Term (IV) | |||

| Term (V) |

Moreover, by Lemma E.2,

| Term (II) |

It follows from Lemma E.1 that with probability at least , we have

| Term (I) |

Lastly, Lemma 5.2 with probability at least , we have

| Term (III) |

Hence, by taking the union bound,

with probability at least .

Appendix F CONCENTRATION INEQUALITIES

Lemma F.1.

(Maurer and Pontil,, 2009, Theorem 4) Let be i.i.d. random variables with mean , and let . Then with probability at least ,

where is the sample variance given by

Next, we need the following Bernstein-type concentration inequality for martingales due to (Beygelzimer et al.,, 2011). We take the version used in (Jin et al.,, 2020, Lemma 9).

Lemma F.2.

(Beygelzimer et al.,, 2011, Theorem 1) Let be a martingale difference sequence with respect to a filtration . Assume that almost surely for all . Then for any and , with probability at least , we have

Lemma F.3 (Azuma’s inequality).

Let be a martingale difference sequence with respect to a filtration . Assume that for . Then with probability at least , we have

Next, we need the following concentration inequalities due to (Cohen et al.,, 2020).

Lemma F.4.

(Cohen et al.,, 2020, Lemma D.3) Let be a sequence of i.i.d. random variables with expectation . Suppose that holds almost surely for all . Then with probability at least , the following holds for all simultaneously:

Lemma F.5.

(Cohen et al.,, 2020, Lemma D.4) Let be a sequence of random variables adapted to the filtration . Suppose that holds almost surely for all . Then with probability at least , the following holds for all simultaneously: